Sprinklr: The Story of Enterprise Social Media's Hidden Giant

I. Introduction & Episode Roadmap

Here is a question worth sitting with: What kind of company manages the public-facing digital presence of Nike, Microsoft, McDonald's, Samsung, and roughly sixty percent of the Fortune 100, processes billions of customer interactions across thirty-plus channels in over eighty countries, and yet remains almost entirely invisible to the average consumer?

The answer is Sprinklr, and its story is one of the most underappreciated sagas in enterprise software.

Sprinklr, trading on the New York Stock Exchange under the ticker CXM, generated nearly $800 million in revenue in its most recent fiscal year. The company serves over 1,900 enterprise clients. Its platform touches the social media posts, customer service chats, advertising campaigns, and consumer research workflows of the world's largest brands. And yet, ask a hundred people on the street if they have heard of Sprinklr, and the answer will almost universally be no. That anonymity is not a failure of marketing. It is the nature of the beast. Sprinklr is infrastructure, the plumbing beneath the customer experience that global brands deliver every day.

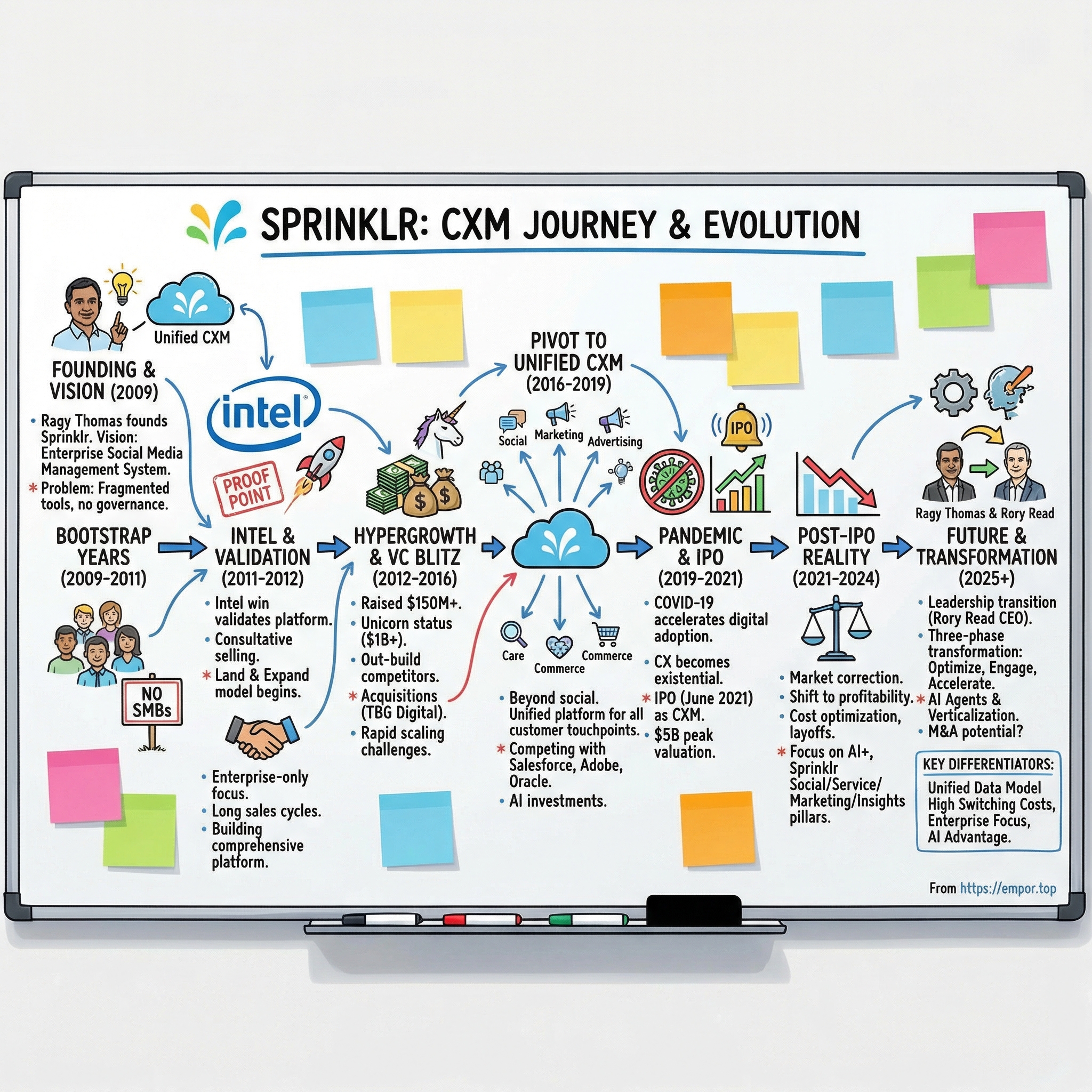

The story of how Sprinklr got here is a story about founder-led tenacity, about a serial entrepreneur from Kerala, India named Ragy Thomas who decided in 2009 that the enterprise world was woefully unprepared for the social media revolution. It is a story about category creation, about the long, patient, sometimes grueling work of convincing the world's largest companies that they needed a product category that did not yet exist. And it is a story about the transition from social media chaos to what the company now calls unified customer experience management, a term Sprinklr effectively coined and then spent more than a decade trying to own.

Why does this matter right now? Because the convergence of generative AI, the explosion of digital customer channels, and the enterprise mandate to consolidate sprawling technology stacks has made Sprinklr's bet more relevant than ever. But it has also made the competitive landscape more brutal. Microsoft, Salesforce, and Adobe are all pushing hard into customer experience. Sprinklr brought in a new CEO in late 2024, the company just executed its largest-ever layoff, and the stock trades at a fraction of its post-IPO peak. The question is whether Sprinklr's fifteen-year head start in unified customer experience, its deep enterprise relationships, and its accumulated data moat give it an enduring advantage, or whether the giants will simply bundle their way to dominance.

Along the way, the themes that emerge are universal to enterprise software: the tension between platform breadth and product depth, the challenge of competing against companies with ten times your resources, the agonizing tradeoff between growth and profitability, and the question every founder-led company must eventually confront, what happens when the founder steps back.

This is the Sprinklr story, from a monsoon childhood in southern India to a $5 billion IPO to a company now fighting for its next chapter.

II. The Founding Context & Ragy Thomas's Origin Story

Ragy Thomas grew up in Kerala, the lush southwestern state of India known for producing an outsized number of the country's engineers and entrepreneurs. He studied engineering, developed a fascination with the emerging internet in the mid-1990s, and eventually made his way to New York, the city that would become the backdrop for his entire entrepreneurial career.

Thomas was not the stereotypical Silicon Valley founder who dropped out of Stanford and raised venture capital from a dorm room. He was an immigrant entrepreneur who understood what it meant to build something from nothing, and his path to technology entrepreneurship was shaped by the practical, engineering-oriented mindset that Kerala's educational system instilled. He moved to the United States, settled in the New York area, and began building businesses at the intersection of technology and marketing.

His first significant venture was Bigfoot Interactive, an email marketing company that Thomas built during the early days of digital marketing. Bigfoot found its niche helping large companies manage email campaigns at scale, and the company attracted enough attention that Publicis Groupe, the French advertising giant, acquired it. Thomas made money on the deal. He gained operational experience running a technology company inside a massive holding company. But he also came away with a restless conviction that Bigfoot had not been "the one," that defining company that would leave a mark on the industry. He was searching for something bigger.

The search ended between 2008 and 2009, during a period when social media underwent its most dramatic transformation from novelty to mainstream force. Twitter, which had launched in 2006, was becoming the real-time pulse of global conversation. Facebook was racing toward half a billion users. YouTube was redefining how brands communicated visually. And for the first time in the history of business, customers had a megaphone that was just as loud as the brands themselves.

For enterprises, this was terrifying. Consider the "United Breaks Guitars" moment. In 2009, musician Dave Carroll posted a YouTube video about United Airlines breaking his guitar during a flight. The video went viral, racking up millions of views and becoming a case study in how a single customer's complaint, amplified by social media, could cause genuine brand damage. United's stock reportedly dropped, and the company scrambled to respond through channels and processes that were utterly unequipped for real-time public crisis management.

Thomas saw this dynamic and recognized the underlying structural problem. It was not that United was uniquely incompetent. It was that no large enterprise had systems for managing this kind of crisis. The entire incident exposed a structural gap in enterprise software that nobody had filled.

Large enterprises were not just bad at social media. They literally had no systems for managing it. A Fortune 500 company might have dozens of brands, operate in forty or fifty countries, employ thousands of people who touched the customer in some way, and face compliance requirements in every jurisdiction. The idea that an intern with a Hootsuite login could manage this was absurd. And the existing enterprise software vendors, the Salesforces and Adobes and Oracles of the world, had been built for a pre-social era. Their CRM systems tracked transactions and support tickets. They were not designed for the messy, real-time, public, multi-channel chaos of social media at enterprise scale.

The agencies were not the answer either. Big ad agencies were charging brands hundreds of thousands of dollars to manage social presence using manual processes and spreadsheets. There was no technology layer, no governance, no analytics, no way to ensure that what the brand was saying on Twitter in Brazil was consistent with what it was saying on Facebook in Germany.

Thomas's insight was deceptively simple: the world's largest companies needed a purpose-built software platform to manage their entire social media presence, across every channel, every country, every department, with the compliance, governance, and analytics that enterprise buyers demanded. Nobody was building this. The CRM vendors saw social as a feature to bolt on. The agencies saw it as a service to bill for. The existing social media tools saw it as a consumer productivity problem. Nobody was building the enterprise-grade platform that a company like Procter & Gamble or Samsung actually needed to manage social at global scale with governance, compliance, and unified analytics.

Thomas decided he would be the one to build it. It was a decision rooted not just in market analysis but in personal conviction. He later described the founding moment as the realization that social media was not a marketing channel but a fundamental shift in the relationship between brands and customers, a shift that demanded an entirely new category of enterprise software.

III. The Bootstrap Years & Early Product (2009-2011)

In September 2009, Ragy Thomas officially founded Sprinklr. The timing was deliberate. The financial crisis had shaken corporate budgets, but the social media tsunami was not waiting for the economy to recover. Every month, the volume of customer conversations happening on social platforms was growing exponentially, and enterprises were falling further behind.

Thomas's original vision was what he called a "social media management system" for enterprises. But from the very beginning, the ambition was broader than that label suggested. Where competitors were building point solutions, a tool for scheduling tweets here, a listening dashboard there, Thomas insisted on building a comprehensive platform. His argument was that enterprises did not need another tool. They needed a system, something that could handle publishing, engagement, listening, analytics, governance, compliance, and workflow automation across every social channel, all in one place.

To understand why this mattered, consider the alternative. A typical startup in the social media management space circa 2010 might build a tool that let you schedule tweets and track mentions. That is a useful feature, but it is not a system. It does not address governance, meaning who is allowed to post on behalf of the brand in which countries. It does not address compliance, meaning how do you ensure that regulated industries like financial services are not making inadvertent disclosures through social posts. It does not address analytics at scale, meaning how do you aggregate and make sense of customer conversations happening across dozens of channels in dozens of languages simultaneously. Thomas wanted to build all of this from day one.

This was an extraordinarily ambitious product vision for a startup. It meant that Sprinklr's early engineering team had to build far more functionality before they could credibly sell to their first customer than a typical startup would. But Thomas believed this was the only path to winning enterprise deals. A Fortune 500 company was not going to stitch together eight different social media tools from eight different startups. They wanted one vendor, one contract, one throat to choke.

Convincing those first Fortune 500 customers to trust a startup with their public-facing social presence was the central challenge of Sprinklr's early years. Thomas had to sell simultaneously to multiple stakeholders within each prospective client: marketing wanted the publishing and engagement tools, IT wanted to know about security and compliance, customer service wanted the listening and routing capabilities, and legal wanted governance controls. This multi-stakeholder enterprise sale was brutally complex for a small company, but it also became a formidable moat once Sprinklr cracked the code.

From day one, Thomas made a decision that would define Sprinklr's trajectory: no small and medium businesses, no mid-market. Sprinklr would sell exclusively to large enterprises. This was counterintuitive in a startup world that worshipped bottoms-up adoption and viral growth. But Thomas understood that the problems he was solving, global compliance, multi-brand governance, cross-channel analytics at scale, simply did not exist for smaller companies. Going downmarket would have diluted the product, distracted the sales team, and undermined the brand positioning that Sprinklr needed to win the Fortune 500.

The competitive landscape in 2009-2011 was crowded but shallow. Hootsuite was the dominant name in social media management, but it was built for individuals and small teams, not global enterprises. Buddy Media, founded in New York by Michael Lazerow, was gaining traction as a Facebook marketing platform. Vitrue was another social media marketing player, focused on helping brands manage their Facebook pages. Radian6, based in Canada, had built a respected social listening tool. And Salesforce was beginning to eye the space, recognizing that social data was becoming integral to customer relationship management.

Each of these competitors was building a piece of the puzzle. Thomas's bet was that Sprinklr could build the whole puzzle, and that enterprises would eventually demand a unified solution rather than cobbling together point products. It was a bet that would take years to prove right, and the early years were a grind of enterprise sales cycles that could stretch six months or longer, all while competitors with more funding and more brand recognition were grabbing market share in simpler segments.

But the DNA was set: enterprise-first, platform-comprehensive, founder-driven. That DNA would carry Sprinklr through everything that followed.

There is an underappreciated aspect of this early period that deserves mention. By choosing the enterprise path, Sprinklr was also choosing a business model that would take far longer to generate revenue than a bottoms-up consumer approach. Enterprise sales cycles measured in quarters, not days. Each customer required custom onboarding, training, and integration work. The total cost to acquire a customer was high, and payback periods were measured in years. Thomas was betting that the lifetime value of an enterprise relationship, the multi-year contracts, the expansion revenue, the near-impossibility of churn once deeply embedded, would more than compensate for the slower start. It was a bet that required both conviction and the willingness to endure years of modest revenue growth before the compound effects kicked in.

IV. The First Inflection Point: Intel & Enterprise Validation (2011-2012)

Every enterprise software company has a lighthouse customer, that first marquee logo that transforms the sales narrative from "trust us, we can do this" to "Intel trusts us, and here is what we built for them." For Sprinklr, that customer was Intel.

Intel's requirements were a perfect encapsulation of why existing social media tools fell short. The chipmaker operated in over forty countries. It had multiple product lines, each with its own marketing team and social presence. It needed governance controls to ensure that a social media manager in Taiwan could not accidentally post something that contradicted corporate messaging in the United States. It needed analytics that rolled up across all channels and geographies into a unified dashboard for leadership. It needed compliance workflows that met regulatory requirements in every jurisdiction where Intel operated. And it needed all of this from a single vendor, because managing fifteen different tools across forty countries was its own nightmare.

Sprinklr delivered. The Intel deployment became the proof point that Thomas needed. It demonstrated that Sprinklr's platform could operate at the scale, complexity, and rigor that the world's largest companies demanded. And in enterprise software, nothing sells like a reference customer. Intel executives talked to their peers at other Fortune 500 companies. Word spread through the tight-knit networks of enterprise IT and marketing leaders. Procter & Gamble came on board. Microsoft became a customer. Nike, McDonald's, and other household names followed.

The Intel win also established a pattern that would define Sprinklr's enterprise sales strategy for years to come. Thomas and his team did not just sell software. They sold a vision of what the customer's social media operation could look like if it were properly unified and governed. They walked into executive meetings with a diagnosis of the customer's current pain, the fragmented tools, the compliance gaps, the inconsistent brand voice across channels, and then presented Sprinklr as the cure. It was consultative selling at its most sophisticated, and it required a sales team that understood not just the product but the organizational dynamics of global enterprises.

What made this land-and-expand motion so powerful was that each new logo validated Sprinklr's platform approach. These were not companies that would tolerate a half-baked product. They had demanding IT security reviews, lengthy procurement cycles, and zero tolerance for downtime. Every successful deployment reinforced the narrative that Sprinklr was the enterprise-grade solution in a market full of consumer-grade tools.

During this period, Sprinklr made another critical strategic decision: building integrations with every major social channel, not just Facebook and Twitter. While competitors focused on the two or three biggest platforms, Sprinklr built connectors to twenty-three-plus social and messaging channels, including regional platforms that mattered in specific geographies. This breadth became a competitive differentiator. A global enterprise operating in China, Japan, Brazil, and Germany needed a platform that could handle WeChat, LINE, VKontakte, and WhatsApp alongside Facebook and Twitter. Sprinklr was one of the few vendors that could.

The revenue model that crystallized during these years was classic enterprise SaaS: six-figure annual contract values, multi-year commitments, and a land-and-expand strategy where initial deployments in one department or geography expanded over time into broader enterprise-wide licenses. A customer might start with Sprinklr for social media management in North America, then expand to Europe, then add customer care capabilities, then bring in the advertising module. Each expansion increased the annual contract value and deepened the integration with the customer's workflows.

This model produced the kind of predictable, recurring revenue that venture capitalists love. The beauty of enterprise SaaS economics is the compounding effect: high retention rates mean that each new customer adds to a growing base of recurring revenue, and expansion within existing accounts provides growth even without acquiring new logos. Sprinklr's metrics during this period told exactly this story, and it was not long before the investor calls started coming in.

V. The Venture Capital Blitz & Hypergrowth (2012-2016)

The first three years had been a bootstrapped grind: long sales cycles, demanding enterprise customers, and the constant challenge of convincing Fortune 500 procurement departments that a startup could be trusted with their brand's public presence. But by 2012, the metrics were undeniable.

In that year, Battery Ventures led Sprinklr's Series A round with approximately $5 million. It was a modest sum by Silicon Valley standards, but it validated the institutional investor thesis that Sprinklr was building something with durable enterprise value. More importantly, Battery brought credibility and connections that accelerated Sprinklr's enterprise sales motion.

What happened next was a venture capital blitz. Sprinklr's growth metrics were exactly what growth-stage investors craved. Net dollar retention, the measure of how much existing customers spend over time relative to their initial contract, was running above 120 percent. This meant that Sprinklr's existing customers were not only staying but spending significantly more each year. In enterprise SaaS, a net dollar retention rate above 120 percent is considered elite. It signals that the product is deeply embedded in customer workflows and that the land-and-expand motion is working.

Between 2013 and 2015, Sprinklr raised over $150 million across multiple rounds. The Series C brought in $40 million. The Series D added $46 million. And the Series E, completed in 2015, was a massive $105 million round that valued Sprinklr at over $1 billion, granting it the coveted unicorn status. The investors included prominent names like Intel Capital, which had seen the platform firsthand as a customer, along with ICONIQ Capital and Sapphire Ventures.

The speed of the fundraising reflected the strength of Sprinklr's underlying metrics. Venture capital firms were falling over themselves to invest in a company that combined Fortune 500 customer logos, triple-digit net dollar retention, and a market that was growing exponentially. The investor deck practically wrote itself: social media is becoming mission-critical for enterprises, enterprises need enterprise-grade tools, Sprinklr is the only enterprise-grade platform, and the market is a fraction of its eventual size.

Thomas deployed this capital with a clear strategy: out-build every competitor through relentless R&D investment. While Buddy Media and Radian6 were being acquired by Salesforce, while Oracle snapped up Vitrue, while Adobe bought Context Optional, Sprinklr stayed independent and kept building. Thomas's conviction was that the market would eventually demand a unified platform, not a Frankenstein assembly of acquired point solutions stitched together by a larger vendor. He had watched Salesforce acquire Buddy Media for $689 million and Radian6 for $326 million, and then struggle to integrate them into a coherent product. This integration tax, the pain and delay of merging disparate codebases, cultures, and data models, was exactly the problem that Sprinklr's single-platform architecture was designed to avoid.

The acquisition spree across the industry also validated Sprinklr's market. When Salesforce, Oracle, and Adobe were all spending hundreds of millions of dollars to buy social media management capabilities, it confirmed that the category was real and that large enterprises were going to spend significant budgets here. Sprinklr's pitch to customers became: "Why buy a stitched-together platform when you can buy a purpose-built one?"

Sprinklr was not entirely acquisition-averse, however. In 2016, the company acquired TBG Digital, a social advertising technology firm based in London, to bolster its paid media capabilities. This was a targeted acquisition that filled a specific product gap rather than an attempt to buy revenue or market share. The social advertising space was booming, with brands pouring billions into Facebook, Instagram, and Twitter ad campaigns, and enterprises needed tools to manage these campaigns at scale across multiple brands and geographies. TBG gave Sprinklr those capabilities and expanded its European footprint.

The pattern was instructive: Sprinklr would build organically where it could and acquire surgically where it needed to accelerate. This was the opposite of the Salesforce approach, which was to acquire broadly and integrate later. Thomas believed that maintaining a single codebase and a unified data model was worth the slower pace of organic development, because the integration headaches that plagued acquired-product portfolios were exactly the problem that Sprinklr's customers were trying to escape.

The cultural challenge during this hypergrowth phase was immense. Sprinklr scaled from roughly 100 employees to over 1,000 in just a few years. Thomas later acknowledged that this rapid scaling nearly destroyed the company's culture. In one particularly dramatic episode, he fired approximately 300 employees and replaced them with 400 new hires in a single year after concluding that the company had "recruited for experience rather than culture." The experience prompted Thomas to develop "The Sprinklr Way," a cultural framework built with input from outside researchers, clients, and former employees. Whether this was visionary leadership or founder-driven chaos depended on who was telling the story.

What was undeniable was the result. By 2016, Sprinklr had established itself as the leading independent enterprise social media management platform, with a billion-dollar-plus valuation, a roster of the world's most recognizable brands, and a product roadmap that was about to pivot dramatically. The social media management category was beginning to commoditize, and Thomas could see it coming. The next chapter would require Sprinklr to become something much bigger.

VI. The Second Inflection Point: Pivot from Social to Unified CXM (2016-2019)

In April 2017, Sprinklr made an announcement that, at the time, seemed like marketing rebranding but would prove to be the most consequential strategic decision in the company's history. The company launched five extensions of its Experience Cloud, with new solutions for marketing, advertising, research, care, and commerce, all unified on what Sprinklr called "the first unified platform for customer experience management."

The timing was not accidental. By 2016, the social media management category was beginning to mature and commoditize. The tools for scheduling posts, monitoring mentions, and running basic social analytics were becoming table stakes. Hootsuite had them. Salesforce Social Studio had them. A dozen smaller vendors had them. If Sprinklr stayed confined to social media management, it would find itself competing on price in a market with diminishing differentiation.

Thomas saw a much larger opportunity. The typical Chief Marketing Officer at a Fortune 500 company was managing somewhere between thirty and fifty different marketing technology tools with no integration between them. One tool for email campaigns, another for social listening, another for advertising, another for customer surveys, another for the contact center, another for competitive intelligence. Each tool had its own data silo, its own login, its own vendor relationship, and its own version of the truth about who the customer was and what they wanted. The result was a fragmented, often contradictory customer experience that frustrated consumers and drove executives crazy.

Think of it this way: imagine running a hospital where the radiology department, the pharmacy, the emergency room, and the billing office all used different patient record systems that could not talk to each other. Every time a patient moved between departments, the staff would have to re-enter information, sometimes getting it wrong, sometimes losing it entirely. That is essentially what the marketing and customer experience technology stack looked like at most large enterprises in 2016. Sprinklr's bet was that it could become the unified patient record system for the entire customer experience.

The expansion was technically ambitious. Sprinklr had to build or significantly enhance its advertising platform, its consumer research tools, its customer care and contact center capabilities, and its commerce features, all while maintaining the depth of its social media management product. The engineering investment was massive, and it meant that Sprinklr was competing not just with social media tools but increasingly with the customer service platforms, advertising platforms, and research tools of much larger competitors.

The "front office" thesis deserves a moment of explanation, because it captures the ambition of the pivot. Enterprise software has historically been organized around the "back office," functions like finance, HR, and supply chain managed by ERP systems from SAP and Oracle, and the "front office," functions like sales, marketing, and customer service managed by CRM systems from Salesforce and others. Thomas argued that neither ERP nor traditional CRM adequately served the modern front office, because neither was designed for the real-time, multi-channel, AI-driven customer interactions that defined modern customer experience. Sprinklr would be the operating system for the front office, the platform that unified every customer-facing function into a single, intelligent system.

The early results were encouraging. McDonald's began using Sprinklr not just for social media but for aggregating drive-thru feedback and operational customer insights. Microsoft used the platform for product development insights, mining social conversations to understand what features customers wanted. These expanded use cases validated the thesis that enterprises would pay more for a unified view of the customer across all touchpoints.

But the risk was real. By expanding into care, advertising, and research, Sprinklr was now competing with Salesforce Service Cloud, Adobe Experience Cloud, and Oracle's marketing suite on their home turf. These were companies with tens of billions of dollars in annual revenue, massive sales forces, and deep existing relationships with the same CIOs and CMOs that Sprinklr was selling to.

The competitive dynamics of this period deserve careful examination. Sprinklr was not the only vendor claiming to offer unified customer experience capabilities. Salesforce had assembled its Customer 360 vision through acquisitions. Adobe was building Experience Cloud around its analytics, personalization, and content management strengths. Oracle had its own marketing cloud. But each of these larger vendors was working with the integration tax of acquired products: different codebases, different data models, different user interfaces stitched together with middleware. The unified experience they promised was often aspirational rather than actual. Sprinklr's advantage was that its platform had been built as a single system from the ground up. There was no integration layer because there was nothing to integrate. This architectural purity was a genuine technical differentiator, though it was difficult to communicate in a sales demo.

The saving grace was timing. Between 2016 and 2019, enterprise "digital transformation" budgets exploded. Every CEO in the Fortune 500 was talking about customer-centricity. Every board was asking whether the company had a digital strategy. This was not just buzzword compliance. The companies that figured out how to deliver seamless, personalized customer experiences across digital and physical channels were winning market share. The ones that did not were watching their NPS scores drop and their customers defect to digitally native competitors.

Sprinklr positioned itself at the center of this transformation. The company invested heavily in AI and machine learning capabilities, building sentiment analysis engines that could understand the emotional tone of millions of social media posts in real time, chatbots that could handle routine customer inquiries, and predictive analytics that helped brands anticipate customer behavior. These AI capabilities were not bolt-on features. They were woven into the fabric of the unified platform, operating across social, care, marketing, and research simultaneously. Every customer interaction, whether it was a tweet, a chatbot conversation, or a survey response, fed into the same AI models, making them smarter over time.

The pivot from social media management to unified CXM was the defining strategic move of Sprinklr's history. It transformed the company's total addressable market from a few billion dollars to, by the company's own estimation, over $80 billion. It also transformed the competitive dynamics, the customer conversation, and the demands on Sprinklr's product and engineering teams. Whether the company could execute on this vastly larger ambition remained the central question heading into 2019.

VII. The Pandemic Acceleration & Path to IPO (2019-2021)

By late 2019, Sprinklr's unified CXM pivot was gaining traction with customers, but the company needed capital to accelerate. The competitive window was narrowing as Salesforce, Adobe, and Microsoft all invested heavily in their own customer experience capabilities. Thomas needed a partner with deep pockets, enterprise software expertise, and a long-term horizon.

In September 2020, Hellman & Friedman, one of the most respected private equity firms in technology, invested $200 million in primary capital into Sprinklr at a valuation of $2.7 billion. The firm also purchased approximately $300 million in secondary stakes from early investors, bringing total capital committed to roughly $500 million. Additionally, Sixth Street Growth provided $150 million in convertible securities. It was a massive vote of confidence, and it gave Sprinklr the war chest to pursue its unified CXM ambitions at scale.

Then COVID-19 rewrote the rules of customer engagement overnight.

When the pandemic hit in March 2020, digital channels did not just grow in importance. For many industries, they became the only channels. Retail stores closed. Airline counters emptied. Hotel lobbies went dark. Bank branches locked their doors. Suddenly, every customer interaction, every complaint, every question, every purchase decision, was happening through digital and social channels. The volume of customer service inquiries flowing through social media, chat, and messaging platforms exploded.

For Sprinklr, this was the ultimate stress test, and the ultimate validation. The company's unified platform, which skeptics had questioned as overly ambitious, proved its worth precisely because it could handle customer interactions across every digital channel from a single pane of glass. Companies that had been managing social media, email, chat, and phone through separate systems were suddenly drowning in volume, and they had no way to coordinate their responses. Sprinklr customers, by contrast, could see every customer interaction in one place, route inquiries to the right team regardless of channel, and scale their response capacity in days rather than months. Airlines used the platform to manage the tsunami of flight cancellation and rebooking inquiries flooding their social channels. Hotels deployed Sprinklr for crisis communications, updating guests across dozens of countries in real time as travel restrictions changed daily. Government agencies used the platform for public health messaging, monitoring social media for misinformation and coordinating rapid response communications.

The pandemic did not just accelerate Sprinklr's growth. It fundamentally shifted the conversation in the C-suite. Before COVID, digital transformation was important. After COVID, it was existential. CFOs who had been reluctant to approve six-figure software expenditures for customer experience suddenly understood that their companies' survival depended on meeting customers where they were: online, on mobile, on social media.

The financial impact was significant. The acceleration in digital customer engagement drove both new customer acquisition and expansion within existing accounts, as companies that had been using Sprinklr for social media management suddenly needed the platform for customer care, crisis communications, and digital advertising as well.

Against this backdrop, Sprinklr made the decision to go public. On June 23, 2021, the company listed on the New York Stock Exchange under the ticker symbol CXM, deliberately chosen to reflect the unified customer experience management identity rather than any association with social media. The IPO raised approximately $266 million, with the company priced at $16 per share. At its post-IPO peak, Sprinklr's market capitalization exceeded $5 billion.

The choice of ticker symbol was telling. The company could have chosen something referencing social media, which was still the core of its brand recognition. Instead, it chose CXM, a deliberate signal to the market that Sprinklr saw itself as a customer experience management company, not a social media tool. This branding decision reflected the strategic pivot that had been years in the making and would define the company's post-IPO identity.

The financial snapshot at the time of the IPO told a story of scale with lingering questions. Subscription revenue was growing at roughly 25 percent year-over-year. The customer base included over 1,400 of the world's largest brands. Average contract values were well into six figures. But the company was still burning cash after twelve years of operation, and the path to profitability remained aspirational rather than concrete.

The initial market reception was enthusiastic, buoyed by the frothy SaaS multiples of 2021 when growth-at-all-costs was still the prevailing investor religion. Snowflake was trading at fifty times revenue. CrowdStrike at forty times. The entire SaaS sector was priced for a future where hypergrowth would continue indefinitely and profitability could wait. Sprinklr, with its impressive customer roster and large addressable market, fit neatly into this narrative.

But that enthusiasm would prove short-lived. The SaaS valuation correction was coming, and it would hit Sprinklr particularly hard. For a company that had spent twelve years prioritizing growth and product development over profitability, the shift in investor expectations would be abrupt and unforgiving. The market was about to demand something that Sprinklr had never delivered: profitable growth.

VIII. Post-IPO Reality & The Profitability Pivot (2021-2024)

The reckoning came swiftly. The Federal Reserve began raising interest rates aggressively in 2022, and virtually overnight, the market's appetite for unprofitable growth stocks evaporated. The SaaS sector, which had enjoyed years of expansion multiples fueled by near-zero interest rates and the pandemic-driven digital acceleration, experienced a brutal correction. Revenue multiples contracted by 60-70 percent across the sector. Sprinklr, as an unprofitable SaaS company with decelerating growth, was hit particularly hard. From its post-IPO highs, the stock fell more than 60 percent, punishing long-term believers and frustrating the early investors who had held through the IPO. The question that analysts and investors had been politely asking for years, "When will Sprinklr be profitable?", was now being asked with considerably less politeness.

Thomas responded with what the company framed as disciplined execution. Cost optimization measures were implemented across the organization. Headcount growth slowed. The company initiated its first round of layoffs in June 2022, cutting approximately 60 employees from the marketing department. In February 2023, another four percent of the workforce, roughly 100 employees, was let go. Thomas described it as a transition to a "productivity-driven" model.

The strategic focus during this period shifted decisively toward proving that Sprinklr's unified platform thesis could generate not just revenue growth but sustainable margins. The company doubled down on its AI investments, launching Sprinklr AI+ as an integrated layer combining proprietary predictive AI models with generative AI capabilities from OpenAI and Google. The thesis was that AI would simultaneously reduce Sprinklr's cost to serve customers and increase the value those customers received, a virtuous cycle that could bend the margin curve upward.

Meanwhile, the product strategy underwent significant refinement. The sprawling feature set was consolidated into four clear pillars: Sprinklr Social, Sprinklr Service, Sprinklr Marketing, and Sprinklr Insights. This simplification was not just cosmetic. It made the sales conversation clearer, reduced product overlap, and allowed customers to understand exactly what they were buying and why. The company also launched Sprinklr Copilot, an always-on AI assistant for customer-facing teams, and began building AI Agents, a low-code platform for creating purpose-built AI bots across marketing, care, and commerce use cases.

The competitive landscape was evolving rapidly. Microsoft launched Dynamics 365 Contact Center in July 2024, a "Copilot-first" solution that directly entered Sprinklr's contact-center-as-a-service territory. Salesforce continued to invest heavily in Service Cloud. Adobe deepened its Experience Cloud capabilities. These were not distant threats. They were direct competitors with vastly greater resources, broader customer relationships, and the ability to bundle CXM capabilities into larger platform deals at little or no incremental cost.

The financial trajectory began showing improvement. Revenue climbed from $618 million in fiscal year 2023 to $732 million in fiscal 2024, an 18 percent growth rate. Non-GAAP operating margins turned positive. Free cash flow improved. But the stock continued to languish, reflecting the market's uncertainty about whether Sprinklr could sustain growth rates high enough to justify its valuation while simultaneously expanding margins.

Customer wins during this period told their own story. Samsung became an official Sprinklr software partner, integrating the platform into its SMART Signage and Hospitality Displays. BT, the British telecommunications giant, selected Sprinklr for unified customer experience management across its operations. These were not just revenue events; they were strategic proof points that Sprinklr's platform could extend beyond social media into broader enterprise workflows. The Samsung partnership, in particular, demonstrated that Sprinklr's data and content capabilities had applications far beyond the traditional CXM use case.

Then came the leadership transition that would redefine Sprinklr's trajectory. In June 2024, the company moved to a co-CEO structure with Thomas and Trac Pham, the former CFO, sharing the top role. The arrangement lasted less than five months. In November 2024, Sprinklr scrapped the co-CEO experiment and appointed Rory Read as sole President and CEO. Thomas transitioned to Chairman of the Board and Advisor to the CEO.

Read's appointment was deeply significant, and investors who studied his background understood exactly what it signaled. Read had previously served as CEO of Vonage Holdings, where he executed a transformation playbook that culminated in Ericsson's $6.2 billion acquisition of the company. Before Vonage, Read led the historic Dell-EMC integration that created Dell Technologies, and he held senior leadership roles at AMD, IBM, and Lenovo. His career was defined by a consistent pattern: walk into a company with a valuable but underperforming asset, optimize operations, sharpen the go-to-market, and position the business for maximum strategic value, whether through accelerated growth or an eventual exit.

The implications were unmistakable. When you hire a CEO whose most prominent achievement was selling a company for $6.2 billion, the market pays attention.

Read wasted no time putting his stamp on the company. In February 2025, Sprinklr executed its largest-ever layoff, cutting approximately 15 percent of the workforce, roughly 500 employees. Read acknowledged that the company had "spread itself too thin" and needed to realign its cost structure with its strategic priorities. The restructuring was designed to redirect investment toward the Service product suite, which Read views as the key differentiator, and toward the go-to-market organization. Read described his approach as a three-phase transformation: first optimize the business, then deepen engagement with the top 500 customers through what he calls "Project Bear Hug," and finally accelerate growth by investing heavily in marketing and sales positioning. The parallels to his Vonage playbook were explicit and intentional.

Fiscal year 2025, which ended in January 2025, showed a company in transition. Revenue grew 9 percent year-over-year to $796 million, a meaningful deceleration from the 18 percent growth in fiscal 2024. Subscription revenue, which accounts for 91 percent of the total, continued to grow but at a moderating pace. Non-GAAP operating income was $33.5 million, positive but modest. The company guided fiscal year 2026 revenue to approximately $854 million. These were not the numbers of a hypergrowth story; they were the numbers of a mature enterprise software company working to balance growth and profitability while undergoing a leadership transition.

IX. The Business Model & What Makes Sprinklr Different

To understand why Sprinklr's enterprise customers stay despite the aggressive competitive landscape, it helps to understand what "unified" actually means in technical terms, and why it matters so much more than it sounds.

Most enterprise software is built as a collection of individual products that are stitched together through integrations after the fact. Imagine a house where each room was designed by a different architect, built by a different contractor, and uses a different electrical system. You can connect them with extension cords and adapters, but the wiring is never native. Data does not flow naturally. Each room has its own version of who lives in the house.

Sprinklr's architecture was built differently. From the beginning, the platform was designed as a single codebase with a unified data model. When a customer tweets a complaint, that interaction lives in the same data layer as their chatbot conversation from last week, their survey response from last month, and their ad engagement from this morning. Marketing, customer service, advertising, and research all see the same customer, in real time, without the latency and data loss that comes from integrating separate systems.

This architectural decision is what makes Sprinklr sticky. Once a large enterprise has deployed the platform across multiple departments and geographies, migrating away means not just replacing software but unwinding years of accumulated data, workflows, compliance configurations, and institutional knowledge. The switching cost is enormous.

Sprinklr's revenue is overwhelmingly subscription-based, accounting for approximately 91 percent of total revenue in fiscal 2024, with professional services making up the remainder. The company targets the Global 2000, with average annual contract values well above $250,000 and some customers paying substantially more. The go-to-market model is traditional enterprise sales: no product-led growth, no freemium tier, no self-serve onboarding. Sales cycles can stretch multiple quarters, involving demos, proofs of concept, security reviews, and procurement negotiations.

The land-and-expand playbook typically starts with one product suite, often Sprinklr Social, deployed in one department or geography. As the initial deployment proves value, the contract expands to additional suites, additional departments, and additional geographies. This expansion dynamic drives the net dollar retention rate above 100 percent.

Partnership strategy plays a critical role. Sprinklr maintains relationships with major systems integrators including Accenture, Deloitte, and IBM, who help deploy the platform in complex enterprise environments. Technology partnerships with Microsoft and AWS provide cloud infrastructure and marketplace distribution. An interesting wrinkle: Microsoft is simultaneously one of Sprinklr's largest customers, a cloud infrastructure partner through Azure, and an emerging competitor through Dynamics 365. This kind of "frenemy" relationship is common in enterprise software, but it underscores the complexity of Sprinklr's competitive position.

The geographic mix tells an important story about both the company's current business and its future opportunity. Approximately 59 percent of revenue comes from the Americas and 41 percent from the rest of the world, with customers spread across more than eighty countries. This international mix has been remarkably stable over recent fiscal years, suggesting that the company has found a natural equilibrium between its domestic and international business. The international business is heavily supported by channel partners and systems integrators who provide localized delivery in regulated industries.

One challenge that bears mentioning is the services burden. Enterprise deployments of Sprinklr require significant implementation effort, customization, training, and ongoing optimization. This high-touch model limits how quickly the company can scale and puts pressure on professional services margins. It is the classic tradeoff of enterprise software: deep customer relationships and high retention, but also high cost to acquire and serve each customer.

For investors tracking Sprinklr's ongoing performance, two KPIs matter above all others. First, net dollar retention rate, which measures whether existing customers are spending more or less over time and serves as the single best indicator of product-market fit and platform stickiness in enterprise SaaS. Second, subscription revenue growth rate, which captures both new customer acquisition and expansion, stripping out the lower-margin services business. These two metrics, taken together, reveal whether Sprinklr's unified platform thesis is translating into durable, compounding revenue, or whether growth is decelerating toward a ceiling.

X. Key Strategic Challenges & Controversies

No company story is complete without examining the tensions and fault lines beneath the surface. Sprinklr has several, and understanding them is essential for any investor evaluating the business.

The founder control question looms large. Through Sprinklr's dual-class share structure, Ragy Thomas holds approximately 43.5 percent of total voting power via his Class B shares, even after stepping down as CEO. Hellman & Friedman controls roughly 45 percent of voting rights through its significant equity stake. Together, these two parties hold approximately 88-89 percent of all voting power, making Sprinklr's governance effectively a two-party arrangement. This concentration has implications: a hostile acquisition bid is virtually impossible, and any strategic transaction, whether a sale, a merger, or a take-private deal, requires the agreement of Thomas and Hellman & Friedman.

There are additional governance considerations worth noting. According to SEC filings, Sprinklr made payments totaling approximately $200,000 to Lyearn Inc., a company wholly owned by Ragy Thomas, for "digital training services." The audit committee reviewed and approved the transaction, but related-party dealings between a company and entities controlled by its founder and controlling shareholder always warrant scrutiny. There were also Section 16(a) filing lapses where Thomas underreported share sales in insider trading filings, later corrected, but indicative of governance gaps.

Workplace culture has been a persistent topic of discussion. Sprinklr's Glassdoor rating sits at 3.4 out of 5.0, with only 53 percent of reviewers saying they would recommend the company to a friend. Common critiques include a high-pressure environment, particularly in the India operations where approximately 59 percent of the workforce is based, frequent management changes, and a pattern of aggressive hiring followed by layoffs. The February 2025 layoff, which cut approximately 15 percent of the workforce or roughly 500 employees, was the most significant. New CEO Rory Read acknowledged that Sprinklr had "spread itself too thin," and the restructuring was designed to realign costs with strategic priorities, particularly the Service product suite.

The product complexity debate is another enduring challenge. Sprinklr's critics argue that the platform tries to do too many things, the "Swiss Army knife" problem. In a market where enterprises can buy best-of-breed tools for specific functions, social listening from Brandwatch, customer service from Zendesk, advertising from The Trade Desk, why pay a premium for an integrated platform that may not be the absolute best at any single function? Sprinklr's counter-argument is that the integration itself is the value: the elimination of data silos, the unified customer view, the reduced vendor management overhead. Both arguments have merit, and the tension between unified platforms and best-of-breed point solutions remains one of the fundamental strategic debates in enterprise software.

The build-versus-buy question deserves honest examination. Several moments in Sprinklr's history presented natural acquisition exit points. When Salesforce was buying Buddy Media and Radian6, Sprinklr could have been part of that consolidation wave. When Microsoft, Adobe, or Oracle were building out their customer experience stacks, Sprinklr's unified platform would have been a logical acquisition. Thomas chose independence each time, betting that the standalone opportunity was larger. That bet created a company with nearly $800 million in annual revenue, but it also created a company that now trades at a market capitalization of roughly $1.4 billion, below the $2.7 billion private valuation Hellman & Friedman paid in 2020. Whether independence was the right call depends entirely on what happens next.

The SMB question continues to surface in every analyst discussion. Could Sprinklr have grown faster if it had built a downmarket product? The argument for is straightforward: the total addressable market expands dramatically when you include mid-market and smaller enterprises, and product-led growth models have proven remarkably efficient at capturing these segments. Companies like HubSpot and Zendesk have built multi-billion-dollar businesses by starting with SMBs and moving upmarket. The counterargument is that Sprinklr's entire value proposition, governance, compliance, global scale, multi-department orchestration, is irrelevant to a company with fifty employees and one social media manager. Building a simplified product for SMBs would have required a separate engineering team, a separate sales motion, and a separate brand, all of which would have diverted resources from the enterprise mission. Thomas chose depth over breadth, and that choice, whether ultimately right or wrong, defined the company.

Data privacy and compliance represent both a competitive advantage and an ongoing cost. Sprinklr's enterprise customers demand GDPR compliance, regional data sovereignty, and rigorous security certifications. Meeting these requirements across eighty-plus countries requires significant ongoing investment in infrastructure and compliance teams. But it also creates a barrier to entry that smaller competitors struggle to match, reinforcing Sprinklr's position with the most demanding enterprise buyers.

XI. Porter's Five Forces Analysis

Stepping back from the narrative to evaluate Sprinklr through the lens of industry structure reveals a business operating in a genuinely difficult competitive environment, but one with pockets of defensibility that are easy to overlook. Michael Porter's framework, despite its age, remains the most rigorous way to assess the structural attractiveness of an industry and a company's position within it.

Competitive rivalry is intense. The customer experience management market is fragmented across several categories: CRM (Salesforce), digital experience platforms (Adobe), enterprise communications (Microsoft), customer service (Zendesk, NICE), social media management (Hootsuite, Khoros), experience management (Qualtrics), and contact center platforms (Genesys, Five9). Sprinklr competes at the intersection of all of these categories, which means it faces different competitors in different product conversations. In a Gartner Magic Quadrant for Content Marketing, Sprinklr is a Leader. In the Forrester Wave for contact center platforms, it is a Strong Performer but not yet a Leader. This unevenness reflects the reality of competing across a broad surface area. The intensity of rivalry compresses pricing power and forces continuous R&D investment.

The threat of new entrants is moderate. Building an enterprise-grade CXM platform requires years of investment in security certifications, compliance frameworks, API integrations with dozens of social and messaging platforms, and the institutional knowledge of how Fortune 500 companies actually operate. These are substantial barriers. However, cloud infrastructure has democratized the technical foundations of software development, and AI is lowering the cost of building sophisticated capabilities. A well-funded startup with a compelling AI-native approach could theoretically bypass years of legacy development. The barrier is not insurmountable, but it remains meaningful.

Supplier power deserves careful and perhaps underappreciated attention. This is a force that many analysts overlook when evaluating Sprinklr, but it may be among the most consequential. Sprinklr's platform depends on API access to social platforms like Meta, X (formerly Twitter), TikTok, and others. If any of these platforms restricts or revokes API access, Sprinklr's ability to deliver core functionality would be impaired. This is not a theoretical risk. Twitter's API pricing changes under Elon Musk's ownership disrupted the entire social media management ecosystem. Cloud infrastructure providers (AWS, Azure) represent another supplier dependency, though these are largely commoditized. Talent is a third dimension of supplier power: Sprinklr competes for AI and engineering talent in a market where compensation expectations have skyrocketed.

Buyer power is significant. Sprinklr's customers are among the world's largest enterprises, and they negotiate accordingly. These are procurement departments with sophisticated vendor management processes, demanding ROI proof, volume discounts, and favorable contract terms. Post-pandemic budget scrutiny has only intensified this dynamic, with CFOs demanding vendor consolidation and clear returns on every software dollar. The counterbalance is switching costs: once a large enterprise has deployed Sprinklr across multiple departments and geographies, the cost and disruption of migrating away are substantial enough to provide significant stickiness.

The threat of substitutes is perhaps the most nuanced and strategically important force. Best-of-breed point solutions represent the most obvious substitute: cheaper, faster to implement, and often best-in-class for a specific function. In-house builds are another risk, particularly for the most tech-savvy enterprises that have the engineering talent to construct custom solutions. And there is a more existential substitution risk: what happens if the social media landscape itself shifts dramatically? If new platforms emerge, existing platforms decline, or consumer communication patterns move to channels that Sprinklr does not cover, the value of the platform diminishes.

XII. Hamilton's 7 Powers Analysis

While Porter's framework assesses industry structure, Hamilton Helmer's 7 Powers framework zeroes in on the sources of durable competitive advantage for an individual company. The picture it reveals for Sprinklr is instructive, and in some ways more sobering than the Porter analysis.

Scale Economies are moderate, and this is worth dwelling on because it reveals a fundamental constraint of enterprise software businesses. Sprinklr's R&D investment, which represents the bulk of its technology advantage, is amortized across a growing but still limited customer base of roughly 1,900 enterprises. As that base grows, the per-customer cost of R&D development decreases, creating a scale advantage. However, implementation and professional services costs scale more linearly with customer count, limiting the overall scale benefit. Compared to a consumer SaaS company with millions of users, Sprinklr's scale economies are real but constrained.

Network Effects are limited, which is one of the key structural challenges of the business. Sprinklr is not a marketplace or a platform where users interact with each other in ways that create self-reinforcing value. There are modest data network effects: more customer interactions flowing through the platform means better AI models, better benchmarking data, and more refined insights. But these are incremental advantages, not the kind of explosive, winner-take-all network effects that define companies like Meta or Uber. A new Sprinklr customer does not make the platform meaningfully more valuable for existing customers in the way that a new Instagram user makes Instagram more valuable for everyone. This is a fundamental limitation of B2B enterprise software, and it means that Sprinklr must compete on product quality, switching costs, and execution rather than on network-driven momentum.

Counter-Positioning has faded from its early potency, and understanding why is critical for assessing Sprinklr's future. In Sprinklr's early years, incumbent CRM and marketing vendors genuinely could not match the unified approach. Their existing products, organizational structures, and incentive systems were oriented around individual product lines. Salesforce's sales compensation, for instance, rewarded representatives for selling Service Cloud or Marketing Cloud as separate products, not for selling a unified customer experience vision. They had been built for a pre-social world and would have had to cannibalize existing product lines to replicate what Sprinklr was building from scratch. This was classic counter-positioning: the incumbent's rational response to the new entrant's strategy was to do nothing, because matching the entrant would damage the incumbent's existing business. But over the past decade, the incumbents have caught up through acquisitions and organic development. Salesforce's Customer 360, Adobe's Experience Cloud, and Microsoft's Dynamics 365 suite all offer multi-product customer experience capabilities. The counter-positioning advantage has not disappeared entirely, but it has diminished significantly.

Switching Costs are Sprinklr's strongest Power. Enterprise customers who have deployed Sprinklr across multiple departments, geographies, and use cases face enormous costs to migrate away. The switching cost includes not just the technology migration itself but the loss of historical data, the retraining of hundreds or thousands of employees, the redesign of workflows and compliance processes, and the organizational disruption of changing a tool that touches customer-facing teams across the entire company. Multi-year contracts enforce this stickiness contractually, but the real barrier is operational. This is the Power that underpins Sprinklr's 90-plus-percent gross retention rate and is the primary reason Fortune 100 customers stay even when competitive alternatives emerge.

Branding is moderate, concentrated within a narrow but influential circle. Among enterprise CXM buyers, CMOs, CIOs, and customer experience leaders at large companies, Sprinklr has strong brand recognition. Gartner Leader positions reinforce this. But outside that narrow audience, the brand carries no weight. This is typical for B2B infrastructure companies and is not necessarily a weakness, but it does mean that Sprinklr cannot rely on brand pull to open doors the way a Salesforce or Microsoft can.

Cornered Resource is limited, and this limitation has become more acute with the leadership transition. Ragy Thomas's product vision and deep expertise represent a unique asset, but with Thomas stepping back from the CEO role, this resource is partially depleted. Sprinklr has proprietary AI models trained on years of customer interaction data, which provide some differentiation. But there are no exclusive platform access agreements, no patents of significant defensive value, and no other resources that competitors cannot eventually replicate or work around.

Process Power is emerging and may become Sprinklr's second-strongest Power over time. More than a decade of deploying complex enterprise software across the world's largest companies has created institutional knowledge about how to implement, customize, optimize, and support CXM platforms at scale. The company's AI models, trained on billions of customer interactions across diverse industries and geographies, represent a form of process power that is difficult to replicate quickly. As Rory Read implements his operational transformation, this process power could become more formalized and defensible.

The overall strategic picture is a company whose competitive position rests primarily on switching costs, with process power as an emerging secondary advantage. This is a viable position, many successful enterprise software companies sustain for decades on switching costs alone, but it is also a vulnerable one. The specific risk for Sprinklr is that competitors like Microsoft and Salesforce can offer integrated CXM capabilities as part of broader platform deals at lower or bundled prices, effectively subsidizing their CXM products with profits from other parts of their portfolio. When a CIO is deciding between paying $500,000 for Sprinklr or adding customer experience capabilities to an existing $50 million Microsoft Azure contract for an incremental $200,000, the math is difficult for the standalone vendor. This bundling dynamic is arguably the single greatest long-term threat to Sprinklr's competitive position, and it is the reason that scale economies and switching costs alone may not be sufficient to defend the business indefinitely.

XIII. Bull vs. Bear Case

The Bull Case for Sprinklr begins with what may be the most compelling thesis in enterprise software: the AI data advantage. In an era where artificial intelligence capabilities are rapidly democratizing through foundation models available to everyone, the companies that will build the most valuable AI applications are those sitting on proprietary, domain-specific datasets. Generic AI can write a customer service response. But AI trained on twelve-plus years of actual customer interactions across thirty channels, spanning ninety-plus industries and eighty-plus countries, can write the right response for this specific customer, at this specific moment, in this specific context. That is the thesis. The generative AI revolution has made unified data platforms more valuable, not less. The quality of AI outputs depends directly on the quality and comprehensiveness of the data feeding them. Sprinklr sits on more than a decade of customer interaction data spanning social media, customer service, advertising, and research for the world's largest brands. That data, unified in a single model, could become the training ground for AI agents that are demonstrably better than anything a competitor can build from scratch. More data leads to better AI, which leads to stickier customers, which leads to more data. If this flywheel accelerates, Sprinklr's position strengthens over time.

The vendor consolidation trend supports the bull case. CFOs at large enterprises are actively reducing the number of software vendors they work with. Every vendor relationship carries overhead: procurement, security review, integration maintenance, training, contract management. When a company using eight different customer experience tools can replace them with one platform, the operational savings alone justify the switch, even if the unified platform is not best-in-class in every individual function. Sprinklr wins these consolidation RFPs because it is the only vendor offering true unification across social, service, marketing, and insights.

International expansion remains early. While 41 percent of revenue already comes from outside the Americas, the penetration in Asia-Pacific, the Middle East, and emerging markets is still nascent. These regions are experiencing the same digital transformation pressures that drove Sprinklr's growth in North America and Europe a decade ago. The company's multi-language, multi-channel platform is well-suited for these markets.

The retention dynamics provide a predictable revenue base. Gross retention rates above 90 percent mean that Sprinklr starts each year with the vast majority of last year's revenue already locked in. On this foundation, even modest growth in new customer acquisition and expansion drives steady revenue gains. And as the company's operational transformation under Rory Read takes hold, there is a clear path toward operating margins in the mid-twenties, which would transform the free cash flow profile.

The Bear Case is equally compelling. Microsoft and Salesforce represent existential competitive threats, not because their individual CXM products are necessarily superior, but because they can afford to bundle customer experience capabilities into larger platform deals. A CIO who is already spending $50 million annually with Microsoft on Azure, Office 365, and Dynamics can add contact center and customer experience capabilities at marginal incremental cost. Competing against a bundled offering from a hyperscaler is one of the most difficult positions in enterprise software.

The SMB market remains unreachable. Sprinklr's platform complexity and price point make it irrelevant for the vast majority of businesses. This is by design, but it caps the total addressable market to the largest enterprises and limits the growth rate ceiling.

AI is a double-edged sword. While Sprinklr's accumulated data is an asset, generative AI is simultaneously democratizing capabilities that used to be differentiating. Sentiment analysis, automated responses, and customer insights that required years of proprietary AI development can now be built in weeks using foundation models. If AI reduces the gap between what Sprinklr offers and what a startup can build from scratch, the company's moat narrows.

The leadership transition introduces uncertainty. Ragy Thomas ran Sprinklr for fifteen years. Rory Read is a proven operator, but his track record is in optimization and exits, not in building category-defining products. If Sprinklr needs to innovate its way to the next level, the question is whether a transformation-focused CEO is the right leader, or whether the company is being positioned for a sale.

The valuation context adds a final dimension. Sprinklr trades at approximately $5.82 per share as of late February 2026, giving it a market capitalization of roughly $1.4 billion. That is less than two times trailing revenue, a significant discount to SaaS peers, where median multiples for profitable, growing software companies tend to range from four to eight times revenue. The company holds approximately $480 million in cash, meaning the enterprise value is barely one times revenue. For context, when Hellman & Friedman invested in 2020, the private valuation was $2.7 billion, nearly double the current public market capitalization. This gap between private and public valuation tells a story about the market's reassessment of Sprinklr's growth trajectory and competitive position.

The macro environment adds pressure from multiple directions. Enterprise software budgets remain under scrutiny as companies grapple with economic uncertainty, and multi-quarter sales cycles mean that any improvement in market conditions takes time to flow through to Sprinklr's revenue. At the same time, the AI investment cycle is creating new budget pools that did not exist two years ago, and Sprinklr's positioning at the intersection of customer experience and AI could allow it to tap into these emerging budgets.

One additional consideration for the bear case: the workforce dynamics bear watching. Sprinklr's heavy concentration of employees in India, approximately 59 percent of the total workforce, creates both cost advantages and operational risks. The India technology labor market has become intensely competitive, with attrition rates at major services companies regularly exceeding 20 percent annually. Multiple rounds of layoffs, culminating in the February 2025 cut, risk damaging employer brand perception in a market where word travels fast. Maintaining engineering and customer success talent quality while managing costs is a balancing act that gets harder with each restructuring cycle.

XIV. The Playbook: Lessons for Founders & Investors

The Sprinklr playbook offers a rich set of strategic lessons that extend well beyond the specifics of customer experience management and resonate across enterprise software more broadly.

Category creation pays off, but it demands extraordinary patience. When Ragy Thomas founded Sprinklr in 2009, the category of "unified customer experience management" did not exist. He had to simultaneously build the product, educate the market, and convince the world's largest companies that they needed something they did not know they needed. This is the hardest thing to do in business. It took more than a decade and hundreds of millions of dollars in venture capital before Sprinklr achieved the scale and market recognition that validated the category bet. For founders considering a category creation strategy, the lesson is clear: you need patient capital, an unshakeable thesis, and the emotional resilience to keep building during the years when the market does not yet understand what you are selling.

Enterprise-first is a legitimate strategy, despite Silicon Valley's obsession with bottoms-up growth. The dominant startup narrative of the 2010s and early 2020s celebrated product-led growth: build something freemium, let individual users adopt it, and grow virally from the bottom up. Sprinklr rejected this entirely. The company never built a self-serve product, never offered a free tier, and never pursued the SMB market. This was not a mistake. It was a deliberate recognition that the problems Sprinklr solved, global compliance, multi-brand governance, cross-channel orchestration, simply did not exist outside the enterprise. Going downmarket would have been a distraction that diluted the product and confused the brand.

Switching costs are more valuable than network effects in enterprise software. In the consumer internet, network effects are the holy grail of competitive advantage. But in enterprise software, switching costs often provide a more durable and predictable moat. Sprinklr's customers stay not because the platform gets better with more users in some network-effects sense, but because the cost and disruption of leaving are prohibitive. Every year a customer stays, the switching cost grows: more historical data, more trained employees, more embedded workflows. This dynamic produces the kind of predictable, compounding revenue that long-term investors value.

The unified platform versus best-of-breed debate has no permanent winner. It oscillates. During periods of innovation, when new capabilities are emerging rapidly, best-of-breed tools tend to win because they move faster and offer cutting-edge features. During periods of consolidation, when enterprises are overwhelmed by tool sprawl and seeking operational efficiency, unified platforms win. Sprinklr has benefited from the consolidation trend, but it must continue to innovate within its unified platform to avoid losing customers to point solutions that leapfrog on specific capabilities.

Timing matters, and Sprinklr has ridden three waves. The company caught the social media wave in 2009, the digital transformation wave in 2016-2019, and is now positioned for the AI wave in 2024 and beyond. Each wave expanded the company's relevance and total addressable market. The ability to recognize and position for successive technology waves is a hallmark of enduring technology companies.

An IPO is not the finish line; it is a new set of constraints. Sprinklr's experience as a public company illustrates how market discipline can force better execution. The pressure to show profitability improvements, the scrutiny of quarterly earnings calls, and the transparency of public disclosure have all pushed Sprinklr toward more disciplined capital allocation and operational efficiency. This is painful for a founder-led company accustomed to investing heavily in long-term vision, but it can produce better outcomes for all stakeholders.

Retention is everything in enterprise SaaS. Losing a large enterprise customer is catastrophic, not just because of the revenue loss but because of the signal it sends to the market. When a Fortune 100 company leaves your platform, competitors use that departure as a sales weapon for years. Sprinklr's gross retention rate above 90 percent is the foundation of its business model. Every strategic decision, from product development to customer success to pricing, should be evaluated through the lens of its impact on retention.

The "optimize and sell" playbook is a legitimate outcome. Not every company needs to be the next Salesforce. Sometimes the highest-value outcome is building a company to the point where it becomes an attractive acquisition target for a larger platform. Rory Read's appointment and the Vonage parallel suggest this may be Sprinklr's path. If so, the company's value to investors will ultimately be determined by its acquisition price, not its standalone growth trajectory. This reframes the investment thesis entirely: the question is not whether Sprinklr can compete independently against Microsoft and Salesforce for the next twenty years, but whether its unified platform, customer base, and data assets are valuable enough that a larger acquirer will pay a premium to own them.

XV. Epilogue: What's Next for Sprinklr

As of early March 2026, Sprinklr stands at a crossroads that will determine whether the next decade looks like the first, or something entirely different.

The question hanging over the company is not whether it has a viable business. It does. Nearly $800 million in annual revenue, $480 million in cash, 1,900-plus enterprise customers including sixty percent of the Fortune 100, and Gartner Leader positions in multiple categories are not the hallmarks of a company in crisis.

The question is what Sprinklr becomes next, and who it becomes it for. Is this a company that will remain independent and compete its way to $2 billion in revenue and sustained profitability? Is it a company that will be acquired by a larger platform vendor looking to fill a customer experience gap? Or is it a company that private equity will take off the public markets to restructure away from quarterly scrutiny?

Rory Read's three-phase transformation plan provides the clearest roadmap. Phase one, business optimization, is underway: the 15 percent workforce reduction in February 2025, cost realignment, and operational tightening. Phase two, which Read has branded "Project Bear Hug," involves intensive engagement with Sprinklr's top 500 enterprise customers representing 90 percent of revenue, hardening the contact center product, and ensuring that the core customer base is deeply satisfied and expanding. Phase three, the acceleration phase, is targeted for calendar year 2026, when Read plans to invest aggressively in go-to-market and marketing, positioning Sprinklr Service as the differentiating platform within the broader suite.

The AI-native future represents both Sprinklr's greatest opportunity and its most demanding technical challenge. The company has launched Sprinklr AI Agents, a low-code platform for building purpose-built AI bots, and is developing vertical-specific AI solutions for eighteen industries including banking, retail, and telecommunications. The aspiration is to become the "AI brain" for enterprise customer experience: not just the system that stores and routes customer interactions, but the intelligence layer that predicts what customers want, automatically resolves routine inquiries, and surfaces insights that drive product and business decisions.