Curtiss-Wright: From Aviation Titans to Industrial Conglomerate

I. Introduction & Episode Roadmap

Picture this: It's 1944, and the sprawling Buffalo factory complex of Curtiss-Wright stretches across 282 acres, employing 45,000 workers who churn out P-40 Warhawk fighters at a rate that would make Henry Ford jealous. Fast forward to today, and Curtiss-Wright—yes, that Curtiss-Wright—doesn't make a single airplane. Instead, this $8 billion market cap company quietly produces the actuators that move Boeing 737 flight controls, the valves that regulate steam in nuclear submarines, and the surface treatments that keep fighter jet components from failing at Mach 2.The modern Curtiss-Wright, with $3.1 billion in 2024 sales and diluted EPS of $10.55, operates in a universe that Glenn Curtiss and the Wright brothers could never have imagined. It's a company that has survived—and thrived—through one of corporate America's most dramatic transformations. How does a company go from building the fighters that won World War II to making the unsexy but essential components that keep modern aircraft, nuclear submarines, and power plants running? That's the story we're unpacking today.

This is a tale of innovation, rivalry, boom and bust, technological disruption, and ultimately, corporate reinvention. It's about two bitter enemies whose companies merged at the worst possible time, created an industrial powerhouse that helped win a world war, then completely missed the jet age—and somehow emerged stronger for it. Along the way, we'll explore how Curtiss-Wright went from employing 180,000 workers during WWII to becoming today's lean, highly profitable industrial specialist with just 8,800 employees.

The journey touches on everything from the birth of aviation to nuclear submarines, from patent wars to production miracles, from the Wankel engine fiasco to today's defense modernization boom. It's a masterclass in corporate survival, strategic pivots, and the surprising value of becoming boring.

II. The Wright Brothers & Glenn Curtiss: Fierce Rivals

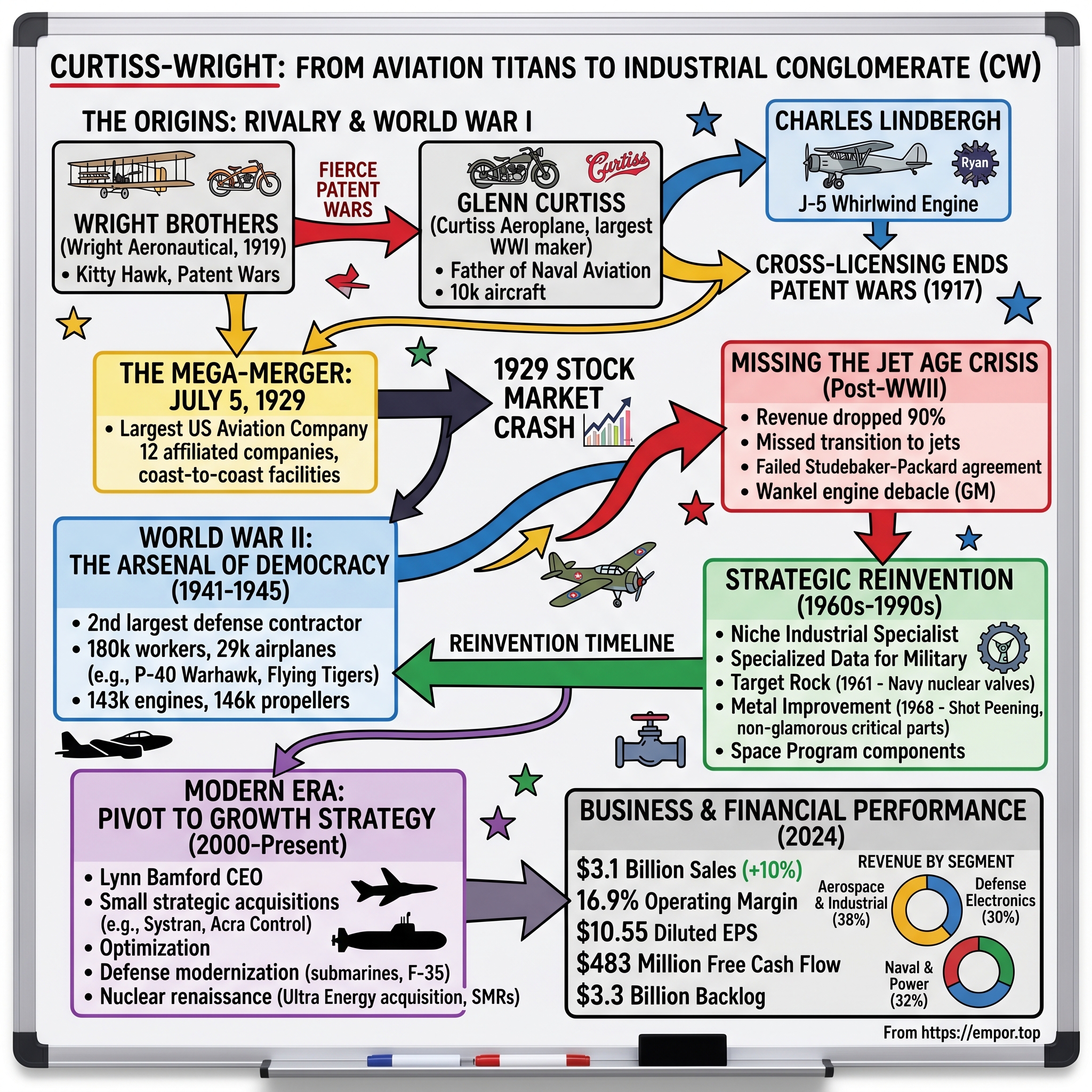

The morning of June 18, 1908, changed everything. Glenn Hammond Curtiss, a motorcycle speed demon from Hammondsport, New York, stood beside his contraption called the "June Bug" on a racetrack in upstate New York. The Aero Club of America officials were there to witness what many thought impossible: controlled flight of over one kilometer. Curtiss climbed aboard, fired up his engine, and flew 5,090 feet in 1 minute and 42.5 seconds. He'd just won the Scientific American Trophy and $2,500—but more importantly, he'd thrown down the gauntlet to the Wright brothers.

This wasn't supposed to happen. The Wrights had achieved first flight at Kitty Hawk in 1903, and they believed their patents covered all forms of controlled flight. Orville and Wilbur saw Curtiss not as a fellow pioneer but as a thief. What followed was one of the most vicious patent wars in American history—a battle that would paradoxically accelerate aviation development while nearly destroying both companies. Curtiss was unlike the methodical Wright brothers in every way. Where they were secretive and cautious, he was flamboyant and public—earning him the title "Father of Naval Aviation." Fascinated by speed, he became the fastest man on Earth on January 23, 1907, when he attained 136.3 miles per hour aboard one of his motorcycles at Ormond Beach, Florida. The Wrights were bicycle mechanics who approached flight like a physics problem. Curtiss was a daredevil who approached it like a business opportunity.

The patent wars were vicious. The Wrights claimed their 1906 patent for "wing warping"—their method of controlling flight by twisting the wings—covered all methods of lateral control, including Curtiss's ailerons (hinged surfaces at the wing edges that are still used today). From 1909 to 1917, the legal battles consumed both companies. The Wrights spent more time in courtrooms than in workshops. Curtiss spent fortunes on lawyers while trying to build a business. World War I proved the patent wars were a luxury America couldn't afford. By the end of World War I, the Curtiss Aeroplane and Motor Company would claim to be the largest aircraft manufacturer in the world, employing 18,000 in Buffalo and 3,000 in Hammondsport, New York. Curtiss produced 10,000 aircraft during that war, and more than 100 in a single week. The government essentially forced a cross-licensing agreement in 1917, ending the legal battles but leaving deep scars.

Meanwhile, on the Wright side, the brothers had sold their company in 1915 to a syndicate of New York financiers. Wilbur had died of typhoid in 1912, and Orville, exhausted by the patent fights, sold his interests and retired. Wright Aeronautical Corporation, incorporated in 1919, focused on engines rather than complete aircraft—a decision that would prove prescient. Wright's masterstroke came with the J-5 Whirlwind engine. Developed by Charles Lawrance and refined by Samuel Heron, the J-5 was revolutionary: 220 horsepower at just 1,800 rpm, with cooling so efficient it could run on a lean fuel mixture. On May 20, 1927, Charles Lindbergh took off from Roosevelt Field in his Ryan monoplane, powered by Wright J-5 Whirlwind Engine No. 7331. When he landed in Paris 33.5 hours later—the engine never missing a beat—Wright Aeronautical became the most famous engine company in the world overnight.

Lindbergh's flight was an international triumph for Wright Aeronautical. The Whirlwind engine never missed a beat. Lindbergh's feat made the J-5C the most popular engine for long distance air travel.

By the late 1920s, both companies had evolved beyond their founders' original visions. Curtiss had become a corporate empire focused on mass production. Wright had become an engineering powerhouse with the world's most reliable aircraft engines. Both were public companies with professional management. The stage was set for what should have been the perfect merger.

III. The 1929 Mega-Merger: Birth of an Aviation Giant

The Biltmore Hotel ballroom in New York City buzzed with excitement on July 5, 1929. Reporters jostled for position as Clement Keys, the Wall Street financier who orchestrated the deal, stepped to the podium. "Gentlemen," he announced, "today marks the creation of the largest aviation company in the world."

Curtiss-Wright formed on July 5, 1929, the result of a merger of 12 companies associated with Curtiss Aeroplane and Motor Company of Buffalo, New York, and Wright Aeronautical of Dayton, Ohio. It was headquartered in Buffalo, New York. With $75 million in capital (equivalent to $1.37 billion in 2024), it became the largest aviation company in the United States.

The numbers were staggering. The merger brought together 18 affiliated companies and 29 subsidiaries. The new Curtiss-Wright Corporation had manufacturing facilities from coast to coast, engineering talent that was the envy of the world, and order books thick with military and civilian contracts. There were three main divisions: the Curtiss-Wright Airplane Division, which manufactured airframes; the Wright Aeronautical Corporation, which produced aircraft engines; and the Curtiss-Wright Propeller Division, which manufactured propellers.

Wall Street loved it. The stock soared. Aviation was the internet of its day—the transformative technology that would reshape civilization. Everyone wanted in. By August 22, Curtiss-Wright was listed on the New York Stock Exchange, trading at multiples that would make today's tech stocks blush.

Three months later, on October 29, 1929, the stock market crashed.

The timing could not have been worse. Curtiss-Wright had been built on leverage and optimism, assembled at the peak of a speculative bubble. Civilian aircraft orders evaporated overnight. Airlines that had placed deposits went bankrupt. The company's stock price collapsed from $75 to under $3.

But here's where the story gets interesting. Unlike many of the high-flying companies of the 1920s, Curtiss-Wright didn't die. It couldn't afford to. The U.S. military, even in the depths of the Depression, needed aircraft. More importantly, the gathering storm clouds in Europe and Asia meant that America's aviation capacity was about to become a matter of national survival.

The 1930s became a decade of quiet preparation. While civilian aviation languished, Curtiss-Wright engineers kept innovating. They developed new cooling systems for radial engines, pioneered aluminum forging techniques, created the dynamic damper to absorb crankshaft vibration. These weren't sexy innovations that made headlines, but they were the building blocks of what would come. In 1937, the P-36 Hawk Fighter won the USAAC competition, resulting in the largest peacetime aircraft order ever given by the Army Air Corps—210 P-36A fighters. This wasn't just a contract; it was validation that Curtiss-Wright could still build world-class aircraft.

The company structure that emerged from the Depression was leaner but more focused. Buffalo remained the heart of aircraft production. Engine manufacturing concentrated in New Jersey and Ohio. The propeller division established itself in Pennsylvania. Each division operated semi-autonomously, competing for resources but united by military contracts that kept the lights on.

By 1939, as Hitler invaded Poland and the world careened toward war, Curtiss-Wright was positioned perfectly. It had survived the worst economic catastrophe in American history. It had maintained its engineering talent. It had production facilities ready to scale. Most importantly, it had something the U.S. military desperately needed: the ability to build aircraft and engines by the thousands.

The merger that had seemed so ill-timed in 1929 would prove to be perfectly positioned for what came next. Sometimes in business, as in life, it's not about timing the market—it's about time in the market. Curtiss-Wright had paid its dues through the Depression. Now it was about to collect.

IV. World War II: The Arsenal of Democracy

The telegram arrived at Curtiss-Wright's Buffalo headquarters at 3:47 PM on December 8, 1941: "URGENT STOP ALL COMMERCIAL PRODUCTION STOP MILITARY PRIORITY ABSOLUTE STOP EXPECT ORDERS FORTHCOMING STOP." Within hours, the entire company transformed. Assembly lines that had been running single shifts went to 24-hour production. Parking lots filled with tents as workers slept between shifts rather than going home. America was at war, and Curtiss-Wright was about to become the second-largest defense contractor in the nation.

In 1940, Curtiss-Wright introduced the famous P-40 Warhawk, which through December 1944 was to have a production run of 13,738 planes and serve with distinction in the Air Forces of 28 nations during World War II. But the P-40 story really began earlier, with a desperate telegram from Claire Chennault in China. The former U.S. Army Air Corps captain had been advising Chiang Kai-shek and knew the Japanese were coming. He needed fighters that could arrive quickly, required minimal maintenance, and could take tremendous punishment. The P-40 fit the bill perfectly.

The Buffalo plant transformed into something out of science fiction. Where 3,000 workers had built planes in 1940, by 1943 there were 45,000—working in shifts so dense that workers literally had to schedule their bathroom breaks. The noise was deafening: rivet guns, grinding wheels, the constant clatter of overhead conveyors moving fuselages from station to station. Quality control inspectors—many of them women who'd never seen an airplane up close before Pearl Harbor—checked every rivet, every weld, every electrical connection.

During World War II, Curtiss-Wright produced 142,840 aircraft engines, 146,468 electric propellers, and 29,269 airplanes. Curtiss-Wright employed 180,000 workers, and ranked second among United States corporations in the value of wartime production contracts, behind only General Motors.

The numbers are staggering, but they don't capture the human drama. In the propeller division in Beaver, Pennsylvania, workers fabricated more than 100,000 propeller blades annually. Each blade was hand-finished, balanced to tolerances measured in fractions of ounces. A single imperfection could cause vibrations that would tear an engine apart at 20,000 feet.

The P-40 wasn't the best fighter of the war—it couldn't climb like a Spitfire or dive like a P-47. But it had two unbeatable advantages: it was available, and it was tough. Flying Tigers pilots learned to use these characteristics, developing tactics that played to the P-40's strengths. They avoided turning fights with nimble Japanese Zeros, instead using diving attacks that leveraged the P-40's superior weight and firepower.

Aircraft production included almost 14,000 P-40 fighters, made famous by their use by Claire Chennault's Flying Tigers in China, over 3,000 C-46 Commando transport aircraft, and later in the war, over 7,000 SB2C Helldivers. The C-46 Commando, in particular, became the workhorse of the China-Burma-India theater, flying "the Hump" over the Himalayas in conditions that would ground modern aircraft.

Revenue numbers tell only part of the story. Annual sales surpassed $1 billion for two consecutive years—roughly $18 billion in today's dollars. But this wasn't normal business. Cost-plus contracts meant profits were regulated but guaranteed. The government provided raw materials, supervised production, even built new factories that Curtiss-Wright operated. It was capitalism meets command economy, and it worked.

Yet success bred problems. The Lockland engine scandal erupted in 1943 when inspectors discovered that officials at the Ohio plant had conspired to approve substandard engines for military use. Wright Aeronautical engines that should have been scrapped were being stamped as airworthy and shipped to combat units. Congressional hearings followed. Criminal prosecutions ensued. The scandal cast a shadow over Curtiss-Wright's magnificent production achievements.

The company's response was telling. Rather than cover up, Curtiss-Wright cooperated fully with investigators, revamped quality control, and instituted procedures that became industry standards. The lesson was clear: in wartime production, there were no acceptable shortcuts. Every engine, every propeller, every aircraft component could mean the difference between a pilot coming home or not.

By 1945, Curtiss-Wright had delivered on its promise to become an arsenal of democracy. But as VJ Day approached, executives knew the party was ending. Orders that had been measured in thousands would soon be measured in dozens. The company that had employed 180,000 people would need to shrink by 90% almost overnight.

V. The Jet Age Crisis: Missing the Technology Transition

The scene at Wright Field in 1946 should have been a wake-up call. A captured German Me 262 jet fighter sat next to Curtiss-Wright's newest propeller-driven prototype. The German plane, despite being designed in desperation with inferior materials, could fly 100 mph faster. One Air Force general, examining both aircraft, turned to a Curtiss-Wright executive and said simply: "Your plane is already obsolete."

He was right. While Curtiss-Wright had been perfecting the reciprocating engine—achieving remarkable power-to-weight ratios and reliability that would have seemed impossible just a decade earlier—the world had moved on. Jets didn't just fly faster; they represented a fundamental shift in aircraft design, maintenance, and military doctrine.

The numbers from this period are brutal. Revenue declined from US$2 billion in 1945 to US$200 million in 1980. This wasn't just a post-war adjustment; it was a complete collapse of the business model. The company that had been second only to General Motors in wartime production value found itself struggling to stay relevant.

The missed opportunities are painful to recount. Curtiss-Wright had actually licensed jet engine technology from Britain's Armstrong Siddeley in 1950, producing the Sapphire engine under license. But they treated it as a side project, not a core business. When the Air Force needed jet engines for the new generation of fighters, they turned to General Electric and Pratt & Whitney—companies that had committed fully to turbine technology.

In aircraft manufacturing, the situation was even worse. The last Curtiss-Wright military aircraft contract was for the C-76 Caravan, a wooden transport that the Army ultimately rejected. After that, nothing. The company that had built nearly 14,000 P-40s couldn't get a contract for a single jet fighter.

But the story gets stranger. In 1956, Studebaker-Packard Corporation, the struggling automaker, signed a management agreement with Curtiss-Wright. The idea was that Curtiss-Wright's defense contracts could subsidize Studebaker's car business while Studebaker's consumer marketing expertise could help Curtiss-Wright diversify. It was a marriage of the desperate, and it lasted only until 1959.

Then came the Wankel rotary engine debacle. In the 1960s, Curtiss-Wright saw the revolutionary Wankel design as its path back to relevance. The rotary engine was smooth, powerful, and compact—perfect for everything from cars to aircraft. Curtiss-Wright licensed the technology and convinced General Motors to pay $50 million for rights in 1970. For a moment, it seemed like the company had found its second act.

But the Wankel never delivered on its promise. Fuel consumption was terrible. Emissions were worse. Seal wear made the engines unreliable. GM abandoned the project. Mazda was the only automaker to make it work, and even they eventually gave up on rotaries. Curtiss-Wright's bet on being the Western Hemisphere's rotary engine kingpin evaporated.

Throughout the 1960s and 1970s, Curtiss-Wright tried everything. They built nuclear reactor components. They made turbochargers for ships. They produced specialized valves for the Navy. Each business was profitable, but none had the scale of the glory days. The company was becoming something its founders would never have recognized: a collection of niche industrial businesses with no unifying vision.

The real tragedy wasn't that Curtiss-Wright missed the jet age—lots of companies fail to navigate technology transitions. It was that they had every opportunity to succeed. They had the engineering talent, the manufacturing expertise, the customer relationships. What they lacked was the courage to cannibalize their existing business in favor of an uncertain future.

By 1980, with revenue at just $200 million, Curtiss-Wright was a shadow of its former self. The company that had helped win World War II was now just another struggling industrial conglomerate. Wall Street had written it off. The aerospace industry had moved on. It would have been easy to predict a slow slide into irrelevance and eventual bankruptcy.

But that's not what happened.

VI. Reinvention as Industrial Conglomerate (1960s–1990s)

The conference room at Curtiss-Wright's new headquarters in Lyndhurst, New Jersey, was modest—a far cry from the grand boardrooms of the company's heyday. It was 1961, and CEO Roland Berner was making a presentation that would have horrified Glenn Curtiss and the Wright brothers. "Gentlemen," he said, pointing to a diagram of submarine valves, "our future isn't in building aircraft. It's in making the critical components that others can't."

The acquisition of Target Rock Corporation in 1961 became the foundation of industrial valves business for Navy nuclear propulsion systems. This wasn't a glamorous business. Target Rock made specialized valves for nuclear submarines—components that had to operate flawlessly at crushing depths, in radioactive environments, for decades without maintenance. Admiral Hyman Rickover, the father of the nuclear Navy, was notorious for his exacting standards. A valve that failed his tests didn't just lose a contract; the company that made it might never work for the Navy again.

But Curtiss-Wright thrived under this pressure. They discovered that the precision required for aircraft engines translated perfectly to nuclear components. The metallurgy expertise developed for high-temperature turbine blades worked for reactor vessels. The quality control systems refined after the Lockland scandal became selling points for nuclear work.

The 1968 acquisition of Metal Improvement Company revealed another path forward. Metal Improvement had perfected shot peening—a process of bombarding metal surfaces with tiny steel balls to increase fatigue resistance. It sounds simple, but the physics are complex. Done right, shot peening can double the lifespan of critical components. Done wrong, it creates stress points that cause catastrophic failures.

Every jet engine made by GE, Pratt & Whitney, or Rolls-Royce now required shot peening services. Landing gear that had to survive thousands of brutal touchdowns needed it. Helicopter blades, turbine shafts, even golf clubs—Metal Improvement found applications everywhere. It wasn't sexy, but it was essential, and margins were exceptional because few companies could match their expertise.

The space program provided another lifeline. Curtiss-Wright couldn't build rockets, but they could machine the components that others designed. Precision-machined rocket motor cases required tolerances measured in ten-thousandths of an inch. Exhaust nozzles had to withstand temperatures that would melt most metals. The company that had mass-produced aircraft engines became a boutique manufacturer of the space age's most demanding components.

Through the 1970s and 1980s, this strategy crystallized: Curtiss-Wright would be the company that made things other companies couldn't make themselves. They wouldn't design the submarine; they'd make the valves that controlled its reactor. They wouldn't build the aircraft; they'd provide the actuators that moved its control surfaces. They wouldn't manufacture the power plant; they'd supply the pumps that kept it running.

Each acquisition followed this logic. Companies with deep technical expertise in narrow niches. Products with high barriers to entry. Customers who valued reliability over price. Markets where being second-best meant being out of business.

The financials reflected this transformation. Margins improved even as revenues stayed flat. Return on invested capital rose. The company generated cash rather than consuming it. By the 1990s, Curtiss-Wright had achieved something remarkable: boring profitability.

Wall Street didn't notice. While investors chased dot-com stocks and aerospace rolled up into mega-mergers, Curtiss-Wright quietly generated 15% returns on equity making valves and surface treatments. The stock languished, trading at single-digit multiples while companies with no profits commanded astronomical valuations.

The 1990s brought new pressures. The end of the Cold War meant defense budgets shrank. The nuclear power industry, traumatized by Three Mile Island and Chernobyl, stopped building new plants. Commercial aerospace consolidated, with Boeing and Airbus squeezing suppliers on price.

Meanwhile, competitors were merging into giants. Lockheed merged with Martin Marietta. Boeing bought McDonnell Douglas. Northrop acquired Grumman. Investment bankers pitched Curtiss-Wright constantly: merge or die, they said. But management resisted. They'd seen what happened to companies swallowed by larger rivals—asset stripping, plant closures, the slow dissolution of everything that made them unique.

Instead, Curtiss-Wright doubled down on its niche strategy. They invested in new shot peening facilities in Europe and Asia. They developed new valve designs for emerging nuclear markets. They created actuators for the next generation of commercial aircraft. Each investment was small, targeted, and profitable.

By 2000, Curtiss-Wright had completed one of business history's most unlikely transformations. The company that had built the planes that won World War II now made components most people would never see. The firm that had employed 180,000 workers now had fewer than 6,000. The corporation that had generated billion-dollar revenues now measured sales in the hundreds of millions.

But they had survived. More than survived—they had found a sustainable niche in the industrial ecosystem. They were the pilot fish to the aerospace and defense sharks, essential but unnoticed. It wasn't glorious, but it was profitable. And as the new millennium dawned, that foundation would prove more valuable than anyone imagined.

VII. Modern Era: The Pivot to Growth Strategy (2000–Present)

The email that changed everything arrived on a Tuesday morning in March 2003. Lynn Bamford, then head of the Commercial/Industrial segment, was reviewing acquisition targets when her team flagged a small Irish company called Systran Corporation. Revenue: $30 million. Employees: 150. Business: specialized data communications for military aircraft. Asking price: reasonable. Strategic fit: perfect.

On June 3, 2024, the Company announced the acquisition of Ultra Nuclear Limited and Weed Instrument Co., Inc. ("Ultra Energy") for $200 million in cash. But we're getting ahead of ourselves. The Ultra Energy deal in 2024 represents the culmination of two decades of transformation that began with small, strategic acquisitions like Systran.

The early 2000s strategy was deceptively simple: buy companies that made products Curtiss-Wright couldn't easily develop internally, in markets where customers valued performance over price. Systran's rugged data acquisition systems for military aircraft fit perfectly. These boxes had to work at 50,000 feet, in temperatures ranging from -65°F to +200°F, while pulling 9 Gs. If they failed, pilots died.

Each acquisition followed a pattern. Due diligence focused less on synergies and more on technical differentiation. Could competitors replicate this technology? How long would it take? What would it cost? If the answers were no, years, and millions, Curtiss-Wright would pay a premium.

The 2011 acquisition of Acra Control for $61 million extended the data acquisition business into flight test instrumentation. When Boeing or Airbus developed a new aircraft, they needed to monitor thousands of parameters during test flights. Acra's systems could capture everything from wing flex to engine vibration, transmitting terabytes of data in real-time to ground stations.

But the real transformation came with the "Pivot to Growth" strategy announced in 2021. For decades, Curtiss-Wright had been content as a quiet, profitable niche player. New CEO Lynn Bamford—yes, the same executive who'd championed the Systran acquisition—had bigger ambitions.

"As we discussed at our Investor Day event in May, we continue to build momentum through the execution of our Pivot to Growth strategy. We remain focused on accelerating operational excellence to drive margin expansion and generate funding to reinvest into the business. As part of this strategy, we recently launched restructuring actions to support volume increases, improve efficiencies and further optimize our operations. These actions are expected to produce both recurring operational savings and increased free cash flow."

The strategy had four pillars: accelerate organic growth through increased R&D, pursue strategic acquisitions, optimize operations through restructuring, and maintain disciplined capital allocation. It sounds like standard corporate speak, but the execution was anything but standard.

The 2022 acquisition of Safran Aerosystems Arresting Company for $240 million brought Curtiss-Wright into the aircraft carrier arresting systems market. Every time a Navy fighter lands on a carrier, it relies on arresting gear to stop in 300 feet. The technology hasn't fundamentally changed since World War II, but the engineering tolerances have. Modern systems must stop 50,000-pound aircraft traveling at 150 mph without damaging the airframe. Only three companies in the world can do this reliably.

The company's three-segment structure evolved to match market realities. Aerospace & Industrial (A&I) focused on commercial aerospace and general industrial markets. Defense Electronics served the Pentagon's insatiable appetite for sensors and communications. Naval & Power combined submarine components with nuclear power generation—two markets with similar requirements for absolute reliability.

Reported sales of $3.1 billion, up 10%, operating income of $529 million, operating margin of 16.9%, and diluted EPS of $10.55 for 2024 represents a company firing on all cylinders. But the real story is in the details. Free cash flow of $483 million means the company generates cash at a rate that would make Silicon Valley jealous. The record backlog of $3.3 billion provides visibility years into the future.

The commercial aerospace recovery post-COVID has been a tailwind, but Curtiss-Wright's exposure is cleverly hedged. They supply components for both Boeing and Airbus. They serve narrow-body and wide-body markets. Their actuators go into military and commercial aircraft. When one market struggles, others compensate.

Defense modernization provides another growth driver. The Pentagon's pivot to peer competition with China means upgrading everything from submarines to satellites. Curtiss-Wright components are designed into programs that will run for decades. The Virginia-class submarine program alone will build boats into the 2040s. The B-21 bomber will fly until 2070. These aren't just orders; they're annuities.

The nuclear power renaissance, long promised but never delivered, finally seems real. Small modular reactors (SMRs) need the same components as traditional plants but in different configurations. Curtiss-Wright's experience with naval reactors—which are essentially SMRs—positions them perfectly. The Ultra Energy acquisition brings nuclear instrumentation expertise that few competitors can match.

But perhaps the most impressive transformation is cultural. The company that once built complete aircraft now celebrates winning a $10 million valve contract. Engineers who might have designed fighters now obsess over actuator reliability. It's not glamorous, but it's profitable.

The "One Curtiss-Wright" initiative breaks down silos between divisions. An actuator developed for aerospace might find applications in industrial automation. Surface treatment technology from Metal Improvement could enhance nuclear components. Cross-selling between divisions sounds mundane, but it drives organic growth without acquisition costs.

Diluted EPS increased to new range of $10.55 to $10.75, up 12% to 15% for 2024 guidance shows management confidence. The three-year targets are even more ambitious: minimum 5% organic revenue growth, minimum 10% EPS growth, free cash flow conversion above 105%. These aren't stretch goals; based on current performance, they're sandbags.

The modern Curtiss-Wright is unrecognizable from its origins but somehow true to its heritage. It's still an engineering company solving hard problems. It still serves defense and aerospace markets. It still values precision and reliability above all else. The difference is focus: instead of building everything, they build the things others can't.

VIII. Current Business & Financial Performance

Walk into any Curtiss-Wright facility today—whether it's the actuator plant in Shelby, North Carolina, or the valve manufacturing center in Cheswick, Pennsylvania—and you'll notice something unusual for an industrial company: the walls are covered with photos of the end products their components go into. An F-35 fighter. A Virginia-class submarine. A Boeing 787. A nuclear power plant. Employees might never see these finished products, but they know their work is inside them, performing critical functions where failure isn't an option.

2024 performance shows a company hitting its stride: $3.1 billion sales (up 10%), operating margin 16.9%, EPS $10.55. These aren't just good numbers; they're exceptional for an industrial manufacturer. The operating margin of 16.9% exceeds many pure-play defense contractors. The 10% revenue growth outpaces GDP by multiples.

Breaking down the segment performance reveals the power of diversification:

Aerospace & Industrial (38% of sales): This segment supplies actuation systems for commercial aircraft, surface treatment services, and industrial valves. The commercial aerospace recovery has been slower than expected—Boeing's troubles and supply chain issues have constrained production. But Curtiss-Wright's content per aircraft keeps growing. A 737 MAX has 40% more Curtiss-Wright content than a 737NG. The 787 has even more. When production eventually normalizes, this segment will soar.

Defense Electronics (30% of sales): The transformation here has been remarkable. What was once a collection of small sensor and communication businesses is now a integrated defense electronics powerhouse. The PacStar tactical communications systems are on every Army brigade's wish list. The rugged computing systems process data from everything from submarine sonars to satellite sensors. Margins here exceed 20%, reflecting the specialized nature of these products.

Naval & Power (32% of sales): The steady Eddie of the portfolio. Nuclear submarine production is increasing for the first time in decades. The Columbia-class ballistic missile submarine program will build 12 boats at $8 billion each. Curtiss-Wright supplies pumps, valves, and control systems for the nuclear propulsion plant—content worth millions per boat. On the commercial side, nuclear plant life extensions require replacement components that must meet exacting specifications. Only a handful of suppliers are qualified.

New orders of $939 million, up 37%, generating a book-to-bill of 1.1x in Q4 2024 indicates accelerating momentum. The book-to-bill ratio—orders divided by sales—above 1.0 means the backlog is growing. For a company with multi-year contracts, this provides exceptional visibility.

Backlog of $3.3 billion, up 16% from December 31, 2023, reflecting higher demand in both our A&D and Commercial markets. This backlog represents more than a year of sales, already contracted and scheduled. Unlike companies that must constantly hunt for new business, Curtiss-Wright starts each year with most of their revenue already booked.

Capital allocation deserves special attention. The company generated record free cash flow of $483 million in 2024, representing a conversion rate above 105% of net income. This cash funds three priorities: organic investment through R&D and capex, strategic acquisitions, and returns to shareholders through dividends and buybacks.

The R&D spend of approximately 3% of sales might seem modest compared to pure-play technology companies, but it's focused on specific applications where Curtiss-Wright already has domain expertise. They're not trying to invent new markets; they're extending their leadership in existing ones.

The acquisition strategy remains disciplined. The Ultra Energy acquisition for $200 million brings nuclear instrumentation expertise and is expected to be accretive to adjusted diluted earnings per share in its first full year of ownership, excluding first year purchase accounting costs, and produce a free cash flow conversion rate in excess of 100%.

Major programs provide long-term stability:

- F-35 Lightning II: Actuators and surface treatments for every aircraft built, with 3,000+ aircraft planned

- Boeing 737 MAX: Flight control actuation and sensing systems, with 4,000+ aircraft backlog

- Virginia-class Submarines: Pumps, valves, and control rod drive mechanisms, with 66 boats planned

- Columbia-class Submarines: Similar content but higher value per boat given larger size

- B-21 Raider: Classified systems worth millions per aircraft

The competitive moats are real and durable:

-

Qualification Barriers: Getting qualified for aerospace or nuclear applications takes years and millions in testing. Once qualified, customers rarely switch suppliers.

-

Design Lock-in: Components designed into platforms that will be produced for decades. Changing suppliers would require expensive recertification.

-

Domain Expertise: The knowledge to make components that work in extreme environments can't be easily replicated. It's accumulated over decades.

-

Scale Economics: In niche markets, Curtiss-Wright often has 30-50% market share. Competitors can't match their economies of scale.

-

Switching Costs: The cost and risk of switching suppliers for critical components far exceeds any potential savings.

Looking at the 2025 guidance, management expects 7-8% sales growth and greater than 10% EPS growth. The margin expansion story continues, with operating margins expected to reach 17.9-18.1%. These aren't heroic assumptions—they're based on contracted backlog and identified productivity improvements.

The balance sheet remains fortress-like with modest leverage and ample liquidity. The company could easily fund a billion-dollar acquisition if the right target appeared. But management remains disciplined, walking away from deals where the price doesn't match the strategic value.

IX. Playbook: Business & Investing Lessons

The Curtiss-Wright story offers a masterclass in corporate survival and transformation, but the lessons aren't always what you'd expect. This isn't a tale of visionary leadership or brilliant strategy—it's about adaptation, focus, and the surprising value of becoming indispensable in unglamorous markets.

Lesson 1: Technology Transitions Are Survivable, But Only With Radical Adaptation

The failure to transition from propeller to jet aircraft should have killed Curtiss-Wright. Revenue collapsing 90% kills most companies. But they survived by completely reimagining their business model. The lesson isn't to predict technology transitions better—it's to build a culture that can survive being wrong.

When jets obsoleted their aircraft, Curtiss-Wright didn't try to catch up. They asked a different question: what capabilities do we have that translate to other markets? Precision machining, metallurgy expertise, quality control systems—these skills were valuable beyond aircraft manufacturing. The company that failed at jets succeeded at nuclear submarines because they transferred capabilities, not products.

Lesson 2: In B2B Markets, Boring Beats Exciting

Silicon Valley celebrates disruption, but Curtiss-Wright proves the value of the opposite strategy. They explicitly target markets where innovation is incremental, customers are conservative, and reliability matters more than features. A nuclear valve is essentially the same today as 30 years ago—just more refined.

This isn't laziness; it's strategic brilliance. In exciting markets, competition is fierce, margins compress, and customers constantly demand more for less. In boring markets, customers pay premiums for certainty. The actuator that moves a fighter jet's control surfaces doesn't need to be innovative—it needs to work every single time for 30 years.

Lesson 3: Conglomerate Structures Can Work in Specific Contexts

Modern finance theory says conglomerates destroy value. Focus is king. Pure plays get higher multiples. Curtiss-Wright proves the exception. Their three segments—Aerospace & Industrial, Defense Electronics, Naval & Power—seem unrelated but share critical characteristics:

- Long development cycles that favor patient capital

- Extreme reliability requirements that create barriers to entry

- Regulated markets where relationships matter as much as technology

- Similar manufacturing processes despite different end products

The conglomerate structure allows Curtiss-Wright to smooth cycles. When commercial aerospace struggles, defense compensates. When nuclear stalls, aerospace carries the load. This isn't diversification for its own sake—it's portfolio construction with purpose.

Lesson 4: Capital Allocation Discipline Beats Growth At Any Price

Through multiple management teams and strategy shifts, one thing remains constant: Curtiss-Wright's capital allocation discipline. They've never made a bet-the-company acquisition. They've never chased revenue growth at the expense of margins. They've never leveraged the balance sheet for financial engineering.

The acquisition criteria are rigid: the target must have defensible technology, serve similar customers, and generate returns above the cost of capital within three years. If these criteria aren't met, they walk away, regardless of banker pressure or competitor moves.

This discipline extends to organic investment. R&D spending stays around 3% of sales—enough to maintain technology leadership but not so much that it destroys current profitability. Capital expenditure runs at depreciation plus a bit more, funding growth without massive infrastructure bets.

Lesson 5: Hidden Assets Have Real Value

The market values what it can see. Software companies with recurring revenue get SaaS multiples. Biotech with promising pipelines get option value. But what about a company with 50% market share in aircraft carrier arresting gear? How do you value being the only qualified supplier of certain nuclear submarine valves?

Curtiss-Wright is full of these hidden assets. The Metal Improvement subsidiary's shot peening technology touches virtually every aircraft flying today. The surface treatment technology prevents fatigue failures in applications from helicopters to wind turbines. These aren't sexy businesses, but they're incredibly valuable to customers who have no alternatives.

Lesson 6: Customer Concentration Can Be A Moat

Conventional wisdom says customer concentration is risky. Curtiss-Wright's top ten customers represent over 50% of revenue. The U.S. government alone is 40%. This should terrify investors, but it doesn't. Why?

Because the switching costs are astronomical. The Navy can't change submarine valve suppliers without years of testing and qualification. Boeing can't swap actuator providers without recertifying the entire flight control system. These aren't vendor relationships; they're engineering partnerships measured in decades.

Lesson 7: Operational Excellence Compounds

The "Pivot to Growth" strategy sounds revolutionary, but it's really about operational blocking and tackling. Reduce inventory turns. Improve on-time delivery. Eliminate quality defects. Standardize processes across facilities. None of this is exciting, but it compounds.

A 50 basis point margin improvement across a $3 billion revenue base is $15 million in operating income. Do that every year for a decade, and you've transformed the company's profitability. Curtiss-Wright's operating margins have expanded from 14% to 17% over five years through hundreds of small improvements.

Lesson 8: Market Position Matters More Than Market Size

Curtiss-Wright deliberately targets small markets where they can be number one or two. The total addressable market for naval nuclear propulsion valves is maybe $200 million annually. The market for aircraft carrier arresting gear is even smaller. But Curtiss-Wright owns these markets.

In small markets, competition is rational. Players know each other. Price wars are suicide because there's no volume to make up for margin compression. Innovation is incremental because customers value reliability over features. It's the opposite of winner-take-all tech markets, and that's exactly the point.

X. Bear vs. Bull Case Analysis

Analyzing Curtiss-Wright requires abandoning traditional growth stock frameworks. This isn't Tesla or Nvidia. It's not going to double revenue in three years or disrupt entire industries. The bear and bull cases rest on more subtle factors—execution, cycle timing, and whether boring businesses deserve premium valuations.

The Bear Case: A Compelling Argument for Caution

The bears start with market cyclicality. Commercial aerospace, despite current optimism, remains cyclical. Boeing's production issues aren't just temporary hiccups—they reflect structural problems in the aerospace supply chain. If Boeing can't ramp 737 production as planned, Curtiss-Wright's Aerospace & Industrial segment suffers. A recession would crater air travel demand, leading to order cancellations and production cuts.

Defense spending dependency creates political risk. Yes, the Pentagon budget seems secure with bipartisan support for competition with China. But priorities shift. A future administration might favor missiles over manned aircraft, space over submarines, cyber over hardware. Curtiss-Wright is leveraged to specific platforms. If the F-35 gets cut, if submarine production slows, if the B-21 program stumbles, revenue evaporates.

Competition from larger primes poses a constant threat. Lockheed Martin, Raytheon, General Dynamics—these giants have resources Curtiss-Wright can't match. They could develop competing technologies, acquire Curtiss-Wright's competitors, or simply insource production. The company's niche market positions are defensible until they're not.

Integration risks from acquisitions multiply with each deal. Ultra Energy might not integrate smoothly. Safran's arresting gear business might have hidden liabilities. The company has executed well historically, but every acquisition is a roll of the dice. One bad deal could destroy years of value creation.

Limited organic growth potential caps upside. Curtiss-Wright's markets grow at GDP plus a bit. They're not riding secular trends like electrification or artificial intelligence. A 5% organic growth rate is success for them. In a market that rewards hypergrowth, steady expansion looks like stagnation.

Valuation already reflects execution. The stock trades at 24x forward earnings—not cheap for an industrial. The market has recognized the quality and priced it in. Where's the upside surprise? What catalyst drives multiple expansion from here?

The Bull Case: The Hidden Compounding Machine

The bulls counter with critical supplier status. Curtiss-Wright isn't just a vendor; they're designed into platforms that will fly for 50 years. The B-52 bomber, first flown in 1952, will operate until 2050. Every one needs Curtiss-Wright components for maintenance. This isn't a revenue stream; it's an annuity.

The nuclear power renaissance is finally real. Not hopeful projections—actual projects with funding. Small modular reactors are being built. Existing plants are extending lives. China is building reactors at a stunning pace. Curtiss-Wright supplies components to all these markets. Nuclear is a 30-year supercycle just beginning.

Defense modernization has decades to run. The U.S. submarine fleet is the oldest it's been since World War II. The Air Force needs 300+ new bombers. The Navy is building two Virginia-class submarines annually, heading to three. These aren't wish lists; they're funded programs with bipartisan support.

Free cash flow generation is exceptional. $483 million in 2024 represents a 15% free cash flow yield. This funds growth investment, acquisitions, and shareholder returns without leverage. Few industrials generate cash at this rate with this consistency.

Management execution has been flawless. Lynn Bamford promised a pivot to growth and delivered. Operating margins expanded. Free cash flow increased. The acquisition strategy works. This team has earned credibility—when they guide to 10% EPS growth, believe them.

Hidden asset value remains unrecognized. The market values Curtiss-Wright like a typical industrial, but it's not. The certification barriers, the sole-source positions, the 30-year program locks—these are worth premium multiples. If private equity ever got comfortable with the defense exposure, this company would be a perfect LBO candidate at 50% premium.

The Verdict: Asymmetric Risk/Reward

The bear case is about multiple compression and cycle timing. The bull case is about compounding and duration. Both are right, but on different time horizons.

Near-term, the bears have valid concerns. Commercial aerospace recovery could disappoint. Defense spending could flatten. The stock could easily trade down 20-30% in a broader market correction or sector rotation.

Long-term, the bulls win. This is a business that compounds value through cycles. The management team has proven they can adapt to changing markets. The end markets—defense, nuclear, aerospace—aren't disappearing. The competitive moats are real and durable.

The key insight: Curtiss-Wright is mispriced not because the market doesn't understand the business, but because it doesn't value the duration. The market sees an industrial trading at 24x earnings. It should see a collection of niche monopolies with 20+ year revenue visibility trading at utility-like multiples for defense-contractor-like growth.

For investors with five-year horizons, the risk/reward is compelling. For traders watching quarterly earnings, it's a minefield. The difference between those perspectives explains why Curtiss-Wright remains misunderstood and arguably mispriced.

XI. Epilogue: What Would the Founders Think?

Glenn Curtiss died in 1930, just one year after the merger that created Curtiss-Wright. Orville Wright lived until 1948, long enough to see the company that bore his name help win World War II but not long enough to see it abandon aircraft manufacturing entirely. What would these aviation pioneers think of the modern Curtiss-Wright—a company that generates $3 billion in revenue without building a single airplane?

The irony is inescapable. Today, Curtiss-Wright is a global, integrated market-facing business that remains a technology leader through this legacy of innovation. The company founded by men obsessed with flight now makes components that others integrate into aircraft. The firm that pioneered aviation manufacturing now specializes in technologies most people never see.

Yet there's something fitting about this evolution. Both Curtiss and the Wrights were, at heart, problem solvers. They didn't set out to build aircraft companies—they set out to solve the problem of human flight. Once that problem was solved, they moved on to others: more powerful engines, better control systems, improved reliability.

Modern Curtiss-Wright continues this tradition, just at a different scale. The problems are smaller but no less critical. How do you make a valve that can operate in a nuclear reactor for 40 years without maintenance? How do you design an actuator that can move a control surface 10 million times without failing? How do you treat a turbine blade surface so it can withstand temperatures that would melt untreated metal?

These aren't the romantic challenges that capture public imagination. No one will make movies about the team that improved submarine valve reliability by 15%. But these incremental innovations, accumulated over decades, enable the systems our modern world depends on.

The company's longevity—95 years and counting—offers lessons about corporate survival. Curtiss-Wright has outlived most of its contemporaries. Pan Am, TWA, Eastern Airlines—gone. McDonnell Douglas, absorbed. Lockheed and Martin Marietta, merged. Grumman, Northrop, Convair, Republic—all either defunct or absorbed into larger entities.

Curtiss-Wright survived by accepting a fundamental truth: corporate identity must be flexible to endure. The company that insists on defining itself by what it makes rather than what problems it solves eventually discovers its products are obsolete. The company that defines itself by its capabilities can evolve as markets change.

Consider the Wright brothers' approach to aviation. They weren't just trying to fly; they were trying to control flight. Their breakthrough wasn't more powerful engines or lighter materials—it was the three-axis control system that made sustained flight possible. Control, not power, was their obsession.

Modern Curtiss-Wright embodies this focus on control. Their actuators control aircraft surfaces. Their valves control fluid flow. Their electronics control data transmission. Their surface treatments control material degradation. They don't build the systems; they build what controls the systems.

Glenn Curtiss took a different approach. He was the showman, the racer, the entrepreneur who saw aviation's commercial potential before anyone else. He built flying schools, developed seaplanes for naval use, created the infrastructure for aviation to become an industry rather than a curiosity.

Today's Curtiss-Wright reflects this commercial pragmatism. They don't chase technical excellence for its own sake. Every innovation must have a customer, every investment must generate returns, every acquisition must be accretive. It's Curtiss's business sense married to Wright precision.

The stock performance tells its own story. From the 2009 financial crisis low around $20 to today's price near $350, Curtiss-Wright has generated returns that would satisfy any investor. But this isn't a momentum story or a meme stock. It's the steady appreciation of a business that compounds value over time.

Recent developments suggest the next chapter is being written. The nuclear renaissance, the defense modernization cycle, the reshoring of critical manufacturing—these trends align perfectly with Curtiss-Wright's capabilities. The company that missed the jet age might be perfectly positioned for the new industrial age.

In 2021 we began the next phase of our evolution with our Pivot to Growth strategy, driven by a renewed drive for top line acceleration through both organic and inorganic sales growth, building on the strengths across our A&D and Commercial markets. We established new long-term targets for the three-year period ending in 2023: 5-10% Total Revenue Growth; Operating Income Growth > Revenue Growth; Top Quartile Margin Performance; >= 10% CAGR Adjusted EPS Growth; > 110% Free Cash Flow Conversion.

What would the founders think? They'd probably be confused by the financial engineering and management speak. But they'd recognize the engineering excellence, the commitment to reliability, the focus on solving hard problems. They'd understand that building the plane and building the components that make the plane possible are both essential.

Most of all, they'd appreciate the survival. In a business world that celebrates disruption and creative destruction, Curtiss-Wright proves that adaptation and evolution can be just as powerful. The company that began with two bitter rivals forcing the U.S. government to intervene in their patent war has become an essential supplier to that same government's most critical defense programs.

The next 100 years? Who knows. Maybe Curtiss-Wright will make components for spacecraft heading to Mars. Maybe they'll build systems for fusion reactors. Maybe they'll develop technologies we can't yet imagine. What's certain is they won't be building complete aircraft, and that's perfectly fine.

The legacy of Glenn Curtiss and the Wright brothers isn't any particular product or technology—it's the idea that hard problems are worth solving, that precision matters, that reliability has value. As long as Curtiss-Wright embodies these principles, the founders' spirit lives on, even if the company they'd recognize is long gone.

XII. Recent News**

Completion of Ultra Energy Acquisition (January 2025)** Curtiss-Wright Corporation completed the acquisition of Ultra Nuclear Limited and Weed Instrument Co., Inc. ("Ultra Energy") for $200 million in cash. This strategic acquisition brings nuclear instrumentation expertise at a critical time for the nuclear renaissance, positioning Curtiss-Wright to capitalize on both SMR development and traditional nuclear plant life extensions.

Record 2024 Financial Performance (February 2025) Reported sales of $3.1 billion, up 10%, operating income of $529 million, operating margin of 16.9%, and diluted EPS of $10.55; Adjusted operating income of $546 million, up 11%; Adjusted operating margin of 17.5%, up 10 basis points; New orders of $3.7 billion, up 20%, reflecting strong demand in our Aerospace & Defense (A&D) markets, and book-to-bill of 1.2x; and Backlog of $3.4 billion, up 20%. The company delivered on all key metrics, with particularly strong order growth indicating continued momentum.

Aggressive Share Repurchase Program (December 2024) This follows a recently completed $100 million opportunistic program from Q3, bringing total expected repurchases to $250 million in 2024. Management's aggressive buyback demonstrates confidence in the business and commitment to returning capital to shareholders while maintaining strategic flexibility for acquisitions.

Strong 2025 Guidance Management issued 2025 guidance reflecting 7-8% sales growth, operating margin expansion to 17.9-18.1%, and double-digit EPS growth. "Looking ahead, our strong backlog at the start of the year, combined with the alignment of our technologies to favorable secular growth trends in our end markets, reinforces our confidence in delivering another strong performance in 2025."

Leadership Continuity Paul J. Ferdenzi, Vice President, General Counsel and Corporate Secretary, plans to retire after a distinguished 25-year career with the Company. Mr. Ferdenzi will continue to serve as a Vice President of the Company to assist the Executive Team with the transition until his retirement at the end of this year. The orderly transition of senior leadership demonstrates organizational depth and succession planning.

XIII. Links & References

Company Resources

- Curtiss-Wright Investor Relations: www.curtisswright.com/investor-relations/

- Annual Reports & SEC Filings: Available through investor relations site

- 2024 Investor Day Presentation: Materials from May 21, 2024 event

- Quarterly Earnings Calls: Webcast replays available on company website

Historical Aviation Resources

- Glenn H. Curtiss Museum, Hammondsport, NY: www.glennhcurtissmuseum.org

- National Museum of Naval Aviation, Pensacola, FL: Features extensive Curtiss aircraft collection

- National Air and Space Museum, Smithsonian: Houses Wright Whirlwind engine and historical documents

- Wright Brothers National Memorial, Kill Devil Hills, NC

Books on Company History

- "Curtiss-Wright: Greatness and Decline" by Louis R. Eltscher and Edward M. Young

- "Glenn Curtiss: Pioneer of Flight" by C.R. Roseberry

- "The Bishop's Boys: A Life of Wilbur and Orville Wright" by Tom D. Crouch

- "Unlocking the Sky: Glenn Hammond Curtiss and the Race to Invent the Airplane" by Seth Shulman

Industry & Market Reports

- Aerospace Industries Association (AIA): Annual industry statistics

- Defense News Top 100: Annual defense contractor rankings

- Nuclear Energy Institute: SMR and nuclear power market data

- IATA Aviation Industry Reports: Commercial aerospace market analysis

Academic & Technical Papers

- "The Patent Wars: Wright Brothers vs. Glenn Curtiss" - Journal of Business History

- "Industrial Conglomerates in the Defense Sector" - Defense Acquisition Research Journal

- "Shot Peening Technology and Applications" - Surface Engineering Technical Papers

- "Nuclear Valve Qualification Standards" - ASME Nuclear Engineering Division

Documentary Resources

- "The Aviation Pioneers" - PBS Documentary Series

- "Arsenal of Democracy: Detroit and WWII Production" - History Channel

- "The Jet Age" - National Geographic special on aviation transition

- Corporate archives at Buffalo History Museum

Investment Research

- Note: Specific sell-side research reports require institutional access

- Value Line Investment Survey: Historical coverage available

- Morningstar: Independent analysis and historical financials

- S&P Capital IQ: Detailed financial metrics and peer comparisons

Trade Publications

- Aviation Week & Space Technology: Coverage of aerospace programs

- Defense News: Defense industry coverage and contract announcements

- Nuclear Engineering International: Nuclear power industry developments

- American Machinist: Manufacturing and industrial technology

Competitor Resources

- Lockheed Martin (LMT): www.lockheedmartin.com

- Raytheon Technologies (RTX): www.rtx.com

- General Dynamics (GD): www.gd.com

- Moog Inc. (MOG.A): www.moog.com

- HEICO Corporation (HEI): www.heico.com

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube