Chevron: From Standard Oil to Energy Supermajor

I. Cold Open & The Big Picture

On July 18, 2025, after nearly two years of legal warfare, Chevron finally closed the books on its $53 billion acquisition of Hess Corporation. The deal had been held hostage by an International Chamber of Commerce arbitration filing from none other than ExxonMobil, which claimed a right of first refusal over Hess's crown jewel: a 30% stake in Guyana's Stabroek Block, one of the most significant oil discoveries of the twenty-first century. When the ICC tribunal ruled in Chevron's favor, CEO Mike Wirth wasted no time. The merger closed the same day.

That single transaction tells you everything about where Chevron stands in the global energy landscape. Here is a company willing to spend more than the GDP of most nations on a single bet, endure years of legal uncertainty against its closest rival, and do it all to secure access to an offshore oil reservoir that most people could not find on a map. This is not timid, defensive energy management. This is a company that believes the world will need oil and gas for decades to come, and it intends to be the one supplying it.

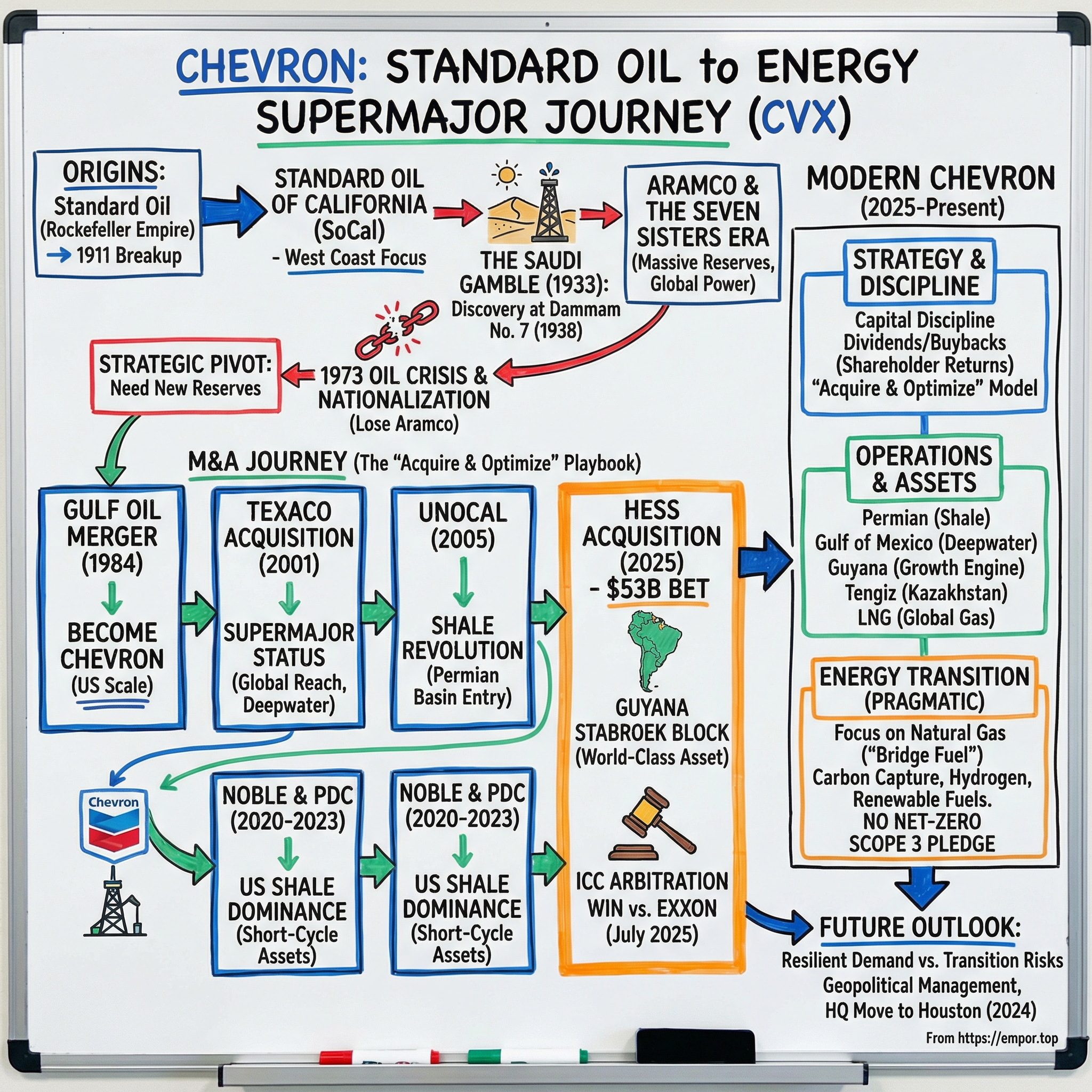

Chevron is the second-largest descendant of John D. Rockefeller's Standard Oil empire, trailing only ExxonMobil in market capitalization among the Standard Oil progeny. Originally known as Standard Oil of California, or "SoCal" for short, the company traces its roots back to the 1870s California gold rush era, when wildcatters first started poking holes in the hillsides north of Los Angeles. Over nearly 150 years, it has grown through a remarkable chain of acquisitions, geopolitical gambles, and strategic pivots into one of the largest publicly traded energy companies on Earth.

In 2023, Chevron ranked 10th on the Fortune 500. It holds a distinction that no other oil and gas company can claim: it is the last remaining oil and gas component of the Dow Jones Industrial Average, a proxy for the American economy that has increasingly tilted toward technology and healthcare. The fact that Chevron still sits in that index says something about the enduring centrality of hydrocarbons to the global economy, even as the energy transition narrative accelerates.

This is a story that spans three centuries of American capitalism. It begins with prospectors in the dusty canyons of Southern California, detours through the deserts of Saudi Arabia, winds through some of the largest corporate mergers in history, and arrives at the present day with a company producing over four million barrels of oil equivalent per day across six continents. Along the way, we will encounter wildcatters, geologists, kings, corporate raiders, and the quiet discipline of a management culture that has navigated more commodity cycles than most companies have existed.

II. Origins: The Pacific Coast Oil Story (1876-1911)

In 1876, the same year the United States celebrated its centennial, a group of prospectors working for a small outfit called Star Oil Works made a discovery that would reshape the American West. At Pico Canyon, about 50 miles north of Los Angeles in the rugged Santa Clarita Valley, they struck oil. It was not a gusher in the dramatic Hollywood sense. It was modest, methodical, and commercially viable. But it marked the birth of the modern California oil industry, and it planted the seed that would eventually become one of the largest corporations in world history.

The California oil story had actually been percolating for years. Native Americans and Spanish missionaries had long known about the tar seeps and natural oil pools scattered across the region. But the technology and capital to extract crude commercially had been focused on Pennsylvania, where Edwin Drake had drilled his famous well in 1859. California was an afterthought, a remote frontier where the railroad barons were the real power brokers.

Star Oil's Pico Canyon discovery changed that calculus. Suddenly, the West Coast had its own petroleum economy.

Three years later, in 1879, Frederick Taylor and a group of investors incorporated the Pacific Coast Oil Company. Their ambition was to consolidate the scattered California oil operations into something more coherent, bringing production, transportation, and refining under one roof.

The company expanded rapidly, discovering new wells including the notable Pico Well No. 4, and building out the infrastructure needed to move crude from remote canyon sites to refineries near the coast. One of those early refineries sat at Alameda Point, across the bay from San Francisco, and had been operating since around 1880, making it one of the oldest refining operations on the West Coast.

This was frontier capitalism at its most raw. There were no environmental regulations, no OSHA, no Securities and Exchange Commission. A company's advantage came from securing land rights, building pipelines before competitors, and locking in refining capacity. Pacific Coast Oil did all three, becoming the dominant oil producer in California by the turn of the century.

Which is precisely why John D. Rockefeller's Standard Oil came calling. In 1900, Standard Oil of New Jersey, the parent company of Rockefeller's sprawling empire, acquired Pacific Coast Oil Company for $761,000. The price seems almost comical by modern standards, but at the time it represented a strategic masterstroke.

Standard Oil gained not just West Coast oil production, but an integrated system of fields, pipelines, tankers, and refineries that gave it dominance from the Rockies to the Pacific.

For the next six years, Pacific Coast Oil operated as a subsidiary within the Standard Oil constellation, producing and refining crude while Standard Oil of Iowa handled the marketing and distribution. In 1906, this arrangement was formalized when the two entities merged into a single corporate entity: Standard Oil Company (California). The West Coast oil business now had a single name, a single balance sheet, and the full backing of the most powerful industrial enterprise the world had ever seen.

Then the government came for Standard Oil. In 1911, the Supreme Court upheld the ruling under the Sherman Antitrust Act that Rockefeller's empire was an illegal monopoly. Standard Oil was broken into 34 independent companies, an act of corporate dismemberment that ranks alongside the breakup of AT&T as one of the most consequential antitrust actions in American history.

Standard Oil of California emerged as one of the larger pieces, inheriting all the West Coast assets: oil fields, pipelines, tankers, refineries, and a retail distribution network. SoCal was now autonomous, forced to compete on its own without the safety net of the Rockefeller empire. It was an abrupt and potentially dangerous liberation.

For investors, the key insight is this: the breakup did not destroy the Standard Oil DNA. It simply scattered it across dozens of independent entities, each carrying the operational discipline, vertical integration instinct, and ruthless efficiency that Rockefeller had bred into the organization. SoCal was one of the strongest fragments, and it would spend the next century proving it.

III. The SoCal Era: Building an Empire (1911-1933)

When the Supreme Court severed Standard Oil of California from the mothership in 1911, the newly independent company found itself in an enviable position. It controlled the dominant share of oil production, refining, and distribution on the West Coast. California's oil industry was booming, fueled by the explosive growth of the automobile and the rapid urbanization of Los Angeles, San Francisco, and the Pacific Northwest. SoCal had the assets, the infrastructure, and the institutional knowledge to capitalize on all of it.

The early post-breakup years were a period of relentless infrastructure buildout. SoCal expanded its refining capacity, laid new pipelines, and pushed its distribution network into every corner of the Pacific states. The company's first refinery at Alameda Point had been supplemented by larger, more modern facilities, and these refineries were running near capacity as demand for gasoline, kerosene, and lubricants surged.

One innovation from this era deserves special mention because it fundamentally changed how Americans interact with oil companies. A SoCal sales manager named John McLean opened what is widely credited as the world's first purpose-built service station in Seattle. Before McLean's innovation, gasoline was sold at general stores, blacksmith shops, and curbside pumps, a haphazard and often dangerous arrangement. You could buy gasoline from a hardware store, a livery stable, or a man with a barrel and a hand pump on the side of the road. McLean's insight was that motorists would pay a premium for convenience, cleanliness, and speed. His service station concept, with dedicated pumps, an attendant, and a small retail space, became the template that every oil company in the world would eventually copy. The branded gas station is so ubiquitous today that it is easy to forget someone had to invent it, and that someone worked for the company that would become Chevron. That innovation also created something more subtle: a direct consumer-facing brand relationship. For the first time, an oil company was not just an anonymous supplier of a commodity; it was a familiar presence on the street corner, a logo that consumers recognized and trusted. That branding advantage persists to this day.

Throughout the 1910s and 1920s, SoCal pushed aggressively into exploration and production, drilling new wells across California's Central Valley and coastal regions. The company also pioneered early innovations in refining technology, improving the yield and quality of gasoline at a time when automobile engines were becoming more powerful and demanding higher-octane fuel. This was the era when Henry Ford's Model T was putting America on wheels, and gasoline demand was growing at double-digit rates year after year. SoCal was the primary supplier for the entire West Coast, and it benefited enormously from being in the right place at exactly the right time.

The automobile revolution also drove a fundamental shift in how oil companies thought about their business. In the early days, kerosene for lamps had been the primary petroleum product. Gasoline was practically a waste byproduct, something refineries struggled to dispose of. But by the 1920s, gasoline had become the dominant product, and the companies that could refine the most and highest-quality gasoline from a barrel of crude held a decisive competitive advantage. SoCal invested heavily in cracking technology, which uses heat and pressure to break down heavier crude molecules into lighter gasoline molecules, effectively getting more gasoline out of each barrel of crude. This is the kind of boring, unglamorous technical work that does not make headlines but compounds returns over decades.

The most significant strategic move of this era came in 1926, when SoCal purchased Pacific Oil Company from the Southern Pacific Railway. This was not just another bolt-on acquisition. Pacific Oil brought with it an extensive network of pipelines and refining assets that stretched from California all the way to Texas, giving SoCal a geographic footprint that extended far beyond its West Coast base for the first time. The purchase effectively doubled SoCal's pipeline capacity and positioned the company as a player in the broader American oil market, not just a regional West Coast producer.

By the early 1930s, SoCal was generating substantial cash flow from its domestic operations. California was producing more oil than any other state, and SoCal was the biggest producer in California. But the company's leadership recognized a fundamental problem: domestic reserves were finite, and the California oil fields, while productive, would not last forever. If SoCal wanted to survive and grow over the long term, it needed to find new sources of crude oil, preferably very large ones, preferably somewhere that competitors had not already staked their claims.

That search would lead the company to one of the most audacious bets in the history of capitalism: a gamble on the deserts of a remote and impoverished kingdom on the other side of the world.

IV. The Saudi Gamble: Discovery That Changed Everything (1933-1948)

The early 1930s were a desperate time for oil companies. The Great Depression had crushed demand. Oil prices had collapsed. Existing fields in the United States, Mexico, and the Dutch East Indies were producing more crude than the world could consume. And yet, paradoxically, the most forward-thinking oil executives were obsessed with finding new reserves. They understood something that seems counterintuitive: in a cyclical commodity business, the companies that secure the cheapest reserves during the downturn are the ones that dominate when demand recovers. The question was where to look.

The answer, for Standard Oil of California, was the Arabian Peninsula. In the early 1930s, geologists had identified promising geological structures in Bahrain, an island just off the Saudi coast, where SoCal had won a concession and struck oil in 1932. The Bahrain discovery tantalized. If there was oil in Bahrain, the same geological formations almost certainly extended beneath the vastly larger Saudi Arabian mainland. The problem was that Saudi Arabia was one of the most remote, inhospitable, and politically uncertain places on Earth. King Abdulaziz ibn Saud had only recently unified the various tribal territories into the Kingdom of Saudi Arabia. The country had almost no modern infrastructure, no roads, no ports capable of handling heavy equipment. The economy depended primarily on pilgrimages to Mecca. There were no guarantees of political stability, let alone oil.

But SoCal's leadership saw opportunity where others saw risk. On May 29, 1933, at the royal palace in Jiddah, SoCal's representative Lloyd N. Hamilton and Saudi Finance Minister Abd Allah al Sulaiman signed a concession agreement granting SoCal exclusive rights to explore for oil across a vast swath of eastern Saudi Arabia. The terms were remarkably favorable: SoCal would pay the Saudi government an initial loan plus modest royalties, and in exchange it received exploration rights covering an area roughly the size of Texas. On November 8, 1933, SoCal created a subsidiary called the California Arabian Standard Oil Company, or CASOC, to manage the concession.

What happened next was five years of brutal, expensive disappointment. On September 23, 1933, just months after the concession was signed, two SoCal geologists, Robert Miller and Schuyler Henry, arrived at the tiny Saudi port of Jubail on the Persian Gulf coast. The scene that greeted them was about as far from San Francisco as imaginable: a fishing village baking in 120-degree heat, surrounded by featureless desert extending in every direction. The geologists had to hire local Bedouin guides, travel by camel, and contend with sandstorms, scorpions, and the complete absence of anything resembling modern logistics.

Drilling began, and the results were agonizing. Well after well came up dry or produced only trace amounts of oil. CASOC drilled at a geological formation called Dammam Dome, and the first six wells were all failures or marginal producers. The geology was maddeningly complex. Geologists could see the structural formations that should hold oil, but the drill bit kept missing the reservoir, or hitting zones where the rock was too tight to flow commercially.

Back in San Francisco, SoCal's board was getting nervous. The company was pouring money into a desert on the other side of the planet with nothing to show for it. Each dry well added to the sunk cost, and the pressure to abandon the concession and write off the losses was growing. This is the classic tension in exploration-stage resource investment: the rational move, from a financial perspective, is often to walk away. But walking away means losing everything you have already invested, and it means forfeiting the option value of what might still be found.

By 1936, the financial strain had become severe enough that SoCal brought in a partner: the Texas Company, later known as Texaco, which purchased a 50% stake in the concession for $21 million in cash and deferred payments, plus a half interest in Texaco's marketing facilities east of the Suez Canal. The Texaco partnership was not a sign of confidence. It was a sign that SoCal could no longer afford to go it alone.

Then, on March 3, 1938, everything changed. The drilling team at Dammam Well No. 7, which had been deepened beyond the formations where previous wells had been drilled, struck oil in the Arab Zone limestone at a depth of about 4,727 feet. The well immediately began producing over 1,500 barrels per day, a rate that confirmed the presence of a massive commercial reservoir. The celebration in the Saudi desert that night was reportedly riotous. After five years of doubt, SoCal had vindicated the biggest exploration bet in its history.

The impact was transformative, not just for the company but for the entire geopolitical order. Saudi Arabia went from a nomadic backwater whose treasury depended on pilgrimage fees to what would become the most important petroleum-producing nation on Earth. For SoCal, the discovery meant access to oil reserves so vast that they dwarfed anything in the Western Hemisphere. The company had essentially locked up a significant portion of the world's cheapest-to-produce crude oil at a time when most competitors were still focused on domestic reserves.

The discoveries did not stop. Over the next decade, CASOC's geologists found reservoir after reservoir beneath the Saudi sands. The crown jewel came in 1948 with the discovery of the Ghawar Field, which would prove to be the largest conventional oil field ever found, stretching roughly 170 miles long and 20 miles wide beneath the desert surface. Ghawar alone contained estimated original oil in place of over 100 billion barrels, a number so staggering that it is hard to comprehend. To put it in context, the entire proven oil reserves of the United States today are roughly 45 billion barrels. One Saudi oil field, discovered by a California company in 1948, held more than twice that amount.

For investors, the Saudi gamble illustrates a principle that has defined Chevron's strategy for nearly a century: the willingness to make enormous, patient bets on resource access, even when the near-term returns are uncertain and the geopolitical risks are substantial. That DNA is directly visible in the Hess acquisition almost ninety years later, where the same logic applies: pay a large upfront price for access to what management believes are generational assets.

V. Aramco & The Seven Sisters Era (1944-1973)

In January 1944, as World War II raged, SoCal and Texaco quietly renamed their Saudi operating subsidiary. The California Arabian Standard Oil Company became the Arabian American Oil Company, Aramco for short. The name change was more than cosmetic. It signaled that this was no longer a speculative California venture in the desert. It was becoming one of the most important commercial enterprises in the world.

By this time, the strategic significance of Saudi oil had become obvious to the American government. President Franklin Roosevelt met with King Abdulaziz aboard the USS Quincy in Egypt's Great Bitter Lake in February 1945, and the two leaders forged an understanding that would become one of the defining relationships of the postwar era: American security guarantees for Saudi Arabia in exchange for reliable oil supply. Aramco was the commercial vehicle through which this geopolitical bargain operated.

The postwar years brought explosive growth. By 1948, the original two-company partnership was no longer sufficient to develop Saudi reserves at the pace the market demanded. SoCal and Texaco invited two additional Standard Oil descendants into the Aramco consortium: Standard Oil of New Jersey, which would later become Exxon, took a 30% stake, and Socony-Vacuum, which would later become Mobil, took 10%.

The resulting ownership structure, with SoCal, Texaco, and Jersey Standard each holding 30% and Socony-Vacuum holding 10%, created a consortium of four of the most powerful oil companies on Earth, all partnered together in the richest oil province ever discovered. This was not competition. This was a cartel by another name.

Italian energy executive Enrico Mattei understood this perfectly. As head of Italy's state oil company ENI, Mattei sought to join the club of Anglo-American companies that controlled global oil. When he was rebuffed, he coined the phrase "the Seven Sisters" to describe the group: SoCal, Texaco, Standard Oil of New Jersey, Socony-Vacuum, Gulf Oil, Anglo-Persian Oil Company (later BP), and Royal Dutch Shell.

Before the 1973 oil crisis, these seven companies controlled approximately 85% of the world's oil reserves. It was, by any measure, one of the most concentrated oligopolies in the history of global commerce. To put that in modern terms: imagine if seven companies controlled 85% of the world's semiconductor manufacturing, or 85% of all cloud computing infrastructure. The geopolitical leverage was staggering.

For SoCal, membership in this exclusive club was extraordinarily lucrative. By 1949, the company had become one of the few American corporations with more than one billion dollars in assets, a milestone that placed it among the very largest industrial enterprises in the country. Revenues surpassed one billion dollars in 1951. By 1957, SoCal was selling $1.7 billion worth of oil products annually and had become the world's seventh-largest oil concern.

The company did not rely solely on its Saudi bonanza. SoCal's Caltex joint venture with Texaco, established alongside the original Saudi partnership, became a major international marketing and refining operation in its own right, operating refineries and selling petroleum products across Asia, Africa, and Australia. Caltex gave SoCal access to the fastest-growing fuel markets in the world, particularly in postwar Japan, which was industrializing at a pace that created insatiable demand for crude oil and refined products.

Back in the United States, SoCal continued to expand. In 1961, it purchased Standard Oil Company of Kentucky, giving it a retail distribution network across the southeastern states that it had never been able to penetrate from its West Coast base. The Kentucky acquisition was classic Standard Oil descendant strategy: buy another Standard Oil fragment and stitch together a more complete national footprint. It was also a telling reminder of the Rockefeller breakup's legacy. Six decades after the Supreme Court shattered the Standard Oil monopoly, the surviving fragments were slowly, deliberately finding ways to recombine, like droplets of mercury drawn inexorably back together.

But the golden age of the Seven Sisters was approaching its end. Throughout the 1950s and 1960s, the oil-producing nations of the Middle East grew increasingly resentful of the lopsided economics of their concession agreements. The lion's share of the profits from their oil went to the American and European companies that extracted it, while the host countries received modest royalties. In 1960, five oil-producing nations, Saudi Arabia, Iran, Iraq, Kuwait, and Venezuela, formed the Organization of the Petroleum Exporting Countries, OPEC, with the explicit goal of gaining more control over production decisions and pricing.

The formation of OPEC was a slow-burning fuse. For a decade, the organization was largely ineffectual, unable to coordinate production decisions or meaningfully influence prices. But the geopolitical dynamics were shifting. The wave of decolonization sweeping across the developing world emboldened oil-producing nations to demand better terms. Libya's revolutionary government, under Colonel Muammar Gaddafi, successfully forced price increases on the oil companies in 1970, demonstrating that the balance of power had begun to tilt.

SoCal and its Seven Sisters partners were sitting on assets that host governments increasingly viewed as rightfully belonging to their people. The question was not whether the balance of power would shift, but when and how dramatically. The answer came in 1973, and it would force SoCal to reinvent itself.

VI. The Gulf Merger & Becoming Chevron (1973-1984)

On October 19, 1973, the day after President Richard Nixon asked Congress for $2.2 billion in emergency military aid to Israel during the Yom Kippur War, Saudi Arabia announced an embargo on oil exports to the United States. The price of crude quadrupled virtually overnight. Gas station lines stretched for blocks across America. The era of cheap, abundant, American-controlled oil was over.

For SoCal, the aftermath was existential. Saudi Arabia began a gradual nationalization of Aramco, purchasing a 25% ownership stake in 1973, increasing to 60% in 1974, and completing the full takeover in 1980. The company that SoCal had built from nothing in the Saudi desert, which had become the most prolific oil enterprise on the planet, was taken away. SoCal retained a management role for a few more years, training Saudi personnel to operate the fields and refineries that the Americans had built. But the crown jewel was gone. The assets, the reserves, the production, all of it now belonged to the Saudi government.

To appreciate the scale of what SoCal lost, consider this: Aramco would eventually become Saudi Aramco, which in 2019 went public in the world's largest IPO, valued at approximately two trillion dollars. That single company is worth more than the entire market capitalization of Chevron and ExxonMobil combined. SoCal had essentially given birth to the most valuable company on Earth, only to have it nationalized.

The loss of Aramco forced a strategic reckoning. SoCal still had its domestic operations, its refineries, and its distribution network, but it had lost access to the cheapest oil reserves on Earth. The company needed to replace those reserves, and fast. The search for non-OPEC oil became the overriding strategic imperative of the late 1970s and early 1980s.

The answer came from an unexpected direction: not from a drilling campaign, but from a corporate raid that turned into the largest merger in American history.

In early 1984, T. Boone Pickens, the legendary corporate raider from Amarillo, Texas, launched a hostile takeover bid for Gulf Oil Corporation, one of the other Seven Sisters. Pickens was the prototype of the 1980s activist investor: a self-made oilman who believed that the major oil companies were sitting on undervalued assets and returning too little to shareholders. Through his company Mesa Petroleum, he had accumulated a significant stake in Gulf and was pressuring the board to unlock shareholder value. Gulf's management, desperate to avoid being taken over by Pickens, went looking for a white knight.

SoCal stepped up. On March 5, 1984, Gulf's board voted to sell the company to SoCal for $13.2 billion in cash, or $80 per share. At the time, it was the largest corporate merger in American history, surpassing Texaco's recent $10.1 billion acquisition of Getty Oil.

The deal was staggering in its scope. SoCal was acquiring Gulf's oil reserves, estimated at 1.8 billion barrels, plus 3.8 trillion cubic feet of natural gas, 42,000 employees, and operations spanning the globe. Gulf had major production in the North Sea, West Africa, and the Gulf of Mexico, plus significant refining and marketing operations across the eastern United States. Overnight, SoCal doubled its reserve base and became the third-largest oil company in the United States, behind only Exxon and Mobil.

Later that same year, the company changed its legal name to Chevron Corporation. The "Chevron" brand had been used at the company's gas stations for decades, a simple V-shaped logo that had become one of the most recognized symbols in American retail. Now the entire corporation would carry that name. Standard Oil of California, the name that connected the company to its Rockefeller-era origins, was retired.

The Gulf merger was not without pain. Integration was enormously complex. Chevron had to divest certain assets to satisfy FTC requirements. Thousands of employees were laid off as redundant operations were consolidated. Gulf's corporate culture, rooted in its Pittsburgh headquarters, clashed with SoCal's San Francisco-based organization. The Washington Post later reported that Chevron's purchase of Gulf "brought assets and headaches" in roughly equal measure. But the strategic logic was sound: Chevron had replaced a significant portion of the reserves it lost when Saudi Arabia nationalized Aramco, and it had done so without the geopolitical risk of operating in the Middle East.

There is also a subtler lesson in the Gulf deal. T. Boone Pickens never intended to run Gulf Oil. His hostile bid was designed to force the company's entrenched management to unlock shareholder value, either through restructuring or a sale. In the end, Pickens profited handsomely from his Gulf shares when SoCal paid the acquisition premium. But the real beneficiary was Chevron, which acquired decades' worth of reserves and infrastructure in a single transaction. The corporate raider shook the tree, and the strategic acquirer caught the fruit. This dynamic, where activism or hostile pressure creates opportunity for well-capitalized strategic buyers, would replay itself repeatedly in the oil industry over the following decades.

The Gulf merger also established a pattern that would define Chevron's growth strategy for the next four decades: acquire large, reserve-rich companies during periods of industry distress, integrate them ruthlessly, and use the combined scale to drive down costs and improve margins. Every major Chevron acquisition since, from Texaco to Hess, has followed this same playbook. The message is clear: Chevron's competitive advantage is not in finding oil. It is in buying companies that have already found it, and then operating those assets more efficiently than the previous owner did.

VII. The Texaco Acquisition: Creating a Supermajor (1999-2001)

The late 1990s saw a wave of mega-mergers sweep through the global oil industry. British Petroleum merged with Amoco in 1998 to form BP Amoco, and the following year Exxon merged with Mobil to create ExxonMobil, the largest publicly traded oil company in the world. The logic was straightforward: as oil prices languished in the teens per barrel through much of the 1990s, the only way to grow earnings was through scale. Larger companies could spread fixed costs over more barrels, negotiate better terms with service providers, and maintain the capital budgets needed to develop increasingly expensive deepwater and frontier assets.

Chevron watched these mergers from the sidelines, and the view was uncomfortable. The company was large by any normal standard, but in the new world of supermajors, it risked being squeezed. ExxonMobil alone was now roughly three times Chevron's size. If Chevron did not find a transformative deal of its own, it faced the prospect of becoming a mid-tier player in an industry that rewarded scale above almost everything else.

The obvious partner was Texaco. The two companies had been intertwined since 1936, when Texaco purchased its 50% stake in the Saudi concession. Their joint venture Caltex had operated refineries and marketing operations across Asia and Africa for decades. Senior executives knew each other personally. The cultures, while different, shared the same Standard Oil heritage. In 1999, Chevron made an initial approach, but Texaco's board rejected it, finding the proposal unacceptable on grounds of complexity, feasibility, risk, and price. The courtship appeared dead.

Then the pressure intensified. With ExxonMobil and BP Amoco now dominating the landscape, Texaco's standalone position looked increasingly vulnerable. The company's financial performance was mediocre, and its stock price reflected the market's skepticism about its ability to compete independently. In October 2000, Chevron and Texaco announced a definitive merger agreement. Chevron would acquire Texaco in an all-stock transaction valued at approximately $36 billion, with the assumption of an additional $7 billion in Texaco debt bringing the total enterprise value to roughly $43 billion.

The deal faced intense regulatory scrutiny. The FTC had good reason to be concerned: two of the seven original Seven Sisters were about to become one, and the combined company would hold enormous market share in refining and retail gasoline sales, particularly on the West Coast and in the Southeast.

On September 7, 2001, the FTC voted 5-0 to approve the merger, but only after Chevron and Texaco agreed to one of the most comprehensive divestiture packages ever required in a merger. The companies were forced to sell off refineries, pipelines, and retail stations to maintain competitive markets. The Equilon joint venture, which had combined Shell and Texaco's refining operations in the western United States, had to be unwound. It was a complex, expensive process, but it was the price of admission to the supermajor club.

The merger closed on October 9, 2001, less than a month after the September 11 attacks, and in the midst of a global economic downturn. The combined entity was temporarily named ChevronTexaco, and it instantly became the second-largest U.S.-based energy company behind ExxonMobil. Chevron shareholders held approximately 61% of the new company, with Texaco shareholders holding 39%.

Integration was challenging. Texaco had a distinct corporate culture, shaped by decades as an independent major, and its employees did not always appreciate being absorbed by what they perceived as a West Coast competitor. Redundant operations had to be eliminated, layoffs were announced, and the two companies' overlapping global operations had to be rationalized. The process took years and consumed significant management attention.

But the strategic result was transformative. Chevron now had a truly global footprint, with operations spanning production, refining, marketing, and chemicals across every major oil-producing region. The Texaco deal brought deepwater Gulf of Mexico assets, a stronger position in West Africa, and one of the most recognized gasoline brands in the world.

It also brought something harder to quantify but equally important: operating expertise in deepwater production that Texaco had developed over decades in the Gulf of Mexico. Deepwater drilling, for those unfamiliar with the technology, is one of the most complex and expensive engineering undertakings in any industry. Platforms floating in thousands of feet of water drill wells that extend miles beneath the ocean floor, operating under extreme pressures and temperatures. The margin for error is essentially zero, as the Deepwater Horizon disaster would later demonstrate for a competitor.

Texaco's deepwater capabilities gave Chevron a head start in a production category that would become increasingly important as onshore reserves matured.

The Texaco merger also had an ironic symmetry. Two companies that had been partners since 1936, when Texaco bought into the Saudi concession, were now formally one. The Caltex joint venture, the Aramco consortium, the decades of collaboration, all of it was now under a single corporate umbrella. In a sense, the Texaco merger was less a combination of rivals than a formalization of a partnership that had existed, in one form or another, for nearly seventy years.

In 2005, the company quietly dropped "Texaco" from its corporate name, reverting to simply Chevron Corporation, though the Texaco brand continued to appear at gas stations across America. The message was clear: Chevron was the surviving identity, and the Texaco acquisition, while transformative, was now fully absorbed into the larger organization.

VIII. Modern Chevron: Shale, Sustainability & Strategy (2001-Present)

The same year Chevron dropped the Texaco name, it made another major acquisition that would prove strategically important far beyond what anyone imagined at the time. In August 2005, Chevron acquired Unocal Corporation for $17.9 billion, beating out a politically controversial $18.5 billion bid from China's CNOOC that was withdrawn amid intense Congressional opposition. Unocal brought significant assets in the Gulf of Thailand and the Caspian Sea, but the most consequential piece of the deal was something few people were paying attention to in 2005: acreage in the Permian Basin of West Texas.

The Permian Basin is the single most important oil-producing region in the United States, and arguably the world, outside of the Middle East. It stretches across roughly 75,000 square miles of West Texas and southeastern New Mexico, and it contains layered geological formations that have been producing oil since the 1920s. What changed everything was the shale revolution, the combination of horizontal drilling and hydraulic fracturing, commonly known as "fracking," that unlocked vast quantities of oil and gas trapped in tight rock formations that had previously been considered uneconomical. Think of it this way: if a conventional oil reservoir is like a lake underground that you can tap with a vertical straw, a shale formation is more like oil trapped in a sponge. You have to drill sideways through the sponge and then crack it open to release the oil. The technology to do this at commercial scale only matured in the mid-2000s, and it transformed the Permian Basin from a mature, declining field into the most prolific oil basin on the continent.

Chevron moved aggressively to build its Permian position. Through Unocal and subsequent acquisitions, the company assembled one of the largest acreage positions in the basin, concentrated in the highly productive Delaware and Midland sub-basins. The Permian is attractive not just because of the volume of oil it contains, but because of the economics. A well in the Permian can be drilled and completed for roughly $7 to $10 million and can generate positive returns at oil prices as low as $40 per barrel, well below the current price. The short-cycle nature of shale production also gives companies flexibility to ramp up or slow down drilling quickly in response to price signals, unlike multi-billion-dollar deepwater projects that take years to bring online.

By 2020, the Permian had become the engine of Chevron's U.S. production growth, and the company was investing billions annually to drill new wells and expand its infrastructure in the region.

The acquisition pace accelerated. In July 2020, at the nadir of the COVID-19 pandemic oil price collapse, Chevron announced the acquisition of Noble Energy in an all-stock deal valued at approximately $5 billion, with a total enterprise value of $13 billion including debt. Noble brought assets in the Permian Basin, the Denver-Julesburg Basin in Colorado, and, critically, significant natural gas operations offshore Israel. The timing was classic Chevron: buying high-quality assets when nobody else wanted to spend money.

Three years later, in May 2023, Chevron announced the acquisition of PDC Energy for approximately $6.3 billion in stock, representing a total enterprise value of $7.6 billion including debt. PDC brought 275,000 net acres adjacent to Chevron's existing operations in Colorado's Denver-Julesburg Basin, plus additional Permian Basin acreage. The deal added over one billion barrels of oil equivalent in proven reserves.

Then came the Hess deal, the biggest of them all. In October 2023, Chevron announced a $53 billion all-stock merger with Hess Corporation. The headline asset was Hess's 30% stake in the Stabroek Block offshore Guyana, operated by ExxonMobil.

The Stabroek Block deserves a moment of explanation, because it is arguably the most important oil discovery of the twenty-first century. Located roughly 120 miles offshore the small South American nation of Guyana, the block covers an area of approximately 6.6 million acres beneath the Atlantic Ocean. Since ExxonMobil's initial discovery there in 2015, the consortium has made more than 30 discoveries, with estimated recoverable resources exceeding 11 billion barrels of oil equivalent. Production from the block reached roughly 900,000 barrels per day by late 2025, with further development phases planned that could push output well above one million barrels per day.

The Hess deal also brought the company's extensive Bakken Shale operations in North Dakota. But make no mistake: this was a Guyana deal. Chevron was willing to spend $53 billion and endure nearly two years of arbitration uncertainty because management believed that Stabroek was the most attractive undeveloped resource base available at any price. The ICC arbitration, which ExxonMobil filed claiming a right of first refusal over Hess's Guyana stake, was the most significant legal obstacle Chevron had faced in decades. When the tribunal ruled in Chevron's favor in July 2025, it was a watershed moment.

Meanwhile, in August 2024, Chevron had announced the relocation of its corporate headquarters from San Ramon, California, to Houston, Texas. CEO Mike Wirth and Vice Chairman Mark Nelson moved to Houston before the end of 2024, with a phased migration of all corporate functions planned through 2029.

The move was both practical and symbolic. On the practical side, most of Chevron's operational leadership was already based in Houston, with roughly 7,000 employees versus 2,000 in San Ramon. California's regulatory environment and political climate had grown increasingly hostile to fossil fuel companies, with state lawsuits against the industry, aggressive emissions regulations, and a general political culture that viewed Big Oil as a villain rather than a partner.

Houston, by contrast, is the undisputed capital of the global oil and gas industry, home to the headquarters of dozens of energy companies and the professional services ecosystem that supports them.

The move also severed Chevron's last physical link to its origins. For over a century, the company had been headquartered in California, first in San Francisco and later in the suburban enclave of San Ramon. The departure for Texas was a clear signal that the company's identity was no longer tied to its California roots but to the global energy industry centered on the Gulf Coast.

Chevron's most recent quarterly results, for the fourth quarter of 2025, showed the combined impact of this acquisition spree. The company reported revenue of $46.9 billion and net income of $2.8 billion. Production averaged 4.05 million barrels of oil equivalent per day, a 21% increase over the prior year, driven primarily by the addition of Hess's output.

Adjusted earnings per share of $1.52 beat analyst expectations, though net income declined 14% year-over-year due to lower crude oil prices. The results illustrated the fundamental trade-off in Chevron's strategy: the acquisition spree has driven impressive production growth, but lower commodity prices can still overwhelm volume gains in terms of bottom-line profitability. The company maintained its dividend and continued its share buyback program, consistent with its long-standing commitment to shareholder returns.

On the energy transition front, Chevron has taken a pragmatic, some would say skeptical, approach. Unlike some European supermajors that have set aggressive renewable energy targets and even rebranded themselves as "energy companies" rather than oil companies, Chevron has stayed firmly in its lane. The company has bet primarily on natural gas as a transition fuel, along with targeted investments in carbon capture, hydrogen, and renewable fuels.

The company has committed to reducing its carbon intensity but has not pledged to reach net-zero Scope 3 emissions. For those unfamiliar with the terminology, Scope 3 emissions are the greenhouse gases produced when customers burn the oil and gas that a company sells, as opposed to Scope 1 and 2 emissions, which come from the company's own operations. Scope 3 typically represents over 80% of total emissions for an oil and gas company, making it the elephant in the room of any climate commitment.

Chevron's refusal to make a net-zero Scope 3 pledge is a clear statement that it does not intend to exit the oil and gas business. This has drawn criticism from climate activists and some institutional investors, but it has also been rewarded by the market, which has generally favored the pragmatic capital allocation of the American supermajors over the more ambitious transition strategies of their European peers.

Shell and BP, which both announced aggressive energy transition targets in 2020, have since scaled back many of those commitments under shareholder pressure, vindicating Chevron's more conservative approach in the eyes of many investors.

IX. Playbook: The Chevron Management Philosophy

Walk into Chevron's new Houston headquarters and the culture is unmistakable. There is a quiet discipline to the place, an institutional memory that stretches back through Standard Oil to the very origins of the modern corporation. Chevron is not a company that moves fast and breaks things. It is a company that moves deliberately and tries very hard not to break anything, especially its balance sheet.

The central element of Chevron's management philosophy is capital discipline through commodity cycles. The oil and gas business is inherently cyclical: prices boom and bust, often with little warning and for reasons entirely outside any company's control. A geopolitical crisis in the Middle East can send prices soaring. A pandemic can make them go negative. A recession can crush demand for years. No other major industry experiences the kind of violent price swings that characterize the oil market.

Chevron's approach is to maintain a conservative financial structure that allows it to keep investing through downturns while competitors are forced to cut budgets and lay off workers. This means keeping debt levels low, maintaining a strong credit rating, and prioritizing free cash flow generation over production growth for its own sake.

The company has maintained its dividend through every major oil price downturn of the past four decades, including the COVID-19 crash in 2020 when crude briefly went negative. Chevron has increased its annual dividend for over 37 consecutive years, a streak that places it among the "Dividend Aristocrats" of the S&P 500. That consistency matters enormously to the pension funds, endowments, and income-focused investors who make up a significant portion of Chevron's shareholder base.

The second pillar is what might be called the "acquire and optimize" strategy. Chevron has grown primarily through large acquisitions rather than organic exploration. The Gulf merger, the Texaco acquisition, the Unocal deal, Noble Energy, PDC Energy, and now Hess: each of these followed the same basic pattern. Chevron identifies companies with high-quality resource bases that are underperforming operationally or financially, acquires them at what it believes is a fair-to-attractive price, and then applies its operational playbook to drive down costs and increase output. This is not glamorous work. It does not generate the kind of excitement that comes from wildcat exploration or frontier discovery. But it has been remarkably effective at compounding shareholder value over time.

Technology and operational excellence form the third pillar. Chevron holds thousands of patents related to drilling, production, refining, and petrochemical processes. The company is one of the leaders in deepwater production technology, operating complex platforms in the Gulf of Mexico, offshore West Africa, and now Guyana that extract oil from reservoirs thousands of feet beneath the ocean floor.

These are engineering marvels that cost billions of dollars to build and require decades of technical expertise to operate safely and efficiently. A single deepwater platform can cost $5 billion or more to construct and can produce for twenty to thirty years. Getting one wrong, whether through engineering failure, cost overruns, or reservoir underperformance, can impair returns for a generation. Chevron's technical capabilities in deepwater and unconventional resource development represent a genuine competitive moat that smaller companies cannot easily replicate.

The fourth element is geopolitical risk management. Chevron operates in over 180 countries, many of which have unstable political environments, opaque legal systems, and histories of resource nationalism. The company has navigated coups, revolutions, sanctions regimes, and nationalizations over a period spanning more than a century.

The loss of Aramco in the 1970s was a formative experience that taught the organization to diversify its political risk across many jurisdictions rather than concentrating in any single country or region. The lesson was painful but enduring: never again would Chevron bet the company on a single host government's goodwill. This explains the recent strategic emphasis on the Western Hemisphere, particularly the Permian Basin and Guyana, where the political and regulatory environments, while far from perfect, are significantly more stable than the Middle East. The Tengiz project in Kazakhstan, where Chevron has operated since the 1990s, is the notable exception. The field is so productive and the reserves so vast that Chevron has been willing to tolerate the considerable political risks of operating in a post-Soviet autocracy.

Finally, there is the question of shareholder returns versus energy transition investment. Under CEO Mike Wirth, who took the helm in 2018, Chevron has been explicit that its primary obligation is to generate returns for shareholders. Wirth, who spent his entire career at Chevron after joining in 1982, is an engineer by training who rose through the refining and chemicals side of the business. He is not flashy. He does not give TED talks or tweet about climate innovation. His public persona is that of a disciplined operator who speaks in measured, precise terms about returns on capital and break-even oil prices. In interviews, he often returns to a simple framework: Chevron will invest in projects that can earn competitive returns at commodity prices below the midcycle average, and it will return excess cash to shareholders rather than chase low-return growth. This is not a complicated strategy, but executing it consistently through volatile commodity cycles requires an unusual degree of institutional discipline.

The company has committed over $75 billion to share buybacks since 2022, while its lower-carbon investments, though growing, remain a small fraction of total capital spending. Wirth has publicly stated that Chevron will invest in lower-carbon technologies that can generate competitive returns, but it will not allocate capital to energy transition projects purely for reputational purposes. This approach has drawn sharp criticism from environmental groups but has generally been well received by the investment community. The market, it seems, prefers a company that returns cash over one that chases politically popular but economically uncertain energy transition projects.

X. Bull vs. Bear: Investment Analysis

The Bull Case

Start with the assets. Chevron now controls arguably the highest-quality portfolio of upstream assets among the publicly traded supermajors. In the Permian Basin, Chevron holds one of the largest and most productive acreage positions, with decades of drilling inventory remaining. In the Gulf of Mexico, the company operates world-class deepwater platforms producing high-margin barrels. And through the Hess acquisition, Chevron now holds a 30% non-operating interest in Guyana's Stabroek Block, which represents one of the most attractive oil development opportunities on the planet. Stabroek combines low break-even costs, high well productivity, and enormous resource potential in a way that very few upstream opportunities can match.

Capital efficiency reinforces the asset advantage. Chevron consistently generates among the highest returns on capital employed in the integrated oil sector. The company's all-in production costs are below the industry average, its refining operations rank among the most efficient in the United States, and its operating margins tend to outperform peers across the commodity cycle.

The dividend and buyback story is compelling. Chevron's multi-decade streak of dividend increases provides a floor of returning cash to shareholders, while its aggressive buyback program, which has retired a meaningful percentage of shares outstanding in recent years, amplifies per-share earnings growth even when absolute profits are flat. For income-oriented investors, Chevron's yield and growth trajectory compare favorably to most alternatives in the energy sector.

Finally, the bulls argue that crude oil demand will remain resilient far longer than consensus believes. Electric vehicle adoption has been slower than projected in many markets, particularly in the United States and developing economies where charging infrastructure remains sparse and vehicle ranges are insufficient for long-distance driving. Emerging economies in Asia and Africa are still early in their industrialization curves, and their per-capita energy consumption will rise substantially over the coming decades. India alone, with 1.4 billion people and per-capita energy consumption roughly one-third of the global average, represents a massive source of incremental oil demand as its economy grows. Petrochemicals, the raw materials for plastics, fertilizers, and synthetic materials, also remain a resilient source of oil demand that is largely unaffected by electrification. Even in the most aggressive energy transition scenarios, petrochemical feedstock demand continues to grow. If oil demand peaks later and declines more slowly than the most aggressive forecasts suggest, companies like Chevron that have invested in low-cost, long-life assets will benefit enormously.

The Bear Case

The bearish argument starts with the demand trajectory. While peak oil demand is not imminent, the direction is clear: renewable energy costs continue to fall, electric vehicle market share is growing, and government policies around the world are increasingly designed to reduce fossil fuel consumption. The International Energy Agency, in its most recent World Energy Outlook, projected that global oil demand could peak before 2030 under its stated policies scenario, though the timing remains highly uncertain and contested by OPEC and the oil industry.

In a world where oil demand peaks in the 2030s and begins to decline, the value of long-life oil assets, the very assets that make Chevron's portfolio so attractive, could become impaired. The Guyana Stabroek Block, for example, is expected to produce for decades. If oil demand is declining by the 2040s, those later barrels may need to be sold into a market with structurally lower prices.

Stranded asset risk is the most extreme version of this concern. If climate policy tightens faster than expected, or if technology breakthroughs accelerate the energy transition, some of the oil reserves on Chevron's books may never be economically produced. This risk is difficult to quantify but impossible to ignore. It is the central paradox of investing in oil companies today: the very long-life reserves that make these companies valuable in a world of sustained demand are the same reserves that could become liabilities in a world of declining demand.

From a Porter's Five Forces perspective, the competitive dynamics are mixed.

The threat of substitutes is the most significant force: every electric vehicle sold, every solar panel installed, and every wind turbine erected represents a barrel of oil that will never be burned. This is the long-term existential risk for any oil company.

Supplier power is moderate, as the oilfield services industry has consolidated significantly in recent years, giving companies like SLB and Halliburton more pricing power. When rig counts rise, service companies can charge premium rates, eating into producer margins.

Buyer power is generally low because oil is a fungible global commodity priced on world markets. No single buyer can dictate terms to a Chevron or an ExxonMobil.

The threat of new entrants is low for conventional oil, where the capital requirements and technical barriers are enormous, but high for renewable energy, where capital requirements and technology barriers are falling rapidly.

Competitive rivalry among the supermajors is intense but generally rational, with companies competing primarily on cost efficiency and portfolio quality rather than on price.

Through the lens of Hamilton Helmer's 7 Powers framework, Chevron possesses elements of several strategic advantages.

Scale economies in refining and petrochemicals provide a cost advantage that smaller competitors cannot match. Process power, the result of decades of operational learning and technology development, gives Chevron an edge in deepwater and unconventional production. Resource advantages come from its premium asset positions in the Permian, Gulf of Mexico, and Guyana.

But Chevron lacks meaningful switching costs, as crude oil is a commodity, and its network effects are limited. Branding matters at the retail pump, but at the wholesale level, a barrel of Chevron crude is interchangeable with a barrel from any other producer.

The company's most durable competitive advantage is probably its counter-positioning relative to national oil companies. NOCs like Saudi Aramco, ADNOC, and Petrobras control vastly more reserves than Chevron, but they are constrained by government mandates, social obligations, and political interference. Chevron, as a publicly traded company with an independent board, can allocate capital more efficiently and respond to market signals more quickly.

Compared to ExxonMobil, its closest peer, Chevron trades at a slight premium on most valuation metrics, reflecting the market's assessment that Chevron's asset quality and growth prospects are marginally superior. However, ExxonMobil's larger scale in refining and chemicals provides more diversification and downstream earnings stability. ExxonMobil also made its own Guyana play, as operator of the Stabroek Block with a 45% interest, meaning it benefits from the same world-class asset without having paid the Hess acquisition premium. Against European supermajors like Shell and TotalEnergies, Chevron's valuation premium is more significant, reflecting American investors' preference for pure-play oil and gas exposure over the more diversified energy transition strategies pursued by the Europeans. This valuation gap has persisted for several years and shows no signs of closing, which raises the interesting question of whether the European companies' lower valuations represent an opportunity or a structural discount that reflects genuine strategic disadvantages.

One myth worth challenging is the notion that Chevron is a "growth company" among the supermajors. With the Hess acquisition now closed, Chevron's production has jumped dramatically, but the organic growth rate excluding acquisitions has been more modest. The Permian Basin provides a genuine organic growth engine, but many of Chevron's other basins are mature and declining. The company's production trajectory over the next five years will depend heavily on the pace of Guyana development and continued Permian drilling, both of which face execution risks. The growth story is real, but it is more nuanced than the headline production figures suggest.

KPIs to Watch: For investors following Chevron's ongoing performance, two metrics matter most. First, upstream production cost per barrel of oil equivalent (including both operating expenses and capital expenditures). This number captures the efficiency of Chevron's exploration and production operations and determines how much free cash flow each barrel generates at any given oil price. Second, free cash flow yield, which measures the total cash returned to shareholders through dividends and buybacks relative to the company's market capitalization. This is the ultimate measure of whether Chevron's capital allocation strategy is working. If production costs per barrel rise while free cash flow yield falls, it would signal that the acquisition-heavy strategy is destroying rather than creating value.

XI. Power & Greed: The Darker Chapters

No honest account of Chevron's history can avoid the company's darker chapters, and there are several that deserve serious scrutiny. The Standard Oil lineage conferred not just operational discipline but also a reputation for ruthless, often predatory, business practices that has followed the company through every decade of its existence.

During the Seven Sisters era, SoCal and Texaco earned the nickname "the terrible twins" for their aggressive approach to securing oil concessions and market share. The two companies operated with a level of coordination and mutual advantage, through the Caltex joint venture and the Aramco consortium, that many observers viewed as fundamentally anticompetitive.

While technically legal under the concession frameworks of the time, their behavior squeezed out independent companies and developing nations alike. Smaller oil companies that tried to break into the Middle East market found themselves frozen out by the interlocking web of concessions, joint ventures, and marketing agreements that the Seven Sisters had constructed. It was, in many ways, a private government that operated parallel to and sometimes in conflict with the actual governments of the countries where the oil was located.

The most infamous chapter is the Ecuador litigation saga. In 1964, Texaco, before its merger with Chevron, began oil production in Ecuador's Oriente region, a pristine stretch of Amazon rainforest. Over the next three decades, the consortium led by Texaco drilled hundreds of wells and built production infrastructure across an area covering roughly 1,700 square miles.

The environmental impact was devastating. According to plaintiffs, the operations dumped billions of gallons of toxic wastewater directly into rivers and streams, contaminated soil across thousands of sites, and caused elevated rates of cancer and other health problems among indigenous communities.

In 1993, Ecuadorian residents filed a class-action lawsuit against Texaco in New York federal court. The case, Aguinda v. Texaco, was eventually dismissed on the grounds that it should be tried in Ecuador rather than the United States. When the plaintiffs refiled in Ecuador in 2003, a new chapter of the saga began. In 2011, an Ecuadorian court issued an $18 billion judgment against Chevron, later reduced to $9.5 billion. Chevron refused to pay, arguing that the judgment was the product of fraud and corruption.

In a remarkable twist, a U.S. federal court in New York ruled in 2014 that the Ecuadorian judgment was indeed the product of racketeering activity. Judge Lewis Kaplan found that the lead plaintiff's attorney, Steven Donziger, had engaged in a pattern of fraud, including ghostwriting expert reports, bribing a judge, and fabricating evidence.

Donziger was subsequently disbarred and eventually charged with criminal contempt, for which he was sentenced to six months in prison. His case became a cause celebre for environmental activists who viewed the prosecution as Chevron-backed retaliation. In 2018, the Permanent Court of Arbitration in The Hague separately ruled that the Ecuador judgment was tainted by fraud and should not be recognized by other nations' courts.

The Ecuador case is, in short, a mess. Environmental damage clearly occurred, indigenous communities clearly suffered. But the legal process intended to provide remedy was itself corrupted, leaving the victims without justice and Chevron in the uncomfortable position of having escaped a massive liability through legal technicalities while never fully addressing the underlying environmental harm.

Texaco did perform a $40 million remediation in the 1990s that Ecuador's government signed off on, but many argue it was grossly insufficient given the scale of contamination. The case remains one of the most contested and emotionally charged environmental disputes in corporate history, and it continues to shape public perception of Chevron decades later.

Beyond Ecuador, Chevron has faced criticism for its operations in countries with authoritarian governments. The company operated in Myanmar for decades, partnering with the military junta through a pipeline joint venture. It has significant operations in Kazakhstan, Nigeria, Angola, and other countries where corruption and human rights concerns are endemic. Chevron's defense, that it operates within legal frameworks and that its presence creates economic benefits for host communities, is factually accurate but morally incomplete. The company profits from political stability that is often maintained through repression.

On the climate front, Chevron, like all major oil companies, spent decades funding industry groups that questioned the science of climate change and lobbied against carbon-reduction policies. The American Petroleum Institute, of which Chevron has long been a leading member, spent millions of dollars on campaigns designed to cast doubt on the scientific consensus around human-caused climate change, even as the evidence grew overwhelming. Internal documents that have emerged through litigation suggest that some oil companies, including Chevron's predecessors, had internal research as early as the 1980s suggesting that fossil fuel combustion was contributing to global warming. The gap between what the industry knew and what it said publicly is the subject of ongoing litigation in multiple jurisdictions. As of early 2026, numerous cities, counties, and states have filed lawsuits against the major oil companies alleging deception about climate change, fraud, and seeking damages for climate-related infrastructure costs. These cases are moving through the courts at varying speeds, and their ultimate outcomes remain uncertain. But they represent a material legal overhang for all the supermajors, Chevron included. Even if the companies ultimately prevail in most of these cases, the legal costs and reputational damage are significant, and the possibility of an adverse ruling that opens the door to massive damages cannot be dismissed.

The labor and community impacts of Chevron's operations also deserve mention. In Richmond, California, where Chevron operates one of the largest oil refineries on the West Coast, the relationship between the company and the surrounding community has been fraught for decades. A major fire at the Richmond refinery in 2012 sent a large plume of toxic smoke over the community, sending thousands of residents to hospitals for treatment. Chevron ultimately settled with the city and county for over $2 million and invested in safety upgrades, but the incident crystallized longstanding community grievances about pollution, health impacts, and the perception that the company prioritized profits over the safety of its neighbors.

XII. Epilogue: What Does the Future Hold?

As of early 2026, Chevron stands at a crossroads that is both entirely unique and fundamentally familiar. The company faces the same question it has faced in every prior transition: how do you preserve and grow value from a dominant position in one energy system while the world begins to transition to another?

The management's answer, articulated clearly by CEO Mike Wirth, is to bet on the world still needing enormous quantities of oil and gas for decades to come, while selectively investing in lower-carbon technologies that can earn competitive returns. The Hess acquisition was the clearest expression of this philosophy: rather than redirecting tens of billions toward wind farms and solar panels, Chevron invested in what it believed was the highest-quality conventional oil asset available.

Natural gas is central to the strategy. Chevron is one of the world's largest producers of liquefied natural gas, or LNG, through its interests in Australia's Gorgon and Wheatstone projects and its operations in the Permian Basin and elsewhere. LNG is essentially natural gas that has been cooled to minus 260 degrees Fahrenheit, turning it into a liquid that can be loaded onto ships and transported across oceans, unlike pipeline gas which can only flow to connected markets. The LNG business has grown enormously over the past decade as Asian and European countries have sought to diversify their energy supply away from pipeline dependence on Russia and the Middle East.

Management views natural gas as a "bridge fuel" that will see growing demand for decades as developing economies transition away from coal for power generation. When burned, natural gas produces roughly half the carbon dioxide of coal per unit of energy generated, making it a meaningful improvement in emissions even if it is not zero-carbon. Whether gas truly serves as a bridge or merely delays the transition to renewables is one of the central debates in energy policy, and the answer matters enormously for Chevron's long-term valuation.

The company has also placed smaller bets on hydrogen production, carbon capture and storage, and renewable fuels. Carbon capture, for those unfamiliar with the concept, involves capturing carbon dioxide emissions from industrial sources or directly from the atmosphere and storing them underground, preventing them from contributing to global warming. The technology works, but it remains expensive and energy-intensive, and critics argue that it serves primarily as a justification for continued fossil fuel production.

These investments are growing but remain modest relative to Chevron's core oil and gas spending. The company's $10 billion lower-carbon investment commitment through 2028, while significant in absolute terms, represents a fraction of its overall capital budget.

The consolidation endgame in the oil industry is also worth watching. Through successive mega-mergers over the past four decades, the original Seven Sisters have been reduced to effectively three Western supermajors: ExxonMobil, Chevron, and Shell, with BP and TotalEnergies occupying slightly smaller positions. Further consolidation among the top tier is certainly possible, though the regulatory obstacles to any combination of these remaining giants would be formidable. A Chevron-Shell combination, for example, would create a company rivaling ExxonMobil in scale, but it would face antitrust scrutiny in dozens of jurisdictions and would require years to close and integrate. More likely is continued bolt-on acquisition activity, as the supermajors acquire smaller independent producers to add inventory and reserves. Companies like ConocoPhillips, Hess (now part of Chevron), Pioneer Natural Resources (acquired by ExxonMobil), and Devon Energy have been the targets of this consolidation wave, and there are fewer attractive independent targets remaining.

There is also the question of what happens when the Western supermajors face off against the national oil companies in a shrinking market. Saudi Aramco, ADNOC, QatarEnergy, and other state-owned producers control the vast majority of the world's remaining conventional reserves and have the lowest production costs. In a world where oil demand is declining, these NOCs could maintain or even increase production at the expense of higher-cost Western producers. Chevron's response has been to focus on assets where it can produce at the lowest possible cost, which is why the Permian, Gulf of Mexico, and Guyana are so central to the strategy. These are assets where Chevron can compete on cost with all but the most advantaged OPEC producers.

The Tengiz expansion project in Kazakhstan, known as the Future Growth Project, reached a major milestone in January 2025 with first oil production. Chevron holds a 50% interest in the Tengiz field through its Tengizchevroil joint venture, and the expansion project, which cost over $48 billion, is expected to significantly increase production from one of the world's largest oil fields. The project's troubled history, with massive cost overruns and years of delays, is a reminder that even the most disciplined operators face enormous execution risks in frontier environments.

In November 2025, Chevron announced a partnership to develop data center infrastructure in West Texas, leveraging natural gas to power the energy-intensive computing facilities that are proliferating as artificial intelligence demands surge. It was a small but symbolically interesting move: an oil company positioning itself as a power provider to the technology industry, bridging the old economy and the new.

Chevron's story is ultimately a story about adaptation. The company has survived the breakup of Standard Oil, the loss of Aramco, the OPEC embargo, the oil price collapse of the 1980s, the industry mega-merger wave, and the rise of the energy transition narrative. Each time, it has emerged larger and more resilient than before.

Whether it can navigate the next chapter, the potential decline of the very commodity that has sustained it for 150 years, with equal success is the defining question for long-term investors. The management team clearly believes it can. The market, for now, is inclined to agree.

But the history of the energy industry is littered with dominant companies that failed to adapt to technological and market shifts. Whether Chevron will be different is a bet that every holder of CVX shares is making, knowingly or not.

XIII. Recent News

Hess Acquisition Closes (July 2025): Chevron completed its $53 billion acquisition of Hess Corporation on July 18, 2025, after winning the ICC arbitration against ExxonMobil over Hess's 30% stake in Guyana's Stabroek Block. The tribunal found that ExxonMobil's claimed right of first refusal did not apply to the merger as structured.

Q4 2025 Earnings (January 2026): Chevron reported fourth-quarter 2025 net income of $2.8 billion on revenue of $46.9 billion. Production averaged 4.05 million barrels of oil equivalent per day, up 21% year-over-year, driven by the Hess acquisition. Adjusted earnings per share of $1.52 exceeded analyst estimates of $1.45.

Headquarters Relocation (August 2024-Ongoing): Chevron announced the relocation of its corporate headquarters from San Ramon, California, to Houston, Texas in August 2024. CEO Mike Wirth and other senior leaders moved before the end of 2024, with a full migration of corporate functions expected through 2029.

Tengiz First Oil (January 2025): The Future Growth Project at Chevron's Tengizchevroil joint venture in Kazakhstan achieved first oil production in January 2025, a major milestone for the multi-billion dollar expansion of one of the world's largest oil fields.

Data Center Power Partnership (November 2025): Chevron announced a partnership to develop natural gas-powered data center infrastructure in West Texas, positioning itself as an energy supplier for the growing artificial intelligence computing industry.

PDC Energy Integration (2023-2024): Chevron completed the integration of PDC Energy's operations, adding over one billion barrels of oil equivalent in proven reserves and 275,000 net acres in the Denver-Julesburg Basin and Permian Basin.

XIV. Links & References

Primary Sources and Company Filings - Chevron Corporation 2025 Annual Report and 10-K filing (SEC EDGAR) - Chevron Q4 2025 Earnings Press Release (chevron.com/newsroom) - Chevron/Hess Merger Proxy Statement (SEC EDGAR) - FTC Consent Agreement: Chevron Corporation and Texaco Inc. (ftc.gov)

Historical References - "The Prize: The Epic Quest for Oil, Money & Power" by Daniel Yergin (Simon & Schuster, 1991) - "The Seven Sisters: The Great Oil Companies and the World They Shaped" by Anthony Sampson (Hodder & Stoughton, 1975) - "Oil, God, and Gold: The Story of Aramco and the Saudi Kings" by Anthony Cave Brown (Houghton Mifflin, 1999) - Chevron Corporate History (chevron.com/who-we-are/history) - SCVHistory.com: Story of Standard Oil Co. of California - Arabian American Oil Company (ARAMCO) entry, Encyclopedia.com

Industry Reports and Analysis - International Energy Agency World Energy Outlook 2025 - EIA Permian Basin Production Reports - Wood Mackenzie: Guyana Stabroek Block Analysis - S&P Global Commodity Insights: Integrated Oil Company Benchmarking

Legal and Regulatory Sources - Chevron Corp. v. Donziger, U.S. District Court, Southern District of New York (2014) - ICC Arbitration: Stabroek Block Joint Operating Agreement Dispute (2025) - Permanent Court of Arbitration: Chevron v. Ecuador (2018)

News Sources - CNBC: "Chevron completes Hess acquisition after defeating Exxon" (July 18, 2025) - Fortune: "Chevron wins huge legal fight against Exxon" (July 18, 2025) - Washington Post: "Chevron's purchase of Gulf brought assets and headaches" (1987) - CNN: "Chevron says it's moving headquarters from Bay Area to Houston" (August 2, 2024)

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube