CVS Health: From Corner Drugstore to Healthcare Colossus

I. Introduction & Episode Roadmap

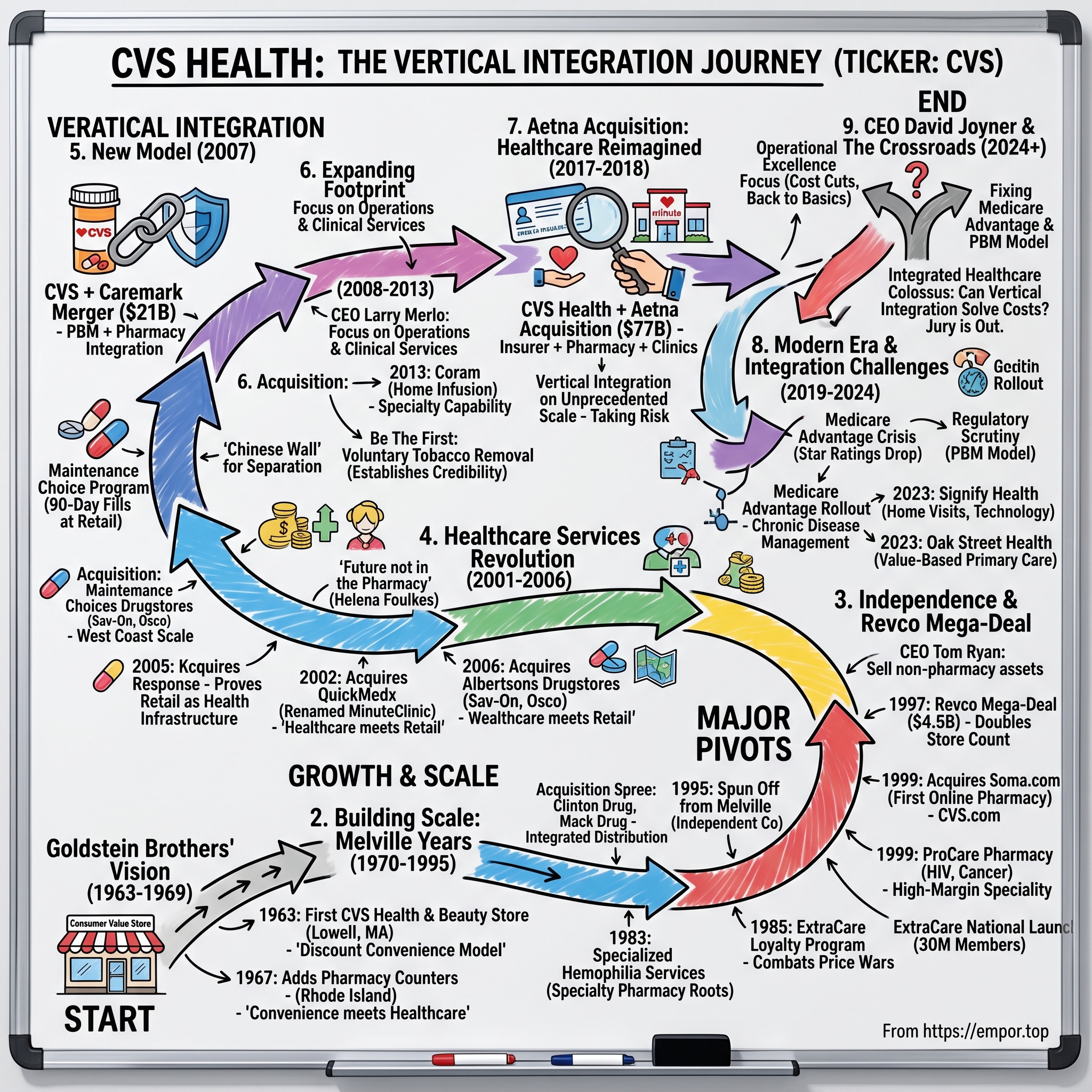

Picture this: It's 2018, and CVS Health CEO Larry Merlo is standing before a packed conference room of Wall Street analysts. He's about to announce the largest healthcare merger in U.S. history—a $77 billion acquisition of insurance giant Aetna. The room is electric with skepticism. How does a company that started selling toothpaste and shampoo in strip malls dare to reshape American healthcare? Yet here stands Merlo, calmly explaining how CVS will become something unprecedented: a vertically integrated healthcare behemoth that touches patients at every point from prescription to primary care to insurance claims. The transformation is staggering. CVS Health annual revenue for 2024 was $372.809B, a 4.2% increase from 2023—making it one of the largest companies in America by revenue, bigger than Microsoft, Apple, or any tech giant save Amazon. This isn't just growth; it's metamorphosis. What started as a chain of health and beauty stores in strip malls now operates as a three-headed healthcare colossus: the nation's largest pharmacy chain with over 9,000 locations, one of the three dominant pharmacy benefit managers (PBMs) controlling drug pricing for millions, and through Aetna, a major health insurer covering 26 million Americans.

The thesis we'll explore is deceptively simple yet profoundly complex: Can vertical integration—the old-school industrial strategy of owning your supply chain—actually solve the Gordian knot of American healthcare costs? While tech companies chase AI moonshots and politicians debate single-payer systems, CVS has been quietly assembling the pieces to become something unprecedented: a company that can theoretically manage your health from the moment you walk into a MinuteClinic with the sniffles to negotiating your cancer drug prices to paying your hospital bills.

What makes this story particularly fascinating for students of business strategy is the sheer audacity of the transformation. This isn't Netflix pivoting from DVDs to streaming—a shift in distribution of the same product. This is more like if Blockbuster had bought Paramount Pictures, then acquired DirecTV, then started manufacturing televisions. Each acquisition wasn't just adding revenue; it was fundamentally changing what kind of company CVS was.

The lessons here transcend healthcare. We'll see how a company can use M&A not just for growth but for complete reinvention. We'll examine what happens when you try to reconcile incompatible business models—high-frequency retail transactions versus complex insurance underwriting—under one roof. We'll witness the challenges of operating in the most regulated industry in America while trying to disrupt it from within.

Most critically, we'll grapple with the central paradox of CVS's strategy: The company makes money from both sides of the healthcare cost equation. Its PBM profits when drug prices are opaque and complex; its insurance arm profits when medical costs are controlled. Its pharmacies want higher reimbursements; its PBM wants to pay less. Can these inherent conflicts be resolved through corporate structure, or is CVS attempting something fundamentally impossible?

As we trace this journey from a single store in Lowell, Massachusetts to a company touching one in three Americans' healthcare, remember that this isn't just corporate history—it's a live experiment in whether American capitalism can solve its own healthcare crisis. The jury is still very much out.

II. Origins: The Goldstein Brothers' Vision (1963–1969)

The year was 1963. The Beatles hadn't yet appeared on Ed Sullivan. Medicare didn't exist. And in Lowell, Massachusetts—a fading mill town 25 miles northwest of Boston—brothers Stanley and Sidney Goldstein were about to make a bet that would reshape American healthcare.

The Goldsteins weren't pharmacists. They weren't healthcare visionaries. They were retailers who ran a successful chain of promotional stores called Consumer Value Stores. But they saw something others missed: the American consumer was changing. The post-war suburban boom meant families were driving everywhere, women were entering the workforce in unprecedented numbers, and shopping habits were shifting from daily errands to weekly hauls. The old model of specialized shops—one for cosmetics, another for medicines, a third for sundries—was dying.

Their first CVS store at 35 Merrimack Street in Lowell was revolutionary for its simplicity. While competitors focused on either pharmacy or beauty products, the Goldsteins created what they called a "health and beauty aid store." No prescription counter initially—just an expertly merchandised selection of shampoos, cosmetics, over-the-counter medicines, and personal care items at discount prices. The innovation wasn't the products; it was the presentation. Wide aisles, bright lighting, clear pricing, self-service. This was shopping as convenience, not consultation.

Ralph Hoagland, who joined as a partner, brought operational discipline to the brothers' merchandising instincts. While Stanley focused on real estate and expansion, Sidney perfected the product mix. They discovered that health and beauty items had magical retail properties: high margins, frequent repurchase cycles, and recession resistance. People might skip a new dress during tough times, but they'd always buy toothpaste.

By 1964, just one year in, CVS had mushroomed to 17 stores. The Goldsteins had found their formula: lease cheap space in strip malls anchored by supermarkets, undercut department store prices by 20-30%, and turn inventory fast. But they were still missing the keystone of their eventual empire.

The pivot came in 1967, and it happened almost by accident. The Goldsteins were struggling to differentiate from discount chains like Caldor and Bradlees that also sold health and beauty aids. During a store visit in Rhode Island, a local pharmacist approached them about leasing space within their store. The brothers initially resisted—pharmacy meant regulation, specialized labor, and slow-moving inventory. But Sidney ran the numbers and discovered something extraordinary: pharmacy customers visited stores twice as often as regular shoppers and spent three times as much annually.

That year, CVS opened its first pharmacy departments in Warwick and Cumberland, Rhode Island. The pharmacist wasn't hidden in the back like at traditional drugstores but positioned prominently where customers could see the professional service integrated with convenient shopping. It was a subtle but radical reimagining of the pharmacy's role—not as a standalone medical service but as part of a broader health and convenience offering.

The timing was perfect. The year 1965 had seen the creation of Medicare and Medicaid, dramatically expanding prescription drug coverage. The birth control pill, approved in 1960, was driving millions of women to pharmacies monthly. Antibiotics and other wonder drugs were becoming mainstream. The Goldsteins weren't just adding a service; they were positioning themselves at the intersection of healthcare and consumerism just as that intersection was becoming the most important corner in American retail.

By 1969, CVS operated 40 stores and was generating revenues that caught the attention of Melville Corporation, a retail conglomerate best known for its Thom McAn shoe stores. When Melville came calling with an acquisition offer, the Goldsteins faced a classic entrepreneur's dilemma. They'd built something successful but lacked the capital for national expansion. Walgreens had 500 stores. Eckerd had 300. CVS needed scale to compete.

The sale to Melville, completed in 1969, valued CVS at roughly $40 million (about $320 million in today's dollars). The Goldsteins walked away wealthy, but more importantly, they'd proven that pharmacy could be democratized, that healthcare and retail weren't separate worlds but complementary businesses.

What the Goldsteins understood—and what would drive CVS for the next five decades—was that Americans wanted healthcare to be convenient, accessible, and affordable. They didn't want to make appointments for basic needs or travel to multiple stores for routine purchases. The corner drugstore model was dying not because people didn't need pharmacies but because the format hadn't evolved with American life.

This foundational insight—that healthcare access was as much about convenience as medicine—would guide every major decision in CVS's history. The Goldsteins didn't just create a store; they created a template for how Americans would increasingly access healthcare: through retail. The prescription counter that started as an afterthought in Rhode Island would become the gateway to an empire.

III. Building Scale: The Melville Years (1970–1995)

When Stanley Goldstein walked into the Melville Corporation boardroom in early 1970 for his first meeting as president of the CVS division, he found skepticism written on every face. Melville's board knew shoes—they'd built an empire on Thom McAn. They knew apparel through their Chess King stores. But pharmacy? That was uncharted territory, a regulatory minefield in an industry dominated by giants like Walgreens and Eckerd.

"Give me five years," Goldstein reportedly told them. "We'll be operating 200 stores generating margins that'll make your shoe business look antiquated." It was a bold promise. CVS had just 100 stores, all clustered in New England. But Goldstein had a playbook that would transform American retail pharmacy.

The first move came in 1972 with the acquisition of 84 Clinton Drug and Discount Stores. Clinton was struggling, bleeding cash, but it had something CVS desperately needed: prime real estate locations across the Northeast corridor. Goldstein didn't want Clinton's management or systems—he wanted their storefronts. Within six months, every Clinton store had been converted to the CVS format, with wider aisles, better lighting, and most critically, a pharmacy that generated 50% of revenues despite occupying just 15% of floor space.

The integration revealed Goldstein's genius for operational efficiency. While competitors maintained separate distribution centers for pharmacy and front-store merchandise, CVS pioneered integrated distribution. Prescription drugs and shampoo arrived on the same truck, were checked in by the same staff, and could be purchased in a single transaction. This seemingly simple innovation cut logistics costs by 30% and allowed CVS to undercut competitors' prices while maintaining margins.

But the real innovation came in 1977 with the acquisition of 36 Mack Drug stores in New Jersey. Mack was a 50-year-old chain, a venerable name in Jersey pharmacy. The conventional playbook would have been to maintain the Mack brand in Jersey while keeping CVS in New England. Instead, Goldstein did something radical: he kept select Mack pharmacists but replaced everything else—the name, the format, the suppliers, even the pharmacy software.

"A pharmacy is only as good as the relationship between the pharmacist and the customer," Goldstein explained to skeptical Melville executives. "We're not buying stores; we're buying trust." The strategy worked. Prescription volumes at converted Mack stores actually increased as customers appreciated the lower prices and better selection while maintaining their relationship with their pharmacist.

The 1980s brought new challenges and opportunities. The Reagan administration's cost-containment efforts meant insurance companies were squeezing pharmacy reimbursements. Meanwhile, the AIDS crisis was creating demand for specialized, high-cost medications that required new handling procedures and patient counseling. CVS's response was to go where others feared to tread.

In 1983, CVS made a prescient move: it began providing specialized pharmacy services for hemophilia patients. Hemophilia drugs were expensive, required careful handling, and involved complex insurance billing. Most pharmacies wanted nothing to do with them. But CVS saw opportunity in complexity. They created dedicated teams, specialized storage facilities, and direct delivery services. The hemophilia program generated 20 times the revenue per patient of traditional prescriptions and established CVS as a player in what would later be called "specialty pharmacy"—now a $300 billion market.

The Melville years weren't without struggles. In 1985, Peoples Drug, a Washington D.C. chain, launched an aggressive price war, offering prescriptions at cost to gain market share. CVS stores in the mid-Atlantic saw same-store sales plummet 15% in three months. The board pressured Goldstein to match Peoples' prices. Instead, he launched ExtraCare, a pioneering loyalty program that offered discounts not on prescriptions but on front-store merchandise to pharmacy customers.

"We're not going to win a race to the bottom on prescription prices," Goldstein told his team. "We're going to make the pharmacy customer so valuable that we can afford to lose money on prescriptions and make it up on everything else they buy." The strategy stabilized sales and would later become the industry standard.

By 1990, CVS had grown to 750 stores, but growth was slowing. The easy targets in the Northeast had been acquired. Expansion into the Southeast meant competing with Eckerd on their home turf. The Midwest was Walgreens territory. The addition of the 23-store Rix Dunnington chain that year felt almost quaint compared to the massive acquisitions of the 1970s.

The real action was happening at Melville headquarters. The conglomerate model that had worked in the 1970s was falling out of fashion on Wall Street. Investors wanted "pure plays"—companies focused on single industries. Melville's portfolio of shoe stores, clothing chains, and pharmacies looked increasingly anachronistic. By 1995, CVS was generating over $5 billion in revenue, accounting for nearly 40% of Melville's total sales but receiving a fraction of corporate investment.

In late 1995, Melville CEO Francis Rooney made a radical decision: spin off CVS as an independent company. The pharmacy chain that had been acquired for $40 million would be valued at over $2.5 billion as a standalone entity. But independence meant CVS would need to find its own path in an increasingly competitive landscape.

As Stanley Goldstein prepared to hand over leadership to Tom Ryan, a fast-rising executive who'd started as a pharmacist, he reflected on what they'd built. CVS had grown from 100 to nearly 1,400 stores, from $300 million to $5 billion in revenue. But more than scale, they'd proven that pharmacy could be more than pills in bottles—it could be the foundation of a healthcare services company.

"We always said we were in the convenience business," Goldstein would later recall. "It just happened that the most convenient thing we could offer was healthcare." This philosophy—healthcare as a consumer service rather than a medical specialty—would guide CVS through its next transformation. The Melville years had given CVS scale. Independence would give it ambition.

IV. Independence & The Revco Mega-Deal (1996–2000)

Tom Ryan stood before 300 CVS store managers at the Foxwoods Resort in Connecticut on a humid August morning in 1996. It was three months after the spin-off from Melville, and CVS was trading at $31 per share—a respectable debut for a newly independent company. But Ryan, who'd been named CEO at just 43, saw danger everywhere he looked.

"Walgreens has 2,100 stores. Rite Aid has 2,500. We have 1,400," Ryan began, his Boston accent cutting through the ballroom. "In eighteen months, one of two things will happen: either we'll be twice our current size, or we'll be part of someone else's growth story." The room fell silent. Everyone knew he was right. The pharmacy chains were consolidating rapidly, and CVS's strong but regional presence made it either predator or prey.

Ryan's first major decision as CEO of the independent CVS was counterintuitive: he sold off everything that wasn't pharmacy. Bob's Stores, a clothing chain CVS had inherited from Melville, was generating decent returns, but Ryan unloaded it for $60 million. "Every dollar and every minute spent on anything other than pharmacy is a distraction," he told the board. "We're not a retailer that happens to have pharmacies. We're a pharmacy company that happens to have retail."

But the real prize was sitting in bankruptcy court in Cleveland. Revco, once the second-largest drugstore chain in America with 2,500 stores, had been destroyed by a failed leveraged buyout in the late 1980s. By 1996, they'd emerged from bankruptcy but were struggling with $1.2 billion in debt and declining same-store sales. Wall Street considered Revco damaged goods. Ryan saw opportunity.

The negotiation was brutal. In November 1996, Ryan flew to Cleveland to meet with Revco CEO Dwayne Hoven. The first offer was $3.5 billion in stock—a 20% premium to Revco's trading price. Hoven laughed. "Tom, you're trying to steal a company with 2,500 stores. Come back when you're serious." Ryan returned two weeks later with a revised offer: $3.7 billion plus assumption of debt. The total deal value approached $4.5 billion—larger than CVS's own market cap.

Wall Street was horrified. CVS shares dropped 15% on the announcement. "Ryan's lost his mind," one analyst told the Wall Street Journal. "He's betting the entire company on fixing someone else's mess." The criticism stung, but Ryan had done his homework. Revco's problems weren't operational—their stores generated solid traffic. The issue was financial engineering from the failed LBO. Strip away the debt, apply CVS's systems, and Revco's stores could be gold mines.

The integration was a masterclass in execution. Ryan created "adoption teams"—one CVS manager paired with one Revco manager for each region. Rather than impose CVS systems wholesale, teams identified best practices from both companies. Revco's photo processing was superior; it became the CVS standard. CVS's pharmacy workflow was more efficient; it was rolled out to all Revco stores.

But the masterstroke was the store rationalization. Ryan identified 400 locations where CVS and Revco stores were within a mile of each other. Conventional wisdom said close the weaker store. Ryan did something different: he closed the stronger store if it had a better real estate value. He then sold the properties to developers, generating $500 million in cash that paid down acquisition debt while keeping the customer base intact.

By mid-1998, with Revco integration ahead of schedule, Ryan made another bold move: acquiring 200 Arbor Drugs locations in Michigan for $1.48 billion. Arbor gave CVS critical mass in the Midwest and added sophisticated pharmacy management systems that would become the backbone of CVS's technology infrastructure.

But Ryan's most visionary move came in 1999 with the acquisition of Soma.com, the first online pharmacy. Started by two Stanford MBAs, Soma.com had burned through $30 million in venture capital trying to sell prescriptions online. They had great technology but no customer base. CVS had 4,000 stores and millions of customers but no digital presence.

"Everyone thinks we're crazy to buy an internet company," Ryan told investors. "But this isn't about competing with our stores—it's about extending them. Order refills online, pick up at the store. Check drug interactions from your computer. Schedule pharmacy consultations via email." Renamed CVS.com, the platform would process 100 million prescriptions annually within five years.

The period's most important innovation, however, wasn't an acquisition but an internal creation. In 1999, CVS launched ProCare Pharmacy, designed for complex drug therapies like HIV treatments, cancer medications, and organ transplant drugs. These medications required specialized handling, extensive patient counseling, and complex insurance navigation. While they represented just 1% of prescriptions, they accounted for 15% of drug spending.

"We're not just dispensing medications anymore," explained Helena Foulkes, then running CVS's specialty division. "We're managing therapy. We have nurses calling patients, monitoring adherence, coordinating with doctors. It's healthcare, not retail." The specialty pharmacy would grow to generate $35 billion annually, becoming CVS's most profitable division.

By 2000, CVS had transformed from a regional player to a national powerhouse. Revenue exceeded $20 billion. The store count approached 4,100. The stock price had tripled since independence. But more importantly, Ryan had redefined what a pharmacy company could be. The ExtraCare program, launched nationally in 1998, had 30 million members and generated the most valuable customer data in healthcare retail.

Yet Ryan knew the transformation was incomplete. At a strategy session in late 2000, he presented a slide that would define CVS's next decade. It showed three interconnected circles: Pharmacy, Insurance, and Clinical Services. "Today we own pharmacy," he said. "To truly transform healthcare, we need all three."

The room was skeptical. Pharmacy was retail. Insurance was financial services. Clinical was healthcare. They were different industries with different regulations, different economics, different cultures. "That's exactly why it will work," Ryan responded. "No one else is crazy enough to try it."

As CVS entered the new millennium, it had proven it could execute massive acquisitions, integrate complex operations, and innovate in traditional retail. The Revco deal, mocked by analysts in 1997, was now studied in business schools as a textbook example of transformative M&A. But the real transformation—from pharmacy chain to healthcare company—was just beginning.

V. The Healthcare Services Revolution (2001–2006)

The memo that would reshape CVS landed on Tom Ryan's desk on a gray February morning in 2001. Written by Helena Foulkes, who'd been promoted to EVP of Strategy, it was titled simply: "The Future is Not in the Pharmacy." Ryan read it three times, then called an emergency executive committee meeting.

"Look at the data," Foulkes argued, spreading charts across the conference table. "Pharmacy margins have declined for five straight years. PBMs are squeezing reimbursements. Mail-order is taking our most profitable prescriptions. If we keep defining ourselves as a pharmacy company, we'll be managing decline, not growth." The room was tense. These executives had just spent five years building the nation's largest pharmacy chain. Now Foulkes was suggesting that wasn't enough.

Her proposal was radical: transform CVS from a place that filled prescriptions to a place that delivered healthcare. "Fifty million Americans have no primary care physician. Emergency rooms are overwhelmed with non-emergency cases. There's a massive gap between what people need and what the healthcare system provides. We have 4,000 locations. We have trusted pharmacists. We have foot traffic. Why aren't we the solution?"

The first step was data. In February 2001, CVS launched ExtraCare Plus, evolving the loyalty program from a discount tool to a health management platform. Members could track prescriptions, receive medication reminders, and get personalized health recommendations based on their purchase history. Within months, CVS had the most comprehensive consumer health database outside of insurance companies.

But data was just foundation. The real revolution came in 2002 when Ryan visited a strange new clinic in Minneapolis. QuickMedx, later renamed MinuteClinic, was the brainchild of Rick Krieger, who'd gotten strep throat while traveling and couldn't get a doctor's appointment for three days. His solution: staff mini-clinics with nurse practitioners who could diagnose and treat common ailments like strep, ear infections, and flu.

"This is it," Ryan told his team after visiting the cramped MinuteClinic in a Cub Foods grocery store. "This is how we become a healthcare company." The board was skeptical. Operating clinics meant medical liability, regulatory complexity, and confrontation with the medical establishment. The American Medical Association was already denouncing retail clinics as "dangerous" and "inappropriate."

Ryan spent 2003 and 2004 in quiet preparation. He hired Dr. Troyen Brennan, a Harvard Medical School professor, as Chief Medical Officer—an unprecedented role for a retail company. Brennan's mandate: design clinical protocols that would make CVS clinics safer than emergency rooms for routine care. Every condition treated would have a detailed protocol. Any case beyond the protocol would be referred to physicians. Electronic health records would track every interaction.

Meanwhile, CVS was quietly transforming its pharmacies. The traditional pharmacy counter—where customers stood in line like at a bank—was replaced with consultation rooms where pharmacists could privately discuss medications. Pharmacists were trained not just to dispense but to provide Medication Therapy Management (MTM), reviewing all of a patient's drugs for interactions and optimization.

The transformation accelerated in 2005 when CVS made a strategic investment in MinuteClinic, taking a minority stake that gave them exclusive rights to host clinics in their stores. But the real breakthrough came from an unexpected source: Hurricane Katrina.

In August 2005, Katrina devastated the Gulf Coast, destroying hospitals and clinics across Louisiana and Mississippi. CVS pharmacies, built to strip-mall standards rather than hospital codes, survived better than medical facilities. Within days, CVS pharmacists were providing emergency services, refilling lost prescriptions without documentation, and administering vaccines. The response earned praise from the CDC and demonstrated that retail locations could serve as healthcare infrastructure.

The Katrina response gave Ryan the credibility to make his biggest move yet. In July 2006, CVS announced it would acquire MinuteClinic outright for $170 million and roll out clinics to 500 stores within two years. The same month, they announced the acquisition of Albertsons' standalone drugstore operations—700 Sav-On and Osco stores—for $2.93 billion, giving CVS critical mass in Southern California and the Mountain West.

But the real coup was hiring away Steven Blumenthal from Aetna to run a new division: CVS Caremark Solutions. Blumenthal's mission: build a PBM within CVS that could compete with the big three—Express Scripts, Medco, and Caremark itself. "We fill one in seven prescriptions in America," Blumenthal argued. "We have the scale. We have the data. Why are we letting others control our economics?"

The medical establishment's response was fierce. The American Medical Association passed a resolution condemning retail clinics. State medical boards launched investigations. Competitor Walgreens publicly declared they would "never compromise patient safety by putting clinics in stores." But patients voted with their feet. MinuteClinic visits grew 300% in the first year. Customer satisfaction scores averaged 4.8 out of 5—higher than most hospitals.

The key was exceeding medical standards while delivering retail convenience. MinuteClinic nurse practitioners had more training than required by any state. Every clinic was connected to local health systems for referrals. Electronic health records meant better documentation than most doctor's offices. And the price—$59 for a strep test versus $150 at urgent care—made healthcare accessible to millions who'd been avoiding treatment due to cost.

By late 2006, the transformation was gaining momentum. CVS operated 60 MinuteClinics treating 15,000 patients weekly. The specialty pharmacy division had grown to $5 billion in revenue. The PBM startup had signed its first major client. But Ryan knew these were just pieces of a larger puzzle.

At the company's investor day in December 2006, Ryan unveiled his vision: "Healthcare is broken because it's fragmented. Patients, providers, pharmacies, and payers all operate in silos. CVS will be the integrator. We'll provide the care in our clinics, fill the prescriptions in our pharmacies, manage the benefits through our PBM, and coordinate it all through technology."

An analyst raised his hand: "Tom, you're describing something that doesn't exist—a vertically integrated healthcare company operating at retail scale. The regulatory challenges alone could sink you."

Ryan smiled. "Exactly. That's why we'll be the only ones who can do it."

The room didn't know it yet, but Ryan had been in secret negotiations for months about a deal that would make his vision reality: the acquisition of Caremark Rx, the nation's second-largest PBM. The healthcare services revolution had set the stage. The Caremark merger would be the main event.

VI. The Caremark Merger: Creating a New Model (2007)

The phone call that would create a $75 billion healthcare giant came at 10:47 PM on a Tuesday night in September 2006. Tom Ryan was in his home office in Rhode Island, reviewing MinuteClinic expansion plans, when Mac Crawford, CEO of Caremark Rx, called with an unexpected message: "Tom, Express Scripts just made a hostile bid for us. $27 billion. My board's going to have to consider it, but I'd rather talk to you first."

Ryan's pulse quickened. Caremark was the prize he'd been eyeing for two years—a PBM managing prescriptions for 35 million Americans, processing 500 million claims annually, and generating $37 billion in revenue. If Express Scripts acquired Caremark, they'd create a PBM monopoly that could dictate terms to every pharmacy in America, including CVS.

"Mac, can you give me 72 hours?" Ryan asked. Crawford agreed, but warned: "Express Scripts is offering $29.25 per share in cash and stock. Whatever you're thinking, it better be compelling."

Ryan immediately called Helena Foulkes and CFO Dave Rickard for an emergency meeting. They worked through the night, modeling scenarios. By dawn, they had their answer: CVS would offer an all-stock deal valuing Caremark at $31 per share—roughly $21 billion. But more importantly, they'd offer something Express Scripts couldn't: a completely new business model.

"Express Scripts plus Caremark is just a bigger PBM," Ryan explained to his board in an emergency session. "CVS plus Caremark is something that's never existed—a company that can manage the entire pharmaceutical supply chain from manufacturer to patient. We negotiate the prices, we manage the benefits, we fill the prescriptions, we provide the clinical services. It's vertical integration on a scale healthcare has never seen."

The board was divided. The deal would require issuing 1.67 billion new shares, diluting existing shareholders by 50%. The cultures were radically different—CVS was retail-focused and decentralized; Caremark was technology-driven and hierarchical. And the regulatory challenges would be unprecedented.

But Ryan had a secret weapon: data showing that CVS pharmacies filled prescriptions 23% cheaper than the industry average when adjusted for mix. "Imagine if we could guarantee those savings to every Caremark client," he argued. "We'd lock in their business for years while driving traffic to our stores. It's a virtuous circle that neither company can create alone."

On November 1, 2006, CVS and Caremark jointly announced the merger. The transaction valued Caremark at approximately $207 per share or approximately $69 billion, though initial reports focused on the equity value of $21 billion. The structure was complex: Caremark shareholders would receive 1.67 CVS shares for each Caremark share, plus a special one-time cash dividend of $2 per share upon closing.

Wall Street's reaction was swift and brutal. CVS stock dropped 14% in hours. "Ryan's lost his mind," declared one CNBC commentator. "He's taking a profitable retail company and tying it to a PBM facing margin pressure and regulatory scrutiny. This is value destruction on an epic scale."

But the real battle was just beginning. Within days, Express Scripts raised its bid to $29 billion and launched a vicious public campaign against the CVS deal. They took out full-page ads in the Wall Street Journal warning that the CVS-Caremark combination would "destroy competition" and "force consumers into CVS stores." They hired an army of lobbyists to push state attorneys general to block the deal.

The regulatory gauntlet was grueling. Ryan and Crawford spent December 2006 and January 2007 in continuous testimony before state regulators. California demanded guarantees that Caremark wouldn't steer patients to CVS stores. New York wanted assurances about data privacy. Texas questioned whether the combination would violate anti-kickback statutes.

The turning point came in February 2007 when the companies announced their integration plan, promising approximately $400 million in purchasing and operating synergies. But more importantly, they unveiled "Maintenance Choice"—a program allowing patients to fill 90-day prescriptions at CVS stores for the same price as mail order. It was a breakthrough that addressed consumer convenience while maintaining PBM economics.

On March 16, 2007, the drama reached its climax at Caremark's shareholder meeting in Nashville. Express Scripts had raised its bid one final time to $30 billion. Activist investors, including billionaire Carl Icahn, were publicly urging Caremark shareholders to reject the CVS deal. Ryan sat in the audience, watching Crawford make the case for their shared vision.

"Express Scripts offers you more money today," Crawford told shareholders. "But CVS offers you participation in something transformative. We're not just combining two companies. We're creating the future of pharmaceutical care in America."

The vote was closer than anyone expected: 52% in favor of the CVS merger, 48% for Express Scripts. But it was enough. On March 22, 2007, CVS Corporation and Caremark Rx officially combined, creating CVS Caremark Corporation with a combined market value of $75 billion.

The integration challenges were immediate and immense. Caremark's Nashville headquarters housed 2,000 employees who suddenly reported to Rhode Island. The computer systems were incompatible—CVS ran on IBM mainframes while Caremark used distributed Unix servers. Most challenging were the conflicting business models: CVS stores wanted maximum reimbursement for prescriptions while Caremark needed to minimize those same payments.

Ryan's solution was radical transparency. He created a "Chinese wall" between the PBM and retail operations, with separate P&Ls and independent management. But he also created integration teams to find synergies: combined purchasing of generic drugs, shared specialty pharmacy operations, and coordinated clinical programs.

The masterstroke was the creation of CVS Caremark's Pharmacy Advisor program. Using combined data from retail and PBM operations, they could identify patients not taking medications as prescribed and intervene with personalized outreach. The program improved adherence by 15% while reducing overall healthcare costs—a win for patients, payers, and CVS Caremark.

By the end of 2007, the doubters were beginning to convert. The new entity controlled the dispensing of about a billion prescriptions per year, or more than 25 percent of total U.S. volume. The stock, which had dropped to $32 after the merger announcement, closed the year at $41. Revenue for the combined company exceeded $75 billion.

At the company's first annual meeting as CVS Caremark, Ryan reflected on what they'd accomplished: "A year ago, we were two separate companies operating in adjacent spaces. Today, we're one company defining a new space. We're not a pharmacy chain with a PBM, or a PBM with pharmacies. We're an integrated pharmacy services company."

But Ryan knew the Caremark integration was just the beginning. In his office, he kept a whiteboard with three columns: "What We Are" (Pharmacy + PBM), "What We're Becoming" (Pharmacy + PBM + Clinics), and "What We Must Be" (Pharmacy + PBM + Clinics + Insurance).

The path to that final column would take another decade and the largest acquisition in healthcare history. But the Caremark merger had proven it was possible to combine seemingly incompatible businesses into something greater than the sum of their parts. The foundation for healthcare transformation was in place.

VII. Expanding the Healthcare Footprint (2008–2013)

Larry Merlo hadn't slept in 36 hours. It was September 15, 2008—the day Lehman Brothers collapsed—and the newly appointed CEO of CVS Caremark was facing his first major crisis. The financial markets were in freefall, credit was frozen, and CVS had $9 billion in debt from the Caremark acquisition. Worse, three major retail chains that owed CVS millions for pharmacy services had just declared bankruptcy.

"We could hunker down and wait for the storm to pass," Merlo told his executive team gathered in the Rhode Island headquarters. "Or we could recognize that chaos creates opportunity. While our competitors are retrenching, we're going to accelerate."

Merlo, who'd started as a pharmacist in Pittsburgh and risen through the ranks, had a different style than the visionary Ryan (who remained as Chairman). Where Ryan painted broad strategic strokes, Merlo obsessed over operational details. His first priority: make the Caremark integration actually work.

The numbers were sobering. Despite promises of $400 million in synergies, the combined company had achieved barely $200 million in the first year. The IT systems still couldn't talk to each other. Caremark clients were complaining about being steered to CVS stores. CVS pharmacists resented filling prescriptions at Caremark's lower reimbursement rates.

Merlo's solution was methodical transformation. He created "Project Symphony"—a three-year initiative to build unified technology infrastructure. Instead of forcing one system on the other, they built new platforms from scratch. The centerpiece was a real-time prescription management system that could track a prescription from doctor to PBM to pharmacy to patient, with full visibility at every step.

But technology was just enablement. The real opportunity was in clinical services. By 2009, MinuteClinic had grown to 500 locations, but they were losing money—$30 million annually. The board wanted to shut them down. Merlo saw different numbers: MinuteClinic patients filled 3.5 times more prescriptions at CVS than average customers and generated 40% higher basket sizes.

"The clinics aren't profit centers," Merlo explained. "They're customer acquisition engines. Every flu shot we give, every strep test we perform, creates a lifetime relationship with that patient." He doubled down, opening 100 new clinics in 2010 despite the recession.

The expansion strategy was surgical. Using Caremark data, CVS could identify exactly where patients were traveling farthest for basic care. They opened clinics in those gaps, often seeing breakeven within months as pent-up demand materialized. By 2011, MinuteClinic was treating a million patients annually and had become the largest retail clinic operator in America.

But Merlo's boldest move came in February 2014, at CVS's annual investor day. Standing before 200 analysts and investors, he made an announcement that sent shockwaves through corporate America: "Effective October 1, 2014, CVS will stop selling all tobacco products in all of our 7,600 stores."

The room erupted. Tobacco generated $2 billion in annual revenue for CVS, with $500 million in pure profit. One analyst practically shouted: "Larry, you're voluntarily giving up half a billion dollars in profit? Have you lost your mind?"

Merlo's response was measured but firm: "We're not a convenience store that happens to have a pharmacy. We're a healthcare company. Selling cigarettes while operating clinics and managing chronic diseases is fundamentally contradictory. This decision will cost us financially in the short term, but it establishes our credibility as a healthcare company for the long term."

The tobacco decision was actually the culmination of a multi-year strategy. In 2012, CVS had quietly begun testing "health hubs"—stores where the pharmacy expanded to include chronic disease management, nutrition counseling, and wellness programs. Customer response was phenomenal, but healthcare partners remained skeptical. How could they trust a company that profited from selling cigarettes?

Helena Foulkes, now President of CVS Pharmacy, had presented Merlo with data showing that removing tobacco would enable partnerships worth far more than cigarette sales. Major health systems would only work with CVS clinics if they stopped selling tobacco. Insurance companies would preferentially steer members to CVS if they were tobacco-free. The math was clear, even if Wall Street couldn't see it.

The tobacco removal was paired with a $50 million campaign called "Be The First"—positioning CVS as leading the creation of a tobacco-free generation. They offered free smoking cessation programs, partnered with schools on prevention, and turned former cigarette shelves into displays for nicotine replacement therapies.

While the public focused on tobacco, Merlo was quietly executing a series of strategic acquisitions that would reshape CVS's capabilities. In 2013, they acquired Coram, a $1.4 billion infusion services company that specialized in delivering complex medications like chemotherapy and antibiotics directly to patients' homes. It was an unglamorous business that required nurses, specialized logistics, and complex insurance billing—exactly the kind of capability CVS needed.

In 2014, the acquisition pace accelerated. CVS bought Navarro Discount Pharmacy, giving them critical mass in South Florida's Hispanic market. They acquired Onofre, Brazil's leading online pharmacy, testing international expansion. Most significantly, they struck a deal to acquire Target's 1,672 pharmacies and 79 clinics for $1.9 billion.

The Target deal was particularly clever. Target wanted out of pharmacy—it was complex, low-margin, and required capabilities they lacked. But they still wanted to offer pharmacy services to drive traffic. CVS's solution: operate pharmacies and clinics within Target stores under the "CVS Pharmacy at Target" brand. CVS got prime retail locations and access to Target's affluent customer base. Target got to offer pharmacy services without operational headaches.

But the crown jewel acquisition came in May 2015: Omnicare, the nation's largest provider of pharmacy services to long-term care facilities, for $12.7 billion. Omnicare served 1.4 million residents in nursing homes and assisted living facilities—a population that consumed 10 times more medications than average. It also gave CVS expertise in managing complex elderly patients who would soon flood Medicare Advantage plans.

By the end of 2015, CVS had transformed from a pharmacy chain with a PBM to something approaching Merlo's vision of an integrated healthcare company. They operated 7,800 pharmacies, 900 MinuteClinics, managed benefits for 65 million Americans, provided specialty drugs to 500,000 patients, and served 1.4 million seniors in long-term care.

Revenue had grown from $87 billion in 2008 to $139 billion in 2015. But more importantly, CVS had capabilities no competitor could match. They could track a patient from their doctor's office (through Caremark) to their pharmacy (CVS retail) to their home (Coram infusion) to their nursing home (Omnicare), with full visibility and coordination at every step.

At a healthcare conference in late 2015, Merlo was asked about the endgame. "We've built the pipes," he said. "We have the physical locations, the PBM relationships, the clinical capabilities, the specialty services. But we're missing one critical piece: the ability to take financial risk for patient outcomes. To truly transform healthcare, we need to be able to say: 'We'll keep this patient healthy, and if we fail, we'll bear the cost.'"

The audience knew what he meant. To take financial risk for patient health, CVS would need to become an insurance company. It seemed impossible—the capital requirements, regulatory approvals, and cultural changes would be immense. But then again, people had said the same thing about the Caremark merger, the tobacco decision, and every other transformation CVS had undertaken.

Unknown to the audience, Merlo had already begun preliminary discussions with a company that could make his vision reality: Aetna, one of the nation's largest health insurers. The conversations would take two years and face unprecedented regulatory scrutiny. But when complete, they would create something America had never seen: a company that could manage every aspect of a patient's healthcare journey. The path to that transformation would be the most challenging yet.

VIII. The Aetna Acquisition: Healthcare Reimagined (2017–2018)

The secret meeting took place in a nondescript Marriott conference room near Hartford-Bradley International Airport on October 26, 2017. Larry Merlo arrived alone, taking the elevator to the third floor where Mark Bertolini, Aetna's CEO, was waiting with just his CFO. No bankers, no lawyers, no advisors. Just four executives about to discuss the largest healthcare merger in American history.

"Mark, I'm going to make this simple," Merlo began. "Amazon is coming for both of us. They've hired 50 people from Express Scripts, they're getting pharmacy licenses state by state, and Bezos has made it clear healthcare is their next trillion-dollar market. Separately, we're both vulnerable. Together, we're unassailable."

Bertolini, a motorcycle-riding yoga practitioner who'd transformed himself from near-death in a skiing accident to running one of America's largest insurers, leaned back. "Larry, what you're proposing isn't just a merger. It's a fundamental reimagining of American healthcare. The regulatory scrutiny alone could destroy both companies."

The context was critical. Just months earlier, the Department of Justice had blocked Aetna's $37 billion merger with Humana and Anthem's $54 billion acquisition of Cigna. The government's message was clear: no more insurance consolidation. But Merlo had a different argument—this wasn't insurance buying insurance. This was a pharmacy company buying an insurer to create something entirely new.

"Think about it," Merlo continued, sketching on a whiteboard. "Aetna spends $60 billion annually on medical costs but has no control over delivery. CVS delivers care to millions but has no insight into total health spending. Combined, we can actually manage population health instead of just processing transactions."

The numbers were staggering. Aetna covered 22 million medical members and 14 million dental members. They processed $60 billion in medical claims annually. CVS filled 1.2 billion prescriptions, operated 1,100 MinuteClinics, and touched 5 million patients daily. Together, they would influence healthcare decisions for nearly 100 million Americans.

But the real innovation wasn't size—it was the model. Merlo and Bertolini envisioned transforming CVS's 9,700 stores into "HealthHUBs"—community health destinations offering everything from chronic disease management to mental health counseling. Aetna's data would identify at-risk patients; CVS's physical presence would intervene before they needed expensive hospital care.

On December 3, 2017, they went public with a joint announcement that shocked the healthcare world. The transaction valued Aetna at approximately $207 per share or approximately $69 billion. Including debt assumption, the total deal value reached $77 billion. The structure was complex: Aetna shareholders would receive $145.00 in cash and 0.8378 CVS Health shares for each Aetna share.

Wall Street's reaction was mixed but fascinating. CVS stock initially dropped 5%, but then something unexpected happened—it started rising. Investors were beginning to understand the strategic logic. "This isn't about synergies," explained one healthcare analyst. "It's about creating a new business model that makes the current healthcare system obsolete."

The regulatory battle began immediately. Within days, the American Medical Association denounced the deal, warning it would "limit competition and choice." The American Hospital Association predicted "dangerous consolidation." Progressive senators Elizabeth Warren and Bernie Sanders called for the deal to be blocked, arguing it would create a "healthcare monopoly."

Merlo and Bertolini spent the next eleven months in regulatory purgatory. They testified before Congress five times. They met with attorneys general from 28 states. They submitted 30,000 pages of documents to the Department of Justice. The scrutiny was unlike anything either company had experienced.

The breakthrough came from an unexpected source: CVS's own data. They could demonstrate that in markets where CVS operated MinuteClinics, emergency room visits for minor conditions dropped 7%, saving the healthcare system $450 million annually. When combined with Aetna's medical management, those savings could reach $2 billion.

But the DOJ had a specific concern: Aetna's Medicare Part D prescription drug business competed directly with CVS's PBM. Their solution was surgical—Aetna agreed to divest its standalone Medicare Part D prescription drug plans, covering approximately 2.2 million members, to WellCare Health Plans. It was a significant concession but preserved the strategic rationale for the merger.

State approvals were even more complex. California demanded that CVS maintain charity care programs. New York required privacy walls between insurance and pharmacy data. Florida insisted on guarantees about prescription access. Each state extracted concessions, turning the merger into 50 different deals.

The most dramatic moment came on October 10, 2018, when Judge Richard Leon of the U.S. District Court for D.C. held hearings on the merger. Leon had previously blocked the Aetna-Humana merger and was skeptical of healthcare consolidation. For six hours, he grilled Merlo and Bertolini about everything from data privacy to pharmacy steering.

"Your Honor," Merlo testified, "this isn't about reducing competition. It's about creating competition against a broken system. Today, healthcare is fragmented, expensive, and inaccessible for millions. We're proposing to fix that by aligning incentives across the entire care continuum."

Leon's decision, delivered on September 4, 2018, was cautiously supportive. He approved the merger with conditions, including regular reporting on consumer impacts and maintaining firewall protections. But his closing comments were telling: "This merger represents an experiment in healthcare delivery. The court cannot predict if it will succeed, but the potential benefits justify allowing it to proceed."

The final hurdle was Aetna's shareholders. On November 28, 2018, they voted overwhelmingly to approve the deal—97% in favor. The merger officially closed that same day, creating CVS Health with combined revenues approaching $200 billion.

But the real work was just beginning. Merlo now faced the challenge of integrating two radically different cultures. CVS was retail-focused, fast-moving, and decentralized. Aetna was process-driven, regulated, and hierarchical. The first joint leadership meeting was telling—CVS executives showed up in khakis and polos; Aetna executives wore suits and ties.

The integration strategy was deliberately slow. Rather than force rapid combination, Merlo created "innovation labs" where teams from both companies could experiment with new models. The first success came in Houston, where they piloted a program using Aetna data to identify pre-diabetic patients and refer them to CVS HealthHUBs for intervention. The result: 23% reduction in progression to diabetes within six months.

By early 2019, the company was already delivering on its promise of $750 million in synergies for 2020. But more importantly, they were proving the model worked. In markets where CVS and Aetna were fully integrated, medical costs grew 2% annually versus 6% elsewhere. Patient satisfaction scores increased 15%. Prescription adherence improved 20%.

At CVS Health's first investor day as a combined company in June 2019, Merlo presented a slide that captured the transformation. It showed a patient journey: visiting a CVS HealthHUB for a diabetes screening, getting medications at the CVS pharmacy, receiving coaching through Aetna's disease management, and avoiding hospitalization through coordinated care. "This isn't theoretical," Merlo said. "This is happening today for millions of Americans."

The Aetna acquisition had transformed CVS from a pharmacy company with health ambitions to a true healthcare company. They now had all the pieces: insurance to understand patient needs, pharmacies to deliver care, clinics to provide services, and data to coordinate everything. The question was no longer whether the model could work, but how fast it could scale.

But even as Merlo celebrated the successful integration, storm clouds were gathering. Amazon had announced its acquisition of PillPack. Walmart was expanding its health clinics. And most ominously, the COVID-19 pandemic was about to test every assumption about healthcare delivery. The integrated model CVS had spent two decades building would soon face its ultimate trial.

IX. Modern Era: Integration Challenges & Opportunities (2019–2024)

Karen Lynch was in her office at 4:47 AM on March 13, 2020, when her phone buzzed with an emergency text from the CDC: "Prepare for immediate nationwide COVID-19 testing deployment. CVS Health designated as primary retail testing partner. Stand by for secure call."

Lynch, who'd joined Aetna in 2012 and was now President of CVS Health after the merger, felt the weight of the moment. In the next 72 hours, CVS would need to transform 1,000 parking lots into testing centers, train 10,000 employees in PPE protocols, and create infrastructure to process millions of tests. The integrated healthcare company that Merlo and Bertolini had envisioned was about to be tested in ways no one had imagined.

"This is our Apollo moment," Lynch told her crisis team assembled via Zoom—itself a novel experience. "Everything we've built—the stores, the clinics, the insurance infrastructure, the data systems—it all comes together now. If we can't deliver healthcare in a pandemic, what's the point of integration?"

The response was extraordinary. Within two weeks, CVS had opened 1,000 drive-through testing sites. The Aetna data systems identified vulnerable populations for priority testing. The PBM negotiated directly with test manufacturers for supply. The MinuteClinic infrastructure was repurposed for specimen collection. By April, CVS was conducting 1.5 million tests monthly—more than most countries.

But testing was just the beginning. When vaccines became available in December 2020, CVS faced an even greater challenge. The government selected CVS and Walgreens to vaccinate 3 million residents and staff at 40,000 long-term care facilities—leveraging the Omnicare acquisition from 2015. Then came retail vaccination for the general public.

The vaccination rollout revealed both the power and problems of CVS's integrated model. The company could identify high-risk Aetna members and proactively schedule their vaccinations. They could track vaccination rates across populations and deploy mobile clinics to underserved areas. By May 2021, CVS had administered 17 million vaccine doses—more than any other pharmacy chain.

Yet the pandemic also exposed deep challenges. The insurance business was in chaos—elective procedures were cancelled, creating windfall profits, then came roaring back with pent-up demand. Medical costs swung wildly from 70% of premiums to 95% in six months. The Medicare Advantage business, which should have been a growth engine, was hemorrhaging money due to Aetna's poor Star ratings inherited from before the merger. The Medicare Advantage crisis was existential. CVS Health's operating income took up to a $1 billion hit in 2024 because of low Medicare Advantage star ratings. Just 21% of the people in the company's Medicare Advantage plans were in plans with 2023 star rating of 4.0 or greater compared with 87% in the 2022 star ratings. The star ratings determined CMS quality bonus payments—lose your stars, lose your profitability.

In October 2021, Lynch made another defining decision. With foot traffic declining and digital pharmacy growing, she announced CVS would close 900 stores over three years—approximately 10% of the chain. But this wasn't retreat; it was concentration. The closed stores were underperformers in oversaturated markets. The resources were redirected to transforming remaining stores into HealthHUBs.The HealthHUB concept was Lynch's signature initiative. These weren't just pharmacies with clinics but comprehensive health destinations occupying 20% of the store footprint, offering everything from sleep apnea assessments to mental health counseling. Early results were promising—HealthHUB locations saw 10% higher revenue and significantly better customer retention. But scaling from 50 test stores to 1,500 planned locations required billions in capital just as the insurance business was hemorrhaging cash.

Lynch's response to the Medicare Advantage crisis was strategic surgery. Rather than chase unprofitable growth, CVS announced it would shrink Medicare Advantage membership by "high single-digit percentage" in 2025, essentially firing unprofitable members. It was a painful admission that growth at any cost didn't work in insurance.

Meanwhile, Lynch was making bold bets on the future. In March 2023, CVS completed its acquisition of Signify Health for $8 billion. Signify Health is a leading technology and services company, focused on provider enablement and bringing clinicians into the home to identify chronic conditions, close gaps in care, and address social determinants of health. Signify has a network of more than 10,000 clinicians in all 50 states, who spend an average of 2.5 times longer with a member during home visits than an average visit with a primary care provider.

Two months later, in May 2023, CVS closed on an even bigger prize: Oak Street Health for $10.6 billion. CVS Health announced it has completed its acquisition of Oak Street Health. The acquisition will broaden CVS Health's value-based primary care platform and significantly benefit patients' long-term health by improving outcomes and reducing costs – particularly for those in underserved communities. CVS Health announced it entered into a definitive agreement to acquire Oak Street Health in an all-cash transaction for $39 per share, representing an enterprise value of approximately $10.6 billion.

These weren't random acquisitions but pieces of a coherent strategy. Signify brought capabilities to assess patients in their homes, identifying health risks before they became expensive emergencies. Oak Street operated 169 value-based primary care centers focused on Medicare patients, with a proven model for keeping seniors healthy and out of hospitals. Together with CVS's existing assets, Lynch was assembling an end-to-end care delivery system.

The integration challenges were immense. Oak Street had a distinctive culture built around hour-long doctor visits and deep community engagement. Signify's clinicians operated independently, visiting patients' homes with minimal corporate oversight. Both models clashed with CVS's standardized, efficiency-driven retail culture.

Lynch's solution was to maintain operational independence while seeking strategic synergies. Oak Street would continue operating under its brand with its founder Mike Pykosz as CEO (though he would depart in November 2024). Signify would remain a separate division. But behind the scenes, CVS was connecting the dots—Aetna data identified high-risk patients, Signify assessed them at home, Oak Street provided ongoing primary care, CVS pharmacies filled prescriptions, and MinuteClinics handled acute needs.

The early results were promising. Aetna members served by Signify almost doubled year over year in the third quarter, while Aetna members enrolled at Oak Street have quadrupled since the acquisition closed. Revenue at Oak Street and Signify increased 36% and 37% year over year in the quarter, respectively.

But storm clouds were gathering by mid-2024. The Medicare Advantage business continued to struggle with medical costs rising faster than premiums. The retail pharmacy faced ongoing reimbursement pressure. Most concerning, the PBM model was under unprecedented scrutiny from both parties in Congress, with legislation threatening to fundamentally restructure how PBMs operate.

In October 2024, Lynch was abruptly replaced as CEO by David Joyner, a longtime CVS executive who'd been running the retail business. The board's message was clear: after years of transformation and acquisition, CVS needed operational excellence, not more vision. Joyner immediately announced $2 billion in cost cuts and a "back to basics" approach focused on improving execution rather than expansion. In October 2024, the board made a decisive move. CVS Health announced that David Joyner was appointed President and Chief Executive Officer, effective October 17, replacing Karen Lynch, who stepped down from her position in agreement with the company's Board of Directors. David brings more than 39 years of health care and pharmacy benefit management experience to the company, where he has focused on driving systemic change across the industry. Most recently, David led the pharmacy services segment at CVS Health.

The choice of Joyner signaled a return to operational fundamentals. Unlike Lynch, who came from insurance, or Merlo, who rose through retail, Joyner was a PBM veteran who understood the complex mechanics of drug pricing and pharmacy networks. His mandate was clear: fix the basics before pursuing grand visions.

By early 2025, CVS Health stood at a crossroads. The company had successfully assembled all the pieces of an integrated healthcare company—insurance, pharmacy, PBM, primary care, home health, and retail clinics. The COVID pandemic had proven the model could work at scale. 88 percent of its Medicare Advantage (MA) members are in 2025 Medicare Advantage Prescription Drug (MAPD) plans that are rated 4 stars or higher (out of 5 stars) by the Centers for Medicare & Medicaid Services. Additionally, more than two out of three (68 percent) Aetna Medicare Advantage members are in a 4.5-star plan for 2025.

Yet fundamental challenges remained. The retail pharmacy business faced continued margin pressure from PBMs—including CVS's own Caremark. The insurance business struggled with medical cost inflation. The PBM model faced existential regulatory threats. And the massive debt from acquisitions limited financial flexibility.

CVS Health on Wednesday reported fourth-quarter revenue and profit that topped estimates, even as its troubled insurance business continued to see higher medical costs. The company also issued a full-year 2025 adjusted earnings outlook of $5.75 to $6 per share, which was in line with Wall Street's expectations.

The integration of healthcare delivery, insurance, and pharmacy had created something unprecedented in American healthcare. Whether this integrated model represented the future of healthcare delivery or an unwieldy conglomerate attempting to reconcile irreconcilable conflicts remained the central question. The next chapter would determine whether CVS Health's grand experiment in vertical integration could deliver on its promise of better, cheaper, more accessible healthcare—or whether the inherent tensions would tear the company apart.

X. Playbook: Business & Investing Lessons

The CVS Health story reads like a masterclass in strategic transformation through M&A, but it's the nuances—the failures alongside the successes—that offer the richest lessons. After analyzing sixty years of decisions, deals, and pivots, certain patterns emerge that transcend healthcare and speak to fundamental truths about building and investing in complex businesses.

The Power (and Peril) of Vertical Integration

CVS's journey from pharmacy to integrated healthcare giant demonstrates both why vertical integration can create extraordinary value and why it's so difficult to execute. The theoretical benefits are compelling: controlling the entire value chain eliminates middleman margins, creates information advantages, and enables optimization across the system. When CVS pharmacists can see Aetna claims data to identify medication gaps, or when MinuteClinic visits drive pharmacy traffic, the synergies are real and measurable.

But vertical integration in healthcare introduces unique complexities. Unlike manufacturing, where you're integrating similar processes with aligned incentives, healthcare integration requires reconciling fundamentally different business models. The PBM wants to minimize drug costs; the pharmacy wants to maximize reimbursements. The insurance arm profits from healthy members who don't use services; the clinic and pharmacy profit from utilization. These aren't just operational challenges—they're structural conflicts that no amount of management skill can fully resolve.

The lesson for investors: vertical integration works best when the integrated components have naturally aligned incentives. When they don't, the company must create artificial mechanisms (like internal transfer pricing or Chinese walls) that reduce the very efficiencies integration was meant to create. CVS has managed these tensions better than most, but the ongoing struggles in Medicare Advantage show that even successful integration has limits.

M&A as Transformation Strategy: The Build vs. Buy Calculus

CVS's acquisition history reveals a sophisticated understanding of when to buy versus build. The pattern is instructive: CVS consistently bought capabilities it couldn't develop internally (PBM technology, insurance expertise, clinical protocols) but built what they could control (store footprint, loyalty programs, distribution).

The Caremark acquisition exemplifies strategic M&A at its best. CVS couldn't build a PBM from scratch—the contracts, systems, and scale would take decades to develop. But by acquiring Caremark, they instantly gained negotiating leverage with drug manufacturers and created a defensible moat around their pharmacy business. The $21 billion price tag seemed steep in 2007 but looks prescient given that independent pharmacies without PBM protection have been decimated.

Contrast this with MinuteClinic, where CVS initially tried to build internally, failed, then acquired the capability for just $170 million. The small acquisition price allowed CVS to experiment and learn before scaling. This "try, fail, buy, scale" approach reduced risk while accelerating capability development.

The Aetna acquisition pushed this strategy to its limit. At $77 billion, it was a bet-the-company move that could only be justified if the integration created something fundamentally new. The jury is still out, but early evidence suggests the benefits are real but harder to capture than anticipated.

Managing Regulatory Complexity: The Hidden Operational Burden

Healthcare might be the most regulated industry in America, with overlapping federal, state, and local requirements that vary by business line. CVS operates under pharmacy board regulations in 50 states, insurance regulations in every market they serve, Medicare and Medicaid rules that change annually, and FDA oversight of their specialty pharmacy operations.

This regulatory complexity creates both moats and millstones. The moat is obvious—new entrants face enormous barriers to replicating CVS's licenses and compliance infrastructure. Amazon's struggles to scale their pharmacy business despite unlimited capital demonstrates how powerful these barriers are.

But regulation also constrains strategic flexibility. When CVS wanted to have Aetna preferentially steer members to CVS pharmacies—a natural synergy of integration—regulatory barriers limited how aggressively they could pursue this strategy. The company has spent billions on compliance infrastructure that adds no direct customer value but is essential for operation.

The investing lesson: in highly regulated industries, competitive advantage often comes not from innovation but from navigating regulatory complexity better than competitors. CVS's willingness to embrace rather than fight regulation—like voluntarily stopping tobacco sales to gain credibility with health regulators—has been a key success factor.

The Data Advantage: From Transactions to Insights

CVS's ExtraCare program, launched in 2001, seemed like a simple loyalty program. But it became the foundation for something much more powerful: the most comprehensive consumer health database outside of government. With 74 million active members generating billions of transactions annually, CVS knows more about American health behavior than perhaps any other company.

This data advantage compounds over time. When CVS knows you fill diabetes medication monthly, buy blood glucose test strips quarterly, and suddenly start purchasing candy frequently, they can intervene with targeted health messaging. When aggregated across populations, this data reveals disease trends, medication adherence patterns, and health disparities that inform everything from store placement to formulary design.

The integration with Aetna multiplied this advantage exponentially. Now CVS can see not just what medications you take but your entire medical history—doctor visits, lab results, hospitalizations. This comprehensive view enables predictive interventions that no single-point player could achieve.

Yet CVS has been surprisingly conservative in monetizing this data advantage, particularly compared to tech companies. Privacy concerns, regulatory constraints, and cultural conservatism have limited their willingness to fully exploit their information advantage. This restraint may be wise—healthcare data breaches can be company-ending events—but it also represents untapped potential.

Capital Allocation in Capital-Intensive Businesses

CVS operates in one of the most capital-intensive sectors outside of utilities and telecommunications. Stores require constant renovation, technology systems need continuous updates, acquisitions demand massive capital, and insurance requires substantial reserves. The company routinely spends $10+ billion annually on capital expenditures and acquisitions.

Their capital allocation strategy reveals important principles. First, they've consistently prioritized strategic capability over financial returns. The MinuteClinic division lost money for years but was funded because it drove pharmacy traffic and built healthcare credibility. Second, they've been willing to sacrifice short-term profits for long-term positioning—the tobacco decision cost $2 billion in annual revenue but enabled partnerships worth far more.

Most importantly, CVS has shown that in capital-intensive businesses, scale economics eventually dominate. Once you've spent the billions to build integrated systems, acquire licenses, and create network density, the marginal cost of serving additional customers approaches zero while competitors face prohibitive entry costs.

Operating Multiple Business Models: The Organizational Challenge

Perhaps CVS's greatest challenge—and most important lesson—involves operating fundamentally different business models within one company. Retail pharmacy is about foot traffic and inventory turns. Insurance is about risk selection and medical management. PBM is about negotiation and network management. Primary care is about patient relationships and clinical quality.

Each business has different metrics, cycles, and cultures. Pharmacy managers think in daily sales; insurance executives think in annual benefit cycles; clinicians think in patient episodes. CVS has tried various organizational structures—from complete integration to arms-length subsidiaries—without finding a perfect solution.

The lesson is that conglomerate complexity has real costs that financial synergies must overcome. CVS has succeeded where others failed (like Amazon's Haven healthcare venture) because they've accepted these complexity costs rather than trying to force artificial simplification.

Network Effects in Healthcare

Traditional network effects—where each additional user makes the service more valuable for all users—are limited in healthcare due to privacy concerns and regulatory barriers. But CVS has created what might be called "ecosystem network effects" where each additional service makes all other services more valuable.

When a patient uses CVS pharmacy, they're more likely to use MinuteClinic. MinuteClinic users are more likely to enroll in Aetna. Aetna members are more likely to use CVS pharmacies. Each touchpoint reinforces the others, creating switching costs and customer lock-in that pure-play competitors can't match.

These ecosystem effects are particularly powerful in Medicare Advantage, where seniors often struggle to navigate complex healthcare systems. CVS's ability to provide integrated services—primary care at Oak Street, medications at CVS, insurance through Aetna, home care via Signify—creates convenience value that competitors offering point solutions can't match.

The Local Presence Paradox

Despite operating at massive scale, healthcare remains stubbornly local. Patients want their pharmacy within 5 miles, their doctor within 15 minutes, their insurance to cover their specific hospital. This local requirement creates a paradox: you need national scale for efficiency but local presence for effectiveness.

CVS has solved this paradox through a hub-and-spoke model. The hubs—distribution centers, insurance operations, PBM systems—operate at national scale with maximum efficiency. The spokes—stores, clinics, sales teams—maintain local presence and relationships. This structure allows CVS to achieve scale economics while maintaining local relevance.

The investment implication: in healthcare, pure digital disruption is limited. Despite billions invested in digital health, the winning models still require physical presence. CVS's 9,000+ locations aren't legacy baggage—they're strategic assets that digital-only competitors can't replicate.

Final Lessons: The Complexity Premium

The overarching lesson from CVS's journey is that in certain industries, complexity itself can be a competitive advantage. While business schools teach simplification and focus, CVS has succeeded by embracing complexity that competitors can't or won't match.

This complexity premium manifests in multiple ways. Regulatory complexity deters new entrants. Operational complexity makes the model difficult to copy. Financial complexity obscures true profitability from competitors. Strategic complexity creates options value—multiple ways to win as the market evolves.

For investors, this means traditional valuation metrics may undervalue complex integrated models like CVS. The market typically applies a "conglomerate discount" to complex businesses. But when complexity creates genuine synergies and competitive advantages, this discount may represent opportunity.

The CVS playbook ultimately teaches that in healthcare—and perhaps other complex, regulated industries—winning requires patient capital, operational excellence, regulatory sophistication, and the willingness to manage contradictions that simpler business models avoid. It's not a strategy for everyone, but for those who can execute it, the rewards can be extraordinary.

XI. Analysis & Bear vs. Bull Case

The investment case for CVS Health in 2025 presents one of the most complex analytical challenges in American business. This isn't a simple growth story or value play—it's a multifaceted bet on the transformation of American healthcare, the sustainability of integrated business models, and the company's ability to execute through unprecedented industry change.

Bull Case: The Integrated Model's Time Has Come

The optimistic case for CVS starts with a simple observation: American healthcare is unsustainably broken, and CVS is the only company with all the pieces to fix it. Healthcare spending approaches 20% of GDP, medical bankruptcies devastate families, and yet health outcomes lag other developed nations. This crisis creates opportunity for anyone who can deliver better care at lower cost.

CVS's integrated model uniquely positions them to capture value from healthcare transformation. Consider the diabetes patient journey: Aetna identifies pre-diabetic members through claims data, Signify Health visits them at home for assessment, Oak Street Health provides ongoing primary care, MinuteClinic handles acute needs, CVS pharmacy manages medications, and Caremark negotiates drug prices. No competitor can match this end-to-end capability.

The numbers support the integration thesis. In markets where CVS has fully deployed its integrated model, medical costs grow 2-3% annually versus 6-7% elsewhere. Patient satisfaction scores exceed 90%. Medication adherence improves 20%. These aren't marginal improvements—they're step-function changes that create sustainable competitive advantages.

Scale economics increasingly favor CVS. With $373 billion in revenue, they have the resources to invest in technology, weather regulatory changes, and acquire new capabilities. Smaller competitors simply can't match CVS's investment in AI-driven medication management, predictive analytics for health interventions, or value-based care infrastructure.

The demographic tailwind is undeniable. Ten thousand Americans turn 65 daily, and this will continue through 2030. These new Medicare beneficiaries need exactly what CVS offers: convenient pharmacy services, accessible primary care, and integrated insurance coverage. CVS's focus on senior care through Oak Street and Medicare Advantage positions them perfectly for this demographic wave.

Regulatory trends, despite short-term challenges, favor integrated models. The shift from fee-for-service to value-based payment rewards companies that can manage total health costs, not just process transactions. CVS's ability to take risk on patient populations and manage across the care continuum aligns with where policy is heading.