Commvault: The Data Protection Pioneer That Survived Its Own Disruption

I. Introduction & Episode Roadmap

There is a graveyard of enterprise software companies that once seemed invincible. Veritas, Legato, Symantec's storage division, the old EMC federation — names that dominated data centers for decades and then faded, were swallowed, or were broken apart. And yet, sitting quietly in Tinton Falls, New Jersey, there is a company that was born inside Bell Labs in 1988, went public in 2006, nearly lost its way in the mid-2010s, endured an activist investor revolt, replaced its founding CEO, bet the company on a cloud transformation — and emerged on the other side with over a billion dollars in annual recurring revenue.

That company is Commvault Systems, ticker CVLT on the NASDAQ.

The central question of this episode is deceptively simple: how did a Bell Labs spinout navigate tape backups, deduplication wars, virtualization, ransomware, and the cloud — and live to tell the tale? In an industry where most incumbents either consolidate or die, Commvault stands as one of the few independent data protection companies still operating at scale, still growing, and still relevant.

The themes here are classic Acquired territory. Enterprise software moats — specifically, how switching costs and process power can sustain a business through multiple technology cycles. The challenge of incumbency — the innovator's dilemma playing out in real-time, with a company forced to cannibalize its own high-margin perpetual license business to survive. And strategic pivots — how leadership changes, product simplification, and a willingness to embrace cloud-native architectures can turn a declining legacy vendor into a credible growth story.

What makes Commvault particularly interesting for investors and operators alike is that it is neither the obvious winner nor the obvious loser in the data protection market. It is the survivor. Veeam is bigger. Rubrik is flashier. The Cohesity-Veritas combination is the newest heavyweight. But Commvault has something none of them have: nearly four decades of continuous operation, a transformation that is measurably working, and a financial profile that generates real free cash flow. Whether that is enough — whether surviving is the same as winning — is the question we are going to spend the next couple of hours unpacking.

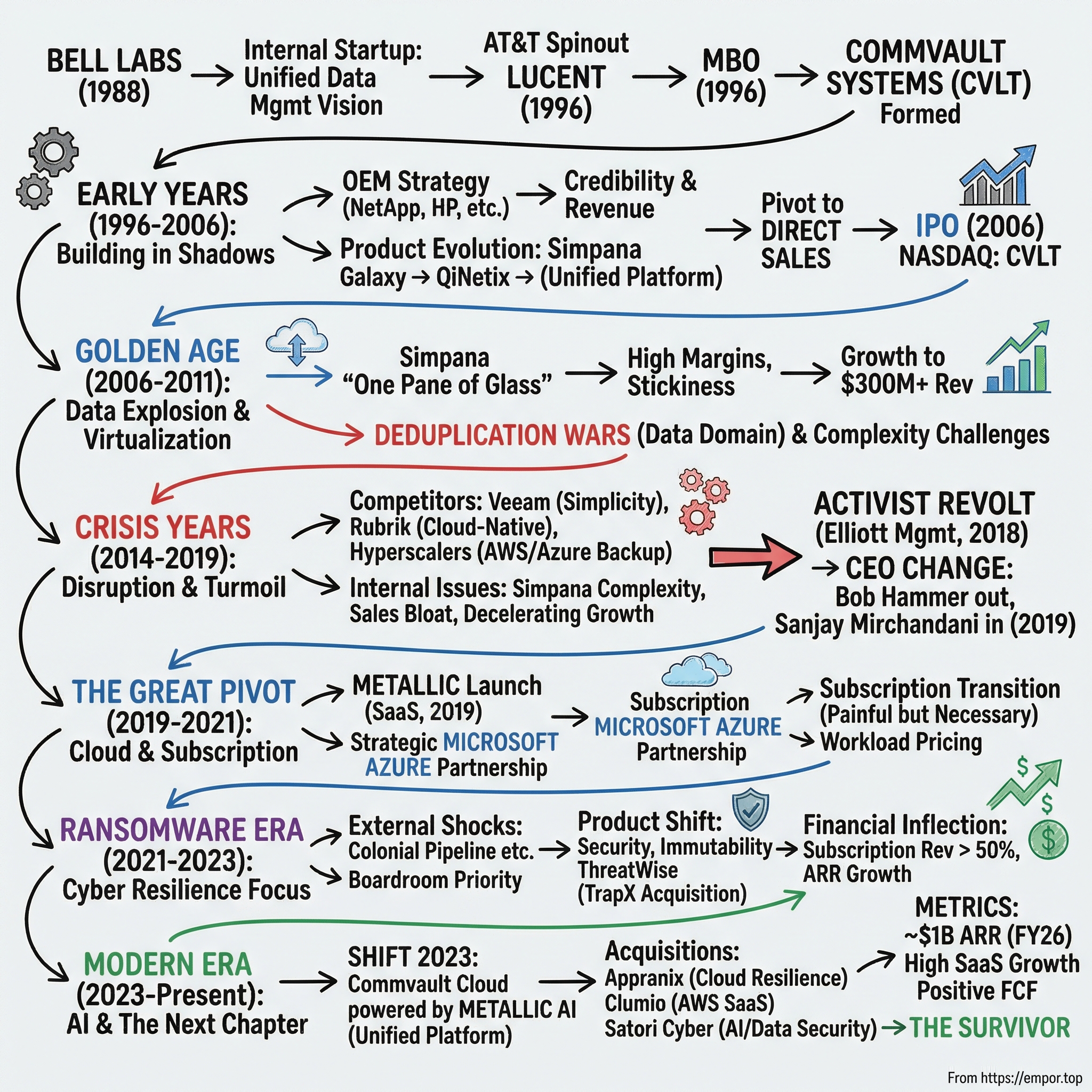

II. The Bell Labs Heritage & Early Genesis (1988–1996)

In the late 1980s, Bell Labs was still the cathedral of American computer science. The transistor had been invented there. Unix had been invented there. The C programming language had been invented there. It was a place where brilliant engineers could spend years working on problems that might not have commercial application for a decade, funded by the reliable cash flows of AT&T's telephone monopoly. But by 1988, that world was starting to crack. The 1984 breakup of AT&T into the Baby Bells had already carved away the local telephone operations, and the remaining AT&T was increasingly focused on finding commercial applications for its research.

Inside this pressure cooker, a small development group formed around a problem that was unglamorous but increasingly urgent: enterprise data was growing exponentially, and the tools for backing it up and recovering it were fundamentally broken. Backup in the late 1980s meant tape. Literal, physical tape. Companies would run nightly backup jobs that consumed hours of processing time, fill cartridges that had to be physically transported to off-site storage facilities, and then pray that when disaster struck, the tapes would actually be readable. Recovery was measured in days, sometimes weeks. The gap between the volume of data enterprises were producing and their ability to protect it was widening fast.

This Bell Labs development group — originally part of AT&T Network Systems — saw an opportunity to build something fundamentally different. Rather than creating yet another point solution that handled one piece of the backup puzzle, they envisioned a unified data management platform that could handle backup, recovery, archiving, and replication from a single architecture. It was a bold bet on convergence at a time when the market was fragmented into dozens of narrow tools, each handling a different operating system, storage medium, or application.

The founding insight was architectural: build a single platform with a common metadata layer that could manage data across any environment. Think of it as the difference between having a separate thermostat, light switch, and security system in your house versus having one integrated smart home controller. Most competitors were building thermostats. This group wanted to build the controller.

The metadata engine — a kind of universal index that tracked where every piece of data lived, when it was last backed up, who owned it, and how it related to other data — became Commvault's foundational intellectual property. It meant the system could intelligently manage data across heterogeneous environments without requiring separate management tools for each one. This was a non-obvious architectural choice at the time, because building a universal data management layer is orders of magnitude harder than building a point solution for a single operating system or application. But it meant that as enterprises added new systems — new databases, new operating systems, new storage platforms — Commvault's single platform could extend to cover them, rather than requiring the customer to buy yet another separate tool.

The AT&T corporate restructuring of the 1990s provided the escape hatch. When AT&T spun off its equipment and technology operations as Lucent Technologies in 1996, the data management group went with it. But Lucent was itself going through massive reorganization, and the small data management unit was not a strategic priority. In May 1996, the team executed a management buyout, purchasing their independence from Lucent and incorporating as CommVault Systems. Scotty R. Neal, who had led the group, became the first CEO.

They were a tiny company with a big vision, a handful of engineers, and a product called Vault98 that handled backup and recovery. What they lacked was commercial experience, sales infrastructure, and capital. They had the Bell Labs pedigree — which mattered enormously for credibility with enterprise buyers who needed to trust their vendor with mission-critical data — but they needed leadership that could turn research-grade technology into a market-ready product.

That leader arrived in March 1998, when N. Robert "Bob" Hammer joined as Chairman, President, and CEO, bringing along Al Bunte as Vice President and COO. Hammer was not a technologist by training — he was an operator and dealmaker who understood how to build enterprise software businesses. Bunte brought operational discipline and a relentless focus on execution. Together, they would shape Commvault for the next two decades and take it from a scrappy Bell Labs spinout to a publicly traded enterprise software company. They also established the company's headquarters in Oceanport, New Jersey — later relocating to Tinton Falls, near the old Fort Monmouth site — keeping the company firmly rooted in the New Jersey corridor that had given birth to Bell Labs and its technological descendants.

III. The Early Years: Building in the Shadows (1996–2006)

Picture the enterprise data protection market in the late 1990s and early 2000s. It was dominated by two giants: Veritas, which had the highest pricing and the most aggressive sales force, and Legato, which had the largest installed base and the longest-selling enterprise backup product. These were the Coca-Cola and Pepsi of the backup world, and they controlled the conversation with the Fortune 500 data center managers who made purchasing decisions. Behind them were a half-dozen other players, all fighting for scraps. The enterprise buyer at a major bank or insurance company was not going to stake their career on some unknown spinout from Bell Labs — not when Veritas had a thousand references and a global support organization.

Into this landscape walked Commvault with its Galaxy product — launched in 2000 as the successor to Vault98 — and an audacious claim: we have a single, unified platform that does everything those other guys need five separate products to do.

The problem was that nobody outside Bell Labs alumni circles had heard of them, they had no direct sales force worth mentioning, and enterprise buyers in the backup space were deeply conservative. When your job is protecting the company's data — the one function where failure means the CEO is calling you at 3 AM — you do not take chances on unproven vendors.

Hammer's solution was elegant: if you cannot beat the giants head-on, sell through them. Commvault pursued an OEM strategy, partnering with established hardware and storage vendors who would resell Commvault's software under their own branding. Hitachi Data Systems became an early reseller. HP and Dell followed, along with over a hundred value-added resellers.

The most significant OEM deal came later, when Commvault entered a global agreement with NetApp. Under this arrangement, NetApp integrated elements of Commvault's software with its own snapshot and replication technology, selling the combined product as NetApp SnapProtect. For Commvault, this was brilliant. NetApp's sales force — hundreds of experienced enterprise salespeople with established relationships in the Fortune 500 — was selling Commvault's technology to enterprises that might never have considered Commvault directly, and every deployment deepened the technology's enterprise credibility.

The OEM approach served three purposes simultaneously. First, it funded R&D — Commvault could invest in product development without the enormous expense of building a global direct sales organization. Second, it built credibility — when an enterprise saw Commvault technology inside a NetApp or HP product, it validated the technology in a way that no amount of marketing could. Third, it generated real revenue.

By 2002, the Galaxy product achieved fifty percent growth in new license revenue, proving that the technology could compete even when sold through partners. This was no small feat in a market where Veritas and Legato had entrenched relationships with the world's largest companies.

Throughout this period, the product was evolving rapidly. What started as backup and recovery expanded into archiving, replication, and search. The Galaxy product gave way to the QiNetix branding, and then, with versions 8 and 9, to the Simpana platform — the product that would become Commvault's calling card for nearly a decade. Simpana was the full realization of the Bell Labs vision: a single, unified platform for data protection that could handle backup, recovery, archiving, deduplication, replication, and search across virtually any enterprise environment. Where competitors required customers to buy and manage separate products for each function — one for VMware backup, another for Oracle, a third for email archiving — Simpana offered it all from a single console, managed by a single team, with a single licensing agreement.

But Hammer and Bunte understood that the OEM strategy had a ceiling. Selling through partners meant giving up margin, losing direct customer relationships, and being at the mercy of partners' sales priorities. A NetApp salesperson had a hundred products to sell; Commvault's backup module was not always at the top of the pitch.

Sometime in the mid-2000s, Commvault made the fateful decision to build its own direct sales force and go to market independently. It was expensive and risky. It meant hiring enterprise salespeople who could navigate six-to-twelve month sales cycles with Fortune 500 IT departments. It meant building a services and support organization from scratch. It meant competing head-to-head with the very partners who had helped build the business.

But it was necessary for the company to control its own destiny — and to capture the full economics of its platform. Under the OEM model, Commvault captured only a fraction of the end-customer price; going direct meant keeping the full margin. This decision, more than any other, set the stage for the IPO. The cultural DNA that crystallized during this period — engineering-led, technically complex, enterprise-focused, deeply proud of the platform architecture — would define Commvault for better and for worse in the decades ahead.

IV. The IPO & The Golden Age of Data Protection (2006–2011)

On September 22, 2006, Commvault Systems began trading on the NASDAQ under the ticker CVLT. The IPO priced at $14.50 per share, with just over eleven million shares offered — roughly six million from the company and five million from selling stockholders. Credit Suisse and Goldman Sachs served as joint book-running managers. It was not a splashy debut by Silicon Valley standards, but for a backup software company from New Jersey, it was a milestone. The company had revenue of roughly $110 million in its most recent fiscal year and was growing at better than thirty percent annually.

The timing was remarkably fortunate. Commvault went public just as several powerful tailwinds converged on the data protection industry. Enterprise data volumes were exploding — driven by email, digital documents, databases, and the early stirrings of what would eventually be called "big data." The regulatory environment was becoming far more demanding, with Sarbanes-Oxley compliance requirements forcing public companies to retain and protect financial records, and HIPAA imposing similar mandates on healthcare data. Virtualization was emerging as a transformative technology, with VMware's ESX platform beginning to reshape how enterprises thought about servers and storage. Every one of these trends meant more data to protect, more complex environments to manage, and more money flowing into data protection budgets.

The Simpana platform was perfectly positioned to capture this demand. While competitors like EMC (which had acquired Legato), Symantec (which had merged with Veritas in a troubled $13.5 billion deal), and IBM required customers to stitch together multiple products for a complete data protection solution, Commvault offered what it called "one pane of glass" — a single management interface for backup, recovery, archiving, deduplication, and compliance. For the CIO who was tired of managing five different backup products from three different vendors, each with its own licensing model, management console, and support contract, Simpana was a revelation. One vendor. One console. One support call.

The economics of this business model were attractive. Enterprise software sold on perpetual licenses generated high gross margins — typically above seventy percent — and came with annual maintenance contracts that provided predictable, recurring revenue streams. Think of it like selling a house and then collecting rent: the upfront license payment was the sale, and the annual maintenance fee — typically around twenty percent of the license value — was the rent, paid every year in exchange for software updates and technical support.

Once a customer deployed Simpana across their environment, the switching costs were enormous. You cannot rip out a backup system the way you might swap a SaaS application. Data protection software is deeply embedded in an organization's infrastructure, connected to every server, every database, every application. The data itself — the backup copies, the archives, the recovery points — is stored in formats specific to the backup vendor. Moving to a competitor means not just learning a new tool but migrating years of protected data, rewriting recovery procedures, retraining staff, and accepting the risk that something will break during the transition.

The result was customer retention rates that any SaaS company would envy, and a compounding effect where the installed base grew the maintenance revenue stream year after year. Each new customer added to a growing annuity of predictable revenue that required minimal incremental cost to service. This is the dream economics of enterprise infrastructure software, and it explains why the market has attracted so much capital over the decades.

Revenue grew briskly through this period. From roughly $110 million at the time of the IPO, Commvault nearly tripled to over $300 million by fiscal year 2011. The company was gaining market share against larger but less focused competitors, and the Simpana platform's technical advantages were winning head-to-head evaluations with increasing frequency.

Gartner placed Commvault in the Leaders quadrant of its Magic Quadrant for Enterprise Backup Software and Integrated Appliances — a critical endorsement in a market where enterprise buyers relied heavily on analyst reports to guide purchasing decisions. Commvault was the scrappy independent that enterprise IT departments were starting to trust — the challenger brand that proved you did not need to buy from the biggest vendor to get the best technology. The stock reflected this success, rising steadily from its $14.50 IPO price throughout the late 2000s as investors recognized the power of the high-margin, high-retention business model.

But embedded in this golden age were the seeds of future challenges. Simpana was powerful, but it was also complex. Deploying it required significant professional services, extensive training, and ongoing tuning — a typical enterprise deployment could take months to fully implement.

Pricing was based on a per-frontend-terabyte model — essentially, customers paid based on the amount of data they were protecting. This made perfect sense in a world of on-premises data centers where data volumes grew predictably at ten to twenty percent per year, but it would become deeply problematic in the cloud era, where data could explode in volume overnight and pricing expectations were fundamentally different.

The very complexity that made Simpana powerful also made it intimidating to evaluate and exhausting to buy, and that opened a door for simpler, more focused competitors who were already starting to build their products. In the hallways of enterprise IT conferences, the whispered complaint about Commvault was always the same: "Great technology. Nightmare to buy and deploy."

V. The Deduplication Wars & Market Consolidation (2011–2014)

By 2011, a technology that had been quietly gaining traction for years suddenly became the center of gravity in the data protection market: deduplication. The concept is straightforward — rather than storing multiple identical copies of the same data, you store one copy and maintain references to it. Imagine a company where ten thousand employees all have the same PowerPoint template in their email. Without deduplication, your backup system stores ten thousand copies of that file. With deduplication, it stores one copy and ten thousand pointers. The storage savings could be dramatic, often reducing backup data volumes by ten-to-one or more. In a world where enterprises were spending hundreds of thousands of dollars on backup storage every year, a technology that could reduce that bill by ninety percent got everyone's attention fast.

The company that changed the game was Data Domain, which built purpose-built deduplication appliances — specialized hardware boxes that sat in the data center and handled deduplication automatically. EMC acquired Data Domain in 2009 for $2.4 billion in a heated bidding war with NetApp, and the appliance model took off.

Suddenly, enterprises could buy a single box, plug it in, and immediately see dramatic improvements in their backup storage efficiency. It was simple, it was fast, and it did not require the kind of deep architectural planning that a full Simpana deployment demanded. The appeal was visceral: rack the box, connect it, and watch your backup storage costs plummet.

This was the first real crack in Commvault's armor. Simpana had deduplication capabilities built into its software, but Commvault was philosophically committed to being a software-only company. It did not build hardware appliances.

The argument was that software-based deduplication was more flexible, could run on any hardware, and avoided vendor lock-in. This was technically correct — software deduplication could protect a wider range of environments — but commercially tone-deaf. Enterprise buyers increasingly wanted simplicity — a box they could deploy in hours, not a platform that took weeks to architect. The Data Domain appliance became the default deduplication solution, and EMC's sales force had the relationships and credibility to place it in every Fortune 500 account.

And then came Veeam. Founded in 2006 — the same year as Commvault's IPO — by Russian-born entrepreneurs Ratmir Timashev and Andrei Baronov, Veeam focused exclusively on backing up VMware virtual machines. While Commvault was trying to be everything to everyone — backup, archive, replication, search, compliance — Veeam did one thing exceptionally well: protect virtual machines, simply and affordably.

The product could be downloaded, installed, and operational in under an hour. Pricing was transparent and aggressive — a fraction of what Commvault charged for equivalent coverage. The user interface was clean and intuitive. It was the classic disruptive innovation playbook right out of Clayton Christensen's textbook: start at the bottom of the market with a simpler, cheaper product, and work your way up.

By the early 2010s, Veeam was growing at triple-digit rates and stealing mid-market deals that Commvault would previously have won. IT administrators loved it because it just worked, and procurement departments loved it because it was affordable.

Commvault's response was to double down on platform breadth. The argument went: yes, Veeam can backup your VMware environment, but what about your physical servers, your Oracle databases, your Exchange servers, your archiving needs? Only Commvault can handle all of it from a single platform.

This was true, but it missed the point. Many enterprises were willing to accept a less comprehensive solution in exchange for simplicity and lower cost. "Good enough" beat "comprehensive but complex" in the mid-market, where most of the growth was happening. The complete platform story still resonated with the largest Global 2000 accounts — banks, governments, healthcare systems that needed to protect everything from mainframes to virtual machines — but the mid-market was moving toward simpler alternatives, and that mid-market was where most of the new revenue growth was happening industry-wide.

Meanwhile, the broader industry was consolidating rapidly. Symantec's troubled marriage with Veritas was producing mediocre results, distracting one of Commvault's largest competitors. EMC was assembling its "federation" of companies — VMware, RSA, Pivotal — and would eventually be acquired by Dell in a $67 billion deal. These mega-mergers consumed management attention and created integration headaches, which should have been an opportunity for an independent, focused player like Commvault.

But Commvault was having its own problems. Revenue growth was decelerating from the twenty-plus percent rates of the golden age into the low teens and then single digits. The stock, which had climbed steadily after the IPO, was becoming volatile. The competitive threats were no longer theoretical — they were showing up in quarterly results, in longer sales cycles, in deals lost to Veeam and emerging cloud-native vendors.

The cloud question was also beginning to crystallize. AWS had launched its core services years earlier, and by the early 2010s, enterprises were starting to experiment with moving workloads to the public cloud. The implications for data protection were profound. If your servers were in AWS instead of your data center, your backup architecture had to change fundamentally. You could not send a tape truck to Amazon's data center. Commvault, like most enterprise software incumbents, treated the cloud as a secondary consideration — something to be supported rather than embraced. The product could back up cloud workloads, technically, but the architecture and pricing model were still oriented around on-premises data centers. This would prove to be a costly miscalculation, and the companies that recognized the cloud's potential earliest — Druva (founded in 2008, SaaS-native on AWS), Rubrik, Cohesity — would use that head start to build formidable competitive positions.

VI. The Crisis Years: Disruption & Leadership Turmoil (2014–2019)

The years from 2014 to 2019 were the most turbulent in Commvault's history — a period when the company faced simultaneous disruption from below, from above, and from within. It is a textbook case of what happens when an incumbent's greatest strengths — technical depth, platform breadth, enterprise relationships — become liabilities in a rapidly changing market.

The disruption from below came from an emerging cohort of cloud-native data protection startups. Veeam, already a formidable competitor, was now generating well over $500 million in annual revenue and expanding aggressively from its VMware beachhead into broader enterprise environments.

But Veeam was not even the most threatening new entrant. Rubrik, founded in 2014 by Bipul Sinha and a team of Google and Oracle veterans, arrived with a bold premise: backup should be invisible. Their product was a converged appliance that combined backup software, storage, and deduplication in a single box that could be deployed in fifteen minutes — compared to the weeks or months a typical Commvault deployment required.

Cohesity, founded the same year by Mohit Aron (co-founder of Nutanix), took a similar approach with its hyperconverged secondary storage platform. Both companies were backed by hundreds of millions in venture capital, hired aggressively, and priced their products to win deals. They were not just cheaper alternatives; they represented a fundamentally different philosophy about what data protection should look like.

The disruption from above came from the public cloud providers themselves. AWS, Azure, and Google Cloud were building their own native backup and disaster recovery capabilities. AWS Backup, launched as a fully managed service, offered basic data protection for AWS workloads at a fraction of the cost of third-party solutions. Azure Backup did the same for Microsoft environments.

These services were not as sophisticated as Commvault or Veeam — they lacked the cross-platform breadth, the granular recovery options, the compliance features that large enterprises required. But for workloads born in the cloud, they were often "good enough." And they had one overwhelming advantage: zero incremental sales effort. If you were already an AWS customer, AWS Backup was right there in the console, activated with a few clicks. No procurement process, no vendor evaluation, no six-month implementation project. No salesperson needed. This is the existential threat that keeps every third-party infrastructure software vendor awake at night: the platform itself gradually absorbing the functionality that used to require a separate product.

The disruption from within was perhaps the most painful. By the mid-2010s, the Simpana platform had become a victim of its own success. Over nearly two decades, Commvault had added feature after feature, capability after capability, until the product could do almost anything — but at the cost of enormous complexity.

Sales cycles had lengthened as prospects struggled to understand the product's full scope. Win rates were declining as simpler alternatives gained mindshare. The pricing model, based on per-frontend-terabyte capacity, made sense in a world of predictable on-premises data growth but broke down in cloud environments where data volumes could spike unpredictably. Customers complained about surprise bills when their data volumes exceeded projections.

Bob Hammer had led Commvault for twenty years — an extraordinary tenure in the volatile world of enterprise software. He was the company's architect, the leader who had taken a Bell Labs research project and built it into a public company with hundreds of millions in revenue. But by the mid-2010s, the market was changing faster than the company could adapt under his leadership.

Revenue growth, which had consistently exceeded twenty percent in the golden years, slowed to low single digits. Fiscal year 2016 actually saw revenue decline slightly. The stock underperformed the broader tech sector for multiple consecutive years, frustrating investors who could see the competitive dynamics deteriorating but felt powerless to effect change.

In 2014, Commvault attempted to address the complexity problem by breaking Simpana into four focused products. The idea was to make the platform more accessible by offering targeted solutions for specific use cases. But the execution was clumsy — the products were still built on the same complex underlying platform, and the market was not convinced that repackaging alone solved the fundamental user experience problem.

By 2015, the company replaced the Simpana branding entirely with the "Commvault Data Platform" and eventually reduced its product count from more than twenty offerings to just four: Commvault Complete Backup and Recovery, HyperScale Technology, Orchestrate, and Activate. But the changes were cosmetic more than structural — the underlying product was still the same Simpana engine, and customers and prospects still experienced the same complexity.

The catalyst for real change came from outside the company. In April 2018, activist investor Elliott Management — one of the most feared and effective activist funds in the world, with a track record of forcing change at companies from AT&T to SAP — disclosed a significant stake in Commvault and published a scorching letter to the board.

Elliott's critique was devastating in its specificity: the company had lost ground in the market due to mismanagement, product complexity was driving customers to competitors, the sales organization was bloated and underperforming, and the executive team needed to be replaced. The letter called for immediate changes at both the board and executive level. By May 2018, Elliott secured a cooperation agreement for two board seats, ensuring it would have a direct voice in governance. The message to Hammer and the existing board was unmistakable: change, or we will change it for you.

One month later, the seventy-six-year-old Hammer announced his retirement as CEO. He would remain on the board temporarily, but his twenty-year tenure at the helm was over. The transition was not immediate — Hammer stayed through the end of fiscal year 2019 while the board searched for his successor — but the message was unambiguous. The era of founder-led, engineering-driven complexity was ending, whether the old guard liked it or not.

On February 5, 2019, Commvault announced its new CEO: Sanjay Mirchandani. His background was a deliberate contrast to Hammer's. Mirchandani had spent eleven years at Microsoft (1995-2006), followed by seven years at EMC — where he served as Chief Information Officer and led Global Centers of Excellence — and then three years at VMware, where he ran the Asia Pacific and Japan business.

Most recently, he had been CEO of Puppet, an open-source IT automation company based in Portland, Oregon, where he had grown the user base to over forty thousand companies. He understood cloud-native architecture. He understood modern software delivery. He understood subscription economics. And he understood that Commvault needed a fundamental cultural transformation, not just a product refresh.

Mirchandani's diagnosis was clear and unsentimental. The product was too complex. The go-to-market was broken — the sales force was structured for large, complex enterprise deals at a time when the market was moving toward faster, lighter purchasing motions. The cloud strategy was unclear, consisting of bolted-on cloud support rather than cloud-native architecture. And the culture was engineering-led when it needed to be customer-obsessed.

He immediately began simplifying the portfolio, restructuring the sales organization, and — most critically — developing a cloud-native strategy that could compete with the likes of Druva, Veeam, and AWS Backup on their own turf. The cultural shift was palpable. Under Hammer, Commvault had been an engineering-first company where the product team drove strategy. Under Mirchandani, the customer's voice would drive product decisions, and simplicity would be valued as highly as comprehensiveness.

Hammer stepped away from the board transition effective March 31, 2019, and Nick Adamo was appointed as Chairman, marking the definitive end of the founding era. The hard work of reinvention was just beginning.

VII. The Great Pivot: Cloud, Subscription & Metallic (2019–2021)

The single most consequential decision of the Mirchandani era came just eight months into his tenure. In October 2019, at the Commvault GO conference, the company unveiled Metallic — a brand-new SaaS backup-as-a-service offering built from the ground up as a separate brand with its own identity, pricing model, and go-to-market strategy. It was Commvault's answer to an existential question: can a thirty-year-old enterprise software company build a credible cloud-native product, or is that capability reserved for startups unburdened by legacy?

To understand why Metallic mattered so much, consider the dilemma Commvault faced. Its traditional product — now called Commvault Complete — was still powerful, still trusted by Fortune 500 customers, and still generating healthy margins. But it was a perpetual-license, on-premises product in a world that was rapidly moving to subscription-based, cloud-delivered software. Every quarter that Commvault continued to optimize for its legacy business was a quarter that cloud-native competitors like Druva gained ground. This is the innovator's dilemma in its purest form: protect today's profitable revenue, or invest in tomorrow's uncertain but necessary growth.

Mirchandani chose both, but with a twist borrowed from the playbook of every successful enterprise software transformation. Rather than trying to cloudify the existing product — a strategy that had failed at dozens of legacy software companies that bolted a cloud interface onto on-premises architecture — he created a separate offering with its own team, its own brand, and its own economics.

Metallic was designed to be operational in fifteen minutes. It ran natively on Microsoft Azure, thanks to a multi-year strategic partnership announced in June 2020 that deeply integrated Metallic with Azure's infrastructure, marketplace, and sales channels. It used consumption-based pricing — you paid for what you used, like a utility bill, rather than committing to a large upfront license based on data volumes you might never reach.

And it was marketed separately, with its own brand identity, so that cloud-native buyers would not be scared off by the Commvault name and its association with complex, on-premises enterprise software.

The Microsoft partnership was critical and worth dwelling on. By hosting Metallic exclusively on Azure and building Metallic Cloud Storage on Azure Blob Storage, Commvault gained access to Microsoft's enormous enterprise distribution network. Metallic became a featured app in the Azure Marketplace, meaning Azure customers could discover and purchase it as naturally as they would any other Azure service.

Joint sales programs meant Microsoft's field salespeople were incentivized to recommend Metallic to their customers. Engineering collaboration ensured tight technical integration. For Microsoft, the deal brought a best-in-class backup solution to Azure customers — a competitive response to AWS's growing ecosystem of data protection partners. For Commvault, it provided the cloud infrastructure, distribution, and credibility that would have taken years and hundreds of millions of dollars to build independently. It was one of the shrewdest partnership moves in enterprise software of the era.

The business model transformation extended far beyond Metallic. Across the entire company, Commvault was shifting from perpetual licenses to subscriptions. This is one of the most gut-wrenching transitions a software company can undertake.

Under a perpetual license model, a customer pays a large lump sum upfront — say, $500,000 — and then a smaller annual maintenance fee of around $100,000. Under subscription, the customer pays perhaps $200,000 per year. The economics are better long-term — higher lifetime value, more predictable revenue, deeper customer engagement — but in the short term, the shift is financially devastating.

That $500,000 deal just became a $200,000 deal in year one. Multiply that across hundreds of customers and the headline revenue numbers crater, even as the underlying business health improves. Wall Street punishes the transition even when it is strategically correct, because analysts anchor on near-term revenue and earnings, not future lifetime value.

Commvault also overhauled its pricing model, moving from the capacity-based per-frontend-terabyte approach — which had become a source of customer frustration as cloud data volumes grew unpredictably — to workload-based pricing that was more aligned with how customers actually consumed the product.

The sales force was restructured to support both the complex enterprise motion required for large Commvault Complete deals and the faster, lighter sales cycle required for Metallic's cloud-native customers. This was not a trivial change — it meant retraining salespeople who had spent careers selling seven-figure enterprise deals to also support smaller, faster transactions that required different skills and different compensation structures.

The partner ecosystem was rebuilt to emphasize cloud marketplaces, managed service providers, and born-in-cloud go-to-market strategies alongside the traditional value-added reseller channel.

Regulatory tailwinds added urgency. GDPR in Europe and CCPA in California created new data protection mandates that required enterprises to know where their data was, control who could access it, and be able to delete it on request. Ransomware insurance providers were increasingly requiring proof of robust backup and recovery capabilities as a condition of coverage. These external forces created a favorable environment for data protection vendors, and Commvault was positioning itself to benefit.

Early results for Metallic were encouraging. The product doubled its customer count every quarter through fiscal year 2021, and by that year it was available in twenty-four countries with over a thousand customers globally. Offerings spanned Microsoft Office 365 backup, Dynamics 365, Azure workloads, endpoint protection, and Kubernetes environments. The broader market repositioning was also taking shape: Commvault was no longer just a "data protection" company but a provider of "intelligent data services," emphasizing security, compliance, and data intelligence alongside traditional backup and recovery.

The timing proved fortuitous in a way no one could have predicted. As Metallic was gaining traction and the subscription transition was beginning to show results, the world was hit by a ransomware pandemic that would fundamentally reshape how enterprises thought about data protection. Recovery, immutability, and threat detection — capabilities that Commvault had been building into its platform for years — suddenly became the most urgent items on every CISO's agenda.

VIII. The Ransomware Era & Competitive Battles (2021–2023)

In May 2021, the Colonial Pipeline — the largest refined products pipeline in the United States, carrying gasoline and jet fuel from Texas to New York Harbor — was shut down by a ransomware attack. Gas stations ran dry across the southeastern United States. The federal government declared a state of emergency. Colonial paid a $4.4 million ransom in Bitcoin to a criminal group called DarkSide. Within weeks, JBS, the world's largest meat processor, paid $11 million to another ransomware gang. Then Kaseya, an IT management software provider, was compromised in a supply-chain attack that cascaded to hundreds of managed service providers and thousands of downstream businesses.

These were not isolated incidents. They were the visible peaks of a ransomware epidemic that had been building for years and that fundamentally changed the calculus of data protection. Before Colonial Pipeline, backup was the boring corner of the IT department — essential but unglamorous, a cost center that CIOs tried to minimize. After Colonial Pipeline, backup was a boardroom topic.

The question was no longer "how cheaply can we protect our data?" but "can we actually recover if we get hit?" The willingness to pay for robust, tested, proven recovery capabilities increased dramatically, and so did the urgency around features like air-gapped storage, immutable backups, and automated recovery orchestration.

To put it in non-technical terms: air-gapping means keeping a copy of your data completely disconnected from any network, so that even if hackers get into everything, they cannot reach that offline copy. Immutability means that once data is backed up, it literally cannot be modified or deleted — not by hackers, not by rogue employees, not even by administrators. These concepts went from niche technical features to boardroom requirements almost overnight.

For Commvault, the ransomware era was a strategic windfall. The company had been building security capabilities into its platform for years, and in January 2022, it accelerated this strategy by acquiring TrapX Security, an Israeli cyber deception company, for approximately $19 million. TrapX's technology was clever: it created decoys and lures that looked like normal applications and data, tricking ransomware into revealing itself before it could encrypt real assets. Think of it as setting up fake safes in a bank so that when burglars crack them open, alarms go off before they reach the real vault. This technology was integrated into the Metallic platform as the ThreatWise add-on, giving Commvault early threat detection capabilities that went beyond traditional backup.

The product innovation accelerated across the board. Commvault introduced threat scanning that could detect ransomware indicators in backup data before recovery, ensuring that organizations did not restore infected files. Automated recovery orchestration allowed customers to define recovery playbooks — step-by-step procedures for restoring systems in a specific order with specific dependencies — that could be executed with minimal human intervention during a crisis.

Zero-trust architecture principles were applied to the backup infrastructure itself — the idea being that if attackers compromise your production environment, they should not be able to reach your backup copies. The backup system became, in effect, the last line of defense — the one system that absolutely had to remain intact when everything else was compromised.

But Commvault was not the only company benefiting from the ransomware tailwind. The competitive landscape was intensifying across the board.

Veeam, still privately held and backed by Insight Partners (which had acquired it for $5 billion in January 2020), had built a massive installed base of over 550,000 customers and was expanding aggressively from the mid-market into enterprise accounts. By the early 2020s, Veeam was approaching $1.5 billion in annual revenue and had established itself as the number one vendor in data protection software according to IDC's market share reports — a remarkable achievement for a company that barely existed a decade earlier.

Rubrik was preparing for its public debut, having raised billions in venture capital and built a compelling cloud-native platform that resonated with enterprises adopting multi-cloud strategies. The company was growing subscription ARR at nearly fifty percent annually and had Microsoft as a strategic investor.

Cohesity and Veritas were engaged in merger discussions that would eventually produce the largest combination in data protection history. Cloud-native pure-plays like Druva — trusted by over five thousand customers including seventy-five of the Fortune 500 — continued to build share with their SaaS-first approach on AWS.

For Commvault, the financial inflection was beginning to materialize. Subscription revenue was crossing critical thresholds. ARR growth was accelerating, crossing $600 million by fiscal year 2023 and continuing to climb.

The transition from perpetual licenses to subscriptions — which had initially depressed headline revenue and tested investors' patience — was now reaching the inflection point where subscription growth was more than offsetting the perpetual decline. The revenue mix was shifting decisively: subscription revenue was surpassing fifty percent of total software revenue, validating the transformation thesis. For investors who had stayed through the painful transition years, the financial model was finally turning the corner.

Throughout this period, Mirchandani continued to execute the transformation playbook. The company deepened its positioning around cyber resilience, broadened Metallic's capabilities, and expanded its partnerships with all three major cloud providers.

The strategy was clear: Commvault's differentiation lay in its hybrid cloud flexibility — the ability to protect on-premises, cloud, and multi-cloud environments from a single platform — its twenty-five-plus years of enterprise trust, and the breadth of its platform across workloads and use cases. In a market where every vendor was racing to add security features, Commvault's argument was that it had the deepest integration between data protection and cyber resilience, backed by decades of enterprise deployment experience that newer competitors simply could not replicate.

IX. Modern Era: AI, Cyber Resilience & The Next Chapter (2023–Present)

On November 8, 2023, Commvault held its annual SHIFT conference in New York City and unveiled the most significant product launch since Metallic: Commvault Cloud, powered by Metallic AI. The name was deliberate and strategic. Rather than maintaining Metallic as a separate brand alongside the traditional Commvault platform — which was creating confusion in the market about which product to buy — the company unified everything. SaaS offerings, on-premises software, hybrid deployments — all under a single platform with a single management interface. Metallic evolved from a standalone SaaS product to the AI intelligence layer that powered the entire Commvault Cloud platform.

The launch introduced several capabilities that signaled Commvault's ambitions beyond traditional backup. Arlie, a generative AI copilot powered by Azure OpenAI Service, could respond to inquiries in plain language — allowing IT administrators to ask questions like "show me all unprotected workloads" or "what is my recovery readiness score?" instead of navigating complex management consoles.

Advanced threat prediction used AI-driven analysis to detect ransomware indicators, including the emerging challenge of shape-shifting AI malware that could evade traditional signature-based detection. Cloudburst Recovery leveraged infrastructure-as-code to automate the rapid reconstruction of entire environments in the cloud, reducing recovery times from days to hours.

The positioning was no longer "data protection" — it was "cyber resilience," a term that encompassed protection, detection, response, and recovery as a unified discipline.

The acquisition strategy accelerated meaningfully starting in 2024, signaling a more aggressive approach to capability building. In April 2024, Commvault acquired Appranix, a cloud cyber resilience startup based in Boston founded by Govind Rangasamy, for approximately $26 million.

Appranix's technology became the foundation for Cloud Rewind, launched at SHIFT 2024 in October — a capability that could automatically discover and catalog all cloud infrastructure components, capture their configurations, and reconstruct entire cloud environments after a cyberattack. Think of it as not just restoring your data, but rebuilding the entire house your data lived in: the networking, the compute instances, the security groups, the load balancers, the DNS configurations. For cloud-first organizations, this addressed a gap that pure data backup could not fill — because recovering data is useless if the infrastructure that data runs on has been destroyed.

In September 2024, Commvault acquired Clumio for just $47 million — a remarkable figure given that Clumio had raised $262 million in venture funding from top-tier investors, representing an eighty-two percent discount to its cumulative investment. This was a sobering illustration of how brutal the cloud-native data protection market had become; even well-funded startups with real technology were running out of runway. Clumio was an AWS-native SaaS data protection platform, and its acquisition immediately deepened Commvault's capabilities for protecting critical AWS workloads including S3 object storage, EC2 compute instances, and RDS databases.

In July 2025, Commvault announced the acquisition of Satori Cyber, an Israeli data and AI security company, closing the deal in August. Satori brought capabilities for discovering, classifying, and protecting sensitive data across cloud databases, data warehouses, and AI platforms — including the ability to monitor data flowing into large language models and assess compliance risk. This was a forward-looking bet on the intersection of data protection and AI governance, an area where few competitors had meaningful capabilities.

The financial performance told the transformation story in numbers. Fiscal year 2025, ending March 31, 2025, delivered total revenue of approximately $996 million — up nineteen percent year-over-year and tantalizingly close to the billion-dollar milestone. Subscription revenue reached $590 million, growing thirty-seven percent, while perpetual license revenue continued its steady decline to a fraction of the total.

Total ARR reached $930 million by the end of fiscal year 2025, with SaaS ARR at $281 million growing at sixty-eight percent. By the second quarter of fiscal year 2026, Commvault crossed the billion-dollar ARR threshold — two quarters earlier than management's own projections, a milestone that underscored the transformation's momentum.

The most recent quarter reported, Q3 FY2026 ending December 2025, showed record revenue of $314 million with subscription revenue of $206 million — now roughly fifteen times the size of the shrinking perpetual license business. The company also demonstrated confidence in its cash generation by returning significant capital to shareholders, completing a buyback program that repurchased over seven million shares for approximately $687 million. On the capital structure side, Commvault issued $785 million in zero-coupon convertible notes due 2030, with a conversion price of $236.88 — a figure well above the current stock price that provides financial flexibility but also implies potential dilution if the stock recovers.

At SHIFT 2025 in November, the company unveiled Commvault Cloud Unity, its next-generation platform with capabilities including Identity Resilience for Active Directory threat detection, Synthetic Recovery that uses AI to detect and surgically remove threats during recovery while preserving clean data, and expanded support for modern data platforms like Databricks.

In February 2026, Commvault introduced Geo Shield, addressing data sovereignty requirements with in-region control of data, operations, and encryption keys — a feature increasingly important as governments around the world impose data localization mandates.

The competitive dynamics continue to evolve rapidly. Rubrik completed its IPO in April 2024, pricing at $32 per share and raising $752 million at a $5.6 billion valuation. The stock performed well initially, nearly tripling from its IPO price before pulling back in early 2026 to around $53, giving it a market capitalization of roughly $11 billion.

The Cohesity-Veritas Data Protection merger closed in December 2024, creating the world's largest data protection software provider with combined revenue exceeding $1.7 billion and a $7 billion valuation — though post-merger integration challenges loom large, as they always do with mergers of this scale. Veeam, the market leader by revenue, completed a secondary sale in December 2024 that valued the company at $15 billion.

Commvault's current challenges are real. After reaching an all-time high near $200 in the summer of 2025, shares have fallen roughly fifty-five percent to the high-$80s by early 2026, driven by a trimmed ARR growth guidance and broader market rotation away from infrastructure software.

Multiple law firms announced investigations into potential securities claims in early 2026 — a common occurrence after significant stock declines that does not necessarily indicate wrongdoing but adds to the uncertainty overhang. These "ambulance-chasing" investigations are a predictable feature of the American legal landscape whenever a stock drops sharply, and investors should assess them with that context in mind.

The identity question looms: is Commvault an "old enterprise software survivor" or a "cloud transformation success story"? The answer is probably both, and the valuation discount to Rubrik either represents a buying opportunity for investors who believe the transformation has durable momentum, or a fair assessment that the growth profile warrants a lower multiple than faster-growing, pure-cloud competitors.

X. Playbook: Business & Investing Lessons

Commvault's nearly four-decade journey offers a masterclass in the dynamics of enterprise software incumbency, and the lessons extend well beyond data protection.

On the double-edged sword of installed base. Commvault's enterprise customer relationships — some stretching back two decades — provided the foundation for its survival. These customers could not easily rip out their backup infrastructure, and the switching costs of migrating years of protected data to a competing platform were enormous. This stickiness bought Commvault time during its most vulnerable period, generating predictable maintenance revenue even as new license sales stagnated. But the same installed base created a gravitational pull toward the status quo. Every decision to simplify the product risked breaking compatibility for existing customers. Every pricing change risked disrupting renewal economics. The installed base was both the safety net and the anchor — and managing that tension is perhaps the single hardest challenge in enterprise software.

On why complexity kills. Simpana's comprehensive feature set was Commvault's greatest competitive advantage in the 2000s and its greatest liability in the 2010s. The lesson is not that platforms are bad — Commvault's unified architecture remains a genuine differentiator. The lesson is that complexity must be managed ruthlessly, and that the internal experience of building a product (where each feature seems logical and necessary) is completely different from the external experience of buying it (where the sheer scope is overwhelming). When Veeam and Rubrik showed enterprises that backup could be simple, they did not just offer a cheaper alternative — they reframed what "good" looked like. The competitive threat was not that they were cheaper; it was that they changed the buying criteria from "which product has the most features?" to "which product can I deploy fastest?"

On the courage to cannibalize. Commvault's subscription transition required deliberately destroying its most profitable revenue stream — perpetual licenses with high upfront payments — in exchange for a subscription model that generated less revenue per customer in year one. Mirchandani's willingness to take that hit, and the board's willingness to support it through several quarters of depressed financial results, was the necessary condition for the company's current growth trajectory.

The playbook is instructive for any legacy software company facing a similar transition: create the new offering as a separate brand (Metallic), give it the freedom to compete without being encumbered by legacy constraints, staff it with people who think cloud-native rather than trying to retrain on-premises veterans, and then gradually unify the platforms once the new model has achieved critical mass. Commvault executed this playbook imperfectly but effectively — and the fact that subscription revenue now dwarfs perpetual licenses by a factor of fifteen is proof that the painful transition was worth the short-term cost.

On the pricing model evolution. Commvault's pricing journey — from capacity-based (per-terabyte) to workload-based to consumption-based — mirrors a broader evolution in enterprise software. Capacity pricing works when data volumes are predictable and growth is linear. Workload pricing works when customers want to pay for what they use rather than what they store. Consumption pricing works in cloud environments where usage is variable and customers expect utility-like billing. The lesson for software companies: your pricing model must evolve with your customers' economic models. When it does not — when customers are paying per terabyte in a world where cloud data explodes unpredictably — it creates friction that competitors can exploit.

On leadership transitions. Commvault's story illustrates the different kinds of leaders companies need at different stages. Bob Hammer was the right leader to take a Bell Labs research project and build it into a public company. Mirchandani brought the cloud experience and customer-obsessed culture that the transformation required. The lesson for boards: do not wait for a crisis — or an activist — to make the leadership change that the market is already demanding.

On ransomware as the great equalizer. The ransomware epidemic was an external shock that fundamentally changed the economics of data protection. It elevated backup from a cost center to a boardroom priority, reduced price sensitivity, and created demand for exactly the kind of enterprise-grade, deeply integrated recovery capabilities that Commvault had been building for years. Market timing matters, and companies that have been investing in capabilities ahead of demand can be the biggest beneficiaries when the world catches up.

XI. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces

Threat of New Entrants: Medium-High. The data protection market has become more accessible to new entrants in the cloud era. A startup can build a cloud-native backup product on AWS or Azure infrastructure without the capital-intensive hardware development that earlier generations required. The success of Rubrik, Cohesity, and Druva demonstrates that well-funded startups can break into the enterprise market relatively quickly. However, meaningful barriers remain. Enterprise buyers require years of compliance certifications, proven recovery track records, and the operational maturity to handle mission-critical deployments. The barrier to entering the market is low; the barrier to winning enterprise trust is high.

Bargaining Power of Suppliers: Low. Commvault builds on public cloud infrastructure that is increasingly commoditized. Azure, AWS, and Google Cloud compete fiercely on price and features, and no single cloud provider has leverage over Commvault's business. Open-source components reduce dependency on proprietary technology suppliers. This is one of the more favorable forces for the company.

Bargaining Power of Buyers: Medium-High. Large enterprises have significant negotiating power, particularly on renewal contracts where they can credibly threaten to evaluate competitors. The switching costs that once locked customers in are eroding as cloud-native architectures make data more portable and migration tools improve. Ransomware urgency has somewhat reduced price sensitivity for security-minded buyers, but the SMB market remains acutely price-conscious. The trend is toward greater buyer power as alternatives multiply.

Threat of Substitutes: High. This is perhaps the most critical force shaping Commvault's competitive position. Cloud-native backup services from AWS and Azure offer basic protection as a built-in feature of the platform, eliminating the need for third-party products for simple use cases. Point solutions for specific workloads chip away at the edges of the total addressable market. Some enterprises are questioning whether they need traditional backup at all in a world of immutable infrastructure and multi-region replication. The philosophical argument — "if my infrastructure is code and my data is replicated across three regions, do I really need a backup product?" — is a genuine long-term threat to the entire category, though the ransomware epidemic has largely kept this argument at bay for now.

Industry Rivalry: Very High. Veeam has a massive installed base, is privately held, was recently valued at $15 billion, and is approaching $2 billion in ARR. Rubrik is public, well-funded, and growing fast. The Cohesity-Veritas combination creates a $7 billion entity, though post-merger integration will consume attention. Cloud-native players like Druva continue to compete effectively. The hyperscalers improve constantly. Price competition is intensifying, feature parity is increasing, and the market is large enough to support multiple players but not so large that everyone can thrive.

Hamilton's 7 Powers

Scale Economies: Moderate. Commvault amortizes its R&D investment across a growing customer base, and cloud infrastructure costs improve with volume. But scale economies in enterprise software are less pronounced than in consumer internet businesses — you cannot serve a million additional customers at near-zero marginal cost. Veeam and Rubrik are achieving similar R&D scale, which limits the advantage.

Network Economics: Weak. Limited direct network effects exist in backup software — one customer's experience does not improve because another customer uses the same product. There are indirect effects through the partner and integration ecosystem: the more customers Commvault has, the more third-party integrations get built, which makes the platform incrementally more attractive. But these effects are modest compared to true platform businesses like Salesforce or ServiceNow.

Counter-Positioning: Lost (was strong). This is one of the most interesting dynamics in the Commvault story. In its early years, Commvault was effectively counter-positioned against point-solution competitors with its unified platform — an approach that incumbents could not easily replicate without cannibalizing their own product portfolios. Today, the situation has reversed. Cloud-native competitors like Rubrik and Druva are counter-positioned against Commvault — their simpler, cloud-first architectures represent an approach that Commvault cannot fully replicate without abandoning its legacy base. Commvault's attempt to reclaim counter-positioning through Commvault Cloud is underway but not yet complete.

Switching Costs: Strong but Eroding. This remains Commvault's most powerful competitive advantage. For large enterprises, switching backup vendors is a multi-year project involving data migration, runbook rewriting, staff retraining, and integration rebuilding. Twenty-plus year customer relationships create organizational inertia that is difficult for competitors to overcome. However, the cloud era is reducing switching costs as standard APIs, common data formats, and easier migration tools become available. Commvault's bet is that hybrid cloud flexibility creates a new form of stickiness that replaces the old on-premises lock-in.

Branding: Moderate. Strong brand in Fortune 500 data centers, built over decades of deployments and reinforced by Gartner Leadership positions. Less relevant in cloud-native and SMB markets, where newer vendors like Rubrik have stronger mindshare. The ransomware-era positioning around cyber resilience is building new brand equity, but brand alone does not win enterprise deals — it gets you on the shortlist.

Cornered Resource: Weak. No unique intellectual property that competitors cannot replicate, no exclusive access to talent or partnerships. Decades of enterprise knowledge are valuable but not irreplaceable. Partnerships with hyperscalers are important but non-exclusive — Rubrik has a deep Microsoft relationship, Druva is tightly integrated with AWS. This creates persistent competitive pressure.

Process Power: Moderate to Strong. This is Commvault's underappreciated strength and arguably the power that has sustained the company through its most difficult periods. Twenty-five-plus years of enterprise sales, implementation, and support have created organizational capabilities that are difficult to replicate. The company knows how to manage complex, multi-year enterprise deployments across heterogeneous environments — the kind of operational knowledge that cannot be acquired through venture capital, only through decades of hard-won experience. The subscription transition playbook demonstrates operational adaptability, and the cultural transformation is showing measurable results.

Overall Power Assessment. Commvault's primary moats are switching costs and process power. Its threatened moat is counter-positioning, which has shifted from offense to defense. The opportunity lies in building scale economies in the cloud era. The risk is that the absence of strong cornered resources or network effects means Commvault must continuously execute to maintain its position — there is no structural advantage that protects the business on autopilot. This is not a "winner-take-all" market; there is room for three or four major players, and Commvault is positioned as a stable number three or four with optionality for upside.

XII. Bear vs. Bull Case & Key Metrics

Bull Case: The Transformation is Real

The optimistic thesis starts with the numbers. Commvault crossed a billion dollars in ARR two quarters ahead of schedule, subscription revenue is growing at thirty percent-plus, and the company generates meaningful free cash flow — over $200 million in fiscal year 2025. The subscription transition is largely complete, with perpetual license revenue now a tiny fraction of total revenue. This is no longer a company "in transition" — it is a company that has transitioned.

The Commvault Cloud platform, now unified under a single architecture, is gaining traction in the mid-market and with cloud-native enterprises who might never have considered traditional Commvault. The ransomware and cyber resilience positioning sustains premium pricing, and the acquisitions of TrapX, Appranix, Clumio, and Satori Cyber have added differentiated capabilities. The strategic partnership with Microsoft continues to deepen, providing distribution and credibility in Azure environments. The recent Satori Cyber acquisition positions Commvault at the intersection of data protection and AI governance — a potentially large emerging market.

The bull case also envisions Commvault as a potential consolidation beneficiary. In a market that may support only three or four major independent players, Commvault's profitable, cash-generative profile makes it an attractive acquisition target for private equity, a strategic buyer, or even a larger competitor like Veeam seeking to consolidate.

The current valuation — roughly four times forward revenue — represents a meaningful discount to Rubrik and Veeam, and could re-rate upward if growth reaccelerates. The stock's decline from all-time highs, while painful for existing shareholders, may have created an entry point for investors who believe the transformation story is durable and that the recent guidance trim was a temporary setback rather than a structural inflection.

Bear Case: Stuck in the Middle

The pessimistic thesis observes that Commvault is neither the market leader (Veeam), the highest-growth cloud-native play (Rubrik), nor the largest entity (Cohesity-Veritas). It occupies the dangerous middle ground of the number three or four player. The legacy customer base generates less revenue each quarter as perpetual licenses decline, and the question is whether cloud ARR can grow fast enough to more than offset the shrinkage and sustain the overall growth trajectory.

Veeam, valued at $15 billion, and Rubrik, with strong public market backing and high-growth brand momentum, have the resources to invest aggressively in sales, marketing, and product development. The hyperscalers continue to improve their native backup capabilities, gradually raising the floor of "good enough" and shrinking the addressable market for third-party vendors.

The stock decline from roughly $200 to roughly $88 — a fifty-five percent drawdown — and the company's decision to trim its ARR growth guidance suggest the market may be pricing in structural deceleration rather than a temporary soft patch.

The hybrid cloud positioning — the ability to serve both on-premises and cloud environments — could prove to be a neither-here-nor-there strategy if the market bifurcates. The law firm investigations following the stock decline, while likely ambulance-chasing, add uncertainty. And the $785 million convertible note issuance, while providing financial flexibility, creates potential dilution if the stock fails to recover to the conversion price of $236.88.

The KPIs That Matter

For investors tracking Commvault's ongoing performance, two metrics matter above all others.

SaaS ARR growth rate. This is the single most important indicator of whether the cloud transformation is succeeding. Total ARR growth is useful but includes term-based subscription deals that can behave more like traditional software. SaaS ARR — which was growing at sixty-eight percent in fiscal year 2025 and forty-four percent in the most recent quarter — represents the pure cloud business. If this growth rate sustains above thirty percent, the transformation narrative holds. If it decelerates meaningfully below that, the "legacy vendor with a cloud wrapper" narrative takes over, and valuation compression follows.

Net revenue retention. This measures whether existing customers are spending more over time (expansion) or less (contraction and churn). In the data protection market, where workloads and data volumes naturally grow, a healthy vendor should see net retention well above one hundred percent — meaning the average customer spends more each year even without accounting for new customers. Commvault does not regularly disclose this metric in granular detail, which is itself worth noting — when companies are proud of a metric, they highlight it. Investors should monitor whether the company provides more transparency on retention, and whether underlying indicators like gross retention, customer count growth, and average deal size suggest healthy expansion dynamics.

XIII. Epilogue & Looking Forward

Commvault's story, as it stands in early 2026, is the story of a company that has earned the right to compete for the future — but has not yet secured it. The transformation from a Bell Labs research project to a public company to a cloud platform serving over twelve thousand subscription customers is genuinely impressive. Very few enterprise software companies of Commvault's vintage have navigated the twin disruptions of cloud computing and subscription economics as effectively. The ones that failed — Symantec's storage division, legacy EMC, the old Veritas before Cohesity acquired its data protection business — serve as cautionary reminders of what could have been.

The data protection market's future is being shaped by forces that play to both Commvault's strengths and its weaknesses. Consolidation will continue — the Cohesity-Veritas merger was likely the first of several combinations, and Commvault could be either an acquirer of smaller players or a target itself.

AI integration is moving from marketing buzzword to operational reality, with Commvault's investments in Arlie, Metallic AI, and the Satori Cyber acquisition positioning it at the intersection of data protection and AI security — an area that barely existed two years ago but is rapidly becoming one of the most important challenges in enterprise computing. The convergence of backup, security, and cyber resilience is creating a larger, more strategic market — one where the buying decision is made by CISOs and board audit committees, not just backup administrators. That elevation from cost center to strategic priority is perhaps the most important structural change in the data protection market in twenty years.

Commvault's biggest advantages heading into this next chapter are the same ones that have sustained it for decades: enterprise trust built over thousands of deployments, technical depth across the broadest range of workloads and environments, and the hybrid cloud flexibility to meet customers wherever their data lives.

Its biggest risks are equally persistent: execution in a market that demands both speed and reliability, competitive intensity from well-funded rivals on every side, and the ever-present threat that the hyperscalers will commoditize the core backup function.

What would surprise us in five years? Perhaps Commvault as an acquirer — using its cash flow and potential currency to consolidate smaller data protection players and build a broader platform.

Perhaps Commvault acquired — by private equity seeking a profitable, growing software business, by Veeam seeking to consolidate the market, or by a strategic buyer like a major cloud provider.

Or perhaps Commvault re-rating as a cloud winner, with its ARR growth and margin profile earning the kind of premium valuation that the market currently reserves for younger, flashier names.

For founders navigating disruption, Commvault offers a hard-earned lesson: survival is not guaranteed, but it is possible if you are willing to change everything about your company except its core mission. The technology changed. The business model changed. The leadership changed. The culture changed.

What did not change was the fundamental purpose — protecting the world's data — and the conviction that a unified platform approach, properly executed, could serve that purpose better than the alternatives.

For investors, Commvault teaches that turnarounds are possible but require patience, that transition metrics matter more than headline numbers during the transformation period, and that the difference between a "legacy vendor" and a "cloud platform" often comes down to execution rather than architecture. Commvault's story is far from over. The next chapter will determine whether this is a cautionary tale of an incumbent that transformed just enough to survive, or a triumphant reinvention story of a company that used its heritage as a foundation for its future.

XIV. Outro & Further Reading

Top Long-Form Resources

Company & Industry: 1. Commvault's quarterly earnings transcripts (2019-present) — the transformation narrative unfolds in real-time through management commentary 2. Gartner Magic Quadrant for Enterprise Backup and Data Protection (annual) — essential for tracking competitive positioning 3. "The Innovator's Dilemma" by Clayton Christensen — the theoretical framework that explains Commvault's mid-2010s crisis almost perfectly 4. Rubrik S-1 filing (2024) — provides deep insight into the cloud-native competitor's economics and positioning

Leadership & Strategy: 5. Sanjay Mirchandani's conference presentations and interviews (2019-present) — the transformation playbook articulated by the leader who executed it 6. "Crossing the Chasm" by Geoffrey Moore — enterprise software go-to-market principles that remain remarkably relevant 7. "The Idea Factory" by Jon Gertner — the definitive history of Bell Labs, where Commvault's story began

Technology & Market: 8. IDC and Gartner data protection market share reports — track the shifting competitive landscape with real numbers 9. Commvault SHIFT conference keynotes (annual) — product strategy and roadmap reveals that signal the company's direction 10. SaaStr content on subscription transitions in enterprise software — context for evaluating Commvault's business model shift

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube