Cavco Industries: From Mobile Homes to Modular Housing Innovation

I. Introduction & Episode Roadmap

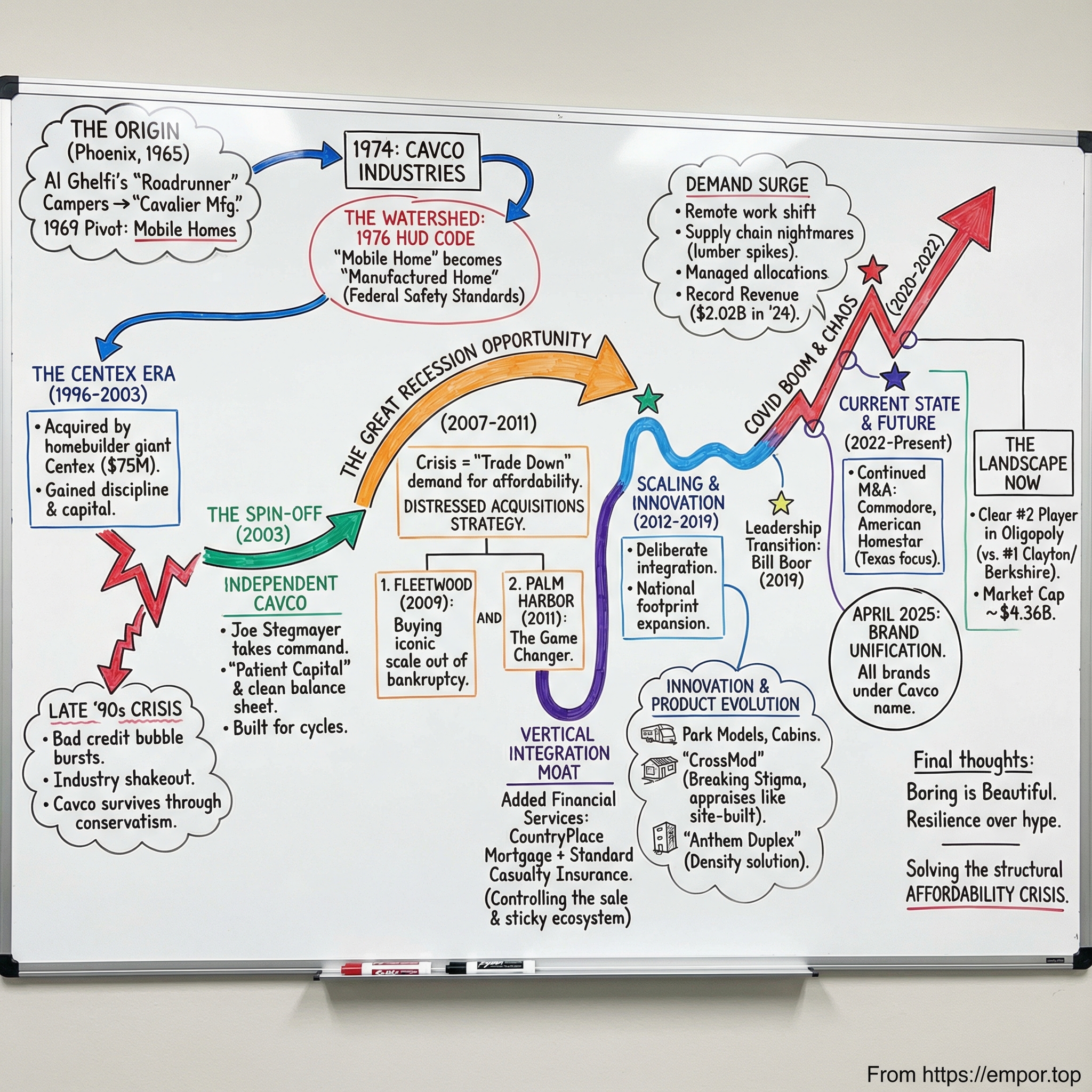

Picture Phoenix in 1965. In the back of his father’s lumberyard, a young entrepreneur named Al Ghelfi is building truck campers—hands-on work, sawdust everywhere, and a simple obsession with doing it well. Word travels fast across Arizona’s desert towns. If you wanted a camper that wouldn’t rattle apart on the road, you called Al. Orders start coming in.

What Al couldn’t have known was that this scrappy little operation would ride six decades of boom-and-bust housing cycles, survive industry shakeouts, pass through corporate ownership, and eventually become Cavco Industries—one of the biggest names in factory-built housing, with a market cap of about $4.36 billion as of February 7, 2025.

This is the story of how a Phoenix-based “mobile home” maker became a vertically integrated housing innovator—and why that evolution matters right now.

Manufactured housing sits at the crossroads of three forces remaking the American housing market: an affordability crisis that’s pushed millions out of traditional homeownership, growing pressure to build more efficiently as climate concerns rise, and a construction labor shortage that makes conventional homebuilding harder and more expensive. Today, more than 22 million Americans live in manufactured homes, and manufactured housing represents roughly one out of every ten new homes built in the U.S. each year.

Against that backdrop, Cavco has pulled off one of the more underappreciated transformation stories in modern American industry. In 2024, it generated $2.02 billion in revenue, up from $1.79 billion the year before. It expanded from a regional manufacturer into a national platform through disciplined acquisitions, vertical integration into financial services, and an operating playbook built to endure the cycle—not just enjoy the up years.

Along the way, we’ll keep coming back to a few big themes: why patient capital tends to beat impatient capital; why “boring” businesses can produce extraordinary outcomes; how vertical integration—when done with purpose—creates real staying power; and how a product still burdened with “trailer park” stigma might be one of the most practical tools America has to address its housing shortage.

Warren Buffett saw the opportunity early. Berkshire Hathaway bought Clayton Homes in 2003 for $1.7 billion, a bet that factory-built housing would only become more relevant as affordability worsened. Today, Cavco is the clear number two player in a highly consolidated industry, where the top three manufacturers account for around 80% of the market. Big enough to matter, but still nimble enough to move—that tension is where Cavco has built its edge.

II. Industry Context: Understanding Factory-Built Housing

Before we jump back into Cavco, we need to get our bearings—because “manufactured housing” might be the most misunderstood corner of American real estate. People talk about “trailers” like they’re all the same thing. They’re not. And the differences aren’t cosmetic; they change everything from regulation, to financing, to resale value.

The Terminology Matters

Start with the vocabulary. “Mobile home,” “manufactured home,” “modular home,” and “park model” get tossed around interchangeably, but they’re fundamentally different products.

A mobile home refers to factory-built housing constructed before June 15, 1976. That date matters because it’s when the federal government implemented what became known as the HUD Code—formally, the Manufactured Home Construction and Safety Standards (MHCSS). With it came national standards governing design and construction strength, durability, transportability, fire resistance, and energy efficiency.

After that line in the sand, the proper term is manufactured home. These homes are built to that comprehensive federal HUD Code. Instead of a patchwork of rules that varied by town or state, there’s one nationwide standard for safety and construction quality.

Modular homes are a different lane entirely. They’re also factory-built, but instead of being governed by the HUD Code, they’re built to local building codes, just like site-built homes. They’re typically installed on permanent foundations and, in many places, can qualify for conventional mortgage financing in the same way a traditional house would.

Then there are park models—a niche where Cavco has become the national leader. These are smaller structures, under 400 square feet, usually placed in RV parks, campgrounds, and vacation communities.

The Stigma Problem

To understand manufactured housing, you also have to confront the image problem. “Trailer park” conjures a very specific picture in the American imagination—and it usually doesn’t include vaulted ceilings, energy-efficient systems, or finishes you’d expect in mainstream new construction.

The 1976 shift from “mobile home” to “manufactured home” wasn’t just a marketing cleanup. It was a reset: higher standards, tighter inspections, and a very different product than what came before. But public perception moves slowly. The stigma stuck.

And here’s the twist: that stigma can function like a moat. Industries with perception problems don’t attract a stampede of new entrants. Few ambitious MBA types grow up dreaming of running a manufactured housing company. The result is a sector that, compared to many others, tends to have steadier competition and more rational behavior.

The Regulatory Watershed

The legal foundation for this transformation was the National Manufactured Housing Construction and Safety Standards Act of 1974, which set the stage for the HUD Code to take effect in 1976.

Before that, “mobile homes” lived in a regulatory Wild West. Depending on where you bought one, standards could range from strict to nonexistent. The category evolved from early 20th-century travel trailers into permanent housing people lived in full-time, but quality and durability were inconsistent—and the reputation followed.

The HUD Code changed the game by creating federal preemption. Homes built to HUD standards can be shipped and sold nationwide, regardless of local building codes. That national uniformity is a big reason modern manufactured housing can operate at scale: standardized production, standardized compliance, and the ability to serve a broad geographic market.

The Scale of the Opportunity

This isn’t a tiny niche. According to the U.S. Census Bureau, manufactured housing accounts for about 6.6% of occupied housing units in the United States, housing nearly 22 million Americans. Other industry reporting puts the figure in the same ballpark, with roughly 20.6 million people living in a manufactured or mobile home. Manufactured homes make up about 9.3% of annual new home starts.

That’s tens of millions of people—more than the populations of New York City, Los Angeles, and Chicago combined—living in factory-built housing.

And the “why” is simple: affordability. In 2024, the average manufactured home sold for $123,300, while the median single-family home value reached $367,282. Even with the important caveat that the manufactured home figure typically excludes land, the gap is enormous.

That price advantage isn’t magic, and it isn’t about cutting corners. It’s about process. Manufactured homes use standard building materials, but they’re built almost entirely off-site in a controlled factory environment. Assembly-line techniques reduce weather delays, theft, vandalism, and material damage, and they rely less on scarce on-site labor.

The key takeaway—for understanding Cavco and this whole industry—is that this isn’t the “mobile home” business of the 1960s. It’s precision manufacturing applied to housing. And once you see it that way, the competitive dynamics, the economics, and the long-term opportunity look very different.

III. Cavco's Origins & The Centex Era (1965–2003)

The Ghelfi family story starts small, the way most enduring American companies do: with a product, a workshop, and a founder who can’t stop tinkering.

In 1965, Al Ghelfi named his camper-building operation Roadrunner Manufacturing. It wasn’t even incorporated at first—just an unincorporated association turning out truck campers and travel trailers in Phoenix. A year later, the business took a new name: Cavalier Manufacturing.

Then came the pivot that set everything in motion. In 1969, Cavalier moved into custom mobile home production, selling wholesale through dealers in Arizona. The logic was straightforward: if you could build a travel trailer, you could build a home that stayed put. By 1973, the company had dropped its original product lines entirely. Mobile homes weren’t a side project anymore—they were the business.

In 1974—right as Congress passed the legislation that would soon lead to the HUD Code—Cavalier Manufacturing changed its name again, this time to Cavco Industries. That same year, Aldo Ghelfi retired as president, and his son, Alfred Ghelfi, moved up from a cluster of roles—vice president, secretary, and treasurer—into the top job.

The 1970s Boom

For mobile home manufacturers, the late 1970s were a wave you wanted to be surfing, not watching from shore. Cavco grew with the industry, and in 1977 it opened a second Phoenix plant to work through a backlog of orders for double-wide homes.

Between 1975 and 1979, sales more than quadrupled, reaching $20.4 million. Cavco also pushed beyond Arizona for the first time, building dealer relationships in New Mexico, Colorado, and California. It was still a regional player, but it was learning how to scale—one plant, one dealer, one new market at a time.

The Centex Acquisition

The defining corporate turning point of Cavco’s early history arrived in December 1996. Centex Corporation—then a major national homebuilder—acquired 80% of Cavco’s outstanding stock, effectively bringing Cavco into the Centex fold. The transaction valued the deal at $75 million, priced at $26.75 per share, and paid shareholders above the market.

Centex’s logic was clear: manufactured housing could be a low-cost complement to its broader homebuilding and mortgage operations.

The mismatch in scale was stark. In 1996, Cavco generated $130.1 million in revenue and $6.2 million in net income on 4,893 homes delivered. Centex, by comparison, generated $3.1 billion in revenue and $53.4 million in net income from more than 12,000 site-built homes.

For Cavco, being inside Centex wasn’t just about capital. It was an education. The company got exposure to the disciplines of large-scale homebuilding—operational rigor, financial services integration, and the kind of systems a major public company demands. More importantly, it learned to think across the full value chain: not just building homes, but capturing margin from manufacturing through retail and financing.

The Crisis That Culled an Industry

Then the industry hit its wall.

In the late 1990s, easy credit had supercharged manufactured home sales. But much of that financing was shaky—often predatory, often extended to borrowers who couldn’t realistically keep up with payments. Defaults surged. Lenders backed away. And when financing disappears in a category where most buyers need a loan, everything freezes.

At Cavco, the mix of oversupply and a changing retail landscape began to distort the business. In fiscal 2000, retail sales jumped 53%, but total sales rose only 3%, to $183.5 million. The company responded by cutting capacity: it closed the Belen plant in August 2000 and the Seguin plant in March 2001.

The downturn got ugly fast. In 2001, both retail and wholesale sales declined by about 30%. Home deliveries fell from 5,950 in 2000 to 4,242 in 2001. Revenue dropped to $123 million, and Cavco posted an operating loss of $6.9 million.

And Cavco wasn’t alone. The crisis devastated the industry’s biggest names. Fleetwood Enterprises and Palm Harbor Homes—both giants at the time, both future pieces of Cavco’s expansion—took enormous hits. Many competitors vanished outright. For manufactured housing, the 1999–2000 collapse was a defining shakeout, the kind that permanently resets who survives and who doesn’t.

Financing was the choke point. With key lenders exiting, it suddenly felt like nobody would finance a manufactured home. And without financing, sales for the industry fell hard.

But Cavco’s performance had a strange twist: even as the market imploded, Cavco’s sales rose modestly. They were taking share.

That pattern—staying conservative, controlling costs, leaning on strong dealer relationships, and coming out of downturns with more relevance than they went in with—became part of Cavco’s DNA. It’s also the thread that leads directly to the next chapter, when Cavco’s future stopped being a subsidiary story and started becoming its own.

IV. The 2003 Spin-Out: Birth of Independent Cavco

By 2003, Centex had made up its mind: manufactured housing wasn’t going to be a core pillar of the company’s future. Cavco was small inside a much larger homebuilding empire, and after the industry’s late-’90s credit blowup, it was hard to argue the division deserved meaningful capital or executive attention.

So in late April, Centex announced it would spin Cavco off. At the time, Cavco was the largest manufactured housing company in Arizona and the 13th-largest in the country. Centex was blunt about the rationale. “Yes, Centex is bowing out of the manufactured housing business,” said Sheila Gallagher, Centex’s vice president of corporate communications. “The business did not turn out to be a major strategic focus for Centex.” She also pointed to the upside for Cavco: outside Centex, it could pursue capital on its own terms instead of competing internally for resources.

The mechanics were straightforward and shareholder-friendly: a tax-free distribution to Centex shareholders, with Cavco emerging as its own publicly held company. In April 2003, Centex formally decided to proceed, and on June 30 the share distribution closed. Cavco stepped into the market as an independent company, with Joseph Stegmayer as chief executive officer.

Joe Stegmayer Takes Command

Stegmayer is the central character of modern Cavco. He wasn’t new to this world—he’d lived through multiple manufactured housing cycles and held senior roles at both Champion Homes and Clayton Homes before landing at Centex. He started his career in 1973 at Worthington Industries, supplying LP gas cylinders to the RV industry, and he brought that same supplier-and-operator mindset into housing: watch the cash, respect the cycle, and obsess over execution.

He joined Cavco in 2000, right as the industry was unraveling. That timing mattered. If you’ve been through a collapse up close, you tend not to build a company on the assumption that good times last forever. Stegmayer pushed a conservative balance sheet and a discipline-first culture—and he saw what the post-crisis landscape really was: a field of weakened competitors and stranded assets, waiting for a patient buyer with cash and operational chops.

The Spinoff Opportunity

For investors who pay attention to corporate plumbing, Cavco’s separation from Centex checked every box for a classic spinoff “special situation.” Centex, an S&P 500 homebuilder, would issue one share of Cavco for every 20 shares of Centex owned—meaning Cavco would land in the accounts of thousands of shareholders who never asked to own a microcap manufactured housing company.

That matters because spinoffs often start life under a cloud of mechanical selling. Index funds can’t hold them. Large institutions can’t be bothered. Plenty of shareholders just don’t want the odd little stub they were handed. And when that selling hits a small stock, price and value can disconnect.

Inside Cavco, the logic was simpler and more important: freedom. As Stegmayer put it, the spinoff worked for both sides because Cavco could now make “small” expansions—new markets, modest capacity adds—that would never have registered as meaningful inside a giant like Centex. And with no debt on the books and real cash flow, Cavco could grow selectively: buy a plant that was about to shut down, or build a new one when the economics actually made sense.

This was the strategic reset in its purest form: a focused company, lean operations, a clean balance sheet, and leadership built for cycles. The next chapter is what happens when that discipline meets opportunity.

V. The Great Recession: Counter-Cyclical Opportunity (2007–2010)

When the Great Recession crushed site-built housing in 2008 and 2009, manufactured housing didn’t escape the pain—but it didn’t implode the way much of residential construction did. Volumes fell, yes. But the category held up better than many people expected.

And you can see why. In a crisis, the housing market doesn’t stop needing homes. It starts demanding cheaper ones. As layoffs spread and credit tightened, buyers who still had to move, form households, or replace housing “traded down” to what they could actually afford. Manufactured housing, already far below the cost of site-built alternatives, became the practical option.

This is where Cavco’s operating philosophy started to look less like caution and more like strategy. The conservative balance sheet it had maintained in the good years gave it oxygen when others were choking. Its factories carried lower fixed costs, and its model moved inventory faster. That meant Cavco could operate profitably at volume levels that would have pushed less efficient competitors into the red.

Distress, in other words, didn’t just create risk. It created opportunity.

Distressed Acquisitions Begin

The downturn turned the industry’s once-untouchable names into bankruptcy auctions. The assets were real—plants, brands, distribution—just stranded. If you had capital and knew how to run them, you could buy scale for pennies on the dollar.

That’s exactly what Cavco did.

In August 2009, Cavco and its investment partner, Third Avenue Value Fund, paid $26.6 million to acquire Fleetwood Homes out of Chapter 11. This wasn’t just any target. Fleetwood was an iconic name that had been building manufactured homes since 1950. At the time, Cavco itself was still relatively small—making manufactured homes, park models, and vacation cabins out of just two plants. This deal was Cavco stepping onto a much bigger stage.

Palm Harbor was next. The Dallas-based manufacturer—along with five subsidiaries—filed for bankruptcy protection, and the auction became another chance to buy meaningful assets at a moment when few buyers had both the balance sheet and the patience to act.

A subsidiary structure tied to Fleetwood (then jointly owned by Cavco and Third Avenue) ultimately made the successful bid: $83.9 million for substantially all of Palm Harbor’s manufactured and modular housing construction and retail operations. But the most strategically important pieces weren’t the factories. The winning package also included Palm Harbor’s insurance and finance subsidiaries: CountryPlace Mortgage and Standard Casualty.

Those additions would matter for years. Manufacturing is cyclical. Financing and insurance—done carefully—can steady the business, expand margins, and help control the customer experience.

By the time the economy started to find its footing again, Cavco had done what great cycle operators do: it used the downturn to buy enduring assets, not to simply survive it. The company came out of the Great Recession with bigger brands, broader reach, and the early building blocks of what would become its financial services segment.

VI. The Transformative Deal: Going Public via Centex Spinco (2010–2011)

By the time the economy started to thaw, Cavco had something most of its peers didn’t: cash, credibility, and a growing set of assets bought out of distress. The next move was about turning that advantage into a repeatable growth machine.

Cavco had already re-entered the public markets after the 2003 Centex separation, but what really mattered was what being public made possible. A public stock isn’t just a scoreboard—it’s a tool. It gives you acquisition currency. It lowers your cost of capital. And it signals to sellers, lenders, and dealers that you’re stable enough to be a long-term home for their business.

That combination proved catalytic. With stock available as consideration, Cavco could pursue acquisitions without draining its cash. With a lower cost of capital, more projects cleared the return bar. And with the added visibility that comes from being public, Cavco began attracting the kind of investors who understood the strategy: stay conservative, buy when others can’t, and compound over time.

The playbook after the listing was straightforward: keep expanding through a mix of acquisitions and organic growth—then integrate relentlessly.

Joe Stegmayer's Building Phase

This was the stretch where Joe Stegmayer’s reputation as the architect of modern Cavco really took shape.

After joining Cavco in 2000, he led the company through a steady build: growing annual sales from $95 million to $600 million, and expanding from three factories in two states to 19 factories in 11 states. Under his tenure as chairman, Cavco also scaled its park model business into the number one builder of park models in the country.

But the point wasn’t just size. It was how that size was assembled—deliberately. Cavco wasn’t sprinting for headline growth. It was stitching together a national footprint step by step, absorbing each new plant, brand, and team before reaching for the next one.

And Stegmayer had an edge that doesn’t show up on financial statements: relationships. Years at Clayton and Champion gave him deep roots in the industry. When a plant owner wanted out, or a distressed asset needed a buyer with both discipline and staying power, Cavco was often the first call.

VII. The Vertical Integration Buildout (2011–2016)

With Cavco’s footprint expanding and its balance sheet still built for cycles, the strategy in the mid-2010s became clear: don’t just sell a home. Own more of the experience around it.

Cavco’s vertical integration push unfolded in three phases. Each one added a new layer of control—over where it could build, how it could sell, and how reliably it could get customers financed and protected.

Phase 1: Manufacturing Footprint Expansion

First came the footprint.

Cavco bought Ocala, Florida-based Chariot Eagle, picking up additional park model RV product lines and, just as importantly, deeper reach in the Southeast. Chariot Eagle wasn’t just another factory; it was a regional institution. Founder Bob Holliday had built a loyal following over three decades, and Cavco was buying into that trust as much as into the production capacity.

The March 2015 deal also captured Cavco’s M&A style in miniature: find strong regional operators with real dealer relationships, keep the people who made the business work, integrate the back office, and let the brand keep doing what it does best. Founded in 1984, Chariot Eagle specialized in park model RVs and smaller manufactured homes designed for planned communities and resorts, and it had grown into one of the largest privately owned park model RV builders in the country.

A couple of months later, Cavco expanded again—this time into geographies it hadn’t meaningfully served before. Through its wholly owned subsidiary FH Group, LLC, Cavco acquired the business and certain assets of Fairmont Homes, Inc., headquartered in Nappanee, Indiana, with manufacturing plants in Indiana and Minnesota. Fairmont was known for manufactured and modular homes, plus park model RVs—exactly the kind of product mix Cavco wanted more of.

The May 2015 Fairmont acquisition added Midwest and Northeast exposure that Cavco previously lacked. Just as important, it brought production capability, a reputation for quality and service, and an established customer base. For Cavco, it wasn’t only about planting flags on a map. It was about being able to serve existing customers in more places—and adding new markets where Fairmont was already well established, including the Midwest, the western Great Plains states, and the Northeast.

Phase 2: The Downstream Move - Financial Services

But the bigger strategic move wasn’t another factory. It was what Cavco had already picked up in the Palm Harbor deal: the ability to finance and insure the customer.

Palm Harbor didn’t just come with manufacturing and retail operations. It brought CountryPlace Mortgage and Standard Casualty, which became the backbone of Cavco’s financial services segment. CountryPlace is an approved Fannie Mae and Freddie Mac seller/servicer and a Ginnie Mae mortgage-backed securities issuer. It offers conforming mortgages, non-conforming mortgages, and home-only loans for factory-built home buyers. Standard Casualty provides property and casualty insurance to owners of manufactured homes.

That mattered because manufactured housing lives and dies on financing availability. Many buyers can’t access traditional mortgage products, in part because manufactured homes are often titled as personal property rather than real estate. That limits options, raises friction, and can kill a deal even when a customer wants the home. By controlling a financing platform, Cavco could help qualified buyers get to “yes” when the rest of the market couldn’t—or wouldn’t—serve them. And it could earn more than just the manufacturing margin in the process.

Insurance added another layer. Manufactured home owners need coverage, and Standard Casualty could keep that premium stream inside the Cavco ecosystem instead of letting it leak to third parties. More control, more stickiness, more economics per customer.

Operationally, Cavco emphasized integration discipline. With Fleetwood since 2009 and Palm Harbor and the related finance and insurance businesses since 2011, the company said it believed the steady integration of these operations with each other—and with Cavco’s legacy units—had gone well.

Phase 3: Full Ownership and Consolidation

The last step was simplifying the ownership structure.

In June 2013, Cavco announced it had entered into an agreement to acquire full ownership of Fleetwood Homes, Inc., the parent company of Fleetwood Homes, Palm Harbor Homes, CountryPlace Mortgage, and Standard Casualty. Cavco already owned 50% of Fleetwood Homes, Inc.; this transaction bought the other 50% from Third Avenue Value Fund and an affiliate.

This wasn’t a sudden change of heart—it was consistent with the original intent when Cavco and Third Avenue formed Fleetwood Homes, Inc. in 2009. There were buyout terms in the shareholders’ agreement, but Cavco and Third Avenue negotiated the purchase about a year earlier than those provisions would have required.

Step back, and the logic of vertical integration here is less about shaving pennies off lumber costs and more about building a more resilient machine. In manufactured housing, controlling the “adjacent” pieces—financing and insurance especially—can be the difference between a customer wanting a home and a customer actually getting one. And when that customer finances through CountryPlace and insures through Standard Casualty, Cavco isn’t just selling a unit. It’s capturing more of the value chain, and making the whole system work better together.

VIII. The Master Stroke: Acquiring Fleetwood and Palm Harbor

The Fleetwood deal in 2009 and the Palm Harbor deal in 2011 were the moments Cavco stopped looking like a careful regional operator and started looking like a consolidator with a national plan. These weren’t ordinary acquisitions. They were rescues—iconic names pulled out of bankruptcy at crisis prices by a buyer disciplined enough to integrate them.

Fleetwood and Palm Harbor had everything Cavco wanted: brands dealers already trusted, real manufacturing capacity, and distribution infrastructure. What they didn’t have, at that moment, was stability. Cavco did.

Fleetwood: An Industry Legend Falls

Fleetwood Enterprises had been building manufactured homes since 1950, becoming one of the best-known names in the entire category. But by 2009, years of industry pressure—followed by the financial crisis—pushed it into Chapter 11.

Cavco acquired Fleetwood’s manufactured housing assets in August 2009 through a Fleetwood subsidiary based in Riverside, California. Cavco’s final bid came in at $21.8 million.

That number tells you everything about the environment. In a panic, you can buy history, capacity, and market presence for a fraction of what it would cost in normal times—if you’re one of the few buyers still standing.

Palm Harbor: Adding Scale and Financial Services

Palm Harbor came into Chapter 11 with $321.3 million in assets and $280.3 million in liabilities. It was a big business in serious trouble.

When Palm Harbor filed in November 2010, Cavco had a clear read on the opportunity: this wasn’t just more production. It was a chance to add scale, retail reach, and—most strategically—financial services.

The winning bid of $83.9 million brought in manufacturing facilities, retail locations, the Palm Harbor brand, and a long list of operating assets: equipment, receivables, inventory, intellectual property, and certain warranty and other liabilities.

But the crown jewels were the finance and insurance businesses tied to Palm Harbor: Standard Casualty Company, Standard Insurance Agency, CountryPlace Acceptance Corp., and CountryPlace Mortgage, Ltd. These subsidiaries weren’t parties to the bankruptcy filing, but their shares were included in the assets acquired by Fleetwood Homes’ subsidiary. That’s how Cavco ended up with the pieces that would become core to its long-term strategy.

The Integration Challenge

Buying distressed assets is easy. Making them work is the hard part.

Bankrupt companies usually arrive with broken processes, bruised dealer relationships, and employees who’ve spent months—sometimes years—living with uncertainty. Customers wonder if warranties will be honored. Dealers wonder if deliveries will show up on time. Culture clashes happen fast.

Cavco’s edge was that it didn’t try to “flip the switch” overnight. It kept what was working—especially local management and brand identities that still mattered to dealers and buyers—while integrating the back office in a measured way. Step by step, it brought these businesses into the Cavco system without blowing up the relationships that made them valuable in the first place.

The result was exactly what Cavco was aiming for: the company roughly doubled, improved margins through scale and operational efficiency, and emerged from the post-crisis years as a true national player—not just a regional manufacturer that happened to survive.

IX. Innovation & Product Evolution (2016–2020)

By 2016, Cavco had earned what it had been chasing for a decade: real scale. But scale in housing is only half the job. The next question was harder: how do you stay relevant as tastes change, regulators evolve, and the competition gets sharper?

The answer was to keep widening the definition of what “factory-built” could be—until it stopped sounding like a compromise and started sounding like a platform.

Beyond the Trailer: Product Diversification

Whatever image the phrase “mobile home” still triggers, Cavco’s product lineup by this point looked nothing like that stereotype. The company built park model RVs for vacation and retirement communities. It built vacation cabins. And it built factory-built commercial structures—everything from workforce housing to schools, along with housing for United States military troops.

On the residential side, Cavco expanded its modular lineup too: single- and multi-section homes in familiar American styles—ranch, split-level, Cape Cod—plus two- and three-story homes and multi-family units. The throughline wasn’t just variety for variety’s sake. It was a deliberate move into categories with different customers, different use cases, and different demand cycles.

CrossMod: Breaking Down Barriers

One of the biggest ceilings on manufactured housing has always been what happens after the sale: financing, appraisals, and the broader system’s tendency to treat these homes as “other.”

CrossMod was the industry’s coordinated attempt to crack that ceiling. The concept was simple: build homes to specifications that help them qualify for conventional financing and appraisal treatment closer to site-built housing. In other words, make the product easier to buy, easier to value, and easier to understand within the existing housing ecosystem.

CrossMod homes must now appraise alongside site-built homes and other CrossMod homes, giving homeowners a clearer path to building equity over time. A 2024 FHFA study found that modern manufactured home properties gain value year over year and, since 2020, have appreciated at a rate on par with site-built homes—evidence that the wealth-building case for modern manufactured housing is stronger than the old stigma suggests.

The Anthem Duplex: Innovation for the Housing Crisis

Cavco’s innovation push also produced something very concrete: density.

In December 2023, the company launched The Anthem, described as the first nationally available, HUD-approved duplex series. The Anthem duplexes were first designed and built at the Cavco-Fleetwood Homes plant in Rocky Mount, Virginia. The series includes four models, and the big idea is straightforward: place a duplex on a single home lot and you immediately double the housing delivered on that footprint.

That makes The Anthem a direct response to one of the most stubborn constraints in the housing crisis: communities that need more homes, but can’t—or won’t—expand outward.

One model in particular, The Blue Ridge, became a proof point. Cavco says it is the first true duplex built on a single frame, and it was displayed at Homes on the Hill in Washington, D.C., part of HUD’s Innovative Housing Showcase.

X. The COVID Era & Housing Boom (2020–2022)

The pandemic didn’t just rattle the economy. It scrambled the basic assumptions of where people wanted to live, how fast they needed to move, and what they could afford. And in that chaos, manufactured housing turned out to be one of the more resilient corners of the housing market.

The Surprising Boom

When COVID-19 pushed millions into remote work, the map of housing demand shifted almost overnight. Apartments in dense cities lost some of their appeal. Space, distance, and price suddenly mattered more. And for a huge number of households, the math led them to the same place: factory-built housing.

Demand surged. Backlogs piled up. Lead times stretched to six months or more as manufacturers tried to keep up with orders.

Supply Chain Chaos

But the boom didn’t come clean.

Material costs swung wildly. Lumber, in particular, spiked to levels that reshaped the economics of building; at one point, lumber alone added more than $36,000 to the cost of an average new home. Labor was tight too, as factories competed for workers in a market where everyone was hiring at once. And even when homes were built, getting them delivered became its own bottleneck—transportation capacity was limited, routes were delayed, and schedules became moving targets.

Cavco’s response looked like the playbook it had been building for years: raise prices to reflect input costs, squeeze more output from existing capacity through efficiency initiatives, and manage allocations carefully so it protected relationships with key dealers rather than chasing short-term wins.

Financial Performance

The demand surge showed up in results. Revenue moved into a new range, margins expanded, and Cavco’s stock followed.

By 2024, Cavco reported $2.02 billion in revenue, up from $1.79 billion the year before, and earnings of $171.04 million, also higher year over year.

The question investors wrestled with coming out of the boom was the one that always hangs over a cyclical business at its best moment: was this simply the top of the cycle—or was the market finally starting to treat Cavco less like a “mobile home” company and more like a structural solution to American housing affordability?

XI. Recent Developments & Strategic Position (2022–Present)

Leadership Transition

After two decades of Joe Stegmayer shaping Cavco’s modern playbook, the company had to manage a messy reality: leadership continuity matters, but so does trust.

Following an internal investigation conducted by independent legal counsel, Cavco said it identified certain violations of company policy related to securities trading activities by Stegmayer. He stepped down as Chairman, President, and CEO, and the board moved him into a non-executive role—an attempt to keep his deep industry and operational experience in the building while handing day-to-day control to someone new.

That “someone new” was William “Bill” Boor, appointed CEO effective April 15, 2019. Boor wasn’t a stranger walking in off the street. He had worked on Cavco’s strategy when it was still inside Centex, participated in the 2003 spinoff process, and had served on Cavco’s board since 2008. His background was also unusually broad for manufactured housing: he had been CEO of Great Lakes Brewing Company since 2015 and held multiple executive roles at Cliffs Natural Resources from 2007 to 2014, after earlier serving as Vice President of Corporate Development at Centex.

In other words: Cavco didn’t just pick a leader. It picked a bridge—someone with firsthand knowledge of how this company was built, board-level context, and an operator’s resume.

Continued M&A: The Commodore Acquisition

Even with leadership changing, the strategy didn’t. Cavco kept doing what it had learned to do best: buy assets that expand footprint and product mix, then integrate.

On September 24, 2021, the company completed its acquisition of the business—and certain assets and liabilities—of The Commodore Corporation, following its July 26, 2021 announcement. Cavco described Commodore as the largest independent builder of manufactured and modular housing in the United States, operating under a variety of brand names and including two wholly owned retail stores. The purchase price totaled $153 million, before certain adjustments at and following closing.

The American Homestar Deal

Cavco doubled down on distribution and presence in one of the most important housing markets in the country: Texas.

The company confirmed it completed the acquisition of the business of American Homestar Corporation and its subsidiaries, effective September 29, 2025. American Homestar—best known as Oak Creek Homes—operates two manufacturing facilities and 19 retail locations. It also writes and sells a limited number of manufactured home loans and acts as an agent for third-party insurers.

Cavco said it acquired American Homestar for $190 million in cash, subject to customary purchase price adjustments. “Throughout the acquisition process, we developed a tremendous respect for what Buck Teeter, Dwayne Teeter, and the entire American Homestar team have built,” Cavco President and CEO Bill Boor said.

The deal expanded Cavco’s footprint in Texas and the South Central U.S. The acquired business had about 800 employees, and for the 12 months ended May 31, 2025, it reported $194 million in revenue, $16.6 million in net income, and $17.8 million in adjusted EBITDA (non-GAAP).

Brand Unification

After years of buying respected regional builders—often keeping their names to preserve local equity—Cavco made a different kind of move: tightening the story it told the market.

On April 1, 2025, Cavco Industries brought its extensive home manufacturing brands under the Cavco name, positioning itself as a unified national brand and aiming to invest more effectively in its stated mission to help solve the affordable housing crisis.

The brands included in this step were: Fleetwood Homes, Palm Harbor Homes, Nationwide Homes, Fairmont Homes, Friendship Homes, Destiny Homes, Chariot Eagle, MidCountry Homes, Commodore Homes, Colony Homes, PennWest Homes, R-Anell Homes, and Solitaire Homes.

XII. The Competitive Landscape & Market Dynamics

Clayton Homes: The 800-Pound Gorilla

If Cavco is the clear number two, Clayton Homes is the force everything else orbits around.

Clayton is the largest builder of manufactured and modular homes in the United States, and it’s been a wholly owned subsidiary of Warren Buffett’s Berkshire Hathaway since 2003. That Berkshire backing doesn’t just mean deep pockets. It means patience: the ability to invest through downturns, play the long game on capacity and distribution, and never be forced into a bad decision because capital got tight.

Clayton’s scale sets the tone for the entire industry. It holds over 40% market share and produces roughly 50,000 homes a year—about half of total industry output. When one company is that large, every competitor has to choose a lane: compete head-to-head on price and footprint, differentiate on product and service, or win through focus and execution in specific regions and channels.

Skyline Champion: The Other Major Player

Then there’s Skyline Champion—the other heavyweight in the ring.

Champion Homes, Inc., formerly Skyline Champion Corp., is a major producer of factory-built housing, spanning manufactured and modular homes, park model RVs, cabins, and accessory dwelling units. With more than 70 years of history, around 9,000 employees, and 46 manufacturing facilities across the United States and western Canada, Skyline Champion has the kind of footprint that lets it serve multiple end markets—single-family, multifamily, hospitality—and pivot mix as demand shifts.

In a category where distribution and logistics matter as much as design, that breadth is real competitive leverage.

The Industry Structure

Zoom out, and manufactured housing looks a lot like a classic oligopoly. The barriers to entry are meaningful: regulatory complexity, the cost and know-how required to run high-throughput factories, and, most importantly, the relationship-intensive dealer network that moves product. Scale matters, and so does credibility—because nobody wants to bet their inventory, financing pipeline, and reputation on a manufacturer that might not be around next year.

That structure has produced a small circle of dominant players, with the biggest names—Clayton, Cavco, and Skyline Champion—defining the market’s pricing discipline and competitive pace.

It’s also why Buffett’s interest here is so instructive. Clayton fits the Berkshire template: a business with durable demand drivers, high barriers to entry, and returns that can be strong without needing constant reinvention. And the stigma that still clings to “mobile homes” acts like a filter—keeping attention and capital away, which is often exactly where Buffett likes to operate.

XIII. The Business Model Deep Dive

Manufacturing Economics

At its core, manufactured housing is a factory business that happens to produce homes. And like any factory business, the math is dominated by fixed costs: the plant, the equipment, and the baseline workforce you need whether you’re shipping 10 homes this week or 100.

That creates powerful operating leverage. When orders are strong and volume rises, those fixed costs get spread across more units and margins widen. When demand drops, the opposite happens: the same cost base gets divided across fewer homes, and profitability can evaporate fast.

That’s why capacity utilization is the dial everyone watches. A plant humming along at high utilization can generate attractive margins. A plant running half-full can struggle to break even. It’s also why consolidation tends to lift industry profitability: the acquirer can consolidate production, keep the best-performing facilities running harder, and rationalize redundant capacity.

The Dealer Model

Manufactured housing also has a very different go-to-market engine than site-built homes. Instead of selling directly to a buyer after months of construction, manufacturers like Cavco typically sell through independent dealers.

The dealer buys homes from the manufacturer, puts them on a retail lot, and sells them to end consumers. Those dealer relationships are a real asset in this industry—hard to build, easy to damage, and incredibly valuable once established.

There’s another key wrinkle: inventory has to be financed while it sits on the lot. Dealers often use floor plan financing to carry that inventory until it sells. Manufacturers may participate in these programs by providing, arranging, or guaranteeing financing for dealer inventory. That cuts both ways. It creates risk—because you’re exposed to dealer credit and market downturns—but it also creates leverage. When times get tight, the manufacturer that can support inventory financing becomes the manufacturer that keeps dealers alive.

And that’s part of why the dealer relationship can be sticky. Switching manufacturers isn’t like changing a vendor on a spreadsheet. Dealers have to learn new product lines, rebuild trust on delivery and warranty performance, and potentially give up co-op advertising support or favorable floor plan terms. The better the manufacturer’s program, the higher the real-world switching cost.

Unit Economics

The manufactured housing value proposition shows up quickly in the pricing.

In 2024, the average cost for a new manufactured home was $109,400, down nearly 4 percent from the previous year. The average for a multi-section home was $164,678, while a new single-section home averaged $81,281.

In practice, that means a basic single-wide might sell for around $80,000, while multi-section homes with more features often land in the $165,000-plus range. Higher-end modular homes and custom builds can go beyond $200,000.

For Cavco and its peers, mix matters as much as volume. Multi-section homes and premium upgrades generally carry better margins than entry-level product. So when buyers shift toward larger homes or more options, it doesn’t just raise average selling price—it tends to improve margins too.

Financial Services Contribution

Then there’s the part of the model most people don’t associate with a “home manufacturer”: finance and insurance.

Cavco’s financial services segment—CountryPlace Mortgage and Standard Casualty—adds profit directly by capturing economics that would otherwise go to third parties. CountryPlace earns margin on loans. Standard Casualty earns premium revenue from homeowners who need coverage.

But the bigger value is strategic. In manufactured housing, financing availability often determines whether a sale happens at all. A buyer who can get financing through CountryPlace is far more likely to close than someone forced to navigate the fragmented lending market on their own. In other words, financial services doesn’t just sit beside the manufacturing business—it helps keep the factories running.

XIV. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces:

1. Threat of New Entrants: LOW

This is not a business you casually decide to enter. A modern manufactured-housing plant takes real capital to build and run, and the HUD Code adds a regulatory learning curve that’s hard to shortcut. The bigger barrier, though, is distribution: dealer relationships aren’t won with a pitch deck, they’re earned over years of hitting delivery dates, standing behind warranties, and being there through the cycle. Add in scale advantages in purchasing, logistics, and marketing, and the economics get tough for a would-be newcomer fast.

2. Bargaining Power of Suppliers: MODERATE

Most core inputs—lumber, steel, appliances—are commodities. That keeps supplier power in check, especially for a scaled buyer like Cavco. Vertical integration into certain components helps smooth out some volatility, too. But as the COVID era made painfully clear, when supply chains seize up, “commoditized” doesn’t always mean “available,” and temporary disruptions can quickly swing leverage back toward suppliers.

3. Bargaining Power of Buyers: MODERATE-HIGH

On paper, dealers can shop around among manufacturers. In practice, switching carries friction: product lines are different, service levels vary, and reputation with customers is on the line. Still, bargaining power is meaningful because end consumers are intensely price-sensitive, which caps how much margin the system can support. And in manufactured housing, financing is often the deal. When loan availability tightens, buyer power rises—because fewer customers can actually transact.

4. Threat of Substitutes: MODERATE

The main substitute is still site-built housing. When the affordability gap is wide, manufactured homes have a strong tailwind; when it narrows, substitution pressure rises. Apartments and rentals compete for the same household budget, especially for first-time buyers deciding whether to rent or own. And while newer alternatives like tiny homes and RVs exist, they tend to serve lifestyle buyers more than the broad, mainstream need for durable housing.

5. Industry Rivalry: MODERATE

This is a consolidated market, and consolidation tends to produce more rational behavior. With the top three players accounting for the bulk of share, price wars are less common than in fragmented industries. Clayton’s dominance also shapes the landscape: it sets a high bar and absorbs a lot of competitive energy. Meanwhile, regional differentiation gives the major players room to coexist without constantly colliding head-on.

Hamilton's 7 Powers:

1. Scale Economies: STRONG

The factory model rewards scale. Higher volume spreads fixed costs, improves purchasing terms, and makes distribution more efficient. Cavco’s national footprint and number-two position give it enough scale to compete effectively—and enough throughput to make its integration and process investments pay off.

2. Network Effects: WEAK

There isn’t a true network effect here in the classic sense. A larger manufacturer doesn’t automatically become more valuable because more people use it. Dealer networks matter a lot, but they don’t compound like a social network or a marketplace.

3. Counter-Positioning: MODERATE

Factory-built housing competes against site-built housing with a fundamentally different cost structure and process. Traditional homebuilders can’t easily “just respond” without rebuilding their operating model. The stigma around manufactured housing also plays both ways: it keeps some competitors away, but it can keep some customers away too.

4. Switching Costs: MODERATE

Dealers incur real costs in switching manufacturers—retraining sales teams, learning new specs, adjusting service and warranty workflows, and rebuilding trust. On the consumer side, financing relationships can add stickiness: when lending and insurance are embedded in the buying process, the system becomes harder to swap out midstream.

5. Branding: MODERATE

Cavco’s portfolio of names—Cavco, Fleetwood, Palm Harbor, and others—has real recognition, especially regionally. But the category’s lingering stigma puts a ceiling on how much “brand” alone can command in pricing power, no matter how strong the reputation is within the industry.

6. Cornered Resource: WEAK-MODERATE

Factories and footprints are valuable, but they’re not exclusive—given enough time and money, others can build them. The more defensible resource is relationship capital: dealer trust, distribution reach, and the institutional know-how built over decades of delivering product through volatile cycles.

7. Process Power: MODERATE-STRONG

This is where Cavco’s edge shows up most clearly. Lean manufacturing discipline, repeatable integration, and an M&A playbook refined over multiple acquisitions create capabilities that are hard to copy quickly. You can buy a factory. It’s much harder to buy the operating rhythm that makes a network of factories run well together.

Primary Powers: Scale Economies + Process Power

Put it together, and Cavco’s advantage isn’t a single magic asset. It’s the combination of scale and execution: a company large enough to matter, and operationally sharp enough to keep compounding that scale through smart capital allocation, disciplined acquisitions, and integration that actually sticks.

XV. Bull vs. Bear Case & Investment Considerations

Bull Case:

Structural Housing Affordability Crisis America’s housing affordability problem isn’t just a “bad year” problem—it’s a long-running supply-and-demand imbalance. Years of underbuilding, layers of regulation that make new construction slow and expensive, and a huge wave of millennials hitting prime household-formation age have combined into a persistent housing shortfall. Manufactured housing doesn’t solve every constraint, but it does one critical thing better than almost anything else: it delivers a real home at a price point millions of households can still reach.

Regulatory Tailwinds The rules are slowly bending in a friendlier direction. ADU laws in California and other states are widening the market for factory-built options. Zoning reform is showing up in more city and state conversations. And at the federal level, manufactured housing is increasingly being talked about as part of the housing solution rather than a category to ignore. If regulation is the gate, this is the gate creaking open.

Vertical Integration Moat Cavco isn’t just a set of factories. It’s factories plus financing plus insurance plus a national footprint and dealer relationships that take years to earn. That combination matters because in this category, the hardest part often isn’t building the home—it’s getting the customer approved, insured, delivered, and satisfied. Replicating that full stack would take an enormous amount of time, capital, and execution.

Balance Sheet Optionality Cavco’s low debt and cash generation give it a simple but powerful advantage: it can play offense when others are forced into defense. In a cyclical business, that optionality is a weapon. It’s how Cavco has historically been able to buy quality assets from distressed sellers and come out of downturns bigger and stronger—exactly the pattern that built the company into the clear number two today.

Bear Case:

Cyclicality Risk Even with the affordability tailwind, manufactured housing is still tied to the economic cycle. When interest rates rise, payments rise, approvals get harder, and buyers pull back. In a recession, volumes can fall quickly, and with factory economics, that can pressure margins just as fast.

Clayton's Competitive Position Clayton has a structural advantage that’s hard to overstate: Berkshire Hathaway behind it. That means deep capital, the ability to invest through downturns, and a time horizon that isn’t measured in quarters. Clayton can out-invest, out-last, and out-wait any publicly traded competitor if it decides a market or channel is strategically important.

Stigma Ceiling Cavco can improve designs, quality, and energy efficiency—and it has—but perception doesn’t update at the same pace. Manufactured housing still carries stigma in many communities, and that can cap adoption, constrain zoning outcomes, and limit premium pricing. Even a great product can be boxed in by a dated mental image.

Disruption Possibilities The housing world is full of would-be revolutionaries. Modular construction startups, 3D-printed housing, and other new approaches could change how buyers and developers think about factory-built construction. At the same time, site-built homebuilders keep getting more efficient. Cavco may be well positioned, but the competitive landscape isn’t frozen.

Key Metrics to Watch:

1. New Home Orders and Backlog This is the earliest read on momentum. Orders tell you what demand looks like right now; backlog tells you how much visibility the company has into future revenue.

2. Average Selling Price and Product Mix In this business, what you sell matters as much as how much you sell. A shift toward multi-section homes and higher-feature builds typically lifts profitability. ASP trends also help tell you whether price increases are sticking—or whether the market is pushing back.

3. Gross Margin Performance Margins are the truth serum. They reflect efficiency, pricing discipline, input costs, and competitive intensity all at once. Holding up margins through a softer environment is one of the clearest signals that the model—and the execution—has real durability.

XVI. Lessons for Founders & Investors: The Playbook

Patient Capital Wins

Cavco didn’t become a national leader on a sprint. It did it the slow way: by staying alive through ugly cycles, building capabilities one layer at a time, and waiting for the right moments to swing. The years after the Centex spinoff gave Cavco room to lay that groundwork without having to manufacture a story every quarter. And when the financial crisis created a once-in-a-generation set of distressed assets, its partnership with Third Avenue Value Fund helped it move with conviction when most capital couldn’t—or wouldn’t.

Vertical Integration Done Right

Cavco’s vertical integration wasn’t about owning everything in sight. It was about owning the parts that make the whole machine work: financing the purchase and insuring the home. Those are natural “touch points” in the customer journey, and controlling them can turn a maybe into a closed sale—while also keeping more economics inside the business. The real test of integration isn’t whether you can bolt on another operation. It’s whether the combined system becomes simpler for the customer and more resilient for the company.

Consolidation in Fragmented Industries

Manufactured housing played out like the textbook: a fragmented industry gets hit by a crisis, weaker players become forced sellers, and the buyer with cash and operational discipline buys at attractive prices. The hidden part—where most consolidations succeed or fail—is integration. Cavco’s advantage was that it didn’t just acquire capacity; it absorbed it, stabilized it, and improved the economics of the combined footprint. That same pattern shows up in other cyclical, relationship-driven industries where assets are durable but ownership isn’t.

Boring is Beautiful

Nobody grows up dreaming of running a manufactured housing company. That’s exactly the point. The category’s lack of glamour keeps competition thinner than it would be in a “hot” sector, and it keeps capital from piling in at the wrong time and driving irrational behavior. For operators willing to commit for decades—not quarters—“boring” can be a feature, not a bug.

The Berkshire Heuristic

Buffett’s involvement is a clue worth taking seriously. Berkshire bought Clayton Homes because manufactured housing has the kind of demand driver Berkshire loves: people will always need a place to live, and affordability only becomes more important when the economy gets tight. Clayton’s dominance doesn’t make life easier for competitors, but it does validate the underlying market—and it reinforces what Cavco’s story shows again and again: in the right structure, with the right discipline, an unglamorous business can compound for a very long time.

XVII. The Future: What's Next for Cavco?

The ADU Opportunity

Accessory dwelling units—small secondary homes placed on single-family lots—could open a meaningful new lane for factory-built housing. California’s ADU-permitting reforms have already helped unlock demand, and Cavco’s model fits the moment: build in a factory, deliver fast, and avoid much of the on-site construction chaos. Whether ADUs become a scaled, repeatable market or remain a patchwork of local wins is still unclear. But for Cavco, the upside is simple: it’s a new use case that doesn’t require the company to reinvent what it already does well.

Institutional Capital Entering

Another shift is happening downstream, in who owns the land. Institutional investors—REITs, private equity, family offices—have increasingly woken up to manufactured housing communities as attractive assets. If that trend continues, it can pull through demand for new homes, as upgraded or expanded communities need fresh inventory. At the same time, more institutional ownership could mean a more professionalized customer base for Cavco: larger buyers, longer planning horizons, and the potential for repeat purchasing across portfolios.

Technology Integration

Factory-built housing is still manufacturing, and manufacturing is increasingly software-driven. IoT sensors, automation, and better design tools are changing how efficiently homes can be built and how consistently quality can be maintained. The winners won’t just be the companies that buy new machines—they’ll be the ones that integrate technology into a system that actually runs better day to day. Cavco’s scale matters here: it has the resources to invest in tools and process upgrades that smaller competitors may simply not be able to justify.

The Succession Question

In a business this cyclical, leadership isn’t a nice-to-have—it’s the steering wheel. Bill Boor has led Cavco since 2019, but long-term investors inevitably ask what comes next, and whether the company can maintain its discipline when the cycle turns. Cavco’s history of developing internal talent and folding in experienced teams through acquisitions suggests it treats succession as a real operating priority, not a slide in a board deck.

Could Berkshire Buy Cavco?

And then there’s the question everyone asks sooner or later: could Berkshire Hathaway buy Cavco and combine it with Clayton? The strategic logic writes itself—more scale, less competition, and near-total national coverage in factory-built housing. But the obstacles are just as real: whether regulators would allow that level of consolidation, and whether Berkshire’s famously strict valuation discipline would line up with Cavco’s market price at the time. For now, it remains a fascinating what-if—one that also underscores just how strategically important this corner of housing has become.

XVIII. Epilogue & Reflections

What makes Cavco’s story remarkable isn’t one clever trick or a single, headline-grabbing bet. It’s the unglamorous thing that’s far rarer: doing the right, fairly obvious things—over and over—through multiple cycles, and actually sticking with them long enough for the compounding to show.

Cavco waited when waiting was the move. Then it pounced when the industry was on its back—buying real assets, recognizable brands, and hard-to-rebuild capabilities at moments when most would-be buyers either couldn’t get financing or didn’t have the stomach. It integrated when integration is where most roll-ups quietly die. It kept its balance sheet from becoming a liability. And it treated dealer relationships like what they really are in this business: the distribution engine you don’t get to rebuild quickly after you break it.

The macro backdrop is what turns all of that from an impressive operating story into something bigger. America’s housing problem isn’t a one-year mismatch. It’s structural: not enough supply, high costs to build, wages that haven’t kept up with home prices, and steady pressure from new household formation. That doesn’t guarantee smooth sailing—this is still a cyclical business—but it does mean the underlying need for affordable housing isn’t fading.

Manufactured housing won’t solve the crisis by itself. Zoning, land, infrastructure, and financing constraints are real, and stigma still shapes what communities will allow. But factory-built housing is one of the few ways to deliver a real home with real quality faster, with less waste, and at a price point that millions of buyers can still reach. And companies like Cavco—especially with financing and insurance capabilities integrated into the platform—make that system work end to end, not just at the factory door.

From Al Ghelfi building campers in a Phoenix lumberyard in 1965 to a national factory-built housing platform worth more than $4 billion in 2025, Cavco is proof of what disciplined execution over a long horizon can produce. Not a hype story. A resilience story. And, increasingly, a story about one practical path toward building more homes in a country that badly needs them.

XIX. Further Reading & Resources

If you want to go deeper, these are the sources that do the best job separating myth from mechanics—how the homes are built, how they’re financed, and how companies like Cavco actually compound over time.

Essential Primary Sources: 1. Cavco Industries Annual Reports & 10-Ks (2011–2025) - Direct from investor relations 2. Berkshire Hathaway Annual Letters (re: Clayton Homes) - Buffett’s view on manufactured housing economics and long-term business quality 3. HUD Manufactured Housing Reports - The industry’s data backbone, plus the regulatory framework that shapes everything 4. Cavco investor presentations and earnings call transcripts - Management’s own narrative, priorities, and operating details

Industry Context: 5. Manufactured Housing Institute research publications - Statistics, policy work, and the industry’s perspective on adoption and constraints 6. Urban Institute manufactured housing research - A strong, research-driven view of market structure and policy implications 7. Federal Reserve manufactured housing financing studies - The financing reality: credit availability, consumer access, and where the bottlenecks form

Background Reading: 8. Joel Greenblatt’s writings on spinoff investing - Useful context for why the 2003 Centex separation mattered and how spinoffs can misprice 9. The Color of Law by Richard Rothstein - How housing policy decisions created today’s landscape, and why “affordable housing” is never just a construction problem 10. Industry trade publications (MHInsider, MHProNews) - Day-to-day industry signal: new products, regulation shifts, and competitive moves

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube