Cousins Properties: The Story of Sun Belt Office's Patient Capital Machine

I. Introduction & Episode Roadmap

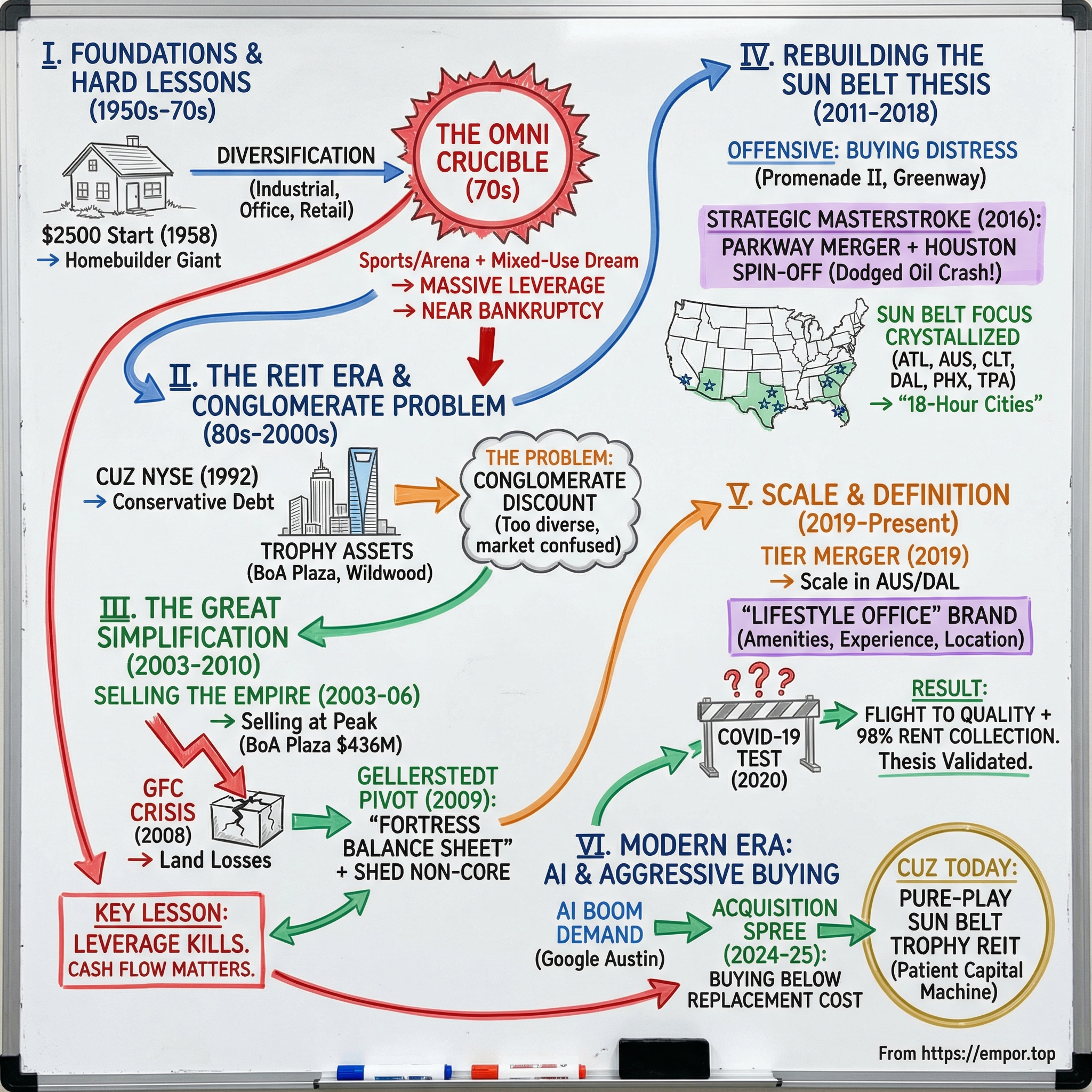

Picture this: it is the summer of 2006 in Atlanta, and a seventy-four-year-old real estate developer named Tom Cousins is about to walk away from the empire he spent nearly five decades building. Over the preceding three years, his company has sold equity in thirty-five projects for a combined 2.7 billion dollars. The crown jewel, Bank of America Plaza, the tallest building in the American South at 1,023 feet, goes for a record-shattering 436 million dollars. Cousins retires as chairman that December, and the company he founded with twenty-five hundred dollars sits on a mountain of cash.

Three years later, the world economy is in ashes. Office buildings across the Sun Belt trade for pennies on the dollar. And the team now running Cousins Properties begins doing something that looks, to outside observers, either brilliantly contrarian or completely insane: they start buying it all back.

Cousins Properties, trading under the ticker CUZ on the New York Stock Exchange, is today an Atlanta-headquartered real estate investment trust with roughly four billion dollars in market capitalization and a laser focus on what it calls "lifestyle office" properties in Sun Belt cities. The portfolio spans about twenty million square feet across Atlanta, Austin, Charlotte, Dallas, Tampa, and Phoenix, with occupancy hovering above ninety percent. In a world where "office" has become almost a dirty word in real estate investing, Cousins has quietly built one of the most disciplined and focused platforms in the business.

The central question of this story is deceptively simple: how did a 1950s Atlanta family real estate business, one that nearly went bankrupt building a sports arena, transform itself into a pure-play Sun Belt office REIT that institutional investors consider a best-in-class operator? The answer involves a founder who learned brutal lessons about leverage, a company that had the courage to sell its identity and then buy it back at a discount, and a thesis about American geography that has played out exactly as predicted, even through a pandemic that was supposed to kill office work forever.

The arc of this story runs through post-war Atlanta's explosive growth, the spectacular rise and near-catastrophic fall of the Omni Coliseum, a painful multi-decade journey from conglomerate to pure-play, and a series of capital allocation decisions that would make even the most disciplined value investors nod with approval. It is a story about patience, focus, and the conviction to bet on where America was heading before anyone else saw it clearly.

II. Post-War Atlanta & The Cousins Family Vision (1950s-1970s)

Thomas G. Cousins was born on December 7, 1931, the second of four children in a Georgia family that moved constantly through the Southeast. His father, Isaac William Cousins, known as Ike, distributed automobiles for General Motors, rotating through Charlotte, Jacksonville, and Atlanta as the company shuffled him around. His mother worked in a department store and later as an office manager. There was nothing about the Cousins family that screamed future real estate titan.

But Tom Cousins had something that would matter enormously: an almost pathological work ethic. By third grade he was cutting grass for neighbors. In high school he lifeguarded, delivered newspapers, jerked sodas at the drug store, and made deliveries. He was competitive by nature, swimming long-distance for the University of Georgia swim team, where he enrolled at sixteen after graduating high school early. He started pre-med, but during his senior year, watching a surgical procedure made him physically ill, and he pivoted to business. He graduated with a BBA from UGA's Terry College of Business in 1952, then served in the Air Force's Strategic Air Command through his ROTC commission.

When Cousins returned to Atlanta in 1954, the city was transforming in ways that would prove pivotal to his career. The phrase "the city too busy to hate" had become Atlanta's unofficial motto as it navigated desegregation more pragmatically than most Southern cities, guided by a business elite that understood racial conflict was bad for commerce. Mayor William Hartsfield and his successor Ivan Allen Jr. cultivated a reputation for Atlanta as a forward-looking, business-friendly metropolis. Coca-Cola's headquarters anchored the downtown economy. Delta Air Lines was turning Hartsfield Airport into the busiest hub in the South. Rich's department store, the Georgia-Pacific Corporation, and a growing cluster of banks were creating a white-collar employment base that would need offices to work in and houses to live in. The population was growing fast enough that someone needed to build for all the newcomers, and Tom Cousins intended to be that someone.

Cousins took a job at Knox Homes Corporation, a manufacturer of prefabricated houses, and within four years had risen to Vice President of Sales and the company's top salesman. But the real education was in understanding the mechanics of development: how land, capital, construction, and demand fit together. In 1958, at twenty-six, he invested twenty-five hundred dollars and founded his own company. The first person he hired was his father. First-year sales were eleven thousand dollars.

The trajectory from there was remarkably steep. Sales hit 1.6 million dollars by 1960, five million by 1962, and Cousins Properties became the largest homebuilder in Georgia before its founder turned forty. The company went public in 1962, raising five hundred thousand dollars in its first stock offering. Cousins was already thinking bigger than houses.

By 1965, Cousins had diversified into industrial parks, downtown Atlanta office buildings, retail centers, apartment complexes, and mortgage lending. He developed a distinctive approach to risk: minimize debt, retain control, and partner with deep-pocketed institutions. Over the years, his joint venture partners would include Coca-Cola, the Ford Foundation, IBM, and NationsBank. The model was elegant: Cousins provided land and development expertise while the institutional partner provided capital and bore most of the downside risk.

Then, in October 1966, came the deal that would define the next two decades of the company's history, for better and for worse. Attorney Bob Troutman offered Cousins the air rights over the Western and Atlantic Railroad yard in downtown Atlanta. The catch was that Cousins had to commit to a five-million-dollar commercial property by year's end to lock in the inexpensive eighty-year lease. It was an enormous gamble for a company that had been building houses just eight years earlier.

Cousins said yes. He built a parking deck designed to support future development above the rail yard. But a parking deck needed a demand driver. And that is how a homebuilder from Georgia ended up in the professional sports business.

In 1968, Cousins purchased the St. Louis Hawks NBA franchise and relocated them to Atlanta, creating the Atlanta Hawks. In 1972, he acquired an NHL expansion franchise, the Atlanta Flames. That same year, on October 14, the Omni Coliseum opened as the home arena for both teams. The seventeen-million-dollar facility was financed entirely with private money, a departure from the publicly subsidized stadium model that was becoming standard across America.

Three years later, in 1975, the broader Omni International Complex opened. Built in conjunction with developer Maurice Alpert, it was a seventy-six-million-dollar mixed-use development featuring office towers, a hotel, upscale restaurants, boutique shops, a movie theater, and an ice-skating rink. It was one of the most ambitious urban mixed-use developments of its era, a prototype for the live-work-play environments that would not become standard for another forty years.

And then it all fell apart.

In March 1978, lender Morgan Guaranty Trust announced plans to foreclose on the Omni International Complex, what was at the time the largest foreclosure in American real estate history. The parking decks never generated enough revenue. Between 1974 and 1977, Cousins lost thirty-three million dollars, wiping out nearly everything the company had earned in its first twelve years of existence. The golden boy of Atlanta real estate was suddenly fighting for survival.

Cousins sold the Hawks in 1977 and the Flames in 1981. He avoided bankruptcy only by convincing creditors to restructure rather than foreclose. It took nearly another decade before he could sell his remaining twenty-five percent interest to Ted Turner, who moved CNN's operations in and renamed the complex CNN Center. Only then did the project turn profitable, but under someone else's ownership.

The Omni experience seared two lessons into the DNA of Cousins Properties. First, leverage kills. Tom Cousins had financed the Omni Complex with the assumption that revenue from multiple streams, sports, hotel, retail, parking, would cover the debt. When several of those streams underperformed simultaneously, there was no margin of safety. Second, the market does not care about your vision if the cash flows do not work. The Omni was architecturally stunning and conceptually ahead of its time, but those qualities meant nothing when the interest payments came due.

What makes this chapter of the story so important is that it did not destroy Tom Cousins. It educated him. He would spend the rest of his career building with far more financial discipline, insisting on conservative debt ratios, joint venture structures that shared risk, and a patient approach to development that prioritized cash-flow stability over grand visions. The Omni was the crucible in which Cousins Properties' identity was forged: ambitious enough to dream big, scarred enough to never bet the company again. Those lessons would ultimately save the company in the next century.

III. The Diversification Era & Going Public (1980s-2000s)

After the Omni catastrophe, a lesser entrepreneur might have retreated into safe, small projects. Cousins did the opposite, but with a critical difference: he became almost pathologically conservative about debt. During the 1970s crisis, the company had retained four hundred acres of land in northern Fulton County in what would become Atlanta's "Golden Corridor," a prescient hold that would become enormously valuable as the metro area expanded northward.

The company's REIT history is more complicated than most. Cousins had formed a separate vehicle called Cousins Mortgage-Equity Investments in 1970, raising 42.5 million dollars when the REIT structure was still new and poorly understood. That vehicle performed disastrously through the 1970s recession, competing poorly against limited partnership tax shelters, and was sold off in 1979. The failed experiment made Cousins wary of the REIT structure for nearly a decade.

Then came the Tax Reform Act of 1986, which eliminated the limited partnership tax shelters that had been sucking capital away from REITs. For non-real-estate investors, a brief explanation: throughout the late 1970s and early 1980s, wealthy individuals had been investing in real estate primarily through limited partnerships that generated paper losses through depreciation deductions, sheltering other income from taxes. The 1986 act eliminated these passive loss deductions, making the limited partnership structure far less attractive. Overnight, the REIT structure, which offered tax-free pass-through of real estate income to shareholders, became the most compelling vehicle for real estate investment. In 1987, Cousins restructured the core company as a real estate investment trust, spinning off management and leasing operations into separate entities. In 1992, the company transferred its listing to the New York Stock Exchange under the ticker CUZ and completed its largest stock offering at the time, netting approximately fifty-eight million dollars. The move to the NYSE was significant: it gave the company access to institutional investors who could not or would not trade on smaller exchanges, expanding the pool of potential shareholders and improving stock liquidity.

The 1982 development of Wildwood Office Park marked the company's modern era in office real estate. A partnership with IBM as anchor tenant and deep-pocketed co-investors including Coca-Cola and NationsBank, the project proved that Cousins could execute large-scale office development. And because Cousins avoided speculative building throughout the 1980s, the company entered the early 1990s real estate recession in remarkably strong shape, holding just one million dollars in debt while competitors were drowning.

Daniel DuPree joined the picture through Cousins' 1992 acquisition of New Market Development Company, which DuPree had founded. New Market had pioneered the "power center" retail concept, shopping centers anchored by big-box retailers like Home Depot and Circuit City. DuPree became President and COO, and under his leadership, Cousins delivered twenty-one percent annualized shareholder returns over five years. He resigned in 2001, citing burnout after "twenty nonstop years" in real estate.

Through the 1990s and early 2000s, Cousins expanded geographically beyond Atlanta into Charlotte, Birmingham, Washington D.C., California, and Dallas, the last through a 1999 joint venture with R. Dary Stone. By 2003, the portfolio included thirty-seven commercial office properties spanning over thirteen million square feet, seven medical office buildings, twelve retail properties, and more than two hundred eighty acres of undeveloped Atlanta land. Revenue had reached 314.8 million dollars with 421 employees.

The company was developing and owning landmark properties that defined the Atlanta skyline. Its portfolio included 191 Peachtree Tower, a forty-story Midtown landmark that would eventually become the company's headquarters; the Pinnacle Building in Buckhead; Bank of America Plaza, the tallest skyscraper in the Southeast; and involvement with the Georgia World Congress Center, the fourth-largest convention center in the country. The developer-operator hybrid model, building properties and retaining ownership, meant Cousins captured value at every stage of the real estate lifecycle: land acquisition, entitlement, construction, lease-up, and long-term operations. This vertical integration gave the company deep expertise across the full spectrum of real estate skills, a knowledge base that would prove invaluable when the company eventually needed to reposition itself in a new strategic direction.

But there was a problem, and it was getting worse every year. The REIT market was becoming increasingly specialized. Investors wanted pure-play vehicles: apartment REITs, industrial REITs, retail REITs, office REITs. Cousins' diversified portfolio, spanning office, retail, medical office, residential land, and mixed-use projects, was getting dinged with what analysts call the "conglomerate discount." Wall Street was essentially telling Cousins that its whole was worth less than the sum of its parts. The question was not whether to simplify but when and how.

For long-term investors, this is one of the most underappreciated dynamics in REIT investing. A diversified portfolio might actually reduce risk in fundamental terms, the same way a conglomerate like General Electric once argued that its breadth provided stability. But if the market will not reward that diversification, if Wall Street persistently applies a discount to the sum-of-the-parts value because it cannot neatly categorize the company, then the rational move is to simplify, even if it means abandoning assets and strategies that define your identity. The conglomerate discount in REITs is particularly punishing because the dividend-dependent investor base demands clarity: they want to know whether they are buying office, retail, or residential exposure, and they will not pay full price for a company that muddies those categories. Cousins was about to learn that lesson the hard way, and then execute on it with remarkable discipline.

IV. The Great Simplification: Shedding Non-Core Assets (2000s-2010)

The strategic inflection point arrived gradually and then all at once. Tom Cousins, approaching his seventies, began planning for succession. In early 2002, he elevated Thomas D. Bell Jr. to President and CEO. Bell was an unusual choice: a former CEO of the advertising giant Young & Rubicam, he had limited real estate experience but strong organizational management credentials. He had joined the Cousins board in 2000 at age fifty-two. Tom Cousins retained the chairmanship, creating a dual-leadership structure that would govern the most consequential period of asset sales in the company's history.

Between 2003 and 2006, Cousins executed what amounted to a controlled liquidation of its most valuable assets. The company sold equity in thirty-five projects, generating 2.7 billion dollars in proceeds. To put that number in context, the entire company's equity market capitalization at the time was a fraction of the value being harvested. These were not fire sales. They were precisely timed transactions at peak valuations, executed with the kind of patience that only a founder with five decades of experience could enforce. The commercial real estate market in the mid-2000s was awash in cheap debt, as securitization and loose lending standards enabled buyers to pay premium prices for income-producing properties. Cousins was a willing seller.

The marquee transaction came in 2006 when Cousins sold Bank of America Plaza for approximately 436 million dollars, or 348 dollars per square foot, an Atlanta record. At 1,023 feet, the tallest building in the southeastern United States, it was the most visible symbol of Cousins' ambitions. Also sold was Frost Bank Tower in Austin, a thirty-three-story landmark that fetched 188 million dollars, another market record. The company used proceeds to fund the acquisition of the Gellerstedt Group, a multifamily development firm, signaling that it was thinking about portfolio recomposition rather than simple harvesting.

Inside the company, these sales generated genuine anguish. These were not just buildings; they were monuments to what Tom Cousins had built. Selling Bank of America Plaza was like selling the family crest. But the math was clear: the assets were trading at peak valuations, the company's diversified structure was depressing its stock price, and the capital could be redeployed more effectively.

Tom Cousins retired as chairman in December 2006 at age seventy-five. The timing was, in hindsight, almost supernaturally good. Within months, the credit markets that had fueled the commercial real estate boom began seizing up. The buyer of Bank of America Plaza, BentleyForbes, would eventually lose the building to receivership, with the property selling in 2012 for just 235 million dollars, less than fifty-five cents on the dollar of what Cousins had received. Atlanta's priciest repo, the press called it.

The internal debates during this period were fierce, and they touched on questions of identity that go deeper than financial engineering. Was the company abandoning Tom Cousins' vision of integrated, mixed-use urban development, the same vision that had driven the Omni Complex and the Wildwood Office Park and dozens of projects across three decades? Or was it finally maturing into something the capital markets could properly value? The answer, uncomfortably, was both. The vision was not wrong, but the corporate structure was. A public REIT needed clarity and focus, not a grab bag of assets across multiple property types.

What emerged from this period was the beginning of a thesis that would take another decade to fully crystallize: Sun Belt office. The logic started with demographics. Atlanta, Austin, Dallas, Charlotte, Phoenix, and Tampa were all growing faster than the national average, fueled by corporate relocations, lower costs of living, business-friendly tax environments, and warmer weather. These cities were becoming knowledge economy hubs, attracting the tech workers, consultants, and financial professionals who occupied Class A office space. If you could own the best office buildings in these specific markets, you would be positioned on the right side of one of the most powerful demographic trends in American history.

But the company was not yet fully focused. The portfolio still contained retail properties, residential land, medical office buildings, and third-party management contracts. The full simplification would take years longer, interrupted by the worst financial crisis since the Great Depression.

V. The Financial Crisis & Leadership Transition (2007-2010)

When the music stopped in 2007 and 2008, Cousins Properties was in a peculiar position. The massive asset sales of 2003 through 2006 had generated billions in proceeds, but the company had also reinvested into new projects, including residential land and a condominium development called 10 Terminus Place in Atlanta. As credit markets froze and real estate values collapsed, those reinvestments turned toxic.

The company recorded impairment charges on residential land holdings and the condominium project. A mezzanine loan to an Asheville, North Carolina condominium developer defaulted. The company took a staggering 126-million-dollar charge to write down its land portfolio as part of a strategic decision to exit land development entirely. The stock, which had hit an all-time high of 56.40 dollars in February 2007, plummeted.

The leadership vacuum became acute. Thomas Bell, the CEO who had overseen the 2003-2006 sales, was not the right person to navigate a crisis of this magnitude. In June 2009, the board turned to Larry L. Gellerstedt III, a real estate veteran who would prove to be the transformative leader the company needed.

Gellerstedt was a particularly interesting choice. A graduate of Princeton and Harvard Business School, he had spent his career in Atlanta real estate, running the Beers Construction division of Holder Construction Group before founding his own development firm, the Gellerstedt Group, which Cousins had acquired in 2006. He understood construction economics from the ground up, literally, and he had the kind of relationship network in Atlanta's business community that could open doors to capital, tenants, and deals. He was not a financial engineer or a Wall Street transplant. He was a builder who understood numbers, and that combination would prove essential.

Gellerstedt arrived at a company that Colin Connolly, who would later succeed him as CEO, later described as "over-levered and subscale." The balance sheet needed repair. The portfolio lacked focus. And the commercial real estate market was as hostile as anyone could remember. Gellerstedt laid out four priorities with military precision: first, focus on core operations driving revenue, meaning lease vacant space and generate management fees; second, strengthen the balance sheet; third, monetize non-core assets prudently; and fourth, invest capital opportunistically when the right moment arrived.

The first three priorities were about survival. The fourth was about offense. And Gellerstedt understood that the crisis, as devastating as it was, represented the greatest buying opportunity in a generation. The question was whether Cousins could get healthy fast enough to exploit it.

Between 2009 and 2011, the company systematically shed everything that was not Sun Belt office. It sold its third-party client services business, encompassing leasing, property management, and project management for other office owners, to Cushman and Wakefield in 2012. It sold retail properties, including five Publix-anchored shopping centers for 79.5 million dollars in 2014, completing its full exit from retail ownership. It reduced land holdings by hundreds of acres. Each divestiture made the company smaller but more focused, and each freed up capital for the coming offensive.

Meanwhile, the financial crisis was creating distress across commercial real estate. Trophy office buildings that had traded at premium valuations just two years earlier were now available at deep discounts. Institutional sellers, facing their own liquidity crises, were desperate to move assets. For a company with Gellerstedt's discipline and Cousins' institutional relationships, it was the setup for a generational trade.

The crisis also forged what the company would later call its "balance sheet fortress" mentality. Having lived through the Omni disaster of the 1970s and the financial crisis of 2008-2009, Cousins' management team developed an almost religious commitment to conservative leverage. Think of it this way: in real estate, there are two kinds of companies. There are companies that borrow aggressively during good times, generating impressive returns on equity when markets are rising, but finding themselves forced sellers when the cycle turns. And there are companies that borrow conservatively, accepting lower returns during boom times but maintaining the liquidity and flexibility to be buyers when everyone else is selling. Cousins had been the first kind of company during the Omni era. After the financial crisis, it was emphatically the second. This would become a defining competitive advantage: when others were scrambling for liquidity, Cousins would be buying.

VI. The Rebuilding: Acquiring the Trophy Portfolio (2011-2014)

Walk into the lobby of Promenade II in Midtown Atlanta today and you are standing in the first building of a remarkable portfolio reconstruction. But in the fall of 2011, when a thirty-something former Morgan Stanley executive named Colin Connolly joined Cousins Properties as Senior Vice President focused on acquisitions and dispositions, the building belonged to someone else and the company's future was far from certain. Connolly had spent his early career in investment banking and real estate private equity, giving him both the financial rigor to evaluate complex transactions and the deal instincts to act quickly when opportunities emerged. His arrival marked the beginning of the most aggressive and disciplined acquisition campaign in the company's history. Over the next three years, Cousins would invest roughly 2.4 billion dollars in trophy office assets, transforming itself from a depleted post-crisis survivor into a major Sun Belt office landlord.

The first move came in November 2011 when Cousins acquired Promenade II, a thirty-eight-story Midtown Atlanta office tower, for 134.7 million dollars, or about 174 dollars per square foot. The seller was Beacon Capital Partners, which had acquired the building from Australian firm Charter Hall. The price was deeply discounted from pre-crisis levels, reflecting both the depressed market and the seller's need for liquidity.

Then, in February 2013, Cousins executed a pair of transactions that signaled much larger ambitions. It acquired Post Oak Central, a 1.3-million-square-foot Houston office complex, for 232.6 million dollars, entering the Houston market for the first time. Simultaneously, it formed a fifty-fifty joint venture with institutional investors advised by J.P. Morgan Asset Management for the Terminus office towers in Buckhead, Atlanta, a pair of high-rises totaling 1.2 million square feet that had become among the most prestigious office addresses in the Southeast.

But the defining transaction came in September 2013 when Cousins announced the acquisition of Greenway Plaza and 777 Main Street from Crescent Real Estate Holdings for approximately 1.1 billion dollars. It was the single largest acquisition in the company's history and the kind of deal that changes the strategic trajectory of an organization permanently.

Greenway Plaza was a ten-building, 4.4-million-square-foot Houston office campus that functioned almost like a self-contained city: restaurants, a health club, banking services, and conference facilities, all anchored by blue-chip tenants including Occidental Oil and Gas, Transocean, and Invesco. At ninety-two percent occupied, it generated stable, predictable cash flows from tenants with strong credit profiles. The deal also included 777 Main Street, a 980,000-square-foot Class A tower in Fort Worth. Management described it as a "transformative acquisition," funded through common stock issuance and non-core asset sales, a structure that avoided the balance sheet strain of debt financing while diluting existing shareholders only at what Gellerstedt believed was an attractive share price.

The strategic logic was compelling. Cousins was acquiring institutional-quality office assets at post-crisis valuations, funded largely by selling non-core assets at reasonable prices. The company was essentially arbitraging the gap between the low prices of premium office buildings in distressed markets and the steadier values of its non-office assets. Connolly, promoted to Chief Investment Officer in May 2013, was the architect of this strategy.

Within just two years, Cousins had gone from subscale and over-levered to owning a trophy portfolio across multiple Sun Belt markets. The acquisitions also brought something less tangible but equally valuable: credibility. Institutional investors and brokers now saw Cousins as a serious, well-capitalized buyer in Sun Belt office. That reputation would pay dividends for years to come.

There was also discipline in what the company did not buy. For every acquisition it closed, Cousins passed on dozens of opportunities that did not meet its quality or location criteria. Suburban office parks, no matter how cheap, did not make the cut. Secondary Sun Belt markets with less compelling growth dynamics were also excluded. The framework was crystallizing: buy premium assets in premium locations within high-growth Sun Belt markets. Everything else was a distraction. This discipline is easy to describe but extraordinarily difficult to practice when competitors are closing deals and the market is rewarding growth. Cousins' willingness to walk away from transactions that did not meet its quality threshold would prove to be as important as the deals it closed.

For investors watching the story unfold, the 2011-2014 period represents a case study in contrarian capital allocation. While most real estate investors were still licking their wounds from the financial crisis, Cousins was building a portfolio of assets that would generate superior returns for the next decade. The courage to buy when others are selling is easy to celebrate in hindsight but agonizing to execute in real time.

VII. Crystallizing the Sun Belt Thesis (2013-2018)

By 2014, Cousins Properties had assembled a formidable portfolio of Sun Belt office assets, but the thesis was not yet pure. The Houston exposure, acquired at bargain prices, became problematic when oil prices collapsed in 2014 and 2015, dragging the energy-dependent market into recession. It was a reminder that not all Sun Belt cities are created equal, and that the specific economic drivers of each market matter enormously.

The company continued pruning. In 2014, it sold 777 Main Street in Fort Worth for 167 million dollars, just a year after acquiring it as part of the Greenway deal, crystallizing a quick gain. The 844,000-square-foot office tower at 2100 Ross in Dallas went for 131 million dollars in 2015. Each sale sharpened the focus on a smaller number of higher-conviction markets.

It was around this time that the concept of "eighteen-hour cities" entered the real estate lexicon. The idea was that certain Sun Belt metros, while not global financial capitals like New York or London, had developed enough economic diversity, cultural amenities, and quality of life to attract young, educated workers who increasingly valued lifestyle alongside career opportunity. Atlanta, Austin, Charlotte, Nashville, and a handful of others fit this description. Cousins had been investing in these markets before the concept had a name.

The development strategy evolved alongside the acquisitions. Rather than simply buying existing buildings, Cousins began selectively developing Class A-plus office space in supply-constrained urban nodes where zoning, entitlement, and construction complexity created natural barriers to competition. The buildings themselves evolved too. The standard corporate office box gave way to amenity-rich environments with ground-floor retail, outdoor terraces, fitness centers, and transit access. These were not just workplaces; they were destinations, designed to compete for the best tenants against both other landlords and the growing allure of remote work.

Then came the move that would truly transform the company's scale. On April 29, 2016, Cousins announced a stock-for-stock merger with Parkway Properties valued at approximately 1.95 billion dollars. But the deal had a twist that revealed the sophistication of Cousins' strategic thinking: simultaneously with the merger, the combined company would spin off all Houston-based assets from both portfolios into a new publicly traded REIT called Parkway, Inc.

The logic was elegant, and it deserves a moment of appreciation for its strategic ingenuity. Cousins wanted Parkway's strong Buckhead Atlanta portfolio, including five major assets totaling three million square feet alongside properties like 3344 Peachtree and Tower Place 200, plus its Tampa and Orlando properties. But it absolutely did not want deeper Houston exposure at a time when the energy sector's collapse had cratered that market's office fundamentals. Oil had fallen from over one hundred dollars per barrel in mid-2014 to under thirty dollars by early 2016, and Houston office vacancy was climbing toward record levels. The spinoff solved both problems. Cousins shareholders received fifty-two percent of the new Houston REIT, capturing any eventual recovery, while the core Cousins entity shed its Houston risk entirely. The new Houston company was later acquired by the Canada Pension Plan Investment Board in 2017, providing a clean exit.

Post-merger, Cousins operated forty-one properties spanning 15.8 million square feet across Atlanta, Austin, Charlotte, Phoenix, Orlando, and Tampa, with average in-place rents of approximately thirty-one dollars per square foot. The integration succeeded both operationally and strategically, generating eighteen million dollars in annual cost savings, exceeding initial projections, and creating the platform that would support the next wave of growth. The property management teams were consolidated, back-office functions were streamlined, and the combined leasing operation benefited from a larger inventory of available spaces to match against tenant requirements. For investors, the Parkway merger was a template for how REIT consolidation should work: geographic alignment, cost synergies, strategic pruning of non-core assets, and an accretive combination that made the whole more valuable than the sum of its parts.

Larry Gellerstedt, who had led the company through its post-crisis transformation, was elevated to Chairman in July 2017, capping nearly a decade of value creation that had grown Cousins' equity market capitalization from roughly 665 million dollars to over 3.4 billion dollars. The leadership transition plan called for Colin Connolly to take over as CEO effective January 1, 2019, ensuring continuity of the strategic vision.

For Sun Belt office believers, the 2016-2018 period was when the thesis moved from contrarian to consensus. Population data confirmed what Cousins had bet on: the top ten destinations for absolute population growth were all Sun Belt metros. Texas alone was adding over half a million residents per year. Corporate headquarters relocations from coastal gateway cities to Sun Belt metros accelerated, with Dallas-Fort Worth and Austin consistently ranking as the top destinations. Tech companies, in particular, were establishing major offices in Austin, Atlanta, and Charlotte, bringing precisely the kind of high-wage knowledge workers who occupied premium office space.

VIII. The TIER Acquisition & Scale (2019)

Colin Connolly's first major move as CEO came just months into his tenure. On March 25, 2019, Cousins announced an all-stock merger with TIER REIT that would create a combined company with an equity market capitalization of roughly 5.9 billion dollars and a total enterprise value of approximately 7.8 billion dollars. The deal, which closed on June 14, 2019, valued TIER at approximately 1.7 billion dollars, with TIER shareholders receiving 2.98 Cousins shares for each TIER share.

The strategic rationale centered on portfolio fit, and the numbers were unusually clean for a REIT merger. TIER's holdings were concentrated in Austin and Dallas, two of the fastest-growing office markets in the country. A remarkable eighty-one percent of the two portfolios overlapped geographically, meaning the merger deepened Cousins' presence in existing markets rather than diluting the thesis with new geographies. This is the opposite of what happens in most real estate mergers, where the acquirer ends up with properties in markets it does not know and does not want. Major tenants in the combined portfolio included Facebook and Amazon, reflecting the growing tech presence in Sun Belt cities and providing exactly the kind of credit-quality tenancy that attracts institutional capital.

Connolly had joined Cousins in 2011 as a deal-maker, and the TIER acquisition bore his fingerprints: precise geographic fit, institutional-quality assets, and a deal structure that avoided dilutive cash payments. The merged company called itself "the preeminent Sun Belt office REIT," and the label was not marketing hyperbole. The combined portfolio of trophy office properties across Atlanta, Austin, Charlotte, Dallas, Phoenix, and Tampa was unmatched in its Sun Belt focus and quality.

Following the merger, the company optimized aggressively. Non-core suburban assets from the TIER portfolio were identified for disposition. The capital allocation framework that had emerged over the preceding decade was now explicit and disciplined: buy or build Class A-plus quality assets in urban or mixed-use locations within core Sun Belt markets, sell everything else.

This is when the company coined the term "lifestyle office" to describe its target, and the branding was more than marketing. It reflected a genuine strategic insight about where office real estate was heading. The best office buildings of the 2020s would not compete merely on location and price per square foot. They would compete on experience: ground-floor restaurants, rooftop terraces, state-of-the-art fitness centers, bicycle storage, EV charging, walkable access to transit and entertainment. These amenities mattered because tenants were using their office spaces as recruiting tools. A twenty-five-year-old software engineer choosing between job offers would visit the office, and the building with the better vibe would tip the scale. Cousins understood this dynamic early, and "lifestyle office" became shorthand for buildings designed to win that competition.

In 2019, Cousins also bought out J.P. Morgan's fifty percent stake in the Terminus towers for an implied total valuation of 503 million dollars, gaining full ownership of two of Buckhead's most prestigious office addresses. It was the final piece of the Atlanta trophy puzzle.

By the end of 2019, the company had achieved something remarkable: a portfolio of pure Sun Belt trophy office assets, a fortress balance sheet, an investment-grade credit rating achieved for the first time, a seasoned management team, and a clear strategic identity that Wall Street could understand and value. The timing was impeccable in every way except one: a novel coronavirus was about to make the entire concept of office work a matter of existential debate.

IX. COVID-19, Remote Work & The Great Office Reckoning (2020-2022)

In March 2020, office buildings across America emptied almost overnight. Cousins Properties' portfolio went from full to roughly twenty percent physical occupancy as companies sent employees home. For a company that had spent the better part of a decade positioning itself as the definitive Sun Belt office landlord, the pandemic was not just a financial crisis. It was a philosophical one. If people could work from home just as effectively, what was the point of a twenty-million-square-foot office portfolio?

The months that followed were among the most psychologically demanding in the company's history. Every business news outlet ran headlines about the death of office real estate. REIT share prices cratered. Analysts downgraded the entire sector. Social media was filled with predictions that employees would never return to offices. For a management team that had spent a decade building the purest expression of Sun Belt office conviction in the public markets, the temptation to hedge, to diversify, to signal doubt, must have been immense.

But the first thing that happened was that rent kept coming in. Cousins collected 98.7 percent of rent from office tenants in the third quarter of 2020, a figure that would have been unthinkable for many property types. The reason was structural: Cousins' tenants were predominantly large, well-capitalized corporations, the kind of companies that were going to survive a pandemic and honor their lease obligations regardless of whether employees were in the building. Long-term leases, often spanning five to ten years, provided contractual stability even as physical occupancy cratered.

The second thing that happened, more slowly but more consequentially, was that the pandemic accelerated trends that were already underway. Flight to quality, the tendency of tenants to upgrade their office space when they signed new leases, had been building for years. COVID supercharged it. Companies that might have renewed in their existing Class B space instead decided that if they were going to ask employees to come back to the office, the office needed to be worth coming back to. That meant newer buildings, better amenities, walkable neighborhoods, and modern air handling systems. It meant exactly the kind of buildings Cousins owned.

The data that emerged over the following two years told a remarkably clear story. Sun Belt markets outperformed gateway cities on virtually every measure of office recovery. Return-to-office rates were consistently higher in Atlanta, Austin, Dallas, and Charlotte than in New York, San Francisco, or Chicago. Corporate tenants continued migrating south and west, attracted by lower costs, warmer weather, and states without income taxes. And within each market, Class A trophy assets dramatically outperformed Class B and C buildings, which saw vacancy rates spiral into the twenties and thirties.

Cousins' response during this period was notable for what it did not do, and in the REIT world, what you do not do during a crisis is often more consequential than what you do. Management did not panic-sell trophy assets at depressed prices, as some competitors were forced to do by covenant violations or liquidity shortfalls. They did not slash the dividend disproportionately, which would have signaled desperation to the market. They did not abandon their development pipeline or retreat from their Sun Belt markets. Instead, they leaned into the thesis, maintaining over one billion dollars in available liquidity and continuing to invest in amenity upgrades, building technology, and tenant experience. The company committed 900 thousand dollars from its nonprofit foundation for COVID-19 relief and social justice organizations, reinforcing tenant relationships during a period of social upheaval.

Leasing activity slowed during the summer of 2020, particularly as COVID case counts spiked in Sun Belt states, but recovered after Labor Day with increased leasing tours. The hybrid work model that emerged, with most companies settling on three days in the office, actually reinforced the premium office thesis: if you only had to go to the office three days a week, you wanted those three days to be in a building that felt like a destination, not a cubicle farm.

By 2022, the contours of the "new normal" for office were becoming clear. Overall office demand was structurally lower than pre-pandemic levels, with national vacancy hovering around fifteen percent and sublease space, which represents tenants trying to offload space they no longer need, reaching record highs in cities like San Francisco and Manhattan. But the distribution was highly bifurcated. Premium assets in growth markets held occupancy and grew rents. Commodity office in saturated markets faced existential vacancy. Older Class B and C buildings in markets like downtown Chicago, parts of Los Angeles, and the outer boroughs of New York were seeing vacancy rates above twenty-five percent, with some approaching functional obsolescence.

Cousins was on the right side of that divide, and the gap was widening. The concept of "office bifurcation" became the defining narrative of post-COVID commercial real estate, and it validated the strategic bet Cousins had been making for over a decade: that owning the best buildings in the best locations in the best-growing markets would provide durable competitive advantages regardless of what happened to the broader office sector.

There is an important myth-versus-reality dynamic worth addressing here. The consensus narrative that emerged during 2020 and 2021 was that "office is dead." This was, to put it bluntly, wrong, or at least wildly overgeneralized. What actually happened was far more nuanced: commodity office in oversupplied markets with declining populations suffered genuine, potentially permanent damage. But premium office in growth markets with diversifying economies experienced a temporary disruption followed by a gradual but unmistakable recovery. The problem with the "office is dead" narrative was that it treated a highly heterogeneous asset class as monolithic. Saying "office is dead" because San Francisco vacancy hit record highs was like saying "retail is dead" because a strip mall in rural Ohio lost its anchor tenant. The truth was always more complex, and Cousins' portfolio was always on the right side of that complexity.

The experience also revealed the durability of the Sun Belt thesis. Companies were not just staying in Sun Belt markets; they were doubling down. Major tech firms expanded in Austin. Financial services companies built out in Charlotte. Corporate headquarters continued relocating from the coasts. The pandemic had not killed the Sun Belt migration; it had accelerated it, as remote work freed individuals and companies to choose locations based on quality of life and cost rather than proximity to a specific office tower.

X. The Modern Era: AI, Acquisitions & Sun Belt 2.0 (2022-Present)

The post-COVID trajectory for Cousins Properties has been defined by a paradox: the company's fundamentals have steadily improved while its stock price has languished, weighed down by the market's broad skepticism toward all things office. This disconnect has created what management views as a generational opportunity to acquire premium assets at prices that would have been unthinkable before the pandemic.

The numbers tell the story of operational recovery. Funds from operations per share bottomed at 2.62 dollars in 2023 and climbed to 2.84 dollars in 2025, with guidance for 2026 calling for a midpoint of 2.92 dollars. Occupancy rose from 87.6 percent at the end of 2023 to 89.2 percent at the end of 2024 and reached 90.7 percent leased by the fourth quarter of 2025. The company has now posted forty-seven consecutive quarters of positive second-generation cash rent roll-ups, meaning that every time a lease expires and is renewed or re-leased, the new rent is higher than the old rent. That streak spans more than a decade.

Leasing momentum has accelerated meaningfully. Full-year 2025 saw 2.1 million square feet signed, the highest volume since 2019, with the fourth quarter alone accounting for 700,000 square feet across thirty-nine leases, the second-highest quarterly volume in four years. The weighted average lease term was a robust 9.6 years, suggesting tenants are making long-term commitments rather than hedging with short-term extensions. This is a critical data point: if companies were genuinely planning to reduce their office footprint permanently, they would be signing shorter leases to preserve flexibility. Instead, nearly ten-year average terms suggest that for the kinds of tenants Cousins attracts, office space remains a core strategic commitment.

The dividend, currently 1.28 dollars per share annually paid in quarterly installments of thirty-two cents, provides a yield of roughly five and a half percent at recent prices. For a REIT with investment-grade credit, growing FFO, and rising occupancy, that yield represents a meaningful income stream while investors wait for the market to re-rate office real estate.

But it is the acquisition activity that truly defines the current era. Cousins embarked on what can only be described as a billion-dollar shopping spree in late 2024 and 2025, taking advantage of distress in the office market to acquire trophy assets at compelling prices. The headline deal was Sail Tower in downtown Austin, an 804,000-square-foot, thirty-five-story LEED Platinum tower acquired for 521.8 million dollars in December 2024. The building is fully leased to Google through 2038, providing investment-grade credit cash flows for over a decade. Google, which had held the lease since the building's completion in 2022 but left it dark for years, finally activated the space in January 2026.

In the same quarter, Cousins acquired Vantage South End, a two-building lifestyle office campus in Charlotte, for 328.5 million dollars. Combined with the Sail Tower deal, the company invested nearly one billion dollars in a single quarter, one of the most productive periods in its history. The acquisitions continued into 2025 with The Link in Uptown Dallas for 218 million dollars in July and 300 South Tryon in Charlotte's Uptown submarket for 317.5 million dollars later in the year.

In total, since 2019, Cousins has invested 2.3 billion dollars in lifestyle office acquisitions, funded by a combination of non-core asset sales, debt issuance, and operating cash flow. The company has raised 1.9 billion dollars in public debt since achieving its investment-grade credit rating. In February 2026, the board authorized a 250-million-dollar share repurchase program, signaling confidence that the stock is undervalued relative to the underlying asset base.

The AI boom has added an unexpected and potentially transformative tailwind. The explosion of artificial intelligence development since late 2022 has triggered a wave of hiring and expansion by technology companies that directly contradicts the "office is dead" narrative. AI development is fundamentally collaborative: models need to be trained, tested, and refined by teams of researchers and engineers working in close physical proximity, sharing whiteboards and GPU clusters and debugging sessions. Remote work for AI teams has proven less effective than for many other tech functions, and companies have responded by securing or expanding physical office space.

Google's decision to finally occupy Sail Tower in Austin is emblematic of this trend. The company held the lease since 2022 but left the building dark during the period of maximum uncertainty about office demand. The activation in January 2026 reflected a corporate decision that physical presence in Austin was essential for the next phase of AI development. Similarly, Amazon signed a full-building lease at Domain 9 in Austin, committing to 330,000 square feet. These are not companies retrenching from office space; they are doubling down, and they are doing it in exactly the markets where Cousins operates.

The competitive landscape has shifted meaningfully. Private equity firms and foreign capital, drawn by the same Sun Belt thesis that Cousins pioneered, are now bidding aggressively for premium office assets in Atlanta, Austin, and Charlotte. Other public REITs, including Highwoods Properties and Piedmont Office Realty Trust, compete directly in several markets. But Cousins' combination of scale, balance sheet strength, and long-standing market relationships, particularly in Austin and Atlanta where it commands outsized portfolio positions, provides durable competitive advantages.

The current portfolio reflects the culmination of decades of strategic refinement. Austin accounts for roughly thirty-six percent of net operating income, Atlanta thirty-one and a half percent, with the remainder split across Charlotte, Tampa, Phoenix, and the newly entered Dallas market. The geographic concentration is deliberate: rather than spreading thin across a dozen Sun Belt cities, Cousins has built depth in a handful of markets where it understands the submarket dynamics, tenant base, and competitive landscape intimately.

The Domain campus in Austin exemplifies the company's approach. Spanning 2.5 million square feet across multiple buildings, the campus is over ninety-nine percent leased to a tenant roster that includes some of the most important technology companies in the world. The adjacent mixed-use environment, with hundreds of shops, restaurants, and residential units, creates an ecosystem that attracts employers and employees alike. Amazon's full-building lease at Domain 9, signed in 2022, validated the thesis that even the largest tech companies would commit to long-term leases in these kinds of environments.

In Nashville, Cousins entered through a fifty-fifty joint venture with J.P. Morgan on the Neuhoff development, a 275-million-dollar mixed-use project that integrates 234,000 square feet of office space with a 319-unit apartment complex and 24,000 square feet of retail. It represents a return to the kind of integrated development that Tom Cousins pioneered with the Omni, but executed with far more financial discipline and in a market with vastly better growth dynamics.

The development pipeline remains intentionally lean, with approximately fifty million dollars in estimated remaining costs. The Norfolk Southern headquarters project in Atlanta, a 750,000-square-foot development with total project costs of approximately 575 million dollars, represents the company's largest active development commitment, anchored by the railroad's decision to consolidate its corporate operations in Midtown Atlanta.

The passing of Tom Cousins on July 29, 2025, at age ninety-three, marked the end of a direct connection to the company's founding era. His philanthropy in his later years was extraordinary: he donated over 200 million dollars to revitalize the East Lake neighborhood in Atlanta, transforming a crime-ridden public housing project into a nationally recognized model of urban renewal. The Cousins Foundation's work demonstrated the same conviction and long-term thinking that had characterized his approach to business. The principles he established after the Omni crisis, conservative leverage, relationship-first business culture, and long-term thinking, are woven into the fabric of how the company operates today.

XI. Business Model Deep Dive & Competitive Moats

To understand Cousins Properties, you need to understand how a REIT actually makes money and why the office REIT model is both more complex and more fragile than most investors appreciate.

A REIT is, at its core, a tax-efficient pass-through vehicle for real estate income. In exchange for distributing at least ninety percent of taxable income to shareholders as dividends, the company pays no corporate income tax. This is a genuine structural advantage, but it comes with constraints: the company cannot hoard cash the way a typical corporation can, which means capital allocation decisions around development, acquisitions, and debt are unusually consequential. Every dollar reinvested in a building is a dollar not distributed to shareholders.

Office REIT economics revolve around a few key metrics. Net operating income, or NOI, is the rental revenue minus property-level operating expenses. For a well-run trophy office portfolio, NOI margins typically range from sixty to seventy percent, reflecting the relatively low marginal cost of operating a building once it is leased. The capitalization rate, or cap rate, is the ratio of NOI to property value, and it functions as the inverse of a price-to-earnings ratio. When cap rates compress, meaning investors are willing to accept lower yields, property values increase. When they expand, values decline.

Cousins' operating model is distinctive in that it integrates development, property management, and leasing under a single corporate umbrella. Many office landlords outsource property management to third-party firms. Cousins manages its buildings directly, which provides better control over tenant experience, operating costs, and building quality. The development capability, honed over decades of building in Sun Belt markets, allows the company to create assets that would otherwise be unavailable in the acquisition market. When Cousins develops a building from scratch, it can customize the design, amenity package, and location to its exact specifications, producing assets that command premium rents.

The Sun Belt advantage operates on multiple levels, and each one reinforces the others.

Construction costs are meaningfully lower than in gateway cities like New York or San Francisco, improving development yields. A building that costs 500 dollars per square foot to construct in Austin might cost 800 or more in Manhattan, for comparable quality.

Business-friendly regulatory environments reduce entitlement timelines and compliance costs. Getting a building permitted in Atlanta takes a fraction of the time required in San Francisco, where environmental review, community input, and political negotiation can add years to a project timeline.

Population tailwinds create organic demand growth that does not depend on stealing tenants from competitors. When a market is adding people and businesses, the total demand for office space grows, creating a rising tide that benefits all landlords but especially those with the best buildings.

And the absence of state income taxes in Texas and Florida serves as a powerful recruiting tool for corporate tenants looking to attract and retain talent. A software engineer earning 200,000 dollars keeps significantly more of that income in Austin than in San Francisco, and employers who locate in no-income-tax states can effectively offer higher after-tax compensation without increasing their payroll costs.

Perhaps the most important but least quantifiable moat is relationship capital. In commercial real estate, deals happen through relationships, not algorithms. Cousins' decades-long presence in Atlanta, its expanding networks in Austin and Charlotte, and its reputation for being a reliable, high-quality operator create informational advantages that are difficult for newcomers to replicate. Brokers bring their best tenants to landlords they trust. Municipalities work more collaboratively with developers who have track records in their communities. And tenants who have had good experiences are more likely to renew.

The replacement cost dynamic is also worth understanding, because it is one of the most important structural advantages in Cousins' favor right now. Think of it like the housing market: when it costs more to build a new house than to buy an existing one, existing homeowners benefit from reduced competition and supported values. The same principle applies to office buildings, but at much larger scale. When construction costs rise, as they have dramatically since 2020 due to labor shortages, supply chain disruptions, and higher materials costs, the cost of building a new office building increases relative to the price of acquiring an existing one. Cousins has explicitly cited this dynamic, noting that its recent acquisitions, including Sail Tower in Austin and 300 South Tryon in Charlotte, were made at prices well below replacement cost. In other words, it would cost significantly more to build these buildings from scratch than Cousins paid to acquire them. That pricing gap provides both a margin of safety on the investment and a competitive moat: potential competitors would need to spend more to create an equivalent asset, making it harder for new supply to enter the market and compete for tenants.

One material accounting consideration that investors should note is that Cousins, like all REITs, carries its properties on the balance sheet at historical cost less depreciation, not at fair market value. This means the book value of the portfolio may significantly understate or overstate the actual market value of the underlying real estate, depending on when assets were acquired and how market conditions have changed. Analysts typically use a net asset value, or NAV, approach to estimate the market value of REIT portfolios, and Cousins has consistently traded at a discount to consensus NAV estimates in recent years, reflecting the market's skepticism toward office real estate broadly rather than concerns specific to Cousins' assets.

XII. Competitive Analysis: Porter's Five Forces

Threat of New Entrants: Medium-High. Building a Sun Belt office portfolio requires significant capital, but capital is available to well-funded competitors, and the barriers to entering these markets are not insurmountable. What is harder to replicate is the local market knowledge, entitlement expertise, and tenant relationships that Cousins has accumulated over decades. A private equity firm can write a check for a billion dollars, but it cannot overnight build the institutional knowledge of which Austin submarket will attract the next wave of tech tenants or which Charlotte zoning board members will support a specific project.

Bargaining Power of Suppliers: Low-Medium. The primary inputs to an office REIT are construction labor and materials, capital, and land. Construction costs have been volatile, but Cousins' scale provides some negotiating leverage with general contractors. Capital markets access, the ability to issue debt and equity at favorable terms, is a genuine competitive advantage: Cousins' investment-grade rating allows it to borrow at lower rates than smaller or lower-rated competitors.

Bargaining Power of Buyers (Tenants): Medium-High. Large corporate tenants, the kind that sign 100,000-square-foot-plus leases, have significant leverage in negotiations. They can choose among multiple landlords, multiple markets, and increasingly, the option of reducing their office footprint entirely. However, flight to quality works in Cousins' favor here. When tenants decide they want to upgrade, the number of buildings that meet their quality, location, and amenity requirements shrinks dramatically, reducing effective competition. Long lease terms spanning five to ten years provide contractual stability once a tenant commits.

Threat of Substitutes: High. This is the existential risk for every office REIT, and it demands clear-eyed assessment rather than dismissal.

Remote and hybrid work represent a genuine structural substitute for physical office space. Coworking and flexible office providers like WeWork's successors offer alternatives to traditional long-term leases. And the concept of what an "office" is continues to evolve, with some companies opting for distributed teams that meet periodically at hotels or conference centers rather than maintaining permanent space. The thesis that in-person collaboration is essential for innovation and culture may prove durable, but it is being tested in real time.

Competitive Rivalry: High. The Sun Belt office market is contested by public REITs including Highwoods Properties with 26.7 million square feet of Sun Belt exposure and Piedmont Office Realty Trust with approximately fifteen million square feet, as well as by private equity firms, pension funds, and sovereign wealth funds. Blackstone, Brookfield, and other major private equity players have been active acquirers of Sun Belt office assets, bringing deep pockets and aggressive pricing to competitive processes. Competition for tenants, acquisitions, development sites, and capital is intense. Differentiation through building quality, location, amenities, and tenant service is critical. The fragmented nature of the office market, where no single landlord controls more than a low single-digit percentage of any metro's total inventory, means that competition plays out building by building and lease by lease rather than at the portfolio level.

XIII. Strategic Power Analysis: Hamilton Helmer's 7 Powers

Scale Economies: Moderate. Cousins benefits from portfolio-level efficiencies in property management, procurement, and capital access. But office REIT scale has natural limits. You cannot centralize the management of a building in Austin from Atlanta in the same way you can centralize software infrastructure. Local market knowledge matters more than pure size.

Network Effects: Weak. There are limited network effects in office real estate. Some tenant clustering benefits exist, particularly in mixed-use environments like The Domain in Austin, where the concentration of amenities and employers creates a self-reinforcing ecosystem. But these effects are modest compared to technology platforms.

Counter-Positioning: Strong Historically, Fading. This is where the Cousins story gets most interesting through the lens of competitive strategy. The decision to focus exclusively on Sun Belt office markets when institutional capital was concentrated in gateway cities like New York, San Francisco, and Chicago was classic counter-positioning. Cousins' established competitors were structurally unable to follow because their existing portfolios and investor mandates were tied to coastal markets. However, as the Sun Belt thesis has become consensus, this advantage has eroded. Every major real estate investor now talks about Sun Belt exposure, which means the asymmetric opportunity is diminishing.

Switching Costs: Moderate-Strong. Tenant relocation is expensive and disruptive. Building out new office space can cost fifty to one hundred dollars per square foot or more. Moving disrupts operations, and location matters for employee commutes and client access. Long-term leases create contractual stickiness. However, leases do expire, and tenants can and do relocate, particularly when their space needs change significantly.

Branding: Moderate. Cousins has a strong brand in Atlanta and growing recognition in Austin and Charlotte. The brand signals quality, stability, and tenant-first service. But in office real estate, the building's location and physical quality typically matter more than the landlord's name. A tenant choosing between two identical buildings will pick the better location regardless of who owns it.

Cornered Resource: Moderate-Strong. This is one of Cousins' most durable advantages. Premium development sites in supply-constrained urban nodes are genuinely scarce. The company's land positions in Austin's Domain, Atlanta's Buckhead and Midtown, and Charlotte's South End represent resources that competitors cannot easily replicate. Long-term tenant relationships and deep institutional knowledge of specific submarkets also qualify as cornered resources.

Process Power: Moderate-Strong. Decades of integrated development and operations have produced organizational capabilities in site selection, entitlement, construction management, leasing, and tenant service that are difficult for competitors to match quickly. The company's disciplined capital allocation culture, forged through the Omni crisis and the financial crisis, manifests in consistent decision-making that avoids the boom-and-bust cycles that plague less disciplined operators.

Overall Assessment: Cousins' most durable powers are Cornered Resource and Process Power. The Counter-Positioning advantage that defined its strategy for a decade is fading as the Sun Belt thesis becomes consensus. This is a natural progression: the best strategic insights eventually get noticed and replicated, which means the company must find new sources of differentiation. Cousins' response has been to shift from geographic arbitrage, owning Sun Belt when others did not, to quality arbitrage, owning the best buildings in Sun Belt markets when many investors are still willing to buy average ones. Whether this new form of differentiation proves as durable as the original geographic insight remains to be seen. The company's future competitive position depends on maintaining its execution advantages and land positions while the informational edge of its geographic thesis diminishes.

XIV. Bull vs. Bear Case & Investment Debate

The Bull Case

The strongest argument for Cousins starts with demographics that are not cyclical but secular. The Sun Belt population is projected to grow by eleven million people over the next decade, a seven percent increase, while non-Sun Belt population grows by less than five hundred thousand. Corporate headquarters relocations show no sign of slowing, with Dallas-Fort Worth and Austin consistently leading destination rankings. These are not trends that reverse when the economy hiccups; they are driven by fundamental quality-of-life, cost, and tax advantages that are structural to these regions.

The flight-to-quality phenomenon in office has been a boon for Cousins' specific portfolio positioning. The company's buildings are young, well-located, and amenity-rich. When the national office vacancy rate is fifteen percent but the prime vacancy rate is closer to ten percent, and the gap between prime and non-prime continues to widen, owning the best buildings in the best markets is a genuine competitive advantage. Cousins' forty-seven-quarter streak of positive rent roll-ups demonstrates that premium assets command pricing power even in a difficult market.

The balance sheet provides strategic optionality. With net debt to EBITDA around five times, a one-billion-dollar undrawn credit facility, and investment-grade credit, Cousins can be a buyer when distress creates opportunities, as it demonstrated with the 2024-2025 acquisition spree. The company is trading at a meaningful discount to estimated net asset value, suggesting that the public market is undervaluing the underlying real estate. The 250-million-dollar share repurchase authorization signals management's agreement with this assessment.

New office supply is at a thirteen-year low nationally, and higher construction costs and interest rates are discouraging new development starts. To build a Class A office tower today costs meaningfully more than it did in 2019, and securing construction financing has become far more difficult as banks have pulled back from office lending. This supply constraint benefits existing trophy landlords by reducing competition for tenants and supporting rents. It is the mirror image of the demand challenge: while hybrid work has reduced overall demand, the simultaneous collapse in new supply means the balance between available space and tenant requirements may tighten faster than the headlines suggest.

The AI boom is generating renewed demand from tech companies that need collaborative space for teams working on cutting-edge technology, a development that was not in anyone's model two years ago.

The Bear Case

The most potent bear argument is that office demand has been structurally impaired by hybrid work, and that the current recovery is merely the first phase of a longer-term decline. If the three-day-in-office norm proves to be a waystation to two days or eventually one, the math on twenty million square feet of office space becomes much less favorable. Generational preferences are moving away from traditional office work, and companies may continue to reduce their physical footprints as leases roll over the next five to ten years.

Interest rates pose a valuation challenge that should not be underestimated. In real estate, the relationship between interest rates and property values is mechanical: higher rates expand capitalization rates (the yield investors demand), which directly compresses property values. A property generating ten million dollars in NOI might be worth 200 million dollars at a five percent cap rate but only 143 million dollars at a seven percent cap rate. That sensitivity means that even a company with growing cash flows can see its asset values decline if the interest rate environment shifts unfavorably. Higher rates also increase borrowing costs for Cousins' floating-rate debt and for tenants whose own financial health depends on access to affordable credit. While Cousins' balance sheet is conservatively managed, the REIT sector broadly is sensitive to the interest rate environment, and any sustained period of higher rates would pressure valuations.

The Sun Belt thesis is now consensus, which creates supply risk. Everyone is building in Austin, Atlanta, and Charlotte, and the same demographic tailwinds that attract office tenants also attract office developers. If supply outpaces demand in specific submarkets, even premium assets could see pressure on occupancy and rents.

Perhaps most importantly, the asymmetric opportunity that defined Cousins' strategy for a decade, betting on Sun Belt growth before others saw it, has largely played out. The stock now trades at a price that reflects the strengths of the Sun Belt thesis, meaning future returns depend more on execution and market conditions than on strategic insight.

There is also a concentration risk that merits attention. Austin and Atlanta together account for roughly two-thirds of Cousins' NOI. If either market experiences a downturn, whether from a tech sector correction in Austin or an economic shock in Atlanta, the portfolio lacks the geographic diversification to buffer the impact. The company has begun addressing this through acquisitions in Charlotte and Dallas, but the dependence on two markets remains a vulnerability that investors should monitor.

Key Metrics to Watch

For investors tracking Cousins' ongoing performance, two metrics stand out as the most informative. First, same-property NOI growth on a cash basis, which captures the organic revenue growth of the existing portfolio, adjusting for acquisitions and dispositions. This metric has been positive but decelerating, posting 4.2 percent in 2023 and 1.2 percent year-to-date through the third quarter of 2025. Sustained positive same-property NOI growth would validate the thesis that premium Sun Belt office is gaining pricing power. A turn to negative growth would signal trouble.

Second, second-generation leasing spreads, meaning the change in rent when an expiring lease is replaced by a new one on the same space. Cousins' forty-seven-quarter positive streak on this metric is the single most important proof point that demand for its specific buildings exceeds supply. If this streak breaks, it would indicate that even premium assets are losing pricing power, undermining the core thesis. Watch these two numbers quarter by quarter: they will tell you more about Cousins' competitive position than any management commentary.

XV. Playbook: Lessons for Founders & Investors

The Cousins Properties story, spanning seven decades from a twenty-five-hundred-dollar investment to a four-billion-dollar enterprise, encodes several lessons that apply far beyond real estate.

Patient capital wins. The sequence of selling assets near peak valuations in 2003-2006, surviving the financial crisis with capital intact, and then buying trophy assets at deep discounts in 2011-2014 required a time horizon that most investors and corporate managers simply do not have. Tom Cousins learned patience the hard way, through the Omni catastrophe, and that institutional memory persisted through multiple leadership transitions.

Focus creates value, but the journey to focus is painful. Cousins spent decades as a diversified real estate company, owning office, retail, residential land, medical office, and mixed-use properties. The conglomerate discount was real and persistent. Shedding these assets meant abandoning parts of the company's identity and acknowledging that the market's judgment, while frustrating, was correct. The company that emerged from this pruning was smaller, simpler, and dramatically more valuable per share.

Conviction in a thesis requires the courage to act before consensus forms. Cousins was investing heavily in Sun Belt office markets when institutional capital was still overwhelmingly focused on New York, San Francisco, and London. The thesis was grounded in demographic data that was publicly available to anyone who cared to look, but acting on it required the confidence to diverge from what the biggest pools of capital were doing.

Balance sheet discipline is a competitive weapon. Twice in the company's history, conservative leverage proved decisive. After the Omni crisis of the 1970s, Cousins entered the 1990s recession with virtually no debt while competitors were devastated. After strengthening the balance sheet in 2009-2011, the company was positioned to be a buyer when others were sellers. In real estate, the companies that survive and thrive through cycles are the ones that borrow conservatively during good times.

Quality over quantity compounds advantages. A portfolio of twenty million square feet of trophy office in the right submarkets is worth more, and generates better returns, than forty million square feet of average office in average locations. Cousins' relentless pruning of non-core assets and refusal to chase yield in lower-quality properties has produced a portfolio that outperforms peers on occupancy, rent growth, and tenant retention.

Timing is not everything, but it is something. Selling Bank of America Plaza months before the credit markets seized up and buying Promenade II near the post-crisis bottom required a combination of strategic judgment, market awareness, and the institutional willingness to act decisively. These were not lucky trades; they were the product of a culture that valued rigorous analysis and had the balance sheet to execute.