Corteva: The Agricultural Giant Born from Chemical Titans

I. Introduction & Episode Roadmap

Picture this: It's June 1, 2019, and the opening bell rings at the New York Stock Exchange. A new agricultural powerhouse begins trading under the ticker CTVA—but this isn't your typical IPO story. No venture capitalists, no Silicon Valley garage, no charismatic founder pitching to skeptics. Instead, Corteva Agriscience emerges fully formed from one of the most complex corporate restructurings in history, wielding $14 billion in annual revenue and 21,000 employees from day one.

The puzzle that captivates us today: How did a company born from a three-way corporate split achieve net sales of approximately $17.23 billion in 2023, commanding one of the top three positions in global agricultural inputs? More intriguingly, why did two chemical titans—Dow and DuPont—merge for $130 billion only to immediately plan their divorce into three separate companies?

This is a story where century-old chemical dynasties collide with modern agriculture, where the legacy of a U.S. Vice President shapes the genetics of our food supply, and where boardroom drama in Delaware determines what seeds get planted in Iowa cornfields. It's about the intersection of Wall Street financial engineering and Main Street farming economics, of patent cliffs and climate change, of feeding 10 billion people while satisfying ESG mandates.

What you'll discover is how Corteva became the unlikely heir to three legendary companies—Pioneer Hi-Bred, Dow AgroSciences, and DuPont Crop Protection—each with their own origin myths and innovation breakthroughs. We'll trace the journey from Henry Wallace's revolutionary hybrid corn experiments in 1920s Iowa to today's gene-edited crops and biological pesticides. We'll decode the strategic chess moves that created, merged, and then split these giants. And we'll examine whether Corteva represents the final form of agricultural consolidation or merely another chapter in an endless cycle of combination and separation.

The stakes couldn't be higher. In an era of climate volatility, geopolitical food insecurity, and technological disruption, Corteva sits at the nexus of humanity's most fundamental challenge: how to sustainably feed a growing planet. Yet Wall Street values it at a modest multiple, farmers grumble about input costs, and environmentalists question its chemical heritage. Is this a misunderstood compounder or a melting ice cube in a warming world?

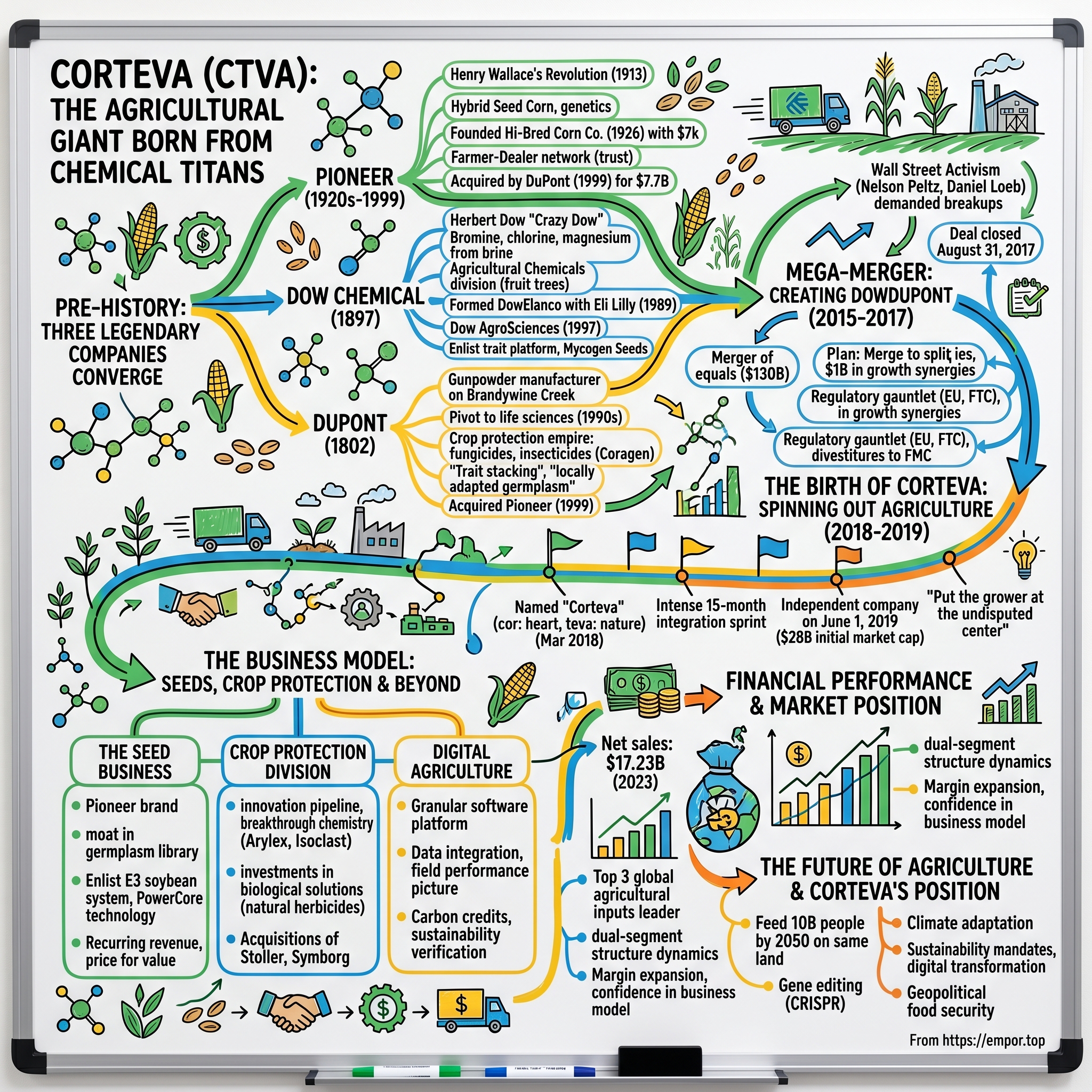

II. The Pre-History: Three Legendary Companies Converge

The Pioneer Story: Henry Wallace's Revolution (1920s–1999)

The year is 1913, and a young Henry Wallace stands in an Iowa cornfield, meticulously hand-pollinating corn plants under the scorching summer sun. His neighbors think he's lost his mind—corn is corn, after all. But Wallace, fresh from Iowa State College where he graduated in 1910, carries a secret weapon: the relatively new science of genetics that has captured his imagination.

Wallace's fascination with genetics wasn't academic abstraction. After visiting Edward East and Donald Jones at the Connecticut Agricultural Experiment Station in 1920, he began what would become one of the most consequential breeding programs in agricultural history. By 1923, working with almost monastic devotion, he produced a high-yielding hybrid he christened "Copper Cross." The farming establishment scoffed—until 1924, when Copper Cross won the gold medal in the Iowa Corn Yield Contest, stunning traditional seed companies.

But Wallace understood something his competitors didn't: hybrid corn wasn't just about yield. It was about creating a renewable business model. Unlike traditional open-pollinated varieties that farmers could save and replant, hybrid seeds lose their vigor in the second generation, ensuring repeat customers. Brilliant science meets brilliant business.

In 1926, this farm journal editor—who would later become Franklin Roosevelt's Vice President—gathered a group of Des Moines businessmen in a small office. The roster reads like a Midwest establishment dream team: his brother James W. Wallace, Fred Lehmann, J.J. Newlin, Simon Casady Jr., and George Kurtzweil. Together they founded the Hi-Bred Corn Company with $7,000 in capital. The company's first sales brochure in 1926 proclaimed: "We have something different to sell—HYBRID SEED CORN—crossed by the most scientific methods."

The early years tested their resolve. Farmers remained skeptical, the Great Depression crushed agricultural prices, and drought devastated crops. But Pioneer (as Hi-Bred was renamed in 1935) persisted with an innovation that would define its culture: the farmer-dealer network. Rather than distant salesmen, Pioneer recruited successful local farmers to sell seeds to their neighbors, creating trust through peer credibility.

By the 1960s, Pioneer had become the world's largest seed company, commanding over 35% of the U.S. hybrid corn market. The company's germplasm library—its collection of genetic material—grew into an irreplaceable vault of agricultural biodiversity. Each variety represented thousands of careful crosses, decades of field testing, and intimate knowledge of local growing conditions.

The endgame came in 1997 when DuPont, seeking to transform from chemicals to life sciences, acquired 20% of Pioneer in a joint venture arrangement. Two years later, in 1999, DuPont paid $7.7 billion to make Pioneer a wholly owned subsidiary—at the time, the largest acquisition in DuPont's 197-year history. Henry Wallace's garage experiment had become a cornerstone of global agriculture.

The Dow Chemical Story: From "Crazy Dow" to Agricultural Innovation

In 1897, a young chemist named Herbert Henry Dow founded his third company in Midland, Michigan. His first had gone bankrupt, the second had ousted him from control, and now the locals called him "Crazy Dow" as he rode his dilapidated bicycle through town, pursuing what seemed an impossible dream: challenging the German chemical monopolies that dominated world markets.

But Dow possessed something more powerful than capital: an inventor's mind inherited from his father, a mechanical engineer who shared technical ideas at the dinner table. A graduate of Case School of Applied Science, Dow was a prolific inventor of chemical processes, particularly fascinated by the bitter brine that oil drillers considered a worthless nuisance. Where others saw waste, Dow saw opportunity—bromine, chlorine, magnesium—an entire chemical empire flowing beneath Michigan's soil.

Dow produced its first agricultural product at a time when U.S. farms had soared to $30 billion in value, establishing an agricultural chemicals division based on a spray for fruit trees. This early foray into agriculture would prove prescient, though Dow himself couldn't have imagined his company would one day help create one of the world's largest agricultural enterprises.

The company's agricultural ambitions accelerated dramatically through the formation of DowElanco in 1989, a joint venture with Eli Lilly that combined Dow's agricultural chemicals with Lilly's plant science capabilities. This partnership brought together herbicides, insecticides, and emerging biotechnology research. When Dow acquired full ownership of DowElanco in 1997, renaming it Dow AgroSciences, it signaled a strategic commitment to becoming a major agricultural player. The transformation accelerated through strategic acquisitions. In 1998, Dow acquired Mycogen Corporation, a biotechnology company that brought critical seed assets and genetic engineering capabilities. Dow integrated these assets with Mycogen Seeds, affiliated with Dow AgroSciences LLC, creating a larger and more efficient platform from which to launch biotechnology products. The company continued its expansion spree, acquiring Cargill Hybrid Seeds' assets in 2000, making the combined entity the third-largest U.S. seed corn producer.

By the early 2000s, Dow AgroSciences had assembled a formidable portfolio: the Enlist trait platform for herbicide tolerance, a growing seed business under brands like Mycogen and PhytoGen, and a deep pipeline of crop protection chemicals. The company wasn't just selling products; it was offering integrated solutions—seeds engineered to work with specific herbicides, creating a lock-in effect that would make farmers think twice before switching suppliers.

The DuPont Agricultural Evolution

While Dow built from chemical heritage into agriculture, DuPont's journey represented one of the most dramatic pivots in corporate history. Founded in 1802 as a gunpowder manufacturer on the banks of Delaware's Brandywine Creek, DuPont had already reinvented itself multiple times—from explosives to chemicals, from nylon stockings to Teflon pans. By the 1990s, leadership saw the future in life sciences, not traditional chemicals.

The transformation began with a shopping spree that would make private equity firms blush. Beyond the crown jewel Pioneer acquisition in 1999, DuPont methodically assembled a crop protection empire. They developed innovative fungicides, insecticides, and herbicides that commanded premium prices. Products like Coragen insecticide and Aproach fungicide became category leaders, protecting everything from corn to specialty vegetables.

But DuPont's agricultural strategy went beyond mere accumulation. They pioneered the concept of "trait stacking"—combining multiple genetic modifications in a single seed. A corn plant could simultaneously resist insects, tolerate herbicides, and use nitrogen more efficiently. It was elegant science that translated into pricing power.

The company also invested heavily in what they called "locally adapted germplasm"—seeds specifically bred for regional conditions. While competitors pushed one-size-fits-all solutions, DuPont's Pioneer brand offered corn varieties optimized for Iowa's deep soils or Brazil's tropical climate. This hyperlocal approach created customer loyalty that transcended price competition.

By 2015, DuPont's agricultural segment generated over $11 billion in revenue, rivaling its performance materials division. The gunpowder company had successfully transformed into an agricultural powerhouse. Yet even as executives celebrated this achievement, activist investors circled, demanding more. The stage was set for the deal that would reshape the industry.

III. The Mega-Merger: Creating DowDuPont (2015–2017)

December 11, 2015. The financial press buzzes with breaking news: Dow Chemical and DuPont, two titans with a combined 319 years of history, announce a "merger of equals" valued at $130 billion. But here's the twist—they're merging only to immediately plan their divorce into three separate companies. It's the corporate equivalent of getting married at the courthouse with divorce papers already drafted.

Andrew Liveris, Dow's charismatic Australian CEO who had led the company since 2004, called it "a significant milestone in the storied histories of our two companies." But his real vision was more ambitious: "This transaction is a game-changer for our industry and reflects the culmination of a vision we have had for more than a decade."

The architect of this three-dimensional chess move wasn't just corporate leadership—it was Wall Street activism. Nelson Peltz's Trian Fund had launched an activist campaign at DuPont, while Daniel Loeb's Third Point targeted Dow. Both demanded breakups, better returns, more focus. The irony? By merging first, the companies could achieve the scale necessary to make the eventual splits viable while capturing $3 billion in cost synergies and approximately $1 billion in growth synergies.

The power structure reflected the "equals" narrative: Liveris would become executive chairman of DowDuPont, while DuPont's Ed Breen—the turnaround artist who had orchestrated Tyco's breakup—would serve as CEO. Breen wasn't even DuPont's CEO when merger talks began; he had just replaced Ellen Kullman in November 2015 after she won a bruising proxy battle with Trian but then abruptly resigned.

The regulatory gauntlet proved brutal. The European Commission ultimately approved the deal in March 2017, but only after DuPont agreed to divest key pesticide products and nearly all of its global crop protection R&D division. The companies struck a $1.6 billion asset swap with FMC Corporation—DuPont acquired FMC's health and nutrition business while selling its herbicide and insecticide properties.

After over a year of regulatory reviews and divestitures, the merger finally closed on August 31, 2017. Dow shareholders received 1.00 share of DowDuPont for each Dow share, while DuPont shareholders received 1.282 shares—a ratio that reflected the relative valuations and gave DuPont shareholders a slight premium.

But even as champagne corks popped in Midland and Wilmington, the real work was just beginning. Integration teams had to develop operating models and organizational designs for each future division, ensuring each would have its own processes, people, assets, systems and licenses to operate independently. The intended separations were expected within 18 months.

The financial engineering was elegant: create enough scale to compete globally, achieve massive cost savings, then split into pure-plays that would command higher multiples than the conglomerate discount that had plagued both companies. It was activism jujitsu—using the activists' own momentum to create something even they hadn't envisioned.

IV. The Birth of Corteva: Spinning Out Agriculture (2018–2019)

The morning of March 27, 2018, marked a pivotal moment in agricultural history. DowDuPont executives gathered to announce the name of their future agricultural spinoff: Corteva Agriscience. The company's name combined "cor" (Latin for "heart") with "teva" (an ancient word for nature)—a poetic touch for what would become a hard-nosed business generating billions in revenue.

But poetry quickly gave way to operational reality. The company was formed in March 2018 as a subsidiary of DowDuPont, beginning an intense 15-month sprint to independence. James C. Collins Jr., a 35-year DuPont veteran who had been Chief Operating Officer for DowDuPont's Agriculture Division, was tapped to lead the charge. Beginning with the announcement of the DowDuPont merger, Collins led the integration of legacy DuPont and Dow agricultural businesses to drive readiness for the ultimate spin of Corteva.

The integration challenge was staggering: combining two proud cultures, harmonizing different IT systems, consolidating R&D pipelines, and creating a unified go-to-market strategy. Collins and his team had to build an entire corporate infrastructure from scratch—treasury functions, investor relations, independent board governance—all while maintaining business momentum in volatile agricultural markets.

Corteva became an independent public company on June 1, 2019 and was previously the Agriculture Division of DowDuPont. The spin mechanics were elegantly simple yet operationally complex: each DowDuPont stockholder receiving one share of Corteva common stock for every three shares of DowDuPont common stock they held as of May 24.

When the opening bell rang that Saturday morning in June, Corteva didn't start small. It began trading with an estimated initial market capitalization of approximately $28 billion, instantly making it one of the world's largest pure-play agricultural companies. The company commanded 22,000 employees across 140 countries, operated 85 production facilities, and maintained one of the industry's deepest R&D pipelines.

Collins articulated a vision that went beyond mere operational excellence: "We really put the grower, the farmer, at the undisputed center of everything we do". But he added a twist: "I believe we have ignored another large constituent here as an industry over the years—and that's the consumer".

The early days of independence proved both liberating and challenging. Free from the conglomerate structure, Corteva could make faster decisions, pursue targeted acquisitions, and align incentives directly with agricultural performance. But it also inherited legacy obligations, including DuPont's pension plan, and faced immediate pressure from farmers dealing with commodity price volatility and extreme weather events.

By 2021, after successfully navigating the spin-off and the COVID-19 pandemic's disruptions, Collins announced his retirement. The board conducted an external search, ultimately appointing Chuck Magro in November 2021. Mr. Magro served as President and Chief Executive Officer of Nutrien from the company's launch in 2018 until April 2021, bringing deep agricultural industry experience from creating the world's largest crop inputs company.

Under Magro's leadership, Corteva made a symbolic but strategic move in 2022, relocating its headquarters from Delaware to Indianapolis, bringing it closer to its Midwest operations and farming customers. The message was clear: Corteva wasn't just another chemical company with an ag division. It was agriculture, pure and focused.

V. The Business Model: Seeds, Crop Protection & Beyond

The Seed Business

At the heart of Corteva's business model beats the genetic engine that Henry Wallace started nearly a century ago. Corteva sells a large portion of their seeds under the Pioneer Hi-Bred International brand, leveraging one of agriculture's most trusted names. But this isn't your grandfather's seed corn operation.

The company's seed portfolio spans the major row crops—corn, soybeans, canola, sunflower—plus specialty crops that command premium margins. In corn alone, Corteva offers over 500 unique hybrids tailored to specific geographies, soil types, and weather patterns. A hybrid optimized for the heavy soils of Illinois won't perform the same in the sandy loams of North Carolina. This hyperlocal customization creates switching costs that go beyond price.

The real moat lies in Corteva's germplasm library—essentially the company's genetic vault. Imagine a seed bank containing millions of genetic variations accumulated over decades, each catalogued with performance data across different environments. Competitors can't simply buy their way into this advantage; it requires generations of breeding, testing, and selection. It's the agricultural equivalent of compound interest, where each breeding cycle builds on the last.

Technology traits represent the highest-margin component of the seed business. The Enlist E3 soybean system exemplifies this approach: soybeans genetically engineered to tolerate specific herbicides, creating a integrated solution where seeds and chemicals work in concert. PowerCore technology stacks multiple insect-resistance traits, reducing the need for insecticide applications. These aren't just seeds; they're biological platforms delivering multiple value streams.

The business model genius lies in the recurring revenue nature. Hybrid seeds lose their vigor in the second generation, ensuring farmers return each planting season. Trait licensing agreements with competitors like Bayer generate royalty streams. And the continuous innovation cycle—new hybrids, new traits, new stacks—creates pricing power even in commodity markets.

Crop Protection Division

Corteva's products for seeds and crop protection, including herbicides, insecticides, fungicides, and biologicals (natural herbicides) are sold in 110 countries. But unlike the seed business with its genetic moats, crop protection faces constant threats: regulatory restrictions, resistance development, and patent expirations.

The chemistry innovation pipeline functions like a pharmaceutical company for plants. It takes 10-12 years and over $250 million to bring a new active ingredient to market. Corteva's advantage comes from its ability to combine new molecules with existing chemistries, creating formulations that extend patent life and improve efficacy. Products like Arylex herbicide and Isoclast insecticide represent breakthrough chemistry that commands premium pricing before generics arrive.

But the real strategic shift is toward biological solutions. Recognizing the growing demand for sustainable agriculture, Corteva made significant investments in biological solutions. The acquisitions of Stoller and Symborg in late 2022 and early 2023 marked a pivotal shift. These aren't your traditional chemicals but living organisms—beneficial bacteria, fungi, and plant extracts—that protect crops through natural mechanisms.

The integration of seed and crop protection creates powerful synergies. Seed treatment technologies apply crop protection directly to seeds before planting, ensuring every plant starts with protection. This delivery mechanism reduces chemical use, improves targeting, and creates a value bundle that's hard for farmers to disaggregate.

Digital Agriculture & Emerging Platforms

The third leg of Corteva's stool—digital agriculture—represents both its highest growth potential and greatest uncertainty. The company's Granular software platform helps farmers manage everything from planting decisions to inventory tracking. But unlike seeds or chemicals, software faces low barriers to entry and winner-take-all dynamics.

Corteva's advantage comes from data integration. When a farmer plants Pioneer seeds, applies Corteva crop protection, and uses Granular software, the company captures a complete picture of that field's performance. This data feedback loop improves product development, enables precision recommendations, and creates switching costs as farmers' historical data accumulates in the platform.

The company is betting that agriculture's digital transformation will mirror other industries, where incumbent advantages in distribution and customer relationships trump pure technology plays. By embedding digital tools within its existing sales channels—those 5,000 sales representatives and thousands of retail partners—Corteva can drive adoption without the customer acquisition costs that plague ag-tech startups.

Emerging platforms like carbon credits and sustainability verification represent optionality rather than current revenue drivers. As corporations seek to offset emissions and consumers demand traceability, Corteva's position at the farm gate could prove valuable. But monetizing these opportunities requires regulatory clarity and market development that remains years away.

VI. Financial Performance & Market Position

The numbers tell a story of scale meeting execution. Corteva reported net sales of approximately $17.23 billion for the full year 2023, positioning it among the elite tier of global agricultural companies. But raw revenue only scratches the surface of the financial engineering at work.

The company's dual-segment structure reveals divergent dynamics. Seed net sales grew 5% in 2023 with organic sales increasing 7%, with price up 13% globally, led by continued execution on the company's price for value strategy and demand for new technology. This pricing power in seeds—achieving double-digit increases even in a commodity business—demonstrates the value farmers place on yield-enhancing genetics.

Conversely, Crop Protection net sales declined 9% and organic sales decreased 12% in 2023, with volume declines largely in Latin America and North America, driven by strategic product exits, inventory destocking, and delayed farmer purchases. This tale of two segments reflects broader industry dynamics: seeds benefiting from technology adoption while crop protection faces generic competition and channel inventory corrections.

Looking ahead, Corteva expects net sales in the range of $17.4 billion to $17.7 billion for 2024, growth of 2% at the mid-point, with Operating EBITDA expected to be in the range of $3.5 billion to $3.7 billion, growth of 6% at the mid-point. The margin expansion story becomes clearer: growing higher-margin seed sales while optimizing the crop protection cost structure.

The Company plans to repurchase approximately $1.0 billion shares in 2024, signaling confidence in the business model despite market volatility. This capital allocation strategy—balancing growth investments with shareholder returns—reflects the mature nature of the agricultural inputs market.

The competitive landscape reveals Corteva's market position. Against Bayer-Monsanto's agricultural revenues of approximately $25 billion, Syngenta's $20 billion (now Chinese-owned via ChemChina), and BASF's agricultural solutions at $10 billion, Corteva holds a formidable position as one of the top three global leaders in the agricultural inputs sector. Its strength lies in its vast germplasm library for seeds and a comprehensive portfolio of crop protection solutions.

Regional dynamics add complexity. North America delivers the highest margins, benefiting from advanced farming practices and premium pricing for technology traits. Latin America offers growth but with volatility—currency fluctuations, political instability, and weather extremes create quarterly swings that test management's guidance credibility. Europe faces regulatory headwinds as the EU restricts chemical usage, while Asia Pacific remains fragmented with local competitors.

The financial model's sustainability hinges on R&D productivity. With approximately $1.4 billion in annual R&D spending—about 8% of sales—Corteva must generate returns that justify this investment. The challenge: agricultural R&D has 10-15 year development cycles, meaning today's profits fund tomorrow's uncertain innovations.

Corteva achieved 20% operating EBITDA margins for the first time in 2024, despite challenging market conditions, with double-digit organic sales growth and 800 basis points of margin improvement in the Crop Protection segment, particularly driven by demand in Brazil. This margin milestone represents years of cost optimization finally bearing fruit.

Yet challenges persist. Corteva faced competitive pricing pressures in Latin America, particularly impacting the Seed business, with Crop Protection prices expected to face low single-digit declines in 2025, despite signs of stabilization in the industry. The pricing power that drove recent results faces headwinds as competitors respond and farmers push back against input cost inflation.

VII. Challenges & Controversies

In September 2022, the Federal Trade Commission sued Syngenta and Corteva, challenging certain US-based discount programs that allegedly block and restrict generic competition from pesticide markets. This wasn't just regulatory saber-rattling—the FTC Chair Lina M. Khan declared the companies were "maintaining their monopolies through harmful tactics that have jacked up pesticide prices for farmers" by "paying off distributors to block generic producers from the market, these giants have deprived farmers of cheaper and more innovative options".

The mechanics of the alleged scheme are deceptively simple. The companies set up "loyalty" programs in which they make payments to distributors—as long as the distributors keep their purchases of competing generic pesticides beneath a very low threshold. Under this scheme, Syngenta and Corteva make more money than they would if they had to compete fairly with generics. Boxing out the competition allows them to keep charging such high prices that, even after compensating the distributors, they can maintain a large profit margin.

In January 2024, a federal judge denied a motion to dismiss the lawsuit, allowing the case to proceed. The legal battle continues under the Trump administration, with discovery set to complete by November 2025—a reminder that regulatory risk transcends political cycles. The legal drama escalated in August 2022 when two agricultural titans went to war over intellectual property. In August 2022, Bayer sued Corteva for breach of contractual obligations related to the development and commercialization of E3 soybeans. Hours later, Corteva then sued Bayer, alleging that Bayer infringed upon its patents on a gene used in Enlist Corn, a product resistant to herbicides including Roundup.

The stakes couldn't be higher. Corteva's Enlist E3 soybeans reached 65% market penetration in the U.S., contributing to $1.9 billion in sales in 2024. This isn't just about royalty payments—it's about control over the next generation of agricultural biotechnology. Each company claims the other is using its technology without permission, creating a Mexican standoff where billions in future revenue hang in the balance.

Beyond corporate battles, environmental and sustainability pressures mount. In February 2020, Corteva ceased production of the pesticide chlorpyrifos after the product was linked to neurological problems in children and following bans in the European Union and some U.S. states. This voluntary withdrawal, while praised by environmental groups, eliminated a profitable product line and signaled vulnerability to regulatory activism.

The biologicals pivot represents both crisis and opportunity. As regulators restrict traditional chemistry and consumers demand "cleaner" agriculture, Corteva must transform its portfolio without sacrificing profitability. The acquisitions of Stoller and Symborg weren't just strategic additions—they were survival moves in a world increasingly hostile to synthetic pesticides.

Climate volatility adds another layer of complexity. Extreme weather events—floods, droughts, unexpected freezes—disrupt planting schedules, alter pest populations, and create demand volatility that makes quarterly guidance a high-wire act. When Brazilian farmers face drought, Corteva's Latin American revenues crater. When Midwest flooding delays planting, seed sales shift unpredictably.

The patent cliff looms large. Key herbicides face generic competition as patents expire, pressuring margins and forcing continuous innovation just to maintain market position. Unlike pharmaceuticals where one blockbuster drug can carry a company for a decade, agricultural chemicals face faster commoditization and more aggressive generic competition.

VIII. Strategy & Competitive Advantages

Corteva's strategic positioning rests on three pillars that competitors struggle to replicate simultaneously: integrated innovation, distribution depth, and farmer intimacy. While Bayer may have superior technology in certain areas and Syngenta might offer better pricing, none match Corteva's balanced portfolio across seeds and crop protection.

The R&D intensity tells the story. Corteva invests more than $1 billion each year in research and development to advance agricultural innovations that help farmers increase yields, protect against devastating weeds and pests. But unlike pharmaceutical R&D where success is binary, agricultural innovation compounds—each season's data improves next year's products.

The germplasm library represents an irreplaceable asset. Decades of breeding data, millions of genetic combinations, performance records across countless environments—this isn't something money can buy. It's agricultural compound interest, where time in the market beats timing the market. When climate patterns shift, Corteva can reach into this genetic vault and find varieties that performed well in similar conditions decades ago.

Distribution might be Corteva's most underappreciated advantage. The Pioneer dealer network—those thousands of farmer-dealers who sell to their neighbors—creates trust that no amount of digital marketing can replicate. When a local farmer who's been successful for 30 years recommends a seed variety, that carries weight no corporate salesperson can match.

The integrated platform approach—seeds engineered to work with specific chemicals, bundled with digital tools—creates switching costs that lock in customers. A farmer using Enlist E3 soybeans needs Enlist herbicides. Once they're trained on Granular software with years of field data, switching to a competitor means starting over.

Capital allocation reflects confidence. The Company expects it will have repurchased approximately $1.0 billion shares in 2024, signaling management's belief that the market undervalues the business. This balanced approach—investing in R&D while returning capital to shareholders—suggests a mature business generating substantial free cash flow.

Yet the strategic challenges are equally formidable. The industry consolidation endgame remains unclear. With only 4-5 major players globally, further mergers face antitrust scrutiny. But standing still while competitors combine isn't an option. Corteva must grow organically in a market where acreage is finite and yield improvements are incremental.

Digital transformation presents both opportunity and threat. While Corteva has agricultural expertise, tech giants like Microsoft and Amazon partner with competitors, bringing cloud computing and AI capabilities that could leapfrog traditional R&D. The question: Can Corteva's agricultural knowledge trump Silicon Valley's technical prowess?

The sustainability mandate creates strategic tension. Farmers need products that work—period. But investors, regulators, and consumers increasingly demand environmental stewardship. Threading this needle—developing products that are both effective and sustainable—requires innovations that don't yet exist.

China looms as both opportunity and threat. The world's largest agricultural market remains fragmented, with local competitors and regulatory barriers limiting access. But Chinese companies, backed by state resources, increasingly compete globally. Syngenta's acquisition by ChemChina signals this shift. Can Corteva compete with state-backed competitors playing by different rules?

IX. The Future of Agriculture & Corteva's Position

Agriculture stands at an inflection point. By 2050, the world must feed 10 billion people using essentially the same amount of arable land, while climate change disrupts traditional growing patterns and consumers demand sustainable practices. This isn't just a business challenge—it's existential for humanity.

Climate adaptation will separate winners from losers. As weather patterns shift, crops that thrived in Iowa might need to move north to Minnesota. Pests previously contained by winter freezes spread into new territories. Water scarcity turns irrigation from convenience to necessity. Corteva's germplasm library and breeding capabilities position it to develop climate-adapted varieties, but the pace of change may outstrip traditional breeding cycles.

Gene editing technologies like CRISPR promise to revolutionize crop development, potentially creating drought-resistant corn or disease-immune soybeans in years rather than decades. But regulatory uncertainty clouds the horizon. While the U.S. embraces gene editing, Europe remains skeptical, and China's position shifts with geopolitical winds. Corteva must invest in these technologies while navigating a patchwork of global regulations.

The sustainability mandates aren't going away. Carbon markets, still nascent, could transform agriculture economics. If farmers can earn significant income from sequestering carbon, crop input companies must adapt their products and recommendations. Corteva's early moves into biologicals and regenerative agriculture practices position it for this transition, but the business model implications remain unclear.

Digital agriculture faces a reckoning. After years of hype, farmers question the ROI of precision agriculture tools. The promise of AI-optimized farming remains largely unfulfilled. Yet the potential is undeniable—satellite imagery detecting disease before symptoms appear, weather models predicting optimal planting windows, algorithms optimizing fertilizer application. The company that cracks this code could dominate the next era of agriculture.

Consolidation end-games present strategic options. Could Corteva merge with BASF's agricultural division, creating a European-American powerhouse? Might a technology company acquire Corteva for its agricultural expertise and customer relationships? Or will Corteva itself become the consolidator, rolling up smaller biotechnology companies and regional players?

The geopolitical dimension adds complexity. Food security is national security. Countries increasingly view agricultural inputs as strategic assets. Export restrictions, technology transfer limitations, and local content requirements fragment the global market. Corteva must balance global scale with local relevance, maintaining operations in countries with different political systems and economic philosophies.

Looking ahead to 2030, several scenarios emerge. In the optimistic case, Corteva's technology bets pay off—gene-edited crops gain acceptance, biologicals match chemical performance, digital tools deliver measurable ROI. The company commands premium multiples as the essential partner for sustainable agriculture.

The pessimistic scenario sees margin compression from all sides—generic competition in chemicals, commodity pricing in seeds, tech disruption in digital. Climate chaos disrupts business planning while regulatory restrictions eliminate profitable products. Corteva becomes a value trap, generating cash but lacking growth.

The most likely path lies between extremes. Corteva remains one of 3-4 essential agricultural input providers, generating steady cash flows but facing constant pressure to innovate. Success comes from incremental improvements—5% better yields, 10% reduced chemical use, 15% improved drought tolerance. Not revolutionary, but essential for feeding the world.

X. Playbook: Lessons from the Corteva Story

The Corteva saga offers a masterclass in corporate restructuring, market positioning, and navigating complex industries. For executives contemplating similar transformations, several lessons emerge.

Executing complex corporate separations requires surgical precision. The DowDuPont merger and tri-party split wasn't just financial engineering—it was organizational surgery. Creating three viable companies from two required decisions about everything from IT systems to pension obligations. Corteva's successful emergence shows that with proper planning, even the most complex separations can create value. The key: start planning the separation before the merger closes.

Building culture and identity post-spin demands intentional effort. Corteva faced the challenge of creating a unified culture from two proud legacies—Dow's chemical heritage and DuPont's agricultural roots. The new name, headquarters move, and focus on farmers over chemicals sent clear signals about the company's identity. Leadership must over-communicate the vision and values, especially when employees' email addresses still show legacy company domains.

Managing cyclical agricultural markets requires financial flexibility. Agriculture doesn't follow quarterly earnings calendars. Weather, commodity prices, and farmer sentiment create volatility that can whipsaw results. Corteva's conservative balance sheet and diverse geographic exposure provide buffers, but management must educate investors about the inherent volatility while delivering through-cycle returns.

Balancing innovation with regulatory reality means playing long games. A new crop protection chemical takes 10-12 years and $250 million to commercialize. Gene-edited crops face uncertain regulatory pathways. Corteva must invest in technologies that might never reach market while maintaining current product lines under regulatory assault. The lesson: maintain a portfolio approach to innovation, with multiple shots on goal.

The power of heritage brands in commodity markets shouldn't be underestimated. The Pioneer brand, nearly 100 years old, still commands premium pricing in corn seed—a seemingly commoditized product. Farmers, conservative by necessity, trust brands their fathers used. While Silicon Valley disrupts other industries, agriculture's relationship-based selling model provides moats that pure technology can't breach.

Integration beats best-of-breed when switching costs are high. Farmers don't want to manage multiple vendors, platforms, and relationships. Corteva's integrated offering—seeds, chemicals, and digital tools from one provider—creates convenience that specialized competitors can't match. The lesson extends beyond agriculture: in B2B markets with complex products, integration often trumps optimization.

XI. Bear vs. Bull Case

Bull Case: The Essential Infrastructure Play

The bull thesis rests on inevitability. The world must feed 10 billion people by 2050. Arable land isn't increasing. Climate change demands adapted crops. Corteva provides essential tools for this challenge. Unlike consumer discretionary products, farmers can't skip planting seasons or delay crop protection. This isn't growth for growth's sake—it's responding to existential need.

The innovation pipeline promises margin expansion. The Enlist platform's penetration from 0% to 65% in just a few years demonstrates Corteva's ability to drive adoption of new technology. With biologicals, gene editing, and digital tools in development, multiple growth vectors exist beyond traditional chemistry. Each successful launch commands premium pricing before generic competition arrives.

Financial flexibility enables opportunistic capital allocation. With investment-grade credit ratings and strong free cash flow generation, Corteva can simultaneously invest in R&D, pursue acquisitions, and return capital to shareholders. The $1 billion share buyback program in 2024 suggests management sees value the market doesn't.

Consolidation optionality provides multiple paths to value creation. As one of the few remaining independent agricultural input companies, Corteva could be an acquisition target at substantial premiums. Alternatively, it could be the acquirer, rolling up smaller players and achieving cost synergies. Either path likely leads to value creation for shareholders.

The ESG transition, while challenging, creates opportunities. As the agricultural industry shifts toward sustainability, companies with credible environmental strategies will command premium valuations. Corteva's investments in biologicals and regenerative agriculture position it as a sustainability leader, potentially attracting ESG-focused investors.

Bear Case: The Melting Ice Cube

The bear thesis sees structural decline masked by financial engineering. Patent expiries create constant pressure as yesterday's innovations become today's generics. The crop protection business faces perpetual margin compression as chemicals lose exclusivity and regulatory restrictions eliminate products. Without breakthrough innovations, Corteva is running to stand still.

Commodity exposure limits pricing power. When corn prices crash, farmers cut spending on inputs. When Brazil's real devalues, dollar-denominated revenues shrink. Unlike software or pharmaceuticals with subscription models or regulated pricing, Corteva faces the brutal economics of commodity agriculture. No amount of innovation changes the fact that farmers operate on thin margins.

Regulatory and environmental headwinds intensify. Europe bans more chemicals each year. The U.S. Environmental Protection Agency faces pressure to restrict pesticides. Consumer groups campaign against GMOs. Each restriction eliminates products that took decades to develop. The regulatory ratchet only tightens, never loosens.

Climate volatility disrupts business planning. Extreme weather events are becoming more frequent and severe. A drought in Brazil, floods in the Midwest, or unexpected frost can destroy quarterly earnings. Climate change doesn't just affect Corteva's customers—it makes the business itself increasingly unpredictable.

Technology disruption looms from unexpected directions. What if vertical farming eliminates the need for herbicides? What if lab-grown meat reduces corn demand for animal feed? What if AI-powered robots replace chemical weed control? Corteva invests billions in incremental improvements while potentially transformative technologies develop outside traditional agriculture.

Patent cliffs and generic competition never end. Every successful product eventually faces generic competition. The Roundup Ready patent expiration devastated Monsanto's margins. Corteva faces similar cliffs as key products lose exclusivity. The company must run faster just to maintain position—a recipe for value destruction, not creation.

XII. Epilogue & Reflections

The Corteva story embodies a paradox: a pure-play company born from conglomerate complexity. Wall Street demanded focus, so Dow and DuPont merged only to split, creating three "pure" companies. Yet Corteva itself combines seeds, chemicals, and digital tools—hardly pure by any definition. Perhaps the lesson is that "focus" is relative, and integration matters more than organizational simplicity.

As potentially the last great agricultural spin-off, Corteva marks an era's end. The century-long cycle of combination and separation in chemicals and agriculture may have run its course. With only a handful of global players remaining, further consolidation faces insurmountable antitrust barriers. Future value creation must come from innovation and execution, not financial engineering.

What would Henry Wallace think of his company today? The Iowa farm boy who revolutionized corn breeding might not recognize the $28 billion corporation selling gene-edited seeds and AI-powered farm management software. Yet the core mission remains: helping farmers grow more food. The tools evolved from hand-pollination to CRISPR, but the purpose endures.

For founders and investors, Corteva offers sobering lessons. Building lasting value requires more than financial engineering or strategic pivots. It demands deep technical expertise, patient capital, and the ability to navigate complex, regulated markets. In agriculture, there are no overnight successes—only decades of compound improvements.

The ultimate judgment on Corteva remains unwritten. Will it become the essential partner for sustainable agriculture, commanding premium valuations as the world recognizes food security's importance? Or will it slowly decay as patents expire, regulations tighten, and new technologies obsolete traditional approaches?

Perhaps the answer lies not in binary outcomes but in adaptation. Companies that survive centuries—like DuPont before its transformation—repeatedly reinvent themselves. Corteva's challenge is maintaining innovation velocity while serving conservative customers in volatile markets. Success requires being simultaneously cutting-edge and reliable, global and local, sustainable and profitable.

The agricultural industry stands at a crossroads between tradition and transformation. Farmers still plant seeds in soil, an act unchanged since civilization began. Yet those seeds now contain genes edited with molecular precision, protected by chemicals designed with supercomputers, and monitored by satellites. Corteva sits at this intersection, translating science into practice, innovation into bushels.

For investors evaluating Corteva, the question isn't just about financial metrics or competitive position. It's about believing in agriculture's future—that feeding 10 billion people requires the tools Corteva provides, that innovation can outpace regulation, that sustainable and profitable aren't mutually exclusive.

The stakes extend beyond shareholder returns. If companies like Corteva fail to deliver productive, sustainable agriculture, the consequences ripple through society. Food security, climate change, and global stability all intersect in the fields where Corteva's products are used. This isn't just business—it's about humanity's future.

As we reflect on Corteva's journey from the DowDuPont merger through independence to today's challenges, one theme emerges: resilience. Through activist campaigns, regulatory battles, patent disputes, and market volatility, the company persists. Like the farms it serves, Corteva embodies agriculture's essential truth: survival requires adaptation, but the mission—feeding the world—never changes.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube