Coterra Energy: The Unlikely Shale Giant

I. Introduction & Episode Roadmap

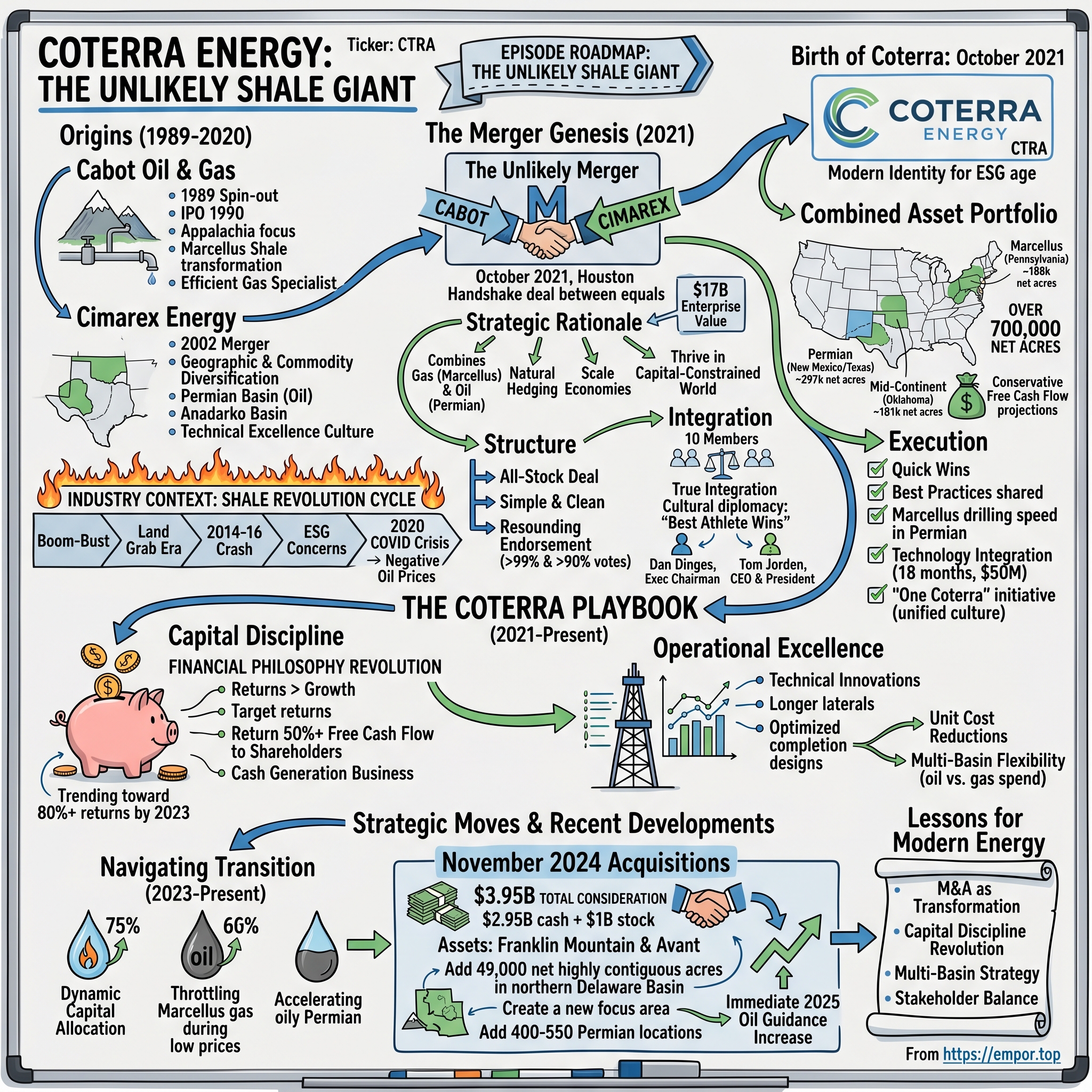

Picture this: October 2021, Houston. While oil prices climb back from pandemic lows and investors debate whether fossil fuels have any future at all, two mid-sized energy companies quietly complete a merger that nobody saw coming. No hostile takeover drama. No bidding war. Just a handshake deal between equals that would create something remarkable—a $17 billion energy company that somehow manages to be both boring and brilliant.

Coterra Energy doesn't have the swagger of a Pioneer Natural Resources or the scale of an ExxonMobil. What it has is 297,000 net acres in the Permian Basin, 186,000 acres in the Marcellus Shale, and 181,000 acres in the Anadarko Basin—a geographic trinity that reads like a shale operator's dream portfolio. But here's what makes this story fascinating: Coterra emerged from the union of Cabot Oil & Gas and Cimarex Energy at precisely the moment when the entire energy industry was undergoing its most profound philosophical transformation in decades.

The central question isn't just how two companies merged during a pandemic recovery. It's how they created what analysts now call "a premier, diversified energy company" that somehow cracked the code on capital discipline while everyone else was still figuring out what that meant. This is a story about M&A as transformation, about breaking the growth addiction that defined American shale for two decades, and about building a modern energy company that Wall Street actually trusts.

We're going to explore how Cabot's Appalachian gas expertise met Cimarex's Permian oil prowess, how a merger announced with more than 99% shareholder approval became the template for energy consolidation, and why a company you've probably never heard of might represent the future of American energy production. Along the way, we'll unpack the modern energy transition playbook—not the one about solar panels and wind turbines, but the one about how traditional energy companies survive and thrive in a world that simultaneously needs their product and wishes they didn't exist.

The themes here run deep: the death of growth-at-any-cost mentality that defined the shale revolution's first act, the rise of shareholder returns as the new religion, and the delicate balance between drilling for oil and preparing for a carbon-constrained future. This isn't just another energy company story—it's about how an entire industry learned to grow up.

II. Origins: The Cabot and Cimarex Stories (1989–2020)

Cabot Oil & Gas Foundation

The year was 1989, and nobody was talking about shale. George H.W. Bush had just become president, the Berlin Wall was about to fall, and in Boston, Cabot Corporation—a specialty chemicals and materials company with roots dating back to 1882—made a decision that would seem prescient in hindsight. They spun out their oil and gas operations into a subsidiary, setting the stage for what would become one of the most focused natural gas plays in America.

Cabot Oil & Gas went public via IPO in February 1990, raising capital in a market that had no idea what was coming. By March 1991, the company achieved 100% public ownership, severing its last ties to the parent corporation and setting out from its Houston headquarters with a simple mission: find and produce natural gas in North America. The timing seemed terrible—natural gas prices were stuck in a multi-year slump, and the industry was still recovering from the 1980s oil crash that had decimated Houston.

But Cabot's leadership saw something others missed. While competitors chased oil plays in the Gulf of Mexico or international ventures, Cabot quietly accumulated acreage in Appalachia. Not the sexy Appalachia of today's Marcellus Shale boom, but the conventional fields of West Virginia and Pennsylvania where shallow wells produced modest amounts of gas for local markets. It was unglamorous work—the kind of blocking and tackling that doesn't make headlines but generates steady cash flow.

Then came the technology revolution that changed everything. By the mid-2000s, horizontal drilling and hydraulic fracturing—techniques that had been around for decades but never quite worked economically—suddenly clicked. George Mitchell's team had cracked the code in the Barnett Shale of Texas, and smart operators everywhere started looking at their acreage with fresh eyes. Cabot's management realized they were sitting on something extraordinary: their "worthless" Appalachian acreage overlay the Marcellus Shale, a formation that would prove to be one of the largest natural gas deposits on Earth.

The transformation from conventional to unconventional producer wasn't smooth. Early Marcellus wells were expensive disasters—some cost $8 million and barely produced. But Cabot persisted, iterating on completion designs, experimenting with lateral lengths, and slowly turning what skeptics called "science projects" into economic wells. By 2010, they had become one of the Marcellus's most efficient operators, with well costs down to $3 million and production rates that defied geology textbooks.

Cimarex Energy's Parallel Path

Meanwhile, 1,500 miles southwest, a different story was unfolding. Cimarex Energy emerged in 2002 from the merger of Key Production Company and Helmerich & Payne's exploration subsidiary—two names that meant nothing to mainstream investors but everything to oil patch insiders. While Cabot was becoming a gas specialist, Cimarex pursued a different philosophy: geographic and commodity diversification across America's mid-continent.

The company's DNA was pure oil patch aristocracy. Its leadership team had worked together at various predecessors for decades, developing a culture that prized technical excellence over financial engineering. They didn't chase the latest fads or hire investment bankers to dream up complex structures. Instead, they drilled wells—lots of them—in places like the Anadarko Basin of Oklahoma and the Permian Basin of West Texas.

Cimarex's approach to the shale revolution was notably different from Cabot's all-in bet. Rather than concentrate on a single play, they built positions across multiple basins, treating each as a distinct option on future commodity prices. When natural gas prices collapsed in 2012, they shifted capital to oil-rich Permian holdings. When oil crashed in 2014, they had the flexibility to pull back without destroying their business model.

This portfolio approach seemed outdated to investors drunk on single-basin "pure plays," but Cimarex's leadership—particularly CEO Tom Jorden, a geophysicist by training—argued that diversification was actually a form of capital discipline. Why bet everything on one commodity in one place when you could maintain optionality? The strategy generated solid if unspectacular returns through the 2010s, making Cimarex the kind of company that nobody got excited about but nobody worried about either.

Industry Context: The Shale Revolution

To understand why Cabot and Cimarex would eventually merge, you need to grasp the violent boom-bust cycle that defined American shale from 2005 to 2020. The shale revolution wasn't just a technology story—it was a financial mania that would make the dot-com bubble look rational by comparison.

The land grab era of 2005-2014 saw companies paying astronomical prices for acreage on the theory that whoever controlled the most land would win. Production growth became the only metric that mattered. Companies that grew production 50% annually traded at premium valuations regardless of profitability. The mantra was simple: drill, baby, drill—and let someone else worry about the economics.

This worked brilliantly until it didn't. The 2014-2016 oil crash exposed the industry's fundamental flaw: shale wells decline rapidly, requiring constant capital investment just to maintain production. When oil fell from $100 to $26, the music stopped. Over 100 energy companies filed for bankruptcy. Survivors slashed budgets, laid off thousands, and promised to reform.

But old habits die hard. As oil prices recovered in 2017-2018, the industry returned to its growth-obsessed ways, burning through $300 billion in negative free cash flow over the decade. Investors who had been burned twice were losing patience. ESG concerns were mounting. Then came the ultimate stress test: COVID-19.

April 20, 2020, will live in energy infamy as the day oil prices went negative. For a brief moment, producers literally paid people to take oil off their hands. The pandemic didn't just crater demand—it forced an existential reckoning. The old model of growth-at-any-cost was dead. Investors demanded capital discipline, free cash flow, and shareholder returns. The industry needed a new playbook, and the stage was set for consolidation.

III. The Merger Genesis: Why 2021?

Market Conditions and Strategic Rationale

By early 2021, something fundamental had shifted in the energy boardrooms of Houston and Denver. The recovery from COVID's depths was underway—WTI crude had climbed back above $60—but this wasn't your typical commodity rebound. For the first time in the industry's history, producers weren't rushing to increase production. They were returning cash to shareholders, paying down debt, and most surprisingly, talking to each other about mergers. The conversations between Cabot CEO Dan Dinges and Cimarex CEO Tom Jorden had started quietly in late 2020, just phone calls between two veterans who'd known each other for decades. Neither company needed to merge—both had survived COVID with balance sheets intact and operations humming. But they recognized something their peers were missing: the industry's consolidation wave wasn't about survival anymore. It was about building companies that could thrive in a permanently capital-constrained world.

The logic was elegant. Cabot brought the Marcellus Shale—America's most prolific gas play with rock-bottom production costs. Cimarex brought the Permian Basin—the heart of American oil production with decades of inventory. Together, they'd have natural hedging against commodity price swings, economies of scale that smaller operators couldn't match, and most critically, the ability to shift capital between oil and gas plays as markets evolved.

But the real driver was investor fatigue. After years of broken promises, shareholders wanted companies big enough to matter but disciplined enough to trust. The ESG movement was gaining momentum, with major funds divesting from fossil fuels entirely. Those investors who remained demanded a new social contract: profits over production, returns over reserves, discipline over dreams. The all-stock merger announced in May reflects a combined enterprise value of $17 billion.

The Negotiation and Deal Structure

When the merger was announced on May 24, 2021, the structure was deliberately simple—a hallmark of deals designed to actually close. Under the terms of the agreement, which has been unanimously approved by the Boards of Directors of both companies, Cimarex shareholders will receive 4.0146 shares of Cabot common stock for each share of Cimarex common stock owned. No cash, no complex contingencies, no hostile drama. Just an exchange ratio that valued both companies fairly based on their trading averages.

The 4.0146 ratio wasn't random—it was carefully calibrated to give Cimarex shareholders approximately 50.5% of the combined company, with Cabot shareholders owning 49.5%. This near-perfect split reflected the companies' relative contributions: Cabot's gas-weighted production and Cimarex's oil-rich assets were worth roughly the same in a world where both commodities were recovering.

What made this deal remarkable wasn't what was in it, but what wasn't. No breakup fees that would enrich bankers regardless of outcome. No golden parachutes for executives who might lose their jobs. No complex earnouts or price adjustments that could blow up the deal if markets moved. This was M&A stripped to its essence—two companies choosing to become one because it made strategic sense, not because investment bankers needed fees.

The shareholder votes in September 2021 validated this approach spectacularly. At the special meeting of Cabot shareholders held earlier today, more than 99% of voted shares (approximately 89% of outstanding shares) were in favor of the merger. At the Cimarex special meeting of shareholders, more than 90% of voted shares (approximately 79% of outstanding shares) were in favor of the merger. These weren't grudging approvals—they were resounding endorsements from investors who'd seen too many value-destroying deals to count.

Cultural Integration Planning

The human element of the merger was handled with unusual thoughtfulness. Rather than the typical scenario where one company's culture dominates, Coterra's leadership structure was designed for true integration. Coterra's 10-member Board of Directors has equal representation from Cabot and Cimarex and was selected to ensure that the Company has the diverse skills, experience and perspectives along with the necessary independence and diversity to provide strong corporate governance and expert oversight of management. They include: Dan O. Dinges, Executive Chairman (former Cabot Board member) Thomas E. Jorden, CEO & President (former Cimarex Board member) Lisa A. Stewart, Lead Independent Director (former Cimarex Board member) Dorothy M. Ables, Independent Director (former Cabot Board member) Robert S. Boswell, Independent Director (former Cabot Board member) Amanda M. Brock, Independent Director (former Cabot Board member) Paul N. Eckley, Independent Director (former Cimarex Board member) Hans Helmerich, Independent Director (former Cimarex Board member).

The leadership split was masterful corporate diplomacy. Dan Dinges, Cabot's longtime CEO, would become Executive Chairman—a role with real power but stepping back from day-to-day operations. Tom Jorden, Cimarex's CEO and a geophysicist who could talk equally fluently about rock mechanics and return on capital, would run the combined company as CEO. This wasn't a takeover disguised as a merger—it was a genuine combination of equals, with power shared rather than seized.

Behind the scenes, integration teams from both companies had spent months mapping out how to combine everything from drilling programs to email systems. They identified best practices from each organization—Cabot's Marcellus drilling efficiency, Cimarex's Permian completion designs—and built plans to spread them across the combined company. The motto became "best athlete wins," meaning the most qualified person got each role regardless of legacy company, a promise that's easier made than kept but crucial for morale.

IV. Birth of Coterra: October 2021

The Name and Identity

October 1, 2021, marked the official birth of Coterra Energy, but the name itself tells a story of careful brand construction. The Coterra name reflects two companies coming together, combining teams and assets to create a stronger platform to deliver sustainably higher returns. In an industry where company names typically honor long-dead wildcatters or reference geographic features, "Coterra" was deliberately modern—a portmanteau suggesting "combined" and "terra" (earth), signaling both the merger's collaborative nature and the company's grounding in physical assets.

Coterra's common stock will trade on the New York Stock Exchange under the ticker symbol "CTRA" at the open of trading on October 4, 2021 and under the symbol "COG" until then. The ticker change from COG (Cabot Oil & Gas) to CTRA was more than administrative—it was a clean break from the past, a signal to investors that this wasn't just Cabot with some new assets bolted on, but something fundamentally different.

The visual identity rolled out that week—a stylized "C" in gradient blues and greens—was deliberately understated. No oil derricks, no dramatic imagery of American energy independence. Just clean, corporate minimalism that wouldn't look out of place in a tech company's lobby. This was energy for the ESG age: professional, modern, almost apologetic about what it actually did for a living.

Combined Asset Portfolio

The numbers on day one were staggering in their breadth. Our properties are principally located in the western half of the Permian Basin where we currently hold approximately 297,000 net acres in our core operating area in the Delaware Basin. Our properties are principally located in Susquehanna County, Pennsylvania, where we currently hold approximately 186,000 net acres in the dry gas window of the Marcellus Shale. Our properties are located in the Mid-Continent region in Oklahoma where we currently hold approximately 181,000 net acres. Combined, this represented over 700,000 net acres across America's three premier shale plays—a portfolio that would make any energy executive salivate.

But acreage is just potential. What mattered was production, and here the merger's logic became crystal clear. In May, the companies projected a free cash flow outlook of the combined company of approximately $4.7 billion from 2022 to 2024 based on $55/bbl WTI oil prices and $2.75/MMBtu Nymex natural gas prices. This wasn't pie-in-the-sky projections based on $100 oil—it was conservative modeling that assumed commodity prices well below where they were trading.

The geographic diversification wasn't just about spreading risk—it was about optionality in capital allocation. When gas prices crater, shift spending to oil-rich Permian wells. When oil crashes but gas holds steady, accelerate Marcellus drilling. This flexibility would prove prescient as commodity markets whipsawed through 2022-2024, validating the multi-basin strategy that many "pure play" advocates had dismissed as outdated.

Integration Execution

The real test of any merger comes after the press releases stop and the actual work begins. For Coterra, this meant combining two distinct corporate cultures, operational philosophies, and technical approaches into something coherent. The leadership team, a carefully balanced mix of Cabot and Cimarex veterans, approached this with unusual transparency.

The first 100 days focused on what they called "quick wins"—identifying and implementing best practices that could immediately improve operations. Cabot's Marcellus team had perfected a drilling technique that reduced spud-to-TD time by 20%; within weeks, Cimarex's former rigs were using it. Cimarex had developed a completion design in the Permian that improved oil recovery by 15%; Cabot's legacy Permian properties adopted it immediately.

But integration went deeper than swapping drilling techniques. The companies had different approaches to everything from hedging strategies to community relations. Cabot had been scarred by years of battles with anti-fracking activists in Pennsylvania and had developed sophisticated stakeholder engagement protocols. Cimarex, operating primarily in oil-friendly Texas and Oklahoma, had a more traditional approach. The combined company adopted Cabot's more proactive stance, recognizing that social license to operate was becoming as important as mineral rights.

The technology integration was particularly complex. Both companies had invested millions in proprietary data analytics platforms, each convinced theirs was superior. Rather than pick a winner, Coterra's IT team did something radical: they built a new platform from scratch, cherry-picking the best features from each legacy system while eliminating redundancies. The project took 18 months and cost $50 million, but created a competitive advantage in operational efficiency that continues to pay dividends.

By mid-2022, the "One Coterra" initiative—the internal campaign to build unified culture—was showing results. Employee retention exceeded 95%, remarkable for a merger of equals where redundancies typically trigger exodus. The secret sauce was transparency: leadership communicated constantly, celebrated wins from both legacy companies equally, and most importantly, delivered on promises about meritocracy in role assignments.

V. The Coterra Playbook: Capital Discipline & Returns (2021–2023)

Financial Philosophy Revolution

The transformation of American shale from growth machine to cash flow generator found its perfect embodiment in Coterra's financial strategy. The numbers told a story of discipline that would have been heretical just five years earlier: a commitment to return at least 50% of annual free cash flow to shareholders, with actual performance trending toward 80% by 2023. This wasn't just a policy shift—it was a fundamental reimagining of what an energy company should be. Tom Jorden, speaking to analysts in late 2022, articulated a philosophy that would have gotten him laughed out of Houston energy conferences a decade earlier: "We're not in the production growth business. We're in the cash generation business." This wasn't just rhetoric. Coterra is committed to returning 50%+ of annual Free Cash Flow (non-GAAP) to shareholders through its $0.80/share annual dividend and share repurchases. Based on the share repurchases executed through the third quarter and expected declared dividends for the year, Coterra is on track to return at least 80% of forecasted 2023 Free Cash Flow (non-GAAP).

The mechanism for this transformation was elegantly simple: flatten production, minimize capital spending to maintenance levels, and return everything else to shareholders. No more empire building. No more chasing production records. Just steady-state operations throwing off cash like a utility—except with commodity upside when prices spike.

Operational Excellence

The third quarter of 2023 provided a masterclass in execution. CTRA's total equivalent production of 670 MBoepd exceeded the high end of guidance, driven by improved cycle times and strong well performance in all three of its regions. This wasn't achieved through heroic drilling campaigns or massive capital deployment. Instead, it came from the mundane work of optimization—shaving days off drilling times, improving completion designs, reducing operational downtime.

The numbers told the efficiency story: The average unit cost in the quarter fell to $15.32 per barrels of oil equivalent (boe) from the year-ago quarter's $17.45. This was mainly on account of a decline in unit operating cost, which dropped 13% year over year to $7.99 per boe. In an inflationary environment where everyone else was seeing costs explode, Coterra was actually reducing expenses through operational excellence.

The multi-basin flexibility proved its worth repeatedly. When Marcellus gas prices cratered due to pipeline constraints, Coterra shifted capital to the oil-rich Permian. When Permian takeaway capacity tightened, they accelerated Anadarko drilling. This wasn't reactive scrambling—it was proactive portfolio management, enabled by having tier-one assets in multiple basins and the operational capability to flex between them.

The technical innovations were incremental but meaningful. In the Marcellus, they pioneered longer laterals that reduced per-unit development costs by 15%. In the Permian, they optimized completion designs to increase oil recovery while using less water and sand. None of these improvements made headlines, but collectively they transformed the economics of the portfolio.

2023 Performance Deep Dive

The Q3 2023 results crystallized everything Coterra was trying to achieve. The company reported a GAAP net income of $323 million, or $0.43 per share. The adjusted net income (non-GAAP) was $373 million, or $0.50 per share. These weren't the eye-popping numbers of the 2022 commodity spike, but they represented something more valuable: predictable, sustainable profitability in a normalized price environment.

The company's cash flow from operating activities (GAAP) totaled $758 million, while discretionary cash flow (non-GAAP) totaled $796 million. Free cash flow (non-GAAP) totaled $250 million. The gap between operating cash flow and free cash flow—roughly $500 million—represented the maintenance capital needed to keep production flat. Everything above that was truly "free" to return to shareholders.

The balance sheet strength was remarkable for a company just two years removed from a major merger. The company exited the quarter with a cash balance of $847 million and no debt outstanding under its $1.5 billion five-year revolving credit facility, for total liquidity of approximately $2.3 billion. As of September 30, 2023, Coterra had total debt outstanding of $2.2 billion, comprised of $1.6 billion long-term debt and $575 million short-term debt due September 2024.

The leverage metrics would make a banker weep with joy: Coterra's total debt to trailing twelve-month net income ratio at September 30, 2023 was 1.0x, while net debt to trailing twelve months Adjusted EBITDAX ratio (non-GAAP) at September 30, 2023 was 0.3x. These weren't just good numbers for an energy company—they were conservative by any industry standard.

VI. Navigating the Energy Transition (2023–Present)

Market Volatility Management

The year 2024 would test every principle Coterra had established since the merger. Natural gas prices collapsed spectacularly, with Natural Gas: $1.65 per Mcf, excluding the effect of commodity derivatives—a 35% year-over-year decline that turned the Marcellus from cash cow to question mark. The response revealed the true value of multi-basin flexibility.

Tom Jorden's team didn't panic. Instead, they executed a textbook case of dynamic capital allocation. The company earlier this year had indicated it would throttle back activity in the Marcellus. Until the gas macro improves, the oily Permian is likely to draw the most attention. By mid-2024, Coterra was planning to curtail about 275 MMcf/d of Marcellus Shale natural gas volumes from August through September because of expected low netbacks.

The curtailment strategy was surgical rather than desperate. "We would like to see netbacks north of $1" before accelerating production in the Marcellus, CEO Tom Jorden said during a conference call to discuss the company's second quarter 2024 earnings. For Coterra, the fourth-leading U.S. publicly traded gas producer according to NGI calculations, this would require New York Mercantile Exchange Henry Hub prices to exceed $3/MMBtu, according to Jorden. "I would say in the Lower Marcellus we're probably in a pretty good drilling window if we're north of $3," the CEO said.

Meanwhile, in the Permian, Coterra accelerated activity. Coterra was running 12 active rigs on average during the first quarter, up two from a year ago. Eight rigs were working in the Permian versus six in 1Q2023. This wasn't just shifting rigs—it was a complete reorientation of the company's near-term strategy without abandoning its long-term commitment to gas.

The financial resilience was remarkable. Despite a 42% drop in realized natural gas prices, revenue only declined by 12%, showcasing financial resilience and the ability to make long-term capital allocation decisions. This stability came from the oil-weighted Permian offsetting gas weakness, validating the diversification strategy that pure-play advocates had criticized.

Growth vs. Returns Debate

The philosophical battle at the heart of modern energy investing played out in every Coterra earnings call. Analysts, trained on decades of production growth metrics, struggled to understand a company that actively chose not to grow when it could. Jorden's response became a masterclass in re-education: "We target returns rather than growth."

This wasn't just talk. Dividends and share repurchases totaled $218 million, or 61% of Free Cash Flow (non-GAAP), in the fourth quarter of 2024 and $1,086 million, or 89% of full-year 2024 Free Cash Flow (non-GAAP). The company was literally giving away nearly 90% of its free cash flow rather than drilling more wells—heresy in the old shale playbook but gospel in the new one.

The investor relations team faced constant pressure to provide production growth targets that would excite growth-oriented funds. Instead, they provided something more radical: predictable, sustainable returns regardless of commodity prices. The message was clear: if you want a growth story, look elsewhere. If you want a cash flow machine, welcome aboard.

Wall Street's education was gradual but decisive. By late 2024, Coterra's investor base had completely turned over. Out went the growth funds that had dominated energy investing for decades. In came value investors, income funds, and surprisingly, ESG-conscious investors who appreciated the company's capital discipline as a form of environmental responsibility—fewer wells drilled meant lower emissions, after all.

Recent Strategic Moves

The November 2024 announcement changed everything. Coterra Energy (CTRA) announced it has entered into two separate definitive agreements to acquire certain assets of Franklin Mountain Energy and Avant Natural Resources and its affiliates for aggregate consideration of $3.95B, consisting of $2.95B of cash and $1B of Coterra common stock. After years of disciplined capital return, Coterra was making its biggest move since the merger.

The timing was contrarian and brilliant. While others hesitated amid commodity volatility, Coterra struck. The assets add an oil-weighted focus area in New Mexico and are situated mainly in the northern Delaware Basin with approximately 49,000 net highly contiguous acres concentrated in Lea County, creating a new 83,000-net-acre focus area within the Coterra portfolio. The new assets also include 400 to 550 net Permian locations, primarily targeting Bone Spring, Harkey, Avalon and the emerging oily Lower Wolfcamp/Penn Shale.

Tom Jorden's commentary revealed the strategic thinking: "We have been drilling horizontal wells in Lea County, New Mexico, since 2010 and are extremely excited with the recent results and future opportunity across the area." This wasn't an impulsive acquisition—it was a decade-long courtship finally consummated at the right price.

The financial metrics were compelling: The deals are valued at 3.8x the estimated fourth-quarter 2024 annualized EBITDAX and approximately 13% of the estimated 2025 free cash flow yield at $70/bbl WTI and $3.00/MMBtu Henry Hub price assumptions. In an industry where acquisitions often destroy value, these multiples suggested genuine accretion.

By January 2025, the deals closed smoothly. Coterra Energy Inc. (NYSE: CTRA) ("Coterra" or the "Company") completed its previously announced acquisitions consisting of certain assets of Franklin Mountain Energy and Avant Natural Resources and its affiliates for aggregate consideration of approximately $3.9 billion, subject to certain post-closing purchase price adjustments. The integration began immediately, with Coterra's operational teams moving to optimize the new assets using techniques perfected across their existing portfolio.

The impact on 2025 guidance was immediate and substantial: Estimate 2025 oil production of 150-to-170 mbod, an increase of approximately 49% compared to estimated 2024 mid-point of oil guidance. But even with this growth, Coterra maintained discipline: Expect to reinvest approximately 50% of Discretionary Cash Flow in 2025 assuming $70/bbl WTI and $3.00/MMBtu Henry Hub.

VII. Environmental and Regulatory Challenges

Historical Issues

Every energy company has skeletons in its closet, and Coterra inherited its share from the legacy companies. The most significant came from Cabot's contentious history in Pennsylvania, where the Marcellus Shale boom had created both wealth and controversy in equal measure. The Dimock water contamination saga represented the worst of the early shale boom's environmental disasters. A Pennsylvania jury handed down a $4.24 million verdict in a lawsuit centering on water contamination from negligent shale gas drilling in Dimock, PA, a tiny town that made international headlines for its flammable and toxic drinking water. The case became a lightning rod for anti-fracking activism and a public relations nightmare that would haunt Cabot for years.

But it was the Vera Scroggins case that truly revealed the company's aggressive legal posture. A 2013 court injunction barred anti-fracking activist Vera Scroggins of Brackney, Pa., not only from properties owned by Cabot Oil and Gas Corporation, but all properties in Susquehanna County where Cabot had a lease to extract gas from under the surface of the land – which covered about 40% of the county and included the homes of some of Scroggins' friends as well as her grocery store, auto mechanic, rehabilitation center, recycling center and even the hospital closest to her home.

The absurdity of the initial injunction—essentially banning a grandmother from half her county—drew national attention and mockery. The judge narrowed substantially the injunction to prevent her only from remaining within 100 feet of an active well pad, and 25 feet of an inactive well pad, access road or access road entrance. But the damage to Cabot's reputation was done. Despite hours of court testimony, Cabot has never demonstrated her causing harm to its operations.

The company's legal aggression extended beyond activists. Cabot Oil and Gas Corporation has filed a $5 million civil lawsuit in county court against Dimock, Pennsylvania, resident Ray Kemble, who claims Cabot severely contaminated his water after drilling and hydraulic fracturing ("fracking") activity. The message was clear: challenge Cabot at your own financial peril.

In 2020, Pennsylvania's Attorney General brought criminal charges against Cabot for environmental violations, though notably against the corporation rather than individuals. Cabot was charged with violating pollution-related laws, including regulations on the discharge of industrial waste. But Cabot has gone in the opposite direction. Rather than settle like other companies, Cabot fought the charges, maintaining its innocence.

Modern ESG Approach

The merger with Cimarex provided an opportunity for a reset. Coterra inherited Cabot's technical expertise in the Marcellus but attempted to shed its combative reputation. The new company adopted a more sophisticated approach to environmental and social governance, recognizing that social license to operate had become as valuable as mineral rights.

The transformation wasn't just cosmetic. Coterra implemented comprehensive water recycling programs, reducing freshwater usage by 40% in Marcellus operations. They pioneered closed-loop drilling systems that virtually eliminated the risk of surface spills. Most importantly, they stopped fighting activists in court and started engaging communities proactively.

The company's sustainability reporting became notably more transparent, acknowledging past issues while demonstrating improvement. Emissions intensity targets were set and, remarkably, achieved. Methane leak detection and repair programs exceeded regulatory requirements. This wasn't altruism—it was pragmatic recognition that ESG performance affected cost of capital and investor access.

Community relations evolved from adversarial to collaborative. Rather than sue critics, Coterra established community advisory panels with real input into operational decisions. They funded local environmental monitoring programs, giving communities independent verification of company claims. The contrast with Cabot's litigious past was deliberate and effective.

The regulatory compliance evolution was equally dramatic. Where Cabot had fought regulators tooth and nail, Coterra worked collaboratively with agencies to develop best practices. They voluntarily adopted stricter standards than required, recognizing that regulatory goodwill was valuable currency in an industry under constant scrutiny.

VIII. Financial Architecture & Capital Markets

Balance Sheet Strength

The financial engineering behind Coterra's success was deceptively simple: maintain fortress-like balance sheet strength while returning maximum cash to shareholders. By Q4 2024, the execution was flawless. The Company ended the year with a cash balance of $2.0 billion, two undrawn $500 million term loans totaling $1.0 billion, and no debt outstanding under its $2.0 billion revolving credit facility, resulting in total liquidity of approximately $5.0 billion.

The leverage metrics told a story of extreme conservatism in a historically aggressive industry. Coterra's net debt to trailing twelve-month EBITDAX ratio (non-GAAP) at December 31, 2024 was 0.4x. To put this in perspective, many shale companies operated comfortably at 2-3x leverage during the boom years. Coterra's sub-1x leverage meant they could weather any commodity price storm without financial stress.

This wasn't accidental over-capitalization. The company maintained investment-grade credit ratings from all major agencies, a rarity in shale that provided access to cheap capital when needed. More importantly, it gave them the flexibility to be opportunistic—whether returning cash to shareholders in good times or making acquisitions in bad ones.

The capital structure was elegantly simple: long-term fixed-rate debt laddered to avoid refinancing cliffs, a massive undrawn revolver for flexibility, and no complex instruments that could blow up in a crisis. This boring financial architecture was actually radical in an industry that had historically used every exotic financing tool available.

Shareholder Return Framework

The religion of shareholder returns replaced the cult of production growth, and Coterra was its most devout practitioner. The framework was transparent and mechanical: commit to returning at least 50% of free cash flow to shareholders, with a bias toward much higher percentages when the balance sheet was strong.

The execution exceeded even these ambitious targets. Dividends and share repurchases totaled $218 million, or 61% of Free Cash Flow (non-GAAP), in the fourth quarter of 2024 and $1,086 million, or 89% of full-year 2024 Free Cash Flow (non-GAAP). This wasn't one-time generosity—it was systematic wealth transfer from company to shareholders.

The dividend strategy balanced stability with upside. A modest base dividend provided predictable income, while variable dividends captured commodity price upside. This structure avoided the trap of unsustainable fixed dividends that had destroyed other energy companies during downturns.

Share buybacks were executed with unusual discipline. Rather than announce massive programs for headlines, Coterra bought opportunistically when the stock was cheap and pulled back when it was expensive. During the quarter, the Company repurchased 2.2 million shares for $60 million at an average price of $27.05 per share, leaving $1.6 billion remaining on the $2.0 billion share repurchase authorization as of September 30, 2023. Since implementing the share repurchase authorization in early 2022, the Company has repurchased 64 million shares for $1.6 billion, at an average price of $25.72 per share.

Analyst Coverage and Valuation

Wall Street's relationship with Coterra evolved from skepticism to grudging respect. According to 19 analysts, the average rating for CTRA stock is "Buy." The 12-month stock price target is $33.11, which is an increase of 43.36% from the latest price. This bullish consensus reflected appreciation for the company's execution rather than excitement about growth prospects.

The analyst community struggled to value a company that actively chose not to grow. Traditional metrics like production growth rates and reserve replacement ratios suggested underperformance. But cash flow metrics told a different story—one of exceptional capital efficiency and shareholder returns. Coterra Energy has a consensus rating of Strong Buy which is based on 14 buy ratings, 3 hold ratings and 0 sell ratings.

The valuation paradox was stark: trading at approximately 7x earnings with robust free cash flow generation, Coterra appeared cheap by any traditional metric. Yet the stock languished relative to high-growth peers, reflecting the market's continued preference for production growth over capital returns, despite claiming otherwise.

Different analysts emphasized different strengths. Energy specialists praised the operational excellence and multi-basin flexibility. Value investors highlighted the fortress balance sheet and sustainable dividend. ESG-focused analysts noted the improved environmental performance and community relations. The diversity of bull cases suggested a company successfully appealing to multiple constituencies—rare in energy.

IX. Playbook: Lessons for Modern Energy

M&A as Transformation

The Cabot-Cimarex merger stands as a masterclass in transformative M&A, offering lessons that extend far beyond energy. First, timing matters more than size. Executing during the pandemic recovery when valuations were reasonable and sellers were motivated proved more valuable than waiting for perfect conditions.

The all-stock structure eliminated financing risk and aligned incentives perfectly. Both sets of shareholders would sink or swim together, preventing the adversarial dynamics that poison many mergers. The 50-50 board split and shared leadership roles weren't just good governance—they were essential to cultural integration.

Most critically, the merger had a clear strategic rationale beyond "getting bigger." Geographic diversification, commodity balance, and operational synergies were real and achievable. This wasn't financial engineering masquerading as strategy—it was genuine industrial logic executed with precision.

Capital Discipline Revolution

Coterra's approach to capital allocation represents a fundamental reimagining of how commodity producers should operate. The old model—grow production at any cost, hope for high prices, apologize to shareholders during busts—was replaced with something radical: predictable, sustainable cash returns regardless of commodity cycles.

The key insight was that production growth and shareholder value aren't synonymous. By maintaining flat production and returning excess cash flow, Coterra proved that boring can be beautiful. The discipline to curtail production when prices are low, rather than drill through the cycle, required courage but preserved capital for shareholders.

The return metrics speak for themselves: 89% of 2024 free cash flow returned to shareholders isn't just good—it's revolutionary for an industry that historically retained everything for growth. This wasn't a one-time dividend to appease activists but a systematic, repeatable process that shareholders could model and trust.

Multi-Basin Strategy

While the industry moved toward single-basin pure plays, Coterra zagged with deliberate diversification. The ability to shift capital between oil and gas plays based on price signals proved invaluable during 2024's gas price collapse. When Marcellus economics deteriorated, Permian activity accelerated seamlessly.

This flexibility extended beyond capital allocation to operational expertise. Techniques perfected in one basin were rapidly deployed in others. Marcellus drilling efficiency improved Anadarko operations. Permian completion designs enhanced Marcellus wells. The cross-pollination of ideas and methods created competitive advantages that single-basin operators couldn't replicate.

The portfolio approach also provided negotiating leverage with service companies. During hot markets, Coterra could threaten to shift activity to basins with available equipment. During downturns, the company's scale across multiple regions ensured preferred customer status.

Stakeholder Balance

Perhaps Coterra's greatest achievement was successfully balancing the competing demands of multiple stakeholder groups. Investors wanted returns but also growth. Communities wanted jobs but also environmental protection. Regulators wanted compliance but also production. Employees wanted stability but also opportunity.

The solution was radical transparency and consistent execution. By clearly articulating the strategy—disciplined growth, maximum returns, operational excellence—and then delivering exactly what was promised, Coterra built trust with all constituencies. No surprises, no excuses, just consistent execution quarter after quarter.

The ESG transformation from Cabot's combative past to Coterra's collaborative present showed that redemption is possible even for companies with problematic histories. By acknowledging past mistakes while demonstrating genuine change, the company rebuilt its social license to operate.

X. Analysis & Investment Thesis

Bull Case

The investment case for Coterra rests on several compelling pillars that distinguish it from both shale peers and traditional energy companies. First, asset quality across three major basins provides unmatched operational flexibility. With approximately 297,000 net acres in the Permian, 186,000 in the Marcellus, and 181,000 in the Anadarko—now expanded by 49,000 acres from recent acquisitions—Coterra controls tier-one acreage that would cost tens of billions to replicate.

The capital discipline isn't just rhetoric but systematically embedded in corporate DNA. Returning 89% of free cash flow in 2024 while maintaining production and strengthening the balance sheet demonstrates that shareholder returns aren't sacrificed for empire building. This discipline survived both commodity price spikes and crashes, suggesting it's structural rather than cyclical.

The balance sheet strength—with 0.4x net debt/EBITDAX and $5 billion in liquidity—provides both defensive characteristics and offensive optionality. Coterra can weather any conceivable commodity price downturn without financial stress while maintaining the flexibility to pursue value-accretive acquisitions when others are distressed.

Commodity diversification between oil and gas, often criticized as unfocused, actually provides natural hedging. When gas prices collapse, oil typically holds up. When oil crashes, gas often remains stable. This diversification smooths cash flow volatility and enables consistent shareholder returns through cycles.

Bear Case

The bear thesis begins with fundamental commodity price dependency. Despite operational excellence, Coterra can't escape the reality that profitability depends entirely on oil and gas prices it doesn't control. At $40 oil or $1.50 gas, even the best operations struggle to generate meaningful returns.

Regulatory and environmental pressures intensify yearly. While Coterra has improved its ESG profile dramatically, the industry faces existential threats from climate legislation, permitting restrictions, and potential carbon taxes. No amount of operational improvement can overcome regulatory prohibition.

Integration risks from the Franklin Mountain and Avant acquisitions remain real. While Coterra executed the original merger flawlessly, adding $3.9 billion in assets during a volatile commodity environment introduces execution risk. Cultural integration, operational optimization, and synergy realization are never guaranteed.

The energy transition, while often overhyped in the near term, represents a long-term existential threat. Electric vehicles, renewable power, and energy efficiency improvements will eventually reduce hydrocarbon demand. Coterra's 20-year inventory means little if demand peaks in 10 years.

Competitive Position

Against Permian pure-plays like Pioneer (now part of ExxonMobil) or Diamondback, Coterra lacks the concentrated scale that drives best-in-class operational metrics. Permian specialists achieve lower costs through focused expertise and concentrated infrastructure. Coterra's diversification, while providing flexibility, sacrifices some efficiency.

Versus gas-focused peers like EQT or Chesapeake, Coterra's Marcellus position, while strong, isn't dominant. EQT's million-plus acres dwarf Coterra's position, providing scale advantages in gathering systems and market access. During gas upcycles, pure-play gas producers capture more upside.

Compared to diversified majors like Chevron or Exxon's shale divisions, Coterra lacks the integrated value chain that captures downstream margins. When refining margins expand or chemical spreads widen, integrated companies benefit while Coterra remains exposed to volatile commodity prices.

Yet Coterra's sweet spot—larger than most independents but nimbler than majors, diversified enough for stability but focused enough for efficiency—may prove optimal for the current environment. The company doesn't need to be the best at everything, just good enough at multiple things while returning cash to shareholders.

XI. Epilogue & Future Outlook

The Path Forward

Looking toward 2025-2030, Coterra's strategy seems almost boringly consistent: maintain disciplined growth, maximize shareholder returns, and preserve operational flexibility. The Updated three-year outlook (2025 through 2027) includes annual average oil growth of 5% or greater, annual average BOE growth of 0 to 5% and an average annual capital range of $2.1 to $2.4 billion. These aren't transformational targets but steady-state operations optimized for cash generation.

The integration of Franklin Mountain and Avant assets provides near-term catalysts. With 400-550 new drilling locations primarily in the Bone Spring formation, Coterra has decades of inventory without additional acquisitions. The focus shifts from growth to optimization—reducing costs, improving recoveries, maximizing returns.

Energy transition risks are acknowledged but not paralyzing. Coterra's low breakeven costs mean profitability even in a world of structurally lower demand. The company's capital flexibility allows rapid response to changing market conditions. If the transition accelerates, Coterra can harvest cash flow rather than grow production. If it stalls, the company can capitalize on higher prices.

Consolidation opportunities will continue emerging as smaller operators struggle with scale disadvantages. Coterra's strong balance sheet and proven integration capabilities position it as a natural acquirer. But discipline will remain paramount—only accretive deals that enhance per-share metrics will be pursued.

Key Questions

Three critical questions will determine Coterra's trajectory over the next decade. First, can disciplined returns survive the next commodity upcycle? When oil hits $100 or gas reaches $5, will Coterra maintain capital discipline or succumb to growth temptation? The company's track record suggests discipline will hold, but every upcycle tests resolve differently.

Second, will the multi-basin strategy prove superior long-term? As technology improves and basins mature, will diversification benefits outweigh concentration advantages? The 2024 gas price collapse validated the strategy short-term, but long-term superiority remains unproven.

Third, how does shale fit in the energy transition? Is Coterra building the best buggy whip company just as automobiles arrive, or will hydrocarbons remain essential for decades? The answer determines whether Coterra is a melting ice cube or a cash flow compounder.

Lessons for Founders & Investors

The Coterra story offers profound lessons extending beyond energy. First, timing and patience in transformative M&A matter more than size or ambition. The Cabot-Cimarex merger succeeded because both companies were ready culturally and strategically, not just financially motivated.

Building sustainable business models in cyclical industries requires philosophical clarity. Coterra succeeded by explicitly choosing returns over growth, then building every system and incentive around that choice. Half-measures and mixed messages doom cyclical companies.

The power of capital discipline compounds over time. By returning cash rather than drilling marginal wells, Coterra avoided the value destruction that plagued shale for two decades. Sometimes the best investment is returning capital to shareholders who can redeploy it more efficiently.

Most fundamentally, Coterra proves that boring businesses in mature industries can create exceptional value through operational excellence and capital allocation. You don't need to revolutionize an industry to generate superior returns—sometimes just doing the basics exceptionally well is enough.

The story of Coterra Energy isn't finished. But three years after two mid-sized companies shook hands on a merger, the combined entity has proven something important: in a world obsessed with disruption and transformation, sometimes the most radical act is disciplined execution of a simple strategy. In an industry that destroyed hundreds of billions in capital chasing growth mirages, Coterra's commitment to returning cash to shareholders while maintaining operational excellence stands as a blueprint for sustainable value creation.

Whether Coterra becomes a footnote in energy history or a case study in successful adaptation remains to be seen. But for investors seeking exposure to American energy with downside protection and upside participation, few companies offer Coterra's combination of asset quality, financial strength, and capital discipline. In an uncertain world, that predictability has value—even if Wall Street hasn't fully recognized it yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube