Constellation Software Inc.: The Ultimate Compounding Machine

I. Introduction & Episode Roadmap (00:00 – 00:10)

On the morning of May 13, 2026, a Constellation Software conference call opened the way it always has: with almost no theatre. No slide deck. No scripted CEO monologue about "transformational quarters." Just a soft-spoken man named Mark Miller telling analysts he had "both Bernie and Jamal" with him to take questions, and reminding everyone the annual meeting was that Friday.1 Within minutes an analyst from BMO used a word that would have been unthinkable in the company's serene past: the "SaaSpocalypse." He wanted to know whether the great 2025–26 software crash had finally dragged private-market valuations down to earth. Miller's answer was almost bored. He and Bernie had just been chatting about it before the call, he said. "Not really."1

That exchange captures the strange moment Constellation Software finds itself in. For two decades this was the quietest great compounder in the Western world — an obscure Toronto holding company that bought tiny, boring software businesses nobody else wanted and turned them into one of the best-performing stocks on the planet. An investor who bought at the 2006 initial public offering, at seventeen Canadian dollars a share, and simply held, would have watched those shares climb more than a hundredfold — a compound annual return of roughly 30% that, over the period, out-ran Microsoft, Apple, and Berkshire Hathaway.2018 The company did it while employing a corporate head office of a few dozen people to oversee, eventually, more than a thousand separate software businesses across the globe.17

Here is the tension that makes 2026 the right time to tell this story. At its 2025 peak the stock traded above CAD 5,000 a share, valuing the company north of CAD 100 billion. As this is written in July 2026, it changes hands closer to CAD 2,700 — a drawdown of roughly 45% from the 52-week high, and a one-year total return of about negative 50%.13 The market that once treated Constellation as a bond-like certainty has abruptly re-rated it as an AI casualty, on fear that artificial intelligence will let customers build their own software or let AI-native upstarts undercut legacy vendors on price.13

For all the drama in the share price, the operating machine did not skip a beat. In the first quarter of 2026 — Miller's first full reporting period in the President's chair — revenue rose about 20% to roughly USD 3.2 billion, net income more than doubled to USD 367 million, and free cash flow available to shareholders grew 44% to USD 733 million, all while the company kept deploying capital into acquisitions and declared its regular USD 1.00 quarterly dividend.1 That is the paradox an investor has to hold in mind through this entire story: a business still executing at full throttle, and a market that has decided the future may look nothing like the past. Which of those two signals to believe is, in the end, the whole question.

And the timing could not be more pointed, because the man who built the whole machine is gone. In September 2025, founder Mark Leonard resigned as President "for health reasons, effective immediately."2 In March 2026 he announced he would not stand for re-election to the board, ending his directorship at the May 15, 2026 annual meeting.4 Into his chair stepped Mark Miller — not a celebrity hire but the ultimate insider, whose own company, Trapeze Group, was the very first business Constellation ever acquired, back in 1995.5 Note the title carefully, because it tells you something about the culture: Miller is President and Chief Operating Officer. Constellation does not use the title "Chief Executive Officer" at all.5

This episode maps four themes. First, the strange unit economics of Vertical Market Software (VMS) — why "boring, niche, and slow-growing" turned out to be a cash-generating toll road. Second, the playbook of extreme decentralization, in which capital is centralized to the point of obsession and everything else is pushed as far away from head office as possible. Third, the "magnetism of hurdle rates" — the scaling dilemma that, in a landmark 2021 letter, forced Leonard to stop hoarding cash for special dividends and to lower his return bar for mega-deals.7 And fourth, the spin-out playbook that created public compounders like Topicus and Lumine.810 Threaded through all of it is the question every long-term owner is now asking: can a machine built in one man's image keep running once he has left the building?

II. The Genesis: Mark Leonard's Epiphany & The VMS Discovery (00:10 – 00:25)

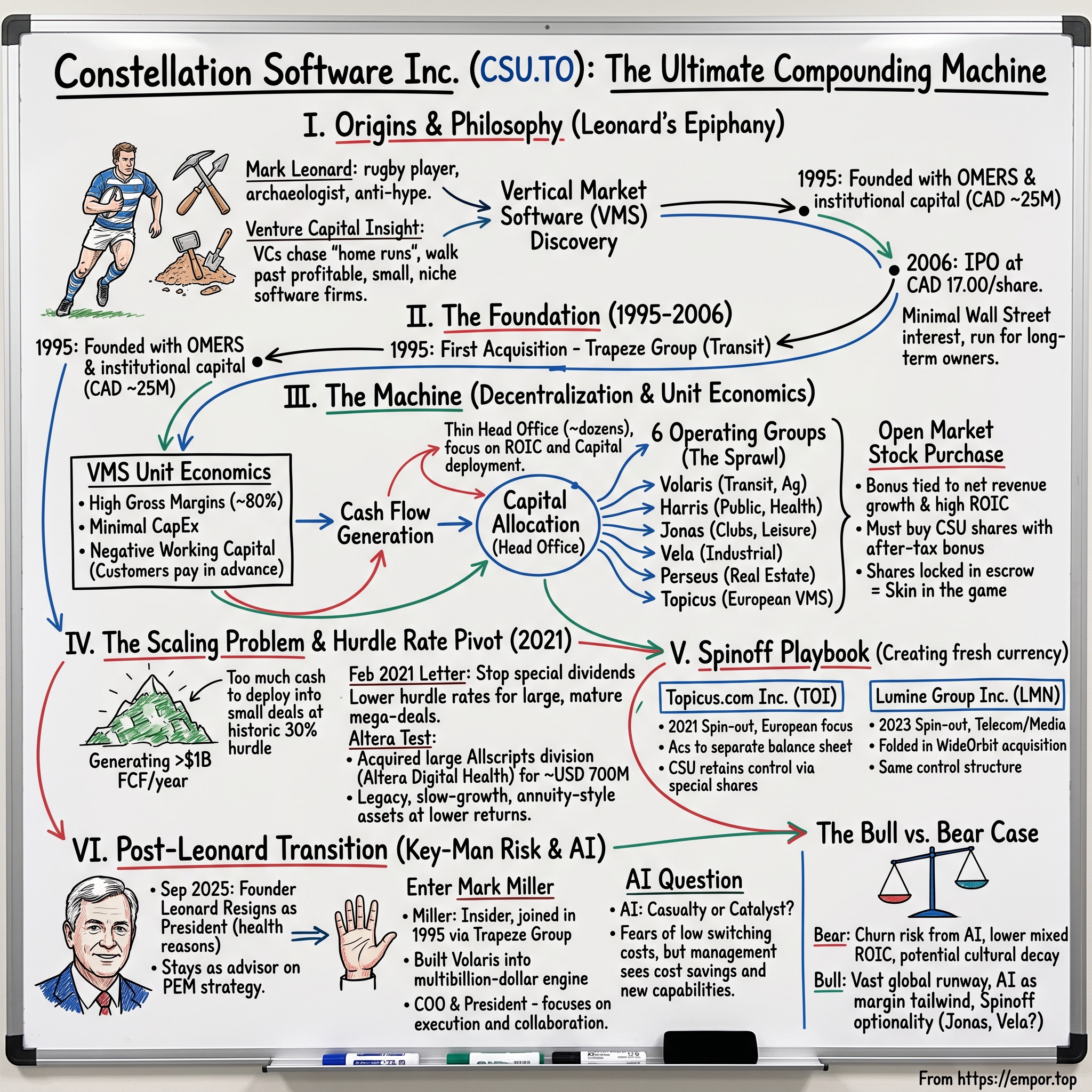

To understand Constellation you first have to understand that its founder did not look, sound, or behave like a technology mogul. Mark Leonard studied archaeology before business. He had been a collegiate rugby player. He was, by every account of those who dealt with him, allergic to the ordinary rituals of public-company life — the roadshows, the guidance, the CNBC hits. For years he declined to be photographed, and his annual letters to shareholders — archived and studied like scripture by a generation of investors — read less like investor-relations documents than like a philosopher-engineer thinking aloud about return on capital.15 This was a man temperamentally incapable of hype, running the most hyped-about compounder of his generation.

The Venture Capitalist's Blind Spot

Before Constellation, Leonard spent his formative professional years in venture capital in Toronto, and it was that vantage point — watching where the money and the talent actually flowed — that produced his defining insight. The specific mechanism he noticed was about attention and economics, not genius. A venture fund with a large pool to deploy cannot be bothered with a software company that will only ever be worth thirty or forty million dollars; the fund's math demands outliers, so it pours money and people into the tiny fraction of bets that might return the whole fund and ignores everything else. But that "everything else" — the thousands of small, profitable, deeply entrenched vertical-software companies quietly serving dentists, funeral homes, marinas, transit agencies, and municipalities — was, in aggregate, an enormous and permanently underpriced asset class hiding in plain sight.17

Leonard's formative years were spent as a venture capitalist at a Toronto firm, and it was there, watching how the VC industry actually behaved, that he had the insight that would define the rest of his life. Venture capital, he observed, spent almost all of its time and money chasing "home runs" — horizontal software with enormous addressable markets, the next platform that might be worth billions. In doing so, it walked straight past a vast population of small, unglamorous, highly specialized software companies serving narrow industries. They would never be home runs. But they threw off cash, almost never lost customers, and could be bought cheaply precisely because nobody else was looking.17

That was the thesis: niche is a feature, not a bug. Consider the kind of software Constellation would come to own — programs that run a city's water-billing system, that manage a Dutch notary's office, that schedule a municipal bus fleet, that keep the books for golf clubs and health clubs. To a Silicon Valley investor these markets are laughably small. But smallness is exactly what makes them defensible. If a single application runs the billing for a mid-sized utility, ripping it out is not a software decision — it is an operational risk that can take down the revenue collection of an essential service. So customers stay, and stay, and stay. Constellation's businesses have historically retained the overwhelming majority of their maintenance and subscription revenue year after year, with attrition low enough that the base compounds quietly on its own.17

The second half of the thesis is about who won't show up to compete. Oracle and Salesforce are not going to build a bespoke product for a global market worth twenty or thirty million dollars a year; the engineering and sales cost could never be justified against a prize that small. So the niche incumbent — often the company that has served that industry for decades — faces no serious threat from big technology, and enjoys quiet, durable pricing power. High switching costs on one side, an absence of well-resourced competitors on the other. That combination is the entire economic foundation on which everything else was built.

Leonard's genuinely radical move was to build an institution designed to do the boring thing the whole venture industry was structurally incapable of doing: buy the singles and the doubles — thousands of them — and never sell. Where a venture capitalist chases the one company that becomes a thousand-bagger, Constellation would assemble a portfolio of companies that each returned a reliable, unspectacular multiple of their purchase price in cash, and let the sheer number of them compound. It is a temperamental inversion as much as a financial one. It requires patience where the industry prized urgency, thrift where the industry prized swagger, and a willingness to be permanently unfashionable. That temperament, more than any spreadsheet, is what the rest of this story is really about.

Founding, and the Eleven Quiet Years

Leonard founded the company in 1995, backed by a small group of institutional investors that included the Ontario pension manager OMERS.20 The initial capital pool is commonly reported at around CAD 25 million, though that precise figure is not confirmed in primary filings.17 The first acquisition, that same year, was Trapeze Group, a maker of software for transit and transportation agencies.5 It was a fitting inaugural purchase: mission-critical, deeply embedded, utterly unglamorous. The template was set on day one.

The eleven years between founding and IPO were the laboratory. Out of the public eye, Leonard and his early lieutenants learned the unglamorous craft that no business school teaches: how to buy a founder's life's work without destroying it, how much autonomy to grant and how much accountability to demand, how to turn the messy particulars of a hundred small deals into a repeatable discipline. By the time the company went public, the essential machine already existed — which is why the IPO functioned less as a fundraising event than as a formality that happened to make the shares liquid. The company did not need the market's money; it needed only to be left alone to compound, and it structured its entire relationship with public investors around that preference.

The company stayed private for eleven years, refining its craft out of the spotlight, before listing on the Toronto Stock Exchange in 2006 at CAD 17.00 per share.20 What is striking is how Leonard treated the IPO — not as a triumph to be sold, but as a mild inconvenience to be minimized. He was famously uninterested in courting Wall Street, disdained the ritual of quarterly guidance, and made clear he would run the business for owners who thought in decades, not quarters. That posture — genuinely unusual for a newly public company — set a tone that would insulate the strategy from short-term market pressure for the next twenty years. The question was whether the elegant thesis could be turned into a repeatable industrial process. That is where the machine comes in.

III. The VMS Blueprint & Unit Economics (00:25 – 00:45)

Picture the cash cycle of a typical Constellation business and you begin to see why the model works so well. A small software company sells mission-critical software to, say, a few hundred municipal clients. Those clients pay their annual maintenance and subscription fees in advance — often before a single hour of support has been delivered that year. Gross margins on that software run above 80%, because once the code is written, serving one more customer costs almost nothing.14 Capital expenditure is trivial; this is not a business of factories and inventory but of engineers and renewal invoices. The result is a company that generates cash almost mechanically, funded in part by its own customers' prepayments.

That last point deserves emphasis, because it is the quiet engine of the entire enterprise: negative working capital. When customers pay ahead, the business collects money before it incurs the cost of serving them, giving it an interest-free source of float. Constellation's consolidated balance sheet has for years carried negative working capital, a structural feature that lets deferred revenue help finance the next acquisition rather than requiring the parent to raise fresh capital.14 In effect, the customers of the businesses Constellation already owns help pay for the businesses it is about to buy. That is capital efficiency of an unusual kind, and it compounds.

The Annuity Underneath

It is worth dwelling on how durable that cash is, because durability is the whole investment case. A typical business unit's revenue is dominated by recurring maintenance and subscription fees that customers renew almost reflexively, year after year, because the software is woven into how they operate. When the installed base barely churns and prices tick up a few points annually, revenue has a gravitational tendency to grind higher on its own — slowly, unspectacularly, but with something close to the reliability of a utility bill. That is why Constellation can pay what look like full prices for tiny software companies and still earn high returns on the cash it deploys: it is buying an annuity with a long tail and a modest built-in escalator, not gambling on a breakout product. The trade-off, which the bears will press later, is that annuities do not grow fast — the organic engine underneath all this is, by design, slow.

Six Groups, One Behavior

Now multiply that single business by more than a thousand, and organize the sprawl. Constellation divides its empire into six autonomous Operating Groups, each a mini-conglomerate with its own leadership, culture, and acquisition pipeline.5 Volaris, the oldest, grew out of that first Trapeze deal and concentrates on transit, logistics, agriculture, and infrastructure. Harris focuses on utilities, the public sector, and healthcare. Jonas serves club management, leisure, fitness, and hospitality. Vela covers industrial niches — oil and gas, mining, manufacturing. Perseus targets homebuilding, real estate, and financial services. And Topicus, now separately listed, is the European platform. Beneath these six sit hundreds of individual business units, each typically retaining the brand and identity it had before Constellation bought it.5

Each group has developed its own dialect of the same language. Harris, built around utilities and the public sector, became known for buying government and healthcare software that practically never gets displaced once installed — the kind of system a water authority or a county government runs for twenty years and dreads ever touching. Jonas turned the unglamorous worlds of country clubs, fitness centers, and hospitality into a sprawling recurring-revenue base. Vela went deep into the industrial economy — energy, mining, manufacturing — where a software failure is measured in shut-down production lines. The verticals could hardly be more different, but the underlying business is identical in every case: mission-critical software, fragmented customers, minimal competition, and a founder eventually looking for a home for the company they spent a career building.

To grasp how far the decentralization runs, consider the arithmetic of attention. If head office truly has only a few dozen people and the group owns well over a thousand businesses, then no one at the center could possibly know the product roadmap of any single unit — and that is precisely the point.17 The operating groups function as intermediate holding companies, each replicating the parent's capital-allocation discipline one level down; beneath them, portfolio managers oversee clusters of business units. It is a fractal structure: the same handful of behaviors — hunt for deals, hold managers to returns on capital, force reinvestment or send the surplus cash upward — repeats at every level, from the twenty-person head office to the two-person software company in a provincial town. Complexity is managed not by controlling it from the center but by pushing identical incentives downward until the system very nearly runs itself.

Capital In, Everything Else Delegated

The division of labor between the center and the periphery is the crux of the design, and it is almost the inverse of a normal corporation. At most companies, headquarters accumulates functions — marketing, product strategy, sales oversight — and pushes budgets down. At Constellation, head office does essentially one thing: allocate capital. It monitors returns, structures debt and taxes, and decides where the cash generated across the empire should be reinvested. Everything else — pricing, product roadmaps, hiring, which customers to chase, how to run the business day to day — is delegated entirely to the business-unit level.17 The corporate office famously numbers only a few dozen people, an almost comically thin layer atop a multibillion-dollar revenue base.17

What does this buy, analytically? It attacks the disease that kills most acquirers: the cost and bureaucracy of integration. And it turns the parent into something closer to an internal capital market than an operating company — a machine whose core competence is judging which small software businesses will earn high returns on the cash deployed into them. The financials of recent years show the scale this reached: Constellation's revenue grew from roughly USD 6.6 billion in 2022 to about USD 8.4 billion in 2023, then USD 10.1 billion in 2024, and USD 11.6 billion in 2025 — the last of those up about 15% year on year, of which only three to four percentage points was organic growth in the existing businesses, the rest bought.141 The company's own headline measure of free cash flow available to shareholders reached roughly USD 1.7 billion in 2025.1 Those are the numbers of a company that has industrialized the acquisition of small software companies. But numbers like that raise an obvious question — how do you keep a thousand far-flung managers pulling in the same direction when head office refuses to manage them? The answer is one of the most distinctive incentive systems in corporate finance.

IV. The Decentralized Machine & The Open-Market Stock Incentive (00:45 – 01:10)

Start with a puzzle that has buried countless roll-ups. A company buys dozens of small businesses, tries to "unlock synergies" by centralizing their operations, and slowly smothers the very qualities — closeness to customers, entrepreneurial urgency, local knowledge — that made those businesses worth buying. The corporate layer swells, decisions slow, founders leave, and the acquired companies decay into mediocrity. Constellation's counter-intuitive escape from this trap is to refuse the premise. It does not integrate. An acquired business generally keeps its name, its management, its product, and its way of doing things. Its manager is treated less like a middle manager and more like an independent chief executive, responsible above all for the return earned on the capital in their business.17

No Bankers, Just Operators

This is why the company can absorb hundreds of acquisitions without collapsing under its own weight: there is almost nothing to absorb. But autonomy without accountability is just anarchy, so the discipline comes from two directions. The first is measurement. Business-unit leaders are held to account for organic revenue growth and for return on invested capital, the twin metrics that reveal whether a business is both growing and deploying cash well. The second is sourcing, and here the design is genuinely unusual: mergers and acquisitions are not run out of a central deal team staffed by bankers. Deal-hunting is pushed down into the operating groups, where associates and managers cultivate relationships with the founders of target companies — often for years — building a proprietary database of tens of thousands of VMS businesses worldwide, tracked patiently until an owner is finally ready to sell.19 On the Q1 2026 call, Chief Investment Officer Bernard Anzarouth described the rhythm plainly: the flow of deals "just comes and goes up and down as the market evolves," neither more nor less than usual, a steady patient harvest rather than a campaign.1

The absence of bankers is not a cost-saving quirk; it is part of the moat. Because deal origination lives inside the operating groups, the people hunting for acquisitions are the same people who understand the vertical intimately and who will still be there years later to oversee whatever they buy. They are not incentivized to close a transaction and move on, as an intermediary is, but to be right about a business over a decade. This also shapes how founders experience selling: they are negotiating not with a private-equity associate modeling a five-year exit but with an operator who intends to own the company forever. On the same call, Miller made a revealing point about how this capability has matured — Constellation now has "better talent to work on those larger transactions" than it did five or ten years ago, deals that are "complicated," with "some hair on them," often multi-geography carve-outs from big corporations, which is why the company increasingly finds itself "on the field" competing for assets it once would have watched from the sidelines.1

Skin in the Game, Bought at Market

Then there is the compensation system, which may be the single most-copied and least-successfully-imitated feature of the company. Constellation does not hand out dilutive stock options — the standard Silicon Valley tool that Leonard viewed with suspicion. Instead, senior managers earn bonuses tied to a formula rewarding net revenue growth and returns on capital above a hurdle. The twist is what they must do with the money. A large portion of any bonus above a threshold — often half or more — must be used to buy Constellation shares on the open market, at prevailing prices, with those shares then locked in escrow for several years.18

The formula rewards two things that can pull against each other — growth and returns on capital — which forces every manager to internalize the central tension of the whole company: growth that destroys returns earns nothing, and returns hoarded without growth earn nothing either. The escrow requirement then converts paper bonuses into locked, at-risk equity. Contrast this with the Silicon Valley norm, where options are granted at a low strike, cost the employee nothing, and pay off richly if the stock rises while costing nothing if it falls — a structure that quietly rewards volatility and dilutes existing owners. Constellation's managers, by contrast, can lose real money they have already earned. That asymmetry is deliberate: it selects for people who behave like owners because, functionally, they have been turned into owners against their own short-term liquidity.

Sit with why that design is so powerful. Because managers buy real shares with real after-tax bonus money, at market prices, they feel dilution and drawdowns exactly as outside shareholders do; there is no free lottery ticket handed out at a discount. Because the shares are escrowed for years, managers are financially chained to the long-term compounding of the whole enterprise, not just their own unit's next quarter. Over two decades this quietly minted a class of manager-owners — hundreds of operators across the world who became wealthy not by cashing out but by continuing to own the parent. It is alignment engineered into the plumbing rather than preached from the stage. The stress test of that culture is arriving now, and management knows it. Asked on the Q1 2026 call whether the plan might be softened after the share-price collapse, CFO Jamal Baksh was flat: no changes, the formula stays, "we still buy shares in the market, the same way we always have," and he added — with the stock down by half — "I'd say this is a great buying opportunity."1 Whether that conviction holds across a thousand managers watching their escrowed shares sink is one of the real open questions of the post-Leonard era. But before we get to succession, we have to confront the problem success itself created.

V. The Scaling Dilemma & The 2021 Hurdle Rate Pivot (01:10 – 01:35)

Every great capital allocator eventually meets the same enemy, and it is not competition — it is arithmetic. In Constellation's early years the math was a joy. The company might generate fifty million dollars of free cash and sprinkle it across fifteen or twenty tiny acquisitions, each bought cheaply enough to earn internal rates of return in the twenties or thirties. Small deals, high returns, easy redeployment. The compounding took care of itself. But success is corrosive to that model in a specific way: as the cash flow grows, the same strategy requires either far more deals or far bigger ones, and both come at a cost.

The Law of Large Numbers

By the early 2020s the problem had become acute. Constellation was generating well over a billion dollars of free cash flow a year and heading higher.14 Deploying that much money into three- and five-million-dollar acquisitions would have required doing hundreds of transactions annually — a volume that strains even a decentralized deal machine, and that guarantees a long tail of ever-smaller, ever-harder-to-find targets. The cash was piling up faster than the traditional playbook could spend it at the traditional returns. The company faced the classic high-class problem of the successful compounder: what do you do when you can no longer reinvest all your cash at your historic rate of return?

The February 2021 Letter

Leonard's answer came in a landmark letter to shareholders released on February 15, 2021 — a document that quietly changed the company's trajectory.7 Two decisions stand out. The first, in his own words, was blunt: "The obvious first step is to stop special dividends in all but the most compelling circumstances."20 Historically, when Constellation could not deploy its excess cash at high hurdle rates, it had returned some of it to shareholders; now it would hold and reinvest more of it internally, and Leonard went so far as to warn that even the regular dividend might eventually be sacrificed to the cause of reinvestment.20 The second decision was subtler and more consequential: Constellation would lower the return bar for its very largest deals. The company had long insisted on lofty returns — a target return on invested capital historically around 30% — but Leonard argued that "if we drop our hurdle rates for these acquisitions, I believe that competent and diligent M&A brokers will include us in more auctions."20 He illustrated the trade-off with plain arithmetic: a 20% return on a $600-million takeover throws off as much annual cash as eight separate $50-million deals.20 For small tuck-ins the high bar would remain; for the big, mature acquisitions that could absorb hundreds of millions of dollars at once, a lower return was now acceptable.7

The Altera Test

This was, in effect, Constellation admitting that to keep growing it had to start competing in a different league, on different terms. The evidence of the pivot showed up quickly in the deal log. In 2022, Harris acquired the hospital and large-physician-practice business of Allscripts — a mature, slow-growing electronic health record operation — for up to USD 700 million, structured as roughly USD 670 million at close plus a contingent earn-out of up to USD 30 million, and rebranded it Altera Digital Health.1112 By Constellation's historical standards this was enormous, and it was exactly the sort of asset the old hurdle rates would never have permitted: legacy, low-growth, priced at a level that only made sense on a lower expected return. The bet was not on growth but on cash extraction — buying a stable, deeply embedded installed base and applying the company's relentless focus on cost and cash flow to stabilize and milk it.

The asset itself was a who's-who of legacy hospital software: the Sunrise and Paragon electronic-health-record platforms, the TouchWorks and Opal systems, and the dbMotion interoperability layer, serving hospitals and large physician practices that could no more rip out their clinical systems overnight than a city could switch its water billing on a whim.1112 That embeddedness was the entire thesis. By outside estimates the price worked out to roughly a single year's revenue — cheap for software, and itself a signal that the asset's high-growth days were behind it. The playbook from there is the one Constellation has run on dozens of tired software businesses: stabilize the product, rationalize the cost base, treat the loyal installed base as an annuity to be carefully maintained and gently repriced rather than a growth engine to be reinvented. Whether the price proves shrewd or merely defensible will play out over a decade, not a quarter — which is precisely the timeframe on which this company has always asked to be judged, and precisely the timeframe over which its critics say the discipline is hardest to hold.

Whether that math works out is precisely where a skeptic should press. Paying up for mature assets at lower returns is a different business from buying tiny gems at thirty percent, and it inevitably drags down the blended return on capital that made the stock legendary. The company's own reported returns on invested capital have been trending down from their historic peaks as this larger-deal strategy has scaled — a fact bulls attribute to a temporary mix shift and bears read as the first crack in the compounding story.13 The pivot also set up a parallel innovation: if the parent was getting too big to deploy capital efficiently, why not create smaller, separately listed vehicles that could?

VI. The Corporate Spinoff Playbook: Topicus & Lumine (01:35 – 01:55)

There is a moment in the life of every sprawling holding company when its own size becomes the constraint, and the elegant response Constellation found was to make itself smaller in public while staying whole in private. The logic of a spin-out, in this company's hands, is not the usual corporate-finance story of "unlocking value" by separating unloved divisions. It is about creating fresh equity currency. A separately listed European or telecom-focused subsidiary can issue its own stock to fund acquisitions in its domain without diluting the parent, and can attract a distinct pool of investors who want pure-play exposure to that niche. It is a way of manufacturing new compounding vehicles out of the parent's own flesh.

Topicus and the European Maze

The first and most important was Topicus. On the last day of 2020 Constellation completed the spin-out of its Total Specific Solutions group — a large European VMS operation acquired earlier — combining it with the Netherlands-based Topicus, a Dutch vertical-software specialist, to form a new public company, Topicus.com Inc. Its shares began trading on the TSX Venture Exchange under the ticker TOI on February 1, 2021.89 The strategic prize was the European VMS market, which is even more fragmented than North America's and, crucially, insulated by geography that maps almost perfectly onto Constellation's decentralized model. Software that handles German tax compliance, French medical records, or Dutch notarial workflows is protected not by technology but by language, regulation, and national borders — a natural moat that rewards patient local buyers and punishes would-be pan-European consolidators. Topicus has since grown into a roughly CAD 7.7 billion company in its own right.9

The distribution mechanics were precise to the point of poetry: for every Constellation share held, investors received 1.859817814 Topicus subordinate voting shares — a dividend-in-kind that handed the parent's own owners direct title to the new company, with an outside Dutch investor group, Joday, taking a comparable minority stake alongside them.8 The purpose was to give Topicus its own euro-denominated balance sheet and acquisition currency, so it could pursue European deals as a local player rather than as the far-flung subsidiary of a Toronto holding company. In fragmented European markets, where a target's founder may never have heard of a mid-cap Canadian acquirer, having a listed, locally understood entity with shares to offer is a genuine sourcing advantage — the equity itself becomes a recruiting tool for deals.

Lumine and the WideOrbit Trick

The second act was Lumine. In February 2023 Constellation carved a communications, media, and telecom software business out of Volaris and spun it out as Lumine Group, distributing shares to Constellation holders as a dividend-in-kind, with the stock beginning to trade under the ticker LMN around late March 2023.10 The spin-out was choreographed with a deal: at the moment of separation, Lumine folded in WideOrbit, a US media and broadcast software company, acquired for a gross purchase price of roughly USD 490 million, with part of the consideration paid in special shares issued to WideOrbit's sellers.10 The effect was to launch a new public compounder that already had a marquee acquisition inside it — an instant, self-funding vehicle for consolidating the global telecom-and-media software niche. Lumine now carries a market value in the range of CAD 5.6 billion.10

Here too the choreography was exact. Constellation shareholders received about 3.0003833 Lumine shares for each Constellation share they owned, and WideOrbit's sellers took part of their consideration not in cash but in special Lumine shares — instantly turning the founders of the acquired business into aligned owners of the vehicle their company was being folded into.10 It was a tidy piece of financial engineering: the target's owners became shareholders in the consolidator, the consolidator went public with a headline asset already inside it, and Constellation seeded an entirely new compounding vehicle without having to fund the whole thing in cash. A cynic would note that these structures also add layers of complexity and related-party entanglement between the parent and its listed children — a point the skeptics will return to.

Control Without Ownership

The financial mechanics of how Constellation retains control while giving away economics are the clever heart of the structure, and they repeat across both deals. Constellation distributes the ordinary, subordinate voting shares of the spin-out to its own shareholders — a tax-efficient way of handing them the upside — while itself keeping a single super-voting share plus a large block of preferred stock. In Topicus that left Constellation with roughly a 30% economic interest but effective voting control; in Lumine it retained a majority economic stake of around 60% alongside the super-voting share.810 The parent thus offloads the compliance burden and independent funding needs of a public listing onto the subsidiary, gives its shareholders a direct stake in the new entity, and yet never loses its grip on the wheel. It is financial engineering in service of the same old philosophy: decentralize everything except control of capital. The open question is whether that philosophy — and the discipline behind it — can outlast the man who authored it.

VII. The Post-Mark Leonard Transition: Enter Mark Miller (01:55 – 02:15)

For years the standard bear argument against Constellation had a single word at its center: key-man risk. So much of the company's magic seemed to reside in one idiosyncratic mind — the letters, the hurdle-rate discipline, the moral authority that kept a thousand managers buying stock in escrow rather than demanding options. In September 2025 that risk stopped being hypothetical. Constellation announced that Mark Leonard had resigned as President "for health reasons, effective immediately," though he would remain, for a time, a director.2 Chairman John Billowits invoked Leonard's "visionary leadership, humility and wisdom" and his "original inception of Constellation in 1995."2 The news was significant enough that Canada's business press covered a normally invisible company's leadership change as front-page material, a measure of how large this quiet compounder had grown in the national imagination.3 The following spring, in March 2026, the company disclosed that Leonard would not stand for re-election to the board, ending his directorship at the May 15, 2026 annual meeting, though he would continue as an advisor — pointedly, on a newer initiative the company calls its Permanent Engaged Minority Shareholder strategy.4 The founder was stepping off the stage, but not quite out of the theatre.

Who Is Mark Miller?

The man who took the President's chair is, in a sense, the most Constellation choice imaginable. Mark Miller is not an outside star. He is the insider's insider: he co-founded Trapeze Group in 1988, the transportation-software company that became the very first business Constellation acquired in 1995, and he has worked within the group for more than three decades.56 He built and led Volaris, the oldest operating group, into a multibillion-dollar engine and is its Executive Chairman; he sits on the boards of Lumine and other Constellation-affiliated entities.56 When he was appointed President, the company stressed that his other roles would remain unchanged, and in December 2025 he also joined the board.5 The symbolism is hard to miss: the empire's second era is being led by the founder of its first acquisition.

If Leonard was the philosopher who defined why Constellation existed, Miller was, for much of that history, the engineer who made it work at scale. Running Volaris, he helped codify the practical machinery of decentralized acquisition — the frameworks for evaluating deals, onboarding founders, setting business-unit metrics, and grooming the next generation of capital allocators — that was later templated across the other operating groups. That background frames both the hope and the worry about his tenure. The hope is that the systems are now robust enough to run without a singular genius at the top, precisely because Miller spent decades building them to be teachable and repeatable. The worry is subtler: an operator's instinct is to optimize and execute the existing system, whereas Leonard's rarer gift was knowing when to change the system itself — to stop the special dividends, to lower the hurdle, to invent the spin-out. Execution can be delegated; that kind of judgment is far harder to institutionalize, and it is precisely the thing shareholders are now trusting a committee and a coach to supply.

Miller's alignment is genuine, though the outline's precise figures deserve a caveat. He is reported to own on the order of 1% of Constellation's shares — a stake worth several hundred million dollars even after the 2026 drawdown — and insider records show him continuing to buy shares on the open market, including a purchase the day after his appointment.16 That exact ownership percentage is drawn from third-party trackers rather than confirmed in a company filing, and readers should treat the specific number as approximate.16 The larger point stands: the new leader has serious, self-funded skin in the game, exactly as the culture demands.

The New Guard, and the Founder Who Stayed

Around him stands a management guard cut from the same cloth. Bernard Anzarouth, the Chief Investment Officer, joined Constellation in 1995 and is the quiet architect of the acquisition-vetting process, working directly with the operating groups to source platform and tuck-in deals.5 Jamal Baksh, the Chief Financial Officer, joined in 2003 as a controller in the Jonas group and rose through finance roles across the company — a guardian of the thin corporate overhead and conservative balance sheet.5 What is notable is the sheer continuity: this is not a new team but the bench that ran the machine underneath Leonard for years.

There is also the matter of what Leonard is still doing. Rather than a clean break, his exit was staged — President, then director, then advisor — and the advisory role he kept is not ceremonial. He is focused on the company's Permanent Engaged Minority Shareholder strategy, an emerging effort to take significant but non-controlling stakes in software businesses Constellation cannot or does not wish to buy outright, an approach already visible in positions such as its investment in Sabre, where the company holds a board seat but keeps the details deliberately private.41 That the founder chose this, of all things, as his parting project is a tell about where he believes the next decade of capital deployment has to go — toward a form of investing that looks less like the classic buy-it-all playbook and more like patient, concentrated minority ownership of larger businesses. It also means the philosophical author of the company has not fully left the room, which cuts both ways: reassuring for continuity, but complicating for a new President still establishing his own authority.

The analytical question is whether operating continuity is the same as philosophical continuity. Leonard's genius was not merely operational; it was in capital-allocation judgment and in the almost religious authority he wielded to keep the culture disciplined when it would have been easy to loosen it. Miller's style, by contrast, is visibly operational and execution-focused. On the Q1 2026 call, asked what he was bringing to the role after six months, he did not offer a grand philosophy — he talked about operating-group leaders sitting together after a board meeting "working on things," about collaboration being "at an all-time high," and, revealingly, about his persistent frustration with organic growth: "I continue to pressure our businesses on organic growth generally. I really would like to see them doing a better job."1 That is the voice of a coach, not a philosopher-king. Whether a coach can preserve what a philosopher built is the wager every current shareholder is now making — and to size that wager, we have to war-game the moat itself.

VIII. The Seven Powers & Competitive Landscape Analysis (02:15 – 02:35)

Strip away the narrative and ask the cold structural question a strategist would ask: what actually protects this business, and how durable is it? Hamilton Helmer's "7 Powers" framework is a useful scalpel here, because Constellation's moat is not one thing but a stack of reinforcing advantages — and naming them precisely also reveals where each could fail.

Power One: Switching Costs

The primary power is switching costs, and they are formidable. When a piece of software runs a customer's core operations — billing a utility's ratepayers, dispatching a city's buses, keeping a broker's compliance records — replacing it is not a purchasing decision but a bet-the-operation project. The cost of ripping it out, migrating the data, retraining the staff, and risking downtime typically dwarfs several years of subscription fees. That is why churn is so low and why price increases meet so little resistance. Miller described the dynamic candidly on the Q1 call: customers are rarely lost to price, because "switching is painful"; they are lost mainly when they go out of business, get acquired, or when a competitor can offer something genuinely different that the customer really needs.1 That last clause is the vulnerability worth underlining — switching costs protect against price competition, not against a genuinely superior new capability, which is exactly the threat AI bulls and bears are now arguing about.

Powers Two and Three: The Cornered Machine and Inverted Scale

The second power is closer to a cornered resource: the acquisition machine itself. Over thirty years Constellation has built a proprietary database of tens of thousands of VMS targets and a reputation, among software founders, as the buyer who will let you keep your name, your team, and your autonomy.19 No other global acquirer has that combination of patience, decentralized deal-sourcing, and a three-decade track record of buying tiny companies and not wrecking them. That reputation is a genuine asset — founders sell to Constellation partly because it is Constellation — though it is one that private equity and a wave of "permanent capital" imitators are now actively trying to replicate. The third power is scale economies of an unusual, inverted kind: head office provides tax structuring, debt financing on favorable terms, legal templates, and capital-allocation expertise to businesses far too small to access any of it alone. A three-million-dollar software company could never borrow like a member of an eleven-billion-dollar enterprise; inside Constellation, it effectively can.

Process Power, and the People Trying to Copy It

There is arguably a fourth power at work here, and it is the hardest of all to copy: process power. Three decades of buying, holding, and improving small software companies have been distilled into a body of institutional knowledge — how to price a deal, how to repair a struggling unit's margins, how to structure a manager's incentives, how to handle cross-border tax and integration-that-isn't-integration — diffused across hundreds of operators rather than locked in one person's head. That is what makes it durable: a competitor cannot poach it by hiring a single executive, because it lives in the routines of the whole organization. The catch, and it is a sharp one, is that process power is built for a specific game. If artificial intelligence genuinely rewrites the rules of how vertical software is built, sold, and defended, then thirty years of accumulated process could curdle into thirty years of accumulated habit — expertise at playing a game that is quietly ending.

It helps to name the competition explicitly. The closest public analog is Roper Technologies, another serial acquirer of niche, cash-generative software businesses, though Roper concentrates its capital in a smaller number of larger platforms rather than thousands of tiny ones. The private-equity software consolidators — the Thoma Bravos and Vistas of the world — are formidable, deep-pocketed buyers, but they operate on a fund clock: they buy to sell within a handful of years, which makes them natural sellers to, rather than permanent competitors with, a buy-and-hold acquirer. That difference is Constellation's structural edge in the auction room. A private-equity buyer must model an exit; Constellation models a perpetuity, and a founder who cares what happens to their employees and their product after the sale often prefers the buyer who is not planning to flip them. The live vulnerability is that capital is fashion: a wave of new "permanent capital" vehicles, family offices, and Constellation-imitators has begun explicitly copying the model, bidding up the very small deals that were once its uncontested hunting ground and slowly eroding the price advantage that made the math work.

Five Forces, One Real Threat

Run the same landscape through Porter's Five Forces and the picture reinforces itself, with caveats. The threat of new entrants into any given niche is low bordering on irrational: why spend five million dollars building software to attack a fifteen-million-dollar market already dominated by an entrenched incumbent with sticky customers? The bargaining power of buyers is limited, because they are fragmented and the software is mission-critical — no single small municipality can dictate terms to its billing-software vendor. Competitive rivalry within niches is muted, because most verticals support only two or three viable players and reliability, not price, is what customers reward. On every axis, the traditional forces of competition are dampened by the very smallness of the markets Constellation chose.

But a good war-game does not stop at the flattering conclusion. The one force Porter's framework handles poorly is the threat of substitutes arriving from an entirely new direction — and that is precisely the AI question hanging over the stock. If generative tools genuinely lower the cost of building software toward zero, the "irrational to enter" logic that protects these niches weakens, and a well-funded AI-native competitor could, in theory, offer the "something genuinely different" that Miller himself identified as the real way customers are lost.1 Management's counter — that AI is more a cost-saver and expansion tool for its embedded businesses than an existential threat — is a claim, not yet a proven fact. Which is the perfect place to lay out the two sides of the case explicitly.

IX. The Investment-Story Spine: Bull vs. Bear Case (02:35 – 02:50)

Every great business eventually gets stress-tested by a skeptical market, and in 2026 Constellation is getting its turn. The stock's roughly 45% fall from its 52-week high, and the "SaaSpocalypse" language now littering its own earnings calls, mean the bull and bear cases are no longer academic — they are being priced in real time.113 Let us take the bear seriously first, because a fair analyst always steel-mans the short.

The Bear Case

The bear case rests on three planks. The first is the reinvestment drag. Constellation's organic growth — the growth of its existing businesses before acquisitions — has historically run only in the low single digits, and Baksh confirmed on the Q1 2026 call that it remained "in line with historical norms."1 A business growing organically at low-single-digit rates is only a great investment if it can keep redeploying its cash at high returns; if acquisition opportunities dry up or get too expensive, what remains is a slow-growth company still carrying a premium multiple. The second plank is hurdle-rate dilution: deploying billions into large, mature deals at mid-teens returns mathematically pulls the blended return on capital down from its storied highs, and the company's own reported returns have indeed been softening.13 The third plank is cultural decay. Without Leonard's moral authority, will managers watching escrowed shares fall by half start to demand options, or resist the open-market purchase mandate? Management insists the plan is untouched, but conviction expressed during a drawdown is cheaper than conviction proven across a full cycle.1

And then there is the valuation itself, the plank a short-seller would hammer hardest. Even after halving, the shares have recently traded at a rich multiple — on the order of fifty times earnings and roughly twenty times EV/EBITDA — well above the peer-group average and embedding an assumption of durable, high-return reinvestment stretching far into the future.13 Strip out that assumption and treat Constellation as what its organic numbers alone would suggest — a slow-growing collection of mature software annuities — and the premium looks difficult to justify. The bear's sharpest point is not that the business is bad; it is that the price has long assumed the machine keeps working exactly as it always has, which leaves a thin margin for disappointment precisely when three sources of disappointment — AI, succession, and the law of large numbers — have arrived at once.13

The activist's version of this critique would go further and poke at the structure itself. The portfolio has become genuinely complex — a parent with two separately listed offspring, super-voting shares, preferred-stock control mechanisms, and a newer push into minority stakes (the "Permanent Engaged Minority Shareholder" strategy, and the "PEM" minority investments discussed on the Q1 call) that, as Baksh acknowledged, do not even show up cleanly in the free-cash-flow metric investors have used for years.14 A skeptic would ask whether disclosure is keeping pace with complexity, whether related-party dynamics among the parent and its listed children are fully transparent, and whether an acquirer that once returned excess cash is now, in the name of "imagination," simply accumulating it. These are fair questions, and management's answers so far are more reassuring in tone than settled in fact.

On the mechanics of that newer minority-investment push, Baksh was at least specific on the Q1 call: the minority stakes carry the same hurdle rate as outright acquisitions, but with a much wider spread of modeled outcomes between best and worst case, which tends to produce a lower price. Because Constellation would book only its pro-rata share of those businesses' cash flows, he acknowledged the company is weighing whether to give investors a new yardstick — closer to the internal "economic net income" measure it already uses to calculate bonuses — rather than the free-cash-flow-to-shareholders figure the market has relied on for two decades.1 For a company whose entire brand rests on disclosure discipline and a single clean measure of progress, that is a meaningful admission: the metrics themselves may have to change, and changing the scorecard mid-game is exactly the kind of move that invites scrutiny.

The Bull Case

Now the bull. Its first plank is runway: the global VMS market outside North America and Western Europe — Eastern Europe, Asia, Latin America — remains vast, fragmented, and largely untouched by both private equity and Constellation itself, suggesting the acquisition machine could run for a very long time before it truly runs out of small companies to buy. The second plank inverts the AI fear: rather than a disruptor, Constellation argues AI is a margin tailwind — its businesses can use AI to write code and handle support more cheaply while deep switching costs keep customers from bolting to speculative startups. Miller's framing on the Q1 call was notably offensive rather than defensive: he sees the tools as "an opportunity to do more for customers," a way for close-to-customer businesses to expand deeper into accounts, not merely to cut costs.1 That is a genuinely plausible thesis — but note it is still a thesis; the revenue proof, as Baksh conceded, "is going to take time."1

It is worth weighing how real that runway actually is rather than taking it on faith. The evidence for it is concrete: Constellation deployed well over a billion dollars into acquisitions again in 2025, and on the Q1 2026 call management described a large-deal pipeline it is now equipped to pursue, with Anzarouth noting the flow of targets has neither thinned nor swelled — the market is simply large enough to keep absorbing capital.1 Vast stretches of the world have barely begun to consolidate their vertical software, and private equity's fund clock makes it a poor fit for tiny, slow-growing targets in far-flung markets. The counter-argument is equally concrete: the imitators are multiplying, prices at the small end have crept upward, and the very largest deals that can now move the needle are exactly the ones where Constellation must compete hardest and accept its lowest returns. Runway, in other words, is genuinely long — but the quality of what lies along it is deteriorating at the margin, which is why the return-on-capital trend matters more than the raw acquisition count.

The AI debate got its most textured airing on that same Q1 2026 call, when an analyst dialing in from Hong Kong tried to sort the portfolio into buckets — low-risk "systems of action" and mission-critical software on one side, higher-risk marketing, lead-generation, and website tools on the other — and asked how much revenue sat in the vulnerable category. Miller resisted the tidy framing. Defensibility, he argued, is "in the eye of the beholder": a business that looks horizontal and exposed can be perfectly safe if its niche is small and its customers deeply served, while the real danger lies anywhere a competitor "can provide something much different" that a customer genuinely needs — with high-churn businesses the likeliest casualties, though those are a small share of recurring revenue.1 It was a notably non-defensive answer, and an honest one: he did not claim immunity, he claimed dispersion, and he pushed responsibility for adapting down to the business units, exactly as the whole model demands. An investor can read that as either admirable candor or an admission that no one at the center actually knows how exposed the portfolio is.

The third bull plank is optionality: Topicus and Lumine proved the spin-out model works, and Jonas, Vela, or Harris could someday be floated the same way, each a potential new compounding vehicle and cash-crystallization event — a source of value creation that is entirely within management's control and independent of the AI question altogether.

Weighing the two, the honest synthesis is that Constellation's competitive moat — the switching costs, the cornered acquisition machine, the inverted scale economies dissected above — remains largely intact and visible in the operating results, while the two things genuinely in question are exogenous and unproven: whether AI changes the deep structure of vertical software, and whether the culture holds without its author. The market has moved from pricing near-certainty to pricing real doubt, which is less a verdict than a reframing of the question. For an owner, the task is not to guess the answer but to watch the right evidence.

Three Numbers That Matter

That is where the KPIs come in. Amid the noise, three numbers matter more than any others for tracking whether the machine is still working. The first is return on invested capital on a consolidated basis — the single clearest signal of whether Constellation is still deploying cash at attractive rates or drifting toward its cost of capital as deals get larger. The second is organic revenue growth, which reveals whether the existing installed base is holding its pricing power and defending itself against AI substitution, or quietly decaying. The third is the free-cash-flow deployment ratio — how much of the cash the company generates it actually reinvests into acquisitions versus letting it pile up idle on the balance sheet, the truest test of whether the "stop the special dividends and reinvest" bet of 2021 is paying off. Track those three, and the story tells itself. (This is analysis for understanding the business, not investment advice, and nothing here is a recommendation to buy or sell.)

X. Epilogue & Key Takeaways (02:50 – 03:00)

Step back and the most surprising thing about the most successful software investor of his generation is what he never did: build software. Mark Leonard's company has written plenty of code over thirty years, but not a single line of it was the point. The point was capital allocation — the disciplined, patient, almost monastic redeployment of cash into hundreds of small, dull, defensible businesses that everyone else was too busy chasing home runs to want. Constellation's genius was to treat the acquisition of vertical-market software as an industrial process and to build the organizational chemistry — decentralization, escrowed open-market ownership, hurdle-rate discipline — that let that process run for two decades without corroding.

For founders and operators, the lessons are concrete and slightly subversive. Real alignment, Constellation's history suggests, does not come from handing out options that cost the recipient nothing; it comes from making managers buy the same shares as everyone else, with their own money, at market prices, and holding them there. And decentralization, done properly, is not merely delegating tasks — it is delegating full responsibility for capital, trusting the person closest to the customer to earn a return, and resisting the constant corporate temptation to "help" by centralizing. Those ideas are easy to admire and, judging by the many imitators who have failed to replicate them, extraordinarily hard to institutionalize.

One myth is worth puncturing on the way out: that Constellation is a "software company" whose fate rides on technology. It is better understood as a capital-allocation institution that happens to deploy into software — closer in spirit to a decentralized Berkshire Hathaway than to a Silicon Valley developer. That reframing matters intensely right now, because the market is currently pricing the company as the former while fearing for it as the latter. If the AI wave mostly reshapes how individual products are built, a disciplined allocator can adapt, redirect capital, and keep compounding through it. If instead AI erodes the switching costs and pricing power that make vertical software an annuity in the first place, then the raw material the allocator feeds on gets cheaper and less durable, and the whole flywheel slows. Which of those two futures arrives is, in a sentence, the entire question of the post-Leonard era.

And yet the story now stands at a genuine hinge. The philosopher-founder has left; a builder runs the machine. The market has swapped its old certainty for fresh fear about AI, valuation, and succession all at once, carving the stock nearly in half. Constellation's history is a powerful argument that structure, discipline, and boring niches can outrun hype over the long run — but history is an argument, not a guarantee, and the next chapter will be written by different hands under harder scrutiny. Whether the compounding machine keeps compounding without the man who imagined it is the question this company will spend the coming years answering, in the only language its founder ever really trusted: returns on capital, reported quarter after quarter, for anyone patient enough to keep score.

References

-

Constellation Software Inc. Announces Results for the First Quarter Ended March 31, 2026 and Declares Quarterly Dividend; Q1 2026 conference call (May 13, 2026) — Constellation Software Inc., 2026-05-12 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Constellation Software Inc. Announces the Resignation of Mark Leonard and Appointment of Mark Miller as President — Constellation Software Inc., 2025-09-25 ↩↩↩

-

Constellation Software founder Mark Leonard resigns — The Globe and Mail, 2025-09-25 ↩

-

Constellation Software Inc. Announces Mark Leonard's Decision to Not Stand for Re-election to Board of Directors — Constellation Software Inc., 2026-03-27 ↩↩↩↩

-

Constellation Software Releases Letter to Shareholders (February 15, 2021 letter) — Constellation Software Inc., 2021-02-15 ↩↩↩

-

Constellation Software Inc. Completes Spin-Out of Topicus.com Inc. — Constellation Software Inc., 2021-01-05 ↩↩↩↩

-

Constellation Software Inc. and Lumine Group Inc. Complete Purchase of WideOrbit Inc. and Lumine Group Spin-Out — Lumine Group Inc., 2023-02-23 ↩↩↩↩↩↩

-

Constellation Software's Harris Operating Group Acquires Allscripts Hospitals and Large Physician Practices Business Segment — GlobeNewswire, 2022-03-02 ↩↩

-

Harris Completes Purchase of Allscripts Hospitals and Large Physician Practices Business Segment — Altera Digital Health, 2022-05-06 ↩↩

-

A Look At Constellation Software (TSX:CSU) Valuation After AI Selloff Jitters And New Sector Acquisitions — Yahoo Finance / Simply Wall St, 2026 ↩↩↩↩↩↩↩

-

Constellation Software Inc. Annual Reports, MD&A and Financial Statements — SEDAR+ ↩↩↩↩

-

Constellation Software Inc. Investor Relations & Shareholder Letters Archive — Constellation Software Inc. ↩

-

Mark Miller Profile and Open Market Share Transactions — Simply Wall St ↩↩

-

The Science of VMS and Constellation Software Analysis — In Practise ↩↩↩↩↩↩↩↩↩

-

Constellation Software's Capital Allocation Playbook and Hurdle Rate Analysis — SBO Financial ↩↩

-

Volaris Group Corporate Acquisition Strategy Overview — Volaris Group ↩↩

-

Constellation Software's roll-up wizard ups his game in major acquisition push (Mark Leonard's 2021 letter; 2006 IPO at C$17; OMERS backing) — The Globe and Mail ↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube