Constellium SE: Forging the Future of Aluminum

I. Introduction & Episode Roadmap

There is a company headquartered on Rue Washington in Paris that most investors have never heard of, yet without it, neither Boeing nor Airbus could build an airplane, Ford could not stamp its best-selling truck, and BMW could not crash-test its SUVs. That company is Constellium SE, and it sits in one of the most quietly powerful positions in global manufacturing.

Constellium is not a household name. It does not make consumer products. It does not have a splashy brand or a charismatic founder tweeting about the future. What it does is take commodity aluminum — the same stuff in soda cans — and transform it into extraordinarily specialized sheets, plates, and structural components that go into the most demanding applications on Earth: aircraft fuselages, automotive crash structures, battery enclosures for electric vehicles, and even components for NASA's Artemis moon mission.

Think of it this way: if the aluminum value chain were a pyramid, at the bottom you have bauxite miners and smelters producing raw metal. That is a brutally commoditized business where the lowest-cost producer wins. At the very top, you have finished aircraft and automobile manufacturers capturing the consumer brand premium. Constellium occupies the critical middle layer — the "sweet spot" of high-value rolled and extruded products — where metallurgical expertise, decades-long customer relationships, and punishing certification requirements create real barriers to entry.

The company generated roughly $8.5 billion in revenue in 2025 and posted a record $846 million in adjusted EBITDA, yet it trades at a valuation that suggests the market still views it as a cyclical commodity player rather than a specialty materials franchise.

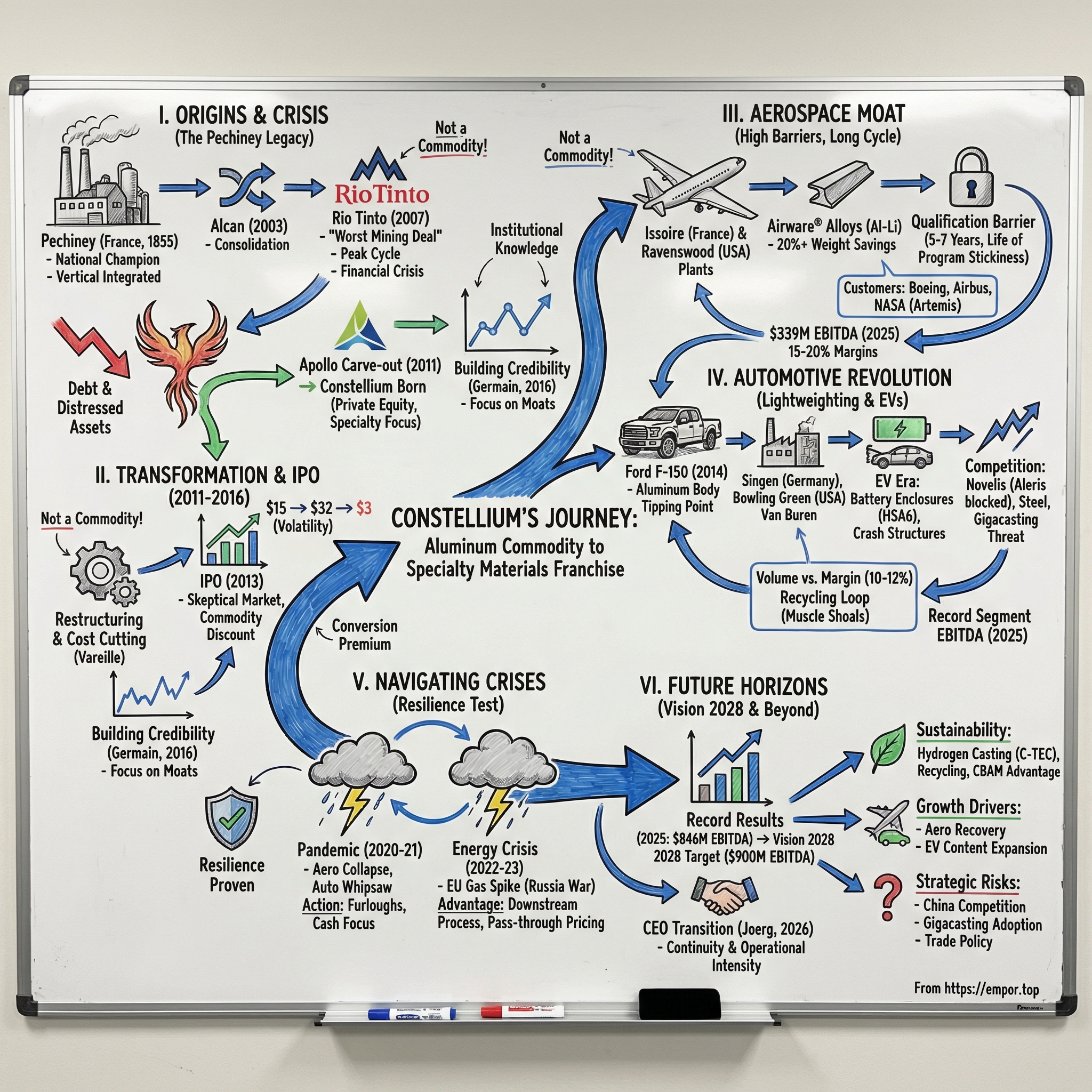

How did a division of a French state-owned aluminum monopoly, carved out through private equity financial engineering during the depths of the financial crisis, become the indispensable supplier sitting between the world's most important aerospace and automotive manufacturers? That story involves 170 years of French industrial history, the worst mining acquisition ever made, a private equity giant named Apollo seeing value where others saw wreckage, and a management team that had to navigate a pandemic, an energy crisis, and the electric vehicle revolution — all while carrying a mountain of debt.

Before diving in, it helps to understand what makes aluminum processing so different from other metals. When most people think of aluminum, they think of soda cans or kitchen foil — cheap, disposable, commodity products. But the aluminum that goes into an aircraft wing or a battery enclosure is as different from can stock as a Formula One engine is from a lawnmower motor. The difference lies in the alloy composition (which elements are added to the base aluminum and in what proportions), the thermomechanical processing (how the metal is heated, rolled, stretched, and aged), and the quality controls (testing every batch to tolerances measured in microns). Constellium operates at the high end of this spectrum, and that is the foundation of everything that follows. This is the story of Constellium.

II. The Pechiney Legacy & Birth from Crisis

Walk into any modern aircraft factory — say, the Airbus final assembly line in Toulouse or Boeing's Everett facility north of Seattle — and you will see enormous sheets of silvery-gray metal being shaped into the curved fuselage panels that form an airplane's skin. Those sheets began their journey as slabs of specially formulated aluminum alloy, cast in plants that trace their heritage to one of the oldest industrial enterprises in France.

In a small town called Salindres in southern France, in 1855, an engineer named Henri Merle founded a caustic-soda factory. Five years later, that factory produced its first aluminum using a chemical process so expensive that the resulting metal was more precious than gold. Napoleon III famously served state dinners on aluminum plates while lesser guests ate from gold and silver. Aluminum was the exotic material of empires.

The company that grew from Merle's factory would eventually become Pechiney — France's aluminum national champion and one of the great industrial dynasties of European history. Under the stewardship of A.R. Pechiney, who managed the firm from 1877 to 1906, the company adopted the electrolytic process for extracting aluminum, transforming it from a curiosity into an industrial commodity. Through a series of mergers over the following decades, the company grew into a vertically integrated giant, controlling everything from bauxite mines in West Africa to rolling mills in Alsace to packaging plants across Europe.

Pechiney's story parallels the arc of aluminum itself — from rare metal to ubiquitous material. By the mid-twentieth century, aluminum was everywhere: in aircraft skins during World War II, in beverage cans during the consumer revolution, in automotive components as fuel efficiency became a concern. And Pechiney was at the center of it all. The French government nationalized the company in 1982 under President Mitterrand's sweeping industrial policy, and it became a symbol of French technological prowess — the kind of company that governments treat as strategic assets rather than mere businesses.

But Pechiney carried a fatal flaw that would ultimately destroy it: extreme vertical integration in a world that was rapidly commoditizing. Owning everything from mines to mills made sense when aluminum was a strategic material controlled by a handful of Western companies. It made far less sense when low-cost smelters in the Middle East, Russia, and China began flooding the market with cheap primary metal. Pechiney's upstream operations — the mining and smelting — became anchors dragging down the genuinely valuable downstream businesses in aerospace and automotive rolled products.

The privatization of Pechiney in 1995 set the stage for what came next: a decade of consolidation that would ultimately tear the company apart.

In 2003, Canadian aluminum giant Alcan launched a public bid for Pechiney at roughly 48.5 euros per share, valuing the French champion at approximately $4.5 billion. Pechiney's board initially rejected the offer, but Alcan turned hostile, and the European Commission cleared the deal — subject to divestitures of rolling mill assets — by the end of the year. The logic was straightforward: Alcan had already absorbed Swiss producer Alusuisse in 1999, and adding Pechiney would create a Western aluminum colossus capable of competing with Alcoa.

The consolidation did not stop there. In May 2007, Alcoa — the American aluminum giant founded by Charles Martin Hall in 1888 — launched a hostile takeover bid for Alcan worth $27 billion. Alcan's board told shareholders to reject it. Two months later, Alcan found a white knight in Rio Tinto, the Anglo-Australian mining giant, which offered $101 per share in an all-cash deal valuing Alcan at a staggering $38.1 billion. The deal closed in October 2007. What had been Pechiney's crown jewels — its aerospace plate mills, its automotive rolling lines, its advanced alloy laboratories — were now buried inside the world's second-largest mining company, rechristened Rio Tinto Alcan.

The sheer scale of the transaction is worth pausing on. Rio Tinto paid $38 billion — roughly the GDP of a small European country — for an aluminum company at the absolute peak of the commodities super-cycle. The deal was financed largely with debt, and Rio Tinto's balance sheet went from healthy to strained overnight. Within months, the global financial crisis would crush commodity prices and vaporize the demand growth that justified the acquisition premium. Rio Tinto's board and CEO would face intense scrutiny. The word "hubris" appeared frequently in analysis of the deal.

The timing could not have been worse. The acquisition closed at the absolute peak of the commodities super-cycle, and within twelve months the global financial crisis had obliterated demand for aluminum. Rio Tinto's Alcan acquisition was later called "the worst mining deal ever" — a $38 billion bet placed at the top of the market. Rio Tinto found itself drowning in debt and desperately looking to sell non-core assets.

Enter Apollo Global Management, the New York-based private equity firm founded by Leon Black. Apollo had built a reputation as one of the most aggressive and analytically rigorous buyers of distressed and undervalued industrial assets. The firm's playbook was well known on Wall Street: identify assets trapped inside larger organizations where their value was obscured, acquire them at a discount, restructure operations, and either take them public or sell them at a significant premium.

In January 2011, Apollo led a consortium that carved out Rio Tinto's Alcan Engineered Products division — the downstream rolled products, aerospace, and automotive businesses — in a leveraged buyout. Apollo took a 51% stake, France's sovereign wealth fund (the Fonds Stratégique d'Investissement) took 10%, and Rio Tinto retained the rest. The inclusion of the FSI was politically essential — the French government was not going to allow the country's aerospace aluminum heritage to pass entirely into the hands of an American private equity firm without retaining a seat at the table. On May 3, 2011, the new entity was formally renamed Constellium, incorporated as a Dutch public limited company with its corporate seat in Amsterdam. What had been Pechiney's finest assets — 170 years in the making, passed through nationalization, privatization, two hostile takeovers, and a financial crisis — were now a private equity portfolio company.

The name itself was carefully chosen. "Constellium" evoked a constellation — a collection of bright points forming a larger pattern — and signaled a decisive break from the Pechiney and Alcan lineage. This was not going to be another chapter in the saga of a French national champion or a Canadian mining empire. It was going to be something new: a focused, specialized, high-value aluminum company built for the twenty-first century.

The question was whether Apollo had bought a diamond or a lump of coal. The answer would depend entirely on whether the new management team could strip away the legacy bloat and reveal the specialty materials business hidden underneath.

III. The Private Equity Makeover (2011-2013)

Private equity firms have a phrase for what Apollo saw in the Alcan Engineered Products portfolio: "orphaned assets." These were businesses that had been neglected — not through malice but through the simple fact that every parent company had different strategic priorities. Pechiney cared about French industrial policy. Alcan cared about integrating three major acquisitions. Rio Tinto cared about mining. Nobody was waking up in the morning focused on optimizing the yield of an aerospace plate mill in Issoire or winning the next automotive body sheet program in Germany. The assets were excellent. The attention they received was not.

When Apollo's deal team first walked through Constellium's plants in Issoire, Neuf-Brisach, and Ravenswood, they saw something that most investors missed: a collection of world-class manufacturing assets burdened by decades of corporate overhead accumulated through those successive parent companies. Each successive parent company had layered on administrative structures, reporting requirements, and strategic mandates that had nothing to do with making the best aerospace aluminum plate on the planet.

Apollo's playbook for industrial carve-outs was well established: cut the corporate fat, invest in the operations that generate real value, and sell the story to public markets within two to three years. The first CEO, Christel Bories, came from within the Pechiney and Alcan lineage, having run Alcan Packaging and then Alcan Engineered Products before the carve-out. But Bories and Apollo clashed on strategic direction — a not-uncommon friction between operating executives and financial sponsors — and she departed before the end of 2011.

Richard "Dick" Evans, a veteran aluminum industry executive who had served as CEO of Alcan and then Rio Tinto Alcan, stepped in as interim chairman and CEO. Evans was an industry elder statesman — 27 years at Kaiser Aluminum before joining Alcan, past chairman of both the US Aluminum Association and the International Aluminum Institute. His role was to stabilize the ship while Apollo found a permanent leader.

That leader arrived in March 2012: Pierre Vareille, a French industrialist who had run FCI, a global connector manufacturer with 14,000 employees across 30 countries. Vareille's earlier career included CEO stints at Wagon Automotive and GFI Aerospace, plus senior roles at Faurecia and Vallourec — a resume that screamed operational excellence in complex manufacturing businesses. Vareille understood something fundamental about Constellium's position: the company was not in the commodity aluminum business. It was in the business of converting commodity aluminum into highly specialized products that customers could not easily source elsewhere.

The restructuring focused on three priorities.

First, stripping away cost structures inherited from three layers of corporate parents. Second, investing in the aerospace and automotive capabilities that generated the highest margins. Third, building a narrative that public market investors could understand — not "we are a European aluminum company" but "we are a specialty materials company serving the most demanding customers in aerospace and automotive."

The aerospace moat was the centerpiece of the story. Think about what it takes to qualify a new aluminum alloy for use in an aircraft fuselage or wing structure. The material must be tested under every conceivable stress condition — fatigue, corrosion, temperature extremes, impact resistance — across thousands of test cycles over multiple years. The qualification process for a new alloy on a major aircraft program typically takes five to seven years. Once an alloy is qualified, neither the airframe manufacturer nor the airline wants to change it. The switching costs are not just financial — they are regulatory and safety-related. Changing a qualified material on a certified aircraft requires re-testing and re-certification with aviation authorities, a process so onerous that it effectively locks suppliers in for the life of the aircraft program.

For automotive, the story was different but equally compelling. Global regulations were tightening fuel efficiency requirements — CAFE standards in the United States, emissions targets in Europe, new energy vehicle mandates in China — and automakers were desperate to reduce vehicle weight. Aluminum body panels and structural components could reduce weight by up to 40% compared to steel equivalents. The mega-trend was unmistakable, and Constellium was positioning itself as the partner that could help OEMs make the transition.

The restructuring was not without human cost. Plant closures and headcount reductions affected communities across Europe that had depended on aluminum manufacturing for generations. The French sovereign wealth fund's 10% stake provided a degree of political cover — this was not a purely Anglo-Saxon financial engineering exercise, but a restructuring with French state participation — but the social tensions were real. Workers at Constellium's plants had seen their employer change names three times in a decade, from Pechiney to Alcan to Rio Tinto Alcan and now to Constellium. Each transition brought uncertainty, restructuring, and the question of whether their plant would survive the next round of optimization.

What kept the plants running — and what Apollo ultimately bet on — was the irreplaceable nature of the skills inside them. A metallurgist at Issoire who had spent twenty years developing and qualifying aerospace alloys could not be replaced by a consulting study or an automation project. The knowledge of how to consistently produce a defect-free aluminum plate that would become part of an aircraft fuselage lived in the hands, eyes, and experience of thousands of skilled workers. This institutional knowledge was Constellium's real asset, and preserving it through the restructuring was as important as cutting costs.

By mid-2012, Apollo had a restructured company with a clear identity, an experienced CEO, and a compelling investment thesis. The path to an IPO was open.

IV. Going Public in a Skeptical Market (2013-2016)

On May 22, 2013, Constellium priced its initial public offering on the New York Stock Exchange at $15 per share — below the initial marketing range of $17 to $19. The company sold roughly 22.2 million Class A ordinary shares, raising approximately $333 million. The stock also carried a listing on the professional segment of NYSE Euronext Paris.

The discount was telling. Investors looked at Constellium and saw a European aluminum company — cyclical, commodity-exposed, overleveraged, and controlled by a private equity sponsor looking for the exit. The "specialty materials" narrative that Apollo and Vareille had carefully constructed collided with the market's deeply ingrained skepticism toward anything that touched commodities, particularly European commodities in the aftermath of the eurozone crisis.

The challenge of investor communication for a company like Constellium cannot be overstated. Most buy-side analysts who cover materials and metals have mental models calibrated to primary aluminum producers — companies whose fortunes rise and fall with the London Metal Exchange aluminum price. Explaining that Constellium's earnings are primarily driven by conversion premiums rather than metal prices requires patient education. Explaining that aerospace qualification cycles create switching costs comparable to enterprise software lock-in requires analogies that bridge the gap between industrial manufacturing and the sectors where most investors spend their time. Management spent these early years as a public company doing exactly this kind of education, one investor meeting at a time.

The Apollo overhang did not help. Private equity sponsors typically sell down their positions after an IPO lockup expires, and the market knew that Apollo's remaining 35%-plus stake was destined for the secondary market. Sure enough, Apollo moved to liquidate its entire remaining position by early 2014. Remarkably, reports indicated that roughly 11% of the IPO proceeds went to pay Apollo for advisory services — a detail that raised eyebrows among governance-minded investors.

Despite the rocky start, Constellium's stock caught a tailwind. The shares surged to an all-time high of $32.61 by July 2014, more than doubling from the IPO price in just over a year, as the aerospace cycle accelerated and automotive lightweighting gained momentum. But the euphoria did not last. By October 2015, the stock had collapsed to an all-time low of $3.38, crushed by commodity price deflation, concerns about European industrial weakness, and debt levels that looked increasingly uncomfortable. The company's high leverage — a hallmark of Apollo's buyout structure — became a liability as investors fled anything with cyclical exposure and significant debt.

These early years as a public company were a crucible. Constellium had to prove that its aerospace business was genuinely different from commodity aluminum, that its automotive programs were gaining traction, and that it could manage its debt burden without a capital raise that would dilute shareholders. The management team under Vareille focused on winning new automotive body sheet programs, expanding the Airware advanced alloy portfolio, and chipping away at the debt pile.

In 2016, a leadership transition brought Jean-Marc Germain to the CEO role. Born in 1966, Germain had spent his career in the aluminum industry — rising through Pechiney and Alcan before serving as president of Novelis's North American operations from 2008 to 2012. He then ran Algeco Scotsman, a modular building company, before returning to the aluminum world at Constellium. Germain understood both the operational intricacies of rolling mills and the financial language of public markets. His decade-long tenure would see the company through its most dramatic challenges and ultimately deliver record financial results.

One critical corporate move during this period: in December 2019, Constellium completed a re-domicile from the Netherlands to France, converting from a Dutch NV to a European company (Societas Europaea, or SE) headquartered in Paris. The move reflected the company's French heritage, aligned its corporate structure with its largest operational footprint, and simplified governance. The stock continued trading on the NYSE under the same CSTM ticker.

The period from 2013 to 2016 was fundamentally about credibility-building. Every quarter, management had to demonstrate that the aerospace business was generating premium margins, that automotive programs were converting from design wins to production revenue, and that the debt load was manageable. The stock's journey from $15 to $32 to $3 and back illustrated the market's uncertainty about whether Constellium was a specialty materials franchise deserving a premium multiple or a cyclical commodity company that happened to serve aerospace and automotive customers. That debate, in many ways, continues to this day.

The valuation discount that plagued Constellium's early public years reflected a market that had not yet internalized the company's competitive positioning. That story would be written — and proven — in the aerospace plants of Issoire and Ravenswood.

V. Aerospace Dominance: Building the Unbreakable Moat

Picture the Issoire plant in the Auvergne region of central France. Roughly 1,600 workers operate four production units — including two casthouses, a plate shop, and a sheet shop — in a facility that ranks among the two most important aerospace plate mills on the planet. The other one also belongs to Constellium: the Ravenswood facility in West Virginia, a 62-acre complex built in 1957, housing one of the largest cold rolling mills in existence and plate stretchers capable of handling the enormous slabs that become wing skins and fuselage panels for the world's aircraft.

To understand why Constellium's aerospace business is different from almost any other aluminum operation, you need to understand what happens to aluminum before it can fly. An aircraft manufacturer does not simply order "aluminum" the way a beverage company orders can stock. Each alloy — each specific combination of aluminum, copper, lithium, zinc, magnesium, and trace elements — must be individually qualified for its intended application on a specific aircraft program. The qualification process involves material characterization, mechanical testing, fatigue testing, corrosion testing, and manufacturing trials, overseen by both the airframe manufacturer and aviation regulators. The whole process typically stretches across five to seven years.

This is where Constellium's Airware family of aluminum-lithium alloys becomes the crown jewel. Developed over more than twenty years of sustained R&D investment, Airware encompasses eight specialized alloy formulations that deliver lower density, higher stiffness, better thermal stability, and superior corrosion resistance compared to conventional aerospace aluminum. In practical terms, Airware enables weight reductions of 20% to 25% in structural aircraft components. These alloys go into fuselage skins, stringers, floor structures, seat tracks, window frames, and wing components on programs including the Boeing 787 Dreamliner and the Airbus A350.

The content numbers are striking. For each Airbus A350 produced, Airbus purchases approximately 75 to 80 metric tons of Airware. The buy-to-fly ratio — meaning how much raw material is needed to produce the finished parts — sits around 20%, which means more than 60 tons of machining turnings are generated per aircraft. Those turnings get recycled, but the sheer volume of material flowing through each aircraft program illustrates the scale and stickiness of these customer relationships.

To make the qualification process tangible, imagine a pharmaceutical company seeking FDA approval for a new drug. The company must conduct years of trials, submit mountains of data, and wait for regulatory review before the drug can enter the market. Now imagine that once the drug is approved, no competitor can substitute their version without going through the entire approval process again — from scratch. That is essentially how aerospace material qualification works. The Nadcap (National Aerospace and Defense Contractors Accreditation Program) certification process alone involves months of formal assessment, but full alloy qualification for a major program can stretch across many years of cumulative testing.

Now here is the critical competitive insight: once Airware or any other Constellium alloy is qualified on an aircraft program, replacing it would require the airframe manufacturer to re-qualify the new material through the same multi-year testing regime, then seek re-certification from the FAA, EASA, and other aviation authorities. No airline wants to fly on an aircraft where the structural material was changed mid-program. No airframe manufacturer wants the cost, delay, and risk of re-qualification. The result is that supplier relationships in aerospace aluminum effectively last for the life of the aircraft program — typically twenty to thirty years of production, plus aftermarket support for decades beyond that.

Constellium's customer roster reads like a who's who of global aerospace. Beyond Boeing and Airbus, the company supplies Embraer, Bombardier, Lockheed Martin, Pilatus, Blue Origin, and NASA. The Ravenswood plant supplied aluminum for NASA's Artemis mission — the program returning humans to the Moon. Constellium has received Airbus's "Accredited Supplier" award, the highest recognition in Airbus's supplier quality improvement program.

The margin profile tells the economic story. Constellium's Aerospace and Transportation segment posted $339 million in adjusted EBITDA in 2025, a 16% increase over the prior year. Segment EBITDA margins in aerospace typically run in the 15% to 20% range — roughly double the margins achievable in commodity aluminum rolling. These are not commodity economics. These are specialty materials economics, protected by certification barriers, proprietary alloy portfolios, and customer relationships measured in decades.

There is also a persistent myth worth addressing: the idea that carbon fiber composites are displacing aluminum in modern aircraft. While composites have indeed gained share — the Boeing 787 and Airbus A350 are roughly 50% composite by weight — aluminum has not disappeared. Instead, the remaining aluminum applications have moved toward higher-performance alloys like Airware that justify their presence precisely because they offer properties that composites cannot match in certain structural applications, particularly those requiring damage tolerance and repairability. The aluminum content per aircraft has actually become more specialized, more valuable, and harder to substitute.

The aftermarket opportunity adds another dimension to the aerospace moat. Aircraft operate for twenty-five to thirty years, and throughout their service lives they require maintenance, repair, and overhaul (MRO) that often involves replacing aluminum structural components with material from the original qualified supplier. This creates a revenue tail that extends decades beyond the initial aircraft delivery. Constellium's long-term partnerships with airframe manufacturers thus encompass not just new-build production but also the lucrative aftermarket business that follows.

To put Constellium's aerospace position in its simplest terms: this is a business where you win a qualification that takes half a decade, then supply material for two to three decades of production, then continue supplying repair material for another two to three decades of service life. The total customer relationship can span fifty years or more. In a world where most businesses are fighting for quarterly customer retention, that kind of durability is extraordinary.

For investors, the aerospace business is the bedrock: high barriers, long contract durations, and margins that reflect genuine pricing power rather than cyclical tailwinds.

VI. The Automotive Revolution: Betting on Lightweighting

In 2014, Ford Motor Company did something that shocked the automotive industry: it announced that the next-generation F-150, America's best-selling vehicle for decades running, would swap its steel body for one made of military-grade aluminum alloy. When the 2015 F-150 rolled off the line, it weighed up to 700 pounds less than its predecessor. The lightweighting revolution had gone mainstream.

The significance of Ford's decision went far beyond one truck model. The F-150 is not just America's best-selling vehicle — it is, in many ways, the bellwether of the entire US automotive industry. If aluminum could work on the F-150, with its demanding requirements for durability, crash performance, and corrosion resistance in every climate from Minnesota winters to Arizona summers, it could work anywhere. The 2015 F-150 was proof of concept for the entire automotive lightweighting thesis.

For Constellium, the Ford decision was a watershed. The company became one of Ford's largest suppliers of aluminum structural components for the F-150 program, investing $40 million to expand its Van Buren, Michigan plant to 210,000 square feet to meet demand. Since 2015, the Van Buren facility has delivered more than 50 million components for Ford's aluminum-intensive trucks and SUVs, including the F-150, F-150 Lightning, Explorer, Super Duty, and Expedition.

But the automotive story was not just about Ford. The regulatory environment was creating irresistible pressure for every global automaker to reduce vehicle weight. In the United States, Corporate Average Fuel Economy (CAFE) standards demanded steadily improving fuel efficiency. In Europe, CO2 emissions targets for new car fleets were ratcheting tighter with every regulatory cycle. In China, new energy vehicle mandates were pushing manufacturers toward electrification and, by extension, lightweighting. The physics are simple: a lighter vehicle travels further on a gallon of gasoline or a kilowatt-hour of battery charge. Aluminum body panels and structural components can reduce weight by roughly 40% compared to steel equivalents, making the material indispensable for meeting regulatory requirements.

Constellium built out its automotive capabilities across multiple geographies to serve OEMs close to their assembly plants. The Singen facility in southern Germany — a plant with over a century of operations, tracing its roots to the early days of European aluminum manufacturing — houses one of the largest extrusion presses in Western Europe. This 100-meganewton machine is capable of producing the complex crash management systems, side impact beams, and structural components that European automakers demand. Extrusion, for those unfamiliar with the process, works like squeezing toothpaste from a tube: a heated aluminum billet is forced through a shaped die to produce a continuous profile with a precise cross-section. The resulting extrusions can be extraordinarily complex in shape, allowing engineers to design components that optimize both strength and weight in ways that would be impossible with traditional stamping. Constellium supplies crash management systems for the BMW X4 and X5, advanced aluminum solutions for the Audi e-tron GT, structural components for Mercedes-Benz, and auto body sheet for the Maserati Grecale.

The Bowling Green, Kentucky plant tells another important chapter of the automotive story. Originally a joint venture formed in 2014 with Japanese aluminum producer UACJ, the facility was purpose-built to produce automotive body sheet with an annual capacity of 100,000 metric tons. In January 2019, Constellium purchased UACJ's 49% stake for $100 million, taking full ownership and control. The move reflected Constellium's confidence in the North American automotive body sheet market and its desire to control its own destiny in a segment where demand was growing rapidly.

The margin math in automotive differs significantly from aerospace, and understanding the difference is key to understanding Constellium's strategy. Automotive EBITDA margins typically run in the 10% to 12% range — lower than aerospace's 15% to 20% — because automakers wield enormous buyer power. When your customer is BMW or Ford, the negotiation dynamic favors the buyer. Automotive programs are competitively bid, often with two or three qualified suppliers competing for a production contract. Price negotiations can be intense, and annual cost-down targets — where the OEM expects the supplier to reduce prices by a fixed percentage each year — are standard practice in the industry.

But the volume potential is massive. A single automotive body sheet program can consume tens of thousands of metric tons annually, compared to the relatively smaller volumes in aerospace. The trade-off is scale for margin. And from a portfolio perspective, automotive provides a diversification benefit: aerospace is tied to aircraft production cycles that can be volatile (as the MAX grounding demonstrated), while automotive demand, though cyclical, follows a different pattern driven by consumer spending, regulatory requirements, and model-year cycles.

Beyond the established German luxury brands, Constellium was also positioning itself to serve the broader European and North American EV supply chain. The company supplied auto body sheet for the Maserati Grecale SUV and was developing relationships with newer EV-focused manufacturers. The total addressable market for automotive aluminum was expanding as every major automaker announced aggressive electrification targets.

The electric vehicle revolution amplified the lightweighting thesis in a way that caught even optimists by surprise. A modern EV battery pack weighs 500 kilograms or more — roughly the weight of a grand piano bolted to the vehicle's floor. That added mass demands compensating weight reduction everywhere else in the vehicle structure: body panels, crash structures, door frames, roof rails. Constellium developed its HSA6 family of alloys specifically for EV battery enclosures, providing both crash and intrusion resistance and thermal management properties. The company also led the ALIVE consortium with BMW and Volvo, developing modular battery enclosure designs that reduced capital costs by 50% to 60% compared to conventional approaches.

The competitive landscape in automotive aluminum was fiercely contested. Novelis, the Hindalco-owned rolled products giant, was the world's largest aluminum rolling company and a formidable competitor. Arconic Corporation, spun off from the old Alcoa empire, competed directly in sheet, plate, and extrusions. Kaiser Aluminum, Norsk Hydro, and AMAG of Austria all contested various segments. Constellium's differentiation rested on its engineering capabilities — the ability to develop alloys tailored to specific OEM requirements — and its geographic proximity to key assembly plants across Europe and North America.

The Neuf-Brisach plant in Alsace, France, deserves mention in the automotive story. Founded in 1967, Neuf-Brisach is one of Europe's largest integrated aluminum rolling facilities, with capacity of 450,000 metric tons annually. The plant houses rolling, finishing, and recycling operations under one roof, including a 240-meter automotive finishing line capable of producing 100,000 tons of automotive body sheet per year. This integrated model — where scrap from the rolling process is recycled on-site and fed back into production — illustrates how Constellium has built closed-loop manufacturing systems that reduce costs, improve sustainability, and deepen customer relationships. Automakers increasingly demand verified recycled content in their supply chains, and Constellium's integrated recycling capabilities provide a competitive edge in winning programs where sustainability credentials matter.

The automotive business was a bet on a mega-trend, and by the mid-2020s that bet was paying off in volume if not always in margins. The question for Constellium was whether it could keep growing the business while defending pricing in the face of powerful customers and increasingly capable competitors.

VII. The Aleris Acquisition That Wasn't (2018-2019)

In the world of specialty aluminum, there were only so many major players. Constellium, Novelis, Arconic, Aleris, Kaiser — each occupied distinct but overlapping niches. And in the logic of industrial consolidation, the number of independent players was destined to shrink. The question was who would acquire whom, and whether regulators would allow it.

Aleris International, a Cleveland-based aluminum rolled products company, was the tantalizing puzzle piece. Aleris had meaningful automotive body sheet capacity in both the United States and Europe, a complementary aerospace business, and the kind of scale that could transform an acquirer's competitive position. For any of the major players, absorbing Aleris would shift the industry's center of gravity.

In July 2018, Novelis — the Hindalco subsidiary — announced its intention to acquire Aleris for approximately $2.6 billion plus the assumption of debt. The deal excited the market and validated the consolidation narrative that had been building for years. But it also set off alarm bells among regulators. In September 2019, the U.S. Department of Justice sued to block the transaction, arguing that combining Novelis and Aleris would give the merged entity roughly 60% of projected total U.S. automotive body sheet capacity — enough market power to raise prices and suppress innovation. The case highlighted just how concentrated the automotive aluminum supply chain had become.

Geopolitical currents complicated matters further. The deal unfolded against the backdrop of the U.S.-China trade war, with aluminum tariffs, industrial policy concerns, and strategic competition coloring every regulatory decision.

China's SAMR (State Administration for Market Regulation) ultimately approved the transaction but imposed conditions, including the divestiture of Aleris's Duffel, Belgium plant. After making concessions to address both U.S. and Chinese regulatory concerns, Novelis completed the acquisition in 2020 for approximately $2.8 billion.

For Constellium, the Novelis-Aleris deal was a competitive event of the first order. The combined entity created a significantly larger competitor in automotive body sheet, raising the stakes for Constellium's own automotive growth strategy. Whether Constellium had seriously pursued Aleris independently is a matter of industry speculation, but the outcome was clear: the organic growth path, rather than transformative M&A, would define Constellium's strategy going forward.

The episode taught the specialty aluminum industry a broader lesson about the limits of consolidation in a multipolar world. Regulators in the United States, Europe, and China each had their own competitive concerns, their own industrial policy agendas, and their own willingness to block or condition deals. Any future mega-deal in the space would have to navigate a thicket of overlapping regulatory jurisdictions — a constraint that effectively favored organic growth and targeted bolt-on acquisitions over industry-reshaping transactions.

Constellium pivoted accordingly, focusing its capital on expanding existing plant capacity, developing new alloy families, and deepening customer relationships. The Bowling Green buyout of UACJ's stake was emblematic of this approach: incremental, strategic, and fully within Constellium's control. The era of transformative deals had given way to the era of operational excellence.

From Constellium's perspective, there was an important silver lining to the Novelis-Aleris outcome. The DOJ's willingness to challenge the deal on antitrust grounds validated the argument that the automotive aluminum market was concentrated enough that further consolidation would be harmful — which, by extension, validated Constellium's own competitive position. If the market were truly commoditized with many interchangeable suppliers, the DOJ would not have cared about one more merger. The fact that regulators treated the combination as anticompetitive affirmed that there were meaningful barriers to entry and limited substitutability among the major players.

The Aleris saga also revealed something about the structure of the specialty aluminum industry that is worth pausing on. Unlike technology or pharmaceuticals, where intellectual property and network effects can create winner-take-all dynamics, the aluminum rolling business is fundamentally regional and relationship-driven. Plants serve customers within a geographic radius, alloy qualifications are customer-specific, and capacity additions take years to build and certify. This means that consolidation does not create the kind of efficiency gains that might be expected in a more standardized industry. Combining two plant networks does not yield dramatic synergies if the plants serve different customers in different regions with different alloy specifications. The regulators understood this — and so did Constellium's management, which increasingly framed its strategy around organic investment and operational excellence rather than acquisition-driven growth.

VIII. Navigating the Pandemic & Supply Chain Crisis (2020-2021)

Constellium entered 2020 already reeling from one crisis. Boeing's 737 MAX had been grounded since March 2019 following two fatal crashes — the longest grounding of a U.S. airliner in history, stretching to twenty months. Boeing had halted 737 production in January 2020, vaporizing demand for the aluminum sheet and plate that Constellium supplied for the program. Aerospace shipment volumes were down, and the company was recalibrating its production schedules for a slower-than-expected MAX return.

Then COVID-19 hit. By March 2020, the world that Constellium had spent a decade building its strategy around — growing global air travel, expanding automotive production, increasing demand for lightweighting — seemed to be collapsing simultaneously.

The pandemic's impact on Constellium was a study in the divergent fortunes of its two major end markets. Aerospace was catastrophic. Global air traffic collapsed by more than 60% in 2020. Airlines parked hundreds of aircraft, deferred deliveries, and slashed orders. Boeing and Airbus dramatically cut production rates — the A320 program dropped from 60 aircraft per month to 40, and widebody programs were cut even more severely. For Constellium's Aerospace and Transportation segment, adjusted EBITDA fell 51% in the second quarter of 2020 compared to the same period in 2019. This was not a downturn. It was an evaporation.

Automotive presented a different pattern: a violent collapse followed by a sharp recovery. The second quarter of 2020 was the worst, with revenue plunging 31% as assembly plants across Europe and North America shut down for weeks. But then something unexpected happened. Consumer demand for vehicles roared back in the second half of 2020, fueled by stimulus payments, suburban migration, and a shift away from public transportation. By the end of the year, automotive was recovering faster than almost anyone had projected.

Constellium's full-year 2020 revenue declined approximately 17% to roughly $5.25 billion. The company responded with a combination of furloughs, cost reductions, and — critically — protecting core capabilities. Management made the deliberate decision not to lay off workers whose specialized skills in aerospace metallurgy and precision rolling would take years to rebuild. In Germany, the kurzarbeit (short-time work) program allowed Constellium to reduce hours without permanent layoffs, preserving institutional knowledge while cutting costs.

The human toll of the pandemic response was significant. While exact headcount reductions were not disclosed in granular detail, the combination of furloughs, reduced hours, and production shutdowns affected thousands of workers across the company's global footprint. In France, the government's chômage partiel (partial unemployment) scheme — similar to Germany's kurzarbeit — provided wage subsidies that allowed Constellium to retain workers even when production lines were idle. Without these European social safety net programs, the company might have been forced into permanent layoffs that would have gutted its ability to ramp production when demand returned.

One of the most remarkable aspects of Constellium's pandemic performance was its cash management. Despite the revenue collapse, the company generated $157 million in free cash flow in 2020 — a testament to aggressive working capital management and capex deferrals. The company also refinanced debt to extend maturities and maintain liquidity, navigating the covenant landscape without requiring a dilutive equity raise.

The semiconductor shortage that gripped the automotive industry in 2021 created an ironic silver lining for Constellium. Because automakers could not obtain enough chips to run their assembly lines at full capacity, the pressure on aluminum supply was moderated. Constellium could serve its automotive customers without the margin-compressing scramble that typically accompanies demand spikes. Meanwhile, aerospace remained in a slow-burn recovery mode — the MAX was recertified by the FAA in November 2020 and resumed commercial flights in December, but the production ramp was gradual and Boeing's quality issues would continue to constrain build rates for years.

By the end of 2021, revenue had rebounded to roughly $8.2 billion — a 26% jump from 2020 — driven primarily by the automotive recovery and rising metal prices that inflated revenue through pass-through mechanisms. The company's diversification across aerospace, automotive, and packaging had proven its value. Companies concentrated solely in aerospace — or solely in automotive — faced far more existential challenges. Constellium's portfolio structure, for all its complexity, had served as a natural hedge.

The pandemic also forced a reckoning with the company's operational footprint. With aerospace volumes depressed, the Issoire and Ravenswood mills operated at reduced capacity — painful given the high fixed costs of these facilities. Conversely, the automotive plants at Van Buren, Bowling Green, and Singen saw demand whipsaw from zero to full capacity in a matter of months. Managing this asymmetric recovery across segments required the kind of operational agility that does not show up in financial statements but defines the difference between companies that emerge from crises stronger and those that emerge diminished.

The Muscle Shoals facility in Alabama, one of Constellium's largest sites, played a critical role in the recovery. The plant produces beverage can stock — one of the steadiest demand segments in the aluminum industry, as people continued buying canned beverages through the pandemic — and operates a recycling center capable of processing more than 25 billion used beverage cans per year, or roughly 340,000 metric tons of recycled aluminum annually. While aerospace collapsed and automotive seesawed, the packaging business provided a stabilizing ballast. The plant's recycling capabilities also reduced reliance on primary aluminum and its associated energy costs — a structural advantage that would become even more important when the energy crisis hit Europe barely a year later.

The pandemic experience reinforced management's conviction in the long-term growth trajectories of both end markets. Aerospace backlogs remained massive even as near-term production was constrained. The automotive lightweighting trend had, if anything, accelerated as the EV transition gained momentum. The question was no longer whether Constellium's end markets would recover, but how quickly — and whether a new crisis would intervene first.

IX. The Energy Crisis & Aluminum's European Challenge (2021-2023)

Just as Constellium was emerging from the pandemic's shadow, with revenue rebounding and automotive demand roaring back, the next crisis arrived from an entirely different direction.

On February 24, 2022, Russia invaded Ukraine, and overnight the economic assumptions underlying European manufacturing were upended. The continent that had built its industrial base on affordable Russian natural gas suddenly faced an energy crisis of existential proportions. TTF natural gas prices — the European benchmark — exploded from roughly €20 per megawatt-hour in early 2021 to a peak of €319 per megawatt-hour on August 26, 2022, the day Russia shut down the Nord Stream pipeline. That was a sixteen-fold increase in less than two years.

For the aluminum industry, the implications were devastating. Primary aluminum smelting is one of the most energy-intensive industrial processes in existence, requiring 13 to 15 megawatt-hours of electricity to produce a single ton of metal. At pre-crisis energy prices, European smelters were competitive. At crisis prices, they were economically unviable. European primary aluminum production collapsed by more than 25% from 2010 levels, creating what the industry described as a 93% structural deficit — meaning Europe was producing only a fraction of the primary aluminum it consumed. Plants like Slovalco in Slovakia shut down entirely. The European aluminum smelting industry, once a cornerstone of the continent's industrial base, was being hollowed out.

To appreciate the scale of the disruption, consider that Europe went from being a major primary aluminum producer to being almost entirely dependent on imports in the span of a few years. The smelters that shut down represent billions of dollars of capital investment and decades of operational expertise — assets that will not easily return even if energy prices normalize, because restarting a cold smelter is enormously expensive and time-consuming. The aluminum industry experienced a permanent restructuring of its European footprint, with primary production migrating to the Middle East (where abundant natural gas provides cheap electricity), Iceland (geothermal power), Canada (hydroelectric power), and China (coal-fired but heavily subsidized).

Here is where Constellium's business model revealed a critical structural advantage. The company is a downstream processor — a roller and fabricator of aluminum — not a primary smelter. Constellium purchases commodity aluminum from global markets and transforms it into specialized products. Its energy consumption, while significant, is a fraction of what primary smelting requires. Rolling, extruding, and heat-treating aluminum are energy-intensive operations, but they do not carry the same existential vulnerability to electricity prices that smelting does.

Furthermore, Constellium's contract structures include pass-through mechanisms for metal prices. The company purchases aluminum at prevailing commodity prices and passes the metal cost through to customers, capturing value in the "conversion premium" — the fabrication fee for transforming commodity metal into specialized products. This means that when aluminum prices spike, Constellium's revenue increases but the company's margin is primarily a function of its fabrication efficiency, not the underlying metal price. The arrangement is not a perfect hedge — working capital requirements increase when metal prices rise, and there can be timing mismatches between purchase and pass-through — but it provides far more protection than a vertically integrated model.

The energy crisis also created a competitive restructuring that, paradoxically, benefited surviving European downstream processors. As European smelters shut down and capacity exited the market, the remaining fabricators faced less domestic competition for customer contracts. Constellium reported a 61% increase in profitability per unit of metal during this period, reflecting improved industry structure and pricing power. European Union gas demand fell by 55 billion cubic meters — a 13% decline and the steepest drop in history — as the continent scrambled to replace Russian supply with LNG imports and demand destruction.

The crisis accelerated Constellium's own energy transition. The company closed its last coal-fired power station at the Singen plant in Germany, cutting the facility's direct greenhouse gas emissions by more than 25% between 2021 and 2025. Management invested in efficiency improvements across the plant network and explored power purchase agreements to lock in more predictable energy costs.

Germany presented a particular strategic tension. It was simultaneously Constellium's most important automotive market — home to BMW, Mercedes, Audi, and Volkswagen — and one of its most energy-vulnerable manufacturing locations. By late 2023, European gas prices had fallen to around €34 per megawatt-hour, but industrial consumers in Europe still faced gas costs roughly 30% higher than China and five times higher than the United States. The structural energy disadvantage was real, and it raised uncomfortable questions about the long-term competitiveness of European manufacturing.

The reshoring narrative gained significant traction during this period. Automakers, aerospace companies, and defense manufacturers increasingly prioritized supply chain resilience over pure cost optimization. Having a domestically located, energy-secure aluminum supplier became a strategic consideration, not just a procurement detail. Constellium's US operations — Muscle Shoals, Ravenswood, Bowling Green, and Van Buren — benefited from this shift in thinking. American natural gas prices, anchored by abundant shale production, were a fraction of European levels. The Inflation Reduction Act and Bipartisan Infrastructure Law provided additional incentives, including the $75 million DOE investment at Ravenswood for low-emission technology.

For Constellium, the energy crisis was a validation of its business model's resilience but also a warning about the fragility of the European industrial ecosystem. The company's downstream positioning, pass-through pricing, and diversified geography provided insulation. But the broader question of whether Europe could sustain energy-intensive manufacturing in a post-Russian-gas world remained open. The 2023 revenue of roughly $8.8 billion and a record adjusted EBITDA of €713 million demonstrated that the company could not only survive but thrive during the crisis — though the tailwind of reduced European competition would eventually moderate as the energy market normalized.

X. The EV Era & Future of Lightweighting (2023-Present)

The energy crisis chapter barely had time to close before the next transformation demanded Constellium's attention. The electric vehicle revolution was rewriting the rules of automotive materials — and creating both enormous opportunities and existential questions for aluminum specialists.

Consider the engineering challenge that defines the modern electric vehicle: a battery pack weighing 500 kilograms or more sits in the floor of the car, adding the equivalent of three or four adult passengers to the vehicle's mass before a single human climbs aboard. Every additional kilogram of battery weight must be compensated by weight reduction elsewhere — body panels, structural members, crash structures, closures — or the vehicle's range, handling, and safety all suffer. This physics problem has made aluminum more essential to automotive engineering than at any point in history.

But the EV era has also introduced a formidable competitive threat: gigacasting. Pioneered by Tesla, gigacasting uses enormous die-casting machines to produce large structural components — entire rear underbodies, for example — as single pieces of cast aluminum rather than assembling them from dozens of individually rolled, stamped, and welded parts. The approach dramatically reduces manufacturing complexity and cost. For a company like Constellium, whose business depends on selling rolled and extruded aluminum products that are subsequently fabricated into components, gigacasting represents a potential displacement of traditional manufacturing processes.

Think of gigacasting as the aluminum equivalent of the smartphone replacing the flip phone — a fundamentally different manufacturing approach that does certain things brilliantly but cannot do everything. A gigacast rear underbody eliminates dozens of stamped and welded parts, saving assembly time and tooling costs. But it uses a different type of aluminum (cast alloys rather than wrought alloys), requires enormous capital investment in the casting machines themselves (each costing $50 million or more), and presents its own challenges in terms of repairability, material properties, and production flexibility.

Constellium's response has been characteristically metallurgical: rather than fighting the gigacasting trend, the company has focused on developing alloys and products for the applications that gigacasting cannot easily address. Structural battery enclosures require materials that combine crash resistance, thermal management properties, and corrosion protection — a combination of requirements that favors Constellium's engineered alloy systems. The company's HSA6 alloy family was developed specifically for this application, providing the crash and intrusion resistance that regulators demand alongside the thermal properties needed to contain and protect battery cells.

In 2025, Constellium achieved a notable milestone: the first industrial-scale hydrogen casting at its C-TEC research center in Voreppe, France, successfully producing a 12-metric-ton aluminum slab intended for EV applications by substituting natural gas with hydrogen in the casting process. The company also inaugurated a new finishing line at its Singen plant in Germany — a 30-million-euro investment in partnership with Lotte Infracell — to produce aluminum foilstock for EV battery applications in Europe. These investments position Constellium for the next generation of EV materials needs, where sustainability credentials and carbon footprint become differentiating factors in OEM procurement decisions.

The competitive landscape for lightweight materials has grown more complex. Aluminum competes not only with traditional steel but with advanced high-strength steel alloys (which are cheaper though heavier), carbon fiber composites (which are lighter but dramatically more expensive), and magnesium alloys (which are lighter still but more difficult to work with). Each material has its sweet spot. Aluminum's advantage lies in its combination of reasonable cost, good formability, excellent recyclability, and well-established manufacturing infrastructure. Constellium's strategic bet is that this combination will keep aluminum at the center of the lightweighting toolkit even as competing materials evolve.

China's growing dominance in aluminum extrusions represents another challenge. Chinese producers have built enormous capacity in extruded aluminum products, competing aggressively on price in global markets. While Constellium's high-value aerospace and specialized automotive products are less vulnerable to Chinese commodity competition, the company's simpler extrusion and industrial products face pricing pressure.

On the aerospace side, the recovery trajectory remained a multi-year story that tested the patience of investors who had been hearing about "pent-up demand" and "massive backlogs" for years. Boeing's ongoing quality and production challenges — including the aftermath of the January 2024 Alaska Airlines door plug incident, which led to renewed FAA scrutiny and production caps — constrained narrow-body production rates well below pre-crisis levels. Airbus was ramping A320neo production toward 75 aircraft per month but faced its own supply chain bottlenecks. New programs, including the A321XLR and Boeing 777X, represented future growth vectors but had been delayed repeatedly. Constellium's 2025 aerospace demand was affected by continued destocking of aluminum products in the global supply chain, though demand for high-value-add products like Airware remained strong.

Sustainability has emerged as a genuine competitive differentiator rather than a mere marketing exercise. The European Union's Carbon Border Adjustment Mechanism (CBAM) places a carbon price on imported aluminum products, potentially advantaging European producers who use cleaner energy and more recycled content. Constellium has achieved Aluminium Stewardship Initiative (ASI) certification at multiple facilities — Muscle Shoals, Bowling Green, Neuf-Brisach, Singen, and Gottmadingen — and its recycling operations at Muscle Shoals process more than 25 billion used beverage cans per year. In June 2025, the company recycled aluminum from end-of-life aircraft in collaboration with TARMAC Aerosave and Airbus, demonstrating a circular economy approach from aircraft to aircraft.

The partnership with Renault Group on the ISA3 project, completed in December 2024, developed a lightweight aluminum door for compact battery EVs that achieved a 14% weight reduction and a 33% reduction in global warming potential compared to conventional designs. These are the kinds of incremental innovations that do not generate headlines but steadily expand Constellium's addressable market within the EV supply chain.

There is also a myth worth addressing about the relationship between EVs and aluminum demand. Some bears argue that gigacasting, by producing larger structural components in single pieces, will reduce total aluminum content per vehicle. The reality is more nuanced. Gigacasting uses cast aluminum alloys — a different product category from the rolled and extruded products that Constellium primarily produces. While gigacasting may displace some stamped aluminum sheet in structural applications, the overall aluminum content per EV remains higher than in comparable internal combustion vehicles because of the need for battery enclosures, thermal management systems, and weight-compensating body structures. The mix of aluminum products changes, but the total addressable market expands. Constellium's challenge is to ensure its rolled and extruded products remain integral to EV architectures even as casting technology evolves.

The 2024 financial year illustrated both the promise and peril of Constellium's position. Revenue came in at approximately $7.3 billion, and adjusted EBITDA was $623 million — down from the 2023 record — as severe flooding from the Rhone River in June 2024 shut down the company's Swiss facilities at Sierre and Chippis for months. The flooding impact cost an estimated $33 million in EBITDA and $45 million in free cash flow. Production restarted by late October and returned to full operations by November. The episode was a stark reminder that even the most carefully managed industrial business remains vulnerable to forces of nature — and that geographic concentration in a single valley can amplify natural disaster risk.

XI. The Business Model Deep Dive

Having traced Constellium's journey from Pechiney's nationalized legacy through private equity transformation, public markets baptism, and serial crises, it is worth stepping back to examine the mechanics of how this business actually makes money.

Constellium's economic engine can be described in a single sentence: buy commodity aluminum, apply metallurgical expertise and manufacturing precision, and sell the resulting product at a substantial premium to the input cost. The spread between what the company pays for raw aluminum and what it charges for finished products — the "conversion premium" — is where all of Constellium's value is created.

This model has an elegant feature: metal price pass-through. Because the cost of the underlying aluminum is contractually passed to customers, Constellium's profitability is theoretically insensitive to swings in commodity prices.

In practice, it is not quite that clean. Rising metal prices inflate working capital requirements because the company must finance larger metal inventories. There are timing lags between purchasing metal and billing customers. And metal premium dynamics — the regional surcharges above the London Metal Exchange benchmark — can create both windfalls and headwinds depending on market conditions. In 2025, favorable metal cost dynamics contributed meaningfully to the record performance of the Packaging and Automotive Rolled Products segment, which posted $353 million in adjusted EBITDA, up 46% from the prior year.

The company operates through three reportable segments. Aerospace and Transportation (A&T) produced the highest-margin products — specialized plate, sheet, and extrusions for aircraft, defense, and space applications — generating $339 million in 2025 adjusted EBITDA. Packaging and Automotive Rolled Products (P&ARP) was the largest segment by volume, producing can stock, automotive body sheet, and heat exchanger materials, and delivered the biggest EBITDA gains in 2025. Automotive Structures and Industry (AS&I) focused on extruded structural components, crash management systems, and hard alloy products, contributing $72 million in adjusted EBITDA.

Customer concentration is a double-edged sword. Constellium's top ten customers represent more than 60% of revenue — a level of concentration that provides deep relationships and predictable volumes but also creates negotiating leverage for buyers and revenue vulnerability if any major customer reduces orders.

When Boeing slows 737 production or a European automaker cuts models, the impact flows directly to Constellium's results. This is not hypothetical — the company lived through exactly this scenario during the MAX grounding and the pandemic.

Capital intensity is an inherent feature of the business. Constellium typically spends $200 million to $300 million per year on capital expenditures to maintain and upgrade its plant network, develop new alloys, and expand capacity. In 2026, the company guided to $115 million in growth capex, concentrated on aerospace and recycling projects at Issoire, Muscle Shoals, and Ravenswood. The Ravenswood facility was selected by the U.S. Department of Energy for up to $75 million in Bipartisan Infrastructure Law and Inflation Reduction Act funding for low-emission technology — a meaningful offset to the company's own capital requirements.

The geographic footprint — major operations in France, Germany, Switzerland, the Czech Republic, and the United States — creates natural hedges and strategic flexibility. European plants serve European OEMs with minimal logistics cost and maximum responsiveness. American plants serve North American customers and benefit from lower energy costs. But the footprint also creates exposure to multiple regulatory regimes, labor markets, and currency fluctuations. The Swiss flooding of June 2024, which shut down Constellium's Sierre and Chippis facilities for months and cost $33 million in EBITDA and $45 million in free cash flow, illustrated the operational risks of a distributed manufacturing network.

The balance sheet story has been one of gradual deleveraging. Net debt stood at approximately $1.7 billion at the end of 2025, representing a leverage ratio of roughly 2.0 times adjusted EBITDA — within management's target range of 1.5 to 2.5 times.

The company has been returning cash to shareholders through a $300 million share repurchase program announced in 2023, of which approximately $194 million had been deployed through the end of 2025, retiring roughly 13.5 million shares. With a market capitalization of approximately $3.5 billion and an enterprise value of roughly $5.2 billion, Constellium trades at about six times trailing adjusted EBITDA — a modest valuation for a company posting record results.

The CEO transition from Jean-Marc Germain to Ingrid Joerg, effective January 1, 2026, marked a new chapter. Joerg, a Swiss citizen who joined Constellium in 2015 as president of Aerospace and Transportation and was promoted to Chief Operating Officer in 2023, brings more than 25 years of aluminum industry experience. Her career included a notable stint as CEO of Aleris Rolled Products Europe — giving her intimate knowledge of one of Constellium's key competitors — as well as leadership roles at Alcoa and AMAG Austria.

Her appointment signaled continuity — she was the architect of the aerospace strategy that delivered record results — while also bringing a fresh operational intensity to the CEO role. The board, chaired by Jean-Christophe Deslarzes since 2022, made the transition smooth by having Germain serve as Special Advisor to the Board and management throughout 2026.

To understand the working capital dynamics, consider what happens when aluminum prices rise. Constellium must purchase more expensive metal to fill its production pipeline, tying up additional cash in inventory before the higher cost is passed through to customers in finished product pricing. This creates a temporary cash absorption that can be significant — tens of millions of dollars in a rising metal price environment. Conversely, when metal prices fall, working capital releases cash as inventory values decline. These swings can make free cash flow volatile from quarter to quarter even when underlying operational performance is steady. Investors who focus only on adjusted EBITDA without understanding the metal-price-driven working capital dynamics can be caught off guard by free cash flow misses that have nothing to do with the company's competitive position.

The geographic diversification of the plant network — France, Germany, Switzerland, Czech Republic, Slovakia, and across the United States — is both a strategic asset and an operational complexity. Each jurisdiction brings its own labor laws, environmental regulations, energy markets, and tax regimes. But the diversification also provides natural hedging against regional risks. When European energy costs spiked, the US operations provided stable margins. When the Swiss flooding disrupted Valais production, other facilities could partially compensate. And having plants near major automotive assembly clusters in southern Germany, northern France, and the US Midwest reduces logistics costs and strengthens customer relationships through proximity.

Management's Vision 2028 targets call for $900 million in adjusted EBITDA and $300 million in free cash flow, with 2026 guidance set at $780 to $820 million in adjusted EBITDA and more than $200 million in free cash flow. These targets imply modest but steady improvement from the 2025 record base, driven by aerospace recovery, automotive program ramps, and continued operational efficiency gains.

XII. Porter's 5 Forces & Hamilton's 7 Powers Analysis

With the business model understood and the historical context established, the analytical frameworks of competitive strategy offer a structured way to assess where Constellium's advantages are real and where they are illusory.

Analyzing Constellium through the lens of competitive strategy reveals a company whose moat is genuine but concentrated — fearsomely strong in one segment, more contested in others.

Supplier Power runs medium to high. Constellium purchases commodity aluminum from a global market with multiple suppliers, which limits any single supplier's leverage. However, the company is exposed to energy costs — particularly in Europe — and to the regional metal premiums that can swing significantly based on logistics and trade policy. The aluminum market is ultimately a commodity market, and while Constellium does not smelt its own metal, it depends on the health and pricing of the upstream supply chain. During the energy crisis, the collapse of European smelting capacity demonstrated how supplier-side disruptions can ripple through the value chain, even for downstream processors.

Buyer Power is the force that most dramatically varies across Constellium's segments. In automotive, buyer power is formidable. A handful of massive OEMs — BMW, Mercedes, Ford, Volkswagen — control enormous purchasing volumes and have the sophistication to play suppliers against each other. Automotive contracts tend to be competitively bid, with price negotiations that favor the buyer. In aerospace, the dynamic flips. Switching costs are so high — years of re-qualification, regulatory re-certification, and supply chain reconfiguration — that once Constellium is locked in as a supplier on an aircraft program, the airframe manufacturer has limited incentive or ability to switch. This is the foundation of Constellium's pricing power in aerospace.

Competitive Rivalry is moderate and segment-specific — a crucial nuance that aggregate industry analysis often misses. In aerospace plate and advanced alloys, Constellium competes primarily with Arconic (spun off from the old Alcoa empire and further split into Howmet Aerospace and Arconic Corporation) and to a lesser extent with Alcoa, Kaiser Aluminum, and a handful of smaller players. The specialized nature of aerospace products, combined with long qualification cycles, limits the intensity of direct price competition. In automotive body sheet and extrusions, rivalry is fiercer. Novelis, now combined with Aleris, is a formidable global competitor. Norsk Hydro, AMAG, and Chinese producers all contest various segments. The automotive business is more prone to competitive bidding and margin pressure.

Threat of Substitutes presents the most nuanced challenge. In automotive, the threat is real and evolving. Advanced high-strength steels continue to improve, offering weight savings that narrow the gap with aluminum at lower cost. Tesla's gigacasting approach could displace traditional rolled and stamped aluminum components with large cast pieces. Carbon fiber composites remain a wild card — currently too expensive for mass-market vehicles but potentially disruptive if manufacturing costs decline. In aerospace, the substitute threat is much lower. While composites have gained share in airframe structures, aluminum's unique combination of damage tolerance, repairability, inspectability, and cost-effectiveness ensures its continued role in critical structural applications.

Threat of New Entrants is low — arguably the lowest of any of the five forces and a key pillar of Constellium's investability. Building a world-class aerospace plate mill requires hundreds of millions of dollars in capital investment and years of construction. Qualifying the resulting products with major airframe manufacturers adds another five to seven years. Establishing the metallurgical expertise, quality systems, and customer relationships that define competitive success in specialty aluminum takes decades. No venture-backed startup is going to disrupt this industry. The real entry threat comes from well-capitalized existing players — Chinese state-backed aluminum companies or Middle Eastern sovereign wealth fund-backed operations — that could build capacity with patient, subsidized capital.

Turning to Hamilton Helmer's 7 Powers framework, the analysis identifies Constellium's competitive position with more precision:

Switching Costs stand out as Constellium's strongest power by a wide margin. In aerospace, the multi-year qualification cycles, regulatory certification requirements, and embedded engineering relationships create switching costs that are measured in years and hundreds of millions of dollars. Once Constellium's Airware alloy is qualified on a Boeing 787 or Airbus A350 program, that relationship is effectively permanent for the life of the production run. This is not a theoretical moat — it is a contractual and regulatory reality that has protected Constellium's aerospace margins through recessions, pandemics, and energy crises.

Process Power is the second most relevant power. Constellium's manufacturing expertise — the accumulated knowledge of how to cast, roll, heat-treat, and finish aluminum alloys to exacting specifications — represents decades of institutional learning that cannot be easily replicated. Yield optimization, quality control systems, and metallurgical trade secrets are embodied in the company's workforce and processes. The C-TEC research center in Voreppe, France, where the company develops next-generation alloys and processes, is the intellectual engine of this process power.

Cornered Resource applies in a limited but meaningful way. Constellium's proprietary alloy formulations — particularly the Airware family — represent genuine intellectual property. The strategic locations of key plants, particularly Issoire and Ravenswood in aerospace and Singen in automotive, provide geographic advantages that competitors cannot replicate without enormous capital investment.

Scale Economies provide regional advantages — being the largest aerospace plate supplier in a given geography confers cost and logistics benefits — but Constellium is not large enough globally to claim dominant scale economies across its full business.

Network Effects, Counter-Positioning, and Branding are not meaningful sources of competitive advantage for Constellium. This is not a platform business, it is not disrupting incumbents with a new business model, and while the Airware brand carries weight in aerospace procurement circles, it does not drive consumer demand or pricing power in the way that consumer brands do.