Castle Biosciences: Precision Oncology's Dark Horse

I. Introduction & Episode Roadmap

Picture this: a dermatologist in Scottsdale, Arizona stares at a biopsy report. The pathology says Stage II melanoma. But what does that actually mean for this particular patient? Should she recommend aggressive treatment—sentinel lymph node biopsy, immunotherapy, the whole arsenal? Or is this one of those cases where the cancer sits quietly, never spreading, and the treatment itself becomes the greater risk? For decades, physicians had no good answer. They relied on anatomical staging—how deep the tumor went, whether it had ulcerated—and made their best guess. Sometimes they guessed right. Sometimes they did not.

Castle Biosciences exists to replace that guess with data.

Trading on the Nasdaq under the ticker CSTL, Castle Biosciences is a precision diagnostics company that generated roughly $344 million in revenue in 2025. That number alone does not capture the ambition. Castle has built something rare in healthcare: a suite of gene expression profiling tests that do not merely describe what a cancer looks like under a microscope, but predict what it is likely to do next. The difference between those two things—description versus prediction—is the difference between a photograph and a weather forecast. One tells you what happened. The other helps you decide what to do.

The central question of this deep dive is deceptively simple: How did a startup based in the suburbs of Houston and Phoenix build a defensible moat in cancer diagnostics, challenge entrenched giants like Myriad Genetics and Exact Sciences, survive a pandemic, navigate the treacherous waters of Medicare reimbursement, execute a bold acquisition strategy with mixed results, and emerge as a platform company with over $300 million in revenue and nearly $300 million in cash?

The answer involves scientific innovation, bureaucratic trench warfare, strategic brilliance, at least one expensive mistake, and the kind of patience that most Silicon Valley entrepreneurs would find physically painful. The themes that run through Castle's story—evidence as moat, reimbursement as product-market fit, the tension between focus and diversification—apply far beyond diagnostics. They are lessons about building durable businesses in regulated industries where the customer, the payer, and the end user are three different parties with three different sets of incentives.

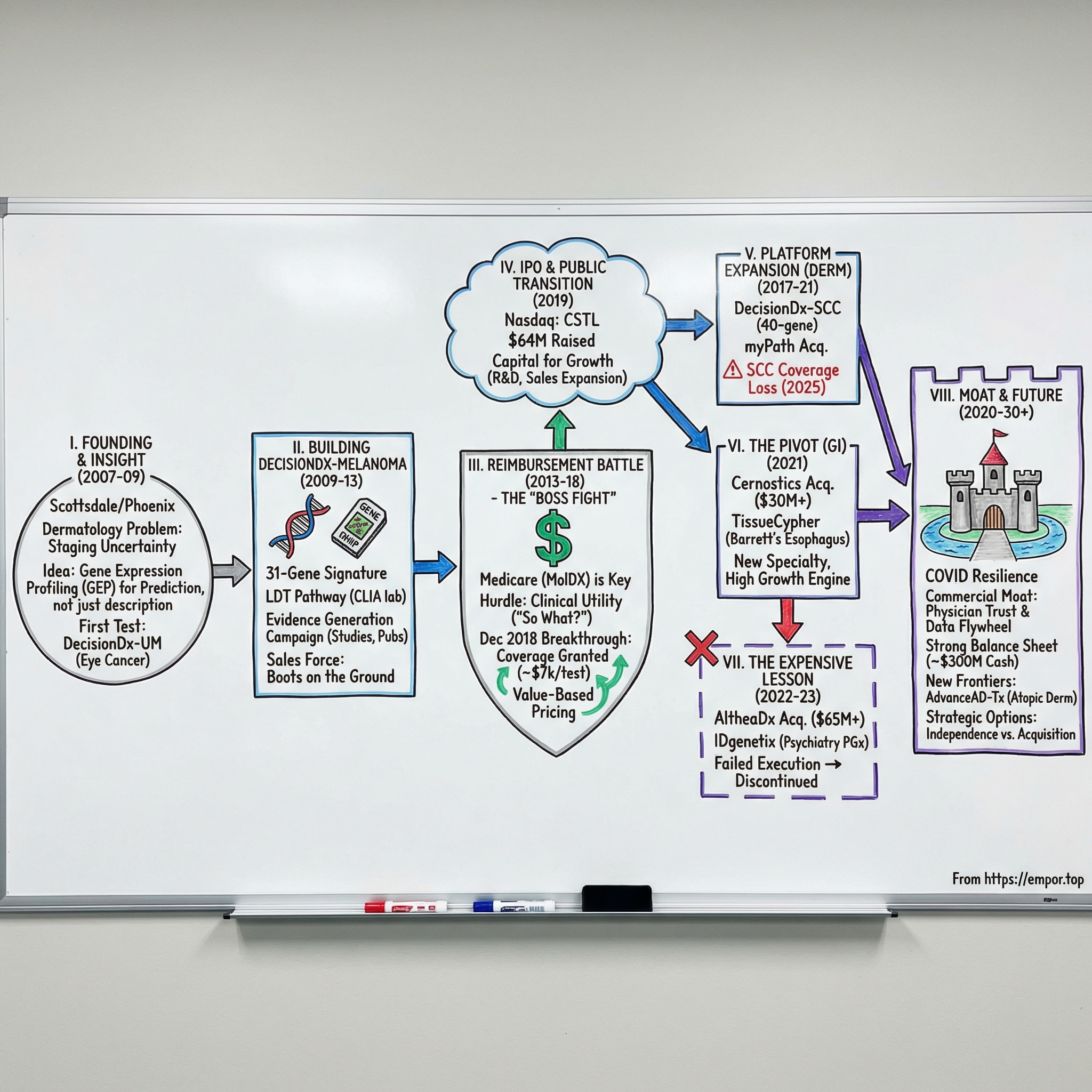

II. Founding Story & The Dermatology Insight (2007–2009)

In September 2007, while the rest of the financial world was beginning to wobble on the precipice of the Great Recession, a small group of entrepreneurs and scientists incorporated a company in Delaware with an unremarkable name and a remarkably ambitious idea. Castle Biosciences would not discover drugs. It would not treat patients directly. Instead, it would try to solve one of oncology's most persistent and costly problems: the inability to know, at the moment of diagnosis, which cancers would kill and which would not.

Derek Maetzold became the company's CEO and has remained in that role ever since—a tenure that now spans nearly two decades, making him one of the longest-serving leaders in the molecular diagnostics space. Maetzold was not a traditional scientist-turned-CEO. He brought a blend of commercial instinct and scientific credibility that proved essential in a field where physicians are deeply skeptical of anything that smells like marketing. He was joined by Kristen Oelschlager, who would serve as Chief Operating Officer, and Toby Juvenal, who took the Chief Commercial Officer role. The three arrived in October 2008—literally as Lehman Brothers was collapsing—and began building.

The founding insight was rooted in a frustration shared by dermatologists and surgical oncologists across the country. Melanoma staging, the system used to classify how dangerous a skin cancer was, relied primarily on anatomical features: how deep the tumor penetrated the skin (measured by something called Breslow thickness), whether it was ulcerated, and how fast the cells were dividing (the mitotic rate). These factors were useful but crude.

Consider the clinical dilemma: two patients walk into a dermatologist's office. Both have Stage II melanomas. Both tumors are the same depth, same size, same appearance under the microscope. The staging system treats them identically. But one patient's cancer will never return. The other's will metastasize within a year—to the lungs, brain, or liver—and become a life-threatening disease. With traditional staging alone, the dermatologist has no way to tell them apart. The result was systematic over-treatment of low-risk patients (subjecting them to surgeries and surveillance they did not need) and under-treatment of high-risk patients (failing to intervene aggressively enough when early action might have mattered). Physicians knew this was inadequate, but they lacked a better tool.

What Castle proposed was conceptually elegant: instead of judging a tumor by its appearance, judge it by what its genes are doing. Gene expression profiling—measuring which genes in a tumor are turned on or off and at what levels—could reveal the biological behavior of a cancer in ways that pathology slides could not. Think of it like this: traditional staging was like judging a book by its cover. Gene expression profiling was like reading the first three chapters. The technology to do this existed. The scientific literature suggested it was feasible. But nobody had turned it into a commercially viable, clinically validated diagnostic test for melanoma.

The early days were spent in Phoenix, where the team built a CLIA-certified laboratory. CLIA—the Clinical Laboratory Improvement Amendments—is the federal regulatory framework that governs laboratory testing in the United States. Getting CLIA certification was table stakes, but it was also a signal of seriousness. This was not consumer genomics, not the ancestry-and-wellness world of 23andMe. This was clinical-grade, physician-ordered diagnostics where a wrong answer could lead to unnecessary surgery or, worse, a missed cancer.

Interestingly, Castle's first commercial test was not for cutaneous melanoma at all. The company licensed technology from Washington University in St. Louis, building on the pioneering work of Dr. J. William Harbour, a renowned ocular oncologist who had identified gene expression signatures that predicted metastatic risk in uveal melanoma—a rare cancer of the eye. Castle launched DecisionDx-UM in December 2009, just over two years after incorporation. Uveal melanoma affects only about 2,500 Americans per year, but the clinical need was acute. Roughly half of uveal melanoma patients develop metastatic disease, almost always to the liver, and once metastases appear, outcomes are grim. The five-year survival rate for metastatic uveal melanoma is in the single digits. A test that could identify high-risk patients at the time of initial diagnosis would fundamentally change surveillance and treatment planning—allowing physicians to catch liver metastases early, when intervention might still be possible, rather than discovering them too late.

It was a small market, but it was the right market for a startup. Castle could prove the concept, build credibility with oncologists and pathologists, learn the mechanics of molecular diagnostics—specimen logistics, laboratory operations, physician reporting, insurance billing—and do it all without competing head-to-head against larger players who had no interest in a 2,500-patient-per-year niche. This is a pattern worth noting: the best beachhead markets are ones that are too small to attract well-resourced incumbents but large enough to sustain a company while it learns and iterates. Castle's decision to start with uveal melanoma rather than going directly after the much larger cutaneous melanoma market showed strategic discipline that belied the team's ambition.

III. Building DecisionDx-Melanoma: Science to Product (2009–2013)

While DecisionDx-UM was Castle's first product, the company always viewed cutaneous melanoma as the main event. The addressable population was orders of magnitude larger—roughly 100,000 Americans are diagnosed with invasive melanoma each year—and the clinical uncertainty was pervasive. The challenge was scientific: could Castle identify a set of genes whose expression patterns reliably predicted which melanomas would metastasize and which would not?

The scientific development took years. Castle's research team analyzed tumor samples, searching for gene signatures—patterns of gene activity—that correlated with metastatic behavior. The process was painstaking: collect tumor samples from patients whose long-term outcomes were known, measure the activity levels of thousands of genes in those samples, and use statistical methods to identify which genes best predicted whether the cancer would spread.

The result was a 31-gene expression profile test that produced a binary classification: Class 1 (low risk of metastasis) or Class 2 (high risk). Later iterations would refine this into a more granular scoring system, but the fundamental architecture was binary prediction. Would this tumor spread, or would it not?

The test used real-time PCR—polymerase chain reaction, the same basic technology that became familiar to millions during COVID testing, though applied in a vastly more sophisticated way—to measure the activity levels of those 31 genes and feed the results through a proprietary algorithm. Think of it like a credit score for a tumor: multiple data points are combined through a complex formula to produce a single, actionable number that predicts future behavior.

A crucial regulatory distinction shaped Castle's entire business model, and it is worth pausing to explain because it affects nearly every company in molecular diagnostics. In the United States, diagnostic tests can reach the market through two fundamentally different pathways.

The first is FDA approval or clearance, which requires extensive clinical trials and regulatory review—a process that can take years and cost tens of millions of dollars, similar in spirit (though not in scale) to drug approval. The second is the Laboratory Developed Test pathway, or LDT. Under this pathway, a CLIA-certified laboratory develops and validates a test internally for use in its own lab. The lab itself is regulated under CLIA, but the specific test does not need individual FDA review. LDTs operate under what has historically been a policy of enforcement discretion by the FDA—the agency has the authority to regulate them but has largely chosen not to. This regulatory gray zone has allowed hundreds of molecular diagnostics companies to bring tests to market without the time and expense of FDA review.

Castle built DecisionDx-Melanoma as an LDT, which allowed it to reach the market faster and with significantly lower capital requirements than the FDA pathway would have demanded. This was not a shortcut; it was the standard approach for molecular diagnostics at the time, and it remains the pathway used by the vast majority of similar tests today. But it came with a trade-off: without the FDA's imprimatur, Castle would need to build clinical credibility through a relentless drumbeat of peer-reviewed publications and real-world evidence studies.

And that is exactly what Castle did. The company embarked on what can only be described as an evidence generation campaign. Study after study was published in journals like JAMA Dermatology, the Journal of the American Academy of Dermatology, and JCO Precision Oncology. Each study expanded the evidence base: validation studies confirming the test's predictive accuracy, clinical utility studies showing it changed physician decisions, health economics studies demonstrating it could reduce unnecessary procedures and costs. This was not a one-year effort. It was a multi-year, multi-million-dollar investment in proving that the science worked, that physicians could trust it, and that it improved outcomes. By the time Castle had built a meaningful body of evidence, it had published more peer-reviewed studies than many of its larger competitors.

The go-to-market challenge was immense. Convincing physicians to change their practice—to order a new test they had never heard of, from a company they had never heard of, using technology they did not fully understand—required more than scientific papers. It required personal relationships.

Castle built a direct sales force that called on dermatologists and surgical oncologists, supported by medical science liaisons who could speak the language of clinical research. The company focused on key opinion leaders at academic medical centers, knowing that if the most respected dermatologists in the country adopted the test, community physicians would follow. Adoption in medicine follows a distinct pattern: academic centers and thought leaders go first, then community-based specialists follow once they see their peers using and publishing about the test. This cascade can take years, but it is durable once established. Castle's boots-on-the-ground approach was expensive and slow, but it was the only way to build the kind of trust that drives adoption in clinical medicine.

Revenue in these early years was modest. Castle billed insurance companies directly for each test, navigating a payer landscape that ranged from cooperative to hostile. Many insurers simply did not cover the test, leaving Castle to collect what it could from patients or eat the cost entirely. The company bootstrapped through this period, keeping operations lean and focused on doing one thing exceptionally well. By 2017, annual revenue had reached approximately $14 million—not a number that would impress a Silicon Valley investor, but evidence that the product worked, physicians wanted it, and the market was real.

IV. The Reimbursement Battle: Healthcare's Hidden Boss Fight (2013–2018)

If Castle's founding insight was scientific, its survival depended on mastering something far less glamorous: the American healthcare reimbursement system. In diagnostics, reimbursement is not a business detail. It is the business. A test can be scientifically brilliant, clinically transformative, and beloved by physicians, but if Medicare and private insurers refuse to pay for it, the company behind it will die. This is the fundamental difference between diagnostics and, say, software. In software, the buyer and the user are usually the same person. In diagnostics, the physician orders the test, the patient receives it, and a third party—the insurance company—decides whether to pay for it. Each of these three parties has different incentives, different information, and different timelines. Navigating this tripartite relationship is the central challenge of building a diagnostics business in the United States.

Medicare, the federal insurance program for Americans over 65, is the single most important payer in cancer diagnostics because cancer disproportionately affects older patients. Roughly 60 percent of new melanoma diagnoses occur in patients over 65. If Medicare does not cover your cancer diagnostic test, you have effectively lost the majority of your addressable market.

Medicare coverage decisions for molecular diagnostics are made through Local Coverage Determinations issued by Medicare Administrative Contractors. For molecular diagnostics, the key contractor was MolDX, a program administered by Palmetto GBA that evaluates the clinical utility of new tests. The process is bureaucratic, evidence-intensive, and slow—often taking years from initial submission to final determination. A company must submit a dossier demonstrating not just that a test is analytically valid (it measures what it claims to measure) and clinically valid (its results correlate with real outcomes), but that it has clinical utility—meaning it actually changes physician behavior in ways that improve patient outcomes or reduce costs.

This third hurdle, clinical utility, is where most diagnostic tests fail. It is the equivalent of the "so what?" question. Your test accurately predicts whether a melanoma will metastasize? So what? Does that prediction change what the physician does? Does the physician order different treatments, different surveillance, different procedures based on the result? And if so, do those changed decisions lead to better outcomes or lower costs? It is not enough to provide information. You must prove that the information changes decisions, and that the changed decisions matter.

Castle spent years building this evidence dossier. The company funded clinical utility studies showing that DecisionDx-Melanoma results changed management decisions in a significant percentage of cases—physicians who received high-risk results were more likely to order additional imaging, recommend sentinel lymph node biopsy, or consider adjuvant therapy. Conversely, physicians who received low-risk results were more likely to reduce surveillance intensity, sparing patients unnecessary procedures and the healthcare system unnecessary costs. Castle also invested in health economics studies quantifying the cost savings. This was not academic vanity. Every publication was a brick in the wall of the reimbursement dossier.

The pivotal moment came on December 3, 2018, when Palmetto GBA issued a favorable Local Coverage Determination for DecisionDx-Melanoma, granting Medicare coverage at a reimbursement rate of approximately $7,193 per test. This was the single most important event in Castle's history up to that point. Medicare coverage did three things simultaneously: it validated the test's clinical utility in the eyes of the medical establishment, it created a reliable revenue stream from the largest payer in oncology diagnostics, and it gave private insurers cover to follow suit. The reimbursement rate itself was notable—over $7,000 per test, reflecting the premium clinical value Castle had demonstrated through its evidence base.

Private payer negotiations followed, though on a slower timeline. Blue Cross Blue Shield plans, Aetna, UnitedHealthcare, and other major insurers gradually added coverage, each requiring its own set of negotiations, evidence submissions, and contract terms. The process was a grind—individual meetings with medical directors, appeals of initial denials, presentations at payer advisory boards. Castle's commercial team became expert at this particular form of bureaucratic warfare. By the time of the company's IPO in mid-2019, private payer coverage was expanding steadily, though it remained incomplete. The lesson for investors was clear: in diagnostics, reimbursement is not a one-time event but an ongoing campaign that requires permanent organizational capability.

Castle's pricing strategy deserves attention. At over $7,000 per test, DecisionDx-Melanoma was not cheap. But Castle positioned the price against the cost of the alternative: unnecessary sentinel lymph node biopsies (roughly $15,000-$25,000 each), unnecessary imaging surveillance, and unnecessary immunotherapy (which can cost $100,000 or more per year). When framed this way, a $7,000 test that prevents even a fraction of unnecessary downstream spending looks like a bargain. This value-based pricing argument was central to Castle's reimbursement success and remains a template for other diagnostic companies.

The revenue impact was immediate and dramatic. Castle's revenue roughly doubled from $23 million in 2018 to $52 million in 2019, driven largely by the Medicare coverage secured in December 2018. The coverage decision unlocked a population of Medicare-eligible melanoma patients who could now access the test with insurance coverage, and it signaled to private payers that the test had met the highest evidentiary standard in American healthcare. For investors, the lesson is stark: in diagnostics, there is a before and after, and the dividing line is reimbursement. Everything Castle had done in the prior decade—the science, the publications, the physician relationships—was necessary but not sufficient. Medicare coverage was the catalyst that converted a promising technology company into a viable business.

V. IPO & Public Market Transition (2019)

By the spring of 2019, Castle Biosciences had achieved something that most diagnostic startups never do: it had a clinically validated test with Medicare coverage, growing physician adoption, expanding private payer coverage, and a revenue run rate approaching $50 million. The question was no longer whether the business was viable. It was how fast it could grow—and how much capital it needed to do so.

The decision to go public was driven by a straightforward calculus. Castle needed capital to expand its sales force, invest in R&D for new tests, and build the commercial infrastructure required to support a multi-product platform. The IPO market in mid-2019 was receptive to healthcare companies with clear clinical differentiation and demonstrated revenue growth. On July 25, 2019, Castle Biosciences listed on the Nasdaq, selling 4 million shares at $16 per share and raising approximately $64 million after underwriting fees.

What did Castle look like at the time of its IPO? Revenue for full-year 2019 would come in at roughly $52 million, more than double the prior year's $23 million. The company had two commercial products—DecisionDx-Melanoma, its flagship, and DecisionDx-UM, its smaller uveal melanoma test. It was not yet profitable on a GAAP basis, but the path to profitability was visible: high gross margins above 80 percent, growing test volumes, and expanding reimbursement coverage. The S-1 filing told the story of a company that had spent a decade building scientific credibility and was now ready to commercialize at scale.

The public market reception was enthusiastic. Castle's stock rose from its $16 IPO price to roughly $26 by year-end 2019, a gain of more than 60 percent in five months. Institutional investors appreciated the combination of high gross margins, predictable revenue growth, and a clear competitive moat built on clinical evidence and physician relationships. The stock would prove volatile in subsequent years, but the IPO established Castle as a legitimate public company and gave it the capital to execute its expansion strategy.

The IPO capital went exactly where management said it would: sales force expansion, R&D investment, and commercial infrastructure. Castle hired medical science liaisons to support clinical education, expanded its direct sales team to cover more territories, and invested in laboratory capacity. The leadership team—Maetzold, Oelschlager, and Juvenal—had now been together for over a decade, an unusual degree of continuity for a company transitioning to the public markets. That stability mattered. Going public imposes enormous demands on management time—earnings calls, investor meetings, SEC filings, board governance—and having a seasoned team that already worked well together allowed Castle to navigate the transition without losing commercial momentum.

For investors evaluating diagnostic companies, Castle's IPO illustrated a pattern worth noting. The company went public after proving its core test worked, after securing reimbursement, and after demonstrating revenue growth—not before. Many diagnostic companies attempt to go public on the promise of future reimbursement or future clinical validation, and the results are often ugly. Castle's patience in waiting until the business fundamentals were established gave it credibility with public market investors and avoided the death spiral of a diagnostic company burning cash while waiting for Medicare coverage that might never come.

The stock's subsequent journey would be anything but boring. From its $16 IPO price, Castle shares would soar to an all-time high of nearly $108 in February 2021—a more than sixfold increase in eighteen months—before beginning a long, painful decline that would eventually bring the stock below its IPO price. But in the summer of 2019, none of that volatility was yet visible. Castle was a fresh public company with a clean balance sheet, a proven product, and a management team that had been together for a decade. The question now was what to do with the capital and the public currency. The answer would come in the form of an aggressive platform expansion that would define Castle's next chapter.

VI. Platform Expansion: Uveal Melanoma & Cutaneous SCC (2017–2021)

The question that every single-product company must eventually answer is this: are you a one-trick pony, or are you a platform? For Castle Biosciences, the question was particularly urgent. DecisionDx-Melanoma was growing impressively, but the total addressable market—roughly 100,000 invasive melanoma diagnoses per year in the United States, not all of which were candidates for gene expression profiling—imposed a ceiling on the product's revenue potential. DecisionDx-UM served a much smaller population of approximately 2,500 annual diagnoses. If Castle was going to justify a premium public market valuation, it needed to demonstrate that its gene expression profiling platform could be applied to additional cancer types.

The company's first significant expansion moved into cutaneous squamous cell carcinoma, the second most common skin cancer in the United States. SCC is far more common than melanoma—roughly 1.8 million cases are diagnosed annually—though only a subset of those cases present the kind of clinical uncertainty where a gene expression test would be useful. Castle developed DecisionDx-SCC, a 40-gene expression profile test that predicted the risk of metastasis in patients with high-risk cutaneous SCC. The test launched commercially in September 2020, and the strategic logic was compelling on multiple dimensions.

First, the technical leverage was real. Castle was not starting from scratch. The same gene expression profiling platform—CLIA lab infrastructure, PCR-based analytics, proprietary algorithmic classification—could be adapted to different gene signatures for different cancer types. The marginal cost of developing a new test was dramatically lower than the cost of building the first one.

Second, the commercial leverage was equally powerful. Castle's sales force already called on dermatologists. Adding a SCC test to the product bag required no new relationships, no new call points, no new specialty to learn. The same physician who ordered DecisionDx-Melanoma could now order DecisionDx-SCC. In sales terms, the incremental cost of selling an additional product to an existing customer is a fraction of the cost of acquiring a new customer.

Third, the clinical validation playbook was established. Castle knew how to design studies, publish results, build KOL networks, and navigate the reimbursement process. Each subsequent test could follow the same recipe faster. The institutional knowledge embedded in Castle's clinical and regulatory teams—who to talk to at MolDX, how to structure a clinical utility study, which journals carry the most weight with payers—was a repeatable asset.

Test volumes for SCC grew rapidly—from roughly 3,500 tests in 2021 to over 16,000 in 2024—and the product appeared to be on a trajectory similar to the early years of DecisionDx-Melanoma. In May 2021, Castle also acquired the myPath Melanoma test from Myriad Genetics for $32.5 million in cash, adding a complementary diagnostic that helped distinguish between benign moles and malignant melanomas. This was a different clinical question than DecisionDx-Melanoma addressed—diagnosis versus prognosis—but it served the same customer base and reinforced Castle's position as the go-to diagnostics partner for dermatologists.

The portfolio approach was working. By 2021, Castle had four commercial products serving dermatology, and revenue had reached $94 million, up from $52 million just two years earlier. The company was no longer a one-product story.

But the SCC story would take a painful turn. Despite strong volume growth and physician adoption, DecisionDx-SCC never secured Medicare coverage. MolDX evaluated the evidence and concluded that the clinical utility data was insufficient—a devastating blow that would fully materialize in early 2025 when Novitas issued a formal non-coverage determination effective April 2025. The SCC experience would become a cautionary tale within Castle's own portfolio: a product that physicians clearly wanted, that was growing rapidly, but that ultimately could not cross the reimbursement threshold. Volume had reached over 16,000 tests in 2024, but without Medicare coverage, the revenue stream was structurally impaired. The gap between physician demand and payer willingness to pay—the fundamental tension in American diagnostics—had claimed a product that many at Castle believed deserved coverage.

Still, the most transformative move was yet to come—one that would take Castle far beyond the skin.

VII. The Cernostics Acquisition & Barrett's Esophagus Play (2021)

In October 2021, Castle Biosciences announced a deal that fundamentally redefined the company's strategic identity. It would acquire Cernostics, Inc., a Pittsburgh-based diagnostics company backed by Illumina Ventures, for approximately $30 million in cash upfront with up to $50 million in additional milestone payments. The prize was TissueCypher, a test for Barrett's esophagus that most investors had never heard of—and that would become Castle's most important growth engine.

Barrett's esophagus is a condition in which the tissue lining the lower esophagus changes composition, typically as a result of chronic acid reflux. It is a pre-cancerous condition—patients with Barrett's esophagus have an elevated risk of developing esophageal adenocarcinoma, one of the deadliest cancers, with a five-year survival rate below 20 percent for advanced disease. The challenge for gastroenterologists was identifying which Barrett's patients would progress to cancer and which would not. The standard approach was periodic endoscopic surveillance with biopsies—an expensive, invasive, and imprecise process that subjected millions of patients to repeated procedures while still missing some cancers.

TissueCypher used an image analysis approach applied to tissue biopsy samples, combining immunofluorescence with a machine learning algorithm to assess the risk of progression to high-grade dysplasia or esophageal cancer. The test gave gastroenterologists something they desperately needed: a way to risk-stratify their Barrett's patients so that high-risk patients could receive more intensive surveillance or intervention while low-risk patients could safely reduce the frequency of their endoscopies.

The strategic rationale was multi-dimensional. Most obviously, it expanded Castle's total addressable market. Barrett's esophagus affects an estimated 3 to 5 million Americans, with roughly 415,000 patients annually meeting the clinical criteria for surveillance—a substantial market. The test had already received Medicare coverage through the Clinical Laboratory Fee Schedule and would subsequently receive Advanced Diagnostic Laboratory Test designation from CMS in March 2022, which set the reimbursement rate at $4,950 per test. But the deal also validated Castle's platform thesis. For the first time, the company was expanding beyond dermatology into a new medical specialty—gastroenterology—with a new type of technology (image-based analysis rather than PCR-based gene expression). If this worked, Castle was not just a dermatology diagnostics company. It was a precision diagnostics platform.

The integration challenges were real. Gastroenterology was a different world from dermatology—different physicians, different practice patterns, different payer dynamics, different KOL networks. Castle needed to build a separate sales force, establish relationships with gastroenterologists and GI academic centers, and navigate a new set of reimbursement conversations. The company invested aggressively, hiring GI-focused sales representatives and medical science liaisons, funding clinical studies in the new specialty, and building the commercial infrastructure to support a two-specialty business.

The results have been extraordinary, and the numbers tell a story of exponential adoption. TissueCypher went from 27 test reports in the partial year following the acquisition's close in December 2021 to roughly 2,100 in 2022, then 7,600 in 2023, then 21,000 in 2024, then over 39,000 in 2025—an 86 percent increase in that final year alone. To put this trajectory in context: it took DecisionDx-Melanoma over a decade to reach 39,000 annual tests. TissueCypher reached the same level in four years from acquisition.

By the fourth quarter of 2025, TissueCypher volume had essentially reached parity with DecisionDx-Melanoma, the company's flagship product. Patient penetration stood at only about 11 percent, suggesting enormous remaining growth potential in a market Castle estimates at roughly $1 billion. The Cernostics acquisition, at a total potential cost of up to $80 million, may prove to be one of the most value-creative deals in recent diagnostics history—a genuine home run that transformed Castle from a skin cancer specialist into a multi-specialty platform.

VIII. The IDgenetix & Neuropsychiatry Bet (2022–2023)

Emboldened by the early success of TissueCypher, Castle made an even bolder move in March 2022. The company announced the acquisition of AltheaDx, a San Diego-based pharmacogenomics company, for $65 million upfront—split evenly between cash and Castle stock—with up to $75 million in additional milestone payments tied to performance and expanded Medicare coverage. The total potential deal value was $140 million, nearly double the Cernostics acquisition.

The asset was IDgenetix, a pharmacogenomic test designed to help psychiatrists optimize medication selection for patients with mental health conditions. The concept was grounded in a genuine clinical problem. Psychiatric medication management is notoriously trial-and-error. A patient diagnosed with major depression might try two, three, four different antidepressants before finding one that works—a process that can take months or years, during which the patient suffers side effects, loses faith in treatment, and generates enormous healthcare costs. Pharmacogenomics offered a potential shortcut: by analyzing a patient's genetic variants that affect drug metabolism, a test could predict which medications were more likely to work and which were more likely to cause adverse reactions.

The strategic logic was defensible on paper. The mental health medication market was enormous—tens of millions of Americans take psychiatric medications—and pharmacogenomics addressed a real clinical pain point. Medicare had expanded coverage for pharmacogenomic testing for certain mental health indications, providing a reimbursement pathway.

And the acquisition would diversify Castle beyond oncology entirely, reducing its dependence on dermatology and potentially creating a third commercial vertical alongside skin and GI. If it worked, Castle would have three distinct physician customer bases ordering three different categories of tests—a level of diversification that would significantly reduce the company's risk profile.

But execution proved far more difficult than strategy. The customer base—psychiatrists—was fundamentally different from dermatologists and gastroenterologists. The call points were different, the practice patterns were different, and the evidence expectations were different. Castle's existing sales force had no relationships in psychiatry, and building those relationships from scratch was expensive and slow. The competitive landscape was also more crowded. Companies like Myriad Genetics (with its GeneSight test) and Genomind were already established in psychiatric pharmacogenomics, with larger evidence bases and deeper physician relationships.

Test volumes for IDgenetix grew—from roughly 3,200 in 2022 to over 17,000 in 2024—but the economics never worked. The cost of building a separate commercial organization for psychiatry, combined with the lower reimbursement rates typical of pharmacogenomics testing, meant that IDgenetix was consuming capital without approaching profitability. By early 2025, management made the difficult decision to discontinue the product. In May 2025, Castle announced it would wind down IDgenetix operations, taking a $20.1 million accelerated amortization charge in the first quarter. The milestone payments were never fully triggered, limiting the total financial damage, but the failure was significant—both in dollar terms and in what it revealed about the limits of Castle's platform ambitions.

The IDgenetix episode offers a sobering counterpoint to the TissueCypher success story. Both were acquisitions of early-stage diagnostic tests in new medical specialties. Both required building new commercial capabilities from scratch. But TissueCypher succeeded because it entered a market with limited competition, a clear clinical need, and strong reimbursement—and because the GI sales force could leverage some degree of overlap with Castle's existing payer relationships. IDgenetix entered a crowded market, faced entrenched competitors, and required building an entirely separate commercial infrastructure in a medical specialty where Castle had zero credibility. The lesson is not that M&A-driven diversification is inherently risky. It is that the specific characteristics of the target market matter enormously, and that managerial hubris—"we've done it before, we can do it again"—is a dangerous mental model when the underlying conditions have changed.

IX. The COVID Impact & Operational Resilience (2020–2021)

When the COVID-19 pandemic shut down elective medical procedures across the United States in March 2020, Castle Biosciences faced an existential stress test. The company's entire business model depended on physicians seeing patients, performing biopsies, and sending tissue samples to Castle's laboratory for analysis. If dermatology visits stopped, biopsies stopped, and if biopsies stopped, test orders stopped. The logic was inescapable.

The impact was immediate and sharp. Revenue in the second quarter of 2020 dropped to $12.7 million, down from $17.4 million in the first quarter—a decline of roughly 27 percent. Dermatology offices shuttered, elective procedures were postponed, and patients stayed home. For a company that had just gone public nine months earlier, the timing was brutal.

Castle's response was disciplined. Management protected the core business—maintaining laboratory operations with essential staff, preserving the commercial team, and continuing clinical studies that would be needed for future reimbursement submissions. The company had entered the pandemic with a strong balance sheet thanks to its IPO proceeds, which meant it could absorb the revenue hit without resorting to layoffs or emergency capital raises. This financial cushion proved critical.

The recovery was swift and revealing. As dermatology practices reopened through the second half of 2020 and into 2021, pent-up demand drove test volumes back to pre-pandemic levels and beyond. Revenue for full-year 2020 came in at roughly $63 million—still growing 21 percent over 2019, despite losing nearly an entire quarter to the shutdown.

By 2021, revenue reached $94 million, a 50 percent increase that more than compensated for the pandemic's disruption. The V-shaped recovery demonstrated something important about Castle's business model: demand for cancer diagnostic testing was not discretionary. It was deferrable but not eliminable. Patients who skipped their dermatology appointments during lockdowns still had their moles checked eventually. The cancer did not take a vacation, and neither did the need for accurate prognosis.

The pandemic also accelerated Castle's adoption of remote sales tools and digital engagement with physicians, capabilities that complemented the traditional in-person sales model without replacing it. These operational adaptations would prove valuable as the company scaled its commercial operations in subsequent years. Castle emerged from COVID leaner, more digitally capable, and—most importantly—with its competitive position intact while some smaller diagnostics competitors had been permanently weakened.

X. Commercial Moat Building: Sales, Marketing & Physician Networks (2015–Present)

The most underappreciated aspect of Castle Biosciences' competitive position is something that does not appear on any financial statement: the depth and density of its physician relationships. In diagnostics, the customer relationship is everything. A dermatologist does not switch from one gene expression test to another because a competitor offers a better price or a slicker sales pitch. The physician switches—or more precisely, starts ordering—because they trust the science, trust the company, and have seen enough evidence and enough peer adoption to feel comfortable changing their clinical practice. Building that trust takes years, and once established, it is remarkably sticky.

Castle's commercial model is built on a direct sales force—roughly 200 to 250 field-based personnel across its dermatology and gastroenterology teams—rather than distributors or laboratory partnerships. This is expensive. SG&A expenses reached $229 million in 2025, representing about two-thirds of revenue. But the direct model gives Castle something invaluable: control over the physician relationship. When a Castle sales representative meets with a dermatologist, they are not competing with other products from the same distributor. They represent Castle exclusively, and they can invest the time to educate the physician on the clinical evidence, walk them through how to interpret results, and address specific concerns about individual patient cases.

Supporting the sales force is a medical affairs team of medical science liaisons—PhD-level scientists who engage with key opinion leaders, present at medical conferences, and facilitate clinical education. This is not marketing disguised as science. The distinction matters enormously in healthcare. Physicians are trained to be skeptical of commercial messaging, and they can smell a sales pitch from across a conference hall. Medical science liaisons speak the language of clinical research, discuss study methodology, and address evidence questions that sales representatives are not qualified to answer. This dual-layer approach—commercial sales for relationship building and logistics, medical affairs for scientific credibility—is the gold standard in specialty diagnostics.

The data flywheel is perhaps Castle's most powerful competitive mechanism, and it deserves careful attention because it is the closest thing to a structural competitive advantage that exists in molecular diagnostics.

Every test Castle runs generates real-world data on patient outcomes. That data feeds into publications—Castle has built a library of over 100 peer-reviewed studies across its product portfolio. Those publications get cited in clinical guidelines. The National Comprehensive Cancer Network guidelines for melanoma now include Castle's DecisionDx-Melanoma test, a milestone that transforms a product from "one of several options" to "standard of care."

Guideline inclusion drives physician adoption, which drives test volume, which generates more data, which enables more publications. The flywheel accelerates with every turn. Once a test is embedded in clinical guidelines and physician workflow, displacing it requires a competitor to generate an equivalent or superior body of evidence—a process that takes years and tens of millions of dollars even if the science is excellent. This is the reason Castle can compete against companies ten times its size: the evidence moat compounds over time, and no amount of capital can shortcut the process of generating and publishing clinical evidence.

As of early 2026, DecisionDx-Melanoma had been ordered by approximately 17,000 clinicians over its lifetime, with a patient penetration rate of about 31 percent—meaning roughly one-third of eligible melanoma patients received the test. That penetration number is both an achievement and an opportunity: it means the product is well-established but has substantial room to grow. TissueCypher's penetration of approximately 11 percent in Barrett's esophagus tells an even more compelling growth story. The commercial machine that Castle built over 15 years of ground-level physician engagement is the engine that converts scientific innovation into revenue.

XI. The Technology & Lab Operations

Walk into Castle Biosciences' CLIA-certified laboratory in Pittsburgh (where TissueCypher is processed) or its primary facility, and what strikes you is the precision of the operation. Turnaround times—the interval between receiving a tissue sample and delivering results to the ordering physician—are measured in business days, not weeks. Speed matters in cancer diagnostics. A patient waiting for melanoma prognosis results is living in a state of acute anxiety. A physician waiting for results is delaying treatment decisions. Every day of delay is a day of uncertainty, and uncertainty is the enemy of both good medicine and patient experience.

The gene expression profiling technology at the heart of Castle's dermatology tests is conceptually straightforward, even if the execution is technically demanding. Here is the simplest way to understand it: DNA is the blueprint of a cell. It contains the instructions for making every protein the cell might ever need. But not all instructions are active at any given time. Gene expression is the process by which specific instructions in the DNA are "read" and converted into RNA, which then directs protein production. By measuring which genes are actively producing RNA—and at what levels—scientists can understand what a cell is actually doing, not just what it theoretically could do.

In a cancerous tumor, gene expression patterns reveal the tumor's biological behavior. Some patterns correlate with aggressive, metastasis-prone tumors. Other patterns correlate with indolent tumors that are unlikely to spread. Castle's proprietary algorithms analyze the expression levels of a specific panel of genes—31 for melanoma, 40 for SCC—and classify the tumor into risk categories. The algorithms were trained on datasets of patients with known outcomes: tumors that did metastasize and tumors that did not. The result is a predictive tool that adds a layer of biological information on top of traditional pathological staging.

TissueCypher uses a different technological approach—immunofluorescence combined with image analysis rather than PCR-based gene expression profiling. Biopsy tissue is stained with fluorescent markers that bind to specific proteins, and the resulting images are analyzed by a machine learning algorithm that identifies patterns associated with progression risk. This is closer to computational pathology than molecular biology, and it represents an interesting technological diversification for Castle. The company now operates across two distinct analytical platforms—molecular and image-based—which provides optionality for future product development.

Castle's intellectual property portfolio includes proprietary gene signatures, algorithmic classifiers, and trade secrets related to laboratory processes and computational methods. The company does not disclose the specific genes in its panels or the details of its classification algorithms, which provides an additional layer of protection beyond formal patent filings. Lab efficiency has improved with scale—the cost of running each additional test is largely marginal, given the fixed costs of maintaining the laboratory, quality systems, and regulatory infrastructure. This creates operating leverage as volumes grow: each incremental test generates high-margin revenue against a relatively stable cost base, which is why Castle's adjusted gross margins have remained consistently around 80 percent even as the product mix has shifted.

XII. Competitive Landscape & Market Dynamics

Castle Biosciences operates in a competitive landscape that is simultaneously fragmented and dominated by a handful of large players. Understanding who competes with Castle—and who does not—is essential for evaluating the company's strategic position.

The diagnostic giants—Exact Sciences (roughly $3.25 billion in 2025 revenue), Myriad Genetics ($825 million), Guardant Health ($982 million), and Roche's Foundation Medicine—operate at a scale that dwarfs Castle's $344 million. Each of these companies has platform-level capabilities in oncology diagnostics, with multiple products, broad payer relationships, and substantial R&D budgets. In theory, any of them could develop a competing melanoma gene expression test. In practice, none has done so successfully, and the reasons illuminate Castle's competitive moat.

The first reason is the evidence barrier. Castle has spent over 15 years and tens of millions of dollars building a clinical evidence base for DecisionDx-Melanoma that now includes over 100 peer-reviewed publications. A competitor entering the market today would need to spend years and comparable sums generating an equivalent evidence base before physicians would consider adopting the new test—and before payers would consider covering it. This is not an insurmountable barrier, but it is a daunting one, particularly for larger companies with many competing investment priorities. Why would Exact Sciences invest $50 million and five years to develop a melanoma prognosis test that might capture a fraction of a $300 million market when it could invest the same resources in expanding its Cologuard franchise, which addresses a multi-billion-dollar market?

The second reason is physician trust. Once a physician is comfortable with a diagnostic test—once they have ordered it dozens or hundreds of times, understand how to interpret the results, and have seen those results validated in their own patients' outcomes—switching to an alternative test requires a compelling reason. The switching costs are not contractual; they are behavioral. Physicians are conservative by training and temperament. They change practice slowly, and they rarely abandon a test that is working for them in favor of an unproven alternative.

The third reason is guideline inclusion. DecisionDx-Melanoma's inclusion in NCCN guidelines creates a self-reinforcing advantage. Physicians follow guidelines. Insurance companies reference guidelines when making coverage decisions. Once a test is in the guidelines, competitors must generate sufficient evidence to earn their own guideline inclusion or argue for the existing test's removal—a process that is political as well as scientific.

The emerging competitive threats are real but not imminent. Liquid biopsy—testing blood rather than tumor tissue for circulating tumor DNA—is advancing rapidly, led by companies like Guardant Health. If liquid biopsy technology achieves sufficient sensitivity and specificity for melanoma prognosis, it could eventually compete with tissue-based gene expression profiling. AI-powered computational pathology—using deep learning to extract prognostic information from standard pathology slides—is another potential disruptor. Companies like PathAI and Paige are developing AI systems that could, in theory, predict tumor behavior from images that are already being collected, eliminating the need for a separate molecular test. These technologies are five to ten years away from broad clinical adoption for melanoma prognosis, but they represent the long-term technological risk to Castle's business model.

The diagnostics industry is also experiencing a wave of private equity-driven consolidation. Large PE-backed platforms are acquiring specialty laboratories and diagnostics companies to build scale, negotiate better payer contracts, and reduce overhead through shared infrastructure. This trend could affect Castle in two ways: it could create new competitors with more resources, or it could create potential acquirers interested in Castle's differentiated products and physician relationships.

In gastroenterology, Castle faces less direct competition for TissueCypher. There is no equivalent commercial test for Barrett's esophagus risk stratification with comparable evidence and reimbursement. Castle's acquisition of Previse in May 2025—which brought an epigenetic test for Barrett's progression risk based on methylation technology from Johns Hopkins—suggests the company intends to build a portfolio approach in GI, owning multiple testing modalities for the same clinical question. This "own the category" strategy—rather than competing for market share within a category—is a distinctly different approach from the one taken by most diagnostics companies, and it could prove to be a significant competitive advantage if Castle can execute across multiple testing platforms.

XIII. Business Model Deep Dive

Castle's revenue model is elegantly simple: test volume multiplied by reimbursement rate. The company receives a tissue sample, runs the test, delivers results, and bills the payer. There are no recurring subscription fees, no platform licensing arrangements, no hardware sales. Each test is a discrete transaction, and revenue growth comes from two levers: increasing the number of tests performed and increasing the average revenue per test.

This simplicity masks considerable operational complexity. The reimbursement rate is not fixed across all payers—Medicare pays approximately $7,193 for DecisionDx-Melanoma and $4,950 for TissueCypher, but private payer rates vary by contract and can be significantly different. Collection rates—the percentage of billed charges actually collected—fluctuate based on payer mix, coverage policies, and the efficiency of Castle's revenue cycle management. Castle has historically been conservative in revenue recognition, recognizing revenue only when collection is reasonably assured, which means that actual cash receipts sometimes lag reported revenue.

The unit economics are attractive. Adjusted gross margins have been consistently around 80 percent, meaning that for every dollar of revenue, roughly 80 cents is gross profit. This is among the highest in the diagnostics industry—comparable to software margins, and significantly higher than traditional clinical laboratories that operate at 40 to 50 percent gross margins.

The margin profile reflects the inherent leverage of molecular testing: the incremental cost of running one additional test is modest (reagents, labor, consumables—roughly $500 to $600 per test based on publicly available data), while the reimbursement per test is substantial (over $7,000 for Melanoma, nearly $5,000 for TissueCypher). As volumes scale, fixed costs—lab infrastructure, quality systems, regulatory compliance—are spread over a larger base, driving further margin expansion. This is the economic engine that makes specialty diagnostics such an attractive business model when a company can achieve reimbursement and physician adoption.

The P&L story is more nuanced and requires careful reading. Castle achieved its first full year of GAAP profitability in 2024, reporting net income of $18.2 million on revenue of $332 million. This was a genuine milestone—the first year in the company's seventeen-year history where reported earnings were positive.

That milestone was quickly followed by a return to GAAP losses in 2025—a net loss of $24.2 million—driven by the DecisionDx-SCC Medicare coverage loss, the IDgenetix discontinuation charges (including $20 million in accelerated amortization), and continued investment in commercial expansion for TissueCypher and AdvanceAD-Tx.

However, operating cash flow remained strongly positive at $64 million in both 2024 and 2025, indicating that the underlying cash economics of the business are healthy despite GAAP accounting noise from amortization and stock-based compensation. This divergence between GAAP losses and positive cash flow is a critical distinction for investors: Castle's business generates more cash than it consumes, even as the income statement shows red ink. The non-cash charges that create this divergence—stock-based compensation of $46 million and intangible asset amortization of $35 million—are real economic costs in different ways, but they do not consume cash.

Capital allocation has been a mixed story. On the positive side, Castle has maintained a fortress balance sheet—nearly $300 million in cash and marketable securities with minimal debt—that provides ample runway for investment and protection against downside scenarios. R&D spending has stabilized at roughly $52 million per year, about 15 percent of revenue, reflecting a disciplined approach to product development. On the negative side, stock-based compensation of $46 million in 2025—representing 13 percent of revenue—is a meaningful ongoing dilution cost that GAAP earnings understate. And the IDgenetix acquisition represented a significant misallocation of capital, with $65 million in upfront consideration yielding no lasting value.

For investors trying to value Castle, the diagnostics business model occupies an unusual position in the investment taxonomy. It is not a biotech with binary clinical trial outcomes. It is not SaaS with recurring subscription revenue. It is something in between: a high-margin, growing business with significant operating leverage, but one whose revenue is episodic (each test is a one-time transaction) and dependent on external factors (reimbursement policies, clinical guidelines) that management can influence but not control. The two KPIs that matter most for tracking Castle's ongoing performance are core test report volume growth (Melanoma plus TissueCypher) and adjusted gross margin per test. These two numbers, together, capture both the demand trajectory and the economic health of the business.

XIV. Porter's Five Forces Analysis

Understanding Castle's strategic position requires examining the industry structure through a systematic lens. Porter's Five Forces framework reveals why certain diagnostics companies thrive while others fade despite having sound science.

The threat of new entrants is paradoxical. On one hand, the capital requirements for launching a CLIA-certified laboratory and developing a gene expression test are modest by healthcare standards—a few million dollars can get a laboratory operational. This is nothing compared to the billions required to develop a new drug. On the other hand, the barriers to commercial success are enormous. Clinical validation studies cost tens of millions and take years. Medicare reimbursement requires an extensive evidence dossier and bureaucratic navigation. Physician adoption requires a direct sales force and years of relationship building. And guideline inclusion—the ultimate competitive moat—requires a body of evidence that takes a decade or more to assemble. The result is a curious dynamic: it is easy to enter the market but extraordinarily difficult to succeed in it. Many diagnostic companies launch with promising science and adequate capital only to perish in the reimbursement desert, never achieving the coverage required to sustain a viable business.

The bargaining power of buyers—in this case, primarily insurance companies—is the single most important force shaping Castle's economics. Payers have enormous leverage. They decide whether a test is covered, how much they will pay for it, and under what clinical circumstances they will authorize it. A single Medicare coverage decision can make or break a product, as Castle learned painfully with DecisionDx-SCC. The loss of Medicare coverage for SCC in early 2025 effectively destroyed a product that had been generating meaningful revenue and growing rapidly. Physicians choose which tests to order, but they do so within the constraints set by payer policies. This three-party dynamic—physician orders, patient receives, payer pays—creates inherent instability because the decision-maker (physician) and the payor (insurance company) have different incentive structures.

Supplier power is low. Laboratory supplies, reagents, and equipment are largely commoditized, with multiple vendors available for most inputs. Castle has no meaningful single-supplier dependencies that could create bottlenecks. The threat of substitutes is moderate and evolving. Traditional staging methods—imaging, pathological examination, clinical assessment—remain the baseline against which Castle's tests are measured. Competing gene expression tests exist in some categories. And longer-term, liquid biopsy and AI pathology represent potential substitutes that could reshape the competitive landscape. Industry rivalry is moderate, fragmented across niche players serving different cancer types and clinical indications. Because each test addresses a specific clinical question for a specific cancer type, direct head-to-head competition is less intense than in broader diagnostics markets like general oncology panels or non-invasive prenatal testing.

XV. Hamilton's 7 Powers Framework Analysis

Hamilton Helmer's 7 Powers framework offers a complementary lens for understanding Castle's competitive moat, one focused specifically on the sources of durable strategic advantage.

Castle's strongest power is counter-positioning. Traditional pathological staging—the incumbent approach to melanoma prognosis—cannot easily adopt gene expression profiling without fundamentally changing its infrastructure, expertise, and business model. Pathology laboratories are built around tissue processing and microscopic examination. Adding molecular testing requires different equipment, different expertise, and different regulatory compliance. Academic medical centers could theoretically develop competing tests, but they lack the commercial infrastructure—sales forces, payer contracting, revenue cycle management—required to scale a diagnostic product nationally. This asymmetry between Castle and the incumbents is a classic counter-positioning advantage: Castle can do what the incumbents do plus more, while the incumbents cannot easily replicate Castle's capabilities without cannibalizing their existing operations.

Process power is Castle's second major strength. The company has built an organizational capability in clinical evidence generation and reimbursement navigation that is genuinely difficult to replicate. Managing the evidence generation pipeline—designing studies, securing IRB approvals, enrolling patients, analyzing data, writing manuscripts, shepherding papers through peer review—is a complex, multi-year process that requires specialized expertise and institutional knowledge. Similarly, the reimbursement process—preparing LCD submissions, negotiating with MAC medical directors, managing private payer contracts—is a bureaucratic art form that Castle has practiced for nearly two decades. These are not capabilities that a well-funded competitor can simply hire into existence. They are built over time through repetition, failure, and organizational learning.

Branding power in diagnostics is unusual but real. The "DecisionDx" brand carries scientific credibility among the dermatology community that has been built through years of publications, conference presentations, and clinical adoption. Trust matters enormously when a physician is making treatment decisions that affect a patient's life. A test from a company with a long track record of validated results will always be preferred over a test from an unknown newcomer, all else being equal.

Scale economies are moderate. Castle's lab has fixed costs that create operating leverage as volumes grow, and the sales force becomes more efficient as physician density within territories increases. But diagnostics is not a winner-take-all market like software. Multiple tests can coexist, and the advantages of scale plateau at relatively modest levels. Network effects are weak to moderate—the data flywheel creates a mild network effect where more tests generate more evidence, which drives more adoption, but this is a slow-moving loop rather than the explosive network effects seen in social platforms. Switching costs are moderate: once a test is embedded in clinical guidelines and physician workflow, it is sticky, but each test is a discrete episode rather than an ongoing subscription, so there is no contractual lock-in. Cornered resources include Castle's longitudinal outcomes database, its proprietary gene signatures, and its relationships with key opinion leaders—assets that competitors cannot easily acquire or replicate.

The overall assessment is that Castle's moat is built primarily on counter-positioning, process power, and branding, with emerging cornered resource advantages in clinical data. This is not the deepest moat in business—it can be eroded by technological disruption or regulatory changes—but it is meaningful and durable in the near to medium term.

XVI. Bear Case vs. Bull Case

Every investment thesis has two sides, and Castle's story is no exception. The bear case and bull case are both credible, and the tension between them drives the stock's volatility.

The bear case starts with reimbursement risk, which is not theoretical but proven. The loss of Medicare coverage for DecisionDx-SCC in early 2025 was a watershed moment that demonstrated how quickly a product's economics can be destroyed by a payer decision. The SCC test had been growing rapidly, with volumes exceeding 16,000 in 2024, and appeared to be on a trajectory toward becoming a meaningful revenue contributor. Then MolDX denied coverage, Novitas followed in February 2025 with an effective date of April 2025, and the revenue stream effectively evaporated. If this can happen to SCC, bears argue, it can happen to Melanoma or TissueCypher. The regulatory and payer environment is inherently unpredictable, and Castle's revenue is concentrated in a small number of products whose economics depend entirely on continued reimbursement.

The IDgenetix failure adds to the bear case. Castle spent at least $65 million acquiring AltheaDx and invested additional capital in commercial buildout, only to discontinue the product less than three years later. This raises legitimate questions about management's capital allocation discipline and about the limits of Castle's platform strategy. Can management reliably evaluate acquisition targets outside its core competency areas? The M&A track record is now one-for-two on major deals—excellent on TissueCypher, poor on IDgenetix. Bears will argue that one success and one failure is not a track record; it is a coin flip.

Technology disruption is the longer-term bear case. If liquid biopsy or AI pathology achieves sufficient accuracy for melanoma and Barrett's esophagus prognosis, Castle's tissue-based tests could become obsolete. The company has limited ability to pivot to these technologies because its entire infrastructure—lab operations, intellectual property, regulatory approvals—is built around tissue analysis. A blood-based or image-based alternative would not just compete with Castle; it would render Castle's core capabilities irrelevant.

The bull case centers on TissueCypher's extraordinary growth trajectory. With only 11 percent patient penetration in a market Castle estimates at $1 billion, TissueCypher is a product in the early innings of its commercial life. If penetration reaches 30 to 40 percent—comparable to where DecisionDx-Melanoma is today—TissueCypher alone could be generating several hundred million dollars in annual revenue. The 86 percent year-over-year volume growth in 2025 suggests the adoption curve is accelerating, not decelerating.

DecisionDx-Melanoma, despite being Castle's oldest product, continues to grow at a healthy 9 percent clip with penetration at only 31 percent. This is a product that still has meaningful runway in its core market, supplemented by potential international expansion and new clinical applications. The November 2025 limited launch of AdvanceAD-Tx—a gene expression test to guide systemic treatment selection for moderate-to-severe atopic dermatitis, targeting a $33 billion total addressable market—represents an entirely new growth vector, though one with no reimbursement yet and immaterial near-term revenue expectations.

The valuation argument is perhaps the most compelling element of the bull case. Castle trades at roughly 1.9 times enterprise value to revenue, a significant discount to diagnostics peers: Exact Sciences at 4.3 times, Guardant at 8.2 times, NeoGenomics at 4.2 times, and Myriad at 3.6 times. On a core growth basis—34 percent in 2025, excluding discontinued products—Castle is growing faster than most of its peers while trading at a lower multiple. The discount reflects the SCC and IDgenetix setbacks, but bulls argue the market has overreacted and that the core business is healthier than the headline numbers suggest.

Castle's balance sheet provides a margin of safety that few specialty diagnostics companies can match. With nearly $300 million in cash and marketable securities and a debt-to-equity ratio of just 0.08, the company can fund its commercial expansion, pursue opportunistic acquisitions, and weather reimbursement setbacks without risking financial distress. The company generated $64 million in operating cash flow in both 2024 and 2025 despite GAAP losses—a testament to the underlying cash economics of the business. This cash generation is particularly impressive because it means Castle is self-funding its growth investments without burning through its cash reserves. Few companies at Castle's stage of development can say the same.

In July 2025, Castle received FDA Breakthrough Device Designation for DecisionDx-Melanoma, opening a potential pathway to FDA authorization that could provide additional regulatory credibility and potentially expand reimbursement. Whether to pursue full FDA authorization is a strategic decision with trade-offs—it would require significant investment but could provide a durable competitive advantage. This decision will be an important signal of management's long-term strategic thinking.

XVII. Leadership & Culture

Derek Maetzold has led Castle Biosciences since its founding in 2007, a tenure of nearly two decades that is exceptional by any standard and virtually unprecedented in the molecular diagnostics industry. Maetzold is not the stereotypical charismatic founder-CEO who lights up conference stages. He is methodical, evidence-oriented, and deeply focused on clinical validation—qualities that mirror the company's culture and strategic approach. In earnings calls, he speaks in the measured, data-heavy language of a scientist, not the visionary hyperbole of a tech entrepreneur. This personality is both an asset and a potential liability: it builds credibility with physicians and scientists who value rigor over showmanship, but it can make Castle's story less compelling to generalist investors accustomed to more promotional management teams.

The broader leadership team reflects Castle's dual identity as both a science company and a commercial enterprise. The presence of Kristen Oelschlager as COO since the company's earliest days provides operational continuity that is rare in high-growth companies. The commercial organization, led through its growth phase by executives with deep specialty diagnostics experience, has been Castle's most important asset. Building a sales force that can credibly discuss gene expression biology with surgical oncologists while simultaneously managing insurance pre-authorization paperwork requires a particular kind of talent—part scientist, part salesperson, part bureaucratic navigator.

Castle's cultural emphasis on evidence and scientific rigor permeates the organization. In an industry where many companies launch tests with minimal evidence and rely on marketing to drive adoption, Castle's approach of leading with publications and clinical validation is distinctive. This culture has costs—it is slower and more capital-intensive than a marketing-led approach—but it creates more durable competitive advantages. Physicians who adopt Castle's tests do so because the evidence convinced them, not because a sales pitch excited them. That kind of adoption is far stickier.

Talent attraction is worth noting. Castle is headquartered in Friendswood, Texas, a suburb of Houston, with laboratory operations in Phoenix and Pittsburgh. These are not traditional biotech hubs like Boston or San Francisco, which means Castle competes for talent on different terms—lower cost of living, but also a smaller pool of experienced diagnostics professionals. The company has approximately 823 employees, a lean headcount relative to its revenue base, suggesting operational discipline. Revenue per employee of roughly $418,000 is a solid number for a diagnostics company, reflecting a workforce that is productive but not yet at the efficiency levels that further scale could enable.

The board of directors includes a mix of healthcare industry veterans, financial professionals, and scientific experts—the kind of governance composition appropriate for a company navigating the intersection of clinical science and public markets. The challenge of managing a public company in a long-cycle business deserves emphasis: Wall Street's quarterly earnings rhythm sits in tension with the multi-year timelines required to validate a new diagnostic test, secure reimbursement, and build physician adoption. Maetzold has navigated this tension by consistently communicating in terms of long-term strategy while delivering short-term results sufficient to maintain investor patience—a balancing act that the IDgenetix failure and SCC coverage loss have made more difficult.

XVIII. Future Outlook & Strategic Options (2024–2030)

Castle enters 2026 at an inflection point. The company's 2026 revenue guidance of $340 to $350 million implies headline growth of roughly flat to slightly positive, reflecting the full-year impact of the SCC and IDgenetix losses. But this headline number obscures what management describes as mid-to-high-teens growth in the core business—DecisionDx-Melanoma and TissueCypher—which together represent Castle's strategic future.

The near-term growth story is anchored by TissueCypher's continued penetration of the Barrett's esophagus market. At 11 percent patient penetration, the test has enormous room to grow, and the 86 percent volume increase in 2025 suggests adoption is accelerating. Expanding private payer coverage remains a key catalyst—while Medicare coverage is established, broader private payer adoption would significantly increase the accessible patient population. Castle's GI franchise received a further boost with the Previse acquisition in May 2025, which brought an epigenetic test for Barrett's progression risk. The first patient enrollment for the development study is expected in the second quarter of 2026, with preliminary data before year-end.

AdvanceAD-Tx represents Castle's most ambitious new product since TissueCypher. Launched in November 2025 in limited access, the 487-gene expression test guides systemic treatment selection for patients with moderate-to-severe atopic dermatitis—a condition that affects millions of Americans and is treated with increasingly expensive biologic and small-molecule therapies. The total addressable market for moderate-to-severe atopic dermatitis treatment is estimated at $33 billion, though the addressable market for the diagnostic test itself is a fraction of that. Early commercial signals are positive—roughly 500 orders by mid-February 2026—but the product has no reimbursement yet, and revenue is expected to be immaterial in 2026. The critical near-term milestone is securing Medicare and private payer coverage, which will require the same multi-year evidence generation campaign that Castle has executed for its other products.

The FDA Breakthrough Device Designation for DecisionDx-Melanoma, received in July 2025, opens an intriguing strategic option. FDA authorization would provide a level of regulatory validation that LDTs do not carry, potentially strengthening Castle's competitive position and providing a more durable moat against regulatory changes that could affect the LDT pathway. However, pursuing FDA authorization is expensive and time-consuming, and Castle has not yet committed to doing so.

Looking further out, Castle's strategic options include geographic expansion into international markets, pharmaceutical partnerships for companion diagnostic development, and additional acquisitions to expand the product portfolio. The company's strong balance sheet provides the financial flexibility to pursue these options selectively. International expansion, while frequently mentioned in investor discussions, would require navigating entirely different regulatory and reimbursement frameworks—each country has its own version of Medicare's coverage process, and the clinical evidence requirements vary. This is not a short-term opportunity, but it represents a meaningful long-term option for a company whose domestic penetration rates still have substantial room to grow.

Pharmaceutical partnerships represent another underdeveloped opportunity. As immunotherapy and targeted therapy drugs proliferate in oncology, pharmaceutical companies increasingly need companion diagnostics to identify which patients are most likely to benefit from their treatments. Castle's gene expression profiling platform, combined with its existing physician relationships and laboratory infrastructure, could make it a valuable partner for pharma companies seeking to develop companion diagnostics for melanoma or other skin cancers. This would create a new revenue stream—one potentially funded by pharma partners rather than Castle's own balance sheet.

The strategic wildcard is whether Castle remains independent or becomes an acquisition target for a larger diagnostics or pharmaceutical company. At a market capitalization below $1 billion and with proven products, growing revenue, and valuable physician relationships, Castle would be an attractive acquisition for a company like Exact Sciences, Roche, or a large private equity-backed diagnostics platform seeking to consolidate the specialty diagnostics market. The question for Castle's board is whether the company is worth more as an independent entity with its own growth trajectory or as part of a larger platform that could accelerate commercialization and provide economies of scale. For now, the company appears committed to independence, but the conversation is inevitable as the diagnostics industry continues to consolidate.

XIX. Lessons for Founders & Investors