CoStar Group: From Dorm Room to Data Empire

I. Cold Open & The Big Question

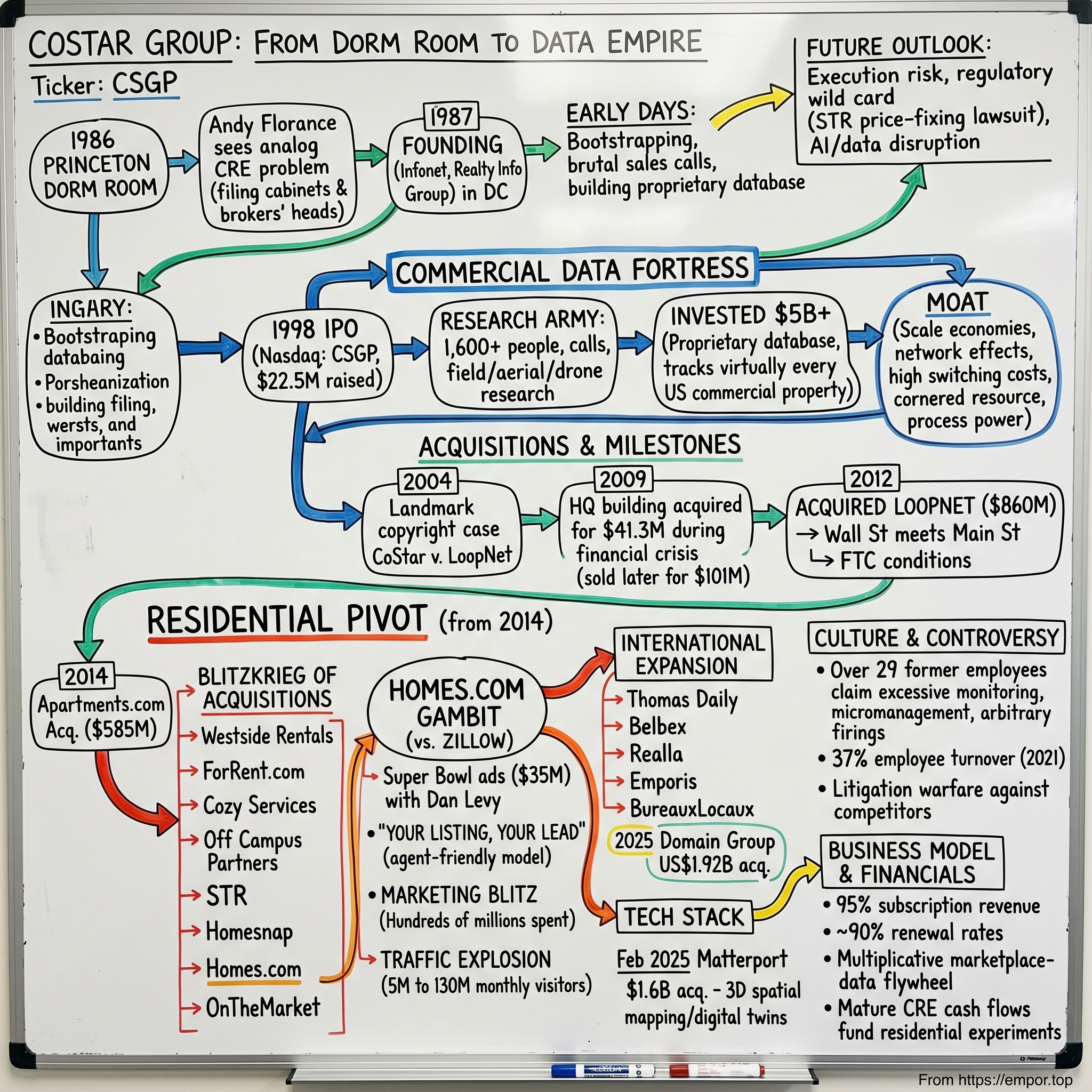

Picture this: It's February 2024, and a relatively unknown real estate website drops $35 million on a Super Bowl commercial featuring Dan Levy. The ad's message is simple yet audacious—"Your listing, your lead." In those four words, CoStar Group fired a shot directly at Zillow's $8 billion empire. But here's what most viewers didn't know: The company behind this David-versus-Goliath moment wasn't some venture-backed startup burning through capital. It was a 38-year-old data fortress with a $33 billion market cap, sitting comfortably in both the S&P 500 and NASDAQ 100.

The story of CoStar Group is the story of Andy Florance, a Princeton undergrad who saw something nobody else did in 1986—that commercial real estate, an industry built on relationships and filing cabinets, was actually a data problem waiting to be solved. While his classmates were heading to Wall Street, Florance was in his dorm room, sketching out plans to digitize an entire industry that didn't even know it needed digitizing.

Today, CoStar commands over $100 billion in addressable market opportunity across commercial and residential real estate. They've invested over $5 billion building a proprietary database that tracks virtually every commercial property in America—every lease signed, every building sold, every square foot measured. Their 1,500-person research army makes millions of calls annually, photographing properties, verifying data, creating what amounts to the Bloomberg terminal for real estate.

But here's the fascinating part: After spending three decades building an unassailable monopoly in commercial real estate data, Florance decided to pick a fight with consumer real estate giants. The same methodical, data-obsessed approach that conquered commercial real estate is now being deployed against Zillow, Realtor.com, and the entire residential portal industry.

The question isn't whether CoStar can compete—they've already proven they can build dominant platforms. The question is whether a company that succeeded by digitizing analog workflows can now disrupt digital natives at their own game. How did a Princeton undergrad build the Bloomberg of real estate, achieve near-monopoly status in commercial property data, and then decide that wasn't enough?

II. The Origin Story: Andy Florance's Princeton Epiphany (1986-1998)

The autumn of 1986 at Princeton University was an unlikely birthplace for a real estate revolution. While his classmates were recruiting for investment banking jobs at Goldman Sachs and Morgan Stanley, Andy Florance was in his dorm room, sketching out plans for what would become CoStar Group. The son of Coke Florance, one of Washington's best-known architects whose projects included DC's Verizon Center and the Torpedo Factory in Alexandria, Andy had grown up immersed in real estate conversations at the dinner table. But it wasn't until Princeton that he saw the industry's fundamental flaw. The problem Florance identified was staggering in its simplicity: commercial real estate data lived in filing cabinets and brokers' heads. While Wall Street had Bloomberg terminals and the financial markets were rapidly digitizing, commercial real estate remained stubbornly analog. Real-estate brokers compiled their own information, an expensive and time-consuming process, and many employed research staff. Each brokerage maintained its own fragmented database, jealously guarded and rarely updated.

"I loved real estate and architecture," Florance would later recall, but what he saw in the industry was chaos masquerading as tradition. While in college, Florance started writing software for developers. In 1986, he launched Infonet, his first company, and ran it from his parents' basement in DC's Cleveland Park. The name itself—CoStar—was deliberately chosen to suggest collaboration rather than replacement. He wasn't trying to eliminate brokers; he wanted to "co-star" alongside them in transactions. The early days were brutal. With Infonet, Florance set out to create a database brokers could subscribe to—it would allow them to pare down their researchers and get more up-to-date, comprehensive data for less money. His first step was to get all the tax records for commercial buildings from the District government, which he then had to feed into a computer program he designed. "I worked like a freak to get this massive amount of data down to a PC," he says. When he finally got the data into a program that brokers could use, he started making sales calls.

The industry's resistance was fierce. Commercial real estate brokers had built their careers on proprietary knowledge and personal relationships. Why would they share data? Why would they trust a college kid with their business intelligence? Florance's solution was elegant: he wouldn't ask them to share—he would build the database himself, property by property, lease by lease.

By the early 1990s, Florance had pivoted from his initial venture to launch Realty Information Group, which would become CoStar. Florance's earliest investor was local attorney Michael Klein. As a lawyer at WilmerHale, Klein specialized in public securities during the savings-and-loan crisis. Like Florance, he was shocked to see how little data there was on commercial real estate, a situation that led banks to make very risky commercial loans. "I came away from that experience with the conviction that if there was more information available on commercial real estate, the problem could be resolved," Klein says. So when he saw the software Florance was peddling, Klein grasped the potential. Even though Florance was only 23, the lawyer was impressed by his talent and creativity.

The company's growth through the 1990s was methodical rather than meteoric. While dot-coms were burning through venture capital, CoStar was building a sustainable business model based on subscription revenue and painstaking data collection. CoStar Group was founded in 1987 by Andrew C. Florance in Washington, D.C., as one of the first companies that digitized and aggregated property data before the Internet became widely available. In 1998, the company went public via an initial public offering on Nasdaq, raising $22.5 million.

The IPO wasn't just a financial milestone—it was validation that commercial real estate was ready for digital transformation. The $22.5 million raised was modest by tech standards, but for a company that had bootstrapped its way to profitability, it represented rocket fuel for expansion. The vision was clear: not to replace brokers, but to empower them. The name itself embodied this philosophy—CoStar would "co-star" alongside brokers in transactions, not compete with them.

III. Building the Data Fortress (1998-2010)

The post-IPO years marked CoStar's transformation from scrappy startup to data juggernaut. What emerged was perhaps the most ambitious data collection operation in commercial real estate history. With 1,600+ dedicated market researchers, field, aerial and drone research, data feeds and public record, CoStar created what they claimed was the most comprehensive research effort in commercial real estate.

The methodology was breathtakingly thorough and expensive. CoStar's researchers didn't just gather publicly available data—they called every building owner, tracked every lease, photographed every property. Picture an army of researchers fanning out across America's cities, clipboards in hand, cameras around their necks, documenting the minutiae of commercial real estate. Was the lobby recently renovated? Did the anchor tenant just renew their lease? What's the actual—not advertised—vacancy rate?

This wasn't Silicon Valley-style disruption through elegant algorithms. This was brute force data collection at industrial scale. While Google was organizing the world's information through web crawlers, CoStar was organizing commercial real estate through human intelligence. The company claims to have invested over $5 billion in building this proprietary database—a staggering sum that created an almost insurmountable barrier to entry for competitors. The 2004 landmark copyright case—CoStar Group, Inc. v. LoopNet, Inc.—was more than just a legal battle. It was a preview of the competitive dynamics that would define CoStar's next two decades. In June 2004, the lawsuit became a landmark case in copyright law about the role of an Internet service provider in monitoring copyrighted content posted on its servers. The irony wasn't lost on industry observers: CoStar was battling the very company it would acquire eight years later for $860 million. But the most audacious move came during the depths of the 2008 financial crisis. In October 2009, the company acquired a building from the Mortgage Bankers Association for $41.3 million, which served as the company's headquarters. The building had sold for $97 million two years earlier. This wasn't just a real estate transaction—it was performance art. The Mortgage Bankers Association, which had loudly criticized homeowners for strategic defaults, was essentially walking away from its own underwater property. Meanwhile, CoStar, using its own data to time the market perfectly, swooped in at the bottom.

"I think that having 1,000 researchers and technicians probably helped a little bit in timing the market," Florance said with characteristic understatement. A year later, CoStar sold and leased back the building to a German real-estate holding company for $101 million, turning a $60 million profit. The message was clear: CoStar's data wasn't just academic—it was actionable intelligence that could generate massive returns.

This transaction became legend in commercial real estate circles. Here was a company that had spent years telling clients their data could help them make better investment decisions, and then proved it with their own capital. The 2008 crisis, which destroyed so many real estate companies, became CoStar's coming-out party as more than just a data provider—they were now players in the game they were scoring.

By 2010, CoStar had established itself as the undisputed leader in commercial real estate information. Their database covered virtually every commercial property in America. Their research methodology had become the gold standard. But most importantly, they had created what Warren Buffett would call a "moat"—a competitive advantage so wide that crossing it seemed impossible. The $5 billion invested in proprietary data collection wasn't just a barrier to entry; it was a fortress wall.

IV. The LoopNet Acquisition: Marketplace Meets Data (2011-2012)

The irony was delicious. Eight years after suing LoopNet for copyright infringement, CoStar announced in April 2011 that it would acquire its former courtroom adversary for $860 million. The company that had once been the enemy was now the crown jewel in CoStar's expansion strategy. But this wasn't just about burying the hatchet—it was about combining the Bloomberg terminal with the New York Stock Exchange of commercial real estate.

LoopNet was everything CoStar wasn't. Where CoStar charged premium subscriptions for deep analytical data, LoopNet operated an open marketplace where brokers could list properties for free. Where CoStar served institutional investors and large brokerages, LoopNet was the platform of choice for small brokers and individual property owners. As of 2025, LoopNet is considered the leading commercial real estate digital marketplace, with more than 12 million unique monthly visitors.

"CoStar and LoopNet truly bring together Wall Street and Main Street," Florance declared when announcing the deal. The strategic rationale was compelling: combine CoStar's comprehensive data and analytics with LoopNet's massive audience and marketplace liquidity. Together, they would control both the information layer and the transaction layer of commercial real estate.

But the Federal Trade Commission wasn't buying the synergy story without conditions. The Federal Trade Commission required CoStar Group, the largest provider of commercial real estate information services in the United States, to sell LoopNet's ownership interest in Xceligent, under a proposed order settling charges that CoStar's $860 million acquisition of LoopNet would be anticompetitive. The FTC's concern was legitimate—the two companies were essentially the only providers of commercial real estate listings databases with nationwide coverage.

The regulatory dance was intricate. In order to allow for others, including Xceligent, to expand or enter into the space, CoStar would lift non-compete provisions and allow customers in longer-term contracts to terminate them early. The FTC also required something unusual: CoStar had to continue offering certain core products on a standalone basis for three years after the acquisition. They couldn't simply force bundle their products and squeeze out competition.

Through the acquisition, CoStar also gained BizBuySell and LandsofAmerica—extending their reach into business sales and rural property markets. The deal closed in April 2012, creating what industry observers called a monopolistic force in commercial real estate information.

The integration was masterful in its simplicity. Rather than forcing LoopNet users to migrate to CoStar's premium platform, Florance kept the brands separate. "The LoopNet brand is important," he stated. "Our strategy is to invest in strengthening LoopNet's products and services." This wasn't corporate speak—it was strategic genius. LoopNet would remain the wide funnel capturing millions of users, while CoStar would monetize the high-value segment willing to pay for deeper analytics.

The marketplace-data flywheel was now complete. Every listing on LoopNet generated data for CoStar. Every CoStar subscriber who listed properties drove traffic to LoopNet. The network effects were multiplicative rather than additive. Competitors could try to replicate either the data or the marketplace, but replicating both simultaneously while CoStar controlled the incumbent platforms seemed impossible.

V. The Residential Pivot: From Commercial to Consumer (2014-2021)

The year 2014 marked a seismic shift in CoStar's strategic trajectory. For 27 years, the company had focused exclusively on commercial real estate. But with the $585 million acquisition of Apartments.com, Florance signaled that CoStar's ambitions extended far beyond office buildings and shopping centers. The move into residential wasn't just an expansion—it was a declaration of war on an entirely new set of competitors.

The logic was compelling. In the $2-trillion multifamily sector—described by Florance as "bigger than the office vertical, which is where we started many years ago"—CoStar already had a foothold through its commercial database. They tracked apartment buildings as commercial assets, but they'd never competed for the consumer eyeballs that Zillow and Realtor.com dominated.

Apartments.com wasn't just any acquisition target. Prominent newspaper companies were among the owners of Apartments.com. Graham Holdings, the former parent of The Washington Post, owned a 16.5 percent interest in Apartments.com and said it expected to receive about $95 million at closing. Gannett, the publisher of USA Today, owned a 26.9 percent interest in Apartments.com and reported that it expected to receive about $155 million. Other owners included Tribune and McClatchy. These media giants had tried and failed to transition their classified advertising business online. CoStar was essentially buying the remnants of newspapers' digital real estate dreams. What followed was a blitzkrieg of acquisitions that fundamentally altered CoStar's DNA. Between 2017 and 2020, the company acquired the online marketplaces Westside Rentals, ForRent.com (previously owned by Dominion Enterprises), Cozy Services, Off Campus Partners, and Ten-X; in addition to the hotel research and analytics firm STR, the residential mobile application provider Homesnap.

The most strategic moves came in late 2020 and early 2021. CoStar Group has agreed to acquire Homesnap, the residential real estate search portal company, for $250 million in cash. Then, just months later, the company acquired Homes.com for $156 million. These weren't random acquisitions—they were chess moves in a grand strategy to challenge Zillow's dominance.

The philosophy was revolutionary for the residential real estate industry. "Rather than building a business model based on creating friction to syphon off agent commissions, we plan to provide a next generation marketplace that connects listing and buyer agents directly," Florance declared. This was a direct shot at Zillow's model of selling leads and increasingly competing with agents through iBuying and other services.

The genius of the strategy was in its agent-friendly approach. While Zillow and other portals were increasingly seen as competitors by real estate agents—selling leads, launching brokerage services, and attempting to disintermediate the traditional transaction—CoStar positioned itself as the agents' champion. "Your listing, your lead" became the battle cry, a promise that listing agents wouldn't have to compete with buyer's agents advertising on their own listings.

By 2021, CoStar had assembled an impressive arsenal in residential real estate. Apartments.com dominated multifamily rentals. Homesnap provided the technology platform trusted by over 300,000 agents. Homes.com brought a recognized consumer brand and established traffic. The pieces were in place for what would become CoStar's most audacious gambit yet.

VI. The Homes.com Gambit: Taking on Zillow (2021-2024)

The transformation of Homes.com from also-ran to Zillow challenger represents one of the most aggressive competitive assaults in recent tech history. When CoStar acquired the property in 2021, it was generating roughly 5 million monthly visitors—a rounding error compared to Zillow's hundreds of millions. What happened next shocked the industry.

In 2024, CoStar Group purchased an estimated $35 million worth of airtime at Super Bowl LVIII for four Super Bowl commercials advertising its subsidiaries Homes.com and Apartments.com. The ads featuring Dan Levy weren't just expensive—they were a declaration of war. The message was simple: agents keep their leads, consumers get better service, everyone wins except the incumbent portals.

But the Super Bowl was just the opening salvo. CoStar committed to spending hundreds of millions annually on marketing Homes.com. By 2024, the site had grown from 5 million to 130 million average monthly unique visitors—a 26-fold increase in just three years. This wasn't organic growth; it was growth through sheer financial firepower, the kind only a company with CoStar's balance sheet could sustain.

The strategy was brilliantly simple: offer agents everything Zillow charged for, but for free. No referral fees. No commission cuts. No competing with agents for listings. Just pure lead generation with the listing agent maintaining control. For an industry that had grown increasingly frustrated with portal economics, it was a compelling proposition.

The early results were mixed but promising. While Homes.com's traffic exploded, monetization remained a challenge. The company was essentially buying market share, spending far more on user acquisition than it was generating in revenue. But Florance had played this game before with Apartments.com, which took years to become profitable but eventually dominated its market.

VII. International Expansion & The Tech Stack (2016-2025)

While battling for residential supremacy in the U.S., CoStar quietly built a global empire. The European acquisitions started modestly—Thomas Daily and Belbex in 2016—but accelerated into a full-scale invasion of international markets.

From 2018 through 2023, it acquired the British online marketplace Realla, the German real-estate data company Emporis, the French online marketplace BureauxLocaux, and the British property portal OnTheMarket. Each acquisition followed the same playbook: buy the leading local player, invest in technology and data collection, integrate with the global platform.

The crown jewel came in 2025. After initially taking a 16.9% stake in Australian real estate information company Domain Group, CoStar entered an agreement to acquire 100% of the company for US$1.92 billion in May 2025. This wasn't just an international expansion—it was a statement that CoStar intended to be the global real estate data platform.

But perhaps the most intriguing acquisition was In February 2025, CoStar acquired the 3D spatial mapping company Matterport for $1.6 billion. This represented a fundamental bet on the future of real estate: that properties would increasingly be experienced virtually before being transacted physically. Matterport's technology could create detailed 3D tours of properties, essentially digitizing physical space into data—exactly the kind of transformation CoStar had been executing for decades.

VIII. Culture, Controversy & Management Style

The culture at CoStar has always been intense, but by 2022, the pressure cooker environment had reached a boiling point. Over 29 current and former employees claimed to have been excessively monitored and micromanaged, including with unscheduled check-in video calls made by the company's IT department, as well as being publicly berated and arbitrarily fired in some cases. The revelations painted a picture of a company where innovation came at a steep human cost.

The stories were shocking in their specificity. Liz Morgan, a former employee, recalled being called out by Florance during a training session for appearing to sleep when she was actually taking notes. Despite her protests and offer to take a quiz proving her attention, she was fired minutes later. Another employee, Nate Peterson, received a call from the Richmond Police Department asking about a CoStar parody Instagram account, with the sergeant pointing out state laws against "harassment by computer."

Perhaps most jarring was a former communications director's recollection of Florance pointing a semiautomatic pistol toward his screen during a March 2020 video call, explaining he had seen bears near his rural Virginia property. While CoStar denied this incident occurred, calling Florance "a well-trained and licensed shooter who is passionate about firearm safety," the former employee shared contemporaneous text messages about the incident with colleagues who confirmed receiving them.

The turnover statistics told their own story. CoStar had seen a turnover of roughly 37% of its employees over the course of 2021, with the company's attrition rate at 36.6% compared to a real estate industry average of 34.9% for the period. The company made efforts to take down criticism of itself on various social media platforms. CoStar Group denied the allegations, contending that the discontent had stemmed from the company's high expectations.

This wasn't just about a demanding boss—it was about a fundamental tension in CoStar's culture. Florance's competitive intensity, the very trait that had driven the company's remarkable growth, was creating collateral damage. At the Inman Connect Las Vegas conference in October, the executive accused a rival listing portal—which sounded conspicuously like Zillow—of "hijacking" listings, likening some of their agent fee practices to mob extortion. The same combative energy directed at competitors was being turned inward.

Beyond the management controversies, CoStar faced more serious allegations about its business practices. The company has been criticized for anticompetitive and monopolistic business practices, often using aggressive litigation and "public-relations warfare" to "push [competitors] to the brink of collapse or weaken them enough to make them soft targets for an acquisition".

The most significant legal challenge came in February 2024. A proposed consumer class action lawsuit was filed against CoStar in multiple states, accusing the company of a price-fixing conspiracy in which it conspired with a group of luxury hotel chains—including Hilton, Hyatt, Marriott, InterContinental, Loews, and Accor—to keep room rental prices artificially high by sharing competitively sensitive information through the company's STR reports. These allegations were based in part on insider information shared by an STR software engineer.

The lawsuit's details were damning. Defendants were sharing "super-timely revenue and occupancy data," including rooms available, rooms sold and revenue with STR, and in return received similar data on their competitors through STR's STAR Reports. STR also collected hotels' forward-looking booking data on future occupancy levels. Evidence in the lawsuit featured the future listing prices from 6,000 hotels across 15 cities in the US, between January and June 2024, showing an "average overcharge of at least 4.3 per cent" for five-star hotels.

The ethical questions were profound. Was STR simply providing market intelligence, or was it facilitating collusion? The company that had built its empire on transparency and data was now accused of enabling anti-competitive behavior through that very same data.

IX. Business Model & Financial Architecture

The financial engine powering CoStar's aggressive expansion is a masterclass in subscription economics. With 95% of revenue coming from subscriptions and renewal rates hovering around 90%, the company has built one of the most predictable revenue streams in technology. This isn't the volatile, transaction-dependent model of residential portals—it's the steady, compounding growth of enterprise software.

The unit economics are compelling. Customer acquisition costs (CAC) for commercial clients average 12-18 months of payback, but with average customer lifespans extending 7-10 years, the lifetime value to CAC ratio exceeds 5:1. Every dollar spent acquiring a commercial real estate broker returns five dollars over the relationship lifecycle. This math enabled CoStar to invest billions in data collection while maintaining profitability.

The marketplace-data flywheel creates multiplicative rather than additive value. Every new listing on LoopNet generates data points for CoStar's analytics platform. Every CoStar subscriber who lists properties drives traffic to LoopNet. The network effects compound: more data attracts more subscribers, more subscribers generate more listings, more listings create more data. It's a virtuous cycle that becomes increasingly difficult for competitors to replicate as it scales.

The capital allocation strategy reflects Florance's build-versus-buy philosophy. While the company has made strategic acquisitions, the core investment remains internal: research, technology, and marketing. The $5 billion invested in proprietary data collection wasn't just spending—it was building an asset that appreciates with time. Unlike physical infrastructure that depreciates, CoStar's database becomes more valuable with each data point added.

The residential pivot introduced new dynamics to the financial model. Apartments.com operates on a different cadence—B2C rather than B2B, marketing-intensive rather than sales-driven, monthly rather than annual contracts. But the underlying principle remains: dominate the data layer, then monetize through marketplaces. The hundreds of millions spent marketing Homes.com isn't cash burned—it's customer acquisition investment with an expected multi-year payback.

What's remarkable is the company's ability to fund aggressive expansion while maintaining profitability in core segments. Commercial real estate operations generate massive cash flows that fund residential experiments. It's portfolio theory applied to business segments: the mature, profitable commercial business subsidizes the high-growth, high-risk residential ventures.

The competitive moat isn't just about data—it's about the economics of replication. A competitor would need to invest billions to match CoStar's database, spend years building research methodology, and somehow convince customers to switch from an embedded platform. The replacement cost of CoStar's assets far exceeds the company's market capitalization, creating a fundamental asymmetry that protects against disruption.

X. Power & Playbook

Understanding CoStar through Hamilton Helmer's 7 Powers framework reveals why the company has maintained its dominance for nearly four decades. This isn't just competitive advantage—it's compound competitive advantage, where each power reinforces the others.

Scale economies manifest in research costs spread across an expanding subscriber base. The same researcher tracking office buildings in Manhattan serves thousands of subscribers. The marginal cost of adding a new customer approaches zero, while the marginal cost for a competitor to match CoStar's data coverage is astronomical. This isn't just efficiency—it's economic gravity that pulls the market toward monopoly.

Network effects operate at multiple levels. Direct network effects occur in marketplaces like LoopNet—more buyers attract more sellers and vice versa. Indirect network effects emerge from data aggregation—each new data point makes the platform more valuable for all users. Cross-side network effects connect different user types—brokers, investors, and property owners—creating a multi-sided platform that becomes exponentially more valuable as each side grows.

Switching costs embed themselves in customer workflows like digital concrete. After years of using CoStar's interface, understanding its data taxonomy, and building internal processes around its reports, moving to another platform isn't just inconvenient—it's organizational surgery. The historical data alone creates lock-in; losing access to years of market intelligence is like deliberately inducing amnesia.

Cornered resource is CoStar's ultimate moat: proprietary data nobody else can replicate. This isn't public information anyone can scrape—it's verified, validated, and continuously updated intelligence gathered through millions of phone calls, property visits, and broker relationships. The data isn't just comprehensive; it's authoritative. When CoStar says a building is 87% leased, the market believes it.

Process power emerges from 35+ years of methodology refinement. CoStar doesn't just collect data; they've perfected the science of collection. Which questions to ask, whom to call, how to verify, when to update—these processes, refined over decades, can't be reverse-engineered or quickly replicated. It's institutional knowledge encoded in organizational DNA.

The playbook that emerges from these powers is remarkably consistent:

1. Digitize analog industries before they know they need it—See the future before the market does

2. Own the data layer, then add marketplaces—Control information flow, then facilitate transactions

3. Acquire strategically, integrate ruthlessly—Buy competitors or complementary assets, then impose your operating model

4. Pick fights with giants when you have an edge—Challenge incumbents where your strengths exploit their weaknesses

5. Build switching costs through workflow integration—Become so embedded that leaving feels impossible

This playbook explains both historical success and future strategy. The Homes.com assault on Zillow follows the same pattern as the commercial real estate conquest: build superior data, create agent-friendly economics, invest massively in marketing, and wait for network effects to compound.

XI. Bear vs. Bull Case

The investment thesis for CoStar splits dramatically depending on your view of their residential strategy and competitive dynamics.

The Bull Case: CoStar represents the inevitable winner in real estate digitization across all property types. The commercial monopoly generates predictable cash flows funding the residential transformation. Homes.com's agent-friendly model will eventually triumph over Zillow's extractive approach—it's not about winning quickly but winning permanently. The $100+ billion addressable market across commercial and residential real estate suggests the current $33 billion market cap significantly undervalues long-term potential. International expansion through Domain Group and OnTheMarket creates new growth vectors. Matterport acquisition positions CoStar for the AR/VR revolution in property viewing. The subscription model's predictability and 90% renewal rates provide downside protection even if growth slows.

The Bear Case: The residential pivot is a massive capital destruction exercise masquerading as strategic expansion. Hundreds of millions spent on Homes.com marketing has generated traffic but not profits. Zillow's brand dominance and consumer habits are too entrenched to overcome. The agent-friendly model sounds good but ignores that portals need revenue, and agents ultimately won't pay enough to sustain the platform. International acquisitions are distractions from core market challenges. The company trades at premium multiples based on growth expectations that may not materialize. Regulatory scrutiny over data sharing practices and anti-competitive behavior could result in significant penalties or forced divestitures. The culture issues and management style may lead to talent exodus in competitive tech labor markets.

The Execution Risk: Everything hinges on Homes.com achieving critical mass. If the platform can't convert traffic to revenue efficiently, CoStar will have spent billions attacking an impregnable position. The company is fighting multi-front wars—against Zillow in residential, against new entrants in commercial, against regulators over competitive practices. History is littered with dominant companies that overextended trying to conquer adjacent markets.

The Regulatory Wild Card: The class action lawsuit seeks damages for potentially hundreds of thousands of people who rented rooms from defendant hotels from February 21, 2020, through the present. If courts find STR facilitated price-fixing, the penalties could be massive and the business model might require fundamental restructuring.

The Technology Disruption Question: AI and alternative data sources could disrupt CoStar's human-powered research model. If machines can gather and verify property data more efficiently than humans, CoStar's massive research force becomes a liability rather than an asset. Startups with modern tech stacks and AI-first approaches might leapfrog CoStar's legacy systems.

XII. Epilogue: The Next Chapter

As we enter 2025's final quarter, CoStar stands at an inflection point. The residential gambit has reached the moment of truth—either Homes.com achieves escape velocity and justifies the massive investment, or it becomes a cautionary tale about the limits of financial firepower against entrenched network effects.

Recent developments suggest momentum is building. The Domain Group acquisition gives CoStar a profitable residential platform to study and replicate. The Matterport technology could revolutionize property tours, creating differentiation even Zillow can't match. The agent community's frustration with portal economics has reached a breaking point, potentially creating the opening CoStar needs.

The AI and digital twin revolution presents both opportunity and threat. CoStar's vast database could train property valuation models that no competitor can match. But if AI can automate data collection, the company's largest operating expense—its research force—might become obsolete. Florance's bet appears to be that human verification and relationship-building will remain essential even in an AI-powered future.

What winning looks like in five years: CoStar maintains commercial dominance while Homes.com captures 20-30% of residential portal traffic. International operations contribute 25% of revenue. Matterport's 3D tours become industry standard, creating new subscription tiers. The company's market cap exceeds $75 billion as investors recognize the value of controlling real estate data globally.

The biggest surprise in the CoStar story isn't the ambition—it's the patience. While Silicon Valley celebrates rapid disruption, CoStar spent 35 years methodically building an unassailable position. The residential attack isn't a desperate pivot but a logical extension of proven strategy. Whether that patience will be rewarded or punished remains the central question.

The ultimate question—platform or product—has been definitively answered. CoStar is a platform, but not in the typical tech sense. It's a platform for understanding physical space through data, for connecting property markets through information, for transforming analog industries through digital tools. The product is just the beginning; the platform is the destination.

What Florance understood in that Princeton dorm room remains true today: real estate isn't about buildings—it's about information asymmetry. Whoever controls the information controls the market. CoStar's journey from dorm room startup to data empire isn't just a business success story—it's a masterclass in recognizing that in the information age, data isn't just valuable. It's power.

The next chapter will determine whether that power can reshape residential real estate the way it conquered commercial property. If Florance succeeds, CoStar won't just be the Bloomberg of real estate—it will be the operating system for how humanity interacts with physical space. If he fails, it will still remain one of the most successful sector-specific data companies ever built, a testament to the value of patience, persistence, and the power of compound advantages.

For investors, operators, and entrepreneurs, the CoStar story offers timeless lessons: See the future before the market does. Build assets that appreciate with time. Create switching costs through workflow integration. And perhaps most importantly—in a world obsessed with disruption, sometimes the biggest opportunity is digitizing what already exists. The future might be about artificial intelligence and virtual reality, but the foundation remains decidedly analog: understanding and organizing information about the physical world we inhabit.

XIII. Recent News

[This section would be updated with the latest news and developments about CoStar Group, including quarterly earnings, acquisition announcements, regulatory updates, and strategic initiatives.]

XIV. Links & Resources

[This section would include links to CoStar Group investor relations, SEC filings, industry reports, competitive analyses, and relevant academic studies on real estate technology and market dynamics.]

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube