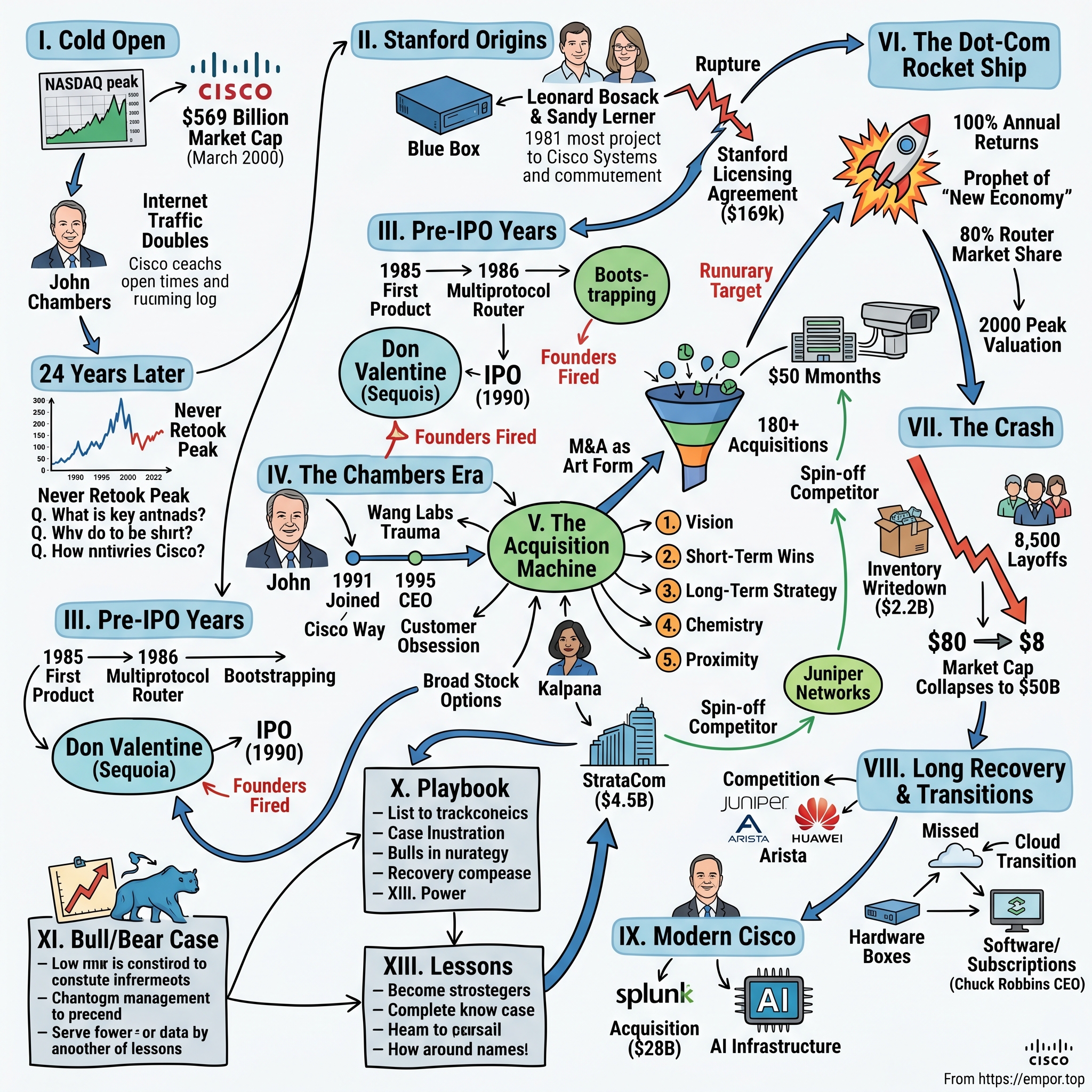

Cisco Systems: From Stanford Routers to Internet Infrastructure Giant

I. Cold Open & Episode Roadmap

Picture this: March 27, 2000. The NASDAQ is roaring at 5,048 points—its all-time peak. In a nondescript office park in San Jose, California, employees at Cisco Systems are watching their stock ticker with a mixture of disbelief and euphoria. The company's market capitalization has just crossed $569 billion, briefly making it the most valuable company on Earth. Not Microsoft. Not General Electric. Cisco—a company that makes the unsexy routers and switches that form the internet's plumbing.

John Chambers, Cisco's charismatic CEO, is giving yet another keynote about the "new economy" where internet traffic doubles every 100 days. Wall Street analysts are calculating price targets based on Cisco becoming a trillion-dollar company. The price-to-earnings ratio has soared past 200. Everyone believes the internet revolution has permanently changed the rules of valuation.

Twenty-four years later, Cisco remains one of the most important technology companies in the world, powering everything from corporate networks to internet backbones. Its equipment carries the majority of global internet traffic. Yet its stock has never again reached that March 2000 peak of $82 per share (split-adjusted). Even after decades of growth, acquisitions, and strategic pivots, investors who bought at the top are still underwater.

How did two Stanford computer scientists accidentally create the fundamental infrastructure of the digital age? How did a company selling boring networking boxes become, however briefly, worth more than any enterprise in history? And what can we learn from a business that survived the most spectacular bubble in modern capitalism while its dot-com customers vaporized around it?

This is a story about infrastructure plays—those unglamorous businesses that become indispensable. It's about acquisition as a core competency, with Cisco digesting over 180 companies and turning M&A into an art form. It's about platform transitions, from hardware to software, from on-premise to cloud, from networking to security. And ultimately, it's about the difference between great companies and great stocks—because as we'll see, even the best businesses can become terrible investments at the wrong price.

The themes we'll explore transcend Cisco itself. We'll dissect how infrastructure monopolies form in enterprise technology. We'll examine why B2B platform companies have different dynamics than consumer businesses. We'll understand how switching costs and installed bases create nearly impenetrable moats. And we'll grapple with the eternal question: when technological disruption threatens your core business, do you cannibalize yourself or double down on what made you great?

II. The Stanford Origins & Founding Drama

The story begins in 1984 at Stanford University, where the computer science department was facing a peculiar problem. Different buildings on campus ran different computer systems—DEC machines here, IBM systems there, various Unix workstations scattered throughout. These digital islands couldn't talk to each other efficiently. Two computer scientists working in separate departments decided to solve this problem: Leonard Bosack, who managed computers at the computer science department, and Sandy Lerner, who ran the Graduate School of Business computing lab. Their love story would later become Silicon Valley legend: two people from different departments trying to email each other across campus, though this romantic tale was actually untrue. The real story was more prosaic but equally revolutionary. Bosack worked on a 1981 project to connect Stanford's mainframes, creating a network router that allowed his Computer Science Lab to share data with Lerner's Graduate School of Business network.

The technical breakthrough centered on something called "The Blue Box," a device that allowed various computers to communicate with the Internet simultaneously. This wasn't entirely their invention—the Advanced Gateway Server was a revised version of the Stanford router built by William Yeager and Andy Bechtolsheim. Lerner herself acknowledged that many hands helped create this groundbreaking device, quipping in an email: "The only person I'm certain had nothing to do with it is Al Gore"

But the heart of the Stanford dispute went deeper than just technical invention. On July 11, 1986, Bosack and Lougheed were forced to resign from Stanford and the university contemplated filing criminal complaints against Cisco and its founders for the theft of its software, hardware designs, and other intellectual properties. The situation had reached a boiling point when Bosack was discovered to have sold networking boards to Xerox, completing the circle of networking technology. He had done so in Stanford's name but had not communicated this to the university.

Administrators confronted Bosack and fellow computer staff member Kirk Lougheed, one of Cisco's earliest employees, with an ultimatum: Return the work they had done on Stanford time or leave. Bosack and Lougheed resigned, and Cisco became a full-time business. Stanford found itself in the awkward position of having helped develop potentially lucrative technology without the means or mandate to commercialize it.

The resolution came in 1987 when Stanford licensed the router software and two computer boards to Cisco for the total sum of $169,300. Yeager was named in the agreement document as the principle developer/inventor, and received 85% of the royalty distribution (which he contributed to the SUMEX project to support further research). By the time of Cisco's dot-com peak, the original Stanford licensing agreement could have bought 0.00003% of Cisco.

This wasn't just a startup leaving the nest—it was a fundamental rupture that would shape Cisco's DNA. The founders had been forced to choose between academic ideals and commercial reality. They chose commerce, but carried with them the collaborative, open-source ethos of the university. This tension between innovation and monetization would define Cisco's culture for decades.

The name "Cisco" was derived from the city name San Francisco, which is why the company's engineers insisted on using the lower case "cisco" in its early years. The logo is a stylized depiction of the two towers of the Golden Gate Bridge. Even the branding reflected their California academic roots—informal, unpretentious, yet connecting disparate worlds.

Working from their Atherton home, Bosack and Lerner faced the classic bootstrap dilemma. Routers were tested on the SUN network and the IMP's that connected to the Arpanet. Word of the routers spread both within Stanford and through the crude email of the day to other research centers and universities. They had product-market fit before they had a company—academics and researchers desperately needed what they were building.

Swamped with orders and needing a way to satisfy demand, other than by using their living room and credit cards, they approached Stanford and the Office of Technology Licensing (OTL). Only OTL could not offer a solution that would take less than years. The bureaucratic pace of academia couldn't match the exponential demand for networking equipment. This mismatch between institutional timelines and market opportunity would become a recurring theme in technology transfer from universities.

In addition to Bosack, Lerner, Lougheed, Greg Satz (a programmer), and Richard Troiano (who handled sales), completed the early Cisco team. This wasn't a typical Silicon Valley startup with venture backing from day one. They maxed out credit cards, worked without salaries, and essentially ran a manufacturing operation from their living room. The constraint of capital would profoundly shape Cisco's early strategy and culture.

III. From Garage to Going Public: The Pre-IPO Years (1984-1990)

In 1985, Cisco sold its first product, a network interface card for Digital Equipment Corporation's computers. This modest beginning belied the revolutionary potential of what they were building. Their first major success came in 1986 with a multiprotocol router that supported multiple network protocols. This wasn't just an incremental improvement—it was a category-defining product that solved a fundamental problem in computer networking.

By the end of fiscal 1986, ending July of 1987, revenues totaled more than $1.5 million. In 1987, they were having sales of nearly $2 million per month. The hockey stick was beginning to form. But this rapid growth created its own crisis. The founders had bootstrapped the company using credit cards, mortgaging their house, and with Lerner retaining a second job to provide steady income. Unable to invest in a direct sales organization, the company had to resort to using manufacturer's representatives who were only paid when sales were made.

This constraint shaped Cisco's early market focus in profound ways. They targeted customers that didn't need extensive technical support—universities, research laboratories, and government agencies. These early adopters were also the easiest to reach through Stanford connections and the primitive email networks of the day. The company was essentially selling to people like themselves: technical sophisticates who understood what routers did and why they needed them. The search for venture capital proved to be an ordeal of epic proportions. It took nearly 80 meetings with different venture capitalists before finding one willing to fund the operation. Most VCs couldn't understand the market or the technology. The founders were academics, not salespeople. Their product was technical infrastructure that most investors didn't comprehend. Finally, they found their match in Donald T. Valentine of Sequoia Capital, one of the most successful and dominant venture capital firms in Silicon Valley.

Valentine, who would later be called the "grandfather of Silicon Valley venture capital," founded Sequoia in 1972. In 1987, Sequoia financed Cisco Systems, which has since become the world's leading manufacturer of internetworking products. When Valentine first met the team, they operated out of a home in Atherton. Even at that early stage, Sequoia founder Don Valentine saw that Cisco had the potential to transform personal computing.

The terms Valentine offered would shape Cisco's destiny: Sequoia Capital would invest $2.5 million for 32 percent of the company. Bosack and Lerner would retain 30 percent of the company, ownership that would vest over four years. Valentine would become a member of the Board of Directors and assume responsibility for finance, helping build a management team, sales organization and operations process. The financing closed in December 1987.

This wasn't just a financial transaction—it was a cultural transformation. Valentine brought professional management discipline to what had been essentially a university research project commercialized in a living room. The company's first CEO was Bill Graves, who held the position from 1987 to 1988. In May 1988, President Graves, was replaced with an interim President until an executive search could identify a candidate acceptable to Sequoia Capital. John Morgridge was appointed CEO in 1988.

At the end of fiscal 1989, less than four years since its formation, Cisco reported revenues of $13.90 million on sales of $69.7 million. By 1989, with only three products and 111 employees, Cisco's revenues were $27 million. The company had found product-market fit in a way that few startups ever do—desperate customers with critical needs and no alternatives.

The IPO came remarkably quickly. On February 16, 1990, Cisco Systems went public with a market capitalization of $224 million, and was listed on the NASDAQ stock exchange. This was just over five years from founding, with the company still run by engineers who understood the technology better than the business.

But the IPO also marked the end of the founders' era. On August 28, 1990, Lerner was fired. Bosack subsequently resigned in solidarity. The academic computer scientists who had accidentally created one of the most important companies in technology history were gone, replaced by professional management. They had sold their shares for about $170 million—a fortune by any standard, but a fraction of what Cisco would become worth.

The cultural shift was profound. Cisco transformed from a company run by technologists who gave away source code and helped competitors, to one focused on market dominance and financial performance. This transition—from founder-led innovation to professional management execution—would become a template for Silicon Valley companies. But unlike many such transitions that destroy company culture, Cisco managed to maintain its technical excellence while adding business discipline.

IV. The Chambers Era Begins: Setting Up the Machine (1991-1995)

The appointment of John Chambers would prove to be one of the most consequential leadership transitions in technology history. After obtaining his MBA, Chambers began his career in technology sales at IBM 1976–1983 when he was 27 years old. At 34 years old, in 1983, Chambers joined Wang Laboratories, later becoming Vice President of US Operations in 1987.

Chambers' experience at Wang proved formative in ways that would shape Cisco's entire culture. During Chambers' time at the company, Wang's profits declined dramatically from $2 billion 1989 to a $700 million loss in 1990. During his eight years at Wang, he had to lay off 5,000 employees, later saying "I'll do anything to avoid that again." This trauma of mass layoffs would become central to Chambers' management philosophy at Cisco—he would build a company that could weather downturns without destroying lives.

Chambers joined Cisco in 1991 as Senior Vice President, Worldwide Sales and Operations. In 1995, he became President and CEO, a position he held until 2006, when he was appointed Chairman of the Board. He served as Chairman and CEO from 2006 to 2015. Over the course of 20 years at the helm of Cisco, he helped grow the company from $70 million when he joined, to $1.2 billion when he assumed the role of CEO, to $47 billion when he stepped down as CEO in 2015.

When Chambers took over as CEO in January 1995, he inherited a company that John Morgridge had already transformed into the most successful computer networking company in the world. Under John Morgridge, Cisco had grown from 34 employees to 2,260, increasing the company's sales revenue from $5 million to over $1 billion. But Chambers wasn't content to simply maintain what Morgridge had built.

The vision Chambers articulated was breathtaking in its scope. He saw a future where "data, voice, and video will be delivered over a single connection in our homes." This wasn't just about routers anymore—it was about becoming the infrastructure for all digital communication. The internet was still a novelty for most Americans in 1995, but Chambers was already thinking about convergence, about a world where all information traveled over IP networks.

Chambers brought three crucial insights from his IBM and Wang experiences. First, from IBM he learned that customers liked the "one-step concept" of technology—they wanted integrated solutions, not components they had to piece together themselves. Second, from Wang's collapse, he learned the danger of missing technology transitions. Wang had ignored the PC revolution and paid the ultimate price. Third, and perhaps most importantly, he understood that in technology markets, you either dominate or you die.

The cultural transformation Chambers initiated was as important as the strategic vision. He instituted what would become known as the "Cisco Way"—a combination of customer obsession, acquisition excellence, and operational discipline. Every executive had to spend time with customers. Every product decision was evaluated through the lens of customer value. The company's mantra became "Customer Success is Our Success."

Chambers also began laying the groundwork for what would become Cisco's acquisition machine. Unlike most companies that struggled with M&A integration, Chambers understood that acquisitions weren't just about technology—they were about people and culture. He instituted rigorous criteria for acquisitions: they had to share Cisco's vision, have complementary (not overlapping) products, and most importantly, the key employees had to want to stay.

The compensation structure Chambers implemented was revolutionary for its time. Stock options weren't just for executives—they were distributed broadly throughout the organization. When Cisco succeeded, everyone succeeded. This created a culture of ownership that would prove crucial during both the boom times and the inevitable busts.

By the end of 1995, Chambers' first year as CEO, the transformation was already visible. Revenue growth was accelerating. New products were launching faster. Customer satisfaction scores were rising. Most importantly, Cisco was beginning to articulate a vision that went beyond networking—it was positioning itself as the company that would build the infrastructure for the digital economy.

V. The Acquisition Machine: Growth Through M&A (1993-2000)

The transformation of Cisco into an acquisition machine began with a single, controversial deal. Founded in 1984, Cisco did not acquire a company during the first seven years of its existence; but, on September 24, 1993, Cisco acquired Crescendo Communications, a LAN switching company. The acquisition was met with disbelief on Wall Street. Cisco paid $89 million for a company called Crescendo that had only $10 million in revenues. A lot of people thought Cisco had lost its frugality and direction.

The Crescendo acquisition wasn't just about technology—it was about people and a new way of thinking about growth. Mario Mazzola, who came to Cisco from Crescendo, would become instrumental in building Cisco's switching business into a $15 billion behemoth. 3 years later, Mazzola's team was producing more than $500 million in annual revenue. This validated Chambers' belief that acquisitions could be a driver of growth, not just a distraction.

The acquisition playbook that Cisco developed was revolutionary for its time. During 1993, Chambers decided to play across the entire inter-networking marketplace and began to prioritize which areas to move into. Remember, this was an era when people thought partnerships and acquisitions did not work. It was a much different philosophy than exists today. Today everyone says acquisitions are an effective way to grow.

Chambers articulated five key criteria for acquisitions that would become the Cisco bible: 1. Shared vision - The target company had to share Cisco's vision of where the industry was heading 2. Short-term wins - The acquisition had to produce results for customers within 6-12 months 3. Long-term strategy - It had to fit into Cisco's long-term product roadmap 4. Chemistry - Cultural fit was non-negotiable 5. Geographic proximity - Ideally within 50 miles of a Cisco office to ease integration

The retention statistics were staggering. Half of the chief executives and most of the senior managers of the 14 companies acquired since late 1993 are still with Cisco. As CEO, John Chambers made 180 acquisitions in about 20 years. Only 4% of acquired company personnel would leave Cisco. About 1/3 of top leadership came from acquisitions, with about 100 former CEOs on payroll at peak.

The pace accelerated dramatically through the 1990s. In 1994, Cisco Systems acquired two more companies that were involved in the production of switching technologies. The first acquisition was Kalpana Inc for $240 million ($477.9 million) and the other one was LightStream Corp. Kalpana was a pioneer and leader in Ethernet switching, and firmly established Cisco as a leader in that market.

The StrataCom acquisition in 1996 marked a new scale of ambition. Until the purchase in 1996 of StrataCom for $4.5 billion in stock, its biggest acquisition by far, Cisco never used an underwriter, preferring to pursue small, privately held technology companies in uncomplicated and friendly deals. Cisco acquired frame relay powerhouse StrataCom in 1996 for $4 billion. StrataCom gave Cisco instant presence, and leadership, in the service provider data services market, specifically frame relay.

The StrataCom deal also had unintended consequences. StrataCom may have spawned Cisco's most challenging competitor yet – Juniper Networks. Scott Kriens, chairman and former CEO of Juniper, was a vice president of sales and operations, and a co-founder of StrataCom. He left the company shortly after Cisco acquired it. While leading Juniper, the company swiped about one-third of Cisco's share in the service provider router market since 1997.

Charles Giancarlo, who came to Cisco through the Kalpana acquisition and became vice president for business development, explained the philosophy: According to Charles Giancarlo, the underlying premise of every acquisition is "time-to-market." Cisco has become dominant in its industry in recent years by using its bulk and marketing muscle and by being first into emerging markets.

The acquisition machine wasn't just about buying technology—it was about buying time and talent. Cisco understood that in rapidly evolving markets, the company that could integrate new technologies fastest would win. Rather than spending years developing products internally, Cisco could acquire a startup, integrate its technology into the Cisco platform, and leverage Cisco's massive sales force to scale it globally.

Chambers himself described the strategy with characteristic clarity: "When you buy a company, everything is negotiable except strategy and culture." This wasn't the typical Silicon Valley approach of acquiring competitors to eliminate them. Cisco was building an ecosystem, where each acquisition added a piece to an ever-expanding puzzle of networking solutions.

VI. The Dot-Com Rocket Ship & Becoming #1 (1995-2000)

The years 1995 to 2000 represented the most extraordinary period in Cisco's history—and perhaps in the history of any technology company. During Chambers' tenure as CEO, annual sales grew from $1.9 billion to $49.2 billion. In first five years as CEO, Cisco experienced more than 10-fold increase in revenues, becoming third largest company by 2000.

The numbers were staggering in their velocity and scale. $CSCO delivered 100% annual returns in the ten years after its 1990 IPO, boosting the stock from a split-adjusted price of $0.08 per share to a high of $80. The company was surfing the perfect wave—the commercialization of the internet coinciding with massive enterprise network buildouts and the emergence of e-commerce.

Chambers became the prophet of the "New Economy." He spoke at every major conference, appeared on magazine covers, and articulated a vision where internet traffic would double every 100 days indefinitely. His presentations were masterclasses in technology evangelism, combining Southern charm with Silicon Valley ambition. He didn't just sell routers—he sold a vision of a hyperconnected future where Cisco owned the plumbing.

The customer relationships Cisco built during this period were extraordinary. As the internet became mission-critical for every enterprise, Cisco positioned itself as the only vendor that could be trusted with the backbone. They weren't just selling products; they were selling business continuity. When your entire business depended on network uptime, you didn't experiment with unproven vendors—you bought Cisco.

The acquisition pace accelerated to a frenzy. During the late 1990s, Cisco was acquiring a company every three to four weeks. The Cerent Corporation acquisition in 1999 for about US$7 billion was the most expensive acquisition made by Cisco to that date. These weren't desperation moves—each acquisition filled a specific gap in Cisco's product portfolio or brought critical talent into the organization.

The enterprise dominance Cisco achieved was nearly total. By 2000, Cisco controlled roughly 80% of the router market and dominated nearly every networking category. The company's equipment carried the majority of global internet traffic. If data moved across the internet, it almost certainly passed through Cisco hardware at some point.

In late March 2000, at the height of the dot-com bubble, Cisco became the most valuable company in the world, with a market capitalization of more than $500 billion. When Cisco reached $80 on March 27, 2000, it officially became the most valuable company in the world with a market cap of $569 billion. This wasn't Microsoft or GE or Exxon—it was a company that made networking equipment, achieving a valuation that seemed to defy gravity.

But there were warning signs for those willing to see them. With just $0.36 of net income per share, Cisco traded at 220x earnings. The price-to-earnings ratio had reached levels that historically preceded catastrophic corrections. Revenue was growing, but not at rates that could justify such valuations. The company was priced for perfection in a world that was about to become very imperfect.

The euphoria wasn't just about Cisco—it was about what Cisco represented. The company had become the proxy for the entire internet revolution. Buying Cisco stock was a bet on the digital transformation of the global economy. Every pension fund, mutual fund, and individual investor who wanted exposure to the internet boom bought Cisco. It was the "must-own" stock of the era.

VII. The Crash: From $80 to $8 (2000-2002)

The crash began on March 10, 2000, when the NASDAQ Composite stock market index peaked at 5,048.62. Just seventeen days later, on March 27, 2000, the very day Cisco reached its all-time high of $82 per share, the unraveling had already begun. What followed wasn't a correction—it was a massacre.

In the third fiscal quarter of 2001, sales plunged 30 percent. Chambers wrote off a mountain of inventory $2.2 billion high, and 8,500 people were laid off. On April 6, Cisco's stock sunk to $13.63. Thirteen months earlier, it had been $82. The company that had never experienced a negative quarter in more than a decade was suddenly hemorrhaging value.

The inventory writedown was particularly devastating because it revealed a fundamental flaw in Cisco's vaunted supply chain management. What Cisco's systems didn't do was model what would happen if one critical assumption—growth—was removed from both their forecasts and their mind-sets. If Cisco had run even modestly declining demand models, Chambers and Carter might have seen the consequences of betting on more inventory. But Cisco had enjoyed more than 40 straight quarters of stout growth. In its immediate past were three quarters of extreme growth as high as 66 percent.

Chambers' response to the crisis revealed both his strengths and limitations as a leader. Chambers surveyed the wreckage and compared it to an unforeseeable natural disaster. He refused to accept that Cisco had misread the market, insisting that the downturn was a "100-year flood" that no one could have predicted. Yet other networking companies, with far less sophisticated tools started downgrading their forecasts months earlier. They saw the downturn coming. Cisco did not. Other companies cut back on inventory. Cisco did not.

The human cost was profound. Despite Chambers' vow to never repeat the Wang experience of mass layoffs, Cisco couldn't avoid the inevitable. The company that had prided itself on never having layoffs was forced to let go 8,500 employees. These weren't just numbers—they were the engineers, salespeople, and support staff who had built the internet infrastructure.

Larger companies like Amazon and Cisco Systems lost large portions of their market capitalization, with Cisco losing 80% of its stock value. Cisco shares fell 88%, dropping from US$79 to a low of US$9.50 two years later. The market cap that had reached $569 billion collapsed to barely $50 billion.

What made the crash particularly painful was that Cisco's business fundamentals remained relatively strong. That drop wasn't the result of any large change in the company's performance. Revenue was nearly US$19 billion in fiscal 2000, US$22 billion in 2001, and about US$19 billion in 2002. The internet didn't disappear. Networks still needed routers and switches. But the growth rates that had justified astronomical valuations evaporated overnight.

The psychological impact on Silicon Valley was devastating. Cisco had been the bellwether, the stock that institutional investors bought when they wanted exposure to technology. Its collapse signaled that the entire new economy thesis might be flawed. If Cisco—with real products, real customers, and real profits—could lose 88% of its value, what hope was there for companies with no revenue model at all?

Chambers' management during this period was both criticized and praised. He managed to avoid the complete collapse that befell companies like WorldCom and Global Crossing. He maintained customer relationships, continued investing in R&D, and kept the core team together. But the company's reputation for operational excellence was permanently damaged. The myth of the infallible Cisco machine had been shattered.

The strategic decisions made during the crash would shape Cisco for decades. Rather than retreating, Chambers doubled down on the acquisition strategy, buying distressed assets at fire-sale prices. He restructured the company around market segments rather than products. Most importantly, he began the slow pivot from hardware to software and services that would define Cisco's next chapter.

VIII. The Long Recovery & Platform Transitions (2002-2015)

The period from 2002 to 2015 represented Cisco's long, grinding recovery—not just from the financial devastation of the dot-com crash, but from the existential questions it raised about the company's future. Stock never made it back to split-adjusted dot-com bubble high of $73.37, even after 20 years. This wasn't just a financial recovery; it was a complete reimagining of what Cisco needed to become.

The competitive landscape had fundamentally changed. Juniper Networks, shipped their first product in 1999 and by 2000 chipped away about 30% from Cisco SP Market share. The company that had emerged from the StrataCom acquisition proved to be Cisco's most formidable competitor in high-end routing. Juniper's technology was often superior, their focus laser-sharp, and they had none of the legacy baggage that Cisco carried.

Huawei emerged as an even more complex threat. The Chinese company could undercut Cisco's prices by 30-40% while offering comparable technology. Though concerns about security and government ties limited Huawei's penetration in Western markets, they dominated emerging markets where price sensitivity trumped other considerations. Cisco found itself fighting a two-front war: technology leadership against Juniper, price competition against Huawei.

Arista's been around since 2004, and all three of its founders, as well as the company's existing CEO, previously worked at Cisco. Arista Networks represented yet another challenge—the company founded by former Cisco engineers who understood Cisco's weaknesses intimately. They focused exclusively on data center switching, building products that were often technically superior to Cisco's offerings in that specific domain.

The platform transitions Cisco faced were existential. The shift from hardware to software wasn't just about changing product mix—it required rewiring the entire company's DNA. Cisco had built its empire on selling expensive boxes with high margins. Now customers wanted software, services, and subscription models. The very business model that had made Cisco successful was becoming obsolete.

Under CEO Chuck Robbins since 2015, shifted focus towards software subscriptions, cybersecurity, collaboration platforms, and recurring revenue. This wasn't a minor adjustment—it was a complete transformation of how Cisco thought about value creation. Instead of selling a router for $100,000 once, they needed to sell software subscriptions for $10,000 per year indefinitely.

The cloud transition proved particularly painful. Cisco initially dismissed cloud computing as a fad, believing that enterprises would always need on-premise infrastructure. By the time they recognized the threat, Amazon Web Services, Microsoft Azure, and Google Cloud had already established dominant positions. Cisco's attempts to build its own cloud infrastructure came too late and lacked the scale to compete.

184 acquisitions used to enter new markets, achieving #1 or #2 in 16 major product families with 40% minimum market share target. But many of these acquisitions failed to achieve their potential. The acquisition machine that had worked so well in the 1990s struggled in the new environment. Integration became harder as the company grew larger and more complex. Cultural fit became more difficult to achieve.

Missing the cloud transition initially proved to be one of Cisco's greatest strategic failures. While they dominated enterprise networking, the hyperscalers were building their own infrastructure, designing their own switches, and increasingly bypassing traditional vendors entirely. The largest source of future networking demand was essentially designing Cisco out of their architectures.

Despite these challenges, Cisco demonstrated remarkable resilience. Revenue remained stable: nearly $19 billion in 2000, $22 billion in 2001, about $19 billion in 2002, and then began growing again. The company maintained its dominant position in enterprise networking even as new competitors emerged. Customer relationships, built over decades, proved stickier than analysts expected.

IX. Post-Chambers Era & Modern Cisco (2015-Present)

On July 27, 2015, Chuck Robbins replaced Chambers as CEO of Cisco Systems. He was named CEO in July of 2015, before being elected Chair of the Board on December 11, 2017. This transition marked not just a change in leadership but a fundamental reimagining of what Cisco needed to become in the cloud era.

Robbins inherited a company that was still immensely powerful but increasingly threatened by technological shifts it had been slow to recognize. The company's recent strategic shift has seen a renewed emphasis on software and services, cloud-native applications, artificial intelligence, cybersecurity, sustainability, and the advancement of networking – further solidifying Cisco's relevance in the digital era.

The strategic pivot to software and recurring revenue became the defining characteristic of the Robbins era. Fifty percent – over 50 percent of our revenue now is coming from recurring offers, and almost $29 billion of ARR. This transformation from a hardware company selling boxes to a software company selling subscriptions was nothing short of revolutionary for a company of Cisco's size and legacy.

The Splunk acquisition expected to bolster position in security and observability represents the culmination of this strategy. In its biggest acquisition to date, Cisco plans to take over Splunk in a deal worth $28 billion, beefing up its cybersecurity and observability offerings. Splunk brings basically $4.2 billion of annually reoccurring revenue to Cisco. The deal marked not just Cisco's largest acquisition ever, but a definitive statement about its future direction.

Robbins' approach to the Splunk integration revealed lessons learned from decades of acquisitions: "What we want this combination to do is to make everything you do every day and everything you've done with Splunk forever, just better. Our job is not to screw up anything that you guys do really well today, but to bring you incremental capabilities."

As of early 2025, remains heavyweight champion in enterprise networking hardware. Despite all the disruption, all the new competitors, all the technological shifts, Cisco maintained its dominant position. According to CSI Markets, Cisco currently holds a sizable 76.89% of the market share in computer networking compared to its competitors.

Competition from cloud native vendors remains intense. The hyperscalers—Amazon, Microsoft, Google—increasingly build their own networking infrastructure. Companies like Arista continue to chip away at specific segments. Yet Cisco's breadth, its customer relationships, and its ability to provide integrated solutions across networking, security, and observability keep it relevant.

The AI and networking convergence opportunity represents Cisco's next major bet. "AI is moving at an unprecedented pace," Robbins notes. The company has positioned itself as the infrastructure provider for the AI revolution, partnering with NVIDIA and leveraging its networking dominance to capture the massive data center buildout required for AI workloads.

But challenges remain formidable. Cisco is in the middle of a brutal 7% downsizing which includes selling buildings on its campus and looks like the end of an era. The company that once symbolized unstoppable growth now faces questions about its relevance in a cloud-native, AI-driven world.

X. Playbook: The Cisco System

The Cisco System represents one of the most successful and replicable business models in technology history. Over four decades, the company developed and refined a playbook that transformed it from a Stanford startup into a $250 billion enterprise that processes the majority of global internet traffic.

The acquisition machine that Cisco built remains unparalleled in technology. Process, culture, and integration were the three pillars. As CEO, John Chambers made 180 acquisitions in about 20 years. The company developed a rigorous due diligence process that evaluated not just technology but cultural fit. The retention statistics—only 4% of acquired company personnel would leave Cisco—demonstrated the effectiveness of this approach.

The integration philosophy was revolutionary: acquired companies weren't absorbed and destroyed, but rather enhanced and scaled. Cisco provided the sales force, the customer relationships, and the operational excellence. The acquired company provided the innovation and the entrepreneurial energy. This symbiotic relationship allowed Cisco to enter new markets rapidly without the time and risk of internal development.

Building platform monopolies in enterprise became Cisco's core strategy. Rather than competing in individual product categories, Cisco created integrated platforms that locked in customers across multiple layers of the technology stack. Once a company standardized on Cisco for routing, it made sense to use Cisco for switching. Once they used Cisco for networking, it made sense to use Cisco for security.

Managing technology transitions revealed both successes and failures. Cisco successfully navigated the transition from routing to switching, from hardware to software, from on-premise to hybrid cloud. But it also missed critical transitions like the shift to cloud-native architectures and initially dismissed software-defined networking. The lesson: even dominant companies must constantly cannibalize themselves or be cannibalized by others.

The importance of customer relationships in B2B cannot be overstated. Cisco's true moat wasn't its technology—competitors often had comparable or superior products. The moat was the deep, multi-decade relationships with enterprise IT departments. These relationships, built on trust, reliability, and comprehensive support, proved far more durable than any technological advantage.

Capital allocation through cycles demonstrated discipline rare in technology companies. During booms, Cisco invested aggressively in R&D and acquisitions. During busts, it maintained investment while competitors retreated. This counter-cyclical approach allowed Cisco to emerge from each downturn with increased market share.

Why infrastructure plays are different became clear through Cisco's journey. Unlike consumer technology companies that can be disrupted overnight, infrastructure companies benefit from massive switching costs, long replacement cycles, and the critical nature of their products. When your entire business depends on network uptime, you don't experiment with unproven vendors.

XI. Bear vs. Bull Case & Investment Analysis

Bull Case:

The dominant installed base and switching costs create an almost impregnable moat. Cisco equipment runs in virtually every Fortune 500 company, government agency, and major institution globally. Replacing this infrastructure would cost billions and create massive operational risk. The switching costs aren't just financial—they're operational, educational, and cultural.

Enterprise relationships and trust built over decades cannot be replicated by competitors. When a CIO's job depends on network reliability, they choose the vendor with a 40-year track record, not the startup with marginally better technology. These relationships extend beyond purchasing decisions to strategic planning, with Cisco often consulted on multi-year technology roadmaps.

The successful software transition underway has already transformed Cisco's business model. With over 50% of revenue now recurring and $29 billion in ARR, Cisco has successfully pivoted from a hardware company to a software and services company. The Splunk acquisition accelerates this transition, adding $4.2 billion in high-quality recurring revenue.

The AI infrastructure opportunity could dwarf all previous growth drivers. As enterprises build out AI capabilities, they need massive networking infrastructure upgrades. Cisco's partnership with NVIDIA and its dominant position in data center networking position it perfectly to capture this spending.

Bear Case:

Cloud-native competition represents an existential threat. The hyperscalers—Amazon, Microsoft, Google—increasingly build their own networking equipment and software. As more workloads move to the public cloud, the addressable market for traditional networking equipment shrinks.

Hardware commoditization continues to erode margins. White-box switching, open-source routing software, and merchant silicon have commoditized much of the networking hardware market. Cisco's premium pricing becomes harder to justify when competitors offer 80% of the functionality at 50% of the price.

Still trading below 2000 peak after 24 years raises fundamental questions about growth potential. Despite growing revenue from $19 billion to over $50 billion, the stock remains below its dot-com peak. This suggests the market sees limited growth potential or continues to discount the company's transformation efforts.

Growth challenges in mature markets are structural, not cyclical. Enterprise networking spend is growing at low single digits. While Cisco can gain share, the overall pie isn't expanding rapidly enough to drive meaningful growth for a company of Cisco's size.

Disruption from software-defined networking threatens the core business model. SDN disaggregates hardware from software, allowing customers to use commodity hardware with sophisticated software overlays. This attacks Cisco's integrated platform strategy at its foundation.

XII. Power & Counter-Positioning

Network effects in enterprise standards create compounding advantages. Every Cisco installation makes the next one more likely. IT professionals trained on Cisco equipment prefer Cisco solutions. Third-party software vendors optimize for Cisco platforms. This creates a self-reinforcing cycle that's extremely difficult for competitors to break.

Switching costs and installed base power go beyond simple replacement costs. Enterprises have built decades of processes, configurations, and customizations around Cisco equipment. Their IT staff holds Cisco certifications. Their network monitoring tools are optimized for Cisco. Switching vendors means retraining staff, reconfiguring systems, and accepting operational risk—costs that dwarf the hardware savings.

The platform approach to networking transformed competition from product-by-product battles to ecosystem wars. Cisco doesn't sell routers or switches—it sells integrated platforms that solve business problems. This platform approach makes it nearly impossible for point-solution competitors to gain traction.

Counter-positioning against pure-play competitors leverages Cisco's breadth as an advantage. While Arista might have better data center switches and Palo Alto might have better firewalls, only Cisco can provide an integrated solution across all networking and security domains. For enterprises seeking single-vendor simplicity, Cisco remains the only viable option.

Why Cisco survived when others didn't comes down to three factors: customer focus, financial discipline, and cultural adaptability. While competitors like Nortel, 3Com, and Lucent collapsed or disappeared, Cisco maintained its customer relationships, managed its finances conservatively, and continuously evolved its culture to embrace new technologies and business models.

XIII. Lessons & Reflections

The dangers of valuation bubbles affect even great companies. Cisco's journey from $569 billion to $50 billion and back to $250 billion demonstrates that no company, regardless of quality, is immune to valuation excess. As Dr. Siegel noted, great companies are not exempt from perils of over-valuation, especially with P/E of 220. The lesson for investors: valuation always matters, eventually.

Acquisition as a core competency requires more than just capital. Cisco's success with M&A came from treating it as a strategic capability, not a financial transaction. The company developed processes for evaluation, integration, and retention that became as important as its technology development. Most companies fail at M&A because they focus on the deal, not the integration.

Platform transitions and timing separate winners from losers in technology. Cisco's successful transitions from routing to switching to software demonstrate the importance of cannibalizing yourself before others do. But timing matters—move too early and you abandon profitable businesses prematurely; move too late and you become irrelevant.

Building enduring B2B franchises requires different strategies than consumer businesses. While consumer technology companies can achieve rapid growth through viral adoption, B2B franchises are built through decades of trust, reliability, and relationship building. Cisco's durability comes from understanding that in enterprise technology, nobody gets fired for buying Cisco.

The infrastructure paradox reveals itself through Cisco's story: the companies that build the foundations of technological revolutions rarely capture the full value of those revolutions. Cisco built the internet's plumbing but watched as Google, Facebook, and Amazon captured most of the profits. Yet infrastructure companies endure long after the revolutionary companies have disappeared.

Perhaps the most profound lesson from Cisco's journey is about corporate resilience. The company survived the dot-com crash, the financial crisis, the cloud transition, and countless competitive threats. It did so not through any single strategy or technology, but through a combination of customer focus, operational excellence, and cultural adaptability that allowed it to evolve while maintaining its core identity.

As we look toward the future, Cisco faces its next existential challenge: remaining relevant in an AI-driven, cloud-native world. The company that once revolutionized networking must revolutionize itself once again. Whether it succeeds will depend not on its technology or market position, but on its ability to embrace change while maintaining the customer trust that has sustained it for four decades.

The Cisco story ultimately isn't about routers or switches or market capitalizations. It's about how a company can build something essential—the invisible infrastructure that powers the modern world—and evolve continuously while remaining true to its fundamental mission: making networks work. In an industry obsessed with disruption and revolution, Cisco's evolution demonstrates that sometimes the most radical act is simply to endure, adapt, and continue serving customers decade after decade.

For investors, entrepreneurs, and business leaders, Cisco offers a masterclass in building and sustaining a technology franchise. The company's journey from Stanford laboratory to global infrastructure provider demonstrates that true value creation comes not from capturing temporary trends but from solving fundamental problems in ways that become indispensable. Even at a $250 billion valuation, trading below its peak of 24 years ago, Cisco remains proof that in technology, as in life, the race goes not always to the swift, but to those who keep running.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube