Cirrus Logic: The Audio Silicon Story

I. Introduction & Episode Roadmap

Somewhere inside your iPhone—tucked in among the A-series processor, the modem, and the flash memory—is a chip you’ve probably never heard of. It’s the one that makes your speakers sound good, keeps your calls clear, helps Siri hear you in a noisy room, and turns tiny electrical signals into the audio and haptics you experience all day long.

That chip is likely from Cirrus Logic.

And Cirrus’s story is one of the strangest, most instructive arcs in modern semiconductors: a company that rode the PC wave, nearly got wiped out when audio became a commodity, spent years wandering without a clear identity, and then—almost unbelievably—became the audio nerve center for the most important consumer product on Earth.

This is the tale of how a once-struggling chipmaker found its edge by specializing harder, betting bigger, and building a relationship that transformed its business—while also tying its fate to a single customer. We’ll go from the messy early days, through the near-death experience, to the Apple inflection point that changed everything, and then into the question that still hangs over Cirrus today: what happens when your greatest strength is also your biggest risk?

I. Introduction & Episode Roadmap

Somewhere inside your iPhone—nestled among the A-series processor, the modem, and the flash memory—sits a chip you’ve never heard of. It’s behind the sound that pours out of your speakers, the clarity of your calls, what Siri can pick out in a noisy room, and even the subtle little tap you feel when you type.

That chip is likely from Cirrus Logic, and its story is one of the more improbable survival tales in semiconductors.

Cirrus Logic is an American fabless chip company that specializes in analog, mixed-signal, and audio DSP silicon. And today, its business is defined by one relationship: in 2025, Apple accounted for about 89% of Cirrus’s revenue—nearly nine out of every ten dollars coming from Cupertino. As of September 30, 2025, Cirrus had roughly $2 billion in trailing twelve-month revenue.

Which tees up the core question, and it’s almost absurdly simple: how did a company that was getting crushed in PC audio end up becoming Apple’s audio brain? And the scarier follow-up: is betting your entire future on one customer genius—or madness?

The truth, like most great business stories, is that it’s both.

Cirrus pulled off a dramatic reinvention—going from a sprawling, unfocused chipmaker that dabbled in everything from graphics to storage and networking into a lean specialist: premium audio silicon, built in lockstep with the most demanding product company on the planet. It didn’t happen cleanly. Along the way, Cirrus nearly ran out of road, shrank dramatically, and ultimately made a deliberate choice to hitch its fate to Apple.

For long-term investors, that choice creates the paradox. Cirrus has a highly profitable model—gross margins are expected to hold in the low-50% range. It throws off real free cash flow. It carries no debt and has around $700 million of net cash, or a bit over $12.50 per share. And yet the stock has long traded at a discount to many semiconductor peers, because Wall Street can’t get comfortable with the customer concentration risk.

So that’s what we’re digging into: is that discount a rational warning sign—or a misunderstanding of what Cirrus has actually built?

II. The Semiconductor Industry Context & Founding

Picture Salt Lake City in 1981. It’s quiet, landlocked, and about as far as you can get from Silicon Valley’s gravitational pull. But that’s where Suhas Patil—an Indian-American professor with a researcher’s résumé and an entrepreneur’s itch—decides to start a company.

Patil (born 1944) wasn’t a classic “silicon cowboy” chip founder. His career ran through academia and big-computing research: from 1970 to 1975 he was an assistant professor of electrical engineering at MIT, and while he was there he served as assistant director of Project MAC (Multi-Access Computer), one of the largest computer science labs in the U.S., known for its work on time-sharing systems. His work touched computer architecture, parallel processing, VLSI devices, and integrated circuit design. In other words: he wasn’t just thinking about chips. He was thinking about systems, and where computing platforms were headed.

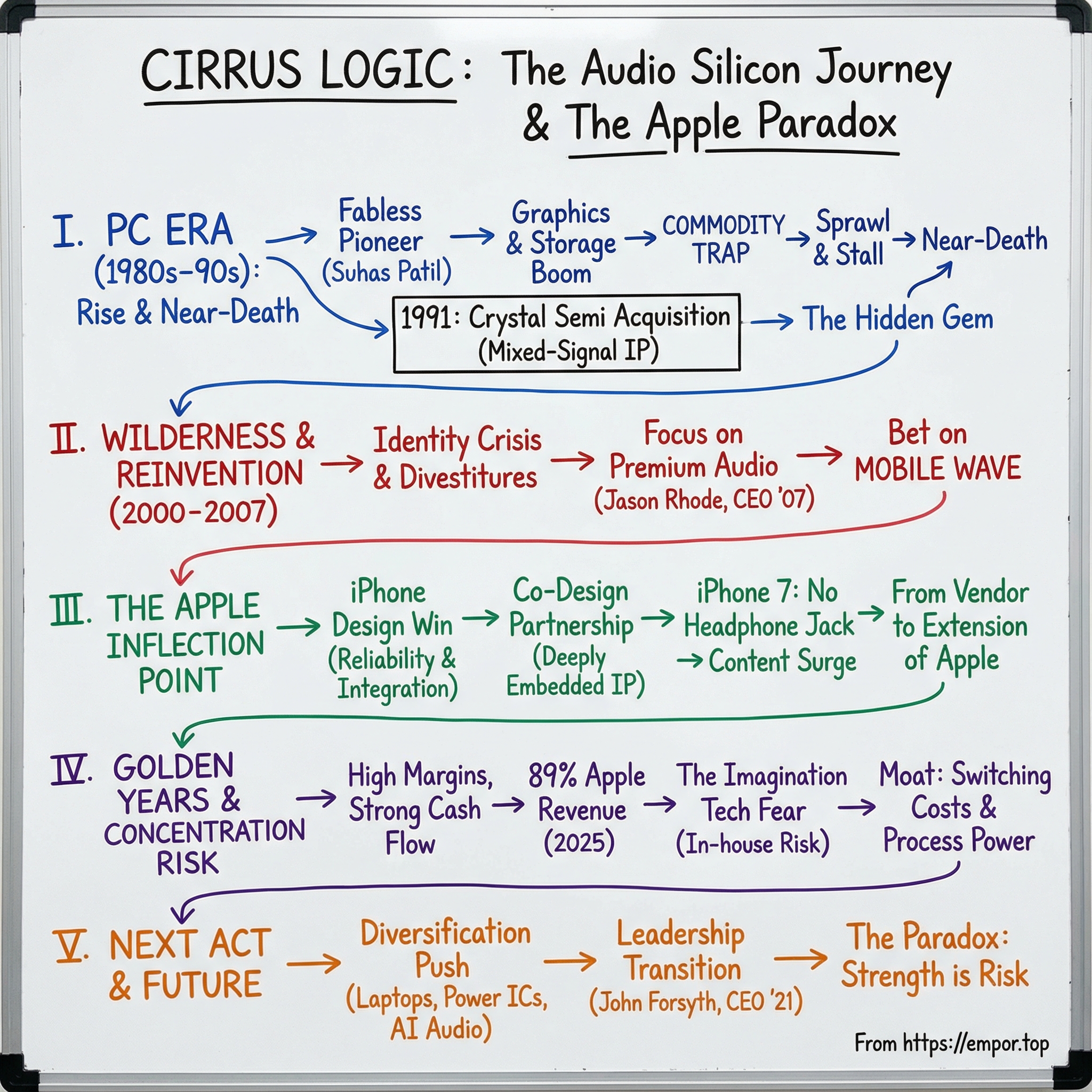

In 1981, Patil founded Patil Systems, Inc. Three years later, the company was renamed Cirrus Logic and moved to Silicon Valley. The bet wasn’t just on what to build—it was on how to build a semiconductor company at all.

Because in the early 1980s, the industry’s default model was brutally capital-intensive. Intel, Texas Instruments, and Motorola were integrated device manufacturers: they designed chips and owned the fabs that made them. If you wanted to compete, you didn’t just need great engineers—you needed to raise staggering sums to build a fabrication plant before you could sell your first unit.

Patil helped push a different idea: go fabless. Let specialized foundries in places like Taiwan and Japan manufacture chips on contract, while the company focuses on design and IP. Cirrus would become one of the earliest companies built around that model—an identity Patil carried forward as founder and later Chairman Emeritus.

In 1983, the company was reorganized by Patil, Kamran Elahian, and venture capitalist Fred Nazem, whose firm, Nazem and Company, provided the first startup round of financing. With the move to Silicon Valley in 1984, Cirrus aimed squarely at the exploding PC components market.

And the timing was perfect. The PC revolution was accelerating: IBM launched the Personal Computer in 1981, and by the mid-’80s, clone makers were churning out compatible machines at scale. Every PC needed key building blocks—graphics, sound, storage controllers—and Cirrus saw a wide-open field.

In January 1985, Michael Hackworth became president and CEO, a role he held until February 1999. In 1989, Cirrus joined the Nasdaq under the symbol CRUS. The IPO didn’t just fund the next phase—it validated the fabless playbook and gave Cirrus the currency to pursue acquisitions and expand its lineup.

Cirrus would later describe itself as having grown from a PC components startup into a global leader in low-power, high-performance mixed-signal processing for top mobile and consumer applications. But the through-line—the trait that helped it survive both booms and busts—was the fabless advantage: iterate quickly, keep capital needs low, and shift manufacturing risk onto partners.

Cirrus didn’t treat fabless as a convenience. It treated it as doctrine. As Hackworth put it in 1993: “We will never eliminate the fabless approach. The foundry thing has provided us with enormous flexibility that we would never ever have if we had to drag our own clean room for fabricating raw chips around with us.”

III. The PC Audio Era: Rise and Near-Death

In 1991, Cirrus made a deal that quietly rewired the whole company: it bought Crystal Semiconductor.

At the time, Cirrus was still best known for PC graphics. Crystal, based in Austin, was a very different animal. Founded in 1984 by Michael J. Callahan and James H. Clardy, it specialized in the unglamorous but essential guts of mixed-signal chips—digital-to-analog converters (DACs) and analog-to-digital converters (ADCs). In plain English: the silicon that translates between the messy, continuous real world and the crisp, binary world computers live in.

And audio is the perfect mixed-signal problem. Your voice, music, and everything you hear are analog waves. Computers store, process, and transmit digital samples. The bridge between those worlds is where Crystal excelled—and where Cirrus, after the acquisition, suddenly had a real edge.

Cirrus acquired Crystal in 1991 for roughly $59 million. In hindsight, it became one of the most important moves in the company’s history. Crystal didn’t just add a product line; it injected the mixed-signal expertise that would eventually define Cirrus, turning audio from a side business into the company’s center of gravity in the years that followed.

In the early 1990s, though, the story still looked like “Cirrus the PC chip supplier.” The company shipped low-cost graphics chips that powered huge numbers of Windows machines, plus audio converters and magnetic storage components. Its 2D Windows accelerators were competitive at the low end—often outperforming rivals like Oak, Trident, and Paradise (Western Digital). A chip like the Cirrus GD5422 in 1992 supported hardware acceleration in both 8-bit and 16-bit color, which mattered when every frame you could squeeze out of a budget PC was a selling point.

Then the industry moved fast—and Cirrus didn’t move fast enough.

By the mid-1990s, as PCs migrated to the PCI bus, Cirrus started falling behind companies like S3 and Trident. When the GD5470 “Mondello” slipped past its announced release date, it wasn’t just a missed product cycle. It dented Cirrus’s credibility in a market that punished hesitation.

The graphics business turned brutal as competition intensified—Nvidia, ATI, and others raised the bar and compressed margins. And instead of leaning into the flexibility that had made Cirrus successful, the company did something almost philosophically backwards: it tied itself to big, capital-heavy manufacturing bets. In 1995, Cirrus agreed to a $600 million joint manufacturing venture with AT&T Microelectronics. For a company that had preached the gospel of staying fabless, that was a self-inflicted weight vest.

The late 1990s became a cascade of problems: slow product development, bad investments, and too much capacity locked up in fabrication ventures. Cirrus began reorganizing in 1996, and restructuring charges helped push the company to a loss of $46.2 million on revenue of $917.2 million. In early 1997, it announced plans to cut 400 jobs.

It was the classic sprawl-and-stall failure mode. Cirrus was trying to play too many games at once—graphics, audio, networking, magnetic storage, video encoding—without establishing a durable advantage in any of them. The unwinding took years. It exited the PC graphics card business in 1998. In 2003, it closed its wireless networking operations. One by one, the side quests got shut down.

The PC era taught Cirrus a lesson the hard way: in commodity markets, being “pretty good” is a fast path to irrelevance. When competition gets fierce and differentiation evaporates, the business becomes a death spiral—lower margins, weaker R&D, slower products, more share loss, repeat.

Cirrus survived. But by the time the dust settled, the company that emerged had been forced to confront an uncomfortable truth: flexibility is only an advantage if you actually use it—and focus is the only way to win markets that won’t forgive mistakes.

IV. The Wilderness Years: Searching for Identity

Between 2000 and 2007, Cirrus Logic drifted through a corporate identity crisis. The company had survived the PC-era shakeout, but survival isn’t the same thing as a strategy. Cirrus knew it had to change. It just couldn’t yet articulate what it wanted to become.

David D. French arrived in June 1998 as president and chief operating officer, and he was named CEO in February 1999. After he stepped in, Cirrus leaned on acquisitions to reposition itself as a supplier of high-performance analog and digital processing chips for consumer entertainment electronics.

French did bring order to the chaos. In April 2000, Cirrus announced it had completed moving its headquarters to Austin, Texas. And as the years went on, management kept stripping away businesses that no longer fit. In June 2005, Cirrus sold its video products operation to an investment firm, which became privately owned Magnum Semiconductor. More divestitures followed, as Cirrus tried to get lighter, simpler, and more coherent.

But clarity still didn’t arrive. Cirrus was selling audio chips into professional gear, home theater receivers, and portable devices—good markets, but scattered. The company kept making moves without a unifying “why.” In 2001, Cirrus bought Peak Audio, picking up CobraNet distributed audio. Around the same time, it announced plans to begin exiting the magnetic storage chip business.

The technical foundation was there. The mixed-signal DNA inherited from Crystal remained a real asset, and the broader market was starting to hint at where the next wave would come from. Premium portable audio was exploding as the world shifted from dedicated MP3 players toward phones that did everything. Cirrus could see the opportunity—but it was still spreading itself across industrial, automotive, energy metering, and consumer applications, without landing a breakout win that could pull the whole company into focus.

That turning point came in May 2007.

Jason Rhode, Ph.D., was appointed president and CEO, and a director of the company. Unlike many turnaround CEOs, Rhode wasn’t an outsider. He joined Cirrus in 1995 and worked his way up through engineering and product leadership—director of marketing for analog and mixed-signal products in 2002, then vice president and general manager of mixed-signal audio products in 2004. He held a B.S. in electrical engineering from San Diego State University, plus M.S. and Ph.D. degrees in electrical engineering from North Carolina State University.

Rhode was an engineer’s engineer—someone who understood what Cirrus actually did well, and what it didn’t. He had already overseen a revitalization of Cirrus’s portfolio of analog and mixed-signal converter ICs for consumer and professional audio markets. Now, as CEO, he brought a thesis that was both simple and bracing: stop trying to be all things to all customers. Pick the highest-value audio problems in the world, and become essential to the companies solving them.

Rhode’s bet was that the next platform shift wasn’t going to be about PCs at all. It was going to be about phones. As smartphones absorbed the jobs of music players, camcorders, and voice recorders, audio stopped being a checkbox feature and became a product differentiator—especially at the premium end. And if that was true, then the company that could deliver great sound, low power, tight integration, and consistent reliability wouldn’t just sell chips. It would help define the experience.

Cirrus finally had a direction. The only question was whether it could turn that direction into the one relationship that would change everything.

V. The Apple Inflection Point: The Bet That Changed Everything

The story of how Cirrus Logic won Apple’s business starts with the incumbent Apple trusted first—and then slowly stopped trusting.

For years, that supplier was Wolfson Microelectronics, a Scottish chip company whose audio codecs showed up all over the golden age of portable media: Microsoft’s Zune line, Cowon MP3 players, Sony’s PSP, even products like the Logitech Squeezebox Duet and the PalmOne Treo. And crucially, Wolfson provided the codec functionality for much of Apple’s iPod lineup, and carried that relationship into early versions of the iPhone and iPod touch.

But Apple doesn’t do “good enough.” As iPods and iPhones got thinner and more tightly packed, audio stopped being just a spec—it became a mechanical and power-management problem. The codec wasn’t simply about sound quality anymore. It had to fit inside an impossibly small box, sip power, behave perfectly across millions of units, and leave room for everything Apple cared about more: battery, display, radios, antennas.

That’s where Cirrus found the crack in the wall.

With the 6th generation iPod Classic and the 2nd generation iPhone, Cirrus replaced Wolfson. The reason wasn’t marketing. It was a very specific technical win: Cirrus offered Apple a codec design that eliminated two large physical capacitors.

That may sound like a footnote, but inside Apple it’s the kind of detail that changes a product. Every millimeter of board space is fought over. Big capacitors can be electrically elegant, but they’re physically expensive. Cirrus’s engineers built an architecture that delivered comparable audio performance while shrinking the footprint—and when you’re trying to shave thickness or squeeze in more battery, that’s not incremental. That’s decisive.

Once Cirrus had a foothold, the relationship broadened. In 2012, Apple added Cirrus’s first digital amplifiers into the iPhone and other devices. From there, Cirrus codecs and amplifiers spread across almost all of Apple’s product lines.

Just as important as the silicon was the way Cirrus fit into Apple’s operating model. Apple wanted reliability, secrecy, and a partner that could move at Apple speed. Cirrus delivered—and over time, the companies’ intellectual property became deeply intertwined through collaboration.

There’s a detail here that explains the real dynamic: you don’t get to open an Apple device and find a chip proudly labeled “Cirrus Logic.” Cirrus provides Apple with IP, engineering, and hardware that ships with Apple part numbers. Apple is in complete control.

That’s what “in the supply chain” actually meant. Cirrus wasn’t selling a commodity component. It was co-designing custom silicon to Apple’s exact acoustic requirements, power budgets, and form factors. And that kind of integration creates switching costs that have nothing to do with price. It’s about risk, validation cycles, and the brutal reality that changing a deeply embedded part can ripple through the entire product.

As Apple’s volumes surged, Cirrus surged with it. From around 2010 to 2014, Cirrus’s revenue took off as the iPhone became the defining consumer electronics product of the era. By the time the iPhone 7 cycle rolled around, Pacific Crest Securities would refer to Cirrus Logic as “likely the biggest winner in the iPhone 7.”

But the better the bet worked, the louder the downside became. On analyst calls, the same question kept coming back: what happens if Apple drops you?

Rhode’s answer was consistent, and in its own way, ruthless: the best defense is to be excellent. Don’t try to diversify your way out of dependence in a hurry. Instead, make yourself operationally indispensable. Stay two generations ahead. Solve problems before Apple has even fully framed them. Make switching feel less like a purchasing decision and more like a product risk Apple would rather not take.

VI. The Golden Years: Peak Apple Dependency

When Apple launched the iPhone 7 in September 2016, Cirrus Logic hit something like a high-water mark. Apple made the decision everyone argued about for months: it killed the 3.5mm headphone jack. And for Cirrus, that “controversial change” looked an awful lot like a new silicon surface area opening up overnight.

Before the iPhone 7, a huge chunk of the headphone ecosystem was basically a free ride from the perspective of chip content. A dumb analog connector. No interface device. No conversion circuitry in the accessory. Then Apple shifted the entire experience to Lightning—meaning adapters, Lightning headphones, microphones, and earphone drivers suddenly needed real electronics to do the job the jack used to do.

As Cirrus put it at the time:

"It's pretty rare that there exists one-plus billion unit market out there that traditionally has zero silicon content and suddenly has a strong reason to have an interface device and some level of conversion circuitry and earphone drivers and microphone pickups and whatnot. So that's a really remarkable opportunity and we're very well situated to capitalize on that."

Inside the phone itself, the changes were just as telling. According to Chipworks, Apple reused the same audio codec from the prior-generation iPhone 6s. But Cirrus’s content still grew: the number of audio amplifiers inside the device increased from two in the iPhone 6s to three in the iPhone 7.

Analysts ran the numbers and came to the same conclusion: Cirrus was becoming more valuable per iPhone. Pacific Crest estimated the iPhone 7 and 7 Plus carried about $2.50 in additional chip content per device versus the iPhone 6s. When you’re shipping into a product line that does well over 200 million units a year, a couple extra dollars of content isn’t a footnote. It’s the whole ballgame. Cirrus’s stock responded accordingly.

But the “golden years” came with a shadow. The deeper Cirrus got embedded, the more the business started to look less like a diversified semiconductor company and more like a specialized extension of Apple’s hardware roadmap.

Apple’s share of Cirrus’s revenue kept climbing—79% in fiscal 2022, 82% in fiscal 2023, and 87% in fiscal 2024. Efforts to diversify helped at the margins, but they didn’t change the reality. Yes, Cirrus showed up in Android flagships. Yes, it sold into home theater and professional audio. But those markets didn’t pay Apple-like ASPs, and they didn’t come close to Apple-like scale.

And that kept the same uncomfortable question front and center on Wall Street: what happens if Apple decides to design its own audio chips?

For investors, the cautionary tale was always sitting there in the background, unspoken but obvious: Imagination Technologies.

VII. The Reality Check: Navigating Platform Transitions

The Imagination Technologies debacle gave Cirrus Logic investors a live-action horror story.

In April 2017, Imagination—the U.K. chip designer whose GPU technology had powered Apple’s A-series graphics for years—said Apple would stop using its intellectual property in future products. The market didn’t wait around for details. Imagination’s shares plunged by roughly two-thirds in a day. Analysts called it out plainly: the biggest risk in the entire business model had just been realized.

Imagination wasn’t some replaceable vendor. It had been deeply embedded in Apple’s chips for nearly a decade. Apple was also a major customer, representing about half of Imagination’s revenue, and even held an 8% stake. None of that mattered when Apple decided it wanted to own its own graphics destiny. Imagination, suddenly missing its economic engine, had no real option except to put itself on the auction block. Later that year it was acquired by Canyon Bridge, backed by state-owned China Reform, for $686 million.

If you owned Cirrus stock, it was impossible not to see yourself in that mirror.

If Apple could bring a GPU in-house—arguably the most complex block in a smartphone after the main processor—why wouldn’t it do the same for audio? Why keep paying an outside supplier when you could just hire the engineers and own the IP?

Cirrus management’s message was calm, and very specific: yes, it was technically possible. But they argued it wasn’t economically rational.

The logic went like this. GPUs are a marquee differentiator and a massive piece of the iPhone’s compute budget, worth a sustained in-house investment. Audio codecs and amplifiers, while critical to user experience, are a much smaller slice of the bill of materials—and they live in a specialized corner of engineering. High-quality mixed-signal design is hard to staff, hard to validate, and hard to get right at Apple’s scale. It’s not just “make the sound good.” It’s ultra-low power, low latency, tiny footprint, consistent performance across huge volume, and an analog-to-digital interface that behaves perfectly in the real world.

But even if management was right, the market didn’t grant Cirrus the benefit of the doubt. The Imagination precedent helped lock a discount into Cirrus’s valuation. Miss a quarter or guide conservatively and investors would jump straight to the worst-case narrative. The stock could swing dramatically on earnings—not always because the long-term business changed, but because confidence in the Apple relationship was so brittle.

And the numbers weren’t exactly comforting. Cirrus’s revenue moved with iPhone cycles, and the company didn’t have another engine large enough to smooth that ride. In fiscal 2024, revenue was $1.789 billion, down from $1.898 billion in fiscal 2023. When Apple demand softened or content shifted, Cirrus felt it immediately—and disproportionately.

Management kept saying the same thing: diversification takes time, and we’re working on it. On calls, the tone was patient. On Wall Street, patience was wearing thin. Was “trust the process” a real strategy—or just what you say when you don’t have a second act yet?

VIII. The Next Act: Beyond Smartphones

By the 2020s, Cirrus’s push to diversify stopped being a vague aspiration and started looking like an actual plan—just one that still lived in the long shadow of the iPhone.

The most obvious “next” market was laptops. If Cirrus could become indispensable in phones by making small devices sound great on tiny power budgets, why not take the same playbook to a category that had famously treated speakers as an afterthought?

That’s the logic behind Cirrus’s effort to get designed into mainstream PCs. The company announced a partnership with Intel and Microsoft to develop a new audio system for future Intel-based laptops—aimed at materially better audio fidelity while protecting battery life. The building blocks are classic Cirrus: high-efficiency power converters, smart amplifiers, and a Hi-Fi audio codec, packaged into a reference design that OEMs can adopt. The work is tied to Intel’s upcoming Lunar Lake series of low-power mobile CPUs.

Cirrus also pointed to real traction here, highlighting that it secured its first high-volume mainstream design win for its latest PC codec, and began shipping its first power product across multiple tier-one laptop makers. The ambition is straightforward: as premium Windows laptops increasingly compete head-to-head with MacBooks, better audio becomes one more spec customers can actually feel—and one more place Cirrus can earn meaningful content per device.

Management framed this broader push as a bet on an expanding opportunity set. Cirrus projected its Served Addressable Market would grow from $6.8 billion in 2025 to $8.5 billion by 2029, with laptops alone representing roughly $1.2 billion of that by 2029. In other words: smartphones were still the core, but the company was trying to build a second pillar that was large enough to matter.

Then there was diversification that wasn’t “audio in a new form factor,” but an outright adjacency. In 2021, Cirrus announced it would acquire Lion Semiconductor, a California-based company, for $335 million in cash. The rationale was about power, not sound: Lion brought intellectual property and products for power applications in smartphones, laptops, and other devices—specifically fast-charging technology built on switched-capacitor architectures. As charging became faster and more complex, power management stopped being a commodity add-on and started looking like another premium mixed-signal problem Cirrus could tackle.

Cirrus was also broadening what it sold into phones themselves. John Forsyth, Cirrus Logic’s president and CEO, described a pipeline that included a third-generation camera controller, new laptop products, and next-generation custom audio components—like a boosted amplifier and the company’s first 22-nanometer smart codec—alongside continued investment in future IP. The camera controller line, in particular, was a signal of intent: use mixed-signal expertise to move into adjacent, high-value blocks that ride the same consumer device cycles.

And even inside the Apple relationship—the one Cirrus could never really escape—the company looked for more places to expand content. In 2018, Cirrus signed an agreement with Apple for an active noise reduction chip for next-generation AirPods. The appeal was obvious: every new Apple product category that shipped in volume created another surface area for Cirrus silicon, beyond the iPhone.

But the honest assessment stayed sobering. In 2025, Apple still accounted for about 89% of Cirrus’s revenue. After years of effort, the concentration problem hadn’t gone away. In some ways, it had gotten worse—proof that building “beyond smartphones” is possible, but building something big enough to dilute Apple is an entirely different challenge.

IX. The Business Model Deep Dive

To understand how Cirrus Logic makes money, you have to understand what it really sells Apple. It’s not a boxed, off-the-shelf chip. It’s a multi-year co-design process that turns Cirrus into something closer to an external extension of Apple’s hardware engineering team.

Unlike commodity suppliers who wait for a spec sheet and then bid on price, Cirrus typically gets pulled in years before a product ever ships. Apple shares the targets—acoustic performance, physical constraints, power budgets, and all the non-negotiable realities of building millions of devices that have to work perfectly. Cirrus responds with architectures that can actually hit those targets. And when the design locks, the parts ship with Apple part numbers and are built exclusively for Apple.

Cirrus has built a broad portfolio to support that model: custom, semi-custom, and general-market ICs across smart codecs, camera controllers, haptic driver and sensing solutions, and boosted amplifiers—paired with the software, tools, and algorithms needed to make the silicon behave the way the product team intended. The point isn’t just to deliver a chip. It’s to deliver a subsystem that helps Apple differentiate the experience.

That co-design approach creates real switching costs in both directions. For Apple, swapping out a deeply integrated audio or mixed-signal component isn’t like changing a memory supplier. It can mean multi-year qualification cycles, acoustic rework, and the kind of operational risk Apple hates. For Cirrus, of course, the stakes are even higher. Losing Apple wouldn’t be a setback. It would be an existential event.

When this model is working, the economics are attractive. Cirrus expects gross margins to hold roughly in the low-50% range—about 51% to 53%—because it’s being paid for engineering and integration, not for being the lowest-cost producer of a generic part.

That’s also why Cirrus spends so aggressively on R&D. It runs around 20% of revenue, because staying in the room with a customer like Apple requires being ahead of the next set of requirements, not catching up to the last one. The company has emphasized investment in high-performance mixed-signal technologies, and noted that more than two-thirds of its new patent filings in calendar 2024 were in that area. Overall, Cirrus reported about 4,260 pending and issued patents worldwide.

The fabless model then shows up in capital allocation. With no factories to build or maintain, operating profit tends to convert efficiently into free cash flow. In the quarter discussed, free cash flow was $87.7 million. Cirrus repurchased 362,000 shares for $40 million that quarter, and as of September 27, 2025, it had $414.1 million remaining under its existing repurchase authorization. The company has generally favored buybacks over dividends, steadily shrinking the share count over time.

Finally, there’s the balance sheet—and it’s intentionally conservative. Cirrus maintained around $700 million of net cash, more than $12.50 per share, and carried no debt. That gives it protection against the revenue volatility that comes with Apple-driven product cycles, and it leaves the door open to do acquisitions when the right adjacent technology comes along.

X. Strategic Analysis: Porter's 5 Forces

Threat of New Entrants: LOW

If you want to compete with Cirrus where it actually makes its money—premium, tightly integrated mixed-signal audio—the front door is basically locked.

Start with the obvious: the IP. Cirrus has about 4,260 pending and issued patents worldwide. That doesn’t make it invincible, but it does mean a new entrant isn’t just building a chip. They’re building a chip while tiptoeing through a patent minefield and assembling deep analog and mixed-signal know-how that takes years to accumulate.

But the bigger barrier is trust. In premium audio, the product is the relationship. Apple doesn’t take flyers on unproven suppliers for flagship devices. Qualification cycles can run around three years, and even after that, Apple would be taking on real switching costs—revalidating performance, reliability, manufacturing, and integration across a system that’s already been tuned end-to-end.

Bargaining Power of Suppliers: MEDIUM

Cirrus is fabless, which means it lives and dies by the foundry ecosystem—primarily TSMC. That sounds scary until you remember it’s not unique. Nearly every major fabless chip company is standing in the same line.

So suppliers have leverage, but it’s not a one-way street. Cirrus matters, but it’s not big enough to dictate terms the way a top-tier CPU or GPU customer might. The result is a fairly balanced dynamic: meaningful dependency, but not a uniquely fragile one.

Bargaining Power of Buyers: VERY HIGH

This is the force you can’t talk around, because it defines the entire Cirrus story.

In 2025, Apple represented about 89% of Cirrus’s revenue. That gives Apple the power to press on pricing, steer development priorities, and—at least in theory—move the business elsewhere.

And yet, the relationship isn’t just a procurement exercise. Apple uses audio as a real product differentiator across iPhone, AirPods, and HomePod, and it needs silicon that can hit brutal constraints on power, size, and performance at enormous scale. Cirrus has been delivering that for more than 15 years. So yes, Apple has the leverage—but Apple also has a strong incentive not to break what’s working.

Threat of Substitutes: MEDIUM

The nightmare scenario is Apple pulling an Imagination Technologies and deciding it wants to own the stack—designing audio processing in-house and integrating away the supplier.

Apple does integrate vendors out at times, but the easiest targets tend to be areas where functionality can be replicated with broadly available software or more general-purpose approaches.

Cirrus’s protection is that mixed-signal is not software. Analog design doesn’t scale the way digital engineering does. It’s specialized, experience-heavy work, and it can be painfully hard to staff and validate. Apple could absolutely do it if it chose to—but it would need to recruit, build, and retain a niche bench of talent for something that’s still a relatively small slice of the iPhone’s overall cost structure.

Competitive Rivalry: MEDIUM-HIGH

At the very top end—where Cirrus is effectively co-designing into Apple’s systems—there aren’t dozens of credible rivals. But that doesn’t mean the competitive pressure disappears.

Cirrus competes against much larger analog and mixed-signal players like Texas Instruments, Analog Devices, Infineon, STMicroelectronics, and Skyworks. And in the more commodity parts of audio, low-cost competitors—especially in China—can turn pricing into a knife fight. Cirrus generally doesn’t try to win that game. Its strategy has been to stay where integration, performance, and trust matter more than being the cheapest line item on a BOM.

XI. Strategic Analysis: Hamilton's 7 Powers

1. Scale Economies: MODERATE

Cirrus does get leverage from scale, mostly by spreading heavy R&D across massive unit volumes—especially the iPhone, which ships in the hundreds of millions per year. But it’s a very particular kind of scale: it’s not “the whole market runs on Cirrus,” it’s “one customer runs at a scale almost no one else can match.” If Apple’s volumes soften, Cirrus can’t magically redeploy that same R&D base across a bunch of other customers overnight.

2. Network Effects: NONE

There’s no user network here, no marketplace flywheel, no “more users makes the product better.” This is straight B2B silicon.

3. Counter-Positioning: NONE

Cirrus didn’t win by attacking an incumbent with a new business model. It won the old-fashioned way: better engineering, better execution, and the willingness to co-design deeply with a demanding customer. The unusual part isn’t how it competes—it’s how concentrated the payoff became.

4. Switching Costs: STRONG

This is the heart of the Cirrus moat. Over years of collaboration, Cirrus and Apple built tightly interlocked designs and shared assumptions—IP, validation routines, acoustic targets, mechanical constraints, and the thousand small details that don’t show up in a datasheet. Add in long qualification cycles, custom integration, and the accumulated trust that comes from shipping at Apple scale, and switching stops being a sourcing decision. It becomes a high-stakes engineering project. Apple can switch, but it would take real time and carry real product risk.

5. Branding: WEAK

Cirrus is essentially invisible to the end customer. You don’t buy an iPhone because it has “Cirrus inside,” and you won’t find Cirrus branding on the silicon in Apple devices. Whatever reputation Cirrus has, it lives inside engineering orgs and supply-chain relationships—not in consumer minds.

6. Cornered Resource: MODERATE

Cirrus’s most valuable resource isn’t a patent portfolio alone—it’s the relationship itself. After roughly fifteen years working with Apple, Cirrus has institutional knowledge about Apple’s acoustic requirements, internal processes, and operational expectations that a competitor can’t reproduce without access. And access is the scarce commodity.

7. Process Power: STRONG

Cirrus has built a repeatable way of working with Apple: how to engage early, iterate fast, meet secrecy requirements, hit launch timelines, and survive the brutal reality of mass production. That process advantage compounds. It’s hard to copy because it isn’t just a playbook—it’s years of lived experience inside Apple’s development cadence.

Overall Assessment: Cirrus has real power, but it’s fragile. Switching costs and process power create a defensible position, yet the same concentration that strengthens the moat also creates existential risk. Cirrus is extremely valuable as long as Apple keeps needing what it does—while controlling far less of its destiny than most companies would ever accept.

XII. Bull vs. Bear Case

🐂 Bull Case:

The bull case on Cirrus starts with a simple claim: the market is pricing the company like it’s living on borrowed time, while the actual business looks more like a long-running co-design partnership that keeps expanding.

First, content per device can still rise. Even in a mature smartphone market, Cirrus doesn’t need iPhone units to explode if it can keep earning more “surface area” inside each generation—smart codecs, boosted amplifiers, haptic drivers, and newer categories like camera controllers. The bet is that Apple keeps pushing for better sound, better capture, better feel, and more integration—and Cirrus keeps being the team that can ship it.

Second, the Apple relationship may be more durable than it looks on a spreadsheet. After roughly fifteen years of working together, Cirrus isn’t just a vendor; it’s part of the development cadence. That history creates real switching costs, not because Apple can’t find another chip company, but because replacing a deeply integrated mixed-signal subsystem is slow, risky, and hard to validate at Apple scale.

Third, diversification is showing signs of life. It’s not a clean “second iPhone,” but management has pointed to meaningful progress in PCs, including its first mainstream consumer laptop design win and expanding work with major PC platform partners. If Cirrus can turn laptop audio and power into a repeatable playbook, it becomes a real incremental growth engine.

Fourth, bulls argue the valuation doesn’t match the quality of the model. This is a high-margin, fabless company with strong cash generation and a fortress-like balance sheet, yet it often trades at a discount to peers largely because investors can’t get past the customer concentration.

🐻 Bear Case:

The bear case is less about whether Cirrus executes well, and more about whether execution even matters when one customer holds the keys.

First, Apple designing in-house is the existential risk. The Imagination Technologies example is the nightmare fuel: after Apple signaled it would stop using Imagination’s IP, the stock collapsed and the company was effectively forced into a sale. The warning is obvious: if Apple ever decides it wants to own audio and mixed-signal the way it chose to own graphics, Cirrus doesn’t have a comparable backup engine.

Second, diversification has been the promise for years, and the scoreboard still reads “Apple.” In 2025, Apple represented about 89% of Cirrus’s revenue—higher than it was five years earlier, not lower. Bears see that as evidence that “we’re working on it” is not the same as escaping the gravitational pull.

Third, smartphone maturity caps the upside. Even if Cirrus adds more content per device, the iPhone is not a unit-growth story anymore. Flat or declining volumes can turn what looks like a great socket into a ceiling.

Fourth, geopolitical exposure adds another layer of uncertainty. Cirrus has cited that roughly half of its revenue is generated in China, which means export controls, supply chain shifts, and broader China–Taiwan tensions can all show up as real business risk, even if demand stays strong.

What to Watch:

For long-term investors evaluating Cirrus Logic, three metrics matter most:

-

Apple Revenue Percentage: The only way to de-risk this story is for non-Apple revenue to grow faster than Apple revenue. Watch whether the percentage trends down meaningfully over multiple years.

-

Gross Margin Stability: Gross margins are expected to stabilize between 51% and 53%. Stable or expanding gross margins indicate Cirrus is being paid for integration and performance, not squeezed like a commodity supplier. Declining margins would be a warning sign.

-

Content per Device Growth: If iPhone units are flat, content becomes the growth lever. Watch for evidence that newer categories—camera controllers, haptic drivers, and power ICs—are turning into durable, repeatable content inside the platform.

XIII. Lessons for Founders & Investors

Cirrus Logic’s story is a bundle of lessons that feel wrong at first—and then start to look inevitable once you understand what the company actually built.

The Concentration Paradox: Sometimes betting big on one customer is rational. The default advice is to diversify so no single buyer can sink you. Cirrus did the opposite and, for long stretches, got stronger because of it. The real variable wasn’t the number of customers—it was the depth of the relationship. A true partnership with the world’s most demanding customer can create switching costs that a wider but thinner customer list simply can’t.

Quality Over Diversification: It’s better to be excellent for one than mediocre for many. Cirrus could have clung to PC graphics, magnetic storage, and networking. Instead, it exited, sold, and trimmed until there was enough focus to become genuinely great at premium audio. That’s what turned “we also do audio” into “we define the audio experience” for the biggest product line in the world.

Moats in B2B: Switching costs and process power take years, not quarters. Cirrus’s moat didn’t come from one miracle chip. It compounded over roughly fifteen years of co-design, quiet execution, and shipping reliably at massive scale. Even a technically capable competitor can’t shortcut trust, validation history, and the muscle memory of working inside a customer’s cadence.

The Fabless Advantage: Capital efficiency buys you time to survive and iterate. Cirrus nearly broke in the 1990s, but it didn’t have giant fabs forcing it to keep running a bad strategy just to cover fixed costs. The fabless model kept the company light enough to restructure, pivot, and keep swinging until it found the right problem to solve.

Strategic Patience: Rhode’s long bet took conviction. When Jason Rhode became CEO in 2007, Cirrus was still cleaning up the past, and the Apple relationship was early. The premium smartphone era hadn’t fully arrived yet. Cirrus’s transformation required sticking with a direction long enough for it to compound—through years where the market would have preferred a faster, safer-looking story.

The Valuation Discount: Wall Street hates concentration, even when the economics are great. Cirrus has often traded at a discount to semiconductor peers despite strong margins and cash generation because investors can’t unsee the dependence on Apple. For long-term investors, that discount can be either a permanent warning label—or an opportunity, if you believe the relationship is more durable than the market assumes.

XIV. Epilogue & Future Outlook

In January 2021, Cirrus Logic handed the keys from its longtime CEO, Jason Rhode, to John Forsyth. Rhode stepped down as chief executive officer and director, and the board appointed Forsyth—then 47 and Cirrus’s president—to take over as president and CEO effective January 1, 2021.

Forsyth wasn’t a stranger parachuting in. He’d been named president in January 2020, and he joined Cirrus in 2014 through the acquisition of Wolfson Microelectronics—the same Wolfson that once held Apple’s codec socket before Cirrus took it over. It’s a neat bit of symmetry: the company Rhode rebuilt around Apple was now being led by an executive who arrived through the purchase of Apple’s former supplier.

The transition signaled continuity more than reinvention. Forsyth had been deeply involved in product strategy during the years Cirrus expanded beyond codecs into amplifiers, power, and other mixed-signal content. He also inherited the same central tension Rhode spent years managing: Apple was still the engine, and reducing dependency on that engine would take time.

As Forsyth put it:

"Today, we reflect on our 40-year journey from a visionary fabless startup to a global leader in mixed-signal solutions," said John Forsyth, CEO of Cirrus Logic. "Our success is built on the dedication and innovation of our talented team, the trust of our customers, and the support of our shareholders. We remain committed to pushing the boundaries of what's possible, driving excellence, and delivering value."

Looking ahead, Cirrus’s opportunity set is being shaped by a handful of big, durable trends. One is AI audio: voice interfaces, ambient computing, and spatial audio. If computing is moving toward systems that listen, interpret, and respond in real time, that puts more weight on the messy edge where microphones, speakers, power, and mixed-signal processing have to work flawlessly.

Another is the push into new device categories—laptops, wearables, and automotive. The company’s challenge isn’t whether these markets exist. It’s whether Cirrus can build meaningful revenue streams there while still funding the relentless R&D it needs to stay ahead in its core Apple-driven business.

Mixed reality is a particularly intriguing wildcard. Devices like Apple’s Vision Pro—and competing platforms—lean heavily on sophisticated spatial audio, which plays directly into Cirrus’s strengths. Automotive is the opposite: slower cycles, longer qualification, less drama quarter-to-quarter, but potentially durable demand as premium vehicles keep pushing for better sound and more advanced in-cabin experiences.

And then there’s the human side of the story: succession. Forsyth has been CEO since 2021, and Cirrus has continued to execute, but the question doesn’t go away—it just moves forward in time. Eventually, Cirrus will need to prove that the culture and the strategy aren’t a single-CEO phenomenon.

Could Cirrus be acquired? In theory, its strategic importance—especially to Apple—makes it tempting. In practice, the very thing that makes it valuable is also what makes it complicated. Apple buying a key supplier could invite regulatory scrutiny and create integration headaches. And for any other would-be acquirer, the customer concentration that defines Cirrus would look less like a prize and more like a risk you inherit.

The most honest reflection is that Cirrus has succeeded by doing the thing MBA textbooks warn you not to do. It concentrated rather than diversified. It went deep with one customer instead of spreading risk across many. It built a business around switching costs and process integration, not around maximum optionality.

For forty years, that contrarian approach worked. The next forty will reveal whether it was enduring strategy—or simply the right bet, made at the right time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube