Corsair Gaming: From Memory Modules to Gaming Empire

I. Introduction and Episode Roadmap

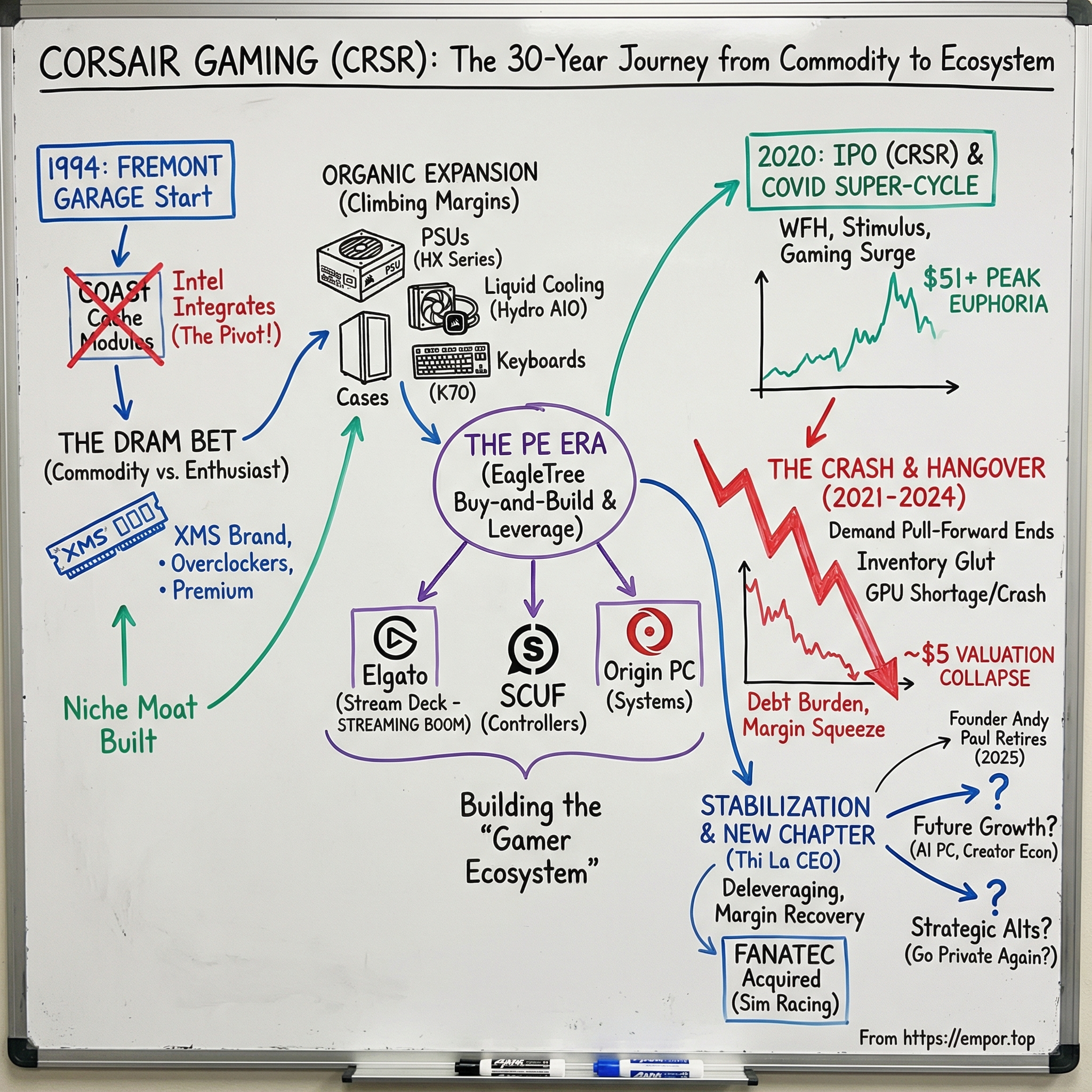

Picture a Fremont, California garage in 1994. Three engineers are staring at a commodity so boring it makes accountants yawn: cache memory modules. Thirty-one years later, the company they built would be worth over a billion and a half dollars at its peak, powering every touchpoint of the modern gaming setup, from the RAM inside your rig to the Stream Deck controlling your Twitch broadcast to the sim racing wheel gripped by Formula 1 fans worldwide. That company is Corsair Gaming.

Corsair is one of those rare hardware companies that somehow built a brand in a business where brands are supposed to be irrelevant. Try explaining to a non-gamer why someone would pay thirty percent more for a stick of memory with a Corsair logo on it. You cannot do it with logic alone. You need to understand the culture, the community, and the almost spiritual attachment that PC enthusiasts have to the companies that helped them overclock their first Pentium.

Today, Corsair trades on the NASDAQ under the ticker CRSR. The company generated nearly $1.5 billion in revenue in fiscal year 2025, sells everything from DRAM modules and power supplies to mechanical keyboards and capture cards, and sits at the center of the PC gaming ecosystem in a way that no other single company quite replicates. Logitech is bigger. Razer is flashier. But neither one touches as many parts of the gaming stack as Corsair does.

The story we are about to tell is not a simple success narrative. It is the story of a company that was right about a market before almost anyone else, that survived the brutal commodity cycles of the DRAM industry, that used private equity money to transform itself through acquisitions, and that went public at possibly the most euphoric moment in gaming hardware history, only to watch its stock lose nearly ninety percent of its value over the next five years. It is a story about timing, about platform risk, about what branding can and cannot do in hardware, and about whether a founder's thirty-one-year vision can survive the transition to professional management.

Here is the central question: How did a DRAM memory module company become the backbone of the PC gaming ecosystem, and can the empire it built endure?

To answer it, we need to go back to a physicist from London who understood something profound about commodity markets that most of his competitors missed entirely.

II. The Founding Context: DRAM Market and Andy Paul's Bet (1994-2000)

To understand Corsair, you have to understand the man who built it, and the unlikely bet he made on a market that most investors would have dismissed as hopelessly commoditized. Andy Paul was not your typical Silicon Valley founder. He was a British-educated physicist, holding an honors degree from The City University of London, who had migrated to California and found his way into the semiconductor industry through a series of engineering and sales roles at Fairchild Semiconductor, one of the foundational companies of Silicon Valley. By the late 1980s, Paul had founded Multichip Technology, which operated as a subsidiary of Cypress Semiconductor. He understood the semiconductor supply chain at a molecular level: how chips got designed, manufactured, packaged, tested, and sold. This was not a software founder's story of garage coding sessions. This was a hardware veteran who knew that the hardest problems in tech were not invention but execution.

In January 1994, Paul co-founded Corsair Microsystems with Don Lieberman and John Beekley in Fremont, California. The name "Corsair" evoked speed, daring, and a bit of pirate swagger, qualities that would prove remarkably fitting for a company that would spend three decades raiding margin pools in commodity hardware markets. Their initial product was something called a COASt module, which stood for "Cache on a Stick." These were Level 2 cache memory modules that plugged into Intel Pentium motherboards to improve processing speed. For non-technical readers, think of L2 cache as a small, ultra-fast holding area between the processor and main memory. It is the difference between a chef having ingredients on the countertop versus having to walk to the pantry for every item. Faster cache means a faster computer.

It was an elegant niche: Intel's Pentium processors needed external L2 cache, and Corsair provided high-quality modules to OEMs who needed reliable components. The mid-1990s PC boom was in full swing, and anyone making quality components for the exploding PC market had a tailwind at their back.

But then Intel did what Intel always does. With the Pentium Pro and subsequent processor generations, Intel integrated the L2 cache directly onto the processor die. Corsair's founding product evaporated overnight. This is a pattern that recurs throughout the technology industry: the platform owner vertically integrates, and the component supplier gets squeezed out. This is the kind of moment that kills hardware startups. Your entire market disappears because your biggest customer's biggest supplier decided to vertically integrate. Paul had to pivot, and he pivoted into DRAM modules.

Now, DRAM is about as close to a pure commodity as you can get in the tech industry. For those unfamiliar, DRAM stands for Dynamic Random Access Memory. It is the short-term memory of your computer, the place where your processor stores the data it is actively working with. Every running application, every open browser tab, every game asset currently being rendered lives in DRAM. Without it, your computer cannot function. But the DRAM chips themselves are manufactured by only three companies: Samsung, SK Hynix, and Micron, who together control roughly ninety-five percent of global production. Companies like Corsair buy raw DRAM chips from these manufacturers, assemble them onto printed circuit boards called DIMMs, test them, and sell them as finished memory modules. The margins are thin, the competition is brutal, and differentiation is almost impossible. Trying to build a brand in DRAM is like trying to build a brand in bottled water. Most people assume it is all the same.

But Andy Paul saw something that the commodity view missed entirely. In the late 1990s and early 2000s, a subculture was emerging on internet forums: overclockers. These were the people who pushed their processors and memory beyond rated specifications, chasing benchmark scores and bragging rights. They cared intensely about memory quality because bad RAM would crash their overclocked systems. They needed modules that were binned, that is, selected for the highest quality silicon, and tested at extreme specifications. And they were willing to pay a premium for reliability.

In 2002, Corsair made the strategic bet that would define the company. Rather than competing for Dell's business against dozens of other module makers on price alone, Corsair launched its XMS product line targeted specifically at PC enthusiasts and overclockers. The modules featured aluminum heat spreaders, which were both functional, helping dissipate heat from overclocked chips, and aesthetic, making the RAM look aggressive and purposeful inside a windowed PC case. This was a revolutionary idea at the time: treating memory not as a faceless commodity but as a performance product with visual identity.

The genius was not just in the product. It was in the channel. Corsair built its early reputation through enthusiast forums, hardware review sites, and retailers like NewEgg that catered specifically to PC builders. The company sponsored overclockers, engaged with the community directly, and cultivated a reputation for standing behind its products with generous warranties. In a market where most RAM came in anonymous packaging, Corsair made memory aspirational. The dot-com boom provided the broader tailwind. PC sales were surging, internet adoption was accelerating, and the idea that your computer was an extension of your identity was taking root among a generation of gamers and tinkerers who would become Corsair's lifelong customers.

There is a useful analogy here to the wine industry. The grapes come from a handful of well-known growing regions, and the raw material is fundamentally similar. But a Napa Valley Cabernet from a respected winemaker commands a massive premium over a box of wine from a supermarket shelf, even though both are fermented grape juice. The difference is selection, testing, presentation, and story. Corsair did to DRAM what premium wine labels did to grapes: they took a commodity input, applied expertise and quality control, wrapped it in a compelling brand narrative, and charged dramatically more for it.

By the end of the decade, Corsair had established itself as the enthusiast memory brand, a phrase that would have seemed absurd to anyone in the semiconductor industry five years earlier. Paul had found something genuinely durable in a commodity market: the willingness of enthusiasts to pay for peace of mind, performance, and identity. It was a small moat, but it was real. And it would prove just durable enough to survive the brutal commodity cycles that lay ahead.

III. Surviving the Commodity Grind: Building Moats in Memory (2000-2007)

Walk into a Fry's Electronics store in Silicon Valley in the spring of 2001 and you would see shelves sagging with unsold memory modules, prices plummeting week by week, and sales associates who had no idea whether the company they worked for would still exist in six months. The dot-com crash of 2000-2001 was a near-death experience for much of the PC industry. DRAM prices collapsed, falling by as much as eighty percent from their peak as the speculative bubble burst and corporate IT spending froze. Manufacturers who had built capacity for the boom found themselves drowning in inventory. Module makers operating on razor-thin margins went bankrupt. For a small company like Corsair, survival required discipline, differentiation, and a relentless focus on the one customer segment that kept buying premium products even in a downturn: gamers.

This is a pattern that deserves attention because it reveals something fundamental about Corsair's business model. In economic downturns, the mainstream PC market contracts sharply. Corporate IT budgets get slashed, consumer spending on new computers drops, and component prices fall. But the enthusiast gamer market behaves differently. Gamers are not buying computers because they need to run Excel. They are buying because gaming is their primary hobby, their social life, their identity. The upgrade cycle for a dedicated gamer is driven by game releases and hardware generations, not by corporate refresh schedules. This does not make the enthusiast market recession-proof, but it makes it recession-resistant in a way that the broader PC market is not.

Corsair leaned into this distinction throughout the 2000s. The XMS branding became the gold standard in enthusiast memory. Every product was tested at rated specifications before shipping, something that sounds obvious but was genuinely unusual in an industry where manufacturers routinely shipped modules that might or might not hit their rated speeds. Corsair introduced more aggressive heat spreader designs, RGB lighting would come later, and expanded its Dominator line as the ultra-premium tier above Vengeance, creating a good-better-best product hierarchy within the memory category.

But Paul understood something crucial: memory alone would never be enough. The DRAM market was inherently cyclical, driven by the oligopolistic dynamics of Samsung, SK Hynix, and Micron. When those three companies expanded capacity, prices crashed. When they constrained supply, prices spiked. Corsair was a price-taker in a market dominated by price-setters. The company could add value through testing, branding, and customer service, but it could never control the underlying economics of the memory chips themselves.

The first major diversification came around 2006, when Corsair entered the power supply market with the HX Series. Power supplies, or PSUs, occupied a similar strategic position to memory: they were essential components in every gaming PC, most people treated them as commodities, and enthusiasts cared deeply about efficiency, reliability, and noise levels. Corsair applied the same playbook: premium positioning, rigorous testing, generous warranties, and aggressive community engagement.

Then came what was arguably the most important pre-acquisition diversification: all-in-one liquid cooling. To understand why this mattered, consider the problem. High-performance processors generate significant heat, often over a hundred watts of thermal energy, and that heat needs to be removed efficiently or the processor will throttle its performance or, worse, sustain damage. Traditional air coolers use large metal heatsinks and fans, but they are bulky, noisy, and limited in their cooling capacity. Custom water cooling loops offer superior thermal performance, but they require the user to assemble a complex system of pumps, reservoirs, tubing, radiators, and water blocks, a process that is expensive, time-consuming, and carries the risk of leaking water inside a computer full of electronics.

Corsair's Hydro Series, launched around 2010-2011 with models like the H50, H60, H80, and H100, solved this problem elegantly. These were closed-loop liquid cooling systems, also called all-in-one or AIO coolers, that came pre-assembled and pre-filled. The user simply mounted the block on the CPU and attached the radiator to the case. No plumbing required. They allowed PC builders to get the thermal performance of water cooling without the complexity of custom loops. The timing was impeccable. Processor thermal design power was increasing, overclocking was becoming more mainstream, and PC cases with transparent side panels were making the interior of a computer into a visual display. A Corsair AIO cooler, with its branded block sitting atop the CPU, became as much a statement of identity as the RAM sticks flanking it.

By 2011, Corsair had also entered the PC case market with the Obsidian Series and launched its first mechanical gaming keyboards, the K60 and K90. Each product category followed the same pattern: identify a component that PC gamers cared about, apply premium branding and quality standards, and leverage the existing enthusiast community to build credibility. The approach was working. Corsair was no longer just a memory company. It was becoming the default brand for the enthusiast PC builder, the company whose logo appeared on multiple components inside a single build.

This diversification mattered enormously for the company's financial profile. Think of it as a pyramid of margin opportunity. At the base were memory modules, generating margins in the low teens on a good day, where the underlying DRAM chips were priced by a global oligopoly and the module maker had limited value-add. In the middle were power supplies, cases, and cooling solutions, products with more design complexity and less commodity price pressure, where margins could stretch into the mid-twenties. At the top were peripherals: keyboards, mice, and headsets, where brand, design, and user experience commanded margins that could approach thirty percent or higher. By spreading across multiple product categories, Corsair was both reducing its dependence on DRAM cycles and steadily climbing the margin pyramid. The company was also building something less tangible but potentially more valuable: an ecosystem. A builder who bought Corsair memory might buy a Corsair PSU, a Corsair cooler, and a Corsair case. Each product reinforced the others.

But organic growth in hardware is slow and capital-intensive. Building a keyboard from scratch requires different engineering expertise than building a memory module. Corsair needed either time or money to accelerate the transformation. It would get both, but not from the public markets. It would get them from private equity.

IV. The Private Equity Era: EagleTree Takes Control (2017)

The private equity chapter of Corsair's story actually begins in 2013, when Francisco Partners, a technology-focused PE firm based in San Francisco, made a seventy-five million dollar strategic investment in Corsair and took a majority stake. Francisco Partners specialized in technology companies with strong market positions but unrealized potential, and Corsair fit the profile perfectly. The firm saw a company with a dominant brand in enthusiast memory and an early presence in gaming peripherals, but one that lacked the capital and organizational infrastructure to scale into a true gaming platform.

Francisco provided the capital and strategic support to help Corsair professionalize its operations, build out its finance and supply chain functions, and expand its product portfolio beyond the enthusiast niche. It was a critical stepping stone, but Francisco was a growth investor, not a long-term operator. Within four years, the firm was looking for an exit, and the gaming hardware market was hot enough to attract premium valuations from buyers looking for platform investments.

On July 26, 2017, EagleTree Capital announced a definitive agreement to acquire a majority stake in Corsair from Francisco Partners in a transaction valued at five hundred and twenty-five million dollars. EagleTree acted through its fund EagleTree Partners IV, with co-investors including IMCO, the Investment Management Corporation of Ontario, and the Honeywell pension fund. Andy Paul maintained a significant equity stake and continued as CEO. Corsair had gone from a bootstrapped memory company to a five-hundred-million-dollar enterprise in twenty-three years, and now it had a private equity owner with an explicit mandate to accelerate growth.

Understanding EagleTree's thesis is essential to understanding everything that happened next. EagleTree saw the same thing that Andy Paul had seen years earlier, but they saw it through the lens of a private equity investor looking for platform plays. PC gaming was growing rapidly. Esports viewership was exploding. Streaming on Twitch and YouTube was creating an entirely new category of content creators who needed hardware. And the market for gaming peripherals and components was fragmented across dozens of companies, most of them small, many of them privately held, and few of them with the brand strength and distribution infrastructure to scale globally. EagleTree called Corsair "the undisputed leader in PC gaming hardware" and saw an opportunity to build a comprehensive gaming ecosystem through acquisitions.

The buy-and-build playbook is one of the most common strategies in private equity, but it only works when three conditions are met: the acquirer has a brand that can absorb new products credibly, the target companies add genuine strategic value rather than just revenue, and the integration does not destroy whatever made the targets valuable in the first place. In consumer hardware, this is particularly tricky because brands carry emotional weight with customers. Gamers are tribal about their gear. Acquiring a beloved brand and mishandling it can alienate exactly the customers you are trying to reach.

EagleTree also brought leverage. Private equity deals are typically funded with significant debt, and the Corsair acquisition was no exception. This debt would later become a significant burden when the business environment deteriorated, but in 2017, with gaming hardware sales growing and interest rates still low, the leverage seemed manageable.

The cultural implications of PE ownership were significant and deserve careful consideration for investors evaluating any company that has gone through a leveraged buyout. Corsair had operated for twenty-three years as a founder-led company with the patience and long-term orientation that implies. Andy Paul could afford to invest in products that might not pay off for years because he was not answering to quarterly earnings expectations. He could accept lower margins in memory because he knew the brand was building long-term customer loyalty. He could move slowly into new categories because he prioritized getting the product right over hitting a quarterly revenue target.

Under EagleTree, the incentives shifted fundamentally. Private equity firms raise funds with a defined life, typically ten years, and they need to return capital to their limited partners within that window. This means the PE clock is always ticking. EagleTree needed to grow Corsair, improve margins, and find an exit, whether through an IPO, a strategic sale, or a secondary buyout, within the typical PE holding period of four to seven years. This meant that acquisitions needed to happen quickly, integration needed to be efficient, and the company needed to show a clear growth trajectory to future buyers.

The incentive structure of PE ownership also affects how a company manages its balance sheet. PE firms use leverage, meaning debt, to amplify returns. If EagleTree invests two hundred million of equity and borrows three hundred million to complete a five hundred million dollar deal, and then sells the company for one billion, the return on EagleTree's equity is enormous. But the debt stays on the company's balance sheet, which means the company bears the downside risk if the business deteriorates. This is exactly what happened when the post-pandemic downturn hit: Corsair was carrying approximately five hundred and fifty million in debt at its IPO, a burden that consumed cash flow and limited strategic flexibility at precisely the moment the company needed both.

In 2018, Corsair completed its rebranding from Corsair Components to Corsair Gaming, Inc. This was not merely a name change. It was a strategic declaration of intent, a signal to customers, competitors, and potential acquisition targets that Corsair saw itself as a gaming platform company, not a component maker that happened to sell to gamers. The distinction matters because it shaped how the company evaluated acquisitions, prioritized product development, and marketed itself to consumers. A components company optimizes for specification and price. A gaming platform company optimizes for ecosystem breadth and brand experience.

The stage was set for the acquisition spree that would define the next chapter.

V. The Acquisition Spree: Building the Gaming Ecosystem (2011-2019)

If Andy Paul's founding insight was that enthusiasts would pay a premium for memory, his second great insight, amplified by EagleTree's capital and urgency, was that the modern gamer's setup was not one product but an ecosystem. Think about what a serious gamer or content creator needs in 2018: a PC with high-performance memory, cooling, storage, and power supply. A case to put it all in. A keyboard, mouse, headset, and mousepad on the desk. A capture card and Stream Deck for streaming. A premium controller for console gaming. Lighting, microphones, green screens. Every one of those products represented a separate purchase decision, a separate brand relationship, and a separate margin opportunity. Corsair's strategy was to own as many of those touchpoints as possible.

The earliest expansions into cases and keyboards during 2011-2013 laid the groundwork. The Obsidian Series cases earned respect from reviewers and builders for their clean aesthetics and thoughtful engineering. The Vengeance K70 keyboard, launched in early 2013, became one of the most iconic mechanical gaming keyboards ever made, with its brushed aluminum frame and Cherry MX switches. These were not acquisitions but organic product launches that demonstrated Corsair could extend its brand beyond memory into categories where design and user experience mattered as much as raw specifications.

But the acquisition that truly transformed Corsair came in July 2018, when the company purchased the gaming division of Elgato Systems for forty-six point six million dollars. To understand why this deal was so significant, you have to understand what was happening in the streaming world at the time. Twitch had exploded from a niche platform for speedrunners and competitive gamers into a mainstream entertainment phenomenon. Fortnite, which had launched its battle royale mode in September 2017, was driving millions of new viewers and aspiring streamers to the platform. And those streamers needed hardware.

Elgato had two products that mattered enormously. The first was its line of capture cards. For non-streamers, a capture card is a device that sits between a gaming console or PC and a streaming computer, capturing the video output so it can be broadcast live to platforms like Twitch or YouTube. Think of it as a translator between the gaming world and the streaming world. Without a capture card, a console gamer has no way to share their gameplay with an audience. Elgato dominated this niche with products that were both technically excellent and remarkably easy to use, a rare combination in streaming hardware where competing products often required hours of configuration.

The second, and ultimately more important, product was the Stream Deck. Launched in May 2017, the Stream Deck was a small control panel with customizable LCD buttons that allowed streamers to trigger scene changes, sound effects, social media posts, and other actions with a single press. Imagine having a miniature dashboard on your desk where each button can do anything you program it to do: switch camera angles, play an intro jingle, tweet that you are live, adjust audio levels, all without touching your keyboard or mouse during a live broadcast. There was nothing else like it on the market. It was a category-creating product that defined an entirely new hardware segment.

The Stream Deck's brilliance was that it turned out to be useful far beyond streaming. Photographers, video editors, music producers, office workers, and even medical professionals discovered that a customizable button panel was an extraordinarily powerful productivity tool. This gave Elgato a growth vector that extended well beyond gaming, into the broader creator economy and knowledge worker market. For forty-seven million dollars, Corsair had acquired what would become arguably its most valuable and differentiated business unit.

The following year, 2019, brought two more significant deals. Corsair acquired Origin PC, a boutique maker of custom high-performance gaming PCs and laptops based in Miami. This gave Corsair a pre-built PC offering to complement its components business, allowing the company to serve both the DIY builder who buys individual parts and the customer who wants a turnkey gaming system.

More strategically significant was the December 2019 acquisition of SCUF Gaming. SCUF made premium gaming controllers with patented features like back paddles, which are extra buttons on the back of the controller that allow gamers to jump, crouch, or reload without taking their thumbs off the joysticks. In competitive gaming, where reaction times are measured in milliseconds, this ergonomic advantage can be the difference between winning and losing a gunfight. SCUF also offered adjustable hair triggers and deep customization options, from trigger sensitivity to thumbstick height. Here was the really interesting thing about SCUF: over ninety percent of professional esports players on console used SCUF controllers. The brand had an authenticity in the competitive gaming community that money alone could not buy. SCUF also represented something strategically important for Corsair: a beachhead in console gaming. Corsair had been almost entirely a PC company, which meant that its fortunes were tied to the health of the PC gaming platform. SCUF gave Corsair exposure to the massive Xbox and PlayStation install bases without requiring the company to compete directly with the console manufacturers themselves.

In November 2020, shortly after the IPO, Corsair also acquired Gamer Sensei, the world's largest esports coaching platform, an exploratory move into gaming services rather than hardware. The deal was small but signaled Corsair's interest in building recurring revenue streams beyond one-time hardware sales.

The portfolio logic was compelling on paper. A serious gamer might now have Corsair RAM, a Corsair PSU, Corsair cooling, and a Corsair case inside their PC. On their desk: a Corsair K70 keyboard, a Corsair mouse, a Corsair headset. For streaming: an Elgato capture card, an Elgato Stream Deck, Elgato lighting. For console gaming: a SCUF controller. The company had created a product ecosystem that touched virtually every aspect of the gaming experience, unified, at least in theory, by the iCUE software platform that allowed users to control RGB lighting and performance settings across all Corsair devices from a single application.

The challenge, as always with buy-and-build strategies, was integration. Corsair adopted a "house of brands" approach, maintaining the Elgato, SCUF, and Origin PC brand identities rather than rebranding everything as Corsair. This preserved the authenticity and community relationships that made those brands valuable, but it also created complexity. Each brand had its own product development priorities, marketing voice, and customer expectations. The question of how tightly to integrate acquired companies is one of the most difficult strategic decisions in consumer hardware, and the answer is rarely obvious until years after the acquisition.

Consider the contrast between Procter and Gamble, which maintains distinct brands like Tide and Gillette, and Apple, which puts a single brand on everything from phones to headphones. Corsair chose the P&G approach for its acquisitions, which preserved brand equity but limited the cross-selling benefits that a unified brand might have enabled. A gamer buying an Elgato Stream Deck might not even realize it is a Corsair company. This is a tradeoff that every conglomerate faces, and there is no universally correct answer. But it does mean that Corsair's ecosystem advantage is less visible to consumers than it would be if every product carried the same brand.

By the end of the decade, Corsair had executed ten acquisitions since 2018, transforming itself from a components company with some peripherals into a diversified gaming platform touching PC building, peripherals, streaming, console gaming, and esports services. The financial backing of EagleTree, which needed an exit within its fund timeline, made the path forward clear: go public.

VI. The Gaming Boom and Path to IPO (2018-2020)

The years leading up to Corsair's IPO were the best the gaming hardware industry had ever experienced, and possibly the best it will ever experience. To appreciate the scale of what was happening, consider a few data points. Fortnite's battle royale mode attracted three hundred and fifty million registered accounts by 2020, turning a generation of teenagers into PC gamers almost overnight. Twitch's concurrent viewership doubled and then doubled again. YouTube Gaming was growing rapidly, particularly in Southeast Asia and Latin America. Esports prize pools were hitting tens of millions of dollars, and the professional gaming ecosystem was beginning to resemble traditional sports in its sponsorship structures and media rights deals. Gaming was no longer a subculture. It was mainstream entertainment, and every new gamer and every new streamer needed hardware.

The streaming economy deserves particular attention because it created an entirely new category of hardware demand. Before Twitch and YouTube Gaming, the audience for streaming hardware was essentially zero. By 2018, there were millions of aspiring content creators who needed capture cards, microphones, lighting, and control interfaces to produce their broadcasts. This was not cannibalization of existing hardware spending. It was net new demand, and Corsair, through its Elgato acquisition, was positioned to capture a disproportionate share of it.

Then came COVID-19. In March 2020, as lockdowns spread globally, something extraordinary happened to the PC gaming market. Millions of people were suddenly working from home, attending school from home, and entertaining themselves at home. They needed better computers. They needed webcams, microphones, and streaming equipment. Government stimulus checks put cash in consumers' pockets with limited ways to spend it. And the pre-existing trend toward PC gaming, already robust, went parabolic.

Corsair found itself in exactly the right place at exactly the right moment. Its components business supplied the parts for new PC builds during the biggest surge in DIY PC building in years. Its peripherals business sold the keyboards, mice, and headsets that remote workers and gamers needed. Its Elgato division supplied streaming equipment to the explosion of new content creators. Demand was so strong that Corsair estimated component shortages alone cost the company at least one hundred million dollars in lost revenue in 2021, roughly ten percent of sales, simply because it could not get enough parts to meet demand.

The financial trajectory was remarkable. Revenue jumped from approximately one point one billion dollars in 2019 to one point seven billion in 2020, a fifty-five percent increase that would have been extraordinary for any hardware company. Revenue continued climbing to one point nine billion in 2021. Corsair was growing faster than the PC gaming market itself, gaining share as its multi-category portfolio allowed it to capture more spending per customer.

Against this backdrop, Corsair explored its options for going public. The company reportedly considered a SPAC transaction in early 2020. For those unfamiliar, a SPAC, or Special Purpose Acquisition Company, is essentially a blank-check company that raises money through its own IPO and then uses that cash to merge with a private company, taking it public without the traditional IPO process. SPACs were enormously popular in 2020 and 2021 because they offered a faster path to public markets, more certainty on valuation through negotiated deal terms, and the ability for the target company to share forward-looking financial projections that would not be permitted in a traditional IPO prospectus. Dozens of companies across technology, electric vehicles, and other sectors went public through SPACs during this period.

Corsair ultimately chose the traditional IPO route, which in retrospect may have been the more conservative but also more credible choice. Many of the SPAC deals from this era eventually unraveled as companies failed to meet the aggressive projections they had shared with investors, destroying trust in the SPAC structure. By taking the traditional route, Corsair preserved its credibility with institutional investors even if it meant accepting more uncertainty around the IPO pricing.

On September 23, 2020, Corsair Gaming listed on the NASDAQ under the ticker CRSR. The IPO was priced at seventeen dollars per share, and the offering raised approximately two hundred and thirty-eight million dollars from a combination of primary shares issued by the company and secondary shares sold by EagleTree. EagleTree had held a ninety-two percent stake prior to the offering, and the IPO was the beginning of what would become a multi-year process of gradually reducing that position through secondary offerings. The initial valuation was approximately one point five six billion dollars. The first day was actually somewhat disappointing, with the stock declining about eleven percent from the IPO price.

But then the pandemic tailwinds really kicked in. Within two months, the stock had more than tripled from its IPO price. On November 24, 2020, Corsair shares hit an all-time closing high of fifty-one dollars and thirty-seven cents, giving the company a market capitalization of nearly five billion dollars. EagleTree conducted secondary offerings to reduce its stake, selling shares in January 2021 and continuing through 2022 and 2023. By May 2023, the firm still held approximately fifty-five percent of outstanding shares.

The narrative on Wall Street was irresistible: Corsair was the "picks and shovels" play in the gaming gold rush, the company that profited no matter which game or platform won, as long as people kept gaming. The analogy referred to the California Gold Rush, where the merchants who sold shovels and supplies to miners often made more money than the miners themselves.

Wall Street loved the story. Corsair touched every part of the gaming setup. It had a founder-CEO with three decades of industry experience. It was growing revenue at fifty percent. Streaming was exploding. The GPU shortage was actually helping Corsair in a perverse way, because even when gamers could not get a new graphics card, they were still buying peripherals, memory upgrades, and streaming equipment. For a brief, euphoric moment, Corsair looked like it might be one of the great hardware growth stories of the decade.

The problem with euphoric moments, of course, is that they end.

VII. The Crash: Post-COVID Reality and Inventory Nightmare (2021-2023)

In the fourth quarter of 2021, something strange started happening to Corsair's order book. After eighteen months of back-ordered products, unfulfilled demand, and apologies to retailers about supply constraints, the phones started ringing less. Reorders slowed. Sell-through data at retail began softening. At first, it looked like a temporary pause. It was not. The reversal, when it came, was swift and brutal. Understanding what happened requires understanding a phenomenon that economic historians call demand pull-forward. During the pandemic, consumers compressed several years of normal purchasing into twelve to eighteen months. People who would have gradually upgraded their PCs over two or three years did it all at once. First-time builders who might have entered the market in 2022 or 2023 built their PCs in 2020. Streamers who were considering upgrading their Elgato gear "next year" bought it now. When the pandemic restrictions eased and stimulus payments stopped, the demand did not normalize. It evaporated.

Simultaneously, the GPU market underwent its own traumatic correction. During 2020-2021, cryptocurrency mining, particularly Ethereum mining, had consumed enormous quantities of GPUs. This pushed GPU prices to two to three times their suggested retail price and created a cascading demand for every other component in a mining rig: power supplies, cases, memory, cooling. When Ethereum completed its transition from Proof of Work to Proof of Stake on September 15, 2022, an event known as The Merge, GPU mining became essentially unprofitable overnight. A flood of used mining GPUs hit the secondary market, depressing new GPU sales. And when fewer people are building or upgrading PCs, they are buying fewer power supplies, fewer cases, fewer sticks of RAM, and fewer cooling systems. Every one of those is a Corsair product.

The financial impact was devastating. Revenue fell from one point nine billion dollars in 2021 to one point three eight billion in 2022, a twenty-eight percent decline. To put that in context, Logitech's comparable decline was approximately twenty percent over a similar period, suggesting that Logitech's broader diversification into enterprise video conferencing and workspace solutions provided some cushion that Corsair, as a pure-play gaming company, lacked. Corsair fell faster and harder than the broader market, raising uncomfortable questions about whether the company had over-expanded, over-inventoried, or simply had less pricing power than investors had assumed.

The global gaming industry itself was not shrinking. Total gaming revenue, including software, services, and hardware, continued to grow. The problem was specific to hardware, and particularly to the DIY PC building segment that represented the core of Corsair's components business. When gamers already have powerful machines built during the pandemic, the upgrade cycle lengthens dramatically. Why buy new RAM when your existing sticks are perfectly adequate? Why upgrade your power supply when the one you installed eighteen months ago handles your current GPU just fine?

The inventory situation was particularly painful and deserves explanation because it reveals how supply chains amplify boom-bust cycles. During the pandemic, when demand was surging, Corsair placed larger orders with its component suppliers, extending lead times and building safety stock to avoid the dreaded "out of stock" message that sends customers to competitors. Retailers did the same thing, over-ordering from Corsair to make sure they had product on shelves. This created a bullwhip effect, a well-known supply chain phenomenon where small changes in consumer demand get amplified into much larger swings in orders upstream.

When demand reversed, the whip cracked in the opposite direction. Corsair was left with excess inventory that had to be worked down over several quarters, often at reduced prices. Channel partners like Amazon, Best Buy, and Micro Center were in the same position, having overstocked during the boom. This meant that even as Corsair reduced production, sell-through at retail remained weak because retailers were clearing their own excess inventory before placing new orders. The result was a multi-quarter destocking cycle where revenue declined faster than actual consumer demand, because the channel was absorbing its own surplus before pulling fresh product from Corsair.

Competition intensified at precisely the wrong moment. The gaming peripherals market attracted well-funded entrants and saw existing players become more aggressive. HP had acquired HyperX from Kingston Technology for four hundred and twenty-five million dollars in 2021, giving HyperX access to HP's massive distribution network and supply chain. GN Store Nord acquired SteelSeries for one point two four billion dollars in 2022, backing the premium gaming headset maker with GN's decades of audio engineering expertise. Razer, which had gone private in 2022 under founder Min-Liang Tan, was freed from public market pressures and investing aggressively. Logitech, with its four-billion-dollar revenue base, could absorb cyclical downturns that would cripple smaller competitors.

Corsair's stock reflected the carnage with an almost sickening precision. From the November 2020 high of fifty-one dollars, shares fell steadily through 2021 and 2022, eventually dropping below ten dollars. The stock would continue sliding, reaching a fifty-two week low of four dollars and forty-eight cents. An investor who bought at the IPO price of seventeen dollars had lost more than seventy percent of their investment. An investor who bought at the peak had lost nearly ninety percent. To put this in perspective, Corsair's market capitalization of roughly six hundred million dollars in early 2026 is actually lower than the five hundred and twenty-five million dollars EagleTree paid for a majority stake in 2017, before the Elgato, SCUF, and Fanatec acquisitions. The market is essentially saying that all of the value created through eight years of acquisitions and organic growth has been destroyed.

This raises a genuine question about whether the public markets are the right home for a company like Corsair. Hardware companies with cyclical revenues, thin margins, and intense competition have historically struggled as public companies unless they reach a scale that provides meaningful insulation from downturns. Corsair, at one and a half billion in revenue, is large enough to be a viable public company but small enough to be vulnerable to the volatility that comes with its market position.

The debt burden inherited from the EagleTree era became a significant concern. Corsair had carried approximately five hundred and fifty million dollars in debt at the time of its IPO, a legacy of the leveraged buyout structure that is standard in PE transactions. In a growing market with strong cash flows, this debt was manageable. In a declining market with compressing margins, it consumed cash that could otherwise have been invested in growth or returned to shareholders. Interest expenses ate into already-thin margins, and the debt overhang weighed on the stock's valuation.

Revenue ticked up modestly to one point four six billion in 2023, but then fell again to one point three two billion in 2024, dipping below even the 2022 trough. Adjusted EBITDA dropped from ninety-five million dollars in 2023 to just fifty-five million in 2024. The company posted a GAAP net loss of nearly one hundred million dollars in 2024, or negative ninety-five cents per diluted share. Gross margins, which had been around twenty-seven percent during the boom years, compressed to roughly twenty-five percent as pricing pressure intensified across every product category. The picture was bleak: four consecutive years of top-line challenges, shrinking profitability, and a stock price that seemed to find new lows every quarter.

Management was not standing still. On February 12, 2025, Corsair announced that Andy Paul, the founder who had led the company for thirty-one years, would retire as CEO effective July 1, 2025. It was the end of an era that had begun in a Fremont garage with cache memory modules and had culminated in a billion-dollar-plus gaming hardware platform.

His successor would be Thi La, who had joined Corsair in 2010 and risen through the ranks to become President and Chief Operating Officer. La's background was in operations and execution rather than the visionary product thinking that had characterized Paul's leadership. She had been instrumental in growing Corsair from a three hundred million dollar company to its current scale and had overseen the expansion from a small range of DIY components to over thirty product lines. The transition was described as long-planned, but the timing, during a period of significant operational challenges, added uncertainty for investors. Founder-to-professional CEO transitions are notoriously difficult in consumer brands, where the founder often embodies the brand's identity in ways that are difficult to transfer.

The question facing Corsair at its nadir was existential, and it is a question that investors continue to debate: was the post-pandemic slump a cyclical correction that would resolve as the PC gaming market normalized, or was it the beginning of a structural decline that would permanently impair the company's earning power? The answer to that question determines whether Corsair at six dollars is a coiled spring or a value trap.

VIII. The Modern Business Model and Product Portfolio (2023-Present)

To understand where Corsair stands today, you need to understand the shape of the business. The company reports in two segments, though the underlying product portfolio is considerably more nuanced.

The first segment is Gaming Components and Systems, which generated roughly two-thirds of total revenue in recent years. This is the business that Corsair was built on: DRAM memory modules under the Vengeance and Dominator brands, power supply units across the RM, HX, and AX tiers, all-in-one liquid coolers under the iCUE and Hydro brands, PC cases, SSDs, and pre-built gaming systems through the Origin PC brand. These are the products that go inside the PC. They tend to be lower margin than peripherals because of the commodity nature of the underlying components, particularly memory. But they also generate substantial revenue because the average selling price of a PSU or a set of DDR5 modules is meaningfully higher than the average selling price of a mousepad or a headset.

The second segment is Gamer and Creator Peripherals, which accounted for roughly one-third of revenue but carries higher gross margins. This includes gaming keyboards, with the iconic K70 still anchoring the lineup, gaming mice, headsets, mousepads, and the portfolio of acquired brands: Elgato's streaming products, SCUF's premium controllers, and as of September 2024, Fanatec's sim racing hardware.

The Fanatec acquisition deserves attention because it illustrates how Corsair continues to expand into adjacent enthusiast niches, and because the circumstances of the deal reveal something about Corsair's opportunistic approach to M&A. Fanatec, the gold standard in sim racing equipment, found itself available because its parent company, German firm Endor AG, went bankrupt. Corsair acquired the Fanatec product line from the bankruptcy proceedings in September 2024, likely at a significant discount to what the brand would have commanded in a competitive auction.

Sim racing, for the uninitiated, is the hobby of racing virtual cars using realistic hardware: a steering wheel with force feedback that simulates the feel of the road, a set of pedals with progressive resistance, and a cockpit setup that can range from a desk-mounted wheel to a full racing simulator costing thousands of dollars. The market is growing rapidly, fueled in part by the global explosion of Formula 1 popularity driven by the Netflix documentary series "Drive to Survive," which introduced millions of new fans to the sport and, by extension, to sim racing as a way to experience the thrill of competing on famous circuits. Fanatec had generated approximately one hundred and ten million dollars in revenue in 2023 before Endor's financial difficulties. Integration was substantially completed by mid-2025, with Fanatec leveraging Corsair's centralized procurement, logistics, and expanding sales channels.

The iCUE software platform is Corsair's attempt to create the software glue that binds its hardware ecosystem together. iCUE, the Corsair Utility Engine, allows users to control RGB lighting across all Corsair devices, monitor system temperatures and performance, manage fan curves, program macros, and update firmware from a single application. The newer iCUE LINK hardware system simplifies cable management by connecting cooling components through a daisy-chained connector, reducing the rat's nest of cables inside a gaming PC.

The software ecosystem creates mild switching costs. A gamer who has carefully configured their RGB profiles, lighting synchronization, and performance settings in iCUE faces some friction when switching to a competitor's products. It is not the kind of deep platform lock-in that Microsoft has with Windows or Apple has with iOS, but it is real enough to influence purchasing decisions at the margin, especially for users with multiple Corsair devices. iCUE also integrates with Elgato's Stream Deck, allowing creators to control their lighting and system settings from the Stream Deck interface, creating cross-product value that neither product would have alone.

Revenue mix matters enormously for Corsair's financial profile. The Peripherals segment, with its higher margins, has been growing as a share of total revenue. In fiscal year 2025, Corsair's overall gross margin hit a record twenty-eight point nine percent, up from roughly twenty-five percent just two years earlier. This improvement came from a combination of mix shift toward higher-margin peripherals, operational efficiencies from integrating acquisitions like Fanatec, and favorable DRAM pricing dynamics as the AI-driven memory shortage pushed up component prices.

Geographically, Corsair remains heavily weighted toward North America, which represents the largest share of revenue. International expansion, particularly in Europe and Asia-Pacific, represents a growth opportunity but also introduces currency risk and the need for localized distribution and marketing.

The direct-to-consumer channel, through Corsair's own website and branded stores on Amazon, is strategically important because it eliminates the margin shared with retailers and gives Corsair direct customer relationships and data. However, direct sales remain a minority of total revenue. Most consumers still buy Corsair products through Amazon, Best Buy, Micro Center, and other retailers, which means that Corsair's pricing power is constrained by the competitive dynamics of retail shelves and search results where it sits alongside Logitech, Razer, HyperX, and SteelSeries.

This is worth pausing on because the retail dynamic fundamentally shapes Corsair's economics. When a consumer searches "gaming keyboard" on Amazon, they see products from a dozen brands ranked by a combination of reviews, price, and Amazon's own algorithms. In this environment, brand premium is harder to maintain than in a specialty retail store where a knowledgeable salesperson might recommend Corsair over a cheaper alternative. The shift toward online purchasing has democratized access to gaming hardware but has also compressed margins across the industry. Corsair's challenge is to maintain brand relevance in an algorithmic marketplace where price sensitivity is the default consumer behavior.

Fiscal year 2025, reported on February 12, 2026, showed genuine signs of stabilization and recovery. Revenue grew twelve percent year-over-year to one point four seven billion dollars. Adjusted EBITDA surged eighty-four percent to one hundred point six million dollars, exceeding the high end of management's guidance. The company reduced debt by fifty-two million dollars during the year, bringing total debt reduction since the IPO to seventy-seven percent. And Corsair authorized its first-ever share repurchase program of fifty million dollars, a signal that management believed the stock was undervalued and the balance sheet could support returning cash to shareholders.

IX. Strategic Crossroads and Key Questions (2024-2025)

Every company faces moments where the path forward is genuinely uncertain, where reasonable people can disagree about the right strategy. Corsair arrives at 2026 at precisely such a moment, a genuine inflection point. The post-pandemic hangover has largely been absorbed. The balance sheet is dramatically healthier than it was at the IPO. Margins are at record levels. A new CEO is at the helm. But the company's stock price, hovering around five to six dollars, reflects deep skepticism about the durability of the recovery and the long-term competitive position.

The first and most fundamental question is whether PC gaming growth is stalling or merely normalizing. This is the question that every investor in gaming hardware must answer before making a commitment. The pandemic years created an illusion of hypergrowth that was never sustainable. If you looked at a Corsair revenue chart in early 2021, you would see a line going up and to the right at a forty-five degree angle. The temptation was to extrapolate that line indefinitely. But the relevant comparison is not 2021 but something more like 2019, when Corsair did approximately one point one billion in revenue. By that measure, the company has grown roughly thirty percent over six years, which is respectable if unspectacular. Industry research firms project the global gaming PC market to grow at a compound annual rate of roughly thirteen percent through 2030, driven by new GPU generations, the ongoing shift to DDR5 memory, and the persistent growth of gaming as a mainstream entertainment category. If these projections are even directionally correct, Corsair has room to grow. But the projections could be wrong.

The console versus PC debate is relevant here. SCUF gives Corsair a meaningful presence in the console ecosystem, and the partnership announced with Microsoft in March 2024 for tournament-grade, cross-platform controllers suggests that Corsair is taking the console opportunity seriously. But SCUF remains a relatively small part of the overall business, and the console controller market is fundamentally different from the PC components market in its competitive dynamics and margin structure.

Content creation appears to be the most durable growth vector. The global game streaming market was estimated at nearly eleven billion dollars in 2024 and is projected to reach over thirty billion by 2033. Elgato's position in this market is strong and differentiated. The Stream Deck has no true peer, and the expansion of the Stream Deck concept into enterprise and productivity use cases, what Corsair calls "Stream Deck Everywhere," opens a much larger addressable market. Elgato's revenue has reportedly surpassed two hundred million dollars with strong double-digit growth, making it the highest-growth and highest-margin part of Corsair's portfolio.

Competitive threats remain acute. Logitech's gaming business alone is roughly the same size as Corsair's entire company. Razer, with over two billion in revenue after its return from private markets, has scale that Corsair lacks. HyperX benefits from HP's distribution muscle. SteelSeries, backed by GN Store Nord's audio engineering expertise, is growing faster than the market. In peripherals specifically, the barriers to entry are low. Anyone can contract with a Taiwanese ODM to produce keyboards, mice, and headsets, slap a brand on them, and sell them on Amazon. The question is whether Corsair's brand, community relationships, and software ecosystem are strong enough to justify a price premium as competition intensifies.

The innovation pipeline is a concern for some observers. The PC gaming hardware industry is fundamentally iterative. Each year brings slightly better keyboards, slightly lighter mice, slightly more efficient coolers. Revolutionary product categories, like the Stream Deck, are rare. Corsair's CES 2026 showcases included products like the MAKR 75, a DIY customizable keyboard with web-based peripheral customization, and continued expansion of the Stream Deck ecosystem. These are solid product launches, but they are evolutionary, not revolutionary.

The capital allocation question is perhaps the most strategically consequential. Corsair has reduced debt by seventy-seven percent from IPO levels and authorized its first share buyback. With the balance sheet in much healthier condition, management must decide how to allocate cash flow between further debt reduction, share repurchases, organic investment, and potential acquisitions. The Fanatec deal shows that Corsair is still willing to acquire. The question is whether the company should be buying or whether, at some point, the right answer is to sell. The possibility of going private again, whether through EagleTree increasing its stake or through a take-private by another PE firm, is not academic. EagleTree still holds approximately fifty-four percent of shares. At a market capitalization of roughly six hundred million dollars, Corsair would be an affordable target for a PE firm looking for a branded consumer hardware platform with turnaround potential.

For the 2026 fiscal year, management has guided for revenue of one point three three to one point four seven billion dollars and adjusted EBITDA of one hundred to one hundred and fifteen million dollars. The guidance implies roughly flat revenue at the midpoint, with tariff headwinds of approximately twelve million dollars partially offset by continued mix shift toward higher-margin peripherals. This is not a high-growth story. It is a margin improvement story, and the question is whether margin improvement alone can rerate a stock that has been priced for decline.

X. Playbook: Business and Strategy Lessons

What can investors, founders, and business strategists learn from Corsair's journey? Every great company story contains lessons that extend beyond the specific industry and era. Corsair's three-decade journey offers a particularly rich set of lessons for investors, founders, and strategists because it touches on so many of the recurring challenges in consumer hardware: commoditization, cyclicality, platform risk, acquisition strategy, and the ever-present tension between growth and profitability.

The Enthusiast Premium Strategy. Corsair proved that you can build a brand in a commodity market, but only if you identify a customer segment that values something beyond the commodity itself. In Corsair's case, that something was a combination of performance assurance, visual identity, and community belonging. The overclockers who bought XMS memory in 2002 were not just buying RAM. They were buying membership in a community of builders and tinkerers who cared about their hardware the way car enthusiasts care about their engines.

This strategy has parallels outside of technology. Think about how Yeti built a premium brand in coolers, a product that is fundamentally a box that keeps things cold. Or how Red Wing built a brand in work boots, a product that is fundamentally leather and rubber. In each case, the company identified a passionate customer segment, delivered a product that was measurably better than the commodity alternative, and wrapped it in a narrative of quality and identity that justified the premium. This strategy works when the premium is real, meaning the product is genuinely better tested, more reliable, or more thoughtfully designed, and when the community values authenticity. It stops working when the premium becomes purely cosmetic or when the community loses trust.

The Buy-and-Build PE Playbook. EagleTree's strategy with Corsair is a textbook case of using private equity capital to consolidate a fragmented market. The acquisitions of Elgato, SCUF, Origin PC, and Fanatec were individually sensible and collectively created a product ecosystem that no competitor has fully replicated. The lesson is that buy-and-build works best when the acquired brands maintain their identity and community credibility, when the parent company provides genuine operational value through distribution, supply chain, and shared technology, and when the acquirer does not over-leverage the balance sheet. On the first two counts, Corsair executed well. On the third, the leverage from the EagleTree era became a meaningful drag during the downturn.

Platform Dependency. Corsair's fortune is inextricably linked to the health of PC gaming. This is not quite the same as being an app on Apple's App Store, where the platform owner can change the rules overnight. But it is a deep structural dependency. If cloud gaming matures to the point where high-end local hardware becomes unnecessary, or if mobile gaming captures an even larger share of the gaming wallet, or if GPU upgrade cycles lengthen beyond five to seven years, Corsair's core business shrinks regardless of how well the company executes. The SCUF acquisition was an explicit hedge against this risk, and the Elgato strategy of expanding beyond gaming into broader productivity is another. But the core business remains a PC gaming bet.

Acquisition Integration: Elgato versus the Rest. Elgato stands as the acquisition success story that every PE firm dreams about. Corsair paid forty-seven million dollars and got a business that now generates over two hundred million in revenue with superior margins and a category-defining product. What made it work was that Elgato had a product, the Stream Deck, that benefited from Corsair's global distribution and marketing muscle while maintaining its own brand identity and product development culture. The lesson is that the best acquisitions bring something the acquirer could not build organically, in a time frame that matters, and at a price that leaves room for value creation.

The Going-Public Timing Lesson. Corsair's IPO in September 2020 was simultaneously perfectly timed and terribly timed, depending on whose perspective you take. From EagleTree's perspective, the timing was excellent. The PE firm began monetizing a position that it had held for three years at valuations far exceeding its entry price. From a public market investor's perspective, the timing was catastrophic. Anyone who bought the stock near its post-IPO highs was buying the peak of an unsustainable demand cycle.

This duality is not unique to Corsair. It is a recurring pattern in IPOs across industries: companies tend to go public when conditions are most favorable for the seller, which by definition means conditions are often least favorable for the buyer. The lesson is that the best time to go public is often the worst time to buy the stock, and that "picks and shovels" narratives, however compelling, do not insulate hardware companies from the cyclicality of their end markets.

Navigating Cyclicality in Consumer Hardware. If there is one lesson that Corsair's post-pandemic experience drives home, it is this: the single hardest thing about managing a consumer hardware company is managing through cycles. During booms, the pressure is to expand capacity, hire aggressively, and order inventory to meet surging demand. During busts, the penalty for having done any of those things is severe. Corsair over-ordered during the pandemic boom, just as virtually every other hardware company did, and spent three years working through the consequences. The companies that navigate cycles best are those with conservative balance sheets, flexible supply chains, and the discipline to resist the euphoria of the boom. Corsair's post-crash debt reduction is a sign that management has internalized this lesson.

Community and Authenticity. In gaming hardware, brand is not built through advertising. It is built through community engagement, product quality, and authenticity. Corsair earned its brand by showing up on enthusiast forums, sponsoring overclockers, and standing behind products with generous warranties. That brand survived the transition to PE ownership, the acquisition spree, the IPO, and the post-pandemic crash. Whether it can survive a generational change in gaming preferences, where younger gamers may care less about custom PC builds and more about cloud-native experiences, is an open question.

The Diversification Paradox. Corsair's expansion from memory into PSUs, cases, cooling, peripherals, streaming gear, controllers, and sim racing equipment created a remarkably broad product portfolio. This breadth is both a strength and a weakness. It is a strength because it allows Corsair to capture multiple purchases from the same customer and provides diversification across product cycles. It is a weakness because it forces the company to compete on multiple fronts simultaneously, spreading R&D and marketing resources across categories where focused competitors like SteelSeries in audio or NZXT in cases can concentrate their efforts. The right answer depends on execution: a well-integrated multi-product ecosystem is more valuable than the sum of its parts, but a poorly integrated collection of brands is worth less.

XI. Porter's Five Forces Analysis

Understanding Corsair's competitive position requires examining the structural forces that shape its industry. Porter's Five Forces framework, developed by Harvard Business School professor Michael Porter, evaluates industry attractiveness by analyzing five key forces that determine competitive intensity and profitability.

Competitive Rivalry: High. This is the defining force in Corsair's industry. The company competes across multiple product categories, and in each one it faces well-funded, capable competitors. In gaming peripherals, Logitech commands roughly fifteen percent global market share, with Razer at twelve percent and Corsair at approximately eleven percent. SteelSeries dominates premium gaming audio. HyperX leverages HP's distribution infrastructure. In components, Corsair competes with Cooler Master, NZXT, Thermaltake, EVGA (in power supplies), and dozens of smaller brands. Switching costs for consumers are low. A gamer who has been using a Corsair keyboard for three years faces essentially zero friction in buying a Razer keyboard next. Differentiation comes through brand perception, aesthetic design, software integration, and to a lesser extent, performance. But none of these creates the kind of durable competitive moat that would allow sustained excess returns. Price competition is intense, particularly in components where the underlying technology is commoditized.

Threat of New Entrants: Medium. The barriers to entering the gaming peripherals market are deceptively low. Taiwanese and Chinese ODMs will design and manufacture keyboards, mice, and headsets to specification for any company willing to place an order. This is how dozens of Amazon-native brands have entered the market with surprisingly competent products at aggressive price points. However, building a trusted consumer brand with global distribution, community credibility, and a multi-product ecosystem is substantially harder. Capital requirements for competing across Corsair's breadth of product categories are significant. And the established players have R&D capabilities, retail relationships, and community goodwill that take years to build. New entrants can nibble at the margins, but displacing an established brand like Corsair in the enthusiast segment is difficult.

Supplier Power: Medium-High. Corsair's components business is fundamentally dependent on DRAM manufacturers. Samsung, SK Hynix, and Micron operate as a tight oligopoly, and their pricing decisions directly impact Corsair's cost of goods and margins. When memory prices spike, as they did during the 2024-2025 AI-driven shortage, Corsair can pass some costs through to consumers but faces a lag effect and margin compression. Peripheral components are sourced from a broader supplier base of Taiwanese ODMs, but Corsair has limited leverage to negotiate pricing against suppliers who serve dozens of competing brands. The saving grace is scale: Corsair is large enough to command better pricing and priority allocation than smaller competitors.

Buyer Power: Medium. Retail consolidation has increased buyer power at the channel level. Amazon alone represents a massive share of gaming hardware sales, and its marketplace dynamics, including algorithmic search ranking, pricing transparency, and house brand competition, put pressure on margins. Best Buy and Micro Center have their own negotiating leverage. End consumers benefit from intense competition and easy price comparison, giving them effective power over pricing. The enthusiast segment is somewhat insulated because brand-loyal gamers will pay a premium for Corsair, but this loyalty is not absolute and can erode if competing products offer meaningfully better value.

Threat of Substitutes: Medium. The most significant substitute threat comes not from other hardware but from platform shifts. Cloud gaming services promise to make high-end local hardware unnecessary by streaming games from remote servers. The idea is simple: instead of buying a two-thousand-dollar gaming PC, you pay a monthly subscription to play games streamed from a powerful remote server, using only a screen and an internet connection. If this model succeeds at scale, the need for high-performance local components, which is the core of Corsair's business, diminishes substantially. Google Stadia's shutdown in January 2023 demonstrated the technical and business model challenges of cloud gaming, but the trend continues with Nvidia GeForce Now, Xbox Cloud Gaming, and Amazon Luna all investing heavily. Mobile gaming continues to take wallet share from PC gaming, particularly among younger and more casual players. The average smartphone is now a more powerful gaming device than a mid-range PC was ten years ago. On the positive side, streaming and content creation hardware, Corsair's most differentiated category, faces less substitution risk because the need for local processing, low-latency capture, and physical control interfaces remains regardless of how games are delivered. A streamer still needs a capture card, a microphone, and a Stream Deck whether their game is running locally or in the cloud.

XII. Hamilton's Seven Powers Analysis

If Porter's Five Forces describes the battlefield, Hamilton Helmer's Seven Powers framework asks a more personal question: does this specific company have any source of durable competitive advantage that would allow it to earn persistent excess returns over time? While Porter tells you about the industry, Helmer tells you about the company's position within it. The honest answer for Corsair is that its powers are limited, and this is the fundamental challenge facing the company.

Scale Economies: Weak to Moderate. Scale economies exist when a company's unit costs decrease as its volume increases, creating a cost advantage that smaller competitors cannot match. Corsair benefits from some manufacturing and distribution scale, particularly in its components business where volume purchasing of DRAM chips and components provides cost advantages over smaller competitors. The company's global distribution infrastructure, built over three decades, is a genuine asset that would be expensive to replicate. But Corsair's scale advantages are not decisive against competitors like Logitech, which is roughly three times Corsair's size, or against the ODM ecosystem in Asia, which provides scale manufacturing to anyone willing to order sufficient quantities.

Network Effects: Weak. Network effects occur when each additional user makes the product more valuable for all existing users, think of how every new person on a telephone network makes the phone more useful for everyone else. True network effects are largely absent in gaming hardware. iCUE does not become more useful because more people use it. The closest Corsair comes to network effects is in the Elgato ecosystem, where the Stream Deck's marketplace of plugins and integrations grows more valuable as more developers and users contribute. The Elgato community of creators has some characteristics of a network, but it is not the kind of winner-take-all network effect that characterizes software platforms.

Counter-Positioning: Weak. Counter-positioning occurs when a challenger adopts a business model that the incumbent cannot replicate without damaging its existing business. Corsair is not counter-positioned against anyone. It competes with similar companies using similar business models across similar product categories. There is no structural reason why Logitech, Razer, or any other competitor cannot offer what Corsair offers.

Switching Costs: Moderate. The iCUE ecosystem creates real but modest switching costs. A gamer who has configured RGB profiles, set up macro keys, and synchronized lighting across a full suite of Corsair products faces meaningful hassle in switching to a competing ecosystem. SCUF's customization creates higher switching costs for professional gamers who have trained extensively with a specific controller configuration. The transition from DDR4 to DDR5 memory creates a one-time switching opportunity but not a durable lock-in. Overall, switching costs exist but are nowhere near the level that enterprise software companies enjoy.

Branding: Strong. This is Corsair's most significant power and the one that has sustained the company through three decades of commodity competition. Branding, in Helmer's framework, is a power that derives from the accumulated positive associations that customers hold about a company, associations built over time through consistent product quality, marketing, and community engagement.

Corsair's brand carries genuine meaning in the enthusiast community: performance, reliability, quality, and authenticity. Walk into any PC building forum and ask for memory recommendations, and Corsair will be among the first brands mentioned. This brand perception allows Corsair to charge a ten to thirty percent premium over unbranded or lesser-known competitors in many categories. The Elgato brand has similar strength in the creator community. SCUF carries premium brand cachet in the competitive console gaming community. Brand is hard to quantify but easy to observe: gamers actively seek out Corsair products and are willing to pay more for the logo. The risk is that brand strength can erode if product quality slips, if competitors close the perception gap, or if a generational shift in gaming culture changes what enthusiasts value.

Cornered Resource: Weak. Corsair has no unique technology, proprietary manufacturing process, or exclusive intellectual property that competitors cannot replicate. The closest thing to a cornered resource was Andy Paul himself, whose thirty-one years of industry knowledge, relationships, and strategic vision were genuinely irreplaceable. His retirement in July 2025 removed this resource, though his successor Thi La brings fourteen years of Corsair experience. The Elgato team and its product design culture could be considered a cornered resource, but it is fragile and could be replicated over time by a sufficiently motivated competitor.

Process Power: Weak to Moderate. Process power refers to organizational capabilities that are embedded in a company's culture and operations and cannot be easily copied. Corsair's product design consistency, its iCUE software development capabilities, and its multi-brand management expertise qualify as moderate process power. But these are not the kind of deeply embedded, culturally specific processes that companies like Toyota or TSMC have built over decades. A well-managed competitor could develop similar capabilities within a few years.

The net assessment is sobering. Corsair's primary power is Brand, supplemented by moderate Switching Costs through its software ecosystem. In a commodity-adjacent hardware market, brand alone is a meaningful but narrow moat. It can sustain premium pricing in good times but may not be enough to prevent margin compression when the market turns against you. Compare this to a company like TSMC, which has Scale Economies, Process Power, and Cornered Resources so deep that its competitive position is virtually unassailable. Or even Logitech, which has greater Scale Economies and broader diversification across both consumer and enterprise markets. Corsair's strategic position, while not hopeless, requires near-flawless execution to maintain profitability in an industry that punishes mistakes severely.

XIII. Bull versus Bear Case

Every investment story has two sides, and the discipline of articulating both the best case and worst case scenarios is essential for any serious investor. After four years of declining stock price and operational challenges, the natural temptation is to assume that the bear case has already played out. But markets can stay irrational in both directions, and the question is whether the current valuation reflects a permanent impairment or a cyclical trough.

The Bull Case. Corsair bears have had the better of the argument for four years, but the bull case deserves a fair hearing because several things have genuinely changed.