Critical Metals Corp: From SPAC to Strategic Minerals Powerhouse

I. Introduction & Episode Roadmap

Picture this scene: October 14, 2025. A mining company that barely existed on Wall Street's radar just six months earlier hits $32.15 per share in frenzied trading. Rumors swirl through financial networks that the Trump administration might take a direct equity stake in the company. Chinese rare earth producers watch nervously as Western governments circle around Greenland's mineral deposits like chess pieces on a geopolitical board.

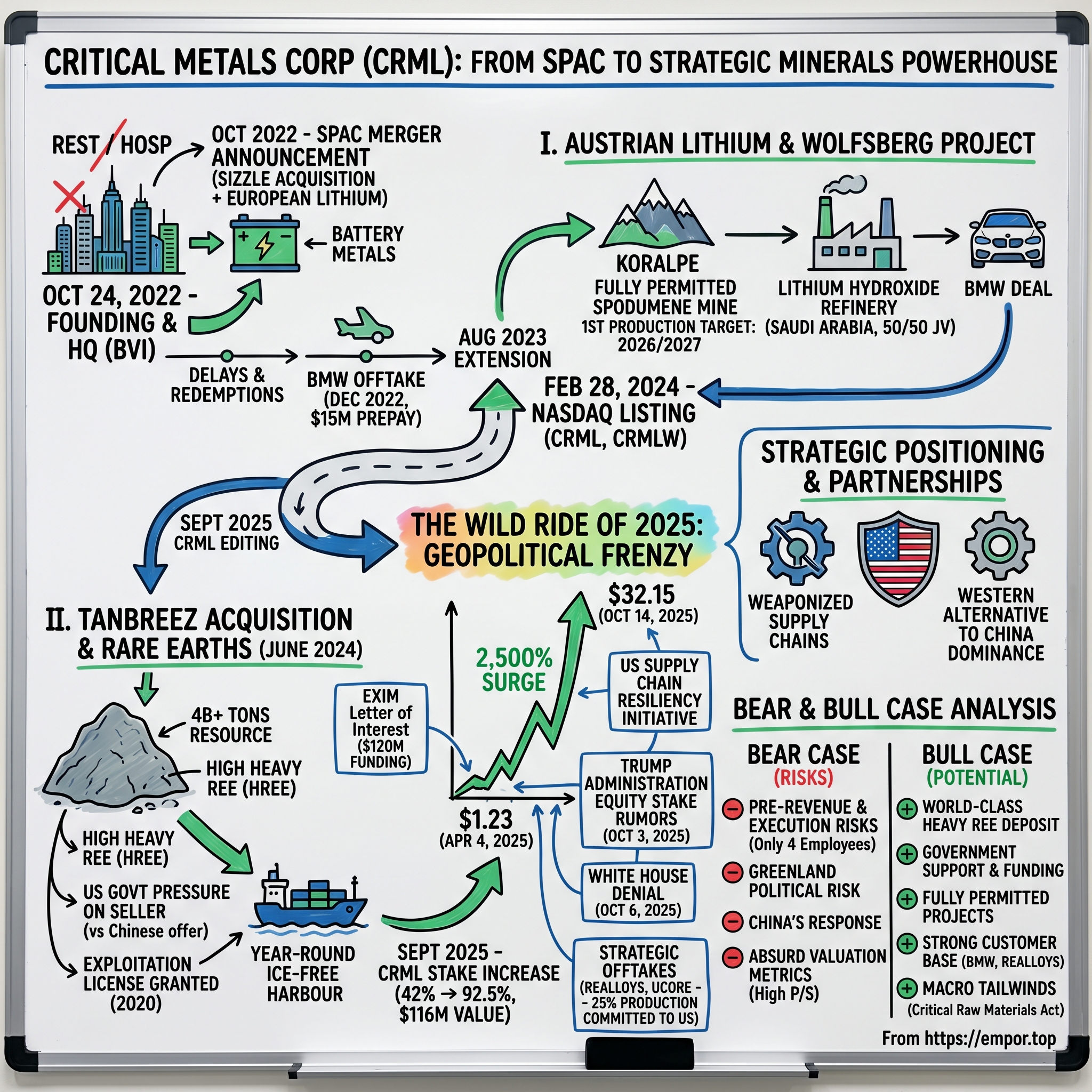

This is the story of Critical Metals Corp (NASDAQ: CRML), a company that reached its all-time high on October 14, 2025 at $32.15, after bottoming at just $1.23 on April 4, 2025. Founded on October 24, 2022 and headquartered in the British Virgin Islands, Critical Metals operates as a mining exploration and development company in Austria and Southern Greenland.

The company represents something far more significant than just another mining venture. It's become a proxy for the West's desperate scramble to break China's stranglehold on rare earth elements—those obscure materials with unpronounceable names that power everything from F-35 fighter jets to Tesla motors. In an era where supply chains have become weapons and minerals have become ammunition, Critical Metals sits at the intersection of geology and geopolitics.

What makes this story particularly compelling isn't just the 2,500% price surge in six months or the government intrigue. It's how a struggling Australian lithium explorer managed to transform itself through a SPAC merger into a potential cornerstone of Western critical mineral supply chains. This metamorphosis involved Austrian lithium deposits once explored by the Nazis, a Greenlandic rare earth deposit that makes Chinese competitors nervous, and enough financial engineering to make Wall Street veterans dizzy.

Our journey takes us from the alpine slopes of Austria's Koralpe mountains to Greenland's ice-free southern fjords, from SPAC conference rooms in Manhattan to the Pentagon's strategic minerals task force. Along the way, we'll encounter colorful characters like Tony Sage—the Perth-based mining entrepreneur who's been pushing this boulder uphill for years—and Gregory Barnes, the geologist who spent decades mapping what might be the world's most important rare earth deposit outside China. This isn't just a business story; it's a tale of how the periodic table became a battlefield.

II. Origins: European Lithium & The Wolfsberg Project

The mountains of Carinthia in southern Austria hold secrets that date back centuries. Local miners have long known about the strange, silvery minerals embedded in the pegmatite formations of the Koralpe range. But it wasn't until the 1980s that geologists began to understand what they were really looking at: one of Europe's potentially most significant lithium deposits, sitting just 270 kilometers southwest of Vienna.

The Wolfsberg project, wholly owned by European Lithium, is located in Carinthia, 20 km east of the industrial town of Wolfsberg, with established infrastructure including access to the European motorway and railway network. The project comprises 22 original and 32 overlapping exploration licenses and a mining license over 11 mining areas, with the mining license able to be held in perpetuity provided its conditions are maintained. The project benefits from significant exploration, extensive metallurgical testing, mining and pre-feasibility studies conducted by past owners.

Enter Tony Sage, a Perth-based entrepreneur with the kind of resume that reads like a business adventure novel—football club owner, mining promoter, eternal optimist. When Sage took the chairman role at European Lithium, he saw opportunity where others saw obstacles. As he commented about the company's 2017 Vienna Stock Exchange listing: "The listing provides a huge benefit to the company as it allows us to source new shareholders from this very wealthy constituency." That Vienna listing made European Lithium the first Australian company ever admitted to the Austrian exchange—a symbolic bridge between old-world mining tradition and new-world entrepreneurial energy.

The technical story of Wolfsberg is equally compelling. This isn't some speculative moose pasture; it's a deposit with over four decades of exploration data. The project is backed by exploration data dating back to the 1980s and boasts an S-K1300 compliant mineral resource that has advanced through multiple stages of technical validation—including detailed engineering assessments and a Definitive Feasibility Study—confirming both its economic viability and production potential.

But here's where the story gets interesting from a strategic perspective. The Wolfsberg lithium project represents the first fully permitted spodumene mine on the continent, with first production targeted for 2026/2027. In a Europe desperate to reduce its dependence on Chinese battery materials, having a fully permitted lithium mine ready to go is like holding four aces in a poker game where everyone else is still waiting for their cards.

The Austrian government understood this. According to Critical Metals, a decree was issued following an audit by official experts from departments including forestry, nature conservation, geology, and hydrogeology. The assessment covered the entire project on the Koralpe mountain range, and since the above-ground facilities required were less than 10 hectares, experts concluded no Environmental Impact Assessment was required by law.

What transformed Wolfsberg from a promising regional project into a strategic asset was the involvement of BMW. The German carmaker entered into a long-term lithium offtake agreement in December 2022 and made a prepayment of $15 million to the company. The BMW deal wasn't just about securing lithium; it was validation from one of Europe's industrial champions that Wolfsberg could deliver.

The December 2022 BMW agreement came at a crucial moment. As Tony Sage commented: "With the signing of the binding offtake agreement with BMW, our first offtake is secured, and we look forward to partnering with BMW in the future." BMW was granted the first right to purchase 100% of the lithium hydroxide produced from the identified resources, with an advance payment of US$15 million to be repaid through equal set offs against lithium hydroxide delivered.

Yet despite all these advantages, European Lithium faced a fundamental problem: scale and capital. The lithium market was experiencing wild swings, and raising money on the Australian Securities Exchange for a European project was proving challenging. The company's share price languished, and the dreams of becoming Europe's lithium champion seemed increasingly distant.

That's when the SPAC opportunity emerged. In the strange alchemy of 2021-2022's SPAC boom, where hundreds of blank-check companies searched desperately for targets, a marriage was arranged that would transform European Lithium's destiny. The matchmaker? Wall Street's endless appetite for battery metals and critical minerals stories.

III. The SPAC Merger: Sizzle Meets European Lithium (2022-2024)

The story of how European Lithium became Critical Metals reads like a financial thriller with multiple plot twists. It began in October 2022, when news broke that would fundamentally reshape the company's trajectory.

Sizzle Acquisition raised $155 million in a November 2021 IPO, initially to focus on target businesses in the restaurant, hospitality, food and beverage industries. At deal announcement in October 2022, the European Lithium transaction was expected to provide approximately $159 million before expenses and the impact of any redemptions.

Think about that for a moment—a SPAC originally hunting for restaurant deals ended up merging with an Austrian lithium miner. Only in the bizarre world of 2022 capital markets could such a pivot make perfect sense. But as strange as it seemed, the economics were compelling. The deal carried an implied pre-money equity value of $750 million and an enterprise value of approximately $838 million.

The path to closing, however, proved more tortuous than anyone anticipated. A vote on the proposed merger was postponed to February 15, 2024, after being rescheduled to February 9—and this was actually the third postponement, with the vote originally scheduled for January. Each delay ratcheted up the tension. Redemptions were eating away at the SPAC's trust like termites in wood.

What many outsiders didn't understand was the complex choreography happening behind the scenes. Sizzle Acquisition won a 6-month extension from shareholders to close the proposed merger, giving them until August 2023. This breathing room proved crucial, as the parties scrambled to secure the minimum funding requirements and navigate regulatory approvals.

The redemption tsunami that hit many SPACs didn't spare Sizzle. Since the IPO, redemptions had removed about 83% of Sizzle's trust, decimating the cash that would be available at closing. This meant that instead of the $155 million originally raised, only a fraction would actually flow to the combined company. The dream of a well-capitalized launch onto NASDAQ was evaporating.

Yet Tony Sage and his team pressed forward with characteristic determination. The delays, while frustrating, actually provided time to line up strategic pieces. The BMW offtake agreement announced in December 2022 gave the deal credibility. European institutional investors, particularly those focused on battery supply chains, began circling.

Finally, after five postponements and mounting skepticism, breakthrough came. European Lithium was to be renamed Critical Metals at deal closing, which was expected as early as February 27, 2024, when shareholders approved the merger.

This strategic move culminated in Critical Metals' ordinary shares and public warrants being listed on The Nasdaq Stock Market LLC with the symbols 'CRML' and 'CRMLW', respectively, from February 28, 2024.

The newly minted Critical Metals hit the NASDAQ boards with a thud rather than a bang. On its debut, CRML was up over 10%, but European Lithium shareholders still held a $1.2 billion stake in the company according to Critical Metals executive chairman Tony Sage. The math might have seemed optimistic, but Sage remained unfazed by both the initial stock price action and lithium market headwinds.

What the market initially missed was that this wasn't really a story about lithium anymore—or at least, not just about lithium. Behind the scenes, Critical Metals was already engineering its next transformation, one that would shift its focus from battery metals to rare earths, from Europe to Greenland, and from commercial markets to strategic government partnerships. The SPAC merger hadn't just provided a NASDAQ listing; it had created a platform for something much bigger.

IV. The Tanbreez Acquisition: Betting Big on Rare Earths (June 2024)

In the early months of 2024, while Critical Metals was still finding its feet as a newly public company, Tony Sage was orchestrating what would become the company's defining move. The target: a massive rare earth deposit in southern Greenland that had been quietly developed for decades by an Australian geologist named Gregory Barnes.

Gregory Barnes, the company's founder and CEO, is a geologist who has studied Greenland's minerals for many years and had been involved with both London Mining (planning to exploit iron ore deposits) and Greenland Minerals. Barnes wasn't your typical mining promoter. He was a technical geologistobsessed with the unique mineralogy of the Ilimaussaq Complex, one of Earth's most unusual geological formations.

The Tanbreez deposit itself reads like a geology textbook's fever dream. The deposit is a highly fractionated ortho-magmatic tantalum–niobium–zirconium–rare earth element deposit in the 1.13-billion-year-old Ilímaussaq intrusive complex. A conservative estimate specifies the resource at more than 4 billion tons, with average grades of 1.75% ZrO2, 0.18% Nb2O5, and 0.6% total rare earth oxides, of which heavy REE make up 30% (including yttrium).

But here's what made Tanbreez special—and what caught the attention of not just mining companies but governments: The deposit is projected to contain over 27% HREEs (heavy rare earth elements), a significant concentration far exceeding typical industry standards. This is critical, as HREEs are in much higher demand due to their superior value and essential role in high-performance applications—such as military-grade systems.

The acquisition announcement in June 2024 sent shockwaves through the rare earth industry. Critical Metals announced it had signed a binding heads of agreement to acquire a controlling interest in the Tanbreez Greenland Rare Earth Mine from Rimbal Pty Ltd, a company controlled by geologist Gregory Barnes. The transaction was valued at up to $211 million.

What most market observers didn't know was the backstory—a tale of geopolitical chess that would make Tom Clancy proud. Former President Joe Biden had successfully lobbied to have Tanbreez sold to Critical Metals for far less than a Chinese firm was offering. The Chinese had been prepared to pay significantly more, but Barnes, under pressure from U.S. officials, chose the Western buyer.

The technical advantages of Tanbreez were matched by its regulatory position. The project was permitted with an exploitation license to mine granted by the Greenland Government in 2020. In the world of rare earth mining, where permitting can take decades, having a license in hand was like having a royal flush.

Up to 2012, Tanbreez spent more than $40 million on developing the asset and submitted a definitive feasibility study to the Greenlandic government—a 19-volume submission weighing 33 kilograms carried out by Danish engineers MT Højgaard. This wasn't some grassroots exploration play; it was a project ready for development.

The strategic location couldn't have been better. As Barnes joked, "We are on what they call the banana coast, the warmest part of the country right in the south. We are on a natural harbour, and it is ice-free all year round" thanks to the Gulf Stream. This meant year-round shipping access—crucial for moving massive quantities of ore to processing facilities.

But the real masterstroke came in September 2025, when Critical Metals dramatically increased its stake. Under a revised agreement, Critical Metals raised its stake from 42% to 92.5% by issuing 14.5 million shares to Rimbal. The agreed price of $8 per share represented a 23% premium to Critical Metals' last close of $6.49, valuing the transaction at $116 million. Barnes waived an earlier requirement for Critical Metals to invest $10 million before qualifying for the increased stake.

This wasn't just about acquiring a mining asset. It was about positioning Critical Metals as the Western alternative to Chinese rare earth dominance. The timing couldn't have been better—or more fraught with geopolitical significance.

V. From $1.23 to $32: The Wild Ride of 2025

April 4, 2025, marked the nadir. CRML touched $1.23, a price that valued the entire company at barely more than the cash on its balance sheet. The lithium market had collapsed, SPAC stocks were toxic, and investors who'd bought into the Critical Metals story were nursing massive losses. It looked like another SPAC disaster story in the making.

Critical Metals reached its all-time high on October 14, 2025 with a price of $32.15, and its all-time low was $1.23 reached on April 4, 2025. That's a 2,500% move in just six months—the kind of return that turns $10,000 into $250,000, the kind of move that creates legends in trading floors and Reddit forums alike.

What triggered such a dramatic reversal? The catalyst came in June with news that would transform Critical Metals from a speculative mining play into a strategic asset. Critical Metals announced it received a Letter of Interest from the Export-Import Bank of the United States (EXIM) for $120 million in non-dilutive funding. Based on preliminary information, EXIM would consider financing up to $120 million with a repayment term of 15 years under EXIM's new Supply Chain Resiliency Initiative.

This wasn't just any loan. The proposed funding package was eligible for special consideration under EXIM's 2019 reauthorization, directing EXIM to mitigate the competitive impact of export support from China through the China and Transformational Exports Program (CTEP). In other words, the U.S. government was essentially backing Critical Metals as a counter to Chinese mineral dominance.

The summer months saw steady accumulation as smart money began to understand what was developing. The Tanbreez Project was expected to produce up to 85,000 metric tons of rare earth material annually, and the company planned to invest $10 million in exploration to increase ownership to 92.5%.

Then came October's explosion. The setup was perfect: a thinly traded stock with massive short interest, a game-changing asset in Greenland, and whispers of government involvement. When Reuters broke the news on October 3, the powder keg ignited.

Reuters reported that Trump administration officials had discussed taking a stake in the company whose flagship project, the Tanbreez mine in Greenland, is one of the world's largest rare earth deposits. The reaction was instantaneous and violent.

Shares surged over 70% as news broke about the Trump administration's consideration of an equity stake in CRML linked to securing Greenland's Tanbreez rare earths. Trading volumes exploded from typical daily volumes of a few hundred thousand shares to tens of millions. The stock was halted multiple times for volatility.

Critical Metals had applied in June for a $50 million grant through the Defense Production Act. In the last six weeks, though, the administration began discussions about converting the grant into an equity stake. The discussions reportedly centered on an 8% stake, though negotiations remained fluid.

But then came the whiplash. On October 6, 2025, a White House official said the Trump administration was not currently considering a deal that would see it take a stake in Critical Metals, after the report suggesting Washington was considering a position sent shares skyrocketing.

The stock didn't collapse on the denial. Why? Because sophisticated investors understood the game being played. The administration was in constant touch with the private sector and had received hundreds of deal proposals involving equity stakes, even if not actively considering an agreement with Critical Metals. The denial was carefully worded—"not currently considering"—leaving the door wide open.

More fuel came from strategic commercial agreements. In October, Critical Metals signed a Letter of Intent to supply 6,750,000 metric tons of rare earth concentrate to REalloys, representing 15% of production. REalloys is described as a vertically integrated U.S. rare-earth manufacturer supplying the U.S. National Defense Stockpile.

The stock hit its peak of $32.15 on October 14 before experiencing significant volatility, falling 19.8% to $24.04 on one day as traders took profits. The wild price action reflected a market trying to price in an unprecedented situation: a mining development company that might become a strategic asset of the U.S. government.

By late October, CRML had become one of the most volatile stocks on NASDAQ. Daily fluctuations of 22.22% from low to high were common, with Bollinger Bands indicating "very high risk." Options activity exploded as traders bet on continued volatility. This wasn't investing anymore; it was speculation on a geopolitical chess match.

VI. Government Interest: The Trump Administration Speculation (October 2025)

The morning of October 3, 2025, started like any other for Critical Metals shareholders. The stock was treading water around $11, still well off its April lows but hardly setting the world on fire. Then, at 7:33 PM GMT, Reuters dropped a bombshell that would transform everything.

Trump administration officials had discussed taking a stake in Critical Metals Corp, four people familiar with the discussions told Reuters, which would give Washington a direct interest in the largest rare earths project in Greenland, the Arctic territory that President Donald Trump once suggested buying.

The story behind the story was even more fascinating. This wasn't some random government interest in a mining company. It represented a fundamental shift in how the U.S. government viewed critical minerals—not just as commodities to be purchased on the open market, but as strategic assets requiring direct government involvement.

Washington had recently taken stakes in Lithium Americas and MP Materials, underscoring Trump's desire for the U.S. to benefit from growing production of minerals used across the global economy. The Critical Metals discussion was part of a broader pattern, but with a unique twist: it involved Greenland, a territory that had captured Trump's imagination since his first term.

The mechanism being discussed was clever. Critical Metals had applied in June for a $50 million grant through the Defense Production Act. In the last six weeks, though, the administration had begun discussions about converting the grant into an equity stake. This would give the government upside participation while avoiding the political optics of a direct cash investment.

Part of the discussion centered on how warrants would be issued to give Washington the stake. Warrants give holders the right to buy stock at a set price. This structure, similar to what the government had used with airlines during COVID, would allow taxpayers to benefit if Critical Metals succeeded.

The market reaction was explosive but also revealing. Shares of Critical Metals surged nearly 53% in premarket trading Monday following Reuters' initial report, reaching their highest levels since the company's public listing. What was particularly interesting was the volume—over 100 million shares traded that day, compared to typical volumes under 1 million.

Then came the government's response, delivered with the kind of calculated ambiguity that keeps markets guessing. The Trump administration was not currently considering a deal, a White House official said Monday, after the report sent shares skyrocketing. Note the careful wording: "not currently considering." Not "will never consider" or "has no interest in." The door remained conspicuously open.

Behind the scenes, the discussions reflected a broader strategic recalculation. "Hundreds of companies are approaching us trying to get the administration to invest in their critical minerals projects," according to a senior Trump administration official. The challenge wasn't finding opportunities; it was choosing which ones aligned with strategic priorities.

The Greenland angle added another dimension. Trump's renewed interest in Greenland wasn't just about rare earths—it was about Arctic sovereignty, shipping routes, and countering Chinese influence in a strategically vital region. Critical Metals, with its Tanbreez project, offered a way to establish an economic foothold.

The equity stake would be separate from a $120 million loan the U.S. Export-Import Bank was considering to help develop Tanbreez. This two-pronged approach—debt plus equity—would give the government both security and upside, a structure that had been successfully used in other strategic sectors.

The Pentagon's interest was particularly acute. Tanbreez contains significant quantities of neodymium-praseodymium (NdPr) used in magnets, but crucially also dysprosium, terbium, and other heavy REEs needed for high-temperature magnets in EV motors and missiles. These weren't just commercial materials; they were defense-critical assets.

Geologist Gregory Barnes agreed to sell to Critical Metals in 2024 after U.S. officials (the Biden administration at the time) lobbied to block a higher offer from a Chinese buyer, ensuring this strategic asset remained in Western hands. The government's interest in potentially taking a stake was the logical next step in this strategic chess game.

Market participants began to realize this wasn't just about one company or one mine. It was about the weaponization of supply chains and the new great game for critical minerals. Countries that controlled these resources would have leverage in everything from electric vehicles to missile defense systems. The speculation around government involvement had transformed Critical Metals from a mining development story into a geopolitical play.

VII. Strategic Positioning & Partnerships

While the headlines focused on stock price gyrations and government intrigue, Critical Metals was quietly assembling a web of strategic partnerships that would define its future. This wasn't just about digging rocks out of the ground—it was about building an entire supply chain architecture for the Western world.

The crown jewel of these partnerships came in October 2025 with REalloys. REalloys' Euclid, Ohio facility supplies advanced rare earth metals and magnet materials to the U.S. Defense Logistics Agency and the DOE Ames National Laboratory, supporting critical defense, energy, and strategic manufacturing initiatives. Under the multi-year offtake arrangement, Critical Metals would supply up to 6,750,000 metric tons of rare earth concentrate, representing approximately 15% of projected production.

"The Tanbreez project presents a remarkable opportunity for REalloys, given its rich, long-life deposits of heavy rare earth elements—vital to the defense industrial base of the United States and our allied nations," said Leonard Sternheim, Chairman of REalloys.

But REalloys was just one piece of the puzzle. Critical Metals had also secured an agreement with Ucore Rare Metals for another 10% of production, meaning 25% of Tanbreez output was already committed to U.S. customers before the first shovel hit the ground. This wasn't random customer acquisition—it was strategic positioning to become indispensable to Western supply chains.

The technical development strategy for Tanbreez showed sophisticated thinking about market entry. Critical Metals' March preliminary economic assessment valued Tanbreez at a pre-tax net present value of $3.04 billion, with an internal rate of return of 180%. These weren't just impressive numbers—they were almost unbelievable for a mining project. The key was the phased approach.

Rather than trying to build a massive operation from day one, the plan followed a modular growth strategy. Initial production would target around 85,000 tonnes of rare earth oxides per annum, scalable to 425,000 tonnes after expansion. This reduced upfront capital requirements while proving the concept to skeptical markets and governments.

On the lithium side, the BMW relationship continued to deepen. BMW had made a $15 million prepayment, and to convert the lithium concentrate from Wolfsberg, Critical Metals teamed up with the Obeikan Group in July to build a lithium hydroxide processing plant in Saudi Arabia. This Middle Eastern connection was unexpected but brilliant—Saudi Arabia had capital, ambition in battery technology, and strategic location between European and Asian markets.

Once commissioned, the refinery under a 50/50 joint venture would produce up to 20,000 tonnes of battery-grade material. It would be the first lithium hydroxide processing plant within the Middle East North Africa region.

The geographic diversification was intentional. Austrian lithium for European batteries, Greenlandic rare earths for American defense systems, Saudi processing for global markets. Each piece reinforced the others, creating what strategists call "defense in depth."

Critical Metals was also working the government relations angle hard. The company had held supply talks with defense contractor Lockheed Martin, among others. These weren't casual conversations—they were strategic discussions about securing supply chains for next-generation weapons systems.

The permitting advantages couldn't be overstated. While competitors struggled for years to get approvals, Critical Metals had inherited fully permitted projects. Wolfsberg was expected to be the first licensed lithium mine in Europe. In Greenland, the exploitation license was already in hand. In a world where permitting could take 10-15 years, this was like starting a marathon 20 miles ahead of the competition.

What made the partnership strategy particularly clever was how it addressed the classic junior miner dilemma: how to fund development without diluting shareholders into oblivion. By securing offtake agreements with prepayments, government loans, and strategic investors, Critical Metals was assembling a financing package that minimized dilution while maximizing strategic value.

The company was also positioning itself at the intersection of multiple government initiatives. The EU's Critical Raw Materials Act, the U.S. Defense Production Act, various national stockpiling programs—Critical Metals had relevance to all of them. This wasn't just opportunistic; it was systematic alignment with Western strategic priorities.

VIII. Bear & Bull Case Analysis

Every spectacular stock story has two sides, and Critical Metals presents one of the starkest contrasts between bear and bull cases in the entire market. Let's examine both with the cold analysis of an institutional investor weighing a position.

The Bear Case: A House of Cards?

The numbers alone should make any rational investor run screaming. In 2025, Critical Metals's revenue was $560,623, an increase of 376.48% compared to the previous year's $117,660. That sounds impressive until you realize the company's market cap peaked at over $2.5 billion. We're talking about a price-to-sales ratio that would make even the most aggressive tech investor blush.

The valuation metrics are genuinely absurd. The company has a colossal price-to-sales ratio of 2856.41, indicating the market may be overvaluing its revenue generation capability. Their enterprise value of $1.6 billion is undermined by a meager revenue base.

Then there's the pre-revenue nature of the actual projects. Neither Wolfsberg nor Tanbreez is producing anything yet. Wolfsberg targets first production for 2026/2027, while Tanbreez is expected to produce up to 85,000 metric tons annually at some future date. That's at least a year away for Wolfsberg, potentially longer for Tanbreez. A lot can go wrong in that time.

The Greenland risk is real and multifaceted. Yes, they have permits, but Greenland's politics are complex. Environmental groups are increasingly active. The Danish government, which ultimately controls Greenland's foreign policy, might have different ideas than local authorities. One political shift could freeze the project.

China's response remains the elephant in the room. China currently dominates the sector, accounting for about 60% of global rare earth production and 85% of processing capacity. In 2023, its production totaled 240,000 tonnes, nearly six times that of the United States. If China decides to flood the market and crash prices—a tactic it's used before—Critical Metals' economics could evaporate.

The execution risk is massive. Mining is hard. Processing rare earths is harder. Building supply chains from scratch is hardest of all. The company has 4 employees as of October 2025. Four. They're attempting to build two major mining operations on different continents with a team smaller than a coffee shop.

The Bull Case: The Next MP Materials?

But then again, MP Materials went from $10 to $60 based on a similar thesis, and Critical Metals arguably has better assets. Let's make the bull case.

First, the resource base is genuinely world-class. The Tanbreez project contains one of the world's largest untapped heavy rare earth deposits, with more than 27% HREE content and an estimated 4.7 billion tonnes of host rock. This isn't some marginal deposit—it's a potential game-changer for Western supply chains.

The government support thesis is compelling even without direct equity investment. EXIM's $120 million funding with 15-year repayment terms would be sufficient for Critical Metals to complete necessary technical studies, pre-production activities, and begin mining. This de-risks the funding question significantly.

The strategic positioning is perhaps unmatched. Critical Metals owns the first fully permitted lithium mine in Europe and a permitted rare earth mine in Greenland. In an industry where permitting is the biggest bottleneck, they've already cleared the highest hurdles.

The customer quality is exceptional. BMW for lithium, REalloys and Ucore for rare earths, potential Lockheed Martin involvement—these aren't speculative customers but blue-chip Western industrials with strategic needs for these materials. The 25% of production already committed to U.S. customers provides revenue visibility most junior miners can only dream of.

The macro tailwinds are hurricane-force. Every Western government is scrambling to secure critical mineral supplies. The EU's Critical Raw Materials Act, the U.S. Inflation Reduction Act, various defense initiatives—all create massive demand for exactly what Critical Metals offers. This isn't a cyclical commodity play; it's a structural shift in how the West thinks about supply chains.

The valuation, while high on current metrics, might be cheap on future production. If the Tanbreez NPV of $3.04 billion is even half right, the current enterprise value of $1.6 billion suggests significant upside. The 180% IRR implies cash flows that could justify much higher valuations.

Finally, there's the optionality value. If the U.S. government does take a stake, if Tanbreez becomes a Western strategic asset, if the lithium market recovers strongly—any of these could send the stock multiples higher. The risk-reward for aggressive investors might be compelling.

IX. Playbook: Lessons for Founders & Investors

The Critical Metals story, regardless of how it ultimately ends, offers a masterclass in financial engineering, strategic positioning, and riding macroeconomic waves. Let's extract the key lessons that founders and investors can apply to their own ventures.

Lesson 1: Timing the Pivot

The transformation from European Lithium (struggling ASX lithium explorer) to Critical Metals (NASDAQ-listed critical minerals platform) wasn't just a rebrand—it was a fundamental strategic pivot executed at exactly the right moment. When lithium markets collapsed in 2024, instead of doubling down, management pivoted to rare earths just as government interest in securing supplies peaked.

The key insight: don't be wedded to your original thesis. Tony Sage started with Austrian lithium but recognized that rare earths offered better strategic value. The ability to evolve the investment thesis while maintaining core operational strengths (mining expertise, government relations) separated Critical Metals from dozens of failed SPAC combinations.

Lesson 2: The SPAC Arbitrage

Despite Sizzle raising $155 million in its IPO, redemptions removed about 83% of the trust. Most people would see this as a disaster. Sage saw it as an opportunity. With most of the original SPAC investors gone, he could rebuild the shareholder base with investors who understood the strategic minerals thesis.

The playbook: Use the SPAC not for its cash (which will likely be redeemed) but for its public listing, regulatory compliance, and ability to tell your story to U.S. institutional investors. The listing itself was worth far more than the depleted trust funds.

Lesson 3: Government Relations as a Moat

Critical Metals didn't just benefit from government interest—they actively cultivated it. The progression from Biden administration pressure on the Tanbreez seller, to EXIM financing, to Trump administration equity discussions wasn't accidental. The company positioned itself as the solution to a government problem.

For founders: identify where your business intersects with government strategic priorities. Don't wait for the government to find you; proactively engage with relevant agencies, understand their pain points, and position your company as the answer.

Lesson 4: Strategic Customers > Financial Investors

The BMW offtake agreement and REalloys partnership weren't just commercial deals—they were strategic validations that changed the company's trajectory. These blue-chip customers provided credibility that no amount of promotional activity could match.

The lesson: prioritize strategic customers who need your product for their own strategic reasons. They'll provide patient capital, technical expertise, and credibility that purely financial investors cannot match.

Lesson 5: Permitting as a Competitive Advantage

In the mining world, having permits is like having a patent that actually works. Both Wolfsberg and Tanbreez came with existing permits—advantages that would take competitors 5-10 years and millions of dollars to replicate.

For investors: look for companies that have already cleared regulatory hurdles. For founders: if you're in a regulated industry, prioritize regulatory compliance and permitting. It's tedious, expensive, and time-consuming—which is exactly why it becomes a moat.

Lesson 6: The Power of Scarcity Narrative

Critical Metals benefited enormously from the scarcity narrative around critical minerals. They didn't create this narrative—geopolitical tensions did—but they positioned themselves perfectly to benefit from it. Every China supply chain scare, every defense department warning about mineral dependence, effectively marketed their company for free.

The playbook: identify macro narratives that will persist for years, not months. Position your company as the beneficiary of these structural trends. Let the macro story do your marketing.

Lesson 7: Managing Extreme Volatility

From $1.23 to $32.15 in six months represents volatility that would break most management teams. Critical Metals managed it by focusing on operational milestones rather than stock price, maintaining consistent messaging, and using the volatility to their advantage (raising capital on spikes).

The key: build a thick skin and a long-term perspective. Extreme volatility attracts speculators, but it also attracts strategic investors looking for asymmetric opportunities. Use the quiet periods to build, and the volatile periods to raise capital and sign deals.

X. Epilogue: What's Next?

As we write this in late 2025, Critical Metals stands at an inflection point. The stock has pulled back from its October highs but remains up several hundred percent from its April lows. The company has transitioned from story to execution. The next 24 months will determine whether this becomes a case study in value creation or a cautionary tale about SPAC excess.

The immediate milestones are clear. Wolfsberg is targeting first production in 2026/2027, while Critical Metals expects to complete a definitive feasibility study for Tanbreez by the end of 2025. These aren't distant promises anymore—they're near-term deliverables that will either validate or invalidate the investment thesis.

The construction phase at Wolfsberg represents the first major test. Mining construction projects are notorious for cost overruns and delays. With BMW waiting for lithium hydroxide and the Saudi processing plant depending on concentrate, any significant delays could cascade through the entire strategy. Success here would provide credibility for the larger Tanbreez development.

Tanbreez requires $290 million in capital expenditure to reach initial commercial production of 85,000 metric tons annually. Even with EXIM's $120 million, there's a funding gap. How Critical Metals bridges this—strategic investors, additional government support, or capital markets—will signal whether the company can execute on its ambitious plans.

The competitive landscape is intensifying. Energy Transition Minerals (formerly Greenland Minerals) continues developing its Kvanefjeld project despite uranium controversies. Australian companies are racing to develop their own rare earth resources. Chinese companies aren't standing still either, expanding production and locking up resources globally. Critical Metals' first-mover advantage in Western supply chains is real but fragile.

The technology evolution adds another variable. Rare earth recycling technologies are improving rapidly. Motor designs that use less rare earth content are in development. Solid-state batteries might reduce lithium demand. While these transitions will take years, they add uncertainty to long-term demand projections.

Government policy remains the biggest wildcard. Will the U.S. government actually take equity stakes in mining companies? Will the EU's Critical Raw Materials Act translate into meaningful support for projects like Wolfsberg? Will Greenland's government maintain its mining-friendly stance? Each policy decision could dramatically impact Critical Metals' trajectory.

The macroeconomic environment has shifted dramatically since the October highs. Interest rates remain elevated, making project financing more expensive. Recession fears could dampen electric vehicle demand. China's economic slowdown might reduce rare earth demand—or prompt them to flood markets to maintain employment. These macro crosscurrents will buffet Critical Metals regardless of execution.

Yet the strategic logic remains compelling. The West needs secure supplies of critical minerals. China's dominance of these supply chains represents an unacceptable strategic vulnerability. Companies like Critical Metals, whatever their current valuation excesses, are attempting to solve a real problem with real assets. That's more than most SPACs can claim.

What success looks like in 3-5 years: Wolfsberg producing battery-grade lithium for European automakers, Tanbreez providing rare earths for Western defense contractors, and Critical Metals established as a cornerstone of Western critical mineral supply chains. The stock price would follow, but more importantly, the company would have achieved something strategically significant.

The bear case remains equally plausible: delays, cost overruns, financing challenges, and competitive responses combining to prevent Critical Metals from achieving its ambitious goals. The stock could easily return to its April lows if execution falters or market sentiment shifts.

For investors, Critical Metals represents a fascinating risk-reward proposition. For policymakers, it's a test case for whether the West can build alternative supply chains. For competitors, it's either a model to emulate or a cautionary tale to avoid. For all of us, it's a window into how the intersection of geology, technology, and geopolitics is reshaping the global economy.

The story of Critical Metals is far from over. Whether it ends as triumph or tragedy, it's already provided lessons in financial engineering, strategic positioning, and the new great game for critical minerals. In a world where supply chains have become weapons and minerals have become ammunition, companies like Critical Metals aren't just investments—they're bets on the future architecture of global power.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube