Charles River Laboratories: The Preclinical Machine

I. Introduction & Episode Roadmap: The Anatomy of the Preclinical Machine

Picture a clean room somewhere in Massachusetts. Behind a series of air-locked doors, past showers and gowning stations and pressure gradients designed to keep the outside world out, sit rows upon rows of laboratory mice — genetically defined, pathogen-free, each one a precision instrument rather than an animal. A few hundred miles south, along a brackish stretch of the Atlantic coast, technicians lift horseshoe crabs from holding tanks, extract a measured volume of their pale blue blood, and return them to the sea. And in a breeding facility in rural Cambodia, thousands of cynomolgus macaques sit at the very front of a supply chain that the entire modern biotechnology industry quietly depends on.

These three images — the mouse, the crab, and the monkey — are the unglamorous foundations of Charles River Laboratories International, Inc. (NYSE: CRL). It is one of the most important companies in medicine that most people have never heard of. By the company's own accounting, Charles River was involved in the development of the overwhelming majority of novel drugs approved by the U.S. Food and Drug Administration in recent years — management has cited figures north of 85% of FDA-approved novel drugs touching its services at some stage.1 If pharmaceutical companies are prospectors hunting for the next blockbuster, Charles River sells them the picks, the shovels, the assay maps, and increasingly the land itself.

But this is not a hagiography. The Charles River of mid-2026 is a company that has just been turned inside out, and the story of how and why is the most interesting thing about it.

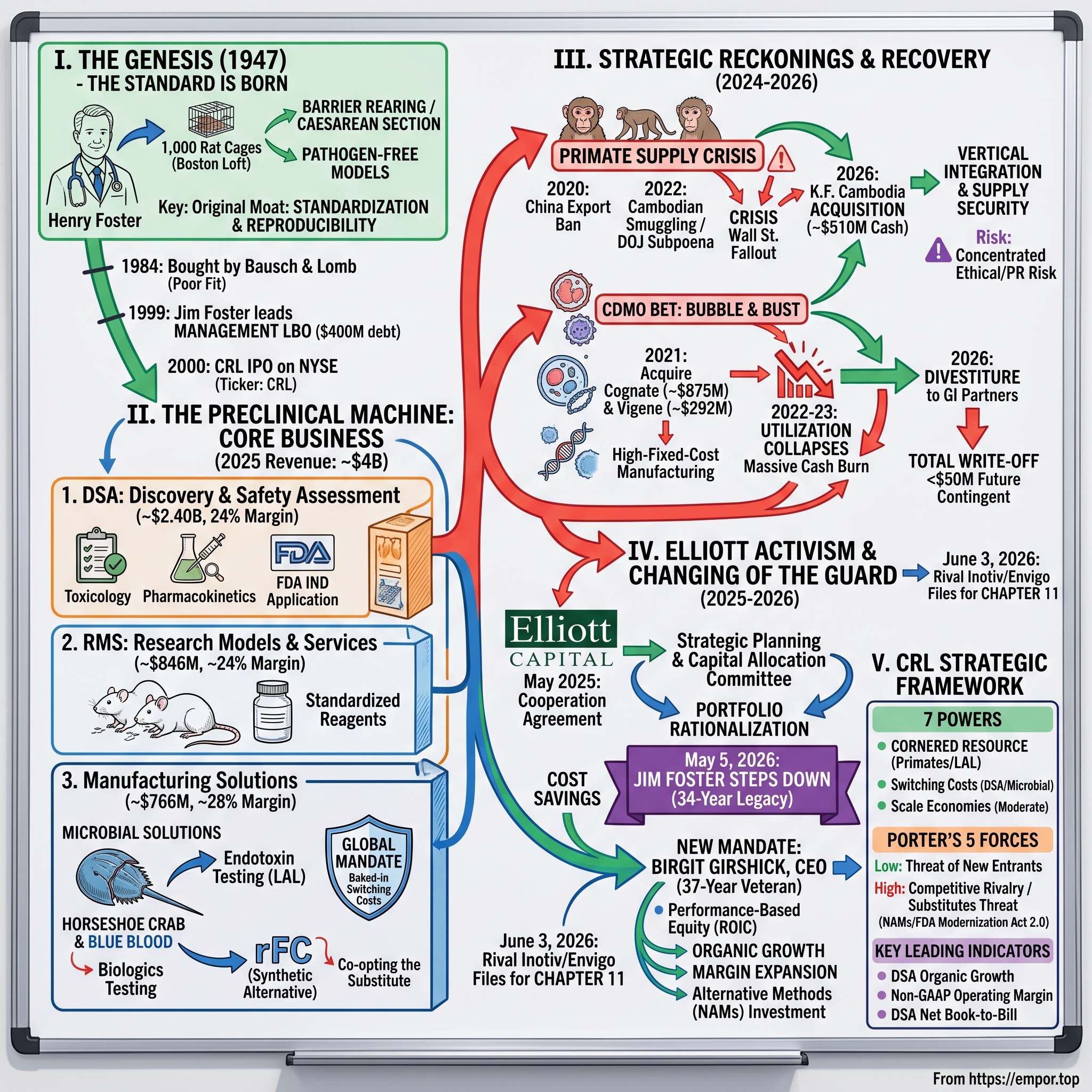

Consider the last six months. After activist investor Elliott Investment Management disclosed a major position and entered a cooperation agreement with the company in May 2025,9 the cascade of change has been relentless. In January 2026, Charles River moved to vertically integrate the most vulnerable link in its supply chain, agreeing to acquire its long-time Cambodian primate supplier, K.F. (Cambodia) Ltd., for roughly $510 million in cash.12 In February 2026, it executed a near-total retreat from a billion-dollar bet on cell and gene therapy manufacturing — divesting its CDMO and cell solutions businesses to private equity firm GI Partners on terms that amounted to a confession, while simultaneously selling European Discovery Services assets to IQVIA for $145 million.47 On May 5, 2026, James C. "Jim" Foster stepped down as CEO after a 34-year run, handing the company to Birgit Girshick, herself a 37-year veteran.6 And on June 3, 2026, the company's largest commercial rival in research models — Inotiv, the owner of Envigo — collapsed into Chapter 11 bankruptcy.8

That is an astonishing amount of corporate seismic activity for a 79-year-old business that breeds rats. So here is the thesis we will test over the next several sections. Charles River is, on one hand, a masterclass in what the strategist Hamilton Helmer calls a "cornered resource" — control of scarce, regulation-mandated inputs that the entire industry must buy. On the other hand, it is a cautionary tale about empire-building at the top of a cycle, about the difference between a service business and a manufacturing business, and about how an industry built on living animals is structurally exposed to ethics, geopolitics, and the boom-bust rhythm of biotech funding. Both things are true at once. Let's start at the beginning — with a thousand second-hand rat cages.

II. The Genesis: Henry Foster, 1,000 Rat Cages, and the LBO of 1999

In 1947, a young veterinarian named Henry Foster did something that, in retrospect, looks either visionary or slightly mad. He bought 1,000 second-hand rat cages from a farm in Virginia, rented a second-floor loft in Boston overlooking the Charles River, and started breeding rats. Then he delivered them himself, in his own car, to the universities and hospitals scattered around the city.15

It is worth sitting with how humble this beginning was. There was no venture capital, no grand strategy deck, no addressable-market analysis. There was a man, a river, and a conviction that biomedical researchers needed something they did not yet have: a reliable animal. Because in the 1940s and 1950s, that was the central, maddening problem of laboratory science. Animals used in research were, to put it bluntly, dirty. A researcher in New York might test a compound on rodents carrying respiratory disease; a colleague in Chicago might run the same experiment on rats riddled with parasites. When their results disagreed — and they constantly did — nobody could tell whether the difference reflected the drug or the diseases the animals happened to be carrying. Science cannot be science if the experiment cannot be replicated, and the unstandardized animal made replication nearly impossible.

Henry Foster's genius was to recognize that the animal itself was a reagent — and that a reagent must be standardized. After moving operations to Wilmington, Massachusetts, Foster pioneered what became known as barrier rearing and the production of "pathogen-free" animals: breeding colonies kept behind elaborate biosecurity barriers, derived by caesarean section to break the chain of maternal infection, raised in filtered air and sterile conditions.15 The result was a laboratory animal that was genetically consistent and microbiologically clean — a rat in Boston that was, for experimental purposes, identical to a rat shipped to a lab in California. Foster had effectively invented the idea of the research model as an industrial product. He didn't just sell rats; he sold reproducibility.

This is the original moat, and it is worth naming the mechanism plainly: once the scientific community and, crucially, the regulators came to accept Charles River's pathogen-free models as the standard, anyone wanting their results trusted had a strong incentive to use the same standardized inputs. Standardization is a quiet but powerful form of lock-in.

For decades, Charles River grew steadily as a private company. Then, in 1984, eye-care giant Bausch & Lomb bought it for $108 million.15 On paper, this made little sense, and in practice it made even less. Bausch & Lomb's world was Ray-Ban sunglasses and contact lenses — consumer optics. Charles River's world was breeding genetically engineered mice for pharmaceutical toxicology. Under Bausch & Lomb's ownership, Henry's son, James C. Foster — a lawyer by training who had joined the family business in 1976 — rose to become CEO in 1992. But by the late 1990s, the lack of strategic fit was glaring. A consumer-products conglomerate had no idea how to value, let alone nurture, a specialized life-sciences infrastructure business buried inside it.

So Jim Foster did what ambitious operators trapped inside an indifferent parent often do: he bought the company out. In 1999, Foster led a management-led leveraged buyout valued at roughly $400 million, backed by the merchant bank Donaldson, Lufkin & Jenrette.15 An LBO loads a company with debt; the discipline of servicing that debt forces focus. And then, in a beautifully timed double-play, Charles River went public on the New York Stock Exchange in 2000 under the ticker CRL, using the IPO proceeds to pay down the buyout debt and arm the balance sheet for an aggressive era of global acquisitions.

In the span of about a year, Jim Foster had liberated the family business, refinanced it through public markets, and set the stage for a two-decade buying spree. What he built on top of that foundation — and what he very nearly destroyed near the end — is the rest of our story. But first, we need to understand exactly what Charles River does, and why drug companies pay it billions of dollars a year to do it.

III. The Preclinical Core: DSA, RMS, and the Economics of Drug Development

To understand Charles River, you have to understand where it sits in the long, brutal journey of a drug. A pharmaceutical molecule begins as an idea, becomes a compound, gets tested in cells and then in animals, and only after clearing those preclinical hurdles is it allowed anywhere near a human being. Charles River lives in that preclinical stretch — the years before the first patient, where most of the money is spent and most of the candidates die.

In fiscal 2025, the company generated total revenue of roughly $4.02 billion, organized into three reportable segments.23 Let's walk through them, because the segment mix tells you almost everything about the business model.

The largest engine is Discovery and Safety Assessment, or DSA, which produced about $2.40 billion — roughly 60% of revenue — at a non-GAAP operating margin in the neighborhood of 24%.23 This is the heart of the modern Charles River. Once a biopharma company has a promising drug candidate, regulators require a battery of studies before it can file an Investigational New Drug application and begin human trials: toxicology to see what doses cause harm, pharmacokinetics to track how the body absorbs and clears the compound, safety pharmacology to probe effects on the heart, lungs, and nervous system. This work is performed under Good Laboratory Practice, a rigorous regulatory framework, and much of it must be done in living systems. It is exacting, heavily audited, and slow — and it is exactly the kind of work a small biotech has neither the facilities nor the expertise to do itself.

The second segment, Research Models and Services (RMS), is the historic cash cow — the direct descendant of Henry Foster's rat loft. In 2025 it generated about $846 million, roughly 21% of revenue, at margins similar to DSA.23 This is the business of breeding and selling those standardized rodents and larger models to academic, government, and commercial labs around the world. It grows slowly, but it is the foundation of the brand and the relationships.

The third segment, Manufacturing Solutions, produced about $766 million — roughly 19% of revenue — but at the highest margin of the three, around 28-29% on a non-GAAP basis.23 After the 2026 divestiture of the loss-making CDMO operations, this segment is a cleaner, consumable-led business centered on Microbial Solutions (endotoxin testing — more on the horseshoe crabs later) and biologics testing. We will return to why this is the crown jewel.

So why do drug companies outsource all of this rather than build it themselves? The answer is fixed cost. Maintaining sprawling, high-security, disease-free animal facilities, GLP-compliant toxicology labs, and the global regulatory machinery to run them is enormously capital-intensive — and for any individual biotech, the demand is lumpy and unpredictable. By outsourcing to Charles River, a drug developer converts a massive, idle fixed cost into a variable, on-demand cost it pays only when it needs a study run. Charles River, in turn, aggregates that demand across thousands of customers and runs its expensive facilities at high utilization. That is the fundamental economic logic of the contract research organization, or CRO.

It also explains the competitive landscape. In research models, Charles River is the global commercial leader with roughly 30% market share. Its most distinctive rival is The Jackson Laboratory, or JAX, a non-profit that holds roughly 16% of the market and functions as the genetic reference source for laboratory mice — a different animal entirely, run as a research institution rather than a profit machine. Privately held Taconic Biosciences specializes in genetically engineered models, and Europe's Janvier Labs rounds out the field.13 On the preclinical safety side, Charles River competes with Labcorp's toxicology operations and, significantly, with the Chinese giants WuXi AppTec (无锡药明康德 WuXi AppTec) and Pharmaron (康龙化成 Pharmaron) — a competitive fact that will become enormously important later in our story.

And then there is Inotiv, owner of the Envigo brand, which until very recently was Charles River's chief commercial rival in both research models and preclinical services. We will save the details, but as of June 3, 2026, Inotiv no longer poses the threat it once did — it is in bankruptcy.8 That reshaping of the competitive map is one of several reasons the Charles River of mid-2026 looks so different from the company of even two years ago. To understand how it nearly went very differently, we have to go back to 2010, and to the deal that didn't happen.

IV. The 2010 Crossroads: JANA Partners and the $1.6B Failed WuXi Gamble

By 2010, Jim Foster wanted a defining deal — the kind of transaction that changes a company's destiny. He found his target in WuXi PharmaTech, the fast-growing Chinese drug-research powerhouse. The logic was seductive. Charles River had world-class preclinical safety and toxicology capabilities, concentrated in the high-cost West. WuXi had enormous, low-cost chemistry and discovery capacity in China, growing at a blistering pace. Bolt them together and you would have an end-to-end, globe-spanning drug-development platform — Western rigor married to Chinese scale and cost. Charles River agreed to acquire WuXi for approximately $1.6 billion.10

It is the kind of deal that looks brilliant on a strategy slide. Shareholders saw something else.

Enter Barry Rosenstein and JANA Partners, the activist hedge fund, which had accumulated a stake of roughly 7%.14 JANA launched a ferocious, very public campaign to kill the deal, and its arguments were a clinic in activist skepticism. First, Charles River was overpaying — the price embedded heroic assumptions. Second, the touted synergies between a Massachusetts animal-toxicology business and a Shanghai chemistry shop were speculative; the two operations served overlapping but not identical customers, and "cross-selling" is the most over-promised word in M&A. Third, and most damning, integrating a large, fast-growing Chinese operation carried serious execution and governance risk for an American company with no real experience operating at scale in China.14 Other large holders, including Relational Investors, joined the chorus of dissent.

What happened next is the part worth remembering. Facing what looked like certain defeat in a shareholder vote, Charles River abandoned the acquisition in late July 2010, paid WuXi a $30 million termination fee, and pivoted immediately to a $500 million stock repurchase program to mollify investors.10 Management had wanted to conquer the world; shareholders made it buy back its own stock instead.

Now, here is where the historian's "what-if" gets genuinely fascinating, and where we should resist the temptation toward neat narratives. In the moment, blocking the WuXi deal looked purely like a defensive, value-protecting move — stop the empire-builder from overpaying. And had the deal closed, Charles River would have owned what became, through the 2010s, one of the fastest-growing CRO platforms on earth. In that sense, the shareholders who blocked it arguably cost the company a decade of compounding growth.

But fast-forward to the period of 2024 through 2026, and the picture inverts. WuXi AppTec — the broader entity that grew out of that ecosystem — now faces an existential threat in the United States from the proposed bipartisan Biosecure Act, federal legislation designed to bar Chinese biotech firms from U.S. government-linked contracts on national-security grounds. A Charles River that had spent the 2010s fusing itself to a Chinese discovery engine would, in 2026, be carrying a geopolitical landmine on its balance sheet. The deal the shareholders forced management to walk away from in 2010 may well have saved the company from a catastrophe fifteen years later.

The lesson is not that activists are always right, or that Foster was always wrong. It is subtler: in capital allocation, the deals you don't do can matter as much as the deals you do, and the consequences of either can take a decade to reveal themselves. That tension between an ambitious CEO and skeptical capital would recur — and the next time, the stakes were biological as well as financial. Because by the early 2020s, Charles River's most acute vulnerability wasn't in China. It was in a monkey.

V. The Primate Cartel: Cambodian Smuggling, DOJ Subpoenas, and the $510M Vertical Integration Masterstroke

Here is a fact that surprises almost everyone outside the industry: the entire modern biotech revolution — monoclonal antibodies, gene therapies, the most sophisticated biologic drugs of our age — runs through a bottleneck shaped like a monkey.

The reason is biological and unavoidable. The standardized rodents that Henry Foster built an empire on are wonderful for testing traditional small-molecule chemical drugs. But the new generation of biologic medicines are large, complex proteins engineered to bind to specific human receptors — and those receptors often simply don't exist, in compatible form, in a rat or a mouse. The drug glides past the rodent's biology without engaging it, telling you nothing. To get a meaningful safety read, you frequently need a non-human primate whose physiology closely resembles ours — specifically, the cynomolgus macaque. The macaque is, in effect, the ultimate gatekeeper of the modern biotech pipeline. No macaques, no safety data; no safety data, no human trials.

For years this dependency hummed along quietly because China supplied roughly 80% of the world's research macaques.13 Then, in 2020, the bottom fell out. As COVID-19 spread, China banned all exports of non-human primates, both to study the virus domestically and as a matter of biosecurity.13 Overnight, 80% of global supply vanished. The industry turned, desperately, to the one place that could scale fast enough: Cambodia. Cambodian exporters became the dominant global source almost overnight — but demand for primates, already surging on the back of a biologics boom, far outstripped what legitimate captive breeding could supply. When demand vastly exceeds honest supply, the conditions for fraud are perfect.

The reckoning came in November 2022 and rolled into 2023. The U.S. Department of Justice indicted Cambodian forestry officials and a major breeding supplier, alleging a scheme to capture endangered wild macaques from the forest and launder them through breeding facilities with falsified paperwork claiming they were "captive-bred."13 This was not a minor compliance footnote. Wild-caught endangered animals are illegal to trade, they carry unknown pathogens that destroy the scientific value of a study, and they sit at the center of international wildlife-protection law. Charles River, as a major importer of Cambodian macaques, received a federal grand jury subpoena and — facing the prospect of unknowingly importing laundered wild animals — voluntarily suspended imports from Cambodia.

The consequences rippled through the whole company. With its primary primate supply frozen, Charles River's DSA segment hit a wall: studies that required macaques couldn't be scheduled, margins compressed under the weight of underutilized capacity and scarce, expensive animals, biologics programs across the industry were delayed, and the stock fell hard as investors digested the idea that the company's single most important growth segment had a supply problem it could not quickly solve. It was a vivid, painful demonstration of the dark side of a cornered resource: when you depend on a scarce input you don't control, that input can hold you hostage.

The resolution came in stages, and then in a single decisive stroke. In mid-2025, the DOJ closed its investigation into Charles River without filing charges, and U.S. Fish & Wildlife cleared previously detained shipments, including a held population of roughly 1,000 macaques.11 The legal cloud lifted. But management had clearly absorbed a lesson it had no intention of forgetting: never again be a price-taker at the mercy of someone else's supply chain and someone else's compliance.

And so, in January 2026, Charles River announced the move that defines its new posture — agreeing to acquire the assets of its long-time Cambodian supplier, K.F. (Cambodia) Ltd., for approximately $510 million in cash.12 Combined with its existing roughly 90% stake in the Mauritius-based breeder Noveprim, the company moved to bring the vast majority of its primate supply in-house.12 The strategic reasoning is straightforward: by owning the breeding operations directly, Charles River controls biosecurity and provenance documentation end-to-end, insulates its most important segment from external supply shocks, and captures the margin that previously went to a third-party supplier.

A skeptic should immediately note the other edge of this sword, and we will return to it: owning a Cambodian monkey farm outright doesn't make the ethical and regulatory scrutiny disappear — it concentrates it directly on Charles River's own balance sheet. Vertical integration solved a supply problem by absorbing a reputational one. Whether that trade is wise depends on execution and on how the politics of primate research evolve. But supply security was only one of two enormous capital-allocation reckonings playing out simultaneously. The other was a billion-dollar bet that went catastrophically wrong.

VI. The CDMO Tragedy: Cognate, Vigene, and the Brutal $1.1B Capital Destruction of 2026

Every cycle has its intoxicating story, and in 2021 the story was cell and gene therapy. Money was nearly free, the biotech index was screaming, and the idea of curing genetic disease with a single engineered dose felt less like science fiction than inevitability. In that euphoric environment, Jim Foster made the bet that would define — and tarnish — the final chapter of his career.

The logic, as with WuXi a decade earlier, had a certain elegance. Charles River already helped biotechs discover and safety-test cell and gene therapies. Why not follow those same molecules downstream into manufacturing — becoming the contract development and manufacturing organization, or CDMO, that actually produces the complex therapies it had helped validate? Capture more of the value chain, deepen the customer relationship, ride the hottest wave in medicine. In March 2021, Charles River acquired CDMO Cognate BioServices for approximately $875 million. Three months later, in June 2021, it acquired Vigene Biosciences, a viral-vector specialist, for roughly $292.5 million plus up to $57.5 million in contingent payments.2 All in, the company deployed well over $1.1 billion to buy its way into advanced-therapeutics manufacturing.

Then the cycle turned, as cycles do. Through 2022 and 2023, the biotech funding bubble deflated. Interest rates rose, speculative capital fled, and funding for early-stage cell and gene therapy programs — exactly the customers a CDMO needs — dried up. And here the structural difference between a CRO and a CDMO becomes the whole story. A service business like preclinical CRO work scales with talent and regulatory expertise; you can flex it. A manufacturing business is the opposite — it is a high-fixed-cost, high-capacity-utilization game, where vast, purpose-built plants must run near full to cover their costs. When utilization at the acquired CDMO facilities collapsed alongside the funding environment, those expensive plants became cash-burning liabilities. The economics inverted from accretive dream to dilutive nightmare.

The accounting told the story in brutal, non-cash honesty. Charles River was forced to write down the goodwill on these businesses repeatedly — including an impairment charge of roughly $215 million in 2024 and further impairments exceeding $370 million in 2025 on its biologics and CDMO-related units.2 When a company impairs goodwill, it is formally admitting that the future cash flows it once paid for will not materialize. More than half a billion dollars of value, conjured at the peak, was being erased.

This is the backdrop against which Elliott Investment Management arrived. In May 2025, the activist firm — having built a major stake — entered a cooperation agreement with Charles River that added four directors to the board, including Steven Barg, Elliott's Global Head of Engagement, and established a Strategic Planning and Capital Allocation Committee to force a disciplined review of the entire portfolio.9 The message was unmistakable: the era of growth-at-any-price M&A was over, and the failed bets were going to be cleaned up.

The capitulation came in February 2026. Charles River announced a definitive agreement to divest its CDMO and cell solutions businesses to private equity firm GI Partners — the operations to be rebranded as Rose BioSolutions — in a transaction completed on May 6, 2026.45 And the terms are where the full scale of the value destruction becomes visible. This was not a sale in any ordinary sense. The deal was structured primarily around up to $50 million in contingent, performance-based future payments, with essentially no upfront cash. More striking still, Charles River agreed to fund up to $45 million of future EBITDA losses and capital expenditures for the divested businesses over a roughly four-year period.4 Read that again: the company was effectively paying to give the business away — accepting future cash obligations to offload assets it had bought for more than a billion dollars. This is about as close to a total write-off as a transaction gets, and it stands as one of the more sobering case studies in cyclical overpayment in recent specialty-pharma history.

On the very same day in February 2026, Charles River also sold its underperforming European Discovery Services assets to IQVIA for $145 million in cash, completing its exit from lower-margin, non-core work and recommitting to a focused, high-margin preclinical CRO identity.7 One divestiture recovered real cash; the other recovered mostly a lesson.

The honest analytical conclusion is not flattering to the prior management's capital allocation: across the WuXi breakup fee and the CDMO write-off, a pattern emerges of ambitious deals struck near cycle peaks that later required expensive unwinding. The reassuring counterpoint is that the company — under activist pressure — proved willing to take the loss decisively rather than nurse a dying business for years. Whether that newfound discipline is durable or merely imposed is the central question hanging over the Girshick era. But before we get there, we need to look at the one part of Charles River that never disappoints — a business built, improbably, on the blood of a creature older than the dinosaurs.

VII. The Hidden Crown Jewel: Horseshoe Crab Blood, LAL, and the Monopolistic Moat of Microbial Solutions

Every injectable drug, every vaccine, every IV bag of saline, every implantable medical device that goes into a human body shares one non-negotiable requirement: it must be proven free of endotoxins. Endotoxins are fragments of the cell walls of Gram-negative bacteria, and even in vanishingly small quantities they can trigger fever, plunging blood pressure, and fatal septic shock. A single contaminated batch of an injectable can kill. So regulators worldwide mandate that these products be tested, every batch, for endotoxin contamination. It is one of the most universal quality requirements in all of medicine.

And for decades, the gold-standard test depended on one of the strangest moats in business — the blue blood of the Atlantic horseshoe crab, Limulus polyphemus.

The horseshoe crab is a living fossil, essentially unchanged for hundreds of millions of years, and its blood contains a remarkable defense mechanism. When the crab's immune cells encounter bacterial endotoxin, they clot almost instantly, walling off the invader. In the 1960s, scientists learned to harness this reaction: an extract of the crab's amebocyte cells, called Limulus Amebocyte Lysate, or LAL, will visibly gel in the presence of even trace endotoxin. It became the FDA-recognized standard for endotoxin detection. Charles River built one of the dominant positions in supplying it. The company harvests horseshoe crabs along the U.S. East Coast, extracts a measured portion of their copper-based (hence blue) blood, and returns the live crabs to the ocean.

The economics of this business are extraordinary, and they reveal why Microbial Solutions sits inside the highest-margin segment in the company. Consider the switching costs from the customer's point of view. When a pharmaceutical manufacturer validates a production line, the specific endotoxin test it uses gets written into the manufacturing standard operating procedures that are filed with and approved by the FDA. Changing that test is not a procurement decision — it is a regulatory event, requiring revalidation and re-filing. Meanwhile, the cost of the LAL test itself is a tiny fraction of a penny per dose, while the cost of a contaminated batch or a regulatory hold is measured in millions of dollars and lost reputations. So you have a product that is cheap, mandatory, consumable, repeat-purchased on every single batch forever, and protected by switching costs that are essentially baked into the customer's regulatory license. That is about as good as a recurring-revenue moat gets.

Naturally, such a position attracts challengers — and here the threat is both ethical and technological. Animal-rights and conservation groups have long objected to the bleeding of horseshoe crabs, whose populations are also ecologically important (migratory shorebirds depend on their eggs). The proposed alternative is Recombinant Factor C, or rFC, a synthetic reagent that reproduces the key clotting protein without any crabs at all. On paper, rFC should eventually displace LAL. In practice, adoption has been remarkably slow, because pharmacopeias and regulators require extensive validation before a new method can be treated as equivalent for an approved product — and manufacturers, facing the switching costs described above, have little incentive to move first.

Charles River's response here was genuinely shrewd, and worth crediting: rather than defend the old technology to the death, it offers both traditional LAL and its own proprietary recombinant testing platform. By selling the synthetic alternative itself, the company captures the customers who do want to move away from animal-derived reagents, neutralizing the disruptor's main advantage while preserving its dominant position in the installed base. It is a textbook example of how an incumbent can co-opt a substitute instead of being killed by it. This consumable, regulation-locked, quietly monopolistic business is, in many ways, the steadiest and most attractive thing Charles River owns — and a useful reminder that beneath all the recent turmoil sits a genuinely durable core. The question for the next decade is whether new leadership can protect that core while disciplining everything around it. Which brings us to the changing of the guard.

VIII. The Changing of the Guard: Jim Foster's Legacy and Birgit Girshick's 2026 Mandate

On May 5, 2026, James C. Foster handed over the company his family had effectively built, ending a 34-year run as CEO and one of the longest active tenures of any leader in the life-sciences industry.6 Any honest accounting of his legacy has to hold two contradictory truths in tension.

On one side of the ledger, Foster's achievement was monumental. He took a sleepy, sub-$100-million animal breeder trapped inside an indifferent consumer-products parent, engineered its liberation through a leveraged buyout and IPO, and over two decades transformed it into a roughly $4 billion global CRO through more than 50 acquisitions. He correctly read the secular shift toward pharmaceutical outsourcing years before it became consensus, and he built the company that the entire industry's drug pipeline now depends on. That is a genuine empire, built by a genuine builder.

On the other side sits the hubris that so often accompanies long tenures and successful empire-building. The same instinct for the bold, transformational deal that served Foster well in the company's growth years curdled, late in his career, into overreach. The CDMO misadventure destroyed more than a billion dollars of capital at the top of a cycle. The primate supply crisis, while not entirely of his making, exposed a strategic vulnerability that prudent management might have hedged earlier. And the cumulative effect was an erosion of credibility with Wall Street that ultimately invited — and arguably required — the Elliott intervention. The very durability that let Foster build the company may also have insulated him from the discipline that would have prevented its late-career missteps. This is the recurring paradox of the founder-adjacent CEO: the conviction that builds the empire is the same conviction that resists course-correction.

His successor is, in one sense, the ultimate continuity choice, and in another, a deliberate pivot. Birgit Girshick joined Charles River in 1989 — a 37-year career inside the company — and most recently served as Chief Operating Officer from 2021.6 She is not a financier parachuted in to break things; she is the executive who ran the operations, who scaled the company's global footprint, and who drove its digital and operational initiatives. The board's bet is that the next chapter requires not vision and dealmaking but execution and discipline — and that someone who knows where every facility, every barrier, and every bottleneck lives is best positioned to deliver it.

Her compensation package signals exactly what the board wants from her. The structure includes a base salary of $1.2 million per year and a target annual cash incentive of 100% of base, or another $1.2 million.6 More telling is the initial equity grant of $9 million, structured 80% as Performance Share Units and only 20% as time-vesting Restricted Stock Units — with the PSUs tied directly to organic revenue growth, operating-margin expansion, and return on invested capital.6 That mix is a pointed rebuke of the past. After a decade in which capital was deployed into value-destroying acquisitions, the new CEO is being paid, above all, to grow organically, widen margins, and earn a real return on the capital already invested. The emphasis on ROIC in particular reads as an institutional promise to never repeat the CDMO mistake. Girshick also holds beneficial ownership of roughly 79,816 shares — a meaningful personal stake worth somewhere in the high-teens of millions of dollars at mid-2026 prices — giving her real skin in the outcome.6

Her mandate is concrete rather than visionary: execute the roughly $70 million in annual cost savings identified by the Elliott-driven strategic review, integrate the newly acquired K.F. Cambodia primate assets cleanly and compliantly, and scale the company's investment in "New Approach Methodologies" — the non-animal testing platforms being developed through its Alternative Methods Advancement Project. That last item is the most strategically loaded, because it means the company's own future partly depends on technologies that could erode its animal-based legacy businesses. How a 37-year insider navigates the cannibalization of her own company's heritage is the defining test of her tenure. To frame that test properly, we need to put the whole business through a rigorous strategic stress test.

IX. Strategic Moats & Stress Test: Hamilton's 7 Powers, Porter's 5 Forces, and the Activist Risk Radar

Let's war-game this business properly, using two of the sharpest analytical lenses available, and then subject it to the kind of scrutiny a skeptical investor would bring.

Start with Hamilton Helmer's 7 Powers, the framework for identifying durable competitive advantage. Charles River exhibits three powers worth examining.

The strongest, by a wide margin, is Cornered Resource. With the acquisition of K.F. Cambodia and its majority stake in Noveprim Mauritius, Charles River now controls a dominant share of the legitimate, compliant global supply of research macaques — the irreplaceable input for biologics safety testing.12 Layer on top of that its access to U.S. horseshoe crab harvesting licenses and the specialized facilities to process them for LAL, and you have ownership of two scarce, hard-to-replicate natural resources that the entire industry must source. This is the rarest and most valuable of the seven powers, and Charles River genuinely possesses it.

Second is Switching Costs, which we have seen operate in two distinct ways. In DSA, moving an ongoing preclinical program from one CRO to another mid-stream means lost time, revalidation, and the risk of regulatory inconsistency — delays that can cost a biotech its funding window. In Microbial Solutions, the endotoxin test is embedded in FDA-approved manufacturing SOPs, making change a regulatory ordeal. Both lock customers in not through contracts but through the friction of regulated science.

Third is Scale Economies, which is real but more moderate. The fixed costs of biosecure breeding barriers, GLP-compliant labs, and global regulatory infrastructure are enormous, creating a high barrier that smaller competitors struggle to clear. But scale in this industry is not infinitely advantaged — JAX, Taconic, and well-capitalized Asian rivals all operate at meaningful scale, so this is a barrier to entry more than a runaway flywheel.

Now Porter's Five Forces. The Threat of New Entrants is low — the capital intensity, regulatory accreditation, and decades of accumulated scientific credibility required to enter preclinical CRO work are prohibitive. The Bargaining Power of Suppliers was historically the company's great weakness, given the primate cartel dynamics of 2020-2023, but vertical integration has substantially mitigated it. The Bargaining Power of Buyers is moderate: large pharma is consolidated and negotiates hard, but the disruption of switching preclinical partners limits how far buyers will push. Competitive Rivalry is genuinely intense in DSA — against Labcorp, WuXi, and Pharmaron — but far more consolidated in RMS (where Charles River and JAX dominate) and in Microbial Solutions (Charles River, Lonza, and bioMérieux).

The most interesting force is the Threat of Substitutes, which is moderate today but potentially high over the long run. The FDA Modernization Act 2.0, signed in late 2022, removed the absolute statutory requirement that drugs be tested in animals before human trials, opening the door to alternatives like organ-on-a-chip systems, human organoids, and in-silico (computer-modeled) toxicology. This is a genuine secular threat to the animal-based heart of the company. Charles River's response — investing in alternative methods through its advancement project, with hundreds of millions earmarked over time — is the right defensive posture, mirroring the LAL-and-rFC playbook of selling the substitute itself. But it is a much harder thing to co-opt a technology shift that could shrink your largest segments than one confined to a single product line.

Now the activist stress test — what would a sharp short-seller hammer on today? Four things. First, the capital-allocation track record: more than half a billion dollars in impairments and a CDMO business effectively given away amount to hard evidence of value destruction, and a skeptic would question whether the culture that produced it has truly changed or merely been restrained by an activist who will eventually move on. Second, the integration and ethical risk of operating a Cambodian primate-breeding operation directly, under intense international scrutiny for wildlife-trafficking and animal-welfare violations — a single scandal could be reputationally and operationally severe. Third, the long-term structural decline of animal testing, which no amount of cost-cutting can reverse. And fourth, the uncomfortable truth that Charles River remains financially tethered to the volatility of biotech funding — when venture and public-market money for small and mid-cap biotech dries up, the marginal demand for Charles River's services dries up with it.

That sets up the risk radar plainly. Regulatory and ESG risk is high, driven by animal-rights pressure and the politics of primate sourcing. Macro and funding risk is high, because biotech funding cycles transmit directly into the company's order book. And execution risk is high, as a new CEO attempts to convert a 79-year-old empire-building culture into a disciplined, return-focused operating machine. Hold all of that in mind as we turn to the central debate: from here, does Charles River win, or does it slowly fade?

X. The Bull vs. Bear Debate: Why We Win or Why We Fail from Here

Let's lay out both cases honestly, because a thoughtful investor should be able to argue either side.

The bull case rests on four pillars. First, refocus and margin recovery: having shed the cash-burning CDMO business and the lower-margin European Discovery assets, Charles River is now a leaner, purer preclinical CRO, and the math of removing dilutive, loss-making operations should push non-GAAP operating margins back toward the historical mid-20s and above. The portfolio cleanup, painful as it was, removes a persistent drag on profitability and management attention. Second, competitive clearance: the June 3, 2026 Chapter 11 filing of Inotiv removed Charles River's primary commercial rival in research models, crippled by debt and litigation.8 When your largest competitor enters bankruptcy, you gain pricing power and the opportunity to absorb its customers — a concrete, near-term tailwind. Third, supply-chain independence: the K.F. Cambodia acquisition closes off the single most acute vulnerability of the prior years, securing the primate pipeline that the company's most important segment depends on. Fourth — and most intriguing — the Biosecure Act windfall: if U.S. legislation continues to push biopharma away from Chinese CROs like WuXi AppTec and Pharmaron, a multi-billion-dollar pool of preclinical work could shift back toward trusted, Western-based providers, and Charles River is arguably the single largest beneficiary of that repatriation.

There is real substance to each of these. But each also carries a caveat the bull case tends to gloss over. Margin recovery assumes demand holds; competitive clearance assumes Inotiv's customers actually migrate to Charles River rather than to JAX or Taconic; supply security came at the cost of concentrated ethical risk; and the Biosecure Act has been debated for years without becoming law, so the windfall remains a thesis, not a fact.

The bear case is equally serious. First, the secular decline of animal testing: the FDA Modernization Act 2.0 is a slow-acting but structural headwind, and as organ-on-a-chip, organoids, and AI-driven modeling mature, the total addressable market for physical research models and traditional in-vivo toxicology will shrink. Charles River is investing in the alternatives, but it is essentially being asked to cannibalize its own franchise gracefully — a feat few incumbents manage. Second, the M&A scar tissue: the more than $1.1 billion CDMO write-off and the 2010 WuXi breakup fee establish a pattern of overpaying at cycle peaks, and a single activist's intervention does not guarantee that pattern is permanently broken. Third, the primate PR and legal vulnerability: by vertically integrating Cambodian breeding operations, the company has painted a target on itself for animal-rights organizations, ESG-screening funds, and federal regulators watching for any wildlife-trafficking or breeding-compliance failure. The very move that secured supply concentrated reputational risk.

Synthesizing the two through our earlier frameworks: the bull case is essentially a bet on the durability of Charles River's cornered resources and switching costs plus a cyclical and geopolitical tailwind. The bear case is a bet that the substitutes force — the slow erosion of the animal-testing paradigm — combined with management's checkered capital allocation, eventually overwhelms those moats. Both can be true on different time horizons: the moats are very real over the next several years, and the substitution threat is very real over the next two decades. Which dominates an investor's view depends largely on time horizon and on confidence in the new management's discipline.

If you had to distill the entire investment debate into the few things that actually matter to watch, here they are. The single most important KPI is DSA segment organic revenue growth, because it is both the largest segment and the most direct read on biopharma demand and pricing power. Second is the consolidated non-GAAP operating margin, the clearest scorecard on whether the promised discipline and cost savings are real. And third, watch DSA net book-to-bill — the ratio of new orders to revenue billed — because it is the leading indicator of demand turning before it shows up in the revenue line. Those three numbers, tracked over time, will tell the story faster than any press release. With that, let's pull out the durable lessons.

XI. The Playbook: Key Lessons for Founders, Investors, and Capital Allocators

Four lessons from the Charles River story are worth carrying into any business analysis.

Lesson one: the bottleneck-asset moat. The most defensible position in any industry is often ownership of its literal starting point. Charles River's enduring power has never come from being the biggest or the cheapest — it has come from controlling the indispensable first inputs: the standardized research model, the macaque, the endotoxin-testing reagent. When you own the chokepoint that everyone downstream must pass through, you possess structural pricing power and a moat that competitors cannot simply out-spend. Henry Foster understood this in 1947 with his pathogen-free rats; the 2026 K.F. Cambodia acquisition is the same insight applied to primates seventy-nine years later. Find the bottleneck, and own it.

Lesson two: the perils of moving downstream. Being a trusted, high-margin service provider at the beginning of a product's lifecycle does not mean you can profitably manufacture the finished product. The CRO business that Charles River mastered is a specialized-talent and regulatory-service game with flexible, variable costs. The CDMO business it stumbled into is a high-capital, high-utilization manufacturing game where idle capacity bleeds cash. The two look adjacent on an org chart and behave like different species in a downturn. Confusing service economics with manufacturing economics cost shareholders more than a billion dollars. Adjacency on a value chain is not the same as capability.

Lesson three: the role of constructive activism. The Elliott intervention of 2025 is a clean example of activist pressure cutting through executive hubris to impose capital discipline. A long-tenured, successful CEO had drifted into value-destroying empire-building, and the internal governance machinery had not stopped him. It took an outside investor with board seats and a capital-allocation committee to force the portfolio rationalization, the cost program, and a structured CEO succession.9 Activism is not always constructive — but when entrenched leadership has stopped self-correcting, an outside catalyst can be the mechanism that restores discipline. The lesson for boards is to internalize that discipline before an activist has to impose it.

Lesson four: geopolitical serendipity, and the value of deals not done. Sometimes the most consequential capital-allocation decision is the acquisition you walk away from. The aborted 2010 WuXi merger felt at the time like a defeat for an ambitious CEO and a win for cost-conscious activists. Fifteen years later, with the Biosecure Act threatening Chinese CROs, the decision not to fuse Charles River to a Chinese platform looks like an accidental masterstroke of risk avoidance. The humbling truth for capital allocators is that the full consequences of a deal — done or undone — may not be legible for a decade, and that luck, not just foresight, plays a real role in long-run outcomes. Intellectual humility about what you cannot foresee is itself a form of risk management.

XII. Epilogue & Wrap-up

The arc of Charles River Laboratories is, in the end, a story about transformation at every scale. It began with one veterinarian, a thousand second-hand cages, and a conviction that biology could be standardized — that an animal could be made into a reliable instrument of science. Seventy-nine years later, it is a $4 billion global infrastructure company sitting at the front of nearly every drug pipeline in the world, controlling cornered resources from the forests of Cambodia to the shores of the Atlantic, navigating the politics of animal welfare, the volatility of biotech funding, and the slow tectonic shift away from animal testing itself.

The company that enters the second half of 2026 is leaner, more focused, and more disciplined than the one that entered 2025 — but that focus was imposed by crisis and activism as much as chosen, and the scar tissue from the CDMO debacle and the primate-supply shock is still fresh. Its moats are genuinely formidable in the near term and genuinely threatened over the long term. That is not a contradiction to be resolved so much as a tension to be managed.

Which leaves the defining question of the Birgit Girshick era. She is the consummate insider — 37 years inside the building, intimate with every facility and bottleneck, chosen precisely because she knows how the machine works. The bet the board has made is that operational mastery and a compensation package tilted hard toward returns on capital will produce the disciplined allocator the company now needs. But the open question is whether someone so deeply woven into the company's history can bring the cold, objective detachment required to keep cannibalizing its own legacy, to resist the next intoxicating cycle-peak deal, and to allocate capital like an outsider while leading like an insider. The next two decades of biopharma — and of Charles River — will turn on the answer.

References

-

SEC Filing Form 10-K for Fiscal Year Ended Dec 28, 2025 — Charles River Laboratories, 2026-02-17 ↩↩↩↩↩↩

-

Charles River Laboratories Reports Fourth-Quarter and Full-Year 2025 Results — Charles River Laboratories, 2026-02-17 ↩↩↩↩

-

Charles River Laboratories Announces Agreement to Divest Its CDMO and Cell Solutions Businesses to GI Partners — Charles River Laboratories, 2026-02-25 ↩↩↩

-

Charles River Laboratories Completes Divestiture of CDMO and Cell Solutions Businesses — Charles River Laboratories, 2026-05-06 ↩

-

Charles River Laboratories Announces Leadership Transition: Birgit Girshick Appointed Chief Executive Officer — Charles River Laboratories, 2026-01-08 ↩↩↩↩↩↩

-

Charles River Laboratories Announces Definitive Agreement to Sell European Discovery Services Assets to IQVIA — Charles River Laboratories, 2026-02-25 ↩↩

-

Inotiv, Inc. Files for Chapter 11 Bankruptcy to Restructure Debt — Inotiv, Inc., 2026-06-03 ↩↩↩

-

Charles River Laboratories and Elliott Investment Management Enter into Cooperation Agreement — BusinessWire, 2025-05-06 ↩↩↩

-

Charles River Laboratories Aborts $1.6 Billion Acquisition of WuXi PharmaTech — Reuters, 2010-07-29 ↩↩

-

DOJ Closes Investigation into Cambodian Macaque Sourcing without Charges — Fierce Biotech, 2025-07-15 ↩

-

Charles River to Acquire Assets of Primate Breeding Partner K.F. (Cambodia) Ltd. — BioPharma Dive, 2026-01-12 ↩↩↩↩

-

The Macaque Monopoly: Inside the High-Stakes Primate Supply Chain — Bloomberg, 2023-04-12 ↩↩↩↩

-

Why Activists Blocked Charles River's 2010 Attempt to Buy WuXi — Institutional Investor, 2010-08-02 ↩↩

-

A History of Standardization: Dr. Henry Foster's Legacy — Charles River Laboratories ↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube