Corebridge Financial: The $20B Spin-Off That "Saved" Retirement

I. Introduction

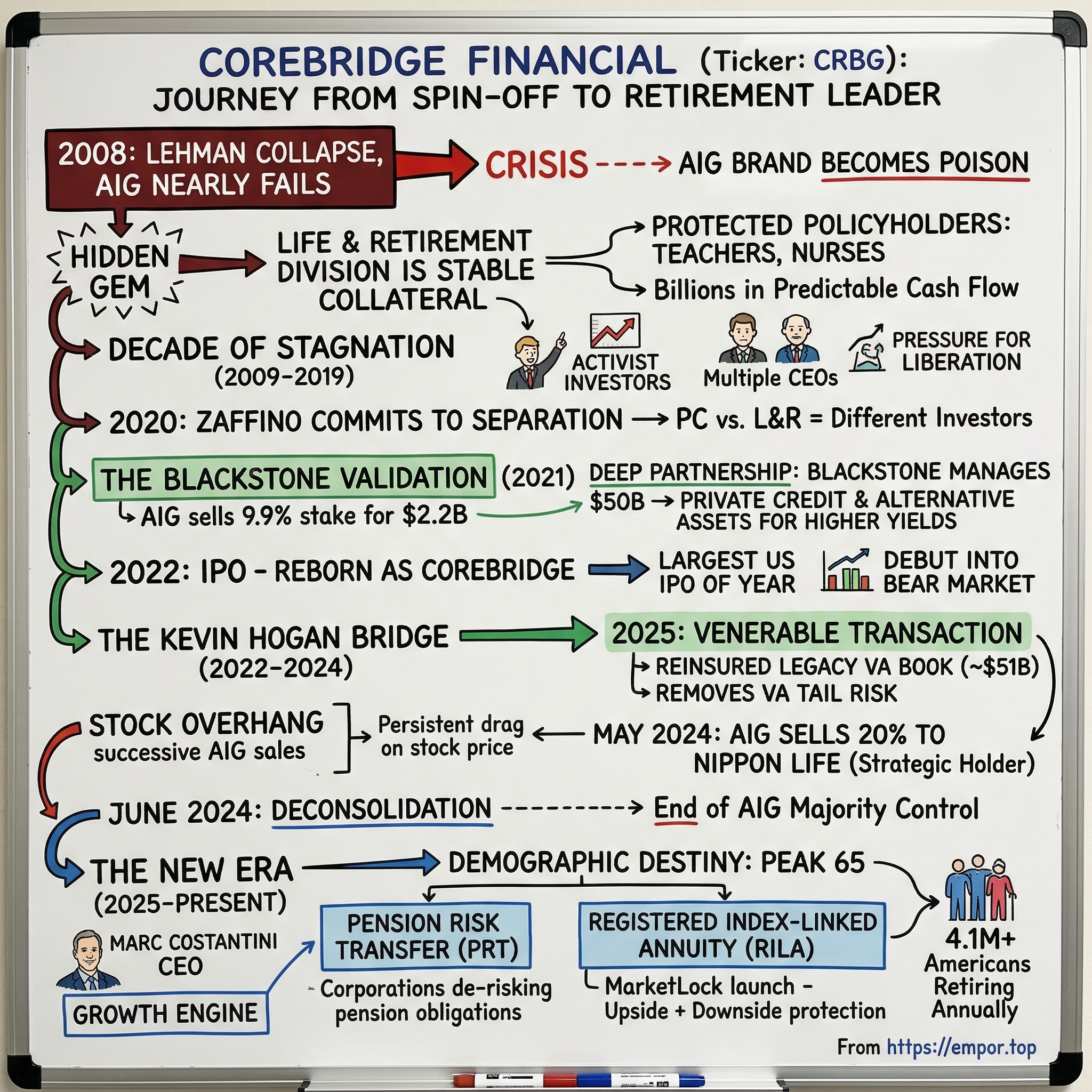

On September 15, 2008, the world watched Lehman Brothers die. But the real terror — the moment that made Hank Paulson's hands shake and Ben Bernanke lose sleep — was not Lehman. It was what almost happened the next day. American International Group, the largest insurance company on the planet, was hours from a collapse that would have made Lehman look like a regional bank failure. AIG's tentacles reached into every corner of the global financial system: pension funds in Norway, municipal bonds in Kansas, life insurance policies in every zip code in America. When the Federal Reserve engineered its $182 billion rescue — the largest government bailout of a private company in history — the public narrative hardened into something simple: AIG was the villain. Reckless. Greedy. The company that sold credit default swaps on subprime mortgages until the whole house of cards came crashing down.

That narrative was true. But it was also incomplete.

Because buried deep inside AIG's labyrinthine corporate structure — underneath the Financial Products division that nearly destroyed the world economy, past the layers of offshore entities and leveraged bets — sat a business that was doing something remarkably boring and remarkably important.

It was collecting premiums from schoolteachers in Texas. It was managing retirement accounts for hospital workers in Ohio. It was writing life insurance policies for families who just wanted to know their kids would be okay.

This business did not blow up. It did not need a bailout. In fact, it was the reason the bailout worked at all — the collateral the Federal Reserve pointed to when it justified lending hundreds of billions of dollars to a company the public wanted to see buried.

That business, AIG's Life and Retirement division, spent the next fourteen years trapped inside a corporate structure that no longer made sense, weighed down by a brand name that had become synonymous with financial catastrophe. Activist investors screamed for its liberation. Three successive CEOs debated the merits of setting it free. And when it finally emerged in September 2022 — reborn as Corebridge Financial, ticker CRBG, in the largest American IPO of that year — it arrived into a market that was itself in crisis, with interest rates spiking and equity valuations cratering.

The story of Corebridge Financial is not a startup story. There is no garage, no pivot, no Series A. It is something rarer and, in many ways, more interesting: the story of a hundred-year-old business that was hidden in plain sight, misunderstood by the market, undervalued by its parent, and finally given the chance to stand on its own.

It is the story of how the "good bank" inside the "bad bank" became a $20 billion independent company managing nearly $400 billion in assets — and why, in an era when eleven thousand Americans turn sixty-five every single day, the boring business of retirement might be the most important growth story nobody is talking about.

Three themes run through every chapter of what follows.

The first is the Great De-conglomeration — the trend sweeping American finance as sprawling conglomerates realize that their parts are worth more than the whole. General Electric did it. United Technologies did it. And AIG, after a decade of resistance, finally did it too.

The second theme is the "yield trade" — the race among insurers and asset managers to squeeze higher returns out of insurance investment portfolios by moving from plain-vanilla bonds into private credit and alternative assets — a race that brought Blackstone to Corebridge's door with a $2.2 billion check.

The third theme is demographic destiny: the massive retirement wave called Peak 65, where more than four million Americans cross the retirement threshold each year from 2024 through 2027, creating a demand surge for guaranteed income products that the industry has never seen before.

Each of these themes converges on Corebridge Financial like three rivers meeting at a delta. Whether that delta produces fertile ground or a flood zone depends on how well a century-old insurer, freshly stripped of its "too big to fail" parent, can reinvent itself in an age when private equity juggernauts like Apollo's Athene and KKR's Global Atlantic are rewriting the rules of the insurance business.

II. Origin Story: The American General Roots (1926–2001)

Houston, Texas, in 1926. The oil boom was roaring, and the city was filling up with roughnecks, wildcatters, and the particular breed of deal-maker that thrives in boomtowns. Gus Sessions Wortham, a Texan insurance man with a knack for reading risk, founded the American General Insurance Company on May 8 of that year. The idea was simple enough: sell insurance to the people pouring into the Gulf Coast. Life policies. Property coverage. The kind of boring financial product that nobody thinks about until they desperately need it.

What made American General interesting was not the founding — plenty of insurance companies started during the Jazz Age — but what came next. Over the following decades, American General became one of the most acquisitive insurers in America. Where other companies grew organically, American General grew by buying competitors, absorbing their books of business, and folding their operations into an ever-expanding Houston-based empire. It was a roll-up strategy before anyone called it that. In an industry defined by patience and compound interest, Wortham's company moved with the restless energy of a Texas oil deal-maker. By the mid-twentieth century, American General had consumed dozens of smaller life insurance companies across the South and Midwest, building a patchwork empire of policy books that stretched from Florida to California.

The most consequential acquisition in the company's first half-century was one that almost nobody noticed at the time: a small company called the Variable Annuity Life Insurance Company, or VALIC. Founded in 1955 in Washington, D.C., by George E. Johnson — a former general counsel at TIAA-CREF — VALIC had a peculiar speciality. It sold tax-deferred annuities to employees of nonprofit organizations. Hospitals. Universities. And, most importantly, public school districts.

Here is why that matters. In the early 1960s, VALIC's founders went on a lobbying blitz through state legislatures, pushing for laws that would allow K-12 public school workers to supplement their retirement savings through what are called 403(b) plans — the nonprofit equivalent of a 401(k). To understand the significance of this, consider what a 403(b) plan actually is. Public school teachers, unlike employees at most private companies, typically cannot participate in 401(k) plans. Instead, they have state pension systems — which provide a base retirement income but often not enough — and the option to make additional tax-deferred contributions through a 403(b). The provider who manages that 403(b) plan becomes embedded in the school district's payroll infrastructure, its human resources onboarding process, and often its financial education programs for employees.

By 1964, VALIC became the first retirement provider to enroll a public school district in a 403(b) program, signing up Florida's Dade County. It was unglamorous work — knocking on school board doors, explaining tax-deferred savings to administrators, building payroll integrations with each district individually. But it was extraordinarily sticky. Once a retirement provider gets embedded in a school district's payroll system, the switching costs are enormous. A district would need to migrate thousands of employee accounts, retrain HR staff on new systems, and notify every participant — all for a product category that most administrators barely think about. Teachers are not going to disrupt their automated payroll deductions and transfer decades of retirement savings because a competitor offers a marginally better fee structure. This is a relationship that, once established, persists for generations. A district that chose VALIC in 1975 likely still uses Corebridge's VALIC platform today.

American General first took a significant interest in VALIC in 1967 and acquired a majority stake by 1975, eventually making it a wholly owned subsidiary. That single move — buying a small annuity company that sold retirement plans to schoolteachers — would become the foundation of a business managing hundreds of billions of dollars half a century later. The K-12 teacher market remains Corebridge's single stickiest distribution channel to this day. It is a textbook example of what Warren Buffett calls a "toll bridge" business: not glamorous, not fast-growing, but virtually impossible to displace and enormously profitable over time.

By the late 1990s, American General had grown into one of the largest life insurance and annuity companies in the United States. It was big enough to attract suitors. In March 2001, Prudential plc — the British insurer, not the American one — announced an agreement to buy American General for $26.5 billion in stock. It would have been one of the largest cross-border financial mergers in history.

It never happened. Prudential's shareholders revolted, driving the stock down 16% and cratering the deal's value.

And that was when Hank Greenberg made his move. Greenberg, the legendary and imperious CEO of AIG who had built it into the world's most powerful insurance conglomerate through sheer force of will and deal-making, swooped in with a competing all-cash bid of $23 billion. The all-cash structure was the key — Prudential had offered stock, which fluctuated with its share price, but Greenberg offered certainty.

American General agreed to pay Prudential a $600 million breakup fee and walked into AIG's arms. It was August 2001 — just weeks before the September 11 attacks would reshape the insurance industry forever.

The American General acquisition gave AIG something it would desperately need seven years later: a massive, stable life insurance and retirement business that generated billions in predictable cash flow. It was the seed of what would eventually become Corebridge Financial. But first, it would have to survive what its new parent was about to do.

III. The AIG Era and The Crisis (2001–2020)

Inside AIG, the former American General operations were reorganized into what became known as the Life and Retirement division. Think of AIG in the 2000s as a financial conglomerate with two entirely different personalities.

On one side sat the property and casualty business — general insurance, commercial lines, the kind of bread-and-butter underwriting that AIG had been built on. On the other side sat Life and Retirement, the Houston-based machine that collected premiums from teachers and nurses, managed 403(b) plans, and sold fixed annuities to retirees. It was the steady hand. The predictable one. The boring one.

And then there was the third entity that nobody outside of AIG really understood: AIG Financial Products, or AIGFP, operating out of a satellite office in Wilton, Connecticut, and an outpost in London's Mayfair. AIGFP was the unit that wrote credit default swaps on subprime mortgage-backed securities — essentially selling insurance against the possibility that pools of American home loans would default. The premiums were lucrative. The risks were supposedly negligible. And by 2007, AIGFP had written swaps on a notional value that would eventually exceed $500 billion.

When the housing market cracked and the subprime mortgages underlying those securities began defaulting in waves, the collateral calls on AIGFP came fast and furious. AIG needed to post billions in cash to its counterparties — Goldman Sachs, Société Générale, Deutsche Bank — and it did not have the money. On September 16, 2008, the day after Lehman Brothers filed for bankruptcy, the Federal Reserve stepped in with an $85 billion emergency credit line. It would ultimately grow to $182 billion. The government seized 79.9% of AIG's equity.

Here is the crucial detail that gets lost in the crisis narrative: the Life and Retirement assets were ring-fenced.

In the United States, life insurance is regulated at the state level, and state insurance commissioners have their own jurisdiction over policyholder reserves — the money set aside to pay claims. Those reserves are legally segregated from the holding company's balance sheet. Even as AIG's holding company was hemorrhaging cash to meet collateral calls from Goldman Sachs and other counterparties, the Life and Retirement reserves sat in their own regulated entities, untouchable by AIG's creditors. The policyholder money — the savings of schoolteachers and hospital workers — was protected.

More than that, the value and stability of the Life and Retirement book was a critical reason the Federal Reserve believed it could lend to AIG and eventually get paid back. When the Fed's lawyers and economists modeled the rescue, they pointed to the Life and Retirement division as the crown jewel — the asset whose liquidation value could repay the government's loans. Without it, there was no justification for the bailout. The good bank was the collateral for the bailout of the bad bank.

The government eventually recovered its full investment in AIG plus a profit — approximately $22.7 billion more than it lent. But the damage to the brand was catastrophic and permanent. AIG became a four-letter word. And the Life and Retirement division — the part that had done nothing wrong — was trapped inside a name that consumers associated with greed and recklessness. Imagine being a financial advisor trying to sell a retirement annuity to a schoolteacher in 2010 and having to say, "This is an AIG product." The brand was poison.

What followed was a decade of stagnation, strategic confusion, and escalating activist pressure.

The Life and Retirement business was profitable. It was growing. But it was stuck — undervalued by AIG's conglomerate structure, held back by AIG's brand toxicity, and governed by leaders who could not agree on whether to set it free.

The activist era began in earnest in October 2015, when Carl Icahn disclosed a large stake in AIG and fired off one of his characteristically blunt public letters. His argument was elegant in its simplicity: AIG was "too big to succeed." The company had been designated a Systemically Important Financial Institution by the Federal Reserve, which meant it was subject to enhanced capital requirements, more invasive regulatory oversight, and greater restrictions on returning cash to shareholders. Icahn's proposed solution was to split AIG into three publicly traded companies — property and casualty insurance, life insurance, and mortgage insurance. Three smaller companies, each below the SIFI threshold, each free to operate without the regulatory burden that came with being "too big to fail."

A month later, hedge fund manager John Paulson — whose fame came from betting against subprime mortgages during the crisis — joined Icahn's campaign. Paulson publicly predicted that the combined value of AIG's separated parts would be 66% higher than the company's stock price. The math was compelling. The conglomerate discount was enormous.

AIG's management, led by CEO Peter Hancock, resisted. Hancock, an intellectual former JPMorgan executive who favored spreadsheets over shareholder letters, laid out a recovery plan to bring AIG's performance in line with peers by the end of 2017. The argument was the classic conglomerate defense: diversification reduces risk, shared services reduce costs, and breaking up the company would trigger tax and regulatory complications that would destroy value.

In January 2016, AIG reached a settlement to avoid a full proxy fight, inviting Paulson and an Icahn representative to join the board. But the board was expanded to sixteen seats, making the activist representatives only two of sixteen votes — a classic corporate governance maneuver that gave the appearance of compromise while diluting activist influence. Icahn, characteristically, was not fooled. He continued to push publicly and privately for a breakup.

It did not work — not the activist campaign's immediate aims, and not Hancock's recovery plan. Four losses in six quarters eroded Hancock's credibility with the board and with investors. A particularly disappointing fourth quarter of 2016, in which AIG reported massive reserve charges, was the final straw. In March 2017, Hancock resigned — the pressure from Icahn and the weight of disappointing earnings too much to bear.

AIG replaced him with Brian Duperreault, a seventy-year-old veteran insurance executive who had worked under Hank Greenberg decades earlier and had most recently been running Hamilton Insurance Group in Bermuda. Duperreault was a turnaround specialist with a reputation for operational discipline and a deep personal network across the global insurance industry. He brought in Peter Zaffino — then the CEO of Marsh, the world's largest insurance brokerage — as his chief operating officer. Together, they stabilized AIG's underwriting and began the painstaking work of rebuilding the company's credibility. But even Duperreault could not fully resolve the fundamental question: should AIG stay together or break apart?

The answer came in 2020, when Zaffino succeeded Duperreault as CEO. Zaffino — a Boston College graduate with an MBA from NYU Stern — was an operator, not a philosopher. He had spent his career in the trenches of insurance distribution and risk management, running Guy Carpenter's reinsurance brokerage and then Marsh's sprawling global operations. He understood the plumbing of the insurance industry better than perhaps anyone in the business.

And when he looked at the data, he saw what the activists had been saying for five years: property and casualty insurance and life and retirement insurance attract fundamentally different investors.

One is a volatility play — returns are driven by catastrophe events, pricing cycles, and underwriting skill. The other is a spread play — returns are driven by the gap between investment yields and the cost of policyholder liabilities. Running them together inside the same company meant that neither side attracted its natural investor base. The sum was literally worth less than its parts.

Zaffino committed to separating the businesses. It would take two more years to execute, involving a strategic partnership with Blackstone, a rebranding exercise, and an IPO into one of the worst equity markets in recent memory. But the decision was made. After five years of activist pressure, three CEOs, and countless board deliberations, AIG was going to let its best business walk out the door.

IV. The Blackstone Validation (2021)

Before you can IPO a business, you need to answer a fundamental question: what is it worth? For a massive, low-growth insurance operation buried inside a conglomerate with a toxic brand, this was not a trivial exercise. Traditional comparables were messy. The analyst community did not have a clean way to value AIG's Life and Retirement division because it had never reported as a standalone entity with its own capital structure, its own investment portfolio, or its own regulatory capital requirements. The conglomerate structure meant everything was intertwined.

Peter Zaffino found an elegant solution.

In July 2021, AIG announced that it was selling a 9.9% equity stake in its Life and Retirement business to Blackstone for $2.2 billion in cash. Think about what that transaction accomplished on multiple levels simultaneously.

First, the valuation signal. A 9.9% stake for $2.2 billion implied a total equity value of approximately $22 billion for the division. That was the first clean market-based valuation the business had ever received. It gave analysts a number to anchor on. It gave prospective IPO investors a reference point. And it came from Blackstone — arguably the most sophisticated alternative asset manager in the world. When Stephen Schwarzman's firm writes a check for $2.2 billion, the market pays attention.

Second, and arguably more important, was what came with the equity stake: a long-term strategic asset management agreement. As part of the deal, Blackstone would take over management of $50 billion of the Life and Retirement division's investment portfolio, with the mandate expected to grow to $92.5 billion over six years. This was not a passive equity investment. It was a deep operational partnership.

To understand why this mattered, you need to understand how the insurance industry's economics were shifting. For decades, life insurers had invested their policyholder reserves — the money they collected from premiums — in traditional investment-grade corporate bonds and government securities. It was safe. It was predictable. And in a low-interest-rate environment, it was increasingly insufficient to generate attractive returns.

The alternative asset managers — Blackstone, Apollo, KKR — had figured out a different playbook. They could originate private credit: direct loans to mid-market companies, structured credit facilities, commercial real estate debt, infrastructure financing.

These assets yielded significantly more than public bonds — typically 100 to 200 basis points higher — while carrying similar or only modestly higher risk profiles when properly underwritten. One hundred basis points sounds small — it is one percentage point — but on a $50 billion portfolio, one hundred basis points of additional yield is $500 million per year. On the full $385 billion that Corebridge manages today, the math becomes staggering.

The catch was that smaller insurers could not access these assets. You needed the origination platform, the structuring capability, and the sheer scale that only the largest alternative managers possessed.

By partnering with Blackstone, Corebridge gained access to this higher-yielding asset class in a way it never could have built on its own. Think of it as the insurer bringing the liabilities — billions in predictable policyholder premiums that need to be invested — and Blackstone bringing the assets — private credit origination capability that generates superior yields. It was a marriage of capabilities, and it transformed Corebridge's investment portfolio from a plain-vanilla bond fund into something far more powerful.

The deal also served as what the market came to call a "Good Housekeeping Seal of Approval." Blackstone's due diligence on the Life and Retirement book was exhaustive. They examined the quality of the assets, the reserves, the actuarial assumptions, the embedded risks in the variable annuity portfolio. A firm managing over $900 billion in assets across real estate, private equity, credit, and hedge funds does not write a $2.2 billion check without understanding exactly what it is buying. The implicit message was: we have looked under every rock, and this book is clean. For prospective IPO investors who might have worried about hidden AIG-era skeletons in the closet, Blackstone's endorsement was worth its weight in gold.

The broader context matters too. The Blackstone-Corebridge deal was part of a seismic shift in the insurance industry. Over the preceding decade, alternative asset managers had been systematically inserting themselves into the insurance value chain. Apollo had created Athene in 2009 by acquiring distressed annuity blocks during the financial crisis. KKR had taken a majority stake in Global Atlantic in 2021. Brookfield was building its own reinsurance platform. The thesis was the same in every case: insurance companies sit on massive pools of long-duration liabilities that need to be invested, and alternative asset managers can generate higher returns on those pools than the insurers' own investment teams. The fee income from managing insurance assets is enormous — and unlike private equity fund fees, it is perpetual, because insurance liabilities never close.

What made the Blackstone-Corebridge partnership distinctive was the scale. Blackstone was not buying a small insurer; it was partnering with one of the largest life and retirement platforms in America. And unlike Apollo, which fully merged with Athene, Blackstone maintained its role as an investment manager rather than an owner-operator. The equity stake was 9.9% — large enough to signal commitment, small enough to avoid regulatory complications that would come with a larger ownership position.

There is an irony here worth noting. The 2008 crisis was caused, in part, by the entanglement of insurance companies with complex financial instruments they did not fully understand. And here, fifteen years later, the path to liberation for AIG's best business ran directly through a deep partnership with one of the most complex financial engineering firms in the world. The difference, of course, was that Blackstone was not selling insurance against risk it could not measure. It was doing something much simpler: using its origination platform to find better-yielding investments for an insurer's conservative portfolio. Same industry. Completely different transaction. But the historical rhyme was hard to miss.

With the Blackstone partnership secured, the stage was set for the biggest IPO of 2022 — and one of the more turbulent debut stories in recent insurance history.

V. The IPO and The Kevin Hogan Bridge (2022–2024)

September 15, 2022. The date carried its own freight of symbolism: the fourteenth anniversary of Lehman Brothers' bankruptcy filing, the event that had set AIG's crisis in motion. Whether the choice was deliberate or coincidental, Corebridge Financial chose that day to begin trading on the New York Stock Exchange under the ticker CRBG, raising $1.68 billion at $21 per share — the low end of its marketed $21 to $24 range.

The timing could hardly have been worse from a market perspective. The Federal Reserve was in the midst of its most aggressive rate-hiking cycle in four decades. The S&P 500 was deep in a bear market, down more than 20% from its January highs. Bond portfolios were suffering their worst losses in a generation. The word "recession" was being whispered with increasing conviction on trading floors from New York to London.

And yet, the IPO got done. In a year when dozens of companies postponed or cancelled their public offerings, Corebridge muscled through the market turbulence and completed the largest American IPO of 2022.

That alone told a story about the underlying demand for the business. Even in a terrible market, institutional investors could see what was underneath: a company managing over $380 billion in assets, serving millions of policyholders, and generating billions in predictable cash flow. The yield was attractive. The demographic tailwind was real. The Blackstone validation was fresh.

Leading the company through this critical passage was Kevin Hogan, an AIG veteran who had spent thirty-eight years inside the organization. Hogan had been running AIG's Life and Retirement division since December 2014 — he knew every corner of the business, every actuarial assumption, every distribution relationship. He was the institutional memory, the person who knew where the bodies were buried and, more importantly, could assure investors there were no bodies left to find.

Hogan was a bridge CEO by design, not by default. A Dartmouth graduate who had started at AIG in 1984 and worked across the company's operations in Chicago, Tokyo, Hong Kong, Singapore, and China before leading the global life insurance operations at Zurich Insurance Group from 2009 to 2013, Hogan returned to AIG to take over the Life and Retirement division in December 2014. He had been preparing it for independence ever since.

His mandate was clear: execute the separation from AIG cleanly, establish Corebridge as a credible standalone company, meet every financial target laid out during the IPO roadshow, and set the stage for a permanent leader to take the company forward.

It was the kind of assignment that required steady hands and a willingness to do unglamorous work — the corporate equivalent of building a house's foundation while everyone asks about the paint color. Hogan negotiated transition service agreements with AIG to ensure that functions previously shared — technology, compliance, human resources — continued without disruption during the separation. He built standalone IT infrastructure, hired hundreds of employees for functions that had previously been shared, and established a separate treasury operation.

He also had to build a new corporate culture for a company that had never had one — Corebridge's employees had always been "AIG people," and now they needed to become something else. New email addresses. New business cards. A new corporate identity. The mundane mechanics of corporate separation are rarely discussed in business school case studies, but they are enormously complex and expensive to execute — and any misstep can disrupt operations, confuse customers, and undermine the very independence the separation was supposed to achieve.

The most consequential strategic move during Hogan's tenure was the de-risking of the variable annuity portfolio. To understand why this mattered, you need a quick detour into what makes variable annuities so treacherous for insurers.

A variable annuity is a retirement product where the customer's money is invested in market-linked sub-accounts — essentially mutual funds inside an insurance wrapper. Many of these products, particularly those sold in the 2000s, came with guaranteed minimum income benefits, known in the industry as GMIBs or GMWBs.

These guarantees promised customers a minimum payout regardless of how the market performed. In good times, the guarantees sat dormant — the market was doing fine, so nobody needed the guarantee. But when markets crashed — as they did in 2008, in 2020, and again during the 2022 bear market — these guarantees became enormously expensive liabilities.

The insurer was on the hook for the difference between the market value of the portfolio and the guaranteed minimum. Think of it this way: if you sold someone an annuity with a guaranteed 5% annual withdrawal rate on their original $100,000 investment, and the market dropped their portfolio value to $60,000, you still owe them $5,000 per year based on the original amount. You have to put aside reserves to cover that gap. It was like having written a massive put option on the stock market, and every time volatility spiked, the reserves required to back those guarantees ballooned.

For Corebridge, these legacy variable annuities were an anchor. Institutional investors looked at the VA book and saw tail risk — the possibility that a severe market downturn could force the company to post billions in additional reserves. It suppressed the company's valuation multiple. Analysts could not give Corebridge a clean growth multiple because the VA guarantees introduced a catastrophic risk scenario that was difficult to model.

Enter Venerable Holdings, a specialized company built explicitly to manage runoff blocks of variable annuities. Venerable's business model is conceptually simple: it acquires VA liabilities from companies that want to get rid of them, concentrates them in a portfolio managed by specialists, and uses hedging strategies and scale to manage the risk more efficiently than the original insurer could.

In June 2025, Corebridge announced what it called a "transformative" transaction: it would reinsure its entire individual retirement variable annuity book to CS Life Re, a Venerable subsidiary. The total account value was approximately $51 billion — $5 billion of general account assets reinsured on a coinsurance basis and $46 billion of separate account assets reinsured on a modified coinsurance basis.

The deal generated approximately $2.8 billion in total value for Corebridge, including roughly $2.1 billion of net distributable proceeds after tax. For Venerable, the transaction increased its total assets under risk management by roughly 77%, making it the dominant player in the VA runoff space.

The largest portion closed in August 2025, covering variable annuities issued by American General Life Insurance Company — representing approximately 90% of the total transaction value. The final tranche, covering policies issued by The United States Life Insurance Company in the City of New York, closed on January 5, 2026. It was, by industry consensus, the largest variable annuity reinsurance transaction ever executed.

The Venerable deal accomplished something that years of financial engineering and hedging programs could not: it removed the variable annuity tail risk from Corebridge's balance sheet in a single stroke. After the transaction closed, legacy VA liabilities represented approximately 1% of the company's balance sheet, down from a significant and hard-to-value exposure that had kept investors cautious. It was the financial equivalent of a cancer patient getting a clean scan — the cloud that had hung over the stock since IPO was finally gone.

But there was another cloud that proved harder to disperse: AIG's stock overhang. At the time of the IPO, AIG retained roughly 78% ownership of Corebridge (Blackstone held its 9.9%). AIG had always intended to sell down its stake over time, but the pace and mechanics of that sell-down created a persistent drag on the stock price.

The secondary offerings came in waves.

A $1.1 billion offering in June 2023. Another billion in November 2023. A $718 million deal at $20.50 per share in December 2023 — that last one particularly painful, as it priced below the IPO price. Then a $876 million offering in May 2024. A billion-dollar block in August 2025. Another in November 2025.

For nearly two years, every time the stock tried to gain momentum, the market anticipated another AIG sale, and the overhang kept a ceiling on the price. It was like trying to fill a bathtub with the drain partially open. Institutional investors who might otherwise have built meaningful positions hesitated, knowing that another wave of supply was always around the corner.

The most significant step in resolving the overhang came in May 2024, when AIG sold a 20% stake — approximately 120 million shares — to Nippon Life Insurance Company of Japan for $3.8 billion at $31.47 per share.

This was a strategic sale, not an open-market dump. Nippon Life, one of the largest life insurers in Japan with over $700 billion in assets, was a long-term holder, not a trader. For Nippon Life, the Corebridge stake represented a strategic entry into the American retirement market at a time when Japan's aging population and ultra-low interest rates made domestic growth virtually impossible. For Corebridge, it replaced a seller (AIG) with a holder (Nippon Life), converting selling pressure into stability.

The deal reduced AIG's ownership to below 50%, and in June 2024, AIG formally waived its right to majority board representation, completing the "deconsolidation" of Corebridge from AIG's financial statements. After sixty-three years of corporate parentage — first American General, then AIG — the retirement business was finally, truly, its own entity.

It is worth noting one additional development in the AIG relationship. In January 2026, AIG announced that Zaffino himself would step down as AIG's CEO by mid-2026, with John Andersen from Aon named as his successor. That transition severs one of the last personal connections between AIG and Corebridge, as Zaffino had continued to serve as chairman of Corebridge's board even after deconsolidation. The era of AIG's influence over Corebridge is drawing to a close.

As of the most recent filings, AIG's stake has been further reduced to approximately 15.5%, with a commitment to maintain at least 9.9% until roughly December 2026 under the terms of the Nippon Life agreement. The overhang is not fully gone, but it has diminished from a thundercloud to a passing shadow.

VI. The New Era: Marc Costantini and The Growth Engine (2025–Present)

Every company gets one chance to pick its first "real" CEO — the leader who is not a caretaker, not a bridge, but the person who defines what the company will become. For Corebridge, that moment came on December 1, 2025, when Marc Costantini officially took the helm.

Costantini's resume reads like it was assembled by a casting director looking for the ideal insurance CEO. A graduate of Montreal's Concordia University and a Fellow of the Society of Actuaries — the profession's highest credential, requiring years of rigorous mathematical examinations — he brought over thirty-five years of industry experience spanning the most relevant domains for Corebridge's future.

At Guardian, he served as CFO and then executive vice president of commercial and government markets. At Munich Re, one of the world's largest reinsurers, he ran corporate development, strategy, and digital solutions for the North American life and health business. Most recently, at Manulife — the Canadian insurance giant — he was the global head of strategy and inforce management, leading corporate strategy, corporate development, and initiatives to improve the profitability and risk profile of Manulife's existing book of business.

That last role is particularly telling. "Inforce management" is insurance jargon for making the most out of policies already on the books — optimizing pricing, improving retention, reducing lapses, and extracting value from long-duration liabilities. It is exactly the skill set required to run a company like Corebridge, where the existing $385 billion book of assets is the most important asset of all.

Look at Costantini's compensation structure and you can read Corebridge's board priorities like a blueprint.

Base salary: $1 million. Target annual cash incentive: $2.5 million. Target annual long-term equity incentive: $8 million, delivered in performance share units, restricted stock, and stock options. A one-time $5.5 million cash signing bonus to replace awards forfeited from his prior employer. A one-time $10 million long-term incentive grant.

Add it up, and approximately 84% of his total compensation is "at risk" — tied to stock price appreciation and return on equity. The message from the board is unambiguous: grow the stock price, improve returns, or leave money on the table.

In his first earnings call as CEO in February 2026, Costantini framed his strategy around three pillars: profitable growth, cash generation, and balance sheet strength. But the most revealing comment was about distribution. "The average relationship with our top twenty-five partners is a quarter century long," he told analysts, "and more than forty percent of our annuity sales came from products that have bespoke features tailored for each specific distributor." That is a remarkable competitive advantage. Corebridge does not just sell generic annuities through independent broker-dealers. It builds custom products — unique riders, fee structures, and features — specifically for its largest distribution partners. That creates switching costs for the distributors themselves, not just the end customers.

The growth story that Costantini inherited — and is now accelerating — has two engines that merit close attention.

The first is Pension Risk Transfer, or PRT. This is a segment of the insurance market that most retail investors have never heard of, and it is growing explosively. Here is how it works: A large corporation — think General Motors, Verizon, FedEx — has a defined benefit pension plan. That plan represents a massive long-term liability on the company's balance sheet. The company is responsible for making monthly payments to retirees for the rest of their lives, and the actuarial risk of those payments — longevity risk, investment risk, interest rate risk — sits squarely on the company's shoulders.

Many corporations want out. They want to "de-risk" their pension obligations by transferring them to an insurance company.

In a PRT transaction, the corporation pays a large lump sum to an insurer like Corebridge, and the insurer assumes the obligation to make pension payments to the retirees going forward. The corporation gets the liability off its balance sheet — no more volatile pension expense on the income statement, no more quarterly actuarial adjustments, no more fiduciary responsibility for investment decisions. The insurer gets a massive block of long-duration liabilities that it can match against its investment portfolio, earning the spread between investment returns and the guaranteed payments.

The deals can be enormous. MetLife and Prudential Financial split a $16 billion pension transfer from IBM in 2022. MetLife handled a $6 billion FedEx transaction in 2018. These are the kinds of mega-transactions that can transform an insurer's balance sheet in a single quarter.

The PRT market is enormous and growing. To grasp the scale: American corporations still carry approximately $3 trillion in defined benefit pension obligations on their balance sheets. These are promises made decades ago, when companies like General Motors and U.S. Steel offered lifetime pensions as standard benefits. Corporate America no longer wants to be in the pension business. The regulatory burden is heavy, the investment risk is significant, and every CFO in America would rather spend capital on growth than on managing pension liabilities for employees who retired twenty years ago.

According to MetLife's 2025 survey, 94% of defined benefit pension plan sponsors with de-risking goals intend to fully divest their pension liabilities — up from 46% in 2015. The demand is not just growing; it is accelerating. Corebridge has over thirty-five years of experience in this market, and its Institutional Markets segment — which includes PRT and guaranteed investment contracts — grew sales 24% in full-year 2025. In the third quarter alone, premiums and deposits in the segment surged 230% over the prior year, driven by new PRT transactions and guaranteed investment contract issuances. The business is inherently lumpy — individual transactions can be worth hundreds of millions or even billions of dollars — but the secular trend is unmistakable.

The second growth engine is a new product called MarketLock, a Registered Index-Linked Annuity, or RILA. To understand why this product is significant, consider the psychology of a sixty-five-year-old baby boomer in 2025. They have lived through the dot-com crash, the 2008 crisis, the COVID crash, and the 2022 bear market. They want their retirement savings to participate in stock market upside — nobody wants to earn 3% in a fixed annuity while the S&P 500 rises 20%. But they also cannot afford another 30% drawdown. They are too old to recover. They need something in between: upside participation with downside protection.

That is exactly what a RILA delivers. MarketLock tracks a market index like the S&P 500 and allows the customer to participate in gains up to a cap rate. On the downside, the insurer absorbs the first layer of losses — typically a 10% or 15% "buffer."

Here is a simple example: suppose a customer invests $100,000 in a RILA with a 10% buffer and a 15% cap. If the S&P 500 rises 20% over the contract term, the customer earns 15% — capped, but still a meaningful return. If the S&P 500 drops 8%, the customer loses nothing — the insurer absorbs the entire loss because it falls within the 10% buffer. If the S&P 500 drops 25%, the customer absorbs only 15% of the loss (the 25% drop minus the 10% buffer). It is not a guarantee of zero loss — that would be a traditional fixed-index annuity — but it provides a meaningful cushion that makes the product psychologically appealing to risk-averse retirees who still want to participate in market growth.

The timing of this product launch was not accidental. The RILA category has been one of the fastest-growing segments of the annuity industry, expanding from virtually nothing in 2015 to over $50 billion in annual sales across the industry by 2025. Corebridge was late to the party — Allianz, Lincoln National, and Equitable had built significant RILA businesses years earlier — but it entered with the advantage of scale and distribution relationships that smaller competitors could not match.

Corebridge launched MarketLock in October 2024, making it the only top-three annuity provider with products in every major annuity category. The results were immediate and striking. In its first full quarter, the product generated $260 million in sales. It passed $1 billion in cumulative sales within nine months of launch. For full-year 2025, MarketLock generated $1.9 billion in sales and was available through more than 200 distribution partners. In under fifteen months, Corebridge went from having no RILA product to being a top-ten RILA provider in the United States. That speed of adoption tells you something about both the product design and the power of Corebridge's distribution network.

VII. Business Model: The Spread

Strip away the complexity of insurance jargon, regulatory capital, and actuarial tables, and Corebridge's business model is remarkably simple. It is a spread business. The company takes in money from customers. It invests that money. And it earns the difference between what it pays customers and what it earns on investments.

Step one: take in money. Corebridge collects premiums and deposits from annuity customers, life insurance policyholders, pension plan participants, and institutional clients. In 2025, total premiums and deposits reached $41.7 billion. The cost of this capital — the rate Corebridge credits to policyholders on their annuity balances — runs approximately 3% to 4%, depending on the product and competitive environment. Think of it as the "interest rate" Corebridge pays to "borrow" money from its customers through insurance products.

Step two: invest the money. Corebridge deploys those funds into a diversified investment portfolio: investment-grade corporate bonds, commercial mortgages, structured credit, and — thanks to the Blackstone partnership — private credit and alternative assets that generate higher yields than public fixed-income markets. The blended portfolio yield runs approximately 5% to 6%.

Step three: pocket the difference. That 1.5 to 2 percentage point spread between the cost of funds and the investment yield is the profit. On a base of $385 billion in assets, even a small spread generates enormous cash flow.

Think of it like a bank's net interest margin, but with two crucial differences. First, the liabilities last decades instead of months — a fixed annuity buyer is committed for ten to fifteen years, not overnight like a bank depositor. Second, the insurer gets to invest in longer-duration, less liquid assets because it knows its liabilities are locked in — an advantage banks, which must maintain daily liquidity for depositor withdrawals, simply do not have.

The beauty of the model is its duration. When a customer buys a fixed annuity or a life insurance policy, they are essentially lending money to Corebridge for ten, twenty, or thirty years. The liabilities are long-duration and predictable. Corebridge can match them against long-duration assets — thirty-year corporate bonds, fifteen-year commercial mortgages — and lock in the spread for years. Unlike a bank, which faces the constant risk of deposit flight, an insurance company's liabilities are contractually locked. Customers cannot withdraw their annuity balances without paying surrender charges — typically 7% to 10% in the early years of the policy, declining to zero after five to ten years.

This is the critical difference between an insurer and a bank, and it matters enormously for understanding Corebridge's risk profile. In March 2023, Silicon Valley Bank collapsed because depositors — who could withdraw their money instantly with no penalty — all ran for the exits at the same time. A life insurer cannot experience a "run on the bank" in the same way. Policyholders who want to surrender their annuities early face financial penalties that make withdrawal economically unattractive. And for products like pension risk transfers and life insurance policies, there is no withdrawal option at all. The money is committed. That funding stability — what the industry calls "liability stickiness" — is the foundation of the business and the reason insurance stocks held up far better than bank stocks during the 2023 banking crisis.

The company operates through four distinct segments, each with its own character and growth profile.

Individual Retirement is the cash cow. This segment sells fixed annuities, variable annuities, fixed-index annuities, and now the MarketLock RILA product to individual customers through independent broker-dealers and financial advisors. In 2025, this segment generated $20.6 billion in premiums and deposits and nearly $3 billion in spread and fee income. It is the largest segment by revenue and the most mature by growth profile.

The way this segment works in practice is worth understanding, because it reveals the distribution dynamics of the entire annuity industry. A sixty-two-year-old retiring teacher in Florida walks into her financial advisor's office. The advisor — who works for an independent broker-dealer like LPL Financial, Raymond James, or Cetera — looks at her $400,000 in savings and recommends a fixed annuity from Corebridge. Why Corebridge? Because the advisor has a relationship with Corebridge's wholesaler, trusts the company's claims-paying history, and knows the product features well. The advisor earns a commission — typically 4% to 7% of the premium — paid by Corebridge. The teacher gets a guaranteed income stream for life. Corebridge gets $400,000 of long-duration capital to invest.

Multiply that scenario by hundreds of thousands of transactions per year, and you begin to see the engine. The competitive landscape is fierce — Athene, Jackson Financial, Lincoln National, and dozens of smaller players all compete for the same advisor's attention — but Corebridge's scale and distribution relationships give it staying power. The company's top twenty-five distribution partners have been with them for an average of twenty-five years. That kind of institutional trust does not switch easily.

Group Retirement is the moat. This is the VALIC franchise — the direct descendant of that 1955 startup that began selling tax-deferred annuities to nonprofit employees. Today, Corebridge is the number-one provider of 403(b) plans to K-12 school districts in the United States.

The business model here is different from Individual Retirement. It is fee-based: Corebridge acts as the recordkeeper and investment platform for school district retirement plans, earning advisory and administration fees rather than spread income. The revenue per account is lower, but the retention rates are extraordinarily high.

The money is incredibly sticky. A schoolteacher who sets up automatic payroll deductions into a VALIC 403(b) plan at age twenty-five will likely keep that arrangement for their entire forty-year career. The switching costs are not just financial — they are logistical and psychological. Changing 403(b) providers means new paperwork, new investment options, new login credentials, and the anxiety of moving a lifetime of retirement savings to an unfamiliar platform. There is no competing with inertia.

Life Insurance is the steady earner. Corebridge sells term life, universal life, and indexed universal life products. This segment is not a growth engine — the life insurance market in the United States has been relatively flat for years — but it generates reliable underwriting margins and diversifies the company's risk profile away from pure spread dependence. The underwriting margin was $1.364 billion in 2025. More importantly, the life insurance book provides a natural hedge against the annuity business. Annuities lose money when people live longer than expected — the company has to keep paying them. Life insurance loses money when people die sooner than expected. These two risks partially offset each other, creating a more stable combined portfolio. Actuaries call this "natural hedging," and it is one reason diversified life and retirement companies tend to trade at higher multiples than pure-play annuity shops.

Institutional Markets is the rocket ship. This is where PRT transactions and guaranteed investment contracts live. It is the fastest-growing segment, with 2025 sales up 24% year over year.

The PRT opportunity alone could make this segment larger than Individual Retirement within a decade if the secular trend of corporate pension de-risking continues at its current pace. The economics are attractive: PRT transactions tend to be large, one-time premium payments that Corebridge can invest against long-duration liabilities.

The challenge is the lumpiness — a single large PRT deal can swing quarterly results dramatically, making quarter-to-quarter comparisons nearly meaningless. In Q3 2025, for example, premiums and deposits in the segment surged 230% over the prior year quarter because of the timing of specific large transactions. Investors who focus on quarterly noise rather than annual trends will find this segment frustrating. But the secular direction of travel is unmistakable.

Together, these four segments create a business that generated $42 billion in total sales in 2025, earned $2.4 billion in adjusted after-tax operating income, and returned $2.6 billion to shareholders through dividends and buybacks — a payout ratio of 110%, meaning Corebridge returned more cash to shareholders than it earned, funded partially by the Venerable transaction proceeds.

One important nuance on the 2025 financials: while adjusted operating income was $2.4 billion, the GAAP net result was a loss of $366 million. The gap between these two numbers is almost entirely driven by non-cash accounting charges related to the Venerable variable annuity reinsurance transaction and losses on embedded derivatives — complex accounting items that reflect mark-to-market volatility rather than actual cash outflows. This is a common pattern in insurance company financials, where GAAP accounting and economic reality can diverge dramatically. Investors who focus exclusively on the GAAP number might conclude Corebridge lost money in 2025; investors who understand the underlying cash flow dynamics see a company that generated more than enough cash to fund a massive buyback program while simultaneously growing its book of business. The operating earnings number, while a non-GAAP metric that should always be scrutinized, provides a more accurate picture of the business's ongoing cash generation capacity.

The Q4 2025 results, reported in early February 2026, underscored this point. The quarter produced $6.34 billion in revenue — up nearly 36% year over year and beating analyst estimates by a wide margin. Operating earnings per share came in at $1.22, roughly 10% above consensus. The beat was driven by strong performance across all four segments, with PRT transactions and the continued ramp of MarketLock providing the most visible growth catalysts.

VIII. Strategic Analysis

Picture a war room where the combatants are not generals but actuaries, asset managers, and private equity titans — all fighting over the same prize: the trillions of dollars flowing into retirement products as America ages. Understanding who wins this war requires looking at Corebridge's competitive position through two complementary lenses: Michael Porter's Five Forces, which examines the structure of the industry, and Hamilton Helmer's Seven Powers, which identifies the durable sources of competitive advantage.

Start with rivalry, which is intense and getting more so. The annuity and retirement insurance market has become one of the most contested spaces in financial services.

On one side are the traditional insurers — MetLife, Prudential Financial, Lincoln National, Jackson Financial — companies with decades of experience and established distribution networks. On the other side are the private equity-backed insurgents — Apollo's Athene, KKR's Global Atlantic, Brookfield Reinsurance — firms that have married alternative asset management capabilities with insurance liabilities to create what some call "financial engineering meets insurance."

The scale of the competitors is sobering. Athene, which merged with Apollo in 2022, now manages over $430 billion in total assets and moved $9.5 billion in annuities in a single quarter in 2025. Apollo's total AUM across all strategies exceeds $930 billion. KKR completed its full acquisition of Global Atlantic in January 2024 and has grown the platform from $72 billion to nearly $200 billion in assets under management. The competition for annuity flows is fierce, and the PE-backed players have a structural advantage: they can access private credit markets at scale through their parent organizations.

Buyer power in this industry is high because distribution is controlled by independent intermediaries. Independent broker-dealers and financial advisors control the flow of annuity sales. If Corebridge does not offer competitive commission structures, attractive product features, and efficient processing, these intermediaries will simply sell a competitor's product instead. This is why Costantini's emphasis on bespoke product design for top distribution partners is so strategically important — it creates switching costs at the distributor level, not just the customer level.

Barriers to entry are enormous, and this is where Corebridge's position is most secure. Starting an insurance company requires billions in statutory capital, extensive regulatory approvals in every state where you want to do business, actuarial talent, and a distribution network that takes decades to build. Consider what it actually takes: an aspiring annuity company would need to file with all fifty state insurance regulators, establish risk-based capital reserves that meet or exceed regulatory minimums in each jurisdiction, build or acquire an actuarial team capable of modeling liabilities that stretch out forty or fifty years, and then convince independent financial advisors — who already have established relationships with existing providers — to learn a new product suite and risk their clients' retirement savings on an unproven name.

The regulatory moat alone — state-by-state licensing, risk-based capital requirements, policyholder protection funds, annual statutory filings — means that new entrants cannot simply appear. Even the PE-backed players entered by acquiring existing insurance companies rather than building from scratch. KKR bought Global Atlantic. Apollo created Athene by merging existing insurance blocks. Nobody builds this from the ground up. This is not fintech, where a software engineer with a clever API can disrupt a market in eighteen months. This is an industry where the barriers are measured in billions of dollars and decades of regulatory compliance history.

The threat of substitutes is moderate and rising. Traditional bank products (CDs, savings accounts), robo-advisors, target-date mutual funds, and even cryptocurrency-based yield products compete for retirement savings. But none of these substitutes offer the tax-deferred compounding, guaranteed income features, and mortality pooling that make annuities uniquely suited for retirement planning. The substitution threat is real for accumulation products but limited for income products — and as more boomers enter the "distribution phase" of retirement, the demand for guaranteed income is increasing, not decreasing.

Supplier power is concentrated in one critical area: the alternative asset managers who manage insurer investment portfolios. Blackstone manages approximately $92 billion of Corebridge's portfolio. That is a significant dependency. If Blackstone's performance deteriorates or the relationship sours, Corebridge would face a complicated and potentially expensive transition. However, the long-term nature of the partnership agreement and the mutual economic interests create strong alignment.

Through the lens of Hamilton Helmer's Seven Powers, Corebridge's competitive position shows three meaningful advantages.

Scale economies are the strongest power. With over $385 billion in assets under management and administration, Corebridge can spread its fixed costs — compliance, technology, regulatory filings, actuarial modeling — over an enormous base.

To put this in perspective: a smaller competitor with $50 billion in AUM faces the same regulatory burden — the same annual filings in fifty states, the same actuarial modeling requirements, the same cybersecurity standards — but has one-seventh the asset base to absorb those costs. Every dollar spent on compliance at Corebridge is borne by $385 billion in assets; the same dollar at a smaller competitor is borne by a fraction of that base. In insurance, size is not just a convenience; it is a necessity for competitive unit economics.

The cornered resource is the Blackstone partnership. Corebridge has exclusive access to Blackstone's private credit origination for its insurance portfolio — a capability that smaller insurers simply cannot replicate. The yields generated by this partnership flow directly into Corebridge's investment returns, widening the spread and improving profitability. This is not a permanent competitive advantage — Blackstone manages assets for multiple insurance clients — but the scale and duration of the Corebridge relationship provide meaningful preferential access.

Branding is the legacy power, and it cuts both ways. Corebridge carries the weight of its AIG history, which still deters some customers and investors. But it also carries the trust earned by ninety-nine years of continuous operation: "We've been paying claims since 1926" is a powerful statement in an industry where trust is the product. In the K-12 teacher market especially, the VALIC brand carries decades of accumulated goodwill and institutional credibility.

The counter-positioning power is where things get interesting. Corebridge's status as a public, independently traded company with transparent financials and regulated capital requirements makes it fundamentally different from the PE-backed platforms. That difference appeals to certain customers, distributors, and regulators who are increasingly uncomfortable with the opacity and leverage that can characterize private equity-owned insurers.

This is not a theoretical concern. In recent years, state insurance regulators and the National Association of Insurance Commissioners have intensified their scrutiny of PE-owned insurance companies. The core worry is straightforward: when an alternative asset manager owns an insurance company, the asset manager earns fees by placing more complex, higher-yielding (and potentially riskier) assets into the insurer's portfolio. That creates a potential conflict of interest — the asset manager benefits from reaching for yield, but the policyholders bear the risk if those assets go bad. Several state regulators have issued guidance or implemented rules requiring additional disclosure and oversight for PE-owned insurers.

Corebridge occupies an interesting middle ground. It is not PE-owned — it is publicly traded with a diverse shareholder base. But it does have a deep partnership with Blackstone, which manages a significant portion of its investment portfolio. This hybrid structure gives it some of the yield advantages of the PE model while maintaining the transparency and regulatory posture of a traditional insurer. Whether this positioning proves to be a durable advantage depends on how aggressively regulators move against the PE-insurance model in the coming years. If regulation tightens meaningfully, Corebridge's structure could become a significant competitive advantage. If the regulatory environment remains accommodative, the PE platforms retain their edge in agility and yield optimization.

IX. The Bear and Bull Case

Every investment thesis has a shadow side, and Corebridge's is no exception. The bear case against Corebridge begins with the overhang that has defined the stock since its debut. AIG still holds approximately 15.5% of the company's shares and, while contractually committed to maintaining at least 9.9% until December 2026, will eventually sell the remainder. Every secondary offering puts selling pressure on the stock, and the market has learned to anticipate these events. Until AIG is fully out, there is a ceiling on how high the stock can trade. The stock's journey tells the story: from $21 at IPO to a trough near $12 in March 2023 during the regional banking panic, then a recovery to an all-time high near $36 in July 2025, and now back to the low $30s in early March 2026. The volatility is partly a function of the business, but it is largely a function of the overhang.

The second bear concern is credit risk, and it deserves careful examination because it represents the single largest existential threat to the business model. Corebridge's profitability depends entirely on the spread between its investment yields and its cost of funds. If the economy enters a serious downturn and the private credit assets that Blackstone has placed in Corebridge's portfolio begin to experience defaults, the spread compresses — or worse, turns negative.

To understand why this matters, consider the math. Corebridge earns roughly 5% to 6% on its investment portfolio and pays roughly 3% to 4% to policyholders. That 1.5 to 2 percentage point spread generates the company's entire profit. If defaults in the private credit portfolio cause investment losses of just 50 basis points — half a percentage point — the spread gets cut by a quarter to a third. If losses hit 1.5 percentage points, the profit disappears entirely. On a $385 billion asset base, even small shifts in credit quality translate into billions of dollars in economic impact.

Private credit, by its nature, is less liquid and less transparent than public bonds. When a publicly traded bond from IBM or Johnson & Johnson drops in value, everyone can see the price in real time. Private credit — direct loans to mid-market companies, structured real estate debt, infrastructure financing — does not trade on an exchange. In a stress scenario, these assets can be harder to value, harder to sell, and harder to assess than traditional fixed-income holdings. Bears argue that Corebridge — and the broader PE-backed insurance model — has been tested only in a benign credit environment. The post-2020 era has been characterized by low defaults, ample liquidity, and rising asset values. Nobody knows what happens when the cycle turns.

Third, competition from the PE-backed platforms is relentless, and this may be the most important structural concern of all. Apollo's Athene is the gorilla in the room, with assets approaching $430 billion and a vertically integrated model that gives it structural cost advantages in sourcing private credit. When Apollo originates a private loan, it can place it directly into Athene's portfolio without the intermediation costs and friction that Corebridge faces when working through Blackstone. KKR's Global Atlantic, at nearly $200 billion in AUM, is growing rapidly and benefits from a similar vertical integration with KKR's credit origination platform.

These platforms have a single-minded focus on spread optimization that is harder for a public company to match. Athene does not have quarterly earnings calls where analysts second-guess its investment portfolio. Global Atlantic does not worry about retail shareholder sentiment. The PE platforms can move faster, take more concentrated positions, and tolerate more complexity — and in a spread business, even small advantages compound over time. A 10 basis point advantage in investment yield, sustained over a decade on hundreds of billions of dollars, translates into billions of incremental profit.

There is also a fourth bear argument that often gets overlooked: interest rate sensitivity. While higher rates have been broadly positive for Corebridge — allowing it to earn more on new investments — a rapid decline in rates would compress new money yields while the company is still locked into its existing crediting rates on outstanding policies. This is the opposite of the problem banks face (where rate cuts help by reducing deposit costs), because insurance crediting rates often have contractual floors that cannot be adjusted downward. A scenario where the Federal Reserve cuts rates aggressively while the economy weakens could pressure Corebridge from both sides simultaneously — falling yields and rising credit losses.

The bull case begins with demography, and it is hard to overstate the force of the underlying trend. The peak of Peak 65 hit in 2025, with approximately 11,400 Americans turning sixty-five every single day — 4.18 million people reaching traditional retirement age in a single year. The numbers remain elevated at over 4.1 million annually through 2027. By 2030, all baby boomers will be sixty-five or older. These are not projections or estimates subject to revision. These are people who are already alive, already aging, already approaching the moment when they need to convert savings into income.

The financial reality facing many of these retirees makes the demand picture even more compelling. Research from the Alliance for Lifetime Income found that more than half of baby boomers turning sixty-five between 2024 and 2030 have retirement assets of $250,000 or less. Given the likelihood of living twenty or more years in retirement, many will likely exhaust their savings and rely primarily on Social Security. For this cohort, converting whatever savings they have into guaranteed lifetime income is not a luxury — it is a necessity. And the primary financial product for converting savings into guaranteed lifetime income is an annuity.

The sheer scale of the retirement wave creates a demand surge that benefits every player in the annuity industry, but it particularly benefits companies with the broadest product suites and the deepest distribution relationships. Corebridge is the only company with a top-ten position in every major annuity category — fixed, variable, fixed-index, and now RILA. It can serve whatever a customer wants. That breadth is a significant competitive advantage in a market where financial advisors want to work with a small number of trusted providers rather than managing relationships with a dozen different insurers.

The second bull argument is multiple expansion, and it requires understanding what has been holding the valuation back. Corebridge trades at a meaningful discount to peers — partly because of the AIG overhang, partly because of the legacy VA risk (now largely resolved through the Venerable transaction), and partly because the company is still in the early innings of establishing its identity as an independent entity. The stock essentially carries a "scarlet letter" discount — the market remembers AIG's sins and applies a guilt-by-association penalty to a business that never committed them.

As AIG continues to exit and the market gains confidence in Corebridge as a standalone operator, that valuation gap should narrow. Consider the progression: Zaffino stepped down from AIG's CEO role in early 2026, severing one of the last personal connections between the two companies. Nippon Life, a long-term strategic holder, now owns 20% — providing stability rather than selling pressure. The Venerable deal removed the VA tail risk. Each of these milestones chips away at the discount. Whether the gap fully closes depends on execution, but the direction of travel is favorable.

Third, capital return is substantial and accelerating. In 2025, Corebridge returned $2.6 billion to shareholders — $2.1 billion in buybacks and the remainder in dividends. The share count has declined from approximately 650 million at IPO to roughly 500 million today, a 23% reduction in just over three years. With the Venerable proceeds largely earmarked for additional buybacks, the share count should continue to shrink. The current dividend yield sits at approximately 3.2%, and the board has increased the quarterly dividend every year since the IPO. For investors who view Corebridge as a "cash flow compounder" — a company that generates far more cash than it needs for growth and returns the excess to shareholders — the math is compelling.

Regardless of where one lands on the bear-bull spectrum, the path forward for Corebridge will be tracked through a handful of critical metrics. For investors following this story going forward, three KPIs deserve primary attention.

The first and most important is net investment spread — the difference between what Corebridge earns on its investment portfolio and what it pays policyholders. This is the most direct measure of profitability, and it captures both sides of the business equation simultaneously: investment performance and liability management. Any compression in the spread, whether from rising crediting rates to stay competitive with Athene, deteriorating asset quality in the Blackstone-managed portfolio, or a shift in product mix toward lower-spread products, flows immediately to the bottom line. Conversely, spread expansion — driven by higher-yielding private credit allocations or favorable interest rate movements — is the most powerful lever for earnings growth. Watch the spread the way you would watch same-store sales at a retailer: it is the single number that tells you whether the core business is getting better or worse.

The second is premiums and deposits growth — the total inflow of new money into the company across all four segments. This measures whether Corebridge is gaining or losing market share in a market that should be growing rapidly thanks to Peak 65 demographics. The 2025 figure of $41.7 billion sets the benchmark. PRT transaction volumes will cause quarterly volatility — a single large pension transfer can move the number by billions — but the full-year trend is what matters. If premiums and deposits are growing faster than the industry average, Corebridge is winning. If they are growing slower, it is losing the competitive battle to Athene and Global Atlantic regardless of what the spread looks like.

The third is operating return on equity, which measures how efficiently Corebridge deploys its capital base to generate earnings. ROE is the metric that connects everything else — it captures spread efficiency, scale leverage, capital allocation discipline, and growth quality in a single number. Costantini's compensation is explicitly tied to ROE improvement, which aligns management incentives with shareholder interests in the most direct way possible. The 2025 figure showed a 20-basis-point improvement year over year — steady but not transformative. Acceleration here would signal that the growth strategy is translating into real economic returns, while deceleration or decline would suggest that growth is coming at the expense of profitability.

X. Playbook: Lessons for Founders and Investors

Step back from the financial details and the competitive analysis, and the Corebridge story offers three durable lessons that extend well beyond the insurance industry — lessons about how value gets created, hidden, and eventually unlocked in complex organizations.

The first is the "Good Bank/Bad Bank" principle. Sometimes the most valuable businesses in the world are buried inside corporate structures that obscure their quality, suppress their valuation, and prevent them from reaching their potential. AIG's Life and Retirement division generated billions in stable cash flow for two decades while being treated by the market as an appendage of a toxic brand. The conglomerate discount was not just a valuation artifact — it was a strategic prison. The business could not invest in its own growth, could not recruit talent unconstrained by AIG's compensation structures, could not build its own brand identity. Every dollar of capital that should have gone to growing the annuity business was instead diverted to shore up AIG's property and casualty operations or pay down government debt.

The broader pattern is worth noting because it recurs throughout financial history. Citigroup spun off Primerica. General Electric shed GE Capital. Prudential Financial split from Prudential plc decades earlier. In each case, a valuable business was trapped inside a complex conglomerate where it was either misunderstood by investors, starved of capital by the parent, or punished by the parent's reputation. The lesson for investors is to look for these hidden gems inside complex conglomerates — businesses trading at discounts not because of their own fundamentals but because of the corporate structure around them. And the lesson for operators is that, sometimes, the bravest strategic move is simply to set a great business free.

The second lesson is the power of niche dominance. The K-12 teacher market — the VALIC franchise — is not the kind of business that gets discussed at Davos or featured in Harvard Business Review case studies. It is unsexy. It is slow-growing. It involves payroll deductions and school board meetings and state legislature lobbying. But it is extraordinarily sticky, enormously profitable on a per-account basis, and virtually impossible to displace once established. Corebridge's dominance in 403(b) plans for public school employees is the clearest illustration of a principle that applies across industries: niche dominance beats broad mediocrity. The deepest moats are often found in the most boring markets.

The third lesson is about the strategic use of partnerships — and specifically about how to choose a partner whose incentives are structurally aligned with your own. The Blackstone deal was not simply a financial transaction. It was a capability acquisition. Corebridge bought access to a private credit origination platform that would have cost billions and taken years to build internally. It also bought credibility — the market's confidence that its book of business was clean and well-managed. And it bought a strategic partner whose interests are deeply aligned: Blackstone earns management fees proportional to the assets Corebridge allocates, so Blackstone wants Corebridge to grow. Corebridge's investment returns improve when Blackstone delivers superior yields, so Corebridge wants Blackstone to perform. Neither party benefits from the other's failure. That structural alignment — not just a contractual agreement but an economic marriage of interests — is what makes the partnership durable.