Cheniere Energy Partners: America's LNG Export Revolution

I. Introduction & The Stakes

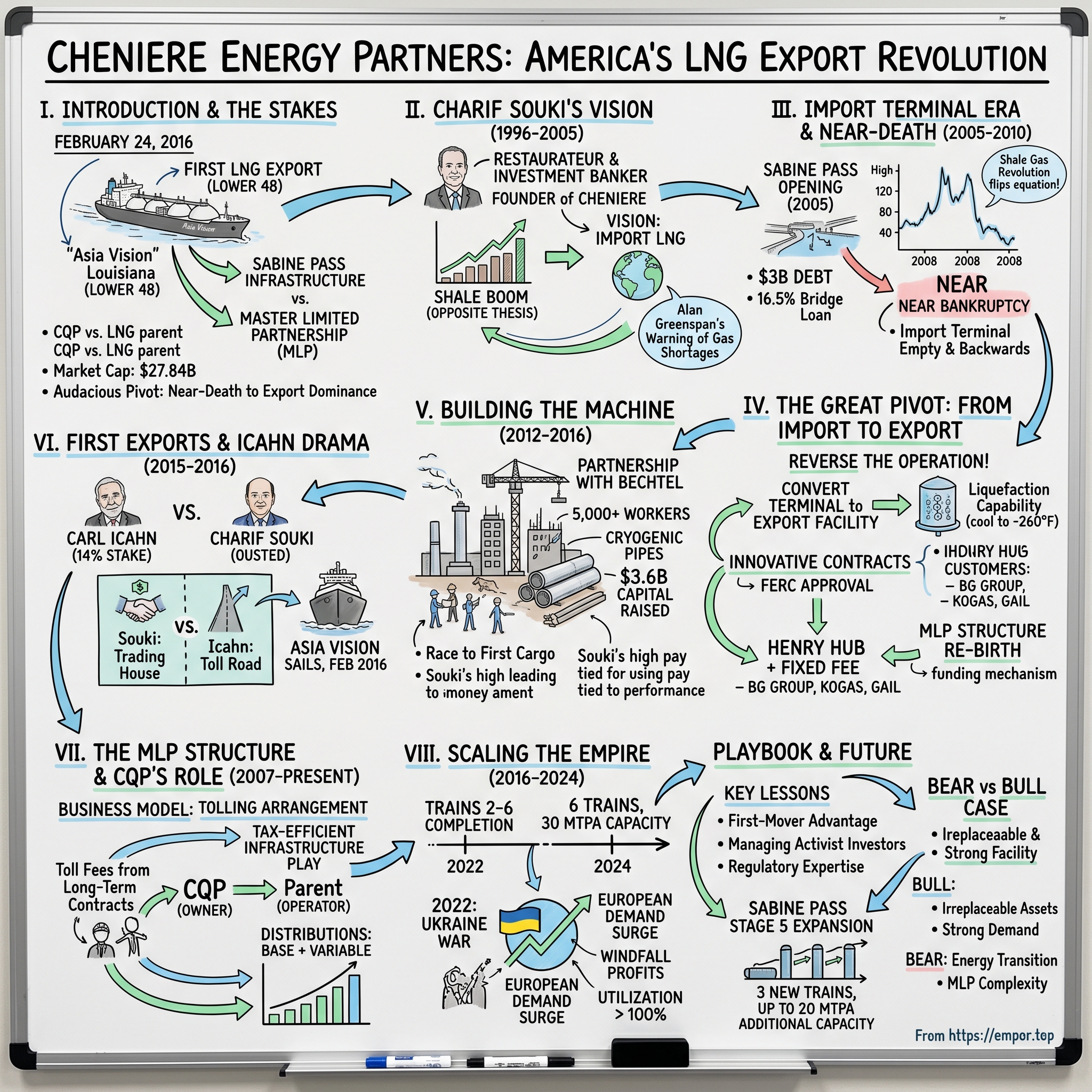

Picture this: February 24, 2016. A massive tanker named Asia Vision slowly pulls away from a dock in Cameron Parish, Louisiana, its hull sitting low in the water, laden with 3 billion cubic feet of super-cooled natural gas. As the vessel begins its journey to Brazil, history quietly unfolds. For the first time since Alaska's Kenai plant shut down in 1969, liquefied natural gas is leaving American shores from the lower 48 states. The company behind this moment? Cheniere Energy—a firm that just eight years earlier teetered on the edge of bankruptcy, having bet everything on exactly the opposite scenario.

The story of Cheniere Energy Partners (CQP) is one of the most audacious pivots in American energy history. It's a tale of how a Lebanese-Egyptian restaurateur turned Wall Street banker built infrastructure to import natural gas into America, only to discover he'd built it backwards. It's about how a company transformed from near-death to becoming the crown jewel of American energy exports, now standing as the largest LNG exporter in the United States and the second-largest producer globally.

But here's where it gets interesting for investors: Cheniere Energy Partners isn't actually Cheniere Energy. It's a master limited partnership (MLP)—a peculiar financial structure that owns and operates the critical Sabine Pass infrastructure while its parent company, Cheniere Energy (ticker: LNG), handles the wheeling and dealing. Think of it as the landlord collecting rent while the parent company runs the hotel. This structure, born from tax efficiency dreams and capital-raising necessities, has created one of the most fascinating dividend machines in American energy. Today, CQP commands a market capitalization of $27.84 billion, making it one of the most valuable energy infrastructure assets in America. But to understand how we got here—how a company went from importing terminals to export dominance, from near-bankruptcy to billions in distributions—we need to go back to the beginning. Back to a time when an unlikely entrepreneur named Charif Souki had a vision that everyone thought was wrong. Twice.

II. The Charif Souki Vision & Cheniere's Origins (1996–2005)

The protagonist of our story cuts an unlikely figure for an energy revolutionary. Charif Souki, born in 1953 in Cairo, Egypt, moved to Beirut, Lebanon in 1957—a cosmopolitan childhood that would later serve him well in the global energy markets. But Souki's path to LNG dominance was anything but direct. Before he became the architect of America's natural gas export revolution, he was slinging steaks and managing restaurants, then pushing papers on Wall Street as an investment banker. Over the course of his colorful career, Charif Souki has been an investment banker, a restaurateur, a wildcatter and now a U.S. natural gas export pioneer. The restaurant venture—including the upscale Mezzaluna chain in Los Angeles and Aspen—taught him about risk, customer service, and the art of the impossible sell. But it was his two decades on Wall Street, specializing in financing small capitalization companies in the energy industry, that gave him the financial engineering skills that would prove essential.

In 1996, at age 43, Souki founded Cheniere Energy with a straightforward if unremarkable plan: drill for oil in the Gulf of Mexico. The company failed to hit a gusher, and Souki transformed it into a developer of natural gas import terminals. This wasn't just a pivot—it was a complete reimagination based on what seemed like an ironclad thesis: America was running out of natural gas.

The data backed him up. By 1999, when Souki began developing Cheniere's LNG business, U.S. natural gas production was stagnating while demand soared. Alan Greenspan himself warned Congress about impending gas shortages. The solution seemed obvious: America would need to import vast quantities of LNG from Qatar, Trinidad, and other gas-rich nations. Souki's plan was to build the infrastructure to receive it.

The centerpiece of this vision was Sabine Pass, a strategic location in Cameron Parish, Louisiana, where the Sabine River meets the Gulf of Mexico. The site offered everything an LNG terminal needed: deep water access for massive tankers, proximity to major pipeline networks, and distance from population centers. Construction began in earnest, with the terminal receiving its first shipment in March 2005.

But here's what makes Souki fascinating as a business leader: he wasn't just building infrastructure—he was selling a narrative. In board meetings and investor presentations, he painted vivid pictures of America's energy future, sketching diagrams and weaving stories with the flair of his restaurateur days. He convinced investors to pour hundreds of millions into what was essentially a bet against American energy production. And for a while, it looked genius.

III. The Import Terminal Era & Near-Death Experience (2005–2010)

The Sabine Pass import terminal opened in 2005 to great fanfare. Here was America's answer to its looming energy crisis—a state-of-the-art facility capable of receiving super-cooled natural gas from around the world, warming it back to gaseous form, and pumping it into America's energy-hungry pipeline network. The timing seemed perfect. Natural gas prices had spiked above $15 per million British thermal units (MMBtu) in late 2005, Hurricane Katrina had exposed the vulnerability of domestic production, and global LNG trade was booming.

But then the music stopped. The 2008 financial crisis hit Cheniere like a sledgehammer. The company's shares are trading at about one-sixth what they were in January, and analysts are talking about bankruptcy. The stock closed Thursday at $5.04, down from $32.64 at the start of the year. But the crisis was merely the catalyst for a deeper problem: the entire premise of the import terminal was evaporating.

International LNG producers had better options. European and Asian markets were paying premium prices for gas, while American prices remained stubbornly low. Why sail to Louisiana when Tokyo would pay three times as much? The beautiful Sabine Pass terminal sat largely empty—a $2 billion monument to a bet gone wrong.

Cheniere, though, finds itself with almost $3 billion in debt and no shareholder equity. In its latest financial filing, it said it arranged a bridge loan, but the interest rate was a whopping 16.5 percent — not exactly a vote of confidence from its bankers. The company's leadership was personally devastated. Since mid-April, Chairman Charif Souki, Vice Chairman Walter Williams and Chief Financial Officer Don Turkleson have been forced to sell most of their holdings — including almost $2.8 million in shares for Souki — as the declining value of their Cheniere shares triggered margin calls.

But here's where the story takes its first dramatic turn. Deep beneath America's heartland, something revolutionary was happening. Hydraulic fracturing and horizontal drilling technologies were unlocking vast reserves of natural gas from shale formations. The Marcellus, the Haynesville, the Eagle Ford—these weren't just new gas fields; they were game-changers that would flip America's energy equation on its head.

When the company failed to hit a gusher, Souki transformed it into a developer of natural gas import terminals. At the time, gas prices were soaring to record highs amid dwindling domestic production. That all changed with the shale boom, which flooded the U.S. market with supply.

By 2009, as Cheniere teetered on bankruptcy's edge, natural gas prices had collapsed from their 2008 highs above $13/MMBtu to under $4. America wasn't running out of gas—it was drowning in it. The import terminal that was supposed to save American energy was now completely backwards. But Souki, ever the visionary salesman, saw opportunity where others saw disaster.

IV. The Great Pivot: From Import to Export (2010–2012)

Imagine being Charif Souki in early 2010. You've built infrastructure designed to do one thing—receive imported gas—at precisely the moment America needs to do the opposite. Most executives would have liquidated, taken their losses, and moved on. Souki did something audacious: he decided to run the entire operation in reverse.

Souki swiftly changed course again, converting Cheniere's import terminal in Louisiana into an export facility and putting the company on track to become the first to ship gas from the lower 48 states. The idea was elegantly simple in concept but staggeringly complex in execution. The Sabine Pass terminal already had the marine infrastructure, storage tanks, and pipeline connections. What it needed was liquefaction capability—the ability to cool natural gas to -260°F, turning it into a liquid that takes up 1/600th the volume.

But first came the regulatory marathon. No company had ever attempted to export LNG from the lower 48 states in the modern era. The regulatory framework didn't even exist. Cheniere needed approval from the Department of Energy to export to countries without free trade agreements with the U.S.—a process that required proving exports were in the "public interest." They needed Federal Energy Regulatory Commission (FERC) approval for the construction itself. On April 16, 2012, the Federal Energy Regulatory Commission granted approval for Houston-based Cheniere Energy to build the first liquefied natural gas (LNG) export terminal in the lower 48 United States. The US$5 billion Sabine Pass LNG project is located at an existing import terminal in Cameron Parish, Louisiana. Obtaining approval from the FERC is one more milestone for our Liquefaction Project, said Charif Souki, Chairman and CEO. We will now finalize the financing arrangements in order to commence construction of the first two LNG trains of our Liquefaction Project promptly.

The regulatory victory was monumental, but it was just the beginning. Souki now had to convince customers to sign 20-year contracts for something that had never been done before—exporting American LNG. He had to raise billions in capital when banks were still skeptical. And he had to do it all while keeping the company afloat with its existing (largely unused) import terminal.

The breakthrough came with the contracts. Souki's genius was in the pricing structure. Traditional LNG contracts were linked to oil prices—a complex formula that made buyers vulnerable to oil market volatility. Cheniere offered something revolutionary: contracts indexed to Henry Hub natural gas prices plus a fixed liquefaction fee. Simple, transparent, and aligned with American gas abundance.

The customers lined up: BG Group for 5.5 million tonnes per annum (mtpa), Gas Natural Fenosa for 3.5 mtpa, KOGAS for 3.5 mtpa, and GAIL (India) for 3.5 mtpa. These weren't just contracts—they were votes of confidence in America's energy future.

Creating the MLP structure was another masterstroke of financial engineering. Cheniere Energy Partners, L.P. was founded in 2003 and is headquartered in Houston, Texas, but it truly came into its own during this pivot period. The MLP structure offered tax efficiency—MLPs don't pay corporate taxes if they distribute most of their income to unitholders. It provided a funding mechanism—yield-hungry investors would buy units, providing capital for construction. And it created a clear division: the MLP would own and operate the infrastructure, collecting steady tolling fees, while the parent company handled the commercial and development risk.

CQP will make quarterly cash distributions on its common units of at least $0.425 per unit, or $1.70 per year, to the extent that it has available cash—a promise that would prove crucial in attracting the right kind of investors. The timing of the 2007 IPO, just before the financial crisis, had been fortuitous. The partnership had access to public markets and a structure that could weather the transformation ahead.

V. Building the Machine: Sabine Pass Construction (2012–2016)

Construction of the project began in January 2012, marking the beginning of one of the most ambitious infrastructure builds in American energy history. Cheniere partnered with Bechtel, the engineering giant that had built Hoover Dam and the Channel Tunnel, to construct the liquefaction trains. The partnership was crucial—Bechtel brought not just engineering expertise but credibility to a project many still viewed skeptically.

The construction site in Cameron Parish became a small city unto itself. At peak, over 5,000 workers swarmed the site, welding massive cryogenic pipes, installing compressors the size of buildings, and constructing storage tanks that could each hold a 747 airplane inside. The logistics were staggering: if you added up all the components for just the first two trains, you'd need 120,000 cubic yards of concrete and 30,000 tons of structural steel.

But construction was just one challenge. Souki was simultaneously managing multiple high-stakes negotiations. Banks needed convincing—ultimately, Cheniere raised $3.6 billion in 2012 from 19 international commercial banks. Customers needed reassuring as mechanical problems and weather delays pushed back timelines. And perhaps most importantly, Souki needed to keep his board aligned on a vision that was burning cash at an unprecedented rate. The compensation numbers tell their own story about the stakes involved. Souki was the highest-paid chief executive officer in the United States in 2013. He earned US$142 million in 2013, including a $133 million stock award that vests as his company hits certain financial and operational goals. This wasn't just excessive compensation—it was a bet on execution, with most of the award tied to construction milestones and stock price targets.

The race to first cargo became an obsession. Every delay cost millions in foregone revenue and tested investor patience. Weather delays, equipment failures, the complexity of integrating systems that had never been integrated before—each setback was scrutinized by analysts who wondered if Cheniere was attempting the impossible.

The customer acquisition strategy revealed another layer of Souki's vision. While securing long-term contracts was essential for financing, he also believed in maintaining exposure to the spot market. This wasn't just about maximizing revenue—it was about creating liquidity in a new market. The customers include BG Gulf Coast LNG, LLC ("BG") for 5.5 mtpa, Gas Natural Fenosa for 3.5 mtpa, KOGAS for 3.5 mtpa and GAIL (India) Ltd. for 3.5 mtpa. These contracts represented approximately 89% of the nominal LNG volumes, leaving room for spot sales that could capture market upside.

By late 2015, as the first train neared completion, tension was building—not just at the construction site, but in the boardroom. The company that had nearly died in 2008 was about to make history. But someone else had been watching, accumulating shares, and preparing to make his move.

VI. First Exports & The Icahn Drama (2015–2016)

The corporate drama that unfolded in late 2015 reads like a Shakespearean tragedy set in the boardrooms of Houston. Carl Icahn, the legendary activist investor who had taken down titans from TWA to Motorola, had quietly amassed nearly a 14% stake in Cheniere. His arrival would transform not just the company's leadership but its entire strategic direction. After amassing nearly 14% interest in Cheniere Energy Inc. stock, activist investor Carl Icahn's sway has been felt again with the exit of Charif Souki. Souki's departure comes about four months after Icahn took a stake in the company. Houston-based Cheniere's board terminated Souki Dec. 13 after 19 years at the company and perhaps months away from the company's first LNG shipments.

The clash was philosophical as much as personal. Icahn told CNBC in an interview on Thursday he was "very instrumental in getting Souki out", taking full responsibility for the action. He called Souki's ideas including buying oil companies, as "harebrained" naming them as the main reason for getting the board to replace Souki. I'll tell you now what he knew — he knew how to go almost bankrupt, because that's what happened to him.

But the deeper disagreement was about Cheniere's future. Souki envisioned the company as a trading powerhouse, using its infrastructure advantage to become a major player in global LNG markets, buying and selling cargoes opportunistically. Icahn wanted something simpler: a toll road that collected fees from long-term contracts. Souki told the Financial Times in September that the Sabine facility would create a global market for LNG that could eventually compete with oil, where millions of short-term deals are done every day. "That fundamentally changes the risk profile" of the company, as one analyst noted.

The timing of the coup was brutal and perhaps strategic. Souki was ousted just weeks before the company's crowning achievement. But on February 24, 2016, history didn't wait for corporate drama to resolve. In February 2016 Sabine Pass made its first LNG shipment. It was the first LNG shipment from the lower 48 states. The United States has exported its first LNG cargo from the lower 48 states, after a tanker set sail from Cheniere Energy's Sabine Pass export terminal in Louisiana. The Asia Vision LNG tanker left the dock at the Sabine Pass terminal at 0139 GMT. The data indicated the tanker was fully loaded, and Cheniere says it is headed for Brazil.

The man who had envisioned, built, and nearly died with this project wasn't there to see his creation fulfill its destiny. But the infrastructure he built—and crucially, the MLP structure he created to own it—would endure and thrive beyond even his ambitious dreams.

VII. The MLP Structure & CQP's Role (2007–Present)

To understand Cheniere Energy Partners' unique position in the American energy landscape, you need to understand the elegant financial engineering of the master limited partnership structure. MLPs are limited by law to apply to enterprises that engage in certain businesses, mostly pertaining to the use of natural resources, such as petroleum and natural gas extraction and transportation. This isn't just regulatory arcana—it's the key to CQP's entire value proposition.

The genius of the MLP structure lies in its tax efficiency. MLPs don't pay corporate taxes as long as they distribute most of their income to unitholders. This creates a powerful alignment: the partnership is incentivized to generate steady, distributable cash flow, while investors receive tax-advantaged income. For yield-hungry investors in a low-rate environment, this was catnip.

Cheniere Energy Partners' IPO in 2007 was perfectly timed—just before the financial crisis froze capital markets. The partnership raised capital when it could, establishing a public currency that would prove invaluable during the transformation from import to export. The promised distributions—CQP will make quarterly cash distributions on its common units of at least $0.425 per unit, or $1.70 per year, to the extent that it has available cash—created a clear covenant with investors.

But here's what makes CQP special among MLPs: its business model. Cheniere Energy Partners is a liquified natural gas producer operating one facility in Sabine Pass, Louisiana. It generates most of its revenue through long-term contracts with customers on a fixed- and variable-fee payout structure. It also generates revenue by selling uncontracted LNG to customers on a short or one-time basis. The profit generated through those activities is split with parent and operator Cheniere Energy.

This isn't a commodity play—it's an infrastructure play. The partnership owns the physical assets: the liquefaction trains, the storage tanks, the marine berths. Customers pay tolling fees to use these facilities, regardless of natural gas or LNG prices. It's the difference between owning an oil well (commodity risk) and owning the pipeline (volume risk, but not price risk).

The relationship with parent Cheniere Energy creates both opportunities and conflicts. The parent company handles commercial development, marketing, and takes more risk. CQP owns and operates mature, cash-flowing assets. This division allows each entity to attract its natural investor base: growth investors for the parent, income investors for the MLP.

The distribution strategy has evolved significantly since those early days. What started as a promise of $1.70 per unit annually has grown substantially as trains came online and cash flows materialized. The coverage ratio—how much cash flow exceeds distributions—provides safety for investors while allowing for distribution growth.

VIII. Scaling the Empire: Trains 2–6 & Beyond (2016–2024)

The years following Souki's departure and the first historic cargo became a masterclass in operational execution. Under new leadership, Cheniere transformed from a development company burning cash to an operational powerhouse generating billions in EBITDA. The buildout was methodical: The first two LNG trains were completed in 2016. Trains 3 and 4 were completed in 2017 and Train 5 in 2019. The sixth train and third berth at SPL were completed in 2022 ahead of schedule and within budget. The numbers tell the story of relentless execution: Through sunny days and some stormy nights, Sabine Pass Liquefaction (SPL) has reliably and safely produced more than 2,000 cargoes since 2016, setting a new standard of excellence in the LNG field. These cargoes have powered factories and homes around the world.

Each train completion was a financial milestone for CQP. The partnership's distribution capacity grew with each operational train, as tolling fees from long-term contracts kicked in. The infrastructure advantage became increasingly apparent: Cheniere Energy Partners, L.P. owns the Sabine Pass LNG terminal located in Cameron Parish, Louisiana, which has natural gas liquefaction facilities consisting of six liquefaction trains that include five LNG storage tanks, vaporizers and three marine berths with a total production capacity of approximately 30 million tons per annum (mtpa) of LNG.

The operational excellence achieved during this period was remarkable. Construction teams learned from each train, reducing costs and timelines. Bechtel and Cheniere developed a rhythm—what took 60 months for Train 1 was accomplished in 50 months for Train 6. The learning curve wasn't just about construction; it was about operations, maintenance, and optimization.

Then came 2022—the year that changed everything. Russia's invasion of Ukraine sent global energy markets into chaos. European nations, desperate to replace Russian pipeline gas, turned to American LNG. Natural gas sold on the U.S. Henry Hub benchmark is trading around $3.94 per million British thermal units, while gas on Europe's TTF hub is topping $26. The infrastructure that Souki had built to import gas, then converted to export it, was now essential to global energy security.

The windfall was staggering. Spot LNG prices reached records, and even contracted volumes benefited from price reopeners and oil-linked formulas that had risen dramatically. CQP, with its fee-based model, captured the volume upside as utilization rates exceeded 100%—a seemingly impossible feat achieved through debottlenecking and optimization.

IX. Business Model & Unit Economics

Understanding CQP's business model requires appreciating the elegance of the tolling arrangement. Imagine owning a bridge where customers pay you to cross, regardless of what's on the other side or how valuable their cargo is. That's essentially CQP's model—customers pay a fixed fee per unit of LNG processed, plus a variable fee tied to Henry Hub prices.

The long-term take-or-pay contracts are the foundation. These 20-year agreements require customers to pay whether they use the capacity or not. It's not just revenue certainty—it's the kind of cash flow stability that makes lenders comfortable and investors sleep well. The customer list reads like a who's who of global energy: BG Group (now Shell), KOGAS, GAIL, Gas Natural Fenosa, and others.

But here's the sophisticated part: the Henry Hub-plus pricing model. Customers pay the cost of feed gas (tied to Henry Hub) plus a liquefaction fee (typically $2.50-3.50 per MMBtu). This structure insulates CQP from commodity price risk while giving customers transparent, market-based pricing. It's a win-win that revolutionized global LNG contracting. The pipeline infrastructure control is another crucial piece. CQP doesn't just own the liquefaction trains; it owns the connective tissue that links gas supply to global markets. The Creole Trail Pipeline, the interconnects to major interstate pipelines—these aren't just pipes; they're the arteries of a vast energy system.

In 2024 the company made an earnings per share (EPS) of $4.26. But EPS doesn't tell the full story for an MLP. The key metric is distributable cash flow—the cash available after maintenance capital expenditures and debt service. For full year 2024, Cheniere Partners paid total cash distributions of $3.25 per common unit, comprised of a base amount equal to $3.10 and a variable amount equal to $0.15.

The distribution coverage ratio—how much cash flow exceeds distributions—provides the margin of safety. Cheniere Energy Partners's dividend payout ratio is 78.6%. This healthy coverage allows for both distribution growth and balance sheet strengthening, a balance that has become increasingly important as the partnership matures.

Why do investors love the MLP structure? Tax efficiency is part of it—distributions are often treated as return of capital, deferring taxes until units are sold. But it's also about alignment. Management's compensation is tied to distribution growth, unitholders want steady income, and the business model generates exactly that kind of cash flow.

Yet the structure has its critics. The complexity of K-1 tax forms, the potential for conflicts between the GP and LP interests, the limitations on institutional ownership—these are real issues. But for the right investor, particularly those seeking yield in a low-rate environment, CQP offers something unique: infrastructure-like stability with energy sector upside.

X. Playbook: Strategic Lessons

The Cheniere story offers a masterclass in strategic pivots, infrastructure development, and financial engineering. Let's distill the key lessons that make this more than just an energy company story.

First-Mover Advantage in Infrastructure: Being first isn't just about timing—it's about creating the market. Cheniere didn't just build the first export terminal; they created the contracting structure, proved the regulatory pathway, and established the operational playbook that everyone else would follow. The first-mover advantage in infrastructure is particularly powerful because of the long lead times and capital intensity that create natural barriers to entry.

The Power of Pivoting: The transformation from import to export wasn't just a business decision—it was an existential bet that required reimagining everything. The lesson isn't that pivots are good (most fail), but that when fundamental assumptions change, clinging to the original plan is fatal. Souki's genius wasn't in predicting the shale revolution; it was in recognizing its implications faster than anyone else and having the courage to act.

Managing Activist Investors: The Icahn saga teaches that founder-CEOs must balance vision with governance. Souki's ousting wasn't just about personality conflicts—it was about differing views on capital allocation, risk management, and strategic direction. The lesson: when you take institutional money, especially from activists, alignment on long-term strategy is essential.

Building Irreplaceable Assets: The Sabine Pass location wasn't chosen randomly. Deep water access, pipeline connectivity, distance from population centers, hurricane-resilient design—every element was strategic. The asset's value isn't just in its physical characteristics but in its position within the broader energy infrastructure network. Once built, it becomes nearly impossible to replicate due to permitting, environmental regulations, and community opposition to new projects.

Capital Intensity as a Moat: The billions required to build LNG infrastructure create a powerful competitive moat. But it's not just about having capital—it's about deploying it efficiently. The learning curve from Train 1 to Train 6 demonstrates how operational excellence compounds over time.

Regulatory Expertise: Cheniere's ability to navigate DOE and FERC approvals, often being the first to establish precedents, became a core competency. In highly regulated industries, understanding not just the rules but how to shape them is invaluable.

The MLP structure itself offers lessons in financial engineering. By separating ownership from operation, Cheniere created distinct investment vehicles for different risk appetites. The parent takes development risk and upside; the MLP offers stable, tax-efficient income. This structure allowed Cheniere to access different pools of capital at different stages of development.

XI. Power & The Future of American Energy

Cheniere Energy Partners sits at the intersection of American energy dominance and global geopolitics. The infrastructure that was nearly worthless in 2009 has become critical to global energy security. When European nations needed to rapidly reduce dependence on Russian gas, American LNG—flowing primarily through Cheniere's terminals—provided the alternative.

The geopolitical implications are profound. LNG exports have become a tool of American foreign policy, strengthening alliances and providing leverage in international negotiations. Every cargo that leaves Sabine Pass carries not just energy but influence. The ability to redirect cargoes from Asia to Europe during crisis demonstrates the flexibility that makes American LNG strategically valuable beyond its BTU content.

Competition is intensifying, but Cheniere's position remains strong. New export projects from Venture Global, Sempra, and others are coming online, but the operational track record, existing infrastructure, and customer relationships create significant advantages. The global LNG market is growing faster than new supply, with Asian demand particularly robust as countries seek cleaner alternatives to coal.

The energy transition question looms large: Is natural gas a bridge fuel or future stranded asset? The pragmatic answer is that gas will likely play a crucial role for decades. LNG enables coal-to-gas switching, the single most impactful near-term emissions reduction strategy. Renewable intermittency requires flexible backup power that gas provides. Industrial processes need high-temperature heat that's difficult to electrify. CQP's 20-year contracts provide visibility through the critical transition period. Expansion opportunities are materializing. On February 29, 2024, Cheniere filed an Application with the FERC for authorization to site, construct and operate the Sabine Pass Stage 5 Expansion Project. The proposed expansion will include an addition of three natural gas liquefaction trains, each with a maximum LNG production capacity of about 300 billion cubic feet per year. This represents up to 20 mtpa of additional capacity—a 67% increase from current levels.

The timing is strategic. European demand remains robust as the continent continues its pivot away from Russian gas. Asian economies, particularly in Southeast Asia, are building import infrastructure rapidly. The energy transition itself creates demand as countries switch from coal to gas as a transitional fuel. CQP stands to benefit directly from this expansion through increased tolling fees and infrastructure utilization.

XII. Bear vs Bull Case

Bull Case:

The bull thesis for CQP rests on its position as irreplaceable infrastructure in a growing market. The 20+ year take-or-pay contracts provide extraordinary visibility—customers like Shell, KOGAS, and GAIL are obligated to pay whether they use the capacity or not. This isn't speculative revenue; it's contractually guaranteed cash flow from creditworthy counterparties.

The growing global LNG demand, especially from Asia, suggests the market will absorb new capacity for decades. China alone could double its LNG imports by 2030. India, Southeast Asia, and even Europe are building import terminals at record pace. The U.S. natural gas cost advantage—Henry Hub consistently trades at a discount to global benchmarks—ensures American LNG remains competitive.

Operational excellence has been proven. The track record of bringing trains online ahead of schedule and under budget demonstrates execution capability. The 2,000+ cargoes shipped without major incident establish reliability that customers value. This operational history reduces execution risk for future expansions.

The expansion optionality at Sabine Pass provides growth within the MLP structure. Unlike many MLPs that must acquire assets to grow, CQP can expand organically on existing land with proven technology and established customer relationships. The Stage 5 expansion could add $1 billion+ in annual EBITDA at minimal risk.

High distribution yield with coverage provides both income and safety. CQP has a dividend yield of 5.84%, attractive in any rate environment but particularly as rates potentially decline. The coverage ratio provides cushion for market volatility while supporting distribution growth.

Bear Case:

The bear thesis centers on long-term energy transition risks. While natural gas is cleaner than coal, it's still a fossil fuel. Aggressive decarbonization policies, particularly in Europe, could reduce demand faster than expected. Renewable energy costs continue to decline, and battery storage is improving. The 20-year contracts provide protection, but what happens in year 21?

MLP structure complexity creates governance challenges. The relationship between the GP and LP creates potential conflicts. Cheniere Energy owns the GP and significant LP units, allowing it to control CQP while extracting value through IDRs (incentive distribution rights) and management fees. Minority unitholders have limited recourse if interests diverge.

Parent company conflicts of interest are structural. Cheniere Energy decides which assets to dropdown to CQP, at what price, and when. The parent handles marketing and could potentially favor its own interests in cargo allocation or commercial decisions. The Icahn episode demonstrated how governance disputes can destroy value quickly.

Global LNG oversupply risk is real. Qatar is massively expanding capacity. Australia continues to develop projects. African LNG is coming online. If supply grows faster than demand, spot prices could collapse, reducing the value of uncontracted capacity and potentially pressuring contract renegotiations.

Commodity price exposure remains despite the fee-based model. While most revenue is fee-based, CQP has some exposure to commodity prices through fuel retention and uncontracted volumes. More importantly, sustained low natural gas prices could impair customer creditworthiness or reduce willingness to honor long-term contracts.

Climate policy and regulatory risks are intensifying. The Biden administration's LNG export permit pause (though later lifted) demonstrated regulatory vulnerability. Carbon taxes, methane regulations, or shifts in energy policy could impact profitability. Environmental opposition to fossil fuel infrastructure is growing globally.

The concentration risk is significant—essentially all cash flow comes from a single facility in hurricane-prone Louisiana. While insurance provides some protection, operational disruption could severely impact distributions.

XIII. Recent News

The LNG market has experienced extraordinary volatility in recent years, largely beneficial to Cheniere. The Ukraine war transformed global energy flows, with European LNG imports surging 60% as the continent scrambled to replace Russian pipeline gas. American LNG, particularly from Sabine Pass, became critical to European energy security.

Current market conditions remain favorable. Asian spot LNG prices have stabilized at levels that ensure healthy margins for U.S. exporters. The arbitrage between Henry Hub and international prices remains wide enough to support continued exports even as new capacity comes online globally.

Regulatory developments have turned more favorable under changing political dynamics. The federal government's recognition of LNG's role in both energy security and emissions reduction (through coal-to-gas switching) has created a more supportive environment for expansion projects.

Recent quarterly results demonstrate operational strength. The company's consistent ability to generate stable EBITDA through various market conditions validates the business model's resilience. Distribution coverage remains healthy, supporting both current yields and future growth.

The Stage 5 expansion project continues to advance through regulatory review. With FERC approval potentially coming in 2026, construction could begin shortly thereafter, with first LNG from the expansion expected around 2030. This timeline aligns well with expected demand growth and existing contract rollovers.

XIV. Links & Resources

For investors seeking deeper understanding, several resources provide valuable context:

- SEC filings and investor presentations from cqpir.cheniere.com offer detailed financial and operational data

- FERC dockets provide insights into expansion projects and regulatory proceedings

- Industry reports from the International Energy Agency and BloombergNEF analyze global LNG market dynamics

- Academic research on MLP structures and energy infrastructure investing provides theoretical framework

- Historical articles from the Houston Chronicle and Wall Street Journal document Cheniere's transformation

- Books like "The Frackers" by Gregory Zuckerman provide context on the shale revolution that enabled Cheniere's pivot

- Podcasts featuring energy experts discuss LNG market evolution and future trends

The Cheniere Energy Partners story is far from over. From near-bankruptcy to essential infrastructure, from import dreams to export reality, from founder-led vision to institutional operation—each transformation has created value while setting up the next challenge. The company that Charif Souki built to import gas, then rebuilt to export it, now stands as a monument to American energy abundance and entrepreneurial adaptation.

For investors, CQP offers something increasingly rare: infrastructure-like stability with meaningful growth potential, tax-efficient income with strategic importance, and exposure to global energy markets with limited commodity risk. The bear cases are real—energy transition, governance complexity, oversupply risks—but the bull case rests on a simple truth: the world needs energy, cleaner energy where possible, and natural gas remains the most practical bridge from where we are to where we're going.

As ships continue to leave Sabine Pass carrying American energy to the world, they carry more than just LNG. They carry the culmination of a remarkable business transformation, the vindication of a controversial pivot, and the ongoing story of how America became an energy superpower. For unitholders of CQP, they also carry the distributions that make this one of the most interesting income investments in the energy sector.

The infrastructure that almost died in 2008 has become irreplaceable. The company that pivoted from import to export has defined an industry. And the MLP that owns it all continues to pay distributions, quarter after quarter, cargo after cargo, in what has become one of the most successful infrastructure investments of the 21st century.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube