Camden Property Trust: The Sunbelt King and the Great Capital Recycle

I. Introduction & Episode Roadmap

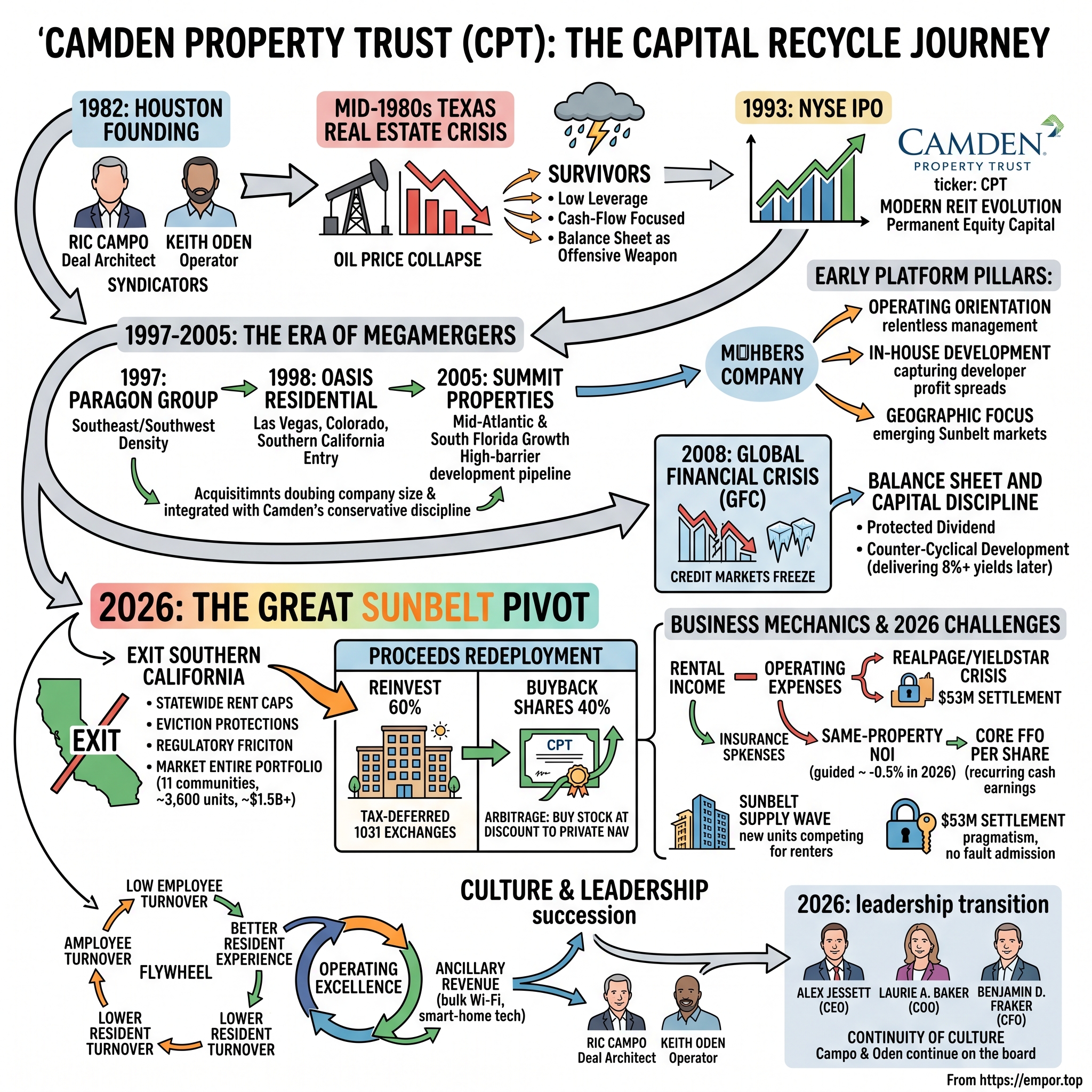

Picture a spreadsheet, not a skyline. It is the winter of 2026, and inside a Houston conference room, the leadership of one of America's largest apartment landlords is staring at two columns of numbers. On the left: eleven apartment communities scattered across Los Angeles, Orange County, San Diego, and the Inland Empire — roughly 3,600 units of stucco and concrete, some of the most stable, supply-starved real estate in the country.1 On the right: the price of the company's own stock, trading at a meaningful discount to what those buildings would fetch in a private sale. The question on the table was not "how do we grow?" It was subtler and more interesting: if the market will sell us our own real estate at a discount, why would we ever buy someone else's at full price?

That question is the spine of this story. The company asking it is Camden Property Trust, ticker CPT on the New York Stock Exchange, an S&P 500 residential real estate investment trust that owns or manages roughly 58,000 to 60,000 apartment homes concentrated in the American Sunbelt — Texas, Florida, Georgia, the Carolinas, Arizona, Colorado, and, for now, a shrinking foothold in California.2 It is not the biggest apartment REIT. It does not own the flashiest towers. But over four decades it has arguably become the most disciplined capital allocator in the multifamily business, and in 2026 it made a bet aggressive enough to make even veteran real estate investors sit up.

Here is the paradox that makes Camden worth two hours of your attention. In 2026 the Sunbelt — Camden's home turf, the region every investor spent the pandemic calling the future — is drowning in new apartment supply. Developers who watched rents spike 20% in Austin and Phoenix in 2021 responded the way developers always do: they built. By 2025 and 2026 that construction wave was hitting the lease-up market all at once, forcing landlords to hand out weeks of free rent just to keep buildings full. Camden's own guidance for full-year 2026 called for same-property net operating income to shrink by roughly half a percent at the midpoint.3 And yet the stock traded at a premium multiple to many peers, and management chose that exact moment to launch one of the boldest capital-reallocation trades in modern REIT history.

The trade: market the entire Southern California portfolio for something north of $1.5 billion, plow roughly 60% of the proceeds into newer Sunbelt communities through tax-deferred 1031 exchanges, and funnel the rest into buying back Camden's own shares at a discount to the private value of its buildings.1 It is a decision that says something profound about how this management team sees the world: that real estate operations are cyclical and messy, but that the arbitrage between public and private valuations is a durable, repeatable source of shareholder value — if you have the balance sheet to act when others can't.

To understand why Camden can make that bet, we have to go back to the beginning — to a Houston that was booming on oil, two young men learning to syndicate apartment deals, and a crash so total it wiped out nearly everyone around them. The lessons of that crash became the company's operating religion. Let's start there.

II. The Founders and the Pre-IPO Texas Real Estate Crisis

In 1982, Houston was the closest thing America had to a gold-rush town. Oil was above $30 a barrel, the city was adding people faster than it could pour foundations, and any reasonably confident person with a calculator and a banker's phone number could put together an apartment deal. Into that frenzy stepped Richard J. "Ric" Campo and D. Keith Oden — two young operators who founded the private partnership that would eventually become Camden Property Trust.4 Campo was the deal architect and capital-markets mind; Oden was the operator, the man who understood what actually happened at the property level once the ink dried. They were, in the language of the era, syndicators: they raised money from investors, bought or built apartments, and managed them for fees and a share of the upside.

Then the floor gave way. When oil prices collapsed in the mid-1980s, they took the Texas economy down with them, and the real estate market didn't just soften — it imploded. Banks failed. The savings-and-loan industry, which had funded much of the construction binge, became one of the great financial catastrophes of the century, ultimately requiring a federal bailout and the creation of the Resolution Trust Corporation to dispose of the wreckage. Half-empty apartment complexes traded for pennies on the dollar. Developers who had leveraged themselves to the eyeballs — which is to say almost all of them — were wiped out.

Campo and Oden survived. That fact, more than any acquisition or IPO, is the origin of the company's identity. They survived because they had done a few unfashionable things during the boom: they kept leverage lower than their peers, they favored cash-flow-producing properties over speculative ground-up bets, and when the crisis hit they did the unglamorous work of negotiating — with lenders, with the FDIC, with the S&L workout specialists picking over the carcass of Texas real estate. Where competitors handed back keys, Campo and Oden restructured, held on, and in some cases bought distressed assets from the very institutions unwinding the mess.

Out of that experience came a philosophy that Camden has repeated, in one form or another, in nearly every downturn since: the balance sheet is not just a defensive shield, it is an offensive weapon. A conservatively financed company doesn't merely avoid dying in a crash — it gets to go shopping while everyone else is forced to sell. That is a very different mental model from the one most real estate entrepreneurs carry, which treats leverage as the accelerant of returns. Campo and Oden had watched leverage work exactly as advertised on the way up and then detonate on the way down, and they never forgot the second half of that lesson.

It is worth pausing on the psychology, because it explains the culture that followed. Most people who live through a wipeout of that scale either leave the industry or become permanently timid. The founders did neither. They internalized the crash not as a reason to fear real estate but as a lesson about how to own it — that the enterprise-ending risk in property was almost never the buildings themselves, which kept collecting rent even in a depression, but the debt stacked on top of them and the maturity that came due when no one would refinance. Get the financing architecture right, the reasoning went, and you could hold quality apartments through almost anything, because Americans need somewhere to live in good times and bad. Housing is among the most defensive forms of real estate precisely because shelter is non-discretionary. That conviction — cyclical revenues, non-cyclical demand for the underlying product, financed conservatively — became the through-line of everything Camden did next.

But surviving a regional crash is not the same as building an enduring enterprise. By the late 1980s and early 1990s, the founders had grasped something structural about their industry: the old model of private syndication funded by regional banks was broken, possibly permanently. The banks that used to write the checks were dead or crippled. Scaling a real estate business the old way — deal by deal, partnership by partnership, with local bank financing — was becoming impossible. Something new was emerging on Wall Street, and it would let real estate operators tap the deepest capital pool in the world. That something was the modern REIT.

III. Going Public: The 1993 IPO & Early REIT Evolution

The real estate investment trust was not a 1990s invention — Congress created the REIT structure in 1960 to let ordinary investors own income-producing property the way they owned stocks. The bargain was simple and elegant: a REIT pays little or no corporate income tax, provided it distributes at least 90% of its taxable income to shareholders as dividends and keeps most of its assets and income in real estate. For decades the structure sat largely dormant. Then, in the early 1990s, as the property crash of the late 1980s left operators starved for capital and private lenders in retreat, a wave of real estate companies raced to the public markets. Pioneers like Kimco in shopping centers and Taubman in malls demonstrated that a well-run property company could raise permanent equity capital from public investors and use it to grow with far less balance-sheet risk than the old bank-financed model.

Camden joined that wave in 1993, listing on the New York Stock Exchange under the ticker CPT and raising roughly $240 million in its initial public offering.5 It went public with a modest Texas-centric portfolio — a fraction of the enterprise it would become — but with a management philosophy already fully formed by the crucible of the 1980s. What made the young public company distinctive was not its size but its mindset. Campo and Oden did not treat apartments the way most of their peers did, as passive, coupon-clipping investments that you bought, financed, and left alone. They treated them as operating businesses — closer to a retail chain than a bond portfolio. Occupancy, resident turnover, renewal rates, ancillary income, on-site staffing: these were levers to be managed relentlessly, not conditions to be accepted.

That operating orientation shaped the second pillar of the early Camden platform: building development and construction in-house rather than buying finished buildings from third-party "merchant" developers. The logic is straightforward once you see it. A merchant builder constructs an apartment community and sells it to a landlord at a price that bakes in the builder's profit. Camden's insight was that if it developed communities itself, it captured that developer profit instead of paying it away. In practical terms, developing a property to a yield — the annual net operating income divided by the total cost to build — of, say, 5.75% to 6.0%, and then having that property valued in the private market at a capitalization rate of 5.0% to 5.5%, creates instant value on day one.[^6] That spread, historically on the order of 100 to 150 basis points, is the difference between a great real estate business and an average one. It only works, however, if you have the land, the entitlement expertise, the construction management, and — crucially — the balance sheet to fund multi-year projects. Camden spent decades assembling exactly those capabilities.

The third pillar was geography. Long before "the Sunbelt" became an investment cliché, Camden was concentrating in low-tax, business-friendly, high-population-growth states: Texas first, then Florida, Arizona, Georgia, and the Carolinas. The bet was demographic and structural. People and jobs were migrating south and west, drawn by cheaper housing, warmer weather, and pro-growth state policies. Apartments in the path of that migration would enjoy steady demand. The strategy carried an obvious embedded weakness, one that would come back to haunt the entire sector in the 2020s — Sunbelt land is cheap and easy to build on, which means supply can flood in exactly when demand is strong. But in the 1990s that was tomorrow's problem. Today's opportunity was scale, and to get it, Camden was about to go on the acquisition spree that would transform it from a Texas operator into a national platform.

IV. The Era of Megamergers: Oasis, Paragon, and Summit

If the 1980s taught Campo and Oden how to survive and the IPO taught them how to fund growth, the decade that followed taught them how to consolidate. Between 1997 and 2005, Camden executed a sequence of mergers that repeatedly doubled its size and stretched its map from the Nevada desert to the Washington, D.C. suburbs. This was real estate as chess, not checkers — each move opened new markets, absorbed a competitor's platform, and tested whether Camden's low-leverage discipline could survive contact with acquired companies that did not share it.

The first big move came in 1997 with the acquisition of the Paragon Group, a transaction that, including assumed debt, approached the billion-dollar mark and added roughly 17,000 apartment units across the Southeast and Southwest.6 Paragon gave Camden something it could not build quickly on its own: instant density in markets where scale translates directly into operating leverage. When you own thousands of units in a single metro, you can staff regional maintenance teams, negotiate bulk pricing on everything from appliances to insurance, and spread marketing costs across a large base. Paragon pushed Camden across the threshold from regional player to serious multifamily operator.

A year later, in 1998, came Oasis Residential — a deal that added Camden roughly $542 million in stock plus the assumption of around $430 million in debt, together valuing the transaction near the billion-dollar level.7 Strategically, Oasis was a leap into new geography: Las Vegas, Colorado, and, for the first time, Southern California. That last one matters enormously to our 2026 story, because the Southern California portfolio Camden spent 2026 trying to exit traces its roots, in part, to this very acquisition. Oasis was also a cultural and financial integration challenge. It carried a heavier debt load than Camden was comfortable with, and the founders moved quickly to apply their own conservative leverage discipline — refinancing, deleveraging, and folding the acquired portfolio into Camden's operating systems. The pattern is instructive: Camden repeatedly bought companies that were run more aggressively than itself and then imposed its own balance-sheet religion on them. The acquisitions expanded the footprint; the integration expanded the discipline.

The capstone of the era was the 2005 acquisition of Summit Properties, a transaction valued at roughly $1.9 billion including assumed debt — one of the largest multifamily REIT mergers of the decade.8 Summit was the prize the others had set up. It extended Camden into the higher-barrier Mid-Atlantic, particularly the Washington, D.C. metro, and deepened its presence in Southeast Florida markets like Miami, Tampa, and Orlando. Those are markets where land is scarcer, entitlement is harder, and new supply is naturally constrained — the structural opposite of cheap-to-build Texas and Arizona.

But timing invites a hard question: did Camden overpay? The Summit deal closed near the peak of the 2000s housing boom, at a capitalization rate below 5% — a rich price by any standard, and one that would look richer still when the entire real estate market collapsed three years later. In candid moments over the following decade, Campo acknowledged that the headline price was full. Yet the more nuanced verdict is that the true value in Summit was not the stabilized buildings but the development pipeline — high-barrier land parcels in supply-constrained submarkets that Camden could develop, over the following ten-plus years, at those attractive yield-on-cost spreads. In other words, Camden paid a premium price for stabilized assets and got a portfolio of future development profits somewhat for free. Whether that made it a good deal depends on how you weight the ten years of downstream development returns against the sting of buying at a cyclical top. It is a genuinely debatable call, and an honest history has to hold both truths at once.

It also foreshadowed the central drama of Camden's next chapter. Because within three years of the Summit deal closing at a sub-5% cap rate, the global financial system seized up — and every real estate company in America discovered exactly how much its balance sheet mattered.

V. Surviving the Global Financial Crisis (GFC): Balance Sheet and Capital Discipline

In the fall of 2008, the machinery that funds real estate simply stopped. Credit markets froze. The commercial paper market — the short-term IOUs that many companies rolled over constantly to fund operations — became untouchable overnight. Property values, which for years had marched upward on a river of cheap debt, went into free fall as buyers vanished and lenders refused to lend. For a leveraged, capital-intensive industry like real estate, it was the equivalent of the oxygen being sucked out of the room.

For apartment REITs, the crisis exposed a brutal sorting mechanism. Companies that had financed themselves with too much short-term debt, or leaned on the commercial paper market, suddenly faced maturities they could not refinance. Their choices were grim: sell assets into a market with no buyers, or issue new equity at rock-bottom stock prices — diluting existing shareholders at the worst possible moment, effectively locking in the crisis-era loss permanently. Many did exactly that. Raising equity at the bottom is the cardinal sin of cyclical investing, and in 2008 and 2009 a number of otherwise respectable REITs had no alternative.

Camden had spent a quarter-century preparing for precisely this. Its balance sheet carried strong investment-grade credit ratings, its debt was laddered so that maturities were spread out rather than bunched into a single cliff, and its leverage was low enough that lenders never doubted the company's solvency. That financial architecture bought Camden something priceless in a panic: the freedom to play defense on its own terms. Management slashed discretionary capital spending, put the development pipeline on ice rather than push half-built projects into a dead market, and hoarded cash. Critically, it protected the dividend at a time when peers were cutting payouts by half or more — a signal to the market that Camden's cash flows were durable and its finances sound. There is an important nuance here worth flagging for the record: like many REITs, Camden did use its equity as a tool during the crisis period, and no apartment company escaped the era unscathed. But it entered the storm from a position of strength rather than desperation, and that distinction shaped everything that followed.

The defensive posture set up the offensive payoff. When the economy began clawing its way back in 2011 and 2012, construction costs were at multi-year lows — contractors were desperate for work, land was cheap, and materials were affordable. Camden, having preserved its firepower, restarted its development engine into that environment and delivered new communities at yields on cost that in some cases exceeded 8% — extraordinary spreads over the cap rates at which those same completed buildings could be sold.9 Developing counter-cyclically, when everyone else was too scared or too broke to build, produced some of the most profitable projects in the company's history. It was the balance-sheet-as-offense philosophy vindicated in the most concrete way possible.

That episode is the Rosetta Stone for understanding Camden's 2026 behavior. Once you have watched a company get rewarded, in hard dollars, for being liquid and disciplined when others were forced sellers, you understand why its instinct — when its own stock trades below the value of its buildings — is to treat that gap not as a problem to endure but as an opportunity to exploit. Which brings us to the boldest expression yet of that instinct: the decision to walk away from California.

VI. The Great Sunbelt Pivot: The 2026 Southern California Exit

For years, owning apartments in Southern California was supposed to be the safe part of the portfolio. Coastal California is the definition of a supply-constrained market — land is scarce, entitlement is a multi-year ordeal, and NIMBY politics strangle new construction. That scarcity underpins durable rents and steady occupancy. On paper, it is exactly the kind of high-barrier real estate that ought to anchor a landlord's holdings. So why did Camden decide, in 2026, to sell all of it?

The answer, in management's telling, is that the paper stability comes at a punishing operational cost. California's regulatory regime — statewide rent caps, repeated extensions of eviction protections, aggressive tenant-rights enforcement, and layers of local compliance — consumes a share of administrative, legal, and management attention wildly out of proportion to the region's contribution to the bottom line. Southern California represented only around a tenth of Camden's operating income, yet it absorbed a disproportionate slice of the headaches. On the company's earnings calls, Executive Vice Chairman Keith Oden captured the sentiment memorably, framing life as a California landlord as a running question of what the next regulatory "bullet" would be.1 When the cash-flow reward is modest and the operational friction is high and rising, the elegant coastal thesis starts to look less like a moat and more like a tax.

So in early 2026 Camden did something few landlords have the discipline to do: it put the entire Southern California portfolio — eleven communities of roughly 3,600 units across the Los Angeles–Orange County and San Diego–Inland Empire markets — up for sale, hiring JLL to market a package valued at something north of $1.5 billion, with expectations running toward the $1.5 billion to $2.0 billion range.110 By mid-2026 the disposition was well advanced, with the bulk of the sale expected to complete around the middle of the year.11 This was not a distressed sale or a trim around the edges. It was a clean strategic exit from an entire region, and a statement that operational simplicity and capital flexibility now outweighed the theoretical safety of supply-constrained cash flows.

The genuinely interesting part is what Camden planned to do with the money, because it reveals the company's whole worldview. Management earmarked roughly 60% of the proceeds — on the order of $1 billion — for tax-deferred 1031 exchanges into newer, higher-quality multifamily communities in landlord-friendly Sunbelt markets.311 A 1031 exchange, named for the section of the U.S. tax code that authorizes it, lets an owner sell one investment property and reinvest the proceeds into a "like-kind" property while deferring the capital-gains tax that would otherwise be due. For a company sitting on decades of appreciation in its California assets, that deferral is worth real money; selling outright and paying the tax would leave far less to redeploy. The exchange mechanism lets Camden rotate out of California and into the Sunbelt without handing a large check to the IRS in the process.

The remaining roughly 40% — modeled at something like $650 million — was aimed not at buying anyone else's real estate but at buying back Camden's own shares.312 Here is the logic that ties the whole trade together. If Camden's stock trades at a discount to the net asset value of its portfolio — that is, if the public market values the company below what its buildings would fetch in a private sale — then every dollar spent repurchasing shares buys a dollar-plus of real estate for less than a dollar. Compare that to acquiring third-party apartments in the private market at cap rates of 5% or lower, and the buyback looks like the higher-return use of capital by a wide margin. In effect, Camden concluded that the cheapest, highest-quality Sunbelt real estate it could buy in 2026 was itself.

The way management discussed the move on its earnings calls is itself revealing, and worth listening to for tone as much as content. Rather than dressing the exit up as a bold growth initiative, Camden's leadership framed it in the flat, arithmetic language it applies to everything — a question of where the marginal dollar earns the best risk-adjusted return, with California's regulatory drag and the discount on its own shares as the two decisive inputs. Analysts pressed on the obvious tension: why exit supply-constrained markets that were, at that very moment, delivering better rent growth than the Sunbelt? Management's answer leaned on the long view — that the regulatory trajectory in California was a one-way ratchet and that the valuation gap on Camden's stock was a here-and-now opportunity that might not persist. Whether you find that persuasive or not, it was consistent with how this team has always talked: unsentimental about assets, focused on relative value, and willing to shrink the company when shrinking is the higher-return path.

That is a genuinely aggressive and self-aware capital-allocation move, and it deserves to be stress-tested rather than applauded. The skeptical case runs like this: Camden is selling structurally supply-constrained coastal cash flows and reinvesting the bulk of the proceeds back into the very Sunbelt markets that are, right now, the most oversupplied in the country. It is trading a defensive asset for operational convenience and a valuation bet. If the Sunbelt supply glut proves deeper or longer-lasting than expected, Camden will have swapped a boring-but-resilient portfolio for a higher-beta one at precisely the wrong moment. The bullish rebuttal is that the buyback locks in a known, quantifiable arbitrage today, while the coastal "safety" was being eroded by a regulatory environment that only ever seems to tighten. Both cases are legitimate. What is not in dispute is that this is the most consequential portfolio decision Camden has made since the Summit merger — and to judge whether it will pay off, an investor first needs to understand exactly how a company like this actually makes money.

VII. The Business Model: Mechanics of a Multifamily REIT

Strip away the real estate mystique and an apartment REIT is a surprisingly legible business: it owns a large collection of rental buildings, collects rent, pays the costs of running those buildings, and passes most of what's left to shareholders. The art is in the details, and a handful of specialized metrics govern how investors judge whether the machine is working. Let's demystify them, because the rest of this story is unintelligible without them.

Start with same-property performance, often abbreviated "same-store." Because a REIT is constantly buying, selling, and developing, its total revenue can rise simply because it owns more buildings this year than last — which tells you nothing about whether the underlying business is healthy. To isolate genuine operating performance, analysts look at the "same-property" pool: the set of communities Camden owned and operated in both the current and prior periods. Same-property revenue growth tells you whether rents and occupancy are rising on a stable base of buildings. Same-property expense growth tells you whether the costs of running those buildings — property taxes, insurance, payroll, utilities, repairs — are under control. The difference between the two, flowing down to same-property net operating income (NOI), is the single cleanest gauge of operating health in the business. NOI is simply property-level rental income minus property-level operating expenses, before the costs of financing and corporate overhead. When Camden guided to full-year 2026 same-property NOI of roughly negative 0.5% at the midpoint — the product of revenue growth around 0.75% being outrun by expense growth near 3.0% — it was telling investors, plainly, that costs were rising faster than rents and that the operating base would tread water at best this year.3

That expense side deserves a beat of its own, because it is where the 2026 pain concentrates. Camden's rents were roughly flat, but its costs were not. Property insurance — especially in coastal Florida and hurricane-and-hail-exposed Texas — has climbed steeply as insurers repriced climate risk, and property taxes levied by fast-growing municipalities have marched upward regardless of what rents do. A landlord can be a superb operator and still watch NOI stall when insurers and tax assessors take a bigger bite every year. This is the unglamorous reality behind the flat guidance: the revenue environment is soft and the cost environment is hostile, a two-front squeeze.

Now the metric that trips up newcomers: earnings. If you look at a REIT's net income under standard accounting rules, you will be badly misled, because accounting requires the company to depreciate its buildings — to record a large annual expense reflecting the theoretical wearing-out of the physical structures. But well-maintained apartment buildings in growing markets do not actually lose value over time; they often appreciate. So net income, dragged down by a huge non-cash depreciation charge, wildly understates the real economics. The industry's answer is Funds From Operations, or FFO, which essentially adds that depreciation back and strips out one-time gains and losses on property sales, producing a truer picture of recurring cash earnings. Camden, like most peers, further refines this into Core FFO, which removes additional non-recurring items — legal settlements, debt-extinguishment costs, and the like — to show the clean, run-rate earning power of the portfolio. When Camden reports Core FFO per share, that is the number Wall Street actually cares about.

The 2025–2026 snapshot, in plain terms: for full-year 2025, Camden guided to Core FFO of about $6.85 per share at the midpoint, with same-property NOI roughly flat as modest revenue gains were offset by those rising insurance and tax costs.13 Coming into 2026, the company set a full-year Core FFO midpoint of about $6.75 per share — a modest step down that reflects the soft operating environment and the dilution from selling California assets faster than the proceeds could be redeployed.3 In the first quarter of 2026, Camden delivered Core FFO of $1.70 per share, about four cents ahead of its own guidance, helped by lower-than-feared bad debt and delinquency and by construction fee income.14 The beat matters less for its size than for what it signals: even in a flat-to-down year, actual operations were running slightly ahead of the cautious script — a small but real data point on execution and on the conservatism baked into guidance.

Finally, the valuation loop that ties directly back to the California trade. Private-market buyers value apartment buildings using capitalization rates — the ratio of a property's annual NOI to its purchase price. In 2025 and 2026, prime Sunbelt apartments were changing hands at cap rates roughly in the 5.0% to 5.5% range.[^6] Apply those cap rates to Camden's NOI and you get an estimate of the private-market value of its entire portfolio — its net asset value, or NAV, once you subtract debt. When Camden's stock price implies a value below that NAV, the company is effectively on sale relative to its own bricks, and buybacks become the obvious move. When the stock trades at a premium to NAV, buying more real estate — or developing it — looks smarter. This constant comparison between public stock price and private property value is the central discipline of REIT capital allocation, and Camden has made it the organizing principle of its 2026 strategy. But whether that strategy pays off depends heavily on a force larger than any single company: the tidal wave of new apartments crashing into the Sunbelt.

VIII. The Sunbelt Supply Wave & The Competitive Matrix

Every boom writes the script for its own hangover, and the Sunbelt apartment market of 2026 is living out a hangover written in 2021. Rewind to the depths and immediate aftermath of the pandemic. As remote work untethered millions of Americans from expensive coastal cities, they poured into Austin, Phoenix, Atlanta, Nashville, Charlotte, and Dallas — chasing lower costs, warmer weather, and no state income tax. Demand for apartments in those metros exploded, and rents followed, with double-digit annual increases in the hottest markets. For landlords, 2021 and early 2022 were a once-in-a-generation party.

Developers, watching those numbers, did what economics guarantees they will do when returns spike and land is cheap: they built, and built, and built. The problem is that apartment buildings take two to three years to design, entitle, finance, and construct. So the supply unleashed by the euphoria of 2021 did not actually hit the market until 2024, 2025, and 2026 — arriving in a giant, delayed wave precisely as demand normalized. The result across much of the Sunbelt has been a record surge of new units competing for renters at the same time. To fill all those brand-new buildings, developers resort to concessions — offering four, six, even eight weeks of free rent to lure tenants — and those giveaways ripple through the whole market, pressuring even established landlords like Camden to hold rents flat or discount to keep occupancy from slipping.

The numbers make the squeeze concrete. Camden's full-year 2026 guidance put same-property revenue growth at a meager 0.75% against expense growth near 3.0%, yielding that roughly negative 0.5% NOI figure.3 The single starkest example in the portfolio is Austin — the poster child of both the boom and the bust — where Camden expected same-property revenues to actually fall by 1.0% to 2.0% in 2026 as an overwhelming supply pipeline collided with slowing in-migration.3 Austin is a warning and a bellwether: the market that led the Sunbelt up is now leading it down, and how quickly Austin's oversupply clears will tell investors a great deal about when the broader region turns. The one genuine comfort in the data is occupancy, which Camden held around 95% — a sign that it is defending occupancy with rent discipline rather than chasing headline rents into a vacancy spiral.14 A landlord that keeps buildings full at flat rents is in far better shape than one posting rent growth on paper while units sit empty.

It is worth pausing here to separate a popular myth from the operating reality, because the Sunbelt narrative has whipsawed investors. The myth, circa 2021, was that Sunbelt apartments were a one-way bet — that structural migration guaranteed permanent rent growth and that the coastal markets were in secular decline. The reality of 2026 is that the Sunbelt is not a growth stock that only goes up; it is a classic cyclical, where the very demand strength that draws residents also draws bulldozers, and where the low barriers to construction convert booms into gluts with a two-to-three-year lag. The corollary myth — that coastal markets were finished — has also been falsified: the same regulatory and geographic friction that makes coastal cities miserable to operate in is exactly what starves them of new supply and hands their landlords pricing power when the Sunbelt is oversupplied. Neither region is a permanent winner. Both are cyclical, and they tend to be out of phase with each other — which is precisely the insight that makes Camden's California-for-Sunbelt swap either shrewd or mistimed, depending on where in the cycle you think each region sits.

To size Camden properly, it helps to line it up against its rivals, because the competitive map explains a lot about strategy. The closest comparison is Mid-America Apartment Communities, MAA, the other great pure-play Sunbelt apartment REIT. MAA is larger, with something approaching 100,000 units, and has historically carried slightly lower leverage and leaned less heavily on internal development than Camden, favoring acquisitions and, more recently, a measured development program. The two are natural mirrors: same region, same supply headwinds, subtly different playbooks. MAA's greater scale gives it purchasing muscle; Camden's development engine gives it the potential to create value at yields above market cap rates when the cycle cooperates.

Then there are the coastal high-barrier REITs — Equity Residential, EQR, and AvalonBay Communities, AVB — concentrated in New York, Boston, Seattle, the San Francisco Bay Area, and Southern California. In 2025 and 2026 these companies enjoyed a striking role reversal. Their coastal markets, starved of new construction by the very land scarcity and regulatory friction that make them a headache to operate, posted stronger rent growth than the oversupplied Sunbelt. The cycle had flipped: the "boring" coastal markets were suddenly the growth story, and the "high-growth" Sunbelt was the laggard. This divergence is the crucial context for Camden's California exit. Management chose to sell coastal exposure — the very exposure that was outperforming in the near term — precisely because it judged the regulatory cost too high and the valuation arbitrage in its own shares too attractive to pass up. Reasonable investors can disagree about whether that was contrarian genius or a mistimed swap of near-term growth for operational ease. Either way, it commits Camden more deeply to a Sunbelt whose supply wave must eventually crest and recede for the thesis to work. And while Camden wrestles with supply, it has also been dragged into a very different kind of fight — one over the software that helped set apartment rents in the first place.

IX. The RealPage/YieldStar Antitrust Crisis & The $53M Settlement

Somewhere in the last decade, the business of pricing an apartment quietly stopped being a human judgment call and became an algorithm's output. For generations, a property manager set rents by feel — checking what the complex down the street charged, eyeballing occupancy, and adjusting. Then came revenue management software, most prominently RealPage's YieldStar platform, which promised to do for apartments what airlines and hotels had long done for seats and rooms: use data and algorithms to optimize the price of every unit, every day, squeezing out the maximum revenue the market would bear. Landlords across the industry, Camden among them, adopted these tools, and for years they were regarded as simply good operational hygiene — the modern, data-driven way to run a portfolio.

Then the framing flipped from efficiency to conspiracy. Tenants, private plaintiffs, and ultimately the U.S. Department of Justice alleged that this software was not merely helping each landlord optimize independently — it was functioning as the hub of a price-fixing cartel. The theory: by feeding their nonpublic, real-time data on occupancy and rents into a common algorithm, competing landlords were effectively coordinating their pricing through a shared intermediary rather than competing on the open market. The DOJ's amended complaint, which named Camden among other large operators, alleged that this arrangement allowed landlords to push rents higher than genuine competition would permit — and, more provocatively, that the software's logic could counsel holding units vacant rather than cutting rents, on the theory that preserving pricing power across the portfolio beat filling every apartment.[^16] Whether that describes illegal collusion or merely widespread use of a popular vendor's product became one of the most closely watched antitrust questions in the country.

For Camden, the litigation resolved — at least the private class-action piece — in the spring of 2026. In early April, the company entered a binding term sheet to settle the private multi-district class-action litigation for $53 million, structured as two equal installments of $26.5 million and subject to court approval.15 Management was emphatic that the settlement carried no admission of fault or liability, framing it as a pragmatic decision to avoid the enormous cost and distraction of protracted antitrust litigation rather than a concession that Camden had done anything wrong.15 Financially, Camden absorbed the settlement as a non-core charge — part of roughly $58 million in non-core FFO items in the first quarter — which is precisely why it lands in reported net income and FFO but is stripped out of the Core FFO number that Wall Street tracks.14 The company signaled it expected no material impact on its dividend, capital plans, or run-rate metrics.

The more durable question is operational, not financial. The settlement reportedly includes prospective commitments governing the disclosure and use of nonpublic data and revenue-management software, even as Camden maintains these require no material change to how it actually operates.15 If algorithmic pricing built on a rich pool of competitors' nonpublic data was genuinely the "secret sauce" behind a decade of apartment revenue optimization, then constraining that data-sharing could, at the margin, erode the pricing precision the whole industry came to rely on. The honest answer is that nobody yet knows how much of the software's value came from shared nonpublic data versus a landlord's own data and general market signals. If most of the edge came from a company's own information and public comparables, the settlement changes little. If a meaningful slice came from the pooling of competitors' secrets, then the entire sector — Camden included — may be quietly less efficient at pricing than it was, right at the moment the Sunbelt supply wave demands every basis point of pricing skill. It is a genuine, if unquantifiable, overhang worth watching. And it points to a deeper question about where Camden's real advantages actually come from — because if it isn't the software, what is it?

X. The Camden Culture: Process Power & Operating Excellence

Here is a fact that sounds like corporate fluff until you follow the money: Camden has spent years near the top of Fortune's "100 Best Companies to Work For" list, frequently ranking among the top 30 employers in America across all industries — not just real estate.16 A hard-nosed investor's first instinct is to dismiss this as feel-good marketing. That instinct is wrong, and understanding why is the key to understanding Camden's most defensible edge. In a business where the physical product — an apartment — is almost perfectly commoditized, and where a rival can build an identical building on the next block, the durable differences between operators come down to execution. And execution, in the apartment business, is overwhelmingly a function of the people on site.

Trace the operational flywheel and the economics of culture become concrete. Camden pays and treats its property managers, leasing agents, and maintenance technicians well, which lowers employee turnover. Lower employee turnover means the person answering the phone, showing the unit, and fixing the air conditioner is experienced and invested rather than a revolving-door hire. That continuity produces a better resident experience, which lowers resident turnover — and resident turnover is astonishingly expensive. Every time a tenant moves out, the landlord eats the cost of make-ready repairs, cleaning, repainting, marketing the vacant unit, and the lost rent during the gap, a bundle that can run anywhere from roughly $2,000 to $4,000 per apartment. Multiply that across tens of thousands of units and a few percentage points of improved retention translates into real, recurring money. Lower turnover also means fewer vacant days, higher renewal rates, and — because satisfied long-term residents pay reliably — lower bad debt. None of this shows up as a single line item you can point to, which is exactly why it is a durable advantage: it is diffuse, cultural, and very hard for a competitor to replicate by writing a check.

Layer on technology and the ancillary-income story gets sharper. Camden was early and aggressive in rolling out bulk internet, managed Wi-Fi, and smart-home features like connected locks and thermostats across its communities. The financial logic is elegant. By negotiating bulk internet contracts at scale and reselling connectivity to residents, and by charging a modest recurring monthly technology fee, Camden generates a stream of high-margin ancillary revenue that flows almost directly to NOI. Because the underlying infrastructure is installed once and serves the building for years, the incremental margin on that fee income is very high. Smart-home technology also cuts operating costs — remote access reduces the need for staff to physically handle keys and turnovers, and connected systems can flag maintenance issues before they become expensive emergencies. It is a rare initiative that raises revenue and lowers cost at the same time.

The appropriate analytical caution is that "great culture" is easy to assert and hard to verify from the outside, and its benefits, while real, are incremental rather than transformational — a point or two of retention here, a slice of ancillary margin there. Culture will not rescue Camden from a market where a competitor is handing out two months of free rent across the street; supply and demand still set the ceiling. What culture and operational excellence do is let Camden earn a bit more than an average operator would from the same buildings in the same market, cycle after cycle. Compounded over decades, that consistency is meaningful — and it happens to be one of the few advantages in this commoditized business that a rival cannot simply buy or build. The question hanging over all of it in 2026 was whether that culture, forged and personified over 33 years by two founders, could survive their departure from day-to-day control.

XI. Transitioning the Crown: The 2026 Leadership Succession

For 33 years, from the 1993 IPO onward, the answer to "who runs Camden?" was simple: Ric Campo and Keith Oden. They were the founders, the survivors of the Texas crash, the architects of every merger and every counter-cyclical bet. A company shaped that thoroughly by two people faces an existential question that has sunk many founder-led enterprises: what happens when the founders step back? In 2026, Camden gave its answer — and it did so with the same deliberate, low-drama discipline it applies to its balance sheet.

On March 27, 2026, Camden announced a leadership transition, effective within days, that had clearly been planned years in advance rather than improvised.17 It was not a rupture; it was a relay handoff executed at full stride, and every runner receiving a baton was a long-tenured insider rather than an outside hire. That distinction is itself a statement of philosophy — Camden chose continuity of culture over the jolt of fresh outside blood, betting that the operating system the founders built was worth preserving intact.

The new chief executive is Alexander J. "Alex" Jessett, who joined Camden back in 1999 and rose through the finance organization to become President and Chief Financial Officer before taking the top job.18 Jessett is, in temperament and background, the embodiment of the Camden way: a capital-markets and balance-sheet mind, respected on Wall Street for guidance transparency and disciplined, clear-eyed capital-allocation modeling. That a CFO — rather than a dealmaker or a development chief — inherited the CEO chair tells you what the board believes matters most for Camden's next chapter: not empire-building, but the patient, unglamorous arithmetic of allocating capital well. He also joined the board of trust managers, formalizing his authority.

Around him, the board promoted a leadership team of equally deep tenure. Laurie A. Baker moved up to President and Chief Operating Officer, elevated from running operations, where she had been the driving force behind the company's digital transformation and its onsite efficiency programs — meaning the person now responsible for day-to-day operations is the same person who built the technology-and-culture flywheel described earlier. Benjamin D. Fraker was promoted to Executive Vice President, Chief Financial Officer and Treasurer, stepping into Jessett's former financial role and preserving continuity in how Camden models and communicates its numbers. The founders did not vanish: Campo became Executive Chairman of the board, and Oden continued as Executive Vice Chairman, keeping both men engaged in strategy and capital allocation while ceding operational command.17 The design keeps decades of institutional memory in the boardroom while handing the operating controls to the executives who had effectively been running the business for years.

How much should investors trust this team? The most reliable evidence is behavior over time, and here the record is substantive. Camden's management has a long history of heavy insider alignment — the leadership group and board have historically held a meaningful equity stake, so their wealth rises and falls with shareholders'. The company has managed its dividend conservatively, protecting it through the GFC rather than overextending in good times and cutting in bad. And across cycles it has built a reputation for under-promising and over-delivering on guidance — the Q1 2026 beat against its own cautious forecast being a small recent example.14 That said, credibility must be tested against the current bet, not just the past. The aggressive 2026 capital recycle — selling stabilized coastal assets to fund buybacks — is a departure in magnitude from the steady-as-she-goes posture, and a skeptic is entitled to ask whether a newly minted CEO is front-loading a bold, legacy-defining move at exactly the wrong point in the Sunbelt cycle. The transition looks like a model of REIT succession planning. Whether it also marks a subtle shift toward more aggressive capital allocation is a question only the next few years will answer. To weigh it properly, we need to place Camden inside a rigorous strategic framework.

XII. Strategic Analysis: Helmer's 7 Powers & Porter's 5 Forces

Strip a company down to its structural sources of advantage and you learn far more than any single quarter's numbers can tell you. Two frameworks are especially useful here: Hamilton Helmer's "7 Powers," which catalogs the durable advantages that let a business earn excess returns, and Michael Porter's "5 Forces," which maps the competitive pressures that erode them. Run Camden through both, and a clear, honest picture emerges — one with real strengths and one glaring structural weakness.

Start with Helmer. The most credible power Camden possesses is Process Power — an advantage embedded in the company's organization and know-how that competitors cannot easily copy even if they know exactly what Camden does. Two engines drive it. The first is the internal development-and-construction platform, decades in the making, that lets Camden create real estate at a yield premium over what it would pay to buy finished buildings. The second is the operating culture explored earlier — the "best places to work" flywheel that quietly lowers employee turnover, resident turnover, and bad debt. Neither can be replicated by writing a check; both took decades to build and depend on accumulated institutional habit. That is the textbook signature of Process Power.

Camden also enjoys genuine Scale Economies. As one of the largest apartment owners in its markets, it buys appliances, smart-home hardware, insurance, and advertising at volumes a regional operator or a merchant builder simply cannot match, spreading fixed costs across tens of thousands of units. In a business of thin operating margins, a few points of cost advantage on insurance or procurement compounds meaningfully. The one Helmer power worth addressing mostly to dismiss it is Counter-Positioning — the idea that an incumbent can't copy a challenger's model without damaging its own. Real estate is far too fragmented and undifferentiated for classic counter-positioning to exist. The closest Camden comes is a kind of capital-allocation counter-positioning: its willingness to shrink itself by buying back stock rather than reflexively growing the asset base, a discipline that ego-driven, growth-at-all-costs operators find culturally difficult to imitate. It is a real behavioral edge, but a soft one.

Now Porter, and the sobering part. The Threat of New Entrants in Camden's core Sunbelt markets is high — dangerously so. Cheap, abundant land and permissive zoning are exactly what make Texas, Georgia, Arizona, and the Carolinas easy to build in, which is the root cause of the very supply wave hammering NOI in 2026. This is Camden's missing moat: unlike the coastal markets it is exiting, its chosen territory has almost no barrier to new construction. It is the central structural irony of the whole enterprise — Camden's home region is attractive precisely because it is easy to build in, and dangerous for precisely the same reason. The Bargaining Power of Buyers — the renters — has risen sharply in 2025 and 2026, as the flood of new units lets tenants demand concessions and shop landlords against one another. The Bargaining Power of Suppliers is largely managed through scale, with two stubborn exceptions that scale cannot fully tame: property insurers repricing climate risk in Florida and Texas, and municipal taxing authorities, both of which extract more every year regardless of Camden's operating skill. And the Intensity of Rivalry is fierce at the hyper-local level, where the competition is quite literally the identical building on the next corner offering an extra month free.

The synthesis is clarifying. Camden has real, durable advantages in how it operates and allocates capital — process, scale, and discipline — but essentially no structural moat around its markets. It cannot stop competitors from building next door. That combination defines both the opportunity and the risk: Camden can reliably out-operate and out-allocate peers over a full cycle, but it cannot escape the brutal supply-and-demand physics of easy-to-build geographies. Which is exactly the tension that the bull and bear cases have to resolve.

XIII. Bull vs. Bear Case & KPIs to Watch

So, does Camden win from here — and what would prove the case wrong? Let's lay out both sides with the intellectual honesty the question deserves, because this is a stock where thoughtful investors genuinely disagree.

The bull case — why Camden wins. The heart of it is the 2026 capital recycle. If management executes the Southern California exit near the top of its expected range and redeploys the proceeds as planned, it will have converted a low-growth, high-friction coastal portfolio into a combination of newer Sunbelt communities and a large slug of repurchased stock bought below the private value of the underlying real estate. Retiring a meaningful chunk of the share count at a discount to NAV is mathematically accretive to Core FFO per share — the fewer shares outstanding, the more each remaining share owns. Pair that financial engineering with the operating thesis: the Sunbelt supply wave is, by its nature, temporary. New construction starts have already collapsed under the weight of high interest rates and falling developer returns, which means the 2024–2026 deluge will not be followed by another. If demand holds up on the strength of long-run demographic tailwinds — continued migration to low-tax, warm, affordable states — then the existing oversupply gets absorbed, concessions burn off, and same-property NOI pivots back to healthy growth, plausibly by late 2027. A company that spent the down-cycle shrinking its share count cheaply would then enjoy amplified per-share growth on the way back up. That is the bull's prize: buy the trough, shrink the count, harvest the recovery.

The bear case — what breaks it. Start with the mirror image of the bull's central move. Reinvesting roughly a billion dollars of California proceeds back into the Sunbelt deepens Camden's exposure to the most oversupplied region in the country, just as it sheds the supply-constrained coastal assets that were actually outperforming in 2025 and 2026. If the supply glut proves stickier than hoped — if migration slows, or if the "temporary" wave lingers into 2028 and beyond — Camden will have concentrated its bet at the wrong time. Second, the macro overhang: if interest rates stay higher for longer, cap rates stay elevated, REIT valuations stay depressed, and the NAV discount that makes buybacks so attractive today could persist or widen, meaning the buyback thesis takes years to be vindicated by the market even if the underlying math is sound. Third, the subtle operational risk from the RealPage settlement — if constraints on data-sharing genuinely dulled the industry's algorithmic pricing edge, Camden loses a sliver of efficiency precisely when soft markets demand maximum pricing skill. And fourth, the governance question a skeptical activist would press: is a newly installed CEO making an aggressive, legacy-defining capital bet at a cyclical low, and is the board — still anchored by the founders — the right check on that ambition, or too deferential to it?

The activist stress test cuts both ways, and it is worth stating plainly. A long-oriented activist might actually cheer Camden's buyback-over-empire discipline as exactly the shareholder-friendly behavior the REIT sector too often lacks. A short-oriented skeptic would counter that selling your best structural assets to buy your own stock is a confession that management can't find anything better to do with capital — and that the whole trade rests on the assumption that today's NAV estimate is right, when NAV itself is just a function of cap rates that could move against you. Both critiques are legitimate. The truth is that Camden's strategy is a bet — a well-reasoned, disciplined, internally consistent bet, but a bet nonetheless, on the Sunbelt cycle turning and on the durability of the public-private valuation gap.

Which is why an investor doesn't need to resolve the debate in the abstract; they can watch three numbers that will reveal, quarter by quarter, which case is winning. First, same-property NOI growth — the cleanest single measure of operating health. The critical thing to watch is the inflection: the pivot from the negative territory of 2026 back toward positive, which would signal the supply wave is being digested. Second, physical occupancy — Camden has been holding around 95%, and it needs to stay stably above roughly 95.0% for the story to hold. Occupancy is the tell that reveals whether flat rents reflect disciplined pricing or hidden weakness; if occupancy slips and rents are flat, the portfolio is in trouble in a way the headline numbers might not immediately show. Third, the development yield spread — the gap between the yields Camden can achieve developing new communities (targeted around 5.75% to 6.0%) and the prevailing market cap rates (around 5.0% to 5.5%).[^6] That spread is the lifeblood of the value-creation engine; if it compresses toward zero, Camden's signature development advantage stops paying, and the company becomes just another buyer of buildings. Track those three, and you will know whether the great capital recycle is working long before the final verdict is in.

XIV. Epilogue & Playbook Lessons

Step back from the quarter-to-quarter noise and Camden's forty-year arc delivers a single, durable lesson for long-term investors: in a cyclical industry, operations are the tide but capital allocation is the moon. Camden cannot control the Sunbelt supply wave any more than it could control the 1980s oil bust or the 2008 credit freeze. What it has controlled, across every one of those cycles, is the strength of its balance sheet and the discipline of its capital decisions — and that discipline is what let it survive the crashes that killed its peers and then go on the offensive while others were paralyzed. The 2026 California trade is simply the latest expression of the same idea the founders learned in the wreckage of Texas real estate: a company that stays liquid and thinks in terms of value rather than size can manufacture returns even when the operating environment is flat or falling, by exploiting the gap between what the public market will pay for its shares and what the private market will pay for its buildings. That public-private arbitrage is the secular thread running through an otherwise cyclical story.

The second lesson is about continuity, and it is quieter but just as important. Camden's 2026 succession — elevating decade-plus insiders into every senior seat while keeping the founders on the board as chairman and vice chairman — is close to a gold standard for how a founder-led company hands off power without losing its soul. The risk in any founder transition is that the culture and the operating system walk out the door with the founders. Camden's design deliberately guards against that: it preserved institutional memory in the boardroom and put operational control in the hands of the very people who had internalized the founders' philosophy over careers spanning multiple cycles. Whether that preserved discipline or merely preserved a comfortable consensus is the open question, and the aggressive capital bet launched almost simultaneously with the handoff means investors will get to watch the answer unfold in real time. The playbook is clear; the execution is still being written.

XV. Outro & Links

The story of Camden Property Trust is, at bottom, the story of two men who learned in a Texas catastrophe that the balance sheet is both shield and sword, and who spent the next four decades building a company around that conviction — through a 1993 IPO, a run of megamergers, the crucible of the financial crisis, a pandemic boom-and-bust in their own backyard, an antitrust reckoning over the software that priced their apartments, and finally a founder handoff paired with the boldest capital reallocation of their careers. It is not a story of a company that found an unassailable moat; the Sunbelt's open, buildable geography guarantees it never will. It is a story of something rarer and, for patient investors, arguably more valuable: a company that has proven, across cycle after cycle, that disciplined capital allocation and operational excellence can compound value even without a moat — provided management keeps its nerve and its balance sheet intact.

For readers who want to go deeper, the primary sources tell the story in management's own words and the regulators' own filings. Camden's investor relations portal and SEC filings — the annual 10-K reports, the quarterly earnings releases and supplementals, and the earnings-call transcripts — are the essential record for tracking the three KPIs above and testing management's guidance against its results. The RealPage antitrust docket and the DOJ's complaint document the legal overhang. And the 2026 disposition and buyback coverage from the real estate trade press chronicles the great capital recycle as it happened. Read them with the same question Camden's own leadership asks every quarter: given what the public and private markets are each willing to pay today, what is the smartest possible use of the next dollar?

References

-

This apartment owner moves to exit California, swapping property for its own shares — CoStar Group, 2026 ↩↩↩↩

-

SEC EDGAR Camden Property Trust CPT Filings — Securities and Exchange Commission, 2026 ↩

-

Camden outlines 2026 core FFO midpoint of $6.75 as it expects Q2 core FFO of $1.65-$1.69 — Seeking Alpha, 2026-04-30 ↩↩↩↩↩↩↩

-

Camden Property Trust 2005 Form 10-K Annual Report — SEC, 2006 ↩

-

Camden Property Trust Form 8-K FY2003 — Securities and Exchange Commission, 2003 ↩

-

Summit Properties Inc Form 425 — Securities and Exchange Commission, 2004 ↩

-

Camden Looks to Exit California With $1.5B Portfolio Sale — The Real Deal, 2026-02-02 ↩

-

Here's why Camden will exit California as it bets big on the Sun Belt — HousingWire, 2026 ↩↩

-

Camden Property Trust Stock Repurchases and Capital Management Strategy — Investing.com, 2026-05-10 ↩

-

Camden Property Trust Announces Third Quarter 2025 Operating Results — Business Wire, 2025-11-06 ↩

-

Camden Property Trust Q1 Core FFO $1.70, 2026 guide $6.75 — StockTitan, 2026-04-30 ↩↩↩↩

-

Camden settles RealPage lawsuit for $53M — Multifamily Dive, 2026-04-13 ↩↩↩

-

Camden Property Trust Official Website — Culture and Careers — Camden, 2026 ↩

-

Camden Property Trust Announces Executive Leadership Transition — Business Wire, 2026-03-27 ↩↩

-

Camden Property Trust (CPT) installs new CEO, COO and CFO with updated contracts — StockTitan, 2026-03-27 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube