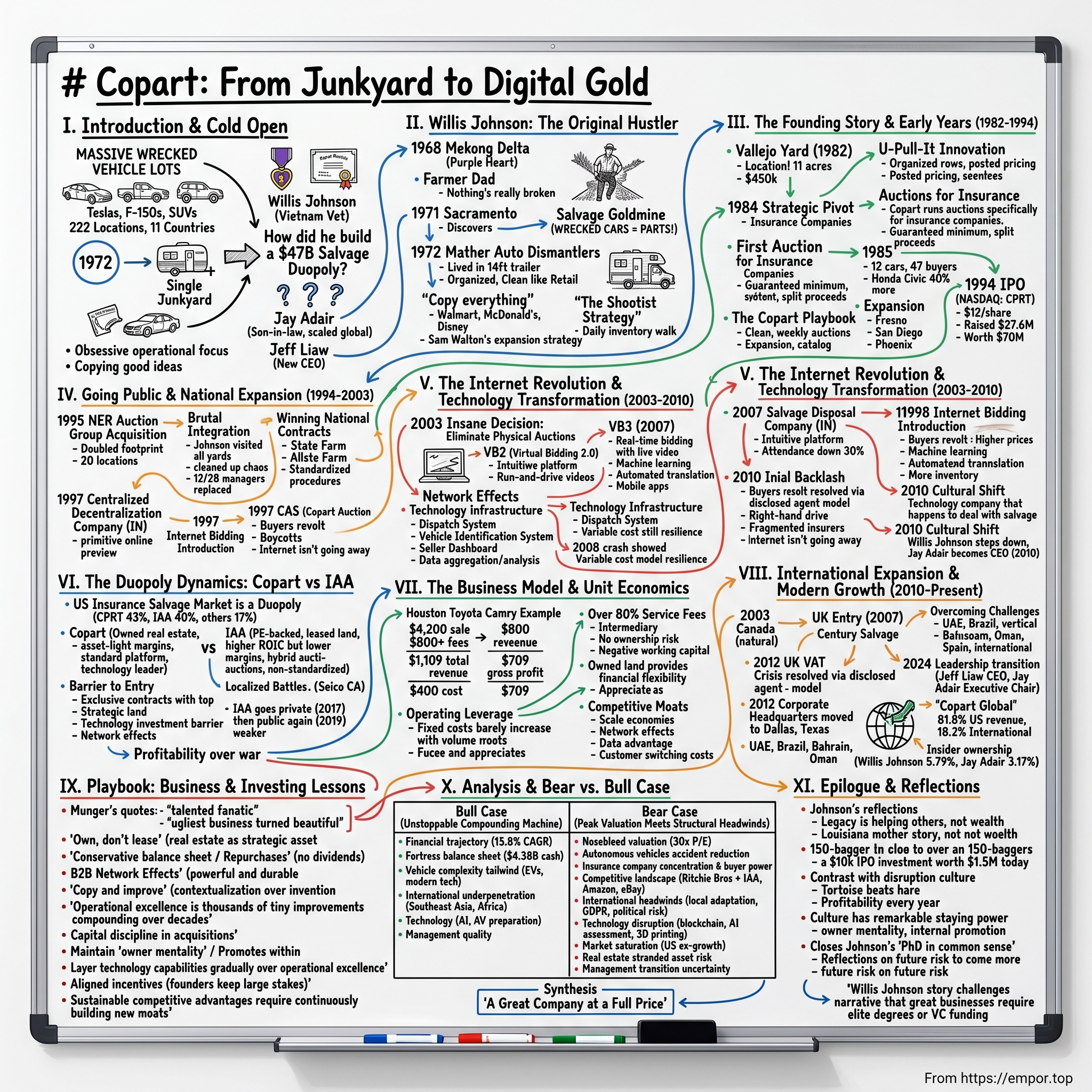

Copart: From Junkyard to Digital Gold

I. Introduction & Cold Open

Picture this: A massive parking lot stretching beyond the horizon, filled with over 10,000 wrecked vehicles—Teslas with crumpled front ends, flood-damaged F-150s, luxury SUVs written off by insurance companies. Now multiply that image by 222 locations across 11 countries. This is Copart's empire today, a $47 billion salvage auction colossus that processes millions of totaled vehicles annually, turning automotive disasters into digital gold.

But rewind to 1972. A Vietnam veteran named Willis Johnson is living in a trailer park in Sacramento, having just scraped together enough money to buy a single junkyard. His family sleeps in that trailer because every dollar matters—the business needs capital more than they need a house. Johnson works 18-hour days, dismantling cars with his bare hands, learning which parts sell and which don't, studying the rhythms of scrap metal prices like a commodity trader studies futures contracts.

The gap between these two images—the trailer park and the global empire—poses a fascinating question: How did a Purple Heart recipient with a high school education and a talent for dismantling cars build one of the most durable duopolies in American business? How did he create a company that Warren Buffett's partner Charlie Munger would later call an example of a "talented fanatic" at work? In 2024 alone, 4.0 million vehicles were processed, across more than 200 locations in 11 countries. This is Copart's patented virtual auction technology, named VB3, at work—turning twisted metal into marketplace gold through digital transformation.

The answer to our opening question lies not in a single innovation or lucky break, but in the systematic application of what Charlie Munger called "fanatical" focus: an obsessive attention to operational details, a willingness to copy shamelessly from anyone with a good idea, and the courage to bet everything on a vision when everyone else thought you were crazy. This is the story of how Willis Johnson built Copart from a single junkyard into a digital auction powerhouse, how his son-in-law Jay Adair scaled it globally, and how the company continues to dominate under new CEO Jeff Liaw.

It's a story about turning the ugliest business imaginable—wrecked cars—into one of the most beautiful business models on Wall Street. It's about building network effects in an industry that didn't know it needed them. And ultimately, it's about why sometimes the best technology companies don't start in Silicon Valley—they start in salvage yards.

II. Willis Johnson: The Original Hustler

The rain was coming down hard in the Mekong Delta when Willis Johnson's helicopter took enemy fire. It was 1968, and the 21-year-old Army specialist from Arkansas was about to earn his Purple Heart the hard way. Shrapnel tore through the chopper's hull, embedding itself in Johnson's leg. As he would later tell employees at Copart company meetings, that moment taught him something crucial: "When you're under fire, you don't panic—you focus on what needs to be done and you execute." He'd carry that battlefield mentality into every business decision for the next five decades.

Johnson was born in 1947 in Clinton, Alabama, but his formative years unfolded on a dairy farm near Siloam Springs, Arkansas. His father wasn't just a farmer—he was a tinkerer, a man who could fix anything with an engine. Young Willis watched his dad strip down tractors and rebuild them from scratch, learning that every machine was just a collection of parts, each with its own value. "My dad taught me that nothing's ever really broken," Johnson would later say. "It's just waiting to be turned into something else."

After his tour in Vietnam, Johnson returned to a country that didn't quite know what to do with its veterans. He bounced between jobs—construction, trucking, whatever paid—before landing in Sacramento in 1971. That's when he discovered the salvage business. He took a job at a local junkyard and immediately recognized something others missed: this wasn't a graveyard for cars, it was a goldmine of parts. Each wrecked vehicle contained dozens of components that someone, somewhere, desperately needed.

In 1972, with $2,000 scraped together from savings and a small loan, Johnson bought Mather Auto Dismantlers, a failing junkyard on the outskirts of Sacramento. The previous owner thought he was getting the better end of the deal—the place was hemorrhaging money, the inventory was a mess, and competition was fierce. But Johnson saw opportunity where others saw chaos. He moved his wife and two young daughters into a 14-foot travel trailer on the property. "We lived in that trailer for two years," his wife Joyce would later recall. "Every penny went back into the business."

Here's where Johnson's genius began to show. While his competitors ran their junkyards like, well, junkyards—cars scattered randomly, parts thrown in piles, customers left to wander and hope—Johnson brought military precision to the chaos. He organized vehicles by make and model. He created an inventory system using index cards. He answered the phone on the first ring and remembered customers' names. Most revolutionary of all: he cleaned the place up. "I wanted it to look like a retail store, not a dump," he explained. "If you respect your business, customers will respect it too."

Johnson became famous for what employees called his "copy everything" philosophy. He'd visit competitors pretending to be a customer, taking mental notes on their operations. He studied Walmart's inventory management. He analyzed McDonald's customer service training. He even took his family to Disneyland—not for fun, but to study how they managed crowds and kept people happy while waiting in lines. "I'm not proud," Johnson would say. "If someone has a better idea, I'll steal it and make it even better."

One story captures Johnson's approach perfectly. In 1978, he watched the John Wayne movie "The Shootist" and noticed how the gunfighter methodically prepared for confrontation—checking his weapons, surveying the battlefield, anticipating every move. The next Monday, Johnson implemented what he called "The Shootist Strategy" at his yard: every morning, managers would walk the entire property, checking inventory, identifying problems before they became crises, preparing for the day's battles. It sounds crazy, but it worked. His yards ran with an efficiency that stunned competitors.

By 1980, Johnson owned three salvage yards and was processing more vehicles than operations ten times his size. But he wasn't satisfied with regional success. He studied Sam Walton's expansion strategy, reading everything he could about how Walmart grew from a single store in Arkansas to a national chain. The lesson was clear: to build something truly great, you needed scale, systems, and capital.

Johnson's employees describe him as a peculiar mix of characteristics: cheap to the point of obsession (he'd reuse paper clips and turn off lights in empty rooms), but willing to bet millions on expansion; tough as nails in negotiation, but generous with employees who showed loyalty; a high school graduate who'd never taken a business class, but who could calculate inventory turns and margin percentages in his head faster than MBAs with spreadsheets.

Charlie Munger would later study Johnson's career and declare him a "talented fanatic"—one of those rare entrepreneurs who combines obsessive focus with practical intelligence. Munger noted that Johnson succeeded not through breakthrough innovation but through "fanatical implementation of simple ideas." Copy what works. Organize better than anyone else. Treat customers with respect. Control your costs. And never, ever stop improving.

This battlefield-tested veteran, living in a trailer with his family, counting paper clips while dreaming of empire, was about to transform an entire industry. He just needed the right opportunity—and in 1982, that opportunity would arrive in the form of a small salvage yard for sale in Vallejo, California. The asking price was steep, the competition was skeptical, but Willis Johnson saw something nobody else did: the foundation for what would become Copart.

III. The Founding Story & Early Years (1982-1994)

The Vallejo salvage yard sat on 11 acres of Northern California soil, halfway between San Francisco and Sacramento. When Willis Johnson first walked the property in early 1982, the owner kept apologizing for its condition—rusted fence posts, oil-stained earth, a cramped office that leaked when it rained. The asking price was $450,000, an astronomical sum for a failing operation that processed maybe 30 cars a month. Johnson's banker laughed when he saw the loan application. His competitors whispered that Willis had finally overreached. But Johnson saw what they missed: Vallejo sat at the intersection of two major highways, equidistant from two metropolitan markets, with room to expand. "Location, location, location," he'd mutter, borrowing the real estate mantra. "Everything else you can fix."

On July 15, 1982, Copart was officially born—though nobody called it that yet. Johnson named it "Copart" by combining "co" (for company) with "part" (for auto parts), a straightforward name for what he assumed would be a straightforward business. But from day one, Johnson ran it differently than any salvage yard in America.

First came the U-Pull-It innovation, though Johnson would bristle at calling it "his" innovation. He'd seen a similar concept at a yard in Los Angeles—customers removing their own parts for a discount—and immediately recognized its brilliance. But where that LA yard was chaotic, Johnson systematized it. He organized cars in rows like a parking lot. He provided wheelbarrows and basic tools. He posted clear pricing on a giant board. Most importantly, he stationed employees throughout the yard to help customers find what they needed. "We're not just selling parts," he told his team. "We're selling an experience."

The numbers told the story: within six months, the Vallejo yard was processing 200 cars a month. Within a year, it was 400. Johnson plowed every dollar of profit back into the operation. He bought better equipment—forklifts that actually worked, a car crusher that could process vehicles in minutes instead of hours. He hired selectively, choosing employees who understood customer service over those who simply knew cars. One early hire remembered Johnson's interview technique: "He didn't ask me about cars. He asked me how I'd treat someone's grandmother if she showed up needing help."

By 1984, Johnson made his first strategic pivot—one that would define Copart's future. He noticed that insurance companies were struggling with totaled vehicles. When a car was declared a total loss, insurers had to somehow dispose of it, usually by calling multiple salvage yards and accepting whatever lowball offer came in. It was inefficient, opaque, and ripe for corruption. Johnson proposed something radical: what if Copart ran auctions specifically for insurance companies?

The insurance executives were skeptical. Auctions meant uncertainty—what if no one bid? What if prices were too low? Johnson countered with a guarantee: Copart would advance the insurance company a minimum amount immediately, then auction the vehicle and split any proceeds above that minimum. If the auction failed to meet the minimum, Copart ate the loss. It was a massive risk, but Johnson had done his homework. He knew that competition between buyers would drive prices up, and that volume would smooth out individual losses.

The first insurance auction was held in October 1985. Twelve insurance company vehicles, 47 registered buyers, and Johnson himself as auctioneer (he'd practiced in front of a mirror for weeks, copying techniques from livestock auctioneers he'd observed). The first car, a wrecked Honda Civic, sold for 40% more than the insurance company's estimated salvage value. By the end of the day, every vehicle had sold above the minimum. The insurance executives were stunned. Word spread quickly through the industry.

But Johnson's real genius wasn't just the auction model—it was the operational excellence behind it. While competitors held auctions monthly, Copart ran them weekly. While others stored cars haphazardly, Copart photographed each vehicle from multiple angles and created detailed condition reports. While others relied on word-of-mouth to attract buyers, Copart published a catalog—yes, an actual printed catalog—mailed to thousands of potential bidders. "We're not running a junkyard," Johnson would say. "We're running a marketplace."

The expansion came fast. Fresno in 1987. San Diego in 1988. Phoenix in 1989. Each new location followed what Johnson called "The Copart Playbook": clean facilities, organize inventory, weekly auctions, exceptional customer service, and relentless focus on the insurance market. He financed growth through a combination of bank loans, seller financing, and sheer cash flow management. Johnson was famous for negotiating 60-day payment terms with sellers while collecting from buyers in 3 days, creating a massive float that funded operations.

By 1990, Copart operated 15 locations across California, Nevada, and Arizona, processing over 50,000 vehicles annually. Revenue hit $35 million. But Johnson knew he'd hit a ceiling. To compete nationally, to win the huge insurance company contracts, he needed capital—real capital, not just bank loans and float. He needed to go public.

The investment bankers who visited Copart's Fairfield headquarters in 1993 didn't know what to make of Willis Johnson. Here was a CEO who answered his own phone, who knew the name of every forklift operator, who could tell you the profit margin on a 1987 Toyota Camry's driver-side door. When they suggested he needed to "professionalize" management before an IPO, Johnson's response was typical: "You want me to hire someone who knows less about this business than me, pay them more, and call that professional? No thanks."

But Johnson did make concessions. He hired a CFO with public company experience. He implemented formal financial controls. He even bought his first suit (off the rack at JCPenney, to the bankers' horror). Most importantly, he articulated a vision that Wall Street could understand: Copart would become the dominant platform connecting insurance companies with salvage buyers, using technology and scale to create an unassailable network effect.

The roadshow was vintage Johnson. Instead of PowerPoints filled with hockey-stick projections, he brought potential investors to actual Copart facilities. He showed them the organized yards, the efficient operations, the steady stream of insurance company trucks delivering inventory. When one investor asked about competitive advantages, Johnson's answer was simple: "While you're asking that question, we just sold six cars. That's our advantage—we execute while others talk."

On March 17, 1994, Copart had its initial public offering (IPO) at $12 per share and debuted on the NASDAQ under the symbol "CPRT." Copart's IPO of 2.3 million shares of stock provided the company with the means to become a national company. The offering raised $27.6 million, valuing the company at roughly $120 million. Willis Johnson retained 62% ownership. He was now worth over $70 million on paper—not bad for a guy who'd been living in a trailer 20 years earlier.

But Johnson didn't celebrate. The morning after the IPO, he was at the Fairfield yard at 5 AM, checking inventory. When an employee congratulated him on becoming rich, Johnson's response captured his mentality: "Paper wealth doesn't mean anything. What matters is how many cars we sell today." That focus on execution over financial engineering would become Copart's hallmark, setting it apart from competitors who would chase growth through leverage and acquisition without Johnson's operational discipline.

The IPO proceeds would fund an acquisition spree that would transform Copart from a regional player into a national force. But first, Johnson had to prove that his model could work beyond California, in markets with different regulations, different competitors, and different customer expectations. The next decade would test whether the Copart playbook was truly scalable—or whether Willis Johnson had simply gotten lucky in his backyard.

IV. Going Public & National Expansion (1994-2003)

The letter arrived at Copart headquarters on a Tuesday morning in April 1995, just thirteen months after the IPO. NER Auction Group, Copart's largest competitor outside California, was for sale. With 28 locations across the Midwest and East Coast, NER would instantly double Copart's footprint. The asking price: $43 million, nearly twice Copart's entire IPO proceeds. Willis Johnson read the letter three times, did some quick math on a napkin, then called his CFO: "We're buying them. Figure out how to pay for it."

In May 1995, Copart began rapid expansion in the United States with the sizable acquisition of NER Auction Group, doubling its number of facilities around the country. The NER acquisition was transformative not just for its scale but for what Johnson learned from it. NER's facilities were everything Copart's weren't—disorganized, poorly maintained, with antagonistic relationships with insurance companies. But they had one invaluable asset: contracts with State Farm, Allstate, and other major insurers. Johnson saw the opportunity immediately: apply Copart's operational excellence to NER's relationships.

The integration was brutal. Johnson personally visited all 28 NER locations in 30 days, often arriving unannounced at 6 AM to see how the yards really operated. At a facility in Detroit, he found cars stacked three high with a forklift from the 1960s that broke down daily. In Cleveland, the "auction" consisted of buyers wandering the yard and making offers to whoever happened to be working. In Chicago, he discovered the manager was buying cars from the yard himself through a shell company, then reselling them at a markup.

Johnson's cleanup was swift and merciless. Twelve of 28 managers were replaced within 60 days. Every yard was reorganized according to the Copart Playbook. Weekly auctions replaced the chaotic bidding free-for-alls. Most importantly, Johnson met personally with every major insurance partner, promising them something they'd never heard from a salvage company: transparency, consistency, and partnership.

The results were immediate. NER's same-store sales grew 40% in the first year under Copart management. Insurance companies that had been ready to terminate contracts instead signed long-term exclusivity agreements. By 1996, the combined company was processing 150,000 vehicles annually, generating $143 million in revenue.

But Johnson understood that true national dominance required more than just buying competitors—it required winning national contracts with insurance companies. These insurers wanted a single partner who could handle salvage from Seattle to Miami, with consistent service and pricing. It was a chicken-and-egg problem: you needed national coverage to win national contracts, but you needed the contracts to justify national expansion.

Johnson's solution was audacious: he announced Copart would have 100 locations by 2000, then started signing contracts based on that promise. When insurance executives questioned whether he could deliver, Johnson would pull out a map marked with planned locations, acquisition targets, and timeline. "I've never missed a promise to a customer," he'd say. "I'm not starting now."

The expansion that followed was unprecedented in the salvage industry. By March 1994, it had added another eight new facilities in Oregon, Washington, and Texas, culminating in the acquisition of the largest volume seller of salvage in the United States, North Texas Salvage Pool of Dallas, Texas. From July 1995 to July 1996 alone, Copart founded six new locations and acquired twelve others. Each acquisition followed the same pattern: identify the leading regional player, offer a premium price, then immediately implement Copart's systems.

The key to making these acquisitions work was what Johnson called "centralized decentralization." Each yard maintained local autonomy for day-to-day operations—they knew their markets, their buyers, their particular challenges. But core functions—IT systems, auction procedures, insurance relationships—were strictly standardized. It was the Walmart model applied to salvage: local face, national scale.

One acquisition stands out for what it taught Johnson about technology. In 1997, Copart bought Salvage Disposal Company of Indiana, a small operation with just three locations. But SDC had something unique: a primitive computer system that let buyers preview inventory online—just text descriptions, no photos, but revolutionary for 1997. Johnson immediately saw the potential. Within six months, every Copart location was uploading inventory to a central database.

The first main step in this process was the creation of the Copart Auction System (CAS) in 1997, which was designed to unify and support the growing business as well as allow Copart facilities and sellers to access information, generate reports, and increase operating efficiencies. The next step came in 1998 with Copart's introduction of internet bidding—a departure from the industry standard of local physical auctions.

The internet initiative almost destroyed the company. Johnson decided Copart would be the first to offer true online bidding—not just previews, but actual purchases. The technology cost $8 million to develop, a massive bet for a company with $35 million in annual profit. Worse, established buyers hated it. They'd built their businesses on information asymmetry, knowing which yards had the best inventory, showing up in person to intimidate casual bidders. Online auctions would level the playing field.

The backlash was fierce. Major buyers threatened boycotts. Yard managers reported that auction attendance dropped 30% in early 1999 as buyers protested. Revenue dipped for the first time in company history. The board pressured Johnson to abandon the online initiative. His response was characteristic: "The internet isn't going away. We can either lead or follow. I don't follow."

Johnson was right. By late 1999, online bidding accounted for 15% of sales. New buyers emerged—smaller operations from rural areas, international purchasers who could never attend in person, even individual consumers looking for project cars. The expanded buyer base drove prices up, which made insurance companies ecstatic. By 2000, Copart's average sale price per vehicle had increased 22%, even as volume grew.

The operational challenges of this growth were staggering. Copart was simultaneously integrating acquisitions, building technology infrastructure, and managing relationships with hundreds of insurance companies. The company hired 2,000 employees between 1995 and 2000. It built a massive technology center in Dallas. It standardized operations across facilities that had operated independently for decades.

The secret to managing this chaos was Johnson's leadership team, particularly a young executive named Jay Adair. Johnson had hired Adair in 1989 as a yard manager in Vallejo—the same facility where Copart began. Adair was everything Johnson wasn't: college-educated, technology-savvy, comfortable with Wall Street. But they shared the same obsession with operational excellence and customer service. By 1996, Adair was running all operations. By 2000, he was President and heir apparent.

The numbers by 2003 were staggering: By 2003, the company grew to 100 locations across the country, processing over 600,000 vehicles annually, with revenue of $358 million. Copart had won exclusive contracts with 5 of the top 10 insurance companies. The stock price had risen from $12 at IPO to $35, adjusting for splits.

But the real achievement was market structure. Through relentless execution and strategic acquisition, Copart had helped create a duopoly with Insurance Auto Auctions (IAA). Together, they controlled over 80% of the insurance salvage market. The smaller players couldn't match their scale, technology, or insurance relationships. It was exactly the market structure Johnson had envisioned a decade earlier.

Yet Johnson knew the next phase would be even more challenging. The internet had changed everything. Buyers could now be anywhere. Competition could come from unexpected directions. And the technology that had given Copart its advantage was evolving so fast that million-dollar investments became obsolete in years. The company needed to transform from a salvage yard operator that used technology into a technology company that happened to move salvage. That transformation would define Copart's next chapter—and determine whether it could maintain its dominance in a digital world.

V. The Internet Revolution & Technology Transformation (2003-2010)

The conference room at Copart's Fairfield headquarters was dead silent. It was January 2003, and Willis Johnson had just announced the most radical decision in company history: Copart would eliminate all physical auctions. Everything would move online. No more auctioneers. No more crowds of bidders. No more of the carnival atmosphere that had defined auto auctions for a century. A yard manager from Texas finally spoke up: "Willis, that's insane. Our buyers will revolt. We'll lose half our volume." Johnson's response was calm but firm: "We'll lose them anyway if we don't change. The question is whether we disrupt ourselves or let someone else do it."

By 2003, the company grew to 100 locations across the country and became the first to launch a completely online auction model. In fiscal year 2004 in North America and fiscal year 2008 in the U.K., Copart discontinued all live auctions and began remarketing vehicles exclusively through VB2. The transition to VB2 (Virtual Bidding 2.0) wasn't just a technology upgrade—it was a complete reimagining of the salvage auction business.

The genesis of this transformation actually started with a failure. In 2001, Copart had launched its first online bidding platform, but it was clunky, slow, and buyers hated it. Only 12% of bids came through the online system. Johnson could have declared victory with that modest digital presence, but he saw the writing on the wall. eBay had gone public and was processing billions in transactions. Amazon was expanding beyond books. The internet wasn't just another sales channel—it was becoming the only channel that mattered.

Johnson hired a team of software engineers from Oracle and gave them a simple mandate: build an auction platform so intuitive that his 75-year-old mother could use it. The team spent six months shadowing buyers at physical auctions, understanding their psychology, their strategies, their frustrations. They discovered something crucial: buyers didn't just want to bid online—they wanted more information than a physical auction could ever provide.

VB2 launched with features that seemed obvious in retrospect but were revolutionary for 2003. High-resolution photos from 10 angles. Detailed damage reports with enhancement tools to zoom in on specific areas. Run-and-drive videos for vehicles that still functioned. Historical pricing data for similar vehicles. Even a "virtual walk-around" feature that simulated examining the car in person.

But the real innovation was the auction mechanism itself. Instead of traditional timed auctions where all bids happened in a compressed window, VB2 used a "proxy bidding" system similar to eBay. Buyers could set maximum bids and the system would automatically increment their offers. Auctions ran for several days, allowing international buyers in different time zones to participate. A "bid now" feature let eager buyers purchase immediately at a premium price.

The numbers validated the strategy immediately. In the first quarter after going fully online, Copart's average sale price increased 18%. The buyer base exploded from 15,000 registered bidders to 45,000 within a year. International sales, previously negligible, reached 10% of volume. Most surprisingly, the elimination of physical auctions actually reduced operating costs by 20%—no more crowd control, no more auction staff, no more maintaining bidding facilities.

One story captures the transformation perfectly. In 2004, a small auto parts dealer in Lithuania discovered Copart's online platform. He started buying specific models popular in Eastern Europe—older BMWs, Mercedes, Volkswagens—that American buyers overlooked. Within two years, he was purchasing 300 vehicles annually, shipping them to Klaipeda, and building a thriving business. This would have been impossible in the physical auction era. Multiply that story by thousands of international buyers, and you understand how VB2 changed everything.

But Johnson wasn't satisfied with just moving auctions online. He wanted Copart to become what he called "the Amazon of salvage"—a platform so dominant that it became the default choice for both sellers and buyers. This required massive technology investments that Wall Street didn't always understand. Between 2003 and 2007, Copart spent $150 million on technology—more than most competitors' entire market caps.

The crown jewel was VB3, launched in 2007. Its VB3 online auction platform, launched in 2003, remains a cornerstone of its competitive edge. If VB2 was evolutionary, VB3 was revolutionary. It introduced real-time bidding with live video feeds, letting remote buyers feel like they were at a physical auction. Machine learning algorithms suggested vehicles based on past bidding history. Automated translation made the platform accessible in 12 languages. Mobile apps let buyers bid from anywhere.

The network effects kicked in with devastating force. More buyers meant higher prices for sellers (insurance companies), which meant more inventory for Copart, which attracted more buyers. It was a virtuous cycle that competitors couldn't break. IAA tried to keep physical auctions running alongside online bidding, satisfying no one. Smaller players couldn't afford the technology investments. By 2008, Copart's market share in online salvage auctions reached 65%.

The technology transformation went beyond just the bidding platform. Copart built proprietary systems for every aspect of the business. The Copart Dispatch System (CDS) optimized tow truck routes using GPS and traffic data, reducing transport costs by 15%. The Vehicle Identification System (VIS) used image recognition to automatically catalog damage, eliminating hours of manual inspection. The Seller Dashboard gave insurance companies real-time visibility into their inventory, claims processing, and settlement speeds.

One innovation deserves special mention: Copart's approach to data. While competitors saw vehicle information as a cost center—something you had to collect but didn't monetize—Johnson saw it as a strategic asset. Copart began aggregating and analyzing millions of auction results, creating the industry's most comprehensive database of salvage values. Insurance companies started using Copart's data to make total-loss decisions before vehicles even arrived at the yard. This data supremacy created switching costs that locked in sellers.

The 2008 financial crisis tested Copart's digital transformation. New car sales plummeted, which meant fewer accidents, which meant less salvage inventory. Competitors with high fixed costs from physical auction infrastructure struggled. Copart's variable cost model—no auctioneers, minimal facility staff, cloud-based technology—allowed it to maintain margins even as volume dropped. The company actually gained market share during the recession, acquiring distressed competitors' contracts and facilities at bargain prices.

By 2010, the transformation was complete. Copart processed 1.2 million vehicles annually, all through online auctions. International buyers accounted for 25% of purchases. The company generated $823 million in revenue with 35% EBITDA margins—unheard of in the traditionally low-margin salvage industry. The stock price had risen to $45, making early investors wealthy and validating Johnson's technology bet.

But perhaps the most important change was cultural. Copart no longer thought of itself as a salvage company that used technology. It was a technology company that happened to deal with salvage. Engineers were recruited from Google and Amazon. Data scientists outnumbered yard workers at headquarters. Product managers obsessed over user experience metrics that would seem alien to traditional auto auctioneers.

This cultural shift came with leadership change. In February 2010, Willis Johnson stepped down as CEO, though he remained Chairman. Jay Adair, his son-in-law who'd been President since 2003, took the helm. Johnson was 63, wealthy beyond imagination, and ready to hand over daily operations. But his real reason was strategic: Copart needed a leader who intuitively understood technology, who could navigate the company through its next phase of growth—international expansion and the coming disruption of autonomous vehicles.

At Johnson's farewell address to employees, he was characteristically blunt: "I built this company from one yard to 100, from zero to a billion in revenue. Jay's job is to take it from 100 to 1,000 yards, from one billion to ten billion. He understands technology in a way I never will. He speaks the language of tomorrow's Copart." The torch had passed, but the foundation Johnson built—operational excellence, customer focus, and willingness to disrupt yourself—would define Copart for decades to come.

VI. The Duopoly Dynamics: Copart vs IAA

The meeting took place in a nondescript Marriott conference room near Chicago O'Hare in September 2011. Executives from Copart and Insurance Auto Auctions (IAA) sat across from each other, ostensibly discussing "industry best practices." But everyone knew the real agenda: could these fierce competitors find a way to peacefully coexist, or would their battle for market dominance destroy them both? Jay Adair, now Copart's CEO, studied his counterpart from IAA. They controlled 80% of the salvage auction market between them. The question was whether that was stable equilibrium or merely a pause before all-out war.

To understand the Copart-IAA duopoly, you need to understand how radically different their approaches were, despite operating in identical markets. The U.S. insurance salvage auction business is a duopoly; Copart claims 43%, IAA 40%, and smaller players 17%, with the closest one representing only 3% of the total market. These market shares had remained remarkably stable for years, suggesting a competitive equilibrium that benefited both players.

IAA's history was the inverse of Copart's. While Willis Johnson built from a single yard up, IAA was created in 1992 through the merger of Insurance Auto Auctions Inc. and Impact Auto Auctions—a top-down consolidation funded by private equity. Where Copart obsessed over operations, IAA focused on financial engineering. Where Copart owned its land, IAA leased to maintain capital efficiency. Where Copart went all-in on digital, IAA hedged its bets with hybrid physical-digital auctions.

The land ownership difference was philosophical and profound. Copart owned 95% of its facilities outright, viewing real estate as a strategic asset. Johnson's logic was simple: "Land appreciates, leases just get more expensive." By 2011, Copart's owned land was worth $1.8 billion—nearly half the company's market cap—providing a cushion during downturns and financing for expansion. IAA, conversely, leased 80% of its facilities, arguing this provided flexibility and better return on invested capital.

The numbers told different stories. IAA's asset-light model generated higher returns on capital—25% vs Copart's 18% in 2011. But Copart's margins were superior—38% EBITDA vs IAA's 31%. The market clearly preferred Copart's approach: it traded at 18x earnings versus IAA's 12x, despite similar growth rates. Investors saw Copart's owned land and superior technology as sustainable competitive advantages.

The technology gap was becoming a chasm. While Copart had moved entirely online by 2004, IAA still ran physical auctions at many locations as late as 2012. IAA's management argued this gave customers choice, but the real reason was organizational inertia. IAA's facilities operated as independent fiefdoms, each with its own processes and systems. Standardizing on a single platform proved nearly impossible.

One insurance executive who worked with both companies explained the difference: "With Copart, I had one interface, one set of reports, one point of contact for problems nationwide. With IAA, every region was different. Their California operations might as well have been a different company from their Texas operations. It was frustrating, but we needed both to have coverage everywhere."

This operational divergence created an interesting dynamic: instead of competing head-to-head, Copart and IAA increasingly served different segments. Copart dominated the high-volume, technology-forward insurance companies that valued consistency and data. IAA retained relationships with regional insurers that preferred local touch and flexibility. The market was bifurcating, and both companies were winning their chosen segments.

The competitive battles, when they occurred, were fierce but localized. In 2012, State Farm's exclusive contract came up for renewal in Texas. Copart and IAA both bid aggressively, with IAA ultimately winning by guaranteeing minimum returns that industry observers called "economically irrational." But Copart retaliated by winning Geico's California business six months later. The tit-for-tat continued, but neither company could deliver a knockout blow.

What prevented all-out war was the industry's unique economics. Insurance companies, the primary sellers, didn't want a monopoly—they needed competition to ensure fair pricing. But they also didn't want fragmentation—managing relationships with dozens of salvage companies was operationally impossible. A duopoly was the perfect structure: enough competition to keep prices honest, enough scale to ensure efficiency.

The barriers to entry were becoming insurmountable. By 2015, Copart and IAA had locked up exclusive contracts with 18 of the top 20 auto insurers. They owned or controlled most strategic land near major metropolitan areas. Their technology investments—Copart had spent $300 million on IT by this point—were impossible for new entrants to match. Even if a competitor emerged, the network effects were too strong: buyers went where the inventory was, sellers went where the buyers were.

Some attempted disruption anyway. In 2014, a Silicon Valley startup called AutoBid raised $50 million to build a "pure-play" online salvage platform without physical facilities. Their pitch was compelling: eliminate the real estate costs, use AI for pricing, create a true digital marketplace. They signed up 10,000 buyers in six months. But they couldn't get inventory. Insurance companies wouldn't trust a company without physical facilities to store and process vehicles. AutoBid shut down in 2016, burning through its entire investment.

The duopoly's stability created interesting strategic decisions. Both companies could have engaged in price wars to gain share, but that would have destroyed profitability for both. Instead, they competed on service and technology while maintaining pricing discipline. It was the same playbook Coke and Pepsi had followed for decades: compete fiercely on marketing and product, but never on price.

By 2017, a new dynamic emerged. IAA, frustrated by its technology deficit and operational challenges, went private in a $2.9 billion leveraged buyout by Ritchie Bros. Auctioneers. The thesis was that combining IAA's insurance relationships with Ritchie's technology platform would create a stronger competitor to Copart. The market was skeptical—IAA's challenges were cultural, not just technological.

The contrast with Copart was stark. While IAA was loading up with debt to go private, Copart was generating $400 million in free cash flow annually. While IAA was trying to integrate with Ritchie Bros, Copart was expanding internationally. While IAA was playing catch-up on technology, Copart was investing in artificial intelligence and autonomous vehicle preparation.

The competitive dynamics took another turn in 2019 when IAA went public again, this time as a standalone company separated from Ritchie Bros. The separation was messy, the integration benefits unrealized, and IAA emerged weaker than before. Its stock traded at just 10x earnings versus Copart's 25x, reflecting the market's view of their relative positions.

But the duopoly endured. By 2020, Copart and IAA still controlled 80% of the market, the same as a decade earlier. The stability was remarkable in an industry being disrupted by electric vehicles, autonomous driving, and changing mobility patterns. Both companies were profitable, growing, and generating cash. The war that everyone expected never came.

Looking back, the Copart-IAA duopoly teaches important lessons about competition and market structure. Sometimes the most profitable outcome isn't monopoly but stable oligopoly. Sometimes the best strategy isn't destroying your competitor but coexisting profitably. And sometimes the most important competitive advantage isn't what you do differently from your rival, but what you both do differently from everyone else—in this case, operating at a scale that no one else could match.

VII. The Business Model & Unit Economics

Picture a single wrecked Toyota Camry arriving at Copart's Houston facility on a Tuesday morning. The insurance company has already declared it a total loss—repair costs exceed the car's value. A Copart truck delivers it to the yard, where it's photographed, cataloged, and listed online within 4 hours. Seven days later, it sells at auction for $4,200 to a buyer in Mexico City who specializes in rebuilt vehicles. Copart collects $800 in fees without ever owning the car. Multiply this transaction by 4.0 million vehicles processed in 2024, and you begin to understand why this business model is so powerful.

Copart derives the largest part, over 80%, of its revenue from service fees collected for use of its online auction platform. The majority of the remainder of revenue comes from the sale of vehicles it actually takes ownership of and then resells. This service-fee model is the key to Copart's economics. The company acts as an intermediary, never taking ownership risk on most vehicles, never tying up capital in inventory, never worrying about depreciation or market timing.

The unit economics are elegant in their simplicity. On a typical transaction, Copart charges the seller (usually an insurance company) a flat fee of around $200-300 plus 5-10% of the sale price. The buyer pays an additional fee of $200-600 depending on the sale price, plus a gate fee of $79-89. On that $4,200 Camry, Copart might collect $200 seller fee + $420 seller percentage (10% of sale) + $400 buyer fee + $89 gate fee = $1,109 total revenue. The direct costs—towing, storage, processing—might total $400. That's $709 in gross profit, roughly 64% margin, on a single vehicle.

But the real magic happens at scale. Those fixed costs—the land, the technology platform, the management infrastructure—barely increase whether Copart processes 100 or 1,000 vehicles per location per month. A yard with $500,000 in annual fixed costs breaking even at 100 cars monthly becomes wildly profitable at 300 cars. This operating leverage explains why Copart's EBITDA margins expanded from 25% to 38% as volume grew.

The land ownership advantage compounds over time. A Copart facility purchased in Phoenix for $2 million in 1995 might be worth $15 million today. That appreciation doesn't show up in earnings, but it provides massive financial flexibility. During the 2008 crisis, Copart borrowed against its real estate at 3% interest rates while competitors with leases faced 8% annual escalations. The owned land also allows infinite customization—Copart can optimize layouts for efficiency rather than accepting whatever configuration a landlord provides.

The working capital dynamics are even more attractive. Insurance companies typically pay Copart within 30 days of sale. Buyers must pay immediately—actually, they must deposit funds before bidding. This negative working capital cycle means growth actually generates cash rather than consuming it. As volume increases, Copart's cash balance grows automatically, providing self-funding for expansion.

The network effects create a moat that strengthens with scale. Copart currently operates more than 200 locations in 11 countries, and has over 175,000 vehicles up for auction every day. More inventory attracts more buyers. More buyers drive higher prices. Higher prices attract more sellers (insurance companies). More sellers bring more inventory. It's a virtuous cycle that's nearly impossible for competitors to break.

Consider the buyer acquisition cost. A new salvage auction company might spend $500 in marketing to acquire each buyer. Copart spends essentially nothing—buyers come because that's where the inventory is. Similarly, seller acquisition costs approach zero for incremental volume. Once Copart has a contract with State Farm, every additional State Farm vehicle costs nothing to acquire.

The technology platform exhibits massive returns to scale. In fiscal year 2024, Copart's total revenue reached $4.2 billion, but the technology infrastructure that processes all those transactions—the servers, software, and systems—might cost $100 million annually to maintain. That's just 2.5% of revenue. A competitor with $400 million in revenue (10% of Copart's size) would need essentially the same technology infrastructure, making it 25% of their revenue. The scale disadvantage is crushing.

The international operations add another dimension. In fiscal year 2024, about 81.8% of the company's total revenue originated in the United States, and around 18.2% came from international markets. These international buyers, particularly from Mexico, Central America, and the Middle East, often pay premium prices for vehicles that American buyers wouldn't touch. A flood-damaged luxury car worthless in Houston might sell for $15,000 to a buyer in Dubai where labor costs make rebuilding economical.

The data advantage is underappreciated. With millions of transactions annually, Copart has the industry's most comprehensive database of salvage values. They know exactly what a 2018 Honda Accord with front-end damage sells for in Dallas versus Detroit, in January versus July, to domestic versus international buyers. This data helps insurance companies make better total-loss decisions, embedding Copart deeper into their workflows.

The capital allocation is remarkably disciplined. From 2014 to 2024, Copart generated roughly $8 billion in free cash flow. They spent $2 billion on acquisitions and facility expansion, returned $4 billion through buybacks, and kept $2 billion in cash for flexibility. No dividends—Johnson believed dividends were tax-inefficient and preferred buybacks. No major debt—the balance sheet remains fortress-like with minimal leverage.

The returns on invested capital tell the story. Copart consistently generates 20%+ ROIC, remarkable for an asset-heavy business with significant real estate holdings. The reason is that seemingly "heavy" assets—the land and facilities—actually require minimal maintenance capital. Once a yard is built, annual maintenance might be 1-2% of its value. Compare that to manufacturing where equipment needs constant updating, or retail where stores need regular remodeling.

The recession-resistance is built into the model. During economic downturns, people drive older cars longer, which means more mechanical failures and accidents involving vehicles not worth repairing. Miles driven might decrease, but the salvage rate (percentage of accidents resulting in total loss) actually increases. Copart's revenue dipped just 5% during the 2008-2009 crisis while maintaining margins—remarkable resilience for a seemingly cyclical business.

The competitive advantages compound. Scale economies, network effects, data advantages, land ownership, customer switching costs—each reinforces the others. A competitor matching any single advantage wouldn't be enough; they'd need to match all simultaneously, requiring billions in capital and decades of execution. It's why the industry structure has remained stable for 20 years despite technological disruption everywhere else.

Looking at unit economics, it's clear why Charlie Munger admired this business. It's simple enough to understand—matching damaged cars with buyers—but complex enough in execution that few can replicate it. It generates predictable cash flows with minimal capital requirements. It strengthens with scale rather than diminishing. And it's run by owner-operators who think in decades, not quarters. The business model isn't just good—it's nearly perfect for long-term value creation.

VIII. International Expansion & Modern Growth (2010-Present)

The email arrived at 3 AM Dallas time in March 2012, sent from Copart's newly appointed UK managing director. "Jay, we have a problem. The UK government just changed VAT rules on salvage vehicles. Our entire business model might be illegal by next month." Jay Adair, six months into his CEO tenure, read it twice, then booked a flight to London for that evening. The international expansion that Willis Johnson had started was about to face its first existential crisis.

Copart's international journey actually began in 2003 with Canada—a natural extension given the geographic proximity and similar insurance structures. But the real prize was the UK, Europe's largest salvage market. In 2007, Copart acquired Century Salvage, a small British operator with just two facilities. The price was modest—$15 million—but the ambition was enormous: use the UK as a beachhead for European domination.

The UK market was different in every conceivable way. Vehicles were right-hand drive, making them worthless for export to continental Europe. The insurance market was fragmented among dozens of companies versus America's consolidated giants. Most challenging: UK law required salvage companies to take title to vehicles, meaning Copart had to actually buy and own inventory rather than just charging fees. It was a complete inversion of their asset-light US model.

Adair's response to the 2012 VAT crisis demonstrated the adaptability that would define Copart's international strategy. Within 72 hours, he had assembled a team of tax lawyers, government relations experts, and operations managers. They crafted a solution: restructure UK operations as a "disclosed agent" model where Copart technically took title but immediately disclosed the ultimate buyer, avoiding the VAT liability. It required rewriting thousands of contracts and retraining hundreds of employees, but it worked. The UK operations didn't miss a single auction.

The UK became Copart's laboratory for international expansion. They learned that what worked in America—massive yards in rural areas—failed in land-scarce Britain. So they built vertical storage systems, stacking cars three high. They discovered UK buyers preferred detailed mechanical assessments over just damage photos. So they hired certified mechanics to inspect every vehicle. They found that UK insurance companies valued speed over price. So they guaranteed settlement within 7 days, faster than any competitor.

By 2015, Copart UK was processing 400,000 vehicles annually—more than the next three competitors combined. The operation was so successful that UK margins actually exceeded US margins, despite the complexity of taking title to vehicles. The key was density: with limited land, Copart maximized throughput per square foot, turning inventory every 15 days versus 30 days in America.

Germany came next, but through acquisition rather than organic growth. In 2018, Copart bought WOM World of Mobility, Germany's largest salvage auction company, for €160 million. WOM brought something valuable: relationships with German insurance companies that had resisted foreign entry for decades. But it also brought challenges: powerful labor unions, strict environmental regulations, and a business culture that prioritized engineering perfection over operational efficiency.

The integration was painful. German employees resisted Copart's standardized processes, arguing that German vehicles required special handling. Environmental regulators demanded extensive documentation for fluid disposal that Copart's systems weren't designed to handle. Most frustrating: German buyers still preferred physical inspections, making the online-only model impossible.

Adair made a crucial decision: instead of forcing the Copart way, he'd adapt to local markets while maintaining core principles. Germany kept physical inspection days but moved bidding online. Spain adopted Copart's technology but maintained local management. Brazil built mega-facilities like the US but created special processes for motorcycle auctions, which comprised 40% of volume.

In 2012, Copart began expanding to the United Arab Emirates, Brazil, Bahrain, Oman, Spain, Ireland and Germany. Each market taught new lessons. In the Middle East, Copart discovered massive demand for luxury vehicles regardless of damage—a Rolls-Royce with frame damage worthless in America might fetch $100,000 from a Dubai buyer. In Brazil, they learned to navigate bureaucracy that made vehicle title transfers take 6 months versus 6 days in the US. In Finland, acquired through Autovahinkokeskus (AVK) in 2018, they found a market where electric vehicle expertise was essential as EVs comprised 30% of new sales.

In 2012, Copart relocated its corporate headquarters from Fairfield, California, to Dallas, Texas. The move was both practical and symbolic. Dallas offered lower costs, better airline connections for international travel, and no state income tax. But more importantly, it signaled Copart's transformation from a California company that happened to operate nationally into a truly global enterprise.

The leadership transition in 2024 marked another inflection point. Jay Adair, after 14 years as CEO, moved to Executive Chairman. Jeff Liaw, the CFO/COO who'd orchestrated much of the international expansion, became CEO. Liaw brought a different perspective: Harvard MBA, Goldman Sachs alumni, fluent in Mandarin. His appointment signaled Copart's recognition that future growth would come from markets where relationships and regulatory navigation mattered as much as operational excellence.

Under Liaw's leadership, Copart has accelerated its international technology investments. The company launched Copart Global, a platform allowing buyers anywhere to bid on vehicles everywhere. A dealer in Mumbai can now bid on cars in Michigan as easily as someone in Detroit. The platform handles currency conversion, shipping logistics, and customs documentation automatically. It's the fulfillment of Willis Johnson's vision of a truly global marketplace, just 40 years later than he imagined.

The numbers validate the international strategy. International revenue grew from $400 million in 2010 to over $760 million in 2024, with margins matching or exceeding US operations. More importantly, international expansion created optionality. When US growth slows, Europe accelerates. When European regulations tighten, South America provides opportunity. The geographic diversification has made Copart more resilient than ever.

But challenges remain. China, the world's largest auto market, remains largely closed to foreign salvage companies. India's potential is enormous but requires navigating complex state-by-state regulations. Electric vehicles pose unique challenges for international shipping due to battery regulations. And everywhere, local competitors are learning from Copart's playbook, improving their operations and technology.

The ownership structure reflects confidence in continued growth. Willis Johnson still owns over 55.8 million shares, a 5.79% stake that keeps him aligned with shareholders. Jay Adair remains one of the largest shareholders, holding 30.6 million shares, or about 3.17% of the company. This concentrated ownership by operators who built the business ensures long-term thinking continues to prevail over quarterly earnings management.

Looking forward, Copart's international expansion is entering a new phase. Rather than just replicating the US model abroad, the company is creating region-specific innovations that sometimes flow back to America. The UK's rapid settlement processes are being tested in California. Germany's environmental documentation systems are improving US compliance. Brazil's motorcycle expertise is helping Copart expand into powersports globally.

The transformation from a Vallejo junkyard to a global platform operating in 11 countries processing millions of vehicles annually is complete. But in many ways, the international story is just beginning. With only 20% of revenue from international markets despite controlling 50%+ market share in several countries, the growth runway remains enormous. The question isn't whether Copart can succeed internationally—they've already proven that. It's how dominant they can become before new competitors or technologies disrupt the model Willis Johnson invented and Jay Adair scaled globally.

IX. Playbook: Business & Investing Lessons

The conference room at Berkshire Hathaway's 2018 annual meeting was packed when Charlie Munger mentioned Copart unprompted during a discussion about business quality. "Willis Johnson is what I call a 'talented fanatic,'" Munger said, borrowing the term from his study of exceptional entrepreneurs. "He took the ugliest business you can imagine—junkyards—and turned it into something beautiful through fanatical execution of simple ideas." The room fell silent. When Munger speaks about specific companies, investors listen.

The first lesson from Copart's playbook is deceptively simple: own, don't lease. While MBA programs teach the virtues of asset-light models and sale-leasebacks, Johnson did the opposite. He bought land when everyone said it was capital inefficient. Today, Copart's real estate portfolio is worth more than many public companies' entire market caps. The land didn't just appreciate—it provided financing flexibility, operational control, and competitive insulation. When COVID hit and IAA's lease costs stayed fixed while revenue plunged, Copart's owned facilities became a massive advantage.

This contrarian approach to capital allocation extends beyond real estate. Johnson had always been cash-strapped with prior business ventures and as a result wanted a very conservative balance sheet. However, he was eventually convinced of the business' resiliency and started to put excess cash to repurchases around 2007. The buyback program has been one of the best capital allocation decisions in corporate America—reducing share count by 30% over 15 years while the stock price increased 10-fold.

The second lesson: network effects in B2B marketplaces are even more powerful than B2C. Everyone understands how Facebook or eBay benefits from network effects, but Copart proves the principle works in the most unlikely places. Every additional insurance company that sends vehicles to Copart attracts more buyers. Every additional buyer drives up prices. Higher prices attract more insurance companies. The flywheel, once spinning, becomes almost impossible to stop. New entrants can't just build better technology—they need to somehow bootstrap both sides of the marketplace simultaneously.

The "copy and improve" innovation strategy deserves special attention. Johnson never claimed to be an inventor. He was a shameless copier who studied Walmart's logistics, McDonald's standardization, Disney's customer service, and Amazon's technology, then adapted each lesson to salvage auctions. But here's the key: he didn't just copy, he contextualized. Walmart's hub-and-spoke distribution wouldn't work for 2-ton vehicles, so Johnson created distributed regional processing. McDonald's standardization was perfect for auction procedures but needed local flexibility for buyer preferences.

The operational excellence that resulted wasn't about any single breakthrough but rather thousands of tiny improvements compounding over decades. Reducing vehicle processing time from 6 hours to 4 hours doesn't sound revolutionary, but multiply that by millions of vehicles and it's transformative. Increasing auction prices by 2% through better photos seems marginal, but compounded over years it doubles profitability. This is what Munger meant by "fanatical"—the relentless pursuit of incremental improvement.

Capital discipline in acquisitions provides another lesson. Copart has acquired dozens of companies but never bet the farm on a single deal. The largest acquisition (NER in 1995) was less than one year's revenue. They've walked away from deals when prices got irrational, even when investment bankers insisted they needed to buy growth. This discipline meant Copart could acquire opportunistically during downturns—buying competitors' facilities during the 2008 crisis at 30 cents on the dollar—rather than desperately during booms.

The cultural elements matter as much as strategy. Copart maintains what employees call "the owner mentality" despite being a $50 billion public company. Managers are compensated based on facility profitability, not corporate metrics they can't control. Willis Johnson's practice of visiting facilities unannounced continues today, with executives regularly working in yards to stay connected to operations. The company promotes almost exclusively from within—Jeff Liaw is the first CEO not to have run a salvage yard.

The approach to technology investment offers lessons for traditional industries facing digital disruption. Copart didn't try to transform overnight into a software company. They maintained operational excellence while gradually layering on technology capabilities. The digital transformation took a decade, allowing the organization to adapt culturally while maintaining profitability. Compare this to competitors who tried massive digital leaps and failed, or traditional retailers who waited too long and got Amazoned.

Risk management through diversification is subtle but crucial. While Copart appears concentrated in salvage auctions, they've actually diversified across multiple dimensions: geography (11 countries), customer types (insurers, dealers, consumers), vehicle categories (cars, motorcycles, boats, RVs), and business models (service fees vs. principal). This diversification happens naturally through scale rather than through forced corporate development initiatives.

The importance of aligned incentives cannot be overstated. With founders and operators maintaining significant equity stakes, Copart makes decisions for long-term value creation rather than quarterly earnings management. They'll accept lower margins to win a strategic contract. They'll invest in technology that won't pay off for years. They'll hold land that generates no current income but provides future optionality. This alignment allows strategic patience that purely professional management rarely exhibits.

The durability of the business model provides perhaps the most important lesson. In an era of constant disruption, Copart has maintained competitive advantages for 40 years. The moat hasn't been static—it evolved from operational excellence to scale to technology to network effects—but it's consistently widened. This teaches that sustainable competitive advantages aren't about finding one unassailable moat but rather continuously building new moats while maintaining existing ones.

For investors, Copart demonstrates the power of investing in businesses with multiple ways to win. If the US market saturates, international provides growth. If vehicle technology changes, Copart's platform adapts. If regulations tighten, Copart's compliance infrastructure becomes more valuable. If competition intensifies, operational excellence and scale provide protection. It's not about predicting the future but rather owning businesses resilient to multiple futures.

The financial metrics validate these lessons. From fiscal 2014 to 2024, revenue grew from roughly $1.16 billion to over $4.24 billion, a compound annual growth rate around 13.8%. Copart's net margin of 33.45% in an industry traditionally considered low-margin proves that operational excellence can transform fundamental economics. Return on invested capital consistently sits around 20%, remarkable for an asset-heavy business.

The Copart playbook ultimately teaches that great businesses aren't built through brilliant strategy alone but through decades of consistent execution. It's not about disrupting industries through venture-funded blitzscaling but rather gradually accumulating advantages that compound over time. It's not about financial engineering but about operational excellence. And it's not about predicting the future but rather building a business model resilient to whatever future arrives.

X. Analysis & Bear vs. Bull Case

The Bull Case: An Unstoppable Compounding Machine

Standing in Copart's Dallas headquarters, you can watch real-time feeds from auctions happening simultaneously in Berlin, São Paulo, and Dubai. Every few seconds, another vehicle sells, another fee hits the revenue line, another data point strengthens the network effect. The bulls see this as just the beginning of a multi-decade growth story that could make today's $47 billion market cap look quaint in retrospect.

The financial trajectory validates their optimism. From fiscal 2014 to 2024, revenue grew from roughly $1.16 billion to over $4.24 billion, a compound annual growth rate around 13.8%. Operating margins have expanded from 27% to 37%, and net margins have held at roughly 32%. This isn't growth through acquisition or financial engineering—it's organic expansion with improving unit economics. Free cash flow in fiscal 2024 came in at roughly $962 million, about 22.7% of revenue.

The balance sheet provides enormous flexibility for whatever comes next. The balance sheet is a fortress: over $4.38 billion in cash & short-term investments, and negligible long-term debt. This isn't idle cash—it's strategic optionality. Copart could acquire IAA if antitrust allowed. They could expand into adjacent markets like heavy equipment or commercial vehicles. They could accelerate international expansion. Or they could simply return it to shareholders through continued buybacks.

Vehicle complexity trends create a powerful secular tailwind. Modern cars are computers on wheels—thousands of sensors, dozens of processors, advanced materials like carbon fiber and aluminum. A minor collision that would have been repairable in a 1990s Honda might total a 2024 Tesla. Electric vehicles amplify this trend: battery packs cost $15,000+ to replace, turning even moderate damage into total losses. Every increase in vehicle complexity expands Copart's addressable market.

The international opportunity remains massively underpenetrated. Copart generates just 20% of revenue internationally despite most of the world's vehicles being outside the US. India's vehicle parc is growing 8% annually. Southeast Asia is motorizing rapidly. Africa represents a completely untapped market. Even developed markets offer room for growth—Copart has less than 20% share in Germany, minimal presence in France, and hasn't entered Italy or Spain meaningfully. The runway for international expansion could last decades.

Technology disruption, rather than threatening Copart, might actually strengthen its position. Autonomous vehicles will still crash—perhaps less frequently, but when they do, the sensor arrays and computing systems will make repairs prohibitively expensive. Shared mobility might reduce vehicle ownership, but fleet vehicles drive more miles and wear out faster, increasing turnover. Electric vehicles eliminate oil changes but introduce battery degradation, creating a new category of total losses.

The competitive dynamics keep improving. Small players can't match Copart's technology investments. Private equity-owned competitors struggle with debt service. Even IAA, the only legitimate rival, trades at a significant multiple discount, suggesting the market sees widening competitive gaps. Meanwhile, Copart's network effects strengthen daily—every additional buyer and seller makes the platform more valuable.

ESG trends favor Copart's model. Vehicle recycling reduces environmental impact versus manufacturing new cars. Copart's digital auctions eliminate millions of miles of buyer travel. Their parts redistribution extends vehicle life cycles. As environmental regulations tighten globally, Copart's infrastructure for proper fluid disposal and parts recycling becomes more valuable. They're not just running auctions—they're enabling the circular economy for automobiles.

Management quality remains exceptional under Jeff Liaw. He combines operational understanding from his COO tenure with financial sophistication from his CFO role. The board includes Willis Johnson and Jay Adair, ensuring institutional memory and long-term thinking. Insider ownership remains high, aligning management with shareholders. The culture of operational excellence that Johnson instilled appears intact despite the leadership transition.

The Bear Case: Peak Valuation Meets Structural Headwinds

The bears look at the same Dallas headquarters and see a different picture: a company trading at nosebleed valuations just as its core market faces unprecedented disruption. At roughly $47 a share, Copart changes hands at about 30 times trailing earnings and 22 times EBITDA, with a free cash flow yield near 2%. These multiples assume continued growth and margin expansion, but what if the opposite occurs?

The valuation implies perfection. At 30x earnings, Copart trades at a premium to high-growth software companies despite being fundamentally a logistics and real estate business. The market values Copart at over $200,000 per employee, suggesting extraordinary productivity expectations. Any disappointment—a quarterly earnings miss, margin compression, slowing growth—could trigger multiple compression that overwhelms operational performance.

Autonomous vehicles represent an existential threat that bulls underestimate. Yes, AVs will still crash, but frequency matters enormously. If accident rates drop 50%, Copart's addressable market shrinks proportionally. Worse, AV fleets might vertically integrate repair operations, cutting out salvage auctions entirely. Waymo or Tesla could handle their own damaged vehicles, depriving Copart of high-value inventory.

Insurance company concentration creates hidden risk. Copart's top 10 insurance clients likely represent 60%+ of volume. If State Farm or Geico decided to internalize salvage operations or squeeze auction fees, Copart would have limited recourse. The insurance industry is consolidating, increasing buyer power. Meanwhile, insurtech startups like Lemonade might disrupt traditional claims processing, potentially bypassing salvage auctions entirely.

The competitive landscape could shift rapidly. Ritchie Bros' acquisition of IAA created a formidable competitor with complementary capabilities in heavy equipment and commercial auctions. Amazon or eBay could enter the market—they already have the technology platform and buyer networks. Chinese companies like Alibaba have shown interest in automotive marketplaces. Even Facebook Marketplace handles individual vehicle sales. The barriers to entry might be lower than bulls assume.

International expansion faces mounting headwinds. Each market requires local adaptation that reduces Copart's scale advantages. Regulatory compliance becomes increasingly complex—GDPR in Europe, data localization laws in India, environmental regulations everywhere. Currency fluctuations eat into returns. Political risk is rising with deglobalization trends. The easy international wins might be behind Copart, not ahead.

Technology disruption could come from unexpected angles. Blockchain-based vehicle history tracking might eliminate information asymmetries that create value for intermediaries. AI-powered damage assessment could allow insurance companies to make total-loss decisions without physical inspection. 3D printing might make previously unrepairable vehicles fixable. Quantum computing could optimize logistics in ways that eliminate Copart's operational advantages.

Market saturation is a mathematical inevitability. Copart already processes millions of vehicles annually. US vehicle sales have plateaued around 17 million units. Average vehicle age is extending as quality improves. Miles driven per capita is declining with remote work. The core US market that drives 80% of revenue might be ex-growth, forcing Copart to rely entirely on margin expansion and international for growth.

The real estate asset that bulls tout could become a liability. Copart owns thousands of acres in locations chosen for 20th-century logistics patterns. If processing becomes more distributed or digital, these facilities could become stranded assets. Commercial real estate is facing structural headwinds with remote work and e-commerce. The land might be worth less than balance sheet values suggest, especially in secondary markets.

Management transition adds uncertainty. Jeff Liaw is untested as CEO during a downturn. The company hasn't faced a real crisis since 2008 when Willis Johnson was running things. The next generation of leadership lacks the founder's entrepreneurial DNA. Culture can erode quickly in large organizations, especially when the founder's presence fades. Copart might be one management misstep away from becoming another formerly great company that lost its way.

The Synthesis: A Great Company at a Full Price

The truth, as usual, lies between extremes. Copart is an exceptional business with a proven model, dominant market position, and secular tailwinds. The operational excellence is real. The network effects are durable. The international opportunity exists. But at 30x earnings, much of this excellence is priced in. The stock requires continued execution perfection and favorable industry dynamics to justify its premium.

For long-term investors, the question isn't whether Copart is a good business—it clearly is—but whether it's a good investment at current prices. The margin of safety that Benjamin Graham advocated is absent. The asymmetry tilts negative: more things can go wrong than right when expectations are this high. Yet quality compounds, and Copart's quality is undeniable.

The lesson for students of business is clearer than the investment decision: Copart demonstrates how operational excellence, sustained over decades, can transform even the most mundane industry into a compounding machine. Whether the stock is a buy, sell, or hold depends on your time horizon, risk tolerance, and belief in management's ability to navigate the disruptions ahead. But the business itself—built from a junkyard into a digital marketplace—stands as a testament to American entrepreneurship and the power of fanatical execution.

XI. Epilogue & Reflections

Willis Johnson sits in his home office in Nashville, Tennessee, 2,000 miles from the Vallejo salvage yard where Copart began. At 77, he's worth over $2.5 billion, but the office looks like it belongs to a small business owner: functional furniture, family photos, and a white board covered with hand-drawn diagrams of operational improvements. When asked about his legacy, Johnson doesn't mention the stock price or his wealth. Instead, he talks about the time a single mother in Louisiana thanked him because Copart's online auction got her $3,000 more for her totaled car than a traditional salvage yard would have paid.

This gap between financial success and personal motivation explains much about Copart's journey. Johnson didn't set out to build a billion-dollar company. He wanted to organize junkyards better. He didn't pursue an IPO for wealth but for capital to serve more customers. He didn't expand internationally for empire building but because buyers in other countries deserved the same transparent marketplace Americans enjoyed. The money followed the mission, not the other way around.

An investment in Willis' Copart in 1994 has been a veritable 150-bagger!! A $10,000 investment at the IPO would be worth $1.5 million today, not counting dividends (though Copart has never paid any, preferring buybacks). But the real returns came from something harder to quantify: proving that operational excellence beats financial engineering, that growing steadily beats growing fast, and that focusing on customers beats focusing on competitors.

The contrast with contemporary business culture is stark. While Silicon Valley celebrates disruption, Copart succeeded through incremental improvement. While private equity firms leverage companies to the hilt, Copart maintains a fortress balance sheet. While tech startups lose money for years chasing growth, Copart has been profitable every year since going public. It's a reminder that there are multiple paths to business success, and sometimes the tortoise beats the hare.

The organizational culture Johnson created continues to perplex business school professors. How does a company maintain entrepreneurial energy at $4 billion in revenue? How do you preserve operational discipline across 200+ facilities? How do you keep employees motivated when the founder's force of personality is no longer present daily? The answer seems to be that culture, once deeply embedded, has remarkable staying power. The thousands of employees Johnson trained, who then trained others, created an institutional memory that transcends any individual.

Yet Copart also demonstrates the limits of even the best business models. At some point, growth slows, competition intensifies, and technology shifts. The company that disrupted physical auctions with online bidding might itself be disrupted by blockchain, AI, or technologies not yet invented. The land that provided competitive advantage might become an anchor as business models evolve. The insurance relationships that seemed permanent might prove temporary as the entire concept of vehicle ownership transforms.