Coupang: The Rocket Delivery Revolution

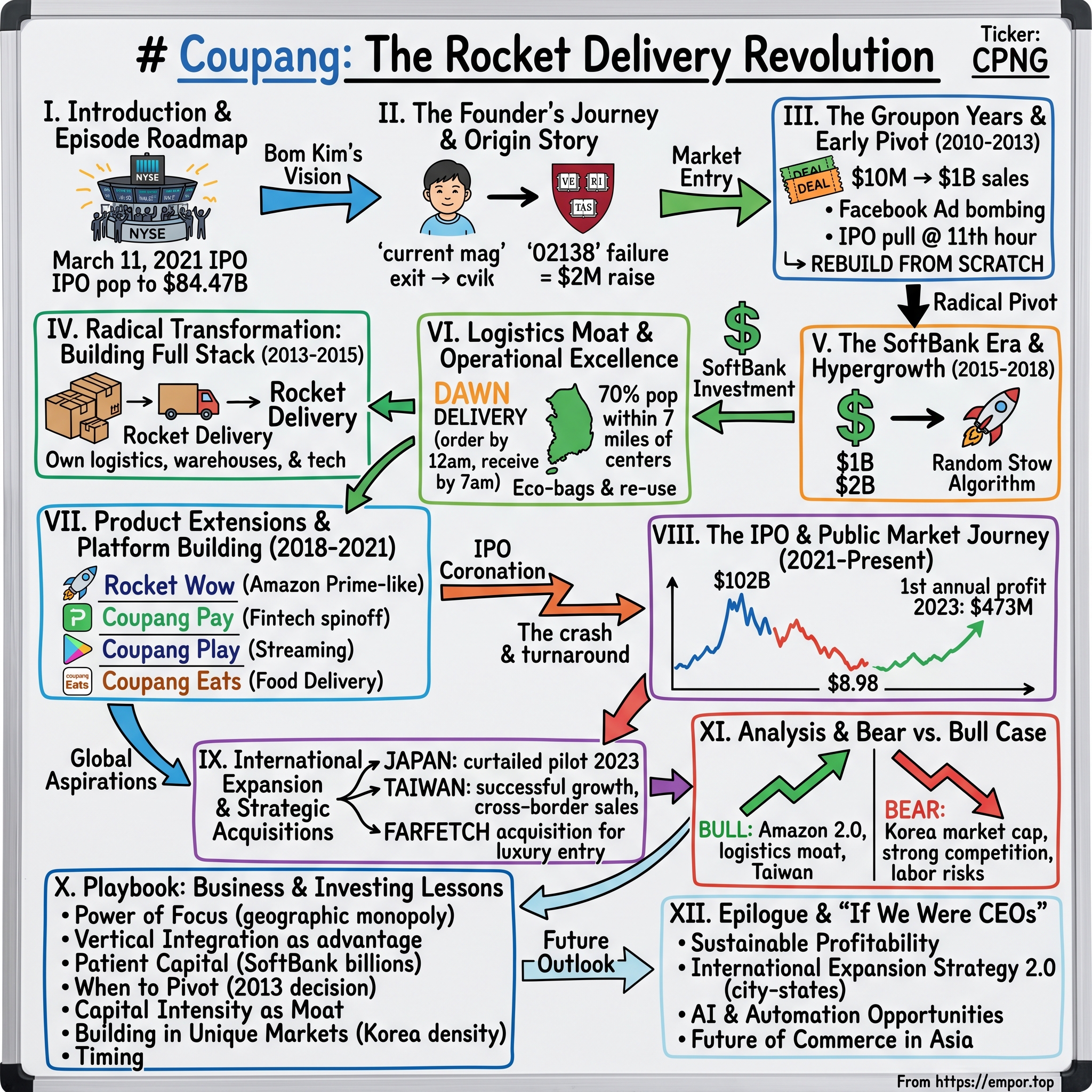

I. Introduction & Episode Roadmap

Picture this: It's March 11, 2021, and the New York Stock Exchange floor is buzzing with an energy not seen since the pandemic began. A Korean e-commerce company most Americans have never heard of is about to go public. When the opening bell rings, Coupang's stock doesn't just pop—it explodes, soaring 41% on its first day to create $84.47 billion in market value. For a brief, shining moment, this company founded by a Harvard dropout is worth more than Target, eBay, or any European retailer. The question hanging in the air: How did a company operating in a country smaller than Kentucky build something this massive?

The answer begins with Bom Kim, a soft-spoken Korean-American who returned to Seoul in 2010 with $2 million and an audacious dream. While Jeff Bezos had the entire continental United States as his canvas, Kim would attempt something arguably harder—building the Amazon of South Korea in a market 1% the size of the US, with established conglomerates like Samsung and LG watching his every move.

What unfolds is a story of radical pivots, near-death experiences, and ultimately, the creation of something unprecedented in global e-commerce. Coupang didn't just copy Amazon's playbook; it rewrote it for Asian density, creating an infrastructure so sophisticated that 70% of South Korea's population now lives within seven miles of a Coupang distribution center. Items ordered before midnight arrive before breakfast. Fresh groceries ordered at 11:59 PM sit on doorsteps by 7 AM.

This is the story of how one company transformed an entire nation's shopping habits, burned through $3.4 billion in venture capital, survived a canceled IPO, and emerged as the definitive case study for building e-commerce dominance in small, dense markets. It's about the brutal math of unit economics, the unexpected advantages of geographical constraints, and why sometimes the best business strategy is to do the thing everyone says is impossible.

We'll trace Coupang's journey from its Groupon-clone origins through its transformation into a logistics powerhouse, examining the pivotal moments when conventional wisdom said "stop" but Bom Kim said "accelerate." We'll explore how SoftBank's billions enabled infrastructure investments that would make even Amazon jealous, and why the company's failed expansion into Japan might have been its most valuable lesson.

But this isn't just a story about South Korea or even Asia—it's about the future of commerce itself, where speed isn't a luxury but table stakes, where vertical integration beats platforms, and where the winners aren't necessarily the first movers but the ones willing to rebuild everything from scratch.

II. The Founder's Journey & Origin Story

The year is 1985, and seven-year-old Bom Kim is leaving Seoul for Massachusetts, his father's Hyundai Construction job taking the family to America. It's a common story for Korean families of that generation—sacrifice everything for education and opportunity. But unlike many immigrant tales, this one would come full circle in the most unexpected way.

At boarding school in Massachusetts, Kim displayed the classic overachiever tendencies that would later define his business approach. Harvard College followed, where in 1998 he launched his first venture: Current Magazine, a publication with the tagline "for students, written by students." The concept was simple but prescient—aggregate student voices, create authentic content, build a media brand around generational identity. When Newsweek acquired it in 2001, Kim had his first exit, his first taste of building something from nothing. The Harvard Business School years tell you everything about Kim's mindset. Just six months into the program, he dropped out, determined to make it on his own. "I had a belief when I was in grad school that I had a very short window to really make something that had an impact," he would later tell CNBC. This wasn't impulsiveness—it was urgency. The same urgency that would later drive him to cancel an IPO at the eleventh hour and rebuild his entire company from scratch.

Between Harvard and Coupang came another venture: 02138, an alumni magazine named after Cambridge's zip code. He raised $4 million to fund 02138 and started Coupang after it folded. The magazine experiment taught Kim valuable lessons about content, community, and ultimately, the limitations of media businesses. When it shuttered in 2008, Kim was ready for something bigger. The initial funding was modest but strategic. Bill Ackman was a "day one investor" in Coupang, investing personally as early as 2010, with Reuters mentioning him as an investor by 2014. Along with Stanley Druckenmiller and other Harvard connections, Kim raised his initial $2 million—seed money that would eventually transform into one of the decade's most spectacular venture returns. The company name itself was perfect marketing: "Coupang"—a play on Coupon and the Korean onomatopoeia for "fun" or "surprise". In a country where wordplay matters and brand names stick, Kim had chosen something memorable, pronounceable, and inherently positive. It suggested both value and delight, two qualities that would become central to the company's identity even as its business model transformed completely.

By 2010, Kim had his funding, his name, and most importantly, his market. South Korea was the perfect laboratory for e-commerce innovation: densely populated, digitally connected, culturally homogeneous enough for standardized solutions but sophisticated enough to demand excellence. What Kim didn't know yet was that his first business model would be completely wrong—and that being wrong would teach him exactly what needed to be built.

III. The Groupon Years & Early Pivot (2010–2013)

The Seoul of 2010 was experiencing its own version of the global daily deals craze. Groupon had just rejected Google's $6 billion acquisition offer, LivingSocial was raising hundreds of millions, and every market worldwide was spawning clones. Kim's Coupang entered this fray not as an innovator but as a fast follower, launching a Korean version of the group-buying model that promised merchants customer traffic and consumers unbeatable discounts.

In 2010, their first year of business, Coupang generated $10 million in sales with over 3 million customers. These numbers were extraordinary for a startup's first year, but they masked a fundamental problem. The business was built on a house of cards: merchants losing money on every deal, customers trained to expect 50% discounts, and Coupang stuck in the middle taking its 15% cut of an unsustainable transaction.

The genius move came from Facebook. Coupang became one of the first Facebook advertisers in Korea when the platform was still finding its footing in Asia. The CPMs were absurdly cheap—so cheap that Coupang could show every Korean Facebook user 72 ads per month. This wasn't sophisticated targeting; it was carpet bombing. But in 2010 Korea, where social media adoption was exploding and e-commerce trust was still building, volume worked better than precision.

Within three years, Kim said the company crossed $1 billion in sales and was on the cusp of an initial public offering. The transformation from $10 million to $1 billion in three years is the kind of growth that makes venture capitalists weak in the knees. Despite stiff competition from TicketMonster and Groupon Korea, Coupang became the #1 player in the space, with cash flow positive operations fueling aggressive expansion.

But Kim was increasingly uncomfortable. The model worked financially—customers flocked to deals, merchants grudgingly participated, Coupang collected its fees. Yet something felt fundamentally broken. "In the traditional sense of commerce, you needed something so you went shopping. But in social commerce, you see a good bargain and suddenly you need it", Kim observed. This inversion of need and desire created a business of impulse rather than intention.

The problems were structural. Selling products and services to highly price sensitive customers in a gamified way with pressure to close a sale hardly created lasting customer satisfaction. Merchants discovered that deal-seekers rarely converted to full-price customers. The steep discounts—often 50% or more—meant restaurants and service providers lost money on every transaction, hoping to make it up in future visits that never materialized.

By 2013, Coupang had everything a company needs for a successful IPO: billion-dollar revenues, market leadership, positive cash flow, a proven management team. Investment bankers were circling, valuations were being discussed, and the roadshow was being planned. This was the moment every founder dreams of—the validation, the liquidity, the global recognition.

But at the eleventh hour, he pulled the deal and radically changed the business model, convinced he could build something better. "We had to ask ourselves: 'Was the business we had built, were the services and experiences that we were providing ... creating that kind of world where the customers we love, their jaws would drop?'" said Kim.

The answer was no. And that "no" would cost him his IPO, his entire business model, and nearly his company. But it would also set the stage for one of the most dramatic pivots in e-commerce history.

IV. The Radical Transformation: Building the Full Stack (2013–2015)

The decision to cancel the IPO in 2013 must have felt like professional suicide. Here was Bom Kim, sitting on a billion-dollar business, telling bankers, investors, and employees that he was walking away from a liquidity event to rebuild everything from scratch. In Silicon Valley, pivots are celebrated. In Korea's more conservative business culture, they're often seen as admissions of failure.

Kim decided to start over; this time reinventing Coupang as an end-to-end shopping platform designed to manage the full customer journey from desktop to door. This wasn't a pivot—it was a demolition. The daily deals business that had generated a billion dollars in sales would be gradually wound down. The marketplace model would be de-emphasized. Instead, Coupang would become something that didn't really exist anywhere in the world: a fully integrated e-commerce company that owned everything from the moment a customer clicked "buy" to the moment a package arrived at their door.

The audacity of this move becomes clear when you understand what Kim was proposing to build. That included creating Coupang's own UPS-style logistics business, Rocket Delivery, intended to "delight" customers and improve South Korea's disjunctured postal system. South Korea in 2013 had a functioning postal system and multiple third-party logistics providers. Building your own delivery network was like Samsung deciding to build its own highways because it didn't like the existing roads.

But Kim had noticed something others hadn't. South Korea's unique geography—70% mountains, with most of the population concentrated in ultra-dense urban clusters—created logistics challenges that generic solutions couldn't solve. The last-mile problem that plagued American e-commerce was actually a last-100-meters problem in Seoul's vertical cities of apartment towers. Traditional logistics companies, designed for moving packages between businesses, were ill-equipped for the complexity of residential delivery in a country where most people lived in secured high-rises.

The capital requirements were staggering. Warehouses had to be built or leased. Thousands of drivers had to be hired and trained. A technology stack had to be created from scratch to orchestrate this ballet of atoms. Inventory had to be purchased and held. This wasn't the asset-light marketplace model that investors loved—it was the opposite, a capital-intensive, operationally complex, margin-compressing strategy that looked like business suicide.

"What seemed like a curse at that time—that we had to build this entire infrastructure, and build the technology to integrate it all, end-to-end, by ourselves, from scratch—ended up becoming a huge blessing," Kim would later reflect. But in 2013-2014, it looked more like a curse than a blessing. The company was burning cash at an alarming rate. The complexity of coordinating warehouses, inventory, drivers, and technology was overwhelming. Competitors with leaner models were growing faster with less capital.

The first version of Rocket Delivery was humble: a promise to deliver within three days, then two, then one. But even this basic promise required revolutionary operational changes. Coupang had to predict what customers would buy, position inventory close to population centers, and create routing algorithms that could handle Korea's addressing system (which, until 2014, didn't use street names but rather a complex system of district and building numbers).

The real innovation wasn't speed—it was reliability. In a market where delivery promises were more suggestions than commitments, Coupang started guaranteeing delivery windows. If they said tomorrow, it would be tomorrow. This required not just logistics infrastructure but a fundamental rethinking of how e-commerce operations worked. Every process had to be redesigned with the delivery promise as the constraint.

By 2015, the transformation was showing early signs of success, but the company was running dangerously low on capital. The pivot had consumed hundreds of millions of dollars, and while customer satisfaction metrics were improving dramatically, the economics were brutal. Coupang needed a investor with deep pockets and a long time horizon—someone willing to bet billions on the idea that in e-commerce, customer experience would ultimately trump everything else.

That investor was about to arrive from Tokyo, checkbook in hand.

V. The SoftBank Era & Hypergrowth (2015–2018)

June 2015 marked the beginning of Coupang's transformation from ambitious startup to massively funded rocket ship. SoftBank announced a definitive agreement to invest $1 billion in Coupang, bringing the total amount of funding raised by Coupang over the past year to nearly $1.5 billion. The round valued the Korean company at $5 billion.

For Masayoshi Son, Coupang represented exactly the kind of bet he loved: a dominant local player in a wealthy market, led by a visionary founder, attacking a massive TAM with a differentiated approach. "SoftBank aims to grow by investing in Internet companies around the world and supporting disruptive entrepreneurs who share a common vision to contribute to people's lives through the Information Revolution", Son said at the time.

The timing was perfect. Coupang's infrastructure build-out was consuming enormous capital just as SoftBank was looking to deploy its war chest. Mobile sales already accounted for over 75 percent of the company's revenue and over 85 percent of its total traffic. This wasn't just e-commerce; it was mobile-first commerce in a country where smartphone penetration exceeded 85%.

With SoftBank's billion dollars, Kim accelerated everything. Rocket Delivery service became possible via 200 warehouses that were approximately 20 million sq. ft across the country, storing approximately 5.3 million types of products with an efficient storage system called Random Stow Algorithm. About 1.7 million Rocket Delivery products were sent out from the logistic centers on a daily basis.

The Random Stow Algorithm was particularly clever. Instead of organizing products by category (all shoes together, all books together), Coupang scattered identical items across multiple locations in each warehouse. This counterintuitive approach meant that any picker could find any item quickly, eliminating bottlenecks and dramatically improving fulfillment speed. It was the kind of operational innovation that only made sense at massive scale—and SoftBank's money enabled that scale.

By 2018, the company was ready for another injection. SoftBank's Vision Fund invested $2 billion at a $9 billion post-money valuation, taking Coupang's total raised to $3.4 billion. Its last round before this was the $1 billion investment from SoftBank in 2015. Kim claimed the company was "approaching" $5 billion in revenue for 2018 with 70 percent annual growth.

The Vision Fund investment came at a complicated time—just days after a CIA report concluded that Saudi Crown Prince Mohammed bin Salman ordered the murder of journalist Jamal Khashoggi. But Kim was focused on the business: "The Vision Fund is a visionary fund [and] we're proud to be selected to work in partnership with it".

What SoftBank's billions enabled was nothing short of revolutionary. More than 5,000 drivers delivered 99.3% of orders in less than 24 hours. 70% of Korean citizens lived within 10 minutes of a Coupang logistic center. The infrastructure wasn't just impressive—it was transformative. Korea's e-commerce landscape was being reshaped around Coupang's capabilities.

The relationship between Son and Kim went beyond investor and founder. Both were outsiders who had returned to their Asian roots after American educations. Both believed in the power of capital to accelerate transformation. And both were willing to endure massive losses in pursuit of market dominance. It was a partnership that would culminate in one of the most spectacular IPOs of the decade—but not before years of bleeding red ink.

VI. The Logistics Moat & Operational Excellence

The heart of Coupang's operation beats in Daegu, where at 3 AM, a ballet of precision unfolds. Thousands of packages move through conveyor systems, sorted by algorithms that know not just where each item needs to go, but when it needs to arrive, who will deliver it, and what route they'll take. This isn't just a warehouse—it's a glimpse into what happens when you rebuild logistics from first principles for the smartphone age.

Rocket Delivery became Coupang's signature: items ordered before midnight delivered overnight by Coupang's own delivery personnel. But the real innovation was Dawn Delivery—enabling shoppers to place orders as late as midnight and have them delivered to their door before 7AM. Think about the operational complexity: a customer places an order at 11:59 PM for toothpaste, kimchi, and a phone charger. By 6 AM, all three items—pulled from different sections of a warehouse, packed by night-shift workers, and loaded onto trucks in optimized routes—sit outside their apartment door.

The unit economics only worked because of Korea's density. In the US, Amazon might drive 20 miles between suburban deliveries. In Seoul, a Coupang driver might make 20 deliveries in a single apartment complex. The elevators become the constraint, not the distances. This density advantage meant Coupang could offer services that would bankrupt American e-commerce companies. Rocket Fresh transformed grocery shopping entirely. Similar to Rocket Delivery, Rocket Fresh delivers fresh foods overnight—users can receive the food by 7am if they order before midnight. The service covers up to 8,500 kinds of foods. The "Rocket Fresh" service reached 87,000 boxes daily by 2019, and by 2020, Coupang was the only e-commerce firm able to deliver fresh food within 24 hours across the country.

The technology infrastructure powering this was staggering. Coupang's data platform helps customers discover more than 300 million items per day and renders search results in a fraction of a second. AI and machine learning predict consumer demand and forward deploy products into fulfillment and delivery networks before they're needed. The company then leverages technology to dynamically route hundreds of millions of orders efficiently.

But perhaps the most impressive innovation was human. Coupang's delivery staff—renamed from "Coupangman" to "Coupangfriend" in 2020 to reflect the growing number of female drivers—became the face of the company. On average, they deliver 50 to 60 packages per day, equipped with personal digital assistants that show optimized routes, display returns to collect, and even remind them when to take breaks.

The environmental innovation was equally impressive. Coupang's re-engineered fulfillment process eliminated cardboard boxes in over 75% of parcels. For Rocket Fresh, they introduced Zero Packaging—delivering in reusable eco-bags that are collected after each delivery. When Rocket Wow subscribers order Rocket Fresh, they can choose Rocket Fresh Eco, where foods arrive in these bags instead of paper boxes.

The operational infrastructure spans over 25 million square feet across over 30 cities—a footprint of over 400 football fields in a country that is 1% the size of the US geographically. This density advantage turned into a competitive moat that would prove nearly impossible for competitors to replicate.

By 2019, one in every two Koreans had downloaded Coupang's mobile application. The company had created something unprecedented: a logistics network so efficient that traditional retail couldn't compete, so reliable that customers planned their lives around it, and so embedded in daily routines that it became infrastructure itself. This wasn't just e-commerce—it was the physical manifestation of the internet's promise of instant gratification.

VII. Product Extensions & Platform Building (2018–2021)

The playbook was clear by 2018: dominate logistics, then layer services on top. Amazon had shown the way with Prime, but Coupang would execute the strategy with Korean characteristics—faster, denser, more integrated. The question wasn't whether to build an ecosystem but how quickly they could lock in customers before competitors caught up.

Rocket Wow launched in 2019 as Coupang's answer to Amazon Prime. For a flat monthly fee—initially KRW 2,900, later adjusted to KRW 4,990 in December 2021—members got unlimited free shipping for millions of products with no minimum spend. But this was just the beginning. Members also enjoyed Dawn Delivery and Same-Day Delivery shipping options, free unlimited returns for 30 days, and Rocket Fresh groceries. By February 2019, there were 1.6 million Rocket Wow Club members; by 2021, it's estimated that 32% of Coupang users were subscribed.

The genius of Rocket Wow wasn't the price—it was the psychology. Once customers paid a monthly fee, every non-Coupang purchase felt like wasted money. The subscription created a mental switching cost that turned occasional shoppers into daily users. Millions of customers were buying from Coupang more than 50 times per year, a frequency that made the service less like shopping and more like a utility. Coupang Pay became the stealth weapon. In mid-2020, the company spun off Coupang Pay as a separate fintech subsidiary. By the end of 2020, Coupang Pay was the second most widely used pay system in Korea, with settlement turnover of KRW 25 trillion. The service grew to 10 million registered users, making it the third biggest player in the local market after Kakao Pay and Naver Pay.

The brilliance of Coupang Pay wasn't just convenience—it was data. Every transaction generated insights about spending patterns, product preferences, and customer behavior. This data fed back into Coupang's recommendation algorithms, inventory planning, and marketing strategies. The payment system became a intelligence-gathering network disguised as a checkout feature. In July 2020, Coupang acquired the assets of Singaporean streaming service HOOQ to form Coupang Play, launched in December 2020. The streaming service was included as part of Coupang's Rocket Wow paid membership—another layer of value to prevent churn. By August 2023, Coupang Play had 6.34 million subscribers with the fastest year-on-year subscriber growth compared to other streaming platforms. After adding sports broadcasting, it reached 8.05 million active users by January 2024.

Coupang Eats rounded out the ecosystem. Leveraging the technology and infrastructure built for Rocket Delivery, Coupang entered food delivery with a crucial difference: 100% of deliveries were handled by drivers directly contracted by Coupang, not gig workers or restaurant employees. This control meant consistent service quality, real-time tracking, and the ability to handle multiple orders efficiently.

The genius of the platform strategy was how each service reinforced the others. Rocket Wow members got free delivery on Coupang Eats orders. Coupang Pay users earned rewards across all services. Coupang Play kept customers engaged even when they weren't shopping. Every touchpoint generated data that improved every other service.

By 2021, the ecosystem was complete. A Korean consumer could wake up to fresh groceries delivered before 7 AM, pay for their morning coffee with Coupang Pay, order lunch through Coupang Eats, receive an afternoon package via Rocket Delivery, and fall asleep watching Coupang Play. This wasn't just market share—it was life share.

VIII. The IPO & Public Market Journey (2021–Present)

March 11, 2021, was supposed to be Coupang's coronation. The company's stock began trading at $63.50 apiece on the New York Stock Exchange, nearly double the $35 IPO price. For a brief, shining moment, the market cap touched $102.2 billion before closing at $49.25 for an $84.47 billion valuation—still a 41% first-day pop that made it the largest US IPO of the year.

The offering raised nearly $4.6 billion, with the company selling 130 million shares after increasing both the price range (from $32-34 to $35) and the share count (from 120 million) due to overwhelming demand. Goldman Sachs, Allen & Co, JPMorgan, BofA Securities and Citigroup led the underwriting syndicate. At the closing price, Coupang was valued higher than Target, eBay, or any European retailer—validation for a company that had operated in the shadow of Korea's chaebols.

For Bom Kim, now worth $8.6 billion according to the Bloomberg Billionaires Index, it was vindication for the 2013 pivot that nearly killed the company. "The IPO... made it the first South Korean company to list directly on the New York Stock Exchange", a symbolic victory for Korean tech. Kim owned approximately 10.2% of the company post-IPO, with SoftBank holding one-third, Greenoaks Capital 16.6%, Maverick Holdings 6.4%, Rose Park Advisors 5.1%, and BlackRock 2.1%.

The pandemic had turbocharged results. 2020 revenue nearly doubled to $12 billion, though the company still reported a net loss of about $475 million—an improvement from the $699 million loss in 2019. More importantly, Coupang had crossed several psychological thresholds: half of Korea's population had the app on their phones, customers were spending 346% more than they had in 2017, and market share had expanded from 18.1% in 2019 to 24.6% in 2020.

But the public markets are cruel teachers. By May 2022, shares had collapsed to just $8.98—down 74% from the IPO price and 87% from the intraday high of $69. The crash reflected multiple factors: global tech selloff, concerns about profitability, labor controversies following worker deaths, and questions about whether Korea's market was large enough to justify the valuation. The turnaround came in the third quarter of 2022, when Coupang posted its first-ever quarterly profit. By 2023, the transformation was complete: the company recorded its first annual operating profit of $473 million on revenue of $24.4 billion. This wasn't just profitability—it was validation of the entire strategy. The company that had burned through billions building infrastructure was finally harvesting the returns.

The numbers told a story of operational leverage finally kicking in. Active customers surpassed 21 million by Q4 2023, up 16% year-over-year. The WOW membership program reached 14 million paid members, a 27% gain. More importantly, total net revenue per Active Customer increased from $284 to $303, proving that the ecosystem strategy was working—customers weren't just staying, they were spending more.

Current ownership remains concentrated among long-term believers. As of the latest filings, SoftBank owns approximately 29-33% of the company, having sold portions of its stake but remaining the largest shareholder. Greenoaks Capital holds 16.6%, Maverick Holdings 6.4%, Rose Park Advisors 5.1%, BlackRock 2.1%, and CEO Bom Kim maintains approximately 10.2%.

The stock has recovered somewhat from its 2022 lows, trading in the $20-30 range through 2024-2025, giving the company a market cap of approximately $50-60 billion—still below the IPO day peak but respectable for a company that's now consistently profitable. The journey from $8.98 to sustainable profitability represents one of the great comeback stories in tech, proving that sometimes the market's impatience is an opportunity for those who understand the long game.

IX. International Expansion & Strategic Acquisitions

The dream of every successful e-commerce company is geographic expansion. Amazon conquered country after country. Alibaba spread across Southeast Asia. For Coupang, with its infrastructure-heavy model perfected for Korean density, the question wasn't whether to expand but where they could replicate their formula. Japan was the obvious first choice. Started trial operations in June 2021, just three months after the IPO when confidence and capital were at their peak. The approach was different from Korea—instead of building the full infrastructure, Coupang Japan focused on quick commerce, promising 10-minute delivery of groceries and daily essentials in Tokyo's Meguro and Setagaya districts.

The failure was swift and decisive. By March 2023, less than two years after launch, Coupang announced it would withdraw from Japan entirely. "We have decided to curtail our pilot in Japan which will allow Coupang to focus our resources on growth opportunities in Korea and Taiwan that we expect to generate more value for customers and stakeholders," the company said in a carefully worded statement.

The reasons for failure were structural. Japan already had Amazon with 20% market share and Rakuten as the homegrown champion. The convenience store culture—with 7-Elevens and FamilyMarts on every corner—made quick delivery less revolutionary. Japanese consumers, particularly the 29% of the population over 65, were wary of new services. The "Satori generation" of young people who shun materialism didn't respond to Coupang's value proposition.

But the real lesson was deeper: Coupang's model wasn't portable. The infrastructure investments that created a moat in Korea became an anchor in markets where the company couldn't achieve dominant share quickly. Without the density, without the scale, without the ability to amortize fixed costs across millions of daily deliveries, the economics collapsed.

Taiwan told a different story. Launched in October 2022 with Rocket Delivery and Rocket Overseas, Coupang found a market more receptive to its offering. Free delivery for orders over NT$490 (about $16 USD) resonated with Taiwanese consumers. The Coupang app became the most downloaded app in Taiwan in Q2 2023. By November 2023, the company was opening its second logistics center with a third planned for 2024.

The difference was timing and competition. Taiwan's e-commerce market was less mature than Japan's, with no dominant player having Amazon's scale or infrastructure. The island's density—even greater than Korea's—made Coupang's logistics model viable. Most importantly, Coupang could leverage its Korean infrastructure for cross-border sales, offering Taiwanese consumers access to Korean products with free shipping.

December 2023 marked Coupang's boldest strategic move yet. Farfetch would be acquired by Coupang in a $500 million deal, providing a lifeline to the luxury platform that was facing bankruptcy. Coupang joined forces with Greenoaks Capital, a US investment firm, for the acquisition, under which it would hold an 80.1% stake in Farfetch via a company to be established for the deal. Greenoaks would take the remaining 19.9% stake.

The Farfetch acquisition was both opportunistic and strategic. Farfetch's market capitalization had nosedived by more than 90% to $250 million from its peak of $23 billion recorded in early 2021, destroyed by overexpansion and operational complexity. "Farfetch is a landmark of the luxury landscape and has been a transformative force in demonstrating that online luxury is the future of luxury retail," Bom Kim said.

For Coupang, Farfetch represented entry into the $400 billion global personal luxury goods market—a segment where logistics excellence and customer service matter even more than in mass retail. By providing access to $500M in capital, this acquisition allowed Farfetch to continue delivering exceptional services for its brand and boutique partners, and to more than four million customers around the world. The deal completed in January 2024 despite bondholder protests, with the acquisition eliminating approximately $1.6 billion dollars of Farfetch debt.

The early results were promising. Based on Visible Alpha consensus, the inclusion of Farfetch in Coupang's developing offerings division was expected to boost the segment's revenue to $3.18 billion in 2024, up from $789 million before the acquisition in 2023. More importantly, Coupang achieved an important milestone in Developing Offerings in Q3 2024, reaching near break-even profitability in Farfetch, earlier than planned.

X. Playbook: Business & Investing Lessons

The Coupang story offers a masterclass in contrarian thinking about e-commerce. While the Silicon Valley playbook preached asset-light marketplaces and platform economics, Kim built the heaviest, most capital-intensive e-commerce operation outside of Amazon. The lessons are profound and often counterintuitive.

The Power of Focus: Coupang spent thirteen years perfecting operations in a single country before meaningful international expansion. This laser focus allowed them to achieve density economics impossible in larger, more dispersed markets. While competitors spread themselves thin across Southeast Asia, Coupang dug deeper into Korea, building infrastructure so embedded in daily life that switching became unthinkable. The lesson: geographic monopoly beats geographic diversity.

Vertical Integration as Competitive Advantage: In an era when everyone was building platforms, Coupang built pipes. They owned the warehouses, employed the drivers, controlled the inventory. This wasn't just operational complexity—it was strategic brilliance. By controlling every touchpoint, Coupang could guarantee service levels competitors couldn't match. When your promise is "before 7 AM," you can't rely on third parties.

The Importance of Patient Capital: SoftBank's billions weren't just money—they were time. The Vision Fund's involvement meant Coupang could lose money for years while building infrastructure. Most e-commerce companies optimize for profitability within 18-24 months. Coupang optimized for dominance over a decade. The difference between venture capital and vision capital is the timeline.

When to Pivot: The 2013 decision to cancel the IPO and rebuild remains one of the gutsiest moves in startup history. Kim walked away from liquidity because the business model was wrong, not broken. The signals were subtle—high revenues but low customer satisfaction, positive cash flow but no competitive moat. Most founders would have taken the money. Kim took the harder path.

Capital Intensity as Moat: Conventional wisdom says capital-light businesses are superior. Coupang proved the opposite. Their $3.4 billion in pre-IPO funding created infrastructure no competitor could replicate. In dense markets with high service expectations, the company with the most capital and the will to deploy it wins. The moat isn't the technology—it's the physical footprint.

Building in Unique Markets: Korea's characteristics—density, connectivity, cultural homogeneity, high smartphone penetration—weren't constraints but accelerants. Coupang designed for these specific conditions rather than trying to port a Western model. The lesson: don't adapt global solutions to local markets; build local solutions that couldn't work globally.

The Role of Timing: Coupang caught three waves perfectly: the daily deals boom funded their initial growth, mobile commerce explosion enabled their pivot, and the pandemic validated their infrastructure investments. But they also created their own timing—building logistics capacity before demand, launching subscriptions before competitors, entering streaming before it was obvious.

The meta-lesson is that in commerce, customer experience eventually wins, but only if you survive long enough for the market to recognize it. Coupang's journey from Groupon clone to logistics powerhouse shows that the best businesses often look like the worst businesses in their early years—capital intensive, operationally complex, margin-compressing. The difference between failure and a Fortune 200 company is execution, capital, and most importantly, conviction.

XI. Analysis & Bear vs. Bull Case

Bull Case:

The optimists see Coupang as Amazon 2.0, better adapted for Asian density and positioned to dominate the next decade of Asian e-commerce. The core Korean business has achieved escape velocity—Q4 2024 net revenues were $8.0 billion, up 21% YoY on a reported basis and 28% YoY on an FX-neutral basis. Excluding Farfetch, the growth was 14% YoY on a reported basis and 21% YoY on an FX-neutral basis. This isn't just growth; it's profitable growth with expanding margins.

The logistics moat is essentially unassailable. No competitor can replicate 25 million square feet of warehouse space and thousands of employed drivers without spending billions and taking years. Meanwhile, Coupang continues to innovate—same-day delivery is becoming hours-delivery, selection continues expanding, and new categories like luxury (through Farfetch) and grocery (through Rocket Fresh) are still early innings.

Taiwan represents proof that the model can travel. After the Japan failure, successful expansion into Taiwan shows Coupang has learned how to identify and enter compatible markets. With Taiwan as a beachhead, expansion into similar dense, connected Asian markets becomes possible. Singapore, Hong Kong, and urban areas of Southeast Asia all share characteristics that make Coupang's model viable.

The Farfetch acquisition opens an entirely new chapter. Luxury e-commerce has different economics—higher margins, less price sensitivity, global reach. Coupang's operational excellence applied to luxury goods could create something unprecedented: Amazon-level logistics with Net-a-Porter-level curation. Early profitability in Farfetch validates this thesis.

Most importantly, the company has turned the corner on profitability while still growing rapidly. This isn't the false choice between growth and profits—it's both, simultaneously, sustainably.

Bear Case:

The skeptics see fundamental limits that no amount of operational excellence can overcome. Korea's population of 51 million caps the addressable market. Even with 100% penetration and infinite wallet share, there's a ceiling on how large Coupang can become. The current market cap already prices in near-perfect execution.

Competition remains fierce and is intensifying. Naver and Kakao, Korea's internet giants, are investing heavily in e-commerce. SSG.com, backed by retail conglomerate Shinsegae, is building its own logistics network. Chinese players like AliExpress are entering with lower prices. And the specter of Amazon entering Korea directly always looms.

The labor model presents ongoing risks. Coupang employs thousands of drivers and warehouse workers in a country with strengthening labor protections and rising wages. Multiple worker deaths have created reputational damage and regulatory scrutiny. Unlike gig economy platforms, Coupang can't easily shift costs to contractors.

International expansion has proven harder than expected. The Japan failure cost hundreds of millions with nothing to show. Taiwan is promising but still subscale. The Farfetch acquisition is a departure from core competencies—luxury is a different business with different customers and different challenges. Integration risks are substantial.

The valuation assumes everything goes right. At current prices, investors are betting on successful international expansion, continued Korean dominance, Farfetch turnaround, and margin expansion—all simultaneously. Any stumble on any dimension could trigger a significant correction.

The Verdict:

The truth, as always, lies between the extremes. Coupang has built something genuinely remarkable—infrastructure that would be nearly impossible to replicate, customer loyalty that borders on dependency, and operational excellence that rivals the best in global commerce. The bear case concerns are real but manageable; the bull case dreams are ambitious but achievable.

The key question isn't whether Coupang is a good business—it demonstrably is. The question is whether it's a good investment at current prices, and that depends entirely on execution in Taiwan, integration of Farfetch, and the company's ability to find new growth vectors in a maturing Korean market. The next five years will determine whether Coupang becomes a regional champion or a global force.

XII. Epilogue & "If We Were CEOs"

If we were running Coupang today, the strategic priorities would be clear but the execution would be incredibly complex. The company sits at an inflection point—dominant in Korea, profitable at scale, but facing the classic challenge of every successful regional player: what comes next?

The Path to Sustainable Profitability: First priority would be cementing profitability without sacrificing growth. The company has proven it can be profitable, but the margins need to expand while maintaining the service quality that created the moat. This means automation—not to replace workers but to augment them. Korean labor will only get more expensive; the answer isn't fewer people but more productive people. Robotic fulfillment centers, AI-powered routing, and predictive analytics need to move from experiments to core operations.

International Expansion Strategy 2.0: Japan taught a valuable lesson: Coupang's model doesn't travel everywhere. But Taiwan is proving it can travel somewhere. The next moves should be surgical—dense city-states and urban corridors where the infrastructure investments can achieve ROI. Singapore is obvious. Hong Kong is logical. Select cities in Southeast Asia—Manila, Jakarta, Bangkok—could work with adapted models. But forget about conquering entire countries. Dominate cities.

AI and Automation Opportunities: The real opportunity isn't in customer-facing AI but in operational AI. Demand prediction, inventory positioning, route optimization, quality control—every operational decision could be enhanced by machine learning. Coupang has the data advantage: billions of transactions, millions of daily deliveries, perfect information about what customers want and when. This data, properly leveraged, could reduce costs by 20-30% while improving service.

The Future of Commerce in Asia: Coupang needs to think beyond e-commerce toward embedded commerce. In Korea, they're already infrastructure. The next step is becoming invisible infrastructure—commerce that happens without conscious decision. Subscription replenishment, predictive ordering, integration with smart homes and IoT devices. When your refrigerator orders milk before you know you're out, that's the future.

Lessons for Building in "Small" Markets: The Coupang story proves that small markets can support massive companies if you achieve sufficient penetration and wallet share. But it requires a different playbook: total vertical integration, density economics, cultural localization, and patient capital. The winners won't be those who adapt global models but those who build native solutions that exploit unique local characteristics.

The ultimate test for Coupang will be whether it can replicate its Korean success elsewhere without losing what made it successful in the first place. The company that emerges from this challenge—whether as a regional champion or global player—will define the next era of Asian commerce.

XIII. Recent News

The latest developments paint a picture of a company hitting its stride. Q4 2024 results announced in February 2025 showed net revenues of $8.0 billion, up 21% YoY on a reported basis and 28% YoY on an FX-neutral basis. Excluding Farfetch, growth was 14% YoY reported and 21% FX-neutral. Gross profit increased 48% YoY to $2.5 billion with gross profit margin at 31.3%, an improvement of 570 bps YoY.

The transformation is remarkable—from burning billions to generating substantial cash flow. The company is now consistently profitable while maintaining aggressive growth rates. The integration of Farfetch is proceeding ahead of schedule, reaching near break-even in Q3 2024. Taiwan continues to gain traction with multiple fulfillment centers operational.

Looking ahead, the focus is on leveraging the infrastructure for new services while maintaining the core promise of unmatched delivery speed and reliability. The company that once seemed like it might burn out before reaching profitability has instead become one of the most impressive operational success stories in global e-commerce.

XIV. Links & Resources

Company Resources: * Coupang Investor Relations: ir.aboutcoupang.com * SEC Filings: sec.gov/edgar (Ticker: CPNG) * Annual Reports and Quarterly Earnings

Key Interviews & Profiles: * CNBC interviews with Bom Kim * Bloomberg profile pieces on Coupang's rise * TechCrunch coverage of the IPO * Forbes Asia coverage of Korean e-commerce

Books & Long-form Analysis: * "The Everything Store" by Brad Stone (Amazon comparison) * "Alibaba: The House That Jack Ma Built" (Asian e-commerce context) * Harvard Business School case studies on Coupang * SoftBank Vision Fund portfolio analyses

Industry Reports: * Korea Internet & Security Agency e-commerce reports * Euromonitor International Korean retail analysis * McKinsey reports on Asian e-commerce * Bain & Company luxury e-commerce studies

Academic Papers: * "Platform Competition in Two-Sided Markets" (Rochet & Tirole) * "Density Economics in E-commerce" (Various) * "The Economics of Vertical Integration in Digital Markets" * Studies on last-mile delivery optimization

Competitive Analysis:

* Naver financial reports and strategy documents

* Kakao Commerce investor materials

* Amazon international expansion history

* Alibaba and JD.com operational strategies

Data Sources: * Statista Korean e-commerce statistics * eMarketer Asia-Pacific retail data * Similar Web traffic analytics * App Annie mobile commerce rankings

The Coupang story is far from over. What started as a daily deals site in Seoul has become one of the most sophisticated logistics operations on the planet, a testament to the power of focus, capital, and relentless execution. Whether it becomes the Amazon of Asia or remains the undisputed king of Korean commerce, Coupang has already secured its place in the pantheon of great e-commerce companies. The next chapter—international expansion, AI integration, and the evolution from commerce company to commerce infrastructure—will determine whether this rocket delivery revolution reaches escape velocity or remains beautifully confined to its peninsular paradise.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube