Coursera: The Story of EdTech's MOOC Pioneer

I. Introduction & Episode Roadmap

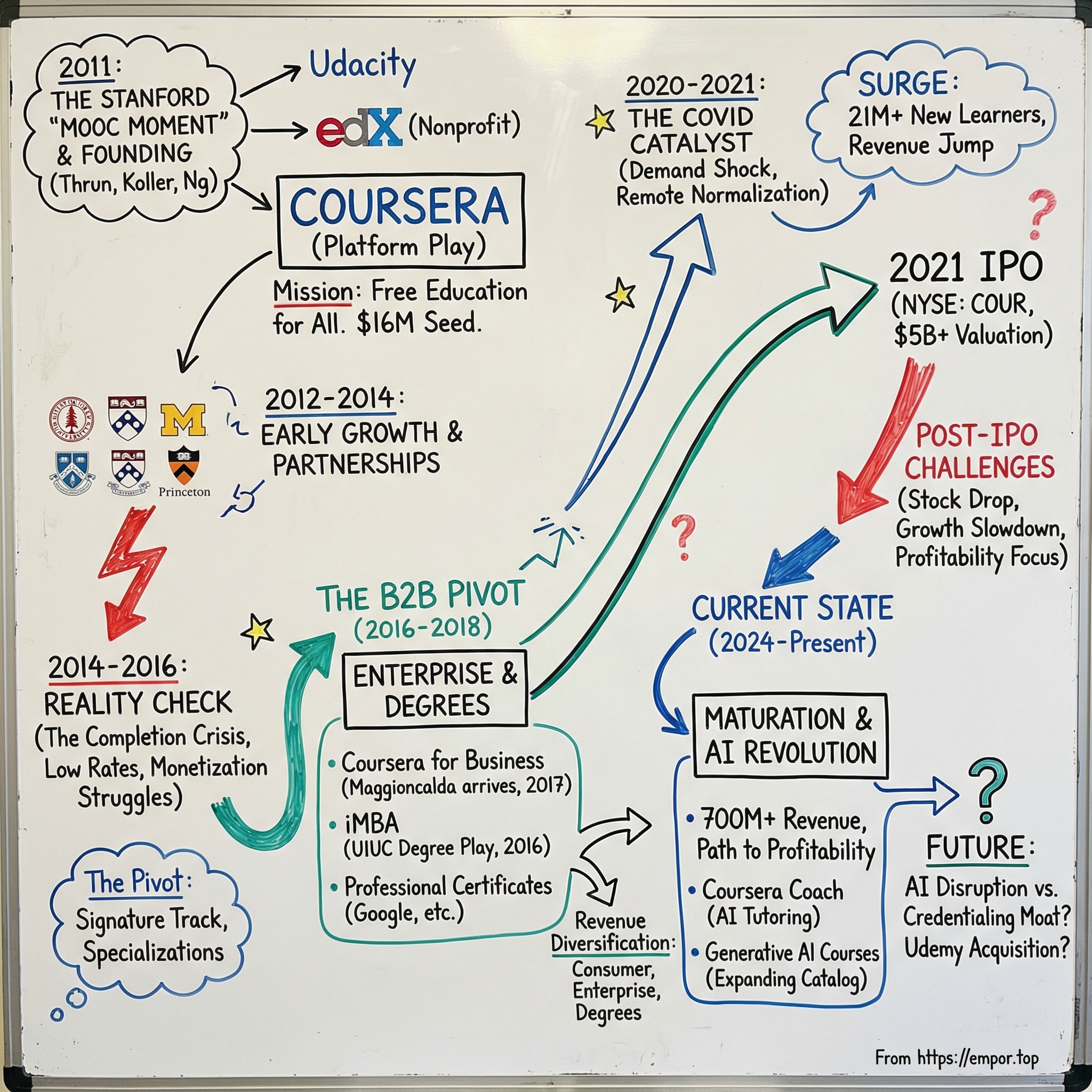

In the fall of 2011, something happened at Stanford University that nobody quite expected. A computer science professor named Sebastian Thrun decided to put his Introduction to Artificial Intelligence course online, free for anyone in the world to take. Within weeks, 160,000 people had signed up. Not 160 students. Not 1,600. A hundred and sixty thousand human beings, from nearly every country on the planet, wanted to learn about AI from a Stanford professor. The internet had produced viral moments before, but this was different. This was education going viral, and it sent shockwaves through an industry that had operated on essentially the same model since the Middle Ages.

That moment spawned three companies. Thrun left Stanford to found Udacity. MIT and Harvard jointly created edX. And two of Thrun's Stanford colleagues, Daphne Koller and Andrew Ng, launched Coursera.

Of the three, Coursera would become the largest, the most ambitious, and arguably the most conflicted. It would grapple with a question that has bedeviled every mission-driven technology company: How do you build a sustainable business when your founding promise was to give something away for free?

Today, Coursera trades on the New York Stock Exchange under the ticker COUR. It serves over 160 million registered learners in virtually every country. Its platform hosts content from more than 325 leading universities and companies, including Stanford, Yale, Google, IBM, and Meta. It generates north of $700 million in annual revenue across three distinct business lines: consumer subscriptions, enterprise workforce training, and fully accredited online degrees. It has been named to TIME's 100 Most Influential Companies list.

But the road from utopian MOOC experiment to publicly traded edtech company was neither straight nor smooth. Coursera's story is one of soaring idealism colliding with brutal market realities. Of completion rates that made investors squirm. Of a business model that took nearly a decade to find. Of a pandemic that became the single greatest growth catalyst in the company's history, followed by the inevitable hangover. And of an AI revolution that could either supercharge the company or render its core product obsolete.

This is the story of how two Stanford professors turned free online lectures into a multi-billion-dollar public company, and what their journey reveals about the intersection of mission and money, education and technology, Silicon Valley ambition and academic tradition.

The key themes: mission versus monetization, the pivot from selling to consumers to selling to corporations, and the question every investor must answer today, which is whether Coursera's moat is deep enough to survive in a world where knowledge has never been cheaper and competition has never been fiercer.

Let's start at the beginning.

II. The Founding Context: The MOOC Moment (2011-2012)

To understand why Coursera exists, you have to understand a very specific moment in the history of technology and education. The year was 2011, and the iPhone was four years old. Broadband had become ubiquitous in the developed world. YouTube had proven that video at scale was not just possible but wildly popular. And yet, the world's best educational content remained locked behind ivy-covered gates, accessible only to the tiny fraction of humanity who could gain admission to and afford elite universities.

Sebastian Thrun, a Google VP and Stanford professor best known for leading the team that built Google's self-driving car prototype, decided to run an experiment. He offered his Stanford artificial intelligence course online, for free, with the same lectures, quizzes, and assignments that his on-campus students received. The result was staggering: 160,000 students enrolled from 190 countries. More people signed up for a single Stanford course than the entire university had graduated in its 120-year history. When the dust settled, the top-performing student in the class was not sitting in a Stanford lecture hall. He was a teenager in Lithuania.

Thrun was so electrified by the experience that he announced he would leave Stanford to start Udacity, famously declaring that having experienced this, going back to teaching 200 students in a lecture hall felt like he was "tasting the future." The New York Times declared 2012 "The Year of the MOOC." MIT and Harvard responded by pooling $60 million to launch edX as a nonprofit.

And at Stanford, two more professors were watching all of this with their own ideas about what it meant.

Daphne Koller and Andrew Ng were both stars in Stanford's computer science department, but they came from very different worlds. Koller grew up in Jerusalem, completed her PhD at Stanford at a remarkably young age, joined the faculty in 1995, and won a MacArthur "genius" fellowship in 2004 at just 36 for her work in probabilistic graphical models. She was one of the most respected AI researchers in the world, the kind of tenured professor who never needs to leave academia. Ng was born in London to Hong Kong parents, grew up in Singapore, and pursued an extraordinarily rigorous academic path: a triple major in computer science, statistics, and economics at Carnegie Mellon, a master's from MIT, and a PhD from Berkeley under the legendary Michael Jordan. At Stanford, he directed the Stanford AI Lab, home to more than 20 faculty members and dozens of research groups. His machine learning course was already one of the most popular on campus.

Both Koller and Ng had been experimenting with online education independently. Ng had put his machine learning course online in 2011, attracting over 100,000 enrollments. Koller had been thinking deeply about how data could transform the learning experience, how the digital footprint of millions of learners could reveal patterns of comprehension and confusion that no classroom observation could ever capture. Together, they saw an opportunity that was subtly different from what Thrun and edX were pursuing. While Udacity would focus on its own proprietary courses and edX would remain a nonprofit consortium, Koller and Ng envisioned a platform play: a technology company that would partner with the world's best universities to distribute their courses globally. The universities would bring the academic prestige, the pedagogical expertise, and the accreditation. Coursera would bring the technology, the distribution, and the scale.

In April 2012, they launched Coursera with a $16 million seed round led by Kleiner Perkins and New Enterprise Associates, two of Silicon Valley's most storied venture firms. John Doerr at Kleiner, who had backed Google and Amazon, saw the same kind of market-creating potential in online education. The founding university partners were Stanford, the University of Pennsylvania, the University of Michigan, and Princeton.

The mission statement was breathtaking in its ambition: "We are committed to making the best education in the world freely available to any person who seeks it."

The competitive landscape was already forming. Udacity, which Thrun had launched earlier in 2012, positioned itself as a creator of original content, building its own courses with its own instructors. EdX, backed by $60 million from MIT and Harvard and structured as a nonprofit, offered a different value proposition: institutional credibility without the commercial pressure of venture-backed returns. Coursera's platform model sat between the two, aggregating content from many universities rather than creating it, and doing so as a for-profit entity that would need to justify its investors' expectations.

The key question, which Koller and Ng acknowledged but perhaps did not fully appreciate at the time, was whether this was a genuine technological breakthrough or simply the act of putting lectures online. The answer, as it turned out, was somewhere in between. The technology was real: adaptive quizzes, peer grading at scale, discussion forums that could handle tens of thousands of participants, and data analytics that could reveal how students learned in ways that a traditional classroom never could. The platform could track where students paused, replayed, or abandoned a lecture, providing pedagogical insights that no physical classroom could match. For the first time, professors could see exactly where their explanations confused students, measured in aggregate across thousands of data points rather than a few raised hands.

But the fundamental challenge of motivation, the question of whether someone sitting alone at a kitchen table in Nairobi or New Delhi would actually complete a 12-week course without the social pressure of classmates and the economic stakes of tuition, that challenge had not been solved. It was the elephant in the room that the soaring enrollment numbers conveniently obscured.

It would take years of painful experimentation before Coursera and the entire MOOC movement would fully reckon with it.

III. The Early Platform Build & University Partnerships (2012-2014)

The early days of Coursera had the feeling of a gold rush. Within four months of launching in April 2012, the platform had crossed one million registered users. By the end of its first year, that number had swelled to four million. University partners were signing up at a pace that stunned even the founders. Beyond the original four, schools like Duke, Johns Hopkins, the University of Edinburgh, and dozens of others rushed to get their courses on the platform, driven by a mixture of genuine idealism, fear of being left behind, and the irresistible marketing opportunity of reaching millions of potential students worldwide.

The initial product was simple but effective: video lectures, typically broken into segments of eight to twelve minutes to match online attention spans, paired with in-video quizzes, weekly assignments, discussion forums, and a certificate of completion. The production values varied wildly. Some professors recorded in professional studios; others propped up a webcam in their offices.

The content ranged from computer science and mathematics to the humanities and social sciences. The best courses, like Ng's own machine learning class and a series of finance courses from Wharton, attracted enrollments in the hundreds of thousands.

The partnership model was Coursera's distinctive innovation and its most important strategic decision. Unlike Udacity, which created its own courses, or edX, which operated as a nonprofit consortium where universities retained more control, Coursera positioned itself as a technology platform and distribution engine. Universities provided the content and their brand names. Coursera provided the platform infrastructure, the global reach, the data analytics, and eventually the monetization mechanisms. Revenue was shared, typically with the university receiving a percentage of any paid offerings. This model gave Coursera access to an extraordinarily broad catalog of content, from Princeton's algorithms course to the University of Pennsylvania's business specializations, without having to build an internal faculty.

International expansion was baked into the DNA from day one. Coursera invested early in subtitles, eventually offering courses in dozens of languages. The platform's global footprint was one of its most striking characteristics. Data from the early years showed that more than 60% of Coursera's learners came from outside the United States, with significant concentrations in India, Brazil, China, and across Europe and Africa. For many of these learners, Coursera represented their first exposure to instruction from a world-class university.

The press coverage was rapturous. Daphne Koller delivered a TED Talk in 2012 that has since been viewed millions of times, laying out the vision of democratized education with the clarity and conviction that only a true believer could muster.

Magazine covers proclaimed that MOOCs would disrupt higher education the way the internet had disrupted media, retail, and music. Breathless articles asked whether universities as we knew them would survive the decade.

But beneath the hype, a fundamental tension was building. The founding mission said "freely available." The venture capitalists who had invested $16 million, followed by a $43 million Series B in 2013 led by GSV Capital and the International Finance Corporation, expected a return on their money. How do you monetize free education?

Coursera's first monetization experiment was the Signature Track, launched in January 2013. For a fee of around $30 to $100, students could receive a verified certificate that authenticated their identity through webcam photos and typing pattern analysis. It was a clever idea: the course remained free, but the credential cost money. By the end of 2013, Coursera had 107 university partners offering 532 courses, and the Signature Track was generating modest but growing revenue. Nine months after launch, Coursera reported 4.7 million registered students and was growing fast.

But a nagging question lingered. Were millions of people actually learning, or were they just signing up, watching a few videos, and disappearing?

The data, when it finally emerged, would shake the MOOC movement to its foundations.

Meanwhile, the competitive landscape was already diverging. Udacity, after its initial MOOC offerings, attempted a bold partnership with San Jose State University to offer for-credit courses in spring 2013. The results were sobering: pass rates in the pilot courses ranged from just 24% to 51%, significantly lower than traditional on-campus sections. The partnership was suspended in July 2013. Thrun publicly acknowledged the disappointing outcomes and pivoted Udacity toward vocational training. EdX continued building its nonprofit platform, adding universities worldwide but struggling with the same engagement challenges. The three companies that had emerged from the same Stanford moment were already heading in three very different directions, each searching for a model that worked.

IV. The Reality Check: Low Completion Rates & Monetization Struggles (2014-2016)

By 2014, the euphoria was giving way to something much more sobering. Researchers at the University of Pennsylvania published a study examining Coursera's own data and found that, on average, only about 4% of students who enrolled in a MOOC completed the course. Other studies put the figure between 5% and 15%, depending on how completion was defined. But any way you sliced it, the numbers were devastating to the narrative. If you enrolled a million people and only 50,000 finished, was that a triumph of access or a monument to abandoned good intentions?

The completion crisis forced a reckoning across the entire MOOC ecosystem, one that would reshape every company in the space. Sebastian Thrun, in a remarkably candid interview with Fast Company in late 2013, described Udacity's product as "lousy" and pivoted his company dramatically toward corporate training and vocational "Nanodegrees." EdX, insulated somewhat by its nonprofit status and the deep pockets of MIT and Harvard, stayed the course but struggled with the same completion challenges.

And Coursera found itself in an identity crisis that would define the next several years of its existence: Were they a public good, like a library or a public school, or were they a business that needed to generate returns for investors?

The completion crisis revealed something deeper about the nature of online learning that the MOOC evangelists had underestimated. Traditional education is not just about content delivery. It is about structure, accountability, social pressure, and economic commitment. When a student pays $50,000 for a year of tuition, they have a powerful financial incentive to show up to class. When a student enrolls for free with a single click, the cost of abandonment is zero. The psychology is fundamentally different, and no amount of pedagogical innovation in video production or quiz design could overcome it without also addressing the motivational architecture.

This was the central insight the MOOC movement had to learn the hard way: content is necessary but not sufficient. Structure, accountability, and stakes matter at least as much as the quality of the lecture.

The comparison to YouTube is instructive. Nobody wrings their hands about the fact that most people who start watching a YouTube video don't finish it, because YouTube is not making promises about educational outcomes. But Coursera was making implicit promises about transformation, about giving a student in rural India access to the same education as a student at Princeton. When 95% of those students never finished the course, the promise felt hollow. The defenders of MOOCs argued, correctly, that even a 5% completion rate on a million enrollments produced 50,000 educated individuals, far more than any single university could teach. The critics countered that conflating "enrolled" with "educated" was a form of self-deception. Both sides had a point, and the debate would continue for years.

In 2014, Coursera brought in Rick Levin as CEO, a choice that signaled the company's ambitions and anxieties simultaneously.

Levin was the former president of Yale University, where he had served for 20 years and oversaw a massive expansion of Yale's campus, endowment, and international footprint. He was an economist by training, deeply credentialed, and deeply connected in the world of higher education. His appointment reassured university partners that Coursera took its academic mission seriously.

But it also reflected a practical reality: two computer science professors, however brilliant, needed someone with operational and institutional gravitas to navigate the increasingly complex business challenges. The era of the professor-led startup was ending. The era of the professional CEO was beginning.

Under Levin's leadership, Coursera began the strategic pivot that would eventually save the company. The first major product innovation was Specializations, launched in January 2014. Rather than individual standalone courses, Specializations bundled three to five related courses together with a capstone project, creating a more structured learning path that looked more like a credential and less like casual browsing. By October 2014, Coursera had launched 18 Specializations in subjects ranging from digital marketing to healthcare informatics, and the format attracted 1.5 million learners in its first year. Critically, 60% of students who completed a Specialization course sequence opted for the paid certificate, a far higher conversion rate than standalone courses.

The company also experimented with subscription models, job-matching services, and enterprise pilots during this period. Each experiment provided data about what learners actually valued and what they were willing to pay for. The picture that emerged was clear: learners who were dabbling or curious were unlikely to pay for anything. Learners who were motivated by career advancement, who needed a credential that an employer would recognize, were willing to pay real money.

This insight would become the foundation of Coursera's eventual business model, but it took time to crystallize. The 2014-2016 period was a wilderness years of sorts, a time when the MOOC hype had collapsed, when mainstream media had moved on to declaring MOOCs a failure, and when the hard work of building a sustainable edtech business was happening out of the spotlight.

The fundraising continued despite the narrative headwinds, a testament to the patient capital thesis that would prove essential to Coursera's survival. The company raised a $63 million Series C in 2015, bringing total funding to over $145 million. The investors were patient, but they were not patient indefinitely.

The company needed to demonstrate that its massive learner base could be converted into paying customers at a scale that justified the capital invested. The existential question, whether online education could actually compete with traditional credentials in the eyes of employers, remained unanswered. But the pieces were slowly falling into place for the next chapter of Coursera's evolution.

One more personnel change set the stage for what came next.

Daphne Koller, the co-founder who had been the company's president and driving force in university partnerships, stepped back from her operational role in 2016 to become chief computing officer at Calico, Alphabet's life sciences venture. Andrew Ng had already shifted his focus to his own AI ventures, including founding DeepLearning.AI and later leading Baidu's AI group.

Their departures marked the end of the founding era. Coursera was no longer a professor's passion project. It was a venture-backed company with over 20 million learners, a former Yale president as CEO, and an urgent need to find a business model that worked at scale.

V. The Degree Play: Scaling Online Graduate Programs (2016-2018)

The breakthrough insight that reshaped Coursera's trajectory came from an unlikely place: the University of Illinois at Urbana-Champaign. In January 2016, Coursera and the university's Gies College of Business launched the iMBA, a fully online, fully accredited Master of Business Administration degree delivered entirely through the Coursera platform. The price tag was approximately $22,000 for the full degree. To appreciate why this mattered, consider that a comparable on-campus MBA at a ranked business school typically cost $70,000 to $120,000, and that was before living expenses. The iMBA offered the same accreditation, the same university name on the diploma, at less than a third of the price.

The initial target was modest: just 200 students in the pilot cohort. By October 2016, the program had enrolled 270 degree-seeking students, exceeding expectations, with another 80 paying for individual courses without committing to the full degree. A second cohort of roughly 175 was planned for early 2017. The unit economics were compelling: the university received a share of tuition revenue, Coursera took its platform and distribution fee, and both sides benefited from scale. An on-campus MBA program has physical constraints, classrooms, housing, faculty availability. An online program can theoretically scale to thousands of students with modest incremental cost.

The degree play represented a fundamental evolution in Coursera's value proposition, and it answered the credentialing question that had haunted the company since its founding. Individual courses and Specializations were useful for learning, but they existed in an awkward middle ground: more structured than YouTube but less credentialed than a university degree. Think of it as the difference between reading a textbook on your own and earning a diploma: the knowledge gained might be identical, but the world treats them very differently. The iMBA was the real thing. Accredited by the same body that accredited the on-campus program. Recognized by employers. Eligible for financial aid. It was the first time a MOOC platform had bridged the gap between informal online learning and the formal higher education system.

The economics of the degree model deserve closer examination because they illuminate why this mattered so much for Coursera's trajectory. A consumer who completes a free course generates zero direct revenue. A consumer who pays for a verified certificate might spend $49 to $79. A consumer who enrolls in a Specialization might spend $200 to $400 over several months.

But a degree student paying $22,000 over two to three years represents an entirely different order of magnitude. Even after the university's revenue share, which typically ranged from 50% to 70% of tuition, Coursera's cut of a single degree student was worth more than hundreds of certificate-paying consumers. The degree business transformed the unit economics of the entire platform.

Coursera expanded the degree portfolio rapidly. By the end of 2018, the platform offered 12 online degrees from eight university partners, including a Master of Computer Science in Data Science from UIUC, programs from HEC Paris, and notably the first bachelor's degree and the first Ivy League master's degree on the platform. The University of Michigan contributed highly sought-after programs in Applied Data Science and Public Health. The University of Colorado Boulder added an electrical engineering master's.

The technology underpinning these programs evolved significantly during this period. Online proctoring allowed students to take exams remotely with identity verification. Collaborative tools enabled group projects and peer interaction. Learning analytics gave instructors unprecedented visibility into student progress and stumbling points.

The experience was not identical to sitting in a lecture hall, but for working adults, often the target demographic for these programs, the flexibility of learning on their own schedule was not a compromise. It was the entire point.

By the end of 2020, Coursera offered 26 online degrees from 13 university partners, with nearly 12,000 degree students generating $29.9 million in degree revenue. The degree segment was growing at nearly 100% year over year, the fastest-growing part of the business. And critically, the degree programs served as proof of concept for the enterprise business: if Coursera could deliver accredited university education at scale, it could certainly deliver professional development training to corporate employees. The degree play was not just a revenue line; it was a credibility bridge that connected Coursera's academic roots to its commercial ambitions.

VI. Coursera for Enterprise & the B2B Pivot (2017-2020)

On August 31, 2016, Coursera made an announcement that, in retrospect, marked the most important strategic pivot in the company's history. It launched Coursera for Business, an enterprise platform that gave corporate teams subscription access to the Coursera catalog for workforce development. The inaugural customers included L'Oreal, Boston Consulting Group, and Axis Bank. The idea was simple but powerful: instead of selling individual courses to individual consumers, sell a subscription to an entire company's workforce.

The timing was driven by a clear-eyed assessment of where the money was. Corporate training was an enormous market, estimated at over $350 billion globally, and it was dominated by legacy providers offering in-person workshops, expensive consulting engagements, and clunky internal learning management systems. Most corporate training was, frankly, terrible. Employees sat through day-long seminars, retained little, and went back to their desks. Companies knew this but had few alternatives at scale. Coursera's proposition was straightforward: give your employees access to courses from the world's best universities and companies, let them learn on their own schedule, and pay a fraction of what traditional training costs.

But launching an enterprise product and actually selling it to Fortune 500 companies are very different things.

The hire that made the difference arrived in June 2017, when Jeff Maggioncalda became Coursera's CEO, replacing Rick Levin. Maggioncalda was an unusual choice for an edtech company. He had spent 18 years as the founding CEO of Financial Engines, the investment advisory firm co-founded by Nobel Prize-winning economist William Sharpe. Under Maggioncalda's leadership, Financial Engines grew from zero to over $275 million in revenue and more than $100 billion in assets under management. He took the company public in 2010 and built it into the largest independent investment advisor in America. He had a Stanford MBA. He knew SaaS economics. He knew enterprise sales. And he understood how to transform a mission-driven organization into a disciplined business machine.

Maggioncalda's impact on the organization was immediate and decisive. He brought in enterprise sales teams, customer success managers, and the full apparatus of a B2B SaaS operation. He shifted the company's orientation from consumer-first to enterprise-first without abandoning the consumer base, which continued to serve as a massive top-of-funnel acquisition channel.

By June 2017, more than 50 companies had signed up for Coursera for Business, including BCG, BNY Mellon, PayPal, and Air France KLM. By 2019, the roster included Mastercard, Southwest Airlines, and Adobe.

Government partnerships became another major growth vector, and one that deserves more attention than it typically receives in the Coursera narrative. It is, in many ways, the hidden story within the Coursera story. Coursera for Government launched in January 2017, targeting workforce development programs for state and national governments. The logic was compelling: governments spend billions annually on workforce training, much of it through legacy providers using outdated methods. A state government trying to retrain thousands of workers displaced by automation needed something scalable, trackable, and affordable. Coursera's platform could deliver training to 10,000 workers as easily as to 100, with data dashboards showing exactly which skills were being developed and at what pace.

Michigan, Singapore, and eventually organizations in over 100 countries signed contracts to provide Coursera access to workers in need of reskilling. India proved to be a particularly fertile ground: state-level agencies in Odisha, Tamil Nadu, Uttar Pradesh, and Telangana launched workforce recovery programs on the platform, reaching hundreds of thousands of young Indians who needed employable skills but had limited access to quality vocational training. These deals were often large, multi-year contracts with significant revenue visibility, exactly the kind of recurring revenue that public market investors would later find attractive.

The content strategy shifted in parallel. And this shift revealed one of the most important insights in Coursera's history: sometimes the most valuable credential comes from an employer, not a university. In January 2018, Coursera partnered with Google to launch the Google IT Support Professional Certificate, part of Google's billion-dollar Grow with Google initiative. The certificate was designed to prepare complete beginners for entry-level IT careers in eight to twelve months. No prior experience was required. The price was affordable. And it carried a powerful implicit message from one of the world's most admired employers: complete this certificate, and we will consider you for entry-level IT roles. The program accumulated over 400,000 enrollments, and over 70% of graduates reported positive career outcomes including new jobs, promotions, or raises.

Google subsequently expanded its certificate portfolio to include Data Analytics, UX Design, Project Management, Cybersecurity, and other in-demand fields.

IBM, Meta, Microsoft, and other technology giants followed with their own professional certificates. This created a new credential category that sat between a free course and a university degree: the industry professional certificate. These industry-branded credentials were arguably more valuable to many learners than university-branded courses because they carried the implicit endorsement of a major employer: "We trained these people, and they are ready to work." For a career-switcher who needed to break into the tech industry, a Google Career Certificate might open more doors than a generic Coursera Specialization, even if the underlying content was similar in quality.

The financial transformation was dramatic. In 2017, Coursera generated an estimated $100 million in revenue, with roughly 90% coming from consumers. By 2019, revenue had grown to $184 million, and the enterprise and degree segments together accounted for approximately 35-40% of the total. Enterprise revenue specifically grew from $26.8 million in 2018 to $48.3 million in 2019, with 240 paid enterprise customers. The revenue per enterprise customer was an order of magnitude higher than revenue per consumer user. Same content, different buyer, fundamentally different economics.

The pricing evolved to match the enterprise value proposition. For teams of 5 to 125 employees, Coursera for Business charged $399 per user per year, a figure that looked like a rounding error compared to the cost of sending even one employee to a multi-day in-person training program. For larger organizations with more than 125 users, enterprise plans were custom-quoted, with dedicated customer success managers, API integrations with existing HR and learning management systems, and detailed analytics dashboards that let L&D leaders track which skills their workforce was building. A Series D round of $64 million in June 2017, valuing the company at approximately $800 million, fueled the enterprise expansion.

Network effects, while not as powerful as those in a pure two-sided marketplace, began to emerge. More learners meant better data on learning patterns, which improved course recommendations and outcomes. More learners also attracted more university and industry partners, who wanted distribution. More partners meant a broader catalog, which attracted more learners. And the enterprise sales motion benefited from the consumer brand: many corporate buyers first encountered Coursera as individual learners before championing it within their organizations. A chief learning officer at a Fortune 500 company who had personally completed a data science Specialization on Coursera over a weekend was far more likely to champion a six-figure enterprise contract than one who had never experienced the platform.

By 2019, the financial transformation was unmistakable. Consumer revenue still represented the majority, but it had declined from roughly 90% of the total in 2017 to approximately 65% by 2020. Enterprise and degree revenue together accounted for the faster-growing, higher-value portion of the business. The company had essentially built a second business on top of its first, using the consumer platform as a distribution and awareness engine while monetizing through higher-value enterprise and degree relationships. It was an elegant solution to the tension that had plagued the company since founding: give away the content, sell the credential, and charge institutions, not individuals, wherever possible.

VII. The COVID Catalyst: Education Goes Digital (2020-2021)

In early March 2020, as universities around the world abruptly shut their doors and millions of workers found themselves suddenly unemployed, Coursera experienced what can only be described as a demand shock. From mid-March onward, more than 21 million new learners flooded onto the platform, a 353% increase year over year. Course enrollments topped 50 million, a 444% surge. The registered learner base jumped from 46.4 million at the end of 2019 to 76.6 million by the end of 2020, adding 30 million users in a single year, more than the company had accumulated in its first seven years combined.

Coursera's response was swift and, in retrospect, strategically shrewd. The company and its university partners sponsored 115 free certification courses for pandemic-affected workers and learners, a program that ran through the end of 2020. It launched a Workforce Recovery Initiative in April 2020, providing free platform access to government agencies. The initiative attracted 1.1 million learners across 70 countries and served 325 government agencies. Governments from 25 U.S. states and over 100 countries used Coursera to provide emergency skills training to displaced workers. The generosity was genuine, but it was also brilliant marketing. Every government official who experienced Coursera's platform during the crisis became a potential paying customer when budgets normalized.

Revenue jumped 59%, from $184 million in 2019 to $293.5 million in 2020. Enterprise revenue grew to $70.8 million from 387 paid enterprise customers, up from 240 the prior year. Degree revenue nearly doubled to $29.9 million with approximately 12,000 enrolled degree students.

The company posted a net loss of $66 million, reflecting heavy investment in growth, but the top-line acceleration was unmistakable.

To put the pandemic surge in perspective: Coursera added more new learners in the three months following mid-March 2020 than it had accumulated in its entire first year of operation. The platform's infrastructure, built to handle gradual organic growth, was suddenly stress-tested at a scale that no one had anticipated. Servers needed to be scaled up. Customer support teams were overwhelmed. University partners scrambled to create new content to meet demand. It was the kind of growth crisis that most startups dream of but few are prepared for. The COVID-19 pandemic had compressed five years of digital education adoption into twelve months.

The tailwind extended beyond the immediate crisis.

The pandemic accelerated three secular trends that all benefited Coursera. First, the normalization of remote work. Once hundreds of millions of workers experienced Zoom meetings and Slack channels as their daily work environment, the idea of learning through a screen felt natural rather than exotic. The psychological barrier to online education, the nagging sense that it was somehow less "real" than in-person learning, evaporated overnight.

Second, the widening skills gap. As digital transformation reshuffled entire industries, from healthcare to finance to retail, employers discovered that their workforces lacked the data literacy, cloud computing knowledge, and digital marketing skills that the post-pandemic economy demanded. Corporate training budgets, which had been cut during the initial crisis, were rapidly redirected toward online upskilling platforms. Coursera was perfectly positioned to capture this demand.

Third, and perhaps most profoundly, the pandemic accelerated the growing skepticism about the cost-benefit equation of traditional higher education. If a graduate program costing six figures could be delivered entirely online, and if the pandemic had demonstrated that online delivery was not merely adequate but in many cases preferred by working adults, then why were universities charging on-campus prices for what was increasingly a remote product? This question, which predated the pandemic but was supercharged by it, created a tailwind for affordable alternatives like Coursera's degree programs. Coursera was riding all three waves simultaneously.

On March 31, 2021, Coursera went public on the New York Stock Exchange in a traditional IPO, underwritten by Morgan Stanley and Goldman Sachs. The company priced 15.7 million shares at $33, the top end of its target range, raising approximately $519 million. Shares opened at $39 and closed their first day at $45, a 36% pop that valued the company at roughly $5.9 billion.

Within a week, the stock touched $62.53, pushing the market capitalization above $7 billion. For a company that had launched nine years earlier with a $16 million seed round and no business model, it was a remarkable outcome.

But IPOs have a way of clarifying tensions that private companies can comfortably ignore. Coursera was now a public company with quarterly earnings calls, analyst coverage, and shareholders who expected returns. Revenue in 2021 grew 41.5% to $415.3 million, a strong performance but slower than the pandemic-fueled 59% of 2020. The net loss widened to $145.2 million as the company invested aggressively in sales, marketing, and product development. The registered learner base reached approximately 97 million by year-end 2021, and the degree student count had grown to roughly 16,000 across a portfolio that now included more than two dozen programs.

The IPO capital, nearly half a billion dollars, gave Coursera financial runway and strategic flexibility. But it also came with expectations. At a market capitalization of $7 billion, investors were valuing the company at roughly 17 times revenue, a multiple that assumed sustained high growth and an eventual path to significant profitability. The question now was whether the pandemic had pulled growth forward, creating a hangover, or whether it had permanently elevated the baseline of demand for online education.

VIII. Post-IPO Challenges & The Path to Profitability (2021-2024)

The answer, as public market investors discovered with painful clarity, was some of both. Coursera's stock peaked at approximately $62 in the first week of April 2021 and then began a long, grinding descent. As the world reopened and workers returned to offices, the frenzied urgency around online learning subsided. Growth rates decelerated.

The stock, which had been priced for hypergrowth, adjusted to reflect a more prosaic reality. By late 2022 and into 2023, shares traded in the teens, representing a decline of more than 70% from the all-time high.

CEO Jeff Maggioncalda navigated the downturn with the discipline one would expect from a veteran public company operator, making the hard decisions the market demanded. In late 2022, he announced workforce reductions as the company adjusted to what he called "lower growth rates and environmental uncertainty." Marketing spend, which had consumed 43% of revenue through the first three quarters of 2022, came under scrutiny. The mandate from the market was unambiguous: show a path to profitability or suffer the consequences.

The revenue picture, however, was more nuanced than the stock chart suggested. Full-year 2023 revenue grew 21% to $636 million, driven primarily by the consumer business, which posted 27% growth on the strength of professional certificates and subscription offerings. The enterprise segment continued to grow, albeit more slowly as corporate training budgets faced scrutiny. The degree segment struggled most conspicuously, with revenue growth slowing to single digits as enrollment in U.S. graduate programs declined broadly, not just on Coursera but across the entire higher education landscape. The degree business, which had been the fastest-growing segment just a few years earlier, proved sensitive to macroeconomic conditions and the competitive dynamics of a market where universities were increasingly launching their own online programs.

The competitive landscape had also intensified significantly during this period. LinkedIn Learning, backed by Microsoft's enormous distribution through the LinkedIn professional network and Microsoft 365 bundle, represented a formidable competitor in corporate learning. Udemy for Business targeted similar enterprise customers with a broader but less curated catalog. Bootcamps continued to attract career-switchers with intensive, short-duration programs. And universities themselves, having been forced online during the pandemic, increasingly questioned why they needed Coursera as an intermediary when they could build their own direct-to-student platforms.

The 2U/edX saga illustrated just how fragile the competitive landscape had become. In 2021, 2U, an online program management company, acquired edX from MIT and Harvard for $800 million, creating a for-profit entity from what had been a nonprofit. By 2023, 2U was drowning in debt and filed for bankruptcy, eventually selling edX's assets. The collapse demonstrated that even well-funded competitors could not take success for granted in the edtech market, but it also removed a rival from the field and created uncertainty for universities that had partnered with edX.

The Pluralsight saga offered another cautionary tale. Vista Equity Partners had acquired the technical learning platform for $3.5 billion in a take-private deal in December 2020, betting that enterprise demand for skills training would justify the premium. By May 2024, Vista had written off the entire value of its investment. In August 2024, lenders led by Blue Owl and Ares Management took full ownership, erasing Vista's equity. Pluralsight subsequently cut 17% of its workforce and relocated its headquarters from Utah to Texas. The write-off sent a clear message to the market: edtech valuations, even in the enterprise segment, could not be taken on faith. Execution mattered. Sustainable unit economics mattered. Hype did not.

Through all of this competitive turbulence, Coursera steadily improved its own unit economics. Gross margins held above 55%. Operating expenses as a percentage of revenue declined. The company made progress toward non-GAAP profitability and generated positive free cash flow, critical milestones for a growth company transitioning to sustainability.

Revenue in 2024 reached approximately $700 million, with full-year 2024 showing continued progress toward GAAP profitability. The registered learner base surpassed 160 million.

The content strategy also evolved. Recognizing that university partnerships alone could not fill every skill gap, Coursera expanded its catalog of industry-specific professional certificates. Twelve Google and IBM Professional Certificates on the platform received ECTS credit recommendations from FIBAA in 2024, enabling credit transfer across 49 European nations, a significant milestone in bridging the gap between informal online credentials and the formal higher education system. The move reflected a broader strategy: make Coursera credentials interoperable with the traditional academic world, increasing their value to learners and reducing the perceived risk for employers.

The metrics that sophisticated investors tracked evolved as the company matured. Enterprise net retention rate, which measures how much existing enterprise customers spend year over year (including upsells, downgrades, and churn), became a critical indicator of stickiness. Paid learner growth, degree enrollments, and the mix shift between segments provided insight into the quality and durability of revenue. The story Coursera needed to tell the market was not about explosive growth, that chapter was over, but about durable competitive advantages, expanding margins, and a credible path to sustained profitability.

IX. Current State & Recent Developments (2024-Present)

The period from 2024 into 2025 and beyond has been defined by two forces: the maturation of Coursera's core business and the arrival of generative AI as both opportunity and existential question.

In the middle of 2025, Coursera made a leadership transition that signaled the start of a new chapter. Greg Hart succeeded Jeff Maggioncalda as CEO. Hart's background was strikingly different from anyone who had previously led the company: he spent 23 years at Amazon, where he created the Alexa voice assistant and the Echo smart speaker line, holds 71 patents, and most recently served as Vice President of Alexa and Echo Devices. He brought the operational intensity and product obsession of Amazon's culture to an education company that needed exactly those qualities.

Maggioncalda's tenure had been transformative: he took Coursera from a mission-driven startup struggling to monetize into a publicly traded company with over $700 million in revenue, a clear enterprise strategy, and improving unit economics. His departure marked the natural end of a chapter, the transition from company-building to company-optimizing.

Hart inherited a business with significant scale, nearly 200 million registered learners and more than 325 university and industry partners, and a clear set of strategic priorities centered on AI integration, enterprise growth, and international expansion.

The generative AI revolution, which has reshaped nearly every sector of the technology industry, presents Coursera with both its greatest opportunity and its most existential threat. On the opportunity side, Coursera launched Coursera Coach, an AI-powered tutoring system that adapts to individual learning styles, provides support in 26 languages, and helps learners stay on track. Since its initial launch in 2023, Coach has exchanged over 34 million messages with more than 2.4 million learners. In June 2025, Coursera Coach won the Newsweek AI Impact Award for outcomes in commercial learning. In July 2025, the company was named to TIME's 100 Most Influential Companies list, specifically for its work in democratizing access to AI education.

The AI content catalog has expanded dramatically. Coursera now offers more than 750 generative AI courses from partners including Google, IBM, DeepLearning.AI (Andrew Ng's own company, in a fitting full-circle moment), Vanderbilt University, and others. The demand for AI skills training has provided a partial offset to the broader normalization of online learning demand, particularly in the enterprise segment where companies are scrambling to upskill their workforces for an AI-augmented future.

But the threat side of the AI equation is real. If ChatGPT can explain quantum mechanics, debug Python code, and provide personalized tutoring on demand, why would a learner pay for a structured course? The answer Coursera bets on is credentialing and structured learning paths: ChatGPT can teach you something, but it cannot give you a certificate from Google or a master's degree from the University of Michigan that an employer will recognize. Whether this distinction holds indefinitely is one of the central uncertainties facing the company.

The financial results for 2025 reflected steady maturation. Full-year revenue reached $757 million, with the fourth quarter delivering $197 million and, notably, $11 million in net income, a milestone in the company's path to sustained GAAP profitability. Management provided 2026 guidance of $805 to $815 million, implying mid-single-digit growth. The enterprise customer base had grown to 1,730 paid accounts by year end, up from around 240 just five years earlier. Net retention rate improved to 93%, still below the 100%+ threshold that signals true enterprise stickiness but trending in the right direction.

Enterprise momentum has continued, with Fortune 500 companies and government mega-deals anchoring the segment. The partnership portfolio has deepened with institutions like Oxford's Said Business School, Microsoft, and expanded Google programs. International markets, particularly India and Latin America, represent the largest growth opportunity. India alone has hundreds of millions of young people who need skills training and cannot access traditional higher education at scale, a demographic perfectly suited to Coursera's platform.

The business model today rests on three pillars: consumer subscriptions and individual course purchases, which provide top-of-funnel awareness and a base of recurring revenue; enterprise contracts for workforce development; and degree programs that generate the highest revenue per learner but face the most competitive pressure. The economics of the university relationship have also evolved. Under a tiered model introduced in 2021, universities receive between 60% and 75% of content revenue, depending on the type of offering and volume. Effective January 2026, Coursera introduced a new 15% platform fee on certain content, a move that signals both the platform's growing leverage and the potential for margin expansion, but also introduces friction with university partners who may view it as a shift in the economics of the relationship. The company's financial health has improved materially since the post-IPO trough, with a clear path to sustained profitability and positive free cash flow generation.

The Coursera for Government program has also matured into a significant business line within the enterprise segment. The platform now serves over 900 governmental organizations in more than 100 countries. U.S. state-level partnerships with agencies in Tennessee, New York, Missouri, and Illinois have provided workforce training to hundreds of thousands of displaced and transitioning workers. Internationally, partnerships with organizations like UNDP and the Mohammed bin Rashid Al Maktoum Knowledge Foundation have extended Coursera's reach into regions where access to quality education remains severely constrained. The platform was added to the U.S. General Services Administration listing, enabling direct procurement by federal agencies, a validation of institutional credibility that few edtech platforms can claim.

Then, in December 2025, came the announcement that may define the next era of the company. Coursera agreed to acquire Udemy in an all-stock transaction valued at approximately $2.5 billion. The deal, expected to close in the second half of 2026 pending regulatory approval, would combine the two largest online learning platforms, creating a combined entity with roughly 200 million registered learners and one of the broadest course catalogs in the world. Udemy, which had gone public in October 2021 and had been trading well below its IPO price, brought a complementary marketplace model with a massive catalog of instructor-created content, a strong enterprise business (Udemy Business), and significant international presence, particularly in emerging markets.

The strategic logic was clear: Coursera's strength in university-partnered content, accredited degrees, and government relationships combined with Udemy's marketplace depth, instructor ecosystem, and enterprise traction would create a platform with unmatched breadth. The competitive implications were significant.

The merged entity would have more content, more learners, more enterprise customers, and more data than any rival in the space. Whether the integration can deliver on this promise, merging two distinct cultures, technology platforms, and business models, remains to be seen. But the ambition was unmistakable.

The scale of the operation today is worth pausing to appreciate. Coursera's catalog includes thousands of courses, hundreds of Specializations, dozens of Professional Certificates, and more than 30 fully accredited online degrees. The platform supports content in dozens of languages and serves learners in virtually every country. It is, by registered user count, the largest MOOC platform in the world, though the gap with competitors narrows when measured by paid users or revenue. The question for investors is not whether Coursera has built something substantial. It clearly has. The question is whether what it has built is defensible enough and profitable enough to justify its public market valuation over the long term.

X. Strategic Framework Analysis

Porter's Five Forces

Threat of New Entrants: Medium-High. The barriers to creating educational content are low. Anyone with a camera and expertise can upload lectures to YouTube or Udemy. But the barriers to replicating Coursera's university partnership network are substantial. Building relationships with Stanford, Yale, Michigan, and hundreds of other institutions took over a decade of trust-building, contract negotiations, and platform development. Technology giants like Google, Amazon, and Microsoft have the resources to enter aggressively, and LinkedIn Learning already has, through Microsoft's ownership. However, the accreditation and university branding that differentiate Coursera's degree programs are not easily replicated by tech companies. The threat is real but moderated by institutional relationships.

Bargaining Power of Suppliers: Medium-High. Universities are Coursera's most critical suppliers, and they hold significant leverage. They control accreditation, which is the single most valuable asset in education. They can, and increasingly do, launch their own online programs or partner with competitors. Content creators, including individual professors and industry experts, have options ranging from YouTube to their own platforms. But Coursera provides something universities struggle to build independently: a global distribution platform with over 160 million registered users, sophisticated technology infrastructure, and a proven enterprise sales channel. Revenue-sharing arrangements give universities ongoing economic incentive to stay, but the leverage is mutual rather than one-sided.

Bargaining Power of Buyers: High. Both enterprise and consumer buyers have abundant alternatives. An enterprise customer can choose LinkedIn Learning, Udemy Business, internal training programs, consulting firms, or a combination of all of these. A consumer can access near-infinite free content on YouTube, take courses on Udemy, enroll directly in a university's online program, or simply use an AI chatbot. Switching costs are low, particularly for consumers. Enterprise customers face somewhat higher switching costs due to integration, employee familiarity, and progress tracking, but these are not insurmountable. Price sensitivity is high across both segments.

Threat of Substitutes: Very High. This is Coursera's most challenging competitive force. The list of substitutes is long and growing: YouTube and free content creators, traditional universities (still dominant for credentialing), corporate training programs, coding bootcamps, AI tutors and assistants, on-the-job apprenticeships, and now generative AI tools that can provide personalized instruction on demand. The fundamental problem is that knowledge itself is increasingly commoditized. What is not commoditized, at least not yet, is the credential, the verified proof that someone has mastered a body of knowledge in a way that an employer will trust. Coursera's strategic challenge is to remain the most credible bridge between commoditized knowledge and valuable credentials.

Competitive Rivalry: High. Direct competitors include Udemy, edX (post-2U bankruptcy), LinkedIn Learning, and Pluralsight (which Vista Equity Partners acquired for $3.5 billion in 2020 and subsequently wrote off entirely, a cautionary tale about edtech valuations). Indirect competitors include universities' own online programs, corporate training departments, and an ever-expanding universe of content creators. The market is fragmented, with no single player commanding dominant share. Differentiation centers on content quality, credential recognition, enterprise features, and increasingly, AI-powered learning experiences.

Hamilton's Seven Powers

Scale Economies: Moderate. Coursera's platform costs do not scale linearly with learners. The marginal cost of serving one additional student is negligible once a course is built. Content creation has high fixed costs but near-zero marginal costs, a favorable structure. However, the company faces ongoing investment in sales teams, content partnerships, and technology development that limit pure operational leverage relative to a software company.

Network Effects: Weak-to-Moderate. Coursera does not benefit from the strong direct network effects of a social platform. One learner's experience does not improve meaningfully because another learner joined. The indirect effects are more meaningful: more learners generate better data for recommendations, attract more university partners, and create a larger funnel for enterprise conversions. But these are modest compared to the network effects enjoyed by platforms like Amazon's marketplace or LinkedIn's professional network.

Counter-Positioning: Historical, Fading. In the early years, Coursera benefited from a classic counter-positioning dynamic: universities could not easily cannibalize their own tuition-paying, on-campus programs by offering the same courses online for free or at deep discounts. Coursera could do what universities could not. But this advantage has largely eroded. Universities have embraced online education, particularly since the pandemic, and many now offer their own direct-to-student online programs.

Switching Costs: Low-to-Moderate. Consumer switching costs are negligible. Enterprise switching costs are moderate, driven by integration with HR systems, employee progress data, and organizational familiarity with the platform. Degree students face high switching costs once enrolled but low costs before committing. Coursera needs to build switching costs through habit formation, data lock-in, and ecosystem integration.

Branding: Moderate. Coursera's brand benefits enormously from its association with top universities. The Coursera name carries credibility in a way that a generic online learning platform would not. However, Coursera's brand is derivative: it borrows prestige from Stanford, Yale, and Google rather than generating it independently. Employer recognition of Coursera certificates, while growing, still lags behind recognition of traditional university credentials. The industry-branded certificates (Google Career Certificates, IBM Professional Certificates) arguably leverage the partner's brand more than Coursera's.

Cornered Resource: Moderate-Strong. Coursera's strongest competitive advantage may be its exclusive or near-exclusive relationships with certain top universities for specific degree programs. These partnerships, built over a decade of trust and collaboration, represent a cornered resource that competitors cannot easily replicate. First-mover advantage in signing premier university partners creates durable, if not impregnable, barriers. The platform also possesses proprietary data and learner insights from 160 million users that constitute a unique asset.

Process Power: Developing. Over 14 years of operating at scale, Coursera has developed deep institutional knowledge about online pedagogy, assessment design, course production, and learner engagement. This operational expertise is difficult for a new entrant to replicate quickly. But it is not impossible over time, which is why process power alone is insufficient.

Primary Power Assessment: Coursera's most durable competitive advantage rests on its cornered resource of university partnerships combined with emerging scale economies. The company is still in the process of building the kind of deep, compounding competitive moat that characterizes truly dominant platform businesses.

Whether it can complete that process before AI reshapes the landscape remains the central strategic question.

The Udemy merger, if completed, would meaningfully alter this power assessment. The combined entity's scale economies would strengthen considerably. The marketplace model's instructor network could be classified as a cornered resource. And the sheer breadth of the combined catalog, from Stanford degrees to Udemy instructor-created courses on niche professional skills, would create a more formidable competitive position than either company commands alone.

The honest assessment today is that Coursera possesses moderate, not dominant, competitive power across most dimensions. It is not a winner-take-all platform business like Google Search or Amazon's marketplace. It operates in a fragmented market with numerous substitutes and relatively low switching costs. Its strongest power, the university partnership network, is real but not impregnable. The bull case requires believing that these moderate powers compound over time, creating something more durable than any single power would suggest. The bear case posits that moderate powers in a highly competitive market with powerful substitutes lead to a commodity business, not a platform monopoly.

XI. Bull vs. Bear Case & Investment Thesis

The Bull Case

The optimistic view of Coursera starts with the sheer size of the addressable market. Global corporate training spending exceeds $400 billion annually. Higher education is a $2 trillion global market. Lifelong learning, the idea that workers will need to continuously update their skills throughout 40-plus-year careers, is not a futuristic concept; it is a present reality driven by technological change, automation, and the rise of AI.

Coursera is the only scaled platform that operates across all three market segments: consumer learning, enterprise workforce development, and accredited university degrees.

The secular trends are powerful. The cost of traditional higher education continues to outpace inflation, pushing more students to seek affordable alternatives. Remote work has normalized remote learning. The skills gap between what employers need and what the workforce can deliver continues to widen, particularly in technology, data science, and AI-related disciplines. And Coursera's international opportunity remains largely untapped: India, Latin America, Southeast Asia, and Africa collectively represent billions of potential learners with limited access to quality education.

AI integration could be transformative. Coursera Coach and similar AI-powered tools have the potential to dramatically improve learning outcomes by providing personalized, adaptive instruction at a fraction of the cost of human tutoring. If AI makes every course feel like a one-on-one session with a brilliant tutor, completion rates could improve meaningfully, which would improve the value proposition, which would improve willingness to pay, which would improve unit economics. The virtuous cycle that MOOCs promised in 2012 but never delivered could finally materialize through AI.

The financial trajectory supports the bull case. Revenue has grown from essentially zero to over $700 million in a little over a decade. The company has demonstrated a credible path to sustained profitability and positive free cash flow. If growth re-accelerates, driven by AI demand, enterprise expansion, or international adoption, multiple expansion could be significant from current depressed levels.

The Udemy merger adds a significant new dimension to the bull case. If the integration succeeds, the combined platform would dominate the online learning market by virtually every metric: registered learners, course catalog breadth, enterprise customer count, and geographic reach. The synergies, both in technology infrastructure and sales force optimization, could meaningfully improve margins.

There is also a strategic optionality argument. Coursera sits at the intersection of education, technology, and credentialing, three domains that are all being reshaped by AI. A platform with 160 million learners, relationships with hundreds of universities, and a growing enterprise client base could be an attractive acquisition target for a technology company seeking to enter the education market, a scenario that would likely deliver significant value to shareholders even if organic growth disappoints. Microsoft has LinkedIn Learning, Google has Grow with Google, but neither has the university partnership network or the degree infrastructure that Coursera has built.

The Bear Case

The bearish argument is equally compelling. Completion rates, the original sin of the MOOC movement, remain problematic. If learners do not finish courses, the value proposition erodes for both consumers and enterprise buyers. Employer recognition of Coursera certificates, while improving, remains limited outside of technology and a handful of other sectors. A Google IT Certificate might open doors at a tech startup, but it is unlikely to impress the hiring committee at a management consulting firm or a law firm.

Competition is intense and comes from every direction. LinkedIn Learning benefits from Microsoft's distribution muscle and the natural integration with LinkedIn's professional network, where 900 million members already go to find jobs and build professional identities. YouTube offers an effectively infinite library of free educational content.

Universities, having been forced to develop online capabilities during the pandemic, increasingly question whether they need a platform intermediary. Some have already pulled content from Coursera to offer it directly.

The consumer business may never be highly profitable. Consumer acquisition costs are high, churn is significant, and price sensitivity limits the ability to raise subscription fees. The enterprise business has better economics but faces aggressive competition and long sales cycles. And the degree business, while growing, is subject to the same enrollment headwinds affecting the broader higher education market.

The Udemy integration itself carries execution risk. Merging two large platforms with different cultures, different technology stacks, and different content models (curated university partnerships versus open marketplace) is notoriously difficult. The $2.5 billion all-stock price tag means existing shareholders bear the dilution risk if the combined entity does not deliver the promised synergies.

Perhaps most importantly, generative AI represents a profound structural threat. If an AI tutor can teach any subject, answer any question, and adapt to any learning style, the value of pre-recorded lecture videos from a professor who cannot interact with the student diminishes. The structured course format, Coursera's core product, could be disintermediated by AI tools that offer more flexible, more personalized, and potentially free learning experiences. Coursera is trying to co-opt AI by building it into its platform, but the question is whether AI strengthens Coursera's moat or floods it.

Consider the analogy to the music industry. Napster and then streaming did not eliminate the need for music, but they destroyed the economics of selling albums. Similarly, AI may not eliminate the need for structured learning, but it could destroy the economics of selling courses. If the "album" is the structured course and the "streaming service" is an AI that can teach anything on demand, Coursera needs to be the entity that creates value beyond the raw content itself: through credentials, community, structure, and employer recognition. The risk is that these additional layers of value prove insufficient to sustain premium pricing in a world of abundant, free AI-powered education.

There is also a regulatory overhang worth noting. The accreditation system that gives university degrees their value is regulated by governments and accrediting bodies. Any changes to accreditation standards, such as recognizing AI-delivered education or alternative credentialing systems, could either benefit or threaten Coursera depending on the specifics. Similarly, data privacy regulations in Europe (GDPR), India, and other markets add compliance costs and limit some forms of learning analytics that Coursera relies on for product improvement and personalization.

Key KPIs to Watch

For investors tracking Coursera's ongoing performance, two metrics stand above all others.

Enterprise Net Retention Rate. This measures how much existing enterprise customers spend year over year, capturing expansion, contraction, and churn in a single number. A net retention rate above 100% means existing customers are spending more over time, a sign of stickiness and value delivery. A rate below 100% signals that the enterprise product is not sufficiently embedded in customer workflows to resist budget cuts and competitive alternatives. This is the single most important indicator of whether Coursera's B2B business is building the kind of durable competitive position that justifies a premium valuation.

Paid Learner Growth. Total registered learners is a vanity metric; what matters is how many people actually pay. Paid learner growth, across consumer subscriptions, professional certificates, and degree enrollments, reflects the health of Coursera's monetization engine. If paid learners grow faster than total learners, the company is getting better at conversion. If paid learner growth decelerates even as total learners increase, it suggests the platform is attracting free riders without converting them to customers. This ratio captures the fundamental tension at the heart of Coursera's business model: reaching everyone while convincing enough people to pay.

XII. Playbook: Lessons for Founders & Investors

Mission-driven can coexist with profit, but requires hard choices. Coursera's founding promise was free education for the world. Its business reality is enterprise subscriptions and paid credentials. The company navigated this tension better than most, but not without painful compromises. The mission now lives in the top of the funnel: free courses attract millions, some of whom convert to paying customers. The lesson is that a mission can be a powerful acquisition tool, but it cannot be the business model.

Market timing matters enormously. The MOOC idea in 2012 was prescient, but the market was not ready. Employers did not recognize online credentials. Universities were ambivalent. Broadband was insufficient in much of the developing world. It took eight years and a global pandemic to create the conditions for Coursera's business model to fully click. The company survived because it had patient capital and a willingness to iterate. Many other edtech startups launched with similar visions in 2012 and 2013 and are long gone. Timing is everything, but survival is what lets you be in the right place when the timing finally arrives.

Pivoting the business model without abandoning the mission. The transition from B2C free to B2B subscriptions and accredited degrees was Coursera's most important strategic maneuver. It required completely different capabilities: enterprise sales teams, customer success functions, university partnership management, and SaaS metrics discipline. Many mission-driven companies resist this kind of pivot because it feels like a betrayal of the founding vision. Coursera's pivot was not a betrayal; it was an evolution that made the mission financially sustainable.

Platform strategies require both sides to win. Early on, some universities complained that Coursera was using their content to build a platform without providing adequate economic returns. The partnerships only became durable when the revenue-sharing arrangements, particularly around degrees and professional certificates, provided meaningful income streams for university partners. A platform that extracts value from its suppliers without sharing it will eventually lose those suppliers.

Beware the hype cycle. The MOOC mania of 2012-2013 set expectations that no company could meet. When completion rates emerged and the initial growth curve flattened, media and investor sentiment swung from euphoria to disdain. Coursera weathered the trough, but the reputational damage from the "MOOCs are dead" narrative took years to overcome. For founders, the lesson is to manage expectations carefully. Hype can raise your valuation, but it can also set a bar that poisons the narrative when reality falls short.

Enterprise sales can transform unit economics. The same course that generates $49 from a consumer can generate thousands per seat when sold to an enterprise customer. Coursera's pivot to enterprise sales fundamentally changed the economics of the business without requiring fundamentally different content. The insight generalizes: if you have a product that individuals value modestly, consider whether institutions, which have larger budgets and greater urgency, would pay a premium for the same product delivered differently.

Credentials matter more than content. In a world of abundant information, knowledge is not the scarce resource; proof of knowledge is. Coursera's evolution from free lectures to verified certificates to professional credentials to accredited degrees reflects this reality. The value is not in the lecture video; it is in the piece of paper (or digital badge) that an employer will recognize. Every edtech company that focuses solely on content quality without addressing the credentialing question is solving the wrong problem.

Partnerships as moats are fragile. University partnerships have been Coursera's most durable competitive advantage, but they are inherently fragile. Universities are partners today and potential competitors tomorrow. They can build their own platforms, partner with competitors, or decide that the revenue share is not favorable enough. Managing these relationships requires constant attention, mutual value creation, and the humility to recognize that the university brand, not the platform brand, is what learners and employers ultimately trust.

Patient capital advantage. Coursera took approximately nine years from founding to IPO, an eternity in Silicon Valley. During those years, the company raised over $460 million in private capital while searching for a sustainable business model. Not every investor has the patience for a decade-long bet, and not every company deserves that patience. But for companies operating in markets that need time to develop, like education, where adoption cycles are measured in academic years rather than product sprints, patient capital is a genuine advantage.

Going public changes everything. As a private company, Coursera could experiment, pivot, and invest in growth without quarterly scrutiny. As a public company, every earnings call became a referendum on whether the growth story was intact. The stock's decline from $62 to the teens forced painful cost-cutting and a strategic refocus on profitability. The lesson is not that going public was wrong, the IPO provided critical capital and liquidity, but that founders should enter the public markets with clear eyes about how the incentive structure changes.

The myth versus reality of disruption. The MOOC narrative began with the premise that online education would disrupt and potentially replace traditional universities. That has not happened, and it probably never will, at least not in the way the early hype suggested. What has happened is subtler and arguably more important: online education has created a parallel pathway that supplements and extends traditional education, reaching populations that the traditional system was never designed to serve. Coursera has not replaced Stanford. It has given a data analyst in Mumbai access to Stanford's machine learning course, a Google career certificate, and a University of Michigan master's degree, all without leaving her city or quitting her job. That is not disruption in the Christensen sense of killing the incumbent. It is expansion of the market itself. For investors, the implication is significant: Coursera's TAM is not the existing higher education market minus displacement; it is the massive, underserved global market for professional education that traditional institutions cannot reach.

XIII. Epilogue: The Future of Learning