Core Scientific: The AI Phoenix and the Power Moat

I. Introduction & Episode Roadmap

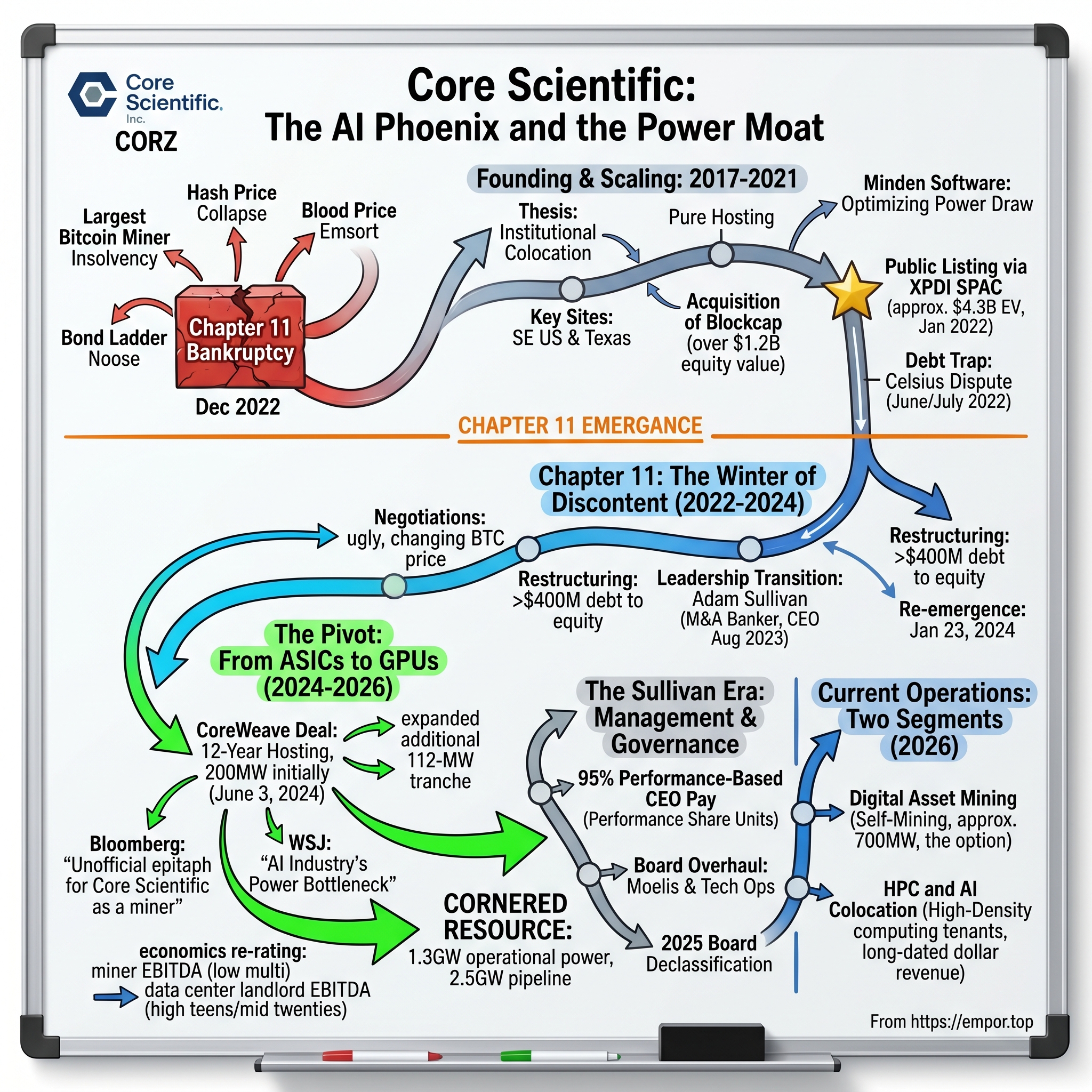

In December 2022, in a sterile courtroom in the Southern District of Texas, the lawyers for Core Scientific filed a stack of paperwork that, on the face of it, looked like an obituary. Chapter 11. The largest bankruptcy in the history of the Bitcoin mining industry. A company that, twelve months earlier, had been hailed as a flagship "institutional" miner, the cleanest balance sheet in a dirty business, was now insolvent. Hash prices had collapsed. Power costs had exploded. And the bond ladder that financed all those whirring 蚂蚁矿机 Antminer rigs in Georgia and Texas had become a noose.1

If you had walked out of that courtroom in late 2022 and told the lawyers that, in less than four years, this same company would be sitting on long-duration contracts with the most coveted name in artificial intelligence infrastructure, would be operating at the heart of the AI compute boom, and would have rejected a nine-billion-dollar buyout offer from one of the most aggressive growth companies on the planet, you would have been politely escorted to the exit.

And yet that is precisely what happened. As of this May 2026 episode, Core Scientific (NASDAQ: CORZ) commands roughly 1.3 gigawatts of operational power infrastructure across North America, with another 2.5 gigawatts in its expansion pipeline.2 Its market capitalization sits in the mid-teens of billions of dollars. Its largest single customer is no longer a crypto hedge fund or a struggling lender — it is CoreWeave, the GPU cloud company that became the symbolic face of the AI compute scarcity trade.[^3]

This is the story of how a left-for-dead Bitcoin miner became, almost overnight, one of the most strategically positioned data center landlords in the United States. It is a story about three things.

First, it is a story about a cornered resource. In 2026, the bottleneck for the AI revolution is not GPUs — Nvidia can manufacture those. It is interconnected, energized, permitted electrical power at industrial scale. That is the resource Core Scientific had already paid for, fought utilities for, and built shells around — for the simple reason that Bitcoin mining had needed exactly the same thing.

Second, it is a story about the brutal arithmetic of leverage. The same financial engineering that let Core Scientific scale to over 700 megawatts of mining infrastructure in record time also vaporized its equity when the cycle turned. The lesson is older than crypto itself: in a commodity business, debt against depreciating hardware is a self-destruct mechanism with a fuse measured in months.

Third, it is a story about a strategic pivot from 比特币 Bitcoin to 人工智能 AI that, in retrospect, looks obvious — but at the time of the bankruptcy emergence in early 2024, was not obvious at all. Most miners doubled down. Core Scientific, under new management, hedged its bet and then, with the June 2024 CoreWeave deal, walked through a door that has, for now, slammed shut behind it.

Strap in. This is Core Scientific.

II. The Gold Rush: Founding & Scaling

To understand Core Scientific, you have to remember what 2017 felt like. Bitcoin was crossing twenty thousand dollars for the first time. The word "ICO" still meant something other than a punchline. Wall Street analysts who had spent five years sneering at crypto were quietly opening Coinbase accounts on burner phones. And in Bellevue, Washington — not in some libertarian basement in Texas — a group of former enterprise infrastructure operators looked at the chaos and asked a deceptively boring question: what if we built the boring, institutional, regulated layer underneath all of this?

That was the founding thesis. Core Scientific would not be a crypto company in the cultural sense. It would be a data center company that happened to host application-specific integrated circuits — ASIC chips — instead of standard servers. The founders' bet was that as soon as institutional capital arrived in earnest, it would want professionally managed colocation, real-time monitoring dashboards, audited SOC reports, and a CEO who could pass muster in front of a Fidelity portfolio manager. Crypto-native garages would not cut it.

The execution plan was equally deliberate: go where the power is cheap, the climate is forgiving, and the local politics are receptive. In practice, that meant the American Southeast and the Texas grid. Over the next four years, Core Scientific raised land flags in Calvert City, Kentucky; in Marble, North Carolina; in Dalton, Georgia; and across multiple sites in Texas. The construction template was a kind of industrial brutalism — long, low, pre-engineered metal buildings filled with row upon row of immersion-friendly racks, fed by 100-megawatt substations built with the local utility. These were not data centers in the Equinix sense. They were power-conversion factories.

By 2021, the cycle was incandescent. Bitcoin had crossed sixty thousand dollars. New 比特大陆 Bitmain rigs were selling at multiples of cost on the secondary market. Lead times for transformers were stretching past a year. And Core Scientific, which had been a pure hosting company, decided that it could not leave the upside on the table for its tenants. It would mine for its own account too — in size.

The vehicle for that pivot was the all-stock acquisition of Blockcap, announced in mid-2021 and pitched at well over a billion dollars of equity value at the time the deal was signed.3 Blockcap was, at heart, a fleet of self-mining ASICs and a management team that knew how to operate them. The strategic logic was clean: combine Blockcap's machines with Core's industrial real estate and become, overnight, one of the largest self-miners in North America. The arithmetic was less clean. Roughly twenty-seven million Core Scientific shares were issued for a hardware-heavy business priced near the peak of the cycle.3 In hindsight — and even at the time, to skeptics — this was paying a cycle-peak multiple for assets whose useful economic life was, at best, three to four years. Bitcoin miners depreciate like fresh produce in July.

Alongside the hardware acquisitions came a more subtle and ultimately more durable buy: the Horizon Computing team, whose software toolset would later be branded internally as "Minden." Minden does the unglamorous work of optimizing power draw, scheduling workloads, and orchestrating thousands of machines across multiple sites in real time. In a world where electricity is your single largest cost line, software that shaves percentage points off your power utilization effectiveness is worth its weight in transformers.

The capstone arrived in January 2022 with the SPAC. Core Scientific merged with Power & Digital Infrastructure Acquisition Corp (the ticker XPDI), public-listing the company at an enterprise value of approximately $4.3 billion in the giddy final innings of the SPAC mania.4 The roadshow narrative was hyper-growth: massive expansion pipeline, premium hosting clients, vertical-integration upside from self-mining. The deck did not dwell on the second-order question — what happens if hash price falls fifty percent and your equipment loans amortize at fifteen percent interest? It would not have to dwell on it. The market would answer it instead.

III. The Debt Trap & The Celsius Dispute

There is a particular flavor of corporate misery that arrives when three things go wrong at once. Your revenue collapses. Your costs spike. And your lenders — who were so friendly six months earlier — start reading their loan documents very carefully. That was 2022 for Core Scientific.

To understand the leverage trap, you have to understand the specific way Bitcoin miners financed themselves at the peak. The dominant structure was equipment-secured debt: a lender — often a specialized digital-asset credit fund — would advance you somewhere between sixty and eighty percent of the invoice price of a new ASIC fleet, take a first lien on the machines, and charge an interest rate that, in the 2021 environment, often started with a "1." That was rational in a world where a single machine generated forty or fifty dollars a day of gross profit. It was lethal in a world where the same machine generated five.

By the summer of 2022, the macro picture had inverted entirely. Bitcoin had collapsed from sixty-nine thousand dollars in November 2021 toward the low twenty-thousands. Network hash rate, paradoxically, kept climbing as machines ordered at the peak finally shipped from 比特大陆 Bitmain's factories — meaning every miner's slice of the daily block reward shrank at the precise moment the dollar value of that reward was collapsing. Meanwhile, natural-gas prices spiked on the back of the Russian invasion of Ukraine, dragging wholesale power prices on the Texas and Southeast grids to multi-year highs. The hash price — the daily revenue per unit of computing power — fell by something on the order of seventy percent peak-to-trough.

And then there was Celsius. Celsius Network was, by 2022, one of Core Scientific's largest hosting customers. Celsius had financed its own ASIC fleet, parked the machines in Core Scientific facilities, and paid monthly hosting fees that covered power, maintenance, and a healthy operator margin. When Celsius itself froze withdrawals in June 2022 and filed for Chapter 11 in July, Core Scientific suddenly had a meaningful piece of its revenue stack become, in legal terms, a disputed claim against a debtor estate. The fight over unpaid power bills, the right to seize and re-deploy the hosted machines, and the proper classification of pre-petition versus post-petition obligations would consume months of senior management's attention and tens of millions of dollars in real and imputed losses.1

By the autumn, the equity market had drawn the obvious conclusion. Core Scientific's stock, which had traded above ten dollars after the SPAC, had collapsed to pennies. Convertible noteholders began circling. A series of disclosures in October and November 2022 made clear that absent a renegotiation, the company would run out of liquidity before year-end. On December 21, 2022, Core Scientific filed for Chapter 11 in the Southern District of Texas — the largest bankruptcy in the brief history of the publicly traded mining sector.1

The morality play writes itself. But the more interesting analytical question is this: was the bankruptcy a failure of strategy, or a failure of timing? The answer, uncomfortably, is "both — but mostly timing." The strategic premise — that interconnected power at industrial scale would prove to be the durable asset — turned out to be exactly right. The execution sin was financing depreciating ASICs with non-recourse-style debt that triggered in a downturn. Had Core Scientific scaled half as fast with half as much leverage, the same power footprint would have survived 2022 intact and the company would have collected the AI windfall as an unrestructured equity. Instead, it had to go through the courthouse first.

The bridge to that second life ran through the bankruptcy estate.

IV. Chapter 11: The Winter of Discontent

Most bankruptcies are funerals. A handful are weddings — a forced introduction between an over-levered operating business and a sober new capital structure. Core Scientific's restructuring, from the first day of the case, was clearly the latter. Management and counsel framed the filing not as a liquidation of a failed miner but as a "balance sheet event" for an operating platform that, on an unlevered basis, still generated cash. The pitch to the court, and to the creditors who would ultimately own the post-emergence equity, was simple: keep the rigs spinning, keep the customer book intact, and the going-concern value will exceed the auction value by an order of magnitude.5

The negotiations were ugly in the way these things always are. Convertible noteholders, equipment lenders, trade creditors, and the equity committee each had a different theory of value and a different incentive to either accelerate or delay. The Celsius dispute had to be wedged into the broader plan. The hedge between "we want our hosting customer to survive" and "we want to be paid for the power we burned for them" required a particular kind of legal contortion. And the spot price of Bitcoin, which conveniently rallied during the case, kept changing the math underneath every model.

The leadership team that walked the company through that period would prove to be the most important inheritance of the entire restructuring. Adam Sullivan, who had joined Core Scientific in 2022 from the boutique investment bank XMS Capital, was elevated to chief executive officer in August 2023 in the middle of the case.6 Sullivan was not a crypto native. He was, by temperament and training, an M&A banker — the kind of executive who talks about "capital structure optionality" more naturally than he talks about hash rate. That biography mattered. The job to be done was not, at that moment, to be the most enthusiastic Bitcoin bull in the room. It was to convert a balance sheet, negotiate with sophisticated creditors, and design an equity structure that would survive an audit. Sullivan was built for that job.

By the time the plan of reorganization was confirmed, the headline restructuring numbers told a clean story. More than four hundred million dollars of pre-petition debt was converted into post-emergence equity. The convertible noteholders received a recovery built around new debt and new shares. Trade creditors were made substantially whole. And the legacy equity, against all the usual rules of bankruptcy, received a meaningful — if heavily diluted — stake in the new company, in exchange for releases and the avoidance of a contested confirmation hearing.5

On January 23, 2024, Core Scientific emerged from Chapter 11 and re-listed on the Nasdaq, this time under the same CORZ ticker but as a fundamentally different company in three respects.5 First, its capital structure had been delivered, with net debt to forward EBITDA a fraction of what it had been at the peak. Second, its board had been overhauled. Third, and most importantly, its narrative had been rewritten in real time. Management was no longer pitching investors a Bitcoin miner. It was pitching a power platform with two customers — itself, in the form of self-mining, and an emergent class of high-density computing tenants.

That narrative pivot would have sounded like restructuring spin in almost any other quarter of the prior decade. It happened to land at exactly the moment that the AI compute market discovered it had a power problem.

V. The Pivot: From ASICs to GPUs

There is a scene that every Core Scientific employee who lived through the spring of 2024 will recount in some version. A site walk in a mining facility — the kind of building designed to dump heat from twenty thousand ASIC rigs into the Texas air — and a delegation of visitors in jackets too nice for the dust. The visitors were not from a hedge fund and not from a hardware vendor. They were from CoreWeave. They were measuring the buildings. They were asking about water. And they were asking how quickly the rooms could be retrofitted for liquid-cooled racks running not at 12 kilowatts of density but at 80 or 100.

The announcement landed on June 3, 2024. Core Scientific and CoreWeave had signed a twelve-year hosting agreement for an initial 200 megawatts of high-performance computing capacity across multiple Core Scientific sites.[^3] Within weeks, the two parties had expanded the relationship with an additional 112-megawatt tranche.[^8] In aggregate, the contracted HPC book — long-duration, dollar-denominated, take-or-pay in structure — went from approximately zero to north of three hundred megawatts in a single quarter. The market reacted accordingly. Bloomberg noted the share price reaction in a piece that became the unofficial epitaph for the "Core Scientific is a miner" framing.7

To understand why CoreWeave came to Core Scientific instead of, say, Equinix or Digital Realty, you have to understand the architectural shift inside the rack. A traditional cloud workload — a web server, a database, an SAP instance — runs comfortably at fifteen kilowatts per rack with conventional air cooling. A rack full of Nvidia's latest Hopper or Blackwell-generation GPU 显卡 accelerators, configured for large-model training, can pull eighty kilowatts and is approaching a hundred-and-twenty. At those densities, air cooling stops being engineering and starts being mythology. You need direct-to-chip liquid cooling, vastly higher floor loading, and shells designed from the foundation up for power conversion at megawatt scale. Bitcoin mining shells — high-ceilinged, electrically dense, deliberately industrial — happened, almost by accident, to be the right starting point. As the Wall Street Journal would put it in an August 2024 piece, the AI industry's power bottleneck had handed the miners an unintended second act.8

The economics of the pivot are equally important to understand in plain terms. Bitcoin mining revenue is, by construction, volatile: it is the product of two highly volatile inputs (BTC price and network hash rate) and one mostly stable input (your own machine fleet). HPC colocation revenue, by contrast, is a long-dated, contractually fixed dollar stream — closer in character to an industrial real estate lease than to a commodity sale. For an equity that had, until the bankruptcy, been valued as an option on Bitcoin price, swapping a meaningful slice of EBITDA into long-duration take-or-pay contracts was a profound re-rating event. Multiples paid for "miner EBITDA" cluster in the low single digits. Multiples paid for "data center landlord EBITDA" with a creditworthy tenant on a twelve-year lease cluster, depending on geography and tenant quality, in the high teens to mid twenties.

The most revealing single decision of Sullivan's tenure followed almost immediately. In June 2024, just days after the initial hosting deal, CoreWeave moved to acquire Core Scientific outright via an unsolicited proposal. The Core Scientific board rejected it. Then, in the autumn of 2025, after more than a year of public courtship and counter-proposals, CoreWeave came back with a sweetened offer that valued the company at roughly nine billion dollars on a fully diluted basis. Again, the board declined.[^11]

The rejection was, in essence, a statement of independent identity. Selling the entire company to CoreWeave at nine billion would have monetized the pivot. Keeping the asset base independent — and signing additional HPC contracts with a broader roster of tenants — kept open the option of being a Tier 0 infrastructure landlord to the entire AI ecosystem rather than a captive subsidiary of one hyperscaler's most aggressive challenger. That bet is, as of this episode, still being adjudicated. But the company is no longer being asked whether it can survive. It is being asked how big it wants to become.

VI. Current Management: The Sullivan Era

Adam Sullivan is not the kind of CEO who shows up to a Bitcoin conference in a hoodie. His public appearances tend toward the muted: dark jacket, sober tie, the affect of a banker who has spent enough nights in restructuring war rooms to know that exuberance, in either direction, is usually a mistake. His background is M&A advisory at XMS Capital, the boutique founded by former Morgan Stanley vice chairman Robert Greenhill's protégés, and earlier roles in the kind of mid-market advisory work where you learn to read indentures the way most people read menus.6 When Core Scientific recruited him in 2022, the explicit job was capital strategy. The implicit job, which arrived faster than anyone planned, was running the company through a Chapter 11 filing and out the other side.

The terms of his appointment as chief executive — formalized in the post-emergence employment agreement filed in June 2024 — tell you almost everything you need to know about how the new board thinks.6 Sullivan's compensation package is heavily weighted toward equity. The cash component is modest by hyperscaler-CEO standards. The equity component, sized in the tens of millions of dollars at grant-date value, is overwhelmingly performance-based: time-vested restricted stock makes up a minority of the package, while the bulk is structured as performance share units that vest only on the achievement of HPC operational milestones and on demanding stock-price hurdles measured over multi-year periods. The shorthand version that circulates among investors — "ninety-five percent at-risk" — slightly oversimplifies the math but is directionally correct.6 Sullivan gets rich if and only if shareholders get rich first.

The board around him reads more like the lobby of Moelis than like a Bitcoin conference. Jordan Levy, the chair, came in as part of the post-emergence governance reset, bringing a long career in technology operating and investing roles. Elizabeth Crain, a co-founder of the investment bank Moelis & Company, brought the Wall Street institutional credibility that the company badly needed in the aftermath of the bankruptcy.[^12] The full slate is light on crypto natives and heavy on capital-markets veterans — which, given the strategic question facing the company (how to finance and price multi-billion-dollar HPC build-outs against long-dated leases), is the right composition.

The 2025 declassification of the board, ratified in the spring proxy vote, was a quietly important governance signal.[^12] Staggered boards have historically been used as anti-takeover armor, and for a company that had just rejected a multi-billion-dollar unsolicited offer, the optics of dismantling that armor mattered. The implicit message to the market was: we are not interested in entrenching ourselves; we are interested in being valued correctly. Whether that message is fully credible after the second rejection of CoreWeave is a fair debate. The structural choice, at least, points in the right direction.

Insider ownership at the executive and director level sits in the low single digits as a percentage of shares outstanding — roughly 1.4% in aggregate based on disclosures around the most recent proxy.[^12] In a post-bankruptcy company where convertible holders and creditors received the lion's share of new equity, that is not surprising. The more meaningful alignment is on the institutional side: large index and active managers including BlackRock and Fidelity emerged from the restructuring with anchor positions, and the float is now broadly held by long-only institutions rather than concentrated in crypto-aligned strategies. That investor base is, in effect, a governance counterweight: it cares about long-duration HPC contracts and credit metrics, not about hash rate vanity statistics.

The combined picture is of a management team and board built for the second act, not the first.

VII. Segment Deep Dive: The 'Hidden' Business

To value Core Scientific in 2026, you have to learn to look at it the way the market is increasingly being forced to look at it: as a power-platform company with two operating segments that happen to share the same substations.

The first segment — Digital Asset Mining — is the legacy business, and it is still meaningful. Roughly 700 megawatts of operational capacity remain dedicated to self-mining Bitcoin, making Core Scientific one of the largest publicly traded miners in North America by deployed hash rate.2 The economics of that segment are exactly what you would expect: when hash price is high, the segment throws off real free cash flow; when hash price compresses, the segment becomes a high-cost operating drag. The post-halving environment of 2024 and the price action of 2025–2026 have, on balance, been kind to the segment, but the analytical framing inside the company has shifted decisively. Mining is no longer the strategic asset. It is the option. Management sizes the self-mining fleet not based on a maximalist Bitcoin thesis but based on the marginal returns of dedicating a megawatt to ASICs versus signing the same megawatt away to a long-duration HPC tenant. As the HPC pipeline matures, the breakeven tilts further toward HPC, and the mining fleet's share of total megawatts will continue to shrink.

The second segment — HPC and AI colocation — is the hidden gem that, as of 2026, is no longer especially hidden. Q1 2026 results, presented on May 8, 2026, showed colocation revenue ramping sharply as the first tranches of the CoreWeave deployment came online, with management guiding to a multi-fold expansion as the contracted backlog cuts in over 2026 and 2027.[^13] The structural attributes of that revenue stream — long duration, dollar-denominated, with a high-quality counterparty and pass-through power economics — are precisely the attributes that bond investors and infrastructure REIT investors pay premium multiples for.

The most underappreciated asset on the entire balance sheet may be the proprietary operations stack. The "Minden" platform — a piece of inherited intellectual property from the Horizon Computing transaction, refined and expanded since — is the software backbone that coordinates power distribution across roughly 1.3 gigawatts of active load. Minden is, in plain language, the tool that decides which machines run, at what frequency, drawing what wattage, in response to real-time grid signals, weather, demand-response programs, and customer SLAs. In a mining context, that capability was worth a few percentage points of efficiency. In an HPC context, where uptime requirements are dramatically higher and SLA penalties dramatically more punitive, that same capability is the difference between a tenant that renews and a tenant that sues.

But the true hidden asset is even simpler. It is the 2.5-gigawatt expansion pipeline of interconnected power across multiple sites.2 Each one of those interconnect studies, each one of those substation builds, each one of those utility purchase agreements represents three to five years of unglamorous, hard-to-replicate work with regional grid operators. In 2026, multiple analysts have remarked that finding 500 megawatts of energized, permitted, AI-ready power in the United States is materially harder than raising five billion dollars of capital to pay for it. Core Scientific has — by accident of its prior life as a Bitcoin miner — already done the harder of the two tasks.

So when management talks about Core Scientific as a "power company," they are not engaged in narrative hand-waving. They are pointing at the most strategically valuable inventory in the AI supply chain.

VIII. Playbook: 7 Powers & Porter's 5 Forces

Strip away the cycles and the courtroom drama, and the question every long-term investor has to answer is the same: what, if anything, structurally protects this business from competition? The Hamilton Helmer 7 Powers framework offers a useful clinical lens, and three of the seven powers map cleanly onto Core Scientific in 2026.

The dominant power is Cornered Resource. The resource is interconnected, energized, permitted electrical power at industrial scale, in jurisdictions friendly to large-load development. That resource is not scarce in any cosmic sense — there is plenty of fuel and plenty of capital. It is scarce in the practical sense that the utility interconnection queues in ERCOT, MISO, SPP, and the Southeast are years long; that local moratoria on large-load connections have proliferated in 2024 and 2025 as residents and regulators wake up to the AI build-out; and that transformer and switchgear lead times remain measured in years rather than months. Core Scientific cleared the queues during the mining build-out, often before AI was even a serious customer segment. That timing advantage is non-replicable. A competitor with infinite capital today cannot conjure 1.3 gigawatts of operational shells and another 2.5 gigawatts of pipeline by next year.

The second power is Counter-Positioning. Conventional data center operators — Equinix, Digital Realty, the major hyperscaler-owned campuses — were architected around the workload mix of the pre-AI cloud era: tens of kilowatts per rack, air-cooled, with strict latency and uptime SLAs negotiated against legacy enterprise tenants. Their physical plants, their service contracts, and their organizational muscle memory all reflect that history. Retrofitting an Equinix facility to support 100-kilowatt liquid-cooled racks is technically possible but commercially awkward — the existing customer base does not need it, and the cost of the retrofit cannibalizes existing returns. Core Scientific, by contrast, never had a legacy cloud customer base to protect. Its shells were built from day one for raw electrical and thermal density. The counter-position is not about being better at the old game; it is about playing a different game.

The third power is Switching Costs. Once a customer like CoreWeave has installed billions of dollars of GPU infrastructure inside a particular Core Scientific shell, signed a twelve-year lease, and integrated the site into its global capacity allocation, the cost of unwinding that arrangement is not just the unwound rent. It is the dismantling and re-shipping of millions of pounds of liquid-cooled hardware, the re-negotiation of a comparable lease in a market with vanishing supply, the loss of operational tenure with a counterparty that has now spent two years learning your site's quirks, and the opportunity cost of every training run that does not happen during the transition. In effect, Core Scientific has stapled itself to a generation of AI infrastructure investment whose mobility costs make the customer relationships sticky on a decade-plus horizon.

The Porter's 5 Forces lens, applied briefly, sharpens the same picture. Bargaining power of buyers is, in the HPC segment, extraordinarily low — the scarcity of energized AI-ready data center capacity is, as of 2026, the binding constraint of the entire compute economy. Bargaining power of suppliers is uneven: on the AI side, Nvidia's pricing power flows to the customer rather than to Core Scientific, which is helpful; on the mining side, 比特大陆 Bitmain's pricing power on ASICs is a real cost-of-goods drag. Threat of new entrants is gated by exactly the resource scarcity that defines the cornered-resource power. Threat of substitutes — primarily the hyperscaler clouds (AWS, Azure, Google Cloud) — is real but indirect: those substitutes are themselves capacity-constrained, and several are exploring leasing arrangements with the same class of independent infrastructure providers. Rivalry among existing competitors — Iris Energy, Cipher Mining, Riot Platforms, Galaxy Digital's Helios site, Applied Digital, and others — is intensifying, but each of these competitors faces the same scarcity constraints from the supply side.

There are two KPIs that, more than any others, will tell investors how the playbook is being executed. The first is contracted HPC megawatts under long-duration leases, both in absolute terms and as a percentage of total operational capacity. That ratio is the single best proxy for the speed of the mix shift away from commodity mining and toward infrastructure-quality cash flow. The second is operational power capacity progression — the rate at which megawatts move from "pipeline" to "energized" — because that progression is the leading indicator of every revenue dollar that follows.

Everything else, in the end, is downstream of those two numbers.

IX. Bull vs. Bear Case & Epilogue

The bull case for Core Scientific writes itself if you are willing to take one analytical leap: that the public market will eventually re-rate the company from "Bitcoin miner that does some hosting" to "power-platform infrastructure landlord that happens to mine Bitcoin with its uncommitted capacity." That re-rating is not a trivial move. Mining equities trade at low single-digit multiples of forward EBITDA, reflecting both the cyclicality of crypto cash flows and the depreciation profile of ASIC fleets. High-quality data center REITs and infrastructure landlords with long-duration creditworthy tenants trade at fifteen to twenty-five times EBITDA depending on tenant quality and geographic footprint. If even half of Core Scientific's EBITDA migrates to the HPC bucket and earns the corresponding multiple, the implied equity value compounds in ways that are hard to model without quickly arriving at very large numbers.

The bull case has three independent legs. The first is the contracted backlog itself: the CoreWeave megawatts already signed, plus whatever incremental tenants the company adds across 2026 and 2027. The second is the expansion pipeline: 2.5 gigawatts of incremental interconnected capacity is, at industry-typical revenue intensity per megawatt, a transformative addition to the revenue base if even a meaningful fraction converts to signed leases. The third, and most speculative, is the operating system optionality of the Minden platform — the idea that a software stack capable of optimizing power flows across gigawatts of mixed-workload infrastructure could itself be a third revenue line, sold to peer operators or used to enter adjacent power-arbitrage and demand-response markets.

The bear case is equally articulable, and serious investors should take it at face value rather than dismiss it. The first risk is regulatory and political. Large-load data center build-outs have become a high-salience issue at the state and municipal level. Texas, Georgia, Kentucky, and other jurisdictions where Core Scientific operates have all seen policy debates in 2024 and 2025 about siting rules, special tariffs for large loads, and in some cases outright moratoria. A wave of "anti-mining" or "anti-large-load" regulation could meaningfully impair the value of pipeline megawatts that have not yet been energized.

The second risk is technological. The current generation of AI training infrastructure, with its 80-to-120-kilowatt rack densities, is at the upper edge of what Core Scientific's shells were originally designed to handle. The next generation — whatever Nvidia and its competitors ship in the back half of the decade — may push rack densities into ranges that require fundamental shell-level retrofits or, in the limit, greenfield builds. If the obsolescence cycle for AI shells turns out to be five years rather than fifteen, the comparison to traditional data center REIT multiples falls apart.

The third risk is concentration. As of 2026, the single largest HPC tenant is CoreWeave by a wide margin, and CoreWeave itself remains a relatively young company with a concentrated customer base of its own. The chain of dependencies — Core Scientific depends on CoreWeave, CoreWeave depends on a small number of hyperscale AI customers, those customers depend on the continued willingness of capital markets to fund AI capex — is real, and stress in any link of that chain transmits backward.

The fourth risk is the legacy mining segment itself. The 700 megawatts still pointed at Bitcoin is, in effect, an embedded long position on hash price. In a benign environment, that position contributes cash flow that funds the HPC pivot. In a malign environment — sharp BTC drawdown, hash rate spike — the segment becomes a cash burn that, even briefly, complicates the clean infrastructure-landlord narrative.

The myth versus reality check is worth running explicitly. The consensus narrative on Core Scientific has flipped from "doomed crypto bankruptcy" in 2022–2023 to "obvious AI winner" in 2024–2026. Both narratives are partially right and partially wrong. The 2022 doom narrative correctly diagnosed the leverage but misjudged the durability of the underlying power platform. The 2024–2026 AI-winner narrative correctly identifies the strategic value of energized capacity but tends to underweight the residual mining cyclicality, the tenant concentration, and the political risk attached to large-load build-outs. Reality, as usual, sits in the middle of the two myths.

The ultimate lesson of Core Scientific, when the dust of the cycle settles, is a lesson in capital allocation. The original team scaled the asset base brilliantly but financed it poorly. The restructuring team inherited a damaged corporate envelope but a strategically priceless physical footprint, and made the single correct decision available to them — to stop buying miners and start buying, in effect, transformers and substations and interconnect rights. The market reward for that re-allocation has been substantial. The work of converting an asset base into a durable, multi-decade infrastructure franchise is, in mid-2026, well underway but not yet finished.

The phoenix has flown. Whether it can stay airborne for the next decade is the only question that matters now.

References

-

Core Scientific Chapter 11 Restructuring Docket — Kroll Restructuring Administration, 2022–2024 ↩↩↩

-

Core Scientific to Acquire Blockcap for $1.2B — CoinDesk, 2021-07-30 ↩↩

-

Annual Report on Form 10-K (FY2023) — SEC EDGAR, 2024-03-12 ↩

-

Plan of Reorganization & Chapter 11 Emergence — Southern District of Texas Court Filings, 2024-01-23 ↩↩↩

-

Adam Sullivan CEO Employment Agreement — SEC Exhibit 10.1, 2024-06-15 ↩↩↩↩

-

Core Scientific's Pivot to AI Hosting Ignites Stock — Bloomberg Technology, 2024-07-20 ↩

-

The Power Bottleneck: Why AI Needs Bitcoin Miners — Wall Street Journal, 2024-08-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube