Cencora: The Evolution of American Pharmaceutical Distribution

I. Introduction & Episode Roadmap

Picture this: Every single day, approximately 20% of all pharmaceuticals consumed in the United States—from life-saving cancer treatments to everyday antibiotics—flow through the distribution centers of a company most Americans have never heard of. In fiscal 2024, this invisible giant generated $294 billion in revenue, making it larger than Microsoft, bigger than Coca-Cola and Disney combined, and the 10th largest company on the Fortune 500. Yet mention "Cencora" at a dinner party, and you'll likely get blank stares.

This is the paradox of pharmaceutical distribution: utterly essential, massively profitable, and completely invisible to the end consumer. While tech titans grab headlines and consumer brands shape culture, Cencora—formerly AmerisourceBergen—quietly operates as one of three companies that form an oligopoly controlling nearly 95% of all drug distribution in America. It's the ultimate toll booth business, sitting between $600 billion worth of pharmaceutical manufacturers and every hospital, pharmacy, and clinic in the nation.

The central question that drives our story today isn't just how a company becomes this large—plenty of businesses achieve scale. The real mystery is this: How did a 19th-century druggist's apprentice named Lucien Napoleon Brunswig, starting with nothing but ambition in 1871 California, lay the foundation for what would become one of the most powerful and essential companies in global healthcare? And perhaps more intriguingly, why does this matter for investors today?

What we're about to uncover is a 150-year saga of relentless consolidation, strategic brilliance, and occasional crisis that transformed American pharmaceutical distribution from thousands of local wholesalers into three global giants. It's a story that teaches us fundamental lessons about scale economics, the power of boring businesses, and why sometimes the best investments are in companies that nobody talks about at cocktail parties.

Our journey will take us from horse-drawn wagons delivering morphine in post-Civil War America to AI-powered distribution centers handling gene therapies worth millions per dose. We'll explore how three separate companies—Bergen, AmeriSource, and Brunswig—each built regional empires before merging into today's behemoth. We'll dissect the economics of why this industry naturally tends toward oligopoly, examine the strategic chess moves that created competitive moats wider than the Grand Canyon, and confront the dark chapter of the opioid crisis that nearly brought the industry to its knees.

Along the way, we'll meet fascinating characters: the visionary David Yost who orchestrated the merger that created modern AmerisourceBergen; Steven Collis, the CEO who transformed it from a domestic distributor into a global healthcare solutions platform; and the current leadership navigating everything from biosimilars to Amazon's healthcare ambitions.

Key themes will emerge throughout our narrative. First, the relentless logic of consolidation in distribution businesses—why scale isn't just an advantage but a survival requirement. Second, how technology transformed what seems like a simple logistics business into a complex, data-driven operation requiring billions in annual investment. Third, the delicate dance of managing relationships with every stakeholder in healthcare—from pharmaceutical giants like Pfizer to corner pharmacies, from regulators to patients. And finally, how a company built on 19th-century principles adapts to 21st-century disruption.

By the end of this journey, you'll understand why Warren Buffett-style investors love these kinds of businesses, why Amazon's pharmacy ambitions keep Cencora executives up at night, and why the next decade might be the most transformative in the company's century-and-a-half history. You'll see how a company can be simultaneously boring and fascinating, stable and dynamic, essential and vulnerable.

So let's begin where all great business stories start: with an ambitious young person, a problem that needs solving, and an industry ripe for transformation. The year is 1871, and Lucien Napoleon Brunswig has just arrived in California with dreams bigger than the Gold Rush itself.

II. The Origins: Three Rivers Converge (1871–2000)

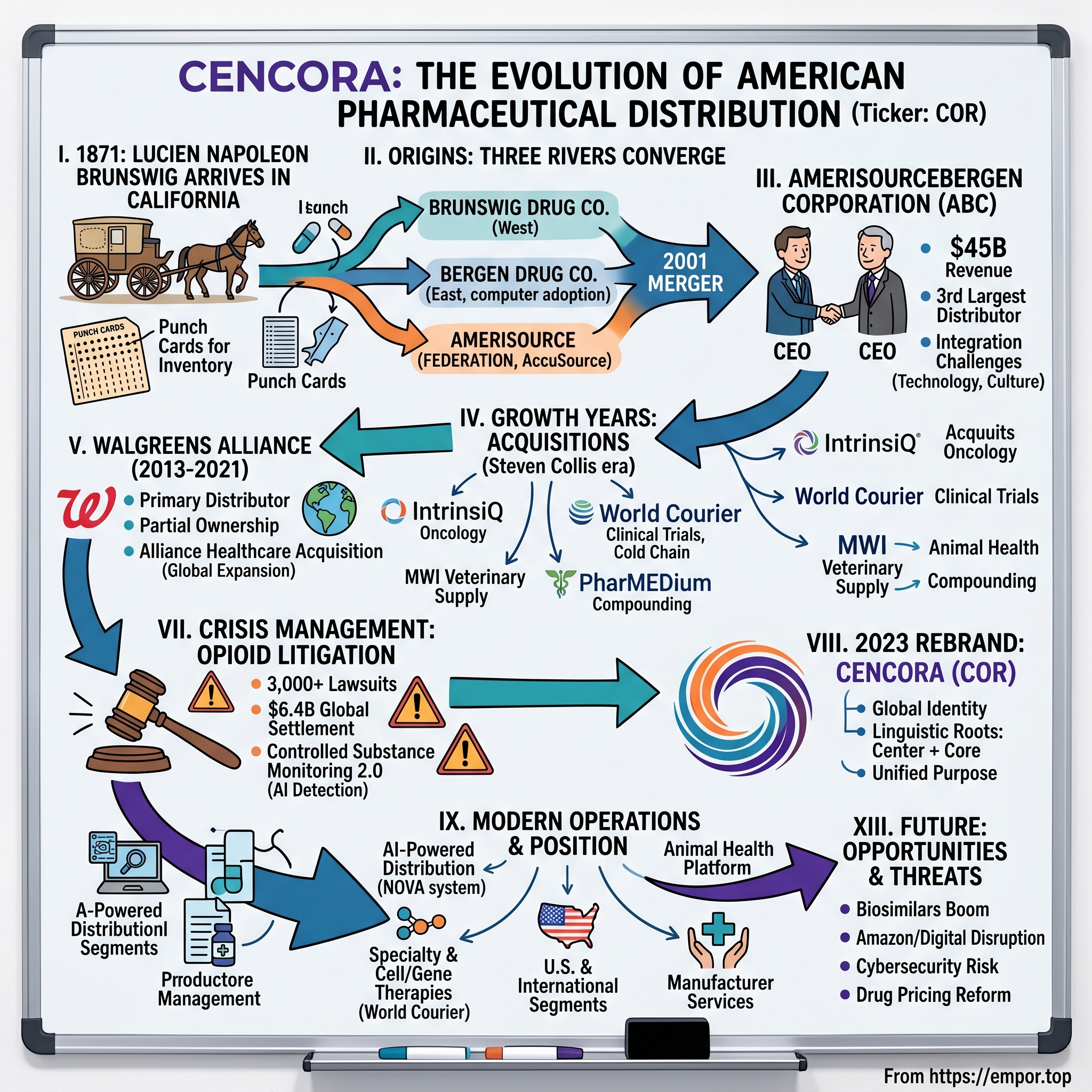

The year 1871 marked more than just another California gold rush tale. While prospectors still scoured the Sierra Nevada for the last glimmers of fortune, a different kind of entrepreneur arrived in Stockton with ambitions that would outlast any gold mine. Lucien Napoleon Brunswig, barely out of his teens, stepped off the train with the skills of a druggist's apprentice and the vision of an empire builder. He couldn't have known that his small wholesale drug operation would become the foundation of a $300 billion colossus, but perhaps he sensed what every great entrepreneur understands: infrastructure beats speculation every time.

Brunswig's timing was extraordinary. Post-Civil War America was experiencing its first pharmaceutical revolution. Morphine, discovered just decades earlier, was being mass-produced. Aspirin would soon follow. The germ theory of disease was transforming medicine from folk remedies to scientific treatments. And critically, the transcontinental railroad had just connected California to eastern pharmaceutical manufacturers. Brunswig positioned himself at the intersection of supply and demand, becoming the crucial link between East Coast drug makers and West Coast pharmacies.

What distinguished Brunswig from dozens of other wholesale druggists wasn't just ambition—it was his obsession with efficiency and technology. While competitors relied on handwritten ledgers and memory, Brunswig invested profits back into systems. He created standardized ordering processes, established credit terms that kept pharmacies loyal, and most importantly, built trust. In an era before FDA regulations, when "patent medicines" could contain anything from alcohol to cocaine, Brunswig guaranteed quality. Pharmacists knew that drugs from Brunswig were genuine, properly stored, and fairly priced.

By 1900, Brunswig Drug Company had expanded beyond California into Arizona, Nevada, and Hawaii. But the real innovation came from Brunswig's sons, who inherited the business and brought a second-generation hunger for modernization. In 1947, while most American businesses still operated with paper and filing cabinets, Brunswig Drug Company became one of the first companies in any industry to use IBM punch cards for inventory management. Think about that: a drug wholesaler was pioneering computer technology before Silicon Valley existed.

Meanwhile, 3,000 miles away in New Jersey, another dynasty was forming. The Bergen Drug Company, founded in 1888 in Hackensack, was building the East Coast equivalent of Brunswig's western empire. Where Brunswig had the frontier spirit of California, Bergen had the density and sophistication of the Northeast corridor. The company served the pharmacies of New York, Philadelphia, and Boston—markets where competition was fierce and margins were thin, forcing operational excellence.

Bergen's breakthrough came from recognizing that pharmaceutical distribution wasn't just about moving boxes—it was about information flow. In 1959, when computers were room-sized machines that cost millions, Bergen installed one of the first computerized inventory systems in the distribution industry. This wasn't just automation; it was transformation. Suddenly, Bergen could track thousands of SKUs in real-time, predict demand patterns, and optimize delivery routes with mathematical precision.

The third river in our confluence started flowing in 1977, when a group of independent regional drug wholesalers realized they needed scale to survive. They formed AmeriSource, initially as a purchasing cooperative but quickly evolving into a full-fledged distribution company. AmeriSource represented a different model—not family dynasty but federation, not top-down but collaborative. It was perfectly suited for the fragmented middle markets between the coasts.

What made AmeriSource special was its introduction of AccuSource in 1994, an electronic ordering system that seems quaint now but was revolutionary then. Pharmacies could dial into AmeriSource's servers via modem, browse inventory, place orders, and receive confirmations—all without picking up a phone. This was e-commerce before Amazon, digital transformation before it had a name. More importantly, it locked in customer relationships. Once a pharmacy invested time learning AccuSource, integrated it into their workflow, and trusted it with their business, switching costs became prohibitive.

By the late 1990s, these three companies—Brunswig on the West Coast, Bergen in the East, and AmeriSource in between—had each built regional kingdoms. But the pharmaceutical landscape was shifting beneath their feet in ways that would make consolidation not just attractive but essential.

The economics of pharmaceutical distribution were becoming brutally clear. Gross margins were shrinking from already-thin 6% to under 4%. The only way to maintain profitability was through scale—spreading fixed costs over more volume, negotiating better terms with manufacturers, and investing in technology that smaller players couldn't afford. The industry supported over 200 regional wholesalers in 1970; by 2000, that number had shrunk to fewer than 50.

But the real catalyst for change was the emergence of specialty pharmaceuticals. These weren't your grandfather's pills that could sit on a shelf for months. These were biologics requiring cold-chain logistics, cancer drugs costing $10,000 per dose, and treatments for rare diseases that needed specialized handling. The infrastructure requirements were exponentially more complex and expensive. Only the largest players could afford the specialized facilities, trained staff, and technology systems necessary to handle these products.

There was also the matter of manufacturer relationships. Pharmaceutical companies were consolidating too—Pfizer acquiring Warner-Lambert, Glaxo merging with SmithKline Beecham. These giants wanted to work with distribution partners who could handle their entire portfolio, provide national coverage, and offer sophisticated data analytics on prescription patterns. Regional wholesalers, no matter how well-run, couldn't meet these demands.

The technology revolution added another layer of pressure. By 2000, the internet was transforming every industry, and pharmaceutical distribution was no exception. But building web-based ordering systems, implementing RFID tracking, and creating real-time inventory management required massive capital investments. A regional player might need to spend 5% of revenue on technology just to stay competitive—money they didn't have.

Perhaps most importantly, the regulatory environment was becoming increasingly complex. HIPAA compliance, DEA regulations for controlled substances, state-level licensing requirements—the burden was overwhelming for smaller players. Larger companies could spread compliance costs across more volume and afford specialized legal and regulatory teams.

The hidden infrastructure of American healthcare that these three companies had built over more than a century was about to consolidate into something unprecedented. Each had pioneered different aspects of the business: Brunswig brought operational excellence and western expansion, Bergen contributed technological innovation and eastern market density, and AmeriSource offered collaborative models and middle-market penetration.

What nobody fully appreciated yet was how powerful the combination would be. It wasn't just about adding revenues or eliminating redundancies. It was about creating a network effect in physical distribution—where each additional node made the entire system more valuable. It was about data aggregation that would give unprecedented visibility into American healthcare consumption. And it was about building bargaining power that could stand toe-to-toe with both Big Pharma and large hospital systems.

The stage was set for one of the most consequential mergers in American business history—one that would create not just a large company but an essential piece of healthcare infrastructure that would prove nearly impossible to displace.

III. The Merger that Created a Giant (2001)

The boardroom at Bergen Brunswig's Orange County headquarters was thick with tension on a humid August evening in 2001. CEO Donald Roden sat across from David Yost, his counterpart at AmeriSource, both men understanding that the next few hours would determine whether their companies would thrive or merely survive in the rapidly consolidating pharmaceutical distribution landscape. Outside, the California sunset painted the sky orange, but inside, the mood was all business—spreadsheets, projections, and the cold calculus of corporate survival.

"We can keep fighting each other for scraps," Yost reportedly said, his Midwestern directness cutting through the formalities, "or we can build something that neither McKesson nor Cardinal can ignore." The math was inescapable. McKesson had just completed its acquisition of HBOC, despite the accounting scandal that followed. Cardinal Health was aggressively expanding through acquisitions. The industry was consolidating into what would inevitably become an oligopoly, and the only question was whether Bergen Brunswig and AmeriSource would be predators or prey.

The merger, announced in August 2001 and completed that October, created AmerisourceBergen Corporation—a name that awkwardly smashed together both legacies but accurately reflected the equal nature of the combination. With combined revenues of $45 billion, the new entity instantly became the third-largest pharmaceutical distributor in America, controlling roughly 23% of the market. But market share was just the beginning of the story.

David Yost, who became CEO of the combined company, brought a fascinating background to the role. An accountant by training who had worked his way up through AmeriSource's finance department, Yost understood that distribution wasn't about moving boxes—it was about managing cash flow, optimizing working capital, and creating information advantages. His vision for AmerisourceBergen wasn't just bigger; it was fundamentally different from what either predecessor company had been.

The integration challenges were monumental. Bergen Brunswig operated 26 distribution centers using one technology platform; AmeriSource had 22 facilities on completely different systems. Bergen's culture was West Coast casual with entrepreneurial flair; AmeriSource was Midwest conservative with a focus on operational discipline. The companies had overlapping facilities in 14 markets, redundant corporate functions, and incompatible processes for everything from customer service to accounts payable.

But Yost and his integration team, led by COO Kurt Hilzinger, approached the merger with surgical precision. Rather than forcing rapid integration that might disrupt customer service, they took what they called a "customer-back" approach. First, ensure no disruption to pharmaceutical deliveries. Second, identify best practices from each company. Third, implement changes gradually with constant monitoring of service levels.

The technology integration alone was a three-year, $150 million project. Rather than choosing one system over another, AmerisourceBergen built an entirely new platform that took the best elements from both companies. Bergen's sophisticated inventory management algorithms were combined with AmeriSource's superior order-entry interface. The result was a system that could handle 15 million transactions daily with 99.9% accuracy—a rate that seems standard now but was revolutionary in 2001.

The economics of the combined entity were compelling. By consolidating purchasing, AmerisourceBergen could negotiate better terms with manufacturers—not just on price but on payment schedules, return policies, and inventory management. A 0.1% improvement in payment terms might seem trivial, but when you're handling $45 billion in inventory, that translates to $45 million in working capital efficiency.

The distribution network optimization was equally powerful. The combined company could serve 98% of the U.S. population with next-day delivery from just 26 strategically located distribution centers. This wasn't just about closing redundant facilities—though they did close eight in the first year. It was about creating a network where inventory could be dynamically allocated based on demand patterns, where emergency shipments could be sourced from multiple locations, and where seasonal fluctuations could be absorbed without disruption.

But the real strategic insight was in specialty pharmaceuticals. Both companies had nascent specialty divisions, but neither had achieved critical mass. The combined entity could afford to build specialized facilities for oncology drugs, create dedicated sales forces for rare disease treatments, and invest in the complex logistics required for biologics. Within eighteen months of the merger, AmerisourceBergen's specialty revenue had grown from $2 billion to $5 billion—a growth rate that would have been impossible for either company alone.

The manufacturer services division represented another strategic breakthrough. Pharmaceutical companies increasingly wanted partners who could do more than just distribute drugs. They needed data analytics on prescription patterns, support for patient assistance programs, and help with inventory management at the hospital level. AmerisourceBergen could now offer a full suite of services that turned them from vendor to strategic partner.

The cultural integration, often the Achilles heel of mergers, was handled with unusual sophistication. Rather than imposing one culture on the other, Yost created what he called a "best athlete" approach. Each position in the combined company would go to the most qualified person regardless of legacy company, and the culture would be built fresh rather than inherited. This meant some awkward moments—Bergen executives reporting to former AmeriSource managers and vice versa—but it prevented the us-versus-them dynamic that poisons many mergers.

The financial markets initially responded with skepticism. The stock price dropped 15% in the first month after the merger announcement, with analysts worried about integration costs and margin pressure. But by the end of 2002, with integration proceeding smoothly and synergies exceeding projections, the stock had recovered and then some. The company was generating $500 million in free cash flow, margins had stabilized at 1.8%, and return on equity exceeded 25%.

The competitive response was swift and aggressive. McKesson accelerated its acquisition strategy, buying smaller regional players to protect market share. Cardinal Health invested heavily in technology, trying to leap-frog AmerisourceBergen's systems advantages. But the die was cast—the industry had crystallized into three major players, each with roughly a third of the market, each too large to be acquired, each essential to the functioning of American healthcare.

What made this merger special wasn't just its size or timing—it was the recognition that in distribution businesses, there's a tipping point where scale becomes self-reinforcing. Once AmerisourceBergen achieved national coverage, manufacturer relationships became stickier. Once they had the volume to justify technology investments, operational advantages compounded. Once they had the data from millions of transactions, they could offer insights that smaller players simply couldn't match.

The creation of AmerisourceBergen also marked a philosophical shift in pharmaceutical distribution. This was no longer about being a passive intermediary between manufacturers and pharmacies. This was about being an active participant in the healthcare ecosystem—managing complexity, ensuring compliance, providing intelligence, and ultimately becoming so embedded in the system that extraction would be nearly impossible.

Looking back, the 2001 merger was the inflection point that transformed American pharmaceutical distribution from a fragmented, regional, low-margin business into a consolidated, national, technology-driven oligopoly. It set the template for everything that would follow: aggressive acquisition strategies, massive technology investments, expansion into adjacent services, and the creation of competitive moats that would prove remarkably durable. The giant had been born, and now it was time to grow.

IV. Building Through Acquisition: The Growth Years (2001–2014)

Steven Collis had an unusual ritual. Every morning before dawn, the newly appointed CEO of AmerisourceBergen would review a handwritten list he kept in his desk drawer—not of financial targets or strategic objectives, but of problems his customers faced that technology hadn't yet solved. "Pain points," he called them, though his British accent made the phrase sound almost elegant. When he assumed the CEO role in July 2011, that list would become the roadmap for one of the most aggressive acquisition sprees in pharmaceutical distribution history.

Collis inherited a solid but unspectacular business. AmerisourceBergen was profitable, stable, and utterly boring to Wall Street. The stock had traded in a narrow range for three years. Analysts described the company with words like "mature" and "steady"—corporate speak for "going nowhere fast." But Collis saw something different. He saw a platform that could be transformed from a distribution company into what he called a "healthcare solutions orchestrator."

The first major move came just months into his tenure. In September 2011, AmerisourceBergen acquired IntrinsiQ for $35 million—a price that seemed almost quaint but represented a strategic earthquake. IntrinsiQ wasn't a distributor; it was a technology company specializing in oncology practice management. They provided software that helped cancer clinics manage everything from chemotherapy protocols to billing codes. Why would a distribution company want this?

Collis understood something his predecessors hadn't fully grasped: in specialty pharmaceuticals, particularly oncology, the product and the service were becoming inseparable. Cancer drugs weren't just expensive—some cost $30,000 per month—they were complex to administer, required careful monitoring, and came with byzantine reimbursement requirements. Oncology practices didn't just need someone to deliver drugs; they needed a partner to help manage the entire treatment process. IntrinsiQ gave AmerisourceBergen a foot in the door of every cancer clinic in America, not as a vendor but as an essential technology partner.

The Premier Source acquisition, completed the same year, attacked a different pain point. Premier Source specialized in "alternate site" distribution—delivering pharmaceuticals to places that weren't traditional pharmacies or hospitals. Think dialysis centers, surgery centers, long-term care facilities. These customers had unique needs: they ordered in smaller quantities, needed more frequent deliveries, and required specialized packaging. Premier Source had built the infrastructure to serve these customers profitably—something the big three distributors had struggled with.

But the real statement of intent came in 2012 with the $520 million acquisition of World Courier. On paper, this made no sense. World Courier didn't distribute pharmaceuticals to pharmacies; they provided specialized logistics for clinical trials. They could ship a single vial of experimental medicine from a lab in Switzerland to a patient in São Paulo, maintaining cold-chain custody the entire way, navigating customs, and ensuring perfect documentation. Their average shipment value was 1,000 times higher than AmerisourceBergen's, their customer base completely different, their expertise seemingly unrelated.

Yet Collis saw the future. Cell and gene therapies were moving from science fiction to reality. These treatments, often costing over $1 million per patient, required logistics capabilities that traditional distribution couldn't provide. They needed to be stored at -180°C, transported in liquid nitrogen, and tracked with military precision. World Courier gave AmerisourceBergen capabilities that would become essential as medicine became more personalized and complex.

The acquisition strategy accelerated in 2015 with two transformative deals. First came MWI Veterinary Supply for $2.5 billion—AmerisourceBergen's entry into animal health. The board initially resisted. "We're a human pharmaceutical company," one director reportedly said. "What do we know about dog medicine?" But Collis painted a different picture. The animal health market was growing at 8% annually, twice the rate of human pharmaceuticals. The customers—veterinary clinics—had similar needs to human healthcare providers but were underserved by technology. And critically, there were synergies: many drugs were used in both human and animal medicine, the distribution infrastructure was similar, and the regulatory requirements overlapped.

MWI wasn't just about entering a new market; it was about applying AmerisourceBergen's capabilities to an adjacent space where they could have competitive advantages. The company's scale allowed them to negotiate better terms with animal health manufacturers. Their technology infrastructure could be adapted for veterinary clinics. Their compliance expertise translated directly. Within two years, the animal health division was generating returns above the corporate average.

The second 2015 mega-deal—PharMEDium for $2.58 billion—addressed a different opportunity. PharMEDium was the largest sterile compounding company in America, preparing customized medications for hospitals. This was a business with significant regulatory risk (compounding pharmacies had been under FDA scrutiny), but also enormous strategic value. Hospitals increasingly wanted to outsource complex pharmaceutical preparation. They needed partners who could prepare chemotherapy doses, create pediatric formulations, and manage sterile preparation rooms. PharMEDium gave AmerisourceBergen a presence inside hospitals that went far beyond traditional distribution.

What distinguished Collis's acquisition strategy from typical corporate empire-building was the intellectual coherence. Each acquisition addressed a specific customer pain point from that hand-written list. Each expanded AmerisourceBergen's capabilities in ways that made them harder to displace. And crucially, each generated data and relationships that made the next acquisition more valuable.

The integration playbook evolved with each deal. Rather than immediately merging operations, AmerisourceBergen would first focus on revenue synergies—cross-selling services, sharing customer relationships, bundling offerings. Cost synergies came later, after customer relationships were secured. This patient approach meant acquisitions took longer to fully integrate but had much higher success rates.

The technology investments during this period were equally aggressive but less visible. Between 2011 and 2014, AmerisourceBergen spent over $1 billion on technology infrastructure—more than many Silicon Valley companies. But this wasn't sexy consumer-facing innovation. This was enterprise resource planning, warehouse automation, predictive analytics, and blockchain pilots for supply chain tracking. Boring? Absolutely. Essential? Completely.

Consider the Good Neighbor Pharmacy program, launched in 2012. This wasn't an acquisition but an internal innovation that showed how the company was thinking differently. Independent pharmacies were getting crushed by CVS and Walgreens. They needed help with everything from store design to marketing to insurance negotiations. AmerisourceBergen created a franchise-like program that gave independents the tools to compete while keeping them as distribution customers. By 2014, over 2,000 pharmacies had joined, creating a network that rivaled the major chains.

The financial results validated the strategy. Revenue grew from $80 billion in 2011 to $120 billion in 2014. More importantly, the revenue mix shifted toward higher-margin services. Specialty pharmaceuticals grew from 15% to 30% of revenue. Manufacturer services expanded from a negligible contribution to over $1 billion in high-margin fees. Return on invested capital increased from 12% to 18%, exceptional for a distribution business.

Wall Street finally took notice. The stock price doubled between 2011 and 2014, outperforming both the S&P 500 and healthcare indices. Analysts upgraded their ratings, with one Goldman Sachs report describing AmerisourceBergen as "transforming from a commodity distributor to a value-added healthcare services company." The boring distributor had become a growth story.

But the most important transformation was in customer relationships. By 2014, AmerisourceBergen wasn't just delivering drugs to customers; they were managing oncology protocols, running hospital pharmacies, providing practice management software, handling clinical trial logistics, and enabling independent pharmacies to survive. They had become, in many cases, impossible to replace without disrupting patient care.

This period established a template that would define AmerisourceBergen's strategy for the next decade: identify a customer pain point, acquire or build capabilities to address it, integrate thoughtfully to preserve value, and leverage the enhanced platform for the next opportunity. It was methodical, unsexy, and incredibly effective. The growth years had transformed AmerisourceBergen from one of three similar distributors into something unique—a healthcare solutions platform disguised as a distribution company. And the transformation was just beginning.

V. The Walgreens Alliance & Strategic Partnership (2013–2021)

The phone call came at 2 AM London time. Stefano Pessina, the Italian billionaire who controlled Walgreens Boots Alliance, had a reputation for unconventional timing and even more unconventional deals. Steven Collis, attending a healthcare conference in Switzerland, took the call in his hotel bathroom to avoid waking his wife. What Pessina proposed over the next forty minutes would reshape the American pharmaceutical supply chain and challenge every assumption about vertical integration in healthcare.

"Steven," Pessina began in his distinctive accent, "we are wasting enormous energy fighting over pennies. What if we stopped competing and started collaborating?" It was March 2013, and Walgreens—America's largest pharmacy chain with over 8,000 stores—was at war with Express Scripts, having just ended a bitter dispute that had cost both companies billions. Pessina, who had built Alliance Boots into Europe's pharmacy giant before selling to Walgreens, understood that the real battle wasn't between pharmacies and distributors but between traditional healthcare and new disruptors like Amazon.

The initial partnership, announced in March 2013, seemed modest enough. AmerisourceBergen would become Walgreens' primary pharmaceutical distributor, and Walgreens would have the option to acquire up to 23% of AmerisourceBergen over time. But the strategic implications were profound. This wasn't just a supply agreement; it was an acknowledgment that the traditional boundaries between manufacturer, distributor, and pharmacy were dissolving.

The economics were compelling for both sides. Walgreens would save an estimated $1 billion annually through better purchasing terms and supply chain efficiency. AmerisourceBergen would gain a guaranteed customer representing 20% of revenues—stability that's gold in the distribution business. But the real value was in what they could build together: data sharing that would optimize inventory across the entire network, joint programs for specialty pharmaceuticals, and coordinated strategies for combating insurance companies' power.

By 2016, the partnership had evolved into partial ownership. Walgreens Boots Alliance purchased 22.7 million shares, taking a 15% stake in AmerisourceBergen. The market initially panicked—was this the beginning of full vertical integration? Would AmerisourceBergen lose its independence? The stock dropped 8% on the announcement. But Collis and Pessina had structured the deal carefully. Walgreens got board representation and strategic input, but AmerisourceBergen remained independent, free to serve CVS, Rite Aid, and thousands of independent pharmacies.

The real masterstroke came in 2018 with the acquisition of H.D. Smith, a regional distributor that Walgreens had initially agreed to buy. In a complex three-way transaction, AmerisourceBergen acquired H.D. Smith's distribution assets while Walgreens took its retail pharmacies. This wasn't just financial engineering—it was strategic positioning. H.D. Smith had deep relationships with independent pharmacies in the Midwest and Southeast. These independents were terrified of being squeezed between the big chains and Amazon. AmerisourceBergen could now offer them a lifeline: the supply chain efficiency of a major distributor combined with programs to help them compete.

But the defining moment of the partnership came in 2021 with the $6.5 billion acquisition of Alliance Healthcare. This wasn't just another acquisition—it was AmerisourceBergen's transformation into a truly global company. Alliance Healthcare, the distribution arm of Walgreens Boots Alliance, operated across 11 European countries, serving 110,000 pharmacies and doctors. The deal structure was elegant: $6.275 billion in cash plus 2 million shares of AmerisourceBergen, deepening Walgreens' ownership while giving AmerisourceBergen European scale.

The Alliance Healthcare acquisition addressed multiple strategic imperatives simultaneously. First, it gave AmerisourceBergen geographic diversification—important as U.S. healthcare policy became increasingly unpredictable. Second, it provided access to European pharmaceutical manufacturers who were increasingly important in biosimilars and specialty drugs. Third, it created a global platform for serving multinational pharmaceutical companies who wanted consistent partners across markets.

The integration of Alliance Healthcare revealed how sophisticated AmerisourceBergen had become at acquisitions. Rather than imposing American processes on European operations, they took what CEO Collis called a "federal approach." Each country maintained its local relationships and cultural nuances while sharing technology platforms, purchasing power, and best practices. The European operations taught the Americans about direct-to-patient distribution models; the Americans shared expertise in specialty pharmaceuticals and data analytics.

The manufacturer services capabilities that came with Alliance Healthcare were particularly valuable. European countries had different models for pharmaceutical distribution—some with single-payer systems, others with complex insurance schemes. Alliance Healthcare had built capabilities to navigate these differences, skills that would become valuable as the U.S. healthcare system potentially evolved toward more government involvement.

Throughout this period, the relationship with Walgreens created unexpected innovations. The two companies jointly developed a program for specialty pharmacies, combining AmerisourceBergen's distribution expertise with Walgreens' retail presence. They created AllianceRx, a combined specialty pharmacy that became one of the largest in America, handling complex medications for conditions like cancer, HIV, and multiple sclerosis. This wasn't just about dispensing drugs—it was about patient support, insurance navigation, and therapy management.

The partnership also accelerated technology adoption. Walgreens and AmerisourceBergen jointly invested in blockchain pilots for pharmaceutical tracking, addressing the growing problem of counterfeit drugs. They collaborated on predictive analytics for flu vaccine demand, ensuring the right vaccines reached the right stores at the right time. They even experimented with drone delivery for rural areas, though this remained more prototype than product.

The financial impact was substantial. The Walgreens partnership provided stability that allowed AmerisourceBergen to invest more aggressively in technology and acquisitions. The guaranteed volume from Walgreens improved negotiations with manufacturers. The strategic alignment helped both companies respond more quickly to market changes. By 2021, AmerisourceBergen's revenue had grown to $214 billion, with international operations contributing nearly 15% following the Alliance Healthcare acquisition.

Yet the partnership wasn't without tensions. Other pharmacy chains worried about AmerisourceBergen's neutrality—would they favor Walgreens in allocation decisions during drug shortages? Independent pharmacies feared being squeezed out. Some investors questioned whether partial vertical integration created more problems than it solved. These concerns required constant management, with Collis spending considerable time reassuring stakeholders that AmerisourceBergen remained an independent, neutral distributor.

The Walgreens alliance also highlighted a fundamental strategic question: in an era of healthcare consolidation, could you remain truly independent? CVS had acquired Aetna, creating a vertically integrated behemoth. UnitedHealth owned both insurance and care delivery through Optum. Amazon was entering pharmacy with unclear but potentially devastating intentions. The Walgreens partnership gave AmerisourceBergen strategic options without full commitment—they could deepen the relationship if vertical integration proved necessary or maintain independence if that remained viable.

Looking back, the Walgreens partnership was about more than financial engineering or supply chain efficiency. It was recognition that healthcare's traditional boundaries were dissolving. Distributors weren't just moving boxes; they were managing patient care. Pharmacies weren't just dispensing pills; they were becoming health clinics. Insurance companies weren't just paying claims; they were directing care. In this blurring landscape, strategic partnerships became essential for survival.

The partnership model—deep collaboration without full integration—might prove to be AmerisourceBergen's most important innovation. It provided the benefits of vertical integration (efficiency, coordination, data sharing) without the downsides (regulatory scrutiny, channel conflict, reduced flexibility). It was a middle path that allowed AmerisourceBergen to serve all customers while having a special relationship with one. And as the next phase of healthcare transformation began, this flexibility would prove invaluable.

VI. The Animal Health Expansion: MWI and Beyond (2015–Present)

Dr. Sarah Chen was performing emergency surgery on a German Shepherd at 3 AM when her inventory system alerted her that she was down to her last vial of propofol. Five years ago, she would have panicked. Now, she simply confirmed the automated reorder on her phone, knowing MWI Veterinary Supply would deliver before her first appointment tomorrow. What Dr. Chen didn't realize was that her simple order confirmation represented the culmination of a strategic bet AmerisourceBergen made in 2015—that the future of animal health would mirror human healthcare's evolution, just a decade behind.

The $2.5 billion acquisition of MWI Veterinary Supply in February 2015 had initially puzzled Wall Street analysts. "Stick to your knitting," one particularly blunt analyst had told Steven Collis on the earnings call. "What's next, distributing to zoos?" But Collis saw patterns others missed. The humanization of pets had fundamentally changed animal healthcare. Americans spent $35 billion on veterinary care in 2015, up from $11 billion just a decade earlier. Dogs were getting chemotherapy. Cats were receiving kidney transplants. Horses were undergoing MRI scans. The sophisticated pharmaceuticals and medical devices needed for these treatments required distribution capabilities that mom-and-pop animal health distributors simply couldn't provide.

MWI wasn't just the largest animal health distributor in America—it was also the most technologically advanced. Their VINE (Veterinary Information Network) platform connected 12,000 veterinary clinics, providing everything from inventory management to prescription processing to continuing education. This wasn't just distribution infrastructure; it was the nervous system of American veterinary medicine.

The integration revealed unexpected synergies. Many pharmaceuticals were used in both human and animal medicine—antibiotics, pain medications, even some cancer drugs. AmerisourceBergen could now negotiate with manufacturers for combined volumes, improving terms for both divisions. The regulatory expertise translated directly—DEA licenses, controlled substance management, cold chain requirements were nearly identical. Even the customer service models were similar, with veterinary clinics having comparable needs to independent pharmacies.

But the real innovation came from applying AmerisourceBergen's human healthcare playbook to animal health. Just as they had created Good Neighbor Pharmacy to support independent pharmacies, they launched Vets First Choice (later rebranded as Covetrus after a merger), providing technology and services to help independent veterinary practices compete with corporate chains. The platform included everything from online pharmacy capabilities to payment processing to client communication tools.

The telehealth revolution, accelerated by COVID-19, hit veterinary medicine with particular force. Pet owners, having experienced telemedicine for themselves, demanded similar convenience for their animals. AmerisourceBergen responded by acquiring and developing platforms that allowed veterinarians to conduct virtual consultations, prescribe medications digitally, and have them delivered directly to pet owners' homes. The traditional model—where pet owners had to physically visit a clinic for every prescription—was crumbling.

AllyDVM, launched in 2018, represented the culmination of this digital transformation. It wasn't just practice management software; it was an entire ecosystem. Veterinarians could manage appointments, process payments, order inventory, communicate with pet owners, and even access AI-powered diagnostic support. The platform processed over $2 billion in transactions annually by 2021, making it one of the largest fintech platforms in veterinary medicine.

The specialty pharmaceutical opportunity in animal health proved particularly lucrative. Monoclonal antibodies for canine cancer, gene therapies for inherited diseases, biologics for chronic conditions—these high-value medications required the same specialized handling as human specialty drugs. AmerisourceBergen's existing infrastructure for human specialty pharmaceuticals could be leveraged with minimal additional investment. By 2020, specialty medications represented 25% of animal health pharmaceutical revenue, with margins significantly higher than traditional medications.

The data insights from animal health created unexpected value. Patterns in pet medication usage often preceded human trends—for instance, increased anxiety medication prescriptions in dogs correlated with subsequent increases in human prescriptions in the same geographic areas. Pharmaceutical manufacturers paid significant fees for these insights, viewing pet populations as valuable sentinel indicators for human health trends.

The international expansion of animal health followed a different pattern than human pharmaceuticals. In many developing countries, veterinary infrastructure was being built fresh without legacy systems. AmerisourceBergen could deploy cloud-based platforms and modern logistics systems without dealing with entrenched competitors or outdated regulations. By 2023, the animal health division had operations in 15 countries, with international revenue growing at 20% annually.

The One Health initiative—recognizing the interconnection between human, animal, and environmental health—became more than just a marketing slogan. When COVID-19 emerged, likely from animal origins, the importance of integrated health surveillance became obvious. AmerisourceBergen's position at the intersection of human and animal health gave them unique visibility into disease patterns. They partnered with the CDC and USDA on surveillance programs, tracking everything from antibiotic resistance to emerging zoonotic diseases.

The competitive dynamics in animal health distribution differed markedly from human pharmaceuticals. Instead of competing with McKesson and Cardinal Health, AmerisourceBergen faced Patterson Companies and Henry Schein. These competitors, primarily focused on dental and medical devices, lacked AmerisourceBergen's pharmaceutical expertise. This created a sustainable competitive advantage—as animal medications became more sophisticated, AmerisourceBergen's capabilities became more valuable.

The direct-to-consumer challenge emerged differently in animal health. Chewy, the pet e-commerce giant, launched Chewy Pharmacy in 2018, threatening traditional distribution models. Rather than fighting this disruption, AmerisourceBergen partnered with online retailers, providing the backend pharmaceutical fulfillment while letting others handle customer acquisition. This "white label" approach allowed them to participate in the direct-to-consumer revolution without channel conflict.

Regulatory changes created both challenges and opportunities. The FDA's increased scrutiny of compounded animal medications created demand for manufactured alternatives. AmerisourceBergen's PharMEDium acquisition, originally focused on human medications, expanded into veterinary compounding, providing standardized preparations that met FDA requirements. This vertical integration into manufacturing, unthinkable in human pharmaceuticals, was possible in the less regulated animal health market.

The financial performance validated the strategy. The animal health division generated $6 billion in revenue by 2023, with EBITDA margins exceeding 8%—double the corporate average. Return on invested capital exceeded 20%, making it one of AmerisourceBergen's most successful acquisitions. The stability of animal health—pet owners don't stop treating sick animals during recessions—provided valuable diversification during economic uncertainty.

Looking forward, the animal health division positioned AmerisourceBergen for emerging opportunities. The growing field of comparative oncology—using naturally occurring cancers in pets to develop human treatments—required integrated human and animal health capabilities. The expansion of gene therapies from humans to animals would leverage existing infrastructure. Even the emerging field of cultivated meat would require pharmaceutical-grade production and distribution capabilities.

The animal health expansion demonstrated AmerisourceBergen's ability to identify and exploit adjacent markets. What seemed like a distraction to Wall Street analysts proved to be a natural extension of core capabilities. By recognizing that animal health was following the same trajectory as human healthcare—just compressed and accelerated—AmerisourceBergen positioned itself to capture value from both evolution and revolution.

More fundamentally, the animal health business proved that AmerisourceBergen's capabilities transcended specific markets. The ability to manage complex supply chains, navigate regulations, integrate technology, and serve diverse customers was transferable. If they could successfully expand from human to animal health, what other adjacent markets might be possible? The question would become increasingly relevant as traditional healthcare boundaries continued to blur.

VII. Crisis Management: The Opioid Litigation

The subpoena arrived on a gray Tuesday morning in November 2017, delivered by two DEA agents who waited in the lobby while AmerisourceBergen's legal team scrambled to understand its implications. The document demanded ten years of records related to opioid distribution, focusing on shipments to pharmacies in West Virginia, Ohio, and Florida. This wasn't the company's first encounter with opioid-related investigations, but something felt different this time. The political climate had shifted. The death toll had become undeniable. And the public was demanding accountability from every link in the pharmaceutical chain.

Steven Collis召集了an emergency meeting of his senior leadership team that afternoon. The general counsel laid out the stark reality: AmerisourceBergen had distributed billions of opioid pills over the past decade, all legally, all following DEA regulations, all ordered by licensed pharmacies. But legal compliance might not be enough anymore. The court of public opinion was rendering its verdict, and the financial markets were already responding—the stock had dropped 7% since news of the investigation leaked.

The numbers were staggering and undeniable. Between 2006 and 2012, AmerisourceBergen had distributed 9.4 billion opioid pills nationwide. In Mingo County, West Virginia—population 25,000—they had shipped enough pills for every resident to have 150 pills per year. The company's defense was technically accurate: they were distributors, not prescribers. They filled orders from licensed pharmacies based on prescriptions from licensed doctors. The DEA set quotas and monitoring requirements, which AmerisourceBergen followed. But technical accuracy wasn't winning the narrative battle.

The first major lawsuit came from Michigan in 2019, seeking damages for the state's opioid crisis response costs. Then Ohio, with its $260 million settlement demand. Oklahoma followed, then Florida, then a cascade of counties, cities, and Native American tribes. By early 2020, AmerisourceBergen faced over 3,000 separate lawsuits. The legal costs alone were approaching $100 million annually, and the potential liability was in the tens of billions.

The company's initial response followed the traditional corporate playbook: deny wrongdoing, assert legal compliance, fight each case individually. But as the death toll mounted—70,000 Americans died from opioid overdoses in 2019 alone—this strategy became untenable. The photographs of victims, the testimony of grieving families, the documentation of pills flooding small communities created a narrative that no amount of legal argumentation could counter.

The turning point came during a deposition in Cleveland, when a plaintiff's attorney presented internal emails from 2008. An AmerisourceBergen compliance officer had flagged a Florida pharmacy ordering unusual quantities of oxycodone. The response from sales: "They're a good customer. They pay on time." The order was filled. That pharmacy was later shut down as a pill mill, but not before distributing millions of pills that ended up on the black market. The email chain was legally ambiguous—no laws were clearly broken—but the optics were devastating.

Collis made a strategic decision that would define his legacy: AmerisourceBergen would participate in a global settlement rather than fight each case. This wasn't an admission of guilt—the company maintained it had followed all regulations—but a recognition that continued litigation would destroy shareholder value and distract from operations. The board initially resisted. Some directors argued that settling would set a dangerous precedent, making distributors liable for the entire pharmaceutical supply chain.

The negotiations were byzantine, involving three distributors (AmerisourceBergen, McKesson, and Cardinal Health), dozens of state attorneys general, thousands of local governments, and teams of lawyers that filled entire hotels. The distributors were united in their position: they would pay for remediation but wouldn't accept criminal liability. The states wanted both money and accountability. The local governments just wanted resources to deal with the crisis.

In July 2021, the framework of a $26 billion global settlement was announced. The three distributors would collectively pay $21 billion over 18 years, with AmerisourceBergen's share approximately $6.4 billion. Additionally, they agreed to establish an independent clearinghouse to track opioid shipments, enhanced monitoring systems, and restrictions on shipping to pharmacies that showed signs of diversion.

The financial impact was significant but manageable. AmerisourceBergen took a $6.7 billion charge, funded through a combination of cash reserves, debt, and future cash flows. The stock initially dropped 12% but recovered within months as investors realized the settlement removed a major uncertainty. The payment schedule—spread over 18 years—meant annual costs of roughly $350 million, less than 0.2% of revenue.

But the operational changes were more profound. AmerisourceBergen implemented what they called "Controlled Substance Monitoring Program 2.0," using artificial intelligence to detect unusual ordering patterns. Any pharmacy showing statistical anomalies—orders increasing more than 30% year-over-year, ratios of controlled to non-controlled substances exceeding thresholds—triggered automatic review. The system generated 10,000 alerts monthly, each requiring human investigation.

The compliance infrastructure expansion was massive. The controlled substances team grew from 50 to 500 employees. Technology investments exceeded $200 million. Training programs reached every employee who touched pharmaceutical distribution. The company even hired former DEA agents to lead regional compliance teams, bringing regulatory expertise in-house.

The reputational rehabilitation required equal attention. AmerisourceBergen launched the "Safe Supply Chain Initiative," partnering with medical schools to educate doctors about appropriate prescribing. They funded addiction treatment programs in hard-hit communities. They supported prescription drug take-back programs, collecting and destroying unused medications. These programs cost millions but were essential for rebuilding trust.

The crisis also catalyzed strategic changes. AmerisourceBergen accelerated its shift toward specialty pharmaceuticals, which had lower diversion risk and higher margins. They expanded medication therapy management services, helping ensure appropriate use of all medications, not just opioids. They even developed blockchain-based tracking systems that could follow individual pills from manufacturer to patient, making diversion nearly impossible.

The relationship with manufacturers evolved significantly. Pharmaceutical companies, facing their own opioid lawsuits, demanded distributors take more responsibility for preventing diversion. This created tension—distributors argued they couldn't be expected to second-guess doctors' prescriptions—but also opportunity. AmerisourceBergen's enhanced monitoring capabilities became a selling point, with manufacturers preferring distributors who could minimize liability risk.

The regulatory environment transformed completely. The DEA, previously focused on quotas and paperwork, now demanded real-time data on shipments. States imposed their own monitoring requirements, creating a patchwork of regulations that required constant navigation. AmerisourceBergen's compliance costs increased five-fold, but this also created barriers to entry—smaller distributors simply couldn't afford the infrastructure.

Looking back, the opioid crisis was AmerisourceBergen's darkest chapter but also a defining moment. The company's initial response—legal but tone-deaf—nearly destroyed decades of reputation building. The settlement, while costly, provided closure and clarity. The operational changes, while expensive, created competitive advantages. Most importantly, the crisis forced a reckoning with the responsibilities that come with being essential infrastructure in healthcare.

The lessons were sobering. Legal compliance wasn't sufficient when public health was at stake. Market position created moral obligations beyond shareholder returns. Crisis management required not just legal and financial expertise but emotional intelligence and social awareness. And sometimes, the cost of fighting was higher than the cost of settling, even when you believed you were right.

By 2023, the acute phase of the crisis had passed. Opioid shipments had declined 40% from their peak. The enhanced monitoring systems had become routine. The settlement payments were built into financial projections. But the scars remained—in communities devastated by addiction, in families destroyed by overdoses, and in a distribution industry forever changed by its role in a national tragedy. AmerisourceBergen had survived, but survival had come at a price measured in more than dollars.

VIII. The Rebrand: From AmerisourceBergen to Cencora (2023)

The focus groups were brutal. When marketing consultants showed the name "AmerisourceBergen" to healthcare professionals in Berlin, Tokyo, and São Paulo, the responses ranged from confusion to complete inability to pronounce it. One German pharmacist attempted "Amerisource-Bergen" five times before giving up, laughing nervously. A Japanese hospital administrator asked if it was three separate companies. The Brazilian doctor simply said, "This is very American, no?" Steven Collis, watching from behind one-way glass, turned to his CMO and said, "We've outgrown our name."

The journey to rebranding had been percolating since the Alliance Healthcare acquisition in 2021. AmerisourceBergen now operated in 50 countries, employed 46,000 people globally, and generated nearly 20% of revenue outside the United States. Yet the name screamed American regional distributor—a legacy of the 2001 merger that created the company. Employees in France felt no connection to "Bergen" or "Amerisource." Partners in Japan struggled to explain what the company did. Even in America, the name had become a liability, forever linked in Google searches to opioid lawsuits.

The board meeting where Collis proposed the rebrand was contentious. "We're throwing away 150 years of brand equity," one director argued. Another worried about the cost—rebranding a $250 billion company wouldn't be cheap. But Collis had data. Employee surveys showed only 31% of international staff felt connected to the company mission. Customer research indicated confusion about capabilities—many thought AmerisourceBergen only distributed drugs in America. And critically, talent acquisition was suffering. Top technology and healthcare executives wouldn't consider joining a company whose name they couldn't pronounce.

The naming process took eighteen months and cost $15 million. The branding firm Lippincott interviewed 500 stakeholders, analyzed 3,000 potential names, and conducted linguistic screening in 50 languages. The criteria were exacting: the name needed to work globally, convey centrality and connection, avoid pharmaceutical clichés, be available as a domain and trademark, and somehow honor the company's heritage while signaling its future.

"Cencora" emerged from an unexpected source. A junior designer, herself an immigrant from Colombia, had been playing with linguistic roots. "Cen" suggested center across Indo-European languages. "Cor" meant heart in Latin, core in English. The "a" ending felt open, global, approachable. When she presented "Cencora" in a brainstorming session, the room went quiet. It was simple, pronounceable, meaningful. It suggested both centeredness and connection, core and heart.

The announcement strategy was carefully orchestrated. On May 15, 2023, Collis stood before employees at 30 locations worldwide, connected via satellite, to unveil the new identity. "We are not changing who we are," he emphasized. "We are declaring who we've become." The visual identity—a dynamic spiral suggesting both connection and movement—replaced the staid blue bars of the old logo. The tagline, "United in our purpose," emphasized global unity while acknowledging local diversity.

Wall Street's reaction was mixed. The stock ticker would change from ABC to COR on August 30, 2023—a symbolic shift from alphabetic accident to meaningful designation. Some analysts dismissed it as expensive corporate navel-gazing. Others saw strategic logic. Jefferies wrote: "The rebrand signals AmerisourceBergen's transformation from U.S. distributor to global healthcare solutions platform. The unified identity should accelerate international expansion and partnership opportunities."

The implementation was staggeringly complex. Over 40 distribution centers needed new signage. Thousands of trucks required repainting. Millions of documents, from invoices to contracts, needed updating. The IT systems alone—changing every instance of "AmerisourceBergen" in code that had accumulated over decades—cost $50 million. Every employee email address changed. Every business card was replaced. Even the company jets were repainted with the new livery.

But the rebrand went deeper than logos and letterheads. Cencora represented a philosophical shift. The company introduced new values: "We unite to create healthier futures." The emphasis shifted from operational excellence (though that remained critical) to purpose and impact. Employee programs were redesigned around these themes. Performance reviews incorporated purpose-driven metrics. Even supplier contracts included commitments to shared values.

The Cencora Impact Foundation, launched simultaneously with a $5 million initial donation, embodied this shift. Rather than traditional corporate charity, the foundation focused on systemic healthcare improvements in underserved communities. The Healthier Futures Grant Program funded innovative approaches to medication access. Employee volunteer programs connected corporate expertise with community needs. This wasn't just reputation management; it was recognition that sustainable business required healthy communities.

The global unification under Cencora had immediate practical benefits. International negotiations simplified when presenting one brand rather than explaining various subsidiaries. Talent mobility increased as employees identified with a global company rather than regional entities. Marketing efficiency improved with consistent messaging across markets. Even customer perception shifted—surveys showed a 40% increase in understanding of company capabilities within six months of the rebrand.

The technology implications were particularly significant. Under the AmerisourceBergen name, each country operation had developed independent systems, creating integration nightmares. The Cencora rebrand coincided with a massive technology harmonization project. Common platforms for inventory management, customer service, and data analytics were rolled out globally. The unified identity made this standardization culturally acceptable—we're all Cencora now, so we should operate consistently.

The manufacturer response exceeded expectations. Pharmaceutical companies had struggled with AmerisourceBergen's fragmented international presence—different names, systems, and processes in each country. Under Cencora, they could negotiate global agreements, implement worldwide programs, and track performance consistently. Pfizer's head of global supply chain noted: "The rebrand isn't just cosmetic. It represents operational unification that makes Cencora a true global partner."

Employee engagement metrics showed dramatic improvement. Pride in employer scores increased 25% globally, with international markets showing even larger gains. Recruitment improved markedly—applications for technology and innovation roles doubled in the first year. Internal collaboration increased as artificial barriers between "AmerisourceBergen U.S." and international subsidiaries dissolved. The unified identity created unified culture.

The financial impact, while difficult to isolate, appeared positive. International revenue growth accelerated from 5% to 8% annually. New global manufacturer partnerships, impossible under the fragmented structure, generated over $500 million in incremental revenue. The stock price appreciated 15% in the six months following the rebrand, outperforming peers. While correlation isn't causation, the unified identity clearly didn't hurt.

The timing proved fortuitous. As healthcare globalized—with Indian manufacturers, Chinese APIs, European biotechs, and American innovation—having a globally coherent identity became essential. The COVID-19 pandemic had shown that health threats were global; health solutions needed to be too. Cencora positioned itself as the connector, the unifier, the core infrastructure for global health.

Yet challenges remained. Some longtime customers, particularly independent American pharmacies, felt abandoned by the seemingly foreign new name. Competitors mocked the rebrand as expensive distraction. Integration of the various operations under the Cencora umbrella remained incomplete. Cultural differences between American efficiency-focus and European relationship-emphasis required constant management.

Looking back, the rebrand from AmerisourceBergen to Cencora was more than corporate cosmetics. It was recognition that the company had fundamentally transformed from its merger-of-equals origins. No longer just American, no longer just distribution, no longer serving just Bergen or AmeriSource legacy customers. Cencora represented what the company had become: central to global healthcare, core to pharmaceutical delivery, connected across borders and cultures.

The rebrand also marked a generational transition. The leaders who had built AmerisourceBergen through mergers and acquisitions were retiring. New leadership, more global in outlook and digital in orientation, was taking charge. The Cencora name gave them freedom to reimagine the company without disrespecting its heritage. It was simultaneously an ending and a beginning—the close of the AmerisourceBergen chapter and the opening of the Cencora era.

IX. Modern Operations & Competitive Position

At 4:47 AM in Cencora's Memphis distribution center, an artificial intelligence system named NOVA makes a decision that would have required three humans and forty minutes just five years ago. A children's hospital in Atlanta needs a rare enzyme replacement therapy for a patient with Pompe disease—a drug that costs $300,000 per year and requires storage at exactly 2-8°C. NOVA instantly calculates optimal routing through three distribution centers, accounting for weather patterns, traffic conditions, FedEx flight schedules, and even the reliability ratings of specific delivery drivers. The drug will arrive at the hospital pharmacy by 10:15 AM, maintained at perfect temperature the entire journey, with real-time tracking visible to everyone from the manufacturer to the treating physician.

This scene, repeated millions of times daily across Cencora's network, illustrates the hidden complexity of modern pharmaceutical distribution. What appears simple—moving drugs from Point A to Point B—actually requires orchestrating one of the most complex supply chains in human history. Cencora handles over 13 million products daily, manages $130 billion in inventory at any moment, and maintains relationships with 450 pharmaceutical manufacturers and 50,000 customer locations. The margin for error is zero; a single mistake could mean death.

The two-segment structure that Cencora operates reflects the fundamental reality of global pharmaceutical markets. The U.S. Healthcare Solutions segment, generating $262 billion in fiscal 2024 revenue (15.7% growth), remains the core. But it's no longer just about traditional distribution. This segment now encompasses specialty networks handling cell and gene therapies, direct-to-patient programs for rare diseases, clinical trial logistics through World Courier, and even physician practice management through various acquired platforms.

The International Healthcare Solutions segment, contributing $32 billion in revenue (5.5% growth), represents the future. Operating across 50 countries, this isn't just Alliance Healthcare's European network anymore. It includes emerging market operations that look nothing like traditional distribution—in Nigeria, Cencora operates mobile pharmacies that reach remote villages; in India, they partner with digital health platforms to enable telemedicine prescriptions; in Brazil, they manage government vaccine programs that reach indigenous populations in the Amazon.

The competitive dynamics with McKesson and Cardinal Health have evolved into something resembling the Cold War doctrine of mutual assured destruction. Each controls roughly 30-35% of the U.S. market. Each has similar capabilities, costs, and customers. Direct competition is pointless—stealing a major customer from a competitor would trigger retaliation that would destroy margins for everyone. Instead, competition happens at the margins: technology capabilities, value-added services, international expansion. The distribution network spans 26 pharmaceutical distribution centers in the US, nine distribution centers in Canada, four specialty distribution centers in the US, though more recent information indicates over 40 distribution centers strategically located throughout the United States. These aren't your grandfather's warehouses with forklifts and clipboards. The new state-of-the-art, highly automated distribution centers leverage AI and ML algorithms to improve demand forecasting, optimize inventory management and enhance customer service.

The technology infrastructure investment is staggering. In May 2024, Cencora disclosed it had been the subject of a cyber incident in which patient information was exposed, highlighting the double-edged sword of digital transformation—more capability but more vulnerability. The company has responded by implementing multiple layers of security, from blockchain-based tracking to AI-powered anomaly detection. Every package, every pill, every delivery is tracked with military precision.

But what truly differentiates Cencora from McKesson and Cardinal in the modern era is the sophistication of their service layer. Through their specialty pharmaceutical networks, they don't just deliver cancer drugs—they manage the entire treatment ecosystem. They handle prior authorization with insurance companies, provide financial assistance programs for patients who can't afford $10,000 monthly medications, train nurses on administration protocols, and even manage the specialized refrigeration units in oncology clinics.

The animal health division has evolved into something nobody anticipated. What started as distribution to veterinary clinics has become a technology platform rivaling anything in human healthcare. They manage operations, client experiences, and deliver products and services for top-notch animal pharmaceutical care by leveraging global solutions and services. The data flowing from millions of pet prescriptions provides insights into disease patterns, drug efficacy, and even predictive models for human health trends.

International operations have moved beyond traditional distribution into market access facilitation. In Europe, where each country has different reimbursement systems, Cencora doesn't just deliver drugs—they navigate the byzantine process of getting new medications approved and paid for. In emerging markets, they're building infrastructure from scratch, using cloud-based systems and mobile technology to leapfrog traditional distribution models.

The manufacturer services division has become increasingly critical. Pharmaceutical companies, facing patent cliffs and pricing pressure, need partners who can do more than move boxes. Cencora provides everything from clinical trial logistics to patient support programs to real-world evidence collection. They can tell Pfizer not just how many doses of a drug were shipped, but how patients responded, what side effects occurred, and which physicians are early adopters of new therapies.

The financial scale enables investments that would be impossible for smaller players. The automation and intelligence built into their tools helps teams deliver at extreme velocities under very tight timelines. In one case, using OpenText Enterprise Performance Engineering enabled the team to identify and resolve issues that led to a greater than 98 percent improvement in application performance.

The customer stickiness created by this complexity is extraordinary. Cencora's healthcare supply chain includes over 31,000 active trading partners, with ongoing onboarding of roughly 900 new partners each month and the exchange of around 800,000 documents daily. Once a hospital integrates Cencora's systems into their operations—inventory management, purchasing, compliance tracking, financial management—switching becomes almost impossible without massive disruption.

The competitive moat isn't just scale anymore—it's the accumulation of thousands of small advantages. The AI system that predicts drug shortages six weeks before they occur. The relationships with 10,000 physicians who trust Cencora's clinical support teams. The compliance infrastructure that ensures perfect DEA reporting. The financial strength to extend credit to hospitals struggling with cash flow. Each advantage is small, but together they create an insurmountable barrier.

Yet vulnerabilities exist. There's particular scrutiny over the role they may have played in opioid epidemic. And like UHG, Cencora was also subject to a major data breach last year. The technology that enables their operations also creates risk—a successful cyberattack could paralyze American healthcare. The consolidation that created efficiency also created fragility—if Cencora's systems failed, 20% of American pharmaceutical supply would stop.

The regulatory environment remains challenging. Drug pricing legislation threatens margins. State-level regulations create operational complexity. The opioid settlement payments, while manageable, remain a constant drain on cash flow. And always lurking is the threat of more aggressive government intervention in pharmaceutical distribution.

Looking at the numbers, the resilience is remarkable. Cencora is ranked #10 on the Fortune 500 and #24 on the Global Fortune 500 with more than $250 billion in annual revenue. The company processes millions of transactions daily with 99.9% accuracy, maintains inventory turns that would make Toyota jealous, and generates returns on capital that shouldn't be possible in a distribution business.

The evolution from simple wholesaler to complex healthcare platform is complete. Modern Cencora doesn't just distribute pharmaceuticals—they enable the entire pharmaceutical ecosystem. They're the invisible infrastructure that makes visible healthcare possible. And in an industry where invisibility often means irrelevance, Cencora has achieved the opposite: becoming so essential that their absence would be catastrophic. It's the ultimate business model—boring, complex, and absolutely indispensable.

X. Financial Analysis & Market Performance

The chief financial officer's pen hovered over the signature line of Cencora's fiscal 2024 10-K, a document that would report $294 billion in revenue—a number so large it loses meaning without context. Revenue increased 12.1 percent to $294.0 billion for the fiscal year, placing Cencora among the top 10 largest companies in America by revenue. Yet despite this massive scale, the stock trades at a market capitalization of roughly $56 billion, implying a price-to-sales ratio of just 0.19—a valuation that would make value investors salivate if they understood the business.

The headline numbers tell a story of consistent execution in a challenging environment. For fiscal year 2024, adjusted diluted EPS increased 14.8 percent to $13.76, demonstrating that Cencora can grow earnings faster than revenue even in a mature industry. This isn't supposed to be possible in distribution—conventional wisdom says margins compress as industries consolidate. Yet Cencora has defied gravity through operational excellence and strategic positioning.

Breaking down the segments reveals where the growth engines truly lie. Revenue within U.S. Healthcare Solutions increased 15.7 percent and revenue within International Healthcare Solutions increased 5.5 percent in the fourth quarter. The U.S. business, despite its maturity, continues to outpace GDP growth by multiples. This isn't just inflation or drug price increases—it's market share gains, new service offerings, and the relentless shift toward specialty pharmaceuticals.

The margin story is perhaps more impressive than the growth narrative. Adjusted operating income margin decreased by 1 basis point to 1.24 percent—maintaining margins in a business where every basis point represents $3 billion in revenue is a feat of operational precision. Consider that Amazon's retail business operates on similar margins but receives a valuation multiple 10 times higher. The difference? Perception and understanding.

Return on equity (ROE) is 141.78% and return on invested capital (ROIC) is 21.31%—numbers that would make even the best technology companies envious. How does a distribution company achieve ROE above 100%? Through negative working capital—Cencora collects payment from customers before paying suppliers, essentially using other people's money to fund operations. It's the same model that made Dell famous, applied at massive scale to healthcare.

The cash generation capability is staggering. Despite the massive opioid settlement obligations and continued investments in technology and acquisitions, Cencora generates billions in free cash flow annually. This cash funds a dividend that, while yielding only 0.78%, has grown consistently. The company announced an 8 percent dividend increase alongside fiscal 2024 results, signaling confidence in continued cash generation.

Working capital management deserves special attention. In a business handling $294 billion in inventory annually, even small improvements in days sales outstanding or days payable outstanding translate to hundreds of millions in cash flow. Cencora has mastered this game, turning inventory approximately 12 times per year—meaning the average pharmaceutical sits in their warehouse for just 30 days. For comparison, a typical retailer turns inventory 4-6 times annually.