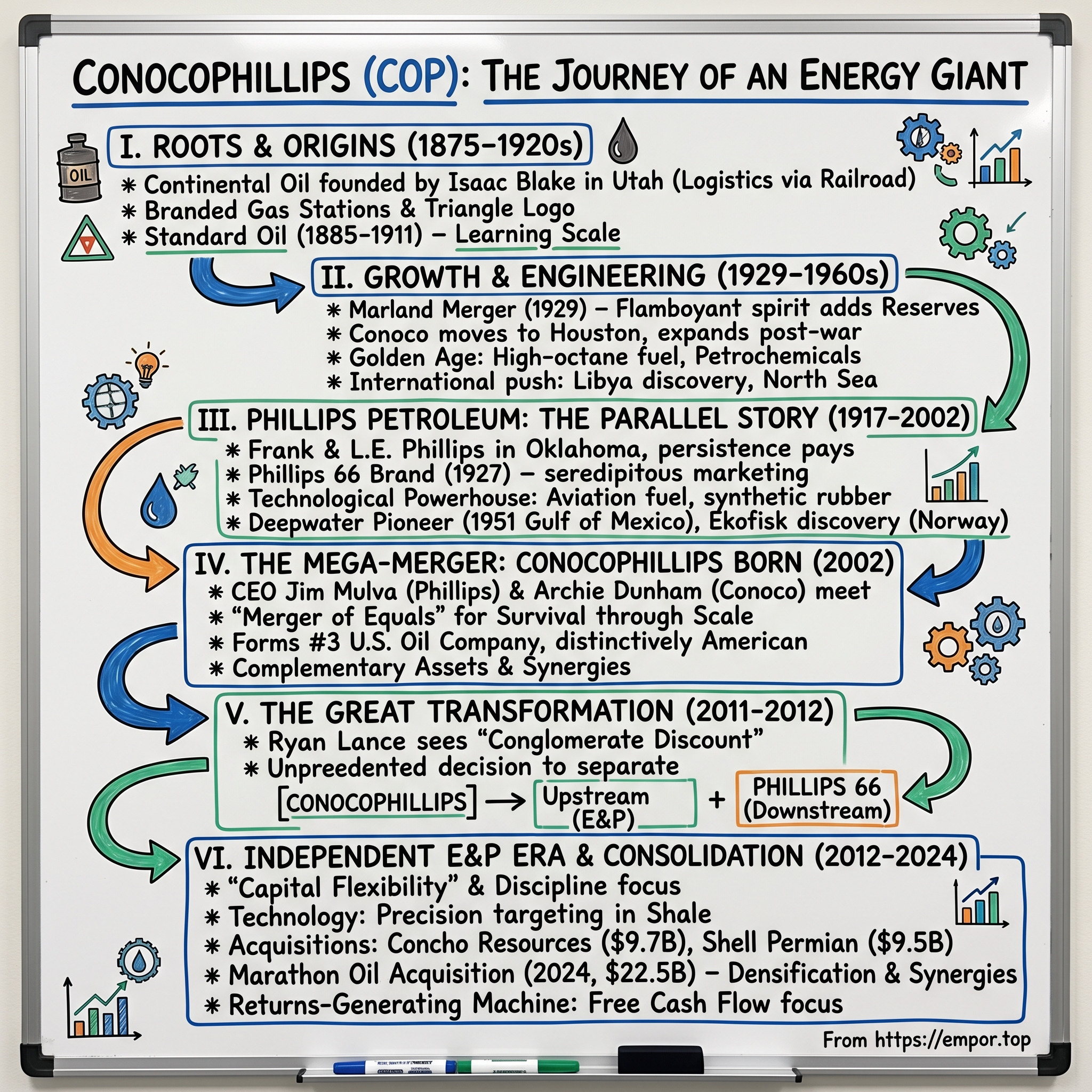

ConocoPhillips: The Story of America's Independent Energy Giant

I. Introduction & Episode Roadmap

The year is 2012. In a Houston boardroom, Ryan Lance stands before a wall of maps showing oil fields from Alaska to Australia. He's about to do something that would have been unthinkable just a decade earlier: voluntarily shrink one of America's oil giants by spinning off half the company. "We're betting everything," he tells his team, "on becoming the best at finding and producing oil—nothing else."

This wasn't corporate surgery born of desperation. ConocoPhillips was profitable, growing, and ranked among the world's six largest oil companies. But Lance saw something others missed: in an era of shale revolution and volatile oil prices, the old integrated oil model—where companies did everything from drilling to running gas stations—was becoming a liability. The future belonged to specialists.

How did we get here? How did a company that started in 1875 selling kerosene from horse-drawn wagons in Utah become a $140 billion pure-play exploration and production powerhouse? The answer involves railroad barons, Oklahoma wildcatters, the breakup of Standard Oil, multiple mega-mergers, and ultimately, the courage to tear apart what previous generations had spent decades assembling.

ConocoPhillips today stands as the world's largest independent E&P company, a position it's defended and expanded through disciplined capital allocation, strategic acquisitions, and an almost religious devotion to shareholder returns. With its recent $22.5 billion acquisition of Marathon Oil completed in November 2024, the company has doubled down on its bet: that in the energy transition era, the winners won't be those who try to do everything, but those who do one thing exceptionally well.

This is the story of transformation at scale—how a company repeatedly reinvented itself across 150 years, from kerosene distributor to Standard Oil subsidiary, from regional player to global major, and finally, from integrated giant to focused specialist. It's a playbook for navigating commodity cycles, managing technological disruption, and most importantly, knowing when to zig while competitors zag.

What you're about to read isn't just corporate history—it's a masterclass in strategic evolution, capital discipline, and the art of creative destruction. From Isaac Blake's first kerosene wagons to today's Permian Basin super-major, every chapter reveals lessons about ambition, adaptation, and the relentless pursuit of efficiency in one of the world's most challenging industries.

II. The Roots: Continental Oil Origins (1875–1920s)

Picture Ogden, Utah, in 1875. The transcontinental railroad had connected the coasts just six years earlier, but most homes still flickered with candlelight and whale oil lamps as darkness fell across the desert. Isaac E. Blake, a sharp-eyed entrepreneur, noticed something peculiar: while Eastern cities were switching to kerosene for lighting, Utah pioneers were stuck paying exorbitant prices for fuel hauled by wagon from primitive Colorado refineries—when they could get it at all.

Blake's insight was elegantly simple: use the railroad. If he could import kerosene from Eastern refineries by rail instead of wagon, he could undercut local prices and transform how the West lit its homes. With this vision, he founded the Continental Oil and Transportation Company in 1875, not as an oil producer or refiner, but as a logistics company—a detail that would prove prophetic for the company's future focus on operational efficiency.

The early Continental Oil was scrappy and innovative. Blake didn't just move kerosene; he revolutionized its distribution. In California, he constructed the state's first pipeline, running from a railroad station in Pico to Ventura, where oil was loaded onto steamers bound for San Francisco. This wasn't drilling or refining—it was pure logistics innovation, finding smarter ways to move product to market.

By 1885, Continental's success caught the attention of the era's ultimate monopolist: John D. Rockefeller's Standard Oil. The absorption into Standard Oil wasn't hostile—it was almost inevitable. Standard Oil was assembling a continental empire, and Continental's Western distribution network filled a crucial gap. For the next 26 years, Continental operated as Standard's Western arm, learning the disciplines of scale, standardization, and market dominance that would serve it well in its independent future.

Then came May 15, 1911—the day the Supreme Court ordered Standard Oil's dissolution. The Sherman Antitrust Act had finally caught up with Rockefeller's empire, splitting it into 34 separate companies. Continental Oil emerged as one of these "baby Standards," suddenly independent again but now armed with Standard's operational sophistication and a dominant position across the Rocky Mountain states.

The newly independent Continental faced an identity crisis. It had distribution expertise and regional dominance, but limited production assets and refining capacity. While other Standard Oil offspring like Esso (later Exxon) and Socony (later Mobil) had inherited massive refineries and oil fields, Continental got the sparse, rugged West—a blessing disguised as a curse.

This geographic isolation forced Continental to become self-reliant and entrepreneurial. The company aggressively expanded into New Mexico and Texas, areas Standard Oil had largely ignored. It pioneered new marketing techniques, introducing the first branded gas station in the West and developing innovative lubricants for the mining industry. The company's triangular logo—later to become iconic—first appeared in 1913, a symbol of quality that helped Continental compete against larger Eastern rivals.

By the 1920s, Continental had transformed from a kerosene distributor into an integrated oil company, albeit a small one. It operated refineries in Colorado and Montana, owned a growing network of gas stations, and had begun modest oil production operations. But the company's real breakthrough was about to come through a merger that would reshape its destiny—and introduce one of the industry's most colorful characters.

The stage was set for Continental's next act: a union with the flamboyant oil pioneer E.W. Marland, whose company would bring not just oil reserves, but a philosophy of aggressive exploration that would define Continental's culture for generations.

III. The Marland Merger & Early Growth (1929–1960s)

E.W. Marland was everything Isaac Blake wasn't—flamboyant where Blake was methodical, a gambler where Blake was a calculator. By 1920, the Pittsburgh lawyer-turned-oilman had built an empire from nothing, controlling one-tenth of the world's oil production from his base in Ponca City, Oklahoma. His mansion rivaled Hearst Castle, his company sponsored polo teams, and he threw parties that drew Hollywood stars to the Oklahoma prairie. Then, almost overnight, he lost it all.

The story of how Marland Oil Company merged with Continental Oil in 1929 is really a tale of Wall Street sharks devouring a dreamer. Marland had borrowed heavily from J.P. Morgan & Company to fund his empire's expansion. When oil prices softened in the late 1920s, Morgan called in the loans. Marland couldn't pay. The bankers' solution was ruthlessly elegant: merge Marland Oil with the smaller but financially stable Continental Oil, with Continental's management taking control.

On paper, it was David swallowing Goliath. Marland Oil was three times Continental's size, with vast Oklahoma oil fields, modern refineries, and that distinctive red triangle logo that would become Conoco's trademark. But Marland himself was pushed out—he would later become Oklahoma's governor, perhaps the only oil executive to trade a boardroom for a statehouse out of spite rather than ambition.

The merged company, now simply called Conoco, moved its headquarters to Ponca City, inheriting Marland's impressive infrastructure along with his bold exploration culture. This cultural fusion—Continental's operational discipline meeting Marland's wildcatter spirit—created a unique corporate DNA that balanced risk-taking with prudent management.

The 1930s tested this balance immediately. The Great Depression crushed oil demand just as the massive East Texas oil field came online, creating a supply glut that drove prices below 10 cents per barrel. Conoco survived through diversification, expanding its retail network and developing specialty products like anti-freeze and industrial lubricants. The company's researchers pioneered high-octane aviation fuel, a innovation that would prove crucial during World War II.

The war years transformed Conoco from a regional player into a national force. The company's refineries ran at maximum capacity producing aviation fuel for the Allied air forces. Its profits funded aggressive post-war expansion—new refineries on the Gulf Coast, petrochemical plants, and a transcontinental pipeline network. By 1949, Conoco had outgrown Ponca City, moving its headquarters to Houston to be closer to the emerging offshore drilling industry.

The 1950s and 60s were Conoco's golden age of engineering. The company built some of the era's most advanced refineries, pioneered catalytic cracking techniques that increased gasoline yields by 40%, and developed the first commercial-scale petrochemical operations in the Rockies. But it was Conoco's international expansion that truly set it apart from regional competitors.

In 1959, Conoco made a bold bet on Libya, acquiring massive concessions in the Sahara Desert. The gamble paid off spectacularly with the discovery of the giant Sarir field in 1961. Within five years, Libya was producing 500,000 barrels per day for Conoco—more than all of its U.S. operations combined. The company followed with successful ventures in the North Sea, Indonesia, and Venezuela, becoming one of the first American independents to operate globally.

Yet even as Conoco grew into a major international player, it maintained the scrappy, innovative culture inherited from both Continental and Marland. The company's researchers developed biodegradable detergents when environmental concerns first emerged, created synthetic motor oils that extended engine life, and pioneered enhanced oil recovery techniques that would later become industry standard.

By 1970, when Conoco adopted its now-iconic red capsule logo, the company had transformed from a regional kerosene distributor into a Fortune 500 giant with operations on six continents. But this was still just the prelude. The real transformation—the merger that would create today's ConocoPhillips—required another player to take the stage, one with an equally storied history and an even more famous brand name.

IV. Phillips Petroleum: The Parallel Story (1917–2002)

Frank Phillips stood in an Oklahoma wheat field in 1905, watching his first well come up dry. He'd invested his life savings—and his banker brother L.E.'s money—into this hole in the ground. Well number two: dry. Number three: dry. By the time Frank and L.E. Phillips had drilled 80 consecutive dry holes, most men would have quit. But on the 81st attempt, they struck oil. "That's when I knew," Frank later said, "that the key to this business wasn't luck—it was persistence multiplied by capital."

The Phillips brothers had left their Iowa farm after Frank heard whispers of vast oil deposits in the Indian Territory that would become Oklahoma. Unlike the gentleman oilmen of Pennsylvania or the Wall Street-backed operations in Texas, the Phillips brothers were prairie populists who understood their customers because they'd been poor themselves. When they founded Phillips Petroleum Company in 1917, they were nearly broke again, having sold their earlier venture, Anchor Oil and Gas, only to watch the buyers strike it rich on wells the brothers had abandoned.

World War I saved them. Oil prices shot from 40 cents to over a dollar per barrel almost overnight. The brothers consolidated their scattered Oklahoma and Kansas leases into Phillips Petroleum, but their real genius was recognizing that finding oil was only half the business—you had to sell it smarter than the competition.

The birth of the Phillips 66 brand in 1927 was pure serendipity mixed with marketing brilliance. During a test drive of their new gasoline blend, a company executive hit 66 miles per hour on Route 66 near Tulsa. "This stuff is like driving on Highway 66!" he exclaimed. Frank Phillips, ever the showman, immediately recognized the power of the number—it was memorable, suggested speed and performance, and tied the brand to America's most famous highway. Within a decade, Phillips 66 stations dotted the American landscape, their distinctive orange and black shields becoming as recognizable as Coca-Cola signs.

But Phillips Petroleum was more than clever marketing. The company pioneered the science of refining, establishing America's first commercial aviation fuel plant in 1930 and developing the catalytic polymerization process that produced the first commercial synthetic rubber during World War II. When the military needed 100-octane aviation fuel for its new high-performance fighters, Phillips engineers figured out how to mass-produce it, earning the company a Navy "E" for excellence.

The post-war years saw Phillips transform from a regional refiner into a technological powerhouse. In 1951, the company drilled the world's first commercial offshore oil well out of sight of land in the Gulf of Mexico, using a war-surplus Navy ship as a drilling platform. The discovery opened an entirely new frontier for the industry and established Phillips as a deepwater pioneer decades before it became fashionable.

Phillips' real differentiation came through chemicals. While other oil companies treated petrochemicals as a sideline, Phillips built an entire division around them. By 1960, the company was the world's largest producer of carbon black for tires, dominated the synthetic rubber market, and had created entirely new categories of plastics and fertilizers. The Phillips 66 Chemical Company became so successful it was almost spun off multiple times, but management believed the integration between fuels and chemicals gave them a competitive edge.

The 1960s brought international expansion and technological leaps. Phillips discovered the massive Ekofisk field in the Norwegian North Sea in 1969, one of the largest oil finds in history. The company pioneered liquefied natural gas technology, building some of the first LNG plants in Alaska and the Middle East. It developed the first commercial coal gasification plant and invested heavily in uranium mining, betting that nuclear power would eventually displace oil.

Yet Phillips never lost its Oklahoma roots or its focus on retail customers. The company sponsored the Phillips 66ers basketball team, which toured the country playing exhibition games and served as unofficial ambassadors for the brand. Phillips stations pioneered credit cards, clean restrooms, and uniformed attendants—small touches that built fierce brand loyalty across Middle America.

By the 1990s, Phillips had grown into one of America's largest oil companies, but it faced a strategic dilemma. It was too small to compete with the emerging super-majors like ExxonMobil and BP, but too large and successful to be an acquisition target. The company tried multiple strategies—joint ventures with Chevron, asset swaps with Conoco, even a failed merger attempt with Ultramar Diamond Shamrock.

The solution came in 2001 when Phillips CEO Jim Mulva met with Conoco's Archie Dunham at a Houston energy conference. Both men recognized the same reality: in a consolidating industry, mid-sized players would either merge or be marginalized. Within six months, they had negotiated one of the largest mergers in corporate history, creating a company that would briefly rank among the world's oil giants—before embarking on an even more radical transformation.

V. The Mega-Merger: ConocoPhillips is Born (2002)

The morning of November 19, 2001, broke cold and clear in Bartlesville, Oklahoma. Jim Mulva, CEO of Phillips Petroleum, stood in his office looking out at the town his company had called home for 84 years. In three hours, he would announce a deal that would end Phillips' independence but possibly save its future. Across the state in Houston, Archie Dunham, Conoco's CEO, was having similar thoughts. Both men knew the math: ExxonMobil, created just two years earlier, had a market cap of $270 billion. BP had swallowed Amoco and ARCO. Chevron had just eaten Texaco. Phillips and Conoco, each worth about $15 billion, were minnows in a shark tank.

The phone call that started it all had come six months earlier at a Houston energy conference. Mulva and Dunham found themselves at the same cocktail reception, commiserating about the industry's consolidation. "We're both too small to compete with the super-majors," Dunham said bluntly, "but too successful to be easy takeover targets." Mulva's response was equally direct: "So why don't we merge with each other?"

The deal they announced that November morning was structured as a "merger of equals" worth $35 billion in enterprise value, creating what would become the third-largest U.S. oil company and the sixth-largest globally. But the numbers only told part of the story. This was really about survival through scale—two proud companies choosing to join forces rather than risk being devoured separately.

Dunham called it "an excellent strategic fit," noting it would position ConocoPhillips as a stronger global energy producer with enhanced capabilities on five continents while generating major synergies. The strategic logic was compelling: Conoco brought deepwater expertise from the Gulf of Mexico and a strong downstream network in the Rockies and Southeast. Phillips contributed the massive Ekofisk field in the North Sea, Alaska production, and that iconic Phillips 66 brand with 11,700 gas stations.

The merger united two companies that had pioneered gas field development in the southern North Sea and led technical innovations in the hostile waters of the northern sector. Their combined technology portfolio was formidable—Conoco's gas-to-liquids expertise, Phillips' LNG capabilities, and both companies' cutting-edge deepwater drilling techniques.

The integration challenges were massive. Phillips had 38,000 employees while Conoco had 20,000. They had overlapping operations in the Permian Basin, duplicate refineries along the Gulf Coast, and competing gas station brands in several markets. The Federal Trade Commission scrutinized every asset, ultimately requiring significant divestitures to preserve competition, particularly in the Rocky Mountain region where both companies had strong positions.

When shareholders of both companies overwhelmingly approved the $15.6 billion merger in March 2002, they were voting for more than just a combination—they were endorsing a vision of American oil independence. Unlike European super-majors BP and Shell, ConocoPhillips would be distinctly American, with deep roots in U.S. production and a commitment to North American energy security.

The merger officially closed on August 30, 2002, with headquarters established in Houston. Archie Dunham delayed his planned retirement to serve as chairman, while Jim Mulva became CEO. The leadership structure reflected the merger's collaborative nature—two companies genuinely trying to blend their cultures rather than one imposing its will on the other.

The companies projected annual cost savings of $750 million within the first year, but the real value came from complementary assets. In Alaska, combining Phillips' Alpine field with Conoco's expertise in harsh-environment drilling created immediate synergies. In the Lower 48, merging their Permian and Mid-Continent positions created critical mass. Internationally, Phillips' Norwegian operations meshed perfectly with Conoco's UK North Sea assets.

The cultural integration proved surprisingly smooth. Both companies shared Midwestern roots, engineering excellence, and a focus on operational efficiency over financial engineering. Where Exxon and Mobil had clashed over corporate philosophy during their merger, Phillips and Conoco found common ground in their shared history as independents who had survived and thrived outside the oil establishment.

By design, 57% of ConocoPhillips' capital would be deployed in upstream operations, with plans to grow that to 60-70% over time. This upstream tilt would prove prescient—within a decade, the company would spin off its entire downstream business to become a pure-play E&P company.

The market initially loved the combination. ConocoPhillips stock rose 15% in the first month post-merger as investors recognized the synergy potential and improved competitive position. But the real test would come in execution—could this merged giant compete with the super-majors while maintaining the agility of an independent?

For the next decade, ConocoPhillips would operate as a traditional integrated oil company, running refineries, gas stations, and chemical plants alongside its drilling operations. But seeds of transformation were already planted. The merger had created scale, but scale alone wouldn't guarantee survival in the coming shale revolution. That would require an even more radical transformation.

VI. The Great Transformation: Spinoff of Phillips 66 (2011-2012)

July 14, 2011. Ryan Lance sat in a Houston conference room studying two charts that would define his legacy. The first showed ConocoPhillips' stock performance—flat for five years despite oil prices doubling. The second displayed what Wall Street analysts called the "conglomerate discount"—integrated oil companies trading at 20-30% below the sum of their parts. Lance turned to his team: "We've spent a decade getting bigger. Now it's time to get focused."

The announcement that day stunned the industry: ConocoPhillips would split itself in two, spinning off all downstream operations—refineries, chemicals, pipelines, and gas stations—into a separate company. "Our unmatched size, scope and capability position us to compete successfully in this business," said Ryan Lance, who would become chairman and chief executive officer. "With an exclusive focus on exploration and production, we will pursue opportunities and take actions to create value for all our stakeholders."

This wasn't restructuring born of crisis. Oil prices were above $100 per barrel. The company was profitable. But Lance and his board saw what others missed: the shale revolution was fundamentally changing the economics of oil production. Nimble independents like EOG Resources were generating returns that dwarfed the integrated majors. The old model—where refineries provided stability when oil prices fell—was becoming a millstone in an era of abundant, cheap shale oil.

The strategic logic was compelling but counterintuitive. For a century, vertical integration had been gospel in the oil industry. Rockefeller built Standard Oil on the principle of controlling every step from wellhead to gas pump. Now ConocoPhillips was voluntarily dismantling what previous generations had painstakingly assembled.

The resulting upstream company would keep the ConocoPhillips name and be led by Chairman and CEO Ryan Lance. The downstream company, led by Chairman and CEO Greg Garland, would be known as Phillips 66. Both companies would be headquartered in Houston.

The mechanics of the split were elegantly simple but operationally complex. ConocoPhillips stockholders received one share of Phillips 66 common stock for every two shares of ConocoPhillips common stock held on the record date of April 16, 2012. Phillips 66 became an independent, publicly traded company in which ConocoPhillips retained no ownership interest.

Behind the scenes, the separation required surgical precision. Two companies that had operated as one for a decade—and whose predecessor companies had been intertwined for even longer—had to be cleanly divided. IT systems had to be separated, employees reassigned, contracts renegotiated. The downstream business alone employed 30,000 people and generated $175 billion in annual revenue.

The IRS provided a private letter ruling confirming the spinoff would be tax-free to shareholders, a crucial condition that saved investors billions in potential tax liability. This wasn't just financial engineering—it was a fundamental reimagining of what an oil company should be in the 21st century.

Lance's vision was radically different from his predecessors. Where previous CEOs sought empire-building through acquisitions and integration, Lance pursued focus through divestiture. "As we move forward with today's strong base, our vision is to pioneer a new standard of E&P excellence," Lance said. "ConocoPhillips has always placed safety, health and environmental stewardship first, and this will not change. In addition, we have an unprecedented opportunity to unlock potential by combining the legacy of our world-class workforce, asset base, technical capability and financial capacity with the focus and culture of an independent company. We believe this will allow us to create value for all our stakeholders and deliver a compelling formula of profitable growth, strong financial returns and a sector-leading dividend."

The market's initial reaction was mixed. Some investors worried about losing the stability of integrated operations. Others questioned whether two smaller companies could compete with giants like ExxonMobil. But Lance had studied the numbers: pure-play E&P companies were trading at 8-10 times EBITDA while integrated oils languished at 5-6 times. The math was undeniable.

On May 1, 2012, the spinoff was complete. ConocoPhillips became the world's largest independent exploration and production company, based on proved reserves and production of liquids and natural gas. Phillips 66 instantly became America's largest refiner, inheriting 15 refineries, 10,000 miles of pipelines, and the iconic Phillips 66 brand.

The transformation went deeper than corporate structure. ConocoPhillips shed 30,000 employees overnight, going from 60,000 to 30,000. The company's revenue dropped from $245 billion to about $60 billion. But Lance saw these as features, not bugs. A smaller, focused company could make decisions faster, allocate capital more efficiently, and respond more nimbly to market changes.

The cultural shift was equally dramatic. For decades, ConocoPhillips executives had to balance upstream and downstream priorities, often making suboptimal compromises. Now, every decision could be evaluated through a single lens: what creates the most value from finding and producing oil and gas?

Wall Street gradually warmed to the story. Within a year of the spinoff, both companies were trading above their pre-split combined value. The "conglomerate discount" had become a "focus premium." Other oil majors took notice—though none would follow ConocoPhillips' radical path for years to come.

Looking back, the 2012 spinoff marked a watershed moment not just for ConocoPhillips but for the entire oil industry. It proved that bigger wasn't always better, that focus could triumph over diversification, and that sometimes the boldest strategy is to become smaller. The independent E&P model that ConocoPhillips pioneered would soon become the template for value creation in American oil.

VII. The Independent E&P Era: Strategy & Execution (2012–2023)

Ryan Lance's desk at ConocoPhillips headquarters looked like a war room in June 2012. Oil prices had crashed from $110 to $80 in just weeks. Analysts who'd cheered the Phillips 66 spinoff were now questioning whether a pure-play E&P company could survive such volatility. Lance gathered his leadership team: "This is exactly why we did the spinoff. Now we prove it works."

Lance proclaimed: "Our unmatched size, scope and capability position us to compete successfully in this business. With an exclusive focus on exploration and production, we will pursue opportunities and take actions to create value for all our stakeholders." But words meant nothing without execution. The newly independent ConocoPhillips needed to demonstrate that focus beats diversification, especially during commodity price chaos.

The first test came quickly. Between 2014 and 2016, oil prices collapsed from $107 to $26 per barrel—the worst crash since 2008. While integrated majors could lean on their refineries (which actually benefited from lower crude prices), ConocoPhillips had no such cushion. Lance's response was ruthlessly disciplined: cut the dividend by 66%, slash capital spending by 60%, and sell $16 billion in non-core assets.

Wall Street hated it initially. But Lance saw what others missed: this wasn't retreat, it was repositioning. Every dollar saved, every asset sold, every project deferred was evaluated against a simple metric—what generates the highest returns at $50 oil? The company shed Canadian oil sands, mature North Sea fields, and marginal U.S. conventional production. What remained was a portfolio of the lowest-cost, highest-return assets globally.

The transformation went deeper than portfolio management. ConocoPhillips pioneered what Lance called "capital flexibility"—the ability to ramp investment up or down by 30% within a single quarter based on price signals. Traditional oil companies planned in five-year cycles; ConocoPhillips operated like a hedge fund, constantly optimizing capital allocation.

Three basins became the company's obsession: the Permian, Eagle Ford, and Bakken—the crown jewels of American shale. These weren't just oil fields; they were manufacturing operations where ConocoPhillips could apply lessons from one well to thousands of others. The company's "Big 3" strategy concentrated 70% of capital in these plays, achieving economies of scale that smaller operators couldn't match.

Technology became a differentiator. While competitors chased acreage, ConocoPhillips invested in completion designs that increased recovery rates by 30%. The company pioneered "precision targeting"—using seismic data and machine learning to place wells within inches of optimal zones. A well that cost $7 million in 2014 could be drilled for $4 million by 2018, with 50% higher production.

Then came the strategic masterstroke. In October 2020, with oil prices still depressed from COVID-19, Lance announced ConocoPhillips would acquire Concho Resources for $9.7 billion in an all-stock transaction. The deal was structured with each share of Concho common stock exchanged for 1.46 shares of ConocoPhillips stock, representing a 15% premium to Concho's closing price.

The Concho acquisition wasn't about getting bigger—it was about getting better. The deal added 550,000 net acres in the Permian (350,000 Delaware acres and 200,000 Midland acres) plus 200,000 bbl/d oil output, increasing ConocoPhillips' Permian production six-fold. More importantly, Concho's acreage was directly adjacent to ConocoPhillips' existing position, creating massive operational synergies.

The acquisition completed in January 2021, with Ryan Lance noting: "We appreciate the strong support for this transaction from the shareholders of both companies. This acquisition results in the combination of two premier companies that can lead the structural change for our vital industry that's critical to investors."

But Lance wasn't done. Nine months later, in September 2021, ConocoPhillips announced it would acquire Shell's Permian assets for $9.5 billion in cash. The assets included approximately 225,000 net acres and producing properties located entirely in Texas, as well as over 600 miles of operated crude, gas and water pipelines and infrastructure.

The Shell deal was different from Concho—it was about consolidation at the bottom of the cycle. Shell, under pressure from European investors to exit fossil fuels, was a motivated seller. ConocoPhillips paid cash, avoiding dilution, and immediately announced $2 billion in additional asset sales to maintain balance sheet strength.

"This deal was justified on three key merits: it meets our rigorous cost of supply framework, we see a way to drive efficiencies from the assets, and the transaction makes our 10-year plan better," Lance explained.

The operational transformation was equally impressive. By 2019, ConocoPhillips was producing 1.3 million barrels per day with just 10,000 employees—compared to 1.5 million barrels with 30,000 employees before the spinoff. Revenue per employee had tripled. The company's break-even price fell from $75 per barrel in 2014 to under $40 by 2020.

Capital allocation became a religion. The company instituted a three-tier returns framework: first, sustain production and pay the dividend at $40 oil; second, grow production 5% annually if oil exceeds $50; third, return all excess cash to shareholders above $50. This wasn't guidance—it was a contract with investors.

The shareholder returns were staggering. Between 2017 and 2023, ConocoPhillips returned over $45 billion to shareholders through dividends and buybacks—more than its entire market cap in 2016. The company's "variable dividend" model, paying out excess cash quarterly, became the template for the industry.

International operations provided ballast. While shale grabbed headlines, assets in Norway, Australia, and Alaska generated steady cash flow with minimal capital investment. The company's position in Qatar's North Field, the world's largest gas field, provided exposure to growing LNG markets without the capital intensity of new projects.

By 2023, the transformation was complete. ConocoPhillips had evolved from an integrated oil company trying to be everything to everyone, into a focused E&P specialist that did one thing exceptionally well: generate returns through cycles. The company that had seemed vulnerable in 2012 was now the model everyone else copied.

The numbers told the story: return on capital employed rose from 3% in 2016 to over 20% by 2022. The stock price quadrupled. Debt fell from $25 billion to under $10 billion. And through it all, production actually grew—proving that discipline and growth weren't mutually exclusive.

VIII. The Marathon Oil Acquisition: Consolidation Continues (2024)

May 29, 2024. The shale consolidation game had reached its endgame, and Ryan Lance knew ConocoPhillips needed one final move. Sitting across from Marathon Oil CEO Lee Tillman in a Houston conference room, Lance laid out his vision: "This isn't about getting bigger. It's about getting better. Your Eagle Ford and Bakken positions fit our portfolio like a glove."

ConocoPhillips and Marathon Oil Corporation announced today that they have entered into a definitive agreement pursuant to which ConocoPhillips will acquire Marathon Oil in an all-stock transaction with an enterprise value of $22.5 billion, inclusive of $5.4 billion of net debt.

The timing was deliberate. Oil prices had stabilized around $80 per barrel, high enough to generate strong cash flows but not so high as to create irrational exuberance. More importantly, the Federal Trade Commission had just cleared several major oil mergers, signaling regulatory openness to consolidation. Lance had watched Exxon acquire Pioneer Natural Resources for $60 billion and Chevron buy Hess for $53 billion. The window for transformative deals was closing.

Marathon Oil shareholders will receive 0.2550 shares of ConocoPhillips common stock for each share of Marathon Oil common stock, representing a 14.7% premium to the closing share price of Marathon Oil on May 28, 2024. The premium was intentionally modest—Lance had learned from the Concho deal that discipline matters more than headlines.

Marathon Oil wasn't just any target. Founded in 1887, it was one of America's original oil companies, with a storied history that included building the Trans-Alaska Pipeline and discovering the massive Yates Field in Texas. But by 2024, Marathon had transformed itself into a focused shale player with premier positions in exactly the basins where ConocoPhillips wanted to grow.

"This acquisition of Marathon Oil further deepens our portfolio and fits within our financial framework, adding high-quality, low cost of supply inventory adjacent to our leading U.S. unconventional position," said Ryan Lance, ConocoPhillips chairman and chief executive officer.

The strategic logic was compelling. Marathon's assets were literally next door to ConocoPhillips' existing operations—same geology, same infrastructure, same regulatory environment. This wasn't diversification; it was densification. By combining adjacent acreage, ConocoPhillips could drill longer laterals, share facilities, and optimize development plans across what were previously competing positions.

ConocoPhillips expects to achieve at least $500 million of run rate cost and capital savings within the first full year following the closing of the transaction. But Lance knew the real synergies would be much higher. In private meetings, his team projected over $1 billion in savings—a number they would later confirm publicly.

The financial engineering was equally sophisticated. Independent of the transaction, ConocoPhillips expects to increase its ordinary base dividend by 34% to 78 cents per share starting in the fourth quarter of 2024. Upon closing of the transaction, ConocoPhillips expects share buybacks to be over $20 billion in the first three years, with over $7 billion in the first full year, at recent commodity prices.

This wasn't just M&A—it was a statement about capital allocation philosophy. While European oil majors were pouring billions into renewable energy projects with uncertain returns, ConocoPhillips was doubling down on what it did best: finding and producing oil and gas at the lowest possible cost and returning the proceeds to shareholders.

Lee Tillman, Marathon's CEO, understood the inevitability of consolidation. Marathon was subscale in a world of giants. Its market cap of $17 billion made it vulnerable to activist investors demanding either a sale or massive cost cuts. Joining ConocoPhillips offered Marathon shareholders a premium plus ownership in a company with the scale to compete globally.

The regulatory review proved more challenging than expected. In July the Federal Trade Commission (FTC) issued a so-called "second request" to each of the Houston, Texas-based oil and gas exploration and production companies asking for further transaction details. The extended antitrust review pushed the closing into November, but ultimately the FTC found no competitive concerns given the fragmented nature of U.S. oil production.

"This acquisition of Marathon Oil is a perfect fit for ConocoPhillips," said Ryan Lance when the deal closed on November 22, 2024. "We have a strong history of seamlessly integrating assets and we expect to deliver synergies of over $1 billion on a run rate basis in the next 12 months."

The integration strategy was surgical. Unlike previous mergers that sought to combine entire companies, ConocoPhillips cherry-picked Marathon's best assets and talent. Marathon's Eagle Ford team, recognized as industry leaders in completion design, took over technical leadership for all of ConocoPhillips' Eagle Ford operations. The Bakken assets were immediately integrated into ConocoPhillips' existing Bakken business unit.

The integration of Marathon Oil's assets is expected to add over 2 billion barrels of resource with an estimated average point forward cost of supply of less than $30 per barrel WTI. This wasn't just about adding barrels—it was about adding the right barrels at the right cost.

The human element was carefully managed. While consolidation inevitably meant workforce reductions—ConocoPhillips indicated potential headquarters staff cuts of up to 25%—the company prioritized retaining Marathon's technical experts and field operators. These were the people who knew every nuance of Marathon's assets, and their expertise was worth more than any synergy target.

The Marathon acquisition marked the culmination of ConocoPhillips' transformation strategy. In just three years, the company had spent over $40 billion on acquisitions—Concho, Shell's Permian assets, and now Marathon—while simultaneously returning over $30 billion to shareholders. This wasn't empire building; it was portfolio optimization at massive scale.

The market's verdict was clear. ConocoPhillips stock rose 5% on the announcement, while the broader energy index was flat. Analysts praised the disciplined approach, reasonable premium, and clear synergy targets. One Wall Street report called it "the template for value-creating consolidation in the shale era."

But perhaps the most telling reaction came from competitors. Within weeks of the Marathon announcement, other independents began exploring mergers. The message was clear: in the new era of American oil, scale matters, but discipline matters more. ConocoPhillips had shown it was possible to get bigger while getting better—and that combination was proving unbeatable.

IX. Business Model & Competitive Position

ConocoPhillips explores for, produces, transports and markets crude oil, bitumen, natural gas, natural gas liquids and liquefied natural gas on a worldwide basis. The company manages its operations through six operating segments, defined by geographic region: Alaska; Lower 48; Canada; Europe, Middle East and North Africa; Asia Pacific; and Other International.

But these dry facts obscure a more fundamental truth: ConocoPhillips has engineered one of the most elegant business models in global energy—a returns-generating machine that thrives on volatility rather than despite it. While competitors chase growth or pivot to renewables, ConocoPhillips has perfected the art of turning rocks into cash.

The genius lies in portfolio construction. Unlike integrated oils that must balance upstream and downstream, or pure shale players concentrated in single basins, ConocoPhillips has assembled a deliberately diverse asset base. The company has operations in 15 countries with production from the United States (49% of 2019 production), Norway (10%), Canada (5%), Australia (12%), Indonesia (4%), Malaysia (4%), Libya (3%), China (3%), and Qatar (6%). The company's production in the United States included production in Alaska, the Eagle Ford Group, the Permian Basin, the Bakken Formation, the Gulf of Mexico and the Anadarko Basin.

This geographic spread isn't random—it's a sophisticated hedge. When U.S. natural gas prices collapse due to associated gas from shale oil wells, ConocoPhillips' Australian LNG operations benefit from strong Asian pricing. When Middle East tensions spike, Norwegian production provides stable European supply. When shale economics tighten, long-life conventional assets in Alaska generate steady cash flow with minimal investment.

The capital allocation framework is where ConocoPhillips truly differentiates itself. Since 2016, the company has operated under a rigid three-tier system. Tier 1: sustain production and pay the base dividend at $40 oil. Tier 2: modest growth investments if oil exceeds $50. Tier 3: return all excess cash to shareholders above $50 through buybacks and variable dividends. This isn't guidance that changes with management whims—it's a mathematical formula that runs the company.

The discipline is almost algorithmic. When oil prices crashed during COVID-19, ConocoPhillips cut capital spending by 35% within weeks, not months. When prices recovered, the company didn't chase growth—it accelerated buybacks. This predictability has transformed ConocoPhillips from a commodity play into something approaching a dividend aristocrat with commodity upside.

Operational excellence underpins everything. In the Permian, ConocoPhillips drills wells 15% faster than the basin average while achieving 20% higher initial production rates. This isn't luck—it's the result of applying lessons from 50,000 wells drilled across multiple basins over decades. Every completion design, every drilling parameter, every artificial lift decision is optimized using machine learning models trained on this massive dataset.

The technology moat is real but subtle. While headlines focus on fracking innovations, ConocoPhillips' true advantage lies in subsurface modeling. The company's proprietary reservoir simulation software can predict production curves with 90% accuracy over 20 years—compared to industry averages of 70% over 5 years. This precision allows ConocoPhillips to high-grade opportunities that competitors might overlook or overpay for assets others undervalue.

Cost structure reveals another competitive advantage. ConocoPhillips' operating costs average $8 per barrel globally—half the industry average. This isn't achieved through corner-cutting but through relentless standardization. A well design in the Eagle Ford uses the same casing program as one in the Bakken. Compression stations in Alaska use identical components to those in Australia. This standardization enables bulk purchasing, simplified maintenance, and rapid knowledge transfer.

The Lower 48 unconventional business operates like a manufacturing system. The company has divided its shale acreage into 10,000 "drilling spacing units," each analyzed for optimal well placement, completion design, and development timing. This granular approach allows ConocoPhillips to maintain flat production while reducing activity by 30%—simply by focusing on the best units and deferring marginal ones.

International operations provide a different kind of value. These long-life, low-decline assets require minimal capital but generate enormous cash flow. The Surmont oil sands in Canada, for instance, will produce for 50+ years with sustaining capital of just $5 per barrel. The Australia Pacific LNG project has contracted sales through 2035 at prices linked to oil, providing natural hedge against U.S. gas price weakness.

The financial flexibility this model creates is extraordinary. ConocoPhillips can generate free cash flow at $30 oil—a price at which most competitors lose money. At $70 oil, the company generates $12 billion in free cash flow on just $8 billion of capital investment. This 150% cash-on-cash return is unmatched among major E&P companies.

Risk management is embedded in the company's DNA. ConocoPhillips maintains no oil price hedges, arguing that shareholders can create their own hedges if desired. Instead, the company manages risk through portfolio diversity, capital flexibility, and balance sheet strength. With debt under $10 billion against cash flow of $20 billion, ConocoPhillips could survive $20 oil for years—though it would quickly cut capital to preserve cash.

The ESG strategy is pragmatic rather than aspirational. While European oils chase net-zero targets through renewable pivots, ConocoPhillips focuses on reducing emissions intensity from existing operations. The company has cut greenhouse gas intensity by 40% since 2016 through simple operational improvements—electrifying drill rigs, eliminating routine flaring, detecting and repairing methane leaks. This approach satisfies ESG investors while avoiding the capital destruction of forced energy transition.

Competitive positioning reveals ConocoPhillips' unique status. It's too large for activists to attack effectively, too disciplined for growth investors to love, too fossil-focused for ESG purists, yet too successful for any constituency to ignore. This positioning in the market's "no man's land" has paradoxically become its greatest strength—ConocoPhillips doesn't need to please everyone, just execute its model.

The ecosystem relationships matter enormously. ConocoPhillips is the preferred partner for national oil companies seeking technical expertise without colonial baggage. It's the buyer of choice for private equity firms exiting shale positions. It's the operator that service companies prioritize during equipment shortages. These relationships, built over decades, create invisible competitive advantages that no amount of capital can quickly replicate.

Looking forward, the business model appears increasingly vindicated. As shale matures and easy gains disappear, operational excellence matters more than acreage acquisition. As investors demand returns over growth, capital discipline becomes paramount. As society grapples with energy transition, a company that can generate massive cash flow to fund whatever comes next—whether carbon capture, hydrogen, or technologies not yet invented—positions itself to win regardless of the outcome.

The ultimate test of any business model is its replicability—can competitors copy it? In ConocoPhillips' case, the answer is theoretically yes but practically no. Any company could adopt similar capital allocation rules, pursue operational excellence, or maintain balance sheet strength. But few have the discipline to maintain these principles through cycles, the asset base to diversify effectively, or the technical capabilities to execute at scale. ConocoPhillips' business model isn't protected by patents or regulations—it's protected by something far more powerful: the difficulty of doing simple things consistently well in a volatile, capital-intensive, technically complex industry.

X. Playbook: Business & Investing Lessons

The conference room at Rice University's business school was packed with MBA students in March 2023. Ryan Lance stood at the podium, looking at eager faces expecting another corporate success story. Instead, he opened with failure: "In 2015, we almost went bankrupt. Our stock hit $31. Analysts said we should liquidate. Today we're at $120. Let me tell you what we learned the hard way."

Lesson 1: The Power of Focus

The single most important decision in ConocoPhillips' modern history wasn't an acquisition or discovery—it was subtraction. The 2012 spinoff of Phillips 66 removed $180 billion in revenue but doubled the equity value within five years. The lesson is counterintuitive: in commodity businesses, complexity is a tax on returns.

Every integrated oil major justifies its model through "value chain optimization" and "cycle mitigation." But ConocoPhillips proved these are largely myths. Refineries don't hedge upstream volatility—they add their own volatility. Chemicals don't smooth earnings—they require different expertise. Gas stations don't lock in customers—they lock in capital.

Focus enables clarity. When every decision is evaluated through a single lens—what generates the highest return on and of capital from E&P—choices become obvious. ConocoPhillips divested $16 billion in assets between 2017-2020 not because they were bad assets, but because capital deployed elsewhere generated higher returns. This discipline is impossible when managing multiple business lines with competing priorities.

Lesson 2: Capital Discipline in Commodity Cycles

The most valuable slide in ConocoPhillips' investor presentations shows capital spending from 2014-2023: $15 billion, $11 billion, $8 billion, $5 billion, $4.5 billion, $6 billion, $7 billion, $8 billion, $8.5 billion, $8.5 billion. While competitors' spending graphs look like EKGs, ConocoPhillips looks like managed decline followed by stability.

This wasn't conservatism—it was mathematics. The company discovered that production growth beyond 5% annually destroyed value in shale due to infrastructure constraints, service cost inflation, and accelerated decline rates. By capping growth, ConocoPhillips avoided the "Red Queen's Race" where companies run faster just to stay in place.

The variable dividend model, introduced in 2020, institutionalized this discipline. Instead of retaining excess cash for "future opportunities," ConocoPhillips committed to distributing it quarterly. This forced management to compete for capital like any other investment—if projects couldn't generate returns above the cost of capital immediately, they didn't get funded.

Lesson 3: M&A as a Tool for Scale and Efficiency

ConocoPhillips' acquisition strategy breaks every investment banking rule. The company doesn't buy for growth—Marathon Oil actually reduced ConocoPhillips' production growth rate. It doesn't buy for diversification—every acquisition has been in adjacent acreage. It doesn't buy for transformation—the targets are doing exactly what ConocoPhillips already does.

Instead, ConocoPhillips buys for efficiency. The Concho acquisition reduced drilling costs by 20% through scale purchasing. The Shell Permian deal eliminated redundant infrastructure. Marathon Oil enabled longer laterals across lease boundaries. These unsexy synergies compound—a 10% reduction in costs at $50 oil doubles profit margins.

The discipline extends to pricing. ConocoPhillips has never won a bidding war because it never overpays. The company uses a simple rule: acquisitions must be accretive at $40 oil. This eliminates 90% of opportunities but ensures the 10% pursued create value even in downturns.

Lesson 4: Shareholder Returns Philosophy

Between 2017 and 2024, ConocoPhillips returned $65 billion to shareholders—more than its entire market cap in 2016. This wasn't financial engineering—it was promise-keeping. The company told investors it would return capital through cycles, then did exactly that.

The mechanism matters. Dividends are sticky—once raised, they're painful to cut. Buybacks are flexible but often poorly timed. ConocoPhillips' solution was elegant: a fixed base dividend that never gets cut, supplemented by variable dividends and opportunistic buybacks. This provides income investors with stability while giving growth investors upside.

The psychological impact is profound. Knowing cash will be returned removes the temptation for empire building. Managers can't hoard capital for rainy days or pet projects. Every dollar retained must compete against the certainty of shareholder returns. This clarity aligns management and shareholders like few other mechanisms.

Lesson 5: Portfolio Management and High-Grading

ConocoPhillips treats its asset portfolio like a fund manager treats stocks—constantly ranking, ruthlessly culling, opportunistically adding. The company maintains a live database ranking every asset by return on capital employed. The bottom 20% are always for sale. The top 20% get accelerated investment. The middle 60% must improve or face divestiture.

This dynamic portfolio management enables continuous improvement without major restructuring. Since 2016, ConocoPhillips has sold over 1 million acres while acquiring 2 million better acres. Production remained flat but margins doubled. This "high-grading" is invisible to casual observers but fundamental to returns.

The discipline extends to exploration. ConocoPhillips spends just 5% of capital on exploration versus 15% industry average. The company argues that buying discovered resources through M&A is more capital efficient than drilling wildcats. This controversial stance has proven correct—ConocoPhillips' finding and development costs are 40% below peers.

Lesson 6: Managing Through Energy Transitions

While competitors pivot to renewables or double down on oil, ConocoPhillips has chosen a third path: maximum cash generation to fund whatever comes next. The company explicitly doesn't predict energy transition outcomes. Instead, it's building a war chest that could fund massive carbon capture, hydrogen infrastructure, or technologies not yet invented.

This optionality strategy is brilliant. If oil demand peaks and declines gradually, ConocoPhillips generates massive cash flow for decades. If breakthrough technologies emerge, the company has capital to invest or acquire. If regulations force rapid transition, ConocoPhillips can return capital and liquidate gracefully. Every scenario is covered.

The ESG approach is similarly pragmatic. Rather than making unrealistic net-zero pledges, ConocoPhillips focuses on reducing emissions intensity through operational improvements. The company has cut methane emissions by 60% simply by fixing leaks and eliminating venting. These improvements satisfy ESG demands while actually saving money.

Lesson 7: The Compound Effect of Consistency

Perhaps the most underappreciated aspect of ConocoPhillips' strategy is its consistency. The same framework announced in 2016 guides decisions in 2024. The same metrics presented to investors in 2017 are updated quarterly without revision. The same management team has executed the same strategy for over a decade.

This consistency compounds. Employees know what's valued and optimize accordingly. Investors know what to expect and price it efficiently. Partners know the company's criteria and bring appropriate opportunities. Competitors know ConocoPhillips won't overpay and often don't bother competing.

In an industry notorious for strategic pivots, management changes, and revised guidance, ConocoPhillips' boring consistency has become its greatest differentiator. The company proves that in volatile, capital-intensive industries, the winner isn't who makes the most brilliant moves but who makes the fewest mistakes.

The ultimate lesson from ConocoPhillips' playbook is that sustainable competitive advantage in commodities doesn't come from proprietary technology, unique assets, or financial engineering. It comes from doing ordinary things extraordinarily well, maintaining discipline when others lose it, and having the courage to stay focused when diversification seems safer. These principles aren't secrets—they're just incredibly difficult to execute consistently. That difficulty is ConocoPhillips' moat.

XI. Analysis & Bear vs. Bull Case

The analyst note from Goldman Sachs in October 2024 captured Wall Street's schizophrenia perfectly: "ConocoPhillips is simultaneously the best-run E&P company globally and a melting ice cube in a warming world." This paradox—operational excellence in a potentially declining industry—defines the investment debate.

Competitive Positioning: The Last Man Standing Advantage

ConocoPhillips occupies a unique position in global energy markets. Too large to be acquired (market cap over $140 billion), too disciplined to be activist targets, too American to face European-style transition pressure, yet too successful to ignore. This positioning creates what strategists call a "local maximum"—dominant within its niche even if the niche itself faces challenges.

Versus other independents, ConocoPhillips enjoys massive scale advantages. EOG Resources may have better Permian rock, Pioneer Natural Resources (before its acquisition by Exxon) had more running room, Devon Energy trades cheaper—but none match ConocoPhillips' combination of asset diversity, capital flexibility, and balance sheet strength. The company is the buyer of last resort, the operator of choice, the partner national oil companies trust.

Against integrated majors, ConocoPhillips wins on focus. ExxonMobil generates higher absolute returns but spreads them across refining, chemicals, and low-carbon solutions. Chevron maintains higher margins but carries downstream baggage. European majors BP and Shell generate comparable upstream returns but destroy value through forced energy transition investments. ConocoPhillips' pure-play model delivers cleaner economics.

Lower 48 Resource Depth: The Shale Maturity Question

The bull case rests heavily on ConocoPhillips' 15-year inventory of premium drilling locations in the Lower 48. With over 10,000 identified locations generating returns above 30% at $50 oil, the company has runway through 2040. The recent acquisitions of Concho, Shell Permian, and Marathon Oil added 8,000 locations, effectively doubling the inventory lifespan.

But bears point to troubling trends. Shale well productivity has plateaued after years of improvement. The best rock has been drilled. Parent-child well interference is reducing recovery rates. Service costs are rising faster than efficiency gains. What generated 50% returns in 2018 now generates 30%. The fear isn't that shale stops working—it's that returns decay to utility-like levels.

ConocoPhillips counters with technology. The company claims its next-generation completion designs can increase recovery by 15% while reducing costs by 10%. Its data analytics identify bypassed pay zones previous operators missed. Its scale enables drilling cost reductions smaller operators can't achieve. The company argues it's in the third inning of shale development, not the ninth.

International Diversification: Hedge or Drag?

ConocoPhillips' international assets generate 50% of cash flow but receive 30% of capital—a deliberate strategy to milk mature assets while investing in North American growth. This portfolio approach provides stability: when U.S. gas prices collapse, Asian LNG contracts cushion the blow. When Permian differentials blow out, North Sea Brent pricing provides relief.

Critics argue international becomes a liability as countries accelerate energy transition. Norway is implementing aggressive carbon taxes. Australia faces LNG export controls. Qatar could nationalize foreign operations. China is pivoting to renewables. The fear is ConocoPhillips owns future stranded assets trading at false valuations today.

The company's response is pragmatic: extract maximum value while possible. ConocoPhillips generates 40% annual returns on its international capital employed—essentially recovering its entire investment every 2.5 years. Even aggressive stranding scenarios struggle to destroy value at this harvest rate.

Energy Transition: Existential Threat or Overblown Fear?

The bear case ultimately reduces to one question: when does oil demand peak? The International Energy Agency says 2030. OPEC says never. ConocoPhillips says it doesn't matter—the company generates sufficient returns even in decline scenarios.

The math is compelling. If oil demand declines 2% annually after 2030, prices need only stay above $50 for ConocoPhillips to generate its cost of capital. The company's break-even is $30 per barrel. With production declining naturally at 5% annually and capital discipline maintaining flat output, ConocoPhillips could theoretically profit through the entire transition.

But transition creates unknown unknowns. Carbon taxes could destroy economics overnight. Stranded asset regulations could prevent development. Social license could evaporate, making operations impossible regardless of economics. Electric vehicle adoption could accelerate beyond projections. These tail risks are unmodellable but real.

Capital Returns Sustainability: The Dividend Aristocrat Question

Bulls love the shareholder return story. ConocoPhillips has returned $65 billion since 2017 and commits to returning over $20 billion in the next three years. At current commodity prices, the company generates 15% free cash flow yields—tech-like returns from an old economy stock.

Bears worry about sustainability. Shareholder returns depend on commodity prices remaining elevated, capital discipline maintaining low costs, and assets generating expected production. Any breakdown—sustained sub-$50 oil, forced transition investments, unexpected decline rates—could force dividend cuts and buyback suspensions.

The company has stress-tested these scenarios. At $40 oil, ConocoPhillips maintains its base dividend and flat production. At $30 oil, it can survive for years by cutting capital. Only sustained sub-$25 oil or aggressive carbon taxes threaten the model—scenarios possible but improbable.

Valuation: Priced for Decline or Opportunity?

At 8x earnings and 4x EBITDA, ConocoPhillips trades at half the S&P 500 multiple despite generating double the free cash flow yield. The market clearly expects terminal decline. Bulls argue this creates opportunity—even modest multiple expansion generates 50% returns. Bears contend the multiple reflects reality—commodity businesses in secular decline deserve discount valuations.

The comparison set matters. Versus other energy companies, ConocoPhillips trades premium to integrated oils but discount to renewable players. Versus industrials with similar capital intensity, it's cheap. Versus tech with similar cash generation, it's laughably undervalued. The reference point determines the conclusion.

The Verdict: A Time-Horizon Investment

ConocoPhillips represents a temporal arbitrage. For investors with 3-5 year horizons, it's nearly perfect—massive cash returns, disciplined management, improving operations. For 10+ year horizons, it's highly uncertain—energy transition, demand destruction, stranded assets. For 20+ year horizons, it might be irrelevant—a melting ice cube in a renewable world.

This time-dependency explains the schizophrenic sentiment. Hedge funds love the near-term cash generation. Pension funds worry about long-term viability. Index funds hold it reluctantly. ESG funds avoid it entirely. The investment case depends entirely on when you need the money back.

Perhaps that's the ultimate bear-bull synthesis: ConocoPhillips is simultaneously the best way to play the current energy system and a bet against the future energy system. It's a company perfected for a world that's passing. Whether that passage takes 5 years or 50 determines whether ConocoPhillips is the trade of the decade or the value trap of the century.

XII. Epilogue & Future Outlook

Standing on the observation deck of ConocoPhillips' Houston headquarters, you can see the entire energy ecosystem—refineries to the east, petrochemical plants to the south, office towers filled with engineers and traders stretching to the horizon. Ryan Lance often brings visitors here, not for the view, but for the metaphor. "Every company you see from here is trying to figure out the same question," he says. "What does winning look like when the game itself might be ending?"

The Role of Independents in Global Energy Markets

ConocoPhillips has proven that independent E&P companies aren't just survivors in a world of integrated giants—they might be the superior model. By focusing exclusively on finding and producing hydrocarbons, independents avoid the capital destruction of forced downstream investments and energy transition pivots. They're the specialists in an era that rewards expertise over diversification.

The numbers support this thesis. Since 2016, independent E&P companies have generated average returns of 15% annually versus 8% for integrated oils. They've returned 2x more capital to shareholders while investing 50% less in growth projects. The market has noticed—the combined market cap of U.S. independents now exceeds that of European majors.

But independents face unique vulnerabilities. Without downstream operations, they're fully exposed to commodity volatility. Without renewable investments, they're targets for ESG divestment. Without government backing, they lack the political protection of national champions. ConocoPhillips' success might be the exception that proves the rule—most independents will struggle to achieve similar scale and efficiency.

Consolidation Endgame in U.S. Shale

The Marathon Oil acquisition likely marks the end of ConocoPhillips' major M&A cycle. Not because the company lacks appetite or capital, but because there's little left to buy. The Permian has consolidated from 50 significant operators in 2015 to fewer than 10 today. The Bakken and Eagle Ford are similarly concentrated. What remains are either too small to matter or too expensive to justify.

This consolidation endgame has profound implications. With fewer buyers, asset values will likely decline. With fewer competitors, capital discipline should improve. With fewer decision-makers, production responses to price signals should accelerate. The U.S. shale industry is transforming from a fragmented wild west into an oligopoly—better for returns, worse for growth.

ConocoPhillips is positioned to be one of three or four survivors who dominate U.S. shale production for the next decade. Alongside ExxonMobil (post-Pioneer acquisition) and Chevron (post-Hess acquisition), these super-independents will control 60% of U.S. shale output. This concentration should enable OPEC-like supply discipline—a profound shift from shale's growth-at-any-cost origins.

Climate Policy and Long-Term Demand Scenarios

The energy transition isn't a question of if but when and how fast. ConocoPhillips' strategy assumes a gradual transition where oil demand peaks around 2030 then declines 1-2% annually. In this scenario, prices remain elevated as supply declines faster than demand, generating strong returns for surviving producers.

But policy could accelerate transition beyond market forces. A global carbon tax of $100 per ton would add $40 to the cost of a barrel of oil, destroying demand. Regulations banning internal combustion engines by 2035 would strand billions in automotive infrastructure. Climate litigation could force producers to pay for past emissions. These policy tail risks are impossible to quantify but potentially devastating.

ConocoPhillips' response is strategic ambiguity. The company invests modestly in carbon capture, maintains options on hydrogen infrastructure, and reduces emissions intensity—enough to claim transition participation without committing capital. This fence-sitting frustrates both climate activists and oil bulls but might be the only rational response to radical uncertainty.

Technology Disruption and Cost Curves

The future of oil might be determined less by electric vehicles than by production technology. If direct air capture makes carbon removal cheaper than emission reduction, oil demand could persist indefinitely. If small modular nuclear reactors make electricity essentially free, electrification accelerates beyond projections. If breakthrough battery technology solves energy storage, renewables dominate regardless of policy.

ConocoPhillips is surprisingly well-positioned for technology disruption. The company's low cost structure means it survives any price environment above $30. Its massive cash generation funds adaptation to whatever technology emerges. Its operational expertise translates to adjacent industries like geothermal or carbon sequestration. The company might not lead the transition, but it should survive it.

The cost curve dynamics favor ConocoPhillips regardless of outcome. In a declining market, high-cost producers exit first—Canadian oil sands, deepwater projects, Arctic developments. ConocoPhillips' shale and conventional assets sit in the lowest quartile of the global cost curve. The company could be the last producer standing, enjoying monopoly-like returns in a declining industry.

Final Reflections: The Paradox of Perfect Execution

ConocoPhillips represents something unique in corporate history—a company that achieved perfect execution just as its industry faces potential obsolescence. Every strategic decision since 2012 has been correct. Every operational metric has improved. Every financial target has been exceeded. Yet the company's future remains fundamentally uncertain.

This paradox reveals a deeper truth about business strategy. Success isn't just about making right decisions—it's about timing. ConocoPhillips mastered the oil business just as society questions oil's future. The company perfected shareholder returns just as shareholders question fossil fuel exposure. It achieved operational excellence just as operations themselves face existential questions.

The lesson for investors and operators is humbling. Even perfect execution can't overcome secular decline. Even brilliant strategy can't defeat societal shifts. Even massive cash generation can't buy immortality. ConocoPhillips might be the best-run company in a dying industry—a masterpiece painted on melting ice.

Yet there's something noble in ConocoPhillips' response to this reality. Rather than deny the transition or desperately pivot, the company has chosen to perfect its craft while it still matters. Every barrel produced efficiently, every dollar returned to shareholders, every ton of carbon avoided—these aren't just financial metrics but a philosophy of excellence in the face of uncertainty.

The story of ConocoPhillips—from kerosene wagons to AI-optimized fracking—is really the story of American energy itself. Entrepreneurial origins, massive consolidation, technological revolution, and now, perhaps, graceful decline. Whether that decline takes decades or generations will determine ConocoPhillips' ultimate legacy. But regardless of outcome, the company has proven something important: in volatile, capital-intensive industries facing existential uncertainty, discipline beats vision, execution beats strategy, and returning cash beats empire building.

The view from that Houston observation deck will look very different in 20 years. Some of those refineries will be shuttered. Some of those office towers will house renewable energy companies. Some of those petrochemical plants will produce hydrogen instead of plastics. But if ConocoPhillips' strategy works, the company will still be there—smaller perhaps, different certainly, but still generating returns from whatever energy system emerges. That's not just corporate strategy—it's corporate evolution. And in business, as in nature, it's not the strongest that survive, but the most adaptable.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube