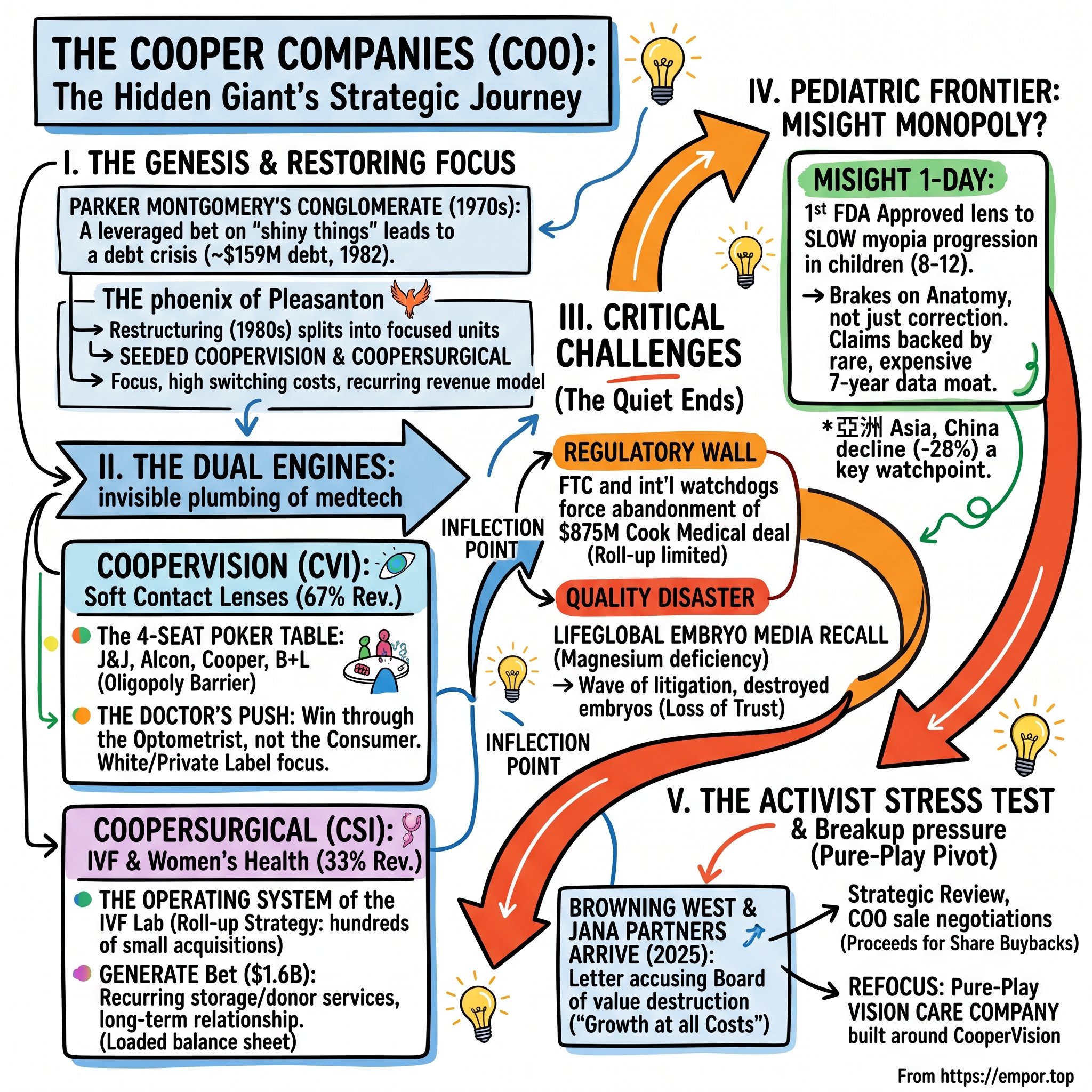

The Cooper Companies: The Hidden Giant of the Optical and IVF Duopolies

I. Introduction & Episode Roadmap

There is a good chance you have spent money with The Cooper Companies this month and have no idea who they are. If you or someone in your household wears soft contact lenses, roughly a one-in-six chance says the little foil blister you peeled open this morning was made by a company headquartered in Pleasanton, California, that almost nobody outside the eye-care industry can name. If you have been through an IVF cycle, the odds are even higher that a Cooper product touched your embryo — the pipette that held it, the dish it grew in, the incubator that kept it at body temperature, or the culture fluid it floated in for five days. Cooper is the invisible plumbing behind two of the most intimate moments in modern medicine: how millions of people see the world, and how they start a family.

This is the paradox that makes Cooper such an instructive case. It is a company that has achieved something most consumer businesses would kill for — recurring, high-margin revenue from products people cannot easily do without — and it has done so while remaining almost completely anonymous. There is no Cooper super-bowl ad, no Cooper flagship store, no Cooper logo on a jersey. The company's entire strategy, in both of its divisions, has been to embed itself so deeply into the workflow of a professional — the optometrist, the embryologist — that the end user never needs to know its name. Anonymity is not an accident of poor marketing; it is the deliberate output of a business model built on being the trusted supplier to the person who actually makes the decision.

Trading on NASDAQ under the ticker COO, Cooper is a company of roughly $4.1 billion in annual revenue and a market capitalization that has hovered in the low-to-mid tens of billions.2 It is built on two engines that share almost nothing except a corporate parent and a name. CooperVision (CVI) makes contact lenses. CooperSurgical (CSI) makes the tools and services of women's health and fertility. In fiscal 2024, CooperVision generated $2,609.4 million — about 67% of the company — and CooperSurgical $1,286.0 million, the remaining 33%.11 Two businesses, two sets of customers, two regulatory worlds, glued together by history rather than logic.

For most of the last two decades, that odd-couple structure hummed along quietly, compounding revenue at a respectable clip while the market largely ignored it. Then, in the space of about two years, the quiet ended. In December 2023, CooperSurgical recalled three lots of embryo-culture fluid that had been silently starving embryos in fertility clinics around the world — a slow-motion tragedy that would eventually touch thousands of would-be parents and metastasize into a wave of litigation.56 In August 2023, U.S. and international antitrust regulators forced Cooper to abandon an $875 million acquisition, effectively telling the company that its fertility roll-up had hit a legal ceiling.4 And in November 2025, the activist firm Browning West showed up with a $500-million-plus stake and a public letter accusing the board of "growth at all costs," strategic incoherence, and a decade of value destruction inside CooperSurgical.1

By mid-2026, the once-sleepy company is running a formal strategic review and openly negotiating the sale of CooperSurgical — the very division it spent thirty years and roughly $4 billion assembling.16 The question every investor now asks is deceptively simple: is Cooper worth more in two pieces than one?

This is the spine of the episode, and it splits into three themes worth holding onto. The first is push versus pull — how you win a consumer market whose consumers never learn your name, by making the doctor your salesforce instead of the shopper. The second is the limits of the roll-up — how a strategy of buying dozens of small companies eventually runs into two hard walls, antitrust law and quality control, both of which Cooper hit within months of each other. The third is the activist as evolutionary pressure — how outside capital can force a comfortable board to do the uncomfortable arithmetic it avoided for years. To understand how a company ended up simultaneously dominant, invisible, and under siege, we have to go back to a conglomerate that nearly went bankrupt twice, run by one of the more colorful dealmakers of the 1970s.

II. The Phoenix of Pleasanton: Genesis, Restructuring, & The 1980 Split

Parker G. Montgomery was a Harvard-trained lawyer who looked at the sleepy world of pharmaceuticals in 1958 and saw a leveraged-buyout opportunity three decades before the term was fashionable. He bought a small drug company, and over the next fifteen years he did what a certain kind of financial mind always does when credit is cheap and ambition is cheaper: he bought everything. By 1967 the vehicle had a name, Cooper Laboratories, and by the early 1970s it had swallowed a sprawling collection of drug, dental, and biomedical businesses, entering the contact-lens trade in 1972.9 Montgomery was assembling a healthcare conglomerate the way a magpie builds a nest — by grabbing whatever shiny thing was within reach and hoping it all held together.

It did not hold together. Montgomery's own later verdict on his 1970s spree was unusually candid: "We had the unhappy coincidence of first shooting our own legs off."9 Recession collided with a pile of poorly integrated acquisitions, and the debt that had powered the empire turned into a noose. By 1982, with debt around $159 million and prime interest rates touching a brutal 21%, interest expense alone was devouring roughly 65% of Cooper's operating profit.9 This is the oldest story in leveraged finance: leverage magnifies genius on the way up and stupidity on the way down, and it does not care which one you actually possessed.

Montgomery's escape hatch, executed in the early 1980s, is the genetic event that produced the modern company. Rather than try to manage the tangle as one entity, he began carving Cooper Laboratories into pieces and selling slices of each to the public — partial IPOs of the divisions to raise cash and restore investor confidence. He gave the maneuver a fittingly grandiose internal name, "Project Supernova," and in 1983 he sold minority stakes in CooperVision and CooperBiomedical to public investors, raising roughly $60 million and buying the company time.9 It is worth pausing on the psychology here. Montgomery was not restructuring out of a sudden conversion to focus; he was doing it because the alternative was insolvency. The discipline was imposed by creditors and a collapsing balance sheet, not chosen — a distinction that will rhyme, forty years later, when a very different form of external pressure forces a very different Cooper board to break the company apart again.

In 1980 the businesses were reorganized into distinct groups: CooperVision for contact lenses, CooperCare for dental and internal medicine, and CooperBiomedical for diagnostics.9 The conglomerate was being deliberately dismantled into its component animals. The entity that survives today, "The Cooper Companies" — a name adopted in 1987 — is the last branch still standing from that split.9

The near-death experience was not metaphorical. In August 1988, shareholders forced Montgomery out over disputes about which assets to sell; federal insider-trading investigations then swept several controlling families off the board, and the company spiraled.9 By 1991 the stock had collapsed to around a dollar a share, and Cooper was posting losses.9 A new operator, Thomas Bender, arrived and did the unglamorous work that saves companies: he sold the losers, cut headcount, and hacked away at the debt, shrinking revenue from well over $600 million to under $100 million before it could grow again cleanly.9 In business, sometimes the bravest move is to get much smaller on purpose.

Out of that wreckage came the strategic DNA that still governs Cooper. The company emerged in the 1990s having learned a specific, hard lesson: broad diversification in medtech is a trap, and durable money is made in narrow niches with high switching costs and recurring demand. It re-anchored around two of them. One was soft contact lenses under CooperVision. The other was women's health, and in 1990 the company formed CooperSurgical, seeding it with the acquisition of a gynecological-instruments maker.9 Two small, unglamorous franchises, chosen precisely because they were unglamorous — the kind of businesses that generate steady cash and rarely attract a price war from a giant. The scars of the conglomerate collapse taught Cooper to prize focus. The irony this story will keep circling back to is that thirty years later, an activist would accuse it of forgetting that very lesson. But first, the crown jewel: how a mid-sized challenger carved out a defensible position in one of the most consolidated markets in all of healthcare.

III. CooperVision: Winning the Optical Oligopoly with "The Doctor's Push"

Picture the global soft contact lens market as a poker table with exactly four seats, and no empty chairs for newcomers. That image is the single most important fact about CooperVision's economics. Manufacturing contact lenses at scale is punishingly capital-intensive — proprietary cast-molding lines and automated packaging plants that run into the hundreds of millions of dollars — and the resulting industry is a stable oligopoly that has barely changed its cast of characters in a generation. The four seats belong to Johnson & Johnson Vision (the Acuvue brand), Alcon, CooperVision, and Bausch + Lomb. By most industry estimates, J&J leads on volume with roughly a quarter to a third of the market, Alcon holds a premium-technology position in the low-to-mid twenties, CooperVision sits around 15–18%, and Bausch + Lomb trails in the low teens.12

Why does a market this large — global soft contact lenses run to well over $10 billion a year — stay locked at four players? The answer is a beautiful illustration of what economists call a scale-economy barrier. A single high-volume cast-molding line, which mass-produces lenses by curing liquid polymer between precision molds, is a nine-figure capital commitment, and it only pays off if you can run billions of units through it. A new entrant would have to sink that capital, achieve regulatory clearance in dozens of jurisdictions, and then somehow win volume away from four incumbents who are already amortizing their plants across enormous existing bases — all while those incumbents cut price to defend their turf. No rational capital allocator attempts it. The result is one of the most stable oligopolies in healthcare, a market where the competitive question is never "who are the players" but only "how is the pie split among the same four."

CooperVision is the reason this whole company is worth studying, because it is the engine: $2,743.8 million of revenue in fiscal 2025, up 5%, thrown off at gross margins that live comfortably in the high-60s.2 Contact lenses are the closest thing consumer healthcare has to a razor-and-blades annuity — a corrective lens is a consumable that a patient with astigmatism or presbyopia buys, throws away, and re-buys, ideally forever. But being the third-largest player in a four-player oligopoly is an awkward spot. You are too big to hide and too small to set prices. Cooper's answer to that dilemma is the strategic heart of the business, and it is genuinely clever.

The Doctor's Push

J&J built Acuvue into a household name the way Procter & Gamble builds a shampoo: consumer advertising, brand pull, get the shopper to walk into the office and ask for it by name. Cooper chose the mirror-image strategy — a push through the eye-care practitioner rather than a pull through the consumer. The optometrist, not the patient, is Cooper's real customer. The company keeps the doctor's economics healthy, protects them from being undercut, and in return the doctor fits patients into Cooper lenses.

The mechanics are worth spelling out because they explain the durability. Cooper is the industry's most aggressive white-labeler and private-labeler: it will manufacture lenses that a large optometry chain or buying group sells under its own house brand, which keeps the practitioner's margin intact and the retail discounter out of the loop. It has historically positioned itself as the player least willing to hand its lenses to the mass discounters that squeeze the local doctor. If your optometrist makes more money and faces less channel conflict prescribing Cooper, Cooper has quietly turned tens of thousands of independent clinicians into a distributed, commission-motivated salesforce it does not have to pay directly. That is the "push" — and it is a moat built out of other people's incentives.

There is an elegant strategic judo in this. J&J's pull model is powerful but expensive — building and defending a consumer brand like Acuvue costs enormous sums in advertising every year, and it puts J&J into structural tension with the very practitioners who write the prescriptions, because a patient who walks in demanding a brand by name is a patient the doctor cannot easily redirect to a more profitable alternative. Cooper turned that tension into a business. By aligning itself with the practitioner rather than going over the practitioner's head, it made itself the industry's preferred partner precisely among the professionals who control the point of sale. The flagship products carry this logic: MyDay, Cooper's premium daily-disposable silicone-hydrogel line, and Biofinity, its workhorse monthly lens, are both sold in significant volume through practitioner channels and private-label arrangements rather than through consumer brand-building. On the fourth-quarter fiscal 2025 call, management specifically flagged the "premium private label MyDay business" as a growth driver — a phrase that captures the whole model in four words: a premium product, sold under someone else's label, through the doctor.2

The limitation of the push model is the mirror image of its strength, and a neutral analyst should name it. Because Cooper deliberately under-invests in consumer brand, it has little direct pull with the end wearer; if the industry ever shifted decisively toward direct-to-consumer purchasing — online subscriptions, disintermediating the optometrist — Cooper's practitioner alliance would protect less of its revenue than J&J's brand would protect of theirs. The recent stumble in China is a live example: management attributed the sharp decline there specifically to the "pure play ecommerce channel," the online-first market where the doctor's push matters least and brand and price matter most.2 The moat is real, but it is a moat around the optometrist's chair, and it is only as durable as the optometrist's role in the transaction.

Toric, Multifocal, and the Physics of Lock-In

The second layer of the strategy is to fight on terrain where price matters least. A standard spherical lens — plain nearsighted or farsighted correction — is a commodity, and commodities invite rebate wars among the four giants. So Cooper leaned into complexity: toric lenses for astigmatism and multifocal lenses for aging eyes. These are not simple products. A toric lens has to be weighted and oriented so it sits on the eye at exactly the right rotational angle; a small change in parameters can leave a patient seeing worse, not better. Once a practitioner has painstakingly dialed in a toric fit that works, neither the doctor nor the patient has any appetite to redo that experiment with a rival's lens to save a few dollars. The switching cost is measured in blurred vision and repeat office visits, which is to say it is very real. Complexity, here, is not a bug the company tolerates; it is the product feature that makes revenue sticky.

The M&A Transfusions

Organic cleverness got Cooper only so far; twice, it bought its way to scale, and the two deals are a study in contrast. The first was the 2005 acquisition of Ocular Sciences for roughly $1.2 billion, which nearly doubled CooperVision's size overnight.10 It also nearly broke it. Integrating Ocular Sciences meant closing factories and rewiring supply chains, and the friction compressed margins for years — a textbook lesson in how paying up for instant scale can buy you an operational headache that takes half a decade to digest.

The second deal was the smarter one. In August 2014, Cooper acquired the UK's Sauflon Pharmaceuticals for approximately $1.2 billion, and this time it was buying a specific, urgent capability: silicone-hydrogel daily-disposable manufacturing at scale.11 The industry was shifting hard toward "one-day" lenses made of the more breathable silicone-hydrogel material — the premium, healthier, higher-margin format championed by Alcon's Dailies Total1 and J&J's Acuvue Oasys 1-Day. Without Sauflon's European capacity, Cooper would have been locked out of the fastest-growing, most defensible segment of its own market. Buying it was less an expansion than an act of competitive survival — the price of staying at the four-seat table.

The push strategy, the complexity moat, and the daily-disposable capacity together explain why CooperVision has been the steady compounder that carried the whole enterprise. But the most valuable thing about this business may not be an adult wearing lenses at all. It may be an eight-year-old in Guangzhou or Seoul who has just been told she is going nearsighted — and that is a market Cooper, almost alone, learned how to own.

IV. The Pediatric Frontier: MiSight and the Myopia Management Monopoly

Walk into a primary school in East Asia and ask how many children wear glasses, and the answer will unsettle you. Across much of the region, 近视 myopia — nearsightedness — has become a genuine public-health epidemic, with prevalence among school-age children in some East Asian cities reported above 80%. This is not a cosmetic issue. High myopia raises the lifetime risk of retinal detachment, glaucoma, and macular degeneration; a generation of children going progressively blurrier is also a generation acquiring elevated risk of serious eye disease decades later. Into this slow crisis, Cooper walked with a product that did something no lens had done before: not just correct a child's vision, but slow the disease itself.

That product is MiSight 1 day, and it is the single most important asset in Cooper's growth story. On November 15, 2019, the U.S. Food and Drug Administration approved MiSight as the first — and, for years, the only — contact lens indicated to slow the progression of myopia in children, for kids aged 8 to 12 at the start of treatment.7 The distinction between "corrects" and "slows progression" is the entire ballgame. Ordinary lenses treat the symptom each morning; MiSight is engineered with concentric optical zones that, in effect, signal the growing eyeball to stop elongating so fast. It is a therapy that happens to look like a contact lens.

To understand why this is genuinely hard to copy, it helps to understand the mechanism in plain terms. A normal corrective lens focuses light sharply onto the center of the retina but lets the peripheral image fall behind the retina, and there is good evidence the growing eye interprets that peripheral blur as a signal to keep elongating — which is exactly the wrong direction. MiSight's design interleaves treatment zones that push some of the light to focus in front of the peripheral retina, sending the eyeball the opposite instruction: stop growing. It is optics used as a brake on anatomy. The child still sees clearly through the correction zones; the treatment happens invisibly in the periphery. This is why the product is a medical device with a therapeutic claim rather than a mere vision aid, and why it had to clear the FDA's device pathway rather than simply reach the market.

The claim rests on unusually strong evidence, which matters enormously for a moat built on regulation. The FDA approval was backed by a multi-year, double-masked, randomized clinical trial across four countries — Singapore, Canada, the United Kingdom, and Portugal — that followed children wearing MiSight against a control group in ordinary lenses. The headline result: MiSight slowed the average progression of myopia by 59% over three years.7 Cooper later extended that dataset out to seven continuous years, a length of pediatric follow-up that is rare in ophthalmology and expensive to replicate.712 For any rival wanting to challenge the claim, the barrier is not a patent so much as time itself: you cannot run a seven-year study in less than seven years.

The competitive landscape in myopia control, however, is not empty, and this is where the "monopoly" framing needs qualification. MiSight competes against three other approaches that a parent and an eye doctor will actively weigh. There is orthokeratology — rigid lenses worn overnight that temporarily reshape the cornea, freeing the child from daytime correction entirely. There is low-dose atropine, a cheap generic eye drop with a substantial body of evidence behind it, which requires no lens at all. And there is a fast-growing category of myopia-control spectacle lenses — most prominently Hoya's MiYOSMART and EssilorLuxottica's Stellest — which apply a conceptually similar peripheral-defocus principle to eyeglasses, sidestepping the whole question of whether a young child can handle contact lenses. Cooper's advantage is that MiSight is the option with the longest, most rigorous, FDA-cleared dataset and a full clinical support ecosystem behind it. But a family choosing between a nightly drop, a pair of glasses, and a daily contact lens is choosing on convenience, cost, and their own child's tolerance as much as on trial data — which is why MiSight's head start is a strong commercial position rather than an unbreachable one.

Here is where the economics get interesting, and where a neutral observer should apply some pressure. Cooper's thesis is that pediatric myopia management creates far stickier revenue than the adult lens business, and the logic is sound: an adult comps-shops for cheaper contacts online, but a child on a myopia-control protocol needs ongoing clinical supervision, tying the family to an eye-care practice for years starting at age eight. To institutionalize that, Cooper co-founded "The Myopia Collective" with the American Optometric Association to train practitioners and normalize myopia management as a standard of care12 — building the ecosystem that turns a product into a protocol. On the fourth-quarter fiscal 2025 earnings call, management reported MiSight growing 37% year over year, with record quarters in the Americas and EMEA, powered by back-to-school fitting campaigns.2

But the skeptic's counterpoint deserves airtime. Thirty-seven percent growth is impressive in percentage terms precisely because the base is still small relative to the $2.7 billion CooperVision total — MiSight is a promising franchise, not yet a needle-mover for the whole company. Its most explosive potential market, Asia, is exactly where Cooper has struggled recently: management disclosed that its China business fell 28% in the fourth quarter of fiscal 2025, hurt by weakness in the online channel.2 The regulatory head start is real and the clinical data is genuinely differentiated, but "monopoly" is a strong word for a franchise whose largest addressable geography is the one where the company is currently losing ground. The bull case requires that MiSight's clinic-locked, long-duration revenue compounds for a decade; the bear case notes that competitors, from spectacle-lens makers to orthokeratology, are racing into myopia control, and that the exclusivity is a head start, not a permanent fence. Which brings us to the other half of the company — the half that generated all the drama, and is now on the auction block.

V. CooperSurgical: Creating the Operating System of the IVF Lab

An embryologist at a fertility clinic in London, Mumbai, or São Paulo begins the most delicate procedure in medicine: taking a single human egg, injecting a single sperm, and coaxing the result to divide into a viable embryo over five days in a dish. Now look at what is on the bench. The micro-pipette holding the egg steady, the finer pipette delivering the sperm, the specialized dish, the incubator maintaining a precise atmosphere, the culture fluid the embryo actually lives in, and — increasingly — the genetic test that screens the embryo before transfer. There is a strong chance that most of those items carry a CooperSurgical label. This is the business Cooper built quietly over three decades, and its ambition was nothing less than to become the operating system of the IVF laboratory.

CooperSurgical generated $1,348.6 million in fiscal 2025, up 5%, roughly a third of the company.2 But that segment-level number hides the strategy, which was assembled not through one grand acquisition but through hundreds of small ones — a patient, decades-long roll-up of the fragmented cottage industry that supplies fertility clinics and OB/GYNs. The logic mirrors CooperVision's complexity moat, applied to a different professional. An embryologist, like an optometrist fitting a toric lens, develops a validated workflow using specific consumables, and does not casually swap them, because in IVF the cost of a variable that ruins an embryo is not a refund — it is a family that does not happen. Standardizing a clinic's entire bench around one supplier's ecosystem is a formidable position, if you can build it and if you can keep the quality flawless. Hold that second condition; it becomes the whole story two sections from now.

The ecosystem is worth walking through, because its comprehensiveness is genuinely impressive and explains why the business was so hard for any single rival to dislodge. At the consumable layer sit the disposables an embryologist burns through every cycle: the micro-manipulation pipettes that hold and inject the egg, the embryo-transfer catheters, the specialized dishes, and the culture media the embryo grows in. At the capital-equipment layer sit the incubators and workstation cabinets — the durable hardware a lab buys once a decade and then feeds with Cooper consumables, a classic razor-and-blades lock-in. And at the services and genomics layer sit the higher-value offerings: pre-implantation genetic testing (PGT), which screens embryos for chromosomal abnormalities before transfer, and — after Generate — the donor banks and cryostorage. In one clinic, Cooper could plausibly supply the dish, the fluid, the pipette, the incubator, the genetic screen, and the freezer. Very few medical-device companies own an entire clinical workflow end to end like that. It is the fertility-lab equivalent of owning the operating system, the applications, and the cloud storage all at once.

The strategic problem — and the seed of the eventual conflict with Browning West — is that owning an entire workflow is not the same as earning a good return on the capital you spent buying it. Hundreds of small acquisitions means hundreds of purchase prices, hundreds of integrations, and a mounting pile of goodwill and intangible amortization on the balance sheet. A roll-up creates a real competitive position and, simultaneously, a real accounting drag; whether the first justifies the second is an empirical question, not a slogan. For most of CooperSurgical's history, management asserted the answer was yes. The activist would later marshal the company's own returns data to argue the answer was no.

The Generate Bet

The most consequential move in CooperSurgical's history was also its most expensive and, in hindsight, its most scrutinized. In late 2021, Cooper announced the acquisition of Generate Life Sciences for approximately $1.6 billion, closing the deal in December of that year.8 Generate was not a consumables business — it was a services business, and that was the point. It ran donor egg and sperm banks, fertility cryopreservation, and newborn stem-cell (cord blood and cord tissue) storage. On trailing revenues of roughly $250 million, the price implied a rich multiple of around six times sales, a valuation that only makes sense if you believe in the strategic story management was telling.8

That story was about margin mix and lifetime relationships. Hardware and disposables are decent businesses, but storage and donor services are recurring, higher-margin, and — crucially — create a multi-decade data relationship with a family. A couple that freezes embryos or banks a newborn's cord blood pays an annual storage fee for years, and Cooper could cross-sell those services through the deep clinic relationships CooperSurgical already owned. On paper, elegant: use the consumables franchise as a distribution channel for the services franchise.

The neutral read is more complicated. Generate loaded Cooper's balance sheet with debt at a moment when interest rates were about to climb, and it brought heavy amortization and integration costs that dragged reported GAAP margins for years afterward — one reason Cooper's GAAP and non-GAAP profit figures diverge so dramatically, a gap we will quantify later. And the ultimate indictment would come from Browning West, which calculated that CooperSurgical had absorbed roughly $4 billion of investment over a decade to generate a cumulative return on invested capital below 5% — a number that, if accurate, means the entire fertility roll-up destroyed economic value even as it grew revenue.1 Whether Generate was a visionary platform purchase or an overpriced diversification is precisely the question the strategic review now exists to answer. But the roll-up did not fail because the strategy was wrong. It failed, at least partly, because it ran headlong into two walls at once — one legal, one made of magnesium.

VI. The Twin Crises: Regulatory Walls and the LifeGlobal Media Disaster

Every roll-up eventually meets its ceiling. Cooper met two in the span of a few months, and together they ended the era of buy-everything expansion in fertility.

The Antitrust Wall

The first wall was the law. In February 2022, Cooper agreed to acquire the reproductive-health business of Cook Medical — a maker of OB/GYN, IVF, and assisted-reproduction devices — for $875 million, structured as $675 million at closing plus $200 million in annual installments.4 Strategically it was consistent with everything CooperSurgical had done: absorb another supplier to the same fertility clinics, deepen the ecosystem. But by 2022 the combination was too tidy for regulators' comfort. The U.S. Federal Trade Commission opened a full-phase investigation, joined by competition authorities in the United Kingdom (the CMA) and Australia (the ACCC), all worried that merging two of the largest suppliers of IVF and reproductive devices would leave clinics — and ultimately patients — with too little choice.4[^13][^14]

On August 1, 2023, Cooper abandoned the deal, paying a $45 million termination fee for the privilege of walking away.4 The FTC framed it as a win for competition, and the message to Cooper was unambiguous: the fertility segment had reached its consolidation limit. The very strategy that had built CooperSurgical — grow by absorbing adjacent suppliers — was now legally capped in its core market. For a business whose entire thesis was ecosystem dominance, hitting an antitrust ceiling was not a speed bump; it was a redefinition of what the division could ever become. (Cooper later bought a narrower slice of Cook's assets that regulators would tolerate, but the transformational deal was dead.)

The Magnesium Catastrophe

The second wall was quality control, and it was far more damaging — because it struck at the one thing an IVF supplier can never lose: trust. On December 5, 2023, CooperSurgical issued an urgent recall of three lots of its LifeGlobal embryo-culture media, the nutrient fluid in which embryos grow during the critical days between fertilization and transfer.56 The defect was chemically simple and clinically devastating: the affected lots were deficient in magnesium, an element embryos need to develop. Deprived of it, embryos in clinics around the world stalled and failed before reaching the blastocyst stage — the point at which they can be implanted.56

Sit with what that means for a moment, because the human dimension is the story. IVF patients are often at the end of a long, expensive, emotionally grinding road; an egg retrieval is a physically demanding procedure that cannot simply be repeated at will. For an unknown number of them, the embryos that failed were not a data point but their best or only chance. Reporting indicated that up to roughly 20,000 patients globally may have been exposed to the affected media, and many were not directly notified — they learned only later that a defective fluid, not their own biology, may have destroyed their embryos.6 A wave of product-liability and negligence lawsuits followed through 2024 and into 2025.

What made the recall so corrosive to the franchise was the peculiar nature of the failure. In most product recalls, the customer discovers the defect and can point to it — a phone battery overheats, a car brake fails. Here the "product" was consumed invisibly inside a biological process whose failure looks identical to ordinary bad luck. A patient whose embryos arrest at day three assumes, devastatingly, that the problem was her eggs, her age, her body. It took the manufacturer's own recall notice to reveal that a controllable manufacturing variable — the concentration of a single mineral — may have been the culprit. For a company that sells its reliability to laboratory directors as the entire value proposition, having to send a notice that says our fluid may have quietly killed your patients' embryos is close to the worst message it could ever transmit. Trust in this business is not a marketing asset; it is the product, and it does not restock as easily as inventory.

For a business whose competitive advantage is being trusted by embryologists to never make exactly this kind of error, the reputational damage cut to the core of the franchise. This is the peril of the roll-up that the bull case on CooperSurgical always underweighted: when you standardize an entire industry's bench around your products, a single manufacturing failure propagates through the whole system at once. Scale is a moat until it becomes a fault line.

By mid-2026, at least, the financial dimension of the crisis had begun to crystallize into a number. In its second fiscal quarter of 2026 (the quarter ended April 30, 2026), Cooper recorded a net litigation charge of $271.6 million — some $324.1 million in accrued liabilities offset by $52.5 million of expected insurance recoveries — after settlement agreements covering more than 95% of claimants came together faster than expected.6 The charge pushed the segment to a reported loss for the quarter even as consolidated net sales hit a record $1,081.5 million, with both CooperVision and CooperSurgical growing 8%.6 Converting an open-ended, terrifying, "unquantifiable" litigation overhang into a mostly-settled, bounded number was, paradoxically, one of the most value-relevant things management did in the entire saga — because it made the division sellable. And selling it is exactly what an activist had been demanding.

VII. The Activist Stress Test: Browning West & The 2026 Pure-Play Pivot

The first shoe dropped in October 2025, and it did not belong to Browning West. Word emerged that JANA Partners — one of the more experienced activist shops in America — had built a new position in Cooper during the third quarter of 2025, a stake later disclosed at roughly $167 million, and was pressing the company to separate its two businesses and sharpen capital allocation.13 For a board accustomed to being ignored by the market, having a seasoned agitator show up demanding a breakup was a jolt. It also put the company "in play" in the eyes of every other event-driven investor watching — which is precisely the kind of moment a second, more concentrated activist waits for.

That second shoe landed on November 19, 2025, and it hit far harder. A public letter arrived on The Cooper Companies' board that read less like a suggestion and more like an indictment. Its author was Browning West, LP, a concentrated, long-term-oriented investment firm that had quietly built a stake exceeding $500 million — enough to be one of Cooper's largest owners and to demand that the board listen.1 Two activists, arriving within a month of each other and pointing at the same structural flaw, are much harder to wave away than one. The letter was notable for how little it relied on rhetoric and how much it relied on Cooper's own numbers.

Browning West is not a typical rabble-rousing activist. It is a concentrated, long-term-oriented investment firm that presents itself as an engaged owner rather than a hit-and-run agitator — the kind of investor that shows up with a multi-year time horizon and a detailed operating thesis built almost entirely from the target's own disclosures, which is precisely what makes its letters harder for a board to dismiss as short-termism. When an owner holding a stake north of half a billion dollars publishes a dedicated campaign website and nominates a full slate of directors, a board reads it as a serious threat of a proxy fight, not a nuisance.1

The core charge was value destruction hiding inside revenue growth. From 2019 to 2024, Browning West pointed out, Cooper's revenue rose 47% — but non-GAAP earnings per share grew only 20%, less than half as fast, and free cash flow actually fell, from $421 million to $288 million.1 Growth was being purchased at a price that shareholders paid and never earned back. That last figure is the one that should stop an investor cold: a company that adds nearly half again as much revenue over five years while shrinking its free cash flow is a company converting sales into something other than owner value. The stock, the firm noted, had underperformed the S&P 500 by more than 100 percentage points over the same window.1 The letter named three root causes: a lack of strategic focus (two unrelated businesses bolted together, breeding inefficiency), a misaligned incentive structure (management compensation that ignored free cash flow and return on invested capital, effectively paying executives to grow the top line regardless of returns), and inadequate board oversight.1

The sharpest single data point was aimed at CooperSurgical: roughly $4 billion invested over a decade to produce a cumulative return on invested capital below 5%.1 Browning West's prescription followed directly — refocus Cooper as a "pure-play vision care company" built around CooperVision, evaluate strategic alternatives for CooperSurgical, and rebuild the incentive system around cash returns rather than growth for its own sake.1 To back the demand, the firm nominated a slate of four directors that read as a who's-who of eye-care and medtech operators: Walt Rosebrough, the long-serving former CEO of sterilization giant Steris; Joe Papa, former CEO of Bausch + Lomb; Andy Pawson, a former Alcon vision-care president; and the firm's own partner, Faraz Athar.1

The Capitulation

What happened next is a small case study in how quickly a quiet board folds when the arithmetic is undeniable and the campaign is credible. Cooper did not fight to the annual meeting. On December 23, 2025 — barely a month after the letter — the company announced a cooperation agreement with Browning West.[^2] It appointed Rosebrough as an independent director effective January 3, 2026, placed him on the Corporate Governance and Nominating Committee, and agreed that the board would give "due and serious consideration" to naming him Chair by the end of 2026.[^2] Longtime chair Robert Weiss would hand the gavel to independent director Colleen Jay, and the board committed to add another medtech-experienced independent director chosen jointly with the activist.[^2] In exchange, Browning West signed the usual standstill and agreed to support the board's slate at the 2026 annual meeting.[^2] A negotiated peace, but on the activist's terms.

Crucially, the board did not merely reshuffle directors; it embraced the substance. Alongside the fourth-quarter fiscal 2025 results on December 4, 2025, Cooper announced a formal strategic review to explore "every opportunity to unlock long-term shareholder value," having begun evaluating strategic alternatives earlier that year and presented initial findings to the board in October.3 Management's language on that call is worth hearing directly, because it reveals a CEO adjusting to new pressure: pressed by an analyst on why the two businesses, which he acknowledged had long "run separately or independently in many ways," were only now being pulled apart, Al White insisted the goal was simply "what's best for our long-term shareholder" and that everything — the reorganization, the buybacks, the review — pointed the same way.3

By the spring of 2026, the review had hardened into an active sale process. On the second-quarter fiscal 2026 call, management confirmed it was advancing discussions with multiple parties that had submitted significant indications of interest in CooperSurgical, that it was proceeding based on interest in the entire business rather than a piecemeal breakup, and that an update could come before the next earnings call.6 The settlement of the LifeGlobal litigation was not incidental to this — it was the enabling condition. No buyer will assume an open-ended embryo-litigation liability, so bounding that liability was the precondition for any clean sale.

Myth versus reality: the automatic re-rating

The consensus bull narrative holds that separating the businesses mechanically closes Cooper's valuation gap to pure-play eye-care peers — that the moment CooperSurgical leaves, the remaining company gets awarded Alcon's premium multiple. It is worth stress-testing that assumption rather than accepting it. The premium that a focused eye-care company commands is not a reward for focus in the abstract; it is a reward for a specific bundle of attributes — high organic growth, expanding margins, clean cash conversion, and a credible growth runway. CooperVision as a standalone would inherit some of those attributes and not others. Its growth is solid but not spectacular, sitting in the mid-single digits organically, and it is currently losing share in its most important growth geography.2 The re-rating is therefore conditional, not automatic: it depends on the standalone vision business demonstrating, quarter after quarter, that it can grow faster and convert cash more cleanly once freed of the surgical drag. The market may extend some of that credit in advance on the announcement of a sale, but it will demand the operating proof before awarding the full premium. "Separate the businesses and the multiple takes care of itself" is a hope; "separate the businesses and then execute" is a plan.

The other half of the thesis — what Cooper does with the cash — is equally load-bearing. Management has indicated the vast majority of sale proceeds would fund share repurchases.6 A buyback is value-creating only if the shares are bought below intrinsic value with money raised at a fair price; it is value-destroying if the company sells a business cheaply and then buys its own stock dear. So the whole pure-play case reduces to two prices and one execution: the price CooperSurgical fetches, the price at which Cooper repurchases stock, and whether the slimmed-down vision company delivers the growth the premium requires. All three are fundamentally questions about the judgment of the person who has run the company since 2018.

VIII. Capital Allocation & Management Assessment: The Al White Era

Albert G. White III is, in the most literal sense, a numbers man who ended up running an eye-care and fertility company. He became President and CEO of The Cooper Companies effective May 1, 2018, but he arrived in the corner office through the finance and strategy track — he had joined as an investor-relations and strategy executive, risen to Chief Financial Officer in late 2016, and also carried the Chief Strategy Officer title before taking the top job.11 That background matters, because a CFO-turned-CEO tends to be fluent in exactly the language an activist speaks: cash conversion, return on capital, the spread between what a company reports and what it actually earns. The irony is that this is precisely the vocabulary Browning West accused him of ignoring.

On alignment, the structure looks impeccable on paper. The overwhelming majority of White's compensation — over 90% of his target pay — is tied to performance metrics, stock options, and equity awards rather than salary, with a large slice of equity linked to multi-year EPS growth and total shareholder return.11 This is the textbook design for aligning a CEO with owners. But alignment with which metric is the whole question, and here the activist landed a real blow: for years the incentive plan leaned on revenue and EPS growth while underweighting free cash flow and return on invested capital — the very measures that would have flashed red on the CooperSurgical roll-up. Management's own response effectively conceded the point. On the fiscal 2025 call, White noted that free cash flow had been added as a bonus metric in 2024, and framed the coming compensation changes as further aligning leadership incentives to the stock's performance.3 When a company starts measuring cash returns only after an activist points out it wasn't, that is itself a data point about the prior regime.

White's operating partner in all of this is CFO Brian Andrews, and the two have run a consistent playbook of setting quarterly guidance and generally meeting it — a discipline that matters when you are asking the market to trust a multi-billion-dollar divestiture. Cooper's near-term guidance track record has, in fairness, been reliable: the company has tended to land inside its revenue and EPS ranges, and it raised rather than lowered its long-term cash-flow ambitions even as the litigation charge hit. The credibility problem was never the quarterly execution; it was the long-arc capital allocation, where hitting the guided number each quarter coexisted, for years, with a stock going nowhere and free cash flow eroding. A management team can be simultaneously good at the ninety-day game and poor at the ten-year one, and that is close to the precise diagnosis an investor should carry into the sale.

The capital-allocation record splits cleanly into two ledgers. On the credit side, White's organic execution has been genuinely good: CooperVision has taken share in premium daily-disposable silicone hydrogels, scaled the MiSight franchise from a science project into a real growth engine, and delivered — by fiscal 2025 — a second consecutive year of double-digit non-GAAP earnings growth, with management targeting a third.2 On the debit side sits the surgical M&A: paying six times sales for Generate, chasing the Cook Medical deal into a regulatory wall and a $45 million breakup fee, and presiding over the quality failure that produced the LifeGlobal recall.468 The pattern is a management team that compounds well when it builds and stumbles when it buys — which is a strong argument for the very refocusing the activist demanded. There is an uncomfortable governance question embedded here that a skeptic would press: the same executive team and much of the same board that approved the surgical roll-up are now the ones running the process to unwind it and deciding how to deploy the proceeds. Activists secured board seats precisely because a clean break with the prior decision-makers strengthens the odds that the sale and the buyback are done on owners' terms rather than management's.

The single most important number for judging this management team is the gap between its two versions of profit. In fiscal 2025, Cooper reported a GAAP operating margin of about 17% but a non-GAAP operating margin of about 26% — and GAAP diluted EPS of $1.87 versus non-GAAP EPS of $4.13.2 A spread that wide, sustained year after year, is a yellow flag worth staring at. Some of it is legitimate acquisition amortization; some of it is the "endless restructuring" that Browning West criticized, including roughly $89 million of reorganization and integration charges in fiscal 2025 alone.2 Under pressure, White has leaned into discipline, promising that those charges will yield about $50 million of annual pre-tax savings — roughly 19 cents of EPS — beginning in fiscal 2026, and raising the free-cash-flow target for fiscal 2026–2028 to more than $2.2 billion.2 The credibility test for the White era is now brutally specific: does the restructuring actually shrink the GAAP-to-non-GAAP gap, and does the sale of CooperSurgical get done at a price that vindicates a decade of surgical spending? Investors will not have to wait long to grade the answer.

IX. Strategic Moats: 7 Powers and Porter's 5 Forces Analysis

Strip away the drama and ask the question that actually determines long-run returns: what, precisely, protects Cooper's profits from being competed away? The honest answer is that the two businesses have very different moats, and the stronger one is the business the company is keeping.

Run CooperVision through Hamilton Helmer's 7 Powers and three powers show up with real force. The first is scale economies. A modern contact-lens plant is a capital monster — hundreds of millions of dollars of proprietary cast-molding and automated packaging equipment — and only very high volumes justify the spend. That capital intensity is why the market has four players and not forty; it is a structural barrier that prevents a would-be entrant from ever matching the incumbents' unit costs. The second is switching costs, already described in the toric and myopia-control context: once a practitioner has trained on and validated a Cooper fit, and wired it into their clinical workflow and practice-management software, moving to a rival imposes friction and clinical risk that outweigh modest price differences. The third, and most time-limited, is a cornered resource — the exclusive, hard-won regulatory position of MiSight, whose approval and multi-year clinical dataset cannot be replicated quickly.7 One should be precise, though: this is a temporal power, a head start measured in years of clinical data, not a permanent patent fortress, and rivals across spectacles, ortho-K, and pharmacology are pushing into myopia control.

It is instructive to contrast Cooper's power set with its rivals', because it reveals why the four incumbents coexist rather than annihilate one another. J&J's dominant power is branding — Acuvue is one of the few contact-lens names an ordinary consumer can recall, and that consumer pull is an asset Cooper has deliberately chosen not to build. Alcon's edge leans on cornered resources of its own in premium lens technology and a broader surgical-ophthalmology franchise. Cooper's powers, as laid out above, cluster around scale economics, practitioner switching costs, and MiSight's regulatory head start. Because each player's advantage rests on a different foundation, the market reaches a kind of equilibrium: nobody can dislodge anybody without an economically irrational price war, so they compete for share at the margins while collectively enjoying attractive returns. This is the quiet luxury of a mature oligopoly, and it is the single best structural reason to like the standalone CooperVision that a divestiture would create.

Now Porter's Five Forces, which sharpen where the profits leak. Rivalry is high in the commodity center of the market — standard spherical lenses are fought over with aggressive rebates among the four giants, which is exactly why Cooper works so hard to compete on complexity rather than price. Buyer power is a two-tier story: the individual optometrist has little leverage, which is the foundation of the whole push strategy, but the giant retail and optical chains that buy in enormous volume — the warehouse clubs and pan-European optical networks — absolutely can squeeze Cooper's margins, and they do. Threat of substitutes is low-to-moderate and, importantly, asymmetric: refractive surgery like LASIK is a genuine long-run substitute for adult vision correction, but there is no surgery a parent will perform on an eight-year-old to control myopia, which is what makes the pediatric franchise structurally more defensible than the adult one. Supplier power and threat of new entrants are both low — the same capital intensity that creates scale economies also all but bars new entrants.

Apply the same frameworks to CooperSurgical and the moat is real but shallower, which is the analytical crux of the entire divestiture debate. The switching-cost logic holds — embryologists don't casually change validated consumables — but the business lacks CooperVision's scale-economy wall (the fertility-consumables market is fragmented, which is why it had to be rolled up rather than dominated organically), its returns on capital have been poor by the activist's math, and, as December 2023 proved, its scale advantage doubles as concentrated operational risk.16 A business whose best power is switching costs, whose returns are sub-5%, and whose downside is destroying customers' embryos is a business a disciplined owner might rationally sell to a buyer better suited to run it. The frameworks, in other words, quietly endorse the breakup. What they cannot tell you is whether the market will pay for it — which is where the bull and bear cases collide.

X. The Investment Spine: Bull vs. Bear Case & Key KPIs

Every investment in Cooper today is, at bottom, a bet on the outcome of a single corporate event and its aftermath. Here is the case on both sides, argued fairly.

The Bull Case

The bull sees a catalyst-rich sum-of-the-parts story finally being unlocked. Cooper sells CooperSurgical — in whole, to one of the multiple interested parties already at the table — for a multi-billion-dollar sum, cleanly shedding the LifeGlobal litigation now that it has been largely settled and bounded.6 Management has signaled the vast majority of proceeds would flow into share repurchases, shrinking the count and levering the per-share value of what remains.6 What remains is a cleaner, faster-growing, higher-margin pure-play vision-care company — the kind of asset the market has historically awarded a premium multiple, closing the valuation discount to a focused peer like Alcon. On top of the re-rating, CooperVision keeps compounding: premium daily-disposable silicone hydrogels take share, the reorganization delivers its $50 million of savings and narrows the embarrassing GAAP-to-non-GAAP gap, and MiSight scales into a multi-decade, clinic-locked myopia franchise as the global epidemic worsens. Focus plus buybacks plus a secular growth engine is a genuinely attractive combination.

The Bear Case

The bear starts by noting that every plank of the bull case is a forecast, not a fact. The sale could disappoint: buyers may balk at residual, hard-to-quantify tails of the embryo litigation despite the settlement, or a fertility-services business earning sub-5% returns on capital may simply not command the price bulls imagine — a low-return asset is worth little to a rational buyer no matter how strategic the seller thinks it is.1 Even a clean divestiture leaves CooperVision exposed to the oligopoly's ugliest dynamic: price and rebate wars in commodity spherical lenses that could compress the very margins the pure-play thesis depends on, at a moment when the company is already losing share in China.2 The restructuring savings could evaporate into yet another year of "one-time" charges — the wide GAAP-to-non-GAAP spread is a bet the bear can point to as unresolved. And the re-rating to a peer multiple assumes the market forgives a management team whose surgical capital allocation an activist just spent a public campaign eviscerating. Buybacks funded by a sale are only value-accretive if the sale price is fair and the shares are bought below intrinsic value — two conditions, not one.

A useful second-layer check sits underneath both cases: the balance sheet and the quality of earnings. Cooper carries a meaningful debt load accumulated across the acquisition years, which is one reason rising interest rates hurt its free cash flow and why deleveraging with sale proceeds is itself a plausible use of cash that competes with buybacks. The persistent gap between GAAP and adjusted earnings — driven by acquisition amortization and recurring "reorganization" charges — is exactly the kind of item a forensic analyst circles, because it is where optimism can hide. Neither is a red flag of impropriety; both are the ordinary residue of a decade of debt-funded M&A, and both should visibly improve if the pure-play strategy is executed cleanly. That is what makes them useful as tests rather than as accusations: they are observable, and they will either mend or they won't.

The neutral synthesis: Cooper is a rare situation where the strategic logic (separate two unrelated businesses) is widely agreed upon, and the entire debate has collapsed onto execution and price. That is a narrower, more knowable question than most investment theses face — but it is not a resolved one, and the range of outcomes on the CooperSurgical sale price is wide. An investor is no longer betting on whether Cooper has a good business — the CooperVision franchise settles that — but on whether a newly pressured board and a finance-trained CEO can sell one asset well, buy their own shares well, and prove out the growth of what remains. Those are three sequential coin-flips management now has to win in public.

The Three KPIs to Watch

Amid all the noise, three metrics tell you whether the thesis is working, and an investor need track only these:

1. CooperVision organic growth, especially daily-disposable silicone hydrogel. This is the health of the core compounding engine. Steady mid-single-digit or better organic growth here, with share gains against J&J and Alcon in the premium daily segment, is the evidence that the pure-play deserves a premium. Watch the Asia/China line specifically, since that is where the recent damage has been.2

2. MiSight global revenue momentum. The myopia franchise is the option value in the stock. The percentage growth rate, and whether it broadens beyond the Americas and EMEA into a recovering Asia, tells you whether the "decades-long clinical monopoly" is a reality or a slide.2

3. The GAAP-to-non-GAAP operating-margin spread. This is the single best lie-detector for the whole story. If the restructuring is real and the M&A churn is truly ending, that ~9-point gap between reported and adjusted margins should visibly narrow toward a clean 25%-plus GAAP margin. If it does not, the "one-time" charges were never one-time, and the activist was right.2

XI. Outro & Lessons for Founders and Investors

The Cooper Companies is, in the end, a story about the two faces of one idea. Niche focus — the lesson Cooper learned the hard way when a 1970s conglomerate nearly killed it — can build an almost unassailable position, as CooperVision's four-seat oligopoly and its practitioner-push machine attest. But the same instinct that says "own a narrow niche completely" curdles into something dangerous when it becomes "own it by buying everything in sight." CooperSurgical is what the roll-up looks like when it works right up until it doesn't: revenue that compounds, returns that don't, an antitrust ceiling, and a quality failure that turned scale into a single point of catastrophic failure.

There is a subtler lesson buried in the accounting. For years, Cooper presented investors with a flattering non-GAAP portrait — adjusted earnings marching upward at a double-digit clip — while the GAAP numbers and, more tellingly, the cash flow told a quieter, less impressive story. The company was not lying; every adjustment was disclosed and defensible line by line. But the aggregate effect was a management team and a market conversation anchored on the version of profit that excluded the very costs its acquisition strategy kept generating. The discipline an investor should take from this is old and unglamorous: when a company asks you to look past its "one-time" charges year after year, the charges are not one-time, and free cash flow is the referee that cannot be adjusted away. Browning West's most powerful weapon was not a clever thesis; it was Cooper's own cash-flow statement.

The second lesson is about the usefulness of pressure. For most of its modern life, Cooper's board was quiet, comfortable, and — the record now suggests — insufficiently rigorous about whether growth was actually creating value. It took an activist with a $500 million check and a spreadsheet full of the company's own numbers to force the arithmetic into daylight, and the board's rapid capitulation is itself evidence that the case was hard to argue with.1[^2] Activist-driven separations are often caricatured as short-term financial engineering, but here the pressure is doing something structurally healthy: forcing a company to stop cross-subsidizing a low-return diversification and refocus on its genuine compounding engine. Whether Cooper emerges as a cleaner, more valuable pure-play — or as a company that sold its second engine cheaply and squandered the proceeds — is the verdict the next few quarters will render. For now, the hidden giant of the optical and IVF worlds has been dragged, finally, into the light, and asked the oldest question in capital allocation: what is this actually worth, and to whom?

References

-

Browning West Delivers Letter to The Cooper Companies Board of Directors — GlobeNewswire, 2025-11-19 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

CooperCompanies Announces Fourth Quarter and Full Year 2025 Results — GlobeNewswire, 2025-12-04 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

CooperCompanies Announces New Chair of the Board and Strategic Review — CooperCompanies, 2025-12-04 ↩↩↩

-

Statement Regarding Termination of CooperCompanies' Attempted Acquisition of Cook Medical's Reproductive Health Business — Federal Trade Commission, 2023-08-01 ↩↩↩↩↩

-

Class 2 Device Recall Database — LifeGlobal Media Recall — U.S. Food and Drug Administration, 2024 ↩↩↩

-

Fertility media recall leaves CooperCompanies with Q2 loss despite record sales — StockTitan, 2026-06-04 ↩↩↩↩↩↩↩↩↩↩↩↩↩

-

CooperCompanies Announces CooperVision Has Received FDA Approval of MiSight for the Treatment of Myopia in Children — GlobeNewswire, 2019-11-18 ↩↩↩↩

-

CooperCompanies Completes Acquisition of Generate Life Sciences — GlobeNewswire, 2021-12-17 ↩↩↩

-

Cooper Companies Merger With Ocular Sciences Completed — CooperCompanies, 2005 ↩

-

The Cooper Companies, Inc. SEC EDGAR Filings — CIK 0000711404 (10-K segment data and proxy compensation disclosures) ↩↩↩↩

-

CooperVision Myopia Management Practitioner Portal — CooperVision ↩↩↩

-

JANA Partners' Strategic Move: Significant Addition of The Cooper Companies Inc (Q3 2025 13F) — Yahoo Finance / GuruFocus, 2025 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube