Capital One: The Data-Driven Revolution in American Finance

I. Introduction & Episode Roadmap

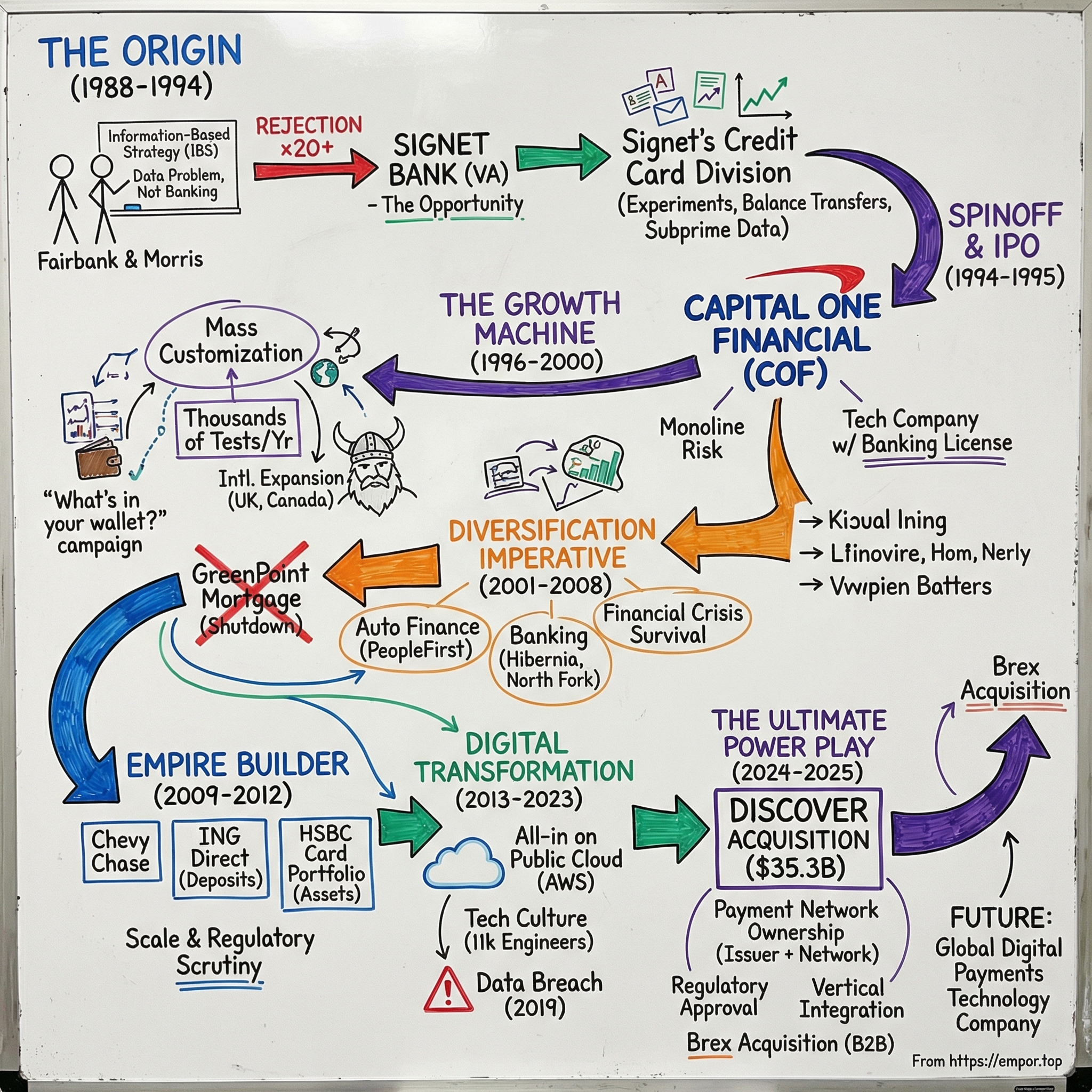

Here is a number that should stop you in your tracks: one company, started by two management consultants who got rejected by more than twenty banks, now sits as the largest credit card issuer in the United States by loan balances, the sixth-largest bank in the country by total assets, and — as of May 2025 — the owner of one of only four major payment networks on the planet. That company is Capital One Financial Corporation, ticker COF, and this is one of the most extraordinary stories in the history of American finance.

Capital One ranked as the ninth-largest bank in the United States by total assets as of September 2024, and the third-largest issuer of Visa and Mastercard credit cards. But those rankings barely capture the ambition. The central question of this story is deceptively simple: how did two consultants — one from California, one from London — use data science to revolutionize credit cards, build a thirty-five-billion-dollar acquisition machine, and ultimately grab for the holy grail of payments by acquiring a network of their own?

The themes that run through this narrative are classic: information-based strategy deployed before the rest of the world understood what that phrase meant; a founder-led transformation that has now stretched across more than three decades with the same CEO at the helm; empire building through M&A that ranged from brilliant to nearly disastrous; and a technology-first philosophy that turned a monoline credit card company into something that looks less like a bank and more like a technology platform with a banking license.

What unfolds is a story of relentless innovation, regulatory battles that nearly derailed the company's biggest bets, one of the largest data breaches in American history, and a culminating acquisition — Discover Financial Services — that fundamentally reshapes the competitive landscape of payments. Along the way, there are lessons about patience, about the power of experimentation at scale, and about what happens when someone treats an entire industry's product as a data problem rather than a banking problem.

Let's start at the beginning — and the beginning is not a boardroom. It's a rejection letter. Actually, it's about twenty-five of them.

II. The Origin Story: Two Consultants and a Bank

Picture a young consultant in his mid-thirties, standing at a whiteboard in Washington, D.C., sometime around 1985. Richard Dana Fairbank — Rick to his colleagues — has just finished sketching out an idea that he believes could transform the entire credit card industry. The room is skeptical. The partners at Strategic Planning Associates, a boutique strategy firm, have seen plenty of ambitious ideas from their consultants. But Fairbank is not pitching a consulting engagement. He is pitching a business.

To understand what Fairbank saw, you need to understand what the credit card industry looked like in the mid-1980s. It was, by any rational analysis, absurd. Every major bank in America offered essentially the same product: a credit card with a 19.8 percent interest rate and a standard annual fee. Whether you were a surgeon with a pristine credit history or a recent college graduate with no track record at all, you got the same terms. The industry treated credit cards as a commodity — a generic product stamped out on an assembly line with zero customization. Banks competed on brand and distribution, not on product design or pricing.

Consider the sheer irrationality of this. A creditworthy consumer with a six-figure income and twenty years of perfect payment history was paying the same interest rate as a recent college graduate with no financial track record. The bank was being compensated the same amount for wildly different levels of risk. Meanwhile, millions of consumers who might have been perfectly good credit risks — people with modest incomes but reliable payment behavior — were being excluded entirely because they did not fit the narrow profile that banks required. It was as if the airline industry charged everyone the same price for every seat on every flight, regardless of when they booked, where they sat, or how far they flew. The inefficiency was staggering — and in every inefficiency, Fairbank saw an opportunity.

Fairbank, the son of a Stanford physicist named William Fairbank and a pioneering researcher named Jane Davenport Fairbank who had worked at MIT's Radiation Laboratory during World War II, brought a scientist's mindset to this problem. He had earned his undergraduate degree in economics from Stanford in 1972 and then, after a period working various jobs, returned to earn his MBA from Stanford Graduate School of Business in 1981, graduating first in his class. He joined Strategic Planning Associates shortly afterward and was tasked with building the firm's banking practice.

What Fairbank recognized was breathtaking in its simplicity: credit cards were not a banking problem. They were a data problem.

If you could gather enough information about individual consumers — their spending habits, their payment behavior, their risk profiles, their responsiveness to different offers — you could design thousands of different credit card products, each one tailored to a specific customer segment. Instead of one-size-fits-all, you could do mass customization. Instead of guessing, you could test. Instead of following the herd, you could run experiments.

He called this concept Information-Based Strategy, or IBS. Think of it as bringing the scientific method to consumer finance. In a laboratory, you do not guess whether a drug works — you design a controlled experiment, administer the drug to a test group and a placebo to a control group, measure the results, and draw conclusions from the data. Fairbank wanted to do the exact same thing with credit cards: design an offer, send it to a carefully selected test group, measure the response rate and credit performance, and use the results to refine the next offer. No intuition, no committee consensus, no "this is how we've always done it." Just evidence.

To build it, he needed a partner.

Enter Nigel William Morris, born in 1958 in the United Kingdom, educated in psychology at North East London Polytechnic and then in business at London Business School, where he earned his MBA and later became a Fellow of the school. Morris was working alongside Fairbank at Strategic Planning Associates, and the two shared a fascination with using data to solve business problems. Where Fairbank was the visionary architect — the big-picture thinker who could see the entire credit card industry as a single, solvable optimization problem — Morris was the operational builder, the person who could take an abstract framework and turn it into a functioning machine. Their partnership was complementary in the deepest sense: Fairbank provided the "what" and "why," Morris provided the "how." Together, they began developing a detailed plan for how a bank could use data analytics, scientific testing, and mass customization to dominate the credit card business.

There was just one problem: they needed a bank willing to let them try.

Between roughly 1986 and 1988, Fairbank and Morris pitched their concept to more than twenty national retail banks across the country. The response was uniform rejection.

Major banks had no interest in overhauling their credit card operations based on a consultant's theory about data. The product was profitable as it was. Why change? The rejections piled up — some polite, some dismissive, all of them wrong.

Then came Signet Bank.

Signet was a regional bank based in Richmond, Virginia — not a household name, not a national powerhouse, not anyone's first choice for a revolutionary experiment. It had roughly a billion dollars in credit card receivables, a rounding error compared to Citibank or Chase. But Signet's leadership had a quality that the larger banks lacked: they were willing to listen. The large banks had no incentive to change — their credit card operations were printing money at 19.8 percent interest rates. Why would they invite two consultants to blow up a profitable business model? Signet, by contrast, had everything to gain and relatively little to lose. The bank's management saw Fairbank and Morris's pitch as an opportunity to leapfrog larger competitors through technology rather than scale — the classic innovator's dilemma in reverse, where the small player embraces disruption because it has no legacy franchise to protect.

There was a critical condition attached: Signet would not hire them as outside consultants. Fairbank and Morris had to become employees of the bank, putting their careers and reputations on the line. No more consulting fees. No safety net. If their idea failed, their careers in banking would be over before they started.

They agreed. In 1988, Richard Fairbank and Nigel Morris walked into Signet Bank's offices in Richmond, Virginia, and began building what would become Capital One.

They warned Signet's leadership that their vision would require "virtually starting over, rebuilding a very different company." They demanded a culture that was nonhierarchical, one that challenged everything. They consulted with Oracle Corporation on how to compile demographics and statistics to identify and segment customer markets. And then they began doing something that no bank had ever done at scale: running experiments.

Their plan was elegant in concept and grueling in execution. They would design credit card offers with different combinations of interest rates, credit limits, annual fees, introductory rates, and marketing messages. They would send these offers to carefully selected customer segments. They would measure the response rates, the default rates, the profitability of each segment. And then they would do it again, thousands of times, constantly refining their models.

The methodology they developed — which Capital One would later call "test-and-learn" — was essentially the scientific method applied to consumer finance. Every business decision became a testable hypothesis. To put this in concrete terms: if a traditional bank wanted to launch a new credit card product, it would convene a committee of senior executives, debate the product's features based on experience and gut instinct, design a marketing campaign based on what had worked before, launch the product nationally, and hope for the best. If it failed, they would learn from the failure — eventually. Fairbank and Morris did it completely differently. They would design not one product but twenty variations. They would send each variation to a small, carefully selected sample of consumers. They would measure the results with statistical rigor. Within weeks, they would know which variation performed best — and they would launch that one at scale while simultaneously testing the next round of variations. The feedback loop was orders of magnitude faster than anything the banking industry had seen.

The real estate crisis of the late 1980s nearly killed the experiment before it could prove itself. Signet's real estate loan portfolio went into severe decline, and the bank's managers wanted to shut down the fledgling credit card program to offset losses. The data-driven card operation, still in its early stages, was burning cash and management attention while the rest of the bank was fighting for survival.

Then came the breakthrough that saved everything.

III. The Signet Years: Building the Machine (1988–1994)

In 1991, Fairbank and Morris launched what would become one of the most consequential direct mail campaigns in financial history. The concept was deceptively simple: offer consumers the ability to transfer their existing credit card balances from other banks to a Signet card at a lower introductory interest rate. This was the balance transfer — a product innovation that seems obvious in hindsight but was revolutionary at the time. No major bank had systematically targeted competitors' customers with a lower-rate offer designed to poach their balances.

The results were staggering. Consumers, who had been paying 19.8 percent interest on their existing cards because every bank charged the same rate, suddenly had an alternative. A typical consumer might receive a letter in the mail offering to transfer their $5,000 balance from their Citibank card at 19.8 percent to a new Signet card at 7.9 percent for an introductory period. The math was obvious: they would save hundreds of dollars in interest. They responded in droves. Signet's credit card operation, which had been managing a modest portfolio, began growing at an extraordinary pace as balance-transfer customers flooded in from larger competitors.

But the balance transfer was just the surface innovation — the tip of the iceberg visible to consumers and competitors. What made it work was the data engine underneath, invisible to the outside world. Fairbank and Morris were not sending the same offer to everyone. They were using their growing database to identify which consumers were most likely to transfer a balance, which ones were most likely to keep that balance (and pay interest on it) rather than churning to the next offer, and which ones represented acceptable credit risks. They were, in effect, using their technological know-how to find the best possible risks among customers not typically offered cards — tapping into what the industry would later call the subprime market, but doing it with a precision that traditional banks could not match.

The test-and-learn methodology scaled rapidly. By 1994, the credit card team was running hundreds of simultaneous experiments. Each experiment had a control group and one or more test groups, with variables ranging from the envelope design to the interest rate to the credit limit to the timing of the mailing. Should the envelope be white or blue? Should the introductory rate be 5.9 percent for six months or 7.9 percent for twelve months? Should the credit limit be $3,000 or $5,000? Should the mailing go out on Tuesday or Thursday? Every one of these questions was answered not by opinion but by experiment. The results fed back into increasingly sophisticated models that could predict consumer behavior with remarkable accuracy. Capital One developed what they called "champion-challenger" methodology: the current best approach (the champion) was constantly tested against experimental alternatives (the challengers). If a challenger outperformed the champion, it became the new champion — and the cycle continued.

Signet's credit card operation quickly became its most profitable enterprise — generating almost two-thirds of Signet's total earnings by the time the spinoff was announced. This was an astonishing imbalance: a small experimental program launched by two outsider consultants was now generating more profit than all of Signet's traditional banking businesses combined. The credit card division had grown from managing roughly a billion dollars in receivables to multiples of that figure in just a few years, powered by a customer acquisition engine that was unlike anything in the banking industry.

This created a paradox that would force the eventual separation. A small regional bank in Virginia was housing a fast-growing, technology-driven credit card business that demanded a fundamentally different culture, different talent, different investment levels, and different strategic ambitions than anything else in Signet's portfolio. The card business was nonhierarchical, experimental, and data-obsessed — a startup culture within a staid banking institution. The rest of Signet was a traditional regional bank focused on branches, mortgages, and commercial lending, where decisions were made through established hierarchies and change happened slowly. The two cultures were oil and water.

The tension became untenable. The credit card division needed capital to grow, talent to recruit, and freedom to innovate at a pace that the parent bank could not support. Signet's management, to their credit, recognized that holding onto the credit card business would constrain both entities. Rather than trying to force a technology startup's culture into a regional bank's structure, they made the decision to let go of their golden goose.

On July 21, 1994, Signet Financial Corp announced the corporate spinoff of its credit card division. It was a bet that would transform American finance — but first, the new company needed a name, a stock listing, and the courage to stand alone.

IV. The IPO and Independence (1994–1995)

The spinoff was initially announced under the name OakStone Financial Corporation — a name chosen to convey financial strength and stability. Richard Fairbank was named Chairman and CEO, Nigel Morris was named President and Chief Operating Officer, and the two men who had been rejected by more than twenty banks just six years earlier were suddenly running a publicly traded company.

The initial public offering priced at sixteen dollars per share in late 1994, and shortly afterward, the company was renamed Capital One Financial Corporation in October 1994. The full separation from Signet was completed in February 1995, and Capital One began trading as an independent entity.

At the time of independence, Capital One ranked among the top ten credit card issuers in the country, serving more than five million credit card customers. It was a remarkable starting position for a company that had begun as two consultants and a whiteboard just seven years earlier.

The early days of independence were not smooth.

Capital One's stock hit an all-time low of $4.62 on December 9, 1994, just weeks after the IPO — a gut-wrenching decline that reflected the market's skepticism about a company that was, in Wall Street's terminology, a "monoline bank." That designation meant that all of Capital One's revenue came from a single product: credit cards.

In good times, a monoline model could produce exceptional returns because all resources were concentrated on one high-margin business. In bad times, there was no diversification to cushion the blow. A recession, a spike in defaults, or a regulatory crackdown on credit card practices could devastate the entire company.

The monoline risk was not theoretical. In 2002, federal regulators — the Federal Reserve Board and the Office of Thrift Supervision — imposed informal enforcement actions on Capital One, requiring the company to increase its loan-loss reserves and modify its revenue reporting. The company acknowledged that its subprime credit card portfolio was larger than investors had previously understood, and the stock price suffered accordingly. This episode forced a strategic rethinking that would shape the company's next decade.

But in the mid-1990s, the immediate challenge was simpler: grow or die. Capital One had built a powerful data engine, but it was competing against far larger banks with deeper pockets, bigger customer bases, and more established brands. The company was spending heavily on customer acquisition — those direct mail campaigns that would eventually make Capital One one of the largest mailers in the United States, second only to Citibank by 1994 in the volume of credit card solicitations sent.

The culture question loomed large from the very beginning. Was Capital One a bank or a technology company?

Fairbank was unequivocal: it was a technology company that happened to have a banking license. He recruited engineers and data scientists alongside traditional bankers. He insisted on a flat organizational structure that prized experimentation over hierarchy.

In 1997, Fairbank took his base salary to zero dollars — a gesture that was as symbolic as it was financial. By tying his entire compensation to long-term stock performance, he signaled that he viewed himself as a founder building a company, not an executive managing one. His interests were perfectly aligned with shareholders: if the stock went up, he was rewarded. If it went down, he earned nothing. This was virtually unheard of among bank CEOs, who typically collected substantial base salaries regardless of stock performance.

The market eventually came around. Capital One's stock recovered from its post-IPO lows and began a sustained climb as the company's growth rates became impossible to ignore. Quarter after quarter, the company reported customer growth, receivables growth, and earnings growth that dwarfed its competitors. Wall Street analysts who had been skeptical of a monoline credit card company gradually converted to believers as the data-driven model proved its superiority over traditional banking approaches.

But Fairbank and Morris were not celebrating. The balance transfer product continued to generate enormous volumes, but they could see the competitive dynamics shifting. Every major bank in America had started copying the balance transfer concept. Consumers were now receiving introductory rate offers from multiple banks simultaneously, creating a "rate surfing" phenomenon where cardholders would transfer their balances to whoever offered the lowest teaser rate, then transfer again when the promotional period expired. The customer acquisition costs were rising, the promotional periods were getting longer, and the margins were compressing. Capital One needed to innovate beyond the balance transfer — or risk becoming just another credit card company in an increasingly commoditized market.

V. The Growth Machine: Innovation and Expansion (1996–2000)

In 1996, Capital One made a decisive pivot. The company moved beyond its reliance on teaser rates to generate new customers and began developing a much broader product portfolio.

The innovation team — which by now was running thousands of experiments per year — rolled out co-branded credit cards, secured cards for consumers with limited credit histories, and joint account products. Co-branded cards carried the logos of retail partners, airlines, or sports teams, giving consumers a reason to choose Capital One beyond the interest rate. Secured cards — which required a cash deposit as collateral — allowed consumers with damaged or limited credit histories to obtain a credit card and rebuild their credit scores. Joint account products served couples and families who wanted shared credit. Each new product was designed, tested, and refined using the same information-based strategy that had powered the balance transfer revolution.

The experimentation machine was scaling at an extraordinary pace. By 1997, Capital One was running approximately 14,000 tests per year. By 2000, that number had grown to 45,000.

Think about what that means operationally. Forty-five thousand controlled experiments in a single year — each one with a hypothesis, a test group, a control group, and a measured outcome. This was not a bank running a few marketing campaigns. This was a scientific research operation that happened to issue credit cards. The sheer volume of experimentation created a compounding advantage: every test generated data, every data point refined the models, and every refined model produced better results on the next round of tests. Competitors who were running dozens or even hundreds of tests per year could not keep pace.

Two structural moves in 1996 dramatically expanded Capital One's strategic options. First, Capital One received approval from the federal government to establish Capital One FSB, a federal savings bank. To understand why this mattered, consider the structural limitation Capital One had been operating under. As a pure credit card company, it could not accept deposits from consumers. It had to fund its lending operations entirely through wholesale capital markets — issuing bonds, securitizing receivables, borrowing from other financial institutions. A savings bank charter changed the equation. Now Capital One could accept and retain deposits on secured cards and — critically — issue automobile installment loans. The savings bank charter opened the door to product lines that had been structurally unavailable to a monoline credit card issuer and provided a cheaper, more stable source of funding.

Second, Capital One expanded internationally, launching operations in the United Kingdom and Canada. The UK expansion, centered in Nottingham with facilities opening between 1997 and 2000, gave Capital One access to a credit card market that was significantly less competitive than the American market. British banks were even further behind in applying data-driven approaches to consumer lending, making Capital One's information-based strategy even more differentiated overseas than it was at home. The Canadian market offered similar opportunities. Capital One would later deepen its Canadian presence by acquiring the Hudson's Bay Company's private credit card portfolio in 2011 and establishing a co-branded credit card partnership with Walmart Canada.

The results spoke for themselves. An article in Chief Executive magazine in 1997 noted that Capital One held $12.6 billion in credit card receivables and served more than nine million customers — nearly double the customer count from just two years earlier. The company's stock price reflected the momentum: Capital One was added to the Standard and Poor's 500 index, and its stock price exceeded one hundred dollars for the first time in 1998. For early investors who had bought at the IPO price of sixteen dollars — let alone those who had the nerve to buy at the December 1994 low of $4.62 — the returns were extraordinary. The stock had increased more than six-fold in barely four years, making it one of the best-performing financial stocks of the decade.

The S&P 500 inclusion was more than a prestige milestone. It forced index funds to buy Capital One shares, broadened the investor base, and validated the company's transformation from a quirky monoline experiment into a mainstream financial institution. Fairbank had proven that a data-driven credit card company could compete with — and outperform — the largest banks in America.

The auto finance entry came in July 1998 when Capital One acquired Summit Acceptance Corporation, a Dallas-based subprime auto lender managing approximately $260 million in loans. This was a calculated move to apply the information-based strategy to a new asset class — and it illustrates one of Fairbank's most important strategic instincts. The logic chain was straightforward: if you could use data to identify the best risks among credit card applicants, you could do the same thing in auto lending. The underlying skill — analyzing consumer data to make better lending decisions than your competitors — was portable across product categories. Summit became a wholly owned subsidiary and was later renamed Capital One Auto Finance, the seed of what would grow into one of the largest auto lending operations in the United States.

The year 2000 marked a symbolic milestone: Capital One joined the Fortune 500, a remarkable ascent for a company that had been an internal division of a regional Virginia bank just six years earlier. Annual earnings reached $470 million on $30 billion in credit card receivables, representing a quadrupling of earnings since the IPO.

The same year, Capital One launched what would become one of the most recognized advertising campaigns in financial services history. The "What's in your wallet?" campaign debuted with a memorably absurd premise: a troupe of marauding Vikings causing comedic chaos in everyday settings, followed by the now-iconic tagline. The campaign was deliberately designed to be unlike any financial services advertising that existed — humorous, slightly irreverent, and instantly memorable. It worked spectacularly. Brand recognition climbed from 61 percent in June 1999 to 92 percent by December 2001, and eventually reached near-universal awareness at 99 percent within three years of launch. The campaign later featured celebrities including Samuel L. Jackson and Jennifer Garner, and has remained in continuous use for over two decades — one of the longest-running advertising campaigns in the financial services industry. The "What's in your wallet?" tagline became so deeply embedded in American culture that it transcended advertising and became a catchphrase, giving Capital One a brand presence that rivaled banks many times its size.

But beneath the headline numbers, Fairbank was already thinking about a fundamental strategic vulnerability. Capital One was still, at its core, a credit card company. The monoline model that had powered its rise was also its greatest weakness. One severe credit cycle, one regulatory intervention, one shift in consumer behavior could threaten the entire enterprise. The next chapter of Capital One's story would be about diversification — and it would require Fairbank to become one of the most aggressive acquirers in American banking history.

VI. Beyond Credit Cards: The Diversification Imperative (2001–2008)

In 1999, Richard Fairbank stood before analysts and made an announcement that surprised no one who had been paying attention: Capital One was going to expand beyond credit cards.

The company would use its expertise in collecting and analyzing consumer data to offer loans, insurance, and other financial products. Fairbank even floated the idea of phone service — a diversification so far afield that it raised eyebrows on Wall Street. The monoline model had been extraordinarily profitable, but Fairbank understood that a company dependent on a single product line was perpetually one recession away from an existential crisis. The regulatory action of 2002, when federal regulators forced Capital One to acknowledge the true size of its subprime portfolio and increase reserves, had only reinforced this conviction.

The diversification began with auto lending. In October 2001, Capital One acquired PeopleFirst Finance, a San Diego-based company with more than 270 employees that billed itself as the nation's largest online motor vehicle lender. PeopleFirst had been founded in the late 1990s and was originating and servicing consumer auto and motorcycle loans primarily through the internet — a distribution model that aligned perfectly with Capital One's data-driven, technology-first approach. The acquisition combined PeopleFirst with the Summit Acceptance operation that Capital One had purchased in 1998. The two entities were merged and rebranded as Capital One Auto Finance Corporation in 2003, creating a unified platform that could originate auto loans both online and through traditional dealer channels.

The auto finance business proved to be one of Capital One's most successful diversification moves. The same information-based strategy that worked for credit cards — using data to identify the best risks, pricing loans precisely based on individual borrower profiles, running thousands of experiments to optimize every aspect of the lending process — translated remarkably well to auto lending. Capital One Auto Finance grew steadily over the next two decades and today ranks as the number-one financier among used-vehicle lenders in the United States, with average auto loans of $77.2 billion as of early 2025.

But auto lending, while valuable, was diversification within the same general category — consumer credit. Fairbank wanted something more fundamental: he wanted branches. Physical bank branches with deposits. To understand why this mattered so much, consider how Capital One funded its credit card lending. When Capital One issued a credit card and a customer carried a balance, Capital One needed capital to fund that balance. Without deposits, the company relied on wholesale capital markets — issuing bonds, selling asset-backed securities, borrowing from institutional lenders. These funding sources worked fine in calm markets but could become expensive or even unavailable during financial crises, precisely when a lender needed them most. Deposits, on the other hand, were stable, cheap, and sticky. A customer who deposited their paycheck into a checking account was unlikely to withdraw it all at once, providing the bank with a reliable pool of low-cost funds. This was the fundamental economic advantage that traditional banks had over monoline lenders — and Fairbank was determined to acquire it.

The first major banking acquisition was Hibernia National Bank in 2005. Hibernia was based in New Orleans with branches across Louisiana and Texas — a solid franchise in a growing region with deep community ties and a loyal customer base. The deal was announced in March 2005 at approximately $5.3 billion, and everything seemed straightforward.

Then came Hurricane Katrina.

On August 29, 2005, one of the most devastating natural disasters in American history struck the Gulf Coast, flooding eighty percent of New Orleans and displacing more than a million residents. Hibernia's branch network was directly in the storm's path. Branches were damaged or destroyed. Employees were displaced. Loan portfolios were threatened as borrowers lost homes and businesses. Most acquirers would have walked away from the deal, invoking a material adverse change clause. Capital One renegotiated the price down to approximately $5.0 billion — a nine percent reduction reflecting the storm's damage — and closed the deal in the fourth quarter of 2005. This decision spoke volumes about Fairbank's strategic commitment. He was not buying Hibernia for its next quarter's earnings; he was buying it for its long-term franchise value — the branch network, the deposit base, the customer relationships. Those assets would recover. The strategic gap they filled — giving Capital One its first physical branch network — was worth more than the short-term disruption.

The following year brought an even larger deal. In March 2006, Capital One announced the acquisition of North Fork Bancorp for approximately $14.6 billion, including $5.2 billion in cash — making it one of the largest bank acquisitions in the country that year. North Fork operated banks in New York and New Jersey, giving Capital One a presence in the nation's largest and wealthiest metropolitan market. The North Fork shareholders received $31.18 per share, representing a 22.8 percent premium. The acquisition made Capital One one of the top ten banks in the United States by deposits and managed loans, fundamentally altering the company's identity from a credit card specialist to a diversified financial institution. In the space of just eighteen months, Fairbank had acquired branch networks spanning the Gulf Coast and the Northeast corridor — a geographic footprint that no organic growth strategy could have achieved in a decade.

But the North Fork deal came with a hidden liability. Bundled inside North Fork was GreenPoint Mortgage, a mortgage lending subsidiary that had been aggressively originating loans during the housing boom. As the subprime mortgage crisis began unfolding in 2007, GreenPoint's loan portfolio deteriorated rapidly. Capital One moved quickly and decisively: on August 20, 2007, less than a year after closing the North Fork acquisition, Fairbank shut down GreenPoint Mortgage entirely. The closure resulted in 1,900 job cuts and $860 million in charges — a painful lesson in the risks of acquisition-driven growth. GreenPoint was later identified among the top twenty-five subprime lenders by the Center for Public Integrity.

The GreenPoint episode is worth dwelling on because it reveals something important about Fairbank's leadership style — and it stands in stark contrast to how most bank CEOs handled the unfolding mortgage crisis. Throughout 2007 and 2008, CEOs at Citigroup, Merrill Lynch, Bear Stearns, and Washington Mutual clung to their mortgage operations long after the problems were obvious, hoping the market would recover, restructuring rather than shutting down, and watching their losses compound quarter after quarter. Many of those banks ultimately failed or were acquired at fire-sale prices. Fairbank cut his losses immediately and completely. He recognized that GreenPoint's problems were structural, not cyclical, and that every dollar and every hour spent on a failing mortgage business was a dollar and an hour diverted from Capital One's core strengths. The speed of the decision — shutdown within months of recognizing the problem — demonstrated a willingness to absorb short-term pain for long-term strategic clarity. It was the kind of decisive action that separates founder-CEOs from professional managers: Fairbank was not protecting a business unit, he was protecting the company.

There is a fascinating footnote to Capital One's pre-crisis operations that illuminates just how central direct mail was to the company's business model. In late 2002, Capital One and the United States Postal Service negotiated the first-ever Negotiated Services Agreement — a customized bulk mail pricing arrangement that gave Capital One declining block rates for volumes above stated thresholds in exchange for Capital One maintaining superior address quality and using electronic notification for undeliverable mail. The agreement was capped at $40.6 million in cumulative discounts over three years and was extended in 2006. Capital One was sending hundreds of millions of direct mail solicitations annually — a volume so enormous that the Postal Service created a bespoke pricing structure that no other mailer qualified for.

When the financial crisis of 2008 hit, Capital One was in a stronger position than many of its peers precisely because of the diversification strategy. The company had reduced its dependency on credit cards, had stable deposit funding from its branch acquisitions, and had already taken the GreenPoint write-down — meaning the worst surprise was already behind it. Capital One accepted $3.57 billion in TARP funding — the government's Troubled Asset Relief Program — a decision that was more about demonstrating solidarity with the banking system than about survival. The company repaid the TARP funds in June 2009, among the earliest major banks to do so, signaling to the market that Capital One's balance sheet was strong enough to stand on its own.

The crisis, while painful, validated Fairbank's conviction that a monoline model was unsustainable and that diversification was an existential necessity, not a strategic luxury. Banks that had remained concentrated in single product lines or geographic markets were devastated. Capital One, with its diversified revenue streams and stable deposit base, emerged not just intact but positioned to go on offense. And go on offense it did — in spectacular fashion.

VII. The Empire Builder: Major Acquisitions Era (2009–2012)

The years 2009 through 2012 represent the most audacious period of empire building in Capital One's history — a three-year stretch in which Fairbank executed a series of acquisitions that fundamentally repositioned the company in American banking. The strategy was bold, the execution was complex, and the regulatory scrutiny was intense. But when the dust settled, Capital One had transformed itself from a mid-tier diversified bank into one of the largest financial institutions in the United States.

The opening move was relatively modest but revealing. In February 2009, with the financial crisis still raging and bank valuations at generational lows, Capital One acquired Chevy Chase Bank for $520 million in cash and stock. Chevy Chase was a well-regarded Washington, D.C.-area bank with a strong branch network in the affluent suburbs of Maryland and Virginia. It had gotten into trouble during the crisis, and its owners were looking for a buyer. Capital One paid what amounted to a distressed price for a franchise that, in normal times, would have commanded a significant premium. The deal expanded Capital One's retail branch footprint in the Mid-Atlantic region — conveniently close to its own McLean, Virginia operations — and demonstrated that Fairbank was prepared to capitalize on the crisis while other banks were still in survival mode. But Chevy Chase was just the appetizer.

The main course arrived in June 2011 when Capital One announced one of the most transformative deals in modern banking history: the acquisition of ING Direct USA from the Dutch financial conglomerate ING Groep. ING Direct was the nation's leading direct bank — an online-only institution with no physical branches, more than seven million customers, and approximately $84.4 billion in deposits. The price tag was approximately $9 billion: $6.3 billion in cash plus roughly 54 million Capital One shares, representing a 9.7 percent ownership stake in the combined company.

The strategic logic was compelling — and it demonstrated the kind of systems thinking that had characterized Capital One from the very beginning. ING Direct's massive deposit base would provide Capital One with low-cost, stable funding to support its credit card and auto lending operations.

Before the deal, Capital One relied heavily on wholesale funding markets and securitization to finance its loan portfolio — sources that worked well in normal times but had proven treacherous during the 2008 crisis. ING Direct's $84 billion in deposits changed that equation dramatically, giving the company a permanent, low-cost source of funds that was largely insulated from capital market volatility.

The acquisition catapulted Capital One from the eighth-largest bank in the United States by deposits to the fifth — bigger than U.S. Bancorp and just below Citigroup.

But the deal faced intense regulatory scrutiny — a preview of the even more grueling process that the Discover acquisition would later endure. The scale of the ING Direct acquisition triggered public hearings and extended review periods. Community groups and consumer advocates raised concerns about concentration in the banking industry and Capital One's compliance record. Critics argued that allowing a credit card company — one with significant exposure to subprime borrowers — to absorb one of the nation's largest deposit bases would create systemic risk. The Federal Reserve and the Office of the Comptroller of the Currency subjected the deal to a level of examination that tested Fairbank's patience and Capital One's regulatory affairs team. The review stretched across eight months, during which time the deal was in limbo and competitors circled, hoping the regulatory process would collapse the transaction.

In February 2012, regulators finally approved the acquisition, and Capital One completed the deal. The company then faced the delicate task of rebranding one of the most recognized online banking platforms in the country. ING Direct's distinctive orange ball logo and bright, consumer-friendly brand had built enormous customer loyalty. Capital One received permission to merge ING Direct into its business in October 2012 and rebranded the platform as Capital One 360 in November 2012, retiring the orange ball in favor of Capital One's swoosh. The transition was handled carefully — Capital One preserved the no-fee, high-rate account structures that had attracted ING Direct's customers, ensuring that the rebranding did not trigger a mass exodus of deposits.

Just two months after announcing the ING Direct deal, Capital One struck again. In August 2011, the company reached an agreement with HSBC to acquire HSBC's domestic credit card operations. This was a different kind of deal — not a bank acquisition, but a portfolio purchase. Capital One paid $31.3 billion in exchange for approximately $28.2 billion in outstanding credit card receivables, $600 million in other assets, and roughly 27 million active accounts. The premium of approximately $2.6 billion represented an 8.75 percent premium to the par value of the receivables. The deal included private-label credit card partnerships with iconic retail brands including Saks Fifth Avenue, Neiman Marcus, and Lord & Taylor.

The timing of these two deals — ING Direct and HSBC — was not coincidental. Fairbank was executing what amounted to a two-part strategic maneuver that, when viewed together, revealed its full brilliance.

On the right side of the balance sheet, ING Direct's deposits provided cheap, stable funding. On the left side, HSBC's credit card portfolio provided high-yielding earning assets. The deposits funded the loans. The loans earned returns on the deposits. Together, they created a self-reinforcing financial flywheel that improved both sides of Capital One's balance sheet simultaneously. It was the same kind of systems-level thinking that had produced the balance transfer innovation a decade and a half earlier — seeing the financial system as a set of interconnected components and designing a strategy that optimized across all of them.

The HSBC credit card acquisition closed in May 2012, and the integration of both ING Direct and the HSBC portfolio consumed much of Capital One's management bandwidth through 2013. The challenges were formidable: integrating millions of customer accounts across different technology platforms, migrating data between incompatible systems, rebranding products while maintaining customer relationships, harmonizing credit policies and risk management frameworks, and doing all of this while continuing to run the existing business. Capital One had to integrate approximately 27 million HSBC card accounts — each with its own billing cycle, interest rate, reward structure, and customer service history — without disrupting the cardholder experience. Simultaneously, the company was converting ING Direct's seven million customers to the Capital One 360 brand, migrating them to new systems while preserving the no-fee, high-rate account structures that had attracted them to ING Direct in the first place.

Capital One's experience with prior acquisitions — Hibernia, North Fork, Chevy Chase — provided a playbook, but the 2011-2012 deals were on an entirely different scale. By the end of 2012, Capital One had become the sixth-largest depository institution and the leading direct bank in the United States, with a credit card portfolio rivaling those of JPMorgan Chase and Citigroup.

The 2009-2012 acquisition spree demonstrated something that would become a hallmark of Capital One's strategy: the ability to use periods of market dislocation and industry restructuring to make transformative deals. Chevy Chase was bought during the financial crisis at distressed valuations. ING Direct was sold because its Dutch parent was under pressure from European regulators to divest non-core assets. HSBC was exiting the U.S. credit card market as part of a global strategic retreat. In each case, Capital One was the buyer precisely because it had the balance sheet strength, the management capability, and the strategic vision to absorb large, complex assets that other potential acquirers either could not or would not pursue.

Fairbank had spent the better part of a decade transforming Capital One from a monoline credit card company into a diversified financial institution with retail branches, a leading direct bank, and one of the largest credit card portfolios in the country. The next transformation would be even more ambitious: turning Capital One into a technology company.

VIII. Digital Transformation & Modern Era (2013–2023)

In 2015, Capital One made an announcement that seemed unremarkable at the time but proved to be one of the most consequential strategic decisions in modern banking: all new applications would be built to run on the public cloud, and all existing applications would be systematically rearchitected for cloud deployment. The company chose Amazon Web Services as its cloud provider, and what followed was a five-year migration that made Capital One the first major financial institution in the United States to exit its on-premises data centers entirely.

To appreciate why this matters, consider what "going to the cloud" means for a bank. For a non-technical audience, here is a simple analogy: traditionally, every major bank operated its own private computing infrastructure — massive, air-conditioned rooms filled with servers that the bank owned, maintained, and secured. This is like owning your own power plant to generate electricity for your home. "Going to the cloud" means moving all of that computing to a shared infrastructure operated by Amazon — it is like switching from your own power plant to the electrical grid. You gain flexibility, scalability, and cost efficiency, but you also depend on someone else's infrastructure. For most companies, this is a straightforward decision. For a bank handling sensitive financial data for millions of consumers, operating in one of the most heavily regulated industries in the economy, and requiring near-perfect uptime, it was an act of extraordinary conviction. Regulators had long viewed cloud computing with suspicion, concerned about data security, vendor concentration risk, and operational resilience.

Capital One closed its last physical data center in 2020, completing a migration that involved shutting down eight data centers and rebuilding roughly 80 percent of its applications to be cloud-native. The company adopted microservices architecture, RESTful APIs, and serverless computing at a scale that would have been impressive for a Silicon Valley startup, let alone a bank managing hundreds of billions of dollars in assets. By 2022, more than a third of Capital One's applications were running on serverless technology, and the company had gone from quarterly or monthly code releases to multiple deployments per day.

The technology transformation was not just about infrastructure. It was about culture — about turning a bank into a software company. Capital One built an 11,000-person technology organization, with approximately 85 percent — roughly 9,000 people — being engineers. To put that in perspective, that is more engineers than many technology companies employ in total. The company launched an internal "Tech College" in 2017 to support continuous learning in software engineering, cloud computing, data science, machine learning, and security. Engineers were given monthly "Invest in Yourself" days dedicated to training and certification. The average time to build a development environment dropped from three months to minutes — a reduction that sounds incremental but is actually transformational, because it means engineers spend their time building products rather than configuring infrastructure. Capital One shifted from waterfall development — where software was planned, built, and released in lengthy sequential phases — to agile methodology and DevOps, where small teams own their products end-to-end and can deploy code changes independently.

In 2018, Capital One opened its new headquarters in McLean, Virginia, designed as a physical embodiment of the company's technology-first identity. The campus featured open floor plans, collaborative workspaces, and a design aesthetic that deliberately evoked Silicon Valley rather than Wall Street. Engineers, designers, and data scientists worked side by side in an environment that looked more like Google's offices than a bank headquarters. The physical space was a statement of intent: this is who we are.

Then came the crisis that tested every element of Capital One's technology strategy.

On July 29, 2019, Capital One publicly disclosed one of the largest data breaches in the history of the financial services industry. A former Amazon Web Services software engineer named Paige Thompson had exploited a misconfigured web application firewall in Capital One's AWS infrastructure between March 22 and 23, 2019. Using a server-side request forgery vulnerability, Thompson accessed Capital One's cloud storage and exfiltrated data affecting 106 million people in the United States and Canada. The compromised data included names, addresses, dates of birth, credit scores, credit limits, and payment histories. Approximately 140,000 Social Security numbers, one million Canadian social insurance numbers, and 80,000 bank account numbers were exposed.

The breach was not discovered until July 19, 2019, when a GitHub user spotted Thompson's post about the stolen data and alerted Capital One. Thompson was arrested within days and was ultimately convicted in June 2022 on seven hacking-related charges. Capital One faced an $80 million penalty from the OCC, a $190 million class-action settlement with affected customers, and total financial losses from the breach estimated at approximately $300 million.

The irony was bitter: Capital One, the bank that had staked its identity on technological sophistication, had been compromised by a misconfigured firewall — a basic operational error, not a sophisticated nation-state attack. The breach exposed a fundamental truth about technology leadership: being the most advanced does not make you the most secure. Complexity creates attack surface, and Capital One's sprawling cloud infrastructure had more potential points of failure than a traditional data center.

But the response demonstrated the same decisive management style that had characterized the GreenPoint shutdown. Capital One invested heavily in security improvements, worked cooperatively with regulators, and earned release from the related consent order by 2022. The company continued its cloud-first strategy without flinching — a decision that reflected Fairbank's conviction that the long-term advantages of cloud computing outweighed the short-term reputational damage of the breach. The incident was a humbling reminder that being a technology leader also means being a target, and that technological sophistication is no substitute for operational rigor in every configuration, every access control, every firewall rule.

Beyond the breach, the 2013-2023 period saw Capital One continue to refine its strategic focus. The company exited mortgage lending in 2017, concluding that the mortgage market's low margins and intense competition did not justify the capital and management attention required. This was another example of Fairbank's willingness to prune businesses that did not fit Capital One's core strengths — a discipline that many diversified financial institutions lack.

The COVID-19 pandemic, which upended virtually every industry beginning in March 2020, paradoxically accelerated trends that played to Capital One's strengths. Digital banking adoption surged as consumers avoided physical branches — a shift that many industry observers expected would take five to ten years happened in five to ten weeks. Capital One's 360 digital platform, built on cloud-native infrastructure, was ideally positioned to absorb this wave of new digital customers. The company's AWS-based infrastructure provided the elasticity to scale up capacity on demand, handling spikes in digital traffic that would have overwhelmed traditional on-premises data centers.

The pandemic's economic effects were more complex. Stimulus payments and reduced consumer spending temporarily improved credit quality across the industry, as consumers used government checks to pay down credit card balances. Credit card charge-off rates dropped to historic lows in 2021. But Capital One's management team, disciplined by decades of data-driven risk management, did not mistake a temporary improvement for a permanent shift. They built reserves in anticipation of the normalization that would inevitably follow — and indeed, charge-off rates began rising again in 2022 and 2023 as stimulus effects faded and consumer spending resumed.

By 2023, Capital One had become something genuinely unusual in American banking: a technology company operating at massive scale within a heavily regulated financial services framework. The company's technology capabilities were not just a competitive advantage — they were the foundation upon which Fairbank would attempt his most ambitious move yet.

IX. The Discover Acquisition: The Ultimate Power Play (2024–2025)

On February 19, 2024, Richard Fairbank made the announcement he had been building toward for thirty-five years.

Capital One would acquire Discover Financial Services in an all-stock transaction valued at $35.3 billion. Discover shareholders would receive 1.0192 Capital One shares for each Discover share, representing a 26.6 percent premium over Discover's closing price of $110.49 on February 16, 2024. At closing, Capital One shareholders would own approximately 60 percent and Discover shareholders approximately 40 percent of the combined company.

The deal would generate an estimated $2.7 billion in cost savings by 2027 — $1.5 billion in expense synergies from combining overlapping operations and $1.2 billion in network synergies from migrating Capital One's card volume onto Discover's rails. Capital One expected to issue roughly 257 million shares of common stock to complete the transaction.

Those financial details were significant, but they were not the reason this deal sent shockwaves through the financial services industry. The reason this deal mattered — the reason Richard Fairbank called it the culmination of a vision he had held since the company's founding — was the network.

What exactly is a payment network, and why was Fairbank willing to spend $35 billion to own one?

To understand the strategic significance, you need to understand the architecture of payments in America. When you swipe a credit card at a store, your transaction travels across a payment network — the "rails" that shuffle digital dollars between consumers, their banks, merchants, and the merchants' banks, collecting tolls along the way. In the United States, there are only four major credit card networks: Visa, Mastercard, American Express, and Discover. Visa and Mastercard are pure network operators — they do not issue cards directly but license their networks to banks like JPMorgan Chase, Citigroup, and Capital One, which issue cards bearing the Visa or Mastercard logo. American Express and Discover operate differently: they are both card issuers and network operators, dealing directly with merchants.

For a card issuer like Capital One, using Visa's or Mastercard's network means paying fees to those networks on every transaction — fees that represent a significant ongoing cost and a strategic dependency. You are essentially renting someone else's highway. Every time a Capital One cardholder swipes their Visa-branded card, Capital One pays Visa for the privilege of using its network. Over millions of transactions, those fees add up to billions of dollars annually across the industry. By acquiring Discover, Capital One would own its own highway. It would be an issuer with its own network, able to deal directly with merchants and eliminate the middleman fees paid to Visa and Mastercard. The economics of this are powerful: instead of paying tolls, you collect them.

Fairbank was explicit about the significance. "That network is a very, very rare asset," he said during the deal announcement. "We have always had a belief that the Holy Grail is to be able to be an issuer with one's own network so that one can deal directly with merchants."

He revealed that this vision had existed from the very beginning — from Capital One's founding in the late 1980s, he had envisioned creating a global digital payments technology company by owning the payment rails and dealing directly with merchants. For nearly four decades, this had been a dream without a viable path. Now, suddenly, the path was open.

The Discover network was accepted by 99 percent of U.S. merchants who take credit cards, matching Visa and Mastercard domestically. Discover also owned the PULSE debit network, which connected approximately 4,500 banks.

And here was a regulatory detail that made the deal even more attractive: the Durbin Amendment, enacted in 2010 to cap debit interchange fees for large banks, was explicitly written to exclude networks like Discover and American Express. This meant that Capital One could migrate its debit card portfolio to the Discover network and maintain interchange fee levels that were protected from the caps imposed on Visa and Mastercard transactions.

Capital One planned to migrate over 25 million debit cards carrying $175 billion in purchase volume to the Discover network, generating estimated network synergies of $1.2 billion in 2027 alone.

But first, the deal had to survive the regulatory gauntlet.

The regulatory review was among the most intensive in recent banking history — and for good reason. The combination of the largest credit card issuer with one of only four payment networks in the country raised fundamental questions about market concentration, consumer protection, and systemic risk. Capital One submitted its formal application in March 2024. Public meetings were held in multiple cities. Hundreds of public comments were submitted. Community groups weighed in on both sides — some praising Capital One's lending commitments, others raising concerns about the company's past regulatory issues and the implications of further consolidation in financial services. Consumer advocates scrutinized Capital One's compliance record, its credit card late fee practices, and the competitive impact of combining the company's massive card portfolio with Discover's network infrastructure. The DOJ's antitrust division also reviewed the deal for competitive concerns. The review consumed the better part of a year, during which Capital One's management team had to maintain deal discipline, keep both organizations focused and motivated, and navigate a politically charged regulatory environment.

In a parallel track, Capital One announced a five-year, $265 billion Community Benefits Plan — described as twice as large as any other community commitment ever developed in connection with a bank acquisition. The plan, developed in partnership with the National Association for Latino Community Asset Builders, NeighborWorks America, the Opportunity Finance Network, and the Woodstock Institute, committed Capital One to $125 billion in credit card lending to low-and-moderate-income consumers, $75 billion in auto finance lending to underserved communities, $44 billion in community development including $35 billion for affordable housing, $15 billion in small business lending, $600 million in capital to nonprofit community development financial institutions, and $575 million in philanthropy. The plan also included the launch of Ventures Lending, a mission-based credit card for underserved small businesses with below-market-rate pricing.

The regulatory dominoes began falling in late 2024. The Delaware State Bank Commissioner approved the transaction on December 18, 2024. Shareholders of both companies voted to approve the deal in February 2025 by overwhelming margins — more than 99.8 percent of Capital One shares and more than 99.3 percent of Discover shares voted in favor.

On April 18, 2025, the Office of the Comptroller of the Currency and the Federal Reserve Board both approved the deal. The OCC's approval was conditional — Capital One was required to submit a plan within 120 days of closing detailing corrective actions for outstanding enforcement actions against Discover Bank, which had been found to have overcharged interchange fees from 2007 through 2023.

The Discover interchange overcharging issue deserves attention, as it became Capital One's problem to resolve upon closing. The Federal Reserve assessed a $100 million fine against Discover for the overcharging, and the FDIC assessed a $150 million civil money penalty plus a requirement for Discover to distribute at least $1.225 billion in restitution to affected merchants. These were not trivial liabilities, and they represented a reminder that the Discover acquisition came with regulatory baggage as well as strategic assets.

On May 18, 2025, Capital One completed the acquisition. The final purchase consideration was $51.8 billion, reflecting the appreciation in Capital One's stock price between announcement and close.

The combined entity became the largest credit card issuer in the United States by loan balances, with approximately 19 percent market share, more than 100 million customers, and combined credit card loans exceeding $250 billion. Capital One was now the sixth-largest bank in the United States by total assets, approaching $669 billion. It had taken Fairbank thirty-seven years — from the founding concept in 1988 to the close in 2025 — to achieve the vision of an issuer with its own network.

The integration began immediately.

Capital One started migrating debit cards to the Discover network and began originating select Capital One credit card accounts — including the Venture, Savor, Quicksilver, and their variants — on the Discover Network. The flagship Venture X remained on the Visa network, and business cards stayed on Mastercard. Full credit card migration was targeted for completion by 2027, with integration costs expected to exceed $2.8 billion.

The early integration period brought some friction. Some cardholders experienced acceptance issues at small businesses with limited Discover network support. International travelers encountered more significant gaps, as Discover's global acceptance still trailed Visa and Mastercard outside the United States. These were expected growing pains, but they underscored the scale of the challenge ahead.

For investors watching the deal close, the critical question was straightforward: could Capital One execute the integration of a company with its own technology stack, its own culture, and its own regulatory baggage while simultaneously migrating hundreds of millions of transactions to a different payment network? The company's track record with ING Direct, HSBC, and prior acquisitions provided some confidence, but the Discover integration was more complex than anything Capital One had attempted before.

X. Playbook: The Capital One Method

Every great company has a playbook — a set of principles and practices that explain how it wins. Capital One's playbook has been remarkably consistent for more than three decades, even as the company has grown from a division of a regional Virginia bank into one of the largest financial institutions in the world.

Understanding this playbook is essential for anyone trying to assess what Capital One will look like in five or ten years. The playbook has six pillars.

The foundation is Information-Based Strategy. From its earliest days inside Signet Bank, Capital One treated every business decision as a testable hypothesis. The test-and-learn methodology — running controlled experiments at massive scale, measuring results, refining models, and repeating — created a compounding data advantage that grew more valuable with every passing year. By the time Capital One was running 45,000 experiments annually in 2000, competitors were not just behind; they were playing a fundamentally different game. Most banks made decisions based on experience, intuition, and committee consensus. Capital One made decisions based on evidence.

The second pillar is M&A as transformation.

Capital One has not used acquisitions to grow incrementally — adding a small bank here, a portfolio there, steadily expanding at the margins. Each major deal has been a strategic chess move designed to fundamentally alter the company's competitive position. Hibernia and North Fork provided the branch network and deposit base needed to escape the monoline trap. ING Direct provided cheap funding at scale. HSBC's credit card portfolio provided earning assets to deploy that funding against. And Discover provided the payment network that Fairbank had coveted since the company's founding.

The pattern is not random; it is a deliberate strategy of using acquisitions to fill strategic gaps that organic growth cannot address.

The third pillar is founder-led vision.

Richard Fairbank has served as CEO since Capital One's IPO in 1994 — a tenure exceeding thirty years. In an industry where CEO turnover is frequent and strategic direction shifts with each new leader, Fairbank's continuity has been an extraordinary competitive advantage. He has maintained a consistent long-term vision while adapting tactics to changing circumstances.

His zero-dollar base salary since 1997, with compensation tied entirely to long-term stock performance, aligns his interests with shareholders in a way that few bank CEOs can match. His 2024 compensation of $30.8 million, plus a $30 million one-time award tied to the Discover deal, and his 2025 compensation of $40 million reflect the board's view that his leadership has been transformational.

The fourth pillar is technology as differentiator.

Being the first major bank to go all-in on the public cloud was not a cost-saving exercise — it was a strategic bet that technology infrastructure would become a competitive weapon. The 11,000-person technology organization, with 9,000 engineers, gives Capital One capabilities that most banks cannot replicate. The ability to deploy code multiple times per day, to run experiments at scale, and to build new products on cloud-native architecture creates a speed advantage that compounds over time.

The fifth pillar is regulatory navigation.

Capital One has operated in one of the most heavily regulated industries in the economy for more than three decades. Rather than viewing regulation as purely a constraint, Fairbank has developed an institutional capability for navigating regulatory processes that has become a competitive advantage in itself. The ability to shepherd the ING Direct, HSBC, and Discover acquisitions through extended regulatory reviews — while maintaining deal momentum and stakeholder confidence — is a capability that few financial institutions possess. The $265 billion Community Benefits Plan associated with the Discover deal exemplifies this approach: proactively addressing community concerns before they become regulatory objections.

The final pillar is patience. In an industry obsessed with quarterly earnings, Capital One has consistently demonstrated a willingness to accept short-term costs for long-term strategic positioning. The GreenPoint shutdown, the exit from mortgage lending, the extended regulatory processes for major acquisitions — each involved near-term pain in service of a longer-term vision. Consider the timeline: Fairbank conceived of owning a payment network in the late 1980s. He acquired one in 2025. That is nearly four decades of patient, strategic positioning — identifying a goal, building the capabilities and scale necessary to pursue it, waiting for the right opportunity, and executing decisively when it arrived. In the world of quarterly-earnings-driven banking, that kind of patience is almost unheard of. It is the mark of a founder who thinks in decades, not fiscal years.

XI. Power Analysis & Competitive Dynamics

Capital One's competitive position has been fundamentally transformed by the Discover acquisition. To understand why, it helps to analyze the company through the lens of several structural advantages — and to compare those advantages against the competitive threats that could erode them.

The most significant is scale in data and technology. Capital One now processes billions of transactions annually across credit cards, debit cards, auto loans, and banking products — and with the Discover network, it sees transaction data not just from its own customers but from every card processed on the Discover rails. Each transaction generates data that feeds into the company's models, improving their predictive accuracy and enabling more precise pricing, marketing, and risk management. This creates a virtuous cycle: more customers generate more data, better data enables better products, better products attract more customers. A competitor entering the market today would need decades of data accumulation to replicate Capital One's analytical capabilities — and they would also need to build or acquire a payment network, a task so difficult that no one has successfully launched a new major credit card network in the United States in over forty years.

The Discover acquisition added a qualitatively different advantage: network economics. Owning the Discover payment network means that Capital One now earns revenue from every transaction processed on the network, regardless of which bank issued the card. The PULSE debit network connects 4,500 financial institutions, creating an embedded infrastructure position that generates recurring revenue with minimal marginal cost. As Capital One migrates its own card portfolio onto the Discover network, it simultaneously eliminates the fees it previously paid to Visa and Mastercard and earns the network revenue that those companies previously captured.

Switching costs in consumer banking are often underestimated by investors and analysts who think of financial products as commodities. Try changing your primary credit card sometime: you will need to update autopay settings across dozens of services — streaming subscriptions, utility bills, insurance premiums, gym memberships — each one requiring you to log in, navigate to payment settings, and enter new card details. Now try changing your primary bank account: you will need to redirect direct deposits from your employer, update bill pay for every recurring payment, transfer recurring payments, notify anyone who sends you money via ACH, and potentially reorder checks. The friction of switching is enormous, and it means that once a customer is acquired and begins using a product as their primary financial tool, retention rates tend to be remarkably high — particularly for customers who use multiple Capital One products across credit cards, banking, and auto lending. Each additional product creates an additional layer of switching cost, making the customer relationship progressively more durable.

Capital One's regulatory position functions as a structural moat. The barriers to entry in banking are enormous: obtaining a banking charter, meeting capital requirements, building compliance infrastructure, and navigating examinations from multiple federal and state regulators. The Discover acquisition further elevates these barriers by adding payment network regulation to the mix. A potential competitor would need not only to build a bank but to build or acquire a payment network — an asset so scarce that only four exist in the United States.

The competitive threats are real and significant. JPMorgan Chase, with its massive scale, $15 billion annual technology budget, and aggressive expansion of its Chase Sapphire and Freedom card franchises, remains the most formidable competitor in credit cards. JPMorgan's advantage is simple: it has more money, more customers, and more products than any other bank in America. If Capital One's information-based strategy is its competitive weapon, JPMorgan's brute-force scale is its counter. The two companies now compete directly across credit cards, consumer banking, and — with Capital One's ownership of Discover — increasingly in the payment network layer.

Fintech companies like SoFi, Chime, and numerous startups continue to target specific segments of Capital One's customer base with digital-first products that offer superior user experience and lower fees. While no single fintech threatens Capital One's overall franchise, collectively they nibble at the edges — attracting younger consumers, eroding fee income, and setting customer expectations for frictionless digital experiences that even the most technology-forward banks struggle to match.

And the long-term threat from Big Tech — Apple, Google, Amazon — looms largest of all. Apple's launch of the Apple Card in partnership with Goldman Sachs, Apple Pay's growing ubiquity as a payment method, and the potential for technology giants to use their platforms and their billions of active users to disintermediate traditional card issuers represent existential questions for the entire industry. These companies have something that no bank possesses: a direct, daily, intimate relationship with consumers through the devices they carry in their pockets. If Apple or Google decided to become serious competitors in lending — not just payments — they could potentially reach more consumers, more quickly, and with lower acquisition costs than any traditional card issuer.

The future of payments presents both opportunity and risk. Real-time payments — instantaneous bank-to-bank transfers that bypass card networks entirely — could reduce the volume of transactions flowing through traditional payment rails. Embedded finance, where payment functionality is built directly into software platforms and marketplaces, could shift power toward technology companies and away from traditional card issuers. And the possibility of central bank digital currencies, where the Federal Reserve itself issues a digital dollar, could fundamentally alter the economics of the payment networks that Capital One just acquired.

The Discover network is valuable in today's regulatory and technological environment, but the environment is evolving. Capital One's bet is that owning the rails positions it to adapt to whatever the payments landscape becomes — that a network owner can pivot to new technologies more easily than a network renter. Whether that bet proves correct depends on how rapidly the payment landscape changes and whether Capital One can evolve the Discover network to accommodate new transaction types, new technologies, and new regulatory frameworks.

XII. Bear vs. Bull Case

Bull Case

The bull case for Capital One begins with the Discover network.

Capital One now possesses one of the most scarce and strategically valuable assets in financial services — a payment network that generates toll-like revenue on every transaction. This positions Capital One uniquely among major banks: it is the only large-scale card issuer that also owns its own network infrastructure.

The strategic optionality is enormous. Capital One can migrate its existing card portfolio to reduce costs. It can attract other banks' cards onto the network to generate additional revenue. It can leverage the PULSE debit network's Durbin Amendment exemption to protect interchange income. And it can use the network's data — seeing both sides of every transaction — to build even more sophisticated risk models and marketing algorithms.

The technology advantage provides a structural cost and speed benefit. Capital One's cloud-native infrastructure, its massive engineering workforce, and its decades of data accumulation create capabilities that competitors cannot quickly replicate. In an industry where technology is increasingly the primary differentiator, Capital One has a meaningful head start.