CenterPoint Energy: Powering the Heartland

I. Introduction & Episode Roadmap

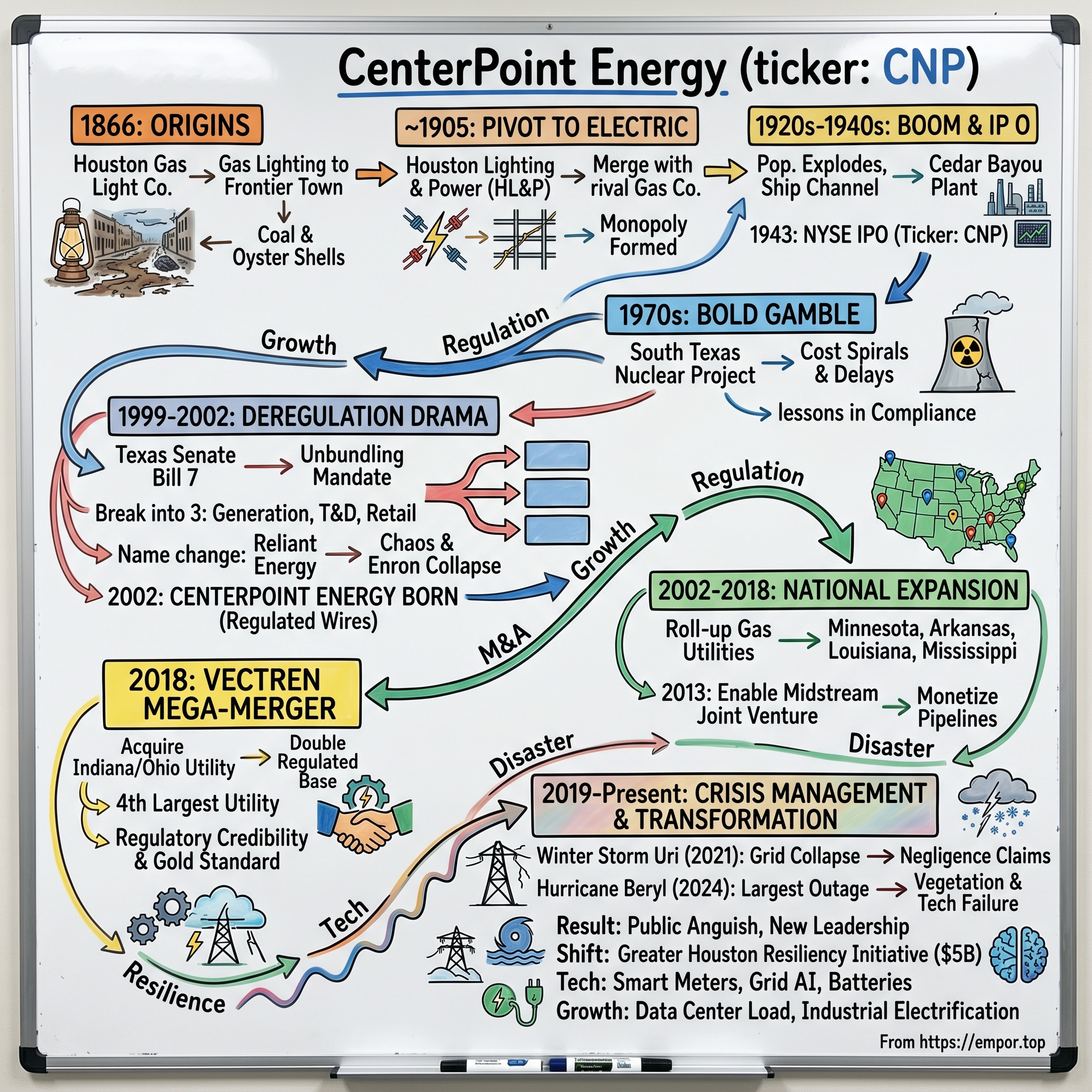

The year is 1866. Houston is barely a city—more swamp than metropolis, with 4,500 souls navigating muddy streets by kerosene lamp and moonlight. A group of local businessmen gather at a wooden table, their faces illuminated by flickering candles, to discuss something audacious: bringing gas lighting to their frontier town. They would crush oyster shells from Galveston Bay, mix them with coal shipped from Pennsylvania, and pipe the resulting gas through iron tubes beneath the dirt roads. This was the birth of Houston Gas Light Company, the ancestor of what would become CenterPoint Energy—today a $44 billion utility colossus serving 7 million customers across eight states.

How does a company that started lighting street lamps in a Texas bayou town transform into one of America's critical infrastructure giants? The answer involves 158 years of boom-bust cycles, political maneuvering, technological disruption, regulatory chess matches, and more than a few natural disasters that would have killed lesser companies. CenterPoint's story is really three interwoven narratives: the rise of Houston from frontier outpost to energy capital, the evolution of American utility regulation from local monopolies to deregulated markets and back again, and the endless tension between providing an essential public service while delivering returns to Wall Street.

Today's CenterPoint Energy operates in a fundamentally different universe from its gas lamp origins. The company runs regulated electric utilities in Texas and Indiana, natural gas distribution systems from Minnesota to Mississippi, and finds itself at the epicenter of America's energy transition. With data centers driving unprecedented electricity demand—CenterPoint forecasts nearly 50% load growth in Houston by 2031—while simultaneously navigating climate disasters that seem to arrive with biblical frequency, the company faces challenges its founders couldn't have imagined.

This episode traces that extraordinary evolution through distinct eras: the gas lamp beginnings when utilities were local monopolies handed out like political favors; the post-war boom when Houston Lighting & Power literally powered the space program; the deregulation drama that split Texas utilities into pieces and created today's competitive market chaos; the expansion years when CenterPoint stopped being a Texas company and became a national player; and the current era of crisis management, where every hurricane becomes a referendum on utility competence and every ice storm triggers legislative hearings.

We'll examine how CenterPoint navigated Texas's unique regulatory environment—part Wild West capitalism, part heavily regulated monopoly—and why the company's 2018 acquisition of Indiana's Vectren for $6 billion represented both its greatest strategic coup and its biggest integration challenge. We'll dissect the business model that allows utilities to earn regulated returns on massive capital investments while customers foot the bill, and explore why Wall Street simultaneously loves and fears these supposedly boring dividend machines.

Along the way, we'll uncover surprising insights: why utilities actually benefit from disasters (hint: reconstruction spending goes into the rate base), how data centers are fundamentally reshaping electricity economics, why Texas's deregulated market creates both the cheapest and most expensive power in America depending on when you measure, and how a company that moves at regulatory speed is trying to adapt to a world demanding Silicon Valley innovation.

Most importantly, we'll explore what CenterPoint teaches us about American infrastructure itself—how essential services get built, maintained, and paid for in a democracy where everyone wants reliable power but nobody wants to pay for it, where climate change is making hundred-year storms into annual events, and where the transition to clean energy collides with the physics of keeping the lights on.

II. The Gas Lamp Era: Origins & Early History (1866–1940s)

Picture Houston in 1866: Buffalo Bayou snakes through downtown, its banks lined with cotton warehouses and sawmills. The Civil War has just ended, Reconstruction is beginning, and this humid outpost 50 miles from the Gulf of Mexico dreams of becoming something more than a malaria-ridden afterthought. The city's leaders—cotton factors, railroad speculators, merchants who'd made fortunes running the Union blockade—understood that modern cities needed modern amenities. Gas lighting wasn't just about seeing at night; it was about signaling to the world that Houston belonged in the same conversation as New Orleans, St. Louis, and other rising Southern cities.

The Houston Gas Light Company's founding documents, signed in that watershed year of 1866, reveal the ambitions and constraints of Gilded Age infrastructure. The company received an exclusive 25-year franchise to lay pipes under Houston's streets—a monopoly granted by city council members who often held stock in the very company they were regulating. This cozy arrangement, shocking to modern sensibilities, was standard practice in 19th-century American cities. Infrastructure was too capital-intensive and too important to leave to pure market competition, yet too profitable to leave to government. The solution: regulated monopolies with deep political connections.

The technical challenge was formidable. Houston Gas Light's engineers had to figure out how to manufacture gas in a subtropical swamp where nothing stayed dry and everything corroded. Their solution was ingeniously local: they crushed oyster shells from Galveston Bay as a source of lime, mixing it with coal barged up Buffalo Bayou. The resulting "water gas" was stored in massive iron gasometers—cylindrical towers that rose and fell with gas pressure, becoming Houston's first industrial landmarks. By 1868, the company had laid four miles of mains and lit 65 street lamps, transforming Houston's nightscape.

But gas lighting was already a dying technology, even as Houston Gas Light expanded. Thomas Edison's incandescent bulb, patented in 1879, pointed toward electricity's dominance. Houston's business elite saw this transition coming and acted with characteristic audacity. On January 9, 1905, they incorporated Houston Lighting & Power Company with $1.5 million in capital—serious money for a city of 45,000 people. The founders included the city's banking dynasties, railroad barons, and cotton kings—names like Jesse Jones, who would later become Franklin Roosevelt's Commerce Secretary, and Will Hogg, son of a Texas governor and oil wildcatter.

Houston Lighting & Power's early years were defined by a bruising competition with Houston Gas Light, which had pivoted to electricity generation to protect its franchise. The two companies strung competing wire networks through downtown, sometimes on the same poles, creating a tangle of infrastructure that regularly sparked fires and electrocuted linemen. Customers played the companies against each other, switching providers for pennies of savings. This wasteful competition couldn't last. In 1911, after secret negotiations at Houston's Rice Hotel, the companies merged under the Houston Lighting & Power banner, creating the monopoly that would power Houston's rise.

The 1920s brought the first great test of this monopoly power. Houston's population exploded from 138,000 in 1920 to 292,000 by 1930, driven by the Spindletop oil discovery and the dredging of the Houston Ship Channel. Houston Lighting & Power had to build generating capacity at breakneck speed, constructing power plants along the ship channel where they could receive coal shipments and discharge cooling water. The Deepwater Generating Station, opened in 1925, became a template for industrial-scale power generation: massive boilers burning pulverized coal, steam turbines spinning at 3,600 rpm, transformers stepping voltage up to 66,000 volts for transmission across Harris County.

The company's growth attracted Wall Street's attention. Investment banks like Dillon, Read & Company saw utilities as perfect vehicles for selling bonds to conservative investors—monopolies with guaranteed returns backed by the inexorable growth of American cities. On August 16, 1943, Houston Lighting & Power's common stock began trading on the New York Stock Exchange, a watershed moment that transformed a regional utility into a national investment proposition. The IPO prospectus makes fascinating reading today: it touts Houston's strategic location, its growing petrochemical industry, its lack of labor unions, and its "favorable regulatory climate"—code for a Public Utility Commission that rarely met a rate increase it didn't approve.

The war years accelerated everything. Houston became "the arsenal of democracy" for petroleum products, with refineries running 24/7 to fuel Allied planes and ships. Houston Lighting & Power's industrial load doubled between 1941 and 1945, forcing the company to build new generating units even as materials were rationed and workers were drafted. The company's engineers performed miracles of improvisation, converting oil-fired boilers to burn natural gas (suddenly abundant from Texas fields), installing second-hand turbines bought from defunct Northeastern factories, and stringing transmission lines with aluminum wire when copper became unavailable.

By war's end, Houston Lighting & Power had become something more than a utility—it was the circulatory system of a booming metropolis. The company powered the refineries along the ship channel, the tool factories that supplied the oil industry, the ice plants that made Houston's climate bearable, and increasingly, the air conditioners that would transform the South. The age of gas lamps was definitively over; the age of electric abundance was beginning. But this transformation from local gas company to regional electric giant was just the prelude to an even more dramatic evolution in the postwar years.

III. Building the Texas Energy Empire (1940s–1990s)

The DC-3 circles over Houston in 1946, and Jesse Jones looks down at his city transformed. Where rice fields and cattle ranches sprawled just five years earlier, now petrochemical plants stretch along the ship channel like a spine of steel and smoke. The war has ended, but Houston's boom has just begun. Jones, back from Washington where he'd run Roosevelt's Reconstruction Finance Corporation, understands that Houston Lighting & Power isn't just serving a city anymore—it's powering an empire. "We need to think bigger," he tells the board. "Texas big."

The numbers told the story: Houston's population doubled from 385,000 in 1940 to 806,000 by 1960, then doubled again to 1.6 million by 1980. But raw population growth understated the transformation. Air conditioning, that great enabler of Sunbelt expansion, changed everything. In 1945, less than 1% of Houston homes had air conditioning; by 1970, it was 95%. Summer peak electricity demand, once a minor bump above winter heating loads, became the defining challenge of system planning. Houston Lighting & Power's peak load grew from 265 megawatts in 1945 to 2,847 megawatts in 1965—a ten-fold increase that required building the equivalent of a major power plant every 18 months.

The company's response was Cedar Bayou Generating Station, opened in 1970 as the largest power plant in Texas—2,400 megawatts of coal and gas-fired capacity on 2,000 acres east of Houston. But Cedar Bayou was just the opening act for Houston Lighting & Power's most audacious gamble: nuclear power. In 1973, as the Arab oil embargo sent energy prices soaring, the company announced plans for the South Texas Nuclear Project, a two-unit, 2,500-megawatt facility that would free Houston from dependence on fossil fuels. The initial cost estimate: $1.4 billion. The initial completion date: 1980.

What followed was a decade-long nightmare that nearly destroyed the company. Construction problems multiplied like cancer cells: faulty concrete pours that had to be jackhammered out and redone, pipe hangers installed backwards, quality control documents falsified by contractors. The Nuclear Regulatory Commission shut down construction in 1980, forcing a complete management overhaul. Brown & Root, the primary contractor (and future Halliburton subsidiary), was fired and sued. Costs spiraled to $5.5 billion by completion in 1988—four times the original estimate. Houston Lighting & Power's stock price collapsed from $18 to $9. Bond ratings dropped to near-junk levels.

Yet the South Texas Nuclear Project, for all its trauma, ultimately proved successful. The plants have operated at over 90% capacity factor for three decades, generating cheap, carbon-free electricity that's worth billions at today's power prices. The project taught Houston Lighting & Power hard lessons about project management, regulatory compliance, and the perils of technological optimism that would shape its culture for decades. More importantly, it demonstrated that even catastrophic execution failures couldn't kill a regulated utility with a captive customer base—a lesson not lost on Wall Street.

While nuclear drama consumed headlines, Houston Lighting & Power's natural gas distribution business quietly became a cash cow. The company had operated gas distribution since the original Houston Gas Light days, but the postwar period transformed this sleepy business into a growth engine. Suburban expansion meant laying gas mains to new subdivisions spreading across Harris County like inkblots. Every new home meant a new gas meter, new monthly bills, new additions to the rate base. The company developed an assembly-line efficiency for suburban infrastructure: trenching crews followed subdivision developers, laying polyethylene pipe in precise grids, installing meters in identical tract homes, turning on service for families fleeing Houston's humid urban core for air-conditioned suburban dreams.

The regulatory environment of this era deserves special attention, because it created the economic moat that still protects CenterPoint today. The Public Utility Commission of Texas, created in 1975, operated on a simple principle: utilities could earn a "fair" return (usually 10-12%) on invested capital, with rates adjusted to ensure that return regardless of operating efficiency. This "cost-plus" model created perverse incentives—the more capital a utility invested, the more profit it earned. Houston Lighting & Power became expert at this game, consistently growing its rate base through system expansion and reliability improvements while maintaining returns at the high end of regulatory allowances.

Competition with other Texas utilities during this period was less about stealing customers—service territories were exclusive monopolies—and more about regulatory capture and political influence. Houston Lighting & Power competed with Dallas's Texas Utilities, San Antonio's City Public Service, and Austin's municipal utility for favorable treatment from legislators and regulators. The company maintained a permanent lobbying presence in Austin, contributed generously to political campaigns, and hired former regulators as "consultants." This soft corruption, perfectly legal and utterly routine, ensured that rate cases generally went the company's way.

The 1980s brought new challenges as industrial customers, facing global competition, demanded lower electricity rates. Houston's petrochemical plants, which consumed vast quantities of power, threatened to build their own generating facilities if rates didn't come down. Houston Lighting & Power responded with complex rate structures: interruptible tariffs for customers willing to curtail usage during peak periods, time-of-use rates that shifted consumption to off-peak hours, and special deals for the very largest customers that smaller consumers effectively subsidized. This industrial rate discrimination, blessed by regulators who feared plant closures more than consumer complaints, became a permanent feature of Texas electricity markets.

By 1990, Houston Lighting & Power had built an empire: 12,000 megawatts of generating capacity, transmission lines stretching across 5,000 square miles, distribution networks serving 1.5 million customers, and a gas system with 500,000 meters. The company employed 12,000 people and generated $3.5 billion in annual revenues. It had survived the nuclear debacle, mastered the regulatory game, and positioned itself as the indispensable engine of Houston's growth. But storm clouds were gathering in Austin, where a new word was entering the utility lexicon: deregulation.

IV. Deregulation Drama & Corporate Restructuring (1999–2002)

The champagne flutes clinked in the Houston Club's private dining room on a humid evening in May 1999. Houston Lighting & Power's executives had just received shareholder approval for something unprecedented: killing their company's century-old name. As of that night, they would be Reliant Energy, a name that focus groups said sounded "modern" and "customer-focused." CEO Steve Letbetter raised his glass: "To the end of monopoly thinking and the beginning of competitive markets." Nobody in that room fully grasped that they were about to blow up their entire business model and reassemble it while the plane was flying.

Texas Senate Bill 7, signed by Governor George W. Bush in 1999, mandated the most radical electricity deregulation in American history. Unlike California's half-hearted attempt that kept utilities owning generation while forcing them to buy from spot markets, Texas went full restructuring. Utilities had to separate into three pieces: power generation (competitive), transmission and distribution (regulated monopoly), and retail sales (competitive). It was like forcing Ford to split into three companies: one that makes engines, one that builds chassis, and one that sells cars—except these companies had to seamlessly work together to keep the lights on every second of every day.

The financial engineering required to accomplish this restructuring was staggering. Reliant Energy had to value and allocate $14 billion in assets, $8 billion in debt, and thousands of contracts between newly independent entities. Investment bankers from Goldman Sachs and Morgan Stanley descended on Houston like an occupying army, their Excel models calculating the net present value of every power plant, transmission line, and customer relationship. The complexity was mind-bending: How do you price intercompany transactions between regulated and unregulated entities? How do you allocate overhead costs? Who gets the tax losses from the nuclear debacle?

On August 31, 2002, the transformation reached its climax with the birth of CenterPoint Energy. The new company would own the regulated wires business—the transmission lines and distribution networks that delivered power across Houston regardless of who generated or sold it. CenterPoint would collect delivery charges from every electron that flowed to Houston customers, earning regulated returns on its $7 billion rate base. It was the safest, most boring part of the old integrated utility—and that was exactly the point. CEO David McClanahan explained to investors: "We're a pure-play regulated utility now. Predictable earnings, stable dividends, no commodity exposure."

The company began trading as CenterPoint Energy (NYSE: CNP) on October 1, 2002, opening at $10.25 per share—a 40% discount to the pre-restructuring Reliant Energy price. The market was skeptical. Investors worried about stranded costs from above-market power purchase agreements, regulatory uncertainty as Texas figured out deregulation's rules in real-time, and massive debt loads from the restructuring. The credit rating agencies were even more pessimistic, dropping CenterPoint to BBB-, one notch above junk.

Meanwhile, the unregulated pieces of old Reliant Energy were experiencing their own drama. Reliant Resources, the competitive retail and generation business, had IPO'd in 2001 at $30 per share, raising $1.8 billion in one of the year's largest offerings. The pitch was compelling: Texas's electricity demand was growing 3% annually, deregulation would let efficient operators capture market share from sleepy municipals, and trading profits would juice returns. Enron's collapse in December 2001 should have been a warning, but Reliant Resources executives insisted they were different—they owned real assets, served real customers, generated real cash flow.

The Texas Genco saga exemplified the chaos of deregulation's early years. This collection of power plants—14,000 megawatts of coal, gas, and nuclear capacity—was carved out of Reliant Energy as a separate company, 81% owned by CenterPoint. The structure was byzantine: CenterPoint couldn't operate the plants (that would violate unbundling rules) but needed to monetize them to pay down debt. Texas regulators mandated that CenterPoint auction its stake by 2004, but to whom? Private equity firms circled like vultures, knowing CenterPoint was a forced seller.

The auction became a case study in negotiating weakness. CenterPoint hired Merrill Lynch to run a formal process, attracting bids from KKR, Blackstone, and Texas Pacific Group. But everyone knew CenterPoint's situation: massive debt maturities looming, rating agencies threatening downgrades, and a regulatory gun to their head. The winning bid came from a consortium led by Blackstone at $3.65 billion—almost $900 million less than book value. CenterPoint executives knew they were being fleeced but had no choice. The alternative was default.

The human toll of restructuring was brutal. Thousands of employees woke up working for different companies, their decades of institutional knowledge suddenly irrelevant. The trading floor at Reliant Resources, built to compete with Enron, hired hotshots from Wall Street who sneered at "dumb utility guys." The CenterPoint operations center, staffed by engineers who'd kept Houston's lights on through hurricanes, watched their former colleagues chase trading profits while they maintained aging infrastructure. The culture clash was total: entrepreneurial cowboys versus steady operators, mark-to-market accounting versus regulatory filings, stock options versus pensions.

California's energy crisis cast a dark shadow over Texas deregulation. As California's wholesale prices spiked 800% in 2000-2001, forcing rolling blackouts and utility bankruptcies, Texas regulators scrambled to avoid similar disasters. They delayed retail competition, strengthened market manipulation rules, and required adequate reserve margins. Reliant Resources, which had trading operations in California, faced investigations and lawsuits alleging market manipulation. Though never proven, the taint damaged credibility and spooked investors.

By late 2002, the grand experiment of deregulation looked like a disaster. Reliant Resources stock had collapsed from $30 to $5. CenterPoint struggled under $7 billion in debt. Residential electricity prices, supposed to fall with competition, had actually increased. Politicians who'd championed deregulation were backpedaling furiously. Yet from this chaos, CenterPoint would emerge with a crucial insight: in deregulated markets, owning the wires—the essential monopoly infrastructure—was the winning position. Generators might go bankrupt, retailers might fail, but someone had to deliver the electrons. That someone would collect their regulated return regardless.

V. The Expansion Era: Going National (2002–2018)

David McClanahan stood before a giant map of the United States in CenterPoint's Houston boardroom in 2003, colored pins marking natural gas distribution territories from Texas to Minnesota. "We're not a Texas utility anymore," he told his strategy team. "We're an infrastructure platform." The transformation from regional monopoly to national operator wouldn't happen through press releases or rebranding campaigns. It would require billions in acquisitions, delicate regulatory negotiations in state capitals from Little Rock to Indianapolis, and the careful integration of wildly different corporate cultures.

The natural gas distribution business became CenterPoint's Trojan horse for geographic expansion. Unlike electric utilities, which required massive generating plants and transmission networks, gas distribution was relatively capital-light—polyethylene pipes, meters, and regulators. CenterPoint already operated gas systems in Texas through its Houston Gas Light heritage. The company's strategists identified a roll-up opportunity: acquire subscale gas utilities in stable regulatory jurisdictions, improve operations through standardization, and earn steady returns on an expanding rate base.

The first major move came in 2004 with the $355 million acquisition of Natural Gas Distribution from Aquila, adding 300,000 customers in Minnesota. Minnesota seemed an unlikely target for a Houston company—different climate, different politics, different everything. But the regulatory environment was attractive: reasonable allowed returns, automatic rate adjustments for commodity costs, and a Public Utilities Commission that valued reliability over low rates. CenterPoint sent teams of Texas engineers to Minneapolis, where they discovered networks still using cast-iron pipes from the 1920s and paper maps in filing cabinets. The modernization opportunity was obvious.

Arkansas and Louisiana followed in rapid succession through a complex series of transactions with Entergy. These weren't clean acquisitions but asset swaps, joint ventures, and territorial exchanges that required hundreds of pages of regulatory filings. CenterPoint traded electric territories it didn't want for gas territories it did, creating a contiguous footprint along the Gulf Coast. By 2008, the company served gas customers from Shreveport to Lake Charles, Texarkana to Little Rock—2.8 million meters generating $400 million in annual earnings.

Enable Midstream, formed in 2013, represented CenterPoint's most ambitious expansion beyond regulated utilities. The company contributed its interstate pipelines and gathering systems into a joint venture with OGE Energy, creating a $11 billion midstream giant. Enable owned 12,000 miles of pipelines stretching from Texas to Oklahoma, gathering systems in the Anadarko and Arkoma basins, and processing plants handling 2.5 billion cubic feet of gas daily. The thesis was compelling: shale drilling was revolutionizing American energy, somebody had to move that gas to market, and Enable's assets sat atop the most prolific shale plays.

The structure was elegant financial engineering. CenterPoint owned 55% of Enable's limited partner units plus 40% of the general partner, providing $300 million in annual distributions without consolidating Enable's $3 billion debt. The dropdown model, pioneered by Kinder Morgan, let CenterPoint monetize midstream assets while maintaining control. Wall Street loved it—CenterPoint stock rose 40% in the year after Enable's IPO as investors valued the company as a utility plus a midstream hybrid.

But Enable also exposed CenterPoint to commodity price volatility it had spent years trying to escape. When oil prices collapsed from $107 to $26 between 2014 and 2016, Enable's distributions cratered. Gathering volumes dropped as shale drillers shut down rigs. Processing margins evaporated as natural gas liquids prices followed oil down. CenterPoint's earnings, supposedly stable and regulated, suddenly swung with commodity markets. The board faced a choice: double down on midstream through Enable acquisitions or retreat to pure-play regulated utilities.

Mississippi operations, acquired piecemeal between 2005 and 2015, illustrated the challenges of multi-state operations. Each state had different regulations, rate structures, and political dynamics. Mississippi's Public Service Commission was elected, not appointed, making rate cases political campaigns. CenterPoint had to navigate racial politics in majority-Black districts, agricultural interests in rural areas, and Gulf Coast communities still recovering from Hurricane Katrina. The company hired local executives, contributed to community organizations, and learned to speak Southern politics, not Texas business.

The operational integration of these far-flung territories was a logistics nightmare. CenterPoint ran different billing systems in different states, incompatible SCADA networks, and procurement processes that hadn't been updated since the Carter administration. The company launched "Project Unity" in 2010—a $500 million technology modernization that standardized everything from work order management to customer billing. Consultants from Accenture descended on every operations center, mapping processes and identifying "synergies." The promised savings: $50 million annually through centralized procurement, shared services, and eliminated redundancies.

Cultural integration proved even harder than systems integration. Minnesota employees, used to consensus-driven decision-making and generous benefits, clashed with Houston's command-and-control culture. Arkansas workers, many third-generation utility employees, resented directives from Texas executives who'd never climbed a pole or fixed a leak. CenterPoint tried everything: cultural ambassadors, employee exchanges, barbecue cookoffs between regions. Some initiatives worked; others became running jokes. The "One CenterPoint" campaign, complete with motivational posters and team-building exercises, was quietly abandoned after employees in multiple states reported it to regulators as an unnecessary expense.

The expansion strategy's financial performance was mixed. Returns on acquired properties generally matched or exceeded hurdle rates, but integration costs consistently overran budgets. The stock price appreciated from $10 in 2003 to $28 by 2017, but lagged pure-play regulated utilities without commodity exposure. Dividend growth, the key metric for utility investors, averaged 4% annually—respectable but not spectacular. The board faced increasing pressure from activist investors to clarify strategy: was CenterPoint a utility, a midstream company, or something else?

By 2017, CenterPoint controlled a sprawling empire: electric operations in Texas, gas distribution in six states, and midstream assets across the Southwest. The company generated $9 billion in revenues and employed 7,600 people. But the organization felt unwieldy, pulled in too many directions, lacking focus. CEO Scott Prochazka, who'd taken over in 2014, began hinting at a transformational transaction that would resolve the strategic confusion. That transaction would be Vectren—the biggest bet in CenterPoint's history.

VI. The Vectren Mega-Merger: Doubling Down (2018–2019)

Scott Prochazka's red-eye from Houston landed in Evansville, Indiana at 6 AM on a frigid February morning in 2018. As his black SUV wound through snow-covered streets toward Vectren's headquarters, he rehearsed his pitch one final time. This wasn't just another acquisition—it was a $6 billion bet that would fundamentally reshape CenterPoint. Either they would emerge as one of America's premier regulated utilities, or they would collapse under the weight of integration complexity and debt. There was no middle ground.

Vectren wasn't on any banker's merger list. The Evansville-based utility was the definition of Midwestern steady: 145 years old, serving 1.4 million electric and gas customers across Indiana and Ohio, generating predictable 5% earnings growth for decades. The company was run by Carl Chapman, an engineer who'd worked his way up from the field and still knew most of the linemen by name. Vectren's board included Evansville's civic elite—bank presidents, hospital executives, the university chancellor. This wasn't a company for sale; it was a community institution.

The strategic rationale that Prochazka pitched was elegant. CenterPoint plus Vectren would create the fourth-largest regulated utility in America by customer count, with complementary geographic footprints and business mixes. Vectren's Indiana electric operations, serving manufacturing-heavy regions around Evansville and Terre Haute, would diversify CenterPoint's Texas concentration. Vectren's Ohio gas distribution would extend CenterPoint's footprint into the industrial Midwest. The combined company would serve over 7 million customers across eight states—true national scale.

But the real attraction was Vectren's regulatory relationships. Indiana's utility commission was considered the gold standard—professional, predictable, allowing returns at the high end of national ranges. Vectren had received rate increases in 15 of its last 16 cases, with allowed returns on equity averaging 10.2%. The company's infrastructure modernization programs, which let it earn returns on safety upgrades outside of rate cases, were models that other utilities studied. This wasn't just acquiring assets; it was acquiring regulatory expertise and credibility.

The negotiation was delicate corporate diplomacy. Vectren's board worried about Texas cowboys destroying Indiana's collaborative utility culture. CenterPoint had to promise that Vectren would maintain its Evansville headquarters, keep local management, and continue community philanthropy. The social issues were as complex as the financial ones. Would Vectren executives report to Houston or maintain autonomy? Would CenterPoint impose its systems on Vectren operations? Would Indiana workers lose their jobs to Texas centralization?

The $72 per share cash offer, announced April 23, 2018, represented a 6% premium to Vectren's all-time high—a "godfather offer" designed to preempt competing bids. CenterPoint would also assume Vectren's $2.3 billion in debt, bringing total transaction value to $8.3 billion. The funding structure was aggressive: $3 billion in new debt, $2 billion in mandatory convertible securities, and cash on hand. CenterPoint's investment bankers at Goldman Sachs promised the leverage was manageable, pointing to $250 million in identified synergies and Enable distributions that would help pay down debt.

Wall Street's reaction was swift and brutal. CenterPoint stock dropped 7% on announcement as investors questioned the strategic logic. Why was a Texas utility buying Indiana coal plants just as America was transitioning to clean energy? How could CenterPoint integrate operations across eight states without destroying value? What happened if Enable's distributions dried up again? The credit rating agencies were even more skeptical, putting CenterPoint on negative watch and warning that a downgrade to junk was possible if integration faltered.

The regulatory approval process became a 15-month marathon across multiple jurisdictions. Indiana regulators worried about out-of-state ownership compromising local service. Ohio commissioners questioned whether CenterPoint had the financial strength to maintain infrastructure investment. Texas regulators wanted assurances that merger costs wouldn't be passed to Houston ratepayers. Each state demanded concessions: rate freezes, local hiring commitments, infrastructure spending promises. CenterPoint's regulatory team, led by former state commissioners who knew how the game was played, methodically worked through each demand.

Integration planning revealed the true complexity of combining these organizations. Vectren ran Oracle financial systems while CenterPoint used SAP. Vectren's union contracts, covering 40% of employees, had different work rules from CenterPoint's Texas operations. Even basic terminology differed—what Vectren called "mains" CenterPoint called "distribution lines." The integration team, 200 people working full-time for 18 months, created thousands of pages of documentation mapping every process, system, and decision point.

Cultural integration proved the hardest challenge. CenterPoint sent Texas executives to Indiana, expecting them to impose Houston efficiency on Midwestern operations. Instead, they encountered sophisticated professionals who'd been running utilities since before some of the Texans were born. Vectren's environmental team had already planned coal plant retirements and renewable replacements—they didn't need Texas telling them about energy transition. The Ohio gas operations ran leak detection programs that were more advanced than anything in CenterPoint's system. The learning was bidirectional, but acknowledging that required humility that didn't come naturally to either organization.

The promised synergies proved both easier and harder to achieve than expected. Procurement savings materialized quickly—combining purchase orders for pipes, meters, and trucks delivered $50 million in year one. But organizational synergies required painful decisions. Duplicate corporate functions were eliminated, meaning hundreds of job losses despite promises to maintain employment. IT systems integration, budgeted at $200 million, ballooned to $350 million as incompatibilities multiplied. The "one company" vision collided with the reality of eight state regulatory jurisdictions, each demanding local presence and responsiveness.

The financing structure that looked clever in PowerPoint proved problematic in practice. Enable's distributions, which were supposed to help fund the acquisition, collapsed as commodity prices weakened. The mandatory convertible securities, designed to maintain investment-grade ratings, confused investors and traded at deep discounts. CenterPoint's stock price languished below $25 throughout 2019, making the converts massively dilutive. The board faced an uncomfortable reality: they'd overpaid for Vectren and overleveraged the balance sheet just as the business environment was deteriorating.

By the merger's first anniversary in February 2019, the combined company was clearly stronger—more diversified, better positioned for energy transition, with improved regulatory relationships. But it was also more complex, more indebted, and more vulnerable to execution mistakes. The integration would continue for years, consuming management attention and capital that could have gone to infrastructure investment. CenterPoint had successfully doubled down on regulated utilities, but at a price that wouldn't be fully understood until the next crisis tested the organization's resilience.

VII. Crisis Management: Storms, Outages & Scrutiny (2019–2024)

The emergency operations center at CenterPoint's Houston headquarters hummed with controlled chaos at 3 AM on February 15, 2021. Outside, temperatures had plunged to 7°F—the coldest in Houston since 1989. Inside, executives watched helplessly as cascading failures rippled across Texas's electric grid. Generation plants frozen, natural gas supplies interrupted, transmission lines sagging under ice loads. CEO Dave Lesar, recruited from Halliburton to manage CenterPoint through crisis, stared at the system status board showing 1.4 million customers without power. "This is our Katrina," he said quietly. He was wrong. It was worse.

Winter Storm Uri wasn't just a natural disaster—it was a systematic failure of every assumption Texas utilities had made about weather, preparedness, and resilience. CenterPoint's infrastructure, designed for hurricanes and 100°F summers, couldn't handle sustained subfreezing temperatures. Transformers exploded as mineral oil congealed. Transmission towers collapsed under ice weight. Natural gas distribution lost pressure as wells froze and demand spiked simultaneously. The company's emergency response plans, refined through dozens of hurricanes, were useless against a threat they'd never seriously contemplated.

The human toll was devastating. At least 246 Texans died from hypothermia, carbon monoxide poisoning from generators, and medical equipment failures. Millions huddled in freezing homes for days, burning furniture for warmth, melting snow for water. The economic damage reached $195 billion—America's costliest natural disaster. But unlike hurricanes, where utilities are heroes restoring power after unavoidable damage, Uri exposed systemic negligence. Why weren't plants winterized after the 2011 freeze? Why didn't regulators mandate cold-weather preparations? Why did the entire system collapse simultaneously?

CenterPoint's response during Uri was competent but insufficient. Crews worked 16-hour shifts in brutal conditions, restoring power to 500,000 customers within 48 hours. The company's natural gas system maintained pressure despite record demand, preventing an even worse catastrophe. But public anger focused on the failures, not the heroics. Social media exploded with images of downtown Houston's empty skyscrapers lit up while residential neighborhoods stayed dark. Politicians demanded investigations. Lawsuits alleged gross negligence. The reputational damage was instant and lasting.

The financial aftermath was complex. CenterPoint incurred $1.3 billion in Uri-related costs: emergency repairs, purchased power at astronomical prices, customer bill credits mandated by regulators. The company sought recovery through securitization—essentially borrowing against future customer bills to spread costs over time. But regulators, facing political pressure, challenged every expense. Was paying $9,000 per megawatt-hour for emergency power prudent or desperate? Should shareholders or ratepayers bear costs from inadequate winterization? The fights would continue for years through rate cases and appeals.

Before Uri's scars had healed, Hurricane Beryl slammed into Houston on July 8, 2024. As a Category 1 storm, Beryl shouldn't have been catastrophic. But its path through CenterPoint's service territory was surgically destructive—2.6 million customers lost power, the largest outage in company history. The storm exposed how climate change was scrambling traditional preparedness. Beryl had rapidly intensified from tropical storm to major hurricane in 48 hours, then weakened just before landfall. CenterPoint had pre-positioned crews for a Category 3 storm that became Category 1, meaning resources were in wrong places when damage occurred differently than modeled.

The Beryl response became a public relations catastrophe. CenterPoint's outage tracker website crashed immediately, leaving customers unable to report problems or get restoration estimates. The company's mobile app showed cryptic error messages. Call centers were overwhelmed, with multi-hour wait times. Social media filled with desperate pleas from hospitals losing backup power, elderly customers without air conditioning in 95°F heat, families with spoiled medicine and rotting food. Local news ran continuous coverage of CenterPoint failures, interviewing angry customers and opportunistic politicians.

The restoration took 12 days—acceptable for a Category 3 hurricane but outrageous for Category 1. CenterPoint blamed "extensive vegetation damage" from trees that hadn't been properly trimmed. Critics noted the company had reduced vegetation management spending by 15% over three years to boost earnings. The company pointed to unprecedented storm frequency. Opponents cited inadequate grid hardening despite collecting billions in rates. Every explanation sounded like an excuse to customers sweating in dark houses while watching CenterPoint executives give press conferences from air-conditioned offices.

Public backlash reached unprecedented levels. Houston Mayor John Whitmire called CenterPoint's response "pathetic" and demanded new leadership. Texas Governor Greg Abbott ordered an investigation into the company's preparedness and response. The Public Utility Commission launched proceedings that could result in penalties up to $1 million per day. Houston Chronicle's editorial board called for breaking up CenterPoint's monopoly. State legislators drafted bills requiring massive infrastructure investments and automatic penalties for extended outages.

CenterPoint's Greater Houston Resiliency Initiative, announced with fanfare in 2024, was both necessary response and desperate attempt at reputation rehabilitation. The company committed $5 billion over five years to grid hardening: replacing wooden poles with steel and concrete, burying critical distribution lines, installing automated switching that could reroute power around damage, deploying battery storage at critical facilities. The plan included hiring 500 additional lineworkers, pre-positioning emergency generators, and creating community resilience centers with backup power and cooling during outages.

But the initiative raised uncomfortable questions about utility incentives. CenterPoint would earn regulated returns on every dollar spent—approximately 10% annually. The worse storms got, the more the company could invest in response, the more profit it earned. This perverse incentive, where utilities benefit from disasters they failed to prevent, infuriated consumer advocates. "They're profiting from their own incompetence," said one activist. "They let the grid deteriorate, wait for inevitable failures, then charge us to fix what should never have broken."

Internal culture during this crisis period was toxic. Employees faced public anger personally—lineworkers were cursed at, customer service representatives received death threats, executives needed security details. Morale plummeted as workers felt abandoned by leadership more focused on financial engineering than operational excellence. Turnover spiked, especially among experienced field personnel who could make similar money with contractors without the abuse. The company hired consultants from McKinsey to assess culture, who delivered a devastating report about "learned helplessness" and "bureaucratic paralysis."

The regulatory response was swift and harsh. The Public Utility Commission ordered comprehensive reviews of emergency preparedness, vegetation management, and infrastructure investment. New rules required detailed restoration time estimates, hourly updates during outages, and automatic bill credits for extended interruptions. Performance metrics were established with financial penalties for missing targets. The commission explicitly warned that continued failures could result in "restructuring remedies"—regulatory speak for potentially breaking up the company.

By late 2024, CenterPoint faced an existential challenge: how to maintain financial performance while massively increasing infrastructure spending, managing more frequent and severe weather events, and rebuilding public trust. The company's stock price reflected this uncertainty, trading at historic discounts to peer utilities. Credit ratings remained under pressure. Dividend growth, sacred to utility investors, was suspended. The transformation from sleepy regulated monopoly to crisis-tested infrastructure company was painful, expensive, and far from complete.

VIII. The Modern Utility: Technology & Transformation (2020s–Present)

Inside CenterPoint's new Grid Operations Center, opened in 2023, dozens of screens display real-time data from 4.2 million smart meters, 15,000 grid sensors, and 500 weather stations. Artificial intelligence algorithms predict equipment failures before they happen. Drone swarms inspect transmission lines after storms. This isn't your grandfather's utility—it's a technology company that happens to deliver electricity and gas. But the transformation from poles-and-wires utility to digital infrastructure platform is creating tensions that challenge CenterPoint's fundamental business model.

The numbers tell a staggering story of demand transformation. CenterPoint forecasts nearly 50% electric load growth in Houston by 2031—the fastest growth since the 1960s. But unlike that era's broad-based industrial expansion, today's growth is concentrated in data centers. Microsoft, Amazon, Google, and Meta are building hyperscale facilities along the Houston Ship Channel, each consuming as much power as 100,000 homes. A single data center campus under construction in Baytown will require 500 megawatts—equivalent to a small city. These aren't just customers; they're load reshaping the entire grid.

The data center boom exposes a fundamental paradox of modern utilities. These customers want three things simultaneously: 100% renewable power for ESG commitments, 99.999% reliability for critical operations, and the lowest possible rates. CenterPoint can deliver any two but not all three. Renewable power is intermittent. Extreme reliability requires redundant infrastructure. Low rates need efficient scale. The company is investing $500 million in dedicated substations and transmission lines for data centers, but recovering costs from other customers triggers rate case battles about subsidization.

Smart grid technology promises operational revolution but delivers implementation headaches. CenterPoint has deployed 2.4 million smart meters since 2020, enabling real-time usage monitoring, remote disconnection, and outage detection. But the data tsunami—50 terabytes daily—overwhelms legacy systems. The company spent $200 million on new data analytics platforms, hired 50 data scientists, and partnered with Microsoft on cloud infrastructure. Yet extracting actionable insights from billions of data points proves harder than vendors promised. Predictive maintenance algorithms generate thousands of false positives. Customer usage analytics raise privacy concerns. The smart grid is smarter but not yet intelligent.

Distribution automation represents the most tangible modernization success. CenterPoint has installed 3,000 automated switches that can isolate faults and restore power without human intervention. During Hurricane Beryl, these systems restored power to 400,000 customers within minutes by automatically rerouting around damaged sections. The technology is proven but expensive—$50,000 per switch plus communication infrastructure and control systems. The company plans 10,000 switches by 2030, a $750 million investment that will fundamentally change restoration dynamics but requires regulatory approval for cost recovery.

The renewable integration challenge is reshaping grid operations in real-time. Texas leads America in wind generation, with 30,000 megawatts of capacity that can provide 40% of state electricity on windy days—or 0% on calm ones. CenterPoint's transmission system must handle these wild swings, maintaining stability as thousands of megawatts appear and disappear. The company is investing in synchronous condensers—massive spinning machines that provide grid inertia without generating power—and static VAR compensators that maintain voltage. This invisible infrastructure, costing hundreds of millions, is essential for renewable integration but impossible for customers to understand.

Battery storage is transitioning from experiment to essential infrastructure. CenterPoint is developing 500 megawatts of utility-scale batteries at strategic substations, providing backup power for critical loads and grid stabilization services. The economics are marginal—batteries cost $400 per kilowatt-hour, last 10-15 years, and degrade with each cycle. But regulators increasingly mandate storage for resilience, and data center customers will pay premiums for battery-backed reliability. The company is testing residential battery programs, where customers' home batteries provide grid services for payments, but coordinating thousands of distributed assets proves technically and contractually complex.

Capital expenditure has reached historic levels—$2.5 billion in 2024 focused on upgrading infrastructure and expanding service capabilities. But the nature of investment has fundamentally changed. Traditional spending on poles, wires, and pipes is straightforward—assets last 40 years with predictable maintenance. Digital infrastructure requires continuous refresh. Software licenses need annual renewal. Cybersecurity demands constant vigilance. The company's IT budget has tripled to $400 million annually, but regulators question whether software is a capital investment deserving returns or an operating expense shareholders should fund.

The cybersecurity threat has evolved from theoretical risk to daily battle. CenterPoint reports 10,000 attempted intrusions monthly, ranging from amateur hackers to state-sponsored groups. The 2021 Colonial Pipeline ransomware attack was a wake-up call—utilities are critical infrastructure that adversaries will target. The company has built a Security Operations Center staffed 24/7, implemented zero-trust architecture, and conducts quarterly penetration testing. But security is only as strong as the weakest link, and CenterPoint has 50,000 networked devices, any of which could be an entry point.

Regulatory frameworks haven't kept pace with technological change. Rate cases still use depreciation schedules from the 1980s, assuming poles last 35 years and meters 20 years. But smart meters become obsolete in 7-10 years as communication standards evolve. Grid management software needs replacement every 3-5 years. Regulators, many trained as lawyers not engineers, struggle to evaluate technology investments. Is a $100 million advanced distribution management system prudent or gold-plating? Should utilities earn returns on software? Who bears the risk when technology investments fail?

The workforce transformation is painful but necessary. CenterPoint needs fewer lineworkers climbing poles but more network engineers managing systems. The company has launched aggressive retraining programs, partnering with community colleges on digital skills curricula. But cultural resistance is strong. Veterans who spent careers mastering physical infrastructure feel devalued by digital transformation. New hires with computer science degrees don't understand utility operations. The company is essentially running two utilities—legacy physical and emerging digital—with different cultures, skills, and values.

Customer expectations have fundamentally shifted. Tesla owners want to sell power back to the grid from their cars. Rooftop solar customers demand net metering at retail rates. Smart home enthusiasts expect real-time pricing that changes every 15 minutes. Industrial customers want to participate in demand response programs that pay them to reduce usage during peaks. CenterPoint is building systems to enable these services, but the complexity is staggering. The company processes 100 million transactions monthly, each requiring accurate measurement, billing, and settlement.

The Texas energy transition paradox becomes more pronounced daily. The state that produces the most oil and gas also generates the most renewable energy. Houston, the global capital of fossil fuels, hosts the most aggressive corporate renewable commitments. CenterPoint must serve both worlds simultaneously—maintaining gas infrastructure for petrochemical plants while building renewable connections for data centers. The company is investing billions in both fossil and renewable infrastructure, a hedge that satisfies no one completely but reflects Texas's complex energy reality.

By 2024's end, CenterPoint has emerged as one of America's most technologically advanced utilities, but the transformation has come at enormous cost—financial, organizational, and human. The company that once defined itself by reliable delivery of commodity electrons must now be a technology platform, energy advisor, and climate adaptation specialist. The skills, systems, and strategies that built a successful 20th-century utility are increasingly irrelevant to 21st-century challenges. Whether CenterPoint can complete this transformation while maintaining financial performance and regulatory compliance remains the existential question.

IX. Business Model & Financial Architecture

The spreadsheet on the CFO's monitor displays CenterPoint's 2024 financial architecture in stark detail: $8.64 billion in revenue, $2.2 billion in EBITDA, $44 billion in assets, $27 billion in debt and equity capitalization. But these numbers obscure the bizarre economics of regulated utilities—a business model where companies profit from spending money, customers pay for investments they don't request, and regulators determine returns through political processes masquerading as financial analysis. Understanding CenterPoint requires decoding this regulated monopoly model that would be illegal in any other industry.

Revenue in 2024 reached $8.64 billion, but the composition reveals the business's true dynamics. The Electric segment generated $3.5 billion from delivering power to 2.6 million Houston customers—not from generating or selling electricity, just from owning the wires that carry it. Natural gas operations contributed $2.876 billion for the nine months ended September 30, 2024, from 4.4 million customers across eight states. These aren't competitive revenues earned by superior service or lower prices. They're regulated revenues determined by formulas that guarantee cost recovery plus allowed returns, regardless of operational efficiency or customer satisfaction.

The rate base is the holy grail of utility economics—the value of invested capital on which regulators allow returns. CenterPoint's rate base has grown from $15 billion in 2019 to $23 billion in 2024 through relentless infrastructure investment. Every dollar spent on poles, pipes, meters, and substations enters the rate base and earns approximately 10% annually for its 40-year depreciation life. This creates a powerful incentive: spend more, earn more. The company's capital expenditure of $2.501 billion in 2024 wasn't just maintaining infrastructure—it was manufacturing future earnings. The company's 10-year capital plan through 2030 totals $47.5 billion, with $500 million in incremental capital investments in grid resiliency. This massive spending isn't driven by customer demand or operational necessity but by financial engineering—more capital invested means more earnings generated, regardless of whether customers need or want the improvements.

The regulatory recovery mechanism is where utility economics becomes truly bizarre. When CenterPoint spends $100 million on infrastructure, it doesn't immediately charge customers. Instead, the investment enters the rate base, and customers pay for it over 40 years through depreciation, plus return on the undepreciated balance, plus taxes on that return. A $100 million investment ultimately costs customers $250-300 million over its life. The utility earns profits not from operational efficiency but from spending money and passing costs to captive customers who have no alternative provider.

Electric versus natural gas segment dynamics reveal different risk-return profiles within the same company. Electric operations generated higher margins—approximately 35% EBITDA margins versus 30% for gas—but face greater weather exposure and infrastructure demands. Electric customers can't switch providers for delivery (though they can choose retail suppliers in Texas), creating true monopoly pricing power. Natural gas operations have steadier volumes but face long-term transition risk as electrification accelerates. The company manages this portfolio effect, using stable gas earnings to offset volatile electric results.

The dividend has been sacred to CenterPoint's investment proposition—until recently. The company paid $0.19 per share quarterly through 2023, yielding approximately 2.5% at recent prices. But dividend growth, the key attraction for utility investors, has stalled as capital needs overwhelm cash generation. The board faces an impossible choice: maintain dividends and constrain infrastructure investment, or cut dividends and risk a shareholder revolt. The current solution—minimal increases while massively expanding capital spending—satisfies no one.

Debt financing has become increasingly complex and expensive. CenterPoint carries $19 billion in long-term debt across multiple entities with different credit profiles. Houston Electric, the regulated Texas utility, maintains investment-grade ratings at BBB+. But the parent company trades at BBB-, one notch above junk, reflecting concerns about financial flexibility. The weighted average cost of debt has risen from 3.5% to 5.2% as Federal Reserve tightening and credit concerns increased borrowing costs. Every 100 basis point increase in rates costs $190 million annually—money that comes directly from earnings.

Securitization has emerged as the financing tool of choice for extraordinary costs. After Winter Storm Uri, CenterPoint issued $1.3 billion in ratepayer-backed bonds, secured by future customer bills. These bonds carry AAA ratings and low interest rates because they're essentially government-guaranteed—regulators must ensure collection through customer rates. It's a brilliant financial innovation that socializes costs while maintaining private profits. Customers pay for disasters through higher bills, investors get protected returns, and utilities avoid balance sheet stress.

The Enable Midstream ownership, once a crown jewel, became an albatross that CenterPoint finally shed. The company sold its stake to Energy Transfer for $1.2 billion in 2021, using proceeds to pay down debt. But the transaction crystallized a $500 million loss and eliminated $300 million in annual distributions. The strategic clarity of becoming a pure-play regulated utility came at the cost of earnings diversity and growth optionality.

Cost of capital regulation represents the most important and least understood aspect of utility economics. Regulators set allowed returns on equity—currently 9.8-10.4% across CenterPoint's jurisdictions—based on academic models, comparable company analysis, and political compromise. These few percentage points determine billions in customer costs and shareholder returns. The company employs armies of experts to argue for higher returns, while consumer advocates push for lower rates. The outcome, decided by political appointees with limited financial expertise, affects millions of customers and billions in market value.

Working capital management in utilities defies normal business logic. CenterPoint collects customer payments monthly but pays major expenses quarterly or annually, creating massive float. The company holds $2 billion in customer deposits—interest-free loans from people who can't pass credit checks. Regulatory assets—costs incurred but not yet recovered through rates—total $3 billion, representing IOUs from future customers. The balance sheet is littered with regulatory constructs that would be meaningless in any competitive business.

The business model's fundamental contradiction becomes clear in crisis. CenterPoint must invest billions in resilience to prevent outages, but earns returns only on capital invested, not outages prevented. The company profits from building infrastructure to fix problems, not from avoiding problems in the first place. This misalignment between social benefit (reliable power) and private incentive (returns on investment) creates the perpetual tension between utilities and their stakeholders.

Looking forward, the traditional utility business model faces existential challenges. Distributed generation, battery storage, and microgrids threaten the monopoly premise. Large customers increasingly self-generate, leaving residential customers to bear fixed costs. Electrification drives load growth but requires massive infrastructure investment. Climate change makes historical planning obsolete. The regulatory compact—monopoly protection in exchange for obligation to serve—strains under technological and environmental pressures.

CenterPoint's financial architecture, built on regulatory monopoly and cost-plus pricing, has generated steady returns for a century. But the model depends on assumptions—captive customers, supportive regulators, predictable demand, stable climate—that are all now in question. Whether the company can evolve its business model while maintaining financial performance will determine not just CenterPoint's future but the viability of the American utility model itself.

X. Playbook: Lessons in Utility Management

The conference room at CenterPoint's disaster recovery facility in Spring, Texas, has no windows—a deliberate design choice for a space where executives confront their worst failures. On the wall hangs a photo from Hurricane Ike in 2008: a sea of blue tarps covering damaged Houston roofs, power lines tangled like spaghetti, a stark reminder that utilities are judged not in normal times but in crisis. CEO Jason Wells points to it during his first all-hands meeting in 2024: "Every decision we make echoes for decades. Every mistake compounds. Every success builds trust we'll need when things go wrong. And things always go wrong."

Managing Through Crisis: Operational and Financial Resilience

The first lesson in utility crisis management is that you're always fighting the last war while the next one approaches from an unexpected angle. CenterPoint mastered hurricane response through decades of coastal storms—pre-positioned crews, mutual aid agreements, staged materials, rehearsed restoration protocols. Then Winter Storm Uri arrived with completely different physics: frozen wellheads, iced transformers, rolling blackouts. The hurricane playbook was worthless. The company learned that resilience isn't about perfecting response to known threats but building adaptive capacity for unknown ones.

Financial resilience requires a different mindset from operational resilience. During Uri, CenterPoint had to purchase replacement power at $9,000 per megawatt-hour—180 times normal prices. The company had credit facilities to cover immediate costs but faced a liquidity crisis as bills came due before regulatory recovery. The solution involved complex treasury management: drawing credit lines, accelerating collections, delaying non-critical payments, and ultimately securitizing costs through ratepayer bonds. The lesson: in crisis, cash is oxygen, and you need multiple ways to breathe.

The Art of Regulatory Relationships

Successful utility executives understand that regulators are political actors constrained by public pressure, precedent, and statutory limits. CenterPoint's approach has evolved from adversarial litigation to collaborative problem-solving. The company now pre-files rate cases with commission staff, incorporates feedback before formal proceedings, and accepts lower returns in exchange for expedited recovery. This isn't capitulation—it's recognition that regulatory relationships are long-term repeated games where today's victory becomes tomorrow's liability.

The company maintains a sophisticated regulatory intelligence operation. Former commissioners serve as advisors. Lawyers monitor every docket in eight states. Economists model rate case outcomes using machine learning. But the most valuable intelligence comes from informal channels: coffee with staff attorneys, lunches with consumer advocates, drinks with legislative aides. These relationships, built over years, provide early warning of shifting regulatory winds and opportunities to shape policy before positions harden.

M&A in Regulated Industries: When to Buy, What to Pay

The Vectren acquisition teaches harsh lessons about utility M&A. CenterPoint paid $72 per share—a 6% premium to all-time highs—for a company with aging coal plants in a declining industrial region. The strategic rationale was sound: geographic diversification, regulatory expertise, economies of scale. But execution complexity overwhelmed strategic benefits. Integration costs exceeded budgets by 75%. Cultural conflicts destroyed productivity. Promised synergies materialized slowly or not at all.

The playbook for successful utility M&A is counterintuitive. Don't chase growth—utilities grow with their service territories, not through acquisition. Don't pay for synergies—regulators will claw them back through rate reductions. Don't expect cultural integration—utilities are local institutions with deep regional roots. Instead, buy distressed assets at discounts, fix operational problems, and earn returns on improvement investments. The best utility acquisitions are opportunistic, not strategic.

Infrastructure Investment Timing and Cycles

Utilities face a fundamental timing challenge: infrastructure lasts decades but technology, climate, and demand patterns change rapidly. CenterPoint's coal plants, built for 60-year lives, became stranded assets in 20 years. Smart meters, supposed to last 20 years, need replacement in 10 as communication standards evolve. The company is investing billions in grid hardening just as distributed generation might make centralized grids obsolete.

The solution is optionality through modularity. Instead of massive centralized power plants, build smaller distributed resources. Rather than underground entire distribution networks, selectively harden critical segments. Deploy technology in phases with exit ramps if adoption disappoints. This approach sacrifices economies of scale for flexibility—a tradeoff traditional utility thinking resists but modern uncertainty demands.

Balancing Stakeholders: Customers, Regulators, Investors, Communities

Every utility decision affects multiple stakeholders with conflicting interests. Customers want low rates and perfect reliability. Regulators demand infrastructure investment and social programs. Investors expect steady returns and dividend growth. Communities desire local jobs and environmental progress. CenterPoint's stakeholder management has evolved from sequential appeasement to simultaneous optimization.

The key insight is that stakeholder interests align more than they initially appear. Reliable service reduces customer complaints and regulatory scrutiny. Infrastructure investment creates jobs while earning returns. Environmental progress attracts ESG investors and improves community relations. The challenge is finding these win-win-win solutions and communicating them effectively to each audience in their language.

The Utility Paradox: Essential Service, Constrained Returns

Utilities operate in a unique economic space: they provide essential services that society cannot function without, yet their returns are capped by regulation. This paradox creates perverse incentives. CenterPoint can't earn excess returns by providing exceptional service, but can destroy value through poor execution. The company can't capture upside from innovation but bears full downside from failure. It must invest billions anticipating future demand but recovers costs only if predictions prove correct.

The playbook for navigating this paradox involves several strategies:

- Regulatory Arbitrage: Operate in multiple jurisdictions to diversify regulatory risk and capture best practices

- Capital Efficiency: Maximize returns within regulatory constraints through financial engineering and operational excellence

- Risk Transfer: Use insurance, securitization, and rate mechanisms to shift risks to parties best able to bear them

- Political Capital: Build relationships and credibility during good times to draw upon during crises

- Narrative Control: Frame infrastructure needs and rate increases as investments in reliability and economic growth, not utility profits

The meta-lesson from CenterPoint's journey is that utility management is as much about political economy as operational excellence. Technical competence is necessary but insufficient. Success requires navigating complex stakeholder dynamics, regulatory processes, and public expectations while maintaining financial discipline and operational reliability. It's a balance few companies achieve consistently, which explains why utility stocks trade at such wide valuation ranges despite providing the same essential service.

XI. Analysis & Investment Perspective

The Excel model on the analyst's screen shows CenterPoint trading at 15.2x forward earnings, a 20% discount to the utility sector average of 19x. The dividend yield of 2.8% sits below the sector's 3.4%. The stock has underperformed the Utilities Select Sector SPDR (XLU) by 30% over three years. These numbers suggest either a value opportunity or a value trap. Understanding which requires dissecting CenterPoint's competitive position, growth drivers, and risk factors with the cold precision of an investment committee memo.

Competitive Positioning vs. Other Major Utilities

CenterPoint occupies an awkward middle ground in the utility landscape. It lacks the scale of NextEra Energy (market cap $180 billion) or Southern Company ($95 billion). It doesn't have Dominion Energy's regulated returns averaging 10.5% or American Electric Power's pure-play electric focus. The company's geographic footprint—heavily Texas with Midwest additions—provides neither the sunbelt growth of Florida utilities nor the stable demographics of Northeast incumbents.

Yet CenterPoint possesses unique strategic assets. Houston Electric serves the fastest-growing major metro in America, with population increasing 20% per decade. The service territory includes the Houston Ship Channel, the largest petrochemical complex in the Western Hemisphere, providing industrial load that's both massive and recession-resistant. The multi-state gas distribution network offers diversification that pure-play electric utilities lack. These aren't the best assets in the utility sector, but they're far from the worst.

Growth Drivers: Electrification, Data Centers, Population GrowthThe data center explosion represents CenterPoint's most significant growth catalyst. Data centers currently account for roughly 4% of total U.S. electricity consumption, but by 2030, that share is projected to rise to 12%, with U.S. data center energy demand set to jump from 224 terawatt-hours in 2025 to 606 terawatt-hours in 2030. Texas is currently home to 342 data centers which together constantly require 7.597 gigawatts of power—8.8% of the state's power as of 2024.

Houston's specific advantages in this boom are compelling. The city's vacancy rate dropped dramatically from 19.7% in H2 2023 to 14.4% in H1 2024, indicating growing market confidence. Major hyperscalers are building massive facilities along the Houston Ship Channel, with a single Baytown campus requiring 500 megawatts. This concentration of demand in CenterPoint's core service territory transforms load growth from hope to certainty.

Population growth provides the steady baseload expansion that underpins utility investment. Houston's metro population grows 2% annually, adding 140,000 residents yearly—each requiring electric and gas connections. But raw population understates the impact. These are predominantly young, high-income households moving from California and the Northeast, with above-average energy consumption from larger homes, multiple EVs, and home offices. The demographic quality matters as much as quantity.

Industrial electrification adds another growth vector. Houston's petrochemical complex, traditionally powered by direct-fired natural gas, is under pressure to reduce emissions. Companies are electrifying processes previously thought impossible to decarbonize—ethylene crackers, hydrogen production, even steel manufacturing. Each conversion represents massive load additions that lock in for decades. CenterPoint is seeing inquiries for connections exceeding 100 megawatts from single industrial customers.

ESG Considerations and Energy Transition Risks

The ESG paradox for CenterPoint is stark: the company enables both the problem and solution of climate change. Its natural gas distribution serves 4.4 million customers burning fossil fuel daily. Its electric transmission enables both coal generation and renewable energy. The company talks sustainability while building gas infrastructure with 40-year depreciation schedules. This cognitive dissonance creates valuation uncertainty that explains part of the stock's discount.

Climate physical risk is existential for Houston-based infrastructure. Hurricane intensity is increasing, with Category 4-5 storms becoming more frequent. Sea level rise threatens coastal substations. Extreme heat stresses equipment beyond design parameters. Drought reduces cooling water for generation. These aren't distant risks—they're current realities affecting operations and requiring billions in adaptation spending that may prove insufficient.

The transition risk is equally complex. Natural gas bans in new construction are spreading from California to traditionally gas-friendly states. Electrification mandates could strand billions in gas infrastructure. Distributed generation and microgrids threaten the centralized utility model. Yet paradoxically, electrification drives electricity demand that benefits CenterPoint's electric business while destroying its gas business. The company is simultaneously winner and loser in the energy transition.

Regulatory Risk Assessment Across Multiple States

Operating in eight state regulatory jurisdictions multiplies complexity exponentially. Texas allows high returns but demands massive infrastructure investment. Indiana provides stability but scrutinizes every expense. Minnesota pursues aggressive decarbonization that challenges gas operations. Mississippi politics inject uncertainty into routine rate cases. Each state's energy policy, political climate, and regulatory philosophy differs, creating a patchwork of risks and opportunities.

The Texas regulatory environment, CenterPoint's most important, is increasingly hostile. The Public Utility Commission, traditionally utility-friendly, has turned adversarial after repeated grid failures. Performance standards with automatic penalties, mandatory infrastructure spending without guaranteed recovery, and threats of structural separation represent a fundamental shift in the regulatory compact. The days of clubby relationships and guaranteed returns are ending.

Capital Markets Access and Financing Strategy

CenterPoint's BBB- credit rating at the parent company level sits precariously one notch above junk. This constraint limits financial flexibility and increases borrowing costs. The company must maintain specific financial metrics—debt-to-EBITDA below 5.5x, funds from operations to debt above 12%—or face downgrades that would dramatically increase capital costs and potentially trigger covenant violations.

The financing strategy relies on regulated subsidiary debt, which maintains higher ratings due to regulatory protection. Houston Electric at BBB+ can borrow more cheaply than the parent. But this structure creates complexity—intercompany loans, dividend restrictions, ring-fencing provisions—that constrains capital allocation flexibility. The company is essentially running multiple utilities with separate capital structures under a holding company umbrella.

Bull Case: Infrastructure Super-Cycle Beneficiary