Centene Corp.: The Sovereign of Subsidized Care

I. Introduction & Episode Roadmap

Start with a number that shouldn't make sense. In the fiscal year that closed on December 31, 2025, Centene Corporation moved $194.8 billion of revenue across its books — a figure that ranks it among the two dozen largest companies in the United States by sales.1 And yet in that same year, the company reported a net loss of $6.7 billion, its worst headline result in modern memory, driven by a single non-cash accounting charge that flushed a decade of acquisitions through the income statement in one violent quarter.1 A Fortune 25 enterprise. A multibillion-dollar loss. Both true. Both, as it turns out, essential to understanding what Centene actually is.

Here is the puzzle we want to solve. How did an obscure, non-profit health plan — one that began life managing care for low-income mothers and children in a single hospital system in Milwaukee, Wisconsin — grow into a leviathan that today insures roughly one in every fourteen Americans, most of them poor, sick, elderly, or some combination of all three? While the household-name giants of American health insurance — UnitedHealthcare, Elevance, Cigna, Aetna — spent decades chasing the fat, stable margins of corporate employer contracts, Centene went the other way. It built its empire in the places the others found too small, too political, too actuarially treacherous to bother with: the Medicaid rolls, the individual insurance exchanges, the dual-eligible poor who qualify for both Medicaid and Medicare at once.

That is the thesis worth testing across the next three hours. Centene is, in effect, a company that turned the regulatory plumbing of the American welfare state into a business model. Its revenue is almost entirely government money — premiums paid by state Medicaid agencies and the federal government to manage the health of populations the government would rather not manage itself. That is either one of the most defensible franchises in American capitalism or one of the most fragile, and the honest answer is that it is both at once, depending on which year and which line of business you look at. The task here is not to decide that Centene is a good company or a bad one. It is to understand the machine — how it makes money, where the money can vanish, who has held the wheel, and what a skeptical investor should watch to know whether the story is working.

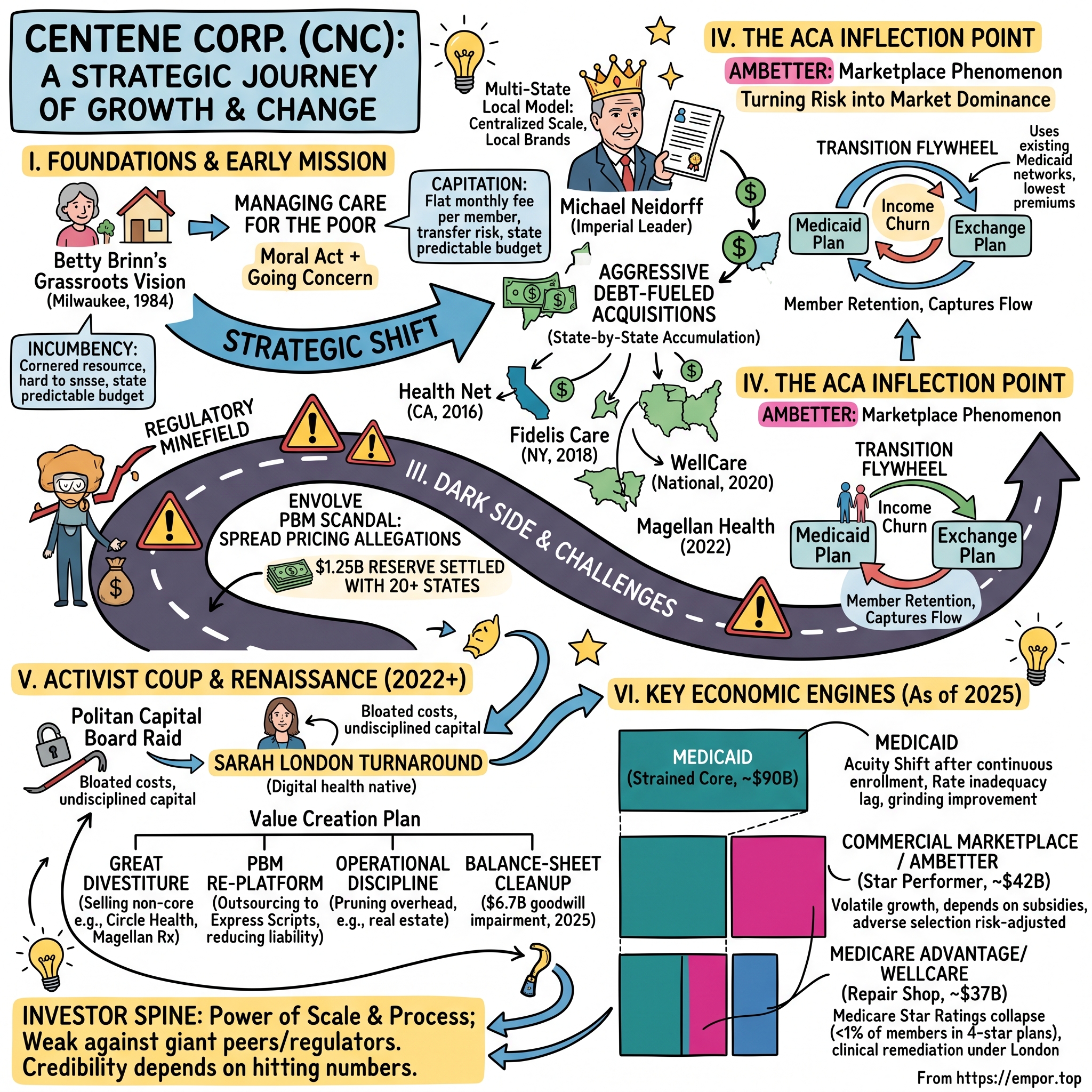

The road ahead runs in five movements. First, the social-mission beginnings — Betty Brinn's grassroots conviction that you could manage the care of the poor and save the taxpayer money at the same time. Second, the Neidorff roll-up machine — a quarter-century of aggressive, debt-fueled, state-by-state acquisition under one of the most singular executives in the industry's history, and the birth, in the wake of the Affordable Care Act, of the "Ambetter" marketplace phenomenon that would become Centene's most profitable surprise. Third, the dark side of the roll-up — a regulatory minefield, a pharmacy-billing scandal that cost the company hundreds of millions in settlements, and an integration hangover that never quite cleared. Fourth, the activist coup — the boardroom raid by Politan Capital that ended Neidorff's reign. And finally, the Sarah London renaissance — the painful, ongoing work of pruning the garden Neidorff planted: divestitures, a $6.7 billion goodwill write-down, and a hard pivot from growth-at-all-costs toward margin discipline.

Before the history, one myth worth puncturing up front, because it colors how people read this company. The popular framing casts Centene as a predator that profits by denying care to the poor — a middleman extracting rents from the welfare state. The reality is more interesting and more unsettling than that cartoon. Centene does not primarily make money by denying care; on its largest business it barely makes money at all, running medical-loss ratios north of 90% that leave single-digit margins by design. Where it makes its real profit is in the arbitrage of complexity — being the entity willing and able to absorb the actuarial risk, the administrative burden, and the political volatility that governments desperately want off their own books. That is a genuinely valuable service, and it is also one that puts the company permanently at the mercy of the very governments that pay it. Hold that tension in mind; it recurs in every chapter.

To understand any of it, you have to go back to Milwaukee, and to a hospital administrator who believed that caring for the poor could be both a moral act and a going concern.

II. The Origins: Betty Brinn and the Managed Medicaid Experiment

Picture Milwaukee in 1984. The industrial Midwest is in the middle of a brutal decade — factories closing, the manufacturing base hollowing out, welfare rolls swelling in the inner city. Inside Family Hospital, a modest facility serving the low-income neighborhoods of the city's north side, a hospital administrator named Elizabeth "Betty" Brinn was wrestling with a problem that had defeated far larger institutions: how do you actually take care of poor people without going broke doing it?

Brinn was an unlikely candidate to launch a healthcare empire. She had come up the hard way, without the pedigree of the hospital executives of her era, and she carried a conviction that the medical system treated the poor as an afterthought — showing up in emergency rooms only when a manageable problem had become a catastrophe. The idea she seized on was, at the time, close to heretical. Rather than wait for low-income mothers and children on welfare to arrive sick and expensive, what if a plan actively managed their care — steered them toward a regular doctor, caught problems early, coordinated the pieces? Out of that conviction she founded what became Family Hospital Health Plan, a small non-profit built to manage healthcare for the Medicaid population of a single Wisconsin county.16

To understand why this was radical, you have to understand how Medicaid worked then, because the mechanism is the whole story. Medicaid — the joint federal-state program for the poor — traditionally paid doctors and hospitals "fee-for-service." A provider performed a service, sent the state a bill, and the state paid it. Simple, and disastrous. Fee-for-service pays for volume, not health. It rewards more tests, more visits, more procedures, and it does nothing to coordinate a diabetic patient's insulin, diet, foot care, and eye exams into anything resembling a plan. Costs ran wild, care stayed fragmented, and outcomes for the poor stayed miserable.

The reform sweeping through statehouses in the 1980s was capitation — and this is the concept to hold onto, because it is the beating heart of Centene's entire business to this day. Under capitation, the state stops paying per-service and instead pays a private company a flat monthly fee for each member enrolled — say, a few hundred dollars per person per month — and hands that company the responsibility, and the risk, for all of that member's covered care. If the plan keeps its members healthy and manages costs below the monthly payment, it keeps the difference. If its members turn out sicker and more expensive than the payment assumed, the plan eats the loss. In one stroke, capitation transfers the actuarial risk of a population off the taxpayer's balance sheet and onto a private insurer's. The state gets a predictable budget line; the insurer gets a bet.

Brinn's wager was that this bet could be won honorably — that preventive medicine, care coordination, and simply paying attention to a population everyone else ignored could improve health and come in under budget, leaving room for both a mission and a margin. It was a genuinely idealistic proposition, and it is worth pausing on, because everything Centene later became — the profits, the scandals, the scale — is a working-out of the tension Brinn built into the foundation: the same capitation contract that funds the care of the poor also pays the insurer more the less care it delivers. Manage that tension well and you have preventive medicine. Manage it badly and you have a company incentivized to deny.

Brinn did not live to see which way her creation would break. She died in 1992, and Milwaukee still remembers her — the Betty Brinn Children's Museum on the city's lakefront carries her name. The health plan she built passed to a group of local investors who saw in her small non-profit the seed of something far larger. In 1997 they gave it a new name built to travel beyond one county and one state: Centene Corporation.16 The mission was about to meet a machine. And the machine arrived in the person of a man who would run the company for the next twenty-five years.

III. The Michael Neidorff Era: Building the Managed Care Roll-Up

Michael Neidorff did not look like a disruptor. When he took over as CEO in 1996, he was a middle-aged healthcare executive with a background running managed-care operations, a taste for fine art and expensive wine, and a management style that colleagues and adversaries alike would come to describe with the same word: imperial.11 Over the next quarter-century he would build Centene into a Fortune 25 company, personally amass one of the largest executive pay packages in the industry, and run the enterprise with a control so total that it eventually became the justification for a boardroom coup. But in 1996 he was simply a man with a blueprint.

The first thing Neidorff did was move the company's center of gravity to St. Louis, Missouri, and start thinking in terms of a map of the United States rather than a map of one county.11 The insight that made the whole thing work — the thing that separated Centene from the dozens of other Medicaid plans that stayed small and eventually got acquired — was deceptively simple. Neidorff understood that healthcare is inescapably local, but its economics are ruthlessly national.

Consider the problem from a governor's chair. A state Medicaid director awarding a multibillion-dollar contract to manage the health of the state's poorest residents does not want to hand that money and that political risk to a faceless Wall Street conglomerate headquartered a thousand miles away. When something goes wrong — and in Medicaid, something always goes wrong — the director wants a local executive in the room, someone who knows the state's hospitals, its legislators, its politics. So Neidorff gave every state its own company. Georgia got Peach State Health Plan. Florida got Sunshine Health. Each state subsidiary carried a local name, a local brand, local executives, local relationships. To the governor, Centene looked like a hometown operator.

But behind that storefront of local plans, Neidorff centralized everything that carried economies of scale — the actuarial modeling, the claims-processing technology, the compliance apparatus, the negotiating leverage — in St. Louis. This is the "multi-state local" model, and it is the closest thing Centene has to a genuine, durable competitive advantage. A single-state Medicaid non-profit has local relationships but no scale. A national health insurer has scale but no local face. Centene manufactured both at once: fifty local companies wearing one national brain.

It is worth dwelling on the man himself, because Centene for twenty-five years was not so much a company with a CEO as a CEO with a company. Neidorff cultivated an air of the connoisseur — art on the walls, an appreciation for the finer things, a boardroom presence that colleagues found by turns charismatic and domineering. He paid himself accordingly; by the late 2010s his compensation ran into the tens of millions annually, among the richest in the industry, and the board that set it was a board he had largely shaped. He held the titles of chairman and chief executive simultaneously for most of his tenure, a concentration of authority that governance purists warn against precisely because it removes the check of an independent chair. For years, the returns were good enough that nobody pressed the point. Founders and founder-like operators are often granted exactly this kind of latitude, and it works — right up until the moment it doesn't. Neidorff's story is a near-perfect illustration of both halves of that sentence.

In 2001, Centene went public on the New York Stock Exchange — a company then generating around $327 million in annual revenue, serving roughly a quarter-million members across three health plans.16 The IPO was not really about the cash. It was about the currency. A public stock gave Neidorff an acquisition weapon, and he was about to spend the next two decades swinging it. To put the scale of what followed in perspective: that $327 million of revenue would compound into more than $190 billion within a single executive's tenure — a roughly 600-fold increase, achieved not through one breakthrough product but through the patient, relentless accumulation of government contracts, one state and one acquisition at a time.

Why does winning a state Medicaid contract matter so much that it is worth this whole apparatus? Because these contracts are, in the language of strategy, a cornered resource — an asset that is scarce, valuable, and awarded through a gate that competitors cannot easily storm. States award Medicaid managed-care contracts through multi-year Request for Proposal cycles, and crucially, they cap the number of winners — often at just two or three plans for an entire state. Win one of those slots and you don't merely gain members; you gain a multi-year, quasi-exclusive franchise to a captive, government-funded revenue stream, while every competitor is locked out until the next RFP cycle, which may be five years away. Then you spend those years sinking roots — signing up the local hospitals and physician groups, building the provider network, embedding into the state's systems — so that by the time the contract comes up for renewal, dislodging you means rebuilding all of it from scratch. The barrier to entry isn't a patent or a brand. It's the RFP itself, and the incumbency it confers.

The catch — and it is the catch that defines the entire economics of this business — is that Medicaid is brutally, almost punishingly, low-margin. Net margins in the low single digits, somewhere in the 1.5% to 3% range in a normal year, are the reality of managing care for the poor on a government budget. There is no pricing power; the state sets the rate. There is no premium product; the benefit is defined by law. The only way to make capitated Medicaid work is scale — spreading the fixed costs of technology, actuarial talent, and compliance across enough members that thin margins on a vast base add up to real money, and building risk-prediction models good enough to bid a hair below competitors while still, just barely, coming out ahead. Neidorff grasped this early: in Medicaid, size is not a vanity. It is the business. The company that is biggest can bid lowest and still survive, which lets it get bigger still.

For the first fifteen years, that flywheel — win an RFP, build the network, use the scale to win the next RFP — was the whole strategy. Then, in 2010, Washington passed a law that would either destroy Centene's world or hand it the greatest growth opportunity in its history. Nobody in the industry was sure which.

IV. The ACA Inflection Point: Transforming Risk into Market Dominance

In March 2010, President Obama signed the Patient Protection and Affordable Care Act — Obamacare — and the American health-insurance industry reacted with something close to dread. The new law did two enormous things at once. It expanded Medicaid eligibility dramatically in the states that chose to participate, flooding the rolls with millions of new low-income adults. And it created the individual insurance exchanges — online marketplaces where people who didn't get coverage through an employer could buy subsidized private plans, and where, for the first time, insurers were forbidden from turning away or overcharging the sick.

That second piece is what terrified the industry. For decades, the profitable way to sell individual insurance had been to cherry-pick the healthy and exclude the sick — deny coverage for pre-existing conditions, price the chronically ill out of the market. The ACA banned all of it. Now anyone could buy a plan regardless of health status, at a price that couldn't be jacked up for being sick. The industry's collective fear was straightforward: the exchanges would become a magnet for the sickest, most expensive patients in America, an adverse-selection death spiral that would drown any insurer foolish enough to wade in. Aetna, Humana, UnitedHealth — the marquee names — would spend the mid-2010s wading in, losing money, and retreating.

Neidorff saw the opposite. Where the corporate insurers saw a market full of sick people they didn't know how to price, Centene saw a market full of low-income people it had been pricing and managing for thirty years. The exchange population — subsidized, price-sensitive, frequently poor, often the same demographic that cycled on and off Medicaid — was Centene's native habitat. The company launched a dedicated marketplace brand, Ambetter Health, and went to war on price.

Here is the mechanism that made Ambetter win, and it is a beautiful piece of strategic reuse. When Centene built its exchange plans, it did not go construct expensive new networks of doctors and hospitals. It simply ran Ambetter on top of the Medicaid provider networks it already owned — the same physicians and facilities, already contracted at Medicaid-style reimbursement rates, already accustomed to the lower payments that come with serving government populations. A narrow network of lower-cost providers is a worse deal for a member who wants unlimited choice of any specialist in the city. But it is a dramatically cheaper network to run — and on the exchanges, where subsidized buyers shop almost entirely on monthly premium, cheapest wins. Ambetter consistently offered among the lowest premiums on the exchange, and the price-sensitive, government-subsidized retail buyer flocked to it. Centene didn't out-market the giants. It out-costed them, using an asset it already had.

Then comes the second, subtler piece of genius — the part that turns two separate businesses into a machine that feeds itself. Call it the transition flywheel. Low-income Americans live with what economists politely call "income churn." A member earning just under the Medicaid eligibility threshold this year takes a few extra shifts, gets a modest raise, and next year earns just over it — losing Medicaid and needing a subsidized exchange plan instead. The following year, hours get cut, and they churn back onto Medicaid. For most insurers, every one of those transitions is a lost customer and a fresh acquisition cost. But because Centene operates both the Medicaid plan and the Ambetter exchange plan in the same market, a member churning off Medicaid can be caught and moved seamlessly into Ambetter, and vice versa. The customer never leaves the Centene ecosystem. The company converts the chaos of poverty — the very income volatility that makes this population "unprofitable" to everyone else — into customer retention. The dual model doesn't just serve two markets. It captures the flow between them.

There is a subtlety here that the corporate insurers missed and that explains why they lost money on the exchanges while Centene made it. The exchange business, like Medicaid, comes with government machinery designed to blunt the risk of covering the sick — risk adjustment, and in the early years, reinsurance and risk corridors. An insurer that understands and models that machinery well can price aggressively low, attract volume, and let the risk-transfer mechanics true up the economics after the fact. An insurer that treats the exchange like a conventional commercial market — pricing to avoid the sick — ends up with too few members, too little scale, and premiums that are uncompetitive. Centene, having spent decades operating inside exactly this kind of government-managed risk pool on the Medicaid side, read the machinery natively. Its rivals were playing a game whose rules they had never had to learn. That, more than any single product decision, is why Ambetter won the exchanges while Aetna and UnitedHealth retreated from them.

What did this actually prove about the business? It demonstrated that Centene's edge was never really about Medicaid as a category — it was about a specific competence: managing thin-margin, government-funded, low-income risk pools better and cheaper than anyone who came at the problem from the commercial side. The ACA didn't create a new business for Centene so much as it revealed how portable the old one was. That competence would carry the company to the top of the exchange market, where it remains the largest player. But it also created a hunger. If Centene's local franchises were this valuable, and if the model was this replicable, then the logical move was to buy every franchise it could get its hands on. The roll-up was about to accelerate into overdrive — and this time, the checks would have a lot more zeros.

V. The M&A Gold Rush: Scale at All Costs

By the middle of the 2010s, Michael Neidorff had a thesis, a public stock, a mountain of debt capacity, and a conviction that in the Medicaid business, the biggest player wins. What followed was one of the most aggressive acquisition sprees in the history of American healthcare — a five-year gold rush in which Centene spent north of $30 billion buying its way to national dominance. Each deal had its own strategic logic. Together they built a colossus and, simultaneously, planted the seeds of the crisis that would nearly consume the company a decade later.

The opening move came in 2016 with Health Net, a roughly $6.8 billion acquisition that instantly made Centene a serious force in California, the largest Medicaid market in the country, and threw in a lucrative federal TRICARE contract serving military families as a bonus.11 California alone was worth the price of admission; the Golden State's Medi-Cal program is a universe unto itself, and Centene now owned a commanding position in it.

Then, in 2018, came the deal that showed Neidorff's eye for the unglamorous prize. Centene paid $3.75 billion for Fidelis Care, a Catholic-affiliated non-profit health plan, in a transaction that closed on July 2, 2018.13 To an outsider, buying a religious charity's health plan sounds like a curiosity. To Neidorff, it was a masterstroke: Fidelis was the dominant government-sponsored plan in New York State, one of the richest and most complex Medicaid and exchange markets in America. Overnight, Centene went from bystander to the number-one position in New York. The pattern was becoming clear — Centene wasn't buying companies, it was buying incumbencies, those cornered-resource state franchises that take years and RFP cycles to build from scratch.

The crown jewel arrived on January 23, 2020, when Centene completed its $17.3 billion acquisition of WellCare Health Plans.12 This was the deal that made Centene the undisputed largest Medicaid managed-care company in the United States, and it did far more than add scale. WellCare brought a substantial Medicare Advantage business — plans for seniors, a market Centene had underweighted — and combining the two companies' footprints created an enterprise serving, at the time, more than 24 million members across all fifty states.12 WellCare shareholders took a mix of cash and Centene stock; the deal was financed with a heavy dose of debt and equity, and it made Centene, by membership, the government-healthcare champion Neidorff had spent a quarter-century building toward.

The spree closed out in early 2022 with a final, different kind of deal: the roughly $2.2 billion acquisition of Magellan Health, a move to bring behavioral-health management and specialty pharmacy capabilities in-house — vertical integration rather than horizontal expansion.14 Behavioral health, as we'll see, was becoming the single fastest-rising cost in the Medicaid book, and owning the capability to manage it looked, on paper, like foresight.

It is worth pausing on what "integration" actually means in this industry, because the word gets thrown around as a euphemism that hides the real difficulty. When Centene bought WellCare, it did not acquire a clean, plug-in business. It acquired millions of members sitting on WellCare's claims-processing platforms, WellCare's provider contracts, WellCare's care-management systems, WellCare's regulatory filings in dozens of states — none of which spoke natively to Centene's own systems. Merging them means migrating members without dropping their claims, reconciling two different ways of coding the same medical procedure, retraining thousands of employees, and doing all of it under the watchful eye of state regulators who can and will penalize errors that hurt members. Do it well and you capture the promised cost synergies. Do it slowly or sloppily — as Centene largely did — and you run two expensive systems in parallel for years, the synergies evaporate, and operational quality slips in exactly the places, like Medicare Star Ratings, where slippage costs real money. The gap between the M&A press release and the operating reality is where fortunes are made and lost, and Centene spent most of the early 2020s on the wrong side of it.

So did they overpay? The uncomfortable answer, visible clearly only in hindsight, is yes — and the evidence is not opinion but accounting. Under relentless pressure to grow, Centene had assembled a sprawling, chaotic collection of assets, each acquired company arriving with its own IT platform, its own claims system, its own management layer, its own way of doing everything. Integration — the unglamorous work of actually welding these companies into one operating system — lagged badly. WellCare in particular came with a difficult integration and, critically, a Medicare Advantage business whose federal quality ratings would deteriorate under Centene's ownership, costing the company hundreds of millions in lost government bonus payments in the years to come. And the prices paid — the premiums above the tangible value of what was bought — piled up on the balance sheet as goodwill, an intangible asset that sits there looking fine until, one day, an auditor decides it no longer reflects reality and forces you to write it off. Centene was accumulating a debt that wasn't on the debt schedule. It would come due in 2025.

For now, though, Neidorff had built his empire. The trouble was that empires run without checks tend to develop rot in the places no one is watching — and by 2021, regulators in twenty states were about to start watching very closely indeed.

VI. The Underbelly: PBM Scandals and the Activist Intervention

The unraveling started, as these things often do, with pharmacy bills. Buried inside Centene was a subsidiary most investors had never heard of: Envolve Pharmacy Solutions, the company's in-house pharmacy benefit manager, or PBM. A PBM is the middleman of the drug-supply chain — the entity that sits between the insurer, the pharmacy, and the drug manufacturer, processing prescription claims, negotiating rebates, and, in theory, using its scale to lower drug costs. In practice, PBMs operate inside one of the most opaque corners of American healthcare, where money moves through mechanisms almost no outsider can trace. And in 2021, state attorneys general started tracing.

The allegation against Envolve was spread pricing, and the concept is worth explaining plainly because it is the whole scandal. When a Medicaid member fills a prescription, the PBM pays the pharmacy one price for the drug and then bills the state Medicaid program a different, higher price — pocketing the "spread" in between. On its own, some spread is a normal part of how PBMs earn money. The problem, regulators alleged, was that Envolve was billing state Medicaid programs for pharmacy services at inflated rates while failing to disclose the discounts and rebates it was collecting from drug manufacturers on the other side — in effect, charging taxpayers twice and hiding the double-dip. Centene, the company built to save states money on the care of the poor, stood accused of quietly overcharging those same states on their drug bills.

The financial reckoning came fast and heavy. In mid-2021, Centene recorded a $1.25 billion reserve to resolve the growing wave of state investigations — an extraordinary sum to set aside for a business line most shareholders didn't know existed.6 The company then began settling with states one by one, on a "no-fault" basis that admitted no wrongdoing while paying to make the problem go away. Ohio extracted a then-record $88.3 million.9 Texas settled for roughly $165.6 million.8 California, the largest, reached a $215 million settlement.[^10] By the time the wave had mostly crested, Centene had struck settlements with more than twenty states, and the running total of payouts climbed into the hundreds of millions and beyond.7 It was, in dollar terms, one of the largest state-level healthcare-billing settlements of its era — and in reputational terms, it was a flashing red light about how the company was being governed.

That light did not go unnoticed on Wall Street. In late 2021, an activist hedge fund named Politan Capital Management, run by a sharp-elbowed former Elliott Management and D.E. Shaw investor named Quentin Koffey, took a major stake in Centene and made its thesis unmistakable: this was a company with a broken governance structure. The argument was pointed. Michael Neidorff had run Centene as an unchecked fiefdom for twenty-five years. Administrative costs were bloated relative to peers. Capital allocation — that acquisition spree — had been undisciplined, buying growth without buying the integration to make it pay. And the Envolve scandal was not an accident but a symptom: a company with real oversight, Politan argued, does not blunder into a nine-figure billing settlement across twenty states. Where there was one problem no one was watching, there were probably others.

The confrontation resolved with startling speed. On December 14, 2021, Centene announced a cooperation agreement with Politan and a wholesale refresh of its board.10 Five new directors were brought in, and the caliber of the names told you who had won: Ken Burdick, the former CEO of WellCare — the very company Centene had just swallowed — and Wayne DeVeydt, the former chief financial officer of Anthem, both respected operators with deep credibility in exactly the businesses where Centene was struggling.10 The board also adopted a mandatory retirement age of 75, a governance provision aimed squarely at one man. This was, in the polite language of corporate governance, a boardroom coup.

And the man it was aimed at was, by then, both under siege and gravely ill. On that same day in December 2021, Centene announced that Michael Neidorff would step down as CEO.11 He formally retired in early 2022 and died on April 7, 2022, at the age of 79.11 It was the end of one of the most consequential and complicated tenures in the history of American managed care — a man who had built a Fortune 25 company from a single-county health plan, and whose success had metastasized into exactly the kind of unaccountable sprawl that undoes empires. The garden he planted was vast, valuable, and badly overgrown. The person handed the shears was someone almost nobody in the investment community had heard of.

VII. The Sarah London Pivot: Pruning the Garden

When Centene named Sarah London its chief executive in March 2022, the reaction in some corners of Wall Street was disbelief. She was 41 years old. She had never run a company of anything close to this size. And she came not from the world of state Medicaid contracts and actuarial risk pools but from the frontier of digital health — a stint at Optum, the technology-and-services arm of UnitedHealth, and time in venture capital at Oak HC/FT, the healthcare-focused firm.11 Handing a $100-billion-plus insurer built on political relationships to a digital-health native looked, to skeptics, like a category error.

But that background was precisely the point. Neidorff's Centene had been built to acquire. London's job was to make it operate. The mandate handed down by the refreshed board was a clean reversal of everything that came before: stop chasing growth through debt-fueled M&A, and start extracting margin and discipline from the sprawling machine already in hand. The strategy she rolled out — branded internally as a value-creation plan — had four distinct thrusts, and each one was, in its own way, a repudiation of the prior era.

The first was the great divestiture — pruning the portfolio back to its core. Neidorff, in his acquisitive enthusiasm, had wandered far from Medicaid, buying international hospital operators and adjacent businesses that had little to do with managing American government health programs. London sold them off. Centene divested Circle Health Group, a private UK hospital operator, for $1.2 billion in a deal that completed in January 2024.15 It unloaded Ribera Salud, a Spanish hospital group. It sold the Magellan Rx pharmacy business to Prime Therapeutics, Magellan's specialty-health unit to Evolent, and its AI-analytics arm, Apixio. Piece by piece, London stripped away the diversification that Neidorff had prized and Politan had derided as "diworsification" — the value-destroying kind of diversification that scatters management attention without adding earnings. The proceeds, more than $5 billion in total, went not into new acquisitions but into buying back Centene's own shares and paying down debt.

The second thrust was the PBM re-platform — and here London made an existential judgment call. After the Envolve disaster, operating a large in-house pharmacy benefit manager wasn't just an operational headache; it was a permanent regulatory liability, an ongoing invitation for the next attorney general to come looking. So London made the decision to get out of the business of running her own PBM at scale. In a multi-year agreement announced on October 25, 2022, Centene outsourced its enormous pharmacy spend — more than $35 billion a year, one of the largest such books in the country — to Express Scripts, the PBM giant owned by Cigna's Evernorth, with the arrangement taking effect in 2024.[^19] The logic was twofold: capture the cost savings that come from plugging into Express Scripts' vastly larger negotiating scale, and, just as importantly, offload the compliance risk. Centene would still pay for its members' drugs, but it would no longer be the middleman that could be accused of skimming the spread.

The third thrust was operational discipline applied to the company's own overhead — the unglamorous cost-cutting that a growth-obsessed culture had ignored for years. Most visibly, London's team moved to reduce Centene's domestic leased real estate footprint by roughly 70%, an aggressive rationalization that took out on the order of $200 million in annual costs from a workforce that, post-pandemic, no longer needed the office space Neidorff's expansion had accumulated. On the Q1 2026 earnings call, management pointed to a consolidated administrative-cost ratio of 7.6% of revenue, down from 7.9% a year earlier — the kind of incremental grind that signals a company actually running the numbers rather than just growing into them.3

The fourth thrust was the balance-sheet cleanup, and it was the most dramatic single act of London's tenure. In the third quarter of 2025, Centene took a staggering $6.723 billion non-cash goodwill impairment charge — an accounting acknowledgment that the prices Neidorff had paid for his acquisitions, WellCare above all, could no longer be justified by the earnings those businesses were actually producing.[^5] The trigger was a brutal 2025: a mid-year collapse in the profitability of the marketplace book (more on that shortly) and a sharp fall in Centene's own stock price forced the write-down. The charge was the direct financial descendant of the M&A gold rush — the deferred bill for a decade of overpaying, finally coming due in a single quarter, and the reason a company with $195 billion in revenue reported a multibillion-dollar loss for the year.1 It flushed the historical premium out of the system. It did not, by itself, fix the underlying businesses that had prompted it.

Whether London's turnaround is genuinely working — or merely rearranging a portfolio while the core margins stay under structural pressure — cannot be settled by narrative. It has to be settled in the three engines that actually produce Centene's revenue. So let's open the hood.

VIII. Financial Engine Room: Segment-Level Proportionality

Centene reports its business in three principal segments, and the cleanest way to see the company is by the money each one moves. In 2025, total GAAP revenue reached $194.8 billion, of which premium and service revenue — the money Centene earns for actually bearing insurance risk and providing services — was $174.6 billion.1 That $174.6 billion is the base worth anatomizing, because it splits into three very different businesses with three very different economics. Medicaid is the giant. Marketplace is the profit engine. Medicare is the repair project. Understanding Centene means understanding why each is what it is.

1. Medicaid: The Core Engine

At $90.2 billion in 2025 premium and service revenue — roughly 52% of the total — Medicaid remains the foundation on which everything else rests, the business managing care for more than 12.5 million members.1 It is also the segment that put Centene through the wringer over the past three years, in a saga that is a case study in how government policy can whipsaw a capitated insurer.

The story is the Medicaid "unwinding." During the COVID-19 pandemic, Congress prohibited states from disenrolling anyone from Medicaid — "continuous enrollment" — which meant the rolls swelled to historic highs as no one, whether or not they still qualified, could be removed.[^20] For Centene, this was a windfall of stable, growing membership. Then, starting in April 2023, the protection ended and states resumed checking eligibility, a process that stretched across 2023 and 2024 and removed millions of people from the Medicaid rolls nationwide.[^20] Centene's Medicaid membership shrank accordingly.

But the shrinkage came with a poisoned twist, and this is the mechanism to understand: the acuity shift. When states began culling the rolls, the healthy members — the ones who rarely used care and were cheapest to cover — were disproportionately the ones who found other coverage or simply fell off. The sicker, higher-cost members, who depend on their coverage and navigate the paperwork to keep it, stayed. Centene was left managing a smaller pool that was, member for member, considerably more expensive. Its capitation rates, negotiated based on the old, healthier population, no longer matched the risk it was actually carrying. The result showed up in the metric that matters most in this business: the Health Benefits Ratio (HBR, also called the medical loss ratio), the share of premium spent on member medical care. In the first quarter of 2026, the Medicaid HBR ran at 93.1% — meaning more than 93 cents of every premium dollar went straight back out as medical cost, leaving almost nothing for administration and profit.3 A healthy Medicaid HBR sits closer to the high 80s; 93.1% is the signature of a book earning far too little for the risk it holds.

Management's response is a grinding, unglamorous campaign on two fronts, and the Q1 2026 earnings call laid it out in unusual detail. On the revenue side, the fix is rate negotiation — going state by state, actuary by actuary, presenting fresh data showing that the remaining members are sicker, and pushing governors and Medicaid directors to raise the monthly per-member payments to match. On the cost side, the fix is trend management — a portfolio of levers to bend the medical-cost curve: tighter utilization management, network optimization to steer members toward higher-performing providers, and an aggressive campaign against fraud, waste, and abuse, particularly in behavioral health. CEO Sarah London singled out applied behavior analysis (ABA) therapy — a fast-growing and, in her telling, frequently over-prescribed and sometimes fraudulently billed service — as a specific target, describing providers "prescribing the maximum number of hours every single week for every single patient."3 Notably, London told analysts she would be "disappointed" if the company merely hit its own 93.7% full-year Medicaid HBR target given first-quarter outperformance — a rare instance of a CEO publicly setting a bar above her own guidance.3

There is a hard truth buried in the rate-negotiation dynamic that investors should sit with, because it defines the tempo of any recovery. Medicaid rates are set on a lag. States build their capitation rates from historical claims data — typically data that is already a year or more old by the time the new rates take effect. So when costs spike in real time, as they did during the acuity shift, the insurer absorbs the gap for the many months it takes for that elevated cost experience to work its way into the "base period" the actuaries use, and then for the states to acknowledge it and adjust. Centene calls this closing the gap between "trend" and "rate," and on the Q1 2026 call management framed the whole 2026 thesis around it: a Medicaid composite rate yield of roughly 4.5% intended to match net medical-cost trend of roughly 4.5%, so that the HBR at least stops rising while the cost-control levers slowly bend it back down.3 The subtlety analysts pressed on the call was whether recent outperformance was durable or merely a mild flu season and favorable weather flattering the quarter — and management, to its credit, conceded that some of the beat was exactly that, refusing to bank the good luck into full-year guidance.3 That kind of candor about the quality of a beat is itself a small credibility signal.

What should an investor make of this? The encouraging read is that the first quarter of 2026 was the third consecutive quarter of Medicaid margin improvement, and that management's explanations were concrete and mechanism-specific rather than hand-waving — a marked contrast to the vaguer reassurances of the prior era.3 The cautious read is that Medicaid margin recovery is entirely dependent on state governments agreeing to pay more, at a moment when those same states face their own budget pressures and new federal policy changes — including looming Medicaid work requirements — that could shrink the rolls further and re-scramble the risk pool all over again. This is a business whose profitability is negotiated, not earned, and the counterparty holds most of the cards.

2. Commercial Marketplace / Ambetter: The Star Performer

If Medicaid is the engine that strains, the commercial marketplace segment — essentially the Ambetter exchange business — has been the engine that paid the bills, generating roughly $42.0 billion in 2025, about 24% of premium and service revenue.1 For years this was Centene's quiet triumph: the narrow-network, lowest-premium model reused the Medicaid provider base to serve price-sensitive exchange buyers, and it did so at margins that Medicaid could only dream of. Ambetter grew to more than 5.5 million members, making Centene the largest player on the ACA exchanges in the country.1 The marketplace was the margin stabilizer that cushioned the blow from the Medicaid acuity crisis.

And then, in 2025, the marketplace delivered the shock that nearly defined the year. In July 2025, Centene did something insurers almost never do: it withdrew its full-year 2025 earnings guidance entirely.4 The reason was a first look at independent actuarial data from Wakely, which analyzes the exchange market: it showed that the overall risk pool across the states Centene served was sicker — higher "morbidity" — than the company had assumed when it priced its 2025 plans. Because exchange plans are subject to a risk-adjustment mechanism (a system that transfers money from insurers with healthier-than-average members to those with sicker-than-average members), a miscalibration of the whole market's health translated into roughly $1.8 billion less risk-adjustment revenue than Centene had booked — a swing of around $2.75 per share.4 Ambetter, it turned out, had been underpriced. The stock cratered, and the shock helped trigger the goodwill write-down that followed in the third quarter.

The 2026 chapter of the marketplace story is dominated by a single policy cliff: the expiration of the enhanced Premium Tax Credits. These enhanced federal subsidies, which had made exchange coverage dramatically more affordable and fueled Ambetter's membership surge, lapsed at the end of 2025 and, as of mid-2026, had not been extended by Congress.17 The mechanical consequence is that subsidized enrollees face sharply higher premiums, and a chunk of them — disproportionately the healthy ones who were only in the market because it was nearly free — drop out. Centene's marketplace membership fell to roughly 3.6 million by the first quarter of 2026, down from the 5.5-million-plus peak.3

Here the Q1 2026 call becomes genuinely interesting, because it reveals how management thinks about its own business. London's argument to analysts was counterintuitive: yes, the healthy members left, and yes, that left Ambetter with a sicker "Silver-tier" population — but in the exchange market, unlike ordinary insurance, sicker can be profitable, because the risk-adjustment mechanism is explicitly designed to pay you more for covering sicker members.3 "The concept of adverse selection can be scary," London told analysts, "but that's not actually the case in Marketplace because the risk adjustment mechanism is specifically designed to counteract adverse selection."3 Centene raised its full-year 2026 adjusted earnings guidance to greater than $3.40 per share on the strength of the quarter — while pointedly not booking the full risk-adjustment benefit it believes it is owed, waiting instead for confirming Wakely data due in June.3 That is either prudence or a company still gun-shy after last year's miss, and reasonable investors can read it either way. The honest assessment: the marketplace is structurally Centene's best business, but 2025 proved that its profitability rests on pricing assumptions about a whole market's health that can be badly wrong, and its size now rests on a federal subsidy that Congress has, for the moment, allowed to lapse.

3. Medicare Advantage / WellCare: The Repair Shop

The third engine — Medicare Advantage and the standalone Part D drug business, largely the inheritance from WellCare — generated about $37.2 billion in 2025, roughly 21% of premium and service revenue, and it has been, bluntly, the problem child.1 The trouble is a government scoring system called Star Ratings.

Here's how it works, in plain terms. The federal Centers for Medicare & Medicaid Services grades every Medicare Advantage plan on a one-to-five-star quality scale, and those stars are not cosmetic — they drive real money. Plans rated four stars and above earn substantial Quality Bonus Payments from the government, extra funding that can be the difference between a profitable plan and a losing one. After the messy WellCare integration, Centene's Star Ratings collapsed. For 2025, less than 1% of Centene's Medicare members were in plans rated four stars or higher — an operational disaster that stripped the company of hundreds of millions of dollars in bonus payments it would otherwise have collected, and left the Medicare segment bleeding.[^7]

The recovery has become one of London's signature turnaround projects, and the early evidence is real. For 2026, Centene's clinical-remediation work drove a dramatic improvement: roughly 18% to 20% of its Medicare members landed in four-star-or-better plans, and the average contract rating climbed to 3.39, up from 3.14 a year earlier.[^7] That is a genuine operational recovery, though it is worth keeping perspective — Centene's ratings had peaked near 3.89 in 2022 before the collapse, so the 2026 figure is a rebound off the bottom, not a return to excellence.[^7] Strategically, London's team has narrowed the Medicare focus toward Dual-Eligible Special Needs Plans (D-SNPs) — plans for people who qualify for both Medicare and Medicaid at once. This is the logical move: the dual-eligible population sits at the exact intersection of Centene's two strongest competencies, aligning the Medicare book with the Medicaid base the company already knows how to manage. On the Q1 2026 call, management said dual-eligible members had reached 40% of the Medicare Advantage portfolio and expressed confidence in a path to breakeven for the segment in 2027 — a target, not an achievement, and one worth holding management to.3

Taken together, the three engines tell a coherent story: a strained core, a volatile profit center, and a repair project showing early progress. The investment question is whether that combination adds up to a durable franchise or a perpetually pressured one — which is where the bull and bear cases finally meet.

IX. The Investor Spine: Playbook, Risk Radar, and Bull vs. Bear

Strip away the history and the personalities, and what does Centene's competitive position actually rest on? It is worth running the company through the frameworks that serious investors use — Hamilton Helmer's "7 Powers" and Michael Porter's five forces — not to award a grade, but to locate precisely where the moat is real and where it is thinner than the story suggests.

The genuine powers are two, and they are narrower than a bull might hope. The first is scale economies. In a business where margins run in the low single digits, being the largest player is not a luxury but the entire game: Centene's national scale lets it spread fixed technology, actuarial, and compliance costs across more members than almost any competitor, and its dominant regional membership concentration lets it demand low reimbursement rates from local hospital and physician groups that need access to its members. The second is process power — the deep, specialized, hard-to-replicate organizational capability required to bid on, win, and then actually execute state Medicaid RFPs while holding the medical loss ratio in check. This is not something a well-funded entrant can buy off the shelf; it is accumulated know-how, built state by state over decades, and it is the closest thing Centene has to a durable edge. The cornered-resource dynamic of the RFP contracts themselves reinforces it: each won contract is a multi-year, capped-competition franchise.

But an honest five-forces reading exposes where the moat gives way. The bargaining power of buyers — here, state and federal governments — is close to absolute. Centene's customers set its prices, define its products, and can change the rules overnight; there is no pricing power against a monopsony buyer that is also a sovereign. The threat of substitutes and rivals is real: UnitedHealth, Elevance, Molina, and CVS/Aetna all compete for the same RFP slots, and in a business where the low bid wins, rivalry compresses margins structurally. What Centene does not face in much measure is the threat of new entrants — the RFP moat and scale requirements keep startups out — but that is cold comfort when the existing rivals are some of the largest and best-capitalized companies in America. The uncomfortable synthesis: Centene has a strong position against small competitors and new entrants, and a weak position against its own giant peers and its government customers. Its moat protects it from the minnows and leaves it exposed to the whales and the regulators.

The activist stress test — what a short-seller would press. It is a useful discipline to argue the other side deliberately, and a skeptical long/short investor would build a pointed case. Start with disclosure and complexity: Centene operates across dozens of state subsidiaries, three regulated segments, and a web of intercompany arrangements, and the segment revenue figures the company reports are premium-and-service revenue, not the full GAAP top line — a distinction that can flatter or obscure depending on how it's presented. Push on the goodwill: a $6.7 billion write-down is management's own admission that capital deployed under the prior regime destroyed value, and there is no guarantee the remaining goodwill on the books is fully clean. Push on leverage: the company carries meaningful debt maturities in December 2027 and the summer of 2028 that will likely be refinanced at higher rates than the notes they replace, a headwind management acknowledged directly on the Q1 2026 call.3 Push on earnings quality: adjusted EPS excludes exactly the kind of charges — impairments, amortization, "one-time" items — that in a serial acquirer are arguably recurring features of the business, not aberrations. And push on the core: if Medicaid margins are structurally set by state budgets and the marketplace depends on federal subsidies Congress can revoke, then what, exactly, is the durable earnings power an investor is underwriting? None of these points are disqualifying, and management has credible answers to several. But an investor who cannot articulate the bear's strongest case has not done the work.

The credibility test — Sarah London's incentives and record. For a turnaround story, management credibility is not a soft factor; it is the investment thesis. On paper, London's incentives are aligned: her 2025 total compensation of roughly $19.5 million was heavily performance-weighted, with only a small fraction — a base salary of about $1.47 million — fixed and the overwhelming majority delivered as at-risk equity and bonus tied to results.5 Her capital-allocation record since 2022 backs the alignment with behavior: rechanneling more than $5 billion of divestiture proceeds into share buybacks and debt paydown rather than the dilutive acquisitions of the prior era is exactly the discipline the activists demanded, and it is the kind of behavior — promises of discipline actually matched by action — that builds credibility over time.3 The counterweight a skeptic would press: London still presided over the 2025 guidance withdrawal and the $6.7 billion write-down, and while much of that inheritance predates her, a genuinely in-control management team is supposed to see a mispriced book before it forces a mid-year guidance pull. The 2026 narrative — concrete trend-management levers, a stated willingness to beat her own targets, a refusal to book uncertain risk-adjustment revenue — reads as more disciplined and more specific than the Neidorff era. Whether it is durably so is the thing the next several quarters will test.

The risk radar — where the case breaks. Three mechanisms deserve an investor's standing attention. First, rate-adequacy lag: the structural time gap between when medical costs rise (the acuity shift, behavioral-health inflation, specialty-drug trend) and when state regulators actually approve the higher premiums to match. Centene is perpetually front-running its own cost curve, and in any given year the states can simply decline to keep up. Second, federal subsidy and policy risk: the lapsed enhanced Premium Tax Credits directly compress the marketplace, and looming Medicaid work requirements could shrink and re-scramble the core book — this is a company whose addressable market is redrawn by legislation. Third, compliance and concentration risk: Centene's revenue is overwhelmingly government money, which means a single regulatory change, a single adverse RFP cycle in a big state, or a single Envolve-style enforcement action can vaporize billions in value with no warning. These are not macro abstractions; they are the specific, business-model-level ways the story ends badly.

The bull case, stated fairly. The portfolio cleanup is essentially complete; the non-core international and adjacent assets are gone and the balance sheet has been scrubbed of its M&A premium. Star Ratings are recovering on schedule, restoring lost Medicare bonus money. The Express Scripts arrangement locks in structural pharmacy savings and removes the compliance albatross. And Ambetter, for all its 2025 volatility, remains a structurally advantaged, market-leading asset whose narrow-network cost position rivals cannot easily match. In this reading, 2025 was the kitchen-sink year, and a leaner, more disciplined Centene emerges into a multi-year margin-recovery runway.

The bear case, stated just as fairly. Medicaid enrollment is structurally shrinking in the post-pandemic, work-requirement world, and the core Medicaid margin is permanently capped by the budgets of cash-strapped states. Medical costs — behavioral health, home health, specialty drugs — are inflating faster than the rate-setting process can accommodate. The marketplace's profitability just proved it can be wiped out by a single mispriced year, and its size depends on a federal subsidy Congress has already let expire. In this reading, Centene is a low-margin, politically exposed utility whose good years are capped and whose bad years are unbounded, dressed up as a turnaround.

The most useful thing an investor can do is ignore the noise and watch a very small number of things. First, the Medicaid HBR — the single clearest gauge of whether rate negotiations are catching up to member acuity; every quarter it grinds down from 93% toward the high-80s is a quarter the core is healing, and every quarter it doesn't is the bear case confirming itself. Second, the marketplace pretax margin and membership — the test of whether Ambetter's structural advantage survives the subsidy cliff, and whether the risk-adjustment bet London is making pays off. Third, the Medicare Star Ratings trajectory — the leading indicator of whether the WellCare repair job is truly done or merely paused. Those three numbers, tracked over time, will tell the story that no press release will.

X. Epilogue & Outro

Centene's journey — from Betty Brinn's single-county health plan for welfare mothers to a $195-billion enterprise insuring one in fourteen Americans — is a genuine masterclass in the evolution of healthcare capitalism, and its central lesson is uncomfortable for anyone who prefers their stories morally tidy. Managing the care of low-income, subsidized, and vulnerable Americans is not merely a social mission that happens to lose money. Executed at scale and with discipline, it is one of the most defensible, if lowest-margin, business models in the country — a franchise built on government contracts that competitors cannot easily storm and a population that no one else wanted to serve. Executed without discipline, as the Neidorff endgame and the Envolve scandal showed, that same model breeds unaccountable sprawl, regulatory blowback, and billions in destroyed value.

The final frame is a study in two temperaments. Michael Neidorff built the garden — the local franchises, the national scale, the acquisitive empire — with a founder's vision and an autocrat's control, and both the achievement and the rot were his. Sarah London was handed the shears, and the work of pruning that garden back to something that can actually be tended is still, in the summer of 2026, unfinished. The Medicaid margin is still recovering, not recovered. The marketplace is profitable, but riding a policy cliff. The Medicare repair is progressing, not complete. Whether London's discipline ultimately proves as durable as her predecessor's ambition was relentless is not a question the story has answered yet. It is a question the next several years — and those three numbers — will decide.

References

-

Centene Corporation Reports 2025 Results and Announces 2026 Guidance — PR Newswire / Centene, 2026-02-06 ↩↩↩↩↩↩↩↩

-

Centene Corporation 2025 Annual Report (Form 10-K) — SEC EDGAR, 2026-03-05 ↩

-

Centene Corporation Reports First Quarter 2026 Results — PR Newswire / Centene, 2026-04-28 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

Centene Corporation Withdraws 2025 Guidance — PR Newswire / Centene, 2025-07-01 ↩↩

-

Centene's Highest-Paid Executives in 2025 (Sarah London Compensation) — Becker's Payer, 2026 ↩

-

Centene Sets Aside $1.25B to Resolve State Medicaid Pharmacy Benefit Probes — Healthcare Dive, 2021-06-14 ↩

-

State-by-State Tracker of Centene Medicaid PBM Envolve Settlements — Healthcare Dive, 2022-12-19 ↩

-

AG Paxton Recovers $165.6 Million for Texas Taxpayers in Settlement with Centene — Texas Attorney General, 2022-09-12 ↩

-

Centene Agrees to Pay a Record $88.3 Million to Settle Medicaid Pharmacy Claims — Ohio Attorney General, 2021-06 ↩

-

Centene and Politan Capital Management Enter into Cooperation Agreement — SEC Schedule 13D/A Filing, 2021-12-14 ↩↩

-

Michael Neidorff, Who Built Centene into a Healthcare Giant, Dies at 79 — St. Louis Post-Dispatch, 2022-04-07 ↩↩↩↩↩↩

-

Centene Completes Acquisition of WellCare, Creating a Leading Healthcare Enterprise — Centene Investor Relations, 2020-01-23 ↩↩

-

Centene Completes Transaction with Fidelis Care — Centene Investor Relations, 2018-07-02 ↩

-

Centene's $2.2B Deal for Magellan Adds Focus on Behavioral Health — Healthcare Dive, 2021-01-04 ↩

-

Centene Completes Divestiture of UK's Circle Health Group for $1.2B — Reuters, 2024-01-18 ↩

-

Centene Corporation Company History — Centene Corporation ↩↩↩

-

The Enhanced Premium Tax Credit Expiration: Analysis and Effects — Congressional Research Service (congress.gov), 2025 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube