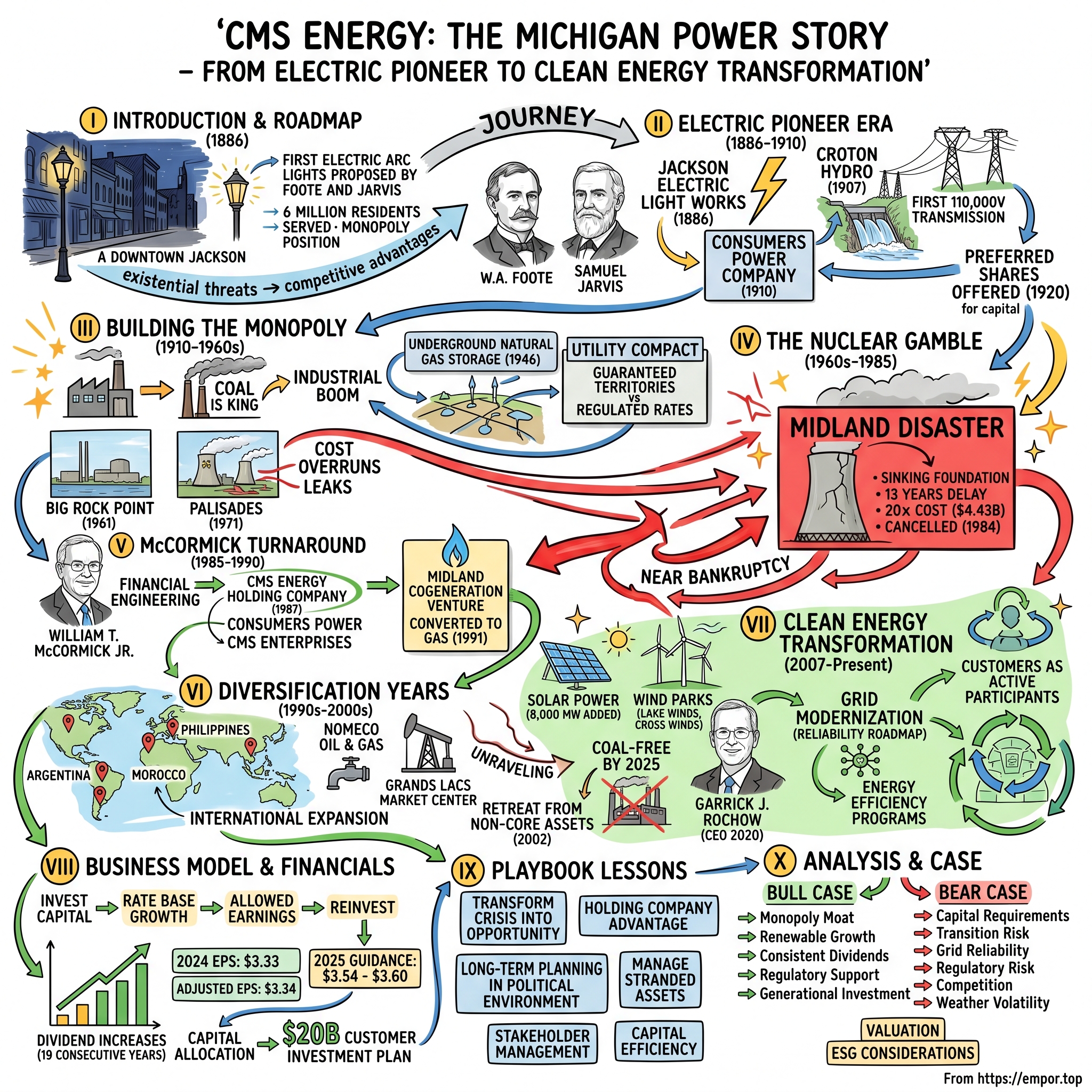

CMS Energy: The Michigan Power Story - From Electric Pioneer to Clean Energy Transformation

I. Introduction & Episode Roadmap

Picture downtown Jackson, Michigan on a cold winter evening in 1886. The streets are dark, lit only by flickering gas lamps and the occasional kerosene lantern. Two men—William Augustine Foote and Samuel Jarvis—stand before city officials with an audacious proposal: illuminate the entire downtown with electric arc lights, a technology so new that most Americans have never seen one. The officials are skeptical. Electric light? In Jackson? But Foote, a local businessman with an engineer's mind, persists. Within months, Jackson's streets blaze with artificial daylight, and the seeds of what would become Michigan's energy backbone are planted.

Today, CMS Energy serves over 6 million of Michigan's 10 million residents—a monopoly position built over 138 years of consolidation, crisis, and reinvention. The company just reported 2024 earnings per share of $3.33, up from $3.01 in 2023, with adjusted EPS hitting $3.34. Behind these steady numbers lies one of American business's most dramatic turnaround stories: a company that nearly collapsed under a nuclear disaster, restructured through financial engineering, and now leads Michigan's $75 billion clean energy transformation.

The central question driving this narrative isn't just how a 19th-century lighting company survived into the 21st century—it's how CMS Energy repeatedly transformed existential threats into competitive advantages. From the Midland nuclear catastrophe that brought the company within days of bankruptcy to today's aggressive pivot toward renewables, this is a story of institutional resilience rarely seen in American utilities.

Four major themes define CMS Energy's arc: the relentless consolidation that created Michigan's utility monopoly, the nuclear gamble that nearly destroyed everything, the holding company restructuring that saved the firm, and the ongoing renewable transition that will determine its next century. Each transformation required not just capital and technology, but a fundamental rethinking of what a utility could be. The updated financial performance reflects CMS Energy's reported earnings per share of $3.33 for 2024, compared to $3.01 for 2023, with adjusted earnings per share of $3.34 versus $3.11 in 2023. The company has also increased its annual dividend by 11 cents per share to $2.17 for 2025, marking the 19th consecutive year of dividend increases, while raising 2025 adjusted earnings guidance to $3.54 to $3.60 per share and reaffirming long-term adjusted EPS growth of 6 to 8 percent, with continued confidence toward the high end.

What makes CMS Energy particularly fascinating for investors is how its monopoly position—often seen as a regulatory burden—has become the foundation for one of America's most ambitious utility transformations. While tech companies grab headlines for disruption, CMS Energy is quietly executing a $75 billion infrastructure overhaul that will reshape how 6 million Michiganders consume energy. The story that follows traces this evolution from gas lamps to smart grids, from near-bankruptcy to billion-dollar capital programs, from coal dependency to renewable leadership.

II. The Electric Pioneer Era: W.A. Foote's Vision (1886-1910)

The transformation began in a flour mill in Adrian, Michigan, in 1884. William Augustine Foote had agreed to have an electric generator installed in his flour mill, which spawned his fascination with electricity and started him tinkering with the idea of electrically-powered streetlights. This wasn't just technological curiosity—Foote saw electricity as a force that could fundamentally reshape Michigan's economy.

On the pivotal day in 1886, William A. Foote and Samuel Jarvis secured their first franchise from the City of Jackson to illuminate a dozen streetlights, though they had to sell the concept of electric streetlights to skeptical city officials. Foote was a flour mill operator from Adrian and Jarvis a foreman at an iron and engine works in Lansing—practical men with engineering minds, not Wall Street financiers. Their partnership would prove transformative.

The company was founded in 1886 as Jackson Electric Light Works by William A. Foote, Samuel Jarvis, of Lansing, and his brother James B. Foote, who was originally tasked to install electric lighting in downtown Jackson. The brothers weren't content with just lighting streets. They envisioned something far grander: an interconnected electric system powered by Michigan's rivers that would link communities and farms statewide.

The early years were marked by relentless acquisition and technical innovation. After a series of acquisitions and mergers involving other local electric, gas, and trolley companies which were properties of W.A. Foote, as well as Anton G. Hodenpyl and Henry D. Walbridge, the company incorporated as Consumers Power Company in 1910 in Maine. This Maine incorporation—a common practice for utilities seeking favorable corporate laws—marked the company's transition from local operator to regional powerhouse.

But the real breakthrough came with hydroelectric power. In 1907, Croton Hydro on the Muskegon River began operating and later became the first facility in the world to transmit electricity at more than 110,000 volts. Think about that achievement: while Thomas Edison and George Westinghouse were fighting the "War of Currents" in New York, Foote was quietly setting world records for electrical transmission in Michigan. This wasn't just technical prowess—it was strategic genius. High-voltage transmission meant Foote could build massive generating stations on remote rivers and deliver power to cities hundreds of miles away.

In 1920, Foote and Jarvis offered preferred shares of their company to the public to secure sufficient financing to enter other energy and power generation sectors. This early embrace of capital markets would become a defining characteristic of the company—using public financing to fund aggressive expansion while maintaining operational control.

The consolidation strategy was methodical. Rather than competing with dozens of local utilities, Foote systematically acquired them, integrating their assets and customers into an ever-expanding network. It became part of the utility holding conglomerate Commonwealth & Southern Corporation, which held utilities in 10 other states. This holding company structure provided access to capital and expertise while preserving local management autonomy—a model that would serve the company well for decades.

By 1910, the pieces were in place: a unified company with a monopoly franchise, access to capital markets, breakthrough transmission technology, and a vision for electrifying all of Michigan. What started as twelve streetlights in Jackson had become the foundation of Michigan's energy infrastructure. The entrepreneurial phase was ending; the era of industrial-scale utility operations was about to begin.

III. Building the Michigan Utility Monopoly (1910-1960s)

The transformation from a collection of local electric companies to Michigan's dominant utility monopoly required more than just acquisitions—it demanded a complete reimagining of what infrastructure could accomplish. The 1920s saw Consumers Power systematically expanding across Michigan's Lower Peninsula, leveraging their 1920 public share offering to finance an unprecedented building spree. The strategy was simple but audacious: build generating capacity ahead of demand, then create the demand through aggressive marketing and new industrial partnerships.

In 1946, the company formed a strategic partnership with Panhandle Company to convert former natural gas fields to underground natural gas storage areas. This move exemplified the company's evolving sophistication—they weren't just generating power anymore, they were creating an integrated energy system that could store, distribute, and balance multiple fuel sources. The underground storage facilities gave Consumers Power a crucial advantage: the ability to buy gas cheap in summer, store it underground, and sell it during peak winter demand.

The post-World War II era brought an industrial boom that transformed Michigan into America's manufacturing heartland. Detroit's auto plants ran three shifts. Factories sprouting across the state demanded reliable, massive amounts of power. Coal became king. The demonstration of pulverized coal steam generators at the Oneida Street Station in Wisconsin in 1919 vastly improved coal combustion, allowing for bigger boilers. In the 1920s, another technological boost came with the advent of once-through boiler applications and reheat steam power plants, along with the Benson steam generator, which was built in 1927. Reheat steam turbines became the norm in the 1930s, when unit ratings soared to a 300-MW output level.

By the 1950s, Consumers Power had embraced coal with religious fervor. Main steam temperatures consistently increased through the 1940s, and the decade also ushered in the first attempts to clean flue gas with dust removal. The 1950s and 1960s were characterized by more technical achievements to improve efficiency—including construction of the first once-through steam generator with a supercritical main steam pressure. Unit ratings of 1,300 MW were reached by the 1970s. These weren't just power plants—they were monuments to industrial might, each turbine capable of powering entire cities.

The regulatory framework that emerged during this period created what economists call the "utility compact": guaranteed monopoly service territories in exchange for regulated rates and universal service obligations. Michigan's Public Service Commission, established in 1939, became the arbiter of this compact. Rate cases became elaborate theatrical productions where utilities demonstrated their capital investments deserved fair returns while consumer advocates argued for lower rates. The system worked because everyone understood the rules: utilities built infrastructure, regulators approved reasonable returns, and customers received reliable power at stable prices.

Commonwealth & Southern Corporation's dissolution in 1946 left Consumers Power as an independent company for the first time since 1910. Rather than weakening the company, independence unleashed aggressive expansion. From 1950 to 1975, Consumers Power's electric customers increased by 80 percent, while natural gas customers increased by more than 100 percent. The company added 19 generating units during this period, a construction pace that would be unthinkable today.

The infrastructure built during this era wasn't just about megawatts—it was about creating an energy system so reliable and ubiquitous that electricity became as essential as water. Every new subdivision got power lines. Every factory could count on uninterrupted service. The grid became invisible precisely because it never failed. This reliability bred complacency, a dangerous mindset as the company prepared to make its biggest gamble yet: nuclear power.

IV. The Nuclear Gamble: From Big Rock to Midland Disaster (1960s-1985)

The story begins not with catastrophe but with optimism—the kind of blind faith in technology that characterized post-war America. CMS Energy's primary subsidiary, Consumers Energy, announced Michigan's first nuclear power plant in 1961, Big Rock Point in Charlevoix, Michigan. This 75-megawatt facility seemed like a triumph of the atomic age, promising electricity "too cheap to meter." Reality proved crueler. Big Rock operated for 35 years but never lived up to its economic promises, plagued by maintenance issues and cost overruns that foreshadowed the disaster to come.

Undeterred by Big Rock's mediocre performance, Consumers Power doubled down. The company announced another nuclear plant, Palisades Nuclear Generating Station on Lake Michigan, which first produced electricity in December, 1971 to serve 400,000 people a day. Palisades cost five times its original budget and suffered from radiation leaks that would later trigger federal investigations and civil fines. Yet even as Palisades struggled, Consumers Power was already committed to its biggest nuclear gamble yet.

Consumers Power Company and Dow Chemical Company first announced their intentions to build the world's first dual-purpose industrial nuclear power plant in December 1967. The plant was to be built on the banks of the Titabawasee River and cost an estimated $300 million and be completed by 1975. The Midland project represented everything wrong with the nuclear industry's hubris: unprecedented technology, aggressive timelines, and a fundamental misunderstanding of regulatory complexity.

The construction site became a comedy of errors that would have been funny if it weren't so expensive. Consumers Power abandoned the project, which was 85% complete, in 1984 citing numerous construction problems, most notably a sinking foundation. These problems included sinking and cracking of some buildings on the site due to poor soil compaction prior to construction, as well as shifting regulatory requirements. Workers later revealed that quality control tests had been falsified, negative results ignored, and improper procedures followed systematically.

With the Three Mile Island incident in 1979, the public awareness increased and the Nuclear Regulatory Council's (NRC) safety standards were toughened. Improperly compacted soils caused several buildings to settle too much and prompted more investigations by the NRC in 1981. After the investigations Consumers Power was fined $38,000 for 13 violations of quality assurance regulations and fined again in 1983 for $120,000 for additional violations. In 1983 the total cost of the plant had reached $4.43 billion.

The relationship with Dow Chemical, initially the project's anchor customer, deteriorated as delays mounted. Consumers Power's relationship with Dow Chemical Company was strained from the point it was clear that the plant would not be finished on time, around 1976. In 1983 Dow Chemical backed out of the contact to build the plant. Then in July 1984 Consumers Power officially halted construction in Midland due to lack of funds, state support, and public support.

The directors of Consumers Power Company announced the cancellation of the Midland nuclear plant on July 16th, 1984; making it the most costly power plan ever abandoned in the United States. The plant was 85% complete, 13 years behind schedule and over 20 times the original cost estimate. Think about that multiplier: a $300 million project had ballooned to over $4 billion with nothing to show for it.

The financial implications were catastrophic. Selby said the utility, the 10th largest in the nation, plans to ask the Public Service Commission for reimbursement from ratepayers for the nearly $4 billion it has spent on the plant. But that will almost certainly spark a struggle with Midland opponents. Michigan Attorney General Frank Kelley led the fight against allowing Consumers Power to pass these costs to ratepayers, arguing that customers shouldn't pay for management incompetence.

By late 1984, Consumers Power teetered on the edge of bankruptcy. Bond ratings plummeted to junk status. The stock price collapsed. Major industrial customers threatened to leave the state rather than pay for the Midland debacle. The company that had powered Michigan's industrial rise now threatened to drag the state's economy down with it. Something radical had to be done, and it would require leadership unlike anything the utility industry had seen before.

V. The McCormick Turnaround: Creating CMS Energy (1985-1990)

In November 1985, with Consumers Power on the brink of collapse, the board hired William T. McCormick Jr., a nuclear physicist with a doctorate from MIT who had been chairman and CEO of American Natural Resources Company and executive vice president of The Coastal Corporation. McCormick wasn't a utility insider—he was an energy dealmaker who understood both the technical and financial sides of the business. His mandate was simple: save the company or liquidate it.

McCormick's first weeks revealed the depth of the crisis. Bond holders were demanding immediate payment. Industrial customers were threatening to build their own power plants rather than subsidize Midland's losses. The Michigan Public Service Commission was hostile to any rate increases. Wall Street had written the company off. McCormick later recalled walking through the abandoned Midland site—$4 billion worth of concrete and steel sitting useless—and thinking, "There has to be a way to salvage something from this disaster."

The solution came from an unlikely source: the 1978 Public Utility Regulatory Policies Act (PURPA), which allowed independent power producers to sell electricity to utilities at "avoided cost" rates. McCormick realized that if he could convert Midland from a regulated nuclear asset to an unregulated gas-fired cogeneration facility, he could escape the regulatory trap that prevented cost recovery. It was financial engineering at its most creative—turning a liability into an asset through regulatory arbitrage.

In 1987, CMS Energy was formed as a holding company with its principal subsidiaries as Consumers Power and CMS Enterprises. This restructuring wasn't just corporate housekeeping—it was a fundamental reimagining of what a utility could be. The holding company structure allowed McCormick to separate regulated utility operations from unregulated ventures, creating financial flexibility that would prove crucial.

On October 23, 1987, CMS Energy became a publicly owned company and was listed at the New York Stock Exchange. The timing seemed terrible—it was Black Monday, when the Dow Jones dropped 22% in a single day. Yet McCormick pressed forward, arguing that the market chaos actually helped by lowering investor expectations and allowing CMS to price its offering attractively.

The Midland conversion became McCormick's signature achievement. By 1984, Dow and Consumers Power were suing each other over the nuclear plant, but McCormick negotiated a settlement that made Dow a partner in the conversion. The Midland Cogeneration Venture transformed the abandoned nuclear plant into what would become, when it began operation in 1991, the world's largest gas-fired steam recovery power plant. Conversion of the plant began in 1986 and was completed at a cost of $500 million, almost twice the original estimate of the nuclear facility—but still a fraction of the $4 billion already spent.

In October 1990, CMS Energy took a $657.2 million pretax charge to write off Midland losses. This massive write-down, painful as it was, finally cleared the books of the nuclear disaster's legacy. McCormick had successfully separated the past from the future, allowing investors to evaluate CMS Energy on its forward prospects rather than its historical mistakes.

The financial engineering extended beyond Midland. McCormick created CMS Generation in 1986, one of the first independent power production companies in the United States. This subsidiary would build and operate power plants outside Michigan, selling electricity in competitive markets rather than through regulated rates. It was a radical departure from the traditional utility model, but McCormick saw that deregulation was coming and positioned CMS to profit from it.

By 1990, CMS Energy had stabilized financially, with investment-grade bond ratings restored and a clear strategic direction. The stock price had tripled from its 1987 IPO levels. Michigan regulators, initially skeptical of McCormick's financial maneuvers, had come to appreciate that he'd saved thousands of jobs and preserved the state's energy infrastructure. The Midland Cogeneration Venture produced 1,370 megawatts of electricity and 1.35 million pounds of steam per hour for Dow Chemical, turning the nuclear white elephant into a productive asset.

McCormick's turnaround playbook would become a template for utility restructuring across America: create a holding company structure, separate regulated from unregulated assets, use financial engineering to monetize stranded costs, and position for deregulation. But McCormick wasn't done. Having saved CMS from bankruptcy, he now wanted to transform it into a global energy company.

VI. The Diversification Years: Independent Power & International Expansion (1990s-2000s)

The 1990s dawned with McCormick's vision clear: transform CMS Energy from a Michigan utility into a global energy conglomerate. Deregulation was sweeping through energy markets worldwide, and McCormick believed the future belonged to companies that could operate across borders and fuel types. In 1994, CMS entered this market on a large scale, founding new joint projects in Argentina, the Philippines, India, and Morocco. Revenues doubled from the previous year and, even more importantly, high rates of return meant that net income from these operations quadrupled from 1993.

The international expansion strategy seemed brilliant on paper. CMS Gas Argentina Company invested in Transportadora de Gas del Norte S.A., providing natural gas transmission services to the northern and central parts of Argentina. In Morocco, CMS partnered on power generation projects aimed at the country's industrialization push. The Philippines ventures capitalized on that nation's desperate need for reliable electricity. Each project promised returns far exceeding what Michigan's regulated rates could deliver.

In 1997, Consumers Power was rebranded as Consumers Energy. The name change signaled more than marketing—it reflected McCormick's belief that the company was no longer just about power generation but about comprehensive energy solutions. The firm was one of the first companies to introduce an online billing system in the late 1990s, a seemingly minor innovation that actually represented a fundamental shift in how utilities thought about customer relationships.

The oil and gas ventures through NOMECO (originally Nomeco Oil and Gas Company) expanded aggressively. By the early 1990s the subsidiary had producing wells in the United States, Australia, Colombia, Equatorial Guinea, and New Zealand with proven reserves of 60 million net equivalent barrels and almost 100 employees. By 1995 proven reserves had almost doubled to 113 million barrels, and revenue from Nomeco was close to $90 million. This wasn't just diversification—it was vertical integration, controlling the fuel supply chain from wellhead to power plant.

In 1994, CMS created Grands Lacs Market Center in St. Clair, which became a major storage and exchange point for US and Canada natural gas markets. This facility exemplified McCormick's strategy: position CMS at critical infrastructure chokepoints where the company could profit from energy flows regardless of who produced or consumed it. The facility could store billions of cubic feet of natural gas and became one of North America's most important gas trading hubs.

But the international adventures began unraveling almost as quickly as they were assembled. The Argentine investments, initially so promising, became a nightmare when that country's economic crisis hit in the late 1990s. In January 2000 and again in July 2000, the representatives of the gas companies agreed, subject to certain conditions, to defer the adjustment of the gas tariffs. When Argentina abandoned its currency peg to the dollar and defaulted on its debt, CMS found itself embroiled in international arbitration that would drag on for years.

The 2006 sale of Palisades plant to Entergy for $380 million marked a symbolic turning point. CMS was retreating from nuclear power entirely, selling the plant that had once represented its atomic ambitions. The sale price, while substantial, was a fraction of what the company had invested in nuclear technology over the decades. It was an admission that the nuclear dream was dead.

In 2001, the firm entered into an exploration agreement with Eritrea for oil exploration in the Dismin Block of the Red Sea. This venture, in one of the world's most politically unstable regions, epitomized the late-stage desperation of the international strategy. By 2002, McCormick's expansionist vision had collided with reality. Round-trip trading scandals at CMS Marketing, Services and Trading—where the company engaged in simultaneous purchases and sales of power at identical prices to inflate revenue figures—led to SEC investigations and McCormick's resignation in May 2002.

The diversification years left a mixed legacy. On one hand, CMS Energy had successfully transformed from a pure Michigan utility into a company with multiple revenue streams and geographic exposure. The company had developed expertise in independent power production, gas trading, and international project development that few utilities could match. On the other hand, many international ventures lost money, distracted management, and ultimately had to be unwound at significant cost.

By the mid-2000s, new management began systematically selling off non-core assets and refocusing on Michigan. The international ventures were sold or written off. NOMECO was wound down. The trading operations were shuttered. What remained was essentially what had always been there: Consumers Energy, serving Michigan customers with electricity and natural gas. The globe-trotting energy conglomerate dream was over. It was time to return to basics—and prepare for the next transformation.

VII. The Clean Energy Transformation (2007-Present)

In 2007, the company announced plans to invest $6 billion in Michigan's energy future to support new power plant technology and identify new energy sources. This wasn't just another capital program—it was the beginning of a fundamental reimagining of what a Midwest utility could be in the 21st century. The coal plants that had powered Michigan's industrial rise were becoming liabilities, both financially and environmentally.

The transformation accelerated dramatically in June 2019 when Michigan regulators approved Consumers Energy's Clean Energy Plan. Consumers Energy today received approval from state regulators for its Clean Energy Plan, ushering in a new era for renewable energy in Michigan. The Clean Energy Plan puts Consumers Energy on a path to eliminate coal; reduce carbon emissions by over 90 percent; and meet customers' future electricity capacity needs with 90 percent clean energy resources by 2040.

Then came the bombshell announcement in June 2021. Consumers Energy today announced a sweeping proposal to stop using coal as a fuel source for electricity by 2025—15 years faster than currently planned. The plan would make the company one of the first in the nation to go coal-free and provide a 20-year blueprint to meet Michigan's energy needs while protecting the environment for future generations. "We are proud to lead Michigan's clean energy transformation and be one of the first utilities in the country to end coal use," President and CEO Garrick Rochow said.

The numbers behind this transition are staggering. The rapid transition to clean, renewable sources includes the addition of nearly 8,000 megawatts of solar power. To put that in perspective, 8,000 MW of solar represents more generation capacity than the company's entire coal fleet at its peak. This isn't incremental change—it's wholesale transformation of the generation portfolio.

The retirement schedule reads like a dismantling of the 20th century's energy infrastructure. If approved by the Michigan Public Service Commission, the updated plan would speed closure of our three coal-fired units at the Campbell generating complex near Holland. Campbell 1 and 2, collectively capable of producing more than 600 megawatts of electricity, would retire in 2025—roughly six years sooner than their scheduled design lives. Campbell 3, capable of generating 840 MW, would also retire in 2025—roughly 15 years sooner than its scheduled design life. The updated proposal also calls for moving up closure of Karn 3 and 4, units that run on natural gas and fuel oil and can generate more than 1,100 MW to meet peak demand, to 2023—about eight years sooner than their design lives. In December 2020, Garrick J. Rochow became President & CEO, marking a new chapter in the clean energy transformation. Rochow, 46, has been with CMS Energy for 17 years, with over 20 years of industry experience, and has held his current position since July 2016. Unlike the financial engineers who led the company through crisis in the 1980s, Rochow is an operations executive with an environmental engineering degree from Michigan Technological University—the perfect background for executing a massive infrastructure transformation.

The wind energy expansion exemplifies the scale of change. Lake Winds Energy Park, a 100-megawatt project, began operating in late 2012. Cross Winds Energy Park in Michigan's Tuscola County opened in 2014, with General Electric supplying 62 1.79-kilowatt wind turbine engines for the project which has a total generating capacity of 105 megawatts. These aren't demonstration projects—they're industrial-scale renewable facilities that can power entire counties.

But wind and solar alone can't solve the intermittency challenge—what happens when the wind doesn't blow and the sun doesn't shine? The company's approach combines multiple strategies. Our plan creates price stability and, by using natural gas as a fuel source to generate baseload power, will save customers about $650 million through 2040 compared to our current plan. Natural gas becomes the bridge fuel, providing reliable backup when renewables can't meet demand.

The Grid modernization component is equally ambitious. The Reliability Roadmap aims to reduce outages through smart grid technology, automated switching, and predictive maintenance. In 2024, the company's highlights include record investments in our electric grid through the Reliability Roadmap, restoring power to over 93% of customers in less than 24 hours—compared to 87% in 2023. This isn't just about keeping the lights on—it's about creating a grid flexible enough to handle two-way power flows from distributed solar, electric vehicle charging, and battery storage.

The financial engineering behind this transformation is as sophisticated as McCormick's restructuring in the 1980s. 2022 CapEx was $2.4 billion total, with only $113 million (5%) in low-carbon generation. But plans call for increasing capital expenditure to $3.1 billion between 2023-2027, with 20% dedicated to clean energy. This represents a quadrupling of clean energy investment while maintaining total capital discipline—a balancing act that requires careful regulatory management.

The company's energy efficiency programs already have helped customers save $2 billion since 2009. Tools such as energy efficiency and demand response and grid optimization will take on a more significant role in our generation portfolio as we retire coal plants. We will help customers lower their energy use by 2 percent per year going forward, which is one of the most aggressive energy efficiency investments anywhere in the country.

Managing the intermittency challenge requires more than just technical solutions—it demands a fundamental rethinking of the utility-customer relationship. Customers can participate in programs to reduce energy waste, shift energy use to more affordable times, invest in charging infrastructure for electric vehicles and support new renewable energy sources. Time-of-use rates, demand response programs, and distributed energy resources turn customers from passive consumers into active grid participants.

The regulatory environment has transformed from adversary to ally. Michigan's Clean, Renewable, and Efficient Energy Act, passed in 2008 and strengthened since, provides a framework for cost recovery on renewable investments. The Michigan Public Service Commission, once skeptical of utility plans, now actively supports the clean energy transition, understanding that Michigan's economic competitiveness depends on sustainable, reliable power.

Yet challenges remain massive. The rapid transition to clean, renewable sources includes the addition of nearly 8,000 megawatts of solar power—but Michigan isn't Arizona. Winter cloud cover, short days, and snow accumulation create capacity factors far below southwestern utilities. The economics work only with continued technology improvements, federal tax credits, and creative financing structures. The transformation continues, but success is far from guaranteed.

VIII. Business Model & Financial Performance

The regulated utility model that nearly destroyed CMS Energy in the 1980s has become its greatest strength in the 2020s. The fundamental equation remains unchanged: invest capital in infrastructure, earn a regulated return, repeat. But the scale and sophistication of execution have transformed dramatically. CMS Energy increased its annual dividend by 11 cents per share to $2.17 for 2025, the 19th increase in as many years. CMS Energy raised its 2025 adjusted earnings guidance to $3.54 to $3.60 from $3.52 to $3.58 per share and reaffirmed long-term adjusted EPS growth of 6 to 8 percent, with continued confidence toward the high end.

The capital allocation strategy reflects a careful balance between growth investment and shareholder returns. A significant component of CMS Energy's strategy involves its updated $20 billion customer investment plan, which represents a $3 billion increase from its previous capital expenditure outlook. This plan is expected to drive rate base growth from $26.2 billion in 2024 to $39.4 billion by 2029, representing an 8.5% annual growth rate. This isn't just maintenance capital—it's transformative investment that fundamentally changes the company's asset mix and earning power.

The rate case process, once an adversarial battle, has evolved into a more collaborative negotiation. The Michigan Public Service Commission today approved a $153,809,000 increase in revenue for Consumers Energy Co., authorizing a number of investments aimed at reducing power outages and making the utility's electric grid more reliable and resilient (Case No. U-21585). Today's order represents a more than 52% reduction from the amount Consumers had sought: a combined $325 million, with $303 million through rates and $22 million in a separate 12-month surcharge for distribution deferral. The Commission authorized a return on common equity of 9.9% and a capital structure of 50% equity and 50% debt. The utility had sought a return on common equity of 10.25% and a capital structure of 49.25% debt to 50.75% equity.

This regulatory decision illustrates the delicate dance between utility needs and consumer protection. A 9.9% allowed return on equity might seem generous in today's low-rate environment, but it's actually below the national average for utilities and reflects Michigan regulators' focus on affordability. The 50/50 debt-equity capital structure requirement ensures financial stability while limiting leverage—a lesson learned from the Midland disaster.

The dividend strategy deserves particular attention. The company also expects consistent dividend growth, targeting a payout ratio of approximately 60% over time. For 2025, the annual dividend per share is set at $2.17, an increase of 11 cents from the previous year. This represents a $2.17 annualized dividend and a yield of 3.0%. CMS Energy's payout ratio is presently 64.20%. This disciplined payout ratio leaves substantial retained earnings for growth investment while providing predictable income to shareholders—a balance that attracts both income and growth investors.

The financial engineering extends to tax optimization. The following is an allocation of the 2022 common stock dividends for United States federal income tax purposes, showing some dividends treated as return of capital rather than ordinary income. This tax-efficient dividend structure reduces the tax burden on shareholders, effectively increasing after-tax returns without affecting the company's cash flow.

The ability of CMS Energy to pay (i) dividends on its capital stock and (ii) its indebtedness, and other obligations and liabilities, depends and will depend substantially upon timely receipt of sufficient dividends or other distributions from its subsidiaries, in particular Consumers and NorthStar. Each of Consumers' and NorthStar's ability to pay dividends on its common stock depends upon its revenues, earnings and other factors. Consumers' revenues and earnings will depend substantially upon rates authorized by the Michigan Public Service Commission. This dependency chain—from regulated rates to utility earnings to holding company dividends—creates both stability and vulnerability.

The renewable transition introduces new financial complexities. Solar and wind projects require massive upfront capital but have minimal operating costs. This shifts the utility's cost structure from variable (fuel) to fixed (capital recovery), potentially increasing earnings volatility during economic downturns when electricity demand falls. The company addresses this through various regulatory mechanisms including decoupling (separating revenue from sales volume) and tracker mechanisms for renewable investments.

CMS Energy also highlighted its preparedness for potential challenges, noting that approximately 90% of its supply chain is domestically sourced with broad vendor redundancy, and 95-100% of its gas supply is domestically sourced. The company emphasized that it has manageable inflationary impacts and is not dependent on imported electricity, positioning it well to navigate the current operating environment. This supply chain resilience, built after pandemic-era disruptions, provides operational stability that translates to financial predictability.

The long-term financial outlook depends critically on regulatory relationships. Utility regulation in Michigan has improved since landmark reforms in 2008 and 2016. Support from policymakers and regulators is critical to producing earnings and dividend growth. CMS' large investment growth plan raises regulatory and project execution risk. Michigan's political environment—a purple state with both environmental advocates and industrial interests—requires careful navigation. The company must balance green ambitions with blue-collar job concerns, renewable mandates with reliability requirements.

The business model's elegance lies in its self-reinforcing nature: capital investment drives rate base growth, which increases allowed earnings, which funds more investment. As long as regulators approve reasonable returns and customers can afford rate increases, this virtuous cycle continues. But it's a high-wire act—one major regulatory denial or customer revolt could unravel the entire strategy.

IX. Playbook: Lessons in Utility Management

The CMS Energy story offers a masterclass in crisis management, strategic pivoting, and long-term value creation that extends far beyond the utility sector. Each major inflection point in the company's history provides lessons that remain relevant for today's executives facing disruption.

Crisis Management: From Near-Bankruptcy to Stability

The Midland nuclear disaster teaches that sunk costs are truly sunk. When Consumers Power had invested $4 billion in a project that was 85% complete, conventional wisdom suggested finishing it at any cost. McCormick's genius was recognizing that the remaining 15% might cost more than starting over. His decision to abandon the nuclear plant and convert it to gas cogeneration seemed radical, but it saved the company. The lesson: when facing existential crisis, radical solutions often beat incremental fixes.

The crisis also demonstrated the power of regulatory arbitrage. By converting Midland from a regulated nuclear asset (where cost recovery was blocked) to an unregulated cogeneration facility (where market prices applied), McCormick escaped an impossible situation. Today's executives should similarly look for regulatory seams and market structure changes that can transform stranded assets into productive investments.

The Holding Company Advantage

Creating CMS Energy as a holding company above Consumers Power wasn't just corporate restructuring—it was strategic architecture. The holding company structure provided financial flexibility to pursue unregulated ventures while protecting the regulated utility from their risks. When international ventures failed in the 2000s, the utility operations remained insulated. This structural separation allowed different parts of the business to operate under different risk profiles and return expectations.

The structure also enabled creative financing. The holding company could issue debt backed by utility dividends, while the utility maintained its own credit rating and borrowing capacity. This dual-track financing reduced overall cost of capital while maintaining financial flexibility. Modern conglomerates should note how structural design can create option value beyond simple diversification.

Long-term Planning in a Political Environment

Utilities operate on 40-year asset lives in 2-year political cycles. CMS Energy's approach—maintaining consistent strategy across multiple CEOs and political administrations—shows how to manage this temporal mismatch. The Clean Energy Plan, developed under one administration and governor, survived political transitions because it addressed concerns across the political spectrum: jobs for unions, reliability for businesses, and environmental progress for activists.

The company's regulatory strategy evolved from confrontation to collaboration. Rather than fighting every rate case decision, CMS Energy began proposing comprehensive settlements that gave all parties something they wanted. Regulators got reliability improvements, consumer advocates got efficiency programs, environmentalists got renewable investments. This "grand bargain" approach reduced regulatory risk and accelerated cost recovery.

Managing Stranded Assets

The nuclear plant retirements and coal plant closures could have created billions in stranded costs. Instead, CMS Energy pioneered creative solutions: selling plants to third parties, converting sites to other uses, and negotiating regulatory settlements that allowed partial cost recovery while avoiding protracted battles. The Palisades sale to Entergy recovered $380 million from an asset many considered worthless.

The coal transition strategy is particularly sophisticated. Rather than fighting environmental regulations, CMS Energy embraced them, accelerating coal retirements to capture federal tax credits and state incentives for renewable replacement. By leading rather than lagging the energy transition, the company turned regulatory compliance from a cost into an opportunity.

The Renewable Transition Economics

CMS Energy's renewable strategy isn't driven by environmental ideology but by economic reality. Solar and wind, with federal tax credits, now offer lower levelized costs than coal operations. But the company didn't bet everything on renewables—natural gas provides the reliability backstop that makes aggressive renewable deployment possible. This "belt and suspenders" approach satisfies both environmental advocates and reliability hawks.

The company's approach to intermittency—combining utility-scale renewables, distributed resources, demand response, and energy efficiency—creates a portfolio effect that reduces risk. No single solution bears the full burden of replacing baseload coal. This diversified approach to the energy transition provides resilience against technology disappointments or policy reversals.

Stakeholder Management

Modern utilities serve multiple masters: regulators, environmentalists, industrial customers, residential consumers, investors, and politicians. CMS Energy's playbook involves sequential coalition building. First, get large industrial customers on board with special rates and reliability guarantees. Then use their political weight to support regulatory approvals. Next, offer consumer advocates efficiency programs and bill assistance. Finally, give environmentalists aggressive renewable targets. Each stakeholder gets enough to support (or at least not oppose) the overall plan.

The company's community engagement around plant closures shows sophisticated stakeholder management. When closing coal plants, CMS Energy doesn't just eliminate jobs—it funds retraining programs, supports local economic development, and often repurposes sites for new economic activity. This approach turns potential opponents into allies and reduces political resistance to necessary changes.

Capital Intensity and Infrastructure Challenge

The $20 billion capital program represents one of the largest infrastructure transformations in Michigan history. Managing projects of this scale requires capabilities most utilities lack: project management expertise, supply chain sophistication, and workforce development. CMS Energy's approach—partnering with established contractors, maintaining vendor diversity, and investing in workforce training—reduces execution risk.

The company treats capital efficiency as seriously as operational efficiency. Every dollar of capital must earn its regulated return, so project selection becomes critical. The company's capital allocation committee, which includes operations, finance, and regulatory executives, ensures investments align with both operational needs and regulatory recovery potential.

The Lesson Synthesis

The CMS Energy playbook ultimately reduces to three principles:

-

Transform Crisis into Opportunity: Every crisis, from Midland to the coal transition, became a catalyst for strategic transformation rather than mere survival.

-

Align Stakeholder Interests: Rather than viewing stakeholders as adversaries, find ways to align their interests with company strategy.

-

Think in Decades, Execute in Quarters: Maintain long-term strategic vision while delivering consistent quarterly results that build credibility.

These lessons apply far beyond utilities. Any capital-intensive, regulated, or politically exposed business can learn from CMS Energy's journey from near-death to industry leadership.

X. Analysis & Investment Case

Bull Case:

The investment thesis for CMS Energy rests on five pillars that create a compelling risk-reward profile for long-term investors. First, the Michigan monopoly position provides an economic moat that Warren Buffett would appreciate. Its principal business is Consumers Energy, a public utility that provides electricity and natural gas to more than 6 million of Michigan's 10 million residents. This isn't just market share—it's an embedded infrastructure position that would take decades and tens of billions to replicate.

Second, the renewable growth trajectory offers both growth and ESG credentials. By 2040, clean, renewable fuel sources such as solar and wind will comprise more than 60 percent of our electric capacity. Combining that growth with advances in energy storage and customer efficiency will allow us to meet customers' needs with 90 percent clean energy resources. The rapid transition to clean, renewable sources includes the addition of nearly 8,000 megawatts of solar power. This massive buildout drives rate base growth while positioning the company as a climate leader.

Third, the dividend track record speaks to financial discipline and shareholder orientation. Nineteen consecutive years of dividend increases through the financial crisis, pandemic, and energy transition demonstrates remarkable consistency. The 60% target payout ratio leaves room for both dividend growth and capital retention, creating a balanced total return proposition.

Fourth, regulatory support has transformed from headwind to tailwind. Michigan's legislative and regulatory framework now actively supports the clean energy transition, with cost recovery mechanisms for renewable investments and grid modernization. The state's 2024 clean energy legislation provides a clear runway for capital deployment with reasonable return expectations.

Fifth, the infrastructure investment opportunity is generational. The combination of grid modernization, renewable buildout, and electrification creates a $20 billion capital program that drives 8.5% annual rate base growth. In a world starved for infrastructure investment opportunities with regulated returns, CMS Energy offers scale, visibility, and regulatory support.

Bear Case:

The bear thesis begins with massive capital requirements that could strain balance sheets and customer affordability. Twenty billion dollars over five years means roughly $4 billion annually—a staggering sum that requires flawless execution and continuous regulatory approval. Any significant disallowance or cost overrun could devastate returns.

The current generation mix poses transition risk that bulls underestimate. Its current energy mix is 36% natural gas, 22% coal, 12% pumped storage, 11% renewables, 10% oil peaking, and 9% nuclear energy. With coal still representing over 20% of generation and gas at 36%, the company faces stranded asset risk if environmental regulations accelerate or gas prices spike. The transition costs could exceed current estimates by billions.

Grid reliability challenges with intermittent resources represent an existential threat poorly understood by investors. Michigan's weather—cloudy winters, still summer days—creates worst-case scenarios for renewable generation. The polar vortex of 2019 showed how quickly reliability can become crisis. As coal plants retire and renewable penetration increases, maintaining grid stability becomes exponentially more complex and expensive.

Regulatory risk never disappears—it only hibernates. Michigan's political purple status means a single election could shift the regulatory environment from supportive to hostile. Industrial customers already complain about rates; residential advocates worry about affordability. The coalition supporting current policies could fracture, leaving CMS Energy exposed to regulatory reversals.

Competition from distributed generation represents a slow-motion disruption that utilities consistently underestimate. As solar-plus-storage costs decline, large customers will increasingly self-generate, leaving utilities with stranded costs spread across a shrinking customer base—the dreaded "utility death spiral." Michigan's industrial customers have both motivation (high rates) and capability (technical sophistication) to defect from the grid.

Weather volatility and storm restoration costs are accelerating beyond model predictions. Climate change doesn't just drive energy transition—it drives extreme weather that damages infrastructure. Ice storms, derechos, and flooding create restoration costs that regulators may not fully compensate, squeezing margins and cash flow.

Valuation and Peer Comparison

Trading at approximately 17-18x forward earnings, CMS Energy commands a premium to slower-growth utilities but a discount to pure-play renewables. This middle-ground valuation reflects the company's hybrid nature: stable utility operations with renewable growth potential. Compared to peers like DTE Energy (Michigan), Xcel Energy (renewable leader), and Southern Company (Southeast regulated), CMS offers superior growth with comparable regulatory stability.

The EV/EBITDA multiple around 12-13x aligns with high-growth regulated utilities, suggesting the market recognizes the capital investment opportunity but remains skeptical of execution. The dividend yield around 3% is below utility averages, reflecting the growth tilt of the investor base. This valuation framework suggests modest multiple expansion potential if execution delivers promised returns.

ESG Considerations and Climate Transition Risks

The ESG narrative is double-edged. Positively, CMS Energy's aggressive decarbonization plan attracts ESG-focused investors and qualifies for green financing at attractive rates. The company's 2040 net-zero commitment and 2025 coal elimination place it among utility climate leaders. This positioning attracts capital from the growing pool of climate-focused funds.

However, transition risks loom large. Stranded asset risk from accelerated coal and gas plant retirements could exceed current provisions. Physical climate risks to Michigan infrastructure—flooding, ice storms, extreme temperatures—may accelerate beyond adaptation investments. Transition technology risks around hydrogen, long-duration storage, or carbon capture could leave the company with stranded R&D investments.

The social license to operate requires careful navigation. Energy affordability concerns could limit rate increases needed to fund the transition. Environmental justice communities near retiring plants demand economic support. Workforce transition from fossil to renewable jobs requires retraining investments. Any misstep could trigger regulatory backlash or social opposition that delays the transformation.

The Investment Synthesis

CMS Energy represents a compelling but complex investment opportunity. For investors seeking regulated utility exposure with above-average growth, the combination of 6-8% earnings growth and 3% dividend yield offers attractive total returns. The clean energy transformation provides both growth drivers and ESG credentials increasingly important to institutional allocators.

However, this isn't a "sleep well at night" utility investment. The massive capital program, technology transition, and regulatory dependencies create execution risk that could derail the investment thesis. Investors must monitor regulatory proceedings, capital project execution, and grid reliability metrics closely.

The optimal investor is one with a 5-10 year horizon who believes in the renewable transition but recognizes the challenges of executing it in a four-season, industrial state. It's an investment in transformation, not stability—appropriate for those who understand both the necessity and difficulty of reimagining America's energy infrastructure.

XI. The Future of Michigan Energy

The next decade will determine whether CMS Energy's transformation from coal-dependent utility to clean energy leader succeeds or stumbles. The company's 2040 net-zero commitment isn't just corporate rhetoric—it's a $20 billion bet that Michigan's economic future depends on sustainable, reliable, and affordable energy. Three critical factors will shape this future: technology evolution, customer behavior, and political dynamics.

Grid modernization represents the invisible revolution underpinning everything else. The company's smart grid investments go beyond simple meter upgrades. Advanced distribution management systems will orchestrate millions of distributed energy resources—rooftop solar, home batteries, electric vehicle chargers—into a coordinated virtual power plant. This isn't science fiction; pilot programs in Grand Rapids and Kalamazoo are already demonstrating how artificial intelligence can predict outages before they occur and reroute power automatically.

The electric vehicle infrastructure buildout presents both opportunity and challenge. Michigan, the birthplace of American automotive, is betting its economic future on electric vehicle manufacturing. Ford's massive EV investments in Dearborn, GM's Factory Zero in Detroit, and Stellantis's retooling all depend on reliable, affordable electricity. CMS Energy must build charging infrastructure that supports both manufacturing and adoption while managing the grid impacts of millions of vehicles charging simultaneously.

The company's approach involves strategic partnerships with automakers and charging networks rather than going it alone. Time-of-use rates incentivize overnight charging when renewable generation exceeds demand. Vehicle-to-grid technology, still experimental, could turn Michigan's EV fleet into a massive distributed battery, storing renewable energy when abundant and supplying it during peak demand.

"We are proud to lead Michigan's clean energy transformation and be one of the first utilities in the country to end coal use," President and CEO Garrick Rochow said. "We are committed to being a force of change and good stewards of our environment, producing reliable, affordable energy for our customers while caring for our communities during this transition." This commitment extends beyond generation to complete electrification of the economy.

Industrial customer retention in a competitive environment requires innovative solutions. Michigan's manufacturers—automotive, chemical, food processing—consume massive amounts of energy and have options. Some threaten to self-generate; others consider relocating to states with cheaper power. CMS Energy's response involves customized solutions: dedicated renewable projects for sustainability-focused customers, interruptible rates for flexible loads, and combined heat and power partnerships that improve overall efficiency.

The company's economic development team works like an investment bank, structuring deals that keep factories in Michigan while meeting their energy needs profitably. Recent wins include securing over 360 megawatts of new load through economic development efforts, from data centers attracted by Michigan's cool climate and renewable power to agricultural processing facilities powered by dedicated solar farms.

Distributed energy resources integration poses the most complex technical challenge. When every customer becomes a potential generator, the traditional one-way grid becomes obsolete. CMS Energy must evolve from monopoly provider to platform operator, orchestrating resources it doesn't own. This requires new capabilities: real-time optimization, blockchain-based energy trading, and regulatory frameworks that fairly compensate distributed resource owners while maintaining grid stability.

The company's approach acknowledges this complexity. Rather than resisting distributed resources, CMS Energy is creating programs that align customer and utility interests. Solar gardens allow customers without suitable roofs to invest in community solar projects. Battery programs provide backup power to customers while giving the utility dispatchable resources for peak shaving. These programs transform potential grid defectors into grid partners.

What Would Different Leadership Do Differently?

A private equity owner might accelerate the transformation more aggressively, shutting coal plants immediately and accepting short-term reliability risks for long-term positioning. They might also pursue regulatory reform more aggressively, pushing for performance-based rates that reward outcomes over inputs.

A tech-oriented leadership might prioritize digital transformation over physical infrastructure, betting that software and algorithms can optimize existing assets rather than building new ones. They might also pursue direct customer relationships through apps and platforms, disintermediating traditional utility touchpoints.

A conservative management team might slow the renewable transition, arguing that reliability and affordability trump environmental goals. They might emphasize gas generation as a decades-long bridge fuel rather than a temporary transition, and resist regulatory mandates that increase costs.

The current leadership's balanced approach—aggressive but not reckless, innovative but not disruptive—reflects Michigan's political and economic reality. In a purple state with strong industrial and environmental constituencies, radical moves in either direction would trigger backlash. The measured pace frustrates both activists wanting faster change and industrialists wanting lower rates, but it may be the only sustainable path forward.

Looking ahead to 2040, CMS Energy envisions a radically different energy system: renewable generation backed by long-duration storage, a digitized grid that self-heals and optimizes in real-time, and customers who actively participate in energy markets rather than passively consuming. Whether this vision materializes depends on technology improvements, regulatory support, and flawless execution of one of America's most ambitious utility transformations.

The ultimate question isn't whether CMS Energy can achieve its clean energy goals—technology and economics increasingly favor renewables. The question is whether it can manage the transition without sacrificing reliability or affordability, the two pillars on which Michigan's industrial economy rests. The company that nearly died from nuclear ambition now bets its future on renewable transformation. History suggests both the possibility of triumph and the potential for catastrophe.

XII. Recent News

The start of 2025 has brought significant developments for CMS Energy, reinforcing both the company's financial strength and the challenges ahead in Michigan's evolving regulatory landscape. CMS Energy announced reported earnings per share of $3.33 for 2024, compared to $3.01 per share for 2023, with adjusted earnings per share for 2024 at $3.34, compared to $3.11 per share for 2023.

The company's 2024 highlights include record investments in the electric grid through the Reliability Roadmap, restoring power to over 93% of customers in less than 24 hours—compared to 87% in 2023, while also landing over 360 megawatts of new load through economic development efforts. This dramatic improvement in restoration times demonstrates tangible progress from the infrastructure investments, addressing one of the key criticisms that has dogged Michigan utilities.

Regulatory Developments and Rate Cases

Michigan regulators approved a $153.8 million annualized electric rate increase for CMS Energy on March 21. This represents a substantial victory for the company, though a previous $92,009,000 increase was 57.4% lower than the $216 million rate increase the utility sought in its initial application. The pattern reveals Michigan regulators' balanced approach: supporting necessary infrastructure investment while protecting consumer affordability.

The regulatory environment continues evolving with Michigan's landmark 2023 energy legislation taking effect. Public Act 235 establishes a renewable energy standard of 50% by 2030 and 60% by 2035. Public Act 235 also establishes a statewide energy storage target of 2,500 MW. These aggressive targets align with CMS Energy's clean energy plans but will require unprecedented capital deployment and operational transformation.

Grid Modernization and Reliability Focus

The Commission partially approved an investment recovery mechanism for improving the reliability and resilience of the electric distribution system, directing Consumers to share its distribution investment plans as soon as reasonably possible, and approving the first year of costs for a pilot program to relocate overhead distribution underground. This underground pilot represents a potential game-changer for Michigan's notoriously unreliable grid, though the costs could prove prohibitive at scale.

Recent utility audits provide unprecedented transparency into utilities' infrastructure and operations, examining the age and condition of equipment, effectiveness of maintenance and tree-trimming schedules, with acknowledgment that it will take time for utilities to make necessary investments to improve reliability, using audit data to shape strategies for reducing outages from severe weather.

Renewable Energy Siting Controversy

Public Acts 233 and 234 of 2023, which preempt existing local siting authority and grant siting authority for utility-scale renewable energy facilities to the Michigan Public Service Commission, took effect on Nov. 29, 2024. MTA and its members stridently opposed the legislation, believing that siting and permitting of renewable facilities should remain with the local community where facilities will be located for the next 20 to 50 years.

This centralization of siting authority removes a significant barrier to renewable development but creates political tension that could complicate CMS Energy's clean energy transition. Rural communities losing local control over massive solar and wind projects may resist in other ways, from litigation to political opposition.

Economic Development Success

The company's economic development achievements deserve particular attention. Landing 360 megawatts of new load represents substantial industrial growth for Michigan, countering the narrative of manufacturing decline. These wins likely include data centers attracted by Michigan's climate and growing renewable capacity, along with reshoring manufacturing operations seeking reliable, increasingly clean power.

Financial Guidance and Investor Confidence

CMS Energy increased its annual dividend by 11 cents per share to $2.17 for 2025, the 19th increase in as many years, while raising 2025 adjusted earnings guidance to $3.54 to $3.60 from $3.52 to $3.58 per share and reaffirming long-term adjusted EPS growth of 6 to 8 percent, with continued confidence toward the high end. This guidance raise signals management confidence despite regulatory pressures and massive capital requirements ahead.

The recent developments paint a picture of a company successfully navigating complex challenges while maintaining financial discipline. The improved reliability metrics address critics' concerns, the regulatory approvals provide revenue certainty, and the economic development wins demonstrate Michigan's continued industrial relevance. Yet the renewable siting controversy and aggressive clean energy mandates remind investors that CMS Energy's transformation journey faces political and operational headwinds that could intensify before they abate.

XIII. Links & Resources

Primary Company Resources: - CMS Energy Investor Relations: www.cmsenergy.com/investor-relations - Annual Reports and 10-K Filings: Available through SEC EDGAR database - Quarterly Earnings Presentations: Posted on company website following earnings calls - Clean Energy Plan Documentation: Consumers Energy sustainability reports

Regulatory Filings and Government Resources: - Michigan Public Service Commission: www.michigan.gov/mpsc - Rate Case Dockets: Available through MPSC e-dockets system - Michigan Energy Legislation (2023): Public Acts 229, 231, 233, 234, and 235 - Federal Energy Regulatory Commission (FERC): www.ferc.gov

Historical Archives and Company History: - Consumers Energy Historical Timeline: Company heritage documentation - Michigan Historical Center: Archives on early electric utilities - Commonwealth & Southern Corporation records: Various university archives - Midland Nuclear Plant documentation: NRC historical records

Industry Analysis and Research: - Edison Electric Institute: Industry statistics and benchmarking - American Public Power Association: Public power perspectives - Nuclear Energy Institute: Historical nuclear plant data - Energy Information Administration (EIA): National and state energy data

Books and Academic Resources: - "The Grid: Biography of an American Technology" by Julie Cohn - "Power Loss: The Origins of Deregulation and Restructuring" by Richard Hirsh - "Nuclear Power and Social Power" by Jerry Brown and Rinaldo Brutoco - Michigan State University Energy Transition Institute publications

Financial Analysis Resources: - S&P Global Market Intelligence: Utility sector analysis - Regulatory Research Associates: State regulatory rankings - Credit rating reports from Moody's, S&P, and Fitch - Sell-side research from major investment banks

Environmental and Clean Energy Resources: - Michigan Environmental Council: State energy policy analysis - Union of Concerned Scientists: Michigan clean energy reports - Lawrence Berkeley National Laboratory: Renewable energy cost studies - National Renewable Energy Laboratory (NREL): Technical feasibility studies

News and Trade Publications: - Crain's Detroit Business: Michigan business coverage - Utility Dive: National utility industry news - Power Engineering Magazine: Technical and industry developments - The Michigan Chronicle: Local community perspectives

Conclusion: The Weight of Transformation

CMS Energy stands at an inflection point that will define not just its next decade, but Michigan's economic future. The company that began with twelve streetlights in Jackson now shoulders the responsibility of powering six million residents through one of history's most complex energy transitions. This isn't merely a business transformation—it's an existential test of whether a 138-year-old utility can reinvent itself fast enough to meet climate imperatives while maintaining the reliability that underpins modern civilization.

The investment case ultimately rests on execution. CMS Energy has proven it can survive existential crisis—the Midland nuclear disaster nearly killed the company but spawned the financial engineering that saved it. The company has demonstrated it can adapt to new realities—abandoning global ambitions to refocus on Michigan when international ventures failed. Now it must prove it can lead transformational change at unprecedented scale and speed.

The $20 billion capital program represents more than infrastructure investment—it's a bet that centralized utilities remain relevant in an increasingly distributed energy future. As rooftop solar costs plummet and battery storage scales, the traditional utility model faces disruption from below. CMS Energy's response—becoming a platform operator that orchestrates distributed resources rather than just a generator—shows strategic sophistication. But strategy and execution are different animals.

Three factors will determine success. First, regulatory relationships must remain constructive as rates inevitably rise to fund the transition. Michigan's purple politics create volatility here—one election could shift the commission from supportive to hostile. Second, operational excellence becomes paramount as the grid complexity explodes. Managing millions of distributed resources while maintaining reliability requires capabilities most utilities lack. Third, technology must cooperate. The renewable transition assumes continued cost declines and performance improvements that aren't guaranteed.

The bear case writes itself: massive capital requirements, stranded asset risks, reliability challenges, and technology uncertainty create multiple failure points. A polar vortex that crashes the grid during peak renewable penetration could trigger political backlash that derails the entire clean energy program. Industrial customers facing higher rates might defect to self-generation, starting the dreaded utility death spiral. Environmental advocates might turn on the company if gas plants operate longer than promised.

Yet the bull case remains compelling. CMS Energy's monopoly position provides pricing power in an inflationary world. The clean energy transition, whatever its challenges, is inevitable—and early movers capture advantages. Federal policy support through the Inflation Reduction Act provides a multi-year tailwind. Michigan's manufacturing renaissance, particularly in EVs, creates load growth opportunities rare among utilities. The company's improved reliability metrics and strong financial performance demonstrate execution capability.

For investors, CMS Energy represents a calculated bet on American infrastructure renewal. It's not a widows-and-orphans utility offering stable dividends and little growth. It's a transformation story with commensurate risks and rewards. The 6-8% earnings growth guidance, if achieved, would place CMS among the fastest-growing utilities nationally. The 3% dividend yield provides income while waiting for the growth story to materialize.

The broader implications extend beyond investment returns. CMS Energy's success or failure will influence how America approaches the energy transition. If a Midwest utility serving a rust-belt state can successfully transform from coal to renewables while maintaining reliability and affordability, it provides a template for national transformation. If it fails, it reinforces skeptics' arguments that the renewable transition is too expensive, too unreliable, and too fast.

History suggests betting against CMS Energy is dangerous. The company has survived and thrived through technological disruption (from gas lights to electric), economic catastrophe (the Great Depression), existential crisis (Midland), and strategic mistakes (international expansion). Each challenge forced adaptation that ultimately strengthened the company. The clean energy transition may be the biggest challenge yet, but it's also the greatest opportunity in the company's 138-year history.

The path forward requires threading multiple needles simultaneously: satisfying environmentalists while maintaining reliability, modernizing infrastructure while controlling costs, embracing distributed resources while preserving the centralized model's economics. It's a high-wire act with no net, performed in full public view with politicians, regulators, and activists shouting from the sidelines.

Yet this is precisely what makes CMS Energy fascinating. In an era of algorithmic trading and quarterly capitalism, here's a company making 40-year bets on physical infrastructure. While Silicon Valley disrupts digital advertising, CMS Energy is reimagining how energy flows through an entire state. The degree of difficulty is extreme, but the societal importance is undeniable.

William Augustine Foote, standing in downtown Jackson in 1886 with his electric arc lights, couldn't have imagined the company his vision would spawn. From those twelve streetlights grew a system that now powers millions of lives. The next chapter—from fossil to renewable, from centralized to distributed, from utility to platform—will be equally transformational. Whether CMS Energy successfully navigates this transformation will determine not just shareholder returns, but how millions of Michiganders live, work, and prosper in the carbon-constrained future.

The story that began with bringing light to darkness continues. The challenge now is bringing clean energy to an industrial economy without losing what made that economy possible: reliable, affordable power available to all. It's a challenge worthy of the company's history, demanding of its capabilities, and critical to its state's future. The outcome remains uncertain, but the attempt is essential. In that attempt lies both the investment opportunity and the societal imperative that makes CMS Energy one of America's most important business stories of the next decade.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube