Comcast: Building the American Cable Empire

I. Introduction & Cold Open

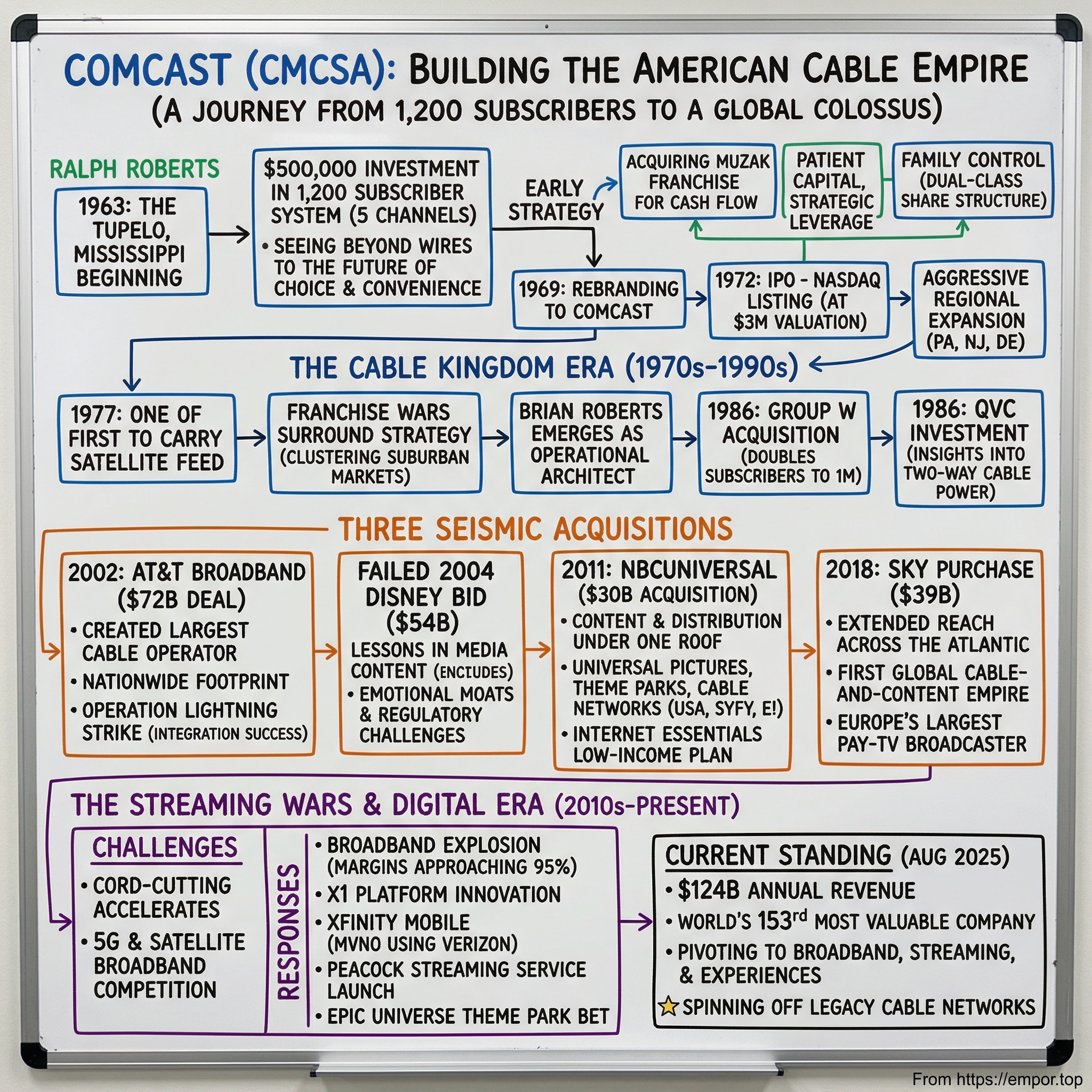

The year is 1963. In a small office in Philadelphia, Ralph Roberts sits across from his investment banker, examining the financials of a tiny cable television system in Tupelo, Mississippi. The system has just 1,200 subscribers, five channels, and operates in a market most East Coast businessmen couldn't find on a map. Roberts, who made his fortune selling men's belts and suspenders, sees something others don't—not just wires and amplifiers, but the foundation of an empire that would one day control how America watches, communicates, and connects.

Fast forward six decades: That $500,000 investment in Tupelo has morphed into Comcast Corporation, a behemoth generating $124 billion in annual revenue with a market capitalization hovering around $124 billion as of August 2025. It stands as the world's 153rd most valuable company, a vertically integrated colossus that owns everything from the cables in your neighborhood to the theme parks where you vacation, from the NBC peacock to the Premier League broadcasts beaming across the Atlantic.

The Comcast story isn't just about organic growth—it's defined by three seismic acquisitions that reshaped American media. The 2002 AT&T Broadband deal for $72 billion (including debt) created the nation's largest cable operator overnight. The 2011 NBCUniversal acquisition for $30 billion brought content and distribution under one roof in ways that would have made the old studio moguls jealous. And the 2018 Sky purchase for $39 billion extended Comcast's reach across the Atlantic, creating the first truly global cable-and-content empire.

But this isn't merely a story of financial engineering and corporate maneuvering. It's about how a family-controlled company navigated technological disruption, regulatory minefields, and changing consumer habits while maintaining an iron grip on power through a dual-class share structure that would make Mark Zuckerberg envious. It's about Brian Roberts, who started as a cable installer and rose to become one of media's most influential executives, wielding 33% voting control with just 1% economic ownership.

Today, as streaming services hemorrhage cash and traditional cable withers, Comcast faces its most existential challenge yet. The company that built its fortune on bundling is being unbundled. The broadband moat that seemed impregnable now faces assault from 5G wireless and Starlink satellites. Yet somehow, the Roberts family empire endures, pivoting from coaxial cables to fiber optics, from linear TV to streaming, from domestic dominance to global ambition.

This is the story of how a belt salesman's leap of faith in rural Mississippi became the backbone of American media infrastructure—and what happens when that backbone starts to bend.

II. The Ralph Roberts Story & Founding (1920–1969)

Ralph Joel Roberts was never supposed to be a media mogul. Born in 1920 to a Jewish immigrant family in New York City, he spent his early years bouncing between ventures with the restless energy of a natural entrepreneur. His father ran a pharmacy, but Ralph had bigger ambitions. After a stint in the Navy during World War II, he tried his hand at manufacturing golf clubs, selling advertising, and eventually found moderate success in the men's accessories business, building Pioneer Suspender Company into a profitable enterprise.

By 1963, Roberts had already lived several business lives. At 43, he'd made and lost money, learned to read balance sheets with a jeweler's eye for detail, and developed an instinct for timing that separated survivors from casualties in American business. When his friend Dan Aaron approached him about a small cable television investment opportunity, Roberts didn't see cables and amplifiers—he saw America changing.

The opportunity was American Cable Systems, a modest operation serving Tupelo, Mississippi, birthplace of Elvis Presley but hardly a media capital. For $500,000—serious money in 1963—Roberts, Aaron, and a young accountant named Julian Brodsky acquired a system with 1,200 subscribers receiving five channels. The previous owners were happy to sell; cable television was seen as a rural curiosity, a technical solution for communities where broadcast signals couldn't reach. Wall Street considered it a utility play at best, a fool's errand at worst.

But Roberts understood something fundamental about American consumer behavior: people would pay for choice and convenience. In Tupelo, where broadcast television signals struggled to penetrate, cable wasn't just an amenity—it was the only way to get clear reception. The business model was elegantly simple: string coaxial cable, maintain the network, collect monthly fees. No content costs, no programming decisions, just pure distribution.

The early days were hardly glamorous. Roberts would drive to Mississippi himself, walking the dusty streets of Tupelo, talking to potential customers, examining utility poles. He quickly grasped that cable's advantage wasn't just technical—it was psychological. In an era when television was becoming America's cultural commons, being excluded from clear reception meant social isolation. Cable connected communities to the broader American conversation.

By 1965, Roberts made his first strategic acquisition, purchasing Storecast Corporation of America, a Muzak franchise operator. This might seem like an odd diversification—what did elevator music have to do with cable television? But Roberts saw the parallel: both were subscription services delivering content through wires. More importantly, Storecast generated steady cash flow that could fund cable expansion. It was financial engineering before the term existed.

The company needed a name that captured its ambitions. In 1969, Roberts combined "communication" and "broadcast" to create Comcast—a portmanteau that suggested both reach and purpose. The rebranding coincided with an aggressive expansion strategy. While competitors focused on large markets where franchise battles were expensive and brutal, Comcast targeted secondary markets where it could achieve dominant positions with less competition.

Roberts also pioneered what would become the Comcast playbook: patient capital, strategic leverage, and family control. He structured deals to maintain voting control even as he brought in outside investors. He hired aggressively from competitors, often paying above market to secure talent. Most importantly, he began grooming his son Brian, who joined the company in 1969 after graduating from Wharton, starting at the bottom as a cable installer in Trenton, New Jersey.

The late 1960s saw Comcast methodically acquiring small systems across Pennsylvania, New Jersey, and Delaware. Each acquisition followed the same pattern: identify underperforming assets, negotiate aggressively on price, integrate operations quickly, and reinvest cash flow into the next deal. By 1969, Comcast served 40,000 subscribers across multiple states—still tiny by national standards but growing with compound reliability.

Roberts' genius wasn't technical—he freely admitted he didn't understand the engineering. Instead, he understood leverage, both financial and operational. Every system Comcast acquired became marginally more valuable as part of a larger network. Shared overhead, bulk programming negotiations, and operational expertise created synergies that made the whole worth more than its parts.

As the 1960s ended, Comcast prepared for its next evolution. The company that started with 1,200 subscribers in Mississippi now had ambitions that stretched far beyond rural cable systems. The 1972 IPO would provide the capital for serious expansion, but more importantly, it would create a currency—publicly traded stock—that could be used for larger acquisitions. Ralph Roberts had built the foundation. Now it was time to build the empire.

III. Building the Cable Kingdom (1970s–1990s)

The morning of November 8, 1972, Ralph Roberts rang the opening bell at NASDAQ for Comcast's initial public offering. The company went public at a $3 million valuation—a modest debut that barely registered in the financial press. Few could have imagined that this small cable operator would one day dwarf the broadcasting networks it carried. But Roberts had a vision that extended beyond wires and amplifiers: he saw cable as the gateway to American homes.

The IPO timing was prescient. Within months, the FCC would relax regulations that had stunted cable growth, allowing systems to import distant signals and offer more channels. Suddenly, cable wasn't just about reception—it was about choice. And no event crystallized this transformation more than HBO's arrival on satellite in 1975.

When Home Box Office announced it would deliver programming via satellite, enabling cable systems to offer premium content, Roberts immediately grasped the implications. In 1977, Comcast became one of the first systems to carry HBO, launching it to their 20,000 Pennsylvania subscribers. The results were staggering: 15% signed up within six months, each paying an additional $7.95 monthly—nearly doubling the average revenue per customer. Roberts later called it "the moment cable became more than utility."

The late 1970s and early 1980s became the era of the franchise wars. Cities across America auctioned exclusive rights to wire their communities for cable, creating a gold rush atmosphere. Comcast's approach was surgical where competitors were scattershot. While TCI's John Malone pursued scale at any cost and Time Warner chased prestige markets, Comcast focused on clustered suburban markets around Philadelphia, Detroit, and New Jersey—affluent areas with stable demographics and limited broadcast reception.

Brian Roberts, now president of the company at age 27, emerged as the strategic architect of this expansion. Where Ralph was the dealmaker and visionary, Brian was the operator and tactician. He pioneered what insiders called the "surround strategy"—acquiring systems adjacent to existing operations to create regional clusters that could share infrastructure and management. It was less sexy than buying Manhattan franchises, but it built a defensible moat.

The 1986 Group W Cable acquisition marked Comcast's emergence as a serious player. For $1 billion, Comcast doubled its subscriber base to one million, gaining systems across the lucrative Northeast corridor. The deal was vintage Roberts: patient negotiation, creative financing (using junk bonds when they were still novel), and flawless integration. Within eighteen months, Comcast had improved Group W's cash flow margins by 8 percentage points through operational discipline.

But the deal that revealed Comcast's ambitions beyond distribution came that same year: the $380 million founding investment in QVC, the home shopping network. Critics scoffed—what did a cable operator know about retail? But Roberts saw the future of interactive television, where the cable pipe could carry commerce, not just content. QVC would eventually generate billions in value, validating Roberts' instinct that cable's real power lay in its two-way capability.

The 1988 acquisition of American Cellular Network for $230 million seemed even more puzzling. Why would a cable company buy wireless spectrum? Brian Roberts, speaking to investors, offered a cryptic response: "Communications technologies converge. The question isn't whether cable and wireless will compete, but when they'll complement." The cellular business would eventually be sold, but not before teaching Comcast valuable lessons about mobile technology that would resurface decades later.

Throughout this expansion, the Roberts family maintained iron control through a dual-class share structure established at IPO. Ralph and Brian controlled 33% of voting rights with just 1% of economic ownership—a structure that allowed them to pursue long-term strategies without activist interference. When questioned about this arrangement at a 1989 shareholder meeting, Ralph was blunt: "We built this company from nothing. We'll run it like owners because we are owners, regardless of the percentages."

The financial engineering was as sophisticated as the operational strategy. Julian Brodsky, the third founder and CFO, pioneered the use of tracking stocks, zero-coupon bonds, and complex partnership structures that minimized taxes while maximizing flexibility. Comcast's balance sheet became a Swiss watch of precisely calibrated leverage—never too conservative to limit growth, never too aggressive to risk the company.

By 1990, Comcast had transformed from a small-town cable operator to a national force with 2 million subscribers. But the industry was consolidating rapidly. TCI had 8 million subscribers, Time Warner had 6 million. To compete, Comcast needed scale, and scale meant bigger deals. The company had proven it could integrate acquisitions, manage complex operations, and navigate regulatory hurdles.

The stage was set for the transformative deals of the 2000s. But first, the 1990s would bring new challenges: the Microsoft investment, the early internet experiments, and the first glimpses of the digital disruption that would reshape entertainment. Comcast had built a cable kingdom. Now it had to defend it against threats no one fully understood yet. The belt salesman's son from Philadelphia was about to face Silicon Valley, and the battle would define the next chapter of American media.

IV. The AT&T Broadband Mega-Deal (1999–2002)

Michael Armstrong's face was ashen as he walked into the AT&T boardroom on a humid July evening in 2001. The former IBM executive had bet AT&T's future on cable, spending $110 billion to acquire TCI and MediaOne, creating AT&T Broadband—the nation's largest cable operator with 13 million subscribers. Now, barely two years later, the strategy was in ruins. AT&T's stock had collapsed from $60 to $15, debt was crushing the company, and Armstrong needed a buyer. Fast.

Across the country in Philadelphia, Brian Roberts had been preparing for this moment for three years. Every Sunday morning, he met with his team in a conference room they called "the war room," walls covered with maps showing every cable system in America, colored pins marking Comcast properties in blue, AT&T in red. Roberts knew Armstrong would eventually buckle. The question was when, and for how much.

The roots of the deal traced back to cable's digital transformation. By 2000, cable wasn't just about television anymore—it was about broadband internet, the killer application that justified massive infrastructure investment. Comcast had 1.2 million broadband subscribers growing at 40% annually; AT&T had 2.2 million. Combined, they would control the pipes delivering high-speed internet to nearly 40% of American homes.

The first approach came in July 2001. Roberts flew to AT&T's Basking Ridge headquarters with a simple proposition: merge the cable operations, create the undisputed industry leader, share the synergies. Armstrong listened politely, then showed Roberts the door. AT&T didn't need Comcast—or so Armstrong believed.

By November, reality had shifted. AT&T's board, led by longtime Roberts ally and Comcast director C. Michael Armstrong (no relation to the CEO), was in revolt. The company needed to raise cash, and Broadband was the only asset worth selling. When news leaked that AT&T was exploring "strategic alternatives," Roberts knew the window was opening.

The auction attracted everyone: AOL Time Warner, Cox Communications, even Microsoft expressed interest. But Roberts had advantages others lacked. Steve Burke, Comcast's head of cable operations and a former Disney executive, had spent months mapping integration plans, identifying $1.5 billion in potential synergies. CFO John Alchin had arranged $60 billion in financing commitments from banks eager to fund the industry's consolidation.

The negotiations played out like a three-dimensional chess match. On December 19, 2001, Roberts made his formal bid: $44.5 billion in stock plus assumption of $27.5 billion in debt, valuing the total transaction at $72 billion. It was a stunning number—the largest media deal in history. But AOL Time Warner countered at $48 billion, and suddenly Comcast looked outgunned.

Roberts' masterstroke came during a Comcast board meeting on December 20. Rather than chase AOL's price, he restructured the deal to give AT&T shareholders more cash—$5 billion—addressing their immediate liquidity needs. He also guaranteed AT&T board seats and promised to maintain dividend payments that AT&T shareholders had come to depend on. It wasn't the highest bid in dollar terms, but it was the most certain to close.

The final negotiations happened in a marathon session starting December 21 and stretching into the early hours of December 22. Roberts, Burke, and Alchin huddled in a conference room at Wachtell, Lipton, Rosen & Katz's Manhattan offices, connected by speakerphone to AT&T's team. As dawn broke over Manhattan, the deal was done: Comcast would pay $31.8 billion in stock and $12.7 billion in cash for AT&T Broadband, creating a colossus with 21.4 million cable subscribers.

"This is a transformative transaction that completes our vision of bringing superior products and services to consumers," Roberts told analysts on the announcement call. What he didn't say was equally important: Comcast now had the scale to dictate terms to programmers, the geographic clustering to dominate major markets, and the broadband footprint to define America's digital future.

The regulatory review was surprisingly smooth—surprising because the combined company would be larger than any previous cable combination. But Roberts had learned from previous deals. Comcast hired an army of lobbyists, made strategic concessions (agreeing to carry unaffiliated internet providers), and emphasized broadband competition from DSL and satellite. The FCC approved the deal in November 2002 with conditions that seemed onerous but were actually manageable.

Integration began before the deal officially closed. Burke implemented "Operation Lightning Strike"—a 100-day plan to combine billing systems, unify branding, and achieve promised synergies. By March 2003, Comcast had exceeded its $1.5 billion synergy target, finding $2.1 billion in annual savings through everything from bulk programming negotiations to consolidated call centers.

The AT&T Broadband acquisition transformed more than Comcast's scale—it changed its DNA. The company inherited sophisticated technology, including early video-on-demand systems and advanced set-top boxes. It gained experienced executives who understood national operations. Most importantly, it acquired the confidence to think bigger.

But the deal also brought challenges that would define Comcast's next decade. Customer service, already a weakness, became a crisis as systems integration created billing errors and service disruptions. The debt load, while manageable, limited financial flexibility just as new competitors emerged. And the sheer size attracted regulatory scrutiny that would intensify with each subsequent move.

As 2003 began, Brian Roberts stood atop an empire his father could hardly have imagined: 21.4 million cable subscribers, 6.3 million digital customers, 3.3 million broadband subscribers, and annual revenues approaching $20 billion. The belt salesman's son from Philadelphia now controlled the largest cable platform in history. The question was what to do with it—and whether content might be the answer.

V. Content Ambitions & Failed Disney Bid (2003–2008)

The letter arrived at Michael Eisner's Bel Air mansion on February 11, 2004, hand-delivered by courier. Brian Roberts' message was cordial but unmistakable: Comcast was offering $54 billion to acquire The Walt Disney Company, including assumption of $12 billion in debt. It was Valentine's Day week, but this was no love letter—it was a declaration of war that would define the limits of cable's imperial ambitions.

Roberts had been planning the Disney assault for months in absolute secrecy. Code-named "Project Saturn" inside Comcast, only six executives knew the full scope. The logic was compelling: Disney owned ABC, ESPN, theme parks, and a content library that stretched from Snow White to Finding Nemo. Combined with Comcast's distribution, it would create the first truly integrated media colossus of the digital age—a company that could make content, distribute it, and control the entire value chain.

The timing seemed perfect. Eisner was embattled, having just lost a no-confidence vote from 43% of Disney shareholders. Roy Disney, nephew of Walt, was in open revolt. The stock had languished for five years. Roberts sensed weakness and pounced, going public with the offer after Eisner refused to engage privately.

"This is a unique opportunity to create one of the world's premier entertainment and communications companies," Roberts told investors on a conference call that morning. The math looked elegant: $27 in cash and 0.78 Comcast shares for each Disney share, a 10% premium. Roberts would run the combined company, Steve Burke would oversee operations, and the Roberts family would maintain control through their super-voting shares.

Eisner's response was immediate and devastating. Within hours, Disney's board unanimously rejected the offer as inadequate. Eisner, a master showman who understood narrative better than any CEO in America, framed Comcast as raiders trying to steal Walt's legacy on the cheap. "Comcast's proposal is not in the best interests of Disney shareholders," the rejection letter stated, but Eisner's private message to allies was more colorful: "Over my dead body."

The battle that followed was unlike anything corporate America had seen. Roberts flew to Florida to court institutional investors, promising to unlock Disney's value through synergies worth $2.5 billion annually. Burke gave presentations showing how ESPN could be leveraged across Comcast's sports networks, how Disney content could drive broadband adoption, how theme park technology could enhance cable services.

But Disney fought back with unusual weapons. Eisner commissioned internal videos shown to employees, portraying Comcast as a soulless monopoly that would destroy Disney magic. He leaked stories about Comcast's customer service problems—"Do you want the cable guy running Disney World?" became an unofficial talking point. Most effectively, he raised the specter of regulatory rejection, noting that Comcast-Disney would control 40% of all television programming.

The knockout blow came from an unexpected source: Steve Jobs. The Apple CEO, who had just sold Pixar to Disney and joined its board, called Roberts personally. "You're thinking about this wrong," Jobs reportedly said. "Content and distribution are different businesses. The future isn't about owning both—it's about making each excellent." Coming from the man who had separated iTunes from record labels, the advice carried weight.

By April 28, 2004, Roberts withdrew the bid. The official statement cited Disney's unwillingness to negotiate, but insiders knew the real reason: the financing was getting wobbly, regulators were signaling concern, and Disney shareholders weren't rallying to Comcast's cause. The empire had reached its boundaries.

The Disney failure taught Roberts crucial lessons that would shape Comcast's next decade. First, hostile takeovers in media were nearly impossible—content companies had emotional moats that financial engineering couldn't breach. Second, size alone didn't guarantee success; integration complexity could destroy value faster than synergies created it. Third, and most importantly, Comcast needed to build content capabilities organically before attempting another transformative content acquisition.

The years following Disney saw Comcast methodically assembling content assets under the radar. In 2004, it sold QVC to Liberty Media for $7.9 billion—a painful departure from an asset Ralph Roberts loved, but necessary to fund new ambitions. The proceeds went toward acquiring regional sports networks, building Comcast SportsNet into a powerhouse that controlled Philadelphia 76ers and Flyers broadcasts.

The Golf Channel acquisition in 2004, E! Entertainment in 2006, and Daily Candy in 2008 were all small deals that barely made headlines. But each taught Comcast how to manage creative talent, produce original programming, and navigate the peculiar economics of content creation. Burke later called this period "our apprenticeship in content"—learning the business through smaller bets before making the big one.

The failed Disney bid had one unexpected benefit: it put Comcast on the map as a serious content player. When General Electric began exploring options for NBC Universal in 2009, Roberts was the first call. This time, there would be no hostile tactics, no public battles, no cultural warfare. Comcast had learned that in content, as in cable, patient capital and friendly negotiations won more than aggressive raids.

As the financial crisis erupted in 2008, Roberts watched media valuations collapse and prepared for the next opportunity. The Disney dream was dead, but something even more ambitious was taking shape. The cable operator that couldn't buy Mickey Mouse was about to acquire the peacock.

VI. The NBCUniversal Acquisition (2009–2013)

Jeff Immelt's voice carried a hint of desperation as he made the call to Brian Roberts on a gray September morning in 2009. The General Electric CEO was drowning—GE Capital had nearly collapsed during the financial crisis, the stock had fallen 70%, and investors were demanding he dismantle the conglomerate Jack Welch built. NBC Universal, once GE's crown jewel, was now a burden Immelt couldn't afford to carry.

"Brian, we need to talk about NBC," Immelt said. Roberts had been expecting this call for six months.

The courtship actually began years earlier, in quiet conversations at media conferences and chance encounters at Manhattan restaurants. Roberts and Immelt would discuss the industry's future, always dancing around the obvious: GE didn't belong in media, and Comcast needed content. But it took Lehman Brothers' collapse and GE's near-death experience to create the conditions for a deal.

By October 2009, secret negotiations were underway at the Wachtell, Lipton offices, the same Manhattan tower where Comcast had sealed the AT&T Broadband deal. The code name was "Project Symphony"—Roberts' mild joke about harmonizing content and distribution. This time, everything was different from Disney. No hostile moves, no public drama, just two CEOs trying to solve each other's problems.

The asset on the table was extraordinary: NBC Universal included the NBC broadcast network, Universal Pictures, cable channels like USA, Syfy, CNBC, and MSNBC, the Universal theme parks, and a library with everything from "Law & Order" to "Jurassic Park." Annual revenues exceeded $15 billion. But the business was struggling—NBC had fallen to fourth place in prime time, Universal was losing ground to Disney in theme parks, and the cable channels faced new competition from digital upstarts.

The deal structure reflected lessons from Disney. Rather than buy NBC Universal outright, Comcast would acquire 51% for $13.8 billion, with GE retaining 49% for a transition period. This allowed GE to partially exit while giving Comcast time to learn the content business with a partner. Critically, Comcast negotiated options to buy GE's remaining stake at predetermined valuations, protecting against future disputes.

When the deal was announced on December 3, 2009, the reaction was mixed. Media executives wondered if a cable operator could run a creative enterprise. Wall Street worried about the $13.8 billion price tag during a recession. Regulators immediately signaled this would face unprecedented scrutiny—a cable giant owning major content raised every antitrust concern imaginable.

The regulatory review became a marathon of unprecedented scope. The FCC and Department of Justice spent 13 months examining every aspect, from program access rules to broadband competition. Comcast hired 137 lobbyists, spent $18 million on advocacy, and Roberts personally visited Washington 30 times. The company made concession after concession: agreeing to carry competing online video services, promising not to withhold NBC content from rivals, even accepting government monitoring of its broadband network. The most dramatic condition came from an unexpected source. On January 18, 2011, the FCC and the United States Department of Justice (DOJ) approved the acquisition, but with a twist: Comcast agreed to offer an internet service plan for qualifying low-income families for at least three years as part of the acquisition. The plan, "Internet Essentials", initially offered a 1.5-megabit connection for $9.95 per month (increased to 5 megabits in 2013) with no activation or equipment fees. It was a brilliant political maneuver—turning a monopoly concern into a digital inclusion initiative.

On January 28, 2011, Comcast Corp. (Comcast) and NBC Universal, Inc. (NBC-U) completed their merger to form a new entity, Comcast-NBC Universal (C-NBCU). The transformation was immediate. Steve Burke, Roberts' longtime lieutenant, became NBC Universal CEO with a mandate to fix what GE had broken. Within months, NBC went from last place to contention in prime time. Universal theme parks, starved of investment under GE, received billions for new attractions. The cable channels were integrated with Comcast's regional sports networks, creating programming synergies GE never imagined.

The real masterstroke came in March 2013, when Comcast exercised its option to buy GE's remaining 49% stake for $16.7 billion—a price set in the original deal that now looked like a bargain as NBC Universal's performance improved. In just over two years, Comcast had gone from pure distribution to owning one of Hollywood's major studios, a broadcast network, and a theme park empire. The total investment of $30.5 billion would generate returns that validated Roberts' vision.

But the most prescient part of the deal was barely noticed at the time. Buried in the acquisition documents was NBC Universal's 32% stake in a small streaming venture called Hulu. While everyone focused on broadcast networks and cable channels, Comcast had inadvertently acquired a foothold in the streaming future—though regulatory conditions prevented them from exercising control. It was a glimpse of battles to come.

The NBC Universal acquisition proved that Comcast could do what it failed to accomplish with Disney: successfully integrate a major content company. Unlike the Disney debacle, this was friendly, methodical, and flawlessly executed. Roberts had learned that in media, as in cable, patience and partnership trumped hostile aggression. The cable empire now had its content crown jewel. The question was whether it could defend both against the digital barbarians gathering at the gates.

VII. The Streaming Wars & Cord-Cutting Era (2010s–Present)

Reed Hastings stood before a room of investors in January 2013, his trademark confidence radiating as he declared Netflix's ambition: "The goal is to become HBO faster than HBO can become us." In a nondescript conference room three thousand miles away, Brian Roberts watched the livestream with his senior team. Someone finally broke the silence: "He's not trying to become HBO. He's trying to become us."

The numbers were still manageable—Netflix had 27 million U.S. subscribers while Comcast had 22 million video customers generating five times the revenue. But Roberts understood exponential math. Netflix was adding subscribers at 25% annually while Comcast's video subscriber count had peaked. For the first time since Tupelo, the fundamental model of cable television was under assault.

Comcast's first response was defensive innovation. The X1 platform, launched in 2012, represented a $1 billion bet that superior technology could stem defections. X1 transformed the clunky cable box into something approaching elegance—voice control, personalized recommendations, integrated apps. By 2014, X1 customers were watching 50% more content and churning 25% less than traditional box users. It seemed like technology might save the bundle.

But the real strategic pivot was hiding in plain sight. While media coverage obsessed over cord-cutting, Comcast's broadband business was exploding. Streaming video didn't replace Comcast's pipes—it made them more valuable. Every Netflix binge, every YouTube session, every Zoom call during the pandemic traveled over Comcast's infrastructure. Broadband subscribers grew from 17 million in 2010 to 32 million by 2024, with margins approaching 95% once infrastructure was deployed.

The wireless threat emerged from an unexpected angle. Verizon and AT&T's 5G rollouts promised home internet without wires—a direct assault on cable's last monopoly. Roberts' response was characteristically counterintuitive: if you can't beat them, use them. In 2017, Comcast launched Xfinity Mobile as an MVNO (mobile virtual network operator) using Verizon's network, bundling wireless with broadband to increase customer stickiness. The wireless strategy was working better than anyone predicted. During the third quarter of this year, Comcast surpassed 7.5 million subscriber lines, and another 1.2 million mobile line additions in 2024 alone. The capital-light MVNO model meant Comcast could offer mobile service without building towers, using Verizon's network while offloading 90% of traffic to its own WiFi hotspots.

The streaming response came late but with force. Peacock, NBC Universal's streaming service, launched in July 2020 to widespread skepticism. Another also-ran in the streaming wars, critics said. But Roberts had learned from Netflix that content alone didn't win—scale and bundling did. Peacock delivered revenue growth of 46%, fueled by a diverse slate of sports and entertainment content, including the incredibly successful Paris Olympics

I'll help you continue this article about Comcast. Let me search for recent information to complete the remaining sections accurately.. The strategy emphasized exclusive content, affordable pricing, and the $5 monthly bundle with Peacock Premium for Xfinity customers.

But Sky, acquired for £30.6 billion (£17.28 per share) in September 2018, proved Roberts' true streaming vision wasn't purely digital—it was global. The £17.28 per share price reflects a record 125% premium over Sky's December 2016 closing price, prior to Fox's initial bid. The auction climax came after a protracted bidding war with Disney-Fox that tested Roberts' financial discipline. Comcast's last sealed bid of £30.6 billion (£17.28 per share), surpassed Fox's £27.6 billion (£15.67 per share) offer in the UK Takeover Panel's supervised blind auction.

The Sky deal transformed Comcast's international profile overnight. Sky is Europe's largest media company and pay-TV broadcaster by revenue (as of 2018), with 23 million subscribers and more than 31,000 employees as of 2019. It brought Premier League rights, sophisticated streaming technology through NOW TV, and cultural relevance across the UK, Germany, and Italy. More importantly, it proved Comcast could execute massive international acquisitions despite investor skepticism about the 7% decline in Comcast's stock price immediately following the win.

The pandemic accelerated every digital trend Roberts had been fighting. Cord-cutting went from trickle to torrent—Comcast lost 2 million video subscribers between 2020 and 2024. Work-from-home made broadband essential but also exposed network limitations. Streaming losses mounted as content costs exploded. Yet somehow, Comcast emerged stronger, validating Roberts' infrastructure-first strategy.

The 2024 numbers told the story of successful adaptation. "We had the best financial performance in our company's 60-year history with record revenue, EBITDA and EPS along with significant free cash flow," said Brian L. Roberts, highlighting 5% connectivity revenue growth, another 1.2 million mobile line additions, and revenue growth of 46% at Peacock. Total revenue reached $123.7 billion for the full year, with the connectivity business proving more resilient than anyone predicted.

The decision to spin off cable networks, announced in late 2024, marked the end of an era. Channels that once commanded billions in carriage fees would be separated into "SpinCo," allowing Comcast to focus on broadband, streaming, and experiences. It was an admission that linear television's decline was irreversible, but also a strategic pivot toward businesses with growth potential.

VIII. Business Model Evolution & Financial Architecture

The transformation of Comcast's business model from 1963 to 2024 reads like a masterclass in financial engineering married to operational excellence. What began as a simple utility play—charging monthly fees for clear television reception—evolved into one of the most complex financial architectures in corporate America, generating cash flows that would make a Silicon Valley unicorn envious.

The original model Ralph Roberts pioneered was elegantly straightforward: high fixed costs for infrastructure, near-zero marginal costs per subscriber, and predictable monthly revenue. A coaxial cable could serve one customer or one thousand with minimal additional expense. This economic reality created natural monopolies—once Comcast wired a neighborhood, competitors rarely found it economical to overbuild.

By the 1980s, the model had evolved to embrace what Roberts called "the annuity business." Cable subscribers rarely churned if service was adequate, creating revenue streams more predictable than government bonds. This stability allowed aggressive leverage—Comcast routinely operated at 3-4x debt-to-EBITDA ratios that would terrify most CEOs but barely concerned the Roberts family. They understood that predictable cash flows could service predictable debt.

The digital transition of the late 1990s added layers of complexity and opportunity. Digital set-top boxes enabled premium tiers, video-on-demand, and eventually broadband—each adding incremental revenue to the same physical plant. A customer paying $30 for basic cable in 1995 was paying $150 for the triple play bundle by 2005. The infrastructure barely changed; the revenue per home quintupled.

Julian Brodsky's financial innovations during this period deserve particular recognition. He pioneered tracking stocks for different business units, allowing investors to value the cable and content businesses separately. He structured acquisitions to minimize tax leakage, often keeping assets in separate entities for years to preserve tax benefits. Most brilliantly, he maintained the dual-class share structure through every transaction, ensuring the Roberts family never lost control despite massive dilution.

The AT&T Broadband acquisition marked a turning point in financial strategy. The deal's $72 billion total value required every trick in the investment banking playbook: bridge loans, high-yield bonds, convertible preferreds, and complex earn-outs. But the real genius was the integration plan that identified $2.1 billion in annual synergies—more than enough to justify the premium paid. Within eighteen months, Comcast had exceeded every financial target, validating the "bigger is better" thesis.

The NBC Universal deal showcased even more sophisticated financial architecture. The initial 51% stake for $13.8 billion included predetermined options to buy GE's remaining stake—essentially locking in future purchase prices when NBC Universal was underperforming. By the time Comcast exercised these options in 2013, the improving business made the preset prices look like theft. Roberts had learned from Disney that hostile premiums destroy value; patient negotiation with aligned incentives creates it.

The broadband era brought the highest margins in Comcast's history. Once the infrastructure was deployed, broadband service generated 95% incremental margins. Every speed upgrade, every price increase dropped straight to the bottom line. By 2020, broadband had become Comcast's profit engine, generating more EBITDA than video despite lower revenues. The capital allocation reflected this reality—billions poured into network upgrades while video infrastructure investment virtually ceased.

But the streaming era challenged every assumption. Peacock required massive content investment with uncertain returns. Parks needed billions in capital expenditure for attractions that might take decades to pay back. The Sky acquisition added international complexity and currency risk. Suddenly, Comcast's traditionally predictable model faced unprecedented volatility.

The response was textbook Roberts: maintain financial flexibility at all costs. Despite the Sky acquisition's massive debt, Comcast kept leverage below 3x through aggressive cash generation and modest share buybacks. The company maintained its investment-grade rating even as competitors leveraged up for streaming wars. When the pandemic hit, Comcast had the balance sheet strength to weather any storm.

The capital allocation philosophy evolved but remained disciplined. Roberts articulated a clear hierarchy: first, invest in the network to maintain competitive advantage; second, pursue strategic M&A that enhances the platform; third, return excess cash to shareholders through dividends and buybacks. The Board of Directors approved a new share repurchase program authorization, effective as of January 31, 2025, of $15 billion, which does not have an expiration date, signaling confidence in long-term cash generation.

The 2024 financial architecture reflected six decades of evolution. Connectivity & Platforms generated steady cash flows with expanding margins. Content & Experiences provided growth optionality with higher volatility. The dual-class structure remained intact, allowing long-term thinking in a short-term market. International operations through Sky diversified revenue while adding complexity. The streaming pivot through Peacock positioned for the future while pressuring near-term profitability.

Yet challenges mounted. The $11 billion in Sky debt added to an already leveraged balance sheet. Theme park investments approached $1 billion annually with long payback periods. Broadband competition from fixed wireless and fiber threatened the core cash engine. Streaming losses, while moderating, still consumed billions in content investment. The financial model that seemed unassailable now faced pressure from every direction.

The ultimate test came in balancing growth investment with shareholder returns. The 6.5% dividend increase to $1.32 per share annually for 2025, alongside the new $15 billion share repurchase authorization, demonstrated confidence. But it also revealed the tightrope walk—investing enough to remain competitive while returning enough to satisfy investors increasingly skeptical of media conglomerates.

IX. Playbook: The Comcast Way

Inside Comcast's Philadelphia headquarters, a framed quote from Ralph Roberts hangs in the boardroom: "It's not about being the biggest. It's about lasting the longest." This philosophy, refined over six decades, created a playbook that transformed a Mississippi cable system into America's media infrastructure backbone. The Comcast Way isn't just strategy—it's institutional DNA, passed from father to son, deal to deal, crisis to crisis.

The foundation is family control with public capital. The Roberts' dual-class structure—33% voting power with 1% economic ownership—seems like governance heresy in an age of shareholder activism. Yet it enabled every transformative decision, from the AT&T Broadband acquisition to the NBC Universal integration. Brian Roberts doesn't worry about quarterly earnings calls or activist campaigns. He worries about decades, not quarters.

This structure created a paradox: a public company that operates like a private one. When Verizon or AT&T pivoted strategies with new CEOs, Comcast maintained course with Brian Roberts at the helm since 1990. When competitors chased growth at any cost, Comcast maintained pricing discipline. When streaming wars erupted, Comcast entered late but deliberately. The family control that governance experts criticize is precisely what enabled long-term value creation.

The M&A excellence runs deeper than financial engineering. Comcast developed an institutional competence in integration that rivals private equity firms. The integration playbook, refined through hundreds of acquisitions, follows a predictable pattern: identify redundancies within days, achieve quick wins within weeks, realize synergies within months. The AT&T Broadband integration, despite combining 21 million subscribers across incompatible systems, exceeded every timeline and financial target.

But the secret sauce is cultural integration. Unlike slash-and-burn acquirers, Comcast selectively retains talent and best practices from targets. Steve Burke came from Disney via the ABC acquisition. Sky's Jeremy Darroch remained CEO post-acquisition. NBC Universal executives were promoted into Comcast corporate roles. This creates a meritocracy that transcends corporate boundaries—perform well, and origin doesn't matter.

Regulatory navigation became core competency through necessity. Every major Comcast deal faced regulatory scrutiny that would kill most transactions. The NBC Universal review took thirteen months and resulted in unprecedented conditions. The failed Time Warner Cable acquisition taught expensive lessons about political limits. Yet Comcast emerged with an unmatched understanding of the regulatory maze.

The lobbying operation is legendary. Comcast spent $14.4 million on federal lobbying in 2023 alone, employing former FCC commissioners, congressional staffers, and administration officials from both parties. But influence goes beyond money—it's about shaping narrative. When the NBC Universal deal faced opposition, Comcast committed to Internet Essentials, turning a monopoly concern into a digital equity initiative. When Sky raised foreign ownership fears, Comcast guaranteed editorial independence for Sky News.

The customer service paradox remains Comcast's Achilles heel and greatest irony. The company that pioneered operational excellence in network management became synonymous with customer service failures. "Comcast customer service" generates more negative Google results than any competitor. The company knows this—spending billions on service improvements, digital tools, and training—yet the reputation persists.

The explanation lies in monopoly psychology. When customers have no choice, resentment builds regardless of service quality. Every service call becomes a reminder of captivity. Comcast could have Amazon-level service, and customers would still complain about the monopoly. Roberts understood this, choosing to focus on network reliability over service perception. Better to be hated but essential than loved but optional.

Technology adoption follows a consistent pattern: fast follower, not first mover. Comcast didn't invent cable modems, but perfected their deployment. Didn't create video-on-demand, but scaled it nationally. Didn't pioneer streaming, but launched Peacock when the model was proven. This approach seems conservative but reflects deep wisdom—let others pay for education, then execute better with more capital.

The X1 platform exemplified this philosophy. While Silicon Valley built streaming boxes, Comcast spent $1 billion creating a superior integrated experience. X1 wasn't revolutionary technology—voice control, recommendation engines, and app integration existed elsewhere. But Comcast combined them into a seamless product that reduced churn and increased engagement. Innovation through integration, not invention.

Vertical integration became religion, despite academic skepticism. Owning content and distribution created conflicts—should Comcast favor NBC content on its pipes? But it also created synergies invisible to critics. NBC's sports rights made Comcast's regional sports networks more valuable. Universal's content library gave Peacock instant scale. Theme parks promoted film franchises while films drove park attendance. The conflicts were manageable; the synergies were transformative.

The management philosophy blends entrepreneurial aggression with operational discipline. Roberts encourages big bets—Sky, NBC Universal, Epic Universe—but demands flawless execution. Executives who deliver get enormous autonomy; those who don't disappear quietly. The culture rewards longevity—many senior executives have twenty-plus year tenures—creating institutional knowledge competitors can't match.

The capital allocation discipline seems boring but proves brilliant. Comcast never pursued transformative technology bets like AT&T's satellite ambitions or Verizon's media adventures. Instead, it invested steadily in network upgrades, strategic content, and selective M&A. The company avoided both the home runs and strikeouts that defined competitors, choosing instead consistent singles and doubles that compound over time.

The Comcast Way isn't perfect—customer service remains problematic, regulatory scrutiny is constant, and the family control structure limits governance evolution. But it created extraordinary value over six decades, transforming a small cable operator into a global media conglomerate. The playbook that Ralph Roberts began and Brian Roberts perfected may face new challenges, but its core principles—patient capital, operational excellence, and strategic integration—remain the foundation of an empire built to last.

X. Analysis & Investment Case

Standing at a $116 billion market capitalization in August 2025, down 21.7% year-over-year, Comcast presents the classic value-versus-growth dilemma that defines modern media investing. The bull case rests on irreplaceable infrastructure and diversified cash flows. The bear case sees technological disruption and secular decline. The truth, as always, lies somewhere between—but where exactly determines whether Comcast is a value trap or opportunity of a generation.

The bull case starts with infrastructure reality. Comcast passes 63 million homes and businesses with its network—a footprint that would cost $200 billion to replicate at current construction costs. While 5G and satellite competitors promise wireless alternatives, physics hasn't changed: fiber and coaxial cable deliver more bandwidth more reliably than any wireless technology. As artificial intelligence drives exponential data growth, Comcast's pipes become more, not less, valuable.

The broadband business model remains extraordinarily attractive despite competitive pressure. With 32 million subscribers generating 95% incremental margins, every price increase flows directly to cash flow. The average revenue per user (ARPU) grew 3.6% in 2024 despite increased competition, proving pricing power persists. Fixed wireless may nibble at the edges, but it can't match cable's capacity for the data-hungry households that generate the highest revenues.

Universal Epic Universe, opening May 22, 2025, transforms Universal Orlando Resort into a weeklong vacation destination comprised of four theme parks, fundamentally changing the competitive dynamics with Disney. The $7 billion theme park investment seems massive, but theme parks generate 20-30% EBITDA margins with decades-long asset lives. "We are seeing great demand in early days since we announced opening day" for Epic Universe, suggesting pent-up demand exists despite macro concerns.

The content library provides optionality bulls love. NBC Universal's combination of broadcast, cable, film, and streaming creates multiple monetization windows for every piece of content. A successful Universal film like "Wicked" generates box office revenue, then streaming views on Peacock, then theme park attractions, then consumer products. This ecosystem approach means content investments compound rather than depreciate.

Sky brings international diversification and streaming expertise. Despite the high acquisition price, Sky's technology platform and established streaming services (NOW TV) provide capabilities Comcast couldn't build organically. The Premier League rights and European footprint create a hedge against US-centric risks while opening new growth markets.

The financial position supports the bull case. Despite massive investments, Comcast maintains investment-grade ratings and leverage below 3x. The company generated sufficient cash to invest $8.3 billion in connectivity infrastructure, build Epic Universe, fund Peacock losses, AND return $16 billion to shareholders in 2023. Few companies combine this investment capacity with shareholder returns.

The bear case, however, is equally compelling. Cord-cutting isn't slowing—it's accelerating. Comcast lost 2 million video subscribers in just four years, and the pace increased in 2024. The planned SpinCo separation of cable networks is essentially admission that linear television is dying. When management gives up on a business generating billions in revenue, investors should worry.

Broadband competition is intensifying from every direction. Verizon and T-Mobile's fixed wireless services are adding millions of subscribers by targeting Comcast's lower-tier customers. Fiber overbuilders are cherry-picking affluent neighborhoods. Starlink promises rural coverage without infrastructure. The broadband monopoly that seemed permanent is fragmenting rapidly.

Streaming remains a money pit despite Peacock's growth. While revenue grew 46% in 2024, Peacock still loses money competing against Netflix's global scale and Disney's content library. The streaming endgame likely has room for only 3-4 global players. Peacock, despite NBC's content and Comcast's distribution, may not make the cut.

Theme parks face structural headwinds beyond Epic Universe's opening boost. Lower attendance at domestic parks followed "a pull-forward of demand in 2022 and 2023, which were record years for the theme parks". Post-pandemic revenge travel is over. Economic uncertainty pressures discretionary spending. Climate change makes outdoor attractions increasingly challenging. The Epic Universe investment might open just as the cycle turns negative.

The technological disruption risk looms largest. Artificial intelligence could make traditional content creation obsolete. Virtual reality might replace physical theme parks. Decentralized networks could eliminate infrastructure advantages. Comcast's entire business model assumes the fundamental structure of media consumption remains stable. History suggests that's a dangerous assumption.

The valuation debate reflects these conflicting narratives. At 7x EBITDA, Comcast trades at a significant discount to historical multiples and peer averages. The 3% dividend yield and aggressive buyback program provide downside support. But value investors have been saying Comcast is cheap for five years while the stock underperformed. Cheap can get cheaper when secular decline accelerates.

The investment case ultimately depends on time horizon and risk tolerance. For value investors, Comcast offers irreplaceable assets at distressed valuations with substantial cash returns. For growth investors, it's a melting ice cube with existential threats and limited upside. For income investors, the dividend seems safe but growth is questionable.

The most intellectually honest assessment: Comcast is neither pure value nor pure trap—it's a complex transition story. The company is successfully navigating from legacy cable to modern connectivity, from linear TV to streaming, from domestic to global. But transitions are messy, expensive, and uncertain. The infrastructure moat is real but eroding. The content is valuable but commoditizing. The theme parks are spectacular but cyclical.

Brian Roberts has proven remarkably adept at evolution—every previous challenge met, every transition managed. But the current transformation is different. It's not about acquiring assets or integrating operations. It's about fundamentally reimagining what Comcast is when cable television dies, broadband commoditizes, and entertainment digitizes. The empire Ralph Roberts built and Brian Roberts expanded faces its greatest test: can it evolve fast enough to survive its own success?

XI. Looking Forward & Wrap-Up

As Brian Roberts stands in his father's original office, preserved exactly as Ralph left it, the weight of legacy and future collides. The memorabilia tells the story—the original Tupelo contract, photos with presidents and moguls, the gavel from the NBC Universal closing. But the question that haunts the room is whether the empire built on coaxial cable can transform into something unrecognizable yet enduring.

The Epic Universe bet represents more than a theme park—it's a statement about physical experience in a digital age. The park features five themed worlds spanning 750 acres (though just 110 acres have been used so far), leaving enormous expansion potential. "There's a lot of room for expansion. We're already thinking about how that plays out", says Universal's leadership, suggesting Epic Universe is just the beginning of a broader experiential strategy.

The numbers support the ambition. Theme parks generate returns that streaming services dream about—20-30% EBITDA margins, decades-long asset lives, and pricing power that outpaces inflation. While Netflix spends billions on content that expires in weeks, a successful theme park attraction generates cash for generations. The Harry Potter lands still drive attendance fifteen years after opening. Epic Universe could anchor cash flows through 2050.

But the real transformation lies in broadband infrastructure's evolution toward artificial intelligence and edge computing. Every AI model needs data centers. Every data center needs fiber connections. Every autonomous vehicle needs low-latency networks. Comcast's 63 million home footprint could become the nervous system for America's AI economy. The company exploring edge computing partnerships could transform from internet provider to AI infrastructure platform.

The international expansion through Sky opens doors barely explored. European broadband penetration lags the US by years. Streaming fragmentation creates opportunities for aggregation. Sports rights, particularly soccer, offer growth potential that American football can't match. Sky's technology platform could become the backbone for Comcast's global ambitions, reversing the typical American-company-buys-foreign-asset-and-ruins-it narrative.

Yet structural challenges loom larger than any specific opportunity. The SpinCo separation of cable networks acknowledges a brutal reality: linear television is dying faster than anyone expected. The networks that generated billions in fees will be orphaned into a separate company, likely to wither or consolidate with other orphans. It's a tacit admission that Comcast can't save everything.

The succession question hovers unspoken but urgent. Brian Roberts is 65, having led Comcast for 35 years. The dual-class structure ensures Roberts control continues, but through whom? His children work in the business but lack Brian's operational experience. Professional management seems inevitable, but can hired executives maintain the long-term thinking that family control enabled? The empire's greatest strength—family ownership—might become its weakness.

Customer relationships remain stubbornly transactional in an age demanding emotional connection. Young consumers don't hate Comcast—they nothing it, which might be worse. The brand evokes utility bills and service calls, not entertainment and connection. While Disney and Netflix occupy cultural mindshare, Comcast remains infrastructure nobody celebrates but everybody needs. Can infrastructure ever be loved, or is being essential enough?

The strategic options narrow as the company grows. At $124 billion in revenue, few acquisitions move the needle. Buying Netflix or merging with another telco would face insurmountable regulatory challenges. International expansion requires massive capital with uncertain returns. Comcast might have reached the limits of financial engineering—future growth must come from innovation, not acquisition.

If we were running Comcast, the path forward would embrace three principles. First, accept that cable television is dead and accelerate the transition. Don't manage decline; amputate quickly. Second, reconceptualize broadband as an AI platform, not internet access. Partner aggressively with cloud providers, build edge computing facilities, enable the infrastructure for America's AI transformation. Third, make Epic Universe the template for global experiential expansion. Physical experiences become more valuable as digital entertainment commoditizes.

The biggest surprise from the Comcast story isn't the growth—it's the durability. A company built on copper wires survived the internet revolution. A distribution business successfully acquired content. A American company bought European assets without destroying them. The adaptability that seems impossible in prospect becomes inevitable in retrospect.

The lesson for investors and operators alike: infrastructure advantages are real but temporary. Every moat eventually fills with sand. The question isn't whether disruption comes but how you respond. Comcast's response—patient capital, operational excellence, strategic flexibility—offers a masterclass in corporate evolution. Not every transition succeeds, but attempting transformation beats accepting decline.

As 2025 unfolds, Comcast stands at an inflection point. The cable business that created the empire is dying. The broadband business that funds it faces competition. The content business that diversified it bleeds cash. The theme park business that might save it requires massive investment. It's a moment demanding courage that would make Ralph Roberts proud—betting the company on an uncertain future rather than managing a certain decline.

The empire Ralph Roberts started with 1,200 subscribers in Tupelo has become something he couldn't have imagined—a global platform connecting hundreds of millions to information, entertainment, and each other. Whether it survives another generation depends on Brian Roberts' final act: transforming Comcast from what it was into what it must become. The coaxial cable that carried five channels to Mississippi now must carry America into the AI age. The belt salesman's son must once again prove that patient capital and operational excellence can overcome any disruption.

The story isn't over. It's evolving. And for all Comcast's challenges, betting against the Roberts family has been a losing proposition for sixty years. The empire might transform beyond recognition, but like the cable that still carries most of America's data, it will endure—adapting, evolving, and connecting whatever comes next.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube