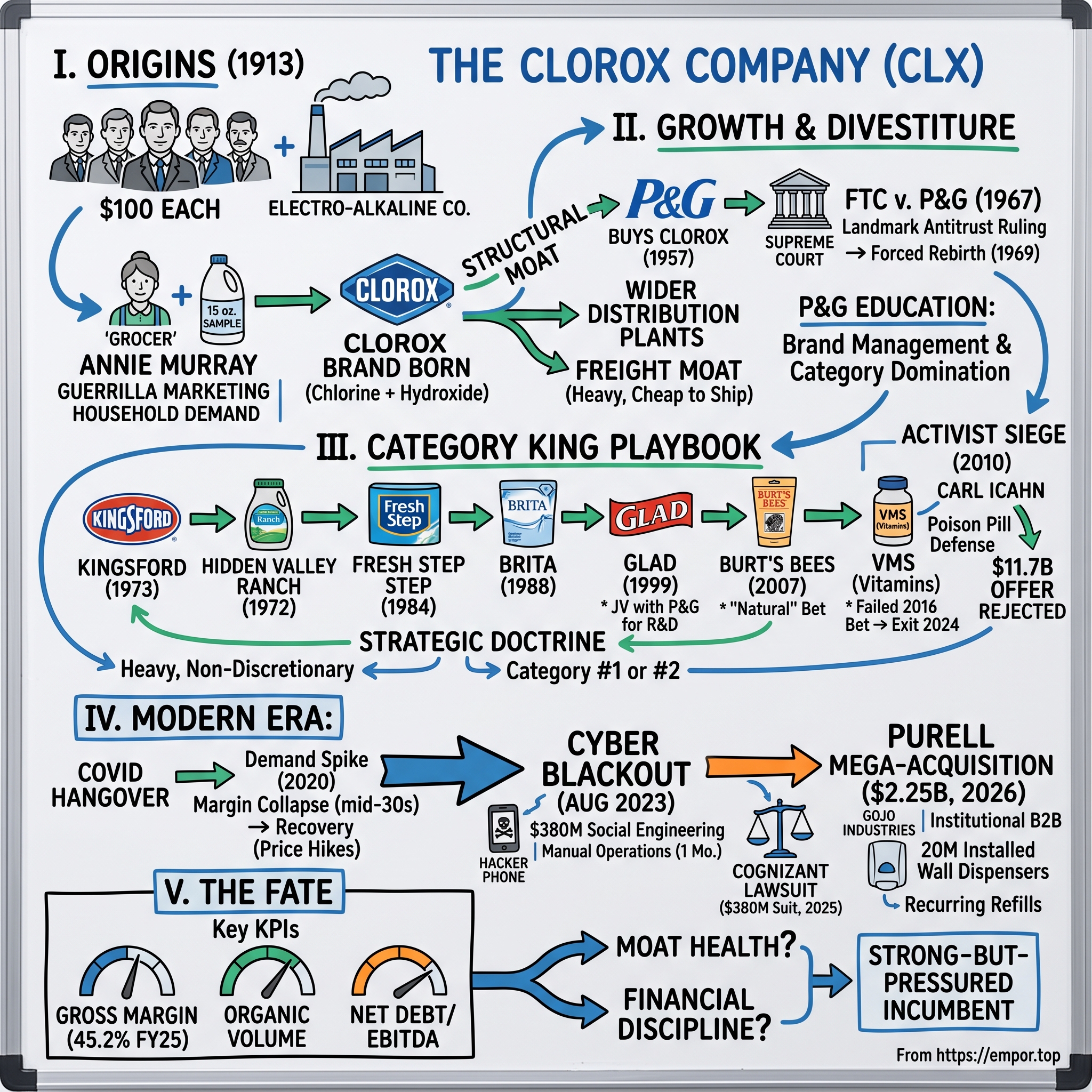

The Clorox Company: The Ultimate Brand Compounder and the $380M Social Engineering Disaster

I. Introduction & Episode Roadmap

Picture a Fortune 500 company—one whose products sit in roughly nine of every ten American homes—reduced, over a single August weekend in 2023, to running its multibillion-dollar order book on paper. Employees at The Clorox Company printed spreadsheets, phoned retailers to confirm shipments, and hand-tallied pallets of bleach and Glad bags while the automated systems that had quietly run the enterprise for decades sat dark. A company synonymous with hygiene and control had, for a few weeks, no control at all.

That image is the paradox at the heart of Clorox. Here is a business whose brand is so dominant that "Clorox" functions as a verb for disinfecting, whose portfolio spans trash bags, water filters, ranch dressing, charcoal, cat litter, and lip balm, and whose gross margins have historically rivaled those of far sexier consumer names. And yet its single most expensive event of the last decade was not a failed product launch or a botched acquisition—it was a phone call to an outsourced help desk.

The story only gets richer from there. In January 2026, Clorox announced its largest acquisition ever: a definitive agreement to buy GOJO Industries, the family-owned maker of Purell, for $2.25 billion in cash.1 The deal is a calculated bet that the future of hygiene profit lies not on retail shelves but bolted to the walls of hospitals, airports, and schools. Six months earlier, in July 2025, Clorox had filed a blockbuster $380 million lawsuit against Cognizant, the IT services giant that ran its help desk, alleging that Cognizant's agents simply handed network credentials to hackers who asked for them.2 Two enormous stories—one offensive, one defensive—unfolding at the same company, at the same time.

To understand how a 113-year-old bleach maker arrived at this moment, this article traces the full arc:

- The Origin Story: how five Oakland businessmen with no chemistry training pooled $100 each in 1913 to run electricity through Bay-water brine—and how a co-founder's wife saved the company by inventing the consumer market for it.

- The Antitrust Exile: how Procter & Gamble bought Clorox, and how the U.S. government's landmark legal war (FTC v. Procter & Gamble Co., 1967) forced Clorox's independent rebirth—and handed it an education in brand management it would spend fifty years exploiting.

- The Category King Playbook: how Clorox replicated bleach-like economics in unrelated niches—charcoal, salad dressing, cat litter, trash bags—by buying #1 and #2 brands in heavy, hard-to-ship, unglamorous categories.

- The COVID Hangover and Cyber Breach: how CEO Linda Rendle managed a demand super-spike, a brutal margin collapse, and then an operational blackout.

- The Modern Investment Case: exiting a failed vitamins bet, debt-financing Purell, and stress-testing Clorox's economic moat against the frameworks investors actually use.

Throughout, the posture here is neutral. Clorox tells a confident story about brands, scale, and switching costs. The job of this piece is to ask what evidence supports that story—and what could break it.

II. Oakland Origins: Five Men, $100 Each, and the Oakland Estuary

On May 3, 1913, on the east shore of San Francisco Bay, five men who between them knew almost nothing about chemistry incorporated a company to make it.3 There was a banker, a coal-and-wood merchant, a bookkeeper, a lawyer, and a miner. Each put in $100—roughly a month's wages for a skilled worker of the era—and together they founded the Electro-Alkaline Company, America's first commercial-scale liquid bleach factory.3 The name told you everything about how little they were thinking about consumers: it described the process, not the product.

The science was elegant in its simplicity and grueling in its practice. Salt brine, drawn from the briny estuary, was pumped into vats and hit with an electrical current. Electrolysis split the sodium chloride and recombined it into sodium hypochlorite—concentrated liquid bleach. It was a genuinely modern chemical process at a time when most American laundries still whitened linens with harsh powders and sunlight. On paper, the founders had a technological edge.

In practice, they had a commercial disaster. The original plan targeted industrial buyers—commercial laundries, breweries, canneries—with heavy drums of powerful bleach. But the product was maddeningly unstable, losing potency in storage. It was expensive to ship because, chemically speaking, bleach is mostly water. And it was unknown, unbranded, and untrusted. Within three years the company was circling the drain. In 1916, an investor named William Murray stepped in, took control, and installed himself as general manager to try to salvage the wreck.3

Annie Murray and the invention of the customer

The turnaround did not come from the factory floor. It came from Murray's wife, Annie, who ran the family's grocery store in downtown Oakland and understood something the five founders never had: there was no market for industrial bleach in Oakland, but there might be an enormous one for household bleach—if only someone made a version a homemaker would actually pour near her family's clothes.

Annie Murray pushed for a gentler, less concentrated formula, diluted to a household-safe strength and sold in a modest amber bottle. She reportedly hand-labeled bottles and gave away fifteen-ounce samples to customers at the store, seeding demand one household at a time.3 It was guerrilla marketing before the term existed, and it worked. Housewives discovered that a splash of the stuff whitened laundry, scrubbed sinks, and—crucially—killed the germs that early-twentieth-century public-health campaigns were teaching Americans to fear. The industrial flop had found its true customer at the kitchen sink.

The brand was christened by fusing the two ingredients at the heart of the chemistry—chlorine and sodium hydroxide—into a single, punchy, invented word: Clorox. In 1914 the company registered the name and its now-iconic diamond trademark.3 It is worth pausing on how good that branding instinct was for a company run by a grocer and a handful of amateurs. A made-up word, easy to say, impossible to confuse, wrapped in a distinctive geometric mark—this is the kind of brand architecture that consumer-goods conglomerates would later pay armies of consultants to design.

But the deepest early moat was not marketing; it was chemistry. Sodium hypochlorite wants to decompose. A bottle that lost its punch on the shelf—or worse, built up pressure and burst—would have destroyed consumer trust before it formed. Solving shelf-life stabilization, so that a bottle bought in spring still worked in autumn and did not explode in the pantry, was a real technical achievement in the 1910s and 1920s. It converted a commodity chemical into a reliable branded product, and reliability is the seed of trust.

The freight moat, discovered by accident

There is a second structural advantage buried in the early history that the founders stumbled into rather than designed, and it deserves attention because it explains the next hundred years of strategy. Bleach is, by weight, overwhelmingly water. A tanker of the stuff is a tanker of mostly H₂O with a small, potent fraction of active chemistry dissolved in it. That makes it ruinously uneconomic to ship long distances: the freight cost per bottle can rival or exceed the value of the contents.

For most businesses, that would be a curse. For an incumbent, it is a gift. It means that a rival in Ohio cannot profitably attack a producer in California, because the trucking bill destroys the rival's margin before it reaches the shelf. Each regional plant is, in effect, a small fortress with a moat made of diesel. Clorox learned early to build production close to demand—by 1917 it was already shipping east via the Panama Canal, and over the decades it assembled a dense national web of plants and distribution centers.3 What began as a logistics workaround hardened into one of the most durable cost advantages in American consumer goods.

Hold that thought. Decades later, when Clorox went looking for new categories to conquer, it would not search for the most glamorous products or the fastest-growing trends. It would search for products shaped like bleach: heavy, cheap, boring, and expensive to move.

Trust compounds through crisis

That trust compounded through crisis. Bleach proved itself a cheap, essential public-health tool through the influenza era, the Great Depression—when a product that made scarce goods last longer and homes sanitary earned fierce loyalty—and World War II, when disinfection was a wartime necessity. Each emergency did the same quiet work: it took a product people bought out of habit and re-established it as a product people needed, reinforcing the association between a brand name and personal safety.

This is the underappreciated engine of consumer-staples compounding. Brands in categories tied to health and fear do not merely accumulate customers; they accumulate trust, and trust is stickier than preference. A consumer who believes a product protects their family does not comparison-shop it with the same ruthlessness they apply to breakfast cereal. That psychological asymmetry is why, a century later, shoppers still pay a premium for a bottle of Clorox over chemically identical generic bleach—a fact we will return to when weighing whether the moat is real or merely inherited.

By mid-century, Clorox was not a niche cleaner; it was a household staple with near-monopoly status in liquid bleach, holding roughly half the national market and far more in some regions. That very dominance would soon make it a target—not of a competitor, but of the biggest consumer-products company in the world.

III. The Procter & Gamble Monopoly and the Supreme Court Showdown

By the mid-1950s, Clorox owned its category the way few consumer companies ever own anything. It held roughly half the U.S. liquid-bleach market, and in many regions far more. To Procter & Gamble, the Cincinnati colossus that had turned soap into a science, this looked less like a competitor and more like an acquisition waiting to happen. In 1957, P&G bought the Clorox Chemical Company.3

On its face, it was a natural fit. P&G had no bleach of its own but sold detergents, and bleach lived in the same aisle, the same wash cycle, the same shopping trip. P&G's distribution muscle and advertising budget could, in theory, make an already-dominant brand unassailable. That was precisely the problem.

The government goes to war

The Federal Trade Commission saw the acquisition not as a helpful product extension but as a threat to competition, and it challenged the deal under Section 7 of the Clayton Act, the statute that bars mergers whose effect "may be substantially to lessen competition." In 1963, the FTC ordered P&G to divest Clorox.3 P&G fought, and the case climbed all the way to the U.S. Supreme Court, which ruled against the merger in 1967 in FTC v. Procter & Gamble Co.

The decision became a landmark for two doctrines that still shape antitrust thinking. First was the product-extension merger theory: because P&G did not itself make bleach, the merger did not eliminate an actual competitor, but it eliminated a potential one—P&G was one of the few firms that could plausibly have entered bleach on its own and disciplined Clorox's pricing. Removing that latent threat, the Court reasoned, harmed competition. Second, and more striking, was the Court's treatment of advertising itself as a barrier to entry. P&G's ability to buy television and print advertising at enormous volume discounts, the Court found, would let the combined company outspend and overwhelm smaller bleach makers, raising the cost of entry and entrenching Clorox's dominance.

There is a delicious irony here for investors. The government's core objection was that Clorox's brand plus P&G's advertising machine would create an almost impregnable competitive position. In striking the deal down, the Court essentially certified, in a Supreme Court opinion, that Clorox possessed exactly the kind of durable advantage that value investors dream about.

The rebirth—and the education

P&G was forced to spin Clorox off, and on January 2, 1969, The Clorox Company returned to independence as a publicly traded firm.3 But the twelve years inside P&G were not wasted exile. Clorox's managers had spent more than a decade embedded in the company that literally invented modern brand management—the discipline of assigning a dedicated "brand manager" to own a product's profit-and-loss, positioning, advertising, and share, and pitting brands against one another to sharpen them. When Clorox walked out the door, it took that entire operating philosophy with it.

To appreciate why that education mattered, it helps to understand what brand management actually is. Before P&G formalized it in the 1930s, most companies organized around functions: manufacturing made things, sales sold them, advertising promoted them, and nobody owned the fate of any individual product. P&G's innovation was to put a single manager in charge of a single brand end-to-end—responsible for its positioning, its advertising, its pricing, its packaging, and above all its profit-and-loss statement. That manager had to defend their brand's share not only against outside rivals but against other P&G brands competing for the same shelf. The system produced a peculiar kind of executive: obsessive about market share data, fluent in consumer research, ruthless about killing what did not work, and temperamentally incapable of letting a brand drift.

Clorox absorbed that entire operating religion. And it absorbed something subtler too—P&G's understanding that in consumer goods, the category is the unit of competition. You do not want to be a strong player in a big market; you want to be the dominant player in a market you can defend. Better to own 60% of charcoal than 8% of soft drinks.

The strategic resolution

The strategic resolution that followed defined the next half-century: apply P&G's category-domination playbook to categories P&G did not touch. Clorox would not try to out-detergent Procter & Gamble—that was suicide, and everyone knew it. Instead it would hunt for unglamorous, defensible niches where a disciplined brand operator with national distribution could establish the kind of share that makes a category yours.

The antitrust exile, in other words, produced a company with an unusual combination: the operating sophistication of a global giant and the strategic humility of a specialist. Clorox knew exactly how to dominate a category, and it knew exactly which categories not to enter. The exile had been a graduate education, and Clorox was about to put it to work.

IV. The Playbook of Category Colonization & Strategic JV

Here is the strategic insight that turned a bleach company into a diversified compounder. Liquid bleach is a wonderful business in one respect and a terrible one in another. Wonderful, because the brand commands trust and pricing power. Terrible, because the product is mostly water—heavy, cheap per pound, and absurdly expensive to ship relative to its value. You cannot economically truck bleach across a continent to undercut a local incumbent; the freight eats the margin.

Clorox took that constraint and turned it into a doctrine. Instead of fighting it, the company went looking for other categories with the same shape: heavy, low-value-to-weight, unglamorous, and dominated by a #1 or #2 brand that a disciplined operator could feed with mass distribution. If freight costs protected bleach from distant competitors, they would protect charcoal and cat litter too. The commodity curse became a moat.

The screening criteria, reconstructed from the pattern of deals, look something like this. The category should be one where a brand can command a premium despite near-identical chemistry, because that premium is the profit. It should be heavy or bulky relative to its price, so geography does the defensive work. It should be purchased repeatedly and non-discretionarily, so demand is predictable through cycles. It should be big enough to matter but small or boring enough that a P&G or Unilever will not bother contesting it. And it should already have a #1 or #2 brand available to buy, because building brand trust from scratch takes decades that an acquirer does not have.

Run that filter across the American household and you get a remarkably specific shopping list—which is more or less exactly what Clorox bought.

Kingsford: turning backyards into a cash machine

Consider charcoal. It is literally burned lumps of carbon—heavy, bulky, cheap, and seasonal. It is also, once you own the leading brand, a beautiful business. Clorox acquired the Kingsford charcoal business in 1973 and rode America's postwar love affair with the backyard grill to a commanding share of the U.S. charcoal market.3 The economics rhyme perfectly with bleach: nobody is shipping briquettes across the country to steal share from the category leader, and every Fourth of July and Labor Day is, in effect, a recurring demand event Clorox owns.

Hidden Valley Ranch: the chemistry of a condiment empire

In 1972, Clorox bought the Hidden Valley Ranch dressing business—the recipe for a tangy, herby dressing that a Santa Barbara–area guest ranch had turned into a mail-order sensation.3 At the time it was a dry seasoning packet you mixed with mayonnaise and buttermilk. Clorox's contribution was, once again, chemistry: cracking the formulation to make a stable, bottled, shelf-ready liquid dressing. That innovation transformed a novelty mix into what would become the best-selling salad dressing in America and, eventually, a condiment found in a majority of U.S. refrigerators. Ranch went from a regional curiosity to a cultural default—on salads, pizza, wings, and vegetables—and Clorox owned the brand that defined it.

There is a lesson in Hidden Valley that generalizes across the whole portfolio. Clorox's most valuable contribution to the brands it bought was rarely marketing genius—it was industrial chemistry and distribution. It took a mail-order seasoning packet and solved the emulsion-stability problem that turned it into a bottled product a supermarket could stock for months. That is the same competence that stabilized sodium hypochlorite in 1915. Clorox is, underneath the brand names, a formulation-and-shelf-stability company, and it repeatedly bought good ideas that were trapped in a form the mass market could not distribute.

Fresh Step and the beauty of recurring necessity

Cat litter is the platonic ideal of a Clorox category: heavy, cheap to make, expensive to ship, and utterly non-discretionary. A cat owner buys litter forever, on a schedule, regardless of the economy. Clorox launched Fresh Step in 1984 and built it into a premium, high-margin franchise by leaning on clumping and odor-control technology that let it charge up for performance.3 The recurring, need-it-now nature of the purchase is exactly the kind of demand a brand compounder covets.

Brita: buying into the health trend

In 1988, Clorox signed agreements to bring Brita water-filtration products to North America, later taking full ownership of the North American business.3 It was a shrewd read of a cultural shift: as consumers grew wary of tap water and wanted "cleaner" hydration without buying endless plastic bottles, a filter pitcher with replaceable cartridges offered a razor-and-blades annuity. The pitcher is the razor; the filters, bought again and again, are the blades.

The Glad chess match

Glad is the most instructive story in the portfolio because it shows Clorox thinking three moves ahead. Clorox gained the Glad trash-bag business through its 1999 merger with First Brands, a deal that nearly doubled the company's size.3 Then came the corporate chess: rather than compete head-on with Procter & Gamble in premium plastic bags, Clorox in 2002 struck a joint venture with its old parent. Clorox would own the majority stake and run the business day-to-day; P&G would take a minority interest and contribute cutting-edge polymer and film R&D—the technology behind stretchable, puncture-resistant innovations like ForceFlex.

Read what that structure actually accomplished. It gave Clorox access to a world-class materials-science lab it did not have to build. It aligned P&G's interests with Clorox's success rather than against it. And most cleverly, it neutralized the single most dangerous potential entrant in the category: by making P&G a partner and profit-sharer in Glad, Clorox removed P&G's incentive to launch a rival premium bag. It was a peace treaty dressed as a joint venture—the same "potential competition" logic the Supreme Court had wielded in 1967, now used by Clorox to its own advantage.

The elegance is worth dwelling on, because it is the single best illustration of institutional memory paying a dividend. In 1967, the Supreme Court had told the world that P&G's potential entry into a category was itself a competitive force worth protecting. Clorox had lived that ruling from the inside. Thirty-five years later, facing the prospect of P&G entering trash bags for real, Clorox did not fight it and did not wait to be attacked. It bought off the threat by making the threat a shareholder. The company understood, better than almost anyone, exactly how dangerous P&G's latent capabilities were—because a court had once dismantled Clorox's ownership over precisely that question.

For investors, the Glad JV is also a useful reminder that not every moat is a wall. Some are treaties. And treaties, unlike freight economics or brand trust, depend on a counterparty's continued willingness to honor them—which makes them real, valuable, and inherently less permanent than the moats that come from physics.

The Burt's Bees gamble: paying up for "natural"

Then, in 2007, Clorox did something that looked completely out of character. It paid $925 million to buy Burt's Bees, the earnest, beeswax-lip-balm-and-natural-personal-care brand, from private-equity firm AEA Investors. The price was roughly thirteen times trailing sales—a staggering multiple for a consumer deal at a time when comparable personal-care acquisitions changed hands at something closer to three to five times sales.

Why would a company famous for buying heavy, cheap, defensible commodities pay a luxury-growth multiple for lip balm? The bet was twofold. First, Clorox was buying a demographic and a trend—"natural," clean-label personal care—that its bleach-and-charcoal portfolio could not organically reach, and that it believed would grow for a generation. There is a real strategic anxiety underneath that: a company whose brands are built on chemicals was watching a consumer shift toward natural, and Burt's Bees was a hedge against its own portfolio going out of fashion. Second, it was buying a distribution arbitrage. Burt's Bees lived in natural-foods stores and specialty channels; Clorox could push it into the mass grocery, drug, and big-box shelves where Clorox already had shelf power, expanding it from a lip-balm niche into a broad natural personal-care line.

But note how thoroughly this deal violated the company's own screening criteria. Lip balm is light, not heavy—no freight moat. It is discretionary, not essential. The category was trendy and therefore attractive to exactly the giants Clorox's doctrine said to avoid. And the price paid was a growth multiple in a company built on buying cash flow cheaply. Burt's Bees was not category colonization; it was trend-chasing with a strong balance sheet.

Whether the thirteen-times price was ever fully justified remains a fair debate—Burt's Bees did grow into a meaningful franchise inside the Lifestyle segment, but "grew into a decent business" is a low bar for a $925 million check. The deeper significance is what it revealed about the company's central tension. The category-colonization model throws off enormous cash but grows slowly, because heavy, boring categories are heavy, boring categories. Public markets demand growth. So Clorox found itself repeatedly tempted to buy growth at prices its own doctrine would never have sanctioned—a temptation that would resurface, disastrously, with vitamins a decade later.

That tension between defensive cash flow and offensive growth would define the next fifteen years. And in 2010, a famous investor noticed that a company generating that much cash while growing that slowly is, in the language of Wall Street, a target.

V. The Activist Siege: Carl Icahn's $11.7B Run on Bleach

By late 2010, a company whose brands quietly minted cash had caught the eye of the most feared investor in America. Carl Icahn—the corporate raider turned "activist," the man who had spent four decades telling boards they were sitting on lazy money—began quietly accumulating Clorox stock. By the time the market understood what was happening, he had built a stake of roughly 9.4%, making him Clorox's single largest shareholder.4

Icahn's thesis was vintage Icahn, and it was not stupid. Clorox, he argued, was a "sitting duck": a collection of category-leading brands with predictable cash flows that would be worth far more inside a global consumer conglomerate than as a standalone company. A larger owner—he floated Procter & Gamble, Unilever, Kimberly-Clark, and others—could strip out hundreds of millions in duplicated corporate overhead, plug Clorox's brands into a worldwide distribution machine, and unlock value that Clorox's own management, in his telling, was too complacent to capture.

The bid

In July 2011, Icahn stopped whispering and made an unsolicited offer: roughly $10.2 billion, or $76.50 per share, to take the whole company.4 When the board brushed it off, he raised it—ultimately to about $11.7 billion, backing the bid with billions in committed financing arranged through Jefferies and even a personal guarantee against a portion of the breakup risk to signal he was serious.4 It was a genuine, financed, hostile run at a beloved American staple.

The defense

Clorox's board, led by CEO Donald Knauss, did not blink. It retained Wachtell, Lipton, Rosen & Katz—the law firm that had literally invented the modern "poison pill"—and adopted a shareholder rights plan designed to make any hostile accumulation prohibitively dilutive.5 The board rejected each iteration of the offer, arguing that Icahn's price undervalued Clorox's standalone cash flows and that his "just sell the company" plan depended on a buyer who did not, in fact, exist.5

That last point was the fatal flaw in Icahn's thesis, and it is where the story turns into a lesson about moats. Icahn needed a strategic acquirer to actually pay up. But the very qualities that made Clorox valuable also made it un-buyable by the obvious suitors. P&G, the natural buyer, would have faced brutal antitrust problems in bleach and bags—the same overlaps the government had blocked in 1967 and structured around in the Glad JV. Other conglomerates feared similar category concentration or simply had no appetite for a bidding war. With no white knight materializing and Clorox's shareholders content to collect a stable, growing dividend, Icahn's leverage evaporated.

He walked away, selling down his stake without forcing a sale.

What the siege proved

For long-term investors, the episode is more than a colorful raid; it is a natural experiment that stress-tested the business model in public, with a motivated adversary and real money on the line. Three findings are worth keeping.

First, the moat was confirmed from an unexpected direction. Icahn's plan died because no strategic buyer could clear antitrust—and the reason antitrust was a problem is that Clorox's share in its core categories was so high that combining it with any logical acquirer would concentrate the market. The company's competitive strength was, paradoxically, the thing that made it impossible to sell. A business can be so dominant that it becomes un-acquirable, and that is a strange and durable form of protection for a standalone shareholder.

Second, shareholder behavior revealed the quality of the cash flows. Icahn was offering a substantial cash premium, and shareholders declined it—not because they loved management, but because they believed the dividend stream and the brand portfolio were worth more held than sold. That is a market verdict on durability, delivered under the most adversarial conditions available.

Third—and this is the honest counterpoint—Icahn was not wrong about everything. His critique that Clorox carried conglomerate overhead across a sprawling, unrelated portfolio, and that its growth did not justify its complexity, was a legitimate observation. It is essentially the same question a skeptic would ask today about a company selling bleach, charcoal, ranch dressing, water filters, lip balm, and hand sanitizer under one roof. The siege did not settle that debate; it merely postponed it.

What the episode did change was management psychology. The clearest lesson a board draws from surviving an activist is that the surest defense is a fat, visible operating margin—nothing repels a "you're mismanaging this" narrative like best-in-class profitability. Clorox spent the following decade obsessed with margin discipline, and that obsession served it well. Right up until a global pandemic made margin the least of its problems.

VI. The COVID Bubble and the Gross Margin Hangover

In September 2020, Linda Rendle became CEO of The Clorox Company at age 42, a 17-year company veteran stepping into the top job at the single strangest moment in the history of the cleaning business. The world was terrified of an invisible pathogen, and Clorox made the products people believed stood between them and it. It is hard to imagine a more intense trial by fire—or a more deceptive one.

Rendle was, in the classic mold, a company lifer. She had joined Clorox out of college and spent nearly two decades climbing through the brand and sales organization—the same P&G-descended apprenticeship system that produced generations of Clorox managers who knew the difference between a share point won on merchandising and a share point won on advertising. She ran the Cleaning division, then became president, then CEO. This matters for how investors should read her decisions: she is not a turnaround artist parachuted in from private equity with a mandate to break things. She is a product of the culture, which tends to make executives excellent at defending and optimizing an existing franchise and, historically at least, less proven at deploying billions into something new.

Her timing was extraordinary. A CEO's first year normally offers a grace period to study the business and set an agenda. Rendle got a demand shock instead.

Demand for disinfecting wipes, bleach, and cleaning sprays did not rise; it detonated. At the peak, demand for some products ran hundreds of percent above normal. Wipes vanished from shelves for months and became a kind of social currency—hoarded, gifted, traded, photographed. For a company that had spent a century preaching hygiene, it was vindication and chaos in equal measure. Clorox could sell every wipe it could make and still leave shelves empty.

IGNITE and the scramble for capacity

Rendle leaned into a strategy the company branded IGNITE—an agenda of digital-first marketing, supply-chain automation, and more personalized consumer engagement. But the immediate imperative was brutally physical: make more product, now. Clorox threw money at the problem, aggressively expanding third-party contract manufacturing, adding lines, and building out logistics capacity to chase demand that felt, in 2020, like it might never end.

It ended. As vaccines rolled out and pandemic anxiety faded, consumer behavior reverted toward its long-run trend with startling speed. And Clorox was left holding the bill for a demand curve that had been a spike, not a step-change: excess capacity, expensive contract-manufacturing commitments signed at peak urgency, and inventory dynamics that whipsawed as retailers worked down the stockpiles they had frantically built.

The margin collapse

Then the macro environment turned on it. Just as volumes normalized, input costs exploded. The price of plastic resin (for bottles and bags), corrugated cardboard, agricultural oils (a key input for Hidden Valley), and domestic freight all surged in the 2021–2022 inflation wave. A company whose gross margin had for years sat in a comfortable, stable mid-40s band watched that margin buckle into the mid-30s—a collapse of roughly ten percentage points that, for a consumer-staples business, is a genuine crisis. The stock reflected the pain.

What does that collapse actually tell an investor? Two things, and they point in opposite directions. On the bearish side, it revealed that Clorox's famous stability is not immune to cost shocks—when several commoditized inputs inflate at once, even a strong brand portfolio bleeds margin, and the company's peak-demand capacity decisions amplified the damage. On the bullish side, the recovery revealed something about pricing power. Rendle's playbook was blunt and effective: successive rounds of price increases across the portfolio, paired with a serious cost-restructuring program to wring out the excess capacity and overhead accumulated during the boom. Retailers, by and large, accepted the price hikes—evidence that consumers would pay up rather than abandon the brands—and margins clawed back toward the 43% range by fiscal 2024, and to 45.2% in fiscal 2025.6

That recovery is the strongest single piece of evidence for Clorox's pricing power in the modern era. When a company can raise prices repeatedly across a portfolio, hold its retail distribution, and rebuild a ten-point margin hole, it has demonstrated something that no investor presentation can assert into existence: customers who will absorb a higher price rather than switch. That is the definition of brand power, measured in cash rather than adjectives.

The bear's reading of the same facts

But a skeptic reads the identical evidence differently, and the skeptical case deserves a fair hearing. Price increases during a broad inflationary wave are the easiest kind to push through, because every brand on the shelf is raising prices simultaneously and the consumer has nowhere to flee. That is not the same as pricing power in a stable-cost environment, where a lone price hike sends shoppers straight to the competitor. The real test comes later, when input costs normalize and retailers start asking why prices have not come back down.

There is a second, subtler concern buried in a price-led recovery: it can mask volume erosion. If revenue holds because each unit costs more while the number of units quietly shrinks, the margin line looks healthy while the franchise slowly hollows out. Consumers do not usually abandon a trusted brand in one dramatic switch; they buy the store brand once, discover it is tolerable, and drift. By the time that shows up in the numbers, the habit is broken.

This is precisely why disentangling price from volume became—and remains—the single most important analytical exercise for anyone underwriting Clorox. Management earned real credit for the margin rebuild. Whether it was bought with durable brand equity or with a temporary inflationary window in which all prices rose together is a question the next few years will answer.

Before that question could be fully answered, however, the company faced a threat that had nothing to do with resin prices or ranch dressing—and everything to do with a phone call.

VII. The $380M Social Engineering Cyber-Catastrophe & The Cognizant Lawsuit

The most expensive attack in Clorox's history did not require a single line of malicious code to breach the perimeter. It required a telephone and a convincing voice. In August 2023, a hacking collective widely identified as Scattered Spider—a loosely organized, English-speaking group notorious for social engineering rather than technical wizardry—set its sights on Clorox.2 Scattered Spider's signature move is not to defeat security software; it is to defeat people, talking their way past the humans who hold the keys.

The help-desk vulnerability

Clorox had outsourced its IT help desk to Cognizant, one of the largest IT-services firms in the world. According to the lawsuit Clorox later filed, the attack was almost insultingly simple. On August 11, 2023, a cybercriminal phoned the Cognizant service desk, claimed to be a Clorox employee, and asked for a password reset and a multi-factor authentication reset. Cognizant's agents, Clorox alleged, did not follow basic identity-verification protocols—they did not confirm the caller was who he claimed to be—and reset the credentials anyway, in effect handing over the keys to Clorox's network.2 In the words of Clorox's complaint, as reported, "The cybercriminal just called the Cognizant Service Desk, asked for credentials to access Clorox's network, and Cognizant handed the credentials right over."7

It is worth pausing on why this works, because the mechanism is the whole story. Multi-factor authentication—the second code from your phone—exists precisely to make a stolen password useless. But every MFA system needs an escape hatch for the employee who genuinely loses their phone, and that hatch is the help desk. A human being with the authority to say "yes, I believe you, here is a new credential." Scattered Spider's entire business model is to find that human. All the encryption, firewalls, and endpoint monitoring in the world route around a person authorized to reset the lock, and the only control protecting that person is a verification script and the discipline to follow it every single time.

Once inside with valid administrator-level access, the attackers were not "hackers" in any technical sense—they were, as far as the systems could tell, legitimate Clorox administrators. That is what makes credential-based intrusion so pernicious: the security tools have nothing to detect. The traffic is authorized. When Clorox identified the intrusion in mid-August, it made a defensive decision that was correct in security terms and catastrophic in operational terms: it took its own network offline to contain the damage, shutting down automated order-processing and warehouse-management systems to stop the attackers from spreading laterally.

That choice deserves sympathy rather than second-guessing. Faced with an adversary holding administrator credentials inside your network, the alternative to pulling the plug is letting them roam—potentially into financial systems, customer data, or the industrial controls that run manufacturing. Clorox chose a certain, enormous, short-term operational loss over an uncertain, potentially existential one. It was almost certainly the right call. It was also spectacularly expensive.

The manual era

For roughly the next month, one of America's most sophisticated consumer-products companies operated like it was 1955. With the automated systems dark, employees processed retailer orders by hand—clipboards, phone calls, manual spreadsheets. Manufacturing ran at a fraction of capacity because the systems that scheduled production and tracked inventory were offline. The result rippled straight to store shelves: gaps where Clorox wipes, bleach, Glad bags, and Kingsford charcoal were supposed to be.

The episode exposed something that applies far beyond Clorox. Decades of supply-chain optimization have removed almost every buffer from the modern consumer-goods business: inventory is lean, production is scheduled algorithmically against real-time demand signals, and orders flow machine-to-machine between manufacturer and retailer with no human in the loop. That efficiency is a genuine competitive advantage—until the machines stop. Then you discover that the institutional knowledge of how to run the company manually retired twenty years ago, and that a system optimized to hold three days of inventory has three days before the shelves empty.

There is a grim irony in the specifics, too. Clorox's greatest categories are the ones people buy on autopilot, on habit, without deliberation. That habit is worth a fortune when the product is there. It is worth nothing when it isn't—because a habitual shopper facing an empty slot does not wait. They reach one shelf over.

The financial damage was severe and concentrated. In the first quarter of fiscal 2024—the quarter that absorbed the brunt of the disruption—net sales fell 20% to $1.4 billion, driven by the volume the company simply could not ship.8 In early October 2023, Clorox had warned investors that the hit would be far worse than any normal quarter, slashing its outlook and disclosing that the attack would materially depress results.9 Direct remediation—IT restoration, forensics, and security consulting—cost roughly $49 million.8 But the far larger number was the business it lost: in its subsequent lawsuit, Clorox pegged total damages at approximately $380 million, of which about $50 million was clean-up cost and roughly $330 million was attributed to its inability to ship product to retailers in the attack's aftermath.2

There is a competitive sting inside that number. Retail shelf space is not neutral ground; it is contested territory, and empty shelves invite invasion. While Clorox's wipes and sprays were missing, rivals like Reckitt's Lysol and lower-priced private-label store brands had an open lane to win placement and trial. Some of that share is recoverable; some, in categories where habit is sticky, may not be. The true cost of the breach is therefore partly unknowable—it lives in a counterfactual of sales that never happened and customers who never came back.

The lawsuit as a test case

In July 2025, Clorox took the fight to court, filing suit against Cognizant in California Superior Court and alleging gross negligence, breach of contract, and related claims.2 Cognizant, for its part, has pushed back hard, arguing that it provided only a "narrow scope" of help-desk services and that responsibility for Clorox's overall security architecture—and for the decisions that turned a credential reset into a company-wide shutdown—rests with Clorox itself.10

Strip away the specifics and this is a landmark liability question for the entire economy: when a company outsources a critical function and the vendor's employees fail at a basic task, who eats the loss?

Both sides have a real argument, which is exactly why the case matters. Clorox's position has intuitive force—it paid a professional vendor to perform a security-sensitive function, that vendor allegedly ignored its own verification protocol, and the direct consequence was a nine-figure loss. If that is not negligence, the word means very little. Cognizant's position is also not frivolous: help-desk contracts are typically priced as low-margin, high-volume commodity services, with liability caps that bear no relationship to the client's enterprise value. A vendor earning modest fees to reset passwords cannot rationally underwrite the entire business-interruption risk of a Fortune 500 manufacturer. And Cognizant will surely argue that a credential reset should not, in a well-architected environment, be able to cascade into a company-wide shutdown—that Clorox's own security design turned a vendor error into a catastrophe.

The outcome will help define how much legal responsibility IT-outsourcing firms bear for their clients' cyber disasters, and the second-order effects could be significant: a decisive Clorox win would likely reprice outsourced IT contracts across the industry, forcing vendors to carry more insurance and charge accordingly. For investors in Clorox specifically, the case is a live, binary overhang—a potential non-dilutive cash recovery if it succeeds, and a permanent reminder of concentrated third-party risk regardless of outcome. Litigation of this scale is slow, and a prudent analysis assigns it option value rather than counting the $380 million as an asset.

The breach also crystallized a strategic lesson that would shape the company's next move. Clorox's retail business had just demonstrated its central weakness in the most expensive way possible: when the product vanished, customers switched instantly, because on a retail shelf nothing stops them. The most valuable hygiene revenue, it turns out, is the kind customers cannot easily walk away from. Which is precisely what Clorox went shopping for.

VIII. Portfolio Cleansing and the $2.25B Purell Mega-Acquisition

Before Clorox could make its biggest offensive bet, it had to admit a mistake. In 2016, the company had pushed into vitamins, minerals, and supplements (VMS), assembling a "Better Health" portfolio of brands like RenewLife, Rainbow Light, Natural Vitality, and NeoCell. The logic—ride the wellness wave—echoed the Burt's Bees playbook. The execution never worked. The VMS business was fragmented, volatile, competitively brutal, and dilutive to the very margins Clorox had fought so hard to protect.

Cutting the VMS drag

Why did it fail? Because vitamins violate nearly every rule that makes Clorox's core categories good. Supplements are light and cheap to ship, so there is no freight moat. Barriers to entry are trivial—anyone can contract-manufacture a bottle of fish oil—which is why the category is crowded with hundreds of brands and relentless private-label attack. Consumer loyalty is weak and fashion-driven, rotating with whatever ingredient the internet is excited about this year. And the retail environment is dominated by exactly the kind of promotional intensity that destroys margins. Clorox bought into a category where its two great weapons—brand trust and distribution scale—simply did not confer the advantage they do in bleach.

On September 10, 2024, Clorox completed the divestiture of the entire Better Health VMS business to an affiliate of Piping Rock Health Products, swallowing an after-tax loss of about $118 million on a business that represented roughly 3% of fiscal 2024 sales.11 Management framed the exit as part of a deliberate effort to reduce volatility and structurally improve margins.11

Read honestly, this is a two-sided fact. It was an admission that the 2016 diversification had been a value-destroying detour—the same trend-chasing impulse that produced the Burt's Bees multiple, repeated with worse results. Investors are entitled to ask why a company with such a clear, well-tested acquisition doctrine keeps wandering away from it. But the willingness to take the loss, exit cleanly, and shrink the company rather than defend a sunk cost is genuinely the kind of capital-allocation discipline that separates good staples operators from empire-builders. Plenty of management teams would have spent another five years insisting the turnaround was imminent.

The VMS exit cleared the decks, financially and strategically. It also set an expectation—of discipline, of focus, of a smaller and sharper portfolio—that made what came next all the more striking.

The Purell blockbuster

On January 22, 2026, Clorox announced the largest acquisition in its history: a definitive agreement to acquire GOJO Industries, the family-owned Akron, Ohio maker of Purell, for $2.25 billion in cash.1 Crucially, the deal carried an estimated $330 million of tax benefits, bringing the net purchase price to roughly $1.92 billion.1 Clorox completed the acquisition on April 1, 2026, and told investors it expected the deal to become accretive to earnings per share beginning in fiscal 2027.1

Now compare the discipline of this deal to the 2007 Burt's Bees splurge. GOJO generated roughly $800 million in annual sales, so the net price of about $1.92 billion worked out to something in the neighborhood of 2.4 times sales—a world away from the thirteen-times multiple Clorox paid for lip balm. This was not a growth-at-any-price bet on a trend. It was a value-conscious acquisition of an entrenched, cash-generative franchise.

Why Purell is a different animal

The strategic heart of the deal is who buys Purell. More than 80% of GOJO's sales come through business-to-business institutional channels—hospitals, schools, airports, offices, restaurants—rather than the retail shelf.1 That B2B skew is the whole point, and it hands Clorox's professional division, Clorox Pro, something its consumer business could never build organically: an installed base of roughly 20 million Purell soap and sanitizer dispensers already mounted on walls across institutional America.1

Think of it as razor-and-blade economics, executed in concrete and steel. Once a hospital bolts Purell dispensers throughout its wards, the switching cost is not just contractual—it is physical. Those dispensers accept proprietary refills designed for their specific locking mechanisms. To switch sanitizer brands, a facilities manager would have to rip out and replace thousands of wall units, retrain staff, and disrupt an infection-control system that is literally life-and-death. So the institution keeps buying Purell refills—high-margin, recurring, non-discretionary consumables—more or less indefinitely. It is the Brita filter model, scaled to the industrial hygiene of an entire hospital system, and it is precisely the kind of hard-to-switch revenue that the 2023 breach taught Clorox to prize.

The B2B buyer also behaves nothing like a retail shopper, and that difference is the strategic prize. A consumer in a supermarket aisle is price-sensitive, disloyal, and one shelf away from a private-label substitute. A hospital infection-control director is none of those things. Their downside from switching to a cheaper sanitizer that staff dislike—and therefore use less—is not a few dollars of margin; it is a hospital-acquired infection outbreak, regulatory scrutiny, and litigation. In that calculus, the cost of the sanitizer is a rounding error against the cost of being wrong. This is why institutional hygiene supports pricing that retail never could, and why a dispenser network is worth more than the sum of its plastic.

There is also a genuine strategic fit, not just financial engineering. Clorox Pro already sold disinfecting products into many of the same institutions through many of the same distributors. Adding Purell means the same salesforce, calling on the same facilities manager, can now sell surface disinfection and hand hygiene—the two halves of an infection-control program—as a bundle. Cross-selling synergies are the most over-promised item in the M&A lexicon, and skepticism is warranted until the numbers show it. But the channel overlap here is real and specific, which is more than can be said for most deal decks.

The bear's questions about Purell

A fair analysis has to name the risks, and there are three worth watching. First, GOJO's revenue base is a post-COVID normalization story: hand-sanitizer demand exploded in 2020 and has been settling since, and an acquirer buying into that curve must be confident it has found its floor rather than catching a still-falling knife. Second, the dispenser moat depends on patents and proprietary fittings that do not last forever—when key patents lapse, third parties can make compatible refills, and the razor-and-blade model erodes into ordinary competition. Third, Clorox is a consumer-marketing company at heart; running a large institutional B2B business is a genuinely different discipline of contracts, distributors, and specification selling. Its track record outside consumer packaged goods is, as VMS demonstrated, mixed.

The debt overhang

But the deal is not free of risk, and the credit market said so immediately. Because the $2.25 billion is being funded primarily with debt, S&P Global placed Clorox on CreditWatch Negative on the day of the announcement, flagging that the transaction would push leverage meaningfully higher—reportedly toward roughly 3.6x EBITDA at closing.12 Management laid out a deleveraging path back toward about 2.5x by the end of calendar 2027 while pledging to protect the dividend.12 That pledge matters enormously: Clorox is a Dividend Aristocrat with a decades-long streak of annual increases, and a leverage misstep or a downgrade could put both the credit rating and the dividend narrative under strain. The Purell deal is thus a genuine test of management's promise of financial discipline—a big, levered swing taken while the company is still recovering from operational shocks. Whether it pays off depends on the durability of the moats it is buying, which is where the analysis turns next.

IX. The Clorox Moats: 7 Powers, Segment Economics & Competitive Benchmarking

To judge whether Clorox can win from here, it helps to see the machine in cross-section. In fiscal 2025, the company generated $7,104 million in net sales across four reportable segments, and each tells a different story about margin, defensibility, and risk.6

Segment economics

Health and Wellness ($2,697 million, ~38% of sales) is the profit engine and the strategic core.6 It houses Clorox disinfecting products, professional cleaning through Clorox Pro, and now GOJO/Purell. This is the highest-margin, most defensible part of the business—and the segment into which the Purell installed base plugs directly. Its growth is the clearest expression of Clorox's thesis that hygiene, especially institutional hygiene, is a structurally advantaged category.

Household ($2,001 million, ~28% of sales) is Glad, Kingsford, and Fresh Step—the heavy, freight-protected commodity brands.6 Market shares are high, but so is exposure: resin inflation hits Glad, charcoal is seasonal and weather-dependent, and these categories are the most vulnerable to consumers trading down to private label when budgets tighten.

Lifestyle ($1,303 million, ~18% of sales) is Hidden Valley, Brita, and Burt's Bees—higher-growth, higher-loyalty, more emotionally resonant brands.6 This is where Clorox looks least like a bleach company and most like a modern branded-consumer play.

International ($1,065 million, ~15% of sales) has been deliberately slimmed down.6 After exiting high-risk, hyperinflationary markets like Argentina, Clorox has narrowed international toward more defensible, higher-margin corridors—another example of the same portfolio discipline that killed VMS.

That international footprint deserves a moment of honesty, because it is the clearest structural limit on the whole thesis. At roughly 15% of sales, Clorox is overwhelmingly a domestic American company—and that is not an accident of ambition but a consequence of its model. The freight economics that protect Clorox at home work against it abroad: you cannot export bleach or charcoal profitably, so international expansion requires building local plants in each market, competing against local incumbents with their own freight moats, and doing it without the brand trust that took a century to accumulate in the United States. The same physics that make the domestic business so defensible make global expansion structurally hard. Investors hoping for an international growth story should understand they are hoping against the company's own economics. Growth, for Clorox, has to come from new categories or new channels—which is precisely why Purell matters so much.

Hamilton Helmer's 7 Powers

Helmer's framework asks which durable "powers" actually protect a business's returns. Clorox scores on several, but with important asymmetries worth naming honestly.

Brand (strong). This is Clorox's signature power. "Clorox" is a verb; Hidden Valley defines ranch; Kingsford defines charcoal. The economic proof is that a bottle of Clorox bleach commands a price premium over chemically identical generic sodium hypochlorite—consumers pay for the trusted label, not the molecules. That psychological preference is what let Clorox push through the post-COVID price hikes that rebuilt its margins.

Scale Economies (strong, and unusually literal). For the heavy commodity brands, Clorox's dense domestic network of plants and distribution centers is a genuine cost barrier. The low value-to-weight of bleach, charcoal, and litter means freight economics punish anyone trying to serve the U.S. from afar—the same insight that started the whole category-colonization strategy. This is a real, structural, geographic moat, but note it is strongest exactly where the brand power is weakest (commodities), and it does little against a domestic private-label maker with its own local plants.

Cornered Resource (moderate). The exclusive Glad joint venture with P&G, which supplies proprietary polymer technology and keeps the most dangerous competitor onside, is a cornered resource of sorts. So too are GOJO's patented dispensing systems and refill mechanisms. These are real but bounded advantages, dependent on patents and contracts that do not last forever.

Switching Costs (high in B2B, near-zero in B2C). This is the crucial asymmetry. On the retail shelf, a shopper faces essentially zero cost to grab the store brand instead—which is exactly why Clorox must spend heavily, historically on the order of 10% of sales, on advertising to keep its brands top-of-mind and defend against private label. In the institutional world, by contrast, those 20 million wall-mounted Purell dispensers create the kind of real switching cost that consumer brands almost never enjoy. The entire strategic logic of the Purell deal is to buy the switching-cost power that Clorox's retail business structurally lacks.

Notably absent from Clorox's power set are network economies and process power in any meaningful degree—Clorox does not get stronger as more people use it in a network sense, and its manufacturing, while efficient, is not a secret others cannot replicate. The moat is brand plus scale plus, now, institutional switching costs. That is a good hand. It is not an infinite one.

Porter's Five Forces

Run Clorox through Porter's lens and the picture is a strong-but-pressured incumbent. Rivalry is intense: Reckitt's Lysol fights Clorox in disinfecting, Church & Dwight's Arm & Hammer battles Fresh Step in litter, and private-label brands attack across the board. Buyer power is high and concentrated—giant retailers, led by Walmart, account for a large share of Clorox's sales (Walmart alone historically well over 10%), giving them enormous leverage on price and terms. Clorox's defense against that buyer power is to own the "must-stock" category leaders a retailer cannot afford not to carry. The threat of substitutes is the private-label question in another form: if store brands are "good enough," the premium erodes. Supplier power showed its teeth in 2021–2022, when commodity suppliers effectively dictated a margin collapse. And the threat of new entrants is low in the heavy commodity categories (freight and scale protect them) but real in the trend-driven Lifestyle categories.

The private-label question, examined properly

Because private label is the single most cited bear argument against every consumer staple, it deserves more than a mention. The theory is simple: store brands offer identical chemistry at a lower price, retailers earn better margins on them and therefore promote them, and over time the branded premium collapses.

The counter-evidence in Clorox's case is that this has been predicted for forty years and has not happened, at least not in the core. Clorox bleach still commands a premium over an identical molecule. That persistence tells us something important: in categories tied to family health and safety, the branded premium is not paying for performance—it is paying for the elimination of doubt. A shopper buying bleach to disinfect a kitchen after handling raw chicken is not optimizing for forty cents; they are buying certainty.

But the bear has a real rejoinder, and it is about which categories. That certainty premium is strongest exactly where the stakes feel highest—disinfecting, hygiene—and weakest where the product is functionally obvious. Nobody feels existential risk about a trash bag or a charcoal briquette. This is why the Household segment, not Health and Wellness, is where private label bites, and why the aggressive post-COVID price increases were a genuine gamble: every increment of price premium widens the gap a store brand can exploit and increases the reward for trying it once. The bull and bear cases here are not really in conflict; they are describing different segments of the same portfolio.

The honest synthesis: Clorox's moat is genuine and multi-layered, but it is not equally deep everywhere. It is deepest in institutional hygiene (physical switching costs), strong in consumer disinfection (trust premium), solid but eroding in heavy commodities (freight and scale, under private-label pressure), and thinnest in the trend-driven Lifestyle brands. Its two biggest structural pressures—concentrated retail buyers and private-label substitution—are precisely the forces a skeptical investor should keep watching. Those pressures put an enormous premium on management, which is where the investment case ultimately rests.

X. The Investment Spine: Linda Rendle's Credibility, Risks, and Bull vs. Bear Case

Every staples business eventually comes down to a bet on the people allocating the capital. So how credible is Linda Rendle's Clorox?

Management credibility, judged by behavior

The case for Rendle is built on a track record of doing hard things and, mostly, following through. She took the top job at the pandemic peak, navigated a demand super-spike, absorbed the worst margin collapse in the company's modern history, and then executed a disciplined recovery—price increases plus cost restructuring—that rebuilt gross margin from the mid-30s to 45.2% by fiscal 2025.6 She cut the failed VMS experiment and ate the loss rather than defending a sunk cost.11 And she managed the 2023 cyber crisis with a reasonable degree of transparency, disclosing the hit early and quantifying the damage.9 Taken together, that is a pattern of setting expectations and meeting them, of explaining misses rather than hiding them, and of pruning the portfolio rather than sprawling it.

The company also structures pay to reinforce the operational focus: the large majority of executives' target compensation is "at-risk" and tied to concrete annual metrics—net sales, net earnings, and gross margin—keeping the team pointed at the exact profitability recovery that shareholders care about. That alignment is a genuine positive, though it carries a subtle risk: heavy weighting on annual net sales and gross margin can incentivize short-term price-led results over long-term volume health.

The case against—or at least the open question—is the pattern the last decade reveals about narrative consistency. Management spent years telling investors the priority was reducing volatility, simplifying the portfolio, and structurally improving margins, and it backed that up by exiting VMS and pruning international. Then, roughly sixteen months after completing the VMS divestiture, it announced the largest acquisition in company history, funded primarily with debt.1 Those two stances are not necessarily contradictory—buying a high-margin, low-volatility B2B hygiene franchise is, on its face, entirely consistent with "reduce volatility and improve margin," and at ~2.4x sales it was bought at a price the doctrine would sanction. But it is a sharp change in posture from shrink-and-simplify to lever-up-and-expand, and shareholders are owed a clear account of it rather than an assumption of good faith.

The strongest version of the bear's concern is this: Clorox's history contains a recurring pattern of buying growth outside its circle of competence when the core business grows too slowly for public-market patience—Burt's Bees at thirteen times sales, then vitamins, then a $2.25 billion levered bet on a business model it has never run before. The strongest version of the bull's rebuttal is that Purell is different in every way that matters: bought cheap, adjacent to an existing division, with real switching costs and a genuine channel fit. Both readings are available from the same facts. Management's credibility on financial discipline will be earned or lost over the next two years, on the deleveraging line, not on the day the deal was announced.

The risk radar

Several risks are material enough to name plainly. Leverage and credit risk is front of mind after the S&P CreditWatch Negative placement; a downgrade would raise the cost of capital and pressure the dividend-growth streak.12 Private-label substitution is the perennial threat—if pinched consumers trade down from Glad, Fresh Step, and Clorox bleach to store brands, the whole pricing-power thesis frays. Execution risk is unusually stacked right now: Clorox is simultaneously integrating GOJO's large B2B operation, prosecuting the Cognizant litigation, and pushing through a major U.S. ERP (enterprise resource planning) system transition—a back-office overhaul so disruptive that management flagged it as the single biggest swing factor in its fiscal 2026 outlook, which guided to a 6–10% net-sales decline largely on ERP-related shipment timing.6 Any one of these is manageable; all three at once is a real test of organizational bandwidth. Layer on the ever-present cybersecurity risk that the 2023 breach made viscerally concrete, and the risk profile of this "boring" staples company is anything but sleepy.

The activist stress test

What would a skeptical long/short investor challenge? Probably three things. First, portfolio complexity: is a company spanning bleach, charcoal, ranch dressing, water filters, lip balm, and now institutional sanitizer really more valuable together than in pieces—the exact question Icahn raised in 2011? Second, capital allocation: after promising discipline and exiting VMS, management immediately levered up for its largest-ever deal; is that opportunism or drift? Third, volume versus price: how much of the margin recovery is durable demand and how much is price hikes quietly masking unit declines? These are the pressure points, and a fair analysis holds them open rather than waving them away.

Bull vs. bear

The bull case: Clorox sustains gross margin at or above the low-to-mid 40s, Purell plugs into Clorox Pro to build a genuinely defensible, high-switching-cost B2B hygiene franchise, the ERP transition proves transitory, and a favorable outcome in the Cognizant suit delivers a non-dilutive cash infusion to accelerate deleveraging. In that world, Clorox is a rare thing: a durable compounder that just added its best moat.

The bear case: S&P follows through with a downgrade, retailers finally push back on further price increases, private label and Lysol keep the shelf space they seized during the 2023 blackout, the ERP transition drags, and the leveraged Purell integration distracts management while the deleveraging timeline slips. In that world, the "safe" staple looks a lot more fragile than its reputation.

Weighing the two cases

Neither case is obviously right, and the honest position is that the outcome hinges on questions that are genuinely open. But it is possible to say which evidence would settle them.

The bull case rests on one testable proposition: that the Purell installed base delivers the switching-cost economics the deal thesis promises. That is not a matter of opinion—it will show up as durable, high-margin, recurring refill revenue inside Health and Wellness, growing regardless of what consumers do at retail. If it does, Clorox will have used a moment of leverage to buy the one power its portfolio structurally lacked, and the deal will look like the best capital allocation in the company's modern history.

The bear case rests on a different testable proposition: that the post-COVID margin recovery was an artifact of an inflationary window rather than durable brand power. That will show up as volume declines quietly accumulating beneath flat or rising revenue, particularly in Household, where private label attacks hardest and the trust premium is thinnest.

Notice that both propositions are measurable, and that they are largely independent of each other. It is entirely possible for Clorox to win the institutional hygiene bet and still watch its retail commodity franchises slowly erode—in which case the company gradually transforms into something quite different from what it has been for a century: less a portfolio of household brand icons, more an industrial hygiene business with a consumer division attached. That may be the most interesting scenario of all, and it is the one the numbers are best positioned to reveal early.

The three KPIs that matter

Cutting through the noise, three metrics tell the story from here:

- Gross margin. The single clearest gauge of pricing power versus input costs. Sustaining it in the mid-40s validates the moat; a slide back toward the 30s would reopen every bearish question.

- Organic volume growth. The truth serum that separates real demand from price hikes. Volume growth alongside price means the brands are healthy; volume declines masked by price mean consumers are quietly leaving.

- Net debt-to-EBITDA. The scoreboard for the Purell bet and the dividend. Watching leverage fall back toward management's ~2.5x target is how investors will know whether the promise of discipline was real.

XI. Epilogue & Key Takeaways for Long-Term Investors

The most arresting lesson of the Clorox story is how a 113-year-old maker of one of the world's most basic products—a company built to survive depressions, wars, and pandemics—could be brought to its knees not by a competitor or a recession but by a single outsourced help-desk agent trusting the wrong voice on the phone. Modern enterprises are dazzlingly efficient and quietly fragile, their sprawling automation resting on a handful of human trust decisions. That fragility is now a permanent line item in the risk assessment of even the sturdiest consumer staple.

The Cognizant litigation, whatever its outcome, has already delivered its most useful lesson free of charge: risk has migrated. For most of Clorox's history, the threats to the business were the ones you could see and touch—a competitor's price cut, a resin shortage, a bad grilling season. Those risks were slow, visible, and manageable by people who understood soap and freight. The risks that now matter most are invisible, instantaneous, and sit outside the company's own walls, inside vendors whose incentives are not aligned with the client's downside. No amount of brand equity built over 113 years protects against a help-desk agent's five-minute lapse of protocol.

Yet the deeper takeaway runs the other way, toward durability. Clorox is, at its core, a basket of #1 and #2 brands in categories that most investors would call boring—bleach, bags, charcoal, litter, dressing, filters, sanitizer. That very boringness, combined with the freight economics that protect heavy commodities and the brand trust that lets identical chemistry command a premium, has made the portfolio one of the more resilient compounders in market history. It survived a Supreme Court dismemberment, an Icahn siege, a pandemic whipsaw, and a paralyzing cyberattack, and it kept paying and raising its dividend through all of it.

But durability is not the same as safety, and the two are constantly confused in the way investors talk about staples. Clorox has survived everything thrown at it, which tempts the conclusion that it always will. The record supports a narrower claim: the portfolio structure—category leadership in defensible niches—has proven remarkably robust to shocks it did not choose. It has been considerably less robust to the choices management made voluntarily, in the moments when slow growth became uncomfortable. The Supreme Court, Carl Icahn, a pandemic, and Scattered Spider all failed to do lasting damage. Vitamins did more harm than any of them, and it was self-inflicted.

That is the frame worth carrying into the Purell era. The question facing Clorox is not whether it can withstand adversity; a century of evidence says it can. The question is whether a management team under permanent pressure to grow a structurally slow-growing business can deploy $2.25 billion of borrowed money with the discipline its own doctrine demands—and whether the moat it just bought is as physical, as recurring, and as durable as the deck says.

The company that Annie Murray saved by handing out fifteen-cent samples at an Oakland grocery store is now a high-tech, multi-category hygiene fortress placing a $2.25 billion bet on the walls of the world's hospitals. Whether that bet compounds the franchise or strains it will be settled not by the confident language of a press release, but by the three numbers—margin, volume, and leverage—that will quietly tell investors, quarter after quarter, whether the moat is still holding.

References

-

Clorox Announces Acquisition of GOJO Industries, Makers of Purell — PR Newswire, 2026-01-22 ↩↩↩↩↩↩↩

-

Clorox files $380 million suit blaming Cognizant for 2023 cyberattack — Cybersecurity Dive, 2025-07-18 ↩↩↩↩↩

-

Carl Icahn Launches Unsolicited $10.2 Billion Hostile Takeover Bid for Clorox — The New York Times, 2011-07-15 ↩↩↩

-

Clorox Rejects Billionaire Carl Icahn's Takeover Offer — The Wall Street Journal, 2011-07-18 ↩↩

-

Clorox Reports Q4 and FY25 Results, Provides FY26 Outlook — PR Newswire, 2025-08-01 ↩↩↩↩↩↩↩↩

-

Hackers fooled Cognizant help desk, says Clorox in $380M cyberattack lawsuit — BleepingComputer, 2025-07-18 ↩

-

Clorox Reports Q1 Fiscal Year 2024 Results, Updates Outlook — The Clorox Company (SEC Form 8-K), 2023-11-01 ↩↩

-

Clorox Slashes Full-Year Guidance on Massive Impact of August Cyberattack — Reuters, 2023-10-04 ↩↩

-

Clorox sues Cognizant for $380M over alleged helpdesk failures in cyberattack — CSO Online, 2025-07-18 ↩

-

Clorox Completes Previously Announced Divestiture of its Better Health VMS Business — PR Newswire, 2024-09-10 ↩↩↩

-

The Clorox Company Ratings Placed on CreditWatch Negative Following Announced GOJO Acquisition — S&P Global, 2026-01-22 ↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube