Chatham Lodging Trust: The Select-Service Strategy

I. Introduction and Episode Roadmap

In the sprawling world of hotel real estate investment trusts, where companies routinely boast portfolios of hundreds or even thousands of properties spread across continents, there exists a quiet outlier. Chatham Lodging Trust owns just thirty-three hotels. It has no international footprint. It operates no glitzy beachfront resorts or soaring urban towers.

And yet, when the worst crisis in the history of the hospitality industry arrived in March 2020, this small, focused REIT emerged with a claim that none of its larger peers could match: the highest RevPAR of any publicly traded lodging REIT during the entire COVID pandemic.

That fact alone deserves unpacking. RevPAR, or revenue per available room, is the hospitality industry's single most important operating metric. It combines both how full your hotels are and how much you can charge per night into one elegant number. For a REIT with roughly thirty-six properties at the time to post the highest RevPAR across the entire publicly traded hotel universe, beating companies with ten or twenty times as many rooms, suggests something more than luck. It suggests a strategy worth studying.

Chatham Lodging Trust trades on the New York Stock Exchange under the ticker CLDT. As of late February 2026, the company operates thirty-three hotels totaling just over five thousand rooms and suites, spread across fifteen states and Washington, D.C. The portfolio is concentrated in two specific niches: upscale extended-stay hotels, which cater to guests staying a week or more, and premium-branded select-service properties, which offer clean rooms and consistent service without the full-service bells and whistles of a traditional hotel. Think Residence Inn, not Ritz-Carlton. Think Homewood Suites, not Hilton flagship.

The big question driving this deep dive is deceptively simple: How does a specialized hotel REIT with a relatively tiny portfolio consistently outperform industry giants?

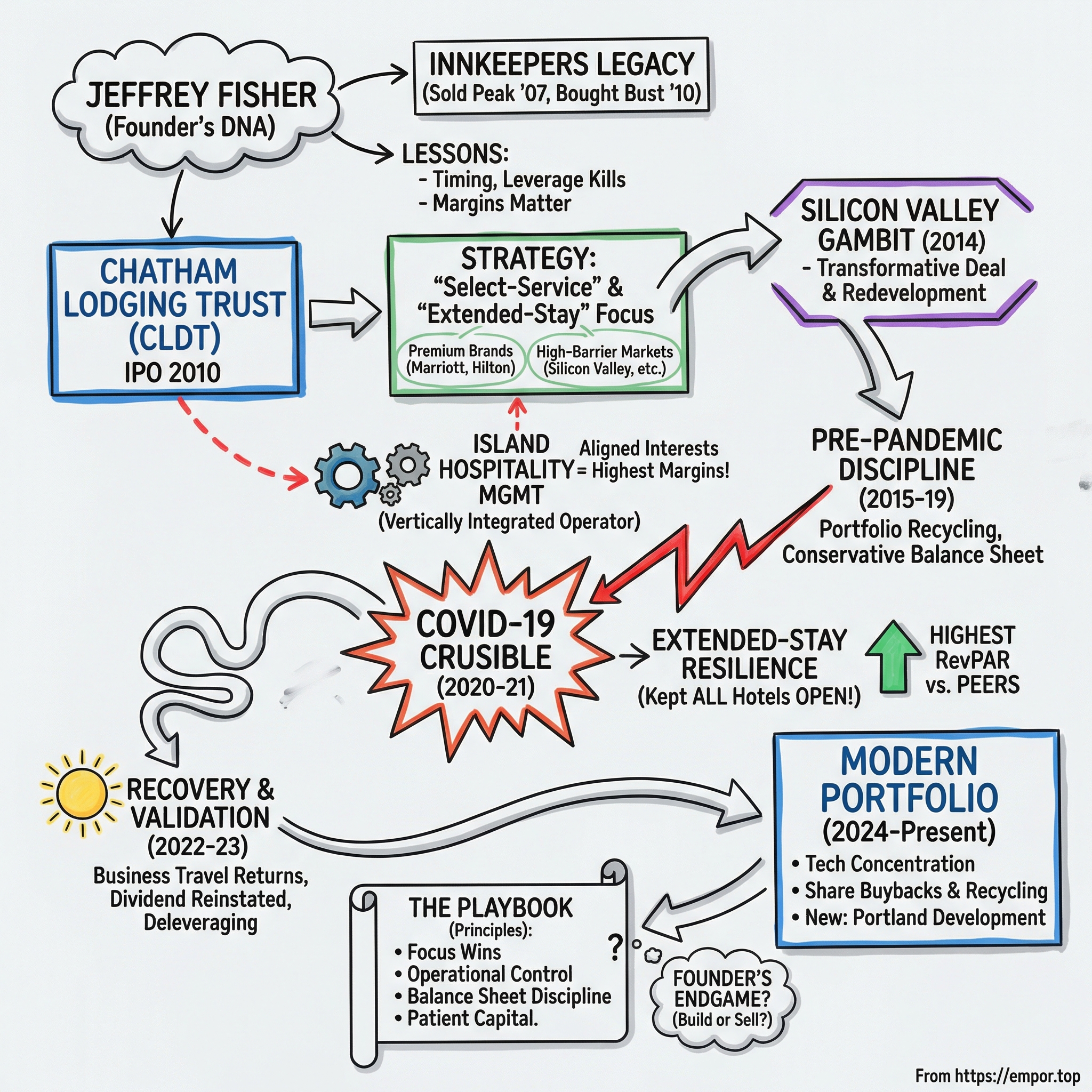

The answer winds through a founder's DNA forged across four decades in hospitality, a contrarian bet placed during the Great Recession, a massive Silicon Valley gambit, the vertically integrated relationship with a management company that produces the highest operating margins in the sector, and a pandemic crucible that validated every strategic choice the company had ever made.

This is a story about capital allocation, operational excellence, and the power of focus in real estate. It is also a story about one man, Jeffrey Fisher, who built and sold a hotel empire before the financial crisis, then built another one from the ashes of the crisis itself. Along the way, Chatham offers a masterclass in a set of principles that extend far beyond hotels: buy right, operate efficiently, maintain financial discipline, and never confuse size with quality.

Before diving in, a quick primer on hotel industry terminology for those less familiar with the sector. A "select-service" hotel offers rooms, breakfast, maybe a small fitness center and pool, but no full restaurant, no room service, no concierge desk, and no banquet halls. Think of it as a hotel that does the essentials extremely well without the overhead of a full resort. "Extended-stay" takes this a step further: rooms include kitchenettes or full kitchens, allowing guests to cook their own meals, and housekeeping visits weekly rather than daily. The combination of these two models creates a cost structure that is fundamentally different from a traditional full-service hotel, and understanding that difference is key to understanding everything Chatham does.

Let us begin where all the best origin stories start: with the founder.

II. Founder's DNA and the Innkeepers Legacy

Picture a conference room in West Palm Beach, Florida, sometime in late 2008. The global financial system is melting down. Hotel values are in freefall. Owners are defaulting on mortgages. And Jeffrey H. Fisher, sitting in that conference room, is not panicking. He is planning.

Fisher is not the kind of CEO who shows up in magazine profiles or keynote stages. He is a deal-maker and an operator, a man whose career has been defined by the intersection of real estate acumen and hotel management expertise. With a receding hairline and the steady, unflappable demeanor of someone who has seen multiple cycles, Fisher approaches hotel investing the way a chess player approaches the board: always thinking three moves ahead, always aware of the risks, always prepared to sacrifice short-term gain for long-term position.

His educational background hints at the analytical rigor that would come to define his approach: a Bachelor of Science in Business Administration from Syracuse University in 1977, a Juris Doctor from Nova Southeastern University in 1980, and a Master of Laws in Taxation from the University of Miami in 1981. Notice the progression: business, then law, then tax law. This is not someone who stumbled into hotels. This is someone who came armed with the legal, financial, and operational toolkit to build institutions. The tax specialization would prove particularly relevant for a career spent structuring real estate investment trusts, where tax efficiency is not an afterthought but a central strategic consideration.

Fisher's hotel career began in earnest in 1986 when he founded JF Hotel Management in West Palm Beach, Florida. His first managed property was a Hampton Inn, the Hilton-branded select-service chain that would become a cornerstone of his investment philosophy for the next four decades.

For eight years, Fisher built JF Hotel Management into a credible operator, learning the granular details of hotel economics: how to optimize housekeeping schedules, negotiate franchise agreements, manage the delicate balance between room rates and occupancy, and squeeze margin out of properties that many institutional investors overlooked. This was the school of hard knocks for hotel management, far removed from the deal-making floors of Wall Street. Fisher learned the business from the ground up, literally walking the hallways of his properties and understanding what drove each line item on the profit and loss statement.

In 1994, Fisher made his first major move into public markets. He founded Innkeepers USA Trust and took it public as a lodging REIT. At the time of its IPO, Innkeepers owned just seven hotels.

Over the next thirteen years, Fisher grew the portfolio tenfold, building Innkeepers into a seventy-four-hotel operation that spanned select-service and extended-stay properties across the United States. The growth was methodical rather than explosive, driven by the same disciplined approach to acquisitions that would later characterize Chatham: find under-managed properties in strong markets, acquire them at reasonable prices, and improve operations. It was not glamorous work, but it was effective, and it produced consistent returns for Innkeepers shareholders throughout the late 1990s and into the 2000s.

Then came the exit that cemented Fisher's reputation for timing. In June 2007, Apollo Investment Corporation, the vehicle founded by private equity titan Leon Black, acquired Innkeepers USA Trust in an all-cash leveraged buyout at $17.75 per share, valuing the company at approximately $1.5 billion in enterprise value. To put that number in perspective: Fisher had started with seven hotels at IPO in 1994 and sold for $1.5 billion thirteen years later. That is a masterful compounding story in its own right. But the truly remarkable part was the timing. Fisher had sold at what would prove to be the absolute peak of the pre-crisis hotel market. Within eighteen months, the global financial system would crater, hotel values would plummet, and the very portfolio Fisher had sold would become a cautionary tale in over-leveraged real estate.

The aftermath was swift and brutal, but not for Fisher. Apollo had loaded Innkeepers with debt to finance the acquisition, a classic leveraged buyout structure that works beautifully when asset values rise and catastrophically when they fall.

In July 2010, Innkeepers USA Trust filed for Chapter 11 bankruptcy protection, saddled with debts exceeding one billion dollars tied directly to the 2007 acquisition. The hotels Fisher had spent thirteen years building were now financial wreckage, their value obliterated not by operational failure but by the capital structure imposed upon them. The properties themselves were fine. Guests were still checking in. Housekeepers were still cleaning rooms. The fundamental business was sound. But when you load a portfolio with debt at the peak of the market and the world subsequently experiences a once-in-a-generation financial crisis, no amount of operational excellence can service the interest payments.

Fisher, meanwhile, had already moved on. Immediately after the Innkeepers sale in 2007, he formed two new entities: Fisher Property Group and Island Hospitality Management. The latter was a direct evolution of JF Hotel Management, rebranded to reflect its growing scale. Island Hospitality would become the operational backbone of everything Fisher built next, managing hotels for both affiliated and unaffiliated owners with the same margin-obsessed efficiency that had characterized his career from the beginning.

The Innkeepers experience taught Fisher several lessons that would shape Chatham's entire philosophy.

First, timing matters enormously in real estate, and the discipline to sell when markets are frothy is just as important as the courage to buy when they are distressed. Second, leverage kills. It was the capital structure that destroyed Innkeepers under Apollo's ownership, not the business itself. Third, select-service and extended-stay hotels generate structurally higher margins than full-service properties because they require less labor, less food and beverage infrastructure, and less capital expenditure to maintain.

These were not abstract observations for Fisher. They were hard-won convictions forged across two decades of direct experience, convictions that would shape every decision Chatham Lodging Trust would make from its founding forward.

The Innkeepers experience taught Fisher several additional lessons beyond leverage and timing. He learned that the hotel management business, separate from hotel ownership, was a durable and scalable enterprise. Managing hotels for fees generates steady cash flow without the capital intensity of ownership. It also keeps you close to the operational realities of the business: occupancy trends, labor markets, brand relationships, and competitive dynamics. By running Island Hospitality alongside any future ownership vehicle, Fisher would always have his finger on the pulse of the industry, a critical advantage when evaluating acquisition opportunities.

By 2009, as the global financial crisis was grinding through the hotel industry and competitors were retrenching, Fisher saw exactly the opportunity he had been preparing for. Hotel values were at generational lows. Owners were desperate to sell. Financing was scarce, which meant that anyone with access to capital could acquire properties at prices that might not be seen again for a decade. The man who had sold at the top was now ready to buy at the bottom. It was time to build again.

III. The IPO and Post-Crisis Playbook (2009-2013)

On October 26, 2009, Chatham Lodging Trust was organized as a Maryland real estate investment trust. To appreciate the audacity of this moment, consider the backdrop. Lehman Brothers had collapsed barely a year earlier. Bear Stearns was a memory. The commercial real estate market was in a state of paralysis, with hotel transaction volumes down more than eighty percent from their 2007 peak. National hotel occupancy rates had plummeted to levels not seen since the early 1990s recession. Lenders were not just pulling back from commercial real estate; many were refusing to underwrite hotel loans at any price. For most hotel investors, 2009 was a year to hunker down and pray. For Jeffrey Fisher, it was the starting gun.

The formation of Chatham was a bet built on a straightforward thesis: the best time to buy hotels is when everyone else is selling them, and the best hotels to buy are the ones that others have neglected. Fisher was not interested in trophy assets or marquee addresses. He wanted well-located, premium-branded select-service and extended-stay properties in markets with high barriers to entry and strong demand generators, properties that a sophisticated operator could improve through targeted renovations, revenue management, and operational discipline.

Chatham completed its initial public offering on April 21, 2010, pricing at twenty dollars per share and raising $150 million from 7.5 million shares. In a gesture that speaks volumes about founder conviction, Fisher personally invested ten million dollars in a concurrent private placement at the same IPO price. When a founder writes a check that size alongside public investors, it sends a signal: this is not a promotional vehicle. This is a business its creator believes in with his own capital.

The company moved with remarkable speed after the IPO. Just five days later, on April 26, 2010, Chatham closed its first acquisition: six Homewood Suites by Hilton hotels purchased from RLJ Development for $73.5 million in an all-cash transaction. Within a month, Chatham had signed contracts to acquire four additional hotels for sixty-one million dollars, approximately $137,000 per key. By late May 2010, barely six weeks after going public, Chatham already owned ten hotels with 1,257 rooms.

The speed was not recklessness. Fisher had spent two decades building relationships with hotel brokers, brand executives, and distressed sellers. He knew exactly which properties he wanted and had been tracking them long before Chatham's IPO. The public offering was simply the mechanism to fund a pipeline he had already assembled. This is a pattern that repeats throughout Chatham's history: preparation meets opportunity, and the company moves faster than competitors expect.

The strategy crystallized quickly around several core principles that Fisher had been refining since his Hampton Inn days in the late 1980s.

First, brand affiliation with the strongest franchise systems: Marriott's Residence Inn and Courtyard, Hilton's Hampton Inn, Homewood Suites, and Hilton Garden Inn, and later Hyatt Place. These brands provide national marketing, loyalty programs, and reservation systems that individual hotels could never replicate on their own. A Residence Inn in Mountain View benefits from Marriott Bonvoy's hundreds of millions of loyalty program members worldwide, a distribution advantage that no independent hotel can match.

Second, geographic focus on high-barrier-to-entry markets near major demand generators, markets where zoning restrictions, land costs, or other factors limit new hotel supply and protect existing properties from competition.

Third, and most importantly, a preference for extended-stay properties.

The extended-stay thesis deserves particular attention because it is the conceptual foundation of everything Chatham does.

Extended-stay hotels cater to guests staying five nights or more, often weeks or months at a time. These guests might be corporate relocations, project-based workers, military personnel, or medical professionals on temporary assignments. The economics of extended-stay are fundamentally different from traditional hotels.

Because guests stay longer, front desk activity is lower, room turnover is less frequent, and housekeeping costs per occupied room night drop dramatically. A traditional hotel might clean every room every day. An extended-stay property might service occupied rooms weekly. The labor savings alone can add hundreds of basis points to operating margins.

Moreover, extended-stay demand is stickier than transient demand. A business traveler choosing between two Marriott properties for a Tuesday night can switch on a whim. A consultant who has settled into a Residence Inn for a six-week project, has unpacked their suitcase, stocked the refrigerator, and established a morning routine at the local coffee shop, is far less likely to move. This stickiness translates into more predictable occupancy and revenue streams, which matters enormously during economic downturns when transient demand evaporates.

There is also a less obvious advantage: the booking window. Extended-stay reservations are typically made weeks or months in advance, compared to days or hours for transient business travel. This gives the revenue management team greater visibility into future occupancy and the ability to optimize pricing with more lead time. For an operationally intense business like hotel management, predictability is extraordinarily valuable.

From inception, Chatham generated the highest operating margins among all lodging REITs, a claim the company has made consistently and that multiple third-party analyses have corroborated. The margin advantage was not merely a function of buying cheap properties. It was the structural advantage of extended-stay and select-service hotels, amplified by Island Hospitality's operational expertise and Fisher's relentless focus on efficiency.

The target acquisition profile was specific and disciplined: under-managed and under-capitalized properties where Island Hospitality could improve operations, typically in markets adjacent to major employers, technology hubs, military installations, or medical centers. Fisher was not looking for shiny new buildings. He was looking for diamonds in the rough, properties where the previous owner had deferred maintenance, under-invested in revenue management, or simply lacked the operational expertise to maximize profitability. Buy right, fix it, run it better. That was the formula.

By 2013, Chatham had assembled a growing portfolio of premium-branded properties in markets like Silicon Valley, the greater Boston area, Portland (Maine), Savannah, and other high-demand markets. The company was profitable, its balance sheet was conservative, and Fisher was watching for the next big opportunity. It arrived in the form of a deal that would transform Chatham from a promising small REIT into a company with a definitive identity.

IV. The Silicon Valley Gambit (2014)

To understand the significance of what happened next, think of it this way: imagine a chess player who sold all his pieces at the highest possible value, watched his opponent go bankrupt trying to use them, then bought the best pieces back at a steep discount, and used the profits to buy even more pieces. That is essentially what Jeffrey Fisher did between 2007 and 2014. And the 2014 Silicon Valley acquisition was the culmination.

In the spring of 2014, Fisher received word that Cerberus Capital Management, the private equity firm that had partnered with Chatham to acquire sixty-four former Innkeepers USA Trust hotels out of bankruptcy back in 2011, was ready to restructure the joint venture portfolio. The transaction that followed was the largest in Chatham's history and a case study in how a small REIT can punch far above its weight through relationships, speed, and strategic vision.

The backstory matters here. In May 2011, Cerberus and Chatham had jointly won a bankruptcy court auction for sixty-four hotels from Fisher's old Innkeepers portfolio, with a winning bid of approximately $1.125 billion including assumed debt. The irony was rich: Fisher was effectively buying back a large chunk of the portfolio he had sold to Apollo in 2007, now available at distressed prices after the leveraged buyout had collapsed. Chatham invested thirty-seven million dollars for a 10.3 percent stake in the joint venture, with Cerberus holding the remaining 89.7 percent.

Three years later, Cerberus was ready to monetize. The restructuring carved the sixty-four-hotel portfolio into distinct pieces, and Chatham positioned itself to capture the most valuable slice: four Residence Inns in Silicon Valley.

The deal closed in June 2014. Chatham acquired the four Silicon Valley Residence Inns for a net cash purchase price of $272.6 million, approximately $363,000 per room across 751 keys. This was not cheap by any conventional measure. But Fisher saw something that the price per key did not capture: each of these properties sat on land in one of the most supply-constrained hotel markets in the world, and each had room to grow.

Silicon Valley in 2014 was in the throes of a technology boom that showed no signs of slowing. Apple, Google, Facebook, and hundreds of smaller companies were hiring tens of thousands of workers, generating massive demand for extended-stay accommodations. Business travelers needed places to stay for weeks or months during project deployments, training programs, and temporary assignments. New hotel supply in the Valley was severely limited by zoning restrictions, land costs, and the lengthy permitting processes typical of California municipalities. The result was a market where existing hotels could command premium rates and maintain high occupancy with minimal competitive threat.

Why Silicon Valley? Consider the market dynamics at the time. In 2014, Apple was building its new spaceship campus in Cupertino. Google was expanding relentlessly across Mountain View and Sunnyvale. LinkedIn, then still independent, was growing its Sunnyvale headquarters. Facebook had taken over the old Sun Microsystems campus in Menlo Park and was hiring thousands. Every one of these companies relied on armies of contractors, consultants, and temporary project workers who needed somewhere to stay for weeks or months at a time. Extended-stay hotels were not a luxury in Silicon Valley; they were infrastructure. And unlike office buildings or apartments, the supply of hotel rooms in the Valley was constrained by California's notoriously restrictive zoning and permitting environment.

Fisher's vision extended beyond simply owning the four properties. He saw redevelopment potential that others had missed. The properties had excess land, parking areas that could be repurposed, and physical layouts that could accommodate additional rooms. Chatham developed plans to expand the total room count by thirty-six percent, adding 272 rooms to bring the combined count from 751 to 1,023, at an estimated cost of approximately fifty-nine million dollars. This was value creation in its purest form: spending fifty-nine million dollars to add rooms that, given Silicon Valley rates, would generate returns far in excess of the capital invested.

Simultaneously, the remaining forty-seven hotels in the Innkeepers portfolio were restructured into a new joint venture between NorthStar Realty Finance Corp. and Chatham. NorthStar acquired Cerberus's interest, while Chatham retained its 10.3 percent stake. The gross purchase price for the forty-seven-hotel portfolio was $958.5 million. Across the entire restructuring, Chatham recognized a non-GAAP economic gain of approximately eighty million dollars, or over three dollars per share, on its original thirty-seven-million-dollar joint venture investment. That is better than a double in three years on a minority stake in a bankruptcy acquisition, a return that speaks to both the quality of the original underwriting and the recovery in hotel values from their crisis lows.

But Fisher was not done. Later in 2014, Chatham expanded its NorthStar relationship with another joint venture: a fifty-two-hotel, nearly seven-thousand-room portfolio acquired from Inland American Real Estate Trust for approximately $1.1 billion. The joint venture was structured with NorthStar holding ninety percent and Chatham ten percent. Island Hospitality Management was tapped to manage thirty-eight of the fifty-two hotels, further expanding the management company's scale and fee base. Chatham also negotiated the direct acquisition of four hotels from the Inland American portfolio for $107 million.

The 2014 transactions transformed Chatham in several ways. The Silicon Valley properties became the company's single largest market and its highest-RevPAR assets, anchoring the portfolio's performance for years to come. The joint venture structures allowed Chatham to participate in billion-dollar portfolio transactions with minimal equity investment, generating outsized returns through promoted interests and management fees. And the deals reinforced Chatham's identity as an opportunistic, relationship-driven acquirer that could move quickly on complex transactions.

The NorthStar joint venture would eventually wind its way through a merger with Colony Capital and subsequent restructurings. In March 2021, Chatham sold its residual 10.3 percent interest in the successor joint venture for $2.8 million. Including earlier distributions of $22.2 million and the original eighty-million-dollar gain, the total return on the original thirty-seven-million-dollar investment exceeded one hundred million dollars. Not bad for a minority stake in a bankruptcy portfolio that Fisher had originally built himself.

There is an important lesson embedded in the 2014 transactions about the power of relationships in real estate. Fisher did not find these deals on a broker's listing page. He found them because he had built Innkeepers, because he had partnered with Cerberus to buy back those same hotels out of bankruptcy, and because he had earned trust through years of operational performance. In commercial real estate, the best deals often go to the people who are already in the room when the conversation starts. Fisher was always in the room.

The Silicon Valley gambit established a template that Chatham would follow repeatedly: find under-managed or under-capitalized properties in high-barrier markets, acquire them using creative structures when possible, improve operations through Island Hospitality, and create value through targeted capital investments. It was a playbook that required patience, operational expertise, and the willingness to concentrate capital in a small number of high-conviction bets rather than spreading it across dozens of mediocre ones.

V. Operational Excellence Through Island Hospitality

If Chatham's acquisition strategy is the brain of the organization, Island Hospitality Management is the muscle. And in the hotel business, muscle matters enormously. A beautiful hotel in a perfect market will produce mediocre returns if it is poorly managed. A modest hotel in a decent market can produce exceptional returns if the operator knows how to extract every dollar of revenue and control every dollar of cost. To understand why Chatham consistently produces the highest operating margins of any publicly traded lodging REIT, you need to understand Island Hospitality and the unusual relationship between the two companies. It is a relationship that creates genuine competitive advantage, but also one that sophisticated investors should examine carefully.

Island Hospitality Management is a privately held hotel management company headquartered in West Palm Beach, Florida. Jeffrey Fisher is its chairman and approximately ninety percent owner. The company evolved from Fisher's original JF Hotel Management firm founded in 1986, through a rebrand as Innkeepers Hospitality in 1998, to its current incarnation as Island Hospitality Management in 2007. Today, Island Hospitality operates over one hundred hotels across nineteen brands in twenty-three states and Washington, D.C., employing between five and ten thousand people.

Here is the structural reality: every hotel that Chatham wholly owns is managed by Island Hospitality. Fisher controls both the owner (as CEO and significant shareholder of Chatham) and the operator (as ninety percent owner of Island Hospitality).

In theory, this creates a potential conflict of interest, as the management company earns fees that come out of the REIT's operating income. In practice, Fisher argues, and the operating results support, that this alignment creates the opposite: an operator whose economic interests are overwhelmingly tied to the performance of the properties it manages.

This matters because of a peculiarity of REIT tax law that non-specialists often find confusing. To maintain its tax-advantaged REIT status, Chatham cannot directly operate its hotels. REITs are pass-through vehicles designed to own real estate, not run businesses. The idea is simple: a REIT collects rent, distributes most of it to shareholders, and pays no corporate income tax. But actually running a hotel, hiring staff, managing guests, cooking breakfast, is considered an active business, not passive real estate ownership. So the hotels must be leased to taxable REIT subsidiaries, which in turn must hire an independent management company to run day-to-day operations.

Most hotel REITs solve this problem by contracting with third-party managers, major hotel companies, or independent management firms that also manage properties for competitors. The result is a management company with divided loyalties and limited incentive to go above and beyond for any single owner.

Chatham's structure is different. Island Hospitality manages all of Chatham's hotels, and while it also manages properties for unaffiliated owners, the Chatham portfolio represents a critical mass of its business. More importantly, Fisher's personal financial interest in Chatham's stock performance means that Island Hospitality is incentivized to maximize property-level profitability in ways that a truly arms-length third-party manager might not be. When Island Hospitality finds a way to reduce housekeeping costs by fifty basis points across the portfolio, that improvement flows directly to Chatham's bottom line and, by extension, to Fisher's net worth through his REIT shareholding.

The margin results speak for themselves. Chatham's select-service and extended-stay hotels operate at gross operating profit margins that consistently exceed those of its lodging REIT peers. In 2022 and 2023, Chatham produced the highest GOP margins among all lodging REITs. In the full year 2025, the company reclaimed the top margin ranking once again, limiting GOP margin decline to just twenty basis points despite essentially flat RevPAR.

To put this in concrete terms, the company has reported GOP margins in the low-to-mid forties on a percentage basis, with hotel EBITDA margins in the low-to-mid thirties. By comparison, a typical full-service hotel might operate at GOP margins in the mid-to-upper twenties. The difference, roughly fifteen percentage points of margin, means that for every dollar of revenue, Chatham keeps roughly fifteen cents more than a full-service peer. Multiply that across five thousand rooms and twelve months, and the cumulative value of operational excellence becomes very large indeed.

How does Island Hospitality achieve these margins? The answer is a combination of structural advantages and operational discipline that, taken together, create a compounding effect that is difficult for competitors to replicate.

The structural piece comes from the portfolio itself: extended-stay and select-service hotels simply require less labor, less food and beverage infrastructure, and less overhead than full-service properties. There are no ballrooms to staff, no room service kitchens to operate, no concierge desks to man. Consider the math: a full-service hotel with a restaurant, room service, banquet facilities, and a spa might require one employee for every two rooms. A select-service hotel might require one employee for every three or four rooms. An extended-stay property, with its weekly housekeeping model and self-service kitchenettes, might need even fewer. When labor represents the single largest operating expense for any hotel, these staffing differences translate directly into margin points.

The operational piece comes from Island Hospitality's relentless focus on efficiency: optimizing staffing models, cross-training employees so that a front desk agent can assist with breakfast service during peak hours, leveraging technology for dynamic revenue management, and making small but cumulative improvements in everything from energy consumption to supply chain procurement. Each individual improvement might be worth ten or twenty basis points. But when you compound dozens of these improvements across thirty-three properties over sixteen years, the cumulative effect is the difference between average industry margins and best-in-class margins.

Island Hospitality also drives value through creative asset management. At Chatham's Hilton Garden Inn in Savannah, the team opened the Toasted Barrel restaurant, a revenue-generating amenity that enhanced the guest experience while contributing to property-level income. Across the portfolio, Island Hospitality has modernized public spaces, converted underutilized meeting rooms into revenue-generating guest rooms, and optimized the use of every square foot. These are not headline-grabbing moves. They are the blocking and tackling of hotel management, executed consistently across dozens of properties over many years.

The management agreement between Chatham and Island Hospitality is a related-party arrangement disclosed in all of Chatham's SEC filings and subject to annual review by Chatham's independent trustees. Investors should monitor this relationship carefully. The alignment of interests that produces industry-leading margins also creates governance questions about whether the management fees paid to Island Hospitality are truly arms-length. To date, the independent trustees have consistently approved the arrangement, and the margin performance provides strong evidence that Chatham's shareholders benefit from the relationship. But the concentration of control in Fisher's hands, across both the REIT and the management company, is a structural feature that bears watching.

Think of it this way: most hotel REITs are like real estate holding companies that outsource operations to contractors. Chatham is more like a vertically integrated company that happens to be structured as a REIT. The tax code requires formal separation between ownership and management, but the economic reality is that Fisher controls both sides of the equation. This gives Chatham the strategic coherence of an owner-operator with the tax advantages of a REIT, a combination that is surprisingly rare in the lodging sector and one of the key reasons for the company's sustained margin outperformance.

The bottom line is this: Island Hospitality is Chatham's secret weapon. It is the operational engine that transforms a collection of select-service hotels into the highest-margin portfolio in the publicly traded lodging REIT universe. And because Fisher owns it, because the people who manage the hotels have skin in the game at every level, the incentive structure produces results that third-party management simply cannot replicate at scale.

VI. Portfolio Optimization and Pre-Pandemic Growth (2015-2019)

Between the transformative 2014 deals and the arrival of COVID-19, Chatham entered a period of steady portfolio refinement that revealed as much about the company's discipline as its earlier acquisitions had revealed about its ambition. This was not a period of dramatic headlines. It was a period of compounding, of quietly making the portfolio better one decision at a time.

The recycling strategy became a defining feature, and it is worth dwelling on because most investors underestimate its importance in REIT management. The concept is straightforward: Chatham would identify properties that no longer fit its criteria, whether due to age, market dynamics, or capital expenditure requirements, sell them at attractive valuations, and redeploy the proceeds into higher-quality assets or balance sheet strengthening. The philosophy was simple: every hotel in the portfolio should be one that Chatham would want to buy today at its current implied valuation. If it would not, it should be sold.

This sounds obvious, but it is surprisingly rare in practice. Many REIT managers resist selling properties because dispositions shrink the portfolio's total asset base, which can reduce management fees and make the company look smaller relative to peers. There is also an emotional dimension: selling a hotel that you bought, renovated, and improved feels like giving up a child. Fisher, having already sold an entire seventy-four-hotel portfolio once before, had no such attachment. Properties were assets to be optimized, not trophies to be collected.

A representative example came in 2019, when Chatham divested two hotels in Pennsylvania for ten million dollars. The sale improved the portfolio's aggregate RevPAR from $133 to $135 and, critically, avoided four million dollars in renovation capital expenditure that the aging properties would have required. This is the kind of quiet, unspectacular decision that creates enormous value over time. Four million dollars saved on renovations plus the reinvestment of ten million dollars in sale proceeds, deployed into better properties or used to reduce debt, compounds into meaningful per-share value creation over a multi-year period.

Geographic concentration intensified during this period. Chatham focused its portfolio on eight to ten markets with strong demand generators: Silicon Valley, greater Boston, coastal markets in Maine and Georgia, the Washington D.C. metro area, and select Sun Belt locations.

The company deliberately avoided the broad national footprint that many larger hotel REITs pursued, believing that deeper knowledge of fewer markets would produce better acquisition decisions, better operations, and better returns. When you know a market intimately, when you know which employers drive demand, which neighborhoods are gentrifying, which intersections have the best visibility, you can underwrite acquisitions with a precision that national-scale operators cannot match.

The extended-stay focus also deepened. By the end of 2019, Chatham had assembled the highest concentration of extended-stay rooms among all publicly traded lodging REITs, a distinction the company maintains today. This was not an accident but a deliberate portfolio construction strategy driven by the margin and demand characteristics discussed earlier. Extended-stay properties generated more income per room, required less capital to maintain, and exhibited more resilient demand patterns during economic softness.

Balance sheet management during this period was conservative by design. Chatham maintained moderate leverage, typically in the mid-thirties as a percentage of hotel investments at cost, and preserved ample liquidity through an unsecured revolving credit facility. Fisher had seen what excessive leverage could do to a hotel portfolio, having watched Apollo's over-levered Innkeepers collapse into bankruptcy. He was determined that Chatham would never face the same fate. The pre-pandemic leverage ratio of approximately thirty-five percent gave Chatham enough financial flexibility to pursue opportunistic acquisitions without putting the company at existential risk during a downturn.

By the end of 2019, the portfolio stood at approximately forty wholly-owned hotels plus joint venture interests. RevPAR had reached a pre-pandemic peak of $145 in the second quarter of 2019, with an average daily rate of $173 and occupancy above eighty-three percent. Operating margins were the highest in the sector. The balance sheet was strong. The portfolio was concentrated in high-quality markets. Everything was in place for continued compounding.

Looking back, the 2015-2019 period might seem uneventful compared to the dramatic acquisitions of 2014 or the crisis that would follow. But the quiet compounding of this era, the steady improvement in portfolio quality, the disciplined balance sheet management, the deepening expertise in a narrow niche, was arguably the most important strategic work Chatham did. It built the foundation that would allow the company to survive what came next. In business as in engineering, the strength of a structure is tested not during calm weather but during storms. Chatham had spent five years quietly reinforcing its foundations. It was about to need every bit of that strength.

And then, in a matter of weeks, the world changed.

VII. The COVID Crucible (2020-2021)

Imagine being the general manager of a Residence Inn in Silicon Valley on March 15, 2020. Two weeks ago, your hotel was running at eighty-plus percent occupancy, filled with tech consultants and project workers. Now, those guests are gone. Their companies have sent everyone home. Conferences are canceled. Flights are grounding. The lobby, which last week buzzed with laptop-tapping road warriors raiding the breakfast buffet, is empty. The question is not "How do we fill rooms?" The question is "Do we even keep the doors open?"

The speed at which COVID-19 dismantled the hotel industry was unlike anything the modern hospitality sector had experienced, including the aftermath of September 11. Chatham began seeing accelerating revenue declines in the second week of March. By March 12, system-wide occupancy had fallen below sixty percent. On March 29, Chatham recorded its lowest single-night occupancy: approximately seventeen percent. In the span of two weeks, the hotel industry experienced a demand collapse that made the Great Recession look like a minor inconvenience.

For Chatham, the immediate human toll was devastating. Approximately seventy percent of the company's employees were laid off, furloughed, or had their hours drastically reduced beginning in mid-March. By the end of June, roughly sixty percent remained laid off or furloughed. These were real people, housekeepers, front desk agents, maintenance workers, and breakfast attendants, whose livelihoods evaporated almost overnight. The hospitality industry's labor crisis, which would constrain recovery for years afterward, was born in these brutal weeks.

The financial response was swift and comprehensive. Chatham suspended its common dividend entirely, preserving approximately $5.3 million per month, or sixty-four million dollars annualized. Capital expenditure plans for 2020 were slashed by ten million dollars. Service levels were reduced to the bare minimum. Every discretionary dollar of spending was eliminated.

Management entered what can only be described as financial fortress mode. The goal was simple: preserve enough cash to survive an uncertain duration of near-zero revenue while keeping every hotel open and every critical system functioning.

In early May 2020, Chatham negotiated an amendment to its $250 million revolving credit facility, securing covenant relief through June 2021 with covenants resuming on an annualized basis thereafter. The company entered the crisis with $58 million in unrestricted cash and $11.6 million in restricted cash. These financial reserves, combined with the dividend suspension and capex cuts, gave Chatham the runway it needed to survive.

But here is where the story diverges from the broader hotel industry narrative. While many hotel owners were forced to close properties entirely, Chatham kept every single hotel open throughout the pandemic. Every one. This was not a philosophical statement about resilience. It was a direct consequence of the extended-stay strategy and Island Hospitality's operating model.

Extended-stay hotels, by their nature, can operate at extremely low occupancy levels and still cover their variable costs. With fewer staff required per occupied room and lower daily operating expenses than full-service properties, a Residence Inn running at twenty percent occupancy can remain cash-flow neutral or even slightly positive when a comparable full-service hotel would be bleeding money. Island Hospitality's ability to rapidly scale staffing down, cross-train remaining employees, and operate hotels at skeleton crew levels was the operational platform that made this possible.

And the demand, while thin, never disappeared entirely. This is one of the most underappreciated aspects of the extended-stay model: even in the worst crisis imaginable, there are people who need a place to live for weeks or months at a time. Extended-stay properties became housing for military personnel deployed to assist with pandemic response, infrastructure workers maintaining critical systems, first responders who could not risk bringing the virus home to their families, and medical professionals on temporary assignments at overwhelmed hospitals. Travel nurses, in particular, became a major demand driver for extended-stay hotels during 2020 and 2021.

These were not luxury travelers. They were essential workers who needed a safe, clean, affordable place to stay for weeks or months at a time. Chatham's Residence Inns and Homewood Suites, with their kitchenettes, separate living areas, and weekly housekeeping model, were perfectly suited to serve this demand. A travel nurse pulling twelve-hour shifts at a nearby hospital could come back to a Residence Inn suite, cook a simple meal in the kitchenette, do laundry on-site, and have the kind of stable living environment that a transient hotel room simply cannot provide. This was not a marketing strategy. It was the natural fit between a product designed for long-term occupancy and a crisis that created millions of displaced workers.

The quarterly numbers tell the recovery story in stark relief. In the second quarter of 2020, Chatham's RevPAR collapsed to thirty-three dollars, a seventy-seven percent decline, with occupancy at thirty-four percent. By the third quarter, RevPAR had jumped seventy-six percent sequentially to fifty-eight dollars, with occupancy recovering to fifty-three percent. By the fourth quarter, RevPAR stood at forty-seven dollars with forty-five percent occupancy. The trajectory was unmistakable: Chatham was recovering faster than the industry, and faster than its lodging REIT peers.

Chatham also demonstrated opportunistic capital allocation during the crisis. The company sold select properties at approximately 6.5 percent capitalization rates on 2019 net operating income, generating thirty-six million dollars to strengthen the balance sheet. Selling hotels during a pandemic sounds counterintuitive, but the logic was sound: these were properties that Chatham had already identified as non-core, and the buyers, many of them private investors with different return requirements, were willing to pay prices that reflected pre-pandemic economics rather than the temporary dislocation.

The company became the second-fastest hotel REIT to return to positive corporate cash flow following the pandemic, a fact that Chatham's management team has highlighted repeatedly in investor presentations and earnings calls. Chatham's RevPAR was the highest of any lodging REIT during the entire COVID period. These were not spin. They were structural outcomes of a strategy that had been deliberately designed, years before anyone had heard of COVID-19, to be resilient in exactly this kind of environment.

It is worth pausing to reflect on what the pandemic revealed about the hotel industry's different models. Full-service hotels, with their restaurants, bars, meeting spaces, and large staffs, were devastated. Many closed entirely. Their fixed cost structures made it impossible to operate at low occupancy levels without hemorrhaging cash. Resort properties experienced their own volatile trajectory, initially collapsing before enjoying a leisure-driven boom in 2021. But extended-stay properties, the quiet workhorses of the industry, proved resilient from day one. They stayed open, served essential workers, and recovered first. The pandemic was, in a very real sense, a natural experiment that tested every hotel category under extreme stress. Extended-stay passed the test decisively.

By the end of 2021, the worst was over, but the scars remained. The hotel industry faced a labor shortage that would take years to resolve. Business travel, once the backbone of select-service and extended-stay demand, was recovering unevenly as remote work reshaped corporate culture. And balance sheets across the lodging REIT sector bore the marks of emergency borrowings, suspended dividends, and deferred maintenance. Chatham had survived, but the question now was whether its model could thrive in a post-pandemic world that looked fundamentally different from the one that preceded it.

VIII. The Recovery and Dividend Reinstatement (2022-2023)

There is a particular kind of satisfaction in watching a thesis that was tested to destruction prove itself correct. For Jeffrey Fisher, 2022 was that moment.

The recovery, when it came, was faster and stronger than almost anyone had predicted. Business travel, which many observers had written off as permanently diminished by Zoom and remote work, came roaring back in 2022. The narrative that "business travel is dead" proved to be one of the pandemic era's great misreadings of human behavior. People, it turns out, still need to meet face to face. Deals still get done over dinners. Training programs still require physical presence. And the kind of extended project work that fills Chatham's Residence Inns, a six-week software implementation, a three-month construction project, a semester-long consulting engagement, proved remarkably resistant to virtualization. Chatham's weekday occupancy, which for lodging investors is the purest measure of business travel demand because leisure travelers predominantly stay on weekends, climbed from approximately sixty percent in the first quarter of 2022 to over seventy percent by May, and then crossed eighty percent in June, the first time weekday occupancy had reached that level since the pandemic began.

The most telling statistic arrived around Labor Day 2022: Tuesday and Wednesday night occupancy jumped to eighty-seven percent, surpassing weekend occupancy of eighty-two percent for the first time since before the pandemic. This was significant because it demonstrated that the business traveler, often prematurely declared extinct by work-from-home advocates, was not only alive but returning in force. For Chatham, whose portfolio was deliberately weighted toward business travel markets and extended-stay demand, this was the ultimate validation.

The financial results were correspondingly strong. Second quarter 2022 RevPAR surged fifty percent year-over-year to $138, with average daily rates up thirty-six percent to $179 and occupancy growing ten percentage points to seventy-seven percent. Chatham produced the highest operating margins of all lodging REITs in 2022, a distinction that underscored both the quality of the portfolio and Island Hospitality's operational execution.

With the business recovering, Chatham's board took a meaningful step in December 2022: reinstating the common dividend for the first time since early 2020.

The initial quarterly dividend was set at seven cents per share, a modest amount that reflected management's prioritization of balance sheet repair over shareholder distributions. Some shareholders had been clamoring for a larger payout, pointing to the strong recovery in occupancy and rates. But management held firm. The message was clear: Chatham would grow the dividend only as the balance sheet strengthened and the recovery proved durable. Patience over populism.

Portfolio recycling continued through this period, now from a position of strength rather than necessity. Chatham sold five hotels averaging twenty-six years old at an approximate six percent yield for $147 million in total proceeds. These were older properties with higher ongoing capital needs, and selling them allowed Chatham to simultaneously improve portfolio quality and strengthen the balance sheet.

The deleveraging was dramatic. Net debt-to-EBITDA was reduced by sixty-three percent from its March 31, 2020 peak, the second-highest reduction among all hotel REITs. This was not just a defensive measure. It was strategic positioning for the next phase of the cycle, building the financial firepower to pursue acquisitions when prices become attractive. A REIT with a clean balance sheet and ample liquidity has options that a leveraged competitor does not.

The 2023 recovery deepened further, and the numbers told a story of a company that was not merely recovering but outperforming. First quarter RevPAR increased twenty-eight percent year-over-year to $116, roughly eleven percentage points above the industry average growth rate. That gap between Chatham's recovery pace and the industry's is telling: it suggests that the company's portfolio was not just benefiting from a rising tide but was genuinely positioned in the right markets with the right product. By the second quarter, RevPAR reached $144, with average daily rates of $182, both approaching pre-pandemic levels. September and October weekday RevPAR hit post-pandemic highs, particularly in Chatham's technology-heavy markets like Silicon Valley and Bellevue, Washington, where the return-to-office movements at major tech companies drove renewed demand for extended-stay accommodations.

During this period, Chatham also formalized its environmental commitments. The company established an ESG Committee in 2022 with oversight of climate risks, human capital management, and diversity initiatives. Environmental targets included a thirty percent reduction in energy intensity and water usage by 2030, a fifty percent reduction in absolute carbon emissions by the same year, and net-zero carbon by 2050. By 2023, the company had invested approximately four million dollars in efficiency improvements across the portfolio and had achieved a twenty-four percent reduction in greenhouse gas emission intensity since 2017. The company earned three of five stars from the Global Real Estate Sustainability Benchmark with an overall score of seventy-five out of one hundred.

These ESG commitments reflected both genuine environmental stewardship and pragmatic business logic. Energy costs are a significant line item for hotel operations, and reductions in consumption translate directly to margin improvement. For Chatham, sustainability and profitability were not competing objectives but complementary ones.

IX. The Modern Portfolio Strategy (2024-Present)

As of late February 2026, Chatham Lodging Trust's portfolio stands at thirty-three hotels totaling 5,021 rooms and suites across fifteen states and Washington, D.C. Fifty-nine percent of rooms are in extended-stay properties, the highest concentration of any publicly traded lodging REIT. Approximately sixty-six percent of hotel EBITDA derives from extended-stay hotels, predominantly Residence Inn by Marriott and Homewood Suites by Hilton.

The brand lineup reads like a roster of the strongest franchise systems in American hospitality. Residence Inn by Marriott dominates with sixteen hotels, anchoring the extended-stay strategy. Homewood Suites by Hilton, Courtyard by Marriott, Hampton Inn and Hampton Inn and Suites, Hilton Garden Inn, Hyatt Place, SpringHill Suites, and Embassy Suites round out the portfolio. Approximately sixty-three percent of the portfolio is affiliated with Marriott International brands and roughly thirty-two percent with Hilton Worldwide brands.

Silicon Valley and Bellevue, Washington remain the portfolio's twin anchors, together generating roughly sixty-five percent or more of hotel EBITDA over trailing twelve-month periods. This concentration in technology-driven markets is both a strength and a vulnerability, a point the bear case addresses in detail. But it also means that Chatham's fortunes are tied to some of the most dynamic economic ecosystems in the world, markets where the demand generators, major technology employers, are themselves among the most valuable companies on earth.

The portfolio refinement continued through 2024 and 2025. In late December 2024, Chatham sold the twenty-seven-year-old, 147-suite Homewood Suites in Billerica, Massachusetts for $17.4 million. The property had been projected to rank among the three lowest RevPAR hotels in the portfolio, generating approximately one million dollars of net operating income in 2025, which equated to a capitalization rate of roughly four percent for the buyer. A planned six-million-dollar renovation was shelved in favor of the sale. This is the capital recycling playbook in its purest form: sell an aging property that would require significant reinvestment, redeploy the proceeds into higher-returning uses, and improve the overall portfolio quality in the process.

Through 2025, Chatham sold four additional hotels for total proceeds of approximately $71.4 million at an approximate six percent capitalization rate. Combined with the Billerica sale, six hotels were divested since December 2024 for approximately one hundred million dollars in aggregate proceeds. These were not fire sales. They were deliberate dispositions of older, lower-RevPAR properties that improved the portfolio's overall quality and reduced the company's forward capital expenditure requirements.

The most notable recent development is Chatham's announcement of a new hotel development in Portland, Maine. The company owns land adjacent to its existing Hampton Inn in downtown Portland, acquired in 2013, with essentially no remaining cost basis. Construction is expected to commence in the coming months, with an opening planned before summer 2028.

This deserves attention because it represents a meaningful departure from Chatham's historical focus on acquisitions over development. Building a hotel from scratch is a fundamentally different discipline than buying and improving an existing one. Development involves construction risk, permitting risk, cost overrun risk, and the risk of opening into a weaker market than the one that existed when the project was approved. Fisher has historically avoided these risks, preferring the certainty of buying operating hotels at known prices. But the Portland opportunity is unusual: the land is already owned with no remaining cost basis, the adjacent Hampton Inn provides market intelligence and operational infrastructure, and Portland's tourism-driven economy supports strong extended-stay demand. The risk-reward calculus is different when you are building on free land in a market you already know intimately.

On the capital allocation front, 2025 marked another milestone. In May, Chatham's board approved the company's first-ever twenty-five-million-dollar share repurchase program. The company repurchased approximately 1.8 million shares, roughly four percent of shares outstanding, at an average price of $6.87 per share. Management indicated its intention to deploy most of the remaining authorization in 2026. The quarterly dividend was increased by twenty-nine percent in 2025, signaling growing confidence in the sustainability of cash flows.

The balance sheet at year-end 2025 was the strongest in Chatham's history. Total consolidated debt stood at $343 million at a 6.2 percent average interest rate, with zero borrowings on the three-hundred-million-dollar revolving credit facility. Net debt of $319 million was down seventy million dollars from the prior year. The leverage ratio of twenty percent, measured as net debt to hotel investments at cost, was the lowest since the company's 2010 IPO.

Looking ahead, Chatham's 2026 guidance projects RevPAR growth of negative 0.5 percent to positive 1.5 percent, adjusted EBITDA of eighty-four to eighty-nine million dollars, and adjusted FFO per share of $1.04 to $1.14. Management expects one or two additional opportunistic hotel dispositions in 2026 and has signaled that external acquisitions could resume as financing costs ease and seller expectations adjust to market realities. On the most recent earnings call, management struck an optimistic tone about the acquisition pipeline, noting that the gap between buyer and seller expectations, which had frozen the transaction market for much of 2023 and 2024, was finally beginning to narrow.

The share repurchase program is another signal worth noting. When a REIT buys back its own stock at a significant discount to estimated private market values, management is effectively telling the market: "Our stock is cheaper than the hotels we could buy." At an average purchase price of $6.87 per share, Fisher clearly believed the market was undervaluing Chatham's portfolio. Whether he is right depends on your view of hotel valuations and the direction of interest rates, but the willingness to put capital behind that conviction is meaningful.

X. Playbook: Business and Investing Lessons

Every great business story distills into a set of principles that transcend the specific industry. Chatham Lodging Trust's sixteen-year journey offers several that deserve attention, not because they are novel, but because the company has actually lived them rather than merely advertising them. Most corporate mission statements claim to value discipline, focus, and operational excellence. Chatham has the results to prove it.

Focus wins. This is the overarching lesson. In an industry where many REITs diversify across full-service, limited-service, resort, and urban properties, Chatham chose to concentrate exclusively on extended-stay and premium select-service hotels. That concentration meant fewer properties to manage, deeper expertise in a specific segment, and a portfolio that was structurally advantaged during both normal times and crisis conditions. The temptation to diversify, to chase the latest hot segment or geographic market, is powerful. Chatham resisted it, and the margin performance vindicates the discipline.

Operational control matters. The Island Hospitality relationship is not merely a management agreement. It is a competitive advantage embedded in the company's structure. When the operator and the owner share aligned economic interests, and when the operator has four decades of experience in exactly the kind of hotels the owner buys, the result is a level of execution that third-party management cannot replicate. Investors should study whether the companies they own have genuine operational advantages or merely claim to.

Balance sheet discipline is non-negotiable. Fisher watched his old Innkeepers portfolio collapse under the weight of Apollo's leveraged buyout. That experience clearly shaped Chatham's conservative approach to debt. The company entered the pandemic with moderate leverage, maintained liquidity throughout, and emerged with the financial strength to pursue offensive capital allocation. In real estate, leverage is a tool. It amplifies returns in good times and accelerates destruction in bad times. Chatham chose to use less of it than most peers, and the pandemic vindicated that choice.

Opportunistic capital allocation requires patience. Chatham's history is punctuated by bursts of activity, the 2010 post-IPO acquisitions, the 2014 Silicon Valley deal, the recent share repurchase program, separated by long periods of apparent inactivity. This pattern reflects a capital allocation philosophy that prizes quality over activity. Fisher does not buy hotels to grow the portfolio. He buys hotels when prices are attractive and the strategic fit is compelling. The willingness to wait, to maintain dry powder through years of discipline, and to strike quickly when opportunity appears is a hallmark of the best capital allocators in any industry.

Small can be beautiful. Chatham's thirty-three-hotel portfolio would fit inside many of its peers' portfolios several times over. But concentrated excellence can outperform sprawling mediocrity. Chatham knows every market it operates in with intimate depth. Management can visit every property multiple times per year. Capital allocation decisions involve a manageable number of assets. The disadvantages of scale, lack of diversification, limited acquisition pipeline, reduced negotiating power, are real. But Chatham's results suggest that the advantages of focus, depth of knowledge, speed of decision-making, and operational consistency can more than compensate.

Crisis preparation is a peacetime activity. The reason Chatham survived the pandemic better than most peers is that every strategic decision made between 2009 and 2019, the extended-stay focus, the conservative balance sheet, the Island Hospitality relationship, the geographic concentration in resilient markets, turned out to be a form of crisis preparation. Companies that prepare for adversity during good times do not need to scramble during bad times. This lesson applies far beyond hotels.

Founder-operator alignment creates value that is difficult to quantify but impossible to ignore. Fisher's dual role as CEO of Chatham and majority owner of Island Hospitality creates an intensity of focus and a level of accountability that purely professional management teams rarely achieve. When your personal wealth is tied to both the owner and the operator of a hotel portfolio, every decision receives a level of scrutiny that simply does not exist in more diffuse organizational structures. The governance risks of this arrangement are real, as discussed earlier, but so are the performance benefits.

Finally, the power of patient capital deserves emphasis. Chatham waited until late 2022 to reinstate its dividend, prioritizing balance sheet repair over shareholder distributions even as some peers were rushing to resume payouts. Management resisted the temptation to declare victory prematurely. In an era of short-term thinking and quarterly pressure, this kind of patience is rare, and it is one of the most reliable indicators of management quality in capital-intensive businesses.

XI. Porter's Five Forces and Hamilton's Seven Powers Analysis

Having told the story, it is time to analyze the business through two of the most rigorous analytical frameworks available to investors. Porter's Five Forces examines the structural attractiveness of the industry Chatham operates in, while Hamilton Helmer's Seven Powers framework identifies the specific sources of durable competitive advantage that Chatham possesses, or lacks. Together, these frameworks provide a comprehensive map of Chatham's competitive position and the durability of its moat.

Starting with the threat of new entrants: the hotel industry presents a paradox. Capital requirements for individual properties are high, but capital is abundantly available through REIT structures, private equity, and institutional investors. Anyone with sufficient capital can buy a franchise agreement from Marriott or Hilton and build a hotel. What protects Chatham is not the difficulty of entering the hotel business generally, but the difficulty of entering its specific markets. Silicon Valley, coastal Maine, downtown Savannah, and the other high-barrier markets where Chatham concentrates its portfolio have limited land availability, restrictive zoning, and lengthy permitting processes that slow new supply growth. Additionally, Chatham's relationships with the major brands and its track record with Island Hospitality give it advantages in sourcing off-market deals that newer entrants lack.

The bargaining power of suppliers is a nuanced consideration. Chatham's most important suppliers are the hotel brands themselves, Marriott, Hilton, and Hyatt, which provide the franchise licenses, loyalty programs, and reservation systems that drive occupancy. These brands hold meaningful power: franchise fees typically run seven to twelve percent of room revenue, and the terms are largely non-negotiable. However, the brands also need capable franchisees who maintain property standards and deliver consistent guest experiences. Chatham's track record as an operator, through Island Hospitality, makes it a desirable franchise partner. Labor is another critical input, and extended-stay hotels' lower labor intensity provides structural insulation from wage inflation, though not immunity, as 2024 and 2025 demonstrated.

The bargaining power of buyers, in this case hotel guests, is high. Business and leisure travelers have abundant choices, and price comparison is frictionless in the age of online travel agencies. However, extended-stay guests exhibit more loyalty than transient travelers. A consultant settling into a Residence Inn for a six-week project is unlikely to switch hotels mid-stay. Corporate contracts, which guarantee certain rates in exchange for volume commitments, provide additional stability. Chatham's RevPAR index of 126 to 144 percent, meaning its hotels consistently outperform their competitive sets by twenty-six to forty-four percent, suggests that the company successfully commands premium pricing despite buyer power.

The threat of substitutes has evolved significantly with the rise of Airbnb and corporate housing alternatives. For transient travelers, Airbnb represents a genuine competitive threat. But for extended-stay guests who need the consistency of hotel services, daily maintenance, weekly housekeeping, front desk support, on-site fitness and laundry facilities, the substitute threat is more limited. Premium brand affiliation provides a quality guarantee that unbranded alternatives cannot match. That said, the lines between hotels and alternative accommodation continue to blur, and Chatham must continuously deliver value that justifies its premium positioning.

Competitive rivalry among hotel REITs is intense. Numerous public and private owners compete for the same properties, the same guests, and the same markets. Chatham differentiates itself through its extended-stay concentration, operational excellence, and margin superiority. But the hotel REIT space includes well-capitalized competitors like Apple Hospitality REIT, Pebblebrook Hotel Trust, RLJ Lodging Trust, and Summit Hotel Properties, all of whom have larger portfolios and, in some cases, broader strategic mandates. Chatham's competitive advantage is not in outbidding rivals for properties but in operating them better and selecting them more carefully.

Turning to Hamilton Helmer's Seven Powers framework, which identifies the specific sources of durable competitive advantage, Chatham's picture becomes more nuanced.

Scale economies are weak. With thirty-three hotels, Chatham cannot achieve the purchasing power, marketing leverage, or operational efficiencies of a Marriott or Hilton. Island Hospitality partially offsets this by managing over one hundred hotels across its entire portfolio, spreading fixed costs across a larger base. But within the REIT itself, scale is not a source of power.

Network effects are essentially absent. Guests choose hotels based on brand, location, and price, not because other guests are staying there. Whatever network effects exist in lodging accrue to the brand loyalty programs of Marriott and Hilton, not to the REIT that owns the physical properties.

Counter-positioning is more interesting. Chatham's exclusive focus on extended-stay and select-service properties when most peers diversify across hotel types represents a strategic position that larger, more diversified REITs would find difficult to replicate without abandoning their existing strategies. The pandemic validated this positioning in dramatic fashion, demonstrating that the extended-stay model generates higher margins, more resilient demand, and faster recovery than diversified hotel portfolios. A larger REIT could theoretically pivot to an extended-stay focus, but doing so would require selling off hundreds of full-service properties and fundamentally restructuring its operations, a move that management teams and boards are psychologically and structurally resistant to making.

Switching costs are weak at the guest level but moderate at the corporate contract level. Extended-stay guests face modest friction when considering a move, primarily the hassle of packing and relocating during a long-term stay. Corporate contracts create somewhat higher switching costs, as renegotiating hotel agreements across a large organization involves administrative burden and relationship disruption.

Branding power is a complex topic for Chatham. The company's brand is essentially invisible to consumers, who see Marriott and Hilton logos, not the Chatham name. However, Chatham has built a meaningful brand among REIT investors, who recognize it as the highest-margin, most operationally disciplined lodging REIT in the public market. Fisher's personal track record, spanning four decades and two public companies, functions as a form of founder brand that attracts capital and deal flow.

Cornered resource is where Chatham's analysis becomes compelling. Island Hospitality Management, Fisher's privately held management company, is a proprietary operating platform that produces industry-leading margins. No other lodging REIT has access to Island Hospitality's capabilities, and the decades of institutional knowledge embedded in the management team cannot be easily replicated. Fisher's relationships with the major brands, developed over forty years of operating Marriott and Hilton properties, and his network of hotel brokers and sellers provide deal flow advantages that newer competitors lack. The prime locations in high-barrier markets, once acquired, are extremely difficult for competitors to replicate given supply constraints.

Process power is Chatham's strongest competitive advantage and its primary moat. The company has developed, over decades, a repeatable process for identifying under-managed properties, acquiring them at attractive prices, improving operations through Island Hospitality, executing targeted capital improvements, and recycling capital through strategic dispositions.

This process encompasses underwriting discipline, operational execution, revenue management, capital allocation, and crisis management, all of which have been tested and refined across multiple economic cycles including the Great Recession and COVID-19. Process power is the hardest competitive advantage to identify from the outside and the hardest to replicate, because it is embedded in organizational culture, institutional knowledge, and hundreds of small decisions made correctly over time. You cannot buy process power. You cannot hire it away from a competitor. You can only build it through years of disciplined execution.

The primary moats, then, are process power and cornered resource, specifically Island Hospitality Management. These are reinforced by moderate counter-positioning through the extended-stay focus. The weakness is scale, which limits Chatham's ability to spread costs, access capital markets at the most favorable terms, and compete for the largest portfolio transactions.

XII. Bull versus Bear Case

The investment case for Chatham Lodging Trust rests on a tension between structural advantages and structural limitations that investors must weigh carefully.

The bull case begins with the extended-stay structural tailwind. The work-from-anywhere movement, rather than destroying business travel, has in many ways extended it. Workers who no longer commute daily to an office may travel more frequently for in-person collaboration, training sessions, and project work that requires multi-week stays.

Cost-conscious corporations increasingly prefer extended-stay hotels over traditional hotels for longer assignments because the per-night rates are lower and the kitchenette amenities reduce meal expenses. A company sending an employee to a Residence Inn for a month saves meaningfully on both lodging and meal per-diems compared to a full-service hotel. These secular trends favor Chatham's portfolio composition more than almost any other publicly traded lodging REIT.

Industry-leading margins provide both offensive and defensive advantages. In a downturn, higher margins mean that Chatham can remain profitable at lower occupancy levels than competitors, as the pandemic demonstrated. In a recovery, margin expansion on incremental revenue drops more to the bottom line. This margin advantage is not a temporary phenomenon but a structural feature of the portfolio composition and the Island Hospitality operating model.

The balance sheet is a significant source of optionality. With leverage at its lowest level since the 2010 IPO, zero borrowings on its revolving credit facility, and net debt down seventy million dollars in 2025 alone, Chatham has the financial capacity to pursue acquisitions, share repurchases, dividend increases, or development projects. This optionality is especially valuable in a period when hotel transaction activity may pick up as financing costs moderate and seller expectations adjust.

Fisher's track record and aligned incentives provide comfort on capital allocation. As both the CEO of Chatham and the majority owner of Island Hospitality, Fisher has meaningful economic exposure to Chatham's success. His history of building and selling Innkeepers at the top of the market, then buying back assets at distressed prices during the crisis, demonstrates a level of capital allocation skill that few REIT executives can claim.

The bear case is equally substantial, and intellectually honest investors must grapple with it.

Scale limitations are real and consequential. With thirty-three hotels, Chatham lacks the negotiating power, diversification benefits, and market presence of larger peers. Apple Hospitality REIT, by comparison, owns over two hundred hotels. Pebblebrook Hotel Trust owns roughly fifty. Even among select-service-focused REITs, Chatham is small. The company's trading liquidity is lower, which means larger institutional investors may avoid it simply because they cannot build a meaningful position without moving the stock price. Analyst coverage is thinner, which limits visibility among potential investors. And the ability to access capital markets at favorable terms is more constrained, because underwriters and lenders give better pricing to larger, more liquid issuers. Size matters in real estate, and Chatham is small.

Business travel's trajectory remains uncertain. While the 2022-2023 recovery was impressive, the long-term question of whether business travel will fully return to pre-pandemic levels remains open. If corporate budgets permanently shift toward virtual meetings and reduced travel, Chatham's business-travel-dependent portfolio would face a structural headwind.

Concentration risk cuts both ways. Thirty-three hotels in fifteen states means that a regional economic downturn, a natural disaster, or a new competitive supply in one or two key markets can have a disproportionate impact on the overall portfolio.