The Cigna Group: The Architect of the Healthcare Flywheel

I. The $200 Billion "Stealth" Giant

Here is a riddle for students of American capitalism: What company generates nearly $275 billion in annual revenue, ranks among the fifteen largest corporations on earth by that measure, and yet most Americans think of it as "just their health insurance company"? The answer is The Cigna Group, and the gap between perception and reality is one of the great mispricings in the market's collective imagination.

Walk into any corporate benefits office in the country and mention Cigna, and someone will nod and say, "Yeah, that's who does our dental." They are not wrong. Cigna Healthcare, the insurance arm, does indeed administer medical, dental, and behavioral health plans for millions of Americans. But here is the twist that separates the casual observer from the informed investor: roughly eighty-five percent of The Cigna Group's revenue does not come from insurance premiums at all. It comes from a sprawling health services operation called Evernorth, which fills prescriptions, manages drug formularies, runs specialty pharmacies, and negotiates drug prices for over a hundred million people, many of whom have never held a Cigna insurance card in their lives.

The thesis of this story is simple, and like all great business stories, it turns on a single fork in the road. In 2015, Anthem, the second-largest health insurer in America, tried to buy Cigna for $54 billion. The Department of Justice blocked the deal. Instead of sulking, Cigna's leadership took the breakup as a liberation. Three years later, they placed a $67 billion bet on Express Scripts, the nation's largest standalone pharmacy benefit manager. That acquisition was the pivot point. It transformed Cigna from a mid-tier health insurer competing on premium pricing into something far more durable: the operating system for how drugs move through the American healthcare supply chain.

To understand why that distinction matters, think of it this way. A health insurer is essentially a toll collector. It sits between employers and hospitals, collecting premiums and paying claims, and the difference between those two numbers, the medical loss ratio, determines profitability. It is an inherently volatile business, subject to the whims of flu seasons, pandemics, and regulatory caprice. A pharmacy benefit manager, by contrast, is more like a logistics company crossed with a purchasing cooperative. It negotiates drug prices with manufacturers, determines which drugs appear on formularies, and processes billions of prescriptions. The margin is thinner per transaction, but the volume is staggering, and critically, the revenue is far more predictable.

The story of how a two-hundred-year-old fire insurance company reinvented itself as a pharmacy and health services giant is the story of disciplined capital allocation, a CEO with an unusually long runway, and the willingness to walk away from the biggest deal in industry history in order to pursue an even bigger one.

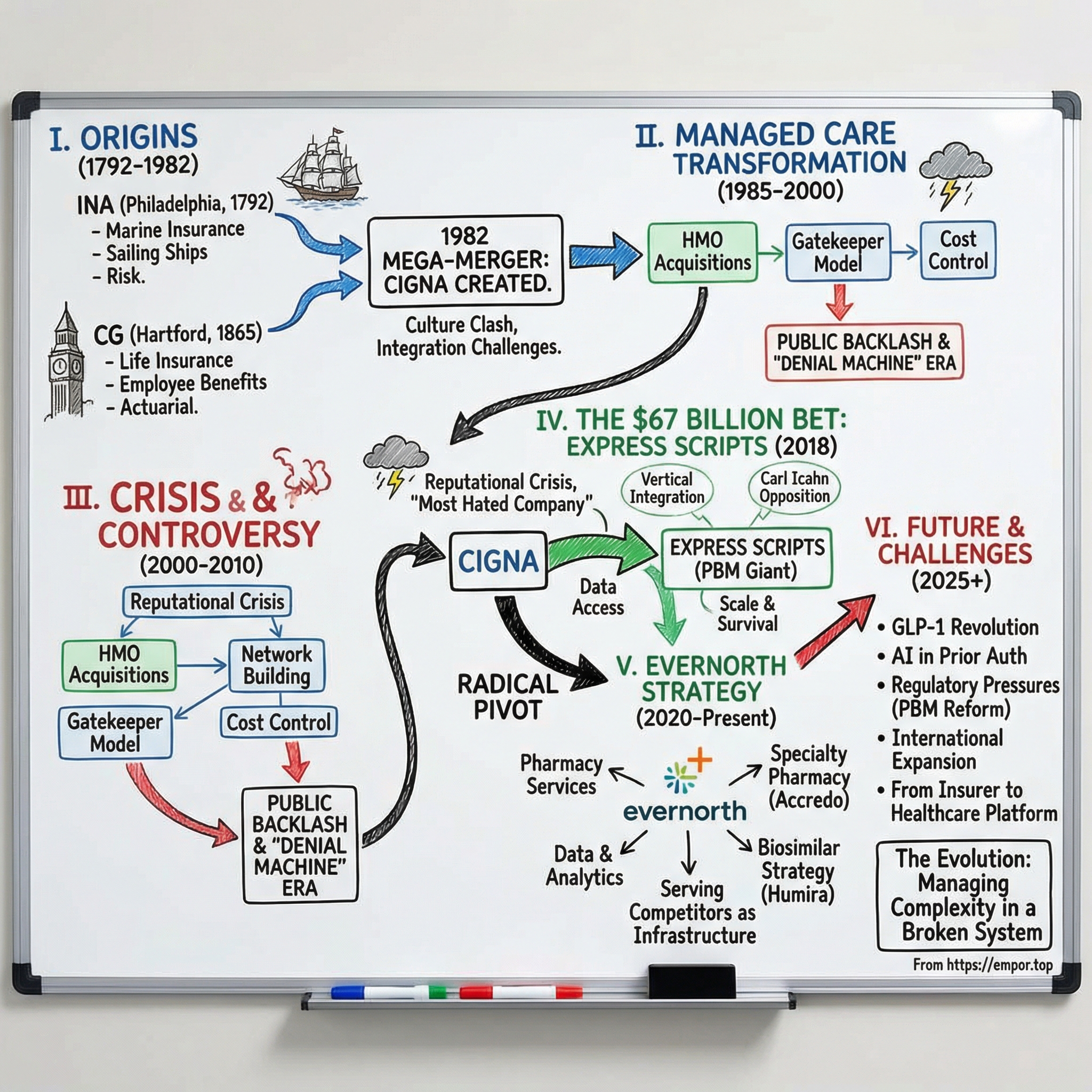

II. Pre-History: The Insurance Company of North America

Philadelphia, November 1792. The ink on the Constitution was barely five years dry. George Washington was still president. And in a room at the Pennsylvania State House, the same building where the Declaration of Independence had been signed sixteen years earlier, a group of merchants gathered to decide what to do with a failed investment vehicle called the Universal Tontine Association. A tontine, for the uninitiated, was a kind of morbid lottery: investors pooled money, and as members died off, the survivors split a growing share of the returns. This particular tontine had collapsed, but the capital remained, and the men in the room had an idea. They would form a general insurance company, one that could write policies on fire, life, and marine risks.

On November 19, 1792, articles of association were adopted. They called it the Insurance Company of North America, or INA. Six hundred thousand dollars in capital was raised by selling forty thousand shares at ten dollars each. Every share was subscribed within eleven days, a pace that would impress a modern venture capitalist. John Maxwell Nesbitt, a merchant and underwriter, was elected president, and INA opened for business on December 15 at 119 South Front Street. Its first policy covered a ship named America on a voyage to Derry. The name was fitting. INA would go on to insure a young nation's ambitions for the next two centuries, building deep expertise in property, casualty, and international markets.

Meanwhile, up the coast in Hartford, Connecticut, a different kind of insurance company was taking shape, though not until seven decades later. Connecticut General Life Insurance Company was chartered in 1865 by a special act of the governor. Its original intended name was "Connecticut Invalid," conceived by a founder who saw a market opportunity in insuring people in poor health, the risks that other companies refused to touch. Someone wisely pointed out that "invalid" could be read as either "a sick person" or "not valid," and the name was changed to Connecticut General before the charter was signed. CG became a pillar of Hartford's insurance establishment, eventually introducing group life policies in 1913 and building a dominant position in employee benefits.

For most of the twentieth century, INA and CG occupied parallel but non-overlapping lanes. INA was international, focused on property and casualty. CG was domestic, focused on life and group benefits. The logic of combining them was the logic of 1980s conglomerate diversification: spread risk across uncorrelated businesses, achieve scale, and present a single face to the corporate benefits buyer.

On March 31, 1982, the merger closed. The new company needed a name, and in a feat of corporate portmanteau that only the early Reagan era could have produced, they mashed together the letters of Connecticut General and INA to create CIGNA. Robert Kilpatrick from CG and Ralph Saul from INA served as joint CEOs, the board was split evenly, and the company immediately had the identity problem that plagues most mergers of equals. Which culture would prevail? The buttoned-up Hartford life insurance world, or the swashbuckling Philadelphia property and casualty world?

The answer, as it turned out, was neither. The 1980s and 1990s were a slog. Cigna wrestled with asbestos liabilities from INA's legacy book, fought through the managed care backlash of the late 1990s, and cycled through leaders. But those decades of grinding through adversity produced something valuable: a risk-averse, capital-efficient culture that prioritized underwriting discipline over growth at any cost. That DNA would prove essential when a new leader arrived with a very different vision for what the company could become.

III. The Cordani Era and The Great Pivot

David Cordani did not parachute into the CEO suite from McKinsey or Goldman Sachs. He grew up in Connecticut, earned his bachelor's degree from Texas A&M, came back east for an MBA at the University of Hartford, and joined Cigna in 1991 as a mid-level employee. He was thirty years old when he walked through the door. He was forty-three when he was named president and chief operating officer in 2008. He became CEO on December 15, 2009, at the age of forty-three, inheriting a company that was still fundamentally defined by its insurance roots.

What made Cordani different was not charisma or public persona. He is not a Steve Jobs or a Jamie Dimon. He is quiet, analytical, and intensely focused on operational metrics. People who have worked with him describe a leader who communicates in spreadsheets and strategy decks, who can recite utilization trends and pharmacy dispensing volumes from memory, and who views healthcare not as a social mission but as an engineering problem. The question he kept asking in those early years as CEO was deceptively simple: Where is the margin, and where is it going?

The answer, when he looked at the data, was unsettling for anyone running a traditional health insurance company. Insurance margins were compressing. The Affordable Care Act, signed into law the year after Cordani became CEO, introduced medical loss ratio floors that capped how much insurers could keep from premiums. Medicare Advantage rates were subject to annual government adjustments. Employer clients were getting more sophisticated about negotiating rates. And the competitive landscape was brutal: UnitedHealth Group was pulling away from the pack, not because of its insurance business, but because of Optum, its fast-growing health services arm.

Cordani saw what was happening and made a bet that would define his tenure. He began reorienting Cigna from "paying claims" to "managing total health." The distinction is subtle but profound. A claims payer is reactive: someone gets sick, sees a doctor, and the insurer writes a check. A total health manager is proactive: it identifies which patients are at risk, steers them toward cost-effective treatments, manages their prescriptions, and captures margin at every step of the care delivery chain.

The strategic logic was sound, but Cordani needed a vehicle. Cigna's existing assets, while solid, were not sufficient to execute the vision. He needed a pharmacy engine, a data platform, and a client base that extended far beyond Cigna's own insurance members. He needed, in other words, a pharmacy benefit manager.

His compensation structure tells the story of how seriously the board took this transformation. By fiscal year 2025, Cordani's total compensation was approximately $22.9 million, of which ninety-two percent was performance-based. The long-term equity component, representing roughly three-quarters of his target pay, was dominated by strategic performance shares tied to adjusted earnings-per-share growth and return on equity. His personal equity stake in the company, approximately 621,000 shares, was worth roughly $177 million. This was not a caretaker CEO clipping coupons. This was a manager whose wealth was welded to the company's long-term compounding trajectory. And to compound, Cigna needed to stop being just an insurer. But first, it had to survive an existential threat from its biggest competitor.

IV. The $54 Billion "Almost": The Anthem Merger

On July 23, 2015, Anthem, the second-largest health insurer in the United States, announced a definitive agreement to acquire Cigna for more than $54 billion, a thirty-eight percent premium to Cigna's market capitalization. The deal would have created the largest health insurer in America, combining the number two and number three players into a behemoth serving roughly fifty-three million medical members.

The strategic logic, from Anthem's perspective, was straightforward: scale begets bargaining power with hospitals and physicians, and bargaining power drives lower costs, which wins more employer contracts, which creates more scale. It was a virtuous cycle on paper. Anthem's CEO at the time, Joseph Swedish, framed it as a "transformational combination" that would "reshape the health insurance industry."

Cordani, by multiple accounts, was never enthusiastic. The merger agreement contained provisions requiring Cigna's cooperation, but the relationship between the two management teams was fractious from the start. Cordani and Swedish reportedly clashed over integration plans, leadership roles, and strategic direction. Cordani was named to serve as president of the combined entity, but the degree to which he would actually control the health services strategy, the part he cared most about, was ambiguous.

Then the Department of Justice intervened. In July 2016, the DOJ sued to block the deal, arguing that combining the second and third-largest commercial insurers would reduce competition in the sale of health insurance to large, national employers. The government's case was strong. On February 8, 2017, U.S. District Judge Amy Berman Jackson issued a ruling blocking the merger, finding that it would substantially lessen competition. The D.C. Circuit Court of Appeals upheld the decision in a two-to-one ruling in April 2017. Anthem formally terminated the merger agreement the following month.

What happened next is where the story gets interesting. The merger agreement had included a $1.85 billion reverse termination fee, payable by Anthem to Cigna if the deal failed to receive antitrust clearance. Cigna sued for the fee. Anthem countersued for $21 billion, alleging that Cigna had deliberately sabotaged the merger by dragging its feet on integration planning and making public statements designed to provoke the DOJ's opposition.

The litigation dragged through Delaware Chancery Court for years. In 2020, Vice Chancellor J. Travis Laster issued a Solomonic ruling: neither company owed the other a cent. Both had breached the merger agreement in various ways, and the equities canceled out. The Delaware Supreme Court affirmed in May 2021. Cigna never collected its $1.85 billion breakup fee.

But here is the point that matters for the long-term investor: Cigna walked away free. No integration headaches. No culture clashes. No three-year distraction trying to merge two enormous IT platforms. While Anthem spent years litigating and licking its wounds, and while Aetna was about to disappear into CVS Health's retail pharmacy empire, Cigna had a clean balance sheet, a clear strategy, and a CEO who had spent the forced waiting period studying the one acquisition that could change everything.

The failed Anthem merger was the "Sliding Doors" moment. In the parallel universe where the DOJ approves the deal, Cigna becomes a division of Anthem, Cordani likely exits within two years, and the Express Scripts acquisition never happens. In our universe, the DOJ's intervention liberated Cigna to pursue a far more ambitious, and ultimately more valuable, transformation. Sometimes the best deal is the one that does not close.

V. The Masterstroke: Express Scripts and the PBM Bet

On March 8, 2018, less than a year after the Anthem debacle concluded, Cigna announced that it had agreed to acquire Express Scripts Holding Company for approximately $67 billion, including the assumption of roughly $15 billion in Express Scripts debt. The per-share consideration was $48.75 in cash plus 0.2434 Cigna shares, representing a thirty-one percent premium to Express Scripts' closing price the day before. It was the largest healthcare deal of 2018 and one of the largest in history.

To understand why Cordani was willing to pay that price, you need to understand what Express Scripts actually was. Founded in 1986 in St. Louis, Express Scripts had grown into the nation's largest standalone pharmacy benefit manager, processing over a billion prescriptions annually and managing drug benefits for roughly one hundred million Americans. A PBM sits at the center of the pharmaceutical supply chain, serving as the middleman between drug manufacturers, pharmacies, and the employers or health plans that pay for prescriptions. It negotiates rebates with manufacturers, determines which drugs appear on the formulary, and operates mail-order and specialty pharmacies that fill prescriptions directly.

The PBM business model is often described as a "toll booth" on drug spending. Every time a prescription is filled, the PBM captures a small margin, either through the spread between what it pays the pharmacy and what it charges the plan, through retained rebates from manufacturers, or through dispensing fees. Individually, these margins are tiny. But multiply them by a billion-plus annual prescriptions and the math becomes compelling.

Express Scripts also brought Accredo, the largest specialty pharmacy in the United States. Specialty drugs, the high-cost biologics and gene therapies that treat conditions like cancer, rheumatoid arthritis, and multiple sclerosis, represented a fast-growing segment of pharmaceutical spending. Accredo's expertise in handling these complex, often injectable medications, which require cold-chain logistics, patient coaching, and prior authorization management, was a critical competitive advantage.

Critics at the time said Cigna overpaid. Express Scripts had been losing major clients, most notably Anthem, which had moved its PBM contract to CVS Caremark in a bitter dispute over pricing. The stock had been under pressure. At roughly twelve times EBITDA, the acquisition multiple was not cheap by historical standards.

But Cordani's logic was different from the consensus view. He was not buying Express Scripts for its current earnings; he was buying it for the platform. The combination would create a company that could see both sides of the healthcare equation simultaneously: the insurance claim and the pharmacy transaction, the clinical outcome and the cost. That data feedback loop, knowing which drugs worked and what they cost in the real world, was the cornerstone of the strategy.

The deal closed on December 20, 2018, after receiving shareholder approval from both companies and regulatory clearance from the DOJ. Because the merger was vertical, combining an insurer with a PBM rather than two insurers, the antitrust review was far smoother than the Anthem saga. Cigna shareholders owned roughly sixty-four percent of the combined entity; Express Scripts shareholders owned thirty-six percent. The combined company emerged with approximately $41 billion in debt, an eye-watering figure that Cordani pledged to reduce aggressively.

The comparison to CVS Health's acquisition of Aetna, which also closed in late 2018 for approximately $70 billion, is instructive. CVS bought an insurer to pair with its existing retail pharmacy chain and PBM, CVS Caremark. The logic was to drive foot traffic into CVS stores by integrating insurance with retail pharmacy. It was a bricks-and-mortar play, predicated on the idea that the corner drugstore could become a "health hub."

Cigna's deal was the inverse. It bought a capital-light, digitally oriented PBM to pair with its existing insurance platform. There were no stores to renovate, no lease obligations to manage, no retail workforce to unionize. Express Scripts' primary assets were its technology platform, its pharmacy network contracts, its manufacturer rebate agreements, and its mail-order and specialty pharmacy operations. The operating leverage was fundamentally different. CVS was betting on physical infrastructure; Cigna was betting on data and logistics. Both deals were bets on vertical integration, but they were bets on very different versions of the future.

VI. "Hidden" Engines: The Rise of Evernorth

In September 2020, Cigna did something that seemed cosmetic but was actually deeply strategic: it rebranded its health services segment under a new name. They called it Evernorth. The name was deliberately chosen to have no obvious connection to Cigna, insurance, or healthcare. It sounded like a technology company or a private equity firm. That was the point.

The rebranding signaled Cigna's ambition to make its health services platform a standalone entity that could serve any client, including, and this is the crucial insight, competitors. Evernorth was designed to be the "Intel Inside" of healthcare: the engine that powered the system regardless of whose logo was on the insurance card. Approximately ninety percent of Evernorth's business comes from external clients, health plans, employers, and government programs that are not Cigna Healthcare customers. This is a staggering figure that most investors miss. Evernorth is not simply the captive pharmacy arm of a health insurer. It is an open platform that competes for, and wins, contracts from rival insurers.

In February 2023, the corporate structure was further clarified. The holding company became "The Cigna Group." The insurance arm became "Cigna Healthcare." And the services arm became "Evernorth Health Services." The organizational chart now reflected the economic reality: Evernorth was not a subsidiary supporting the insurance business. It was the main event.

The numbers tell the story with brutal clarity. In fiscal year 2025, Evernorth generated approximately $235 billion in revenue, representing roughly eighty-five percent of The Cigna Group's total revenue of $275 billion. Express Scripts pharmacy revenue grew eighteen percent year over year. Specialty and care services, led by Accredo, grew fourteen percent, driven by biosimilar adoption and volume growth. The insurance arm, Cigna Healthcare, contributed the remaining fifteen percent of revenue, and its contribution actually declined eleven percent in absolute terms, partly due to the divestiture of the Medicare Advantage business.

This revenue split represents a fundamental inversion of the company's identity. The Cigna Group is not a health insurer that happens to own a PBM. It is a pharmacy and health services company that happens to own a health insurer. The tail is not just wagging the dog; the tail has become the dog.

Within Evernorth, several engines drive growth. Express Scripts, the core PBM, processes prescriptions, manages formularies, and operates the mail-order pharmacy network. Accredo, the specialty pharmacy, handles the highest-cost, most complex medications and has become a critical profit center as specialty drug spending continues to outpace traditional pharmacy spending. MDLIVE, acquired in 2021, provides virtual care and telehealth services. And eviCore handles medical benefit management, essentially the utilization review function that determines whether a procedure or treatment is medically necessary before the insurer agrees to pay.

The strategic capstone came in January 2024, when Cigna announced the sale of its Medicare Advantage, Medicare Supplemental Benefits, Medicare Part D, and CareAllies businesses to Health Care Service Corporation, the nation's largest customer-owned health insurer, for $3.3 billion. The deal closed on March 19, 2025. The divested business included approximately 600,000 Medicare Advantage members, 450,000 Medicare Supplement members, and 2.5 million Medicare Part D members.

The rationale was elegant in its clarity. Medicare Advantage had become a margin trap. Medical costs in the senior population were rising faster than government reimbursement rates, squeezing margins for every insurer in the space. Humana, which derived the majority of its revenue from Medicare Advantage, was under severe pressure. UnitedHealthcare's Medicare business, while profitable, was consuming enormous management attention. Cordani looked at the return on capital in Medicare Advantage, compared it to the return on capital in Evernorth's PBM and specialty pharmacy businesses, and made the call. The capital was redeployed into share buybacks and reinvestment in the services platform.

For investors, the Medicare divestiture was the clearest signal yet that Cigna's management viewed the company's future as a health services compounder, not a diversified insurer. They were willing to shrink the insurance business to grow the services business, a trade that only makes sense if you believe the services business has a wider moat and a longer runway.

VII. The Playbook: Moats, Powers, and Competitive Position

To evaluate The Cigna Group through the lens of competitive strategy, it helps to step back and ask a fundamental question: What makes it hard for someone to replicate what Evernorth does? The answer involves several interlocking advantages that, taken together, constitute a formidable competitive position.

Start with switching costs. When a large employer or health plan selects Evernorth or Express Scripts as its pharmacy benefit manager, the implementation process is not a simple contract signing. It involves integrating pharmacy data feeds with the client's HR and benefits platforms, configuring formulary designs, establishing clinical protocols, training benefits administrators, and migrating millions of member records. The entire process typically takes six to twelve months, and the disruption risk during a transition is significant: members may lose access to their current medications, prior authorizations may lapse, and customer service volumes spike. Once an enterprise is embedded on the platform, the switching cost is not just financial. It is operational, clinical, and reputational. A benefits director who botches a PBM transition will hear about it from every employee whose prescription was delayed.

Then there is scale. The Cigna Group, through Evernorth, purchases pharmaceuticals on behalf of more than a hundred million people. At that volume, the company functions as one of the largest group purchasing organizations on the planet. Drug manufacturers negotiate rebates with PBMs based on the volume of prescriptions the PBM can steer toward their products. The larger the covered population, the larger the rebates, and the lower the effective cost of goods sold. This creates a classic scale economy: Evernorth can offer employers lower drug costs than smaller PBMs because it buys in larger quantities, and the lower costs attract more employers, which increases the volume further. New entrants face a chicken-and-egg problem. Without volume, they cannot negotiate competitive rebates. Without competitive rebates, they cannot win volume.

The third advantage is data, and this is where the vertical integration of insurer plus PBM creates something genuinely difficult to replicate. Cigna knows two things about a drug that most companies know only one of. It knows the clinical outcome, whether the drug actually worked for the patient, because it sees the medical claims on the insurance side. And it knows the cost, what the drug cost to procure and dispense, because it sees the pharmacy transaction on the PBM side. This closed-loop feedback system allows Evernorth to make formulary decisions based on value, not just price. It can identify which drugs produce the best outcomes per dollar spent and design benefit structures that steer patients toward those drugs. Competitors that operate only a PBM, without an insurance arm, or only an insurer, without a pharmacy platform, see only half the picture.

Against this backdrop, the competitive landscape is essentially a three-player oligopoly. Express Scripts (Evernorth), CVS Caremark, and OptumRx (UnitedHealth Group) collectively manage pharmacy benefits for the vast majority of Americans. Each has pursued vertical integration, but through different architectures. UnitedHealth paired its insurer with Optum, a sprawling health services conglomerate that includes a PBM, physician practices, and data analytics. CVS paired its PBM with a retail pharmacy chain and an insurer (Aetna). Cigna paired its insurer with a standalone PBM and specialty pharmacy.

Applying Hamilton Helmer's framework, Cigna's position rests primarily on three of the Seven Powers. Switching costs create customer captivity. Scale economies create a cost advantage that compounds with volume. And the data feedback loop between insurance claims and pharmacy transactions creates a form of cornered resource: proprietary insight into drug value that cannot be easily replicated by competitors who lack the same vertical integration.

The Porter's Five Forces analysis reveals a mixed picture. Supplier power is moderate: drug manufacturers are large and sophisticated, but they need PBM distribution to reach patients, giving the Big Three PBMs countervailing bargaining power. Buyer power is increasing: large employers and health plans are demanding greater transparency and pushing for pass-through pricing models that compress PBM margins. The threat of new entrants is low in the core PBM business, given the scale and switching cost barriers, but non-traditional players like Amazon Pharmacy and Mark Cuban's Cost Plus Drugs are nibbling at the edges. The threat of substitutes is emerging through direct-to-consumer pharmacy models and government programs that bypass PBMs entirely. And competitive rivalry among the Big Three is intense but rational: all three have invested billions in vertical integration and have strong incentives to maintain pricing discipline.

For investors tracking Evernorth's competitive health, two metrics matter above all others. First, pharmacy script volume growth, which measures whether Evernorth is gaining or losing market share in its core PBM business. Consistent positive script growth signals that switching costs are holding and that the platform remains competitive on price and service. Second, the Evernorth segment adjusted income from operations margin, which captures the profitability of the services business after accounting for drug costs, dispensing expenses, and administrative overhead. This margin reflects the company's ability to extract value from its scale and data advantages. Together, these two metrics, volume and margin, tell you whether the flywheel is accelerating or decelerating.

VIII. Bear vs. Bull: The Future of the Toll Booth

The bear case for The Cigna Group centers on a single word: regulation. The pharmacy benefit management industry has operated for decades in a regime of remarkable opacity. PBMs negotiated rebates with drug manufacturers, retained a portion of those rebates as profit, and disclosed relatively little about the economics of the arrangement to their clients. This "black box" model was enormously profitable, but it attracted bipartisan political ire as drug prices became a top-of-mind issue for American voters.

The regulatory reckoning arrived in earnest in February 2026. An omnibus federal funding bill mandated sweeping changes to PBM economics in Medicare Part D: delinking PBM compensation from drug list prices, requiring flat-dollar fair-market-value fees for PBM services, imposing transparency requirements for group health plans, and requiring PBMs to pass through one hundred percent of rebates and other manufacturer payments to plan clients. The following day, the Federal Trade Commission announced a landmark consent order and settlement with Express Scripts specifically, requiring the company to stop preferring high-list-price drug versions over lower-cost alternatives on standard formularies, to offer plan sponsors a product where member out-of-pocket costs are based on net cost rather than list price, and to reshore its group purchasing organization, Ascent, from Switzerland to the United States.

These are not hypothetical risks. They are enacted law and binding regulatory orders. The question for investors is not whether PBM transparency will come, but whether the transition will compress Evernorth's margins permanently or whether Cigna can adapt its business model to thrive under the new rules.

The bear argument runs as follows: the traditional PBM spread model, buying drugs at one price and selling them at a higher price while retaining manufacturer rebates, is being legislated out of existence. As transparency requirements force PBMs to pass through rebates and charge explicit fees for their services, the economics become more visible and more competitive. Employers and health plans can shop for the lowest fee, commoditizing PBM services. The "toll booth" becomes a "utility," and utility-like businesses earn utility-like returns.

State-level reform is compounding the federal pressure. Iowa enacted sweeping PBM legislation in 2025 requiring one hundred percent rebate pass-through and pharmacy reimbursement based on actual acquisition cost. The Pharmacy Benefit Manager Transparency Act of 2025, introduced in Congress with bipartisan support, would extend similar requirements nationally. Each new law chips away at the opacity that historically protected PBM margins.

The bull case acknowledges the regulatory headwind but argues that it is manageable, and that the secular tailwinds are far more powerful. The strongest of these is the biosimilar wave. Over the past several years, some of the most expensive branded drugs in history have lost or are losing patent protection. Humira, the world's best-selling drug for nearly two decades, went off-patent in 2023. Stelara, another blockbuster biologic, followed. As biosimilar alternatives enter the market at significant discounts to the branded originals, PBMs are positioned to capture enormous value.

Here is why: when a PBM shifts a formulary from a branded biologic costing, say, $80,000 per year to a biosimilar costing $40,000, the PBM generates savings for the plan sponsor, captures a share of those savings as a fee, and often earns dispensing margin through its specialty pharmacy (in Cigna's case, Accredo). The Big Three PBMs have gone further, developing their own private-label biosimilars and placing them in preferred formulary positions. Express Scripts' formulary for 2025 and 2026 favors its own biosimilar products, effectively integrating manufacturing economics with distribution economics.

The bull case also rests on Cigna's deliberate de-risking of its business mix. By selling the Medicare Advantage business and concentrating on Evernorth, management has reduced exposure to the most volatile and politically sensitive segment of health insurance. The remaining Cigna Healthcare business is predominantly commercial, serving employers and individuals, where the company has more pricing flexibility and where medical cost trends are more manageable.

The management credibility factor also weighs on the bull side of the ledger. David Cordani, who announced in March 2026 that he will retire as CEO effective July 1, 2026, with President and COO Brian Evanko succeeding him, has delivered a remarkable track record. Over his tenure, the company has generated adjusted EPS growth averaging in the low double digits, well within the stated ten-to-thirteen percent target range. The share buyback program has been aggressive and well-timed: over $8.6 billion returned to shareholders in fiscal year 2024 alone, including a $3.2 billion accelerated share repurchase. The 2026 guidance calls for adjusted EPS of at least $30.25 and adjusted revenues of approximately $280 billion. Evernorth is expected to generate at least $6.9 billion in pre-tax adjusted income; Cigna Healthcare at least $4.5 billion.

The stock, trading at roughly $262 as of late March 2026, sits approximately twenty-five percent below its fifty-two-week high of $350, reflecting the managed care sector's broader selloff amid regulatory uncertainty and elevated medical utilization trends. The question is whether this discount represents a genuine impairment of the business model or a temporary sentiment dislocation in a stock that has historically rewarded patient holders.

The honest answer is that both the bear and bull cases have merit. The regulatory environment is genuinely more hostile than at any point in PBM history. But the structural advantages of scale, switching costs, and the biosimilar tailwind are equally genuine. The resolution will depend on management's ability to transition from an opaque spread-based model to a transparent fee-based model without destroying the economics that make the business attractive. It is, in essence, a test of whether the moat is built on opacity or on genuine operational superiority.

IX. Epilogue: The Outro

On a spring day in 1792, a group of Philadelphia merchants pooled their capital and created an insurance company to protect ships sailing across the Atlantic. Two hundred and thirty-four years later, the corporate descendant of that enterprise generates a quarter of a trillion dollars in annual revenue by managing the flow of pharmaceuticals through the most complex healthcare system on earth. The journey from fire insurance to pharmacy benefit management is not a straight line. It runs through two centuries of mergers, identity crises, regulatory battles, and strategic pivots that would strain any organization's institutional memory.

What makes The Cigna Group's story distinctive is not the longevity itself, plenty of American companies have survived for two centuries, but the willingness of its leadership to repeatedly abandon what the company was in pursuit of what it could become. The 1982 merger that created the Cigna name was an act of reinvention. The pivot away from property and casualty insurance in the 1990s was another. The decision to walk away from the Anthem merger, endure years of litigation, and emerge with the freedom to pursue Express Scripts was perhaps the most consequential act of strategic patience in recent healthcare history. And the creation of Evernorth, the deliberate repositioning of a health insurer as a health services platform, was the culmination of a transformation that David Cordani spent the better part of two decades engineering.

Can a non-founder-led, legacy corporation actually innovate? The conventional wisdom in Silicon Valley says no. Founders have vision; professional managers have spreadsheets. But Cordani's Cigna offers a counterexample. The Express Scripts acquisition was not a defensive move or a diversification play. It was a thesis-driven bet on a specific view of how healthcare economics would evolve, executed by a career insider who understood the industry's plumbing better than any founder parachuting in from the outside could have.

As Cordani prepares to hand the reins to Brian Evanko in mid-2026, the company he leaves behind is almost unrecognizable from the one he inherited. The insurance business that once defined Cigna now contributes a minority of revenue. The pharmacy and health services platform that barely existed when he became CEO now generates the vast majority of the company's economic value. The Medicare Advantage business, once considered a growth engine, has been sold off to sharpen the portfolio's focus.

The question going forward is whether the flywheel Cordani built, scale purchasing power feeding lower drug costs feeding more client wins feeding greater scale, can continue to accelerate under new leadership and in a more transparent regulatory environment. The architecture is in place. The data advantages are real. The switching costs are high. But the political winds are shifting, and the era of PBM opacity is ending.

What remains is the same question that faced those Philadelphia merchants in 1792: Can you build a durable institution by sitting at the center of a complex system of risk and commerce, adding value at every node, and earning a margin on the flow? For The Cigna Group, the answer to that question is worth roughly $70 billion. The market, as always, will render its verdict in real time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube