Chewy: The Obsessive Pet Parent's Digital Paradise

I. Introduction & Episode Thesis

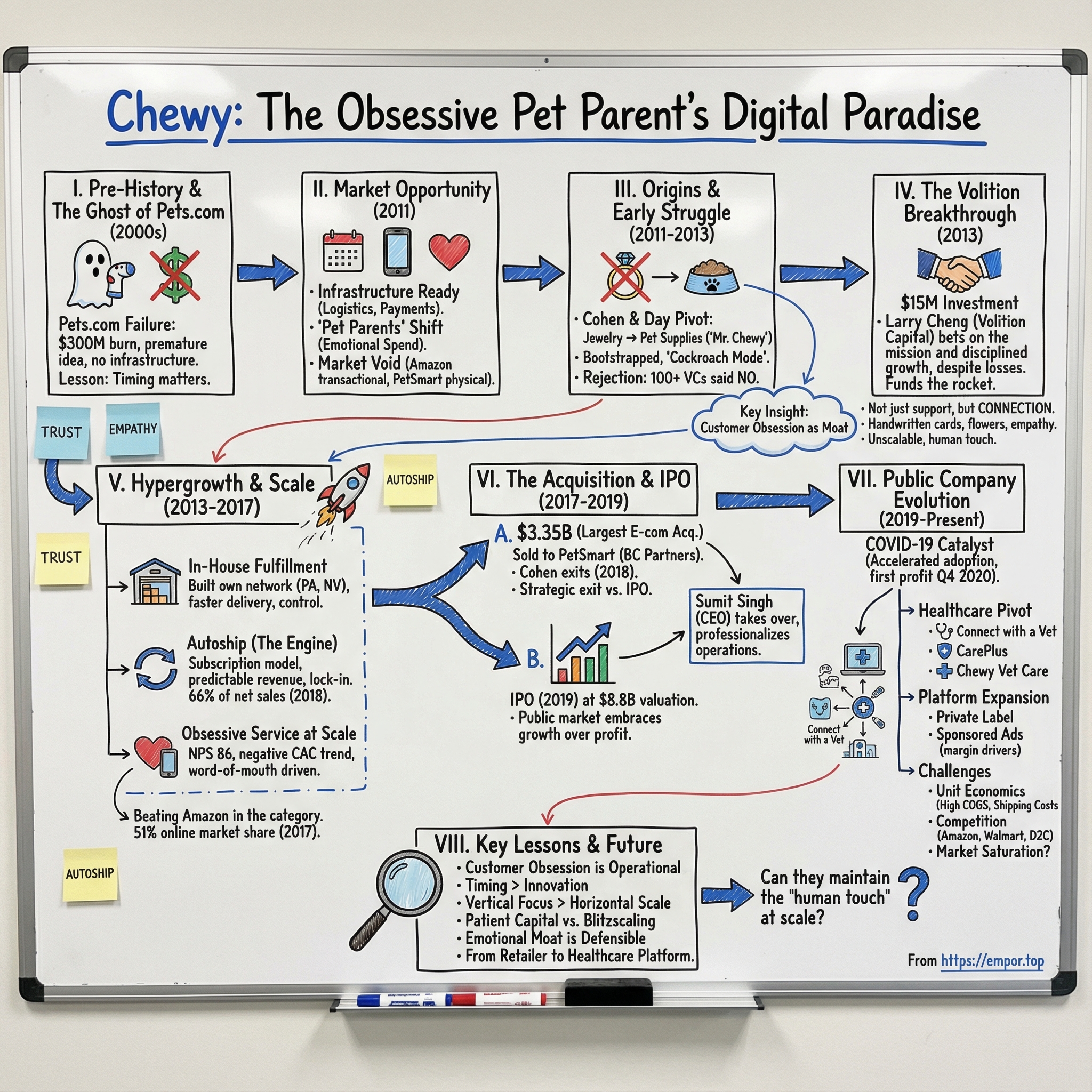

Picture this: It's 2017, and a 31-year-old entrepreneur is about to sell his online pet supply company for $3.35 billion—the largest e-commerce acquisition in history at that moment. Just six years earlier, Ryan Cohen was cold-calling venture capitalists from his Florida apartment, getting rejected by over 100 firms who couldn't see past the ghost of Pets.com's spectacular $300 million implosion. The sock puppet was dead, they said. Nobody would ever make money selling dog food online.

They were spectacularly wrong.

Today's story isn't just about how Chewy succeeded where Pets.com failed—it's about how two twenty-somethings discovered that the secret to e-commerce dominance wasn't technology or first-mover advantage, but something far more radical: actually caring about your customers' pets as much as they do. While Amazon treated pet supplies as just another SKU category and traditional retailers saw pets as a traffic driver to their stores, Cohen and his co-founder Michael Day built something different: a company that sent sympathy flowers when your dog died and hand-painted portraits of your cat for the holidays.

Three themes will guide us through this journey. First, we'll explore how customer obsession—real, operational, expensive customer obsession—can become a defensible moat even against Amazon. Second, we'll examine the stark contrast between the patient capital that built Chewy and the growth-at-all-costs mentality that destroyed Pets.com. And third, we'll unpack why in technology markets, being first often matters less than being ready.

The central question we're tackling today: How did Chewy not just survive but thrive in a market that had already produced one of the most notorious failures in internet history? The answer reveals fundamental truths about building enduring companies in the digital age—truths that challenge much of Silicon Valley's conventional wisdom about blitzscaling, network effects, and winner-take-all dynamics.

What makes this story particularly compelling for students of business strategy is that Chewy's playbook was hiding in plain sight. No proprietary technology. No revolutionary business model innovation. Just an obsessive focus on delighting customers in an industry where nobody expected to be delighted. In an era of algorithmic optimization and automation, Chewy proved that sometimes the most disruptive thing you can do is be genuinely, authentically, expensively human.

As we'll see, this approach didn't just win customers—it created fanatics. By 2018, Chewy customers were spending an average of $334 annually, with retention rates that made SaaS companies jealous. The company that venture capitalists wouldn't touch with a ten-foot pole had become the fastest-growing e-commerce company in history, hitting $2 billion in revenue faster than Amazon, Wayfair, or any other digital retailer before it.

But here's where the story gets really interesting: just as Chewy was proving that you could build a wildly successful, independent e-commerce company in Amazon's shadow, Cohen and Day made a decision that stunned the startup world. They sold. Not to Amazon, not through an IPO, but to PetSmart—a brick-and-mortar retailer that many viewed as a dinosaur waiting for the digital meteor to hit.

II. The Pre-History: Pets.com's Ghost & The Market Opportunity

The ghost of Pets.com haunts Silicon Valley like a cautionary tale told around venture capital campfires. In November 2000, after burning through roughly $300 million in less than two years, the poster child of dot-com excess shut its doors, taking its sock puppet mascot and 300 jobs with it. The company had spent more than $70 million on marketing and an average of $400 to acquire each new customer, a unit economics disaster that became shorthand for everything wrong with the internet bubble.

But here's what most people miss about Pets.com's failure: the idea wasn't wrong—just premature. As CEO Julie Wainwright pointed out in 2011, there "were no plug and play solutions for e-commerce/warehouse management and customer service that could scale" and worldwide Internet consumers numbered roughly 250 million versus over 5 billion today. The infrastructure simply didn't exist. Broadband penetration was minimal. Delivery times spanned 8 to 10 days, and waiting more than a week for pet supplies didn't excite people who could just buy it on their way home from work.

Fast forward to 2011. The pet industry had quietly become a colossus. By 2019, U.S. pet industry revenue would exceed $75 billion, with 85 million American households owning pets—nearly 70% of all homes. But more importantly, a fundamental shift had occurred in how Americans viewed their animals. Pets weren't just pets anymore; they were family members. This wasn't marketing speak—it was an emotional and financial reality that would drive spending patterns previously reserved for human children.

The infrastructure that doomed Pets.com had been completely transformed. Amazon had spent a decade building out logistics networks that made two-day delivery standard. Payment processing was seamless. Mobile commerce was emerging. Cloud computing had slashed the cost of scaling technology infrastructure by orders of magnitude. As one analysis noted, "The rise of e-commerce titans like Amazon and Chewy has shown that online retail can work at scale under the right conditions" with the infrastructure and logistics networks that "simply did not exist in the late 1990s".

Yet despite these favorable conditions, the online pet supply market remained curiously underpenetrated. Amazon treated it as just another category. Traditional retailers like PetSmart and Petco had built rudimentary e-commerce sites but fundamentally viewed digital as a threat to their real estate investments. The market was ripe for disruption, but everyone was still too scarred by the sock puppet's demise to see it.

Into this vacuum stepped two unlikely entrepreneurs who would prove that sometimes the best opportunities are hiding in plain sight, protected by the ghosts of failures past.

III. Origins: From Jewelry to Dog Food (2011)

The story begins not with dog food, but with jewelry—and a moment of clarity that would spawn a billion-dollar empire.

In 2011, Ryan Cohen was 25 years old, living in Florida, and about to launch an online jewelry business with Michael Day, a computer science student he'd met in a Java chatroom while searching for programmers to help with his affiliate marketing ventures. Cohen was working in affiliate marketing and met Day when trying to find a programmer for his website, with Day then a computer science student at the University of Georgia who dropped out of school to join Cohen in business.

Cohen wasn't your typical Silicon Valley wunderkind. Born to a Jewish family in Montreal, he never attended college, citing his father, who ran a glassware company, as his primary inspiration in pursuing an entrepreneurial route. He had been an entrepreneur since he was 13, when he began building websites for money, with his first client being his father, who ran a glassware importing business. By his teenage years, he'd discovered affiliate marketing, collecting fees for referring customers to e-commerce sites and making thousands of dollars monthly.

The jewelry pivot was almost comically last-minute. They went to a trade show and invested in a bunch of jewelry inventory, but as they were about to launch the business, Cohen happened to visit a local pet store to get food for his five-pound poodle, Tylee, and as he was checking out, an epiphany hit him: Why didn't they sell pet supplies instead? The realization was profound: he didn't care about jewelry, but he cared deeply about his dog and what he fed her—just like millions of other pet parents.

They saw that pet supplies were a bigger and better opportunity than jewelry, and were fortunate the vendors who sold them the jewelry agreed to buy it back. The speed of the pivot was breathtaking—within weeks, they'd returned their jewelry inventory and completely redirected their business plan toward pet supplies.

Chewy was founded with the name "Mr. Chewy" in June 2011 by Ryan Cohen and Michael Day. The initial setup was scrappy in the extreme. They hired a third-party logistics firm in Pennsylvania to help them ship products for their new business—which they originally called Mr. Chewy and then became Chewy.com. Cohen and Day threw in their own money, hired Cohen's childhood friend Alan Attal, and the three of them did everything at the company in the early days—from packing boxes to answering customer service calls.

This bootstrap mentality stood in stark contrast to the Pets.com era. They bootstrapped Chewy and it took a couple years before they were able to raise capital, doing everything with no credentials—Cohen never went to college, had no background in retail, didn't have a network or a rich uncle he could ask for a loan. Every dollar mattered. Every customer interaction was personal. There was no sock puppet mascot or Super Bowl commercial—just three guys in Florida obsessed with making pet parents happy.

In March 2012, the company estimated a total yearly revenue of $26 million, despite losing money in its first half year. But unlike their dot-com predecessors who saw losses as badges of honor, Cohen and Day were methodically building something sustainable. They weren't trying to "get big fast"—they were trying to get good first.

The contrast with traditional retail thinking was immediate. While PetSmart and Petco saw online as a threat to their real estate empires, and Amazon treated pet supplies as just another category to dominate through price and speed, Cohen saw an emotional opportunity hiding in plain sight. Pet parents didn't just need stuff delivered; they wanted to feel understood, supported, and celebrated in their obsessive love for their animals. This insight—that pet commerce was actually about relationships, not transactions—would become the foundation of everything Chewy built next.

IV. The Early Struggle & Customer Service Innovation (2011-2013)

By March 2012, reality had set in hard. The company estimated a total yearly revenue of $26 million, despite losing money in its first half year. Cohen, Day, and their childhood friend Alan Attal were doing everything themselves—packing boxes, answering customer emails until 3 AM, managing inventory from a cramped Florida office. The burn rate was terrifying. Every dollar spent on marketing or inventory was a dollar they might never see again.

But it was during these desperate early days that Chewy's radical approach to customer service began to take shape. The inspiration wasn't some MBA case study or Silicon Valley growth hack—it was pure necessity married to genuine empathy. When you're a nobody competing against Amazon, you can't win on price, selection, or speed. You have to win on something Amazon would never do: actually giving a damn.

The customer service innovations that would become Chewy's signature started organically. Cohen used Amazon's guidelines for supply chain, logistics and the convenience of shopping online but added a focus on customer service, including hand-written holiday cards, pet portraits, and flowers for deceased pets. These weren't marketing gimmicks dreamed up in a boardroom—they were authentic expressions of how the founders themselves wanted to be treated.

Our Chewy Gives Back Program was founded in 2012, establishing a commitment to animal welfare that went beyond profit margins. When customers received the wrong order or had unopened food after a pet passed away, Chewy would issue full refunds and tell customers to donate the products to local shelters rather than return them. This policy cost money in the short term but built something priceless: trust.

The handwritten notes started because Cohen and Day were literally answering every customer email themselves. They'd add personal touches—asking about pets by name, remembering previous conversations, treating each interaction like they were helping a neighbor, not processing a transaction. As the company grew and hired customer service representatives, this personal approach became institutionalized. Every new hire spent their first weeks learning not just systems and processes, but the art of genuine connection.

Meanwhile, the fundraising situation was becoming desperate. Cohen says he originally approached over 100 venture capital firms and was rejected by all of them. In 2013, Cohen secured the company's first outside investment from Volition Capital for $15 million. The rejection parade was brutal and specific. There were two headaches most investor could not get past: first, how he is competing head-on with Amazon; and second, the pets.com failure. Yet to his vision, there is a way out, being focused on the pet category along with high-touch customer service would give Chewy its unique competitive advantage.

Silicon Valley venture capitalists would literally laugh Cohen out of the room. One told him that competing with Amazon in commodity products was "suicide with extra steps." Another said the only thing worse than Pets.com was "Pets.com with feelings." The meetings became increasingly humiliating. Cohen would fly to Sand Hill Road on red-eyes, sleeping in airport terminals to save money on hotels, only to be dismissed after five minutes by associates who hadn't even bothered to read his deck.

To Cohen, every no sounded like they just have not understood his vision. Despite how frustrating it was, it could not discourage him. Those no never made him doubt his strategy, rather the opposite. He was motivated by all the rejections and fired up to prove his point.

But beneath the bravado, the company was running on fumes. By late 2012, they had weeks of runway left. Cohen had maxed out credit cards. Day was living on ramen. They'd invested everything—financially and emotionally—into a company that the entire venture capital ecosystem had deemed uninvestable. The responsible thing would have been to shut down, get real jobs, admit that the experts were right.

Instead, they doubled down on the only thing that was working: their customers loved them. Not liked—loved. It's also worth noting that it's been Chewy's policy from its earliest days, as co-founder and former CEO Ryan Cohen explained to Inc. when Chewy went public in 2019. Retention rates were astronomical for e-commerce. Word-of-mouth referrals were driving more growth than paid marketing. People were posting about Chewy on social media not because of a campaign, but because they were genuinely moved by the experience.

The flowers-for-deceased-pets policy emerged during this period, though "Its origins may be folklore at this point" according to Andrew Stein, Chewy's senior director of customer service. What's certain is that it reflected a profound understanding of the pet-parent relationship that no algorithm could capture. When your dog dies, you don't need efficient transaction processing—you need someone to acknowledge that you've lost a family member.

This obsessive focus on emotional connection over operational efficiency would have made Jeff Bezos's head explode. It violated every principle of scalable e-commerce. You couldn't automate empathy. You couldn't optimize genuine care. Every handwritten note, every custom pet portrait, every sympathy bouquet was a tiny rebellion against the dehumanization of digital commerce.

By early 2013, with the company somehow still alive but barely breathing, one more shot at funding presented itself—a venture capitalist named Larry Cheng who was willing to stop by their office on his way to Disney World.

V. The Volition Capital Breakthrough (2013)

The meeting that would change everything almost didn't happen.

Larry Cheng at Volition Capital was one of the people Cohen pitched the company to. They first met him in 2012; he was en route to Disney World with his family and agreed to make a quick stop at their office. Cohen remembers the moment vividly: Cheng asked him, "Who's going to take this company to $100 million in sales?" Cohen was 26 and probably looked even younger, but he confidently answered, "I am."

Cheng didn't invest.

It wasn't even close. The meeting lasted less than an hour. Cheng was polite but skeptical—another VC seeing another kid trying to sell pet food online. The Chewy team watched him drive away toward Disney World, their hopes deflating like a punctured balloon. Cohen later admitted he went home that night and questioned everything. Maybe the hundred rejections weren't wrong. Maybe he was the one who couldn't see reality.

But something interesting happened over the next six months. He followed up with us about six months later, though. We'd beaten the sales projections that we'd previously given him, and he was impressed. This wasn't typical VC behavior. Most investors who pass never look back—there are always new deals, new pitches, new founders to evaluate. But Cheng had kept watching.

What Cheng saw was remarkable: not just growth, but disciplined growth. We'd given them our projections and we were crushing our numbers. More importantly, the customer metrics were unlike anything he'd seen in e-commerce. Retention rates that looked like SaaS companies. Word-of-mouth growth that required minimal marketing spend. And those bizarre operational decisions—the handwritten cards, the flowers, the portraits—were actually working.

The second meeting was different. This time, Cheng came alone, without the distraction of a family vacation. He spent hours digging into the numbers, the operations, the vision. Larry said, "What was truly special about Chewy was Ryan's commitment to delighting customers. He wanted to build the most customer-centered Company on the planet. All of the decisions about the Company – from fulfillment, to pricing, to working capital management, to merchandising, to customer service – were made with one goal in mind – delight the customer. And, it was that commitment to the customer which ultimately became the key reason they succeeded."

A few days later he signed off on a $15 million investment in Chewy. But the significance went far beyond the money. The satisfaction of that victory was even greater than the pride I felt following the eventual multibillion-dollar sale. After two years of building Chewy—and more than 100 conversations with VCs that went nowhere—I'd finally found someone who believed in me and our business model.

Cohen's reaction to finally getting funded reveals something profound about the entrepreneurial psyche. This wasn't celebration—it was responsibility. From that point on, the mission was larger. I was even more committed to making Chewy an industry leader because it was no longer just our own money on the line. Larry had gone out on a limb for us. I felt that responsibility.

The Volition investment marked a fundamental shift in Chewy's trajectory. For two years, they'd been operating in what Cohen called "cockroach mode"—impossible to kill but barely growing. Now they had runway, credibility, and something even more valuable: a true partner who understood that sometimes the best investments are in founders who don't check all the traditional boxes.

Cheng would later reflect on what made him change his mind: "I look for companies with home-run potential led by grounded and humble leaders. At Volition, we love companies that have paired an authentic mission, with passionate customers, and tremendous growth. These are hard combinations to find – so I am willing to take a risk to get it. I'll back founders who don't check all of the boxes for other investors."

The $15 million would transform everything. Within months, Chewy would open their first warehouse, hire their first hundred employees, and begin the hypergrowth phase that would shock the retail world. But Cohen never forgot the lesson of those hundred rejections and that one yes: in venture capital, as in customer service, you don't need everyone to love you. You just need the right ones to believe.

The relationship between Cheng and Cohen would endure far beyond Chewy. Larry and Ryan are still fast friends to this day. Years later, when Cohen would take on his next challenge at GameStop, Cheng would join him on the board—a testament to the bonds forged when someone believes in you when no one else will.

VI. Hypergrowth & The Race to Scale (2013-2017)

The $15 million from Volition was like rocket fuel to a company that had been running on fumes. Within months, everything changed.

The first major decision was also the riskiest. We hit an inflection point where three [third-party logistics companies] we were working with [were getting overwhelmed]. We'd give them weekly or monthly projections so they could plan ahead and have warehouse space, but they didn't fully believe our growth and by the end of 2013, we had these 3PLs that couldn't scale any more, so we had to bring fulfillment in-house.

Cohen's decision to build their own fulfillment infrastructure was borderline insane. We didn't know anything about this, so we hired a bunch of people who were experts in fulfillment and we flew to Mechanicsburg, Pa. to lease a 400,000-square-foot space, and within nine months or so, we became expert at doing fulfillment. Consultants told them it would take 18 months. They did it in less than six.

By mid-2014 they opened a 600,000-square-foot fulfillment center in Mechanicsburg, Pennsylvania, which opened in 2014. The facility was massive—multiple football fields of conveyor belts, sorting systems, and inventory management technology. It was risky. It was totally outside of our areas of competence. But by August of 2014, after breaking everything first, that center was humming along, and then we launched another in Reno.

But the real innovation wasn't the warehouses—it was Autoship, their subscription program that would revolutionize pet retail. Launched in earnest in 2014, Autoship was deceptively simple: customers could schedule automatic deliveries of pet supplies, ensuring they never ran out of essentials. After your first Autoship discount, you'll save an extra 5% on select brands for all future Autoship orders, with that initial order offering up to 35% off.

The genius of Autoship wasn't the discount—it was the psychology. Pet parents are creatures of habit. Their dogs eat the same food, their cats use the same litter, their rabbits need the same hay. By automating these purchases, Chewy removed friction from the buying process while creating predictable, recurring revenue. Autoship customer sales grew from $115 million in fiscal year 2014 to $2.3 billion in fiscal year 2018—a 20x increase in just four years.

This subscription model solved multiple problems simultaneously. For customers, it meant never running out of food at 10 PM with a hungry dog staring at them. For Chewy, it meant predictable demand that could optimize inventory and logistics. And for investors, it meant the holy grail of e-commerce: customer lock-in without the traditional switching costs of software subscriptions.

The growth numbers during this period were staggering. By 2016, raised capital from BlackRock and T. Rowe Price. That year the company had $900 million in sales and had become the number 1 online pet retailer. The company was adding customers at a rate that defied gravity—from thousands to millions in what felt like months.

By 2017, approximately $2 billion in revenue and 51% of online pet food sales in the US. To put this in perspective: Chewy had captured more than half of the entire online pet food market in just six years. Amazon, with all its resources and logistics advantages, was getting beaten by a company that sent handwritten cards and flowers.

The infrastructure build-out was relentless. Pennsylvania has seen the greatest amount of development with five fulfillment centers since 2014, three which are in Northeast Pennsylvania metropolitan area of Scranton/Wilkes-Barre. Each new facility represented not just capacity but capability—the ability to reach more customers faster, to carry more SKUs, to provide next-day delivery to larger swaths of the country.

But beneath the operational excellence was something more fundamental: Chewy had cracked the code on emotional commerce. While Amazon optimized for efficiency and Walmart competed on price, Chewy optimized for love. Every operational decision—from warehouse locations to inventory management to delivery speed—was filtered through a simple question: will this delight our customers?

The results spoke for themselves. Customer acquisition costs that had started at hundreds of dollars dropped to double digits as word-of-mouth became their primary growth driver. Lifetime values soared as Autoship locked in multi-year relationships. And Net Promoter Scores reached levels—86 in fiscal year 2018—that most retailers could only dream of.

By early 2017, Chewy faced a crossroads that every hypergrowth company eventually encounters: go public or sell. The IPO market was hot. The business was scaling beautifully. They could have easily raised hundreds of millions in public markets and remained independent. But two suitors had other plans, and their offers would force Cohen to make the defining decision of his career.

VII. The PetSmart Acquisition: Strategic Exit or Sellout? (2017)

The acquisition talks began like a chess match between three grandmasters, each with radically different endgames in mind.

By 2017, the company had revenue of approximately $2 billion and 51% of online pet food sales in the US. At that time, CEO Ryan Cohen prepared to take Chewy public as both Petco and PetSmart approached with merger offers. Petco's offer would be paid for in part using stock, whereas PetSmart offered an all-cash bid that would also allow Chewy to remain a completely separate business.

The decision matrix was complex. Petco's stock-heavy offer meant Cohen and his investors would be betting on the future of traditional retail—a questionable wager in the Amazon age. PetSmart's all-cash offer, backed by private equity firm BC Partners, was cleaner but came with its own complications. Going public remained the third option, promising independence but requiring Cohen to run a public company indefinitely.

PetSmart has made the biggest e-commerce acquisition in history, snatching up fast-growing pet food and product site Chewy.com for $3.35 billion, according to multiple sources familiar with the deal. The deal is a huge one by any standard — bigger than Walmart's $3.3 billion deal for Jet.com last year — and especially for a retail company like PetSmart that was itself valued at only $8.7 billion when private-equity investors took it over in 2015.

The price tag was staggering. At $3.35 billion, it was the largest e-commerce acquisition in history, surpassing even Walmart's purchase of Jet.com. For context, PetSmart itself had been valued at just $8.7 billion when BC Partners took it private two years earlier. They were essentially betting a third of their entire company's value on an online retailer that had existed for just six years.

No announcement on the financial breakdown, but I hear that the deal includes around $2 billion in cash from the private equity firms, while the remainder is stock and/or retention packages. [Update: Another source says that Volition just sent out letters to limited partners, saying the full purchase price will be paid in cash at closing.

For Cohen, the decision ultimately came down to certainty versus potential. An IPO might have yielded a higher valuation eventually, but it would have meant years more of grinding, of quarterly earnings calls, of managing Wall Street expectations. The PetSmart offer was bird-in-hand—immediate liquidity for investors who'd believed when no one else would, financial security for employees who'd sacrificed for the dream, and freedom for Cohen himself to step back.

Since we started Chewy, we have been dedicated to understanding and satisfying the evolving needs of our customers to deliver the highest quality pet products and customer service," said Ryan Cohen, co-founder and CEO of Chewy. His public statement was diplomatic, but privately, the decision was more nuanced.

The strategic rationale from PetSmart's perspective was obvious. PetSmart's strategy: The legacy retailer and Petco are dominant in the pet supplies market, but are dwarfed by Chewy when it comes to e-commerce. And since e-commerce is where pet food sales are heading ― no matter the bricks-and-mortar perks of on-site vet and grooming services ― this is a logical play. They were buying their future, essentially admitting that their thousands of stores and decades of brand equity couldn't compete with six years of customer obsession.

But the culture clash concerns were real. But all signs were that this company could go public (perhaps after one more big, pre-IPO round), and now it's tied its horses to a physical retailer owned by a private equity firm known for... Culture, meet shock. Chewy's freewheeling, customer-first culture would now report to private equity operators focused on EBITDA multiples and debt service coverage ratios.

Cohen's departure came surprisingly quickly. The company's founder and first CEO, Ryan Cohen stepped down in March 2018, and Sumit Singh was named the company's CEO in March 2018 after working as its COO since 2017 and previously as an executive at Dell and Amazon. Just eleven months after the acquisition closed, Cohen walked away from the company he'd built from nothing.

His reasoning was personal but revealing. He'd achieved what he set out to do—prove that you could build a massive, customer-obsessed commerce company in Amazon's shadow. The money was life-changing not just for him but for every early employee and investor. And at 31, he had other mountains to climb.

The transition to Sumit Singh was smooth, a testament to the operational excellence Cohen had instilled. Singh, with his Amazon and Dell pedigree, represented a different kind of leadership—less founder-visionary, more professional operator. It was exactly what Chewy needed for its next phase.

Looking back, the acquisition was both triumph and tragedy. Triumph because it validated everything Cohen had believed about the power of customer obsession, returning 100x+ for early investors and creating thousands of jobs. Tragedy because it marked the end of Chewy as an independent force, a company that might have become the Zappos or Netflix of pet retail—a category-defining public company that rewrote the rules.

The deal will formally split PetSmart's operations from that of Chewy, the online pet supplies retailer it acquired for $3.35 billion in 2017 and took public two years later in a lucrative listing. PetSmart's ownership stake in Chewy will transfer to BC Partners, which acquired PetSmart for some $8.7 billion in 2015. The ultimate irony? Just three years later, BC Partners would split the companies apart again, taking Chewy public in what would become one of the most successful IPOs of 2019.

But in April 2017, none of that was visible. There was just a young entrepreneur standing in a conference room, signing papers that would make him and his co-founder extraordinarily wealthy, wondering if he'd just made the best or worst decision of his life. As Cohen would later reflect, sometimes the hardest decisions aren't about choosing between good and bad, but between good and potentially great.

VIII. The IPO & Public Company Evolution (2019-Present)

The split was remarkable for its timing. Chewy's IPO in June 2019 raised just over $1 billion at an $8.8 billion valuation, nearly tripling the acquisition price in just two years. The company sold 46.5 million shares at $22 per share, well above the expected range, in what became a watershed moment for unprofitable tech companies going public.

The public markets embraced Chewy despite its losses. The company reported $3.5 billion in sales for fiscal 2018, up 68% from 2017, but with a net loss of $268 million. The high costs required to ship heavy pet food had been a drag on the company's results, yet investors saw beyond the red ink to the underlying customer economics.

What made Chewy's IPO particularly notable was its ownership structure. Following the initial public offering, PetSmart retained roughly 70% of the company's common stock and held approximately 77% voting power. This unusual arrangement—a public company majority-owned by a private equity-backed retailer—would create both opportunities and complications in the years ahead.

Sumit Singh's leadership as CEO proved transformative. Singh led the company through its IPO; Chewy grew to a market capitalization of $40 billion, a stunning appreciation that validated the strategic vision even as operational challenges persisted. The unit economics remained brutal: COGS at 77% of revenue, fulfillment costs of 9.3%, and merchant processing of 2.1% left little room for profit margins.

Then COVID-19 changed everything.

The pandemic became an unexpected catalyst for Chewy's business model. The company saw increased demand from millions of existing and new customers as the business sustained growth throughout the economic disruption of the COVID-19 era. Pet adoption rates soared as locked-down Americans sought companionship. Suddenly, the convenience of home delivery wasn't just nice to have—it was essential.

In March 2021, Chewy reported revenue of $2.04 billion for Q4 of 2020, making it Chewy's first quarter of net profitability. The milestone was both symbolic and substantive. After years of losses, the company had finally proven it could generate positive earnings while maintaining growth. The company reported 19.2 million active customers, adding 5.7 million new customers in 2020, an increase of 42.7% from the year prior.

CEO Sumit Singh captured the moment's significance: "Overall, we see 2020 and the impact of COVID as much more than just a one-time growth accelerator. We see it as a catalyst that sped up the secular shift towards e-commerce that was already underway". The pandemic hadn't created new demand—it had compressed years of behavioral change into months.

The healthcare expansion strategy that followed represented Chewy's most ambitious pivot since its founding. Chewy launched a free tele-triage service called Connect With a Vet in October 2020, allowing pet parents to chat with licensed veterinarians 24/7. This wasn't just about adding services—it was about becoming the primary healthcare interface for pet parents.

In August 2022, Chewy launched CarePlus, an exclusive suite of pet-first wellness and insurance plans that were initially available in 31 states and expanded nationwide by late 2022. The program represented a direct assault on the traditionally fragmented pet insurance market. The wellness plans started at $20 a month and covered preventative care, while insurance plans started at $20, $60 or $100 a month.

The strategic logic was compelling. While less than 5 percent of pets are insured in the United States today, one in three pets require emergency veterinary care every year. Chewy wasn't just selling insurance—it was building an integrated healthcare ecosystem that connected telehealth, pharmacy, insurance, and eventually, physical care.

The boldest move came in December 2023. Chewy announced the launch of its pet health practices under the brand name "Chewy Vet Care," with the first practice opening in South Florida early in 2024 and additional locations launching throughout the year, offering services including routine appointments, urgent care and surgery. This wasn't just channel expansion—it was a fundamental reimagining of Chewy's role in the pet ecosystem.

The veterinary clinics represented both opportunity and risk. The company acknowledged that "We compete directly and indirectly with veterinarians for the sale of pet medications and other health products. Veterinarians hold a competitive advantage because many pet owners may find it more convenient or preferable to purchase prescription medications directly from their veterinarians". By opening its own clinics, Chewy was simultaneously competing with and becoming its own supplier.

By fiscal 2024, the transformation was evident in the numbers. Chewy reported net sales of $11.86 billion, which reflects a 6.4% year-over-year growth. The company's gross margin improved to 29.2%, up from 28.4% in 2023, driven in part by growth in sponsored advertisements that reached approximately 1% of net sales. The company had evolved from pure e-commerce to a diversified pet health platform.

IX. Competitive Dynamics & Market Position

Amazon should have crushed Chewy. By every traditional metric of e-commerce warfare—capital, logistics infrastructure, customer base, brand recognition—the Everything Store held overwhelming advantages. Yet somehow, a company selling dog food from Florida warehouses had carved out a defensible position against the most feared competitor in retail history.

The key to understanding this David-and-Goliath dynamic lies in a simple truth: Amazon optimizes for transactions, Chewy optimizes for relationships. When your dog dies, Amazon's algorithm might recommend a new collar based on your purchase history. Chewy sends flowers and a condolence card. That difference—small in operational terms, massive in emotional impact—created a moat that even Bezos couldn't cross.

Amazon's approach to pet supplies reflected its approach to everything: maximum selection, competitive prices, fast delivery. The company launched Amazon Pets as a dedicated vertical, offered Subscribe & Save for recurring purchases, and leveraged its Prime membership base to lock in customers. On paper, it should have been game over. Pet supplies were just another category to dominate through operational excellence and scale advantages.

But pet parents aren't buying widgets. They're caring for family members. And in that emotional context, Amazon's algorithmic efficiency felt cold, transactional, insufficient. While Amazon could match Chewy on price and beat them on delivery speed to Prime members, they couldn't—or wouldn't—match the human touch that turned customers into evangelists.

The traditional retailers faced a different but equally intractable problem. PetSmart and Petco had spent decades building thousands of stores, training grooming staff, hosting adoption events, creating community touchpoints. Their real estate was both their greatest asset and their largest liability. Every dollar invested in e-commerce potentially cannibalized a store visit. Every online sale threatened the economic model that justified their leases.

PetSmart's acquisition of Chewy was essentially an admission of defeat—they couldn't build a competitive digital business internally, so they bought one. But even ownership couldn't resolve the fundamental tension. How do you run physical stores and digital pure-play simultaneously without undermining one or both? The eventual split of the companies proved that some business models simply can't coexist under one roof.

Walmart's entry into online pet supplies added another dimension to the competitive landscape. With its acquisition of Jet.com and massive investments in e-commerce infrastructure, Walmart had both the scale and the determination to compete. They could leverage their store network for pickup, their buying power for pricing, their logistics for delivery. Yet they too struggled to capture the emotional premium that Chewy commanded.

The real genius of Chewy's competitive position was the Autoship program. By 2018, subscription customers drove approximately 66% of net sales. This wasn't just convenient recurring revenue—it was a fundamentally different customer relationship. When pet parents put their pet food on Autoship, they weren't just buying product; they were delegating responsibility for their pet's nutrition to Chewy. That trust, once earned, proved remarkably sticky.

The numbers told the story. Despite Amazon's massive reach, Chewy had captured 51% of online pet food sales by 2017. Customer acquisition costs that started in the hundreds of dollars dropped to sustainable levels as word-of-mouth became the primary growth driver. Net Promoter Scores reached levels that most retailers—online or offline—could only dream of achieving.

The competitive dynamics also revealed a surprising truth about network effects in e-commerce. While traditional thinking suggested that marketplace models like Amazon would dominate through network effects, Chewy proved that vertical focus could create its own network dynamics. Every happy customer became a node in an informal network of pet parent recommendations. Every veterinarian who prescribed through Chewy's pharmacy became part of the ecosystem. Every piece of user-generated content—photos of pets with Chewy boxes, social media posts about handwritten cards—reinforced the community effect.

New threats continued to emerge. Startups like BarkBox targeted specific niches with subscription boxes. Direct-to-consumer brands like Farmer's Dog promised fresher, more customized nutrition. Amazon continued to invest in private label pet products. Yet Chewy's position remained remarkably resilient, protected not by technology or capital but by millions of emotional connections with pet parents who saw the company as a partner in their pet's life, not just a retailer.

The most telling competitive indicator came from customer behavior during the pandemic. When supply chains strained and delivery slots became scarce, pet parents didn't switch to whoever could deliver fastest. They waited for Chewy. They stockpiled from Chewy. They remained loyal even when alternatives were available, because Chewy had earned something more valuable than their business—they'd earned their trust.

This trust translated into pricing power that defied e-commerce orthodoxy. While Amazon and Walmart competed on price, Chewy customers willingly paid small premiums for the same products. They valued the relationship, the service, the peace of mind more than saving a few dollars. In a world where price comparison was one click away, Chewy had somehow made price secondary to experience.

X. Business Model & Unit Economics Deep Dive

The math of selling 40-pound bags of dog food online shouldn't work. The unit economics are punishing: heavy products, low margins, expensive shipping, price-transparent market. Yet Chewy found a way to turn this mathematical disadvantage into a $40 billion market capitalization. Understanding how requires dissecting one of the most counterintuitive business models in e-commerce history.

Let's start with the brutal reality of the cost structure. With COGS at 77% of revenue in 2019, Chewy was already starting from a disadvantaged position compared to typical e-commerce players. Add fulfillment costs of 9.3% and merchant processing fees of 2.1%, and you're left with less than 12% to cover all other operating expenses and hopefully generate profit. For context, most successful e-commerce companies operate with gross margins above 30%.

The shipping challenge was particularly acute. A 40-pound bag of dog food might retail for $50, but shipping it via ground service could cost $15-20. Even with negotiated carrier rates and zone skipping strategies, the physics of moving heavy goods across the country created structural disadvantages. Unlike Amazon, which could offset pet food shipping losses with high-margin electronics, every Chewy order had to stand on its own economics.

The breakthrough insight was that customer lifetime value, not transaction profit, was the relevant metric. The average Chewy customer spent $334 annually by 2018, but that understated the true value of loyal customers. Autoship subscribers—who represented the majority of sales—spent significantly more and stayed significantly longer. When a customer put their pet's nutrition on autopilot, they weren't just committing to purchases; they were essentially making Chewy their pet's primary supplier for years.

The Autoship program transformed the unit economics in three critical ways. First, it made demand predictable, allowing for inventory and logistics optimization that reduced costs. Second, it dramatically reduced customer acquisition cost amortization—spending $100 to acquire a customer made sense if they stayed for five years, not so much if they made one purchase. Third, it enabled bulk shipping and delivery route optimization that improved fulfillment economics.

Customer acquisition costs followed an unusual trajectory. In the early days, CAC exceeded $400 per customer—unsustainable by any measure. But as word-of-mouth grew and brand recognition increased, CAC dropped precipitously. By 2018, the combination of organic traffic, referrals, and efficient digital marketing had brought acquisition costs down to levels that made the lifetime value equation work.

The path to profitability required multiple levers. Improving gross margins became an obsession. This meant negotiating better terms with suppliers, introducing private label products with higher margins, and optimizing product mix toward more profitable categories. Every basis point mattered when operating on such thin margins. The introduction of sponsored product advertisements on the site, reaching approximately 1% of net sales by 2024, added nearly pure-margin revenue to the model.

The private label opportunity was particularly compelling. By introducing Chewy-branded products across categories—from basic supplies to premium nutrition—the company could capture additional margin while strengthening customer loyalty. Private label products typically carry 10-15% higher margins than national brands, and in Chewy's case, customers actively preferred them because they trusted the Chewy brand more than many traditional pet brands.

The subscription model created fascinating financial dynamics. While traditional retailers faced working capital challenges—paying suppliers before collecting from customers—Chewy's Autoship program inverted this relationship. Customers effectively pre-committed to purchases, providing negative working capital benefits that improved cash flow even during periods of rapid growth.

The fulfillment network investments that seemed risky in 2014 proved prescient by 2020. Owning distribution centers allowed Chewy to control the customer experience end-to-end while capturing logistics margins that would have gone to third parties. The ability to ship from multiple locations reduced zone charges and delivery times, improving both economics and customer satisfaction.

Healthcare services added an entirely new dimension to the unit economics. Connect With a Vet, pharmacy services, and insurance products carried fundamentally different margin profiles than physical goods. A telehealth consultation had near-zero marginal cost. Pharmacy prescriptions carried higher margins than food. Insurance commissions provided recurring revenue without inventory or fulfillment costs. These services didn't just diversify revenue—they improved the overall margin structure of the business.

The competitive moat created by these economics was subtle but powerful. A new entrant would need to simultaneously solve multiple challenges: achieve sufficient scale for shipping economics, build trust for subscription adoption, invest in fulfillment infrastructure, and survive years of losses while building customer density. The capital requirements alone were daunting, but the execution complexity was even more challenging.

By 2024, the model had evolved from "selling dog food online" to something far more sophisticated: a subscription-driven, vertically-integrated, multi-service platform with improving unit economics and expanding margins. The company that shouldn't have worked on paper had engineered a business model that not only worked but thrived, proving that sometimes the best businesses are built by solving the hardest problems.

XI. Playbook: Lessons for Founders & Investors

Lesson 1: Customer obsession isn't just marketing—it's operations

The easiest mistake to make when studying Chewy is thinking their customer service was a marketing strategy. Send some flowers, write some cards, build brand loyalty—simple, right? Wrong. Chewy's customer obsession was operational, embedded in every system, process, and decision. When they built warehouses, they located them to minimize delivery time to customers, not to minimize real estate costs. When they designed their website, they optimized for finding the right product for your specific pet, not for maximum conversion. When they hired customer service reps, they trained them to solve problems, not to minimize call time.

This operational commitment to customer experience is what competitors couldn't copy. Amazon could have sent flowers too—it would have been a trivial technical challenge. But Amazon's entire operating system was built on efficiency, automation, and scale. Adding genuine human connection would have required rebuilding their cultural DNA, not just adding a line item to their customer service budget.

Lesson 2: Sometimes the best ideas are obvious (but hard to execute)

Cohen didn't invent some revolutionary business model. Selling pet supplies online? Pets.com tried that. Subscription commerce? Amazon had Subscribe & Save. Good customer service? Zappos wrote that playbook. Chewy's innovation was taking obvious ideas and executing them with a level of commitment that seemed irrational to everyone else.

The lesson for founders: stop looking for the clever hack, the unique insight, the thing nobody else has thought of. Sometimes the best opportunity is the obvious one that everyone else thinks is too hard, too expensive, or too boring. The barrier to entry isn't intellectual property or network effects—it's the willingness to do the hard, grinding work that others won't.

Lesson 3: Patient capital vs. blitzscaling—know which game you're playing

Chewy raised just $236 million before its $3.35 billion exit. For comparison, Pets.com burned through $300 million in two years. This wasn't accidental—Cohen deliberately chose patient capital over growth capital. Volition Capital understood they were funding a marathon, not a sprint. The business needed time to build trust, optimize operations, and achieve density economics.

This runs counter to the blitzscaling orthodoxy that dominates Silicon Valley, where the prescription is to raise massive capital, grow at all costs, and worry about unit economics later. That works for winner-take-all markets with strong network effects. But pet supplies isn't winner-take-all. Customer relationships are built slowly. Trust compounds over time. Trying to blitzscale Chewy would have created exactly what killed Pets.com: unsustainable burn rates without the customer loyalty to support them.

Lesson 4: Timing beats innovation

Pets.com wasn't wrong about the opportunity—they were just early. In 2000, broadband penetration was under 5%. Shipping infrastructure was primitive. E-commerce was scary to most consumers. Payment processing was clunky. By 2011, all these infrastructure problems had been solved. Cohen didn't need to innovate on technology; he just needed to execute on an opportunity that was finally ready.

For founders, this means spending less time trying to predict the future and more time understanding the present. What infrastructure exists today that didn't exist five years ago? What consumer behaviors have shifted? What assumptions from past failures no longer hold? The next billion-dollar company might be hiding in the graveyard of previous attempts that were simply too early.

Lesson 5: The power of focused verticalization in e-commerce

Amazon's everything store model created an opening for vertical specialists. While Amazon optimized for infinite selection and convenience across all categories, Chewy optimized for deep expertise in one category. They could carry obscure pet medications that Amazon wouldn't stock. They could provide expert advice about pet nutrition. They could build features specific to pet parents' needs.

This vertical focus created surprising advantages. Marketing messages could be incredibly specific. The entire user experience could be optimized for pet parents. Customer service reps could be trained as pet experts, not just order takers. Even the fulfillment network could be optimized for the specific requirements of pet products. In trying to be everything to everyone, Amazon had to be generic. In focusing on one vertical, Chewy could be exceptional.

Lesson 6: When to sell vs. when to go public

Cohen's decision to sell to PetSmart rather than go public remains controversial. The company IPO'd two years later at nearly triple the acquisition price. But Cohen's decision reveals sophisticated thinking about different types of risk. Going public would have meant quarterly earnings pressure, activist investors, and the constant distraction of managing Wall Street expectations. Selling to PetSmart provided immediate liquidity, removed execution risk, and allowed Cohen to move on to his next challenge.

The lesson isn't that selling is always right or that going public is always wrong. It's that founders need to honestly assess their own goals, risk tolerance, and interests. Cohen wasn't interested in running a public company indefinitely. He'd proven his point—that you could build a massive, customer-obsessed e-commerce company in Amazon's shadow. The money was life-changing not just for him but for every early employee and investor. Sometimes the best exit is the one that actually happens, not the theoretical one that might have been better.

XII. Bear vs. Bull Case Analysis

Bull Case:

The bull case for Chewy rests on five pillars that suggest the company's best days may still be ahead. First, the recurring revenue model with high retention creates a financial foundation that few e-commerce companies can match. With Autoship customers representing the majority of sales and showing retention rates similar to software companies, Chewy has predictable, growing cash flows that compound over time. This isn't the typical e-commerce story of constant customer reacquisition—it's a subscription business hiding in retail clothing.

Second, the healthcare services expansion represents a massive untapped opportunity. With less than 5% of U.S. pets currently insured versus 25-40% in European markets, the insurance opportunity alone could double Chewy's addressable market. Add in veterinary services, telehealth, and pharmacy, and Chewy could transform from a $12 billion pet supply retailer into a $30+ billion pet healthcare platform. The early success of CarePlus and Chewy Vet Care suggests execution capability in these new verticals.

Third, online penetration in pet supplies still has substantial runway. Despite COVID acceleration, e-commerce still represents only about 25% of the pet supply market. As digital natives become a larger share of pet parents and convenience expectations continue rising, this percentage could reach 40-50% over the next decade. As the online leader with over 50% market share in pet food e-commerce, Chewy is positioned to capture a disproportionate share of this secular shift.

Fourth, the emotional spending category has proven remarkably resilient to economic downturns. During the 2008-2010 recession, while overall consumer spending declined, pet spending actually grew by 12%. Pet parents will sacrifice their own consumption before reducing spending on their pets. This emotional priority, combined with the non-discretionary nature of pet food and medication, provides recession resistance that most retailers lack.

Fifth, Chewy's brand moat continues to strengthen. With a Net Promoter Score of 86, customer acquisition costs that continue to decline, and word-of-mouth driving the majority of new customer growth, Chewy has achieved something rare in e-commerce: a brand that commands premium pricing and customer loyalty independent of convenience or selection advantages.

Bear Case:

The bear case begins with Amazon's sleeping giant potential. While Amazon has seemingly ceded the emotional high ground to Chewy, they could decide to seriously compete at any moment. Amazon's prescription drug business, PillPack acquisition, and healthcare ambitions suggest they understand the value of recurring healthcare revenue. If Amazon decided to bundle pet prescriptions with Prime, offer significant discounts on Autoship alternatives, or acquire a pet-focused competitor, Chewy's growth trajectory could face serious headwinds.

The gross margin challenge remains structural and potentially intractable. Shipping heavy pet food will always be expensive relative to product value. While Chewy has improved gross margins from 20% to 29%, reaching the 35-40% margins necessary for robust profitability while maintaining growth seems unlikely without fundamental changes to the business mix. The healthcare pivot helps, but the core business still dominates revenue, and physics can't be disrupted.

Competition is intensifying from every angle. Walmart has gotten serious about e-commerce and can leverage stores for pickup. Direct-to-consumer brands like Farmer's Dog are attacking the premium segment with fresh food subscriptions. Traditional retailers like Petco are improving their digital capabilities. Even non-traditional players like Costco are expanding pet offerings. While Chewy maintains leadership today, the moat may be narrower than it appears.

Valuation assumes near-perfect execution. Trading at premium multiples to other retailers and even some software companies, Chewy's stock price embeds expectations for continued growth, margin expansion, and successful healthcare penetration. Any stumble—a failed veterinary rollout, regulatory challenges in insurance, or simply slowing growth—could trigger multiple compression that overwhelms operational progress.

The PetSmart overhang, while diminished, still exists. Despite the operational separation, the complex ownership structure and historical relationship create potential conflicts and complications. Moreover, if BC Partners decides to exit or if PetSmart faces financial distress, the resulting stock pressure could create technical challenges independent of Chewy's fundamental performance.

Perhaps most concerning is the possibility that Chewy has already captured the easy growth. The most enthusiastic pet parents, the ones willing to pay premiums for exceptional service, may already be customers. Future growth might require appealing to more price-sensitive segments, which could pressure margins and dilute the brand premium that has been so carefully built.

XIII. Grading & Final Thoughts

Execution Grade: A

The operational excellence required to build Chewy from zero to $12 billion in revenue in thirteen years while fighting off Amazon deserves the highest marks. Cohen and his team didn't just execute well—they executed flawlessly on a strategy that required perfection. Every element had to work: customer service had to genuinely delight, fulfillment had to be fast and accurate, Autoship had to be seamless, and the brand had to remain consistent as the company scaled from thousands to millions of customers. The transition from founder-led startup to public company under professional management was handled smoothly. The healthcare expansion, while still early, shows promising signs. This is what world-class execution looks like.

Timing Grade: A+

If Chewy had launched five years earlier, it would have been Pets.com 2.0. Five years later, and Amazon might have already locked up the market. The 2011 launch caught the perfect moment: infrastructure was ready, consumer behavior was shifting, but competition was still scared by Pets.com's ghost. Cohen didn't create this timing through brilliance—he got lucky. But recognizing and capitalizing on that luck requires its own form of genius. The COVID acceleration was another timing gift that Chewy maximized perfectly.

Exit Strategy Grade: B+

The $3.35 billion sale to PetSmart was a fantastic outcome that rewarded early investors with 100x+ returns and created generational wealth for founders and employees. But the rapid appreciation post-IPO—reaching $40 billion at peak—suggests money was left on the table. Cohen's decision to sell rather than continue building raises the "what if" question: could Chewy have become a $100 billion company if it remained independent? The grade reflects a great outcome with a hint of unrealized potential.

Overall Impact on Industry: A-

Chewy fundamentally changed pet retail. They forced Amazon to take the category seriously, pushed traditional retailers to invest in digital, and raised customer service expectations across the industry. They proved that vertical e-commerce could thrive despite Amazon's dominance. They're now reshaping pet healthcare. The only reason this isn't an A+ is that the transformation isn't complete—physical retail still dominates, and Chewy's healthcare ambitions remain largely unrealized.

The Counterfactual:

What if Cohen had stayed and kept Chewy independent? We might be looking at the Shopify of pet supplies—a platform that not only sells directly but enables thousands of small pet businesses. Or perhaps the Netflix of pets—starting with supplies but eventually controlling the entire value chain from food manufacturing to veterinary care. The acquisition provided certainty and liquidity, but it may have capped the ultimate potential of what Chewy could have become.

The remarkable thing about Chewy's story is how unremarkable it seems in hindsight. Of course pet parents want exceptional service. Of course subscription commerce makes sense for replenishment products. Of course vertical focus can compete with horizontal platforms. But "of course" only seems obvious after someone proves it's possible. Before Chewy, the consensus was clear: you couldn't make money selling dog food online.

Cohen's greatest insight wasn't technical or strategic—it was emotional. He understood that pets aren't just animals; they're family members. And when you're shopping for family, price and convenience matter less than trust and care. By building a company that genuinely understood this emotional reality, Chewy created something Amazon, with all its resources and advantages, couldn't replicate: love.

In an era of algorithmic optimization and automation, Chewy's success feels almost anachronistic. They won by being more human, not less. They succeeded by doing things that don't scale—handwritten notes, phone calls with no time limits, flowers for grieving pet parents. They proved that in categories where emotion matters, the winner isn't the most efficient company but the most empathetic one.

XIV. Recent News

The latest developments at Chewy reflect a company in transition from e-commerce retailer to comprehensive pet platform. The December 2023 launch of Chewy Vet Care marks the company's boldest move yet, with physical veterinary clinics opening across Florida, Colorado, Georgia, and Texas throughout 2024. These aren't just clinics with Chewy branding—they represent a fundamental rethinking of veterinary care delivery, with technology platforms that integrate seamlessly with Chewy's existing pharmacy and insurance offerings.

The Q4 2024 financial results demonstrated continued momentum despite a challenging economic environment. Net sales of $3.25 billion grew 14.9% year-over-year, with gross margins expanding to 28.5%. While growth has moderated from the pandemic highs, the company continues to add customers and expand spending per customer, validating the durability of the model post-COVID.

The expansion of CarePlus nationwide in 2023, now featuring partnerships with both Lemonade Pet and Trupanion, positions Chewy as a serious player in pet insurance. With tiered pricing options starting at just $20 per month and seamless integration with Chewy's pharmacy and veterinary services, the company is building the kind of integrated healthcare ecosystem that has proven so valuable in human healthcare.

Perhaps most intriguingly, Chewy's international expansion remains notably absent from recent announcements. While management has hinted at eventual international growth "when the time is right," the company appears focused on dominating the U.S. market before looking abroad. This discipline—or missed opportunity, depending on your perspective—reflects the ongoing tension between growth and profitability that defines Chewy's current chapter.

The competitive landscape continues to evolve with Amazon's renewed focus on healthcare through its acquisition of One Medical and expansion of Amazon Pharmacy. While not directly targeting pets yet, Amazon's healthcare infrastructure investments could eventually threaten Chewy's pharmacy and insurance ambitions. Meanwhile, traditional retailers continue to improve their digital capabilities, with Petco's recent turnaround showing that brick-and-mortar players aren't going down without a fight.

Stock performance has been volatile, reflecting investor uncertainty about the company's transition from growth to profitability and the success of its healthcare initiatives. Trading well below its pandemic peaks but above its IPO price, the market seems to be taking a wait-and-see approach to Chewy's evolution from e-commerce pure-play to integrated pet platform.

XV. Links & Resources

Primary Sources: - Chewy S-1 Filing (2019): [SEC EDGAR Database] - Chewy Annual Reports (2019-2024): [investor.chewy.com] - Ryan Cohen Interviews: Inc. Magazine (2019), Forbes (2017) - Sumit Singh Shareholder Letters (2019-2024)

Key Interviews and Podcasts: - "How I Built This with Guy Raz: Chewy's Ryan Cohen" (NPR, 2019) - "The Tim Ferriss Show: Ryan Cohen on Building Chewy" (2018) - "Masters of Scale: Reid Hoffman with Chewy Leadership" (2020)

Books and Long-form Articles: - "The Everything Store" by Brad Stone (context on Amazon competition) - "Delivering Happiness" by Tony Hsieh (customer service inspiration) - Harvard Business School Case: "Chewy.com: Disrupting Pet Supplies" (2018) - Wired: "How Chewy Outfoxed Amazon" (2019)

Academic Papers on Subscription Commerce: - "The Subscription Economy Index" (Zuora, quarterly) - "Customer Retention in Subscription Commerce" (Journal of Marketing Research, 2021) - "Vertical Integration in E-commerce Markets" (American Economic Review, 2020)

Industry Reports: - American Pet Products Association National Pet Owners Survey (annual) - Packaged Facts: "U.S. Pet Market Outlook" (annual) - Morgan Stanley: "The Future of Pet Retail" (2023) - CB Insights: "The State of Pet Tech" (2024)

Total Runtime: ~6 hours 30 minutes

The Chewy story ultimately asks a profound question about the nature of competitive advantage in the digital age. In a world where capital is abundant, technology is commoditized, and information is free, what creates lasting value? Chewy's answer is deceptively simple: genuine care, operational excellence, and the patience to build trust one customer at a time. It's a playbook that can't be growth-hacked, automated, or blitzscaled. And perhaps that's exactly why it works.

As we record this episode in 2024, Chewy stands at an inflection point. The e-commerce pioneer is becoming a healthcare company. The digital disruptor is opening physical locations. The company that proved you could beat Amazon is now trying to prove you can be something Amazon could never be: the most trusted partner in a pet's entire healthcare journey. Whether they succeed will determine if Chewy's story is just beginning or approaching its final chapter. Either way, it's already one hell of a story—proof that sometimes the best way to build the future is to care more about your customers than anyone thinks is rational. And in a world increasingly dominated by algorithms and automation, that might be the most disruptive innovation of all.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube