Charter Communications: The Cable Consolidator's Quest

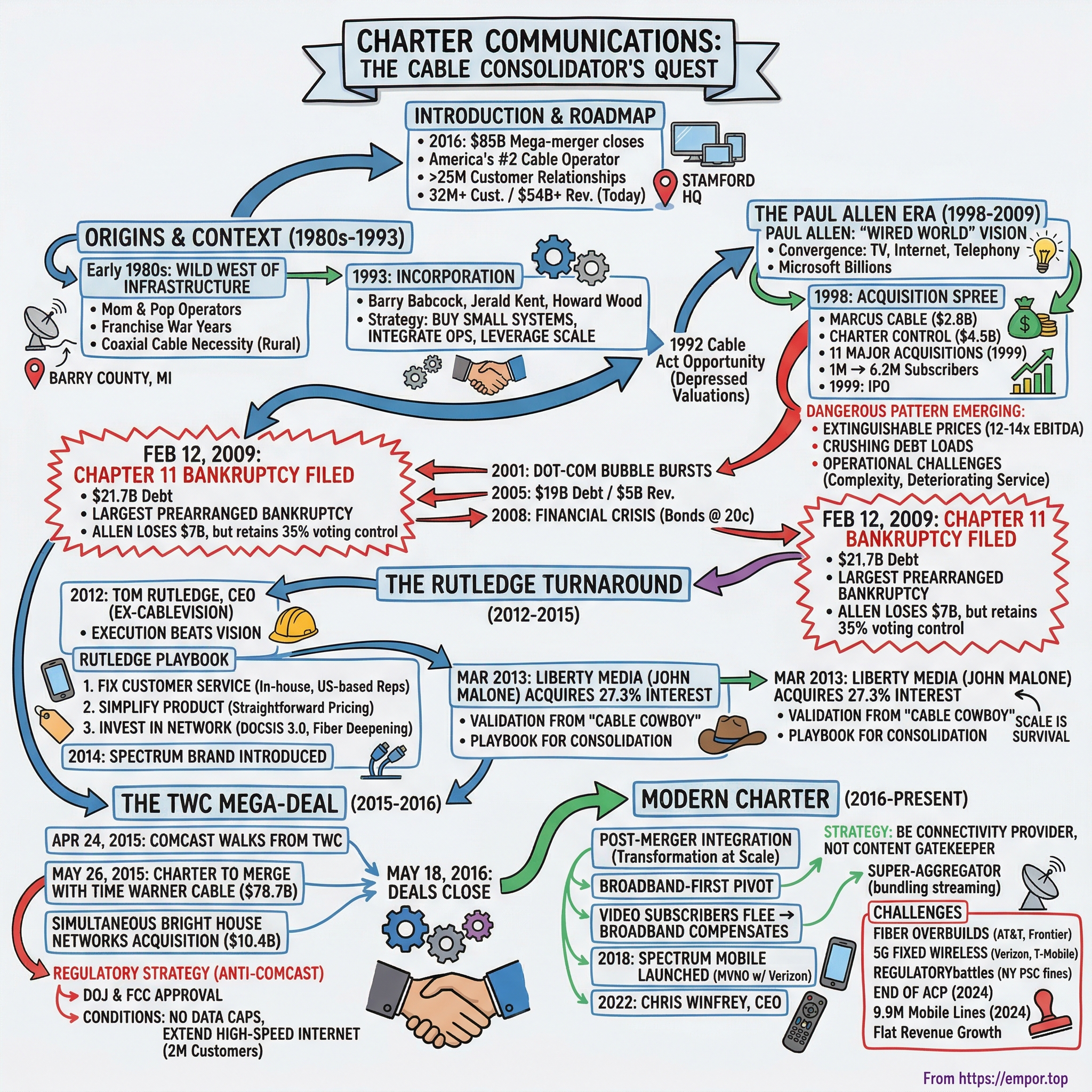

I. Introduction & Episode Roadmap

Picture this: It's May 2016, and Tom Rutledge stands in Charter Communications' new Stamford headquarters, watching as screens across the trading floor light up with confirmation. The $85 billion mega-merger creating America's second-largest cable operator has just closed. Charter now controls over 25 million customer relationships across 41 states—a staggering transformation for a company that, just seven years earlier, had emerged from one of the largest pre-packaged bankruptcies in U.S. history.

Today, Charter Communications serves over 32 million customers, generating north of $54 billion in annual revenue. It's a $100+ billion market cap giant that controls critical last-mile infrastructure across America. Yet this is a company built on the ruins of spectacular failures, multiple bankruptcies, and one of the most devastating individual investment losses in corporate history—Paul Allen's $7 billion wipeout.

The provocative question at the heart of Charter's story isn't just how three former cable executives built a telecom giant. It's how a company weaponized bankruptcy, turned catastrophic overleveraging into competitive advantage, and consolidated an entire industry while its founding visionary lost nearly everything. This is a tale of financial engineering meeting operational excellence, where debt becomes both destroyer and enabler, and where the line between failure and strategy blurs beyond recognition.

What you're about to discover is the playbook for cable consolidation—how to build scale in capital-intensive industries, manage through bankruptcy while maintaining control, and transform from content distributor to connectivity provider. We'll explore the art of buying distressed assets, the dangers of vision without discipline, and why in cable, as in few other industries, size isn't just an advantage—it's survival.

The themes we'll track: consolidation as destiny, debt as double-edged sword, the crucial difference between financial and operational leadership, and how regulatory capture can become competitive moat. From Barry County, Michigan to Wall Street's biggest stages, from Paul Allen's billions to John Malone's chess moves, this is the story of how Charter Communications conquered cable by first conquering failure itself.

II. Origins & The Cable Industry Context (1980s–1993)

The rain hammered against the windows of a small Michigan office in 1980 as Charles Leonard signed the papers creating Charter Communications CATV Systems. Barry County, Michigan—population 50,000, mostly rural, the kind of place where cable television wasn't a luxury but a necessity if you wanted to receive any signal at all through the dense forests and rolling hills. Leonard wasn't thinking about building an empire. He was thinking about connecting neighbors to the outside world, one coaxial cable at a time.

The early 1980s cable landscape was the Wild West of American infrastructure. Thousands of mom-and-pop operators strung wire across the country, each controlling tiny fiefdoms granted by local franchise agreements. The big promise? Instead of three fuzzy broadcast channels, you could deliver twenty, thirty, even forty crystal-clear channels. HBO had launched in 1972, CNN in 1980—suddenly cable wasn't just about reception, it was about exclusive content you couldn't get over the air.

These were the franchise war years. Cities and towns auctioned off exclusive rights to wire their communities, and operators bid aggressively, promising everything from public access channels to free hookups for schools. The economics were intoxicating: high upfront capital costs, but once you wired a neighborhood, you had a monopoly on multichannel video. Subscribers paid monthly, churn was low, and cash flow was predictable. Wall Street was starting to notice.

Enter three men who would transform Leonard's modest Michigan system into something far grander. Barry Babcock, Jerald Kent, and Howard Wood weren't industry outsiders—they were battle-tested veterans from Cencom Cable Associates, a St. Louis-based operator that had grown through aggressive acquisitions before selling to Hallmark Cards in 1991. The trio had watched the Cencom playbook: buy small systems, integrate operations, leverage scale for better programming deals, repeat. They believed they could do it better.

In January 1993, Babcock, Kent, and Wood formally incorporated Charter Communications, Inc., acquiring Leonard's Michigan systems as their foundation. But their timing was fascinating—and fraught. The Cable Television Consumer Protection and Competition Act of 1992 had just passed, giving the FCC power to regulate cable rates for the first time in years. The industry recoiled. Stock prices tumbled. Suddenly, cable systems were selling at discounts.

Where others saw regulatory disaster, the Charter founders saw opportunity. "The 1992 Cable Act was our friend," Kent would later recall. "It scared away buyers, depressed valuations, but we knew the fundamentals hadn't changed. People weren't going to suddenly stop watching television."

Their strategy was surgical. Target rural and suburban systems in the Southeast and Midwest—markets too small for the big players but large enough to generate solid cash flow. Integrate aggressively, cutting redundant costs. Use the savings to upgrade plant and equipment. Most importantly, cluster systems geographically to create regional density, reducing operational costs and increasing leverage with programmers. In February 1994, Charter announced its first major move. It would spend nearly $200 million to acquire ten cable systems in Louisiana, Georgia, and Alabama. The systems were acquired from the McDonald Group of Birmingham, Alabama, and served about 100,000 subscribers in the Southeast. This wasn't just an acquisition—it was a declaration of intent. The Southeast strategy was deliberate: less competitive, more rural, cheaper to acquire, easier to cluster.

The founders were building something different from the coastal giants. While TCI and Time Warner fought over major metropolitan areas, Charter quietly assembled rural and suburban territories like a chess player controlling the center of the board. They understood a fundamental truth about cable economics: a clustered 100,000 subscribers in contiguous markets was worth more than 200,000 scattered across the country. Programming costs were the same, but operational efficiency in clustered markets was transformative.

By 1995, Charter had emerged as the 15th largest Multiple System Operator (MSO) in the United States—impressive for a company barely two years old. They were proving that disciplined acquisition and integration could build scale rapidly. But what they needed was capital—serious capital—to compete with the giants. The stage was set for a transformation that would either catapult Charter into the big leagues or destroy it entirely. And in 1998, a billionaire from Seattle would provide exactly that opportunity.

III. The Paul Allen Era: Vision Meets Reality (1998–2009)

Paul Allen sat in his Seattle office in early 1998, Microsoft billions in the bank, staring at a map of America's cable systems. The co-founder of the software giant had left day-to-day operations years earlier, but his mind hadn't stopped racing. He saw something others didn't: the convergence of television, internet, and telephony into a single pipe. His "Wired World" vision imagined cable systems as the nervous system of the digital age—not just carrying TV signals, but becoming the platform for all communications. Charter Communications was about to become his laboratory.

In 1998, Paul Allen bought a controlling interest. The company paid $2.8 billion to acquire Dallas-based cable company Marcus Cable. Charter Communications had one million customers in 1998. But Allen wasn't done. A month after the Marcus Cable deal, he paid $4.5 billion for his controlling stake in Charter itself—a staggering premium that raised eyebrows across Wall Street. In total, Allen had deployed over $7 billion in less than sixty days.

The "Wired World" vision was intoxicating in its ambition. Allen imagined Charter's cables carrying not just television but high-speed internet, telephone service, interactive gaming, home security, and services not yet invented. This wasn't just about being a cable company—it was about owning the digital highway into American homes. He hired top engineers from Microsoft and telecom companies, established research labs, and began plotting a transformation that would make Charter the most advanced cable operator in America.

What followed was an acquisition spree unprecedented in cable history. Throughout 1999, Charter executed eleven major acquisitions, each one larger and more audacious than the last. The company was consuming competitors like a financial black hole. By year's end, Charter had ballooned from one million to 6.2 million subscribers—a 520% increase in a single year. The deals were coming so fast that integration teams were still working on March's acquisition when December's deal closed.

In November 1999, the company went public, trading on the Nasdaq stock exchange. At the time, it had 3.9 million customers and the IPO raised approximately $3.5 billion—one of the largest offerings of the dot-com era. The market loved the story: a visionary billionaire building the cable company of the future. Charter's stock soared, and Allen's paper wealth multiplied.

But beneath the euphoria, a dangerous pattern was emerging. Many of these acquisitions were made at extravagant, top-of-the-market prices. Allen was paying 12-14 times EBITDA when historical multiples were 8-10 times. The acquired companies brought not just subscribers but crushing debt loads. Charter's leverage ratio was climbing toward dangerous territory—from 4x EBITDA to 6x, then 8x, then beyond what any cable company had previously sustained.

The operational challenges were equally daunting. Each acquired system had different billing platforms, different channel lineups, different technical standards. Charter's corporate staff, still based in St. Louis, grew from dozens to thousands seemingly overnight. Integration costs soared. Customer service deteriorated. The company that had prided itself on operational excellence was drowning in complexity.

By 2001, the cracks were showing. The dot-com bubble had burst, taking cable valuations with it. The convergence revolution Allen had bet on was happening, but more slowly than expected. Telephone-over-cable technology was expensive and unreliable. High-speed internet adoption was growing but not fast enough to offset the massive debt payments. Charter was burning through cash, and the capital markets had turned hostile.

Allen tried everything. He personally injected hundreds of millions more. He hired and fired executives. He renegotiated programming contracts. But the math was inexorable. By 2005, Charter was carrying over $19 billion in debt against $5 billion in annual revenue. Interest payments alone were consuming nearly 20% of revenue. The company was technically solvent but functionally paralyzed.

The 2008 financial crisis was the final blow. Credit markets froze. Charter's bonds traded at 20 cents on the dollar. The company that had once symbolized cable's digital future now represented its debt-fueled past. On February 12, 2009, Charter Communications filed for Chapter 11 bankruptcy protection. With $21.7 billion in debt, it was the largest so-called "prearranged bankruptcy" in history at the time.

Paul Allen's grand experiment had failed catastrophically. His personal losses were staggering—estimated at $7 billion, one of the largest individual investment losses in American corporate history. Yet remarkably, Allen didn't walk away. Through careful negotiation and legal maneuvering, he retained a 35% voting stake in the reorganized company. He had lost his fortune but kept his seat at the table. The question now was whether Charter could rise from the ashes of Allen's ambition.

IV. The Bankruptcy & Restructuring (2009–2011)

The February morning in 2009 when Charter filed for bankruptcy was orchestrated like a symphony. While Lehman Brothers' chaotic collapse months earlier had sent shockwaves through markets, Charter's bankruptcy was different—prearranged, prepackaged, and precisely planned. In the Manhattan offices of Kirkland & Ellis, lawyers had worked for months crafting a bankruptcy that would somehow reduce debt by $8 billion while keeping the company operational and Allen partially in control. This wasn't a corporate death; it was a financial metamorphosis.

The numbers were staggering and stark. Charter entered bankruptcy with $21.7 billion in debt against an enterprise value of roughly $13 billion. The company was generating solid operational cash flow—about $1.8 billion annually—but interest payments were devouring $1.6 billion of that. It was like trying to fill a bathtub with the drain wide open. Something had to give, and that something was the debt holders' claims.

The prearranged nature of Charter's bankruptcy was crucial. Before filing, the company had negotiated with major creditors, securing agreement from holders of about $15 billion in debt. The plan was elegant in its simplicity: convert $8 billion of debt into equity, inject $3 billion in new capital, and refinance the remaining obligations at lower rates. Debt holders would own most of the company, but operations would continue uninterrupted. Customers wouldn't lose service. Employees would keep their jobs. The beast would keep breathing.

But not everyone was happy. A group of junior creditors, led by JPMorgan Chase, saw an opportunity. They had purchased Charter's debt at distressed prices—sometimes as low as 15 cents on the dollar—and now wanted to control the reorganization. The dispute centered on the valuation of Charter post-bankruptcy. JPMorgan argued the company was worth far more than the plan assumed, meaning junior creditors deserved a bigger piece. The fight would culminate in one of the most dramatic bankruptcy trials of the financial crisis.

The trial, held in Manhattan's bankruptcy court in late 2009, became a masterclass in financial engineering and legal strategy. JPMorgan brought in expert witnesses arguing Charter was worth $18 billion or more. Allen's team countered that the company was worth perhaps $14 billion at best. The difference meant billions in value allocation. Judge James Peck presided over testimony that ranged from cable industry economics to the minutiae of plant depreciation schedules.

The most fascinating aspect was how Allen maintained influence despite his catastrophic losses. Through a complex series of agreements, he retained 35% voting control while owning just 4% of the economic equity. He also negotiated a board seat and veto rights over major decisions. For someone who had lost $7 billion, it was a remarkable salvage operation. "Paul Allen may have lost his money," one restructuring advisor noted, "but he didn't lose his power."

On November 30, 2009, its bankruptcy plan was approved. The plan reduced debt from $21.7 billion to about $13 billion, added $3 billion in new financing, and gave the company breathing room to invest in operations. Apollo Management, Oaktree Capital, and other sophisticated distressed investors became major shareholders. These weren't cable guys—they were financial engineers who saw opportunity in Charter's infrastructure and cash flow.

Charter emerged from bankruptcy on the same day the plan was approved, despite continued objections from some creditors. The speed was intentional. Every day in bankruptcy meant more legal fees, more uncertainty, more customer defections. The new Charter was leaner—same revenue, same customers, but with $8 billion less debt. Interest payments dropped from $1.6 billion to under $1 billion annually. Suddenly, the company had money to invest in its network and operations.

The restructuring revealed profound lessons about leverage in capital-intensive industries. Charter's operations had never failed—the company maintained its subscriber base throughout bankruptcy, continued generating cash flow, and even gained market share in broadband. The failure was entirely financial, a mismatch between debt load and cash generation. The infrastructure—the actual cables in the ground—retained its value regardless of the corporate structure above it.

The new ownership structure was a who's who of distressed debt investing. Apollo brought operational expertise from other turnarounds. Oaktree understood cable economics from previous investments. These weren't passive investors; they were activists who knew Charter needed new leadership to fulfill its potential. They began searching for a CEO who could merge operational excellence with financial discipline.

What emerged from bankruptcy wasn't just a restructured Charter but a blueprint for cable consolidation. The company had proven that even catastrophic overleveraging couldn't destroy the underlying value of cable infrastructure. With the right leadership and strategy, Charter could still become the giant Paul Allen had envisioned—just without the crushing debt that had nearly killed it. The stage was set for the next act, and the private equity owners knew exactly who they wanted to lead it.

V. The Rutledge Turnaround (2012–2015)

Tom Rutledge's hands were still calloused from his days as a lineman when he walked into Charter's temporary boardroom in early 2012. The 58-year-old executive had started his career in 1977 stringing cable in pole-to-pole installations, and those formative years climbing poles in all weather had given him something MBA-trained executives often lacked: an intimate understanding of how cable systems actually worked. Now, after transforming Cablevision into one of the industry's best operators, he was being handed the keys to a post-bankruptcy giant with enormous potential and equally enormous problems.

In late 2012, with longtime Cablevision executive Thomas Rutledge named as their CEO, Charter relocated its corporate headquarters from St. Louis, Missouri, to Stamford, Connecticut. The headquarters move was symbolic but significant. St. Louis represented Charter's entrepreneurial past; Stamford put the company in the heart of the Northeast corridor, closer to programmers, investors, and the talent pool Rutledge needed to execute his vision.

Rutledge's background was the opposite of Paul Allen's visionary futurism. At Cablevision, serving the hypercompetitive New York market, he had learned that execution beats vision every time. His philosophy was deceptively simple: deliver what you promise, price it fairly, and treat customers with respect. Under his leadership as COO, Cablevision had achieved industry-leading customer satisfaction scores while maintaining the highest average revenue per user in cable.

The playbook Rutledge brought to Charter was methodical and unglamorous. First, fix customer service. Charter's call centers were disasters—long hold times, multiple transfers, inconsistent information. Rutledge mandated that all customer service representatives be brought in-house and based in the United States. No more outsourcing to save pennies while destroying customer relationships. He implemented a single-call resolution metric: solve the customer's problem on the first call or consider it a failure.

Second, simplify the product. Charter's pricing was a maze of promotional rates, hidden fees, and expiring discounts that confused customers and bred resentment. Rutledge introduced straightforward pricing—one rate for internet, one for video, one for voice. No contracts. No hidden fees. The price you saw was the price you paid. Wall Street was skeptical; wouldn't this reduce revenue per customer? Rutledge's response: "I'd rather have a satisfied customer paying $100 than an angry one paying $110."

Third, invest in the network. Charter had emerged from bankruptcy with reduced debt but aging infrastructure. Many systems still offered maximum internet speeds of 30 Mbps when competitors were pushing 100 Mbps or higher. Rutledge launched a massive capital investment program, upgrading systems to DOCSIS 3.0, pushing fiber deeper into neighborhoods, and preparing for the all-digital transition. The spending was aggressive—over $4 billion annually—but Rutledge knew that in broadband, speed sells.

The introduction of the Spectrum brand in 2014 unified Charter's scattered identity. For years, the company had operated under various names from acquisitions—Charter, Bresnan, Optimum West. Spectrum represented a fresh start, a promise of simplicity and reliability. The logo was clean, modern, deliberately understated. This wasn't about flash; it was about fundamental service delivery. But the true game-changer came in March 2013. Liberty Media, a company controlled by former TCI CEO John C. Malone, would be acquiring a 27.3% ownership interest in the company from investment funds tied to Apollo Management, Oaktree Capital Management and Crestview Partners to buy about 26.9 million shares and about 1.1 million warrants in Charter. The price tag: $2.62 billion at $95.50 per share. John Malone—the legendary "Cable Cowboy" who had built TCI into America's largest cable company before selling to AT&T in 1999—was back in the U.S. cable game.

Malone's entry transformed everything. This wasn't just capital; it was validation from the industry's most successful consolidator. Rutledge acknowledged the significance: "Liberty Media and John Malone have a well proven track record in our industry and in creating shareholder value." What Rutledge didn't say publicly was that Malone brought something even more valuable: a playbook for consolidation and the relationships to execute it.

The chemistry between Rutledge and Malone was immediate and powerful. Both understood that cable's future lay in scale—massive, market-dominating scale. Malone had tried and failed to acquire Time Warner Cable in 2013, losing out to Comcast's $45 billion bid. But Comcast's deal would face regulatory challenges, and both men sensed opportunity. They began positioning Charter as the alternative acquirer, the "good guy" who could consolidate without triggering antitrust concerns.

Charter's failed attempts at Time Warner Cable in 2013-2014 were instructive rather than devastating. The company bid $37 billion, then $38 billion, each time being rebuffed by TWC's board who preferred Comcast's higher offer. But Rutledge was playing a longer game. He knew Comcast-TWC would face intense regulatory scrutiny. He kept Charter's powder dry, its operations improving, its balance sheet strengthening. When opportunity came, he would be ready.

The transformation under Rutledge was remarkable. Customer satisfaction scores improved dramatically. Broadband speeds increased while prices stabilized. The company began winning back customers who had defected to satellite and telco competitors. By 2015, Charter was generating over $2 billion in free cash flow, had reduced its leverage ratio to manageable levels, and was positioned as the industry's operational leader. The company that had emerged from bankruptcy as a financial engineering project was becoming an operational powerhouse. And soon, very soon, it would get its chance at the transformative deal that would define its future.

VI. The Time Warner Cable Mega-Deal (2015–2016)

The phone call came at 6 AM on April 24, 2015. Tom Rutledge was already at his desk in Stamford when the news broke: Comcast was walking away from its $45 billion acquisition of Time Warner Cable. Regulatory pressure had proven insurmountable. Within minutes, Rutledge was on the phone with John Malone. "This is our moment," Malone said simply. By noon, Charter's deal team was assembled. By evening, initial contact with TWC had been made. The consolidation opportunity of a generation had just opened, and Charter was ready to strike. On May 26, 2015, Charter Communications, Inc. and Time Warner Cable Inc. announced that they have entered into a definitive agreement for Charter to merge with Time Warner Cable. The deal valued Time Warner Cable at $78.7 billion. Charter would provide $100.00 in cash and shares of a new public parent company ("New Charter") equivalent to 0.5409 shares of CHTR for each Time Warner Cable share outstanding. The deal valued each Time Warner Cable share at approximately $195.71 based on Charter's market closing price on May 20—a 14% premium to TWC's unaffected price.

But this wasn't just about TWC. In a masterstroke of complexity, Charter simultaneously amended its agreement to acquire Bright House Networks for $10.4 billion, creating a three-way combination that would reshape American cable. Bright House, the sixth-largest cable operator with 2.5 million customers primarily in Florida, had been family-owned by the Newhouse family. The structure was Byzantine: Charter and Advance/Newhouse would form a partnership, with New Charter owning 86-87% and Advance/Newhouse owning 13-14%, receiving both cash and convertible securities.

The financing architecture revealed John Malone's fingerprints. Liberty Broadband agreed to purchase $4.3 billion of newly issued shares of New Charter at closing, plus another $700 million previously committed. This would give Liberty approximately 25% ownership and effective control through supervoting shares. Malone had learned from the Allen era: control didn't require majority ownership if you structured it correctly.

The regulatory strategy was surgical. Charter positioned itself as the anti-Comcast—smaller, less vertically integrated, without NBC Universal's content conflicts. Rutledge flew to Washington repeatedly, meeting with FCC Chairman Tom Wheeler and Department of Justice officials. The message was consistent: "We're an infrastructure company, not a media conglomerate. We want to connect Americans, not control what they watch. "The regulatory negotiations revealed Charter's strategic brilliance. The Department of Justice approved the massive cable deal and FCC Chairman Tom Wheeler circulated an order that would approve the combination of Charter, TWC and BHN subject to conditions. But these weren't punitive conditions—they were guardrails Charter could live with, even leverage as competitive advantages.

The key concessions were transformative. Charter would not be permitted to launch usage-based broadband pricing or impose data caps and would not be allowed to charge interconnection fees, including for online video providers. For seven years, Charter agreed to conditions that essentially forced it to be consumer-friendly—no data caps when competitors were implementing them, no interconnection fees when others were extracting tolls from Netflix and streaming services.

The conditions placed on FCC approval would require Charter to extend high-speed internet access to another two million customers within five years, with one million served by a broadband competitor. This wasn't a burden—it was an excuse to build out infrastructure with regulatory blessing, funded by the merger synergies.

The integration planning was meticulous. Charter had learned from past merger disasters in cable. They established "clean rooms" where integration teams could plan without violating pre-merger restrictions. They mapped every system, every headend, every billing platform. The goal wasn't just to combine companies but to create a unified operation that could realize $800 million in annual cost synergies within three years.

On May 18, 2016, Charter finalized acquisition of Time Warner Cable and its sister company Bright House Networks, making it the third-largest pay television service in the United States. The numbers were staggering: 25 million customer relationships, presence in 41 states, second-largest broadband provider, third-largest video provider. Charter's market cap had grown from $10 billion post-bankruptcy to over $100 billion at closing.

The Spectrum rebrand was immediate and total. In 2017, Charter stopped using the TWC and BHN branding and fully integrate the two services' subscribers into the Spectrum brand. Every truck was repainted, every storefront redesigned, every bill reformatted. This wasn't three companies operating under one ownership—this was one company, one brand, one vision.

Tom Rutledge stood in the same Stamford headquarters where the journey had begun, now overseeing an empire that would have been unimaginable when Charter emerged from bankruptcy seven years earlier. The company that Paul Allen had nearly destroyed with overleveraging had used disciplined acquisition and operational excellence to become exactly what Allen had envisioned—just without the crippling debt. The transformation was complete, but the challenges of being a cable giant in the streaming age were just beginning.

VII. Modern Charter: Scale, Competition, and Challenges (2016–Present)

The honeymoon lasted exactly 47 days. On July 4, 2016, less than two months after closing the Time Warner Cable acquisition, Charter's network operations center lit up with alarms. A massive outage had knocked out service for 300,000 customers across Los Angeles—on Independence Day, when millions were home streaming. The TWC infrastructure Charter had inherited was showing its age, and the integration challenges were more complex than any spreadsheet had captured. Tom Rutledge personally took command of the war room. "This is why we bought them," he told his team. "Not for what they are, but for what we'll make them."

The post-merger integration was a masterclass in operational transformation at scale. Charter had inherited three different billing systems, five different email platforms, and dozens of different channel lineups. The company deployed 10,000 technicians to physically audit every headend, every node, every mile of plant. They discovered TWC systems still running on equipment from the 1990s, Bright House networks that hadn't been upgraded in a decade. The capital investment required was staggering—$7 billion annually, more than Charter's entire revenue just five years earlier.

But Rutledge's strategy was working. By standardizing on all-digital service, Charter could offer minimum speeds of 200 Mbps when AT&T and Frontier were struggling to deliver 25 Mbps over copper. The company eliminated outdated analog channels, freeing spectrum for broadband capacity. Customer satisfaction scores, while still not industry-leading, improved dramatically from the TWC nadir. Churn rates dropped. Average revenue per user climbed.

The broadband-first pivot was prescient and essential. Video subscribers were fleeing traditional cable at an accelerating pace—Charter was losing 200,000 video customers per quarter by 2018. But broadband additions more than compensated. As Netflix, Disney+, and other streaming services proliferated, they all required one thing: high-speed internet. Charter wasn't competing with streaming; it was enabling it. "We're not a TV company that offers internet," Rutledge would say. "We're a connectivity company that happens to offer TV."On June 30, 2018, Charter launched Spectrum Mobile, a mobile virtual network operator service. The timing was perfect—consumers wanted bundled services, and Charter could offer internet, video, and now mobile on a single bill. Using an MVNO agreement with Verizon, Charter avoided the massive capital expenditure of building wireless infrastructure while capturing the growing convergence opportunity. Within five years, Spectrum Mobile would grow to over 8 million lines, becoming one of the fastest-growing wireless services in America.

But regulatory battles erupted with devastating force. In June 2018, the New York Public Service Commission fined Charter $2 million for failing to meet obligations it agreed to as conditions of its acquisition of Time Warner Cable. The company had promised to extend broadband to 145,000 underserved homes but had fallen short. Then, in a shocking escalation on July 27, 2018, the NYPSC voted to retroactively reverse its approval of Charter's acquisition of TWC, ordering the company to sell its New York operations.

The New York battle became a corporate crisis. Charter had 2.6 million customers in the state, generating billions in revenue. The prospect of forced divestiture sent the stock plummeting. Rutledge personally led negotiations with Governor Andrew Cuomo's administration. After months of brinkmanship, Charter agreed to pay $174 million in penalties and extend broadband to an additional 145,000 homes. The crisis passed, but the message was clear: even giants could be brought to heel by determined regulators.

The competitive landscape was transforming with frightening speed. AT&T and Verizon were deploying fiber-to-the-home in Charter's markets, offering symmetrical gigabit speeds that cable's DOCSIS technology couldn't match. T-Mobile and Verizon launched fixed wireless services, using 5G to deliver home broadband without wires. Streaming services were unbundling the video package, with customers cobbling together Netflix, Hulu, Disney+, and others instead of buying traditional cable.

Charter's response was to double down on simplicity and value. The company launched Spectrum One, bundling internet and mobile for a single price. They invested heavily in DOCSIS 4.0 technology, pushing toward multi-gigabit speeds. They abandoned the battle for video margins, essentially offering TV service at cost to retain broadband customers. The strategy was clear: be the connectivity provider, not the content gatekeeper.

Labor relations exploded into crisis in 2017 when 1,800 technicians in New York went on strike, the longest strike in U.S. cable history, lasting until 2020. The workers, represented by the International Brotherhood of Electrical Workers, protested Charter's healthcare and retirement benefit changes post-merger. Customers faced installation delays, service disruptions, and the spectacle of picketing workers outside Charter stores. The strike cost hundreds of millions in lost productivity and damaged Charter's reputation in its most important market. The financial performance tells a complex story. As of December 31, 2024, Charter served 30.1 million Internet customers, having lost 177,000 in the fourth quarter alone. The broadband business, once invincible, was facing unprecedented pressure from fiber overbuilds and fixed wireless competition. Yet mobile was exploding—9.9 million lines by year-end 2024, with 2.1 million added during the year, generating 37.4% revenue growth. Fourth quarter revenue of $13.9 billion grew by just 1.6% year-over-year, revealing the mature nature of the core business.

The end of the Affordable Connectivity Program (ACP) in May 2024 delivered a body blow, removing subsidies that had helped low-income customers afford broadband. Charter lost tens of thousands of subscribers who could no longer afford service without government assistance. Management argued they would have shown broadband growth without the ACP impact, but the market was unforgiving.

Leadership transition marked a new era. Chris Winfrey succeeded Tom Rutledge as CEO in December 2022, inheriting both the empire Rutledge had built and its challenges. Winfrey, a Charter veteran who had run the company's operations, represented continuity but also evolution. His focus shifted to convergence—bundling broadband, mobile, and streaming services into integrated packages that increased customer stickiness.

The streaming wars had transformed Charter from gatekeeper to aggregator. Instead of fighting streaming services, Charter embraced them, bundling Disney+, Paramount+, and other services into its packages. The company became a super-aggregator, simplifying the confusing streaming landscape for customers while earning commissions from streaming providers. It was a far cry from the days when cable operators controlled what America watched.

Today's Charter is a study in contrasts. It's a $55 billion revenue giant that barely grows. It has irreplaceable infrastructure being challenged by new technologies. It's a monopoly in some markets facing fierce competition in others. The company that rose from bankruptcy to become America's second-largest broadband provider now fights to maintain relevance in an age of fiber, 5G, and streaming. The consolidation story that defined Charter's rise has given way to a new narrative: survival through transformation in an industry being disrupted from every angle.

VIII. Playbook: Business & Investment Lessons

The conference room at Apollo Management's Manhattan offices in 2010 was thick with cigarette smoke—one of the last places in New York where you could still smoke indoors—as distressed debt investors dissected Charter's bankruptcy. "The lesson here," said one veteran, stubbing out his Marlboro, "is that in cable, the infrastructure survives everything. Management comes and goes, capital structures explode, but those cables in the ground keep generating cash." That insight would drive billions in cable investments over the next decade and reveals the first principle of the Charter playbook: in capital-intensive industries, physical assets create value independent of financial engineering.

The Consolidation Playbook: When to Buy, When to Wait

Charter's acquisition history reads like a masterclass in market timing. The company thrived by buying when others were selling—during the 1992 Cable Act regulatory panic, after the 2009 financial crisis, following Comcast's failed TWC acquisition. The pattern is unmistakable: regulatory uncertainty and market disruption create buying opportunities for those with capital and conviction.

But equally important was knowing when not to buy. Charter walked away from overpriced assets repeatedly in the late 1990s while Paul Allen was paying anything to anybody. They let Comcast overpay for TWC initially, knowing regulatory challenges would likely kill the deal. The discipline to wait, to let others make mistakes, proved as valuable as the aggression to strike when opportunity emerged. In consolidating industries, the second mover often wins.

Managing Through Bankruptcy: Pre-packaged vs. Traditional Chapter 11

Charter's 2009 bankruptcy wasn't a failure—it was a strategic reset that preserved operational value while shedding impossible debt. The pre-packaged nature was crucial. By negotiating with creditors before filing, Charter maintained customer relationships, kept employees, and emerged in just nine months. Traditional bankruptcy, with its uncertainty and operational disruption, would have destroyed far more value.

The genius was in the details. Paul Allen maintained influence despite catastrophic losses through creative structuring—35% voting control with 4% economic ownership. This wasn't charity from creditors; they recognized that Allen's relationships and industry knowledge had value beyond his capital. The lesson: in distressed situations, control and economics can be separated to preserve essential expertise while rightsizing the capital structure.

Debt as Tool and Trap: The Allen Cautionary Tale

Paul Allen's $7 billion loss at Charter stands as one of history's great investment disasters, yet the assets he assembled ultimately created enormous value—just not for him. The difference between Allen's failure and Rutledge's success wasn't vision but leverage. Allen used debt to buy growth at any price; Rutledge used it to fund integration and improvement of assets bought at reasonable valuations.

The math is unforgiving: at 8x EBITDA leverage (where Charter was pre-bankruptcy), every 1% increase in interest rates costs 8% of EBITDA in additional interest expense. At 4x leverage (where Charter operates today), the same rate increase costs just 4% of EBITDA. In capital-intensive industries, the difference between aggressive and reckless leverage is often just two turns of debt—but those two turns can mean the difference between fortune and ruin.

Operational Excellence vs. Financial Engineering

The contrast between the Allen and Rutledge eras illuminates a fundamental truth: operational excellence beats financial engineering every time. Allen's Charter had brilliant financial architecture but mediocre operations. Rutledge's Charter had simpler finances but superior execution. Customer service improvements, network upgrades, and pricing simplification—these mundane operational improvements created more value than all of Allen's visionary acquisitions.

The numbers tell the story. Under Allen, Charter's average revenue per user (ARPU) grew through price increases that drove customer defection. Under Rutledge, ARPU grew through value creation—faster speeds, better service, new products—that reduced churn. Same metric, opposite approach, dramatically different outcomes. In subscription businesses, keeping customers is cheaper than finding new ones.

The Importance of Scale in Capital-Intensive Industries

Charter's journey from 100,000 to 30+ million customers reveals why scale matters in cable. Programming costs, the industry's largest expense after infrastructure, barely budge whether you have one million or ten million subscribers. ESPN charges roughly the same per-subscriber fee regardless of your size—but your negotiating leverage changes dramatically. At Charter's current scale, a $0.10 per month per subscriber savings on ESPN translates to $36 million annually.

Scale economics extend beyond programming. A customer service call center needs minimum staffing whether serving 100,000 or one million customers. Billing systems, network monitoring, executive overhead—all have massive fixed cost components. This creates a vicious cycle for subscale operators: higher per-customer costs lead to higher prices or lower margins, making them either uncompetitive or attractive acquisition targets. In cable, you either consolidate or get consolidated.

Regulatory Management and Political Capital

Charter's successful navigation of the TWC merger approval, contrasted with Comcast's failure, demonstrates the importance of regulatory strategy. Charter positioned itself as the "good consolidator"—no vertical integration, no content conflicts, commitments to net neutrality and no data caps. They turned regulatory conditions into competitive advantages, marketing "no data caps" as a consumer benefit while competitors imposed them.

The company's approach to franchise negotiations reveals another lesson: local relationships matter in regulated industries. Charter maintains government affairs professionals in every major market, contributes to local causes, and ensures mayors and city councils know their local Charter manager. When franchise renewal comes every 10-15 years, these relationships prove invaluable. Political capital, like financial capital, must be accumulated before you need it.

Brand Transitions and Customer Retention

The Spectrum rebrand following the TWC acquisition could have been a disaster. History is littered with failed rebrandings that confused customers and destroyed value. Charter's approach was instructive: complete and immediate. No gradual transition, no dual branding, no confusion. Every truck, every bill, every storefront changed simultaneously. The estimated cost exceeded $100 million, but the alternative—years of brand confusion—would have cost far more in customer defection and operational complexity.

The Shift from Content Distribution to Connectivity Provider

Charter's evolution from cable TV company to broadband provider represents a fundamental strategy shift that many industries face: when your core product becomes commoditized, move up or down the value chain. Charter couldn't compete with Netflix on content, so it became the pipe Netflix needed to reach customers. Video became a customer acquisition tool for broadband rather than a profit center itself.

This transition required painful choices. Video margins collapsed from 40% to near zero. Programming costs continued rising while subscribers fled. But broadband margins held at 60%+, and broadband subscribers continued growing even as video declined. The lesson: cannibalize yourself before others do it for you. Charter's willingness to sacrifice video profitability to protect broadband positioning saved the company.

The Charter playbook ultimately reduces to this: in capital-intensive industries with network effects, scale wins—but only when combined with operational excellence and financial discipline. Buy distressed assets, integrate aggressively, manage leverage carefully, and remember that in infrastructure businesses, the assets outlive everything else.

IX. Bear vs. Bull Case

The investment debate over Charter Communications crystallizes around a fundamental question: Is this an irreplaceable infrastructure monopoly generating predictable cash flows, or a melting ice cube facing technological obsolescence? The bulls see a toll road for the digital age; the bears see the next Blockbuster Video. Both sides marshal compelling evidence, and the truth likely contains elements of each narrative.

Bull Case: The Infrastructure Imperative

"Show me another way to deliver gigabit speeds to 50 million American homes without spending $500 billion," challenges a Charter board member privately. This is the bulls' core argument: Charter's hybrid fiber-coaxial network, built over 40 years and impossible to replicate economically, represents irreplaceable infrastructure in an increasingly connected world.

The last-mile advantage is profound. Charter's cables pass 57 million homes and businesses. To replicate this network with fiber would cost $1,000-$2,000 per home passed—roughly $60-120 billion. Even mighty AT&T and Verizon have largely abandoned wholesale fiber overbuilds, focusing instead on selective deployments. The physics and economics of running fiber to every suburban and rural home remain daunting. Charter's existing infrastructure, already amortized, can be upgraded to multi-gigabit speeds for a fraction of new-build costs.

Scale benefits in programming negotiations, while declining in importance as video shrinks, remain material. Charter's 12 million remaining video subscribers still provide leverage in retransmission consent negotiations with broadcasters. More importantly, the company's scale in broadband—30 million subscribers—creates negotiating power with streaming services eager for distribution and reduced churn. The bundling deals with Disney+, Paramount+, and others wouldn't exist without Charter's reach.

Broadband penetration continues growing, albeit slowly. Despite the narrative of market saturation, Charter adds 1-2 million new homes passed annually through edge-outs and new construction. Rural broadband initiatives, funded by government subsidies, open previously uneconomic territories. The work-from-home revolution made high-speed internet essential rather than optional. Households that once shared 25 Mbps now demand 500 Mbps or more as multiple family members video conference simultaneously.

Capital allocation has transformed under current management. The Rutledge era's aggressive capital spending is moderating. Network upgrades are largely complete. The company generates $8+ billion in annual free cash flow, returning most to shareholders through buybacks. With the stock trading at historic low multiples—often below 8x EBITDA—buybacks are massively accretive. Charter has reduced share count by 40% since 2016, dramatically increasing per-share value even with modest total growth.

The mobile convergence opportunity remains early innings. Spectrum Mobile's 10 million lines generate minimal profit today but represent tomorrow's growth engine. As 5G enables true fixed-mobile convergence, Charter can offer integrated connectivity solutions no pure-play wireless or wireline provider can match. The recent T-Mobile MVNO agreement for business customers opens new markets. Bundling reduces churn, increases ARPU, and creates competitive moats.

Bear Case: The Disruption Avalanche

"Charter is fighting yesterday's war with yesterday's weapons," argues a prominent short seller. The bear case rests on accelerating technological and competitive disruption that will erode Charter's monopoly power faster than investors expect.

Cord-cutting acceleration is relentless and profitable video may never return. Charter loses 300,000 video subscribers quarterly, accelerating each year. Video revenues declined from $17 billion to $11 billion in five years. The company essentially gives away video service at cost, destroying what was once a 40% margin business. Streaming unbundling has permanently broken the cable TV model. Younger consumers will never subscribe to traditional cable, viewing it as their parents' technology.

Fiber overbuilds from telcos represent existential threats in key markets. AT&T and Frontier are deploying fiber aggressively in Charter's footprint. Where fiber exists, Charter loses 30-40% market share over time. Fiber offers symmetrical speeds (equal upload/download) that cable's DOCSIS technology cannot match. For work-from-home professionals and content creators, fiber's technical superiority is decisive. Cherry-picking Charter's most profitable dense markets, fiber overbuilders destroy the economics of cable's geographic monopoly.

5G fixed wireless competition is more formidable than expected. Verizon and T-Mobile have collectively added 5 million fixed wireless subscribers in three years, mostly taken from cable. While current 5G speeds lag cable, the technology improves rapidly. For price-conscious consumers, "good enough" 100 Mbps 5G at $30 monthly beats Charter's 300 Mbps at $60. The wireless companies can undercut cable pricing because home broadband uses excess network capacity, generating nearly 100% incremental margins.

Regulatory overhang threatens both operations and economics. The New York battles demonstrated regulatory vulnerability—states can effectively confiscate the business through impossible conditions. Net neutrality regulations could return, limiting pricing flexibility and network management. Franchise fees and taxes consume 5-7% of revenue and continue rising. Political pressure for broadband price regulation intensifies as internet becomes essential utility. The Biden administration's emphasis on broadband competition and affordability creates constant regulatory uncertainty.

High debt levels remain despite deleveraging. Charter carries $95 billion in debt, generating $5 billion in annual interest expense. Rising rates increased interest costs by $500 million annually. While leverage ratios improved, absolute debt levels constrain flexibility. In a recession, with customers trading down or disconnecting service, fixed interest costs could quickly pressure cash flow. The investment-grade rating hangs by a thread; any downgrade would increase borrowing costs materially.

Customer satisfaction challenges persist despite improvements. Charter's American Customer Satisfaction Index score, while improved, remains below industry averages. Social media amplifies every service failure. Younger consumers expect Netflix-level user experience from their internet provider. The company's reputation, damaged during the TWC integration, hasn't fully recovered. In competitive markets, poor customer perception translates directly to share loss.

The Balanced Reality

The truth likely lies between these extremes. Charter's infrastructure has enduring value but faces unprecedented competition. The company will likely remain highly cash-generative but struggle to grow. The broadband business appears defensible in most markets but vulnerable in others. Mobile provides growth but at lower margins than traditional cable services.

Key variables to watch: fiber overbuild pace (accelerating or moderating?), 5G fixed wireless quality (improving or plateauing?), regulatory actions (punitive or manageable?), and capital allocation (value-creating buybacks or desperate acquisitions?). The difference between Charter as a melting ice cube and a cash-flow machine may ultimately depend on management's ability to navigate these challenges while maintaining operational excellence and financial discipline.

For investors, Charter represents a complex bet on American infrastructure, technological evolution, and management execution. The asymmetry is striking: bears see 50% downside as competition erodes the monopoly; bulls see 100% upside as the market recognizes infrastructure value. Both cannot be right, but both could be wrong if Charter transforms into something entirely different—neither traditional cable company nor pure broadband provider, but a new form of integrated connectivity platform for the 5G age.

X. Epilogue & "What Would We Do?"

Standing in Charter's Stamford headquarters, you can see Long Island Sound stretching toward the horizon—the same view John Malone contemplated when orchestrating the TWC acquisition. The cable industry's future seems equally vast and uncertain. Charter has traveled from a rural Michigan system to America's connectivity backbone, through bankruptcy and transformation, to arrive at an inflection point that will define its next chapter. The question isn't what Charter was or is, but what it must become.

The Future of Cable: Infrastructure Play or Obsolescence?

The binary framing—infrastructure versus obsolescence—misses the nuanced reality. Cable systems are evolving into something unprecedented: hybrid networks that blur the distinction between fixed and mobile, content and connectivity, service provider and platform. Charter's coaxial cables, once carrying analog TV signals, now support 10 gigabit data speeds. The same infrastructure that delivered "I Love Lucy" now enables remote surgery and virtual reality.

The evolution to DOCSIS 4.0 and eventual DOCSIS 5.0 will push speeds to 25+ gigabits, matching and exceeding fiber capabilities. But speed alone won't determine winners. The future belongs to companies that seamlessly integrate multiple access technologies—cable, fiber, 5G, satellite—into unified service offerings. Charter's challenge is transforming from a cable company that offers mobile to a connectivity platform that uses whatever technology best serves each use case.

Convergence Strategies: Fixed-Mobile, Enterprise, Edge Computing

If we ran Charter tomorrow, the strategic priority would be clear: accelerate convergence across every dimension. Fixed-mobile convergence isn't just bundling home internet with cell phones—it's creating services that dynamically shift between networks based on availability, speed, and cost. Imagine your device seamlessly moving from home WiFi to CBRS private networks to macro cellular without interruption, always choosing the optimal connection.

The enterprise opportunity remains vastly underpenetrated. Charter generates less than 10% of revenue from business services while commanding infrastructure in every major business district. Small and medium businesses need more than internet access—they need integrated communications, cloud connectivity, security, and managed services. Charter should aggressively build or acquire enterprise capabilities, following Comcast's successful business services playbook but moving faster and thinking bigger.

Edge computing represents the next frontier. Charter's 200,000+ network nodes could host distributed computing resources, bringing processing power closer to end users. This positions Charter to capture value from augmented reality, autonomous vehicles, and IoT applications that require ultra-low latency. Why let Amazon or Microsoft own the edge when Charter controls the physical infrastructure? The company should partner with or acquire edge computing capabilities immediately.

International Expansion Possibilities

Charter's domestic focus, while historically appropriate, may be strategically limiting. Liberty Global's European success demonstrates that cable consolidation opportunities exist globally. Markets like Mexico, Brazil, and India have fragmented cable industries ripe for consolidation. Charter's operational expertise, particularly in network upgrades and customer service transformation, could create enormous value in underdeveloped markets.

But international expansion should follow a different model than traditional M&A. Partner with local operators, provide technology and expertise in exchange for equity stakes, and build asset-light management agreements. This capital-efficient approach reduces risk while capturing upside from operational improvements. Think of it as exporting the Charter playbook rather than the Charter balance sheet.

The Next Wave of Consolidation?

Domestic consolidation isn't finished. Charter and Comcast together serve 75 million customers but in largely non-overlapping territories. A merger seems impossible today given regulatory barriers, but industry dynamics may force reconsideration. As national 5G providers and global technology platforms increase competitive pressure, regulators may recognize that regional cable monopolies need national scale to compete effectively.

More likely is creative quasi-consolidation through deeper partnerships. The Comcast-Charter mobile partnership hints at possibilities: joint purchasing, shared technology development, coordinated spectrum strategies. Extended to other areas—streaming aggregation, enterprise services, edge computing—such partnerships could capture consolidation benefits without regulatory friction. The future may not be one giant cable company but allied regional giants operating as a virtual national platform.

Key Lessons for Entrepreneurs and Investors

Charter's journey from startup to giant offers timeless lessons that transcend industry:

First, leverage is rocket fuel that burns both ways. Paul Allen's billions couldn't overcome bad leverage; Tom Rutledge's operational excellence meant nothing without balance sheet repair. In capital-intensive industries, the cost of capital often matters more than operational efficiency. Entrepreneurs should think of leverage not as a growth accelerator but as a risk amplifier that must be carefully calibrated to cash flow stability.

Second, timing beats brilliance. Charter succeeded not by being smarter but by buying when others were selling and waiting when others were buying. The same assets that bankrupted Allen made Rutledge successful—purchased at different prices under different conditions. For investors, patience and price discipline matter more than strategic vision.

Third, physical infrastructure creates enduring value even as business models evolve. Charter's cables have carried analog TV, digital TV, internet, and now mobile backhaul. The use cases changed; the infrastructure endured. Entrepreneurs should distinguish between temporary business models and permanent infrastructure, investing in the latter while remaining flexible on the former.

Fourth, operational excellence compounds quietly but powerfully. Charter's customer service improvements, network upgrades, and pricing simplification seem mundane compared to Allen's "Wired World" vision. Yet these boring operational improvements created billions in value while the grand vision destroyed billions. In mature industries, excellence in execution beats brilliance in strategy.

Finally, consolidation is destiny in scale industries. Every capital-intensive, network-effect business eventually consolidates to a handful of players. Fighting this gravity is futile; surfing the consolidation wave can be enormously profitable. Entrepreneurs should position for inevitable consolidation from day one, building with eventual integration in mind.

Final Reflections on Building Through Bankruptcy and Consolidation

Charter Communications stands as a monument to American financial capitalism—its possibilities and perils, its creative destruction and wealth creation. A company that emerged from rural Michigan to wire America for the digital age. That survived catastrophic overleveraging to become stronger. That transformed from three entrepreneurs' vision to a $100 billion enterprise serving 32 million customers.

But Charter's story isn't really about cable or technology or even money. It's about the relentless American impulse to build, to connect, to consolidate, to improve. It's about infrastructure as the physical manifestation of economic ambition. It's about how bankruptcy can be rebirth, how failure can precede success, how patient capital and operational excellence can transform industries.

Looking forward, Charter faces challenges that would terrify most management teams: technological disruption, regulatory pressure, competitive threats from every angle. Yet the company has survived and thrived through worse. The infrastructure endures. The cash flow continues. The consolidation opportunities remain.

What would we do if handed Charter's controls tomorrow? Think like an infrastructure company, not a cable company. Embrace every access technology. Accelerate convergence. Expand edge computing capabilities. Deepen enterprise penetration. Export the playbook internationally. Partner creatively with supposed competitors. And above all, remember that in connectivity, as in all infrastructure, the assets outlive the business models, the physical outlasts the financial, and patient operators ultimately defeat financial engineers.

Charter's next chapter remains unwritten, but its history provides the template: buy distressed assets, integrate relentlessly, manage leverage carefully, execute operationally, and trust that essential infrastructure creates value across cycles and through disruption. The company that emerged from bankruptcy to conquer cable may need to transform again—but transformation, not stability, has always been Charter's destiny.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube