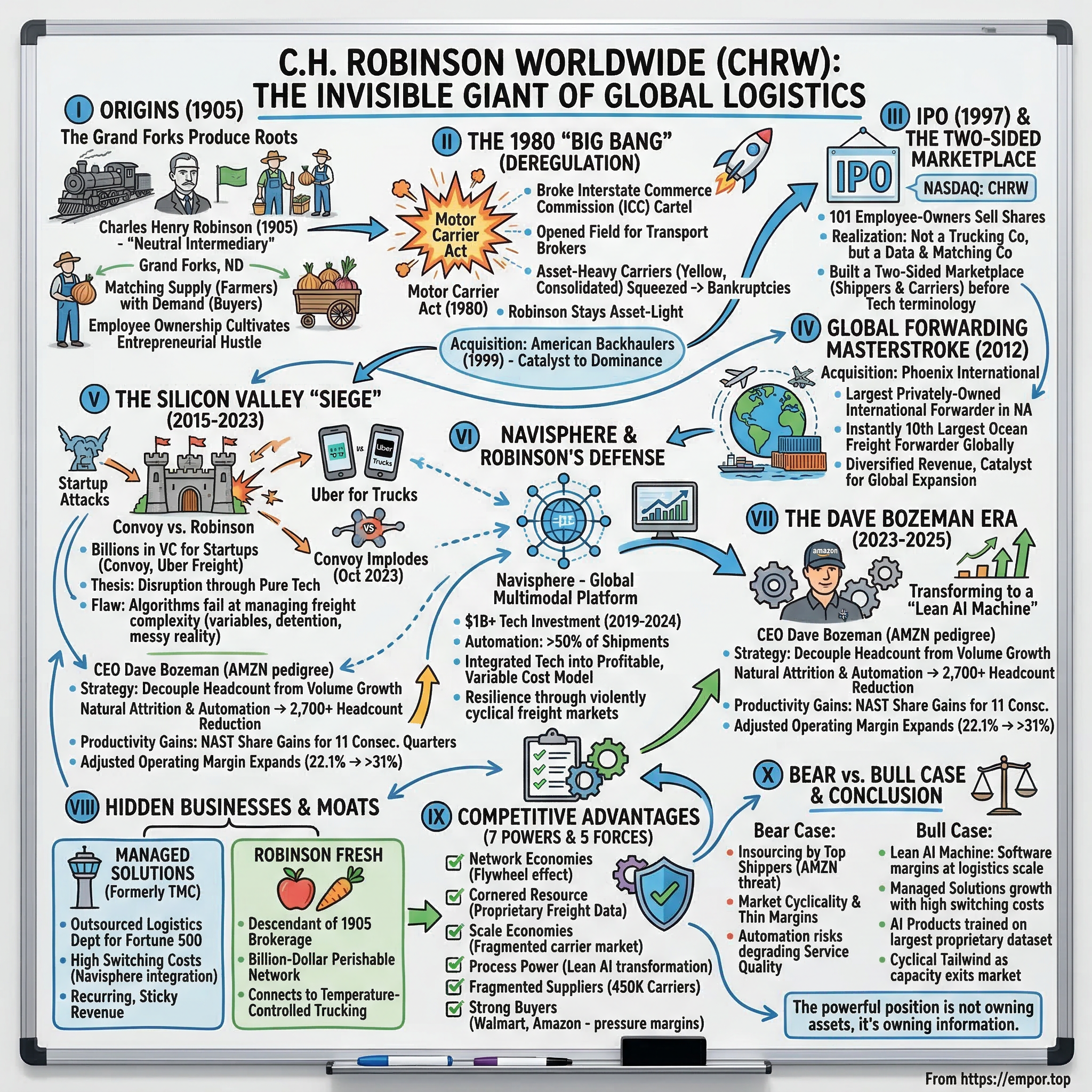

C.H. Robinson: The Invisible Giant of Global Logistics

I. Introduction and Episode Roadmap

What if you could run a multi-billion dollar trucking empire without owning a single truck? No depots. No diesel bills. No mechanics. No fleets parked in lots depreciating while you sleep. Just phones, data, relationships, and an almost supernatural ability to match someone who needs something moved with someone who can move it.

That is the story of C.H. Robinson Worldwide, ticker CHRW on the NASDAQ, the number one third-party logistics provider in North America. In fiscal year 2025, the company orchestrated the movement of roughly sixteen billion dollars worth of freight across the planet. It connected approximately 83,000 shippers with a network of 450,000 contract carriers. It managed truckload, less-than-truckload, ocean, air, and intermodal shipments spanning six continents. And it did all of this while employing around 13,000 people and owning essentially zero trucks, zero ships, and zero planes.

The "asset-light" model is one of the most counterintuitive business strategies in industrial America. When the economy booms and freight rates surge, Robinson earns fatter spreads on every load. When the economy craters and capacity goes slack, Robinson's costs fall faster than its revenues because it has no fixed fleet to feed. It is the rare business that bends but does not break regardless of where the cycle turns. In 2022, at the peak of the post-pandemic freight supercycle, Robinson generated nearly $25 billion in revenue and $1.27 billion in operating income. By 2023, that same freight market had cratered, spot rates were down over twenty percent, and the business produced just $515 million in operating income. Many asset-heavy carriers laid off thousands. Robinson survived, adjusted, and by 2025 had pushed operating income back to nearly $800 million, not by growing revenue, but by ruthlessly cutting costs under a new CEO with an Amazonian pedigree.

This story spans three intertwined threads. First, the deregulation "Big Bang" of 1980 that created the modern freight brokerage industry from nothing. Second, the Silicon Valley "siege" of 2015 to 2023, when billions of venture capital dollars poured into startups promising to be the "Uber for Trucks," only to watch the most prominent of them implode. And third, the Dave Bozeman transformation, which began in mid-2023 and is turning Robinson from a people-intensive brokerage into what management calls a "Lean AI Machine." If that transformation succeeds, it could redefine what a logistics company looks like in the age of artificial intelligence.

But before any of that, there was a man in North Dakota, a wagon full of onions, and the simple insight that knowing where things are and where they need to go is worth more than actually hauling them.

II. Origins: The Grand Forks Produce Roots

Picture Grand Forks, North Dakota, in the first years of the twentieth century. The transcontinental railroad has just reached the territory, connecting the Red River Valley's fertile farmland to the great markets of Chicago and beyond. Settlers are pouring in. The Dakota Territory is producing grain, potatoes, onions, and sugar beets at a pace that outstrips the ability of local merchants to sell them. What these farmers desperately need is not another buyer standing at the loading dock, but someone who knows where the buyers are, hundreds of miles away, and can arrange the shipment before the produce spoils.

Enter Charles Henry Robinson. A native New Yorker and former traveling salesman from St. Louis, Robinson recognized the opportunity hiding in plain sight. In May 1905, he formed a partnership with Grand Forks-based Nash Brothers, the forerunner of Nash Finch Company and the leading wholesaler in North Dakota. The partnership was incorporated as C.H. Robinson Co., with Robinson named as the company's first president. The business model was deceptively simple: Robinson would act as a "neutral intermediary" between farmers and distant buyers. He never owned the produce. He never drove the wagons. He took a commission for solving the oldest problem in commerce, matching supply with demand across distance and time.

In the early 1900s, this was not a trivial problem. There were no centralized databases, no real-time pricing feeds, no GPS tracking. The information asymmetry was enormous. Knowing that a carload of onions was sitting in a warehouse in Grand Forks while a buyer in Chicago was scrambling for supply was the entire competitive advantage. Robinson's edge was not capital or machinery. It was knowledge, relationships, and hustle. That cultural DNA, the instinct to broker rather than own, to intermediate rather than operate, would become the defining characteristic of the company for the next 121 years.

The colorful local folklore claims Robinson himself "sold out a couple of years later and ran off with Annie Oakley, the showgirl shootist of Buffalo Bill Cody's Wild West Show fame," supposedly dying around 1909. Whether or not the legend holds water, the company outlived its founder by more than a century. By 1913, the Robinson-Nash partnership had dissolved, with Nash Finch principals becoming sole owners. Branch offices sprouted across Minnesota, Iowa, Wisconsin, Illinois, and Texas. When a fire struck Grand Forks, the headquarters moved to Minneapolis around 1918, planting the company in what would become one of America's great logistics corridors.

For the next sixty years, C.H. Robinson operated as a regional produce brokerage, steadily expanding its network of growers, buyers, and transportation contacts. By 1976, the Nash Finch shareholders had been bought out, and the company became one hundred percent employee-owned. This employee ownership model created a deeply entrepreneurial culture. Every broker was an owner. Every commission check was a dividend. The hustle was not abstract corporate strategy. It was personal.

What mattered most about this long, quiet period was not any single deal or expansion. It was the culture it cemented. Robinson bred a generation of brokers who thought in terms of high-frequency transactions, thin margins, and volume. A produce broker might handle dozens of calls a day, each one a mini-negotiation. Speed, accuracy, and relationship management were everything. When the trucking industry deregulated in 1980 and suddenly millions of new freight transactions needed intermediaries, Robinson's people were already wired for exactly that kind of work. The produce roots were not a quaint origin story. They were the training ground for what came next.

III. The 1980 "Big Bang": Motor Carrier Act

On July 1, 1980, President Jimmy Carter signed the Motor Carrier Act into law, and the American trucking industry changed overnight. Before that date, the industry was effectively a regulated cartel. The Interstate Commerce Commission, operating under the Motor Carrier Act of 1935, controlled virtually every aspect of interstate trucking. Rate bureaus, groups of carriers organized by region, collected cost data, developed tariff schedules, and submitted them to the ICC for approval. Carriers could not freely enter new markets. They could not serve new routes without government permission. They could not meaningfully compete on price. The 1948 Reed-Bulwinkle Act had even exempted carriers from antitrust laws, allowing them to fix rates in concert. It was, by design, a system that rewarded scale, terminals, and union labor. The "Big Four" national less-than-truckload carriers, Yellow Freight, Roadway, ABF Freight, and Consolidated Freightways, dominated this cozy world.

The Motor Carrier Act of 1980 blew it all up. The legislation removed most rate-making authority from rate bureaus, eliminated restrictions on what commodities carriers could haul, and deregulated the routes and geographic regions carriers could serve. Most critically for Robinson's future, it opened the field for transport brokers. For the first time, anyone with a phone, a license, and a Rolodex could legally arrange the movement of freight without owning a single truck.

The reaction of the legacy carriers was predictable. Companies like Yellow Freight and Consolidated Freightways had built their empires on an asset-heavy model: enormous terminal networks, thousands of company-owned trucks, union workforces governed by Teamsters contracts. Deregulation unleashed a wave of nonunion competitors with lower cost structures, and the old guard found itself squeezed. Consolidated Freightways filed for bankruptcy in 2002, costing 15,500 employees their jobs and shuttering a two-billion-dollar operation. Yellow Corporation limped along for two more decades before filing for bankruptcy in August 2023, the largest trucking bankruptcy in American history, affecting 30,000 workers. The asset-heavy model, which had seemed impregnable under regulation, became a millstone in the deregulated era.

Robinson's response was the opposite. The company stayed asset-light. Rather than buying trucks and building terminals to compete head-on with the legacy carriers, Robinson leveraged its brokerage DNA. The same skills that had made it effective at matching produce growers with buyers were perfectly suited to matching shippers with carriers in the newly deregulated market. If it fits in a trailer, Robinson could broker it. The transition from produce to "everything" was not a strategic pivot. It was a natural extension of what the company already knew how to do.

A pivotal catalyst came in 1999, when Robinson acquired American Backhaulers for approximately $136 million in cash and stock. American Backhaulers had been one of the first dedicated freight brokerages to emerge after deregulation, commencing operations in 1981. With 5,700 customers and 525 employees, it gave Robinson an immediate step-change in truckload brokerage scale. Industry veterans later acknowledged that this acquisition catalyzed Robinson's transformation into the dominant freight broker in North America.

By the time Robinson went public on October 15, 1997, listing on the NASDAQ under ticker CHRW, the company had already evolved far beyond its produce roots. The IPO raised $190 million, largely for the 101 employee-owners who sold their shares, and valued the company at approximately $743 million. Gross revenues stood at $1.79 billion and net revenues at $206 million, growing at fifteen percent annually. At 3.6 times net revenue, the market was assigning a premium to what it recognized as a rare animal: a capital-light, high-return-on-equity logistics platform disguised as a shipping company.

What the IPO crystallized was a revelation that Robinson's leadership had understood for years but that Wall Street was only beginning to grasp. Robinson was not really a trucking company. It was a data and matching company. Its competitive advantage was not rolling stock or terminal real estate. It was the accumulated intelligence of millions of transactions, the knowledge of which lanes were tight, which carriers were reliable, which routes were profitable, and which shippers could be trusted to pay on time. In the language of modern tech, Robinson had built a two-sided marketplace long before anyone in Silicon Valley had coined the term.

IV. The M&A Masterstroke: Phoenix International

By 2012, C.H. Robinson was the undisputed king of North American freight brokerage. Its domestic truckload and LTL operations hummed with the efficiency of a machine that had been refined over decades. But outside the borders of the United States, the company was a different story. In the world of global ocean and air forwarding, where containers cross oceans and pallets fly between continents, Robinson was a marginal player. Its existing Global Forwarding division generated roughly $114 million in annual net revenue, a rounding error in a market dominated by European giants like Kuehne+Nagel, DHL, and DB Schenker. If Robinson wanted to be a true global logistics platform, it needed to buy its way in.

On September 25, 2012, Robinson announced the acquisition of Phoenix International, the largest privately-owned international freight forwarder, non-vessel operating common carrier, and customs broker headquartered in North America. Based in Wood Dale, Illinois, near Chicago, Phoenix had built a formidable operation: 2,000 employees across 76 offices in 15 countries, 15,000 global customers, and approximately 250,000 twenty-foot equivalent units of ocean freight in 2011, with seventy-two percent concentrated on the lucrative transpacific trade lanes. Its revenue split roughly sixty percent ocean freight, twenty percent air freight, and twenty percent customs clearance.

The price was $635 million, split ninety percent cash and ten percent newly issued Robinson stock. Against Phoenix's trailing EBITDA of approximately $50 million, that worked out to roughly 12.5 times, a rich multiple by the standards of freight forwarding acquisitions. At the time, critics questioned whether Robinson was overpaying. Phoenix's gross revenues were around $807 million with net revenues of $161 million, but its adjusted operating income was only about $48 million. For a company that had grown almost entirely organically, spending $635 million on a single deal, the largest in its 107-year history, was a bold departure.

The strategic logic, however, was compelling. This was a classic "buy versus build" decision, and building a global forwarding operation from scratch would have taken years and carried even greater risk. Phoenix's forwarding division generated more net revenue than Robinson's entire existing forwarding operation. Overnight, the acquisition made Robinson the tenth largest ocean freight forwarder globally and provided the "nucleus" for what would eventually grow into a segment contributing roughly thirty percent of the company's adjusted gross profit.

The integration was not without friction. Merging two distinct cultures, Robinson's scrappy Midwestern brokerage ethos with Phoenix's internationally oriented forwarding expertise, required patience. But the timing proved prescient. When the "freight recessions" of the late 2010s hammered domestic truckload rates, Robinson's newly diversified revenue base provided a cushion. Global Forwarding revenues surged during the pandemic-era supply chain chaos, reaching $6.8 billion in 2022 as ocean freight rates exploded to historic highs. What had looked like an overpayment in 2012 looked like theft a decade later.

The Phoenix acquisition also gave Robinson something less tangible but equally important: credibility with multinational shippers. A Fortune 500 company shipping containers from Shanghai to Chicago wants a single provider that can manage the ocean crossing, clear customs, arrange drayage from the port, and deliver via truck to the final destination. Before Phoenix, Robinson could only offer the last leg. After Phoenix, it could offer door-to-door. That capability became the foundation for Robinson's Managed Solutions business, which we will explore shortly, and fundamentally changed the company's value proposition from "domestic broker" to "global logistics partner."

The deal closed in the fourth quarter of 2012, and Robinson used existing cash and a new revolving credit facility to fund it. In the years that followed, the Global Forwarding segment became Robinson's primary growth engine for international expansion, with non-US revenues climbing from $1.4 billion in 2016 to $2.9 billion by 2024. The bet on Phoenix was a watershed moment, the point where Robinson stopped being a North American specialist and started becoming a global platform.

V. The Silicon Valley "Siege": Convoy vs. Robinson

In October 2015, a startup called Convoy launched in Seattle with a premise so intuitive it seemed inevitable: apply the ride-sharing model to trucking. Just as Uber had matched riders with drivers through an app, Convoy would match shippers with truckers, cutting out the traditional broker and replacing human negotiation with algorithms. The founding team came from Amazon. The backers read like a who's who of West Coast capitalism: Jeff Bezos, Bill Gates, the venture arms of Alphabet and Salesforce, and Al Gore's Generation Investment Management. By the time the dust settled, Convoy had raised approximately $828 million across multiple funding rounds, reaching a peak valuation of $3.8 billion in April 2022.

Convoy was not alone. Uber Freight, launched in 2017, attacked the same opportunity. So did Transfix, Loadsmart, and a dozen smaller players. The collective thesis was straightforward: the freight brokerage industry was antiquated, relationship-dependent, and ripe for technological disruption. Robinson's army of human brokers, sitting in cubicles making phone calls, was a dinosaur waiting for the asteroid. The future was algorithmic matching, dynamic pricing, and zero human intervention.

For a while, the narrative was compelling. Venture capitalists poured billions into digital freight brokerages. Convoy's Series D in November 2019 raised $400 million and valued the company at $2.75 billion. Its Series E in April 2022 pushed that to $3.8 billion with another $160 million, plus $100 million in venture debt. At its peak, Convoy employed roughly 1,500 people and was rapidly scaling its transaction volume.

But the "disruption" thesis contained a fatal flaw that the freight market would brutally expose. The digital-only brokers had built their businesses during one of the most favorable freight markets in history. From 2020 through early 2022, pandemic-fueled demand, port congestion, and driver shortages sent spot freight rates to record levels. In that environment, almost any broker, digital or traditional, could make money. The real test would come when the cycle turned.

It turned savagely. By mid-2022, freight rates began collapsing. Spot truckload rates fell over twenty percent from their peaks. Contract rates declined fifteen percent. The flood of new carrier capacity that had entered the market during the boom, attracted by high rates, suddenly found itself chasing shrinking demand. For Convoy, the math became lethal. The company was burning venture capital to subsidize below-market rates, a customer acquisition strategy that only works if the funding spigot remains open. When the Federal Reserve's aggressive monetary tightening simultaneously dried up the venture capital market, Convoy was caught in what CEO Dan Lewis later called "the perfect storm."

On October 19, 2023, Convoy ceased operations. There was no formal bankruptcy filing, no restructuring. Lewis simply sent employees a memo: "Today is your last day at the company." A four-month search for an acquirer had failed. Staff had already been whittled from 1,500 to roughly 500. Eight hundred million dollars in venture capital had evaporated.

The failure illuminated a fundamental misunderstanding about freight brokerage. Matching a shipper with a carrier is not like matching a rider with a driver. A truckload shipment involves dozens of variables: commodity type, weight, lane characteristics, detention risk, payment terms, insurance requirements, seasonal capacity fluctuations, and the ever-present possibility that something will go wrong in transit. When it does go wrong, someone needs to pick up the phone and solve the problem. Algorithms are excellent at optimization. They are less effective at managing the messy, relationship-intensive reality of moving physical goods across a continent. Robinson's human brokers, augmented by technology, proved more resilient than the pure-tech approach.

Meanwhile, Robinson had not been standing still. The company's response to the Silicon Valley siege was not to dismiss the threat but to absorb it. Starting in 2019, Robinson committed to spending $1 billion over five years on technology, with roughly eighty percent allocated to new capabilities and twenty percent to infrastructure. The crown jewel of this investment was Navisphere, a global multimodal transportation management platform originally launched in November 2012 and continuously enhanced since. By 2025, Navisphere processed over 55 million digital transactions monthly. More than fifty percent of Robinson's shipments were fully automated, and over seventy-five percent of customer interactions occurred digitally.

The critical difference between Robinson's technology strategy and Convoy's was the business model underneath. Robinson invested in technology while maintaining profitability and a variable cost structure. When freight volumes dropped, Robinson's costs dropped with them because its carrier payments were variable. Convoy, funded by venture capital, had fixed costs (employee salaries, office leases, technology infrastructure) that did not flex with the cycle. It was the classic mismatch of fixed costs against cyclical revenue, and the freight cycle showed no mercy.

Uber Freight suffered its own version of this reckoning. Through 2023 and into 2024, the division conducted multiple rounds of layoffs, with EBITDA losses widening as revenue declined. Shippers reportedly departed due to inconsistent service quality, a recurring theme among purely digital brokers that lacked Robinson's depth of carrier relationships and institutional knowledge.

The Convoy implosion was more than a single company's failure. It was a vindication of Robinson's counter-positioning strategy. Robinson had taken the best ideas from the digital upstarts, automated matching, dynamic pricing, real-time visibility, and embedded them within a proven operational framework that had survived every freight cycle since deregulation. The tech bros came for the freight industry, and the freight industry said, "welcome to trucking."

VI. The "New" Guard: The Dave Bozeman Era

In the summer of 2022, an activist investment firm called Ancora Holdings Group began circling C.H. Robinson. Ancora's thesis was blunt: Robinson was fat, undermanaged, and technologically behind despite its billion-dollar tech pledge. The company's operating margins had compressed. Headcount had grown faster than revenue. The activist argued for a tech-first CEO, operational discipline, and potentially divesting non-core international assets.

Ancora won two board seats, and the pressure proved irresistible. CEO Scott Anderson, who had led the company since 2019, stepped down. The board launched a search for a leader who could bring the operational intensity of Big Tech to a 118-year-old logistics company. On June 26, 2023, they found their answer in Dave Bozeman.

Bozeman's resume reads like a masterclass in operational excellence across multiple industries. He spent sixteen years at Harley-Davidson beginning in 1992, working his way up through manufacturing and operations. He then moved to Caterpillar from 2008 to 2016, rising to Senior Vice President of Enterprise Systems. But the defining chapter of his career was his stint at Amazon from 2017 to 2022, where he served as Vice President of Amazon Transportation Services. In that role, Bozeman built and scaled Amazon's middle-mile global transportation network, encompassing ground, air, over-the-road, digital freight shipping, and small parcel operations. He was, in essence, building from within Amazon the kind of logistics machine that Robinson had spent a century assembling from the outside. Before joining Robinson, he had a brief stint at Ford Motor Company as Vice President of the Customer Service Division.

The hire sent an unmistakable signal to Wall Street. Robinson was not looking for a custodial manager to keep the trains running. It was importing Amazonian operational DNA, the relentless focus on automation, the obsession with removing "touches" from every process, the willingness to restructure ruthlessly in pursuit of efficiency. Bozeman's compensation structure reflected the urgency of the mandate. His base salary was set at $1 million, but approximately eighty-nine percent of his total compensation, which came to roughly $8.8 million, was performance-based, tied to stock options, restricted stock units, and performance share units keyed specifically to adjusted operating margin expansion and operating leverage improvement.

Translation: Bozeman gets paid to remove human labor from the shipment process and to make every dollar of gross profit flow more efficiently to the operating income line. If he fails to expand margins and demonstrate that Robinson can grow volume without proportionally growing headcount, his compensation shrinks dramatically.

Bozeman moved fast. In his first full year, he initiated what he called the "Lean AI" transformation. The numbers tell the story with startling clarity. When Bozeman took over in the third quarter of 2023, Robinson had 15,577 total employees. By mid-2025, that number had fallen to 12,858, a reduction of roughly 2,700 people, or 17.4 percent. Critically, these reductions came largely through natural attrition, leveraging the industry's naturally high turnover rates in the low-to-mid teens, rather than mass layoffs. Bozeman's philosophy, repeated on every earnings call, was simple: "decouple headcount from volume growth."

The productivity gains were striking. In the North American Surface Transportation segment, headcount fell from 6,278 to 5,283 employees, a 15.8 percent decrease, while truckload volume grew and market share expanded for eleven consecutive quarters. The company automated between 250 and 500 hours of manual tasks daily. By the fourth quarter of 2025, Robinson had deployed over thirty proprietary AI agents handling tasks that once required human intervention, from LTL freight classification to carrier communication. A new LTL pickup optimization agent reduced return-trip pickups by forty-two percent and automated ninety-five percent of related quality checks.

The financial impact was immediate. Adjusted operating margin expanded from 22.1 percent in 2023 to 28.1 percent in 2024, a 600 basis-point leap, and continued climbing to over 31 percent in the third quarter of 2025. Operating income rose from $515 million in 2023 to $795 million in 2025, even as total revenue actually declined from $17.6 billion to $16.2 billion, a testament to the power of operating leverage in a business where gross profit margins are naturally thin. Robinson was making more money on less revenue, the hallmark of a genuine efficiency transformation.

Bozeman also executed on Ancora's divestiture demands. In the summer of 2024, Robinson sold its European Surface Transportation business, which served 6,500 shippers and 15,000 carriers, to German freight forwarder Sennder Technologies. The move allowed Robinson to focus its resources on the higher-margin North American and global forwarding markets where it held structural advantages.

The market noticed. Robinson's stock, which had languished below $90 during the depths of the freight recession in 2023, more than doubled, trading near $170 by early 2026 with a market capitalization of approximately $20 billion. Bozeman's personal stake, reported at over 190,000 shares, aligned his interests with shareholders in a way that few "hired gun" CEOs can claim.

VII. Hidden Businesses: The TMC and Navisphere Story

Behind the headlines about truckload brokerage and the Convoy rivalry, Robinson has been quietly building a business that may ultimately prove more valuable than its core brokerage operation. It is called Managed Solutions, formerly known as TMC, the Transportation Management Center, and it represents a fundamentally different model from transactional freight brokerage.

Here is the distinction, and it matters enormously. In traditional brokerage, Robinson arranges individual shipments. A shipper calls with a load, Robinson finds a carrier, takes a spread, and the transaction is complete. The relationship is inherently transactional and low-switching-cost. A shipper can call Robinson for one load and a competitor for the next. But in Managed Solutions, Robinson effectively becomes the client's logistics department. It installs its Navisphere technology platform, embeds dedicated logistics professionals, and manages the shipper's entire transportation operation end to end, across all modes, all carriers, and all geographies. Think of it as outsourcing your supply chain brain to Robinson.

TMC has operated since 1999, initially headquartered in Chicago with Global Control Tower locations in Amsterdam, Sao Paulo, Shanghai, and Wroclaw. The business managed over 10.4 million shipments and $3.1 billion in freight under management. Its clients are not small companies looking for spot coverage. They are Fortune 500 enterprises that need a partner to run their entire logistics infrastructure, providing savings of up to twenty-five percent on addressable supply chain costs.

In November 2024, Robinson rebranded the offering as "C.H. Robinson Managed Solutions," combining its transportation management system technology, third-party logistics managed transportation, and fourth-party logistics services under a single brand. The rebrand was not cosmetic. It signaled Robinson's strategic intent to compete directly with pure-play 4PL providers and TMS software companies by offering an integrated solution that neither category can match alone.

The strategic brilliance of Managed Solutions is its switching costs. Once Robinson's technology and people are embedded in a client's operation, the cost of ripping them out and replacing them with a competitor is enormous, not just financially, but operationally. Migration risk, data loss, retraining, and the inevitable disruption to daily logistics operations create what amounts to Fort Knox-level switching costs. This is sticky revenue in an industry where most revenue is anything but.

The technology platform at the heart of all this is Navisphere. Originally launched on November 19, 2012, Navisphere has evolved from a basic transportation management system into a comprehensive digital logistics ecosystem. It connects Robinson's 83,000 shippers and 450,000 contract carriers through a suite of integrated products: Navisphere Vision for supply chain visibility and optimization, Navisphere Carrier for carrier freight-finding and documentation, and Navisphere Driver for mobile stop updates and bill-of-lading management. In 2019, Robinson launched Freightquote by C.H. Robinson, a web portal specifically designed for small and medium businesses to get real-time rate comparisons and book shipments with a credit card.

The $1 billion technology investment pledged in 2019, with roughly eighty percent going to new capabilities and twenty percent to infrastructure, funded not just Navisphere enhancements but also Robinson Labs, an internal technology innovation incubator. By 2025, Robinson maintained a team of over 450 in-house engineers and data scientists, a number that had been deliberately optimized downward from a peak of over 1,000 as the company shifted from building foundational infrastructure to deploying AI agents that multiply the output of each engineer.

The data asset underlying Navisphere deserves special attention. Robinson sees more freight transactions across more lanes than virtually any other private entity in North America. That accumulated dataset, tens of millions of loads with associated pricing, timing, carrier performance, and lane-specific characteristics, is both a competitive moat and a product in its own right. Robinson sells visibility and analytics back to shippers through Navisphere, effectively monetizing its position as the central node in the North American freight network.

Then there is Robinson Fresh, the direct descendant of the 1905 produce brokerage that started it all. It remains a billion-dollar-plus business that buys, sells, and markets fresh fruits, vegetables, and perishable items sourced from a global network of growers across 36 countries. The operation maintains 10 million square feet of refrigerated storage, 7.5 million square feet of dry warehouse space, six managed service centers, and 175 distribution centers across North America. Robinson Fresh is the exclusive marketer of licensed brands including Mott's, Welch's, Tropicana, Green Giant Fresh, and Glory Foods, alongside proprietary brands like MelonUp and Rosemont Farms.

Robinson Fresh represents roughly five percent of the company's adjusted gross profit, contributing around $40 million per quarter, but its strategic value exceeds its financial weight. The produce business keeps Robinson deeply connected to the temperature-controlled trucking market, providing carrier volume and relationships that benefit the core brokerage. It also represents a capability that no digital freight startup could ever replicate: the institutional knowledge required to move perishable goods without breaking the cold chain. When Convoy's algorithms were optimizing for price and speed, Robinson's produce brokers were ensuring that a trailer of strawberries from California arrived in Chicago at precisely thirty-four degrees Fahrenheit. That kind of expertise does not fit neatly into a pitch deck.

VIII. Playbook: 7 Powers and 5 Forces

To understand whether Robinson's competitive advantages are durable or decaying, it helps to apply the two most rigorous frameworks in strategy analysis: Hamilton Helmer's 7 Powers and Michael Porter's 5 Forces.

Start with scale economies. Robinson's position as the number one 3PL in North America allows it to buy carrier capacity more cheaply than smaller competitors. When you are the largest buyer in a fragmented supplier market, you get better rates, better service, and better capacity access, particularly during tight markets when carriers prioritize their highest-volume relationships. The company's gross profit in 2025 was $1.36 billion, generated on $16.2 billion of revenue, implying that even small percentage improvements in carrier pricing or shipper rates cascade into meaningful profit gains given the enormous transaction volume.

The network economies are perhaps Robinson's most powerful structural advantage, and they function as a classic flywheel. More shippers using Robinson's platform generate more data on lanes, rates, and carrier performance. That data enables better matching algorithms, which in turn attract more carriers to the network because they get more loads and less deadhead. More carriers mean better coverage and lower prices for shippers, which attracts still more shippers. This flywheel has been spinning for over four decades, and the data advantage it has created is nearly impossible for a new entrant to replicate.

Robinson's cornered resource is its data. The company processes millions of freight transactions annually across every major lane in North America. It knows, with a precision that borders on omniscience, what the going rate is on the Dallas-to-Atlanta lane on a Tuesday in March, which carriers are reliable on that route, and how those rates will shift when a weather event disrupts capacity in the Southeast. This is not data that can be scraped from the internet or synthesized from public sources. It is accumulated through actual market participation, and it compounds over time. The more transactions Robinson handles, the more accurate its pricing models become, and the more value it can offer both shippers and carriers.

Switching costs present a nuanced picture. For a single transactional load, switching costs are essentially zero. A shipper can move a load with Robinson today and a competitor tomorrow. This is the industry's structural weakness and the reason gross margins in brokerage are persistently thin. However, for Managed Solutions clients, where Robinson's technology and personnel are embedded in the shipper's operations, switching costs are massive. The disparity between these two customer types is the central tension in Robinson's business model and the reason the Managed Solutions segment is so strategically important.

The process power element is emerging under Bozeman. His systematic elimination of manual touches, deployment of AI agents, and Lean operational methodology are creating a cost structure that competitors cannot easily replicate. This is not a technology advantage per se, since any company can buy similar AI tools. It is an organizational capability, the ability to integrate those tools into a complex, high-volume operation while maintaining service quality. That organizational process, honed across thousands of small improvements, constitutes genuine process power.

Now consider Porter's 5 Forces. The threat of new entrants has been meaningfully tested and found manageable. Silicon Valley's best effort to disrupt the industry, backed by nearly a billion dollars in venture capital and the most famous tech investors alive, ended in Convoy's shutdown and Uber Freight's retreat. The barrier is not technology. It is the combination of carrier relationships, shipper trust, data scale, and the operational complexity of actually moving freight reliably day after day. Supplier power is fragmented and weak. Robinson works with 450,000 contract carriers, and the North American trucking market is one of the most fragmented industries in the world. No single carrier has meaningful leverage over Robinson. On the other hand, buyer power is the persistent squeeze. Robinson's largest shippers, companies like Walmart, Amazon, and major consumer goods manufacturers, have enormous leverage and constantly pressure margins. The rivalry among existing competitors is intense, with XPO Logistics, Echo Global Logistics (acquired by Jordan Company), and numerous regional brokers competing aggressively. The threat of substitutes includes shippers insourcing their own brokerage operations, the Amazon threat that represents the most credible bear case.

What makes Robinson's position genuinely difficult to attack is the combination of these forces. Any competitor must simultaneously build carrier scale, shipper volume, data depth, technology capability, and operational expertise. Doing any one of these is straightforward. Doing all of them simultaneously, while remaining profitable through violent freight cycles, is the challenge that has defeated every challenger to date.

The two to three KPIs that matter most for tracking Robinson's ongoing performance are: first, adjusted operating margin, which captures the Bozeman transformation's progress in converting gross profit into operating income and reflects the efficiency gains from automation and headcount reduction. It moved from 22.1 percent in 2023 to 28.1 percent in 2024 and over 31 percent by mid-2025. Second, NAST truckload volume growth relative to the market, which measures whether Robinson is gaining or losing share independent of cycle effects, and which showed eleven consecutive quarters of share gains as of Q4 2025. These two metrics, margin expansion and relative volume growth, together tell you whether Robinson is becoming a better business or merely riding the cycle.

IX. Bear vs. Bull Case and Conclusion

The bear case for C.H. Robinson centers on a single, existential question: what happens if the largest shippers decide to cut out the middleman entirely?

Amazon already operates one of the most sophisticated logistics networks on earth. Walmart has invested billions in its own supply chain infrastructure. If either company, or a coalition of major shippers, decides to build an in-house brokerage operation for their external freight needs, Robinson loses some of its most valuable customers and gains a terrifying competitor. This is not a hypothetical. Amazon's freight brokerage arm has been steadily expanding, initially to handle its own overflow capacity, but with the infrastructure to serve third parties. The commoditization risk is real. If brokerage becomes a feature of a larger logistics platform rather than a standalone service, Robinson's core business could face secular margin compression.

Beyond insourcing, the bear case includes the persistent cyclicality of the freight market. Robinson's revenues swung from $24.7 billion in 2022 to $16.2 billion in 2025, a decline of over thirty percent. While the asset-light model protects the downside, it also limits the upside during booms when asset-heavy carriers with their own trucks capture the full margin rather than paying it to carriers. The thin gross margins in brokerage, roughly eight to nine percent of revenue, mean that even small pricing concessions from powerful buyers can dramatically impact profitability.

There is also the question of whether the Bozeman transformation has a ceiling. Removing 2,700 employees and automating hundreds of hours of daily tasks is impressive, but at some point, further headcount reductions risk degrading the service quality that differentiates Robinson from the digital brokers that failed. The produce business taught Robinson that freight is messy and relationships matter. If automation goes too far, the company risks losing the human expertise that its largest clients value most.

The bull case is equally compelling, and it begins with the "Lean AI Machine" thesis. If Bozeman achieves his productivity targets, reducing human touches by thirty percent or more across the shipment lifecycle, Robinson could begin to resemble a software-margin business operating at logistics-industry scale. Adjusted operating margins above thirty percent, sustained through the cycle, would place Robinson in a category occupied by very few industrial companies. The company generated $895 million in free cash flow in 2025 and returned over $650 million to shareholders through dividends and buybacks, demonstrating the cash generation power of the model even in a depressed freight market.

The Managed Solutions growth story provides the bull case's second pillar. As more companies seek to outsource logistics complexity to trusted partners, Robinson's integrated offering, Navisphere technology combined with dedicated operational expertise, positions it to capture a growing share of a total addressable market that dwarfs the transactional brokerage pool. Every Managed Solutions client represents years of embedded revenue with high switching costs, the kind of recurring relationship that commands premium multiples.

The data moat is the third pillar. Robinson's dataset of North American freight transactions is a living, growing asset that becomes more valuable with every load brokered. As AI capabilities improve, the ability to deploy models trained on the industry's largest proprietary dataset represents a compounding advantage. Robinson is not just using AI to cut costs. It is using its data to build AI products that no competitor can replicate, because no competitor has the data.

The freight market itself may provide a cyclical tailwind. The Cass Freight Shipment Index declined year-over-year for thirteen consecutive quarters through 2025, hitting its lowest fourth-quarter level since 2009. Freight markets are cyclical, and the longer the downturn persists, the more carrier capacity exits the market, setting the stage for the inevitable upturn. When that upturn arrives, Robinson's expanded margins and leaner cost structure could produce earnings power that the current valuation does not fully reflect.

Robinson carries a net debt-to-EBITDA ratio of approximately 1.65 times, conservative by any standard, and the quarterly dividend was recently raised to $0.63 per share, yielding roughly 1.5 percent. The balance sheet provides ample capacity for further share repurchases, bolt-on acquisitions, or technology investment.

The company today trades at roughly $170 per share with a market capitalization near $20 billion, a far cry from the $743 million IPO valuation of 1997, but a reflection of both the growth achieved and the market's confidence in the Bozeman transformation's trajectory.

X. Epilogue

C.H. Robinson enters 2026 at an inflection point. The freight market shows early signs of stabilization after one of the longest downturns in modern history. Dave Bozeman is eighteen months into a transformation that has already delivered measurable results in margin expansion, market share gains, and AI deployment. The question is no longer whether Robinson can survive the digital age. Convoy's ashes answered that. The question is whether Robinson can become the platform that defines the next era of logistics.

For founders and operators studying the asset-light model, Robinson's 121-year history offers a masterclass in counter-positioning. While competitors bought trucks, Robinson bought data. While startups burned venture capital to acquire customers, Robinson invested in technology while remaining profitable. While the industry consolidated around asset-heavy scale, Robinson proved that the most valuable asset in logistics is not a truck, a ship, or a warehouse. It is the knowledge of who needs what moved, where, when, and at what price.

Is C.H. Robinson a logistics company or a data company? The answer, as with most great businesses, is that the question itself reveals the moat. Robinson is both, and the inability to neatly categorize it is precisely what makes it so difficult to disrupt. The produce broker from Grand Forks, North Dakota, figured out something in 1905 that Silicon Valley spent $828 million learning in 2023: in a world of physical goods, the most powerful position is not owning the assets. It is owning the information.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube