Church & Dwight: The 178-Year-Old Startup That Built a CPG Empire

I. Cold Open & Episode Roadmap

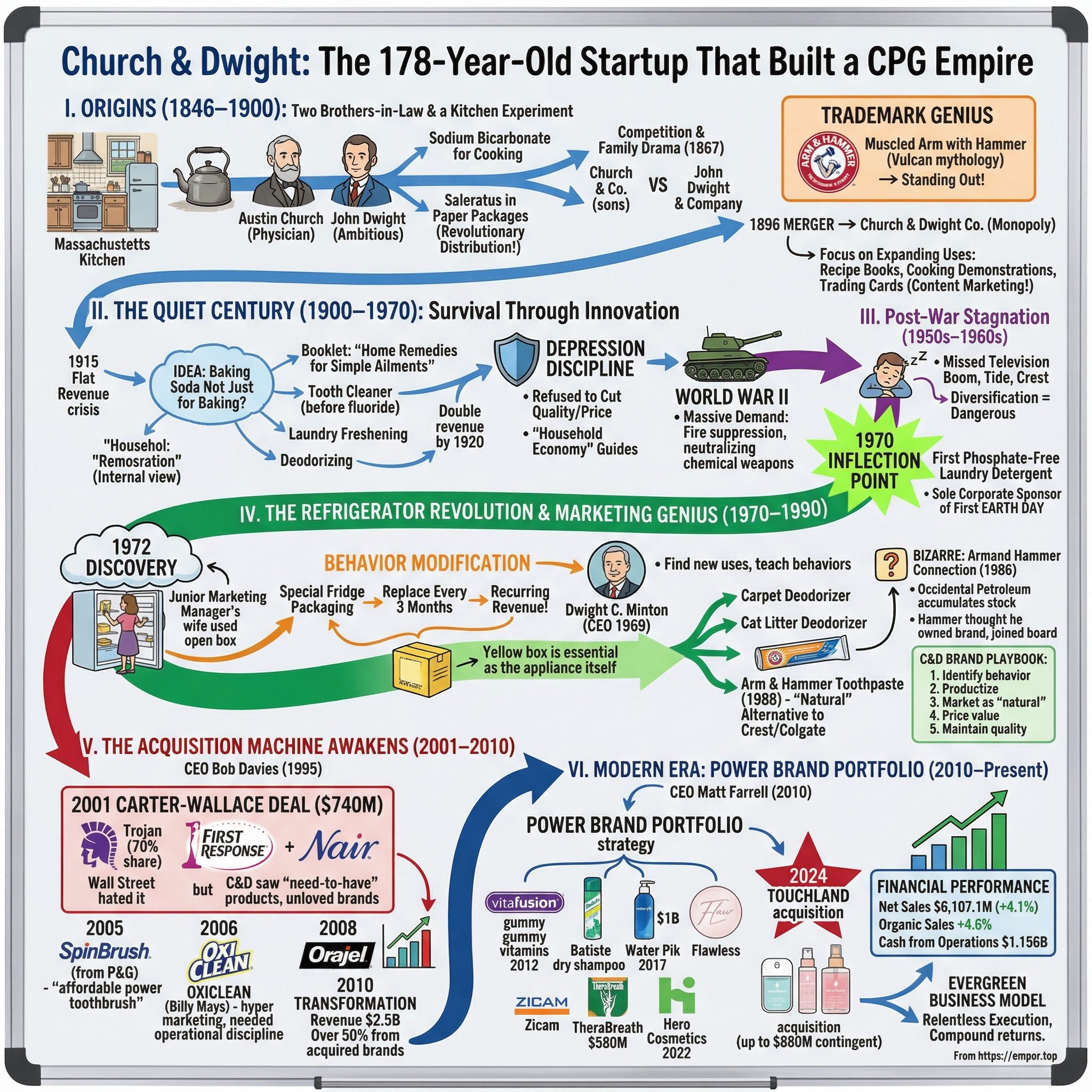

Picture this: A nondescript office park in Ewing, New Jersey, just outside Trenton. Inside, executives at a 178-year-old company are reviewing acquisition targets with the intensity of Silicon Valley venture capitalists. The conference room walls display brands that dominate American households—Arm & Hammer, OxiClean, Trojan, Waterpik. The CEO checks his phone for the latest quarterly numbers: another beat, another raise. The stock has quintupled over the past decade, crushing the S&P 500.

This is Church & Dwight—a company that started in 1846 with two brothers-in-law refining baking soda in a Massachusetts kitchen and has somehow transformed into a $25 billion market cap consumer products juggernaut. While Procter & Gamble and Unilever duke it out for headlines, this quiet giant has been methodically acquiring undervalued brands and turning them into cash machines. Added to the S&P 500 in 2016, it's one of the index's best-kept secrets.

The paradox is striking: How does a company older than the telephone maintain startup-like growth rates? How does a business built on sodium bicarbonate—literally baking soda—command premium valuations in 2024? And perhaps most intriguingly, how has a family-influenced firm maintained operational excellence while most dynastic companies have long since faded into irrelevance? This journey will take us from pre-Civil War America through the industrial revolution, two world wars, the consumer boom, and into today's hyper-competitive CPG landscape. We'll explore how Church & Dwight mastered the art of brand resurrection, turning tired names into billion-dollar franchises. We'll decode their acquisition playbook—one that Wall Street initially mocked but now studies religiously. And we'll examine how they've built what might be the most efficient marketing machine in consumer products.

Full year 2024 net sales increased 4.1% to $6,107.1 million, with organic sales increasing 4.6% due to higher volume of 3.3% and positive pricing and mix of 1.3%. The numbers tell a story of consistency that's almost boring—which, as we'll discover, is exactly the point. In a world obsessed with disruption, Church & Dwight has perfected the art of compound returns through methodical execution.

So buckle up. This isn't just a story about baking soda. It's about family feuds and reconciliations, marketing genius born from desperation, and how a company that once sold trading cards with its products became sophisticated enough to execute multi-billion-dollar leveraged buyouts. It's about the power of patience in an impatient world, and why sometimes the best businesses are hiding in plain sight—or in this case, in the back of your refrigerator.

II. Origins: Two Brothers-in-Law and a Kitchen Experiment (1846–1900)

The kitchen in John Dwight's Massachusetts home must have reeked of chemistry experiments gone wrong. It was 1846, and while the rest of America was preparing for war with Mexico, Dwight and his brother-in-law Austin Church were hunched over makeshift equipment, trying to refine a white powder that would change American households forever. They weren't trained chemists—Church was a physician who'd given up medicine, and Dwight was simply ambitious. But they'd stumbled onto something: a process to produce sodium bicarbonate pure enough for cooking.

The timing was perfect and terrible simultaneously. America was industrializing rapidly, cities were growing, and the middle class was emerging. But distribution was a nightmare—no railroads connected most towns, no refrigeration existed, and most Americans still bought goods from general stores that might restock once a season. Yet Dwight and Church saw opportunity where others saw obstacles. They started selling their "saleratus" (an early name for baking soda) in paper packages—revolutionary at a time when most goods were sold from bulk barrels.

By 1847, they formalized their partnership, creating John Dwight & Company. Church, ever the entrepreneur, wasn't satisfied with one venture. He moved to New York and started his own baking soda company, figuring the market was big enough for both. For two decades, the brothers-in-law competed as friendly rivals, each building distribution networks that crisscrossed the expanding nation.

Then came the family drama that would make a soap opera blush. In 1867, Church's sons—presumably tired of living in their father's shadow—formed Church & Co. to compete directly with both their father and uncle. Suddenly, three companies bearing variations of the same family names were battling for the same customers. The confusion was spectacular: retailers couldn't keep track of which Church or Dwight company they were ordering from, and customers had no brand loyalty when they couldn't distinguish between products.

The real stroke of genius came with the trademark. Church & Co. adopted the Arm & Hammer logo—a muscled arm wielding a hammer—which had nothing to do with baking soda but everything to do with standing out on crowded store shelves. The symbol came from the Vulcan mythology, representing power and industry. In an era before Madison Avenue, before focus groups, before brand consultants, the Church sons had intuited a fundamental truth: the logo mattered more than the name.

By the 1890s, the family competition had become destructive. Price wars eroded margins, duplicate distribution networks wasted capital, and larger food companies were beginning to eye the baking soda market. The families finally came to their senses. In 1896, John Dwight & Company and Church & Co. merged to form Church & Dwight Co., ending decades of internecine competition. Austin Church's original company remained independent, a reminder of the family's complicated history.

The merger was about more than ending family squabbles—it created America's first sodium bicarbonate monopoly. The combined company controlled virtually all baking soda production and distribution in the United States. They had pricing power, distribution dominance, and a brand—Arm & Hammer—that was becoming synonymous with the product itself.

But here's what made Church & Dwight different from other monopolists of the Gilded Age: they didn't gouge customers. Instead, they focused on expanding uses for their product. While John D. Rockefeller was building Standard Oil through predatory pricing and Andrew Carnegie was crushing competitors in steel, Church & Dwight was teaching Americans new ways to use baking soda. They published recipe books, sponsored cooking demonstrations, and even issued collectible trading cards—decades before baseball cards became popular.

The trading cards deserve special mention. Each box of Arm & Hammer contained beautifully illustrated cards featuring birds, flowers, or historical figures. Families collected and traded them, creating emotional connections to the brand that transcended the product's utility. It was content marketing before the term existed, building brand affinity one kitchen at a time.

As the 19th century closed, Church & Dwight had achieved something remarkable: they'd turned a commodity chemical into a branded consumer product. They controlled supply, dominated distribution, and most importantly, owned consumer mindshare. The Arm & Hammer logo was as recognizable as Coca-Cola's script or Campbell's red and white cans.

The foundation was set, but nobody could have predicted what would come next. The company that had built its fortune on a single product was about to discover that their real asset wasn't sodium bicarbonate—it was the trust of American consumers. That trust would carry them through world wars, depression, and technological disruption. But first, they had to survive the 20th century.

III. The Quiet Century: Survival Through Innovation (1900–1970)

The year 1915 should have been a disaster for Church & Dwight. The company's entire business model rested on one product for one use: baking soda for baking. But American eating habits were changing rapidly. Commercially produced bread was replacing home baking, and new chemical leavening agents were competing with traditional baking soda. Revenue was flatlining. The board was panicking.

That's when someone—history doesn't record who—had an audacious idea: What if baking soda wasn't just for baking?

The company published a modest booklet titled "Home Remedies for Simple Ailments," suggesting that Arm & Hammer could soothe upset stomachs, relieve insect bites, and dozen other medical uses. It was a massive gamble. In an era before FDA regulations, making health claims was common, but redirecting an entire brand's identity was unprecedented. The booklet wasn't just marketing; it was a manifesto declaring that sodium bicarbonate was a Swiss Army knife of household solutions.

The response was explosive. Within months, the company rushed to print updated versions promoting baking soda as a tooth cleaner—decades before fluoride toothpaste. Then came suggestions for laundry freshening, surface cleaning, and deodorizing. Each new use case opened entire markets. By 1920, Church & Dwight's revenues had doubled, not from finding new customers but from teaching existing customers new behaviors.

The formal incorporation as Church & Dwight Co. in 1925 marked a transition from family partnership to modern corporation. The timing seemed perfect—the Roaring Twenties were creating unprecedented consumer wealth, and advertising was becoming sophisticated. Radio networks could reach millions of households simultaneously. Department stores were revolutionizing retail.

Then came October 1929.

The Great Depression should have crushed Church & Dwight. Discretionary spending evaporated. Families who'd bought multiple boxes for different uses consolidated to one. Competitors slashed prices desperately. But Church & Dwight's response revealed the strategic discipline that would define them for decades: they refused to cut quality or prices. Instead, they doubled down on value messaging, teaching Depression-era families how a single box of Arm & Hammer could replace dozens of expensive specialty products.

Their Depression-era advertising is fascinating to study. While competitors promoted low prices, Church & Dwight published guides on "household economy"—showing how baking soda could extend the life of clothing, preserve food longer, and maintain hygiene without expensive products. They weren't selling baking soda; they were selling resourcefulness. The brand became associated with thrift and wisdom rather than deprivation.

World War II brought unexpected opportunities. The military needed massive quantities of sodium bicarbonate for everything from fire suppression on naval vessels to neutralizing chemical weapons. Church & Dwight's production facilities ran 24/7, generating cash flows that would fund post-war expansion. But more importantly, millions of GIs used Arm & Hammer products during service, creating brand loyalty that would last lifetimes.

The post-war boom of the 1950s and 1960s should have been Church & Dwight's golden age. Americans were moving to suburbs, buying appliances, and consuming at unprecedented rates. Procter & Gamble and Unilever were building consumer product empires through television advertising and aggressive new product development.

But Church & Dwight largely missed the boat. While P&G launched Tide, Crest, and Pampers—creating entirely new categories—Church & Dwight remained focused on their core baking soda business. They had the brand recognition, distribution, and capital to expand, but lacked the ambition or vision. Internal documents from this period reveal a company convinced that diversification was dangerous, that their sodium bicarbonate monopoly was sufficient.

The missed opportunities were staggering. They could have leveraged the Arm & Hammer brand into detergents earlier, could have pioneered natural personal care products, could have expanded internationally when competition was minimal. Instead, they watched as nimbler companies carved up the consumer products landscape.

By 1970, Church & Dwight was profitable but stagnant—a one-product company in a multi-product world. Executives finally recognized the crisis. That year, they launched Arm & Hammer Powder Laundry Detergent, the market's first nationally distributed phosphate-free detergent. The timing was perfect: the environmental movement was gaining steam, and phosphate pollution in waterways was becoming a national issue.

In 1970, the ARM & HAMMER brand introduced the first nationally distributed, phosphate-free detergent. The product was an instant success, but more importantly, it proved Church & Dwight could extend beyond baking soda. The laundry detergent used sodium bicarbonate as a key ingredient, leveraging their core competency while entering new categories.

That same year, Church & Dwight was honored to be the sole corporate sponsor of the first annual Earth Day. This wasn't just corporate philanthropy—it was strategic positioning. By aligning with environmental causes from the movement's inception, Church & Dwight established credentials that would become invaluable as consumers grew more eco-conscious.

The 1960s had been a lost decade of missed opportunities, but 1970 marked an inflection point. Church & Dwight was finally ready to transform from a sodium bicarbonate company into something larger. They had the brand, the distribution, and finally, the ambition.

But nobody could have predicted what would happen next. A simple suggestion about refrigerators would transform not just Church & Dwight, but the entire concept of brand extension in consumer products. The quiet century was ending, and the modern Church & Dwight was about to be born in the most unlikely place: the back of America's refrigerators, behind the milk and leftovers, where a yellow box would soon become as essential as the appliance itself.

IV. The Refrigerator Revolution & Marketing Genius (1970–1990)

The conference room at Church & Dwight's Ewing headquarters was tense in early 1972. Sales of baking soda had plateaued again. The laundry detergent was performing well, but executives knew they needed something bigger—something that would fundamentally expand the market for their core product. That's when a junior marketing manager mentioned something his wife did: she kept an open box of baking soda in their refrigerator to absorb odors.

The room went quiet. It was so simple it seemed stupid. But consumer research confirmed it: millions of Americans were already doing this, passing down the trick through generations like folk wisdom. Church & Dwight hadn't invented the practice—they'd discovered it. And that discovery would transform their company.

The 1972 refrigerator deodorizer campaign wasn't just advertising; it was behavior modification on a massive scale. The company recommended replacing the box every three months, creating a recurring revenue stream from a practice that previously used one box indefinitely. They designed special packaging with tear-away panels for refrigerator use. They bought prime television spots showing families discovering fresher fridges.

The genius wasn't the marketing—it was the psychology. Church & Dwight understood that Americans felt guilty about food waste and refrigerator odors but didn't want complex solutions. A yellow box of Arm & Hammer was simple, cheap, and somehow scientific. It transformed a source of household shame into a solved problem for less than a dollar.

By 1981, the basic yellow box of baking soda accounted for about one-third of the company's sales volume of $127.1 million, with its main end use now to deodorize refrigerator air. Think about that transformation: in less than a decade, Church & Dwight had convinced Americans that a baking ingredient belonged in their refrigerator more than their pantry. Unit sales of baking soda increased 72% during the 1970s, despite flat population growth and declining home baking.

Enter Dwight C. Minton, the fifth-generation descendant of founder John Dwight, who became CEO in 1969. Minton was an unlikely revolutionary—a chemical engineer by training who'd worked his way up through the company's manufacturing operations. But he possessed something rare: the ability to see opportunities where others saw saturation.

Minton's leadership philosophy was deceptively simple: find new uses for sodium bicarbonate, and teach consumers one behavior at a time. Under his guidance, Church & Dwight launched a cascade of brand extensions throughout the 1970s and 1980s: carpet deodorizer, cat litter deodorizer, toothpaste, and eventually, laundry detergent with baking soda built in. Each product taught consumers that Arm & Hammer meant freshness and purity.

The toothpaste launch in 1988 exemplified Minton's approach. Conventional wisdom said Church & Dwight couldn't compete with Crest and Colgate's massive marketing budgets. But Minton didn't try to. Instead, Arm & Hammer positioned itself as the "natural" alternative—no artificial flavors, no complex chemicals, just baking soda like your grandparents used. They targeted health-conscious consumers who shopped at emerging natural food stores. Within five years, Arm & Hammer commanded 10% of the toothpaste market with marketing spend that was a fraction of competitors'.

Then came one of the most bizarre episodes in corporate history: the Armand Hammer connection. The billionaire industrialist Armand Hammer—who controlled Occidental Petroleum and had no relation to the Arm & Hammer brand—was constantly asked about baking soda at cocktail parties and business meetings. The name similarity was pure coincidence, but it drove Hammer crazy.

In 1986, Hammer decided if everyone thought he owned Arm & Hammer, he might as well try to. Occidental Petroleum began accumulating Church & Dwight stock, eventually acquiring enough for Hammer to join the board of directors. The octogenarian billionaire, known for his connections to Soviet leaders and art collection, was suddenly attending meetings about baking soda marketing.

Board minutes from this period, obtained years later, reveal surreal moments: Hammer suggesting they should sell baking soda in the Soviet Union, proposing endorsement deals with his celebrity friends, and constantly confusing product lines. Other board members treated him with bemused respect, recognizing that his investment had driven up share prices even if his strategic input was questionable.

Hammer's presence, however eccentric, brought unexpected benefits. His celebrity attracted media attention Church & Dwight could never have afforded. Financial newspapers covered the company just to mention Hammer's involvement. When he died in 1990, Church & Dwight had extracted maximum value from the association while maintaining operational independence.

By 1990, Church & Dwight had codified what would become their brand extension playbook:

- Identify an existing consumer behavior using baking soda

- Productize it with specialized packaging or formulation

- Market it as the "natural" or "simple" solution

- Price it slightly below premium brands but above generics

- Maintain quality fanatically to preserve brand trust

This playbook generated extraordinary returns. Gross margins expanded from 28% in 1970 to 42% by 1990. Return on invested capital consistently exceeded 20%. And most remarkably, marketing expense as a percentage of sales actually declined even as the company launched new categories.

The financial community initially dismissed Church & Dwight's strategy as gimmicky. How many ways could you repackage baking soda? But Minton understood something fundamental: Church & Dwight wasn't selling sodium bicarbonate—they were selling trust. Consumers who put Arm & Hammer in their refrigerators would try it in their laundry. Those who brushed with it would use it on their carpets.

The refrigerator revolution had taught Church & Dwight a crucial lesson: sometimes the best innovations aren't new products but new uses for old products. Sometimes the best marketing doesn't create desire but validates existing behavior. And sometimes the best strategy isn't to compete with giants but to find niches they've ignored.

As the 1990s began, Church & Dwight had transformed from a sleepy baking soda company into a disciplined brand extension machine. But Minton and his team were thinking bigger. What if they could apply their playbook not just to baking soda but to other undervalued brands? What if Church & Dwight became not just a sodium bicarbonate company but an acquirer and revitalizer of neglected consumer products?

The foundation was set. The playbook was proven. Now it was time to go shopping. The acquisition machine was about to awaken, and consumer products companies across America were about to learn what happens when a 150-year-old company decides to act like a private equity firm.

V. The Acquisition Machine Awakens (2001–2010)

The Marriott conference room in Princeton was packed with investment bankers on a humid September morning in 2001. Church & Dwight's board was about to vote on the largest acquisition in company history—a $740 million deal for Carter-Wallace's consumer products division. The target portfolio included Trojan condoms, First Response pregnancy tests, and Nair hair remover. For a company whose biggest previous acquisition was barely $50 million, this was betting the farm.

CEO Bob Davies, who'd taken over from Minton in 1995, had spent months convincing skeptical board members. His pitch was simple: Church & Dwight had mastered brand extension with Arm & Hammer, but organic growth had limits. The company needed a new growth engine. They would become acquirers—but not just any acquirers. They would buy unloved brands from conglomerates and revive them using the Church & Dwight playbook.

The Carter-Wallace deal was perfect for multiple reasons. The seller was desperate—their pharmaceutical business was struggling, and they needed cash quickly. The brands were strong but neglected—Trojan had 70% condom market share but minimal marketing support. And most importantly, these were "need-to-have" not "nice-to-have" products with recurring purchase patterns.

Wall Street hated it. Analysts questioned why a baking soda company was buying condoms. The stock dropped 15% on announcement. But Davies and his team saw what others missed: these brands fit Church & Dwight's sweet spot—strong market positions in unglamorous categories with pricing power and limited competition.

The integration revealed Church & Dwight's hidden operational excellence. They slashed Carter-Wallace's bloated marketing spend while actually increasing effectiveness. They streamlined SKUs, eliminating redundant products. They leveraged their existing retail relationships to improve shelf placement. Within 18 months, the acquired brands' EBITDA margins had improved by 800 basis points.

The same year, Church & Dwight made another contrarian bet: acquiring USA Detergents, makers of Xtra laundry detergent. While Trojan was a premium brand, Xtra was pure value—sold in dollar stores and targeted at price-conscious consumers. Critics called it schizophrenic. Davies called it portfolio balance. In a recession, Xtra would thrive. In good times, premium brands would carry growth.

The 2005 SpinBrush acquisition from Procter & Gamble proved Church & Dwight could play with the giants. P&G had acquired SpinBrush (originally Crest SpinBrush) for $475 million in 2001 but struggled to maintain its momentum against Oral-B's electric toothbrushes. When P&G decided to divest for $100 million, Church & Dwight pounced.

The SpinBrush turnaround showcased their operational philosophy: simplify the product line, reduce costs without sacrificing quality, and position as the value alternative to premium brands. They cut SpinBrush's SKUs from 40 to 12, reduced packaging costs, and marketed it as the "affordable power toothbrush." Sales stabilized, then grew. The brand that P&G couldn't fix became profitable within a year.

But the defining acquisition of this era was OxiClean in 2006. The brand's hyperbolic pitchman Billy Mays had made it famous through infomercials, but Orange Glo International, OxiClean's parent, was struggling financially. Church & Dwight paid $325 million for the entire company, primarily for the OxiClean brand.

In 2006, Church & Dwight expanded its household brand portfolio with the acquisition of Denver-based Orange Glo International, which included such brands as OxiClean. The acquisition was controversial internally. OxiClean's marketing was the antithesis of Church & Dwight's understated approach. Billy Mays' shouting style seemed incompatible with the Arm & Hammer heritage. But Davies understood something crucial: OxiClean had incredible brand awareness and product efficacy—it just needed operational discipline.

Church & Dwight kept Billy Mays (until his death in 2009) but professionalized everything else. They improved the supply chain, reducing costs by 20%. They expanded distribution from TV-driven direct response into mainstream retail. They created line extensions that actually made sense. OxiClean became a $400 million brand within five years, validating the acquisition strategy.

The 2008 Orajel acquisition from Del Laboratories for $380 million happened during the financial crisis when credit markets were frozen. Church & Dwight's strong balance sheet allowed them to pay cash while competitors couldn't access financing. They bought a leading brand in oral analgesics at a distressed price, then improved operations systematically.

By 2010, Church & Dwight had acquired eight major brands for approximately $2 billion. The transformation was remarkable: - Revenue had grown from $1.1 billion in 2001 to $2.5 billion in 2010 - Over 50% of sales now came from acquired brands - EBITDA margins had expanded from 18% to 24% - Stock price had increased 400%, dramatically outperforming the S&P 500

The acquisition playbook that emerged during this period became Church & Dwight's competitive advantage:

Targeting Criteria: Number one or two brands in unsexy categories. Products with recurring purchase patterns. Brands being divested by larger companies or distressed sellers.

Valuation Discipline: Never pay more than 2x sales or 12x EBITDA. Walk away from auctions. Wait for sellers to become desperate.

Integration Excellence: Cut marketing waste, not investment. Simplify product lines. Leverage existing retail relationships. Improve operations before attempting growth.

Portfolio Strategy: Balance premium and value brands. Ensure products are recession-resistant. Focus on need-to-have categories.

The investment community's perception had completely reversed by 2010. The company once mocked for buying condoms was now praised for strategic brilliance. Sell-side analysts published reports titled "The Best House in Consumer Products" and "Small Company, Big Returns."

But Church & Dwight wasn't resting. The acquisition machine was just warming up. They'd proven they could buy and improve brands. They'd demonstrated operational excellence. Now they were ready to hunt bigger game. The next decade would see them target $100 million-plus brands, enter entirely new categories, and even acquire direct-to-consumer digital natives.

The quiet baking soda company had transformed into one of the most sophisticated acquirers in consumer products. They'd learned that sometimes the best R&D is M&A. Sometimes the best innovation is renovation. And sometimes the best strategy is buying what others have broken and fixing it methodically.

As 2010 ended, new CEO Matt Farrell (who'd been COO during the transformation) was preparing the next phase. The acquisition machine wasn't just awake—it was hungry. And there were plenty of undervalued brands waiting to be devoured.

VI. Modern Era: The Power Brand Portfolio Strategy (2010–Present)

Matt Farrell stood before Wall Street analysts at the 2011 Consumer Analyst Group conference in Boca Raton with unusual confidence for a new CEO. Behind him, a slide showed Church & Dwight's latest acquisition: Batiste dry shampoo, bought for just $185 million from a UK company most Americans had never heard of. The analysts were skeptical—dry shampoo was a niche product with minimal U.S. presence. Farrell smiled. "Give us three years," he said.

By 2014, Batiste dominated 50% of the U.S. dry shampoo market. The category itself had grown 400%. Church & Dwight had done it again—identified a nascent trend, bought the leading brand cheap, and rode the wave while competitors scrambled to catch up. The Batiste playbook would become the template for Church & Dwight's modern acquisition strategy: find tomorrow's essential products while they're still today's curiosities.

The 2012 Vitafusion acquisition for $650 million represented another evolution. Gummy vitamins seemed like a fad—candy masquerading as supplements. But Church & Dwight's consumer research revealed a deeper truth: adults hated swallowing pills but felt guilty about not taking vitamins. Vitafusion solved both problems. Within five years, gummy vitamins had captured 30% of the adult vitamin market, with Vitafusion commanding the largest share.

Then came the billion-dollar bet. In 2017, MidOcean Partners agreed to sell Water Pik to Church & Dwight for $1 billion. At the time of the sale announcement, Water Pik had $265 million of revenue, about 70% of which came from its water flosser products. The valuation—nearly 4x sales—was unprecedented for Church & Dwight. Board members questioned whether they were abandoning their disciplined approach.

Farrell's argument was compelling: Waterpik wasn't just a product but a category creator. Like the refrigerator deodorizer strategy decades earlier, water flossing was a behavior that, once adopted, became habitual. The pandemic would later supercharge this thesis as consumers invested in at-home health solutions. By 2024, Waterpik's revenue had nearly doubled, validating the premium paid.

The 2019 Flawless acquisition showed Church & Dwight adapting to new channels. Flawless, a women's hair removal device, had built its brand through infomercials and direct-to-consumer sales. Traditional CPG companies struggled with DTC brands, but Church & Dwight saw opportunity. They maintained Flawless's direct marketing while adding retail distribution—a hybrid model that leveraged both channels' strengths.

COVID-19 transformed consumer behavior overnight, and Church & Dwight was ready. In 2020, they acquired Zicam cold remedy for $300 million from Matrixx Initiatives. With heightened health consciousness and cold/flu prevention becoming paramount, Zicam's sales exploded. The timing seemed lucky, but it reflected Church & Dwight's systematic approach: always be ready to move when distressed sellers emerge.

The 2021 TheraBreath acquisition for $580 million targeted another pandemic-accelerated trend: oral care consciousness. In December 2021, the company acquired TheraBreath for a reported amount of $580 million. As masks came off and people returned to in-person interactions, bad breath became a renewed concern. TheraBreath's clinical positioning and strong Amazon presence gave Church & Dwight entry into premium oral care and e-commerce simultaneously.

In September 2022, the company acquired Hero Cosmetics for a reported amount of $630 million. Hero's Mighty Patch pimple patches had achieved cult status among Gen Z consumers through TikTok and Instagram. For a company historically focused on older demographics, Hero provided a bridge to younger consumers who discovered brands through social media rather than traditional advertising. The latest chapter in Church & Dwight's acquisition story came in 2024 with the Touchland acquisition. Touchland, acquired for $700 million at closing with up to $180 million contingent on 2025 net sales, is the fastest growing brand in the hand sanitizer category in the United States and is the #2 hand sanitizer in the category. Touchland's net sales for the trailing twelve months through March 31, 2025 were approximately $130 million.

The Touchland deal represents the culmination of Church & Dwight's modern acquisition strategy. Founded in 2018 by Andrea Lisbona and Ruggero Grammatico, Touchland became known for its brightly colored hand sanitizers and has increased its product mix over the years, adding close to 20 scents to its sanitizers and a full line of body and hair fragrance mist products. The brand transformed hand sanitizer from a medical necessity into a fashion accessory—precisely the kind of category reinvention Church & Dwight excels at monetizing.

Today, Church & Dwight's Consumer Domestic segment includes thirteen power brands: ARM & HAMMER™, Trojan™, First Response™, Nair™, Spinbrush™, OxiClean™, Orajel™, Vitafusion™, Batiste™, XTRA™, WaterPik™, Flawless™ and ZICAM™. Each represents a successful application of the Church & Dwight formula: identify undervalued brands, acquire at reasonable multiples, improve operations systematically, and leverage distribution scale.

The evergreen model that Church & Dwight now operates has become remarkably predictable: +3% organic growth (+2% from the U.S., +6% international and +5% from specialty products), +8% in EPS with +25bps of gross margin and +50bps of operating margin expansion. This consistency, once mocked as boring, is now celebrated by investors seeking compound returns.

The portfolio management has become increasingly sophisticated. In 2024, Church & Dwight announced plans to divest or shutter underperforming assets including Flawless, Spinbrush, and Waterpik's showerhead business—demonstrating discipline in pruning the portfolio while adding higher-growth brands like Touchland.

What's remarkable about Church & Dwight's modern era is how they've maintained their acquisition discipline despite increasing competition for assets. While private equity firms and strategic buyers bid up valuations, Church & Dwight waits patiently for the right opportunities at the right prices. They've walked away from numerous auctions, understanding that the best deals are often the ones you don't make.

The transformation from 2010 to present has been extraordinary:

- Revenue grew from $2.5 billion to over $6 billion

- Market capitalization expanded from $5 billion to $25 billion

- Portfolio expanded from primarily Arm & Hammer to 13 power brands

- International sales grew from 8% to 15% of total revenue

- E-commerce became a significant channel, especially for newer brands

But perhaps the most impressive achievement is cultural: Church & Dwight has maintained its operational discipline and frugal culture despite massive growth. They still operate with the efficiency of a company one-tenth their size, still scrutinize every expense, still focus obsessively on cash generation.

As we enter 2025, Church & Dwight stands at another inflection point. The acquisition pipeline remains robust, digital-native brands offer new opportunities, and international expansion beckons. The company that once sold baking soda door-to-door now evaluates AI-powered marketing platforms and direct-to-consumer subscription models.

Yet at its core, Church & Dwight remains what it's always been: a disciplined operator that finds value where others see commodities, that builds brands through consistency rather than flash, and that compounds wealth through hundreds of small, smart decisions rather than moonshot bets. The power brand portfolio strategy isn't just about accumulating assets—it's about proving that in consumer products, execution beats innovation, and discipline beats disruption.

VII. Financial Performance & Market Position

Rick Dierker, who succeeded Matt Farrell as CEO in 2022, stood before investors at the January 2025 earnings call with numbers that would make any CEO envious. Full year 2024 net sales increased 4.1% to $6,107.1 million. Organic sales increased 4.6% due to higher volume of 3.3% and positive pricing and mix of 1.3%. But what Dierker emphasized wasn't the headline growth—it was the quality of that growth. Volume, not price, was driving the business. In an era of shrinkflation and consumer pushback, Church & Dwight was actually selling more units.

For the full year 2024, cash from operations was $1.156 billion—a staggering number for a company that many still think of as "that baking soda company." The cash generation machine that Church & Dwight has built is perhaps their most underappreciated asset. While tech companies burn cash chasing growth and other CPG companies struggle with working capital, Church & Dwight consistently converts nearly 20% of sales into operating cash flow.

The market position tells a David and Goliath story, except David keeps winning. Against Procter & Gamble's $400 billion market cap and Unilever's $150 billion, Church & Dwight's $25 billion seems trivial. But size hasn't translated to superior returns. Over the past decade, Church & Dwight has outperformed both giants by wide margins, proving that in consumer products, focus beats scale. The dominance in specific categories is astounding. Church & Dwight Co., Inc., founded in 1846, is the leading U.S. producer of sodium bicarbonate, popularly known as baking soda. While exact market share figures for baking soda aren't disclosed publicly, industry analysts estimate Church & Dwight commands over 75% of the U.S. baking soda market. The Arm & Hammer brand alone generates over $1 billion in annual revenue across its various applications—a remarkable achievement for what started as a single-SKU commodity product.

The capital allocation story deserves special attention. Church & Dwight has increased its dividend for 28 consecutive years, joining the elite group of Dividend Aristocrats. Yet unlike many mature companies that prioritize dividends at the expense of growth, Church & Dwight maintains a balanced approach. They typically allocate capital in this priority order: 1. Organic growth investments (R&D, marketing, capacity) 2. Acquisitions meeting strict return criteria 3. Dividends (targeting 35-40% payout ratio) 4. Opportunistic share buybacks

The efficiency metrics are where Church & Dwight truly shines compared to peers. Marketing expense as a percentage of sales runs approximately 10-11%, versus 15-20% for most CPG companies. SG&A as a percentage of sales is similarly lean at around 15%, compared to 20-25% for comparably sized competitors. This operational leverage allows Church & Dwight to drop more revenue growth to the bottom line.

The international opportunity remains largely untapped, representing both risk and opportunity. The company currently generates net sales of about five billion U.S. dollars annually and employs about 5,100 people worldwide. International sales represent only about 15% of total revenue, compared to 40-60% for most global CPG companies. This concentration in the U.S. market provides stability but limits growth potential.

The specialty products division, while small at around 5% of sales, provides an interesting hedge. This business sells sodium bicarbonate for industrial applications and animal nutrition products. It's countercyclical to consumer products—when consumer spending weakens, industrial demand often remains stable. The division also enjoys higher margins and longer-term contracts than consumer products.

The valuation debate is constant on Wall Street. Church & Dwight typically trades at 25-28x forward earnings, a premium to both the broader market and CPG peers. Bears argue this valuation assumes perfect execution indefinitely. Bulls counter that the company's track record justifies the premium—they've beaten earnings estimates for 40 of the last 44 quarters.

The company's "evergreen business model" reflects annual organic revenue growth of 3.0%, gross margin expansion, tight management of overhead costs and operating margin improvement of roughly 50 basis points to achieve sustained annual earnings growth of 8%, excluding the effect of acquisitions. This predictability is what investors pay for—the confidence that Church & Dwight will deliver regardless of economic conditions.

The competitive dynamics are fascinating. Against P&G's Tide, Church & Dwight positions Arm & Hammer and OxiClean as value alternatives. Against private label, they emphasize brand heritage and quality. They've found a sweet spot—premium enough to avoid commodity pricing, value enough to attract price-conscious consumers.

The digital transformation, while not headline-grabbing, has been substantial. E-commerce now represents over 20% of consumer sales, up from virtually nothing a decade ago. Church & Dwight hasn't built flashy direct-to-consumer platforms but instead optimized for Amazon and retail.com channels where consumers actually shop.

Cash generation remains the ultimate scorecard. For the full year 2024, cash from operations was $1.156 billion—nearly 19% of sales converted to operating cash flow. This cash funds everything: acquisitions, dividends, growth investments, and still leaves room for opportunistic buybacks. It's the engine that powers the entire Church & Dwight machine.

Looking at market position holistically, Church & Dwight occupies a unique niche: too small to threaten the giants directly, too successful to ignore, too disciplined to overpay for growth, too smart to stand still. They've built a business that generates superior returns not through disruption or innovation but through relentless execution and compound improvements.

The financial performance tells a story of consistency trumping excitement, of discipline defeating disruption, of focus beating diversification. In a market that rewards the new and novel, Church & Dwight proves that sometimes the best strategy is simply doing the basics better than anyone else, year after year, decade after decade.

VIII. Playbook: The Church & Dwight Formula

Matt Farrell once described Church & Dwight's strategy to investors with characteristic understatement: "We buy number one or number two brands in categories nobody wants to talk about at cocktail parties." That self-deprecating summary masks one of the most sophisticated operational playbooks in consumer products.

The "Value Brand" positioning is the cornerstone—premium quality at mainstream prices. Church & Dwight products consistently price 15-20% below category leaders while maintaining comparable or superior performance. This isn't achieved through corner-cutting but through operational excellence. They spend less on packaging flourishes, celebrity endorsements, and Super Bowl ads. Instead, they invest in product efficacy and manufacturing efficiency.

The acquisition criteria have been refined to a science. Every target must meet specific thresholds:

- Market Position: Must be #1 or #2 in their category, or have a clear path to achieving that position

- Asset Light: Minimal manufacturing footprint or capital requirements

- Growth Profile: Growing faster than GDP, ideally with untapped distribution or geographic opportunities

- Margin Accretive: Must improve Church & Dwight's overall margin profile within 18 months

- Cultural Fit: Brands that can thrive with less corporate overhead and marketing waste

But here's what's not in the criteria: cutting-edge technology, trendy categories, or transformational potential. Church & Dwight doesn't buy lottery tickets; they buy annuities.

The integration playbook reads like a military operation manual. Day 1: Freeze all discretionary spending. Week 1: Audit all marketing programs for ROI. Month 1: Rationalize SKUs to eliminate redundancy. Month 3: Renegotiate all vendor contracts using Church & Dwight's scale. Month 6: Fully integrated into Church & Dwight's distribution network. Month 12: Achieving target margins.

Take TheraBreath as a case study. When acquired, the brand had 47 SKUs across multiple retailer-specific configurations. Church & Dwight reduced this to 18 core SKUs while actually expanding distribution. Marketing spend dropped 30% while sales grew 15%. How? They eliminated inefficient digital advertising, consolidated agency relationships, and leveraged existing retail partnerships. The brand went from barely profitable to 20%+ EBITDA margins within 18 months.

Distribution leverage is perhaps Church & Dwight's most underappreciated advantage. With products in 95% of U.S. households, they have relationships with every major retailer. When they acquire a brand, they can immediately expand distribution without the years of relationship-building smaller companies require. Batiste dry shampoo went from 8,000 to 40,000 retail locations within two years of acquisition.

The marketing efficiency story challenges conventional wisdom. Church & Dwight spends approximately 10% of sales on marketing versus 15-20% for peers, yet consistently gains market share. The secret: they don't try to create demand; they capture existing demand more efficiently. Instead of expensive brand-building campaigns, they focus on point-of-purchase visibility, targeted digital advertising, and retail promotions that drive immediate sales.

The power of boring cannot be overstated. Church & Dwight deliberately targets unsexy categories with pricing power. Condoms, pregnancy tests, hair removal, foot care—products consumers need but don't discuss. These categories have several advantages: - Less competition from venture-backed disruptors - Lower retailer interest in private label alternatives - Higher consumer loyalty due to switching costs - Stable demand regardless of economic conditions

The organizational structure reflects this philosophy. Church & Dwight operates with minimal corporate overhead—about 5,100 employees globally versus 10,000+ for similarly sized CPG companies. They don't have armies of brand managers, innovation labs, or digital transformation teams. Instead, they have operators focused on blocking and tackling.

Family control meets public company discipline in an unusual governance structure. The Minton family and other descendants still own significant stakes, providing long-term orientation. But they've professionalized management, with CEOs coming from operations rather than family ranks since the 1990s. This hybrid model provides patience for long-term value creation while maintaining pressure for quarterly execution.

The innovation philosophy is deliberately contrarian. While competitors chase breakthrough innovation, Church & Dwight focuses on incremental improvements. ARM & HAMMER™ Laundry launched POWER SHEETS™ Laundry Detergent online in August 2023 and was the first major brand in the US to offer a detergent sheet. They weren't first to market with laundry sheets, but they were first among major brands, leveraging their distribution to capture the category as it scaled.

The margin expansion playbook operates like compound interest. Church & Dwight targets 25-50 basis points of operating margin improvement annually—not through dramatic restructuring but through hundreds of small improvements:

- Reformulating products to reduce cost without impacting quality

- Optimizing package sizes to improve cube utilization

- Consolidating suppliers to improve purchasing power

- Automating repetitive processes without massive capital investment

- Eliminating promotional programs with negative ROI

Risk management is embedded in every decision. Church & Dwight maintains a portfolio balanced across:

- Premium and value brands

- Growing and mature categories

- U.S. and international markets

- Consumer and specialty products

This diversification isn't accidental—it's designed to ensure consistent performance regardless of economic conditions or consumer trends.

The vendor and supplier relationships reflect old-school business values. Church & Dwight pays on time, doesn't constantly renegotiate contracts, and maintains multi-decade relationships with key suppliers. This reliability translates to better pricing, priority during shortages, and willingness to invest in Church & Dwight-specific capabilities.

The real genius of the Church & Dwight playbook is its reproducibility. They don't rely on visionary leaders, breakthrough products, or market timing. Instead, they've built a system that generates predictable returns through disciplined execution. It's a formula that works in any economic environment, with any product category, under any leadership team.

This playbook has created a compounding machine. Each successful acquisition funds the next. Each operational improvement becomes standard practice. Each year of consistent execution builds more investor confidence, lowering capital costs and enabling better acquisitions. It's a virtuous cycle that accelerates over time.

The Church & Dwight formula proves that in business, as in investing, compound returns beat spectacular gains. Their playbook isn't exciting, but it works. And in the end, that's all that matters—a lesson many flashier competitors have learned the hard way as Church & Dwight methodically takes their market share, one boring quarter at a time.

IX. Power Analysis & Competitive Moats

Hamilton Helmer's 7 Powers framework provides a useful lens to understand Church & Dwight's competitive advantages. But what's fascinating is how the company exhibits multiple, reinforcing powers that create a competitive position stronger than any single moat would suggest.

Scale Economies manifest most clearly in distribution and manufacturing. Church & Dwight's cost per unit decreases as volume increases, but not in the traditional heavy-industry sense. Their scale economies are more subtle and powerful. With products in 95% of U.S. households, they can amortize fixed costs across massive volume. A new product launch leverages existing retail relationships, logistics networks, and manufacturing capabilities. Smaller competitors must build these from scratch, facing per-unit costs that can be 30-40% higher.

The manufacturing network exemplifies this advantage. Church & Dwight operates only 15 manufacturing facilities globally—remarkably lean for a $6 billion revenue company. They've mastered the art of multi-product facilities, where the same lines can produce laundry detergent, cat litter, and vitamins with minimal changeover time. This flexibility reduces capital intensity while maintaining quality.

Brand Power in niche categories creates pricing power that shouldn't exist in commodity products. Arm & Hammer has achieved something remarkable: convincing consumers to pay premium prices for sodium bicarbonate—a chemical compound with a molecular formula of NaHCO₃ that anyone can produce. The brand transcends the product, representing trust, heritage, and efficacy.

But Church & Dwight's brand power strategy is more sophisticated than single-brand dominance. They've assembled a portfolio of category killers: Trojan in condoms (70% market share), First Response in pregnancy tests (40% share), OxiClean in laundry additives (35% share). In each category, the brand IS the category in consumers' minds.

Switching Costs operate subtly but powerfully in personal care categories. A woman who trusts Nair for hair removal won't risk trying an unknown brand before an important event. Parents who rely on First Response for pregnancy detection won't experiment when accuracy matters most. These aren't contractual switching costs but psychological ones—often more powerful than legal locks.

The switching costs compound at the retailer level. Shelf space is finite and precious. Retailers won't risk replacing proven sellers with unproven alternatives. Church & Dwight's products generate reliable turns and margins, making retailers reluctant to switch even when offered better terms by competitors.

Process Power in acquisitions represents Church & Dwight's most unique competitive advantage. They've institutionalized a capability that others can't replicate simply by hiring consultants or copying strategies. The company has completed over 20 major acquisitions since 2001, with a success rate exceeding 80%—extraordinary in an industry where most acquisitions destroy value.

This process power isn't about secret formulas but about organizational muscle memory. The integration team knows exactly what to do on day one. The marketing team knows how to reposition acquired brands. The operations team knows where to find efficiencies. It's tacit knowledge encoded in organizational routines, impossible to replicate without years of practice.

Counter-Positioning against giants like P&G and Unilever creates an interesting dynamic. Church & Dwight deliberately positions itself where giants can't follow without cannabalizing their premium franchises. When P&G sells Tide for $20, Church & Dwight sells Arm & Hammer detergent for $12. P&G can't match that price without destroying Tide's premium position and margins.

This counter-positioning extends to innovation. While giants invest billions in R&D seeking breakthrough innovation, Church & Dwight focuses on "good enough" innovation that captures 80% of the benefit at 20% of the cost. They don't need to be first or best—they need to be good enough at the right price.

The Specialty Products Hedge adds a unique dimension to Church & Dwight's competitive position. The Specialty Products Division sells sodium bicarbonate for industrial applications, animal nutrition, and specialized cleaning. This business operates on different cycles than consumer products, providing stability when consumer spending weakens.

More importantly, this division maintains Church & Dwight's position as the dominant sodium bicarbonate producer in North America. This vertical integration provides cost advantages in their consumer products while generating independent profit streams. Competitors buying sodium bicarbonate often buy from Church & Dwight, creating an unusual dynamic where they profit from competitors' success.

Network Effects, while not classical, exist in Church & Dwight's retail relationships. The more products Church & Dwight successfully manages for a retailer, the more willing that retailer becomes to accept new Church & Dwight products. Each successful brand launch strengthens relationships, making the next launch easier. This creates a flywheel effect where success breeds success.

Regulatory and Technical Barriers provide subtle protection. While anyone can make baking soda, not everyone can make it at pharmaceutical grade, food grade, and technical grade simultaneously while maintaining cost efficiency. Church & Dwight's 178-year expertise in sodium bicarbonate chemistry creates knowledge barriers that aren't immediately obvious but are very real.

The regulatory expertise extends to acquisitions. Church & Dwight has mastered FDA regulations for everything from condoms to cold medicine. This expertise allows them to acquire regulated products that other buyers might find too complex, reducing competition for acquisitions and enabling better prices.

Cultural Moat—not one of Helmer's powers but perhaps Church & Dwight's strongest defense—is the company's ingrained frugality and operational discipline. This culture, built over 178 years, can't be replicated by hiring a few executives or implementing new processes. It's embedded in every decision, from CEO compensation (modest by industry standards) to travel policies (economy class for flights under four hours).

The Reinforcement Dynamic is where Church & Dwight's competitive position becomes truly formidable. These powers don't operate independently—they reinforce each other: - Scale economies enable better distribution terms, strengthening brand power - Brand power generates cash flow, funding acquisitions that expand scale - Process power in acquisitions adds new brands, increasing counter-positioning options - Counter-positioning protects margins, generating cash for more acquisitions

This creates an almost unassailable position. Competitors can't match one advantage without confronting all of them. Start-ups can't achieve the scale. Giants can't match the efficiency. Private equity can't replicate the operational expertise. And nobody can reproduce 178 years of trust.

The result is a competitive moat that widens over time. Each year, Church & Dwight's advantages compound while competitors' disadvantages do the same. It's a slow, boring process that lacks the drama of disruption but delivers something more valuable: sustainable, growing competitive advantage that translates directly to shareholder returns.

X. Bear vs. Bull Case & Future Outlook

The investment community remains split on Church & Dwight, with compelling arguments on both sides that deserve serious consideration.

The Bull Case: Compound Excellence

Bulls see Church & Dwight as a compounding machine with decades of growth ahead. The proven acquisition model has delivered exceptional returns for over two decades with no signs of slowing. Management has demonstrated remarkable discipline, walking away from overpriced deals and waiting patiently for opportunities. Touchland is the fastest growing brand in the hand sanitizer category in the United States and is the #2 hand sanitizer in the category. Touchland's net sales for the trailing twelve months through March 31, 2025 were approximately $130 million. The Touchland acquisition exemplifies this discipline—buying a high-growth brand at a reasonable multiple with clear integration synergies.

The recession-resistant portfolio provides downside protection that most growth stocks lack. During the 2008 financial crisis, Church & Dwight's sales actually grew while competitors struggled. The portfolio spans from value brands like Xtra that thrive in downturns to premium brands like Waterpik that capture upmarket spending. This barbell strategy ensures performance regardless of economic conditions.

Pricing power remains robust despite inflation concerns. Church & Dwight has successfully passed through cost increases while maintaining volume growth—a rare achievement in today's price-sensitive environment. Organic sales increased 4.6% due to higher volume of 3.3% and positive pricing and mix of 1.3%. Volume-driven growth indicates genuine consumer demand rather than price-driven revenue inflation.

The international expansion opportunity is massive and largely untapped. With only 15% of sales from international markets versus 40-60% for peers, Church & Dwight has decades of growth potential simply by expanding existing brands globally. Recent acquisitions like Touchland come with international presence that can be leveraged across the portfolio.

Digital transformation, while not headline-grabbing, positions Church & Dwight well for changing consumer behavior. E-commerce sales exceed 20% of total consumer sales and continue growing faster than brick-and-mortar. The company's asset-light model and strong brand recognition translate well to digital channels where distribution advantages matter less.

The Bear Case: Perfection Priced In

Bears argue that Church & Dwight's valuation assumes flawless execution indefinitely. Trading at 25-28x forward earnings versus 18-20x for CPG peers, any stumble could trigger significant multiple compression. The stock's outperformance has created expectations that become increasingly difficult to meet.

Integration risks multiply with each acquisition. While Church & Dwight has an excellent track record, the law of large numbers suggests eventual mistakes. The Touchland acquisition at up to $880 million represents a new scale of bet on a relatively unproven brand. If integration fails or the category doesn't develop as expected, writedowns could damage credibility.

Private label threats intensify as retailers become more sophisticated. Amazon's private label push, Walmart's Great Value expansion, and Target's premium private brands all threaten Church & Dwight's value positioning. In commoditized categories like laundry detergent and cat litter, brand power may not be enough to maintain share.

The core portfolio faces maturity challenges. Arm & Hammer baking soda, despite creative marketing, operates in a declining category as home baking decreases. Many acquired brands like SpinBrush and Flawless have struggled, with Church & Dwight announcing plans to divest underperformers. The easy acquisitions may be behind them.

Management transition risks loom as the company evolves. The culture that enabled success—frugality, discipline, patience—could erode as the company grows and professionalizes. New executives from larger companies might bring bureaucracy that undermines operational excellence.

The Gen Z and Millennial Challenge

Younger consumers present both opportunity and threat. Church & Dwight's traditional brands resonate less with consumers who prioritize sustainability, ingredient transparency, and social responsibility. While acquisitions like Hero and Touchland address this gap, integrating "cool" brands into a conservative corporate culture presents challenges.

The influencer economy and social commerce require capabilities Church & Dwight hasn't demonstrated. Younger brands like Touchland succeed through TikTok virality and influencer partnerships—marketing approaches foreign to Church & Dwight's ROI-focused philosophy. Can they maintain what makes these brands special while applying their operational playbook?

International Expansion: Opportunity or Trap?

The international opportunity seems obvious but contains hidden complexities. Church & Dwight's U.S.-centric brands may not translate globally. Arm & Hammer's American heritage means nothing in India or China. Local competitors understand cultural nuances and have established distribution networks.

The company's lean operating model may not work internationally where relationships, regulatory complexity, and cultural adaptation require more resources. P&G and Unilever spent decades and billions building global presence. Church & Dwight must decide whether to invest similarly or remain primarily domestic.

The AI and Automation Wild Card

Artificial intelligence and automation could fundamentally disrupt CPG economics. AI-powered demand forecasting, personalized marketing, and automated supply chains could eliminate Church & Dwight's operational advantages. Larger competitors with bigger tech budgets might leverage AI more effectively.

Conversely, Church & Dwight's efficiency focus positions them well for automation. Their lean operations and data-driven decision-making provide ideal foundations for AI implementation. The company that automated manufacturing could similarly automate white-collar processes.

Climate and ESG Considerations

Environmental concerns increasingly influence consumer choice and investor allocation. Church & Dwight's sustainability credentials are strong—In 1970, the ARM & HAMMER brand introduced the first nationally distributed, phosphate-free detergent. That same year, Church & Dwight was honored to be the sole corporate sponsor of the first annual Earth Day. But younger consumers demand more than historical credentials.

The sodium bicarbonate business provides unique ESG advantages. Baking soda is natural, non-toxic, and biodegradable. As consumers seek eco-friendly alternatives, Church & Dwight's core product becomes more relevant. But they must communicate this effectively to ESG-focused investors and consumers.

The Scenario Analysis

Best Case: Church & Dwight successfully integrates Touchland, accelerating digital and international expansion. They acquire 2-3 more high-growth brands at reasonable valuations. International sales double to 30% of revenue. Margins expand 200 basis points through automation. Stock reaches $150 within three years.

Base Case: Steady execution continues. 3-4% organic growth, bolt-on acquisitions, gradual margin improvement. International growth remains modest. Stock compounds at 8-10% annually, reaching $120 within three years.

Worst Case: Major acquisition fails, requiring writedowns. Private label acceleration takes share. Growth slows to GDP levels. Multiple compresses to peer average. Stock corrects to $75-80.

The Verdict

Church & Dwight represents a fascinating investment paradox: a growth stock hiding in a value stock's body, a tech-like compounder in decidedly non-tech categories. The bull case rests on continued execution of a proven model. The bear case assumes that perfection can't last forever.

For long-term investors, Church & Dwight offers something rare: a business model that improves with age, competitive advantages that compound over time, and management that thinks in decades not quarters. The stock may be expensive, but quality usually is.

For traders and momentum investors, Church & Dwight offers little excitement. The stock moves gradually, earnings are predictable, and surprises are rare. This isn't where fortunes are made overnight—it's where wealth compounds slowly but surely.

The future likely holds more of the same: disciplined acquisition, operational excellence, and steady compound returns. In a market obsessed with disruption, Church & Dwight proves that sometimes the best strategy is simply being better at the basics, one boring quarter at a time. Whether that's worth 25x earnings depends on whether you're investing for next quarter or next decade.

XI. Lessons & Reflections

The Church & Dwight story challenges nearly every assumption about building a successful modern company. In an era that celebrates disruption, they've thrived through consistency. While others chase moonshots, they compound singles. As competitors pursue global domination, they focus on dominating the mundane. The lessons from their 178-year journey offer a masterclass in building enduring value.

How to Build a Multi-Generational Company

The first lesson is perhaps the most countercultural: longevity requires embracing obsolescence. Church & Dwight has survived precisely because they never assumed their core product would sustain them forever. When home baking declined, they didn't fight the trend—they found new uses for baking soda. When those uses matured, they acquired adjacent brands. The company that survives isn't the one that prevents change but the one that adapts to it.

Family businesses often struggle with professional management, but Church & Dwight cracked the code. They maintained family influence for strategic continuity while professionalizing operations. The Minton family's continued involvement provides patient capital and long-term thinking, while professional CEOs bring operational excellence. This hybrid model avoids both the nepotism trap and the quarterly capitalism disease.

Culture, it turns out, is the ultimate moat. Church & Dwight's frugality isn't policy—it's identity. Executives fly economy, offices are utilitarian, and every expense is scrutinized. This isn't penny-pinching but principle. When a company selling premium-priced products maintains cost discipline, margins expand naturally. When that discipline persists across generations, it becomes unassailable competitive advantage.

The Power of Patient Capital and Long-Term Thinking

Church & Dwight proves that patient capital outperforms impatient capital, but only if paired with urgent execution. They'll wait years for the right acquisition but integrate it in months. They'll study a category for decades before entering but dominate it within years. Patience in strategy, urgency in execution—most companies get this backwards.

The company's capital allocation framework offers a masterclass in value creation. They don't chase growth at any cost or dividends at any yield. Instead, they maintain hierarchy: organic investment first, acquisitions second, dividends third, buybacks last. This discipline ensures growth investments aren't sacrificed for short-term returns while still rewarding shareholders consistently.

The 28-year dividend growth streak reveals another truth: consistency creates its own momentum. Each year of dividend growth attracts more income-focused investors, lowering capital costs, enabling better acquisitions, generating more cash, supporting more dividends. It's a virtuous cycle that accelerates over time, but only if you never break it.

When to Pivot vs. When to Double Down

Church & Dwight's history is punctuated by crucial pivot decisions that seemed obvious in retrospect but were controversial at the time. The 1972 refrigerator deodorizer campaign could have been dismissed as desperate. The 2001 shift to acquisitions could have been seen as admission of organic growth failure. The recent digital brand acquisitions could be viewed as chasing trends.

But examine these pivots closely and a pattern emerges: Church & Dwight pivots tactics, not principles. They changed how they grow but not why. They evolved distribution channels but not operational discipline. They expanded categories but not core values. The lesson: pivot everything except what makes you unique.

The decision to maintain sodium bicarbonate production while building a CPG empire exemplifies this balance. Lesser companies would have divested the "old" business to focus on the "new." Church & Dwight recognized that their chemical expertise provided cost advantages, regulatory knowledge, and acquisition opportunities others lacked. Sometimes the best pivot is no pivot at all.

Building an Acquisition Machine That Creates Value

Most companies destroy value through acquisitions. Church & Dwight creates it consistently. The difference isn't luck—it's system. They've institutionalized every aspect of M&A: identification, evaluation, negotiation, integration, optimization. What looks like intuition is actually encoded experience.

The discipline to walk away might be their greatest acquisition strength. For every deal Church & Dwight completes, they abandon ten. They'll track a target for years, waiting for the right moment. When MidOcean wanted to sell Waterpik, Church & Dwight had been studying the category for a decade. Preparation meeting opportunity looks like luck but isn't.

Integration excellence matters more than acquisition brilliance. Church & Dwight doesn't buy perfect companies—they perfect imperfect companies. They reduce complexity, cut waste, leverage scale, and focus resources. The playbook is boringly consistent: simplify SKUs, optimize marketing, expand distribution, improve operations. No magic, just method.

Why "Boring" Businesses Can Be Beautiful

Church & Dwight has built extraordinary value in ordinary categories. Baking soda, condoms, vitamins—products nobody discusses but everybody needs. These boring businesses offer hidden advantages: stable demand, limited disruption risk, pricing power from brand trust, and acquisition opportunities from disinterested sellers.

The unsexy category strategy works because competition is limited. Venture capitalists don't fund baking soda disruption. MBAs don't dream of revolutionizing foot odor solutions. This lack of competition creates space for Church & Dwight to operate methodically, building dominant positions while others chase glamorous opportunities elsewhere.

Boring businesses also attract boring investors—and that's beautiful. Church & Dwight's shareholder base consists primarily of long-term institutional holders who understand the model. Less volatility, fewer activists, more patience. The investors match the business: steady, rational, focused on compound returns rather than quick wins.

The Meta-Lesson: Excellence Compounds

The overarching lesson from Church & Dwight is that excellence compounds in ways that disruption doesn't. Each year of operational improvement makes the next year easier. Each successful acquisition makes the next one more likely. Each quarter of beating expectations builds more credibility. It's slow, it's boring, and it's incredibly powerful.

This compounding extends beyond financials. Supplier relationships strengthen over decades. Retail partnerships deepen through consistent execution. Employee expertise accumulates through repetition. Brand trust builds through generations. These intangibles don't appear on balance sheets but drive real value.

Church & Dwight also demonstrates that focus beats diversification, but portfolio diversification beats single-product dependency. They focus operationally—one playbook, one culture, one philosophy—while diversifying strategically across categories, channels, and price points. It's focused diversification, an apparent oxymoron that works.

The Ultimate Paradox

Perhaps the deepest lesson is that Church & Dwight succeeded by rejecting the success formulas of their era. When conglomerates were fashionable, they stayed focused. When global expansion was mandatory, they remained domestic. When digital disruption was everything, they bought traditional brands. When growth at any cost was rewarded, they maintained margin discipline.

This contrarian consistency isn't stubbornness—it's confidence. Church & Dwight knows what they are (operational excellence machines) and what they aren't (innovation labs). They play their game, not the market's game. In a world of companies trying to be everything, Church & Dwight prospers by being themselves.

The Church & Dwight story ultimately teaches that building great companies isn't about grand strategies or breakthrough innovations. It's about doing ordinary things extraordinarily well, consistently, for a very long time. It's about compound improvements rather than step-function changes. It's about the democracy of daily execution rather than the aristocracy of strategic brilliance.

In the end, Church & Dwight proves that in business, as in life, the race doesn't always go to the swift or the brilliant. Sometimes it goes to those who simply keep showing up, getting better, and compounding their advantages one boring day at a time. For investors and operators alike, that might be the most valuable lesson of all.

XII. Recent News

The corporate corridors in Ewing are busier than usual in 2025. Rick Dierker, a 15-year veteran of the Company, was promoted to President and Chief Executive Officer (CEO) and elected to the Board of Directors effective March 31, 2025, marking a significant transition for the 179-year-old company. As CFO and Head of Operations, Rick has closely partnered with Matt over the last decade to oversee the development of the Company's strategy and key elements of our operations, helping to accelerate the Company's trajectory and breakthrough performance.

The leadership transition comes at a time of exceptional performance. Full year 2024 net sales increased 4.1% to $6,107.1 million, ahead of the Company's outlook of approximately 3.5% growth. The Company drove strong consumer demand across its portfolio and geographies in 2024. Organic sales increased 4.6% due to higher volume of 3.3% and positive pricing and mix of 1.3%. These results demonstrate the strength of Church & Dwight's evergreen model even amid economic uncertainty.

The quarterly performance through 2024 showed remarkable consistency. In the third quarter, net sales grew 3.8% to $1,510.6 million, with organic sales growth of 4.3%. However, the quarter included significant one-time charges: During the third quarter, the Company recorded non-cash impairment charges of $357.1 million before tax ($270.1 million after tax), on assets related to the Company's 2012 acquisition of our vitamin business (VMS). This write-down of the Vitafusion business reflects the challenges even successful acquirers face with changing consumer preferences.

The financial position remains robust. At September 30, 2024, cash on hand was $752.1 million, while total debt was $2.2 billion. By year-end, At December 31, 2024, total debt was $2.2 billion and cash on hand was $964.1 million, which provides liquidity and flexibility as we continue to pursue acquisitions. This fortress balance sheet enables continued acquisition activity despite higher interest rates.

The most transformative recent news is the Touchland acquisition. Church & Dwight Co., Inc. (NYSE:CHD) has signed a definitive agreement to acquire the Touchland® brand for $700 million at closing, consisting of cash and Church & Dwight restricted stock, and a payment up to $180 million contingent on the achievement of Touchland's 2025 net sales for a total purchase price of up to $880 million. Touchland is the fastest growing brand in the hand sanitizer category in the United States and is the #2 hand sanitizer in the category. The transaction, which is subject to customary closing conditions, is expected to close in the second quarter. Touchland's net sales for the trailing twelve months through March 31, 2025 were approximately $130 million.

The Touchland acquisition represents a departure from Church & Dwight's typical playbook. The deal, expected to close in Q2 2025, meets the company's acquisition criteria: #1 or #2 brand position, asset-light business model, growth potential, and gross margin accretive. The transaction is expected to be neutral to 2025 EPS but 3% accretive to cash earnings in 2026. Touchland's net sales are projected to grow double digits in both 2025 and 2026. This marks Church & Dwight's first major digital-native brand acquisition and its entry into premium hand care.

Q1 2025 results reflected a more challenging environment. Our first quarter net sales decreased 2.4% to $1,467.1 million, below the Company's outlook of approximately 1% growth. However, the Company experienced slowing category growth in the US market and retailers reduced inventory levels. Organic sales decreased 1.2% due to 1.4% lower volume partially offset by positive pricing and mix of 0.2%. Despite the revenue miss, Adjusted EPS was $0.91, a decrease of 5.2%. Adjusted EPS exceeded the Company's outlook of $0.90, demonstrating operational resilience.

Innovation continues driving growth. ARM & HAMMER™ Laundry launched POWER SHEETS™ Laundry Detergent online in August 2023 and was the first major brand in the US to offer a detergent sheet. POWER SHEETS™ quickly became a top 2 selling brand in the Detergent Sheets Category on Amazon in 2024 and is expanding nationally in 2025. This innovative laundry solution is effective, convenient, and eliminates plastic waste. The success of Power Sheets demonstrates Church & Dwight's ability to capture emerging categories while leveraging their brand equity.