Cognex: The Eyes of the Machine Age

I. Introduction: The "Invisible" Monopoly of Sight

Every time you receive an Amazon package, a machine read the barcode on that box at blinding speed—not with a laser, but with an intelligent camera that understood what it was looking at. Every time an iPhone is assembled in Zhengzhou, machine vision systems verify that every connector, every screw, every millimeter of glass meets Apple's exacting tolerances. Every time a Tesla battery pack is inspected for microscopic defects that could cause a thermal runaway, a system is making judgments that no human eye could reliably make at production speed. And in an astonishing number of these cases, the "eyes" belong to the same company: Cognex Corporation.

Cognex is one of those rare businesses that most consumers have never heard of, yet touches nearly every manufactured object they own. With a market capitalization hovering around nine billion dollars and revenues approaching a billion annually, the Natick, Massachusetts-based company has quietly built what amounts to a monopoly on machine sight. Together with its chief rival, Japan's Keyence, Cognex commands nearly half of the global machine vision market—a market projected to grow from roughly sixteen billion dollars in 2025 to nearly twenty-four billion by 2030.

The thesis is deceptively simple: a group of MIT researchers figured out how to teach computers to see, and then spent four decades turning that capability into an indispensable layer of the global supply chain. But the execution of that thesis—the strategic pivots, the cultural choices, the acquisitions, the competitive warfare—is a masterclass in building a durable technology business inside the messy, unglamorous world of industrial automation.

The story moves through three distinct eras. There is the founding era of Dr. Robert Shillman—"Dr. Bob"—a charismatic, eccentric professor who bet his life savings on machine vision and built a culture so distinctive that employees still call themselves "Cognoids." There is the scaling era of Robert Willett, a Danaher-trained operator who took over as CEO in 2011 and grew revenue fivefold by bringing discipline to the chaos. And now there is the emerging era of Matthew Moschner, the company's youngest-ever CEO, who took the reins in mid-2025 with a mandate to make Cognex an "AI-First" company. Each transition tells us something about how great technology companies evolve—and what they must sacrifice to grow.

But before the AI mandates and the billion-dollar revenue targets, there was a professor, a pair of graduate students, and eighty-six thousand dollars.

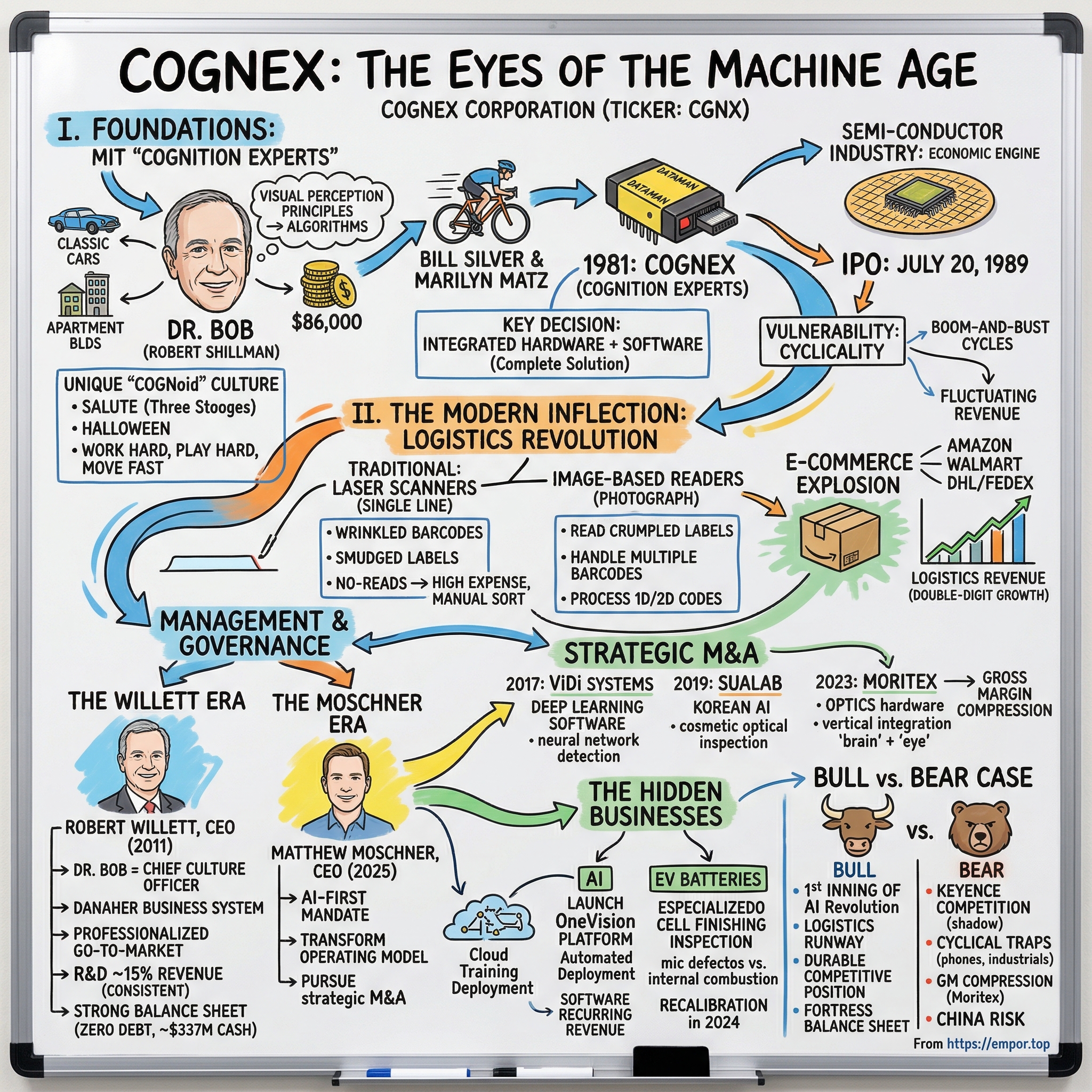

II. Foundations: The MIT "Cognition Experts"

In 1981, Dr. Robert Shillman was a lecturer at MIT, teaching courses on human visual perception—the neuroscience of how our brains interpret what our eyes capture. He was, by all accounts, a brilliant and unconventional academic. But Shillman had a side hustle that gave him something most professors lack: capital. He had spent years buying, restoring, and selling classic cars, and fixing up apartment buildings. By the time he decided to leave academia, he had accumulated roughly eighty-six thousand dollars—his entire net worth, what he sometimes called his "retirement fund."

Shillman's insight was that the same principles governing human vision could be translated into algorithms. If you could teach a computer to recognize patterns, read characters, and identify defects the way a human quality inspector does—but faster, more consistently, and without fatigue—you would have something enormously valuable. The name he chose for his company reflected this ambition: Cognex, short for "Cognition Experts."

He recruited two MIT graduate students, Bill Silver and Marilyn Matz, to join him as co-founders. The pitch was so audacious—leave MIT to build vision software in a tiny office—that Shillman reportedly sweetened the deal by offering each of them a free racing bicycle. It is a founding story that feels almost too perfectly MIT: brilliant, scrappy, and slightly absurd.

The early years were defined by two things: the technology and the culture. On the technology side, Cognex's first product was an optical character recognition system—essentially, a machine that could read printed text on products and components. This was the DataMan, and it represented one of the first commercially viable OCR systems in the world. The key decision Shillman made early on was to integrate hardware and software into a single system rather than selling software alone. This was not the easier path. A software consultancy would have been cheaper to run and faster to market. But Shillman understood that industrial customers needed a complete solution—a box they could plug in and trust. That hardware-plus-software integration philosophy would become a defining competitive advantage for decades.

On the culture side, Shillman built something genuinely unusual for an industrial technology company. Employees were called "Cognoids"—a playful nod to their shared identity as quasi-alien beings dedicated to machine vision. The company's unofficial salute was borrowed from the Three Stooges. Halloween became the unofficial corporate holiday, celebrated with an enthusiasm that would make most HR departments nervous. The motto was "Work Hard, Play Hard, and Move Fast—in that order." The ordering mattered. Shillman was fanatical about results, but he believed that a culture of humor, camaraderie, and genuine weirdness would attract and retain the kind of engineering talent that would otherwise be seduced by the prestige of MIT's research labs or the stock options of Silicon Valley.

This cultural glue proved critical during the company's first major pivot. The general-purpose OCR market turned out to be smaller and more competitive than Shillman had hoped. But one industry was desperate for machine vision: semiconductors. As chip geometries shrank and production volumes exploded in the late 1980s and 1990s, the semiconductor industry needed systems that could inspect wafers, read tiny identification marks, and catch defects invisible to the human eye. Cognex became the "eyes" of the chip-making machines, and the semiconductor industry became the company's economic engine. In 1995, the company acquired Acumen, a developer of wafer identification systems, cementing its position.

Cognex went public on July 20, 1989, and the semiconductor business provided the revenue and credibility to sustain a public-market presence. But it also introduced a vulnerability that would haunt the company for years: cyclicality. The semiconductor industry is notorious for its boom-and-bust capital expenditure cycles. When chipmakers are building new fabs, they buy vision systems by the truckload. When they are not, orders fall off a cliff. Cognex's revenue would swing wildly from year to year, making it a frustrating stock for investors seeking predictability.

The company needed a second act—a market that was large, growing, and less cyclical than semiconductors. It would take nearly two decades to find it, but when it did, the transformation was dramatic.

III. The Modern Inflection: The Logistics Revolution

Somewhere in the late 2000s, a quiet realization began to form inside Cognex's engineering labs: reading barcodes on moving boxes might be a bigger business than inspecting silicon wafers.

To understand why this was revolutionary, you need to understand the state of barcode reading at the time. For decades, the logistics industry—warehouses, distribution centers, sortation facilities—relied on laser scanners to read barcodes on packages. These scanners worked by projecting a thin beam of light across a barcode and measuring the reflections. They were fast, cheap, and adequate for a world where packages moved at moderate speeds and barcodes were generally clean and well-printed.

But the e-commerce explosion changed everything. As companies like Amazon scaled their fulfillment operations to handle millions of packages per day, the limitations of laser scanners became painfully apparent. Laser scanners capture only a single line of data. If a barcode is wrinkled, smudged, partially torn, or oriented at an odd angle—which happens constantly in a high-speed warehouse—the scanner fails. The industry called these "no-reads," and at scale, even a small no-read rate was enormously expensive. A package that cannot be read must be manually sorted, creating bottlenecks, adding labor costs, and slowing throughput. One major fashion retailer found that switching from laser scanners to image-based readers reduced their no-read rate from six percent to under one percent, saving roughly a million dollars per year at a single facility.

Cognex's image-based barcode readers worked on a fundamentally different principle. Instead of a laser line, they captured a full image of the package—essentially taking a photograph—and then used software algorithms to find and decode every barcode in the frame, regardless of orientation, condition, or type. They could read crumpled labels, handle multiple barcodes simultaneously, and process 1D and 2D codes that laser scanners could not touch. The pitch was irresistible: "If a human can read it, the machine can read it. And if a human can't read it, the machine probably still can."

The timing could not have been better. Amazon was building fulfillment centers at a staggering pace. Other e-commerce players—Walmart, JD.com, Alibaba's Cainiao—were racing to keep up. Third-party logistics providers like DHL and FedEx were modernizing their sortation infrastructure. All of them needed vision systems that could handle the chaos of high-speed package handling, and Cognex had exactly the right product at exactly the right moment.

This shift fundamentally changed the character of Cognex as a business. The semiconductor-driven revenue was inherently cyclical, tied to capital expenditure cycles that were largely beyond Cognex's control. But logistics revenue was structural—driven by the secular growth of e-commerce, which showed no signs of slowing. Every new fulfillment center, every warehouse automation project, every sortation line upgrade represented a potential Cognex sale. The company was no longer a cyclical semiconductor play; it was becoming a structural e-commerce and automation play.

By 2024 and 2025, the transformation was undeniable. Logistics delivered double-digit growth in both years, led by large e-commerce customers. The segment had moved from a "hidden" initiative buried in the financial statements to the primary growth engine of the company. Management guided for logistics growth to moderate to mid-to-high single digits in 2026 after two consecutive years of outsized performance—but even that moderation reflected a mature, scaled business rather than a flash-in-the-pan trend.

The strategic implications were profound. Cognex had found a market that was not only large and growing but also played directly to its technical strengths. High-speed barcode reading requires exactly the kind of hardware-software integration, advanced algorithms, and reliability engineering that Cognex had been building for decades. It was, in retrospect, the perfect second act. And it set the stage for a management transition that would determine whether the company could scale from a quirky founder-led firm into a disciplined global enterprise.

IV. Management and Governance: The Willett Era

In March 2011, Robert Willett became CEO of Cognex, and Dr. Bob stepped into a newly created role: Chief Culture Officer. The title was telling. Shillman was not leaving the building—he remained Chairman of the Board—but he was explicitly acknowledging that the company needed a different kind of leader for its next chapter. He would guard the soul; Willett would build the machine.

Willett's background read like a playbook for exactly this kind of transition. Before joining Cognex in 2008 as EVP and President of the Modular Vision Systems Division, he had spent years in the orbit of Danaher Corporation—one of the most admired industrial conglomerates in the world. Willett had been CEO of Willett International, a global coding and marking company, which he sold to Danaher in 2003. After the acquisition, Danaher merged his company into Videojet Technologies, where Willett served as President. He then rose to Group VP of Business Development and Innovation for Danaher's Product Identification group.

For those unfamiliar with the Danaher playbook, it is worth a brief detour. Danaher is famous for the "Danaher Business System"—a relentless, Toyota-inspired approach to continuous improvement, operational efficiency, and disciplined capital allocation. Companies that pass through the Danaher machine tend to emerge leaner, more process-driven, and significantly more profitable. The executives who learn the system carry it with them like a professional DNA. When Willett arrived at Cognex, he brought what might be called "Danaher-lite"—the discipline and operational rigor without the soul-crushing intensity that sometimes characterizes pure Danaher culture.

The results spoke for themselves. During Willett's seventeen-year tenure, Cognex grew revenue roughly fivefold, reaching nearly a billion dollars by 2025. He oversaw the logistics revolution, the deep learning acquisitions, and the Moritex deal. He built out the global sales infrastructure and professionalized the company's go-to-market strategy. Under his watch, Cognex achieved adjusted EBITDA margins above twenty percent a full year ahead of plan, with targets set to reach twenty-five percent by the end of 2026.

But perhaps Willett's most important contribution was structural. He maintained the flat organizational culture that Shillman had built—the Cognoid identity, the irreverence, the emphasis on engineering talent—while layering on the operational frameworks needed to run a global enterprise. He created programs to identify and develop "High-Potential" employees, ensuring that top engineering talent had career paths that did not require leaving for Google or Apple. He kept R&D spending remarkably consistent at roughly one hundred thirty-five to one hundred forty million dollars per year—between fourteen and seventeen percent of revenue—regardless of the business cycle. That consistency is striking. Most industrial companies cut R&D during downturns. Cognex did not. The message was clear: technology leadership is not a discretionary expense.

Willett's own compensation was heavily weighted toward long-term stock performance, with a significant equity stake that aligned his interests with shareholders. The capital allocation philosophy under his watch was disciplined and shareholder-friendly: aggressive share buybacks funded from operating cash flow, a modest but growing dividend, and a fortress balance sheet with zero debt. By the end of 2025, Cognex held over three hundred thirty-seven million dollars in cash and short-term investments against zero debt—a net cash position that gave the company enormous strategic flexibility.

The CEO transition that followed was equally telling. In June 2025, Matthew Moschner—who had joined Cognex in 2017 and risen to President and COO—became CEO at age thirty-seven, making him one of the youngest CEOs in the industrial technology sector. Willett did not disappear; he remained on the Board as Executive Director, providing continuity. The succession was the product of a multi-year planning process, not a crisis or a surprise. Moschner's mandate was explicitly forward-looking: make Cognex an "AI-First" company, transform the operating model, and pursue strategic M&A.

The contrast between the three eras of Cognex leadership is instructive. Shillman provided the vision and the culture—the "why" of the company. Willett provided the scale and the discipline—the "how." Moschner is now tasked with providing the transformation—the "what's next." Each transition preserved what mattered from the previous era while adding what was needed for the next. That is harder than it sounds, and it is one of the reasons Cognex has endured where many founder-led technology companies have not.

For investors, the key question is whether the management team can execute on the ambitious margin and growth targets while simultaneously investing in AI capabilities. The early evidence is encouraging. The twenty-percent EBITDA milestone hit a year early. The cost reduction program is targeting thirty-five to forty million dollars in additional net savings in 2026. And the recent analyst upgrades—Goldman Sachs flipping from a long-held Sell to a Buy in December 2025, JP Morgan upgrading to Neutral in March 2026—suggest that the institutional investment community is increasingly comfortable with the trajectory.

V. M&A Strategy: Buying the Future

Cognex has never been an acquisitive company in the traditional sense. It does not buy revenue. It does not pursue roll-up strategies. It does not do "transformational" mega-mergers. Instead, it does something much harder and much smarter: it buys capability gaps. Every significant acquisition in Cognex's history has been driven by a single question—what can we not build ourselves fast enough, and who has already built it?

The most consequential of these capability acquisitions began in April 2017, when Cognex acquired ViDi Systems, a small Swiss company founded in 2012 by Dr. Reto Wyss. ViDi had developed deep learning software specifically designed for machine vision applications—the ability to train neural networks to detect defects, classify objects, and read characters in ways that traditional rule-based algorithms could not. The deal terms were not disclosed, which typically means the price was modest, likely in the low tens of millions. But the strategic value was enormous. ViDi gave Cognex its first foothold in deep learning at a time when the rest of the industrial automation world was still debating whether AI was relevant to manufacturing.

Think about what ViDi represented. Traditional machine vision works by programming explicit rules: "this edge should be this many pixels wide," "this color should fall within this range," "this shape should match this template." These rule-based systems are powerful for well-defined, repeatable tasks. But they struggle with variability. A scratch on a machined surface might be acceptable in one orientation but not another. A character printed on a rough surface might look different every time. A defect on an organic material like food or wood is inherently irregular. Deep learning flipped the paradigm. Instead of programming rules, you show the system thousands of examples of "good" and "bad," and the neural network learns to distinguish between them on its own. It is the difference between giving someone a rulebook and giving them experience.

Two years later, in October 2019, Cognex made a much larger and more visible bet: the acquisition of SUALAB, a Seoul-based AI firm, for approximately one hundred ninety-five million dollars. SUALAB, founded in 2013, had built deep learning capabilities specifically for cosmetic optical inspection across displays, solar panels, printed circuit boards, and semiconductors. The acquisition brought roughly fifty engineers and substantial intellectual property into the Cognex fold.

The SUALAB price tag raised eyebrows. One hundred ninety-five million dollars for a company with limited commercial revenue was, by industrial automation standards, a Silicon Valley-style valuation. But the logic becomes clearer when you consider the competitive landscape. Keyence, Cognex's primary rival, was investing heavily in its own AI capabilities. Basler, the German camera maker, was moving upmarket. Chinese competitors were emerging with lower-cost alternatives. Cognex needed to lock up the best deep learning talent and IP before someone else did. In this context, the premium was not about paying for revenue—it was about paying for preemption. The alternative—letting SUALAB fall into Keyence's hands—was far more expensive than the acquisition price.

The third major deal—and the most strategically ambitious—came in October 2023 with the acquisition of Moritex Corporation for approximately two hundred seventy-five million dollars in cash. Moritex was a Japanese optics company founded in 1973 with roughly five hundred employees, specializing in machine vision lenses, lighting systems, and optical components. Cognex acquired it from a private equity consortium of Trustar Capital and CITIC Capital.

The Moritex deal represented something new for Cognex: vertical integration of the physical optical stack. Historically, Cognex had focused on the "brain"—the software algorithms and processing hardware that interpret visual data. But the quality of that interpretation depends critically on the "eye"—the lenses and lighting that capture the image in the first place. By acquiring Moritex, Cognex could now optimize the entire chain from photon to decision: the lens captures the light, the sensor converts it to data, and the AI interprets the result. No competitor could offer the same level of integration.

The financial impact was immediate. Moritex added roughly six to eight percent to Cognex's consolidated revenue. However, it also contributed to a compression in gross margins—optics hardware carries lower margins than Cognex's traditional software-heavy business. Gross margins declined from the mid-seventies percent range historically to about sixty-seven percent by 2025. This is a trade-off that the market is still evaluating. The bet is that the integration advantages and cross-selling opportunities will more than compensate for the near-term margin dilution.

More recently, Cognex demonstrated that its M&A strategy is not just about buying—it is also about pruning. In April 2026, the company completed the divestiture of Moritex's Japan-focused trading business, which did not fit Cognex's core vision technology strategy. The company also exited roughly twenty-two million dollars of non-core, low-growth, or low-margin revenue lines including mobile SDK and Edge Intelligence products. This portfolio optimization reflected a maturation in how Cognex thinks about capital allocation: acquire for capability, divest for focus.

The verdict on Cognex's M&A strategy is that it is surgical rather than aggressive. The company rarely buys, but when it does, it buys assets that fill specific technological gaps and that would be dangerous in a competitor's hands. It pays premium prices for premium assets and then works to integrate them into its platform. It is a strategy that requires patience, strong internal R&D capabilities to evaluate targets, and the willingness to accept short-term margin pressure for long-term competitive advantage.

VI. The Hidden Businesses: AI and EV Batteries

There is a version of the Cognex story that most investors know: industrial cameras, barcode readers, factory automation. And then there is the version that is quietly reshaping the company's future: artificial intelligence sold as judgment, and the electrification of the global auto fleet.

The AI story begins with the acquisitions of ViDi and SUALAB, but it has evolved far beyond those foundations. Cognex's deep learning capabilities are no longer a research project or a product extension—they are becoming the centerpiece of the company's software strategy. The In-Sight D900 vision system, launched with embedded deep learning capabilities, allowed factory operators to deploy AI-based inspection without needing data science expertise. But the real breakthrough came in 2025 with the launch of the OneVision Platform.

OneVision represents a philosophical shift in how Cognex sells machine vision. The traditional model required significant on-site engineering: a Cognex application engineer would visit a factory, study the inspection task, configure the vision system, and train the algorithms for that specific application. It worked, but it did not scale. OneVision flips this model. A factory operator can upload images of defective and non-defective parts to a cloud platform, where Cognex's AI models are automatically trained and then deployed back to the factory cameras. The vision system essentially programs itself.

The implications are significant. If OneVision works as intended, it dramatically lowers the barrier to adoption for machine vision. Factories that previously could not justify the cost of a Cognex application engineer can now deploy AI-powered inspection with minimal human intervention. It also shifts revenue toward higher-margin software and recurring cloud services, away from one-time hardware sales. Under CEO Moschner's "AI-First" mandate, this is the strategic direction: make AI capabilities the primary differentiator and revenue driver, with hardware serving as the delivery mechanism.

The EV battery opportunity is equally compelling in theory, though the reality has been more complicated. The transition from internal combustion engines to electric vehicles does not just change the powertrain—it fundamentally changes the quality inspection requirements. A traditional engine block requires vision inspection of machined surfaces and assembly verification. An EV battery pack requires inspection of individual cells—prismatic, pouch, or cylindrical—for microscopic defects that could cause thermal runaway, fire, or catastrophic failure. The inspection density is roughly ten times greater for an EV battery pack than for a comparable internal combustion engine component.

Cognex positioned itself aggressively for this opportunity, developing specialized cell finishing inspection solutions for all major battery form factors. The company entered 2024 with ambitious expectations for EV-related revenue. Those expectations collided with reality. The global EV market, while still growing, hit a period of recalibration in 2024 as automakers pulled back on battery investment timelines, particularly in Europe and North America. Cognex's automotive segment declined fourteen percent that year, and the company fell roughly fifty million dollars short of its initial stretch goals for EV-related revenue.

This shortfall is worth dwelling on because it illustrates a broader tension in the Cognex story. The long-term opportunity in EV battery inspection is real and substantial. Every major automaker is building gigafactories. Every gigafactory will need vision systems. But the timing and pace of that buildout is subject to political, economic, and technological uncertainties that even the best-positioned supplier cannot control. For investors, the EV battery business represents genuine optionality—a potential growth driver that could add hundreds of millions in revenue over the next decade—but it is not yet a reliable contributor to near-term results.

There is also a less visible dimension to the software story that deserves attention. Cognex's high-margin software products—the VisionPro libraries, the deep learning tools, the OneVision platform—are often bundled with hardware sales and buried in consolidated financial reporting. The true profitability of the software business is difficult to isolate from public filings. But the directional trend is clear: as AI-powered software becomes a larger share of the product mix, Cognex's blended margins should improve over time, partially offsetting the dilution from the Moritex hardware integration. This software-hardware dynamic—selling a five-thousand-dollar camera to pull through fifty thousand dollars of high-margin software—is the fundamental economic engine that makes Cognex more of a software company than its industrial classification suggests.

The hidden businesses represent the optionality in Cognex's story. AI-on-the-edge is not a marketing buzzword here; it is a concrete product strategy with real revenue implications. EV battery inspection is a massive addressable market that is still in its early innings despite near-term volatility. Together, they offer a growth trajectory that extends well beyond the company's current logistics and factory automation foundations.

VII. The Frameworks: 7 Powers and 5 Forces

To understand whether Cognex's competitive position is truly durable—or merely the product of a favorable cycle—it helps to apply the structural frameworks that separate temporary advantages from genuine moats.

Hamilton Helmer's 7 Powers

The most potent power in Cognex's arsenal is switching costs. Once a Cognex vision system is integrated into a Ford assembly line or a DHL sortation center, it is not just a piece of hardware sitting on a conveyor belt. It is embedded in the factory's operational workflow, connected to the plant's control systems, and supported by engineers who have been trained on Cognex's proprietary software tools. Switching to a competitor—say, Keyence—does not just mean buying new cameras. It means retraining the engineering staff, rewriting the inspection algorithms, recertifying the production line, and accepting weeks or months of reduced throughput during the transition. For a factory running at high utilization, the cost of that disruption vastly exceeds any potential savings from switching vendors. This is why Cognex's customer retention rates are remarkably high, and why the company's revenue has a degree of recurring-like predictability even though most sales are technically one-time hardware purchases.

The second power is cornered resources. Cognex's proprietary software libraries—VisionPro for industrial inspection, the deep learning algorithms inherited from ViDi and SUALAB—represent intellectual property that has been refined over decades of deployment in thousands of factories worldwide. These are not generic computer vision tools. They are purpose-built for the specific challenges of industrial environments: variable lighting, vibration, dust, extreme temperatures, and the need for microsecond response times. The closest analogy might be ASML's lithography expertise in semiconductors—a body of knowledge so deep and application-specific that it cannot be replicated by throwing money and engineers at the problem.

The third power is scale economies, particularly in R&D. Cognex spends roughly fifteen percent of revenue on research and development—around one hundred forty million dollars per year—more than almost any peer in the machine vision space. Because this R&D investment is amortized across a global customer base spanning dozens of industries, Cognex can afford to develop specialized solutions that smaller competitors cannot justify. Basler, for example, is a strong camera hardware company, but it lacks the software R&D depth to compete with Cognex on AI-powered inspection. The R&D scale advantage is self-reinforcing: more customers generate more data, which improves the algorithms, which attracts more customers.

Porter's Five Forces

The competitive rivalry between Cognex and Keyence is one of the most fascinating dynamics in industrial technology. Both companies are enormously profitable, both command premium prices, and both have loyal customer bases. But they compete in fundamentally different ways.

Keyence wins on distribution and sales force execution. The company employs thousands of direct salespeople worldwide who visit factories relentlessly, demonstrate products in person, and provide immediate technical support. Keyence's model is high-touch, high-volume, and extraordinarily disciplined. If Cognex is the specialist surgeon, Keyence is the world's best general practitioner—capable of handling the vast majority of vision applications with speed and efficiency.

Cognex wins on complexity. When the inspection task is straightforward—reading a barcode, measuring a dimension, checking for presence or absence—Keyence is a formidable competitor with arguably superior go-to-market execution. But when the task involves deep learning, multi-camera coordination, high-speed decision-making, or integration across an entire production line, Cognex's deeper software stack and application engineering capabilities give it an edge. The competitive dynamic is not a zero-sum price war—both companies maintain gross margins above sixty-five percent—but rather a segmentation of the market along a complexity axis.

The threat of substitutes is, counterintuitively, declining rather than increasing. One might expect that cheap cameras and open-source computer vision software would commoditize the machine vision market. In practice, the opposite is happening. As manufacturing becomes more automated, quality tolerances tighten, and product complexity increases, the demand for sophisticated, reliable vision systems is growing. A cheap generic camera running open-source OpenCV might work in a university lab, but it cannot deliver the microsecond latency, nine-nine-nine reliability, and industrial hardening that a high-speed production line demands. The world is moving toward more complexity in machine vision, not less.

The bargaining power of suppliers is moderate. Cognex uses standard electronic components and image sensors from suppliers like Sony, which gives it reasonable sourcing flexibility. The Moritex acquisition actually reduced supplier power by bringing optical component manufacturing in-house.

The bargaining power of buyers is the most nuanced force. Cognex's largest customers—the Amazons, the Apples, the Fords—have enormous purchasing leverage. But they also have enormous switching costs, as discussed above. The result is a dynamic where large customers negotiate hard on price but rarely actually switch vendors. The real risk is concentration: while Cognex does not disclose individual customer names, the logistics segment's reliance on a small number of large e-commerce players creates concentration risk that investors should monitor carefully.

The threat of new entrants is moderate and rising, primarily from China. Chinese machine vision companies are developing capabilities rapidly, often with government support, and competing aggressively on price in their domestic market. Cognex's sixteen percent of revenue from Greater China is exposed to this competitive pressure. However, Chinese competitors have struggled to match the software sophistication and reliability track record that premium customers in North America and Europe demand. The more likely scenario is a bifurcation of the market: Chinese companies dominating lower-complexity applications in Asia, while Cognex and Keyence retain the high-complexity, high-margin segments globally.

VIII. The Playbook: Business and Investing Lessons

Cognex offers several strategic lessons that extend well beyond the machine vision industry. Each one reflects a choice that was not obvious at the time but proved decisive in retrospect.

Hardware as a Trojan Horse for Software

The most important economic dynamic in Cognex's business is one that the financial statements do not fully reveal. On the surface, Cognex looks like a hardware company—it sells cameras, sensors, and barcode readers. But the real value, and the real margin, lives in the software. A Cognex camera might sell for five thousand dollars. The VisionPro software license, the deep learning tools, the application-specific algorithms, and the ongoing software updates can add tens of thousands of dollars in high-margin revenue over the life of the system. The hardware is the Trojan horse—the necessary physical entry point that pulls through a much larger software opportunity.

This model creates a fascinating dynamic. Competitors who focus only on hardware—like Basler—are competing on a dimension that Cognex is increasingly willing to commoditize. And competitors who focus only on software—like various AI startups—lack the industrial-grade hardware platform to deliver their algorithms into factory environments. Cognex's integration of both, deepened by the Moritex acquisition, creates a full-stack offering that is difficult to unbundle.

The Fast Follower in M&A

Cognex has perfected a particular approach to technology acquisition that might be called "industrial fast following." The company does not invest in speculative, early-stage research. It does not build internal AI labs from scratch. Instead, it lets startups and academic researchers de-risk new technologies—deep learning, advanced optics, edge computing—and then acquires the winners once the technology is proven. ViDi and SUALAB were both founded by researchers who spent years developing deep learning for industrial vision before Cognex stepped in to "industrialize" their work.

This approach requires two capabilities that are rare in combination: the technical sophistication to evaluate which startups have genuinely differentiated technology, and the operational discipline to integrate acquisitions without destroying the innovation that made them valuable. Cognex has demonstrated both. The ViDi technology is now embedded across the product line. The SUALAB engineers have been integrated into the R&D organization. The Moritex optics are being cross-sold with Cognex vision systems. Each acquisition has been digested and deployed, not just warehoused.

Culture as a Moat

The Cognoid culture is not just a quirky footnote in the Cognex story—it is a genuine competitive advantage. In an industry where the scarcest resource is engineering talent, Cognex competes for the same graduates as Google, Apple, Amazon, and dozens of well-funded AI startups. It cannot match their compensation packages dollar for dollar. What it can offer is something that many engineers value even more: a sense of belonging to something distinctive, a culture that rewards creativity and tolerates eccentricity, and the opportunity to work on problems where their software runs physical machines in the real world.

The High-Potential employee development program that Willett built ensures that top talent has clear advancement paths. The consistent R&D spending—never cut during downturns—signals that engineering is the priority, not an expense to be managed. And the Cognoid identity itself, however goofy it may sound to outsiders, creates an in-group loyalty that reduces turnover and preserves institutional knowledge. In a business where the most valuable assets walk out the door every evening, culture is not a soft concept—it is an economic moat.

Capital Allocation: The Fortress Balance Sheet

Cognex's approach to capital allocation is a case study in patience and discipline. The company has maintained a zero-debt balance sheet for years, carrying hundreds of millions in cash and short-term investments at all times. As of the end of 2025, the balance sheet held over three hundred thirty-seven million in cash against zero debt, giving the company a net cash position of nearly two hundred million even after accounting for lease obligations.

This fortress balance sheet serves multiple strategic purposes. It provides the financial flexibility to pursue acquisitions—like the two-hundred-seventy-five-million-dollar Moritex deal—without taking on debt or diluting shareholders. It provides a cushion during cyclical downturns, allowing Cognex to maintain R&D spending and engineering headcount when competitors are cutting. And it provides the confidence to pursue aggressive share buybacks. In February 2026, the board authorized an additional five hundred million dollars in buyback capacity, bringing total available repurchase authority to six hundred fifty million. Since the previous program began, the company retired over eight million shares—nearly five percent of shares outstanding—for three hundred thirty-six million dollars.

The buyback strategy is particularly noteworthy because it has been executed through cycles rather than just at market peaks. Cognex has been a consistent buyer of its own stock in both good times and bad, suggesting genuine conviction in the long-term value of the business rather than mere financial engineering.

IX. Bull vs. Bear Case and Synthesis

The Bear Case: The Keyence Shadow and Cyclical Traps

The most persistent bear argument against Cognex centers on Keyence. The Japanese giant is larger, more profitable, and arguably has superior go-to-market execution. Keyence's direct sales model—thousands of sales engineers visiting factories daily—creates a distribution advantage that Cognex cannot easily replicate. If Keyence decided to compete aggressively on price in the logistics segment, it could compress Cognex's margins significantly. Keyence has historically competed on value rather than price, but the possibility remains a structural overhang.

The cyclicality concern is also real. Despite the logistics diversification, Cognex remains exposed to capital expenditure cycles in semiconductors, automotive, and consumer electronics. The "smartphone cycle"—essentially, the Apple upgrade cadence and its impact on Asian consumer electronics manufacturing—still moves the needle on revenue. The sharp decline from the 2021 revenue peak of over one billion dollars to eight hundred thirty-eight million in 2023 was a reminder that Cognex is not immune to industrial downturns.

Gross margin compression is another concern that merits attention. The decline from the mid-seventies to roughly sixty-seven percent, driven partly by the Moritex hardware integration and partly by product mix shifts, is significant. If margins stabilize at current levels rather than recovering, the long-term earnings power of the business is lower than historical models suggest. Management's cost reduction initiatives and software mix improvement need to deliver on their promises.

China risk is concentrated and growing. With sixteen percent of revenue from Greater China, Cognex is exposed to both geopolitical tensions—tariffs, export controls, technology restrictions—and competitive pressure from domestic Chinese rivals. The April 2026 tariff-driven market selloff was a tangible reminder of this exposure.

Finally, the valuation itself incorporates significant optimism. At roughly seventy-eight times trailing earnings, Cognex is priced for substantial earnings growth. If the recovery stalls, if the AI-First strategy takes longer than expected to generate returns, or if the EV battery opportunity remains delayed, the stock could face a meaningful re-rating.

The Bull Case: Inning One of the AI-on-the-Edge Revolution

The bull case begins with a simple observation: the world is still overwhelmingly uninspected. The vast majority of manufactured goods are produced without machine vision. Most warehouses still rely on manual processes or basic automation. The penetration of AI-powered inspection is in its earliest stages. If Cognex can become the default platform for machine vision—the "Windows" of industrial sight—the current revenue base represents a tiny fraction of the addressable market.

The AI-First strategy under Moschner is the catalyst that could unlock this potential. The OneVision Platform, with its cloud-based training and automated deployment, addresses the single biggest barrier to machine vision adoption: the need for specialized engineering expertise. If OneVision can make AI-powered inspection as easy to deploy as installing a smartphone app, the addressable market expands dramatically—from the thousands of factories that can afford Cognex application engineers to the millions of factories and warehouses that cannot.

The logistics opportunity has room to run. E-commerce penetration continues to grow globally, warehouse automation is still in its middle innings, and the integration of AI-based quality inspection into logistics workflows—not just barcode reading, but package damage detection, dimensional verification, and automated routing—represents a natural extension of Cognex's existing capabilities.

The competitive position, as analyzed through both Porter's Five Forces and Helmer's 7 Powers, is genuinely durable. Switching costs, cornered resources in proprietary AI algorithms, and R&D scale economies create multiple reinforcing advantages. The full-stack integration—from Moritex optics to Cognex AI software—is something no competitor can currently match.

The balance sheet provides both defensive resilience and offensive optionality. With over three hundred million in cash, zero debt, and board-authorized buyback capacity of six hundred fifty million, Cognex can simultaneously weather downturns, pursue acquisitions, and return capital to shareholders. The recent wave of analyst upgrades—Goldman Sachs' flip from Sell to Buy, JP Morgan's upgrade, HSBC's positive initiation—suggests that institutional sentiment is turning.

The KPIs That Matter

For investors tracking Cognex's ongoing performance, three metrics cut through the noise and reveal the health of the business.

First, logistics revenue growth rate. This is the single best indicator of whether Cognex's structural transformation from a cyclical semiconductor play to a secular automation play is holding. Double-digit growth signals continued e-commerce adoption and market share gains. A sustained deceleration below mid-single digits would suggest the logistics opportunity is maturing faster than expected.

Second, adjusted EBITDA margin trajectory. Management has laid out a clear path from the twenty-one-percent level achieved in 2025 to a target of twenty-five to thirty-one percent through the cycle. This metric captures the combined impact of cost reductions, software mix improvement, Moritex integration, and operating leverage. It is the clearest measure of whether the management team is executing on its profitability commitments.

The Narrative Conclusion

Cognex is not a camera company. It is not even, really, a machine vision company—though that is what it says on the label. It is a certainty company. It sells the ability for a global economy to run at a hundred times human speed without making mistakes. Every package sorted, every chip inspected, every battery cell verified—each one represents a moment where a Cognex system provided certainty that a human could not.

The company sits at the intersection of three massive secular trends: the automation of manufacturing, the digitization of logistics, and the deployment of AI at the edge. Its competitive moats—switching costs, proprietary AI, R&D scale, full-stack integration—are deep and reinforcing. Its balance sheet is pristine. Its management transition has been orderly and thoughtful. And its addressable market is growing, not shrinking.

The risks are real—Keyence competition, cyclical exposure, China risk, valuation—and they deserve careful monitoring. But the structural position is one that few industrial technology companies can claim. Cognex has spent forty-five years learning to see. The question now is whether the world is ready to look through its eyes.

X. Epilogue

Under its new leadership, Cognex enters 2026 with a clear strategic identity and an ambitious agenda. Matthew Moschner's AI-First mandate is not a pivot—it is an acceleration of a trajectory that began with ViDi nearly a decade ago. The operating model transformation, targeting thirty-five to forty million dollars in additional cost reductions, is designed to fund AI investment while expanding margins. The M&A pipeline is active, with management signaling that capability-driven acquisitions remain a priority.

Robert Willett remains on the Board, providing institutional memory. Dr. Bob, now Chairman Emeritus and Adviser, still embodies the cultural DNA that makes Cognex distinctive. His "Work Hard, Play Hard, Move Fast" philosophy—once the mantra of a scrappy startup in a thousand-square-foot office—has proven durable enough to guide a company approaching a billion dollars in revenue and nine billion in market capitalization.

The machine vision market is projected to grow at over eight percent annually through 2030, driven by manufacturing automation, e-commerce logistics, AI adoption, and the electrification of transportation. Cognex is positioned at the center of all four trends. Whether it captures its share of that growth—and whether the market rewards it for doing so—will depend on execution in AI, discipline in capital allocation, and the ability to maintain the cultural vitality that has defined the company since three MIT researchers and a pair of racing bicycles started it all.

The machine that sees is the machine that builds the future. Cognex intends to be its eyes.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube