CF Industries: The Sovereign of North American Nitrogen

I. Introduction & Episode Roadmap

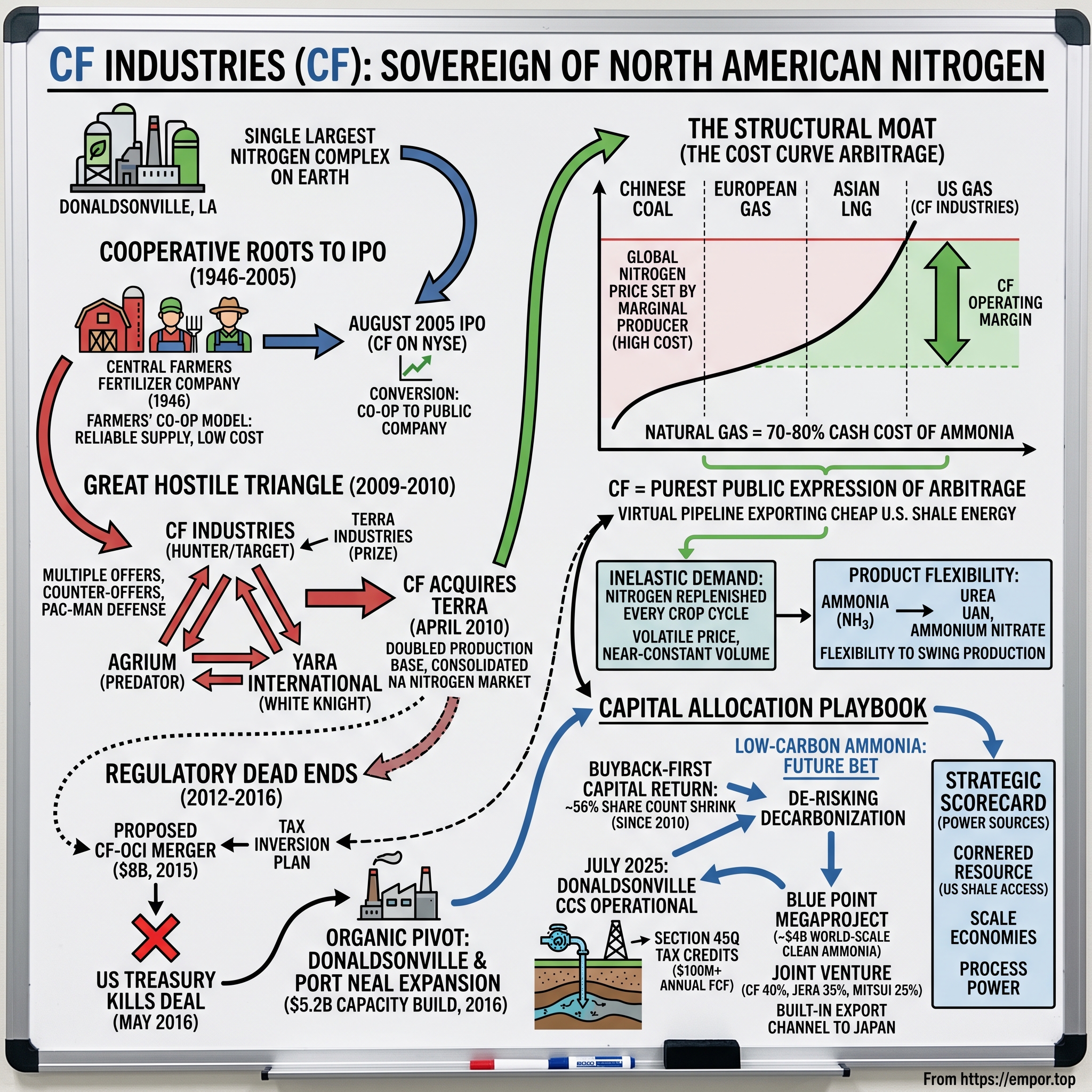

Picture a chemical plant the size of a small city rising out of the sugarcane flats along the Mississippi River in Ascension Parish, Louisiana. Steam plumes drift off cracking towers; a lattice of pipe racks carries superheated gas between reformers; ocean-going vessels and mile-long unit trains queue at the fence line. This is Donaldsonville — the single largest nitrogen complex on the planet — and on any given day it is quietly performing one of the most lucrative acts of arbitrage in American industry: turning cheap molecules of shale gas pulled out of the ground a few hundred miles away into fertilizer that the rest of the world is desperate to buy at prices set by producers paying five to ten times as much for the same raw material.

The company that owns it, CF Industries Holdings, does not look like a growth stock and never has. It sells a commodity that has existed in essentially its current chemical form since before the First World War. Its customers are farmers and agricultural retailers. Its product volatilizes into the air and washes into rivers. And yet in fiscal year 2025 this unglamorous business generated net sales of roughly $7.08 billion, adjusted EBITDA of $2.89 billion, and net earnings attributable to common stockholders of $1.46 billion — about $8.97 per diluted share — while converting more than $1.7 billion of that into free cash flow.1 For a company whose entire physical output could be described as "nitrogen and water," those are remarkable numbers.

The thesis worth interrogating over the next two hours is deceptively simple. CF is the purest publicly traded expression of a structural cost-curve arbitrage: it converts North American natural gas into globally traded crop nutrients, effectively acting as a virtual pipeline that exports cheap U.S. shale energy in molecular form. When the spread between American gas and European or Asian gas is wide, CF captures nearly the entire gap as operating margin, because the global price of fertilizer is set by the highest-cost producer still needed to balance supply. When the spread narrows, so does the magic. Everything else — the M&A history, the buybacks, the decarbonization pivot — is a variation on that single melody.

But a melody is not a fortress, and the honest question is whether this advantage is permanent or merely cyclical dressed up as structural. To answer it, this story walks three epics. The first is the Great Hostile Triangle of 2009–2010, a cinematic, year-long M&A brawl involving CF, Terra Industries, Agrium, and Norway's Yara that nearly ended with CF itself being swallowed — and instead ended with CF consolidating the North American nitrogen market. The second is the inversion that wasn't: an $8 billion cross-border merger with OCI N.V. that the U.S. Treasury killed in 2016, forcing CF to bet the company on a massive organic expansion instead. The third is the de-risking of decarbonization, in which CF is using the Inflation Reduction Act's 45Q tax credits to turn carbon capture from ESG public relations into hard, low-risk cash flow.

Before diving in, it is worth naming the central myth this story has to puncture, because it distorts how many investors approach CF. The myth is that CF is a boring, low-quality commodity business whose good years are simply luck — a producer of an undifferentiated product with no control over its own destiny, riding a gas-price wave it happened to be standing in front of. The reality is more interesting and more uncomfortable: CF is a genuinely low-cost, high-return operator whose margins are cyclical but whose cost position is structural, run by a management team that has, for better and worse, made a series of deliberate, aggressive, sometimes contrarian capital decisions that shaped the outcome. The luck is real — no one at CF drilled the Marcellus shale or started a European energy war — but so is the skill in converting that luck into permanent per-share value. Getting the balance between the two right is the first act of analysis on this company, and most casual observers get it wrong in one direction or the other.

The core question underneath all of it: can a cyclical commodity producer command a permanent structural premium, or will global energy rebalancing and a capital-intensive pivot to clean hydrogen eventually erode the moat that today looks unassailable? Let's start not with the company, but with the chemistry — because you cannot understand CF's economics without understanding the reaction that sits at the heart of the modern world's food supply.

II. The Haber-Bosch Legacy & Industrial Nitrogen Economics

There is a reasonable argument that the single most important industrial chemical reaction ever discovered is one almost no consumer has heard of. In 1909, the German chemist Fritz Haber demonstrated that atmospheric nitrogen ($N_2$) — inert, abundant, making up 78% of the air we breathe but biologically useless in that form — could be forced to combine with hydrogen ($H_2$) under crushing pressure and temperature to make ammonia ($NH_3$). Carl Bosch then industrialized it at BASF. The Haber-Bosch process is the reason roughly half the nitrogen atoms in your body arrived there via a factory rather than a bacterium. Take it away and the planet feeds perhaps four billion people instead of eight.

For an investor, the interesting part is not the Nobel-winning chemistry but the economics that flow from it. Making ammonia requires hydrogen, and the cheapest industrial source of hydrogen is natural gas — methane, $CH_4$. Here is the crucial subtlety: in a nitrogen plant, natural gas is not merely the fuel that heats the reaction. It is the physical feedstock, the actual source of the hydrogen atoms that get married to nitrogen. That dual role is why natural gas represents somewhere between 70% and 80% of the cash cost of manufacturing ammonia.2 A nitrogen producer is, in the most literal sense, a machine for converting gas into fertilizer. Its profitability is a leveraged bet on the price of that one input relative to what competitors pay for theirs.

Ammonia is the mother molecule. Everything else in the nitrogen world is a downstream derivative of it. React ammonia with carbon dioxide and you get urea, the most transportable and globally traded solid nitrogen fertilizer. Dissolve urea and ammonium nitrate together in water and you get UAN — urea ammonium nitrate — a liquid prized by American corn farmers for how evenly it can be sprayed. React ammonia with nitric acid and you get ammonium nitrate. Strip and purify a stream and you can sell diesel exhaust fluid to trucks. But it all begins with $NH_3$, which means it all begins with gas.

Now the demand side, which is where nitrogen quietly diverges from its fellow crop nutrients in a way that matters enormously. Farmers apply three primary macronutrients: nitrogen, phosphate, and potash. Phosphate and potash bind to soil particles; they linger in the ground, so in a bad year a farmer can skip a season's application and draw down the soil bank without much penalty. Nitrogen does not cooperate. It volatilizes into the atmosphere and leaches away with the rain, so it must be replenished every single crop cycle, without exception, or yields collapse. That single agronomic fact converts what looks like a boom-bust commodity into something with a stubbornly recurring, remarkably inelastic demand profile. Farmers argue about price; they do not argue about whether to apply nitrogen.

It is worth dwelling on why that inelasticity is so valuable to an equity investor, because it inverts the usual commodity anxiety. In most commodities, the terror is demand: a recession, a substitution, a technology shift can hollow out the order book overnight. Nitrogen is close to immune to that. Global grain consumption grinds upward with population and rising protein diets, and the agronomy forbids skipping. What varies is not whether the world applies nitrogen but at what price — and price volatility, unlike demand destruction, is something a low-cost producer can actually exploit. When prices spike, CF earns spectacularly; when they fall, the tonnage still moves because it must. That asymmetry — volatile price, near-constant volume — is the quiet reason nitrogen producers can survive cycles that would bankrupt a producer of something genuinely discretionary.

The final piece is how the price gets set. Nitrogen fertilizer is a globally fungible commodity shipped in bulk across oceans, which means no single producer sets the price — the market does, and it does so at the cash cost of the marginal producer, the highest-cost ton of supply still required to satisfy the last increment of demand. Historically that marginal ton has come from a coal-based producer in China or a gas-importing producer in Europe. When those high-cost producers face expensive feedstock, the global clearing price rises to keep them solvent — and a low-cost producer sitting far down the cost curve pockets the difference.

The China piece deserves a moment, because for years it was the single most important swing factor in the global nitrogen market and the source of the 2015–2016 glut that so punished CF. China built enormous coal-based urea capacity, and when Beijing encouraged exports, that high-cost supply flooded the seaborne market and dragged down the global price — hurting everyone, including low-cost CF. When Beijing instead restricts exports to keep fertilizer at home for its own food security, that marginal supply vanishes from the world market and prices firm. The upshot is that CF's fortunes have long been partly hostage to Chinese industrial and agricultural policy — a producer half a world away, burning a different fuel, setting the price at which Louisiana ammonia clears. Understanding that is essential to understanding why a "structural" advantage can still produce wildly variable annual profits: the cost position is stable, but the marginal ton that sets the price is set by policy decisions in Beijing and energy markets in Europe that no one at CF's suburban Chicago headquarters controls. That is the entire game, and it is why the story of CF is, at bottom, the story of where it sits on that curve. To understand how it got there, we have to go back to a farmers' cooperative founded in the shadow of the Second World War.

III. The Cooperative Roots to IPO (1946–2005)

CF Industries did not begin life as a profit-maximizing enterprise. It began in 1946 as Central Farmers Fertilizer Company, a federation of regional agricultural cooperatives that banded together for a single, unglamorous purpose: to guarantee their member-owners — the co-ops, and behind them the farmers — a reliable supply of plant nutrients at the lowest possible cost.3 For nearly six decades that was the whole mission. CF was not trying to earn a return on equity. It was a buyers' club with factories, a supply-assurance utility owned by the very people who consumed its output. Profit, in the ordinary corporate sense, was almost beside the point; the "dividend" was cheap, dependable fertilizer showing up when the planting window opened.

That model worked beautifully in a world of stable, domestic agriculture. It worked far less well once fertilizer became a globalized, capital-intensive commodity business in which staying competitive meant building world-scale plants costing billions of dollars. The late-1990s and early-2000s farm depression exposed the flaw. A cooperative exists to minimize cost for its members, not to accumulate capital, which makes it chronically under-capitalized precisely when the industry demands enormous, cyclical investment. CF's owner-members wanted cheap fertilizer today; the business needed retained earnings and access to public markets to survive tomorrow. Those two imperatives could not both be satisfied inside a co-op structure.

The resolution came in August 2005, when CF Industries Holdings reorganized out of its cooperative skin and listed on the New York Stock Exchange. The IPO priced roughly 47.4 million shares at $16.00 each and delivered net proceeds of about $715 million after underwriting discounts, and in the same reorganization the company formally ceased to be a cooperative — winding down the legacy supply contracts that had bound it to its member-owners.3 In one transaction, a buyers' club became a public commodity producer answerable to outside shareholders rather than to the farmers buying its product.

To appreciate why this transition was so wrenching, it helps to sit inside the cooperative's dilemma at the turn of the millennium. A co-op's members do not want the enterprise to be rich; they want their own farms to be, and every dollar the central organization retains to reinvest is a dollar not passed back to members as lower prices. That is a fine arrangement when the capital intensity of the business is manageable. But nitrogen production had become a game of billion-dollar world-scale plants, ocean logistics, and multi-year cyclical swings that could wipe out a thinly capitalized producer in a single bad stretch. The member-owners were being asked, in effect, to behave like patient institutional investors — to forgo cheap fertilizer now so the enterprise could build war-chest capital for later — which is precisely the thing a cooperative structure is designed not to do. The mismatch was structural, not a failure of will.

The 2005 listing resolved it by changing who the owners were. Public shareholders want return on capital; they are perfectly happy for the company to retain earnings and build scale if it compounds their equity. Overnight, CF acquired an owner base whose interests aligned with the capital-hungry reality of the industry. This is the underappreciated genius of the reorganization: it did not just raise $715 million, it swapped one set of owners with one objective for another set with the opposite objective, and in doing so unlocked the company's ability to act like the aggressive consolidator it would become within four years.

It is worth pausing on what that conversion actually changed, because it is the hinge of everything that follows. As a cooperative, CF's incentive was to sell fertilizer to its members as cheaply as possible. As a public company, its incentive inverted completely: sell as dear as the market allows and return the surplus to shareholders. The same plants, the same molecules, the same cost-curve position — but a diametrically opposed objective function. The newly public CF would spend the next twenty years learning to exploit the structural advantage its cooperative founders had built almost by accident: a fleet of North American plants sitting on top of what would soon become the cheapest natural gas in the industrial world. First, though, it would have to survive being hunted.

IV. The Great Fertilizer Wars of 2009–2010: The Hostile Triangle

Every industry has one deal era that old hands still talk about, and for North American nitrogen it is the fourteen-month brawl that ran from January 2009 to April 2010. It had four players and the structure of a chess endgame in which every piece was simultaneously attacker and target. CF Industries was the newly public challenger, hungry for scale. Terra Industries was the prize — a pure-play nitrogen producer with a coveted footprint in the U.S. Corn Belt. Agrium, the Canadian retail-and-wholesale giant that would later merge into Nutrien, was the predator circling CF. And Yara International, the Norwegian state-linked global nitrogen champion, would enter late as a would-be white knight.

The opening move came in January 2009, when CF launched an unsolicited, all-stock bid to acquire Terra — an offer valuing Terra at roughly $2.1 billion, which Terra's board promptly rejected as far too low. That rejection might have ended things. Instead, it triggered one of the more audacious counter-moves in M&A history. In February 2009, Agrium turned the board around: rather than let CF bulk up by swallowing Terra, Agrium launched its own hostile bid for CF, initially valuing the company at about $3.6 billion — on the explicit condition that CF abandon its pursuit of Terra.5 It was a corporate "pac-man" defense in reverse: the hunter trying to devour its prey before the prey could devour someone else.

For the better part of a year, CF's management fought a two-front war — beating back Agrium's advances while sweetening its own offers for Terra. Agrium escalated relentlessly, eventually raising its bid for CF to roughly $5.43 billion and, at one point, persuading a majority of CF's shareholders to tender into its offer.5 CF's board held the line, arguing the price still undervalued the strategic logic of a consolidated North American nitrogen platform. By January 2010, exhausted and unable to close on Terra at a price Terra's board would accept, CF formally withdrew its bid. The war looked over, and CF looked like the loser.

Then came the twist. In February 2010, Yara stepped in as Terra's white knight, signing a friendly agreement to acquire Terra for about $4.1 billion. Cornered and seemingly out of the game, CF chose to blow up the board. In March 2010 it launched a binding, largely cash offer directly to Terra's shareholders — ultimately worth roughly $4.6 billion — that Terra's board was compelled to declare a "superior proposal."4 Terra broke its contract with Yara, paid the Norwegians a breakup fee of about $123 million for their trouble, and delivered itself to CF.5 With the prize gone, Agrium withdrew its hostile bid for CF, and by April 2010 the smoke cleared: CF had acquired Terra, doubled its production base, and emerged not as the hunted but as the consolidator.

Step back and look at the mechanics of that final move, because it is a small masterclass in how M&A law actually works. Terra's board had signed a binding agreement with Yara, but under Delaware fiduciary doctrine a board cannot simply ignore a demonstrably better offer that lands before the deal closes — its duty runs to shareholders, not to the counterparty it happened to sign with first. By structuring its March 2010 bid as a binding, largely cash proposal at a clearly superior value, CF forced Terra's directors into a corner where declaring it a "superior proposal," paying Yara its contractual breakup fee, and switching partners was arguably the only defensible choice. CF did not persuade Terra's board so much as it removed the board's discretion to say no. It was aggressive, expensive, and completely within the rules — the kind of move that earns a reputation, and CF's willingness to play the game to its final square is part of what made the company feared in subsequent negotiations.

The strategic meaning of the Terra deal is hard to overstate, and it is the single most important inflection point in CF's modern history. It eliminated the most logical domestic competitor, added five major production complexes, and — critically — gave CF the scale it would need to exploit the shale gas revolution that was, at that very moment, beginning to collapse North American natural gas prices. A company that a year earlier had nearly been absorbed by a Canadian rival now controlled the largest nitrogen footprint on the continent, just as the continent's feedstock was about to become the cheapest on Earth. Timing, in commodities, is often indistinguishable from genius. But CF's leadership was about to learn that not every ambitious deal survives contact with the government.

V. Regulatory Dead Ends and the Organic Pivot (2012–2016)

Flush with the confidence of the Terra victory and watching the shale boom widen its cost advantage year after year, CF's management set its sights on a far grander prize in the mid-2010s: global scale, achieved through financial engineering as much as industrial logic. The vehicle was to be a roughly $8 billion combination with the European, North American, and global distribution assets of OCI N.V., the sprawling nitrogen and construction empire controlled by the Egyptian billionaire Nassef Sawiris.

The deal was seductive on two levels. Industrially, it would have knitted together a fertilizer colossus spanning both sides of the Atlantic. Financially — and this was the part that made bankers salivate and regulators bristle — it was structured as a tax inversion. By combining with OCI's assets and relocating its corporate domicile to the United Kingdom, CF would have shed a large chunk of its U.S. corporate tax burden, boosting per-share earnings without selling a single additional ton of fertilizer. In the 2014–2015 window, inversions were the fashionable arbitrage of corporate America, with Pfizer's proposed merger with Allergan the marquee example.

Washington had other ideas. In April 2016, the U.S. Treasury and the IRS issued aggressive new anti-inversion regulations explicitly designed to strip the tax benefit out of exactly this kind of transaction — rules that, in the same stroke, killed the Pfizer-Allergan deal. The economic rationale for the CF-OCI combination evaporated overnight. In May 2016, the two companies mutually terminated the transaction, and CF was left to pay OCI a $150 million termination fee and to write off tens of millions more in transaction and bridge-financing costs.6 For a management team that had won the Terra war by out-maneuvering everyone, being beaten by a rule change from the Treasury was a bracing lesson in the limits of corporate cleverness.

Denied global scale by inorganic means, CF did the only thing left: it doubled down on the ground it already owned. Even as the OCI drama played out, the company was completing a monumental organic expansion — roughly $5.2 billion of new capacity at its flagship Donaldsonville, Louisiana, and Port Neal, Iowa, complexes, finished in late 2016.[^7] It was the largest capital project in company history, a bet-the-balance-sheet wager that the cheapest way to grow was simply to build more plants on top of America's cheap gas rather than to buy someone else's.

There is a deeper lesson in the failed inversion than "the government can change the rules," and it is about the difference between financial and industrial value creation. The OCI deal's headline appeal was a tax rate, not a better fertilizer business — the industrial logic of combining the assets was real but secondary to the domicile arbitrage. When the tax benefit vanished, so did most of the deal's rationale, which tells you how much of the value had been financial engineering rather than operating synergy. CF's subsequent behavior suggests the management team internalized that lesson: everything it has done since — the organic build, the risk-shared Blue Point structure, the buyback-first capital return — has been about industrial and per-share value rather than balance-sheet cleverness. Sometimes the most useful thing a failed deal does is inoculate a company against the temptation that produced it.

The timing looked, at first, like a disaster. The new capacity came online in 2015–2016 precisely as global fertilizer prices crashed under a wave of Chinese oversupply. CF had spent billions to expand into a glut; the stock languished, and skeptics openly wondered whether management had destroyed shareholder value at the top of the cycle. This is the crucible of the bear case, and it deserves to be taken seriously: for a multi-year stretch, CF looked exactly like a capital-allocation cautionary tale — a company that overpaid to grow, botched a financial-engineering scheme, and got punished for it. What the skeptics could not yet see was that the very assets drawing their scorn were about to become the engine of one of the great cash harvests in industrial history. The reason why lies in a spread between two obscure natural gas indices.

VI. The Structural Moat: Shale Gas Economics & Feedstock Spreads

Here is the number that explains almost everything about why CF prints cash. It takes roughly 33 MMBtu of natural gas to manufacture one metric ton of ammonia. That conversion ratio is fixed by chemistry; it is essentially the same for CF as for a competitor in Germany or China. What is not fixed — what varies wildly by geography and by year — is the price of those 33 units of gas. And in that variance lives the entire moat.

Consider the arithmetic. North American producers like CF buy gas indexed to Henry Hub, the U.S. benchmark, which for much of the shale era has traded in a $2.00–$3.00 per MMBtu band. At $2.50, the raw-material cost of the gas going into a ton of ammonia is about $82.50. Now look at a European competitor buying gas at the Dutch Title Transfer Facility (TTF) benchmark, which after 2022 repeatedly spiked into the $15–$30+ range as the continent scrambled to replace Russian pipeline supply. At $15, that same ton of ammonia carries a gas cost of roughly $495 — six times CF's. Asian producers fare little better, reliant on high-cost imported LNG priced off the Japan-Korea Marker (JKM) or, in China's case, on coal gasification that is both dirtier and often more expensive still.

Now recall the pricing mechanism from earlier: the global market clears at the cash cost of the marginal, high-cost producer. When a European or Chinese producer needs, say, $400 per ton of ammonia-equivalent revenue just to cover feedstock and stay in the market, the global price rises to meet that need — and CF, whose feedstock cost is a fraction of that, banks the enormous difference as operating margin. CF is not out-selling anyone or out-marketing anyone. It is simply standing at the bottom of the cost curve while the price is set at the top, harvesting the gap. This is the mechanism that transforms a boring commodity into 40%-plus EBITDA margins, and it is why the Donaldsonville and Port Neal expansions that looked so foolish in 2016 became money machines by 2021.

The obvious analytical caution is that a moat made of a spread is only as durable as the spread. CF does not control Henry Hub, TTF, or JKM. Its super-normal margins are a function of a gap it did not create and cannot defend — a gap that widened dramatically after 2022 for reasons (a European energy crisis, a war) that had nothing to do with CF's operational skill. An investor has to hold two ideas at once: the cost advantage is real and structural in that North American gas is genuinely and persistently cheaper, but the size of the profit it generates is cyclical and partly a windfall. The company's job is to convert windfall years into permanent per-share value before the spread reverts. Whether it has done so is the subject of the next section.

How that margin translates into product is worth grounding in the actual segment mix. In fiscal 2024 — a more normalized year than the 2022 peak — CF's ammonia segment sold about 4.09 million product tons for roughly $1.74 billion, the pure foundation of the chemical stack sold directly to farmers and industrial users. Granular urea contributed about 4.52 million tons and $1.60 billion, the globally transportable workhorse. UAN, the liquid favored in the Corn Belt, added about 6.77 million tons and $1.68 billion. Ammonium nitrate chipped in $419 million, and a catch-all "other" category — led by diesel exhaust fluid — another $503 million.2 By fiscal 2025, with prices firmer, the same portfolio scaled up sharply: ammonia revenue rose to roughly $2.18 billion and UAN to $2.16 billion, with urea at about $1.78 billion.1 The mix tells you CF is not a one-product bet but a flexible nitrogen refinery — and, as we will see, that flexibility to swing production toward whichever derivative is most valuable on a given day is itself a quiet source of margin.

That flexibility is more concrete than it sounds. On the May 2026 earnings call, management described being able to shift a plant between producing urea and UAN within a single eight-to-ten-hour shift, chasing whichever product carried the better margin that week — and, when urea prices ran well ahead of UAN, doing exactly that.[^9] A company that can re-point its output at the most valuable molecule in real time is capturing a spread that a single-product plant simply cannot. The same logic extends to geography: CF can send a ton of Donaldsonville urea up the Mississippi into the Corn Belt or out through the Gulf for export, depending on where the netback is highest on a given day. Owning both the plants and a distribution network of pipelines, barges, rail, and deep-water port access turns the company into an optimization engine rather than a passive price-taker — it cannot set the price, but it can consistently sell into the highest-value channel available.

There is a second-layer point buried in the segment data that is easy to miss: the "other" category, driven largely by diesel exhaust fluid, is a small but instructive hedge. DEF — a high-purity urea solution sprayed into diesel truck exhaust to cut emissions — is tied to freight and trucking activity rather than to planting seasons, giving CF a sliver of demand that marches to a different drummer than agriculture. It will never move the needle the way ammonia or UAN does, but it illustrates the company's instinct to find every incremental, higher-value home for the same nitrogen molecule. The through-line across the whole portfolio is that CF treats nitrogen as a stream to be routed, not a product to be dumped — and the persistently high plant utilization rates that result, typically in the 90-95% range, are the operating evidence that the routing works. A commodity plant only earns its cost advantage if it actually runs; idle capacity converts a cost edge into a fixed-cost anchor. CF's utilization record is, in that sense, the unglamorous proof that the moat is being harvested rather than merely owned. What management does with the resulting cash is where the real discipline shows.

VII. The Capital Allocation Playbook & The Leadership Transition (2019–2026)

On January 4, 2026, after twelve years running the company, W. Anthony "Tony" Will stepped down as CEO of CF Industries and handed the corner office to Christopher D. Bohn.[^10] It was the least dramatic major event in this entire story — no boardroom coup, no activist campaign, no surprise — and that is precisely the point. CF telegraphed the succession months in advance, in June 2025, naming Bohn as the successor and giving the market half a year to digest it.[^10] In an industry defined by violent price swings, the company treats its own governance as a study in continuity.

Bohn is not an outsider brought in to shake things up; he is the institution made flesh. He joined CF in September 2009 — in the very thick of the Terra war — and spent the next decade and a half inside the machine, serving as chief financial officer from 2019 to 2024 and then as chief operating officer before taking the top job. That means the person now steering CF was a hands-on architect of the corporate planning behind the Terra integration, the $5.2 billion expansion, and the post-2020 cash-harvesting era. Continuity of strategy is not a slogan at CF; it is a biographical fact. The obvious question an independent analyst should ask is whether that continuity becomes complacency — whether an insider who helped build the current playbook can credibly challenge it when conditions change. The counterweight is Bohn's compensation, which management describes as heavily weighted toward performance RSUs tied to return on invested capital and capital efficiency rather than to raw growth or empire-building.[^8]

The clearest expression of CF's philosophy is a metric it talks about more than revenue: nitrogen production capacity per share. The logic is almost aggressively unfashionable. Rather than reinvesting every dollar of cash flow into new plants — the empire-building instinct that afflicts most cyclical producers at the top of a cycle — CF treats its own shares as the asset to accumulate. If the share count keeps shrinking while capacity holds steady, then each remaining share lays claim to a larger slice of the same nitrogen output. The buyback is not a financial afterthought; it is the strategy.

And the buyback record is genuinely extraordinary. Since 2010, CF has deployed roughly $11.3 billion to repurchase about 215.8 million shares, shrinking its outstanding count by an astonishing 56% — the company has, in effect, bought back and retired more than half of itself.[^8] A $3 billion authorization running from 2022 was completed in October 2025, retiring some 37.6 million shares, and management immediately rolled into a fresh $2 billion authorization to run through 2029.[^8] In fiscal 2025 alone, CF repurchased 16.6 million shares for about $1.34 billion.1 The effect on per-share figures is mechanical but powerful: net earnings that were roughly flat in dollar terms translate into materially higher earnings per share simply because there are fewer shares to divide them among.

That said, an independent reading has to note where discipline shades into opportunism — and to CF's credit, management seems to know the difference. On the May 2026 first-quarter call, CFO-in-waiting commentary was blunt that the company had deliberately gone light on buybacks that quarter, repurchasing just 150,000 shares for about $15 million, because geopolitical uncertainty made the team cautious about deploying cash into an unsettled market; roughly $1.7 billion of authorization remained open.[^9] That same first-quarter result was flattered by a roughly $170 million gain from the resolution of long-running litigation with Orica and Nelson Brothers — a US$169.5 million settlement whose proceeds landed in April 2026 — a reminder that even a low-drama operator carries the occasional one-off that investors should strip out when judging the underlying run-rate.7 Buying back stock only when management judges it below intrinsic value is exactly what shareholders should want, but it also means the "relentless" buyback is, in practice, discretionary and cycle-timed — a lever management pulls hardest when cash is abundant and the stock is cheap, which is a different and more defensible thing than a mechanical commitment. Alongside the repurchases, CF has repaired and held an investment-grade balance sheet, keeping leverage low and a multi-billion-dollar cash buffer to ride out the down-cycles that its own history guarantees will come. The dividend is deliberately modest — CF pays a steady but unremarkable cash dividend, distributing on the order of $326 million in fiscal 2025 — precisely because management treats the buyback, not the dividend, as its primary return lever.1 The reasoning is coherent: a dividend is a promise that is painful to cut in a down-cycle, whereas a buyback can be dialed up when the stock is cheap and cash is flush and quietly dialed down when it is not. For a business whose cash flows swing as violently as CF's, that optionality is a feature, not a dodge — though it also means shareholders relying on CF for income are looking at the wrong company.

On the question of management credibility, the record is unusually clean by commodity-industry standards, and it is worth being specific about why. CF's leadership has, across several years of calls and presentations, told a remarkably consistent story — cheap gas, big plants, high utilization, shrink the share count, decarbonize by addition — and has largely done what it said, from completing the $3 billion authorization on schedule to taking Blue Point to a final investment decision with the risk-sharing structure it had long signaled it wanted. The narrative does not lurch. That consistency is itself an analytical asset: a management team whose framing survives contact with wildly different price environments is easier to underwrite than one that reinvents its thesis every quarter. The caveat, flagged earlier and worth repeating here as a discipline, is that consistency of story is not the same as being right — the "CF premium" and "structurally tighter mid-cycle" framing that dominates the most recent calls is exactly the kind of upbeat narrative that is impossible to falsify until the next down-cycle tests it. Disciplined capital return, however, is the harvest of a mature asset base. The more interesting question is what CF is planting for the next decade — and the answer runs through a tax credit and a deep saline aquifer under Louisiana.

VIII. Low-Carbon Ammonia: 45Q Credits and the $4B Blue Point Megaproject

For years, "green ammonia" was the kind of phrase that appeared in ESG slide decks and nowhere near a cash flow statement. The pitch was real enough: ammonia, because it carries hydrogen in a form that is far easier to ship and store than hydrogen itself, is a leading candidate to become a clean fuel — burned in the boilers of Asian power plants co-fired with coal, or bunkered into the tanks of ocean-going ships as a zero-carbon marine fuel. The problem was always cost. Making ammonia "green" by splitting water with renewable electricity (electrolysis) is brutally capital-intensive and, at scale, uneconomic today.

It helps to understand why ammonia keeps showing up in decarbonization conversations at all, because the logic is genuinely elegant. Hydrogen is the clean fuel everyone wants, but as a gas it is a nightmare to move and store — it must be either compressed to enormous pressures or chilled to near absolute zero, and it leaks through almost anything. Ammonia solves the problem by chemically locking three hydrogen atoms onto a nitrogen atom, producing a liquid that ships and stores using infrastructure the world already understands, because it has been moving ammonia by pipeline and tanker for a century. Burn it, or crack the hydrogen back out at the destination, and you have delivered clean energy in a form that behaves like a normal industrial liquid. That is why Japanese and Korean utilities are seriously studying co-firing ammonia in coal power plants, and why shipping lines eye it as a marine bunker fuel: it is the most practical way yet found to carry hydrogen across an ocean.

CF made a pointed strategic choice to sidestep that trap. Rather than chase green ammonia, it prioritized blue ammonia — conventional production via steam methane reforming, but with the carbon dioxide byproduct captured and permanently sequestered underground rather than vented. The unit economics, management argues, are vastly superior, because blue ammonia leverages the existing, low-cost gas-based plants CF already runs while bolting on carbon capture, instead of building an entirely new and expensive electrolysis stack. It is a characteristically pragmatic CF move: decarbonize by addition to a proven asset, not by betting on an unproven one.

The first concrete proof arrived in July 2025, when CF began operating a carbon dioxide capture and sequestration project at Donaldsonville, partnering with ExxonMobil to transport and permanently store the captured $CO_2$ in deep geological formations — with capacity to sequester up to about 2.0 million metric tons of $CO_2$ per year.[^12] CF had earlier signed a parallel large-scale capture agreement with ExxonMobil covering its Yazoo City, Mississippi, complex, underlining that this is a program rather than a one-off.[^13] The financial engine behind it is Section 45Q of the tax code, expanded under the Inflation Reduction Act, which provides a federal credit of up to $85 per metric ton of $CO_2$ permanently sequestered.[^14] Do the arithmetic on 2 million tons and you can see why management frames this not as an environmental gesture but as a cash-flow project: CF has indicated the Donaldsonville sequestration adds on the order of $100 million per year of incremental, low-risk free cash flow.[^12]

This is the genuinely novel part of the CF story, and it deserves a skeptic's scrutiny as much as an enthusiast's. On its face, 45Q converts a cost (carbon emissions) into a revenue stream (tax credits) using infrastructure CF largely already owns — cheap gas, existing plants, and, crucially, the deep saline aquifers beneath Louisiana that make sequestration geologically feasible. That is close to free money, and it is available to CF in a way it is not available to a European or Asian competitor lacking either the geology or the U.S. tax regime. The catch is policy risk: a credit created by legislation can be curtailed by legislation, and the entire economics rest on the durability of 45Q and on captured $CO_2$ actually staying underground under regulatory scrutiny.

The bigger bet is Blue Point. In April 2025, CF took final investment decision on a roughly $4.0 billion world-scale clean ammonia facility in Louisiana, structured as a joint venture: CF holds 40%, Japan's 株式会社JERA holds 35%, and 三井物産株式会社 Mitsui & Co. holds 25%.[^11] Production is slated to begin late in the decade — management's most recent guidance points to startup late in 2029 — adding more than 1.5 million tons of gross ammonia capacity.[^9][^11] The structure is as important as the plant. JERA, Japan's largest power generator, and Mitsui provide a built-in, long-term export channel into Japan's electricity system, effectively pre-selling a captive, premium-priced low-carbon market. Just as importantly, the 40% ownership means CF is deliberately not funding the whole thing off its own balance sheet — it is sharing the capital risk with partners who also happen to be the customers. That is the OCI/expansion lesson, learned and applied: grow, but do not bet the company alone. Whether Japanese demand for co-fired ammonia actually materializes at the scale and price the JV assumes is the open question — and it is the hinge of the entire clean-ammonia thesis.

There is a nearer-term, less speculative channel that is already producing revenue, and management is increasingly vocal about it: selling low-carbon nitrogen at a premium to industrial and consumer-goods buyers under pressure to cut their own supply-chain emissions. On the May 2026 call, management pointed to agreements with the likes of PepsiCo and the ethanol producer POET, framing decarbonized product as a way to command a price premium over conventional nitrogen while helping customers reduce their reported "scope" emissions.[^9] Europe's carbon border adjustment mechanism (CBAM), which will tax the embedded carbon of imported fertilizer, adds a second pull: a low-carbon CF ton shipped into Europe carries a smaller CBAM liability than a high-carbon rival's, effectively widening CF's landed-cost advantage in a market it already serves. Management's argument is that decarbonization is not a cost center it is grudgingly funding but an optionality it uniquely possesses — cheap gas, U.S. tax credits, favorable geology, and existing customer relationships combine into a low-carbon franchise a European or Chinese producer cannot easily assemble.

The independent counterpoint is that almost all of these premium streams are still small, early, and dependent on policy scaffolding — 45Q credits, CBAM, and government or utility willingness to pay up for clean molecules. Strip away the subsidies and mandates and much of the "premium" thins out. The bull would say that is precisely the point: CF is positioned to collect subsidies and premiums that competitors cannot, and it is doing so with assets it largely already owns, so the incremental capital at risk is modest relative to the potential cash. The bear would counter that a growth engine running on tax credits and regulatory tailwinds is only as durable as the politics behind them. Both are right, which is why low-carbon ammonia belongs in the "promising but unproven" column rather than the "banked" one — a real call option, not yet a certainty.

IX. The Strategic Scorecard: Porter's Five Forces & Seven Powers

Strip away the narrative and put CF on the analytical bench, and the picture that emerges is of a business with one overwhelming source of power and a scattering of weaker ones — which is exactly what you would expect of a commodity producer that has managed, against the odds, to earn structural returns.

Hamilton Helmer's Seven Powers

The dominant power is a Cornered Resource, and it is close to definitional. CF's privileged, low-cost access to North American shale gas at Henry Hub pricing — against rivals tethered to TTF, JKM, or Chinese coal — is the un-replicable input advantage that no amount of operational effort can match. A European competitor cannot simply relocate to Louisiana; the resource is geographically cornered, and CF sits on it. This is the power that does the heavy lifting, and it is genuine.

Scale Economies are the second real power. Donaldsonville is the single largest nitrogen complex on Earth, and operating a small number of giant, consolidated assets lets CF dilute fixed costs, leverage owned pipeline and port distribution, and run at persistently high utilization. A larger nitrogen network is a cheaper-per-ton nitrogen network. Process Power exists but is more modest — decades of accumulated expertise in the genuinely hazardous logistics of moving anhydrous ammonia by pipeline, rail, barge, and deep-water vessel, including owned port infrastructure. It is a real capability, but not one that would take a determined rival a generation to replicate.

And then the powers collapse. Switching Costs are weak to nonexistent: nitrogen is a pure commodity, and a farmer or retailer buys on price, local availability, and delivery timing, not loyalty. Network Effects, Brand, and Counter-Positioning are essentially negligible — no farmer pays more for a CF urea molecule than an identical Koch or Nutrien one. The honest conclusion is that CF's moat is narrow but deep: it rests almost entirely on cost position, with scale as reinforcement, and almost nothing on the softer, stickier powers that protect consumer or software franchises. That makes it powerful in wide-spread years and vulnerable in narrow-spread ones.

It is worth being precise about what "cornered resource" means here, because it is doing so much work in the thesis. CF does not own the gas — it buys it on the open market like anyone else in North America. What it owns is the location: a fleet of plants and a distribution network sitting physically on top of the continent's cheap-gas basins and connected to both the export docks of the Gulf and the demand of the Corn Belt. A rival cannot conjure that position by writing a check, because the constraint is not capital but geography, permitting, and time — the very barriers that make new entry so slow. That is what elevates a mere cost advantage into something closer to a cornered resource: it is not that CF is cleverer at buying gas, it is that it has spent a century and billions of dollars building irreplaceable physical access to the cheapest feedstock-to-market corridor in the industry. The power is real. What it is not is permanent in magnitude — the position is durable, but the profit it throws off rises and falls with a spread CF cannot set.

Porter's Five Forces

The threat of new entrants is very low, and this is a meaningful protection. A greenfield world-scale nitrogen plant costs $3–4 billion, takes years of complex environmental permitting, and runs headlong into local opposition to siting hazardous chemical facilities — CF's own Blue Point timeline, with construction contingent on permits and startup not until 2029, is a live illustration of how slow this is. Threat of substitutes is extremely low: plants require nitrogen to grow, and organic alternatives like manure cannot be scaled to industrial agriculture. Supplier power is low, because abundant North American gas makes CF a coveted, high-volume customer rather than a hostage to any pipeline.

The forces that bite are on the demand and rivalry side. Buyer power is moderate: the consolidation of agricultural retail into giants like Nutrien Ag Solutions gives buyers some negotiating leverage, though they cannot afford to run short during the tight planting window. Competitive rivalry is high but rational — global prices are violently volatile, but the concentrated set of North American players (CF, Nutrien, Koch, OCI) has historically avoided destructive localized price wars, competing on cost position rather than suicidal discounting. The net read: CF is structurally protected from new competition and substitution, but remains fully exposed to the commodity cycle and to buyers who are themselves consolidating. That tension is the heart of the investment debate.

X. The Investment Spine: Bull vs. Bear and the Activist Stress Test

The "Why Win / Why Not" Investment Case

The bull case — call it the sovereign cash harvest — runs as follows. The structural spread between U.S. and global natural gas is durable, not a one-off, because North American shale genuinely is among the cheapest gas on Earth and the plants that consume it are already built. On that foundation, CF runs at high utilization and 40%-plus EBITDA margins across most of the cycle, converts an industry-leading share of that EBITDA into free cash flow, and funnels the cash into shrinking its own share count. Layer on low-carbon ammonia as a genuinely new, higher-margin, policy-subsidized growth engine — 45Q cash today, Blue Point exports tomorrow — and you have a cyclical business that has found a way to compound per-share value across cycles rather than merely riding them.

The bear case is the cyclical trap. Every element of the bull case depends on the gas spread staying wide, and spreads revert. If global LNG capacity surges (a wave of new export terminals is due later this decade), or if Europe permanently de-industrializes its chemical sector and simply stops being the high-cost marginal producer, the global clearing price of nitrogen falls and CF's windfall margins compress toward something ordinary. Meanwhile the $4 billion Blue Point bet could suffer the classic megaproject fate — delays, cost overruns — or worse, arrive into a world where Asian demand for co-fired ammonia never materializes because batteries, nuclear, or cheaper hydrogen win the decarbonization race. And underneath it all sits ordinary agricultural risk: a severe farm downturn or a run of poor U.S. crop years compresses nitrogen demand regardless of the gas spread.

The megaproject risk on Blue Point deserves to be taken as seriously as the demand risk, because industrial history is a graveyard of world-scale plants that arrived late and over budget. A $4 billion greenfield facility, even a partnered one, carries construction, permitting, and commissioning risk that does not fully retire until the plant is running at nameplate — and CF's own guidance already shows the timeline stretching, with construction contingent on permits and startup pushed to late 2029.[^9] Every year of delay is a year the capital sits idle and the low-carbon export thesis remains unproven. The mitigant is the ownership structure: at 40%, CF's share of a cost overrun is proportionally smaller than it would be on a wholly owned build, and its partners are motivated, deep-pocketed industrial companies rather than passive financiers. But partnership cuts both ways — it also means CF does not fully control the project's pace or priorities, and that decisions must be negotiated three ways. The lesson CF took from the 2016 expansion was to share the risk; the price of sharing risk is sharing control, and whether that trade proves wise will not be knowable until Blue Point either starts up cleanly or does not.

There is also a subtler bear thread worth naming: the possibility that the entire "low-carbon premium" narrative is a solution in search of a durable problem. If clean electricity from renewables plus storage, or a revival of nuclear, out-competes ammonia co-firing in Asian power generation, the premium export market CF is building toward may simply never reach the scale the Blue Point economics assume — leaving CF with a perfectly good conventional ammonia plant it could have built for less without the clean-fuel ambitions. The bet is not that ammonia is a good hydrogen carrier in the abstract; it is that it will win a specific competition against other decarbonization pathways in specific markets. That is a genuine technological and policy wager, and reasonable people can doubt it.

The Activist & Skeptical Investor Stress Test

The sharpest challenge a skeptic can level is that CF was, for the better part of a decade, a value trap in disguise. From roughly 2012 to 2020, the stock went almost nowhere while the company poured billions into the Donaldsonville and Port Neal expansions and burned $150 million-plus terminating the OCI inversion.6 For eight years, an investor earned close to nothing while management built assets and made a failed detour into financial engineering. That is not a hypothetical criticism; it is the historical record.

The counter-evidence is the harvest that followed. The assets that looked like dead money in 2016 generated the enormous cash flows of 2021–2025 — including $1.46 billion of net earnings in fiscal 2025 — and the buyback program retired more than half the shares, so that the per-share earnings power of the surviving equity rose dramatically.1[^8] The bet, in other words, eventually paid, but only for investors patient enough to sit through the barren years — which tells you something important about the temperament this stock demands.

Where an activist would plant a flag today is on capital-allocation guardrails. Having watched CF nearly repeat the "build big and alone at the wrong time" mistake, a skeptic would demand that management never again fund a massive, un-partnered greenfield expansion off its own balance sheet. The 40% ownership structure of Blue Point is, encouragingly, exactly the discipline an activist would prescribe — CF has offloaded the majority of the capital risk onto JERA and Mitsui, who double as the customers. On the May 2026 call, management was explicitly asked whether tight markets and a "better return profile" might tempt it to accelerate a second Blue Point unit, and the answer was notably cautious: nothing imminent, disciplined investment philosophy unchanged, a desire to prove out the first unit before committing to the next.[^9] For now, at least, the words are the right ones. The job of a shareholder is to check that the behavior keeps matching them.

How CF Stacks Up Against the Field

It sharpens the picture to place CF against its peers, because the comparison reveals what is genuinely distinctive and what is merely industry-standard. Nutrien, the Canadian giant born from the 2018 merger of Agrium and PotashCorp, is far larger and more diversified — it spans nitrogen, potash, and a vast agricultural retail network — which gives it stability but also dilutes its exposure to the nitrogen cost-curve advantage that is CF's entire reason for being. Koch, privately held, competes hard on cost but does not offer public investors a pure vehicle. OCI, CF's would-be inversion partner, retains European and other international assets that leave it more exposed to exactly the high-cost gas that CF is positioned to profit against. The point of the comparison is not that CF is "better" in some absolute sense but that it is the most concentrated bet available: a nearly pure-play North American nitrogen producer, unhedged and undiversified, which is a virtue when the gas spread is wide and a liability when it is not. An investor choosing CF over Nutrien is, whether they realize it or not, choosing more torque and less ballast.

That concentration is the crux of the whole analysis. Nutrien's retail arm cushions its earnings across the cycle; CF has no such cushion, by design. Management's implicit argument is that the cushion is not worth its cost — that a lower-cost, higher-utilization, aggressively-buying-back pure-play compounds per-share value faster across a full cycle than a diversified conglomerate does, provided investors can stomach the volatility in between. The last five years support that argument; the eight years before them undercut it. Which stretch is representative of the next decade is, in the end, the entire debate.

The 3 KPIs That Matter Most

Three metrics tell you almost everything about how this business is actually doing, and an investor tracking them needs little else. The first is the Henry Hub versus TTF/JKM (and Chinese coal) spread — the single absolute driver of CF's super-normal margin, and the variable that determines whether a given year is a windfall or a grind. The second is nitrogen tons of capacity per share outstanding, the truest measure of the equity-cannibalization strategy: is management genuinely shrinking the share count faster than it dilutes it, so that each share commands more nitrogen over time? The third is low-carbon project execution — specifically, whether the Donaldsonville 45Q cash flows arrive as promised and whether Blue Point stays on its budget and its late-2029 timeline. Get those three right and you have the pulse of the company; the quarterly noise around them is mostly noise.

XI. Outro & Epilogue

CF Industries is, in the end, a story about how a sleepy agricultural cooperative founded to buy fertilizer cheaply for its members became one of the most structurally advantaged cash generators in the industrial world — by inverting its own purpose. It survived being hunted by Agrium, out-maneuvered Yara to consolidate the North American nitrogen market, absorbed a bruising defeat when the U.S. Treasury killed its inversion dream, and then bet the balance sheet on organic assets that looked foolish for years before becoming a cash monster in the 2020s. The through-line is not brilliance so much as a stubborn commitment to a single, unfashionable idea: own the cheapest feedstock, run the biggest plants, and use the resulting cash to buy back your own shares rather than to build an empire.

The Christopher Bohn era, which formally began in January 2026, is defined less by a new strategy than by the absence of one. The company has moved from building its physical assets to harvesting their cash-generating power, and the succession itself — telegraphed a year in advance, handed to a sixteen-year insider — signals a management that views continuity as the strategy. On the May 2026 earnings call, Bohn leaned into a new framing he called the "CF premium": the argument that recent geopolitical supply shocks have exposed how fragile much of the world's low-cost nitrogen capacity really is, and that CF's combination of cheap and geopolitically secure North American assets deserves to be valued at a premium to fragile first-quartile producers elsewhere.[^9] It is a compelling narrative. It is also, an independent observer should note, precisely the kind of "our cycle is different this time" argument that commodity managements reach for near the top — plausible, self-serving, and unfalsifiable until the spread reverts and we find out.

The genuinely surprising note to end on is the one the outline flagged at the start: the eventual winner of a slice of the energy transition may not be a Silicon Valley startup or a solar developer, but a 79-year-old, asset-heavy fertilizer company in Louisiana, quietly monetizing federal tax credits by pumping carbon dioxide into deep saline aquifers beneath the Mississippi Delta. Whether that turns out to be a durable second act or a policy-dependent sideshow will depend on things CF does not control — the price of gas half a world away, the durability of an act of Congress, and whether Japan really wants to burn ammonia in its power plants. What CF does control, it has controlled about as well as a commodity producer can. The rest is the cycle, and the cycle always comes back around.

References

-

CF Industries Holdings, Inc. Reports Full Year 2025 Net Earnings of $1.46 Billion, Adjusted EBITDA of $2.89 Billion — CF Industries, 2026-02-18 ↩↩↩↩↩

-

CF Industries Holdings, Inc. 2024 Annual Report on Form 10-K — SEC EDGAR, 2025-02-21 ↩↩

-

CF Industries Holdings, Inc. Annual Report on Form 10-K (FY2005) — SEC EDGAR, 2006 ↩↩

-

Simpson Thacher Represents CF Industries in its Acquisition of Terra Industries — Simpson Thacher & Bartlett, 2010-04-15 ↩

-

CF Finally Wins Terra — Chemical & Engineering News (American Chemical Society), 2010-03-22 ↩↩↩

-

CF Industries and OCI call off $8 billion fertilizer merger — Reuters, 2016-05-23 ↩↩

-

CF Industries and Orica Reach US$169.5M Litigation Settlement — Indian Chemical News, 2026-03-24 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube