CEVA Inc.: The Story of Silicon Licensing's Quiet Giant

I. Introduction and Episode Roadmap

There is a company whose technology sits inside your smartphone, your wireless earbuds, your car's safety systems, and your smart home devices. Its processors have shipped in over twenty billion devices worldwide. And yet, if you stopped a hundred people on the street and asked them to name it, not a single one would recognize it.

That company is CEVA.

CEVA Inc. is a semiconductor intellectual property licensor based in Rockville, Maryland, with deep roots in Israel's engineering ecosystem. It designs digital signal processor cores, wireless connectivity platforms, and AI inference engines, then licenses those designs to chipmakers who embed them into their own silicon. CEVA does not manufacture a single transistor. It does not sell a single chip. And yet, by the end of 2025, more than twenty-one billion devices had shipped with CEVA technology inside, at a rate exceeding two billion units per year. Every second of every day, roughly sixty-five chips containing CEVA intellectual property roll off production lines somewhere in the world.

The puzzle at the heart of CEVA's story is one that applies to an entire class of invisible infrastructure companies: How do you build a durable business when your customers are the ones who get all the credit?

CEVA's name never appears on a product box. Its brand carries zero consumer recognition. Its revenue in 2025, at roughly one hundred ten million dollars, would barely register as a rounding error on the income statements of the companies whose chips contain its technology. And yet, CEVA has survived and reinvented itself through at least three near-death experiences across a quarter century of operation, each time emerging with a broader product portfolio and a more resilient business model.

This is a story about the economics of intellectual property licensing, about what happens when the customers who power your revenue get acquired or go bankrupt, about the geopolitical entanglements of selling technology to China, and about whether a company with fewer than five hundred employees can carve out a lasting position in an industry dominated by trillion-dollar giants.

It is the story of how DSP cores designed in an Israeli office park ended up in billions of pockets, and whether the next twenty billion devices will carry CEVA inside them too.

II. The Semiconductor Context: Why IP Licensing Exists

To understand CEVA, you first need to understand a brutal economic fact about modern chip design: it is staggeringly expensive, and getting more so every year. Designing a cutting-edge system-on-chip at the most advanced process nodes now costs north of five hundred million dollars before a single chip is manufactured. That figure includes the engineering teams, the electronic design automation software licenses, the mask sets, and the verification and testing infrastructure. For all but the largest semiconductor companies, designing every component of a complex chip from scratch is economically impossible.

This is where IP licensing enters the picture. Think of it like architecture. If you are building a skyscraper, you do not reinvent concrete or steel. You license proven structural designs, proven elevator systems, proven HVAC configurations. In the semiconductor world, IP licensors provide proven, pre-verified building blocks: processor cores, communications interfaces, memory controllers, and signal processing engines. A chipmaker licensing this IP can focus its own engineering resources on the parts of the chip that differentiate its product, while relying on licensed blocks for everything else.

The company that popularized this model was ARM Holdings, founded in Cambridge, England, in 1990. ARM designed energy-efficient processor cores and licensed the designs to chipmakers, collecting an upfront fee when a customer signed up and a per-unit royalty every time a chip shipped. ARM never manufactured silicon. It sold blueprints. By the time Apple introduced the iPhone in 2007, ARM's processor architecture had become the beating heart of virtually every mobile device on the planet. ARM's model proved that you could build a massively valuable company by being invisible, embedded deep within other companies' products.

But ARM licensed general-purpose CPU cores, the brains of the chip. CEVA carved out a different niche: digital signal processors, or DSPs.

If a CPU is the brain that runs your operating system and applications, a DSP is the specialist that handles the continuous, real-time mathematical operations that make wireless communications, audio processing, and image recognition possible. When your phone connects to a cell tower, a DSP is crunching the math to modulate and demodulate the radio signals. When your wireless earbuds cancel background noise, a DSP is performing the acoustic calculations in real time. When a car's camera system identifies a pedestrian, a DSP-like processor is running the neural network inference.

Here is the key difference, and it is worth dwelling on because it is fundamental to understanding CEVA's entire business.

DSPs are optimized for performing the same mathematical operation, specifically multiply-and-accumulate calculations, billions of times per second, at extremely low power consumption. Think of it like the difference between a Swiss Army knife and a surgeon's scalpel. A general-purpose CPU is the Swiss Army knife: flexible, capable of many tasks, but not optimal for any single one. A DSP is the scalpel: designed to do one narrow class of operations with extraordinary speed and precision, consuming a fraction of the power. A GPU can handle similar parallel math, but it burns far more energy and takes up more silicon area. For battery-powered devices where every milliwatt matters, DSPs hit the sweet spot.

This entire ecosystem, the fabless semiconductor revolution, found particularly fertile ground in Israel. Starting with Motorola's establishment of an R&D center in 1964, Israel built one of the world's densest concentrations of semiconductor expertise. Intel, IBM, Qualcomm, and dozens of others set up design centers there, training a generation of engineers who then founded their own companies. Over seventy Israeli semiconductor startups have been acquired for a collective value exceeding forty-four billion dollars. Names like Mobileye, Mellanox, and Habana Labs emerged from this ecosystem. CEVA, born from the same soil, would take a different path: not building chips for acquisition, but licensing the intellectual property that goes inside other people's chips.

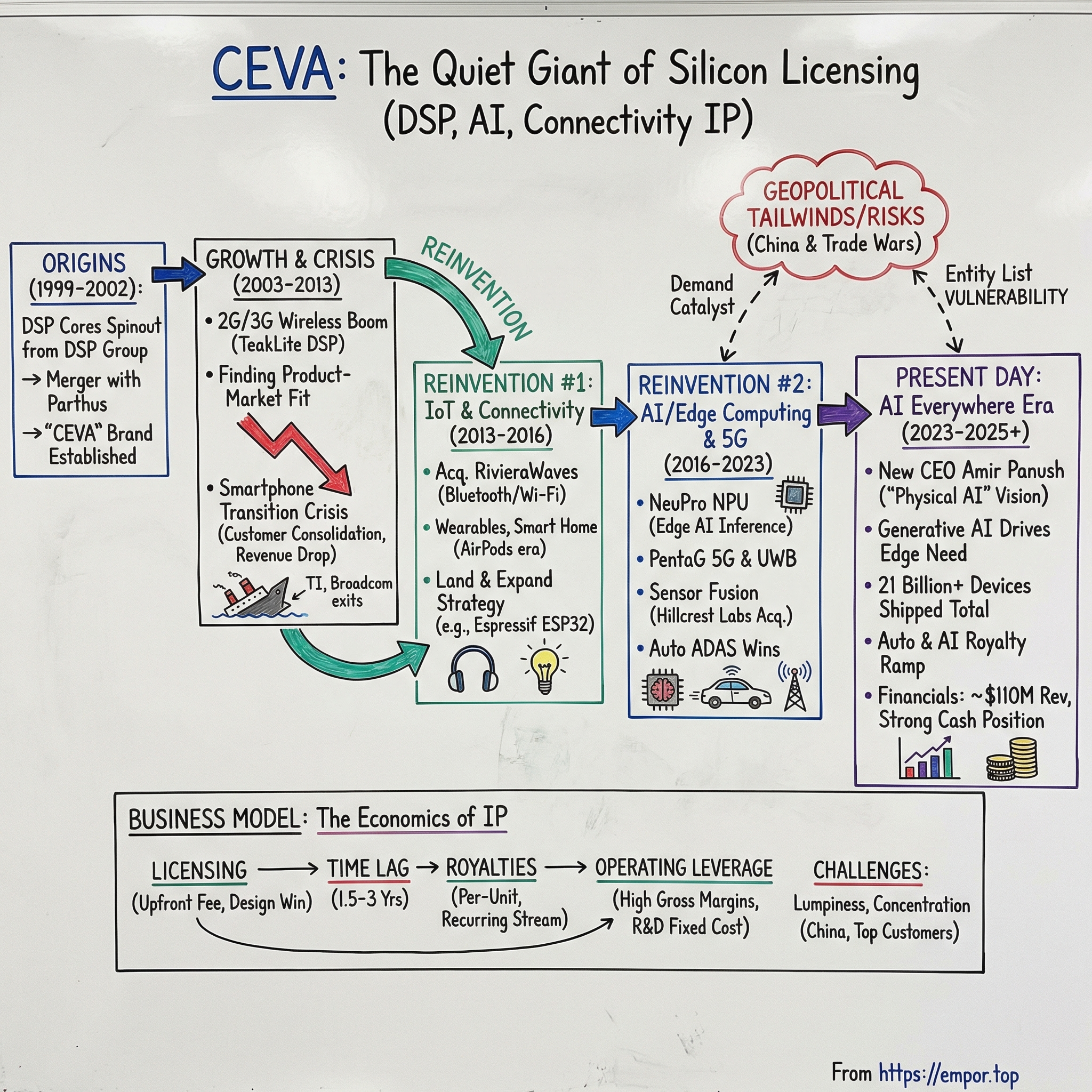

III. Origins: DSP Group Spinout to CEVA (1999-2002)

The story begins in 1987, when an Israeli entrepreneur named Davidi Gilo founded DSP Group in San Jose, California. Gilo recognized early that digital signal processing would become critical to consumer electronics, and DSP Group quickly established itself as a pioneer. In 1989, the company developed the world's first telephony answering device speech processor, a niche product that demonstrated the commercial viability of specialized DSP silicon. DSP Group went public on NASDAQ in 1994 and became a major player in cordless phone chips.

By the mid-1990s, DSP Group had grown ambitious. In 1996, it spun off its cellular chip division as DSP Communications, which also listed on NASDAQ. That same year, Eliyahu "Eli" Ayalon, an Israeli engineer and executive, took the helm as President and CEO of DSP Group. Ayalon would become one of the central figures in CEVA's origin story, a methodical strategist who understood that DSP Group's real competitive advantage was not in manufacturing chips but in designing the processor architectures themselves.

The validation of that insight came spectacularly in 1999, when Intel acquired DSP Communications for 1.6 billion dollars. Intel wanted DSP Communications' cellular baseband technology for its own mobile ambitions. The deal demonstrated something profound: DSP architecture, the intellectual property itself, could be enormously valuable even when separated from the chip manufacturing business. Ayalon, still running DSP Group, drew the logical conclusion. Later that year, he established a new subsidiary called DSP Cores, Inc., a Delaware corporation whose sole mission was to license DSP intellectual property to other chipmakers. It was this subsidiary that would eventually become CEVA.

Meanwhile, across the Irish Sea, a parallel story was unfolding. In 1993, Brian Long and Peter McManamon had founded a company called Silicon Systems Ltd in Dublin, Ireland. Renamed Parthus Technologies, the firm developed IP platforms for mobile internet devices, targeting the emerging 3G cellular, Bluetooth, and GPS markets. Parthus went public on the London Stock Exchange in May 2000, raising capital at what turned out to be the worst possible moment: the dot-com bubble was already deflating. Parthus had strong technology but was burning cash in a collapsing market for telecom IP.

In April 2002, DSP Group announced that it would merge its IP licensing subsidiary with Parthus Technologies. The deal made strategic sense for both sides. DSP Group would unlock value from its IP licensing business while focusing on its core cordless phone chip business. Parthus would gain access to proven DSP architectures and a viable business model. DSP Group shareholders received a 50.1 percent stake in the combined entity, giving them effective control.

The merger closed on November 1, 2002, creating ParthusCeva, Inc., which began trading on NASDAQ under the ticker PCVA and on the London Stock Exchange. The early months were rocky. Kevin Fielding, the first CEO drawn from the Parthus side, lasted barely seven months before being replaced by Chet Silvestri in June 2003. Silvestri stabilized operations and, in December 2003, oversaw a pivotal rebranding: the "Parthus" prefix was dropped, the company became simply CEVA, Inc., and the ticker changed to CEVA.

The name itself carried no obvious meaning. It was not an acronym and had no public etymology. Some speculated it derived from the Hebrew word for "area" or "direction," but the company never confirmed any origin. It was a clean, short, pronounceable brand designed to stand on its own in a market where customers cared about technical specifications, not company heritage. In a B2B industry where brand recognition matters far less than technical performance, the name was perfectly adequate. Nobody bought a CEVA DSP core because the name inspired confidence; they bought it because it worked.

Those early years were lean. Revenue hovered around thirty-five to thirty-eight million dollars, and the stock briefly touched a low of $2.90 in February 2003. The company had approximately four hundred employees spread between Israel, Ireland, and the United States, developing DSP cores like the CEVA-Oak and CEVA-TeakLite for the wireless communications market. The business model was simple in concept but challenging in execution: license DSP core designs to chipmakers for an upfront fee, then collect a per-unit royalty every time those chipmakers shipped a chip containing CEVA technology. The upfront fees provided near-term revenue. The royalties, which took years to materialize as customers completed chip designs and ramped production, represented the long-term prize.

IV. The 2G/3G Wireless Boom: Finding Product-Market Fit (2003-2009)

In May 2005, CEVA found the leader who would define its next era. Gideon Wertheizer, who had been with DSP Group since 1990 in roles spanning VLSI design, marketing, and strategic business development, was appointed CEO. He replaced Silvestri and would go on to lead CEVA for the next seventeen years, making him one of the longest-serving CEOs in the semiconductor IP industry.

Wertheizer was an engineer's CEO: technically deep, strategically patient, and comfortable with the unglamorous work of building customer relationships in an industry where design wins took years to convert into revenue. Where some semiconductor executives chased quarterly headlines, Wertheizer played a longer game, understanding that the real value of his company was being built in customer design labs, not in press releases.

His timing was excellent. The global mobile phone market was exploding. Nokia was shipping hundreds of millions of handsets per year. Motorola's RAZR was the must-have gadget. Samsung, LG, and Sony Ericsson were competing fiercely for market share. And all of these phones needed baseband processors to handle their cellular communications, processors built around DSP cores.

To appreciate the scale: in 2005, the world shipped approximately eight hundred million mobile phones. By 2008, that number exceeded one billion. Every single one of those phones needed at least one DSP core to handle the radio signal processing that makes cellular communication possible. It was, from CEVA's perspective, the greatest addressable market in the history of semiconductor IP.

CEVA's TeakLite DSP family became the workhorse of this era. The TeakLite architecture hit a sweet spot: it was powerful enough for 2G and early 3G baseband processing, compact enough to fit in cost-sensitive feature phones, and power-efficient enough for all-day battery life. Chipmakers like Texas Instruments and Broadcom licensed TeakLite cores for their baseband processors, which then shipped inside handsets from virtually every major brand.

The licensing model worked like this: a tier-one chipmaker would pay CEVA an upfront license fee, typically in the low single-digit millions, for the right to incorporate a TeakLite core into a specific chip design. CEVA would provide the register-transfer-level design files, verification environments, software development tools, and technical support. The chipmaker's engineers would then integrate the CEVA core alongside their own proprietary logic, fabricate the chip at a foundry like TSMC, and sell it to handset makers. Every time one of those chips shipped, CEVA would receive a royalty payment, typically a few cents per unit.

The math was compelling on both sides. For the chipmaker, licensing a proven DSP core from CEVA cost a fraction of what it would take to design one from scratch, and it reduced time-to-market by a year or more. For CEVA, each new licensee represented a potential stream of royalty revenue that could last for the entire production life of a chip, often five to seven years.

The competitive landscape during this period included several rival DSP IP vendors. Tensilica, founded in 1997 in Santa Clara, offered configurable processor cores that could be optimized for DSP workloads. ARC International provided embedded processor cores with DSP extensions. But CEVA consistently outperformed these competitors in the cellular baseband market, in part because its cores were purpose-built for wireless signal processing rather than adapted from general-purpose architectures. When a customer needed to squeeze maximum baseband performance from minimum silicon area and power budget, CEVA's specialization was a decisive advantage.

By 2008, CEVA's revenue had climbed to forty million dollars, and the company had established itself as the dominant provider of licensable DSP cores for cellular baseband applications. The numbers were striking: by the third quarter of 2010, CEVA-powered cellular baseband processors were shipping at a rate of 178 million units per quarter, giving CEVA a thirty-six percent market share, ahead of Qualcomm, Texas Instruments, and MediaTek. The company would later claim that one in every three handsets shipped worldwide contained a CEVA DSP core.

By 2011, CEVA reported ninety percent market share in licensable DSP IP. Revenue hit sixty million dollars that year, the company's best performance to date. Over seventy-five companies had licensed TeakLite cores, and the technology had shipped in more than two billion devices.

Geographically, Asia became the center of gravity. Chinese chipmakers in particular embraced IP licensing as a shortcut to competitive products. Companies like Spreadtrum (later Unisoc) and RDA Microelectronics licensed CEVA cores for their low-cost 2G and 3G baseband chips, which powered hundreds of millions of feature phones sold across China, India, Southeast Asia, and Africa. For CEVA, this Asian tilt would become both its greatest growth engine and, eventually, its most significant geopolitical vulnerability.

The challenge during this period was managing investor expectations around the inherent lumpiness of the business. A single large licensing deal could swing quarterly revenue by thirty percent. Royalties, while more predictable, were still subject to the boom-and-bust cycles of the handset market. CEVA was building something genuinely valuable, a recurring royalty base that grew with every new chip design that went into production, but the quarterly financial statements often obscured that underlying momentum. It was a business that rewarded patience, not quarterly optimization. But patience was about to be tested in ways no one at CEVA anticipated.

V. First Inflection Point: The Smartphone Transition Crisis (2010-2013)

In 2007, Steve Jobs walked onto a stage in San Francisco and introduced the iPhone. Five years later, CEVA nearly went under because of what that moment set in motion.

The smartphone revolution did not just change how people used phones. It restructured the entire economics of the mobile semiconductor industry. Feature phones had been a fragmented, competitive market with dozens of chipmakers serving dozens of handset brands. The smartphone era consolidated that market with brutal efficiency. Apple designed its own application processors and eventually began working toward its own modem. Qualcomm, with its integrated Snapdragon platform combining CPU, GPU, DSP, and modem on a single chip, became the dominant supplier for Android devices.

The result was a wave of consolidation that wiped out many of CEVA's most important customers. To understand the magnitude of this disruption, consider that before the iPhone, the mobile baseband chip market supported more than a dozen independent vendors. Within five years, that number would collapse to fewer than five.

The casualties came in rapid succession. Texas Instruments, one of CEVA's most significant licensees, announced in September 2012 that it was exiting the mobile processor market entirely, claiming the move would save two hundred million dollars annually. Broadcom quit the baseband business in 2014. ST-Ericsson dissolved. Infineon's mobile arm was sold to Intel for 1.4 billion dollars. Freescale, Marvell, and others retreated from mobile. The list of companies that had licensed CEVA cores for mobile baseband and subsequently exited the market reads like a casualty report from a war, which in many ways it was.

For CEVA, the impact was devastating. Revenue peaked at sixty million dollars in 2011, then fell eleven percent to fifty-four million in 2012 and another nine percent to forty-nine million in 2013. That nineteen percent decline from peak to trough does not fully convey the severity of the crisis. CEVA's business model depended on a broad base of competing chipmakers, each licensing DSP cores for their own baseband designs. When those competitors consolidated or exited, CEVA lost not just current revenue but the entire pipeline of future royalties that those customers' chips would have generated.

The crisis was compounded by a perverse mix shift. Even as the total number of CEVA-powered chips shipped continued to grow, hitting record unit volumes of over three hundred million in a single quarter by late 2012, the average revenue per unit declined. Feature phones using CEVA-based 2G basebands were being replaced by smartphones using integrated platforms from Qualcomm. The phones that still used CEVA cores were increasingly the cheapest ones, generating the lowest royalties per unit. CEVA was shipping more chips than ever but making less money from them.

Inside the company, the strategic debate was existential. Some argued that CEVA should double down on its cellular baseband heritage, designing higher-performance DSP cores for LTE and hoping that new licensees would emerge to challenge Qualcomm's dominance. Others argued that the baseband market was irrevocably consolidating and that CEVA needed to find entirely new applications for its technology.

Wertheizer, characteristically methodical, chose a middle path: invest in next-generation cellular DSP cores (the CEVA-XC family for LTE-Advanced) while simultaneously diversifying into adjacent markets like IoT connectivity, audio processing, and computer vision.

The LTE bet was not foolish. Samsung, which was building its own Exynos modem chips, continued to license CEVA's high-performance CEVA-XC DSP cores for LTE baseband processing. In a market where Qualcomm had become the default choice, Samsung's determination to maintain its own modem capability was one of the few bright spots for CEVA's cellular business. And in China, companies like Spreadtrum were licensing CEVA-XC cores to build LTE basebands for the price-sensitive mid-tier smartphone market that Qualcomm was not aggressively pursuing.

But the diversification imperative was clear. The pivot was not optional. It was survive or die.

What saved CEVA during this period was, paradoxically, the very breadth of its installed base. Hundreds of millions of devices were still shipping with CEVA cores, generating royalty revenue even as new licensing deals slowed. That royalty stream, modest but persistent, provided the financial runway for CEVA to reinvent itself. Competitors who had entered the DSP IP market without that installed base advantage simply did not survive the transition.

CEVA's near-death experience in 2012-2013 remains a textbook example of the platform risk inherent in IP licensing: when your customers' business models collapse, your own is never far behind. But it also demonstrated the surprising resilience of a royalty-based model. Even in crisis, the embedded installed base kept generating cash, buying time for the next chapter.

VI. Reinvention #1: IoT, Bluetooth, and Connectivity (2013-2016)

The Internet of Things was one of the most overhyped technology trends of the 2010s. Billions of connected devices were perpetually "just around the corner," and venture capitalists poured money into IoT startups with abandon. Most of those startups failed. But beneath the hype cycle, a real and durable market was emerging: billions of devices that needed low-power wireless connectivity.

Bluetooth earbuds. Smart home sensors. Wearable fitness trackers. Industrial monitors. Connected appliances. All of them needed small, cheap, power-efficient wireless chips. And those chips needed IP.

Wertheizer identified this opportunity and, in a move that was uncharacteristic for a company that had primarily grown organically, decided to buy his way in. In July 2014, CEVA acquired RivieraWaves, a twenty-nine-person company based in Sophia-Antipolis on the French Riviera, for approximately nineteen million dollars.

RivieraWaves had developed Bluetooth and Wi-Fi IP platforms, complete solutions that included both the physical layer and the media access control layer needed for wireless connectivity. The company was tiny, barely breakeven on 3.6 million dollars in annual revenue, but its technology was mature and already deployed with several leading semiconductor companies. Founded just four years earlier in 2010, the team had packed an impressive amount of engineering into a small package.

The acquisition was transformative for CEVA. Overnight, it expanded the company's addressable market from cellular baseband DSP, a consolidating market, to wireless connectivity for IoT, a rapidly expanding one. The Bluetooth IP in particular would prove to be a gold mine.

As the wearables market took off, powered by products like the Apple Watch, Fitbit trackers, and eventually AirPods, the demand for licensed Bluetooth IP surged. Chipmakers building dedicated wireless connectivity chips for these devices needed proven, low-power Bluetooth stacks, and CEVA (rebranding the products as Ceva-Waves) became the leading supplier.

The scale of the Bluetooth opportunity became clear when Apple launched AirPods in December 2016. The wireless earbud market, essentially nonexistent a year earlier, became one of the fastest-growing consumer electronics categories in history. While Apple designed its own W1 chip for AirPods, the explosive demand for wireless earbuds created a massive market for third-party alternatives. Companies across China, Taiwan, and Korea raced to build competing products, and many of them used chips containing CEVA Bluetooth IP.

By the end of the decade, CEVA would claim a forty-five percent market share in true wireless stereo earbuds (excluding Apple) and its Bluetooth shipments would surpass one billion units per year, a staggering number for an IP core that had been acquired for just nineteen million dollars. The return on that acquisition is one of the most impressive in semiconductor IP history. Nineteen million dollars for technology that, within a decade, would be generating hundreds of millions of device shipments annually and contributing meaningfully to CEVA's royalty revenue. Wertheizer's decision to acquire rather than build was validated decisively.

The connectivity pivot also extended to other wireless protocols. CEVA developed IP for Wi-Fi, particularly targeting the low-power variants used in IoT devices. Wi-Fi shipments using CEVA IP would grow steadily, reaching 179 million units in 2024 and a record 266 million in 2025. The company built platforms for NB-IoT (Narrowband Internet of Things), a cellular protocol designed for low-bandwidth, battery-powered sensors that could operate for years on a single battery. And later, it would add ultra-wideband technology.

By 2025, CEVA would claim sixty-eight percent market share in wireless connectivity IP overall, a dominant position built almost entirely from the foundation of that nineteen-million-dollar French acquisition.

One particular design win illustrated the power of the "land and expand" strategy. Espressif Systems, a Chinese fabless semiconductor company, licensed CEVA's Bluetooth IP for its ESP32 chip. The ESP32 became one of the most ubiquitous IoT chips in the world, used in everything from hobby projects to commercial products, shipping in hundreds of millions of units. A single licensing relationship, originating from a small Chinese startup, generated a royalty stream that persisted for years as the ESP32 family expanded into new variants and applications.

Financially, the diversification strategy stabilized CEVA during a critical period. After bottoming at forty-nine million dollars in 2013, revenue recovered to fifty-one million in 2014, fifty-nine million in 2015, and seventy-three million in 2016, surpassing the pre-crisis peak. The mix was shifting too: cellular baseband was no longer the dominant revenue driver. Connectivity, audio, and emerging applications were contributing a growing share. CEVA was becoming a multi-market platform company rather than a single-product DSP licensor.

But CEVA remained fundamentally challenged. ARM was expanding into DSP-like workloads with its Cortex-M and Cortex-A processors. Cadence, having acquired DSP IP competitor Tensilica in 2013, had the resources of a major EDA company behind its competing cores. Synopsys offered its own ARC processor cores. These competitors were all larger, better capitalized, and more diversified than CEVA. Surviving the smartphone crisis was an achievement. The question was whether CEVA could build a position defensible enough to thrive in the next technology wave.

VII. Second Inflection Point: The AI/Edge Computing Pivot (2016-2020)

The deep learning revolution arrived in the semiconductor world like a tidal wave. Starting around 2012 with AlexNet's breakthrough performance on the ImageNet competition, neural networks rapidly proved their superiority at tasks ranging from image recognition to speech understanding to natural language processing. By 2016, every major technology company was investing heavily in AI, and the semiconductor industry was scrambling to build hardware optimized for the new workloads.

CEVA's management, led by Wertheizer and Chief Technology Officer Erez Bar-Niv, recognized an opportunity hiding in plain sight. Neural network inference, the process of running a trained model to make predictions, is fundamentally a mathematical operation: billions of multiply-and-accumulate calculations performed on matrices of numbers. That is precisely what DSPs are designed to do. The architectural DNA of CEVA's products, optimized over two decades for exactly these kinds of repetitive math operations, could be adapted for AI workloads.

Think of it this way: training an AI model is like writing a cookbook, requiring creativity, experimentation, and enormous computing resources. That is why training happens on massive GPU clusters in data centers, where power consumption and chip cost are secondary concerns. Running the trained model, inference, is like following the recipe: repetitive, precise, and highly parallelizable. It is the same set of mathematical operations performed millions of times on different data inputs.

DSPs were built to "follow recipes" at blinding speed. Their architectures were already optimized for the exact mathematical operations that dominate neural network computation. The leap from signal processing to neural network inference was shorter than it might appear from the outside.

In 2017, CEVA launched the NeuPro family, its first AI processors designed specifically for deep learning inference at the edge. The naming was deliberate: NeuPro signaled that this was not a repurposed DSP but a purpose-built neural processing unit.

The initial products targeted computer vision applications: smartphones performing computational photography (the portrait mode background blur on your phone requires real-time neural network inference), surveillance cameras identifying people and objects, and automotive systems detecting pedestrians and lane markings. Each of these applications requires running neural networks hundreds or thousands of times per second, on a power budget measured in milliwatts, inside chips that cost a few dollars. That is an engineering challenge radically different from running GPT-4 in a data center, and it requires radically different hardware.

The edge AI thesis that underpinned this strategy was straightforward. While cloud-based AI processing, running models on massive GPU clusters in data centers, would dominate training and large-scale inference, there were billions of devices that needed to run AI locally. A self-driving car cannot wait for a round trip to the cloud to decide whether to brake. A security camera processing a hundred frames per second cannot stream all that video to a remote server. A smartphone applying portrait mode blur needs to process the image on-device for instant results.

These edge inference workloads required processors that combined strong AI performance with extremely low power consumption, exactly the trade-off CEVA had been optimizing for decades.

The numbers tell the story of why edge AI matters: by some estimates, the world generates over three hundred million terabytes of data per day, much of it from sensors, cameras, and microphones at the edge. Transmitting even a small fraction of that data to the cloud for processing would overwhelm global network infrastructure. The only scalable solution is to process most of that data where it is generated, on the device itself. That requires embedded AI processors, and CEVA wanted to be the company licensing those processors.

The product line evolved rapidly. The CEVA-XM4 and XM6 vision processors combined traditional DSP capabilities with dedicated neural network acceleration. The SensPro architecture, introduced in 2020, merged vision, radar, LiDAR, and AI processing into a single platform targeting automotive and industrial applications. And the NeuPro-M, launched in 2022, represented a substantial leap forward: a heterogeneous architecture that could scale from two trillion operations per second in IoT devices to two hundred fifty-six TOPS in data center configurations.

The market positioning was ambitious. CEVA was competing not just against other IP licensors like Cadence and Synopsys but against custom silicon designs from companies like Google (with its Tensor Processing Unit), Apple (with its Neural Engine), and an armada of well-funded AI chip startups. The pitch to customers was pragmatic rather than revolutionary: licensing CEVA's AI IP was faster and cheaper than designing a custom NPU from scratch, especially for companies that needed AI capability but were not large enough to justify a dedicated AI silicon team.

Building the software ecosystem proved as important as the hardware architecture. CEVA invested heavily in making its AI processors compatible with popular machine learning frameworks like TensorFlow and PyTorch. The company developed NeuPro Studio, an integrated development environment that allowed customers to optimize and deploy neural network models on CEVA hardware. In the AI processor market, hardware without a mature software stack is essentially useless. Customers do not just license a processor core; they license an entire development environment.

Key design wins during this period came disproportionately from Chinese semiconductor companies, which were aggressively building AI-capable chips for smartphones, surveillance cameras, and smart home devices. CEVA also secured automotive design wins, with NXP integrating CEVA's SensPro AI DSP into its S32-series real-time processors for software-defined vehicles.

Financially, the AI pivot contributed to CEVA's strongest growth period. Revenue climbed from seventy-three million in 2016 to eighty-eight million in 2017 and continued growing, reaching one hundred million for the first time in 2020. But the relationship between AI licensing revenue and AI royalty revenue had a multi-year lag built in. Customers who licensed NeuPro in 2017 or 2018 would not ship production silicon until 2020 or 2021 at the earliest. The long-term bet was that AI would eventually become CEVA's largest royalty contributor, but proving that thesis required years of patient investment. And the question of where all those AI-hungry customers were located raised a different kind of concern entirely.

VIII. The China Question and Geopolitical Tailwinds (2017-2021)

In 2015, the Chinese government published "Made in China 2025," a sweeping industrial policy that identified semiconductor self-sufficiency as a national strategic priority. China was importing over two hundred billion dollars worth of semiconductors annually, more than it spent on crude oil. Beijing wanted to change that, and it began pouring tens of billions of dollars into domestic chip companies through subsidies, government procurement preferences, and targeted investment funds.

For CEVA, this created a powerful tailwind. Chinese fabless semiconductor companies, racing to develop competitive chips quickly, were voracious consumers of licensed IP. Building a DSP core or a Bluetooth stack from scratch takes years. Licensing proven IP from CEVA could compress that timeline to months. The economic logic was irresistible for companies under political pressure to deliver domestic alternatives to Western chips.

Unisoc (formerly Spreadtrum), which had been licensing CEVA DSP cores since the feature phone era, expanded its use of CEVA IP into 4G, 5G, and IoT. Dozens of other Chinese chipmakers followed. By 2021, China accounted for fifty-nine percent of CEVA's total revenue. By 2022, that figure reached sixty-three percent. CEVA had effectively become a China-dependent company, with well over half its business tied to a single country's semiconductor ambitions.

This concentration created an extraordinary geopolitical vulnerability. When the United States placed Huawei on the Entity List in May 2019, restricting American companies from selling technology to the Chinese telecom giant, the ripple effects reached every corner of the semiconductor supply chain. CEVA, as a U.S.-incorporated company, was directly subject to these restrictions. Any customer on the Entity List became off-limits for new licensing agreements, and even royalty collections faced legal scrutiny.

CEVA's management attempted to position the company as "Switzerland" in the U.S.-China tech war, a neutral technology provider serving customers on both sides of the geopolitical divide. But the reality was more complicated. Each new round of U.S. export controls created uncertainty about whether CEVA could continue serving its Chinese customers.

At the same time, the export controls paradoxically accelerated Chinese demand for licensed IP. As Chinese companies were cut off from buying finished American chips, they doubled down on designing their own, using licensed IP blocks from companies like CEVA as building materials. The sanctions were simultaneously a threat and a catalyst.

This dynamic created a bizarre strategic reality. The more the U.S. government restricted Chinese access to advanced chips, the more Chinese companies needed to license IP to build their own alternatives. CEVA was, in effect, benefiting from the very geopolitical tensions that also posed the greatest risk to its business. It was like selling umbrellas during a hurricane: the worse the storm got, the more customers showed up, but the hurricane could also blow the store away.

The double-edged nature of CEVA's China exposure became a central topic on every earnings call. Analysts pressed management on customer concentration risk, on the possibility of broader export controls, and on whether CEVA was building a business that could be disrupted by a single policy decision in Washington. Management's response was consistent: CEVA was diversifying its customer base geographically and by end market, but China would remain a significant portion of revenue because that is where the volume growth in semiconductor design was happening.

By 2024, China's share of CEVA's revenue dipped to forty-nine percent, suggesting some success in geographic diversification. But in the first half of 2025, it bounced back to approximately sixty percent, demonstrating how difficult it is to reduce dependence on the world's most active market for new chip designs.

For investors, the China question remains the single most important risk factor in CEVA's story: a risk that simultaneously drives the company's growth and threatens its stability. No amount of strategic positioning can fully mitigate a risk that is fundamentally political in nature. And the risk is not binary: even short of outright restrictions, the mere threat of policy changes creates uncertainty that depresses valuation multiples and makes long-term planning difficult.

IX. Third Inflection Point: 5G, UWB, and Sensing Fusion (2020-2023)

Every new generation of wireless technology creates disruption in the semiconductor industry, and 5G was no exception. The jump from 4G LTE to 5G New Radio required fundamentally new modem architectures, new radio frequency designs, and new baseband processing capabilities. For CEVA, this represented both an opportunity and a test: could it provide competitive 5G IP to chipmakers designing their own modem alternatives to Qualcomm's integrated solutions?

CEVA's answer was the PentaG platform, launched in 2018 as the company's first comprehensive 5G New Radio IP solution. The second-generation PentaG2, introduced in 2022, delivered a four-fold improvement in power efficiency and covered the full range of 3GPP profiles, from low-bandwidth IoT applications to high-throughput enhanced mobile broadband. The PentaG-RAN variant targeted 5G infrastructure, providing baseband processing IP for the base stations and small cells that form the backbone of 5G networks.

The most intriguing 5G development for CEVA, however, was one the company could not publicly discuss in detail. In early 2025, CEVA reported receiving its first royalty payment from a "leading US OEM" that had incorporated CEVA technology into an in-house 5G modem. The identity of the customer was an open secret in the semiconductor industry: Apple, which had been developing its own cellular modem to replace Qualcomm's baseband chips, had used CEVA IP in its C1 modem chip.

The significance was profound. Apple, the company that had driven the smartphone consolidation that nearly destroyed CEVA a decade earlier, was now a CEVA royalty customer. The irony was almost too perfect. More practically, Apple ships over two hundred million iPhones per year. If the C1 modem scales across the iPhone lineup, the royalty contribution could become one of CEVA's most material revenue streams, a remarkable outcome for a company that was nearly killed by the smartphone era.

Beyond 5G, CEVA expanded into ultra-wideband technology, a short-range wireless protocol that enables centimeter-level precision positioning. Apple's U1 chip, introduced in the iPhone 11 in 2019, popularized UWB for consumer applications like AirTags and digital car keys. The broader industry followed, with UWB finding applications in automotive (child presence detection, digital keys), industrial tracking, and smart home devices. CEVA launched its Ceva-Waves UWB platform in 2021, extending its connectivity portfolio into yet another wireless protocol.

The sensor fusion strategy also took shape during this period. In July 2019, CEVA acquired Hillcrest Labs from InterDigital, gaining the MotionEngine sensor fusion platform that had been shipped in over one hundred million devices. Hillcrest had spent more than fifteen years developing its sensor processing technology, originally for consumer electronics like smart TV remote controls and gaming devices.

MotionEngine fused data from accelerometers, gyroscopes, and magnetometers to enable intelligent motion sensing in VR headsets, remote controls, robotics, and wearables. Combined with CEVA's existing vision and audio processing capabilities, the acquisition made CEVA a comprehensive sensing platform: a company that could process data from cameras, microphones, motion sensors, radar, and LiDAR, all through licensed IP.

This period also saw CEVA's one significant strategic misstep. In May 2021, the company acquired Intrinsix Corporation, a Massachusetts-based custom SoC design services firm, for thirty-three million dollars. The idea was to offer turnkey chip design services alongside IP licensing. But design services are a fundamentally different business from IP licensing: lower margins, more labor intensity, different customer dynamics. By September 2023, CEVA had sold Intrinsix to Cadence Design Systems, effectively acknowledging the acquisition had been a dead end. The episode was a reminder that diversification can be taken too far and that CEVA's core competency was designing IP, not designing chips.

The broader financial trajectory during this period was a roller coaster. Revenue surged from one hundred million in 2020 to a record one hundred twenty-three million in 2021, then to one hundred thirty-one million in 2022, driven by the post-COVID boom in chip demand and a surge in licensing activity. For a brief moment, it looked like CEVA might finally be achieving escape velocity.

Then it crashed twenty-six percent to ninety-seven million in 2023 as the semiconductor industry entered a cyclical downturn. COVID-era supply chain chaos, which had initially created a chip shortage that inflated orders, was followed by an inventory correction as customers discovered they had over-ordered. The whipsaw effect, from shortage to glut, hit CEVA's customers hard. When chipmakers reduce production to work through excess inventory, royalties to IP licensors dry up immediately. The lumpiness that had always characterized the business model was on full, painful display.

X. Present Day: The AI Everywhere Era (2023-2025)

In January 2023, CEVA entered a new era with a new leader. Gideon Wertheizer, after seventeen years as CEO, retired and handed the reins to Amir Panush. Wertheizer had guided the company through its smartphone crisis and IoT reinvention, building revenue from thirty-five million to over one hundred thirty million at the peak. He remained on the board in an advisory role.

Panush brought a different background to the job. He had previously served as CEO and General Manager of InvenSense within the TDK group, where he had more than doubled revenue. Before that, he held leadership roles at Qualcomm and Atheros Communications. Where Wertheizer was the patient engineer-CEO, Panush was a commercially oriented executive experienced in the sensor and connectivity markets that CEVA was targeting.

Panush inherited a company in transition. The 2023 revenue decline to ninety-seven million dollars reflected the cyclical downturn, but it also masked positive underlying trends. The number of licensing deals was growing, the AI product line was gaining traction, and the installed base of CEVA-powered devices continued to expand.

The generative AI explosion of 2023-2024, triggered by ChatGPT and the large language model revolution, posed an existential question for CEVA's edge AI strategy. If the most impressive AI capabilities required massive data center GPU clusters, did edge AI inference still matter?

CEVA's answer was that generative AI actually reinforced the need for edge processing. Privacy regulations in Europe and Asia are pushing computation toward local processing. Latency-sensitive applications cannot tolerate cloud round-trips. Bandwidth limitations make it impractical to stream all sensor data to remote servers. And power constraints in battery-operated devices make cloud connectivity for every inference operation economically absurd.

A smart doorbell camera cannot stream every frame to a cloud server for analysis. An autonomous vehicle cannot tolerate cloud round-trip latency when deciding whether to brake. A hearing aid performing real-time noise cancellation needs on-device AI, period. The sheer volume of data generated by edge sensors, cameras, microphones, and motion detectors, vastly exceeds what can be economically transmitted to the cloud. Most AI inference, by volume of operations if not by revenue, will happen at the edge.

In 2025, CEVA declared it a "breakthrough year" for AI. The company signed ten NeuPro NPU licensing agreements, more than doubling its AI customer base. AI-related licensing contributed over twenty percent of total licensing revenue, with AI representing approximately one-third of licensing revenue in the second and third quarters. Six AI customers were expected to have production silicon by the end of 2026, with royalties potentially beginning in early 2027. Panush branded the company's vision as "Physical AI," the convergence of connectivity, sensing, and inference inside intelligent edge devices.

The full-year 2025 financial results, announced on February 17, 2026, showed modest top-line growth but improving underlying metrics. Total revenue reached one hundred ten million dollars, up two percent from the prior year. Licensing revenue grew six percent to sixty-four million, while royalties dipped two percent to forty-six million due to smartphone softness and memory-related supply shortages. The company signed fifty-four licensing deals, up twenty-six percent from forty-three in the prior year. Units shipped reached 2.1 billion, up six percent.

The fourth quarter was CEVA's strongest ever, with record revenue of thirty-one million dollars and a non-GAAP operating margin of eighteen percent. That fourth quarter run rate, if annualized, would imply roughly one hundred twenty-five million in annual revenue, close to the prior peak.

On the balance sheet, CEVA ended 2025 with two hundred twenty-two million dollars in cash and investments against just four million in debt. The company is not capital-constrained; quite the opposite. In November 2025, the company had raised approximately sixty-three million dollars through an underwritten public offering, earmarked for potential acquisitions in complementary technologies. The offering diluted shareholders by approximately twelve percent, a price Panush was willing to pay for strategic flexibility.

Looking ahead, management guided for eight to twelve percent revenue growth in 2026, implying revenue of approximately one hundred eighteen to one hundred twenty-three million dollars, with non-GAAP operating income growth of thirty-five to forty percent. The growth drivers are clear: automotive ADAS design wins beginning to generate royalties, continued Bluetooth and Wi-Fi IoT momentum, the Apple modem royalty stream, and new AI NPU customers entering production.

Whether Panush can push CEVA past the revenue threshold where operating leverage kicks in remains the defining question of his tenure. After two decades of hovering between fifty and one hundred thirty million in revenue, never sustaining breakout growth, the next two years will reveal whether the company's AI and automotive bets can change the trajectory.

XI. Business Model Deep Dive: How CEVA Actually Makes Money

The mechanics of CEVA's revenue model deserve careful examination because they explain both the company's resilience and its frustrating financial volatility.

Licensing revenue is the upfront payment a customer makes to access CEVA's IP for a specific chip design. These fees typically range from the low hundreds of thousands for a simple Bluetooth core to several million dollars for a complex AI processor platform. In 2025, CEVA generated sixty-four million in licensing revenue across fifty-four deals, implying an average deal size of roughly 1.2 million dollars. But that average obscures enormous variance: a simple connectivity IP license might be a few hundred thousand dollars, while a comprehensive NeuPro NPU platform license could be several million.

Royalty revenue is the per-unit payment collected every time a customer ships a chip containing CEVA technology. In 2025, CEVA collected forty-six million dollars in royalties on 2.1 billion units shipped, implying an average royalty of approximately two cents per unit. Again, the average masks significant variance. A basic Bluetooth chip might generate a fraction of a cent in royalty, while a 5G modem chip could generate substantially more given the modem's higher average selling price.

The fundamental tension in the business model is the time lag between licensing and royalties. When CEVA signs a licensing deal, the customer typically spends eighteen to thirty-six months designing, verifying, and taping out a chip. Then the chip enters production ramp, starting with small volumes and gradually scaling. It can take three to five years from a licensing agreement to meaningful royalty revenue. This creates a paradox: CEVA's licensing activity today determines its royalty revenue in 2028 or 2029, but investors analyzing quarterly results often miss this forward indicator.

The "land and expand" strategy is central to CEVA's growth playbook. A customer might initially license a single Bluetooth core. Satisfied with the technology and support, they license Wi-Fi for their next chip. Then they add a CEVA DSP for audio processing. Then an AI NPU for on-device inference. Over time, a single customer relationship can grow from a few hundred thousand dollars in licensing to millions, with royalties scaling across multiple product lines. In 2025, CEVA reported that several customers were licensing three or more IP blocks, representing exactly this multi-product expansion.

Customer concentration is the business model's Achilles' heel. While CEVA has over four hundred licensees and lists over two hundred twenty companies on its public licensee page, including blue-chip names like Samsung, Intel, MediaTek, Broadcom, NXP, Renesas, STMicroelectronics, and Sony, the revenue distribution is heavily skewed. The top five customers accounted for approximately forty-five percent of revenue in the third quarter of 2025, and Unisoc alone represented approximately eleven percent. In an industry where customers can be acquired, sanctioned, or simply decide to design their own IP, this concentration creates meaningful risk.

Operating leverage is CEVA's most compelling financial characteristic, and also its most frustrating one. The company spends approximately seventy-five million dollars per year on R&D, regardless of how many customers license the resulting IP. If CEVA can grow revenue to one hundred fifty or two hundred million dollars, the incremental revenue drops almost entirely to the bottom line because there is virtually no incremental cost to serve additional licensees or collect additional royalties. Gross margins already exceed eighty-seven percent.

The challenge is that CEVA has spent more than two decades trying to reach the scale where this operating leverage produces consistently attractive profitability, and it has not yet gotten there. At one hundred ten million in revenue, the company barely generates positive non-GAAP operating income of about ten million dollars. The promise of the model is that it becomes extraordinarily profitable at scale. The risk is that scale may never arrive.

Compared to ARM, which generates over three billion dollars in annual revenue with operating margins exceeding forty percent, CEVA's model is structurally identical but economically subscale. Both companies license IP and collect royalties. Both have minimal cost of goods sold. But ARM's processor cores are in virtually every mobile device on the planet, giving it a royalty base that dwarfs CEVA's. The comparison is less about business model quality and more about market size and dominance: ARM won the general-purpose mobile processor market, while CEVA occupies narrower niches in DSP, connectivity, and edge AI.

XII. Strategic Frameworks: Porter's Five Forces and Hamilton's Seven Powers

Analyzing CEVA through established strategic frameworks reveals a company with genuine competitive advantages that are nonetheless narrower and more vulnerable than they might appear.

Starting with Porter's Five Forces: the threat of new entrants into the semiconductor IP licensing market is moderate. The technical barriers are formidable: designing a production-quality DSP or NPU core requires deep expertise in processor architecture, silicon implementation, verification methodology, and software toolchain development. Building the customer relationships and ecosystem support that make customers willing to bet their chip designs on your IP takes a decade or more. However, the barriers are not insurmountable. Well-funded startups, particularly those backed by strategic investors, continue to enter the market with AI-focused processor IP.

Supplier bargaining power is minimal. CEVA's primary inputs are engineering talent and electronic design automation software licenses from companies like Cadence and Synopsys. While EDA tools are expensive and the talent market in Israel is competitive, these costs are manageable and do not give suppliers meaningful leverage over CEVA's pricing or strategy. There is an interesting irony here: Cadence and Synopsys are simultaneously CEVA's EDA tool suppliers and its IP licensing competitors, a dynamic that creates occasional tension but has not materially disadvantaged CEVA.

Buyer bargaining power is CEVA's most significant competitive challenge. CEVA's customers are large, sophisticated semiconductor companies like Unisoc, NXP, Samsung, and MediaTek. These customers have alternatives: they can license IP from Cadence (Tensilica), Synopsys (ARC), ARM (Ethos NPU), or Imagination Technologies. They can also design their own processor cores internally, and many do. This competition gives buyers significant negotiating leverage on licensing fees and royalty rates. Every new design generation represents a renegotiation opportunity for the customer and a retention challenge for CEVA.

The threat of substitutes is perhaps the most critical force. CEVA's IP competes not just against other licensable IP but against the fundamental decision of whether to license IP at all. The largest semiconductor companies, Apple, Qualcomm, NVIDIA, Google, increasingly design their own processor cores for critical workloads. As more companies move toward custom silicon, the addressable market for licensed IP could shrink in the highest-value segments.

CEVA's counterargument is that custom design is only economical for the very largest companies, and that the long tail of hundreds of smaller chipmakers will always need licensed IP. That argument is valid today but could erode if design tools become more accessible or if AI itself lowers the cost of custom chip design.

Competitive rivalry is intense and asymmetric. Cadence and Synopsys, as diversified EDA and IP companies with annual revenues exceeding five and six billion dollars respectively, can subsidize their IP businesses with profits from other divisions. A competitive IP core from Cadence's Tensilica division does not need to be independently profitable; it just needs to be good enough to sell alongside Cadence's design tools. That is an enormous structural advantage against a pure-play IP licensor like CEVA.

ARM, with its dominant position in mobile processors and its expansion into AI with the Ethos NPU family, represents a competitive threat that could expand into CEVA's core markets at any time. ARM's customer relationships are deeper, its sales force larger, and its brand recognition incomparably stronger.

Within the narrower DSP and connectivity IP segments, CEVA maintains strong market share, including the claimed sixty-eight percent of the wireless connectivity IP market. But maintaining that position requires continuous innovation against well-resourced competitors who view IP licensing as one piece of a much larger business.

Turning to Hamilton Helmer's Seven Powers framework, the picture is mixed. CEVA possesses genuine switching costs: once a chipmaker designs a chip around CEVA's DSP or NPU architecture, switching to a competitor's architecture for the next chip generation requires re-engineering the entire signal processing or AI pipeline. The software written for a CEVA core does not run on a Tensilica core. This creates meaningful stickiness, but only for the duration of that specific product generation. Each new chip design is a new decision point where the customer can switch.

Scale economics are limited. CEVA's R&D costs do not decline dramatically as it adds customers. Each new IP core family requires significant engineering investment regardless of how many customers license it. Network effects exist but are modest: CEVA's ecosystem of development tools, software libraries, and trained engineers creates some gravitational pull, but these effects are far weaker than those enjoyed by software platforms.

Counter-positioning was historically one of CEVA's strengths. The value proposition, license proven IP instead of spending years and millions designing your own, was a classic counter-position against in-house development. But as more companies invest in custom silicon teams and as EDA tools improve, this counter-position has weakened.

Cornered resources consist of CEVA's patent portfolio (158 patents as of the end of 2024) and its deep institutional expertise in DSP architecture built over more than two decades. These resources are real but not insurmountable. Patents expire. Engineers change companies. Expertise can be replicated with sufficient investment.

Process power, Helmer's seventh force, is moderate. CEVA has accumulated over two decades of experience in designing optimal IP cores for signal processing and wireless connectivity. That institutional knowledge, the accumulated understanding of what trade-offs work in real silicon, cannot be easily documented or transferred. But it is not unique. Cadence's Tensilica team and ARM's processor architects possess comparable depth in their respective domains.

The verdict is that CEVA's moat is real but narrow. Switching costs and specialized expertise provide genuine protection within existing customer relationships and product generations. But power shifts back to the customer with each new design cycle, and CEVA must continually earn its position through superior technology, better support, and competitive pricing. This is a company that must run fast just to stay in place.

XIII. Bull vs. Bear Case

The bull case for CEVA rests on several converging secular trends and a business model that has not yet reached its natural operating leverage inflection point.

Edge AI remains in its infancy. Despite the attention lavished on cloud-based large language models, the vast majority of AI inference will ultimately run on devices at the edge of the network. Privacy regulations in Europe and elsewhere are pushing computation toward local processing. Latency-sensitive applications in automotive, industrial, and healthcare cannot tolerate cloud round-trips. Power-constrained devices like earbuds, sensors, and wearables need on-device intelligence. CEVA's NeuPro NPU family targets exactly these workloads, and the ten licensing deals signed in 2025 suggest meaningful customer adoption.

The 5G and connectivity cycle provides durable demand. Every new wireless standard creates a design cycle that generates licensing revenue, and every device implementing that standard generates royalties. CEVA's connectivity IP portfolio, spanning Bluetooth 6.0, Wi-Fi 6/7, 5G NR, NB-IoT, and UWB, positions it to capture royalties across the entire spectrum of wireless devices. The sixty-eight percent market share in wireless connectivity IP suggests a dominant position that is difficult to dislodge.

Automotive represents a long-duration growth driver. ADAS systems are becoming standard equipment in new vehicles worldwide, and each system requires vision processing, radar processing, sensor fusion, and AI inference. Automotive design cycles are notoriously slow, with three to five years from design win to production ramp, but the royalty streams they produce are equally long-lived, often lasting a decade or more. CEVA signed seven automotive licensing deals in 2025, with production silicon expected by the end of 2026.

The Apple modem represents a potential step function. If Apple's C1 modem ships in hundreds of millions of iPhones annually, the per-unit royalty could add meaningfully to CEVA's royalty base. This single customer relationship could substantially boost smartphone royalty contribution.

Operating leverage is the financial bull case in a single phrase. With gross margins above eighty-seven percent, essentially all incremental revenue drops to operating income. If CEVA can grow revenue from one hundred ten million to one hundred fifty million, non-GAAP operating income could potentially quadruple from its current base. The fixed-cost nature of R&D means revenue growth translates into disproportionate earnings growth.

Acquisition premium also deserves mention. CEVA's wireless connectivity IP, AI NPU technology, and automotive design wins would be strategically valuable to larger semiconductor or IP companies like Cadence, Synopsys, or Qualcomm. The company's relatively modest market capitalization, in the range of five hundred to six hundred million dollars, makes it a digestible target. For a company like Cadence, which generates over five billion in annual revenue, acquiring CEVA would be a bolt-on deal that could meaningfully expand its IP portfolio in connectivity and AI.

The bear case, however, is equally compelling and arguably more grounded in historical evidence.

Commoditization is the central risk. ARM continues to expand its processor portfolio into DSP-like and AI workloads. Cadence's Tensilica and Synopsys's ARC processors are formidable competitors backed by companies with vastly larger R&D budgets. If these competitors offer "good enough" alternatives to CEVA's specialized IP, pricing pressure could intensify and market share could erode. The addressable market may increasingly be limited to the long tail of mid-tier and emerging chipmakers, a viable market but one with limited pricing power.

China exposure represents a binary geopolitical risk. With approximately sixty percent of revenue derived from Chinese customers, a single policy decision in Washington, expanding export controls to cover semiconductor IP licensing to certain Chinese entities, could devastate CEVA's business. The company has limited ability to diversify away from China because that is where the marginal demand for licensed semiconductor IP is strongest.

Customer concentration compounds the risk. When a single customer like Unisoc represents eleven percent of revenue, and the top five account for forty-five percent, the loss of any major relationship would be material.

Revenue predictability remains elusive. After more than two decades as a public company, CEVA's quarterly revenue remains difficult to model. The 2022-2023 swing from one hundred thirty-one million to ninety-seven million dollars, a twenty-six percent decline, underscored the inherent volatility. The company has a history of guiding to royalty ramps that arrive later than expected. The Intrinsix acquisition and subsequent divestiture represent a strategic misstep.

The persistent gap between GAAP and non-GAAP results, driven by stock-based compensation that has been substantial relative to the company's revenue, warrants scrutiny. CEVA has been GAAP unprofitable for multiple consecutive years, even at revenue levels well above its historical average. Investors must decide whether non-GAAP profitability or GAAP profitability is the more relevant measure of the business.

The two key performance indicators that matter most for tracking CEVA's trajectory are: first, the quarterly royalty revenue run rate, which measures whether the installed base of CEVA-powered devices is growing and whether the per-unit economics are improving; and second, the number and composition of new licensing deals, which serves as a leading indicator of royalty revenue two to four years into the future. The mix of those deals, specifically the proportion that are AI-related and automotive-related, reveals whether CEVA is successfully diversifying into higher-value markets. If royalty revenue inflects upward sustainably and licensing deal flow accelerates in high-value segments, the business is working. If either stalls, the structural challenges will dominate.

XIV. The Playbook: Lessons for Founders and Investors

CEVA's twenty-four-year journey as a public company yields lessons that apply broadly to technology businesses operating in similar models and market structures.

IP licensing businesses must survive multiple technology transitions, and survival requires diversification. CEVA nearly died when the smartphone transition consolidated its customer base. It recovered only because management had the foresight, and the financial runway from existing royalties, to pivot into IoT connectivity and then AI. A single-product IP company is a ticking clock: eventually, the market for that product will mature, consolidate, or be disrupted.

Semiconductor investing requires a fundamentally different time horizon than software investing. When CEVA signs an AI NPU licensing deal today, the resulting royalty revenue will not appear until 2028 or 2029, after the customer completes chip design, fabrication, testing, and production ramp. Analyzing current-quarter revenue tells you almost nothing about the company's trajectory. The signal is in the pipeline: how many deals were signed, in which markets, and at what complexity level.

Customer concentration in semiconductor IP licensing is an inherent structural feature, not a management failure. The semiconductor industry is concentrated, with the top ten chipmakers accounting for the vast majority of global chip revenue. An IP licensor serving that industry will inevitably derive a significant portion of its revenue from a handful of large customers. The mitigation is not to eliminate concentration, which is impossible, but to diversify across end markets so that the loss of any single customer does not threaten the entire business.

The royalty model demands patience that most investors cannot sustain. CEVA's royalty base took decades to build. A licensing deal signed in 2014 with a Chinese chipmaker might not generate meaningful royalties until 2017, and those royalties might continue flowing until 2024. The compound effect of hundreds of such relationships creates a royalty stream that is remarkably durable, but the time required to build it is measured in years, not quarters.

In technology licensing, the ecosystem is the product. CEVA's customers do not just license a processor design. They license development tools, software libraries, reference implementations, verification environments, and access to a community of engineers who know how to use the technology. A technically superior IP core without a mature ecosystem will lose to a technically adequate core with a rich one. This is the same dynamic that made Windows dominant over technically superior operating systems in the 1990s: it is the ecosystem, not the technology, that creates lock-in.

Geopolitical risk has become a first-order consideration in semiconductor investing, on par with technology risk and market risk. CEVA's China exposure cannot be analyzed in isolation. It is intertwined with U.S. export control policy, Chinese industrial policy, and the broader technological decoupling between the world's two largest economies. Any investment thesis for a semiconductor IP company must now include a geopolitical scenario analysis, a requirement that did not exist even a decade ago.

Small specialized IP companies face an existential strategic choice: continuously reinvent or consolidate. CEVA has chosen reinvention, pivoting from cellular DSP to IoT connectivity to AI inference. Each pivot has required significant R&D investment and carried execution risk. The alternative, selling to a larger company that can embed CEVA's IP within a broader platform, remains an ever-present option. DSP Group itself was eventually acquired by Synaptics for five hundred forty-nine million dollars in 2021, validating that consolidation is a natural endpoint for many semiconductor IP companies.

Finally, fabless IP models have great economics if you achieve scale. CEVA has not quite gotten there. The gap between CEVA's business model quality and its financial results is a function of scale, and closing that gap remains the central challenge of the company's next chapter. ARM's journey offers both inspiration and caution: it took ARM two full decades from founding to reach the scale where its model generated significant profitability. CEVA is now twenty-four years old and still searching for its version of that inflection point.

XV. What Would We Do If We Ran CEVA?

Running CEVA in 2026 means confronting a genuinely difficult strategic landscape. The company has strong technology, a broad product portfolio, dominant positions in wireless connectivity IP, a growing AI business, and a clean balance sheet with over two hundred twenty million in cash. But it also has single-digit non-GAAP operating margins, persistent GAAP losses, heavy China exposure, and a stock price that has been under pressure.

The most impactful strategic decision is product focus. CEVA's portfolio spans DSP cores, Bluetooth, Wi-Fi, UWB, 5G, NB-IoT, sensor fusion, vision processing, and AI NPUs. Count those: that is nine distinct product categories, each requiring dedicated engineering teams, each competing against specialized rivals. That breadth is impressive for a company with fewer than five hundred employees, but it also risks spreading engineering resources too thin.

The highest-value opportunities are automotive ADAS, where design wins are sticky and long-lived, and AI NPUs, where per-unit royalties are significantly higher than connectivity. A ruthless prioritization of these two markets, with connectivity maintained but not expanded aggressively, would concentrate R&D dollars where the payoff is greatest.

Geographic diversification must accelerate. Sixty percent revenue exposure to China is not sustainable given the trajectory of U.S.-China technology relations. This does not mean abandoning Chinese customers, who represent legitimate, legal business. It means aggressively investing in customer development in India, where semiconductor design activity is growing rapidly, along with Southeast Asia, Europe (particularly automotive), and North America. The Apple modem relationship, if it expands, would naturally reduce China concentration as a percentage of the total.

The business model itself deserves examination. Pure IP licensing has worked for a quarter century. But hybrid models are emerging. Some IP companies are beginning to offer pre-integrated subsystems: combinations of processor cores, software stacks, and reference designs closer to turnkey solutions. CEVA's connectivity platforms already move in this direction. Pushing further could increase switching costs and command higher royalties.

Acquisitions should be targeted and disciplined. The sixty-three million raised in November 2025 was explicitly earmarked for M&A. The most valuable acquisition targets would be companies with complementary IP in areas adjacent to CEVA's existing portfolio. The Intrinsix experience should serve as a cautionary tale: acquisitions that move CEVA away from its core IP licensing model are unlikely to succeed.

And there is the harder question that management and the board must continually evaluate: whether CEVA should remain independent at all. Cadence, Synopsys, Qualcomm, and other larger companies have historically acquired semiconductor IP companies to expand their portfolios. CEVA's wireless connectivity IP, AI NPU technology, and automotive design wins would be strategically valuable to any of these acquirers. An acquirer with a larger sales force, deeper customer relationships, and cross-selling opportunities could potentially extract significantly more value from CEVA's technology than CEVA can independently.

Whether independence or acquisition represents the better path depends on execution over the next two to three years. If the AI licensing deals convert to meaningful royalties, if the automotive ramp materializes, and if revenue grows toward the one hundred fifty million dollar level where operating leverage truly kicks in, independence becomes increasingly viable. If growth stalls in the current range, the case for finding a larger home becomes compelling.

The precedent is clear. In the semiconductor IP space, consolidation is the norm, not the exception. Imagination Technologies was taken private. MIPS was acquired by Wave Computing (and later Syntacore). Tensilica was absorbed by Cadence. ARM itself was acquired by SoftBank for thirty-two billion dollars in 2016 before re-listing in 2023. The question for CEVA is not whether consolidation happens in this industry, but whether CEVA will be one of the consolidators or one of the consolidated.

XVI. Epilogue and Final Reflections

CEVA's story is, at its core, a story about the forgotten middle layer of the technology stack. Consumers interact with products. They know Apple, Samsung, and Google. Investors follow the chip companies: Qualcomm, NVIDIA, Broadcom. But between the product brands and the chip brands sits a layer of intellectual property that enables everything and gets credit for nothing.

CEVA operates in that layer, designing the signal processing engines and wireless connectivity platforms that make modern devices possible, then collecting a few cents every time one of those devices ships. It is the invisible plumbing of the digital world: unglamorous, essential, and utterly unknown to the people who depend on it daily.

The story matters because it reveals both the power and the limitations of the IP licensing model. The power is evident: CEVA has survived for over two decades, weathered multiple existential crises, and built a technology portfolio that ships in over two billion devices per year, all with fewer than five hundred employees and minimal capital expenditure. No factories, no inventory, no supply chain complexity. Just intellectual property and the people who create it.

The limitations are equally clear: despite twenty-four years of operation and over twenty billion cumulative device shipments, CEVA generates barely one hundred ten million dollars in annual revenue and remains GAAP unprofitable. The model creates incredible optionality but demands extraordinary patience. Two cents per chip, multiplied by two billion chips, equals forty-six million in royalty revenue. That is both impressive and sobering.

The three inflection points, the smartphone consolidation crisis of 2010-2013, the IoT and AI pivot of 2014-2020, and the current generative AI era, each tested whether CEVA's management could recognize a technological shift, adapt the product portfolio, and find new customers before the old ones disappeared. Each time, the company reinvented itself just in time.

Perhaps the most surprising insight from CEVA's journey is that being "good enough" at many things can be more durable than being great at one thing in the IP licensing business. CEVA is not the best AI processor. It is not the best Bluetooth IP provider. It is not the best DSP core. But it offers a broad portfolio of competitive-enough technology with the integration, tools, and support that mid-tier chipmakers need. This "good enough across a broad portfolio" strategy may lack the dramatic appeal of a best-in-class single product, but it has proved remarkably resilient because it gives customers a reason to consolidate their IP spending with a single vendor.