COPT Defense Properties: The Landlord to America's Intelligence Community

I. Introduction and Episode Roadmap

There is a 500-acre campus in Annapolis Junction, Maryland, nestled between the Baltimore-Washington Parkway and Route 32, where tens of thousands of people drive to work every morning, badge through security checkpoints, and disappear into buildings with no signage. They cannot discuss what they do. They cannot work from home. And in many cases, they cannot even tell their families which building they sit in. These people work for the National Security Agency, the Defense Intelligence Agency, U.S. Cyber Command, and the constellation of defense contractors that orbit around them — Northrop Grumman, Booz Allen Hamilton, Leidos, and dozens more.

Somebody owns those buildings. Somebody collects the rent checks from the most secretive agencies in the United States government. That somebody is COPT Defense Properties, ticker CDP on the New York Stock Exchange, and this is one of the most unusual business stories in American real estate.

COPT Defense Properties is a Real Estate Investment Trust — a REIT — that has spent nearly three decades transforming itself from a generic suburban office landlord into the dominant real estate provider to America's intelligence apparatus. Today the company owns over 200 properties totaling more than 25 million square feet, with roughly 90% of its rental revenue coming from defense and intelligence tenants. The U.S. government directly accounts for more than a third of rental revenue, and the rest comes overwhelmingly from defense contractors who must locate within a short drive of the installations they serve.

The central question of this story is deceptively simple: How did a suburban Maryland office developer become the indispensable landlord to America's intelligence community? The answer involves post-9/11 budget explosions, a willingness to embrace concentration risk that terrified competitors, and the patient accumulation of advantages that have compounded into something approaching a genuine monopoly in a niche most investors have never heard of.

This is a story about the REITification of national security infrastructure — about what happens when you apply disciplined capital allocation and real estate development expertise to one of the most essential and least understood corners of the American economy. It is also a story about moats, because the moat around this business is not a metaphor. The moat is literal: security fences, armed guards, electromagnetic shielding, and the hard reality that when a tenant invests millions of dollars building a Sensitive Compartmented Information Facility inside your building, they are not casually relocating to a WeWork across town.

Think about that for a moment. In an era when the biggest debate in commercial real estate is whether anyone will ever return to the office, COPT owns buildings where people never stopped coming in. Where tenants cannot leave even if they wanted to. Where the U.S. government — the most creditworthy tenant on Earth — signs leases measured not in years but in decades. Where the competitive moat is not brand recognition or network effects but electromagnetic shielding and vault-grade doors.

What makes this different from every other office REIT story? Office REITs, broadly speaking, have been a disaster for the past several years. Remote work gutted demand for commercial office space. Vacancy rates spiked. Values collapsed. Major landlords defaulted on loans. And yet COPT Defense Properties sailed through this carnage almost entirely unscathed, because you cannot analyze intercepted communications from your kitchen table. You cannot process satellite imagery on your personal laptop. Classified work requires classified spaces, and classified spaces require specialized landlords who understand how to build and operate them.

This is also a story about the compounding power of strategic patience. COPT did not stumble into its dominant position. It built that position over three decades through a series of decisions that, individually, seemed incremental but collectively created something approaching a natural monopoly in one of the most essential and least understood corners of the American economy. The company's evolution mirrors the broader evolution of American national security — from a post-Cold War world searching for purpose to a post-9/11 world drowning in threats, from the War on Terror to great power competition with China, from human intelligence to artificial intelligence.

That is the business. And to understand how it came to be, we need to go back to the late 1980s.

II. Founding Context and The Birth of COPT (1988-1999)

Before this story begins in earnest, a quick primer on the REIT structure, because it matters enormously for what follows. A Real Estate Investment Trust is a company that owns income-producing real estate and is required by law to distribute at least 90% of its taxable income to shareholders as dividends. In exchange, the REIT pays no corporate-level income tax. This structure, created by Congress in 1960, essentially allows ordinary investors to buy shares in a diversified portfolio of real estate the way they might buy shares in any other public company. The key implication: REITs are perpetual capital-raising machines. They cannot retain much earnings, so growth requires either debt or issuing new equity, which means the market's perception of your strategy directly determines your cost of capital and therefore your ability to grow. Keep that in mind.

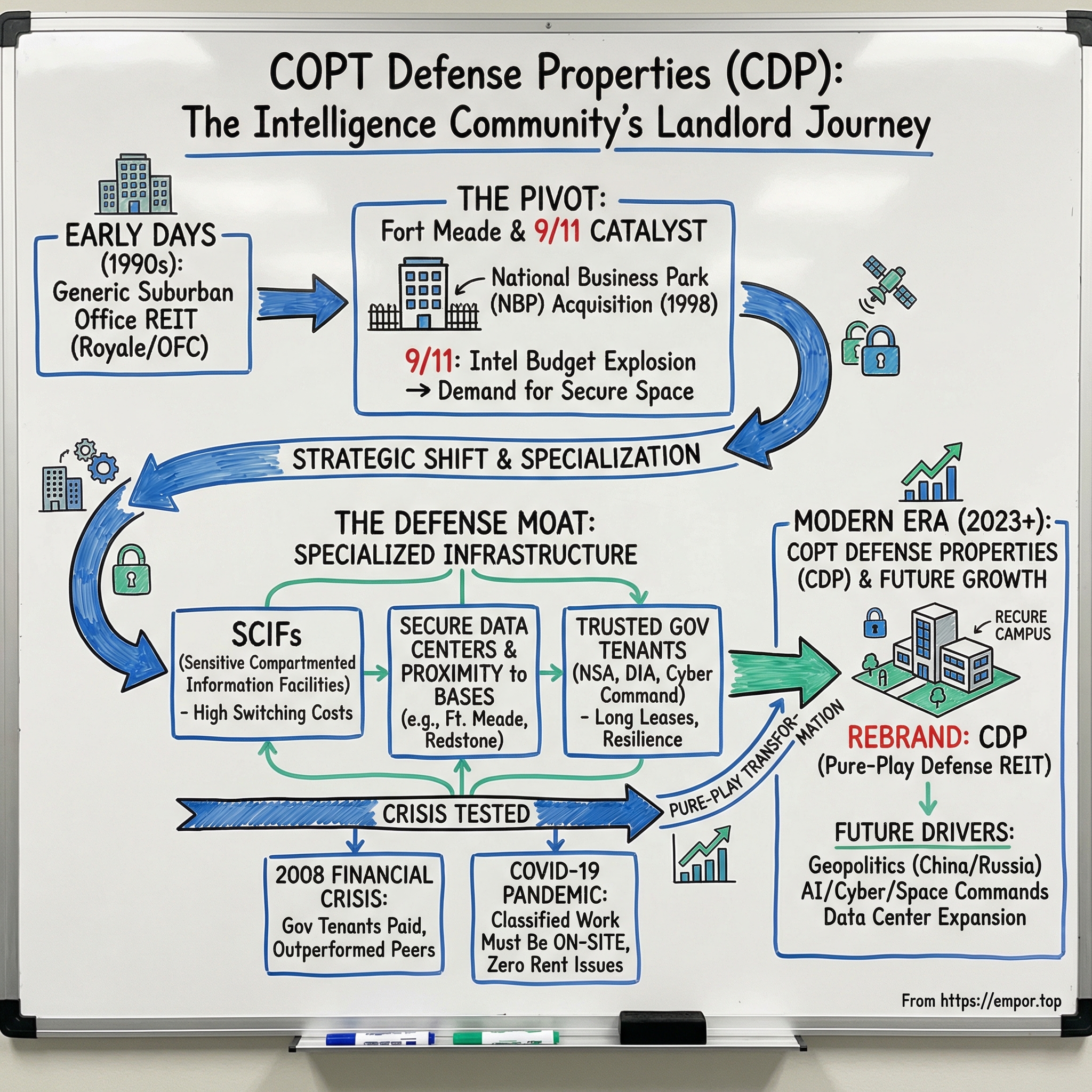

The corporate entity that eventually became COPT Defense Properties was born in 1988 in Minneapolis as Royale Investments, Inc. — a name that tells you exactly nothing about what it would become. Royale went public on NASDAQ in the early 1990s with a modest portfolio of retail properties. It was, by all accounts, an unremarkable vehicle — the kind of tiny public company that traded on thin volume and attracted no institutional attention whatsoever. If you were looking for the future landlord of America's intelligence community, this would be the last place you would look.

The transformation began with Clay W. Hamlin III, a man whose resume reads like a curriculum vitae designed by a committee of overachievers. Born in 1945 in Buffalo, New York, Hamlin attended the Nichols School, then the University of Pennsylvania where he earned his undergraduate degree, an MBA from the Wharton School, and — because apparently two Ivy League degrees were insufficient — a law degree from Temple University. He was also a CPA, a former All-Ivy tennis player inducted into Penn's Tennis Hall of Fame, and a practiced attorney at white-shoe Philadelphia firms Pepper Hamilton & Scheetz and Saul Ewing. The man collected credentials the way some people collect stamps.

In 1989, Hamlin partnered with Jay H. Shidler, a legendary Hawaii-based real estate investor, to form Hamlin/Shidler Investment Corporation. Their focus: commercial real estate in the Mid-Atlantic region, specifically the Baltimore-Washington corridor. Shidler brought capital and deal-making acumen. Hamlin brought operational expertise and deep knowledge of the region's real estate dynamics.

In October 1997, they engineered the deal that created the modern company. Royale Investments acquired the Mid-Atlantic operations of The Shidler Group, and the company was rechristened Corporate Office Properties Trust. Shidler became Chairman of the Board. Hamlin became CEO.

The deal itself was instructive. By using the existing public shell of Royale Investments, Hamlin and Shidler avoided the expense and uncertainty of a traditional IPO. They inherited a public listing, a shareholder base, and the ability to issue equity — all critical capabilities for a REIT that would need to raise capital continuously to fund growth. It was the kind of clever financial engineering that characterized Hamlin's approach: strategic, efficient, and designed to create maximum optionality with minimum friction.

The following April, the company moved its listing to the New York Stock Exchange under the ticker "OFC," a rather prosaic symbol for what would become one of the most unusual REITs in America.

The strategy at this point was straightforward: own and operate Class A suburban office buildings in the Baltimore-Washington corridor. This was not a particularly differentiated thesis. The BW corridor was — and remains — one of the most government-dense metropolitan areas in the world. The Pentagon sits at one end. Fort Meade and the NSA sit in the middle. Aberdeen Proving Ground and the Army's research labs anchor the northern stretch. In between, dozens of agencies, defense contractors, and technology companies were all growing, and they all needed office space. The demand environment was strong, but COPT was positioned as one of several regional office landlords competing for this business — indistinguishable, from an investor's perspective, from any other suburban office play in a government-heavy market.

Then came the 1998 acquisition that put real scale on the map. COPT purchased 16 buildings totaling 1.6 million square feet from Constellation Real Estate Group, a subsidiary of Constellation Energy, Baltimore Gas & Electric's parent company. The deal was structured as a stock-and-cash transaction valued at approximately $203 million, with Constellation receiving a 41.5% stake in the company. This was transformative — it more than doubled the portfolio and gave COPT a substantial footprint across the Baltimore-Washington region, including properties that would prove strategically valuable in ways nobody fully appreciated at the time.

Among those properties was a cluster of buildings in a place called the National Business Park, sitting on roughly 500 acres of land directly adjacent to a sprawling military installation called Fort Meade. At the time, this was just one piece of a diversified suburban office portfolio — a few buildings in a business park that happened to be near a military base. There was nothing in the 1998 annual report to suggest that this particular cluster of properties would prove to be the most strategically valuable real estate in the entire portfolio, or that it would eventually define the entire company's identity.

The late 1990s were an interesting time for the REIT industry more broadly. The sector was still maturing — the modern REIT era had really only begun with the IPO wave of the early 1990s, and investors were still developing the analytical frameworks for evaluating these vehicles. The concept of a "specialty REIT" — one focused on a particular property type or tenant niche rather than broad diversification — was still novel. Most office REITs competed on the same basic dimensions: building quality, location desirability, tenant creditworthiness, and lease terms. The idea that a REIT could build a durable competitive advantage by specializing in one particular type of tenant, with one particular set of building requirements, in one particular geographic corridor, was not yet part of the playbook.

The seed had been planted. But nobody — not Hamlin, not Shidler, not the market — yet understood what it would grow into.

III. The Fort Meade Awakening and Pre-9/11 Positioning (1999-2001)

Fort George G. Meade covers approximately 5,000 acres of central Maryland, situated roughly halfway between Baltimore and Washington, D.C. If you drove past it on the Baltimore-Washington Parkway in the late 1990s, you might not have given it a second glance — another sprawling military installation in a corridor dotted with them.

But behind those fences, Fort Meade had quietly become one of the most important military installations in the world. The National Security Agency — the signals intelligence colossus responsible for intercepting foreign communications and protecting American information systems — had called Fort Meade home since the 1950s. The Defense Information Systems Agency was there too, along with a growing cluster of intelligence and defense operations that would eventually encompass over 116 federal agencies and military commands. By workforce alone, Fort Meade was the second-largest Army installation in the country. By strategic significance, it was arguably the first.

The NSA had a problem. It was growing — fast. The digital revolution was creating exponentially more signals to intercept, more data to process, more codes to break. The agency needed more people, and those people needed offices. But the NSA campus itself was constrained. Building on the installation was slow, bureaucratic, and expensive. Government construction timelines were measured in decades, not quarters. And the agency's vast ecosystem of contractors — the Booz Allens and Northrop Grummans and SIGINTs of the world — needed to be physically close to Fort Meade but could not operate inside the installation's gates.

This is where the National Business Park entered the picture. Located at the southwest corner of Route 32 and the Baltimore-Washington Parkway, the NBP was literally across the street from the NSA. You could stand in its parking lot and see the agency's distinctive black glass buildings. The commute from NBP to NSA was measured not in miles but in minutes — sometimes single-digit minutes.

By 2000, the NBP comprised roughly 900,000 rentable square feet. COPT's first government lease at the park was for a building at 2730 Hercules Road, leased directly to the U.S. Government.

This was an early education in a very different kind of landlording — one that required patience, discretion, and a willingness to learn a new vocabulary of acronyms and security protocols.

Government tenants do not operate like corporate tenants. The lease structures are different — governed by appropriations cycles, General Services Administration schedules, and multi-year funding commitments that work nothing like the standard commercial lease. The buildout requirements are different — SCIFs, security systems, electromagnetic shielding, acoustic protection, access control systems that make corporate lobby security look quaint. The relationship dynamics are different — building trust with government procurement officers and agency facility managers requires patience, security clearances, and a track record that cannot be faked or fast-tracked.

A Sensitive Compartmented Information Facility — a SCIF — deserves a moment of explanation, because it is the single most important concept in understanding COPT's business model. A SCIF is an enclosed area within a building specifically designed and accredited to process classified intelligence information. Think of it as a vault that happens to be an office. The walls must meet specific Sound Transmission Class ratings — a minimum STC of 45, meaning normal human speech cannot be heard from outside. The facility may require electromagnetic shielding to prevent electronic eavesdropping. All electrical and communications systems must be isolated. The doors are vault-grade. The access controls require multiple authentication technologies. Construction costs run between $350 and $1,000 per square foot — many multiples of standard office buildout — and the accreditation process typically takes 12 to 18 months but can stretch to 36 months.

Here is the critical insight: once a tenant has invested millions of dollars building a SCIF inside a building and spent two years getting it accredited, they are not moving. The switching costs are astronomical. The accreditation alone is a bureaucratic ordeal that nobody voluntarily repeats. This creates a tenant stickiness that is essentially unprecedented in commercial real estate.

COPT was learning all of this in real time during the late 1990s and early 2000s — a period of institutional education that would prove far more valuable than any land acquisition.

The company's management team was developing specialized expertise in government lease structures, SCIF construction requirements, and the unique rhythms of defense and intelligence contracting. Most traditional office REITs wanted nothing to do with this market. The leases were structured differently. The buildouts were expensive and specialized. The tenants were agencies and contractors most people had never heard of. It was a niche that required patience and expertise, and the returns were not obviously superior to vanilla commercial office.

There was also a subtlety to government real estate that most commercial developers never grasped: the ecosystem dynamic. Government agencies and the contractors who serve them must be co-located. An NSA analyst working on a classified program might need to meet face-to-face with the Northrop Grumman engineers building the system, the Booz Allen consultants providing analytical support, and the SAIC technicians maintaining the infrastructure — multiple times per day, in spaces where classified discussions can occur. This meant that once you established a critical mass of government and contractor tenants in a location, you created a gravitational pull that attracted additional tenants. Each new lease made the location more valuable for everyone else. It was a network effect built not on software but on security clearances and proximity.

By the turn of the millennium, COPT had accumulated something that would prove more valuable than any physical asset: deep institutional knowledge of how to serve the most demanding landlord-tenant relationship in American real estate. They understood the procurement cycles, the appropriations timelines, the security requirements, the bureaucratic rhythms, and — perhaps most importantly — the unwritten rules of trust and discretion that governed relationships with the intelligence community.

But the relationships COPT built during this period — the trust, the track record, the institutional knowledge — would prove invaluable when the world changed on a Tuesday morning in September 2001.

IV. 9/11 and the Inflection Point: Becoming a Defense REIT (2001-2008)

On September 11, 2001, the world shifted — and with it, the trajectory of a suburban Maryland office REIT that most investors had never heard of. The attacks on the World Trade Center and the Pentagon did not just reshape American foreign policy and military strategy. They triggered the largest sustained increase in intelligence and defense spending in a generation, and that spending needed to go somewhere physical. It needed buildings. Offices. Secure facilities. Data centers. And it needed them close to the installations where America's intelligence apparatus was headquartered.

The numbers were staggering. Between 2001 and 2011, the Pentagon's annual budget more than doubled, reaching $691 billion. Within that surge, intelligence spending grew even faster — the classified intelligence budget, estimated by experts at roughly $30 billion before 9/11, would more than double over the following decade. The NSA, already the largest employer at Fort Meade, expanded aggressively. New missions were created. New agencies were established. The creation of the Department of Homeland Security in 2002 consolidated 22 federal agencies under one umbrella. The establishment of the Director of National Intelligence in 2004 created a new coordinating layer atop the 17 agencies of the intelligence community. The steady ramp-up of signals intelligence capabilities — driven by the explosion of digital communications that terrorists and adversaries now used — demanded computing infrastructure on a scale the NSA had never previously needed.

All of this required physical infrastructure. Buildings with SCIFs. Secure computing facilities. Office space for the tens of thousands of additional intelligence professionals and contractors being hired. And that infrastructure needed to be located near the installations where the intelligence community was headquartered — not in downtown Washington or suburban office parks miles away, but within the security perimeter or directly adjacent to Fort Meade, Fort Belvoir, and the other nerve centers of American intelligence.

COPT's management made a strategic decision that was, in retrospect, the defining choice in the company's history: lean into this wave with everything they had. Rather than treating the defense and intelligence niche as one segment of a diversified portfolio, they began reorienting the entire company around it. While other suburban office landlords in the corridor viewed the intelligence community as just another tenant category — nice to have but not worth specializing in — COPT's leadership recognized something deeper. The intelligence infrastructure boom was not a temporary blip. It was a generational shift in how the United States projected power, and it would require a generational commitment of physical infrastructure to support.

This was controversial. In REIT investing, diversification is gospel. The conventional wisdom holds that concentrating your tenant base in a single sector — especially one dependent on government appropriations — is reckless. What happens when budgets get cut? What happens when a new administration decides to slash intelligence spending? What happens when a war ends? These were legitimate questions, and they would haunt COPT's stock price during lean years. But management's conviction was that the defense and intelligence opportunity was generational, and that half-measures would mean losing the race for strategic land and relationships to competitors who might never materialize anyway.

The National Business Park became ground zero for this strategy. While competitors debated the merits of defense concentration from the safety of their boardrooms, COPT was on the ground acquiring parcels and signing leases.

The company systematically acquired additional parcels around Fort Meade, expanding the NBP from roughly 900,000 square feet at the turn of the millennium to over 3.2 million square feet over the following dozen years. That represented a compound annual growth rate of approximately 12% — significantly outpacing the broader Baltimore-Washington Class A office market, which grew at roughly 9% annually during the same period. COPT was not merely participating in the market. It was capturing a disproportionate share of the growth.

The Base Realignment and Closure process — known as BRAC — added rocket fuel. BRAC is the congressionally authorized process by which the Department of Defense consolidates military installations and relocates personnel. The 2005 BRAC round directed thousands of additional personnel to Fort Meade and to Fort Belvoir in Northern Virginia, where the National Geospatial-Intelligence Agency relocated its headquarters in 2011, bringing roughly 19,300 additional personnel and requiring 6.2 million square feet of space in the area. Each relocated employee represented potential demand for contractor office space in the surrounding communities — demand that COPT was uniquely positioned to capture.

The competitive advantage was becoming clear. Building to government specifications — SCIFs, hardened facilities, electromagnetic shielding, multi-factor access control — required specialized knowledge that generic office developers simply did not possess. Understanding government lease structures — how appropriations work, how multi-year commitments are structured, how GSA schedules function — required years of institutional learning. And perhaps most importantly, earning the trust of the intelligence community's facility managers required a track record that could not be acquired; it had to be built year by year, project by project.

By 2008, defense and government tenants had become the majority of COPT's revenue. The company had achieved a total return of 648% in the decade since its NYSE listing in 1998 — among the highest returns of any publicly traded REIT in the country during that period. Clay Hamlin, who served as CEO through 2005, had laid the strategic foundation. Randall Griffin, who succeeded him, was pushing the development pipeline hard. Griffin brought an eclectic background — he had previously served as Vice President of Development for EuroDisney Development in Paris from 1990 to 1993, managing all non-theme park development for the 5,000-acre project — and he directed $3.8 billion in development activity during his tenure at COPT through early 2012. The pivot from generalist office REIT to defense-focused landlord was essentially complete.

The development model that emerged during this period was distinctive and deliberately conservative. Rather than building speculatively and hoping to fill the space, COPT focused on build-to-suit projects where the tenant committed before construction began. A government agency or defense contractor would identify a space requirement, COPT would propose a building tailored to those specifications, and the lease would be signed before the first shovel hit dirt. This eliminated lease-up risk and produced predictable returns. The trade-off was slower growth — you could only develop as fast as tenants committed — but the quality of that growth was exceptional. Every new building was essentially pre-sold.

The lease terms reflected the unique economics of the relationship. Government and defense contractor leases typically ran 10 to 15 years, with built-in rent escalators that provided organic revenue growth. Compare that to the typical commercial office lease of five to seven years, with tenants who might negotiate hard for concessions at renewal or simply leave. COPT's tenants signed longer, paid more reliably, and renewed at higher rates than virtually any other category of office tenant in America.

For investors watching this transformation, the implications were becoming undeniable. COPT had built something that looked less like a typical office REIT and more like a toll booth on the highway of American intelligence spending. Every dollar Congress appropriated for signals intelligence, cybersecurity, or defense contractor support eventually translated into demand for the kind of specialized space that COPT was building. The question was whether this concentration was brilliant positioning or dangerous dependence. The financial crisis was about to provide a compelling answer.

V. The Financial Crisis and the Government Tenant Advantage (2008-2010)

When Lehman Brothers collapsed in September 2008 and the American financial system teetered on the edge of the abyss, the office REIT sector went into free fall. Corporate tenants defaulted on leases, vacancy rates spiked, property values cratered, and equity prices followed. The NAREIT All Equity REITs Index plummeted 67% from its January 2007 high to its February 2009 low, with the steepest decline — a breathtaking 60% drop — occurring in just five months between September 2008 and February 2009. Office REITs, exposed to corporate tenants whose businesses were imploding, were among the hardest hit.

COPT was a revelation. From July 2008 through June 2009 — the very worst stretch of the crisis — the total return for the office REIT sector excluding COPT fell approximately 50%. COPT's total return during the same period declined by only 10%. That is a 40-percentage-point spread in a single year, and it was not luck. It was the direct consequence of the strategic choices the company had been making for the preceding decade.

The logic was elegant in its simplicity. The United States government does not default on its leases. It cannot go bankrupt. Intelligence agencies do not furlough their analysts because GDP contracted. The War on Terror did not pause for a financial crisis. While commercial landlords were watching tenants break leases and go dark, COPT's tenants — NSA, DIA, Northrop Grumman, Booz Allen Hamilton — kept showing up, kept paying rent, and in many cases kept expanding. Government credit quality is the gold standard, backed by the full faith and credit of the United States. For the first time, the broader REIT investing community fully grasped what "government tenant" really meant.

The crisis created a secondary advantage: capital access. In the REIT world, the ability to raise equity capital at favorable prices is everything — it determines whether you can grow, acquire, and develop, or whether you are stuck managing a stagnant portfolio. When capital markets partially reopened in 2009 and 2010, COPT found itself in the enviable position of being one of the few office REITs that could issue equity without massively diluting existing shareholders. The company's stock had declined far less than its peers, which meant its cost of equity capital was far lower. This created a window of opportunity that management exploited aggressively, selling non-core suburban office assets and redeploying proceeds into developments near Fort Meade and other defense installations. The result was a kind of strategic arbitrage: selling generic assets at crisis prices while investing in defense assets at prices that reflected COPT's privileged access to a market that almost nobody else could serve.

The financial crisis did not merely validate COPT's strategy — it catalyzed a flight to quality within REIT investing. Institutional investors who had previously dismissed the company's government concentration as a risk factor began to view it as an asset. The narrative flipped. Concentration risk became "mission-critical tenant base." Government dependence became "recession-proof revenue stream." The market was beginning to understand what COPT's management had understood for years: in real estate, the best tenant is the one who absolutely, positively has to be in your building, and nobody fits that description like the intelligence community.

The crisis also highlighted a concept that real estate investors often discuss but rarely see demonstrated so cleanly: the difference between credit risk and occupancy risk. In commercial office, the two are closely linked — a tenant's creditworthiness deteriorates, they default on the lease, and the space goes empty. With government tenants, credit risk is essentially zero. The U.S. government, whatever its fiscal challenges, has never failed to honor a real estate lease. This means the only real risk for COPT is occupancy — whether the government continues to need the space. And given that intelligence operations are not discretionary, the occupancy risk proved minimal as well.

The crisis also exposed a structural advantage that would become even more apparent during the COVID era a decade later. Government and intelligence workers cannot work from home. This is not a preference or a policy choice — it is a physical impossibility. You cannot access classified systems from a residential internet connection. You cannot store Top Secret documents in your home office. The work requires being physically present in a SCIF, which requires being physically present in a COPT building. This created a floor under occupancy rates that simply did not exist for commercial office landlords.

The lesson was clear, and the market internalized it. COPT's government tenant base was not merely a nice-to-have diversification benefit — it was a fundamentally different risk profile that warranted a different valuation framework. The company was not really competing with other office REITs. It was operating in a parallel universe where the rules of commercial real estate — cyclical demand, tenant creditworthiness, work-from-home optionality — simply did not apply in the same way.

VI. The Build-Out Years: Creating an Irreplaceable Footprint (2010-2016)

Picture a map of the eastern United States with pins marking America's most sensitive military and intelligence installations. Fort Meade in Maryland, home to the NSA and Cyber Command. Redstone Arsenal in Alabama, the Army's missile and space nerve center. Fort Belvoir in Virginia, home to intelligence agencies and defense logistics. Lackland Air Force Base in Texas, where NSA operates a major cryptologic center. Naval Surface Warfare Center Dahlgren in Virginia, where the Navy tests weapons systems and develops electronic warfare capabilities. Now imagine a single real estate company methodically planting its flag next to each of these pins, acquiring land, building facilities, and establishing the kind of institutional presence that would be nearly impossible to dislodge.

That is precisely what COPT did during the build-out years. With the financial crisis receding and the defense thesis now validated in the market's eyes, the company entered its most ambitious expansion phase. It was not merely growing — it was systematically building what management believed would be an irreplaceable footprint across America's most important defense and intelligence installations.

In April 2011, under CEO Roger Waesche, COPT launched a Strategic Reallocation Plan that made the transformation explicit. The company announced it would sell $512 million in non-strategic suburban office properties and concentrate the portfolio entirely on defense and intelligence locations. Waesche, who had joined the company's predecessor entity in December 1984 and had been instrumental in taking it public, was a lifer who understood both the company's roots and its future. He had served as CFO from 1999 to 2006, then COO from 2006 to 2011, before ascending to CEO. A Loyola University-trained accountant who started his career at Coopers & Lybrand, Waesche brought financial discipline to the strategic vision — selling assets at good prices and reinvesting in the defense niche with precision.

By the end of 2012, COPT had completed $394 million in operating property dispositions with another $50 million in land sales planned. In October 2012, the company raised approximately $205 million in an equity offering to fund its development pipeline. Over 1.2 million square feet of development leasing was completed that year alone. The message was clear: this was not a diversified office REIT that happened to have some government tenants. This was a defense real estate company that was systematically shedding everything else.

The geographic expansion beyond Fort Meade was deliberate and strategic. The company targeted locations adjacent to the nation's most important defense installations, applying the same playbook that had worked at the National Business Park.

Redstone Arsenal in Huntsville, Alabama was the most significant new market. COPT formed a joint venture with Jim Wilson & Associates to develop Redstone Gateway, a 468-acre campus adjacent to the Arsenal. The land was U.S. Government-owned, leased to the joint venture under the Army's Enhanced Use Lease program. The master lease was negotiated with the U.S. Army in 2009, followed by a tax increment financing deal with the City of Huntsville in 2010. The planned build-out would eventually encompass over 4.4 million square feet of Class A office space across three phases, plus hotels, retail, and educational facilities. By 2025, Redstone Gateway had grown to 2.6 million square feet across 23 properties, running at an occupancy rate between 97% and 98.4%. The BRAC round of 2005 had directed 4,700 additional military and civilian workers to Redstone Arsenal, creating exactly the kind of demand surge that COPT's model was built to capture.

Other expansion sites followed the same logic — each one adjacent to a specific installation, each one serving a specific cluster of defense and intelligence missions.

Patriot Ridge in Springfield, Virginia, covered 15 acres near Fort Belvoir, serving the growing intelligence community presence that BRAC had created. Northern Virginia properties in Chantilly, Herndon, and Tysons Corner served what insiders call the "intelligence community corridor" — the stretch of Northern Virginia where the CIA, NRO, and their vast contractor ecosystems are concentrated. Facilities near the Naval Surface Warfare Center Dahlgren Division in Virginia served Navy research and development operations, including electronic warfare and missile defense testing. A campus in San Antonio, Texas, totaling approximately one million square feet, sat near Lackland Air Force Base, home to NSA Texas and Air Force Cyber Command elements.

Each site replicated the same playbook: identify an installation with growing personnel and contractor needs, acquire the best available adjacent land, develop facilities to government specifications, and establish the kind of landlord presence that becomes the default option for every new space requirement in the area.

The tenant roster read like a roster of America's defense establishment: NSA, DIA, Northrop Grumman, Lockheed Martin, Booz Allen Hamilton, SAIC, Leidos, and Computer Sciences Corporation. What made this ecosystem particularly powerful was the co-location dynamic. Government agencies need their contractors nearby — ideally within a few minutes' drive. Contractors need to be near the agencies they serve. This creates a gravitational pull that concentrates demand in the handful of locations with the right proximity, the right security infrastructure, and the right landlord relationships. Once you establish a critical mass of tenants in one of these locations, the ecosystem becomes self-reinforcing. New contractors locate there because the agencies are there. Agencies expand there because the contractor support infrastructure exists. Each new tenant makes the location more valuable for every other tenant.

The development playbook was deliberately conservative. COPT focused on build-to-suit projects that were pre-leased with long-term commitments before construction even began. This was not speculative development — the tenant was committed, the lease was signed, and the risk was construction execution rather than lease-up. Stabilized yields were predictable. The company also engaged in strategic land banking — acquiring parcels near key installations before competitors recognized their value. In real estate, you can replicate a building, but you cannot replicate a location. Owning the land adjacent to Fort Meade or Redstone Arsenal is a cornered resource that no competitor can create from nothing.

The data center adjacency was the next logical extension. The intelligence community's insatiable demand for computing power — processing satellite imagery, decrypting communications, running machine learning models on vast surveillance datasets — required massive data center infrastructure. Think of a data center shell as the building equivalent of an empty hard drive enclosure: COPT constructs the physical structure — the walls, the power infrastructure, the cooling systems, the security perimeter — and the tenant fills it with servers, networking equipment, and the classified computing systems that power modern intelligence operations. COPT began developing these data center shells as purpose-built structures designed to house exactly this kind of infrastructure. By 2025, 31 single-tenant data center shells totaling 5.9 million square feet had become a significant part of the portfolio. This positioned the company at the intersection of two powerful trends: the growth of intelligence spending and the explosion of data center demand.

For anyone asking why a well-capitalized competitor — an Amazon, a Blackstone, a Prologis — could not simply enter this market and replicate COPT's position, the answer involved multiple interlocking barriers. You needed the land, which was finite and largely controlled by COPT. You needed the construction expertise for SCIFs and secure facilities, which required years of specialized knowledge. You needed the relationships with government procurement officers and agency facility managers, which required a track record built over decades. You needed security clearances for your personnel. And you needed the patience to navigate government leasing timelines that would drive most commercial developers to madness. These barriers were not just high — they were the kind that compound over time, getting higher with each year of experience and each successful project.

VII. Sequestration, Budget Cuts, and Defense Spending Volatility (2013-2017)

The bull case for COPT Defense Properties always had an asterisk, and in 2013, that asterisk materialized. The Budget Control Act of 2011 had imposed automatic spending cuts — known as sequestration — that took effect in March 2013 when Congress failed to reach a deficit reduction agreement. Defense spending outlays fell from $670 billion in fiscal year 2012 to approximately $628 billion in 2013, a decline of $43 billion or 6.4%. They fell further to $593 billion in fiscal 2014, another $34 billion reduction.

The market reaction was swift and predictable. COPT's stock came under pressure as investors re-examined the concentration risk that had been largely forgiven during the crisis years. The thesis that had seemed so compelling — government tenants as the ultimate safe haven — suddenly looked like it could cut both ways. If the government was the best tenant because it always paid, what happened when the government decided to pay for less space?

COPT's tenant base became, in management's words, "very unwilling to make long-term commitments to space." Decisions were deferred. Expansion plans were shelved. The company's focus on the federal government — which had been its greatest strength during the financial crisis — was "seen by some investors as a liability." It was a humbling reversal.

But the reality, as so often happens, was more nuanced than the narrative. Intelligence spending and overall defense spending are not the same thing. When Congress cuts the defense budget, it does not cut every line item equally. Aircraft carriers and fighter jets might get deferred. Troop levels might get reduced. Base maintenance budgets might get squeezed. But signals intelligence? Cybersecurity? Counterterrorism surveillance? These are capabilities that presidents and intelligence directors fight to protect regardless of the broader budget environment, because they are the capabilities that directly prevent the next 9/11.

The Bipartisan Budget Act of 2013 subsequently increased sequestration caps by $45 billion for fiscal 2014 and $18 billion for fiscal 2015. Defense accounts absorbed a modest 5.6% cut in 2013, and through creative use of the Overseas Contingency Operations budget — essentially a war spending account not subject to sequestration caps — the Pentagon "almost entirely avoided cuts in 2014."

The intelligence community was even more protected. This is a critical distinction that many generalist investors miss. The intelligence budget operates under its own appropriations structure, classified and separate from the broader defense budget. It enjoys bipartisan support that most government programs would envy — no senator, regardless of party, wants to be the one who voted to cut intelligence funding right before the next terrorist attack or cyber breach. The result is that intelligence spending is the most politically protected discretionary category in the entire federal budget, and it is COPT's core customer base.

The true test of COPT's moat came not from budget appropriations but from lease expirations and renewals. When leases came due during the sequestration era, would tenants renew or leave? The answer was overwhelmingly the former. The reasons were structural: the switching costs embedded in SCIF buildouts, the proximity requirements of intelligence work, the limited alternative locations near key installations, and the sheer bureaucratic difficulty of relocating classified operations. Tenants stayed because they had to stay. There was simply nowhere better to go.

COPT continued its portfolio transformation throughout this period, using the budget uncertainty as an opportunity to accelerate dispositions of non-defense assets. The logic was counterintuitive but sound: if the market was worried about defense concentration, suburban office assets could be sold at relatively attractive prices to buyers who valued diversification. COPT would then recycle those proceeds into defense properties that it could acquire or develop at more favorable valuations because the sequestration anxiety was keeping other capital away.

By the end of 2015, the company had sold over $150 million in suburban properties, with approximately $200 million in additional buildings and non-strategic land under contract. An additional $95 million in suburban properties were headed for disposition in 2016. Every dollar of non-defense asset sold was a dollar reinvested in the core strategy. The portfolio was being purified, methodically and relentlessly, through every market environment.

The sequestration experience taught investors — and COPT's management — an important lesson about the distinction between growth risk and survival risk. Government volatility is real, but it is fundamentally different from commercial volatility. When a corporation hits financial trouble during a recession, it might go bankrupt, break its lease, and leave the landlord with an empty building and zero rent — that is survival risk for a landlord. When the government tightens its belt during sequestration, it pauses expansion plans but continues to pay rent on every existing lease — that is growth risk, a categorically different and far less dangerous proposition.

Consider the analogy of a utility company during a mild recession. Customers might use slightly less electricity, but they do not disconnect entirely. Revenue growth slows, but revenue itself remains stable. COPT's defense tenants behaved the same way during sequestration: they delayed new commitments but honored every existing obligation. Once the market internalized this distinction between growth risk and survival risk, the thesis re-established itself.

The period also revealed the importance of investor temperament. COPT's strategy required shareholders who understood that defense budget cycles would create periods of anxiety and underperformance. The company was not — and could never be — a growth REIT that delivered steady, linear earnings increases every quarter. It was a business tied to geopolitical realities and Congressional appropriations, and those forces move in cycles. The investors who recognized this and held through the sequestration era were rewarded when defense spending began climbing again in the later part of the decade.

VIII. The Rebrand and Full Commitment: Becoming COPT Defense Properties (2020-2023)

In 2020, the COVID-19 pandemic delivered a verdict on office real estate that made the financial crisis look like a practice round. Across the country, corporate tenants sent employees home, discovered that remote work actually functioned, and began questioning whether they needed all that expensive office space. Vacancy rates climbed. Lease negotiations turned adversarial. Sublease space flooded the market. The commercial office sector entered what some analysts would call a structural decline.

COPT's experience during COVID was almost comically different. Government agencies kept operating. Defense contractors kept building weapons systems and analyzing intelligence. NSA analysts kept intercepting signals. Cyber Command kept defending networks. Classified work cannot be done remotely — not because of corporate policy or managerial preference, but because of physics and law. You cannot access a Top Secret/SCI network from your home Wi-Fi. You cannot process satellite imagery on a laptop at Starbucks. The work requires being physically present in a SCIF, inside a secure facility, within proximity of the installation being supported.

The result: COPT experienced essentially zero rent collection issues during the pandemic. While the rest of the office REIT world was granting rent deferrals, renegotiating leases, and watching tenants disappear, COPT's tenants showed up to work every day and paid every dollar of rent owed. Think about that contrast for a moment. In downtown Manhattan, office buildings stood empty for months. In San Francisco, technology companies abandoned entire floors. In Chicago and Los Angeles, landlords were desperately offering free rent periods just to keep tenants from breaking leases. And in Annapolis Junction, Maryland, the parking lots at the National Business Park were full. The SCIFs were staffed. The intelligence mission continued. The rent checks cleared.

The contrast was impossible for the market to ignore.

This validation accelerated a decision that had been building for years.

On September 5, 2023, the company made what might seem like a small administrative change but was actually one of the most symbolically important announcements in its history: it was changing its name from Corporate Office Properties Trust to COPT Defense Properties. Ten days later, on September 15, the NYSE ticker changed from "OFC" to "CDP." The evolution in portfolio composition told the story clearly: defense and intelligence tenants represented 87% of core portfolio annualized rental revenue in 2020, 88% in 2021, 91% in 2022, and 90.3% by 2025.

The rebrand was more than cosmetic. It was a declaration. The company was telling the investment community, in the clearest possible terms: we are not an office REIT. Stop benchmarking us against Boston Properties and Vornado and SL Green. We are a defense infrastructure company that happens to be structured as a REIT. Our tenants are the NSA, not law firms. Our competitive dynamics are driven by geopolitics, not WeWork. Our occupancy rates are determined by intelligence budgets, not corporate headcount decisions.

The remaining non-defense assets were steadily sold off. The company sold DC-6, its wholesale data center asset, for $222.5 million in January 2022. Suburban office properties that had been the company's bread and butter two decades earlier were disposed of without sentiment. By the time the rebrand was official, COPT Defense Properties was one of the purest-play investment vehicles in the public markets — a company with a single, clearly defined mission serving a single, clearly defined customer base.

Stephen Budorick, who had become CEO in May 2016, was the right leader for this phase. A 33-year industry veteran, Budorick had joined COPT as EVP and COO in September 2011 after stints at Callahan Capital Partners, Trizec Properties, and LaSalle Partners. With a BS in Industrial Engineering from the University of Illinois and an MBA from the University of Chicago, he brought both operational rigor and strategic clarity. His tenure had been marked by disciplined execution of the portfolio transformation that his predecessors — Hamlin, Griffin, and Waesche — had initiated. The 30-year journey from generic suburban office REIT to pure-play defense real estate company was, under Budorick's stewardship, now complete.

The name change also served a practical capital markets purpose. Institutional investors increasingly use screens and filters to identify investments by sector and theme. A company called "Corporate Office Properties Trust" trading under "OFC" would inevitably get lumped in with the broader office REIT sector — a sector that was, by 2023, among the most despised in all of real estate investing. By rebranding as COPT Defense Properties under the ticker CDP, the company was essentially asking to be re-categorized. "Do not compare us to Boston Properties," the rebrand declared. "Compare us to defense contractors. Compare us to essential infrastructure. Compare us to anything except the office sector that is being destroyed by remote work."

The timing was deliberate. By September 2023, the work-from-home revolution had thoroughly decimated the office REIT sector. Major office landlords were defaulting on loans, handing back keys to lenders, and watching their stock prices crater to fractions of their pre-pandemic values. San Francisco office vacancy hit 30%. New York's largest office REIT traded at a fraction of book value. And through all of this, COPT's occupancy rate hovered above 94%, its tenants showed up to work every day, and its FFO per share kept growing. The contrast was so stark that it demanded a naming convention that made the distinction explicit.

For investors, the rebrand crystallized both the opportunity and the risk. The opportunity was a company with an irreplaceable portfolio, extraordinary tenant stickiness, recession-proof revenue, and increasing barriers to entry. The risk was that all of these qualities depended on a single factor: the sustained commitment of the United States government to intelligence and defense spending. That commitment had been robust for two decades. The question was whether it would remain so.

IX. Modern Era: Geopolitics, Cyber Warfare, and the China Factor (2021-Present)

The geopolitical environment of the mid-2020s has been, from COPT Defense Properties' perspective, almost tailor-made to sustain demand for its product. Great power competition with China and Russia has replaced the War on Terror as the organizing principle of American national security policy, but the infrastructure requirements are, if anything, more intensive.

Consider the sheer volume of threat vectors that the U.S. intelligence community now confronts simultaneously. Russia's invasion of Ukraine in February 2022 triggered the largest European land war since World War II and refocused American intelligence capabilities on state-on-state conflict — tracking Russian force movements, intercepting military communications, supporting Ukrainian battlefield intelligence. Taiwan tensions have placed the Indo-Pacific at the center of strategic planning, with the intelligence community monitoring Chinese military buildup, naval activity, and cyberspace operations around the clock. Cyberattacks against American critical infrastructure — from the SolarWinds breach to the Colonial Pipeline ransomware attack to the more recent Salt Typhoon campaign targeting U.S. telecommunications — have elevated cybersecurity to a first-tier national security priority requiring both offensive and defensive capabilities. The rise of artificial intelligence has created entirely new categories of intelligence collection and analysis, requiring facilities designed for high-performance computing. And space has been formally recognized as a warfighting domain with the creation of Space Force in 2019.

Each of these developments translates into demand for the kind of secure, specialized facilities that COPT builds and operates. And critically, these are not alternative priorities competing for limited funding — they are additive requirements, each generating its own infrastructure needs.

The numbers bear this out. The "One Big Beautiful Bill Act" passed in the current session includes $150 billion in additional defense spending over four years, with $113 billion allocated for 2026 alone. Total 2026 defense spending is projected at nearly $950 billion, representing a 13% year-over-year increase — the largest nominal increase in 25 years. Intelligence spending is projected at $116 billion, a 14% increase. Cybersecurity spending will exceed $16 billion, also a 14% increase. The Golden Dome missile defense shield program has $25 billion appropriated for 2026, with a total projected cost of $175 billion.

Perhaps the most significant recent development for COPT came on September 2, 2025, when the Trump Administration announced that U.S. Space Command would relocate its headquarters from Colorado Springs to Redstone Arsenal in Huntsville, Alabama — precisely where COPT operates its Redstone Gateway campus. This was a catalytic event. The relocation will bring approximately 1,400 Space Command jobs to the area over five years, and the expected contractor tail runs at a 2:1 ratio, meaning each military or civilian position generates demand for roughly two contractor positions nearby. COPT is already the dominant landlord at Redstone Gateway, with 2.6 million square feet of space running at near-full occupancy. The Space Command relocation represents a demand shock that plays directly into the company's strongest position.

COPT has also expanded into the data center shell business with conviction, extending the defense playbook into a new but adjacent asset class.

In late September 2024, the company acquired a 365-acre land parcel near Des Moines, Iowa, for $32 million. The site can accommodate approximately 3.3 million square feet of development supported by an estimated one gigawatt of power capacity, and it is being built out for an existing Fortune 100 cloud computing tenant. Des Moines is the fifth-largest hyperscale data center market in the United States. This represents a natural extension of the defense playbook: acquire strategic land, build purpose-designed infrastructure for mission-critical tenants, and lock in long-term lease commitments.

The portfolio today tells the story of decades of patient accumulation. As of December 31, 2025, COPT owns 207 properties totaling 25.1 million square feet. The defense/IT portfolio alone comprises 201 properties — including 24 through joint ventures — totaling 23.2 million square feet at 95.5% occupancy and 96.5% leased. Within that portfolio sits 167 office properties at 16.7 million square feet, 31 single-tenant data center shells at 5.9 million square feet, and six regional office properties at roughly two million square feet.

The tenant roster reflects the full breadth of America's national security establishment. The U.S. Government directly accounts for 35.4% of annualized rental revenue. The top ten tenants collectively represent 64.4%. Missions supported span signals intelligence, human intelligence, missile defense, space activities, law enforcement, and cybersecurity. Lease terms for new development and investment deals average 14.5 years. Vacancy leasing averages 6.9 years. Tenant retention runs at approximately 80%, with secure full-building government leases — roughly 1.5 million square feet — showing near-100% expected retention.

The tenant mix reveals the full scope of what COPT serves. The missions supported inside these buildings span the entire breadth of the intelligence and defense establishment: signals intelligence — the interception and analysis of electronic communications; human intelligence — the recruitment and management of human sources; missile defense — the systems that detect and intercept incoming threats; space activities — the satellites and ground stations that provide global surveillance; law enforcement — the agencies that investigate terrorism and transnational crime; and cybersecurity — the teams that defend American networks and attack adversary systems. Each of these missions is growing. Each requires physical space. And each is tied to appropriations that enjoy bipartisan political support.

The supply constraint that protects this business has only tightened over time. Land near key defense installations is finite, controlled, and increasingly difficult to entitle. You cannot zone new land into existence next to Fort Meade. You cannot get a building permit for a SCIF-ready facility without navigating a web of security requirements, environmental reviews, and military coordination that would deter all but the most committed developers. Security requirements for new development have become more stringent, not less, as threats have evolved. The track record requirements for winning government business effectively exclude new entrants — the government wants to work with landlords who have demonstrated, over years of successful projects, that they can deliver and maintain the kind of facilities that classified operations demand. COPT has spent over three decades building relationships, expertise, and physical infrastructure that cannot be replicated by throwing money at the problem.

X. The Business Model Deep Dive

Understanding how COPT Defense Properties actually makes money requires understanding how government leasing works, because it operates on different principles than commercial real estate.

When a corporation leases office space, the commitment depends on the company's creditworthiness, business outlook, and willingness to honor a contract. When the U.S. government leases office space, the commitment depends on Congressional appropriations — the annual process by which Congress allocates federal spending. Government leases are typically funded through multi-year appropriations or continuing resolutions, and they carry the full faith and credit of the United States. This is, quite literally, the safest credit in the world.

The leasing process works through the General Services Administration, which serves as the government's real estate broker. Agencies identify space requirements, GSA solicits proposals from landlords, and leases are structured according to standardized schedules with built-in rent escalators. The process is slower and more bureaucratic than commercial leasing, but the resulting commitments are harder than granite. Government leases typically run 10 to 15 years for new developments, with renewal options that tenants almost invariably exercise because the alternative — relocating classified operations — is prohibitively expensive and operationally disruptive.

COPT's revenue visibility is exceptional by REIT standards. The combination of long lease terms, high renewal rates, and built-in escalators creates a revenue stream that is both predictable and growing. Development leases average 14.5 years — nearly three times the length of a typical commercial office lease. Even renewing leases average 6.1 years. The company targets tenant retention of 80% and has been consistently achieving that threshold or better. For context, the typical U.S. office REIT in the post-COVID era would be thrilled with 70% retention. COPT's 80%+ retention rate, achieved in a market where its tenants literally cannot replicate their workspace elsewhere, reflects the structural stickiness that makes this business fundamentally different from its peers.

The development economics are deliberately conservative. COPT focuses on build-to-suit projects where the tenant is committed before construction begins. This eliminates lease-up risk — the risk that a completed building sits empty while the developer searches for tenants. The company commits capital to a project only after securing a long-term lease commitment, builds to the tenant's specifications including any SCIF or security requirements, and delivers a stabilized asset with a known yield. The yields on these developments have historically been attractive relative to the risk, because the specialized nature of the work limits competition and the long lease terms provide excellent risk-adjusted returns.

Capital allocation follows the REIT playbook with a defense twist.

Because REITs must distribute at least 90% of taxable income as dividends, they cannot fund growth primarily through retained earnings the way a technology company or manufacturer can. Growth capital must come from the thin slice of retained cash flow above the dividend, from new debt, or from issuing new equity to shareholders. COPT's current quarterly dividend is $0.32 per share, annualized at $1.28, representing a yield of approximately 3.9%. The most recent increase — 4.9%, announced in February 2026 — reflects confidence in the earnings trajectory. The development pipeline as of early 2026 included six properties totaling 882,000 square feet, 86% pre-leased, representing $448 million in total estimated investment. That 86% pre-lease rate bears emphasis — in the commercial office world, a developer might break ground with 30% or 40% of a building pre-leased and hope to fill the rest during construction. COPT breaks ground with near-certainty about who will occupy the building and for how long. The company targets $250 million in new investment commitments annually.

Financially, the company delivered revenue of $763.9 million in 2025, with FFO per share of $2.72 — a 5.8% increase over the prior year. For those unfamiliar with REIT accounting, Funds From Operations, or FFO, is the standard profitability metric for REITs. Unlike earnings per share, which includes non-cash depreciation charges that distort real estate economics, FFO adds back depreciation to give a cleaner picture of how much cash the business generates. Think of it as the REIT equivalent of free cash flow. COPT's FFO per share has grown in each of the past seven consecutive years, representing a 5.0% compound annual growth rate since 2019. That is not spectacular by technology standards, but for a REIT in a sector — office — that has been broadly shrinking, it is a remarkable achievement.

Same-property cash net operating income grew 4.1% in 2025, demonstrating that the existing portfolio is generating more rent over time, not just growing through new development. The 2026 guidance projects FFO per share of $2.71 to $2.79, with a midpoint of $2.75, implying modest growth as the company digests a significant development pipeline.

The balance sheet reflects the capital-intensive nature of the business. Total debt stands at approximately $2.8 billion, with 95% at fixed rates — a prudent structure given the interest rate volatility of recent years. The debt-to-equity ratio runs approximately 1.6 to 1.9 times, which is within the normal range for a development-oriented REIT but worth monitoring. Interest coverage of approximately 2.8 times provides a reasonable cushion, though it leaves less room for error than some investors might prefer.

Recent capital markets activity has been proactive. The company issued $400 million of 4.50% Senior Notes due 2030 to refinance 2.25% notes maturing in March 2026 — a significant increase in borrowing cost that reflects the new interest rate reality but was executed smoothly. The revolving credit facility was upsized from $600 million to $800 million while the borrowing spread was reduced by 20 basis points, a sign of lender confidence. A new $200 million revolving development credit facility provides additional flexibility for the pipeline.

One underappreciated aspect of the financial model is the development yield spread. When COPT builds a new property on a pre-leased basis, the stabilized yield — the net operating income divided by the total development cost — typically exceeds the capitalization rate at which the completed property would trade in the private market. In plain language: the property is worth more than it cost to build. This value creation through development is a meaningful driver of shareholder returns, and it is available to COPT precisely because of the specialized nature of the work. A developer without SCIF expertise, government relationships, and strategic land cannot replicate these economics, so the yield spread is protected by the same barriers that protect the broader business.

The trade-off inherent in this business model is important for investors to understand. COPT offers stability and predictability that few REITs can match. Government tenants do not default. Intelligence spending is insulated from economic cycles. SCIF-driven switching costs create near-permanent occupancy. But this stability comes at the cost of explosive upside. COPT will never deliver the kind of growth that a fast-expanding data center REIT or industrial logistics platform might deliver. The ceiling on growth is set by defense appropriations and the pace of new facility development, both of which move incrementally rather than exponentially. Investors are buying a compounding machine, not a rocket ship. The question is whether that compounding — 5% FFO per share growth, a nearly 4% dividend yield, and modest multiple expansion as the market increasingly appreciates the moat — adds up to a satisfying long-term return. For investors with the right time horizon and temperament, the answer has historically been yes.

XI. Competitive Analysis: Porter's Five Forces and Hamilton's Seven Powers

To understand COPT Defense Properties' competitive position with rigor, it helps to apply two of the most powerful frameworks in business strategy: Michael Porter's Five Forces, which analyzes industry structure, and Hamilton Helmer's Seven Powers, which identifies sources of durable competitive advantage.

What emerges is a picture of a company with genuine, durable advantages — but also meaningful constraints that investors should not ignore.

Starting with Porter's Five Forces — the foundational framework for analyzing industry competitive dynamics — the picture is striking.

The threat of new entrants is genuinely low. Entering the defense real estate market requires security clearances for personnel, specialized construction expertise for SCIFs and hardened facilities, relationships with government procurement officers that take years to build, and — most critically — land near key installations that is finite and largely spoken for. A new entrant would need to acquire strategic parcels, develop construction capabilities, earn government trust, and wait years for lease opportunities, all while competing against an incumbent with three decades of track record. This is not a market where venture capital or private equity can simply write a large check and buy market share.

The bargaining power of suppliers is moderate. Construction costs are a meaningful input, and the specialized contractors capable of SCIF work are a limited pool. Land near key installations is by definition a constrained resource. But COPT's scale and long-standing relationships with contractors mitigate supplier power to some degree.

Buyer power — the government's negotiating leverage — is medium to high. The federal government is the most sophisticated procurement entity in the world. It has budget constraints, appropriations cycles, and a sprawling bureaucracy of contracting officers trained to extract value. However, the government's bargaining power is significantly offset by enormous switching costs. When you have invested millions in SCIF construction and years in accreditation, and when there are limited alternative locations near the installation you need to serve, your theoretical negotiating leverage is heavily constrained by practical reality.

The threat of substitutes is remarkably low. Classified work cannot be done from a coworking space, a home office, or a standard commercial building. There is no Zoom call substitute for an in-person briefing with Top Secret/SCI materials spread across a conference table inside a SCIF. There is no cloud computing workaround for the requirement to process classified data inside physically shielded facilities. The government can build its own facilities, but it has increasingly preferred leasing because it is faster — private development typically delivers a building in 18 to 24 months versus five to ten years for government construction — and shifts both construction risk and maintenance responsibility to the private sector. This trend toward leasing rather than building has been consistent across administrations of both parties, and it shows no signs of reversing.

No technology substitute exists for physical secure space. This is perhaps the most important sentence in this entire analysis. Every other form of office demand faces some degree of technology substitution risk — videoconferencing for meetings, collaboration software for teamwork, cloud computing for data processing. None of these substitutes work when the information is classified. Physics trumps technology: you cannot encrypt a person sitting at a desk.

Competitive rivalry is minimal. There are simply very few companies competing in this specific niche. COPT is the dominant player by a wide margin. Other real estate companies — including some private developers in the Baltimore-Washington corridor — do operate near defense installations, but none has the scale, the track record, or the strategic land position that COPT possesses. The rational industry structure — few competitors, high barriers, specialized requirements — does not lend itself to destructive price competition. This is closer to a natural oligopoly than a competitive market.

Taken together, Porter's Five Forces paint a picture of an industry structure that heavily favors the incumbent. Low entry threat, low substitute threat, low rivalry, and buyer power constrained by switching costs — this is about as favorable an industry structure as one encounters in publicly traded real estate.

Turning to Hamilton Helmer's Seven Powers framework, three powers stand out as primary sources of COPT's competitive advantage.

The first is Cornered Resource. COPT controls strategic land parcels adjacent to America's most important defense installations — parcels that cannot be created, relocated, or replicated. The National Business Park's 500 acres next to Fort Meade, the 468-acre Redstone Gateway adjacent to Redstone Arsenal, properties near Fort Belvoir, Lackland Air Force Base, and Naval Surface Warfare Center Dahlgren — these are finite, irreplaceable assets. No amount of capital can create new land next to the NSA.

The second is Switching Costs. A tenant with a SCIF in a COPT building faces extraordinary costs to relocate. The SCIF construction investment ($350 to $1,000 per square foot), the accreditation timeline (12 to 36 months), the operational disruption of moving classified systems, the personnel impact of changing work locations for cleared employees — all of these create a tenant lock-in that borders on permanent. This is reflected in the company's high retention rates and the extremely long lease terms for mission-critical facilities.

The third is Process Power. Three decades of experience building SCIF-compliant facilities, navigating government lease structures, managing security requirements, and maintaining relationships with the intelligence community have created institutional knowledge that is deeply embedded in COPT's organization. This is not the kind of expertise that can be hired away or reverse-engineered. It is the accumulated wisdom of thousands of government transactions, hundreds of SCIF buildouts, and decades of trust-building with the most security-conscious customer base in the world.

Counter-positioning is also relevant. Traditional office REITs are structured around diversification — spreading risk across multiple geographies, tenant industries, and lease types. COPT's strategy of deliberately concentrating in a single niche violates this orthodoxy so fundamentally that established office REITs would need to restructure their entire investment thesis to compete. They will not do this because their existing investor base expects diversification, their management teams are evaluated on diversified metrics, and the market would punish them for embracing concentration risk.

Scale economies are moderate — COPT benefits from spreading specialized expertise across a larger portfolio — and network effects are largely absent in this business. Branding matters in the sense that reputation with government tenants is critical, but this is really a subset of process power rather than traditional consumer branding.

There is one additional dynamic worth noting that does not fit neatly into either framework but matters enormously: the co-location flywheel. When an intelligence agency establishes operations in a COPT property, its contractors must follow. When contractors cluster around the agency, the agency's workforce has more reasons to stay. When both are present in critical mass, new agencies and new contractors are attracted to the same location. This creates a virtuous cycle that is self-reinforcing in a way that resembles a network effect, even if it does not technically qualify as one in Helmer's framework. The National Business Park is the purest expression of this dynamic — a location where the density of intelligence community tenants has reached a critical mass that makes it the default location for any new requirement in the Fort Meade area.

The overall picture is a company whose competitive advantages are deeply structural and self-reinforcing. The longer COPT operates, the more land it controls, the more relationships it builds, the more expertise it accumulates, and the harder it becomes for any competitor to challenge its position. These are advantages that compound over time, which is exactly what long-term investors want to see.

XII. Bull versus Bear Case and Investment Considerations

Every investment thesis deserves to be stress-tested, and COPT Defense Properties is no exception. For all the structural advantages described above, this is a company with genuine risks that investors must weigh honestly.

The bull case rests on a convergence of structural advantages that few public companies can match. Geopolitical tensions — great power competition with China, the ongoing conflict in Ukraine, global cyber threats, the weaponization of space — support sustained intelligence and defense spending for the foreseeable future. The 2026 defense budget approaching $950 billion, with intelligence spending at $116 billion, represents a 13% year-over-year increase that is the largest nominal increase in 25 years. These are not cyclical fluctuations; they reflect a fundamental reorientation of American national security priorities that transcends political parties. Both Democrats and Republicans have demonstrated consistent support for intelligence spending, making this one of the most reliably funded corners of the federal budget.

The portfolio itself is irreplaceable. The cornered resource advantage — owning strategic land adjacent to installations that the U.S. government has operated for decades and will continue to operate for decades more — cannot be competed away. New competitors cannot create Fort Meade, cannot move the NSA, and cannot manufacture proximity. The switching costs embedded in SCIF construction and accreditation create tenant retention rates that most landlords can only dream of. The recession-resistant revenue stream — demonstrated during both the 2008 financial crisis and the 2020 pandemic — provides a stability premium in an asset class that has historically been cyclical.

The Space Command relocation to Redstone Arsenal, the expansion of Cyber Command, the growth of AI-driven intelligence analysis, and the increasing data center requirements of the intelligence community all represent organic growth catalysts that build on COPT's existing advantages rather than requiring the company to enter new, unfamiliar markets.

The barriers to entry have only increased over time. Security requirements have become more stringent. The government's preference for working with established, trusted landlords has intensified. And COPT's track record has lengthened to the point where it is essentially impossible for a new entrant to compete on experience.

The bear case deserves equally serious consideration, and honest investors should not dismiss it.