Cardinal Infrastructure Group: The "Picks and Shovels" of the AI Boom

I. The Hook

Picture a red-clay job site on the outskirts of Raleigh in the brutal humidity of a Carolina July. Before a single server rack is bolted down inside a $10 billion data center, before the fiber is pulled and the chips arrive on flatbeds, somebody has to move the earth. Somebody has to cut the pad flat to within a fraction of an inch, bury miles of water and sewer pipe, channel the stormwater so the campus does not flood, and pave the roads that the cranes will roll in on. That somebody, increasingly, has been a company most investors had never heard of until a few months ago: Cardinal Infrastructure Group.

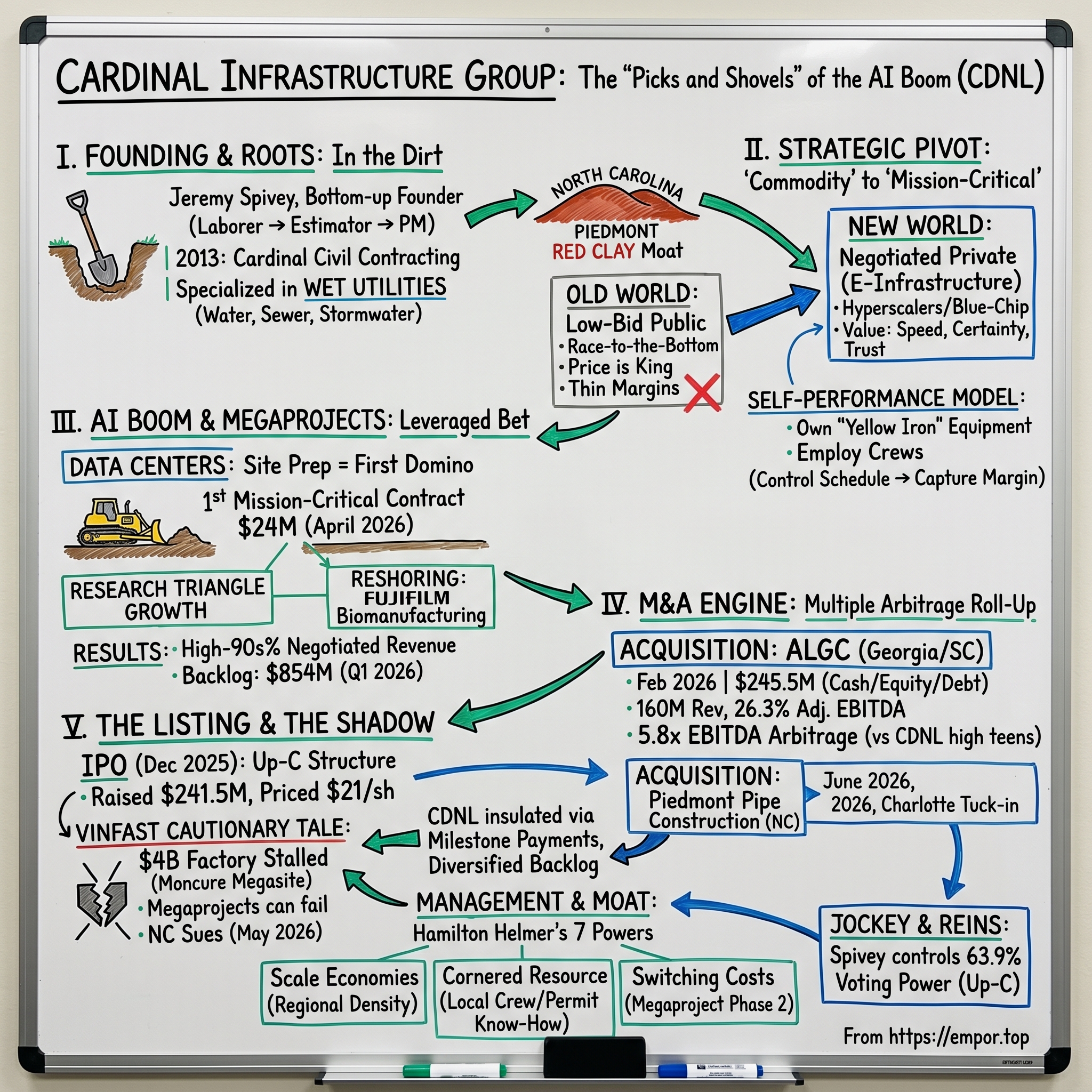

Here is the improbable part. Cardinal was founded in 2013 as a small utility crew digging trenches in North Carolina.1 It did the unglamorous, back-breaking "wet utility" work — water, sewer, stormwater — that nobody writes magazine profiles about. Twelve years later, in December 2025, it walked onto the Nasdaq Global Select Market, priced its IPO at $21 a share, and raised roughly $241.5 million in gross proceeds.2 Within the first quarter of 2026 it was reporting revenue up 105% year over year and a backlog of work at an all-time high.3 A trench-digging contractor had become a public-market growth story.

The thesis we want to test in this episode is a deceptively simple one. Cardinal is not, in the way that matters, a construction company. It is a platform sitting underneath the two largest capital-spending waves of the decade — the buildout of the physical layer of artificial intelligence, and the reshoring of advanced American manufacturing. When Wall Street talks about the AI trade, it talks about 엔비디아 NVIDIA and the hyperscalers. But every one of those gleaming data centers begins as a hole in the ground, and the company that digs the hole, lays the pipe, and certifies the dirt captures a small but very real slice of every dollar spent. Cardinal has positioned itself to be that company across the fastest-growing corridor in the country.

This is a story about a founder who started on the bottom rung and never let go of control. It is about a strategic pivot — away from the race-to-the-bottom world of public low-bid contracting and toward the high-trust, high-margin world of negotiated work for blue-chip clients — that quietly rewired the entire economics of the business. It is about an acquisition spree funded by an arbitrage so clean it almost feels unfair. And it is about a cautionary tale named VinFast, a $4 billion factory that never got built, sitting in the same red clay just down the road as a permanent reminder of what happens when megaprojects go wrong.

We will travel from a single utility crew to a $2 billion-plus market debut, and we will try to answer the question every long-term investor eventually asks about a company like this: is Cardinal the next Sterling Infrastructure, or is it something the market has not yet learned to price? Let us start where every good infrastructure story starts — in the dirt.

II. Founding & The Spivey Roots

The most important thing to understand about Jeremy Spivey is that he did not arrive at civil construction through a business school case study or a private-equity spreadsheet. He arrived through a shovel.

Spivey is what you might call a "bottom-up" founder — the kind who learned the business by physically performing nearly every job in it before he ever owned one. He started out on a utility crew, the crews that show up at dawn in steel-toed boots to dig and lay the pipe that carries a city's water and waste. From there he worked his way upward through the unglamorous ladder of civil construction: laborer, then estimator — the person who has to price a job accurately enough to win it but high enough to survive it — and then project manager, the role where you learn that schedules and weather and soil conditions will humble even the best plan on paper. By the time he founded Cardinal Civil Contracting in 2013, Spivey had stood in essentially every position on a job site.1

That biography matters because it explains the company's DNA. A founder who has personally priced jobs knows, in his bones, where money leaks out of a construction business — and it leaks, almost always, at the seams between subcontractors. Every time a general contractor hands a piece of scope to an outside crew, it gives away margin and gives up control of the schedule. Spivey's instinct, formed by years of watching that happen, was to keep the work in-house. That single conviction would later become the company's defining strategic advantage, but in 2013 it was simply how a guy who knew the trade preferred to operate.

Cardinal's early niche was the hard stuff: wet utilities. Water lines, sanitary sewer, storm drainage — the underground systems that are invisible when they work and catastrophic when they fail. There is a reason this became a moat rather than a commodity. North Carolina's Piedmont region sits on a notoriously stubborn red clay, dense and unforgiving, that turns to slick paste when wet and concrete when dry. Trenching it, shoring it, and getting pipe laid at precise grade in those conditions is genuinely difficult, and the margin for error underground is small — a mistake is buried, literally, and expensive to fix. By specializing in the work most contractors found miserable, Cardinal built a reservoir of hard-won expertise. Doing the difficult thing well, in a specific place, is one of the oldest and most durable forms of competitive advantage there is.

And the timing of where Spivey planted the flag could hardly have been better. Cardinal was born into the post-recession Raleigh boom, just as the North Carolina Research Triangle — the corridor anchored by Raleigh, Durham, and Chapel Hill, with its universities, its talent, and its comparatively cheap land — was tipping from a quiet academic region into one of the fastest-growing metros in the United States. Every new subdivision, office park, and campus needed exactly what Cardinal sold: somebody to put in the underground utilities and prepare the site. A company that does site work is, in the end, a leveraged bet on the growth of the ground it stands on. Spivey had bet on the right ground.

For its first several years, Cardinal grew the way most successful contractors grow — steadily, on reputation, one job at a time, mostly through the conventional channel of competitive public bidding. It was a good business. It was not yet a remarkable one. The leap from good to remarkable would come from a decision, made around 2021, to walk away from the very market that had built the company.

III. The Strategic Pivot: From "Low-Bid" to "Negotiated"

Every commodity business eventually arrives at the same fork in the road, and somewhere around 2021 Cardinal arrived at its own. On one path lay the world it had grown up in: public low-bid contracting, where state departments of transportation and municipalities post a project, contractors submit sealed bids, and — with brutal simplicity — the lowest number wins. On the other path lay something less crowded and far more lucrative. Spivey chose the second path, and that choice is the hinge on which the entire modern Cardinal story turns.

To appreciate why, you have to understand what the low-bid world does to a contractor's soul and balance sheet. When price is the only variable that decides who wins, every competitor is incentivized to shave their estimate to the bone, assume the best case on weather and soil, and pray. The winner is frequently just the company that made the biggest mistake in its own favor. Margins are thin, disputes are constant, and the work is, economically, a commodity — interchangeable, undifferentiated, and forever one recession away from a price war. You can be the best dirt contractor in North Carolina and still make mediocre returns if the only thing your customer cares about is your number.

Spivey's insight was that a different kind of customer had quietly entered the market — one for whom price was not the first question. When a technology giant decides to build a data center, or a pharmaceutical company a manufacturing plant, the project is measured not in the cost of the dirt work but in the revenue that the finished facility will generate the moment it switches on. For those clients, a site-work contractor who is six weeks late or who blows up a schedule is not a savings opportunity; he is a catastrophe costing millions a day in delayed capacity. What those customers want is speed and certainty, and they are willing to pay a premium for a contractor they can trust to deliver both. Price is no longer the point. Reliability is the point.

So Cardinal repositioned itself to serve precisely that customer, organizing its highest-value work under what it calls E-Infrastructure Solutions — site development for blue-chip technology and industrial clients rather than for the lowest-bid public market.4 The contracts here are typically negotiated rather than competitively bid: the client selects Cardinal based on its track record, its equipment, and its ability to self-perform, and the two sides negotiate scope and price directly. That is a completely different game. In a negotiated job, the contractor is chosen for trust, not just for thrift — and trust, unlike a low bid, is something competitors cannot simply undercut.

Underpinning the whole pivot is the model Spivey had believed in since his crew days: self-performance. Cardinal owns the "yellow iron" — the excavators, dozers, scrapers, and graders that are the working capital of earthmoving — and it employs the crews that operate them, rather than renting equipment and hiring subcontractors job to job.4 On a low-bid paving job, owning your own fleet is a nice-to-have. On a mission-critical campus where the client is paying for certainty, it is the whole ballgame. When you control the iron and the labor, you control the schedule, and when you control the schedule you can credibly promise the one thing the customer values most. You also capture the margin that competitors bleed away to their subcontractors on every line of scope — the "hidden" margin that is invisible on a bid sheet but very visible in an operating statement.

This is the part long-term investors should sit with, because it is the engine of everything that follows. A pivot from commodity low-bid work to negotiated, self-performed, mission-critical work is not a marketing repositioning; it is a change in the fundamental economics of the enterprise — higher margins, stickier customers, and pricing power where there used to be none. The question was whether there would be enough of that high-value work to fill the order book. By 2026, the answer had become emphatically clear, and it was being driven by the most voracious consumer of dirt the modern economy has ever produced.

IV. The "Hidden" Business: Data Centers & Mission-Critical Sites

In April 2026, Cardinal put out a press release that, on its face, looked modest: the company had been awarded a $24 million contract to deliver full-site civil infrastructure for the first phase of a large, multi-phase data center campus.5 Twenty-four million dollars is not, by the standards of a company guiding to nearly $700 million in annual revenue, a headline number. But the language around it told you this was a threshold moment. It was, the company noted, the first mission-critical data center contract in Cardinal's history.5 The trench-digging utility crew had just been handed a piece of the AI buildout.

To understand why that matters, you have to understand where site work sits in the life of a data center. The popular imagination of an AI data center is all servers and cooling and electricity — the expensive, high-technology guts. But none of it can begin until the ground is ready, and getting the ground ready is harder than it sounds. Cardinal's scope on a campus like this includes the full civil package: the wet utilities it cut its teeth on, mass earthwork to carve a buildable pad out of rolling terrain, erosion and sediment control to satisfy environmental regulators, the storm drainage and stormwater management that keep a multi-hundred-acre site from washing out, and the paving and surface work that lets construction traffic move.5 All of it, self-performed. Site preparation is the first domino in the buildout, and until it falls nothing else can.

Here is the analogy worth holding onto. If the AI boom is a gold rush, the hyperscalers are the prospectors and the chipmakers are selling the most expensive picks. Cardinal is selling something even more fundamental: it is leveling the ground the whole mine is built on. The "picks and shovels" framing is almost too literal in this case — Cardinal quite literally operates the shovels. And because site prep happens at the very front of the project, the company gets paid early in the cycle, before the more speculative parts of a campus are even financed.

The most telling number in the entire Cardinal story is not a revenue figure. It is the mix. By the company's account, the overwhelming majority of its revenue — in the high-90s percent — now comes from negotiated rather than competitively bid contracts, a complete inversion of where a traditional civil contractor sits.6 Sit with that. A business that a few years earlier lived and died in sealed-bid auctions had remade itself so thoroughly that almost none of its revenue was won on price alone anymore. That figure is the cleanest single proof that the pivot we just walked through actually happened in the financials and not merely in the investor deck. It is the difference between a company that talks about pricing power and one that has it.

Surrounding all of this is a regional megaproject boom that gives Cardinal an embarrassment of demand. The Research Triangle has become a magnet for exactly the kind of mission-critical construction the company is built to serve. Down in Holly Springs, the Japanese pharmaceutical and imaging conglomerate 富士フイルム FUJIFILM — through its FUJIFILM Diosynth Biotechnologies arm — has been pouring billions into one of the largest biomanufacturing facilities in North America, a project emblematic of the advanced-manufacturing wave washing over the corridor.[^7] Whether or not Cardinal holds any single contract there, facilities of that scale reset the entire local market for site work: they pull in talent, they validate the region for the next investor, and they create a pipeline of complex, schedule-critical jobs that play directly to Cardinal's strengths. The order book reflected it. By the end of the first quarter of 2026, the company's backlog had swelled to a record $854 million.3

A backlog like that does two things at once. It is a revenue forecast — more than a year of work already under contract — and it is a vote of confidence, a tangible measure of how many sophisticated customers have decided Cardinal is the crew they trust. But a growing backlog also raises a capital question: how do you staff and equip a business doubling in size without drowning in the cost of organic growth? Cardinal's answer was to go shopping — and to do it at a price that turned heads across the Southeast.

V. M&A & Capital Deployment: Benchmarking the ALGC Deal

On February 18, 2026, barely two months after its market debut, Cardinal announced the deal that would define its first year as a public company: the acquisition of A.L. Grading Contractors, a Sugar Hill, Georgia site-development firm, for total consideration of $245.5 million.7 For a company that had just raised roughly that same amount in its IPO, it was an audacious opening move — and the math behind it explains why management was willing to be audacious.

Start with what Cardinal was buying. ALGC was no bolt-on. It was a full-service site contractor — grading, underground utilities, erosion control, land clearing — serving large commercial, industrial, and residential projects across Georgia and South Carolina, with more than 300 employees.7 On an unaudited basis, ALGC had generated roughly $160 million of revenue with an adjusted EBITDA margin of about 26.3% over the trailing twelve months ended September 2025.7 That margin is the number to linger on: 26 cents of operating cash profit on every revenue dollar is a genuinely strong figure for site work, and it was actually higher than Cardinal's own corporate margin — meaning the acquisition would lift, not dilute, the combined company's profitability.

Now the arbitrage, which is where the deal goes from sensible to remarkable. ALGC's roughly $160 million of revenue at a 26.3% margin implies something on the order of $42 million of adjusted EBITDA. Pay $245.5 million for that, and you are buying the business at roughly 5.8 times EBITDA.8 Meanwhile, Cardinal's own stock, as a fast-growing public infrastructure name riding the AI narrative, traded at a far richer multiple — in the high teens on the same measure. The mechanism is almost magical: Cardinal could acquire a private competitor's earnings at single-digit multiples and have the public market immediately re-rate those same earnings at roughly three times the price. Buy at 5.8x, get valued at 18x. That is what we have called, in other episodes, multiple arbitrage — and in the fragmented, family-owned world of Southeastern site contractors, the supply of 5.8x sellers is deep.9

The structure of the deal told you how the company intends to keep playing this game. Of the $245.5 million, only $48.6 million was cash; the rest came as $116.9 million of newly issued equity — subject to a six-month lockup — and an $80 million extension of Cardinal's credit facility, with the company simultaneously upsizing its term loan to $200 million.7 Paying with stock when your stock is expensive is the disciplined way to run an arbitrage roll-up: you spend the overvalued currency, not the cash. And by handing the seller equity with a lockup, Cardinal aligned ALGC's leadership with the combined company's future rather than simply cashing them out. Lee Wood, ALGC's president, stayed on to run his business and was slated to join Cardinal's board — the human glue that keeps an acquired contractor's relationships and crews from walking out the door.7

Strategically, ALGC was Cardinal's first real expansion outside the Carolinas, planting the flag in Georgia — a state riding the same Sun Belt growth and reshoring tailwinds, and home to its own surge of data center and manufacturing investment.7 It transformed Cardinal in one stroke from a North Carolina specialist into a multi-state Southeastern platform.

And then, to show the strategy was not a one-off, Cardinal moved again. On June 2, 2026, it announced the acquisition of Piedmont Pipe Construction, a wet-utility contractor founded in 1999 and based in Denver, North Carolina, just northwest of Charlotte.10 Where ALGC was a margin-accretive expansion into a new state, Piedmont was a classic tuck-in: a deepening of the company's original wet-utility core in the fast-growing Charlotte market, folded directly under the Cardinal Civil Contracting brand.10 The terms were not disclosed, which itself signals a smaller, private-scale deal.10 Doubling down on the unglamorous pipe business — the very thing it started with — even as it chased glamorous data center work, told you Cardinal had no intention of abandoning the dense, repeatable, locally-moated work that built it. For investors, the pattern to watch is now established: use an expensive public currency to roll up cheaper private contractors, building regional density one acquisition at a time. The engine was running. The question the market kept asking was how this engine had gotten public in the first place — and why it arrived under a cloud.

VI. The Current State: The IPO and the VinFast Shadow

Cardinal's path onto the public markets was, in its own quiet way, a contrarian trade. The company had originally filed to raise as little as $100 million.11 By the time shares began trading on December 10, 2025, demand had pushed the deal far larger, and Cardinal priced at $21.00 per share for roughly $241.5 million in gross proceeds.2 Part of the early friction was a labeling problem. To a Wall Street accustomed to sorting companies into tidy boxes, "civil contractor" reads as cyclical, low-margin, and unglamorous — the kind of business that trades at a single-digit multiple and gets ignored. It took the market a beat to recognize that the thing it was looking at was less a paving company and more a mission-critical infrastructure platform levered to AI and reshoring. When the penny dropped, the re-rating followed.

The mechanics of the listing also told you something about who was really in charge. Cardinal went public through an "Up-C" structure — an umbrella-partnership C-corporation arrangement common when founder-owned operating businesses list while preserving the founders' favorable pass-through tax treatment.12 We will return to the control implications in a moment, because they are central to the investment case. For now, the relevant point is that the Up-C is a signal: this was a founder taking his company public on his own terms, not a private-equity exit dressing itself up for the public.

But no account of Cardinal's present moment is complete without the ghost that hangs over the entire region — VinFast. The Vietnamese electric-vehicle maker, controlled by the country's wealthiest businessman, Phạm Nhật Vượng, and his Vingroup conglomerate, had in March 2022 announced one of the largest economic-development deals in North Carolina history: a roughly $4 billion factory at the Moncure megasite in Chatham County, promising about 7,500 jobs in exchange for up to $1.25 billion in state and county incentives.13 It was exactly the kind of transformational megaproject that makes a site-work contractor's decade. And then it stalled. Construction benchmarks slipped, the operational deadline of mid-2026 became unreachable, and the company effectively abandoned active work on the site for more than a year.14

The matter came to a head in the spring of 2026. After formally notifying the company in January that it was in breach, North Carolina's attorney general, Jeff Jackson, filed suit on May 21, 2026, seeking to reclaim the megasite land and to claw back the full value of the public funds disbursed for site preparation.14 A $4 billion factory had become a courtroom fight over who pays for the dirt work already done. For anyone bullish on the Southeastern infrastructure boom, VinFast is the sobering counter-example: megaprojects can and do collapse, and when they do, the contractors and taxpayers tied to them can be left holding the bag.

Which raises the obvious and important question — how exposed is Cardinal to exactly this failure mode? The honest answer is that the company's structure provides meaningful, though not total, insulation. Cardinal's revenue is spread across that $854 million backlog of many separate projects and a widening roster of clients, not concentrated in any single megaproject whose cancellation would crater the business.3 Site-work contracts are typically structured around milestone payments — the contractor bills and collects as defined phases of work are completed — so the capital at risk on any one job is the cost of the next increment of work, not the value of the entire campus. A contractor who has been paid through Phase 1 and has not yet mobilized Phase 2 can absorb a cancellation far better than the developer can. The VinFast precedent is a genuine risk to the demand environment and a reminder that booked backlog is not the same as cash in the bank — but it is not, on the evidence, an existential threat to a diversified, milestone-paid contractor. The structure was deliberate. And the man who built that structure had also made very sure he would never lose control of it.

VII. Management & Ownership

If you want to understand a founder-led company, follow the votes. And at Cardinal, the votes run almost entirely through one man.

Jeremy Spivey occupies both the chairman and chief executive roles, and his fingerprints are on every strategic decision we have discussed — the pivot to negotiated work, the insistence on self-performance, the arbitrage-driven M&A.15 But the more revealing fact is structural. Through the Up-C arrangement, Cardinal's continuing equity holders hold a class of high-vote Class B shares that, together, command roughly 63.9% of the company's combined voting power — meaning control of the public company rests firmly with the pre-IPO insiders led by Spivey, even as outside shareholders own a large slice of the economics.12 On top of that, Spivey personally held beneficial ownership of more than 12.2 million Class A shares, about 45% of that class.15 In plain terms: the founder controls the company through the ballot box and is enormously exposed to it through his own net worth.

For a long-term investor, that combination cuts both ways, and it is worth being clear-eyed about both edges. The bull reading is alignment in its purest form. A founder whose personal fortune is overwhelmingly tied up in the stock — a stake worth hundreds of millions at the IPO valuation — does not need a compensation consultant to make him think like an owner; he is the owner. Every decision about how to deploy capital, how aggressively to bid, how to integrate an acquisition, is being made by someone who eats the consequences directly. That is the kind of skin in the game that tends to produce patient, long-horizon decisions rather than quarter-to-quarter financial engineering. The bear reading is the flip side of the same coin: dual-class control means public shareholders are, in the end, passengers. If Spivey makes a bad call, there is no activist, no proxy fight, no board revolt that can easily overrule him. You are betting on the jockey, and you have handed him the reins for the duration.

Alongside Spivey sits chief financial officer Mike Rowe, who has taken on the increasingly important job of translating a fast-moving, acquisition-hungry operating story into the language of institutional investors — including the road-show and conference circuit that a newly public company lives on.16 In a roll-up that runs on multiple arbitrage and a leveraged balance sheet, the CFO's discipline around the term loan, the equity issuance, and the integration math is not a back-office function; it is half the strategy.

The culture that holds it all together is best captured in a phrase that fits the company perfectly: dirt and data. On one side are the boots-on-the-ground crews, the equipment operators and pipe-layers who do genuinely hard physical work in genuinely hard conditions — the part of the company that traces straight back to Spivey's own beginnings on a utility crew. On the other side is the increasingly sophisticated estimating, scheduling, and project-management apparatus required to bid and deliver hundred-million-dollar mission-critical campuses on time. The competitive magic is in marrying the two: a workforce that can actually move the earth, run by a management layer precise enough to promise a hyperscaler a date and hit it. That marriage is harder to replicate than either half alone — which brings us to the question of just how durable Cardinal's advantages really are.

VIII. Analysis: The Powers and the Forces

Let us war-game this business properly, using the two frameworks we return to again and again — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — and let us be honest about where Cardinal's moat is real and where it is thinner than the bulls would like.

Start with scale economies, the most tangible of Cardinal's powers. Site work is a business of logistics: of getting expensive equipment and skilled crews to a job site and keeping them productively busy. A contractor with regional density — many active projects clustered in the same metro — can move a dozer from one job to the next without it sitting idle on a lowboy trailer for two days, can keep its best crews fully utilized, and can spread the fixed cost of its yard, its fleet maintenance, and its estimating department across more revenue. This is precisely why Cardinal's M&A strategy targets density rather than national sprawl: each tuck-in like Piedmont makes the equipment and labor already in the region more efficient. A national contractor with the same total revenue spread thinly across twenty states would have worse economics than Cardinal concentrated in three. In site work, regional density genuinely beats national breadth.

Next, the cornered resource — and here the resource is human and bureaucratic rather than physical. The binding constraint on the entire Southeastern construction boom is not demand; it is the scarce supply of skilled crews who can execute complex work, and the even scarcer local knowledge of how to navigate permitting, erosion-control regulations, and inspection regimes in specific jurisdictions. Knowing which county inspector wants what, how to get a stormwater permit approved without a three-month delay, where to find an operator who can cut grade in red clay — this know-how is accumulated over years and cannot be bought off a shelf. By acquiring established local contractors, Cardinal is not just buying revenue; it is buying their crews and their permitting relationships, the things a new entrant simply cannot conjure.

Then switching costs, which on a multi-phase megaproject are close to absolute. Once Cardinal has begun site work on Phase 1 of a $10 billion campus — once it holds the as-built knowledge of what is buried where, once its crews are mobilized and its schedule is woven into the developer's — firing it and bringing in a replacement for Phase 2 means re-bidding, re-mobilizing, and re-learning the site, all while the clock on a multi-million-dollar-a-day facility keeps ticking. The client's own desperate need for speed becomes the incumbent contractor's lock-in. This is the power that makes that first mission-critical contract so much more valuable than its $24 million face value suggests: it is a foot in the door of a relationship that can run for years.

Now turn the lens to Porter's Five Forces, because the framework's chief virtue is that it forces you to specify which market you are analyzing — and Cardinal lives in two very different ones. In the negotiated, mission-critical niche, competitive rivalry is comparatively low: the set of contractors a hyperscaler will trust with a schedule-critical campus is small, and the basis of competition is reliability rather than price, which protects margins. In the low-bid paving and public-works world Cardinal deliberately walked away from, rivalry is savage and undifferentiated — which is exactly why it left.

The same split governs buyer power, and this is the single most important strategic insight in the whole analysis. A state department of transportation awarding a low-bid paving contract holds enormous power over the contractor: there are many bidders, the work is a commodity, and price rules. But a technology giant that needs a data center operational "yesterday" to capture AI demand is in a structurally weaker bargaining position than its size would suggest — it needs this contractor, on this schedule, and a few weeks of delay costs it far more than any price concession it could extract. Cardinal's entire strategic migration can be read as a deliberate move from markets where the buyer holds the power to markets where, paradoxically, the giant customer holds less of it. As for the threat of new entrants and substitutes: the capital intensity of a modern equipment fleet, the scarcity of skilled crews, and the simple physical reality that there is no substitute for moving earth all keep the barriers meaningfully high — though never infinitely so, because a determined competitor with capital can, over time, buy iron and poach crews.

The honest verdict is that Cardinal's powers are real but regional and relationship-dependent rather than structural and permanent. This is not a software company with a zero-marginal-cost network effect. It is a very good operator that has assembled durable local advantages in the right places at the right time. For an investor, that distinction matters enormously: it means the moat must be continuously re-earned through execution and reinvestment, not merely defended. Which is the perfect segue into the lessons this whole story teaches.

IX. The Playbook: Business & Investing Lessons

Strip Cardinal down to its load-bearing ideas and three lessons stand out — each one a principle that travels well beyond civil construction.

The first is that vertical integration is the only reliable way to protect margin in a labor-constrained world. The instinct of most growth companies is to stay "asset-light," to outsource the messy, capital-heavy parts of the work and rent capacity as needed. Cardinal did the opposite, and in its market the opposite was right. When the binding constraint is the availability of skilled crews and the certainty of the schedule, the company that owns the iron and employs the labor controls its own destiny, while the asset-light competitor is left bidding against everyone else for the same scarce subcontractors. Owning the means of production looks expensive on the balance sheet until you realize it is the very thing the customer is paying a premium for. In a world short on hands, controlling the hands is the moat.

The second lesson is the one Spivey lived in 2021: do not be a commodity. The single most consequential decision in this entire story was the choice to walk away from a market — public low-bid work — where the company was demonstrably good but structurally unable to earn good returns, and to migrate toward work where complexity is high and the timeline is tight. The same crews, the same equipment, the same red clay, but pointed at customers who value certainty over price. The economics did not change because the work changed; they changed because the customer changed. When you find yourself competing only on price, the answer is rarely to cut price further. It is to find the customer for whom price is not the first question.

The third lesson is the quiet one that ties the M&A strategy to the operating strategy: regional density beats national breadth in physical infrastructure. It is tempting, when a strategy works, to spread it as widely and as fast as possible. Cardinal's discipline has been to deepen rather than dilute — to buy the contractor down the road that makes its existing fleet and crews more productive, rather than to plant a thin flag in a distant state for the sake of the map. In a business where the unit economics are set by how far you have to haul a dozer and how well you know the local inspector, concentration is not a limitation on growth; it is the source of the advantage. These three ideas are also, conveniently, the lens through which to weigh the bull and bear cases that close the book.

X. Epilogue & Bear vs. Bull Case

So where does this leave a long-term investor trying to size up a twelve-year-old trench-digging company that became a public-market AI proxy in the span of a single news cycle? As always, the truth lives in the tension between two coherent stories.

The bull case is that Cardinal is early in a genuine golden age of American physical infrastructure. The AI buildout shows no sign of slowing, and every dollar of data center capital expenditure begins with site work that someone has to perform. Layer on the reshoring of advanced manufacturing — semiconductors, pharmaceuticals, EV supply chains — concentrated disproportionately in exactly the Southeastern corridor Cardinal dominates, and you have a demand environment that could absorb the company's capacity for years. The strategic flywheel reinforces the story: a record $854 million backlog feeding revenue that more than doubled year over year,3 margins lifted by acquisitions bought at a fraction of the company's own multiple,8 and a founder with overwhelming skin in the game compounding it all. If the negotiated, mission-critical thesis holds, Cardinal is not a cyclical contractor at all but a structural beneficiary of the largest capital-spending wave in a generation.

The bear case is equally grounded, and it begins with the very thing that makes the bull case exciting: this is still, fundamentally, a construction company, and construction is cyclical, capital-intensive, and exposed to forces management does not control. The most acute risk is labor — the same crew scarcity that protects Cardinal's margins could, if it worsens, cap the company's ability to grow into its backlog or compress profitability through wage inflation. The second is interest rates: site work tied to commercial and residential building is sensitive to financing costs, and a higher-for-longer rate environment could chill the development pipeline beyond the data center segment. The third is the one with a name and a courthouse address — VinFast — the standing proof that even a $4 billion, heavily incentivized megaproject can evaporate, and that backlog and announced investment are promises, not cash.14 A roll-up funded partly by leverage and by an elevated stock price is also, by construction, vulnerable to a de-rating: if the market stops paying eighteen times for these earnings, the arbitrage that powers the M&A engine sputters.

For those reasons, the things actually worth watching on this company are few and specific. Track the backlog — both its size and, more importantly, its composition, because a backlog that keeps growing while staying weighted toward negotiated mission-critical work is the truest sign the thesis is intact. Track the mix of negotiated versus competitively bid revenue, the high-90s figure that is the entire proof of the company's pricing power; any meaningful drift back toward low-bid work would signal the moat eroding.6 And track the adjusted EBITDA margin, the company having guided to above 20% for 20263 — the number where the benefits of self-performance, regional density, and accretive M&A either show up or do not. Those three tell you almost everything about whether the strategy is working, without requiring you to forecast a single data center.

The inevitable closing comparison is to Sterling Infrastructure, the Texas-rooted, Nasdaq-listed civil and e-infrastructure company that pioneered much of this exact playbook — pivoting from low-bid transportation work toward high-margin data center and mission-critical site development, and earning a premium multiple for it. Cardinal is, in many respects, walking the same road a few years behind, in a different but equally fertile region, with a founder who still controls the wheel. Whether it ends up as a smaller regional echo of that story or grows into something larger will depend on the things this episode has tried to surface: the durability of the negotiated mix, the discipline of the M&A arbitrage, the supply of crews, and the staying power of the AI and reshoring waves that are, for now, filling its order book to record highs. The dirt, at least, is not going anywhere. The question is who gets paid to move it — and for the moment, in the red clay of the Carolinas and Georgia, the answer is increasingly Cardinal.

References

-

Construction services provider Cardinal Infrastructure Group files for a $100 million IPO — Renaissance Capital, 2025 ↩↩

-

Cardinal Infrastructure Group prices upsized IPO / CDNL begins trading — Renaissance Capital, 2025-12-10 ↩↩

-

Cardinal Infrastructure Group Inc. Announces First Quarter 2026 Results and Raises 2026 Outlook — PR Newswire, 2026-05-12 ↩↩↩↩↩

-

Cardinal Infrastructure Group Inc. — Form 424B4 Prospectus, U.S. SEC, 2025-12 ↩↩

-

Cardinal Infrastructure Group Awarded Contract for Large-Scale Data Center Campus Development — PR Newswire, 2026-04 ↩↩↩

-

Cardinal Infrastructure Group Inc. — Form 10-K (FY2025), U.S. SEC ↩↩

-

Cardinal Infrastructure Group (CDNL) Announces the Acquisition of A. L. Grading Contractors — PR Newswire, 2026-02-18 ↩↩↩↩↩↩

-

Cardinal Infrastructure Group Buys ALGC for $245.5 Million; Increases Term Loan to $200 Million — TradingView News (Reuters), 2026-02-18 ↩↩

-

The Southeast M&A Boom: Infrastructure Multiples Benchmarked — Reuters, 2026-02-25 ↩

-

Cardinal Infrastructure Group Announces Acquisition of Piedmont Pipe Construction — PR Newswire, 2026-06-02 ↩↩↩

-

Cardinal Infrastructure Group Inc. — Definitive Proxy Statement (DEF 14A): Up-C structure and Class B voting power, U.S. SEC ↩↩

-

North Carolina sues EV-maker VinFast over megasite project — Spectrum News, 2026-05-22 ↩

-

North Carolina Sues VinFast to Acquire Shovel-Ready Manufacturing Site — North Carolina Department of Justice, 2026-05-21 ↩↩↩

-

Spivey reports stake in Cardinal Infrastructure — Schedule 13G filing, U.S. SEC / StockTitan ↩↩

-

Cardinal Infrastructure Group Q1 Earnings Call Highlights — TradingView News (MarketBeat), 2026-05-12 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube