Coeur Mining: America's Silver Dynasty — From Idaho's Silver Valley to a Modern Precious Metals Powerhouse

I. Introduction & Episode Roadmap

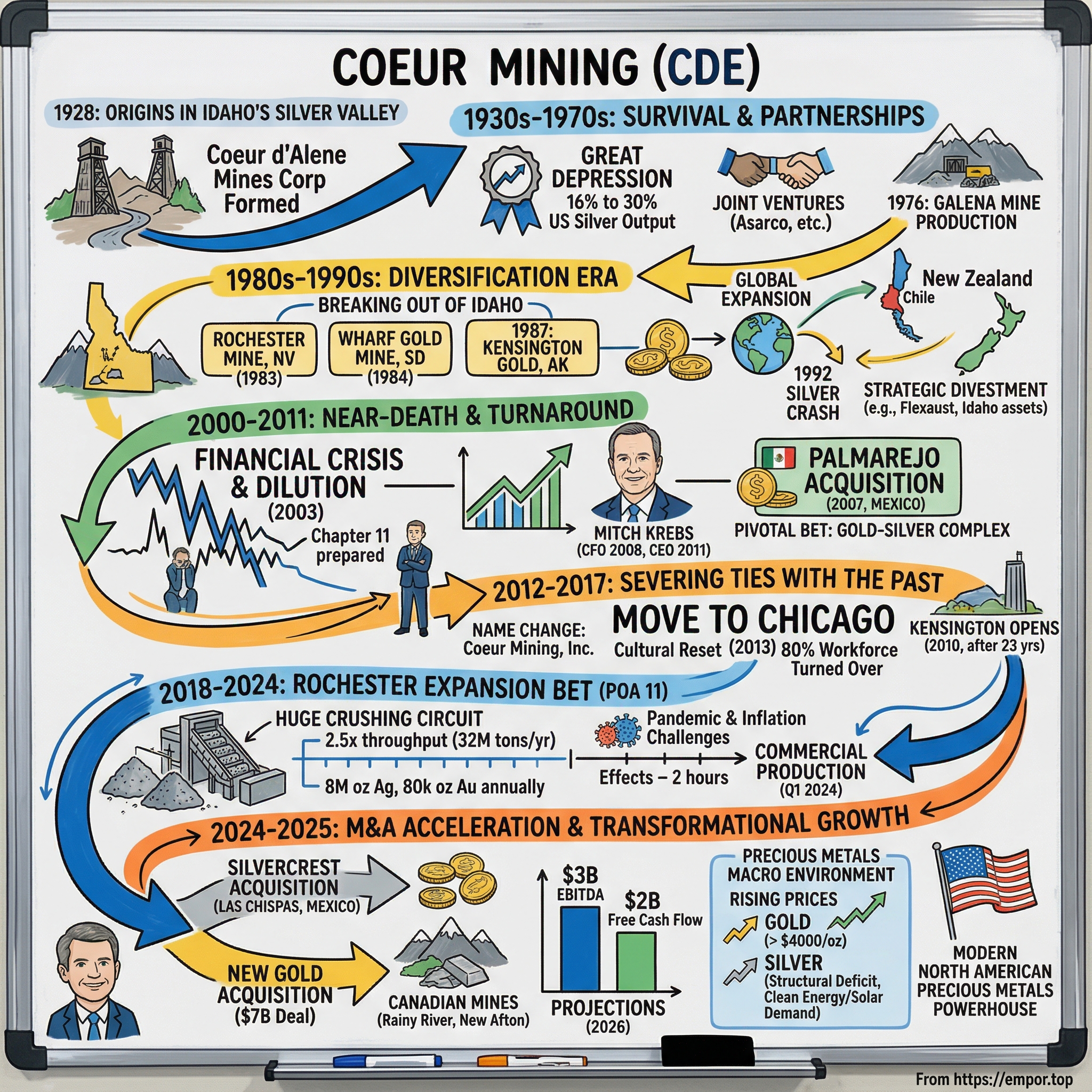

Picture the northern Idaho panhandle in 1928—a narrow valley choked with mine shafts, ore carts, and the relentless clatter of extraction. The Coeur d'Alene region had been producing silver since prospectors arrived in the 1880s, and by the late 1920s, record production levels encouraged a wave of optimism. Inspired by this climate of optimism, the Coeur d'Alene Mines Corporation was formed. Nobody involved could have imagined that this fledgling operation would survive the Great Depression, multiple near-death experiences, commodity crashes, and almost a century of industry upheaval to emerge as one of North America's most significant precious metals producers.

Today, Coeur Mining is a U.S.-based, well-diversified, growing precious metals producer with five wholly-owned operations: the Las Chispas silver-gold mine in Sonora, Mexico, the Palmarejo gold-silver complex in Chihuahua, Mexico, the Rochester silver-gold mine in Nevada, the Kensington gold mine in Alaska and the Wharf gold mine in South Dakota. In addition, the Company wholly-owns the Silvertip polymetallic exploration project in British Columbia.

The big question driving this deep dive: How did a 1928 Idaho silver miner survive nearly a century, pivot from being a pure-play silver producer to a diversified gold-silver producer, and emerge as a major North American precious metals player—now poised to become one of the world's largest miners through transformational M&A?

The answer lies in a story of survival, strategic reinvention, and an M&A playbook that has accelerated dramatically in recent years. 2025 production guidance ranges of 380,000-440,000 ounces of gold and 16.7-20.3 million ounces of silver represent expected year-over-year increases of 20% and 62%, respectively. And with the recently announced $7 billion acquisition of New Gold, Coeur is positioning itself for an even more dramatic transformation.

Just two years ago, Coeur's full-year EBITDA totaled $142 million and its free cash flow was negative $297 million. "With the addition of New Gold's two Canadian operations to our five current operating mines we expect to generate approximately $3 billion of EBITDA and approximately $2 billion of free cash flow in 2026 at significantly lower overall costs and higher margins."

This is a story about commodity cycles, capital allocation, the courage to transform, and what happens when nearly a century of institutional knowledge meets a once-in-a-generation bull market for precious metals.

II. Founding & The Idaho Silver Era (1928–1980s)

Origins in America's Silver Valley

The Coeur d'Alene district of Idaho occupies a special place in American mining history. The Coeur d'Alene district of Idaho has been an important producer of lead, silver, and zinc since the 19th century. Idaho and Utah were the great silver-lead producing states, accounting for over 40 percent of the country's total output during the period 1907-30, with most of Idaho's output coming from the Coeur d'Alene district of Shoshone County.

The valley itself carries a violent, dramatic history. Miners and prospectors came to the region after gold and silver deposits were found in the Coeur d'Alene Mountains and the Northern Pacific Railroad came to the region in 1883. In the 1890s, two significant miners' uprisings took place in the Coeur d'Alene Mining District, where the workers struggled with high risk and low pay. The labor wars of 1892 and 1899 saw dynamite, martial law, and federal troops—setting a precedent for the high-stakes, boom-bust nature of precious metals mining.

By 1903, Burke Canyon was the most developed mining region in the Coeur d'Alene Mountains and was home to seven dividend-paying mines. Other mines soon began production throughout the Coeur d'Alene mining district, including the Bunker Hill Mine (1886), Star-Morning Mine (1887), Sunshine Mine (1890), Galena Mine (1922) and Lucky Friday Mine (1942).

It was into this bustling, established mining ecosystem that Coeur d'Alene Mines Corporation was born. Coeur Mining was formed in 1928 to mine silver in the Coeur d'Alene region of Idaho. The company was an important mine operator in northern Idaho for many decades and among others operated the Coeur d'Alene Silver Mine, the Coeur Mine and the Galena Mine.

Surviving the Depression

The timing of Coeur's founding was, on paper, terrible. The Great Depression hit American industry with devastating force within a year of the company's incorporation. Yet the precious metals industry has always marched to its own drummer. Unfortunately, by the early 1930s, the overall economic depression began to be felt within the industry, forcing several mines to close. In Idaho, however, the silver production levels were sustained better than in most other states, and the company's share of production grew from 16 percent of the country's output to 30 percent in 1933. Coeur's flagship, the Coeur d'Alene Silver Mine, provided income until the 1950s when the mine was shut down due to poor metal prices.

This early resilience established a pattern that would define Coeur for nearly a century: the ability to survive when competitors failed, often by being in the right geography with the right deposits.

Key Early Milestones

The Siderite vein, the main vein of the Mineral Point mining operation was discovered by Coeur d'Alene Mines Corp in 1935.

The four companies were major shareholders in Consolidated Silver, a company formed in 1967 to consolidate several mining properties near the Silver Summit mine.

The first orebody in the modern Coeur mine operations was discovered in 1969 by Asarco, Inc. This partnership with Asarco would prove crucial—Construction of the Coeur mine–the newest mine in the 100-year-old-plus mining district–began in the 1970s, costing $20 million for the mine and mill, with commercial production beginning in 1976. The company began stockpiling ore in that year when silver sustained a yearly average of $4.63 per ounce, before rising to a high of $5.34 per ounce in 1980.

In 1979 four Idaho silver mining companies had formed a joint venture agreeing to rehabilitate and reopen Consolidated Silver Corporation's Silver Summit mine and to begin an extensive exploration program on that company's mining properties.

The lesson from Coeur's first five decades was clear: this was a company built to survive, not dominate. It operated within a complex ecosystem of joint ventures, partnerships, and shared infrastructure—the way mining had been done in the Silver Valley for a century. But this model would eventually reach its limits.

III. Diversification & Geographic Expansion (1980s–1990s)

Breaking Out of Idaho

By the 1980s, Coeur's leadership recognized that dependence on a single region—even one as prolific as the Silver Valley—represented an existential risk. The company began an aggressive diversification campaign that would fundamentally reshape its asset base.

1983: Coeur acquired Asarco's operating lease on the Rochester Mine in Nevada. Production began in 1986 and the mine continues to operate. This acquisition, for a heap-leach surface operation in the Humboldt Mountains, would prove to be one of the most consequential in company history—Rochester remains a cornerstone asset nearly four decades later.

1984: Coeur became the sole owner of the Wharf Gold Mine in South Dakota, following the merger of Wharf Ltd. and Wharf USA, Inc. 1987: Acquired a 50% interest in the Kensington Property in Alaska. The remaining 50% was purchased in 1995 and production commenced in 2010.

The Kensington acquisition deserves particular attention because of its remarkable gestation period. Coeur acquired 50% of the Kensington property in 1987 and then 100% in 1995. After considerable exploration work involving option agreements with a number of different companies and a court case that contested permits issued by the US Army Corps of Engineers, the Kensington mine was finally put into Production on July 3, 2010. Twenty-three years from first acquisition to first production—a timeline that speaks to both the complexity of mine permitting and Coeur's patient, long-term orientation.

Global Expansion

The late 1980s and 1990s saw Coeur extend its reach across the Americas and beyond:

1990: Acquired the Fachinal property in Chile from a Chilean exploration company. The underground gold-silver Fachinal mine also known as the Cerro Bayo Mine was put into production in 1985 and closed in 2008. The Cerro Bayo assets were sold in 2010 to Mandalay Resources Corporation.

1991: Coeur acquired all of the outstanding common stock of Callahan Mining Corporation. This acquisition included the Galena Mine and the Flexaust Company, which manufactured flexible hose, duct and metal tubing.

The Flexaust acquisition deserves a moment of reflection because it represents one of the stranger chapters in Coeur's history. A precious metals miner owning an industrial hose manufacturer? Coeur sold Flexaust in 1995—presumably recognizing that manufacturing flexible ductwork and mining silver are fundamentally different businesses.

1993: Acquired an 80% operating interest in the Golden Cross Mine from Cyprus Gold New Zealand Limited. The mine is an underground and surface gold mine located near Waihi, New Zealand. The mine was closed in 1998.

The 1992 Silver Price Crash & Survival

The early 1990s brought one of silver's periodic collapses—and a test of Coeur's survival instincts. Silver prices declined to $3.93 per ounce in 1992, forcing the company to place the Coeur and Galena mines on standby.

At $3.93 per ounce, few silver mining operations could cover their costs. The response was a complex corporate restructuring:

1995: Coeur and ASARCO placed their interests in northern Idaho mines (Coeur, Galena and Calday mines) into a new corporation, Silver Valley Resources Corporation. The Coeur Mine was subsequently closed in 1998 and the Galena Mine continued to operate until 2006 when Coeur sold its interests in Silver Valley Resources to U.S. Silver Corporation.

This was the beginning of the end for Coeur's presence in its namesake region. The company that had been born in the Silver Valley, that carried its name, was gradually divesting its Idaho heritage—a process that would culminate years later in a complete exit.

The 1990s diversification strategy produced mixed results. Some acquisitions (Rochester, Wharf, Kensington) became long-term core assets. Others (Golden Cross, Cerro Bayo, Flexaust) proved to be distractions or disappointments. But the overall strategic direction was correct: Coeur needed geographic diversification to survive commodity cycles.

IV. The Near-Death Experience & Turnaround (2000–2011)

Building New Mines

As the new millennium began, Coeur pushed forward with ambitious development projects even as its financial position deteriorated:

Coeur acquired the San Bartolome property in 1999 and began current mining operations in 2008. The San Bartolomé mine sits near Potosi, Bolivia—a world heritage site. Mining of silver and silver-tin veins from Cerro Rico, a volcanic mountain adjacent to Potosi, began in the mid 1500s and has been continuous for over 450 years. In the 1650s, Potosi was the largest city in the western hemisphere with 160,000 residents.

2002: Coeur acquired the Martha underground silver mine in Argentina from Yamana Resources Inc. Coeur operated the mine until September 2012 when it was shut down.

2005: Acquired all of the silver production and reserves, up to 20 million payable ounces, contained at the Endeavor Mine in Australia as well as all of the silver production and reserves, up to 17.2 million payable ounces, at the Broken Hill Mine in Australia.

Financial Crisis & Near-Bankruptcy

Beneath the surface of aggressive acquisition activity, Coeur was in serious trouble. The company had over-extended, and when the 2003 credit crunch hit, the consequences were nearly fatal.

When he rejoined, the mining company's balance sheet was in such bad shape that lawyers were preparing a Chapter 11 bankruptcy filing. The company took extraordinary measures in 2003 that included issuing more than 44 million new shares of stock and selling $37 million in debt that could convert to equity. Existing shareholders were pummeled by the dilution.

The man at the center of this crisis was a young finance professional named Mitchell Krebs. He joined Coeur in 1995 after spending several years in the investment banking industry in New York. Mr. Krebs has held various positions in the corporate development department, including Senior Vice President of Corporate Development. In March 2008, Mr. Krebs was named Chief Financial Officer, a position he held until being appointed President and CEO.

After the debt restructuring, Wheeler pursued new growth opportunities. The company acquired silver reserves in Australia and a large property in Mexico. Wheeler also wanted to begin drilling in Alaska and Bolivia at mines the company had owned for years but never developed.

Except for a three-year shut down from 2007 to 2010 due to low reserves and metal prices, the mine has operated continuously since re-opening. Even Rochester—the company's Nevada workhorse—went dark during these difficult years.

The Palmarejo Acquisition: A Pivotal Bet

If there was a single transaction that would define Coeur's eventual revival, it was Palmarejo. 2007: Acquired the Palmarejo project from Bolnisi Gold NL and Palmarejo Silver and Gold Corporation. The Palmarejo Mine was put into production in 2008 and continues to operate.

Palmarejo Mine is a surface and underground gold and silver mine located about 420 kilometers by road southwest of the city of Chihuahua in northwestern Mexico. The property consists of over 12,000 hectares of mineral claims encompassing several silver and gold veins systems. Small-scale underground mining for silver veins in the Palmarejo area has occurred intermittently since the early 1800s. Coeur acquired the property in 2007 and mining commenced in 2008.

The Pamerejo mine produces ore from surface and underground operations that target a number of silver-gold vein systems. The ore is processed using flotation and cyanide leaching to produce silver-gold bars. In 2012, the mine produced 8.2 million ounces of silver and 106,038 ounces of gold.

Palmarejo represented a critical strategic shift: this was not just a silver mine, but a gold-silver complex. As Coeur would later demonstrate, gold exposure provided critical hedging against silver price volatility.

Mitch Krebs Takes the Helm

In July 2011, Mitchell Krebs was elevated from CFO to President and CEO. President and Chief Executive Officer of Coeur Mining, Inc., since 2011. Mr. Krebs joined Coeur in 1995 after spending several years in the investment banking industry in New York.

He holds a BS in Economics from the Wharton School at the University of Pennsylvania and an MBA from Harvard University. This pedigree—Wharton undergraduate, Harvard MBA, Wall Street investment banking—was unusual for a mining CEO and would shape Krebs's approach to the business.

During his 20-year tenure with Coeur, Mr. Krebs has led nearly $2 billion in capital-raising and debt-restructuring activities and has facilitated over $2 billion of acquisitions and divestitures. Prior to becoming the company's President and Chief Executive Officer, he was its Chief Financial Officer.

Krebs inherited a company that had survived its near-death experience but remained subscale, undercapitalized, and strategically unfocused. What followed would be one of the more dramatic corporate transformations in mining history.

V. The "Severing Ties with the Past" Era (2012–2017)

The Great Restructuring

Krebs surveyed the mining landscape and reached a stark conclusion about the industry's recent history. He later characterized the decade from 2002 to 2012 as "the lost decade of returns"—a period when silver and gold prices rose more than four times, yet profit margins were flat because of uncontrolled spending throughout the industry.

In 2012, the executives of Coeur Mining Inc. found themselves between a rock and a hard place. Wanting to reinvent itself after appointing new CEO Mitchell Krebs in July 2011, Coeur came up with an ambitious plan: move the company's corporate headquarters from the pleasant scenery of Coeur d'Alene, Idaho — its home since 1985 — to the concrete jungle of Chicago.

The Chicago Move: A Cultural Reset

The decision to leave Coeur d'Alene was not merely logistical—it was philosophical. Krebs wanted to "sever the ties with the past," as he put it. The legacy thinking of how the company was run and how companies in the industry were run needed to end.

By leaving the distant northwest, Coeur executives said the company could better coordinate travel among mining sites across the globe while directing its business in the country's third largest market. But much like extracting valuable minerals from the earth's hardened interior, Coeur's move would require a lot of heavy lifting.

For starters, 80 percent of the company's corporate employees in Coeur d'Alene decided not to make the move, meaning Coeur would work to provide those workers adequate outplacement resources.

Think about that: 80% of the corporate workforce chose not to relocate. This was effectively a complete reset of the headquarters team.

"Relocating our headquarters to Illinois will improve our access to key stakeholders and to our operations," said Mitchell J. Krebs, Coeur's President and CEO. "Chicago is a global, pro-business city, an international transportation hub and provides access to a broad and deep talent pool."

The company expects to complete the move to Chicago in the third quarter of 2013 and to hire at least 60 employees at its downtown headquarters by the end of 2014. In addition, Coeur intends to change its name to Coeur Mining in mid-May following its Annual Meeting.

In 2013 the company changed its name to Coeur Mining, Inc. from Coeur d'Alene Mines and moved its head office to Chicago, Illinois from Coeur d'Alene, Idaho.

Part of Chicago's allure was the city's two airports — O'Hare International Airport and Midway International Airport — which Kerr said would make it easier for employees to travel to the company's mines in Alaska, Nevada, Bolivia and Mexico. Proximity to convenient air travel would encourage employees to take a more hands-on approach by visiting Coeur's mining sites, something many employees didn't do prior. "There used to be a very hands-off approach to the sites, and as long as the results were there, there was less back-and-forth going to the sites."

The move, which also included relocating the company's headquarters to Chicago from Idaho, was part of a broad restructuring program initiated by CEO Mitchell Krebbs in 2012 in a bid to transform Coeur into a leaner and stronger company amid the severe headwinds facing the industry back then.

Kensington Finally Opens

After 23 years of exploration, permitting battles, and patience, Kensington finally reached commercial production. After considerable exploration work involving option agreements with a number of different companies and a court case that contested permits issued by the US Army Corps of Engineers, the Kensington mine was finally put into Production on July 3, 2010. The Kensington mine is an underground vein-style gold mine with several individual vein systems including the Kensington, Eureka, Raven, Elmira and Julian-Empire veins. The mine uses the cut-and-fill or stope-and-fill underground mining method. In 2012, the mine produced 82,125 ounces of gold.

Continued Acquisition Strategy

Even as Krebs restructured operations, Coeur continued building its development pipeline:

2013: Established Coeur Capital, Inc. to hold royalties and strategic investments.

2017: Coeur acquired all claims and infrastructure to the Silvertip mine in northern British Columbia. Silvertip represented an option on a high-grade silver-zinc-lead project in an emerging district.

Leaving Idaho: The Final Chapter

The firm sold its remaining assets in the region in July, 2006. After 78 years, Coeur d'Alene Mines Corporation had no mines in Coeur d'Alene. The company that carried the Silver Valley's name in its corporate identity had completed its transformation into something altogether different.

Though known as a silver producer, you might be surprised to learn how dramatically Coeur's product mix has changed in recent years. Today, Coeur gets a little more than 60% of its revenues from gold.

This transition from pure-play silver miner to diversified precious metals producer was complete. The question now was whether Coeur could execute on its growth ambitions—which would require the largest capital project in company history.

VI. The Rochester Expansion Bet: All-In on Scale (2018–2024)

The Largest Capital Project in Company History

If the Chicago move represented Coeur's cultural transformation, the Rochester expansion—known internally as POA 11 (Mine Plan of Operations Amendment 11)—represented its operational transformation. This was a bet-the-company infrastructure investment designed to turn Rochester from a mid-sized heap leach operation into one of the world's largest.

The recently completed expansion at Coeur Mining's Rochester silver-gold mine, otherwise known as Mine Plan of Operations Amendment 11 (POA 11), was a 10-year process. At full capacity, the ore throughput for the mine, which is located 120 miles northeast of Reno, Nevada, will now be 32 million tons per year, or 2.5 times greater than historic levels.

Of the five mines that Coeur Mining Inc operates in North America, Rochester is its largest. The 2020 expansion of the Rochester mine is the largest expansion project in Coeur's history, aiming to maximise reserve growth and benefit from larger-scale operations.

The expansion is more than doubling the planned annual crusher throughput capacity from roughly 14 million tons to over 28 million tons. This will take the mine's average annual silver and gold production to over 8.0 million ounces and approximately 80,000 ounces, respectively, for the initial ten years post-expansion.

The "White Knuckle" Years

Krebs later described the period from 2019-2023 as "white-knuckle days and months and quarters"—and with good reason. The original cost estimate for the expansion was $425 million with completion expected in early 2023. Reality intervened.

The original cost estimate for the POA 11 expansion was $425 million and the original timeline to completion was early 2023. Over time, the price tag grew to $730 million, and the timeline was pushed out one year. The project was affected by external forces beyond the company's control.

Construction on POA 11 started in 2020, at the same time as the onset of COVID-19. The pandemic not only impacted activities at the mine as far as construction, but it also impacted Coeur's ability to secure various components, which extended timelines. COVID-19 was only one of the obstacles the company had to overcome. The original plan called for the cash flow from the Rochester mine to help finance the expansion.

The timing couldn't have been worse. Starting a major construction project at the onset of a global pandemic, with supply chain chaos, labor shortages, and cost inflation—this was the definition of adverse circumstances.

"Our team has done a good job of designing a lot of flexibility into the project," he said. "The fact that it's behind us now and that everyone can see this really is a big deal." The original cost estimate for the POA 11 expansion was $425 million and the original timeline to completion was early 2023.

Commercial Production Achieved (2023-2024)

Coeur Mining, Inc. today announced the achievement of several critical milestones at its major Rochester expansion project in Nevada, including the production of the first silver and gold ounces. Following a ramp-up period expected to last into early 2024, Rochester is expected to drive a step-change in the Company's overall production levels, cost profile, and cash flow.

Coeur Mining today provided an update on its newly-expanded Rochester silver and gold mine in Nevada, including the achievement of commercial production at the operation as of March 31, 2024. Commissioning of the new three-stage crushing circuit and truck load-out facility was completed on March 7. Since then, the crushing circuit has operated at an average throughput of nearly 70,000 tons per day and has exceeded 88,000 tons per day, leading to the declaration of commercial production as of the end of the first quarter. Ramp-up to full design capacity of 88,000 tons per day—or approximately 32 million tons per year—remains on schedule for completion during the first half of 2024.

By Q2 2024, Rochester had achieved full ramp-up. The Rochester expansion, a significant growth project for Coeur, is now operational and showing improving performance with increasing free cash flow. The mine generated $29.6 million in free cash flow during Q3 2025, a substantial improvement from a negative $6.9 million in Q3 2024.

The Rochester expansion represented an enormous risk—a $730 million bet on silver's future at a time when the company was generating modest cash flow. But by the time the project was complete, the precious metals landscape had fundamentally shifted, and Coeur was positioned to capture the upside.

VII. The M&A Acceleration (2024–2025)

SilverCrest Acquisition: Adding Las Chispas

With Rochester expansion largely behind it, Coeur's management pivoted to external growth. In October 2024, they announced a transformational acquisition:

Coeur Mining, Inc. ("Coeur") (NYSE: CDE) and SilverCrest Metals Inc. ("SilverCrest") (TSX: SIL; NYSE American: SILV) announce that they have entered into a definitive agreement (the "Agreement") whereby, a wholly-owned subsidiary of Coeur will acquire all of the issued and outstanding shares of SilverCrest pursuant to a court-approved plan of arrangement (the "Transaction").

With the addition of the Las Chispas mine – one of the world's lowest-cost and highest-grade silver/gold operations – the combined company is expected to produce 21 million ounces of silver annually.

This represents an 18% premium based on 20-day volume-weighted average prices of Coeur and SilverCrest each as at October 3, 2024 on the NYSE and NYSE American, respectively, and a 22% premium to the October 3, 2024 closing price of SilverCrest on the NYSE American. This implies a total equity value of approximately $1.7 billion based on SilverCrest's common shares outstanding. Upon completion of the Transaction, existing Coeur stockholders and SilverCrest shareholders will own approximately 63% and 37% of the outstanding common stock of the combined company, respectively.

The merged company will own five mines in North America, with three of them considered top silver producers — Rochester in Nevada; Palmarejo in Mexico's Chihuahua; and Las Chispas in Sonora, also Mexico. Las Chispas mine, which began production in late 2022, has shown strong operational performance.

Under the terms of the Agreement, Coeur acquired all of the issued and outstanding common shares of SilverCrest, with SilverCrest shareholders receiving 1.6022 Coeur common shares for each SilverCrest common share. Coeur issued 239,331,799 shares in the Transaction.

The deal closed in February 2025. "With the closing of the SilverCrest transaction last week, we're delighted to welcome the Las Chispas team to the Company, and to have Eric Fier and Pierre Beaudoin join our Board of Directors."

New Gold Acquisition: Becoming a Senior Producer

But Coeur wasn't done. On November 3, 2025—just weeks before this writing—the company announced an even larger transaction:

Coeur Mining (NYSE: CDE) is acquiring Canada's New Gold (TSX: NGD) in an all-stock deal valued at about $7 billion, creating a new North American mining heavyweight amid record gold prices and renewed investor enthusiasm for precious metals.

The addition of New Gold's two Canadian mines results in a combined company with seven North American operations generating $3 billion of expected EBITDA and $2 billion of expected free cash flow in 2026 from production of approximately 20 million ounces of silver, 900,000 ounces of gold and 100 million pounds of copper.

The Exchange Ratio implies consideration of $8.51 per New Gold common share, based on the closing price of Coeur shares of common stock on the New York Stock Exchange ("NYSE") on October 31, 2025. This represents a 16% premium to the October 31, 2025 closing price of New Gold on the NYSE American. In the aggregate, this implies a total equity value of approximately $7 billion based on New Gold's common shares outstanding and a pro forma combined equity market capitalization of approximately $20 billion.

Upon completion of the Transaction, existing Coeur stockholders and New Gold shareholders will own approximately 62% and 38% of the outstanding common stock of the combined company, respectively.

New Gold brings two Canadian mines to the combination: New Gold Inc. is a Canadian mining company that owns and operates the New Afton gold-silver-copper mine in British Columbia and the Rainy River gold-silver mine in Ontario, Canada.

In 2025, the Toronto-based miner expects its consolidated gold production to increase by 16% to 325,000-365,000 oz., driven mainly by the improved production profile at Rainy River. Over the next three years, the mine located 65 kilometres northwest of Fort Frances, Ontario, is expected to have average production of 300,000 oz. per year.

"Both companies are in the early stages of generating significant cash flow after several years of heavy investment. We believe this is an extraordinary opportunity to create an unrivaled North American-only, mining powerhouse at just the right time," said Mitchell J. Krebs.

The transaction is expected to close in the first half of 2026. Upon completion, Coeur CEO Mitchell J. Krebs will lead the combined company, with New Gold CEO Patrick Godin joining Coeur's board. The transaction is expected to close in the first half of 2026.

The Transformation in Numbers

The scale of Coeur's transformation is difficult to overstate. Consider the trajectory:

"With the addition of New Gold's two Canadian operations to our five current operating mines we expect to generate approximately $3 billion of EBITDA and approximately $2 billion of free cash flow in 2026 at significantly lower overall costs and higher margins. Just two years ago, Coeur's full-year EBITDA totaled $142 million and its free cash flow was ($297) million. Even comparing to our expected approximate $1 billion of EBITDA and $550 million of free cash flow in 2025 highlights the extent to which this transaction helps accelerate Coeur's ongoing repositioning as a larger, more resilient, lower cost, and lower risk company."

From negative $297 million in free cash flow to projected $2 billion in free cash flow—in the span of three years. This is what commodity leverage combined with operational execution looks like.

VIII. The 2025 Inflection Point & Financial Transformation

Record Results

Coeur's financial transformation in 2025 has been remarkable. Coeur Mining achieved record quarterly production supported by solid cost performance across its operations. The company reported record quarterly net income of $266.8 million ($0.41 per share), significantly higher than the $70.7 million ($0.11 per share) reported in Q2 2025. Adjusted net income reached $147.3 million ($0.23 per share), up from $127.4 million ($0.20 per share) in the previous quarter.

Adjusted EBITDA reaching $299 million (54% margin) in Q3 2025, compared to $126 million (40% margin) in the same period last year.

Operating cash flow reached $237.7 million, up from $111.1 million in Q3 2024, while capital expenditures remained relatively controlled at $49.0 million compared to $42.0 million in the prior-year period.

The third quarter saw Coeur Mining benefit from higher realized metal prices, with gold averaging $3,148 per ounce (compared to $2,309 in Q3 2024) and silver averaging $38.93 per ounce (versus $29.86 in Q3 2024). Gold sales increased to 114,495 ounces, up from 96,913 ounces in the same period last year, while silver sales rose to 5.0 million ounces from 3.0 million ounces.

Balance Sheet Strength

One of the most notable achievements in Q3 2025 was the significant strengthening of Coeur's balance sheet.

"Together with the benefit of higher gold and silver prices, we saw a step change in our financial results in the quarter, including an impressive $146 million of free cash flow, while we eliminated the remaining balance on our RCF and began buying..."

Coeur has also initiated a share repurchase program, with approximately 10% of the $75 million authorization completed during the quarter. This reflects management's confidence in the company's financial position and commitment to returning value to shareholders.

2024 Full-Year Performance

For the full year, Coeur reported revenue of $1.1 billion, cash flow from operating activities of $174 million and GAAP net income from continuing operations of $59 million, or $0.15 per share.

The company noted significant increases in both gold and silver production, with an impressive year-over-year EBITDA growth of 138% to $339 million.

The company's cost structure has also improved dramatically. The company has benefited from subsiding inflationary cost pressures across most categories, helping to maintain competitive cost structures. While labor costs have seen a modest increase, materials, parts, and supplies costs per ore ton mined have decreased to $4.06 in Q3 2025 from $4.56 in Q3 2023.

IX. The Precious Metals Macro Environment

Gold's Record Rally

The macro backdrop for Coeur's transformation couldn't be more favorable. Gold broke a new record high on Oct. 10, surpassing $4,000 per ounce for the first time, and continued to climb since then. The gold price rally of nearly 50% in 2025 is likely to continue as demand from central banks, ETFs and even retail investors remains strong. On Oct. 21, the rally hit a wall, with a drop of as much as 6%, the biggest daily loss in 12 years. Still, gold has surged about 50% in 2025, cementing its status as one of 2025's top-performing assets.

The merger comes amid a record-setting rally in gold, which climbed above $4,000 an ounce this year and which the sector expects to surpass the $5,000 mark in the next 12 months. Shares of both Coeur and New Gold have tripled in 2025.

Prices are expected to average $3,675/oz by the fourth quarter of 2025 and climb toward $4,000 by mid-2026. Central bank and investor demand for gold is set to remain strong, averaging around 710 tonnes a quarter this year.

Consistently high levels of purchases by CBs (900 tonnes forecasted in 2025) are expected, given the current macro environment as well as a further expansion in investor holdings, particularly from exchange-traded funds (ETFs) and China. Even with three consecutive years of more than 1,000 tonnes of CB gold purchases, the structural trend of higher CB buying has further to run in 2025 and 2026.

Silver's Structural Deficit

While gold has captured headlines, silver's fundamentals may be even more compelling for Coeur. Michael DiRienzo, president and CEO of trade body The Silver Institute, said global silver demand reached 1.2 billion ounces in 2024, driven by the photovoltaic (PV) solar market which uses silver to make equipment such as solar panels. Industrial consumption is a major driver for the silver market.

The numbers tell a compelling story: 2024 marked a record year with industrial consumption reaching an astonishing 680 million ounces, according to the Silver Institute's World Silver Survey. More significantly, 2024 represents the fifth consecutive year of market deficit, with demand exceeding mining output by approximately 215 million ounces – the largest annual shortfall ever recorded.

According to data from the World Silver Survey 2025, industrial fabrication demand reached a new record of 680.5 million ounces in 2024, maintaining upward momentum through 2025. The supply side remains structurally tight: analysts project a market deficit of roughly 149 million ounces this year, marking five consecutive years where demand has outpaced annual mine production.

"Silver's structural deficit is projected to continue in 2025, and could pose challenges to the energy transition if the deficit continues. "If we are really going to have all these gigawatts and terawatts of renewable power out there, where will it all come from [to achieve net-zero emissions] by the year 2060?"

The Clean Energy Connection

Silver's role in the energy transition has fundamentally changed its demand profile. The solar energy sector has emerged as silver's fastest-growing demand source, consuming approximately 140 million ounces in 2024 – a figure projected to reach 200 million ounces annually by 2028 according to Metals Focus. Silver's critical role in photovoltaic (PV) technology stems from its unmatched electrical conductivity and durability. In traditional crystalline silicon solar cells, silver paste is screen-printed onto the front and rear surfaces to form the electrical contacts that collect and transmit the electricity generated.

In 2024, solar alone absorbed 232 million ounces, up from just 60 million ounces in 2015, according to the Silver Institute.

Silver's high conductivity and ductility make EVs more efficient by establishing lightweight but strong electrical connections between batteries and other car components. Battery electric vehicles use between ~25-50 grams of silver per vehicle.

The electrification theme extends beyond solar into electric vehicle battery systems, charging infrastructure, and grid modernization, all requiring significant silver content per unit. This creates compounding demand pressure as multiple green technologies scale simultaneously. Unlike cyclical industrial metals, silver's green energy applications represent secular demand shifts with limited substitution potential, particularly in high-conductivity applications where performance cannot be compromised.

For Coeur, this structural shift represents a fundamental tailwind. The company's scale in silver production positions it to benefit from what appears to be a multi-year demand story driven by forces far larger than jewelry or investment demand.

X. Competitive Positioning & Industry Context

The Competitive Landscape

Coeur Mining's main competitors include Barrick Gold Corporation, Newmont Corporation, Hecla Mining Company, Kinross Gold Corporation, and First Majestic Silver Corp. Key competitors include Barrick Gold, Newmont Corporation, Hecla Mining, Kinross Gold, and First Majestic Silver, each presenting unique challenges and opportunities for Coeur Mining in the industry.

Coeur Mining, Inc. is a precious metals mining company listed on the New York Stock exchange. It operates five mines located in North America. Coeur employs 2,200 people and in 2012 it was the world's 9th largest silver producer.

With the New Gold acquisition, Coeur's competitive positioning will shift dramatically. For 2026, Coeur estimates production of approximately 20 million ounces of silver, 900,000 ounces of gold and 100 million pounds of copper. Notably, the merger will position the company as one of the five largest silver producers in the world, with the white metal representing 30 percent of its total metal reserves.

Coeur, which operates a total of five mines in the United States and Mexico, plans to combine with New Gold, owner of the Rainy River gold mine in Ontario and the New Afton copper-gold mine in B.C. The combined company will have seven operations producing about 1.25 million gold-equivalent ounces next year, including 900,000 ounces of gold and 20 million ounces of silver.

Strategic Advantages

Strategic Mine Locations: Coeur Mining operates a number of gold and silver mines strategically located in the U.S. This geographical advantage allows the company to minimize transportation costs and logistical challenges, giving it a competitive edge in the market.

The company's North American focus provides jurisdictional diversification while avoiding the political risks associated with mining in less stable regions. All operations are in the United States, Canada, or Mexico—developed countries with established mining legal frameworks.

Commitment to Sustainability: Coeur Mining is dedicated to sustainable mining practices and environmental stewardship. By prioritizing sustainability in its operations, the company not only meets regulatory requirements but also enhances its reputation and attracts socially responsible investors.

The company also emphasizes its strong corporate culture as a core competitive advantage. The recent biennial culture survey achieved a 92% participation rate, surpassing industry benchmarks and improving 13% over 2023 and 44% since 2019, reflecting growing trust and engagement among employees.

XI. Bull Case, Bear Case & Risk Analysis

The Bull Case

1. Structural Precious Metals Tailwind: Gold at $4,000+ and silver benefiting from both investment demand and irreplaceable industrial applications creates a favorable environment for precious metals producers. Central bank buying, geopolitical uncertainty, and dollar weakness support sustained high prices.

2. Operational Leverage at Scale: With Rochester expansion complete, Las Chispas integrated, and New Gold pending, Coeur's fixed cost base supports dramatically higher free cash flow at current metal prices. The projected leap from $142 million EBITDA in 2023 to $3 billion in 2026 (post-New Gold) represents extraordinary operating leverage.

3. Exploration Upside: Coeur Mining continues to invest in exploration to drive organic growth, with a planned investment of $85 million for 2025, significantly higher than in previous years. This strategic focus on exploration aims to extend mine lives and identify new opportunities within the company's existing property portfolio.

4. North American Focus: 100% North American operations provide jurisdictional premium versus competitors with exposure to politically volatile regions. Supply chain reliability and regulatory predictability are increasingly valued by investors.

5. Management Track Record: Krebs has guided Coeur through near-bankruptcy, a complete operational restructuring, the Rochester expansion, and now two transformational acquisitions. The team has demonstrated ability to execute complex projects.

The Bear Case

1. Commodity Price Dependence: Dependence on Precious Metal Prices: The company's financial performance is heavily reliant on the prices of gold and silver, which can be volatile and subject to market fluctuations. A sustained decline in gold and silver prices would significantly impact profitability.

2. Integration Risk: Two major acquisitions in quick succession (SilverCrest and New Gold) create substantial integration risk. Cultural differences, system harmonization, and management bandwidth could impair execution.

3. Geopolitical Exposure: While North American-focused, significant Mexican exposure carries some political risk. Changes in mining taxation, environmental regulation, or permitting could impact operations.

4. Cost Inflation: High Operational Costs: The mining industry is characterized by high operational costs, and fluctuations in resource prices can significantly impact profitability. Despite recent improvements, mining is inherently capital-intensive.

5. Dilution: Both recent acquisitions were all-stock transactions. Existing shareholders have been significantly diluted to fund growth—Coeur issued 239,331,799 shares in the Transaction for SilverCrest alone, and the New Gold deal will add more shares outstanding.

Porter's Five Forces Analysis

Supplier Power (Moderate): Mining requires specialized equipment from concentrated suppliers, but Coeur's scale provides negotiating leverage. Energy costs remain a variable expense subject to market forces.

Buyer Power (Low): Gold and silver are commodity products sold at spot prices. Coeur has no customer concentration risk—the market absorbs whatever it produces.

Threat of New Entrants (Low): Mining requires massive capital investment, long permitting timelines, and technical expertise. Barriers to entry are substantial. "Profitable mining customers will continue to drive the de-bottlenecking of projects and underpin capex growth out to the end of the decade. But a super-cycle in the form of a substantial greenfield uptick is unlikely, given the permitting and regulatory constraints."

Threat of Substitutes (Low for Gold, Moderate for Silver): Gold has no industrial substitutes for its monetary/store-of-value function. Silver faces some substitution risk in industrial applications through thrifting, though silver's green energy applications represent secular demand shifts with limited substitution potential, particularly in high-conductivity applications where performance cannot be compromised.

Competitive Rivalry (Moderate to High): The mining industry is fragmented with many competitors of varying scale. However, high-quality deposits are finite, and disciplined capital allocation has improved industry dynamics.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Post-New Gold, Coeur will operate at significantly greater scale, spreading fixed costs across a larger production base. Rochester's expansion is explicitly designed to capture scale economics.

Network Effects: Not applicable to mining.

Counter-Positioning: Coeur's North American-only strategy could be viewed as counter-positioning against global miners with diverse geopolitical exposure—a choice that incumbents may struggle to replicate.

Switching Costs: Not applicable—gold and silver are fungible commodities.

Branding: Limited applicability, though ESG credentials and operational track record matter for institutional investors.

Cornered Resource: This is where mining companies derive their power. High-quality mineral deposits are inherently scarce. Coeur's reserve base, particularly following acquisitions, represents cornered resources that competitors cannot easily replicate.

Process Power: Coeur's 95+ years of mining experience and specific operational expertise in underground silver-gold mining represents accumulated know-how. "With over 15 years of experience operating our Palmarejo underground silver and gold operation next door in Chihuahua, we look forward to adding the high-quality Las Chispas mine to create a leading global silver company."

XII. Key Metrics & What to Watch

For long-term fundamental investors tracking Coeur's ongoing performance, three KPIs stand out as most critical:

1. All-In Sustaining Costs (AISC) per Gold Equivalent Ounce

AISC captures the full cost of production including sustaining capital—the truest measure of operational efficiency and margin potential. As Rochester ramps to full throughput and acquisition synergies are realized, AISC should decline. Watch for quarterly progression toward management's cost guidance and comparison to industry benchmarks.

2. Free Cash Flow

After years of heavy capital investment, Coeur has reached a free cash flow inflection point. "Looking ahead to the second half of the year, we expect even higher gold and silver production levels consistent with our re-affirmed 2025 production and cost guidance." The company's ability to convert EBITDA into free cash flow—and what it does with that cash (debt reduction, buybacks, dividends, exploration)—will determine long-term value creation.

3. Reserve Replacement Ratio

Mining depletes reserves by definition. The ability to replace depleted reserves through exploration and acquisition determines long-term sustainability. Top exploration priorities for the Company's 2024 exploration program were achieved, including: (1) Kensington reaching a five year proven and probable reserve mine life. Watch for reserve updates that demonstrate mine life extension across the portfolio.

XIII. Regulatory & Accounting Considerations

Material Risks

Permitting Risk: Mining operations require extensive permits that can be challenged or delayed. Kensington's 23-year journey from acquisition to production illustrates this risk. Any new development projects face similar uncertainty.

Environmental Liabilities: The Coeur d'Alene region's history illustrates mining's environmental legacy. In 1983, the U.S. Environmental Protection Agency (EPA) listed a 21-square mile mining area in northern Idaho as a Superfund site. EPA extended those boundaries in 1998 to include areas throughout the 1500-square mile area Coeur d'Alene River Basin project area. Under Superfund, EPA has developed a plan to clean up the contaminated area that will cost an estimated $359 million over 3 decades. While Coeur exited Idaho years ago, active operations carry reclamation obligations.

Metal Streaming Agreements: Coeur has various streaming and royalty agreements that affect its effective metal realizations. Coeur operates on both sides of the streaming scale—it has been selling metal streams to streaming companies like Franco Nevada Corp. for several years. Coeur struck a fresh gold streaming agreement with Franco-Nevada wherein it will sell 50% of gold production from Palmarejo to Franco Nevada for $800 an ounce or the spot price, whichever is lower.

Accounting Judgments

Reserve Estimates: Mineral reserve and resource calculations involve significant judgment around commodity prices, recovery rates, and cost assumptions. Changes in these assumptions can materially impact reported reserves and asset values.

Acquisition Accounting: With two major acquisitions in close succession, fair value allocations for acquired assets and goodwill determination involve significant management judgment. Watch for any subsequent impairment charges.

Depreciation/Depletion: Mining assets are depleted based on reserves extracted versus total reserves—changes in reserve estimates directly impact quarterly depreciation expense.

XIV. Conclusion: The Making of a Mining Major

The story of Coeur Mining is, in many ways, the story of American precious metals mining itself. Born in Idaho's Silver Valley during a moment of optimism, the company survived the Depression, navigated commodity cycles, nearly went bankrupt, and ultimately reinvented itself completely—leaving its namesake region behind and emerging as a diversified, professionally managed precious metals producer.

"We got a chance to push reset on a lot of systems, processes and functions, which is rare for a company that's been around this long."

Mitchell Krebs's observation about the Chicago move could apply to Coeur's entire journey. The company has pushed reset repeatedly—each time emerging stronger and more strategically focused.

The 2024-2025 period represents perhaps the most dramatic reset of all. With the Rochester expansion complete, Las Chispas integrated, and New Gold pending closure, Coeur stands on the threshold of becoming something qualitatively different from what it has been for most of its history.

"This transaction provides clear and compelling benefits for New Gold and Coeur shareholders by bringing together two companies with similar cultures to create a stronger, more resilient and larger scale precious metals mining company," said Mitchell J. Krebs. "We believe this is an extraordinary opportunity to create an unrivalled North American-only, mining powerhouse at just the right time."

Whether this transformation succeeds will depend on execution—integrating acquisitions, maintaining operational discipline, and navigating the inevitable commodity cycles that have defined precious metals for centuries. The company's 95-year survival record suggests an institutional resilience that shouldn't be underestimated.

For investors, Coeur offers exposure to a company at an inflection point—one with significant commodity leverage, operational momentum, and strategic optionality. The risks are real: integration challenges, commodity price dependence, and the inherent uncertainty of mining. But so are the opportunities: a structural bull market in precious metals, industrial silver demand from the energy transition, and a management team with demonstrated ability to execute transformational change.

From Idaho's Silver Valley to a North American mining powerhouse—Coeur's century-long journey continues.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube