CBIZ: The Great American Accounting Roll-up

I. Introduction and Episode Roadmap

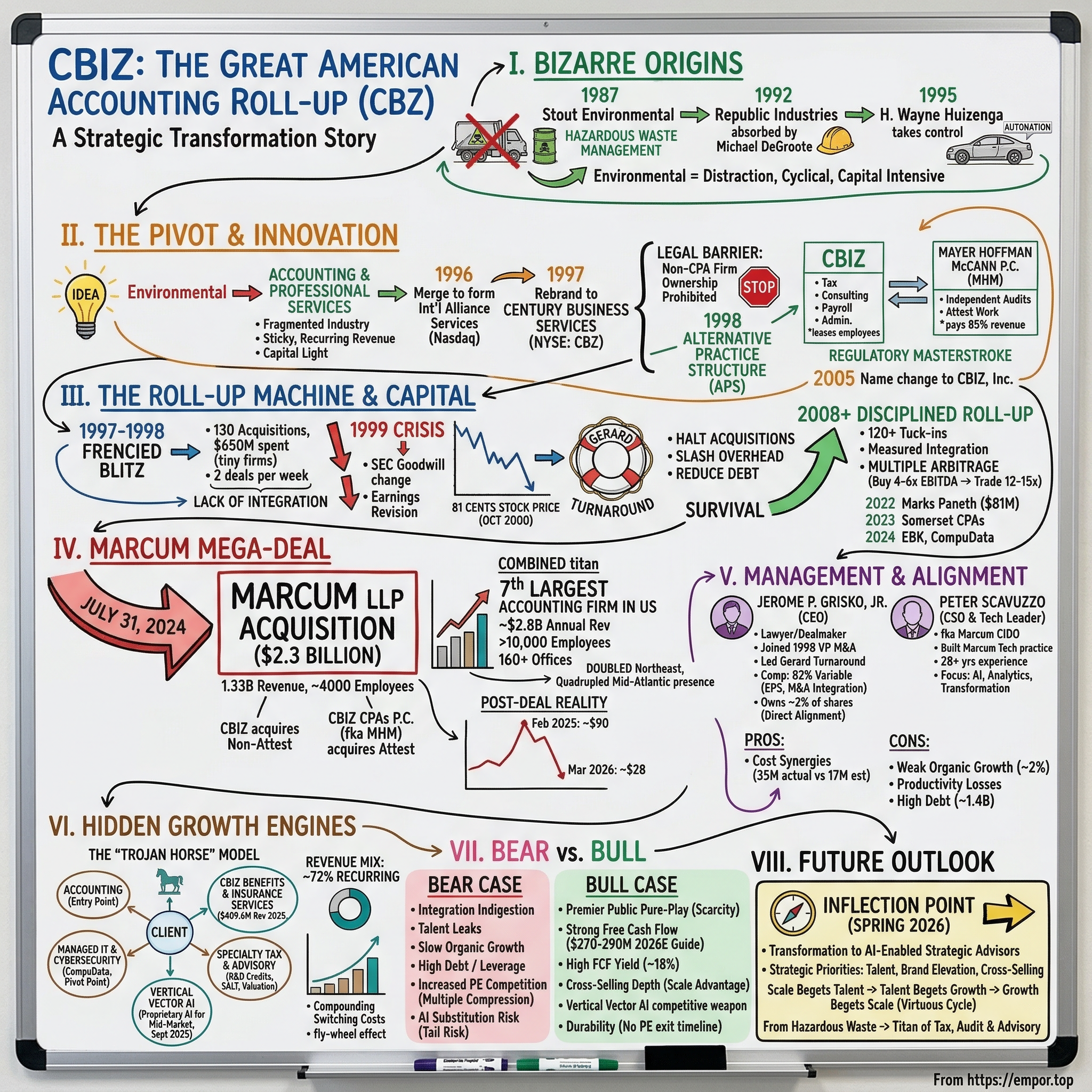

How did a 1980s hazardous waste management company transform into a three-billion-dollar titan of tax, audit, and advisory? That question sounds absurd. It sounds like the setup to a business school joke, or maybe a cautionary tale about corporate mission drift. But it is neither. It is the actual, factual origin story of CBIZ, Inc., and it is one of the strangest, most strategically brilliant corporate metamorphoses in modern American business history.

CBIZ, trading on the New York Stock Exchange under the ticker CBZ, is the seventh-largest accounting and professional services provider in the United States. With over ten thousand employees, more than 160 offices across 21 major metropolitan markets, and annual revenue approaching three billion dollars, it sits in rarefied company alongside the likes of RSM, Baker Tilly, and BDO.

But unlike those firms, which grew organically from traditional CPA partnerships over decades, CBIZ was built through something far more audacious: a relentless, decades-long roll-up of small and mid-sized accounting practices, stitched together by a regulatory innovation so clever it essentially created an entirely new category of public company.

For investors, CBIZ represents something genuinely rare. The accounting profession in America generates hundreds of billions of dollars in annual revenue, yet the vast majority of that revenue flows through private partnerships that are structurally incapable of accessing public capital markets. State licensing laws prohibit non-CPAs from owning accounting firms. The SEC requires auditors to be independent of their clients. These regulations were designed, quite deliberately, to keep Wall Street out of the audit room.

CBIZ figured out how to thread that needle more than two decades before private equity firms started flooding the sector with capital. It remains one of the only ways public market investors can gain direct exposure to the massive, highly fragmented, and extraordinarily sticky CPA services industry.

Here is a number that puts the opportunity in perspective: the American accounting profession generates an estimated 150 billion dollars in annual revenue. There are roughly 46,000 CPA firms in the United States, the vast majority of them small partnerships with fewer than 20 professionals. That is an industry with the fragmentation profile of dry cleaning or dental practices, but with the recurring revenue characteristics and regulatory moats of a utility. The opportunity to consolidate that landscape was obvious. The barriers to doing so were not.

The story ahead covers the bizarre origins in hazardous waste disposal, a near-death experience that took the stock to 81 cents, the regulatory architecture that made the entire business model possible, a massive 2.3-billion-dollar acquisition that doubled the company overnight, hidden high-margin businesses that most investors overlook, and the management team whose incentives are tightly aligned with shareholder outcomes. This is the story of how a company nobody was watching became one of the most consequential players in American professional services. And it starts, improbably enough, with contaminated soil.

II. The Pivot: From Hazardous Waste to White-Collar Stickiness

In 1987, somewhere in the industrial heartland of America, a Delaware corporation called Stout Environmental, Inc. came into existence. It was the kind of company that made perfect sense for its era. The 1980s were the decade when American industry finally began confronting the toxic legacies of post-war industrialism. Superfund legislation had created a massive market for environmental remediation, and firms capable of cleaning up contaminated sites were in genuine demand. Stout Environmental was a player in that world, a company built around hazardous waste management, remediation contracts, and regulatory compliance work.

The company's trajectory changed dramatically in 1992 when it was absorbed into Republic Industries, the corporate vehicle of Michael G. DeGroote.

DeGroote was a Belgian-born Canadian entrepreneur who had previously built Laidlaw Transport from a 21-truck operation with 400,000 dollars in annual revenue into a diversified transportation and waste colossus generating more than half a billion dollars. DeGroote was a serial acquirer of the old school, a man who understood intuitively that fragmented industries could be consolidated into something much larger than the sum of their parts. He had done it with trucking. He had done it with school busing. Now he was doing it with waste disposal.

But the truly consequential figure in this chapter was H. Wayne Huizenga, the Fort Lauderdale dealmaker who had already built Waste Management into the world's largest garbage company and co-founded Blockbuster Video, turning a single store concept into a global entertainment franchise.

Huizenga arrived at Republic Industries in the summer of 1995, investing 64 million dollars of his own money and raising an additional 168 million to take control as chairman. His vision for Republic, however, had nothing whatsoever to do with environmental cleanup. Huizenga wanted to build an automotive empire.

He began buying hundreds of car dealerships, constructing AutoNation superstores, and acquiring car rental agencies at a breathtaking pace. The environmental operations were a distraction, a legacy asset from an earlier era.

In April 1995, Republic spun off its hazardous waste operations into a separate entity called Republic Environmental Systems, and once Huizenga took the wheel, the environmental business was essentially orphaned.

And here is where the story pivots. Freed from Huizenga's automotive ambitions, the environmental business found itself at a crossroads.

The economics of hazardous waste remediation were brutal: capital intensive, deeply cyclical, dependent on government contracts and regulatory mandates that could shift with every election cycle. Heavy equipment. Contaminated sites. Permitting battles. Environmental lawsuits. This was not a business that generated predictable, high-margin cash flows.

The company's leadership looked at this reality and asked a question that would change everything: what if there was a business that was the exact opposite of environmental cleanup? Something capital-light, highly fragmented, and incredibly sticky?

The answer was accounting.

It is worth pausing to appreciate just how radical this pivot was. Environmental remediation and accounting have almost nothing in common operationally, culturally, or financially. One involves hard hats, hazmat suits, and heavy machinery. The other involves spreadsheets, tax codes, and conference rooms. One requires massive capital investment in equipment and site access. The other requires almost no physical capital beyond office space and computers. One is project-based, with revenue that ends when the site is clean. The other is relationship-based, with revenue that recurs annually as long as the client stays in business.

But from a financial engineering perspective, the two industries share one crucial characteristic: extreme fragmentation. Just as the environmental remediation market was populated by thousands of small, local operators, the accounting profession was populated by tens of thousands of small, local CPA firms. And fragmented industries are roll-up industries. The playbook was the same. The business was just better.

In May 1996, the entity merged with Alliance Holding Corporation, a Cleveland-based company centered around Century Surety Company, a specialty insurance carrier. The resulting combination created International Alliance Services, Inc., which began trading on the Nasdaq. The vision was elegantly simple but genuinely novel for its time: merge outsourced insurance with outsourced accounting and advisory services to create a one-stop shop for middle-market businesses. A single firm that could administer a benefit plan and also insure it. A single relationship that could handle a company's taxes and its employee health coverage.

By 1997, the company had shed its environmental operations entirely and rebranded as Century Business Services, Inc., moving to the New York Stock Exchange under the ticker CBZ. The transformation from hazardous waste to white-collar professional services was complete in barely 18 months.

But the most important innovation was still to come. There was a fundamental legal problem with rolling up accounting firms, and it was not a minor technicality. State laws across America mandate that only licensed CPAs can own CPA firms. The SEC requires auditors to be independent of their clients. A publicly traded company simply buying up accounting practices would compromise the very audit independence that makes those practices valuable. It appeared to be an insuperable barrier, the kind of structural constraint that kills business models before they are born.

Enter the Alternative Practice Structure, or APS. In 1998, Century Business Services partnered with Mayer Hoffman McCann P.C., a Kansas City-based CPA firm, under a framework sanctioned by the AICPA's Code of Professional Conduct.

Think of it like this: imagine you want to own a law firm, but the bar association says only lawyers can own law firms. So instead, you create a separate company that employs all the lawyers, owns all the office space, provides all the technology and marketing, and leases those lawyers back to the law firm to do the actual legal work. You get the economic benefit of the law firm without technically owning it. That is essentially what CBIZ did with accounting.

The mechanics were ingenious.

CBIZ would acquire the non-attest functions of CPA firms: everything from tax preparation to consulting to payroll processing. Mayer Hoffman McCann would handle the independent audits, the "attest" work that regulators said only CPAs could perform.

Virtually all of MHM's shareholders became salaried employees of CBIZ, then were "leased" back to MHM to perform attest work. CBIZ provided office space, equipment, marketing, IT infrastructure, everything. In exchange, MHM paid CBIZ approximately 85 percent of its revenues.

This was the regulatory masterstroke that unlocked the entire national roll-up strategy. CBIZ captured the economics of running a massive accounting practice without technically owning the CPA firm. MHM retained the legal form of an independent practice, satisfying regulators. The SEC later confirmed that the two entities were "viewed as a single entity for SEC auditor independence purposes," which created its own compliance complexities but validated the fundamental architecture.

The structure was not without controversy.

In 2015, the SEC instituted proceedings against MHM after discovering that Tradebot Systems, a high-frequency trading broker-dealer and MHM audit client, had been investing in CBIZ stock from 2008 through at least 2013. Because CBIZ and MHM are effectively treated as one entity for independence purposes, Tradebot's CBIZ stock positions impaired MHM's independence with respect to its Tradebot audits.

The SEC imposed a 1.5-million-dollar penalty and required remediation of quality control procedures. The episode highlighted the ongoing compliance complexity of operating an APS at scale, but it did not threaten the fundamental viability of the model. It is, however, a regulatory overhang that investors should be aware of: the APS structure requires constant vigilance around independence rules, and future SEC enforcement actions, while unlikely to be existential, could create reputational risk and compliance costs.

The final piece of branding simplification came on August 1, 2005, when the company officially changed its legal name from Century Business Services to CBIZ, Inc. The CBIZ trademark had become the company's actual identity across its hundreds of practice locations, and the old name was clunky, generic, and forgettable. The ticker remained CBZ.

What had begun as a hazardous waste company was now, unmistakably, a professional services platform. And it was about to start acquiring with a discipline and consistency that would make it one of the most successful roll-ups in American business history. But first, it had to survive a near-death experience that nearly destroyed everything.

III. The Roll-Up Machine and Capital Deployment

Before the disciplined machine came the frenzied blitz. And before the frenzied blitz nearly killed the company, there was the intoxicating rush of deal velocity that defined the late 1990s, a decade when roll-up strategies were the most fashionable idea on Wall Street and every fragmented industry seemed ripe for consolidation.

From early 1997 through late 1998, Century Business Services executed one of the most aggressive acquisition campaigns in the history of professional services. The numbers are staggering even by the hyperactive standards of late-90s dealmaking.

The company screened between fifteen hundred and two thousand acquisition candidates. It conducted due diligence on roughly a thousand companies. And it ultimately acquired approximately 130 firms, spending around 650 million dollars.

That works out to an average deal size of barely five million dollars: tiny regional CPA practices, benefits consultancies, and payroll processors snapped up at a pace of nearly two deals per week. By mid-1998, Century Business Services operated over 100 offices across 28 states.

The company was not alone in this ambition. American Express Tax and Business Services and H&R Block's RSM McGladrey were also attempting to consolidate the accounting profession at the same time. Both had deeper pockets and stronger brand recognition.

Both would eventually fail. American Express sold its accounting division to H&R Block for roughly 220 million dollars, and H&R Block later exited the professional services consolidation business altogether. The fact that CBIZ outlasted both of these far larger competitors suggests its model had genuine operational advantages, or at least more resilient DNA.

But the euphoria ran headlong into the cold reality of integration. And this is where the CBIZ story becomes a cautionary tale before it becomes a success story.

Different firms ran on different systems. They had different cultures, different compensation structures, different ways of serving clients. They had been acquired on different terms, with different earnout provisions and different retention agreements. Welding 130 distinct organizations into a coherent whole proved far more difficult than the dealmakers had anticipated.

The crisis came to a head in December 1999. The company was forced to revise its goodwill accounting after the SEC required it to shorten its amortization period from 40 years, an aggressive posture, to the more standard 15 years. This accounting change cascaded into an earnings revision that turned projected profits into losses. Instead of earning 12 to 14 cents per share in the fourth quarter, the company now projected it might lose as much as two cents per share.

The market's reaction was devastating. Short sellers descended on the stock like sharks on chum. By October 2000, CBZ shares hit an all-time low of 81 cents. Eighty-one cents. Down from peaks above 20 dollars just two years earlier. That is a decline of more than 95 percent. The company had suffered what one historical account called "significant credibility damage," which is the polite way of saying investors thought the entire enterprise might be catastrophically mismanaged.

The board brought in Steven L. Gerard as CEO in October 2000. Gerard was a veteran corporate executive with turnaround experience, and his prescription was methodical and unsentimental.

Acquisitions were halted entirely. Not slowed, not made more selective. Halted.

Underperforming units were sold or shuttered. Administrative functions were consolidated across the group. Corporate overhead was slashed by 25 percent. Debt was reduced from 147 million dollars to 50 million in just 18 months.

It was the corporate equivalent of emergency surgery: stop the bleeding first, ask questions later.

The turnaround worked. Gerard served as CEO for 16 years, a tenure of remarkable stability for a company that had been on the brink of oblivion. During his watch, revenues grew from approximately 546 million dollars to 750 million, and the stock increased nearly tenfold while significantly outperforming major indices. Gerard passed away in April 2022, and the company released a formal tribute acknowledging his role in saving and building CBIZ. Without his intervention, it is entirely possible that CBIZ would have joined the long list of 1990s roll-up casualties: companies like Loewen Group, U.S. Office Products, and MedPartners that burned brightly and then imploded.

The near-death experience also contains a deeper lesson about the economics of professional services consolidation. The reason the 1997-1998 blitz failed was not that the underlying businesses were bad. The individual CPA firms and benefits consultancies that CBIZ acquired were, for the most part, solid, profitable operations with loyal client bases. The problem was that the consolidator had confused speed with strategy. Buying 130 firms in 18 months meant there was no time to integrate any of them properly. There was no shared technology platform. There was no unified culture. There was no common brand identity. There was no cross-selling infrastructure. Each acquired firm continued to operate as an island, but now with the added burden of corporate overhead, goodwill amortization, and reporting requirements that it had never dealt with as an independent partnership.

The lesson of the Gerard era was seared into the company's institutional memory: acquisition velocity without integration discipline is a formula for destruction.

When CBIZ resumed acquiring, beginning around 2008, it was a fundamentally different operation. The post-crisis roll-up strategy was measured, quality-first, and ruthlessly consistent. Over 120 acquisitions since 2008, all of them carefully vetted tuck-in deals until the Marcum transaction. The typical target was a regional accounting, benefits, or advisory firm with a strong local market position, stable client relationships, experienced leadership willing to stay on, and clearly identifiable integration pathways.

The typical price was four to six times EBITDA.

The multiple arbitrage was textbook, the kind of financial engineering that business school professors use to explain roll-up economics. CBIZ was buying small, localized firms at four to six times EBITDA, integrating them onto its national platform, and having those earnings valued at CBIZ's public market multiple, which for years traded between 12 and 15 times EBITDA and sometimes higher. Buy at five, trade at thirteen. The math was beautiful in its simplicity, and it worked for over a decade.

Some representative deals illustrate the strategy's evolution over time.

In 2022, CBIZ acquired Marks Paneth LLP for 81 million dollars in cash, adding 138 million in revenue, more than 600 team members, and a Top 50 national ranking with particular strength in New York real estate, construction, and hospitality. This was a significant step up in deal size from the typical five-to-ten-million-dollar tuck-in, signaling CBIZ's growing appetite for transformative acquisitions.

In 2023, the acquisition of Somerset CPAs and Advisors, the fifth-largest accounting firm in Indianapolis with 250 employees and 55 million in revenue, gave CBIZ its first significant presence in Indiana and extended its reach into Nashville, Tennessee. Also in 2023, Pivot Point Security, a Hamilton, New Jersey-based cybersecurity firm with just 30 employees, signaled an intriguing expansion into information security consulting, a service line that had nothing to do with traditional accounting but everything to do with the evolving needs of middle-market clients.

In early 2024, EBK, a Colorado Springs accounting firm with 50 employees and roughly nine million in revenue, filled a geographic gap. And in March 2024, CompuData, a Philadelphia-based technology solutions provider with 60 employees and 20 million in annual revenue, expanded CBIZ's managed IT capabilities.

Each deal followed the same two-track structure perfected in 1998: CBIZ acquired the non-attest assets while Mayer Hoffman McCann simultaneously acquired the attest assets. This bifurcated approach preserved regulatory independence while allowing CBIZ to capture the full economics of the acquired practice. It was a system, refined over more than a hundred iterations, that worked like clockwork.

But as private equity flooded into the accounting sector in the early 2020s, driving up multiples for quality firms, the old playbook of cheap tuck-ins became harder to execute. PE firms were suddenly willing to pay ten to twelve times EBITDA or more for top-twenty accounting firms. The arbitrage that had powered CBIZ's value creation for over a decade was compressing.

CBIZ adapted, shifting from high-volume opportunistic acquisitions to larger, strategic platform deals targeting geographic expansion and deep specialty niches. But the underlying logic remained unchanged. Accounting revenue is the holy grail of capital deployment for any serial acquirer.

It is recurring: tax returns must be filed every year, audits must be completed every year, employee benefits must be administered every year.

It is recession-resistant: companies cut advertising budgets and delay capital expenditures during downturns, but they do not stop filing taxes or complying with audit requirements. During the 2008-2009 financial crisis, the accounting profession was one of the few sectors that did not experience mass layoffs. Clients may have negotiated harder on fees, but they did not stop engaging.

And it is inflation-protected: as wages, healthcare costs, and regulatory complexity increase, the fees that professional services firms charge increase alongside them. An accounting firm's cost base is predominantly labor, and labor costs are passed through to clients in the form of higher billing rates. This is fundamentally different from a manufacturing company, where rising input costs may not be fully recoverable in pricing.

Once a middle-market CFO entrusts these functions to a single provider, the switching costs are enormous. Not just the direct cost of finding new providers and negotiating new contracts, but the information asymmetry cost of rebuilding the institutional knowledge that years of relationship carry. Your accountant knows the history. They know which deductions have been aggressive, which state filings are complicated, which employee benefit plans have unusual provisions. Replacing that knowledge is painful, risky, and expensive.

CBIZ's client retention rate sits at approximately 90 percent, and roughly 72 percent of its revenue comes from recurring engagements. For a serial acquirer, this is the dream: buy a practice, integrate it, and watch the revenue compound with minimal churn for decades. The question, as CBIZ entered 2024, was whether the company was ready for a deal that was not a tuck-in at all, but a transformation.

IV. The Marcum Mega-Deal: Doubling Down

On July 31, 2024, CBIZ announced the largest deal in its 37-year history, and the accounting world took notice. The target was Marcum LLP, a national accounting and advisory firm with approximately 1.33 billion dollars in annual revenue and around four thousand employees. The price was 2.3 billion dollars. This was not a tuck-in. This was a merger of near-equals, the kind of bet-the-company transaction that either defines a CEO's legacy or destroys it.

To understand why this deal mattered so much, you first need to understand Marcum. The firm traced its roots to a small Long Island practice called Marcum and Kliegman, founded in 1951. For its first three decades, it was exactly what it sounded like: a modest, regional CPA firm serving local businesses and families.

That changed when Jeffrey M. Weiner joined as the firm's seventh employee in 1981, fresh from Hofstra University. Weiner was named managing partner in 1990, when Marcum was still relatively obscure, a firm with perhaps a few dozen professionals operating on Long Island and in lower Manhattan.

What Weiner did over the next 33 years was remarkable. He transformed Marcum into one of the most aggressive acquirers in American accounting, absorbing dozens of competitors and building specialty practices across real estate, technology, financial services, healthcare, and litigation support.

Real estate was the crown jewel. Marcum became the go-to auditor for New York City's real estate industry, a position of enormous influence and profitability in a market where a single commercial property transaction could generate hundreds of thousands of dollars in advisory fees. By the time CBIZ came calling, Marcum was the thirteenth-largest accounting firm in the United States by revenue, with particular dominance in New York City and the broader Northeast.

The deal was structured as a cash-and-stock transaction: 1.1 billion dollars in cash and 14.4 million shares of CBIZ common stock valued at roughly 76 dollars and 84 cents per share. Consistent with the longstanding Alternative Practice Structure, the transaction split into two simultaneous tracks. CBIZ acquired Marcum's non-attest business. CBIZ CPAs P.C., the entity formerly known as Mayer Hoffman McCann, which had been renamed just three months earlier in August 2024 to better align branding, simultaneously acquired Marcum's attest assets.

The renaming of Mayer Hoffman McCann to CBIZ CPAs was itself significant. It formalized what had been true operationally since 1998: CBIZ and its associated CPA firm were, for all practical purposes, a single enterprise. The 25-year fiction of "Mayer Hoffman McCann" as a recognizable independent brand was retired in favor of a name that made the affiliation unmistakable.

The strategic rationale for Marcum was compelling on multiple dimensions. Before the deal, CBIZ and MHM ranked eleventh in the U.S. accounting firm revenue tables at 1.42 billion dollars. Marcum ranked thirteenth at 1.33 billion. Their combination vaulted the resulting entity to the seventh spot nationally, leapfrogging BDO and Grant Thornton, creating a firm with expected combined annualized revenue of approximately 2.8 billion dollars, over ten thousand team members, and more than 160 offices across 21 major markets.

The deal instantly doubled CBIZ's practices in New York and New England while quadrupling its Mid-Atlantic presence, the markets where Marcum was historically strongest. Chris Spurio, CBIZ's Financial Services president, said it plainly: "The combination of these two was just too good to pass up."

Allan Koltin, one of the accounting industry's most closely watched independent consultants, called the transaction "groundbreaking," noting it validated non-CPA firm ownership in accounting and would encourage further private equity participation in the sector. The advisors on either side underscored the deal's significance: CBIZ retained Perella Weinberg Partners and BakerHostetler, while Marcum was advised by Deutsche Bank and Dechert LLP. When you see Perella Weinberg and Deutsche Bank on opposite sides of a professional services transaction, you know the stakes are high.

But did CBIZ overpay? This is the question that haunted the stock from the moment the deal was announced. At 2.3 billion dollars, the acquisition represented a substantial premium to CBIZ's historical deal multiples. The company had spent years buying practices at four to six times EBITDA. The Marcum deal came at a time when PE-backed competitors were bidding up accounting practices to ten to twelve times earnings and sometimes higher.

In a market where roughly one-third of the top 30 U.S. accounting firms had aligned with financial sponsors, the premium may have been the cost of remaining competitive. The alternative, watching Marcum get snapped up by a private equity buyer and become a well-funded competitor, was arguably worse. But paying up for an asset, even a good one, only works if the integration delivers the promised synergies and the organic growth engine keeps running.

The deal closed on November 1, 2024. And then began the hard part.

Merging two massive professional services organizations is one of the most culturally complex integration challenges in business. These are not manufacturing companies where you can consolidate production lines and lay off redundant factory workers. They are people businesses, fundamentally and irreducibly, where the product walks out the door every evening. If those people feel undervalued, culturally misaligned, or uncertain about their future, they leave. And in professional services, when partners leave, they take their client relationships with them. A departing tax partner does not leave behind a machine that keeps producing tax returns. They leave behind an empty office and a Rolodex of clients who are now getting phone calls from a competitor.

The early integration results were genuinely mixed in a way that gave both bulls and bears ammunition.

On the positive side, cost synergies substantially exceeded initial targets. Management had originally projected 17 to 18 million dollars of cost savings in the first full year; actual 2025 cost synergies came in at 35 million dollars, roughly double the initial estimate. Redundant office leases were consolidated. Duplicate administrative functions were eliminated. Technology platforms were unified. The combined entity began operating on a single infrastructure faster than many observers expected.

But the revenue side told a different story. Organic revenue growth in 2025, the first full year of the combined entity, came in at only approximately two percent, well below what investors had expected for a firm of CBIZ's enhanced scale. Management attributed the softness to a combination of industry-wide weak demand from mid-market clients and the "productivity losses often experienced in the first year after combining two similarly sized organizations."

Translation: when you are simultaneously migrating systems, rebranding offices, reassigning client relationships, and integrating compensation structures, your people are spending time on internal logistics instead of serving clients and winning new business.

The full-year 2025 financials showed the combined entity generating 2.76 billion dollars in total revenue, adjusted EBITDA of 446.9 million dollars, and adjusted EPS of 3.61 dollars. Operating cash flow was 192.5 million dollars. The National Practices segment actually contracted by six percent. These were solid numbers by any absolute standard, but the organic growth rate disappointed a market that had priced in acceleration, not deceleration.

The stock price told the story of that disappointment. After reaching an all-time high of approximately 90 dollars in February 2025 on post-integration optimism, shares subsequently declined sharply. As of early March 2026, they trade around 28 dollars, a decline of roughly 63 percent from peak. The company's market capitalization has compressed to approximately 1.5 billion dollars, less than the cash portion of what it paid for Marcum alone.

Whether the Marcum integration represents a temporary digestion period or a more structural challenge will define CBIZ's next chapter. The company has been here before, of course. The 1997-1998 acquisition blitz also produced a period of integration pain that lasted years. But there is a crucial difference: in 1999, CBIZ was a chaotic collection of 130 unintegrated firms with no shared infrastructure. In 2025, CBIZ brought 25 years of integration experience, established systems, a proven APS framework, and a management team that had lived through the consequences of doing it wrong. Whether that institutional knowledge is sufficient to navigate a deal of Marcum's magnitude, a deal that is qualitatively different from anything CBIZ had attempted before, is the question that the next two to three years will answer.

The financial stakes are enormous. CBIZ repurchased 2.5 million shares for 168 million dollars in 2025, a significant capital allocation decision that reflects management's belief that the stock is undervalued relative to the company's intrinsic worth. If they are right, those repurchases will prove to be among the most value-accretive capital deployment decisions in the company's history. If they are wrong, that capital would have been better deployed against the 1.4-billion-dollar debt balance.

V. The Architects: Current Management and Incentive Alignment

Jerome P. Grisko, Jr., universally known as Jerry, is not the kind of CEO you would expect to find running one of the largest accounting firms in America. He is a lawyer, not an accountant, which makes him something of an anomaly in an industry where the path to the top almost always runs through audit rooms and tax preparation desks. But then again, CBIZ has never been a typical accounting firm.

Grisko spent eleven years at Baker and Hostetler, one of Cleveland's most prominent law firms, where he specialized in mergers, acquisitions, and divestitures. He was not a litigator or a regulatory specialist. He was a dealmaker, and that background proved decisive.

He joined Century Business Services in September 1998, right at the peak of the acquisition frenzy, as Vice President of Mergers and Acquisitions. He was the person screening deals, structuring transactions, and negotiating terms during the most intense period of acquisition activity in the company's history. Three months later, he was promoted to Senior Vice President. By February 2000, barely 18 months after arriving, he was named President and Chief Operating Officer.

That velocity of promotion, from outside hire to president in less than two years, is almost unheard of in professional services. It suggests the board recognized almost immediately that Grisko possessed something the company desperately needed: the ability to match acquisition ambition with operational discipline.

Grisko served as COO through the entire Steven Gerard turnaround era, which was the crucible that forged his management philosophy. He watched from the inside as 130 hastily acquired firms struggled to integrate. He saw the stock hit 81 cents. He lived through the agonizing process of selling underperforming units, shuttering redundant offices, and rebuilding credibility with a skeptical market.

Those years, from 2000 through 2016, taught him what works and what does not in professional services consolidation. When Gerard retired from the CEO role in March 2016, Grisko was the obvious and only successor. He has served as President and CEO since, presiding over the company's transformation from a loose, decentralized confederation of local firms into a genuinely integrated national platform.

His compensation structure reveals the alignment that long-term investors want to see.

Grisko's total compensation in 2023 was 5.21 million dollars, including a base salary of 943,750 dollars. The critical detail is the mix: approximately 82 percent of his compensation is variable, weighted toward stock awards, annual bonuses, and Performance Share Units tied strictly to EPS growth and successful M&A integration.

Only about 18 percent is fixed salary.

This structure makes it nearly impossible for Grisko to enrich himself through empire building alone. If the acquisitions do not translate into earnings growth, if the Marcum integration does not deliver, his compensation suffers accordingly.

The Performance Share Units are particularly well-designed because they vest based on multi-year EPS targets, not revenue targets. That distinction matters enormously: it means Grisko gets paid for profitable growth, not just growth. A CEO whose bonuses are tied to revenue could rationally pursue value-destructive acquisitions that boost the top line while destroying margins. A CEO whose bonuses are tied to EPS cannot.

Grisko directly owns roughly two percent of CBIZ's outstanding shares. At the stock's all-time high of approximately 90 dollars in February 2025, that stake was worth north of 65 million dollars. At current prices around 28 dollars, it is worth considerably less, which means Grisko is feeling the same pain as every other shareholder. This is the kind of management ownership that matters: not token stakes purchased with bonus money, but a meaningful concentration of personal wealth tied directly to long-term stock performance.

His strategic philosophy has been articulated with remarkable consistency across a decade of earnings calls: organic growth through cross-selling, selective acquisitions of high-quality firms, and relentless integration discipline. No bombast. No moonshot rhetoric. Just steady, compound, execute. On the Marcum deal, the biggest bet of his career, he was characteristically measured: "Now, with over 10,000 team members, we will offer clients an enhanced breadth of services and depth of expertise unmatched in our industries."

The other executive who demands attention is Peter Scavuzzo, who arrived at CBIZ not through recruitment but through acquisition. Scavuzzo was the Chief Information and Digital Officer at Marcum LLP and simultaneously served as CEO of Marcum Technology, the firm's managed IT subsidiary. He was not just a technology executive. He was the person who had built Marcum's technology practice from scratch, understanding both the technical infrastructure and the business model of selling managed IT services to middle-market clients.

Following the November 2024 closing, Scavuzzo was appointed to a newly created role: Senior Vice President, Chief Strategy Officer and National Leader of Technology. The title is a mouthful, but the mandate is clear. Scavuzzo is responsible for transformation, innovation, artificial intelligence, business intelligence, and analytics across the entire combined enterprise.

He holds a Master of Science from NYU's Polytechnic School of Engineering and brings more than 28 years of technology experience across professional services, manufacturing, and higher education. He has become CBIZ's chief public spokesman on artificial intelligence, "advising and sharing his knowledge and experience with client executives, professional associations, and industry peers," as the company describes it.

In September 2025, Scavuzzo led the launch of Vertical Vector AI, CBIZ's proprietary AI platform for middle-market businesses. His appointment was a deliberate signal that CBIZ intends to compete not just as an accounting firm, but as a technology-enabled professional services platform where tech leadership is as critical as tax leadership.

There is a broader point worth making about the management structure. In many roll-up companies, the CEO is a dealmaker first and an operator second. The incentive structure rewards closing transactions, not integrating them. The compensation committee pays for revenue growth, not earnings quality. CBIZ appears to have largely avoided this trap. Grisko's background as a dealmaker is balanced by his decades of operational experience. His compensation is tied to EPS, not revenue. And his personal stake in the company ensures that his interests and shareholders' interests are genuinely aligned.

The Grisko-Scavuzzo partnership represents a bet on the future of professional services: the disciplined operator paired with the technology architect. Whether that combination can navigate the post-Marcum integration while simultaneously building the technology infrastructure to compete with deep-pocketed PE-backed rivals is the central management question facing CBIZ.

VI. The "Hidden" Growth Engines Inside CBIZ

Here is the narrative most people get wrong about CBIZ: they think it is an accounting firm. It is not. Or rather, accounting is the front door, the relationship that gets CBIZ into the building. What happens after the door opens is where the real value creation occurs. CBIZ is better understood as a B2B services platform that uses accounting as its customer acquisition channel.

Think of it this way. A middle-market CEO, running a manufacturing company with 200 employees and 80 million dollars in revenue, needs someone to do the company's taxes. The CEO hires CBIZ. The engagement goes well. The CBIZ relationship partner, who has now spent months reviewing the company's financial statements, notices that the employee benefits plan is expensive, poorly structured, and administered by a small local broker who has not reviewed the plan design in years.

The partner introduces the company to CBIZ Benefits and Insurance Services. Six months later, CBIZ is administering the company's health plan, retirement plan, and property and casualty coverage. Then the CEO mentions a potential acquisition target. CBIZ's transaction advisory team steps in to perform due diligence. Then a ransomware scare prompts a cybersecurity assessment. CBIZ CompuData gets the call. Then someone asks about R&D tax credits. Then state and local tax planning. Then valuation services for estate planning.

This is the Trojan Horse model, and it is extraordinarily powerful. The CPA is the ultimate trusted advisor in middle-market America. The relationship is inherently intimate: the accountant sees everything. Every revenue line, every expense category, every compensation decision, every debt covenant. No other professional advisor has that level of financial transparency with a client. Once a CEO trusts you with that access, the cross-selling begins. And each additional service deepens the switching costs, making it progressively harder for a competitor to displace the relationship.

This is why CBIZ's client retention rate is approximately 90 percent: it is not that competitors are not trying to poach clients, it is that the entanglement of multi-service relationships makes switching genuinely painful.

CBIZ Benefits and Insurance Services is the massive, hidden gem that most investors overlook when they file CBIZ under "accounting firm" in their mental models. This segment generated 409.6 million dollars in revenue in 2025, providing employee benefits consulting and brokerage, property and casualty insurance, retirement plan advisory, payroll and human capital management, actuarial services, and group benefits administration. That is a substantial business in its own right, larger than many standalone insurance brokerages.

Critically, CBIZ does not assume underwriting risk. It does not write insurance policies or hold reserves against claims. It acts as an intermediary, earning commissions and advisory fees for placing coverage with carriers and consulting on plan design. This distinction matters enormously for the financial profile: the revenue is high-margin and largely recurring without the balance sheet risk and earnings volatility that insurance underwriters carry. When a hurricane hits Florida, Allstate takes a massive earnings hit. CBIZ does not. CBIZ might actually benefit, because storm damage drives demand for property and casualty advisory and claims consulting.

The segment also serves as a powerful counterbalance to the seasonality of the tax business. Tax revenue peaks heavily in the first and second quarters, tracking the annual filing deadlines in March and April. Benefits consulting revenue, by contrast, is more evenly distributed throughout the year, with its own peak around annual enrollment periods in the fourth quarter. This natural offset smooths CBIZ's overall revenue profile and cash flow characteristics in ways that a pure-play accounting firm simply cannot achieve.

The firm has won "Best Places to Work in Insurance" recognition for ten consecutive years. In a people business, the ability to recruit and retain top benefits consultants directly translates to client retention and revenue stability. Those consultants bring their books of business with them when they join, and their departure would mean client losses.

Managed IT and cybersecurity is the fastest-growing frontier, and this is where CBIZ's platform strategy gets genuinely interesting. Through acquisitions like CompuData in March 2024 and Pivot Point Security in 2023, CBIZ is building a technology services practice that answers a new mid-market reality.

The same companies that need annual audits and tax preparation also need someone to secure their cloud infrastructure, assess their cybersecurity posture, prepare for CMMC compliance, and manage their day-to-day IT environments. And here is the insight that makes this cross-sell so natural: the firm that already has access to all of your financial data, that already knows the intimate details of your business operations, is a uniquely trusted candidate to also manage your technology infrastructure. You would not hand the keys to your network to a stranger. But the firm that does your taxes is not a stranger.

CompuData, founded in 1971, brought five decades of experience as a technology solutions provider for small and mid-sized organizations. Its service stack includes cloud computing on Microsoft Azure, accounting and ERP software implementation as a Sage Diamond Partner, managed IT services, and a full cybersecurity suite including endpoint detection and response, SIEM solutions, and regulatory compliance consulting. The company's CMMC Registered Provider Organization certification positions it to serve clients with Department of Defense supply chain requirements, a growing and specialized niche.

Specialty tax and advisory practices represent the high-value apex of CBIZ's service pyramid. R&D tax credits, state and local tax consulting (known as SALT), valuation services, litigation support, and transaction advisory. These are the high-margin, specialized knowledge products that justify premium fee structures and that local CPA firms simply cannot replicate.

A three-partner CPA firm in Dayton, Ohio cannot maintain the depth of expertise needed to navigate a multi-state SALT analysis for a company with operations in 15 states, or structure an R&D credit study for a technology company, or provide expert witness testimony in a complex business valuation dispute. CBIZ can, because it spreads that specialized talent across a national client base of more than 100,000 businesses.

In September 2025, the technology ambition crystallized with the launch of Vertical Vector AI, a proprietary artificial intelligence platform designed specifically for middle-market businesses. Built under Peter Scavuzzo's leadership, the platform addresses the question every mid-market CFO is currently wrestling with: how do we capture the productivity benefits of AI without feeding our confidential financial data into a generic consumer tool?

Vertical Vector AI integrates with a company's own Microsoft Azure tenant, connecting directly to its proprietary datasets within existing security protocols and governance frameworks. Rather than sending sensitive financial data to a third-party AI service, the platform operates within the client's own cloud infrastructure. It includes a pre-built prompt library covering accounting, tax, HR, and compliance workflows, with Microsoft Teams integration for accessible deployment.

This is an important strategic move because it repositions CBIZ from pure service provider to technology partner, adding yet another layer of switching costs to an already sticky relationship. If your AI workflows, your automation templates, your compliance prompts are all built on a CBIZ platform integrated with your own cloud infrastructure, the cost of switching accounting firms just increased by an order of magnitude.

There is one more "hidden" business worth mentioning because it is genuinely unusual. CBIZ's National Practices segment, the smallest at roughly 47 million dollars in 2025 revenue, includes a managed networking and hardware services contract with a single large client under a cost-plus arrangement running through December 2028. It also historically included Myers and Stauffer LC, an independent national governmental healthcare consulting firm headquartered in Kansas City that operates under its own Administrative Services Agreement with CBIZ. In 2024, CBIZ sold CBIZ KA Consulting Services, a component of this group. The segment is small and declining, contracting six percent in 2025, but it illustrates the breadth of CBIZ's service tentacles and the variety of revenue streams flowing through the platform.

The combined picture is of a company that has built, piece by piece, a comprehensive B2B services platform that happens to have accounting as its entry point. Each additional service line deepens the client relationship, increases revenue per client, raises switching costs, and creates cross-selling opportunities that drive organic growth without requiring additional customer acquisition spend.

Consider the revenue composition: Financial Services accounted for 2.3 billion dollars or roughly 83 percent of 2025 revenue. Benefits and Insurance contributed 409.6 million dollars or about 15 percent. National Practices added the remaining 47 million. That Financial Services segment delivered same-unit revenue growth of 7.2 percent in the fourth quarter of 2024, with growth "from every major service line," as management reported. The overall revenue mix is approximately 72 percent recurring, providing extraordinary cash flow predictability compared to a project-based advisory firm.

In the language of platform economics, it is a flywheel. And it is the primary reason that CBIZ's business model is fundamentally different from a traditional accounting partnership.

VII. Playbook: Framework Analysis

To understand CBIZ's competitive position with analytical rigor, it helps to apply the frameworks that sophisticated investors use to evaluate business quality.

Switching Costs are the most important power in CBIZ's arsenal, and they deserve extended examination because they are the foundation on which the entire business model rests. In Hamilton Helmer's Seven Powers framework, switching costs create durable competitive advantage when the cost of changing suppliers is high enough relative to the value of the current offering that rational buyers will not switch even when presented with a marginally better or cheaper alternative.

CBIZ may be the most compelling example of compounding switching costs in all of professional services.

Consider a mid-market company that uses CBIZ for corporate tax compliance, payroll processing, employee benefits administration, property and casualty insurance, retirement plan management, and cybersecurity monitoring. To switch providers, that company would need to simultaneously replace six different service relationships.

It would need to migrate years of financial data, tax filing history, benefits enrollment records, and IT configurations. It would need to retrain internal teams on new systems, new reporting formats, new contact people, and new processes. And it would need to accept the risk that the transition period introduces errors in tax filings, gaps in insurance coverage, or security vulnerabilities in IT infrastructure.

Any one of those services alone might be switchable. All six together? The pain is immense.

And it grows with every additional service CBIZ provides. This is the strategic logic behind the cross-selling model: each new service is not just incremental revenue, it is another lock on the door.

Scale Economies, Helmer's second relevant power for CBIZ, operate at multiple levels. CBIZ spreads its centralized back-office infrastructure, national compliance systems, technology investments, and specialized talent across a revenue base approaching three billion dollars. The cost of maintaining a national tax research library, building a proprietary AI platform, operating offshore talent centers, or hiring specialists in niche areas like international tax treaty compliance is largely fixed. Each additional dollar of revenue generated against that fixed cost base drops disproportionately to the bottom line.

A regional five-partner CPA firm cannot amortize an AI platform across ten thousand clients. It cannot maintain a team of R&D tax credit specialists who serve clients across 30 states. It cannot invest in CMMC cybersecurity certification to serve defense contractors. CBIZ can do all of these things because scale converts fixed investments into competitive advantages.

Now turn to Porter's Five Forces, which assess the structural attractiveness of the industry itself.

Rivalry in CBIZ's competitive space is intense and layered, operating on at least three distinct levels.

At the top, the Big Four command the largest public company audits and advisory mandates at a scale that dwarfs CBIZ. Deloitte alone generates over 33 billion dollars in U.S. revenue. But the Big Four largely ignore the middle market. The compliance requirements, fee expectations, and service models are fundamentally different for a 50-million-dollar privately held manufacturer than for a Fortune 500 public company. CBIZ does not compete with the Big Four, and the Big Four have no interest in competing with CBIZ.

In the middle tier, firms like RSM, Baker Tilly, and BDO compete directly with CBIZ for the same middle-market clients. These are capable, well-managed firms with national footprints and strong reputations. But they are also facing the same consolidation pressures and talent challenges that CBIZ faces.

The real disruption is coming from the third tier: private equity. Grant Thornton sold a 60 percent stake to New Mountain Capital in 2024. CohnReznick secured a minority investment from Apax Partners in early 2025, adopting an APS structure similar to the one CBIZ pioneered. Citrin Cooperman completed a PE-to-PE ownership transfer with Blackstone at a reported two-billion-dollar valuation. Wipfli secured its own New Mountain Capital investment in August 2025.

By one estimate, roughly 147 deals between 2020 and 2025 created approximately 200 billion dollars in new enterprise value in the accounting sector. One-third of the top 30 U.S. accounting firms now have private equity backing. These PE-backed competitors deploy capital at scale, build technology platforms aggressively, and recruit talent with the promise of liquidity events that traditional partnerships cannot offer.

There is an irony worth noting: the APS structure that CBIZ pioneered in 1998 is essentially the same regulatory architecture that PE-backed firms are now adopting. CBIZ has been doing this for 25 years. But the PE-backed competitors have access to essentially unlimited capital, and in a people business, capital can be deployed through guaranteed compensation packages and equity participation that a publicly traded company may find difficult to match.

The threat of substitutes, particularly from AI and automation, deserves nuanced treatment. Tax preparation software, automated bookkeeping tools, and AI-powered compliance platforms are genuinely capable of handling routine, low-complexity work that once required human accountants. For a small firm dependent on basic tax return preparation, this is an existential threat.

But for a firm like CBIZ, the dynamics cut differently. Think about what AI does well: pattern matching, data extraction, calculation, document processing, rules-based analysis. These are exactly the tasks that make up the low-margin, high-volume compliance work. If AI handles routine data entry and basic return preparation, freeing human professionals for high-value advisory, complex tax planning, and strategic consulting, the net effect could be margin expansion rather than revenue loss.

CBIZ's launch of Vertical Vector AI suggests management views artificial intelligence as a competitive weapon. The firms with scale to invest in AI infrastructure will widen their advantage over smaller competitors who lack the resources.

There is a useful analogy here. When ATMs were introduced in the 1970s, many predicted they would destroy bank branch employment. Instead, ATMs reduced the cost per branch, which allowed banks to open more branches, which increased total banking employment. The technology automated the routine transaction work, freeing branch employees to focus on higher-value activities like mortgage origination and wealth management. AI may do for accounting what ATMs did for banking: automate the routine, expand the addressable market, and shift the workforce toward higher-value advisory services. If that analogy holds, firms with the scale to invest in AI, like CBIZ, will be the biggest beneficiaries.

The threat of new entrants is moderate and evolving. The APS structure that CBIZ pioneered is no longer proprietary knowledge. PE-backed firms are adopting the same regulatory architecture, and new entrants with deep capital reserves are entering the market. However, the barriers to building a truly integrated, national, multi-service platform remain substantial. It took CBIZ 25 years and over 120 acquisitions to get where it is. A PE-backed firm starting from scratch, or even starting from a top-20 accounting platform, faces years of integration work before it can offer the cross-selling density that CBIZ has built.

Supplier power in professional services is essentially the power of labor. Accountants, tax specialists, benefits consultants, and cybersecurity professionals are the "suppliers" in this framework, and their bargaining power is increasing. The accounting profession faces a well-documented talent shortage: fewer students are entering the CPA pipeline, and the 150-hour education requirement for CPA licensure has been a persistent barrier to entry. This labor scarcity is a structural challenge for the entire industry, but it disproportionately hurts small firms that cannot match the compensation, benefits, career development, and geographic flexibility that a national platform like CBIZ can offer.

Buyer power in CBIZ's market is remarkably low. Regulatory complexity is increasing, not decreasing. The U.S. tax code grows more intricate with every legislative cycle. Cybersecurity compliance requirements multiply annually. Employee benefits regulation demands specialized expertise that most mid-market companies cannot build in-house. These companies are forced buyers of professional services. They cannot choose not to file taxes or comply with audit requirements. This is a structural tailwind that shows no sign of abating.

For investors tracking CBIZ's ongoing performance, two key performance indicators matter above all others. First, organic revenue growth: the rate at which CBIZ grows its revenue excluding acquisitions. This isolates the underlying health of the business. Is CBIZ winning new clients, expanding relationships with existing ones, and retaining its talent? The company historically targeted five to seven percent. The two percent achieved in 2025 was a meaningful shortfall.

Second, same-unit revenue growth: revenue growth at offices and practices that have been part of CBIZ for at least twelve months. This strips out both acquisitions and divestitures, revealing the true operating momentum of the existing business. These two numbers, more than any financial engineering or acquisition multiple, will determine whether CBIZ creates or destroys value over the next decade.

VIII. Bear vs. Bull Case

The case against CBIZ starts with the most immediate and visceral risk: integration indigestion.

The Marcum deal was not a routine tuck-in. It was the combination of two similarly sized national organizations, each with deeply embedded cultures, established hierarchies, different technology platforms, and overlapping geographic footprints. In the annals of professional services M&A, deals of this magnitude have a sobering track record. The Deloitte-Touche merger in 1989, the Price Waterhouse-Coopers and Lybrand combination in 1998, and the failed Ernst and Young-KPMG merger attempt were all defined by the difficulty of merging partnership cultures where individual partners have enormous autonomy and strong personal client relationships.

Professional services mergers fail in a specific way: talented professionals, feeling displaced or undervalued in the combined entity, leave. And they do not leave quietly. They leave with their client relationships, which in professional services is the equivalent of walking out with the factory.

The first full year of Marcum integration offered uncomfortable evidence that this risk is not hypothetical. Organic revenue growth came in at approximately two percent. Management's 2026 guidance of two to five percent is cautious at best. Integration costs of 70 to 80 million dollars are expected to continue through 2026.

The balance sheet carries approximately 1.4 billion dollars in acquisition-related debt, financed through a new two-billion-dollar credit facility established to fund the Marcum transaction. That leverage, while manageable in a stable revenue environment, constrains CBIZ's strategic flexibility.

The company cannot simultaneously service significant debt, fund ongoing integration costs, pursue additional meaningful acquisitions, and return substantial capital to shareholders. Something has to give.

The competitive landscape has also shifted in ways that undermine CBIZ's historical advantage. For years, the company executed a classic multiple arbitrage: buying firms cheaply and having those earnings valued at a public market premium. But private equity's entry into accounting has driven up acquisition multiples across the board. When PE firms pay upwards of twelve times EBITDA for top-tier practices, CBIZ's ability to buy at four to six times evaporates. The easy arbitrage that powered decades of value creation may be structurally impaired.

Then there is the AI substitution risk. The consensus view is that AI will automate low-value compliance work and free professionals for high-value advisory. That is probably directionally correct. But there is a scenario worth considering: what if AI-powered compliance tools become good enough that mid-market companies can handle routine tax and accounting functions in-house? In that scenario, the "trusted advisor" relationship that drives CBIZ's entire cross-selling model never forms in the first place. The entry point that leads to benefits, insurance, cybersecurity, and advisory engagements simply does not exist. This is a tail risk, not a base case, but it is worth flagging because the entire business model depends on that initial accounting relationship as the gateway to everything else.

Now for the bull case, which rests on structural advantages that are genuinely difficult to replicate.

CBIZ remains the premier public pure-play in the accounting and professional services space. There is literally no other way for public market investors to gain direct, concentrated exposure to this enormous, sticky, recession-resistant industry without buying a private partnership or investing in a PE fund. That scarcity has real value. When the market last appreciated this scarcity, in February 2025, CBZ traded above 90 dollars. The question is not whether scarcity value exists, but when the market will again be willing to pay for it.

The free cash flow story is genuinely compelling. Management guided for 270 to 290 million dollars of free cash flow in 2026. At the company's current market capitalization of approximately 1.5 billion dollars, that implies a free cash flow yield of roughly 18 percent.

For context, the S&P 500 averages a free cash flow yield of approximately four percent. CBIZ is trading at nearly five times the market's average free cash flow yield.

That gap implies the market is pricing in substantial downside risk: the possibility that the Marcum integration fails, organic growth stalls permanently, or the competitive environment worsens materially. If even some of that risk proves overstated, if organic growth recovers to four or five percent and the balance sheet begins to delever, the current valuation could prove to be a significant opportunity for patient investors willing to look past the near-term integration noise.

The cross-selling density argument is perhaps the most powerful element of the bull case.

The Marcum combination created unprecedented depth in key metropolitan markets, particularly New York City, where the combined entity now possesses the scale to compete for engagements that neither firm could have won independently.

The "one firm" model, where a single relationship partner offers a mid-market CEO access to tax, audit, benefits, cybersecurity, AI, and advisory services under one roof, is a value proposition that no local CPA firm can match in breadth and no Big Four firm is willing to offer at the middle-market price point.

If the integration succeeds in enabling genuine cross-selling, each Marcum client becomes an opportunity for three, four, or five additional CBIZ service relationships. The integration math on the cost side is already proving out: 35 million dollars of 2025 synergies against an initial estimate of 17 to 18 million. The revenue synergy story, which takes longer to develop, is the next chapter.

As AI automates the low-margin compliance work, CBIZ's high-margin advisory, benefits, and insurance segments could emerge as even larger proportions of the revenue mix. The benefits and insurance business alone generates over 400 million dollars in annual revenue at margins well above the company average. If the advisory and technology segments follow the same trajectory, CBIZ could evolve from a mid-teens return business into a genuinely high-return platform.

The key advantage CBIZ holds over PE-backed competitors is durability, and this point deserves emphasis because it may be the single most underappreciated aspect of the CBIZ story.

Private equity operates on fund timelines, typically five to seven years. When a PE firm acquires a 60 percent stake in an accounting firm, it does so with the expectation of generating a return within that window, usually through revenue growth, margin expansion, and a sale to the next buyer at a higher multiple. This creates pressure to grow fast, integrate fast, and exit fast. It also means that during economic downturns, when organic growth slows and exit multiples compress, the PE-backed firm faces conflicting pressures: the fund needs to return capital, but the market conditions do not support an exit at the target valuation.

CBIZ has no exit horizon. It has been building this platform for 25 years and can continue compounding indefinitely. When the next recession comes, and PE-backed accounting firms face pressure to deliver returns to their limited partners on schedule, CBIZ can simply keep doing what it has been doing: serving clients, retaining talent, and acquiring distressed practices at favorable prices. Recessions have historically been excellent buying opportunities for well-capitalized roll-up operators, and CBIZ has the institutional patience and structural permanence to take advantage.

History teaches that consolidation waves in professional services tend to overheat, then collapse. American Express and H&R Block tried to roll up accounting in the 1990s and failed. CBIZ survived where they did not. Whether the PE-backed wave of the 2020s will produce durable enterprises or follow the same arc remains the industry's central unanswered question. But CBIZ's quarter-century track record of surviving, adapting, and ultimately thriving through competitive cycles is a data point that deserves weight.

IX. Epilogue and Future Outlook

In the spring of 2026, CBIZ stands at a genuine inflection point.

The largest acquisition in the company's history has been completed. The combined organization operates on unified systems. Integration synergies are exceeding initial projections. And 2026 free cash flow guidance of 270 to 290 million dollars suggests the underlying economics of the business remain strong.

But the stock price, having declined roughly 63 percent from its all-time high to around 28 dollars, tells a story of market skepticism that management has not yet overcome.

The skepticism is not unreasonable. Organic growth of two percent was a disappointment. The 2026 guidance of two to five percent is cautious. The competitive landscape, with PE-backed firms aggressively recruiting talent and bidding up acquisition targets, is more challenging than at any point in CBIZ's history.

But zoom out, and the structural picture tells a different story.

The accounting and professional services industry in the United States is undergoing its most significant transformation in a generation. The traditional partnership model, which governed the profession for over a century, is giving way to a new reality of institutional capital, technology investment, and national scale.

CBIZ was the first mover in this transformation, pioneering the Alternative Practice Structure in 1998 and building a national platform through disciplined acquisition while its competitors were still debating whether outside capital was appropriate for the profession.

Management has outlined four strategic priorities for 2026: talent attraction and retention, national brand elevation, industry specialization with particular emphasis on construction where CBIZ now ranks number one nationally, and cross-selling the enhanced service depth created by the Marcum combination.

The talent question looms particularly large. The accounting profession faces a well-documented pipeline crisis. The number of students sitting for the CPA exam has declined steadily for years, and the 150-credit-hour education requirement for licensure has been widely criticized as a barrier to entry that discourages talented graduates from pursuing the profession.

For CBIZ, this creates both risk and opportunity. The risk is obvious: if there are not enough qualified professionals entering the pipeline, growth is constrained regardless of how many acquisition targets are available.

The opportunity is more subtle: in a tight labor market, the firms that can offer the best compensation, the best technology tools, the best career development paths, and the most interesting client work will attract the best talent. A national platform with three billion dollars in revenue, AI-enabled workflows, and a diverse array of service lines across multiple geographies is inherently more attractive to ambitious young professionals than a three-partner local firm.

Scale begets talent. Talent begets growth. Growth begets scale.

This virtuous cycle, if CBIZ can sustain it, could prove to be the company's most durable competitive advantage in the decade ahead. The firms that attract the best people will serve clients best, which will generate the highest margins, which will fund the most investment in technology and talent, which will attract the next generation of professionals. The question is whether CBIZ, burdened by integration complexity and a compressed stock price, can maintain the momentum needed to keep this flywheel spinning.

The transition from "accountants" to "AI-enabled strategic advisors" is the company's long-term vision. Vertical Vector AI, the technology investments, the cybersecurity practice, and the specialty advisory capabilities are all steps along that path.

Whether the execution matches the ambition, in a landscape more competitive and fast-moving than any CBIZ has previously faced, remains to be seen. But the raw materials are in place: a national platform with unmatched scale in the middle market, a management team with skin in the game, a regulatory architecture proven over 25 years, and a client base of more than 100,000 businesses whose needs for professional services are only growing more complex.

From hazardous waste to accounting. From 81 cents a share to 90 dollars. From a chaotic conglomerate of 130 hastily acquired firms to a disciplined national platform with three billion dollars in revenue and ten thousand professionals. The genius of applying a ruthless roll-up model to a historically fragmented, localized, and highly regulated industry has been demonstrated across nearly four decades of corporate reinvention. The next chapter will determine whether that genius can compound through the most competitive environment the industry has ever faced.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube