Chubb: From Marine Underwriters to Global Insurance Powerhouse

I. Introduction & Cold Open

Picture this: Two insurance companies, born in different centuries—one in the era of steamships and telegraphs, the other in the age of corporate jets and fax machines—collide in a $29.5 billion merger that reshapes the global insurance landscape. It's a cloudy morning in Warren, New Jersey, just weeks after the merger announcement. Evan Greenberg, the sinewy, shaven-skulled, 60-year-old executive, stands in the four-story atrium lobby at Chubb's headquarters, looking up at unsmiling employees who lean over the railings to hear from their new boss. "This is like giving a speech in the Roman Colosseum," he tells his audience. "I hope there's no lions and that you don't choose to throw anything at me." Nervous giggles cascade down.

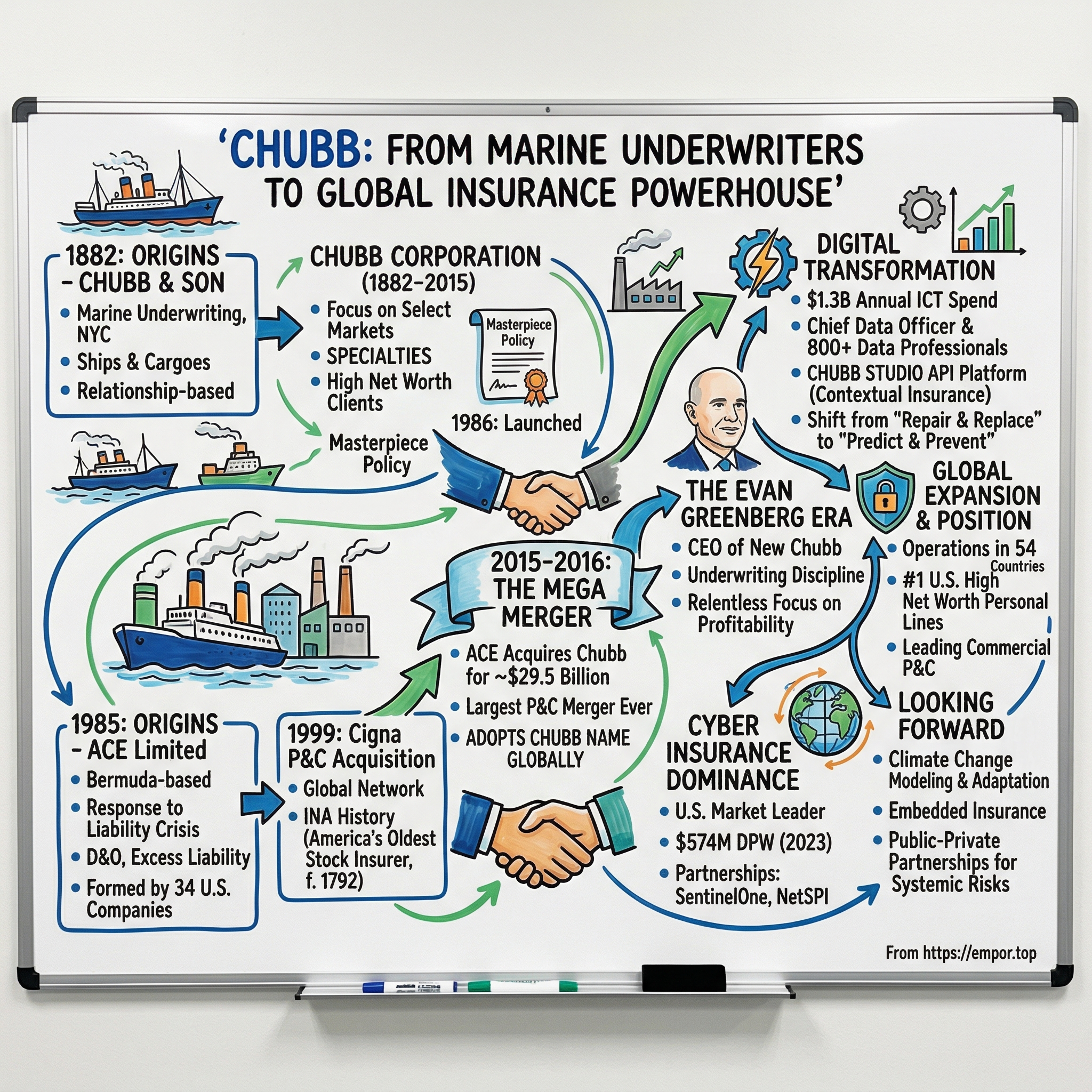

The paradox is striking. ACE Limited was established in 1985 in response to the U.S. liability insurance crisis of the mid-1980s, formed with the assistance of insurance broker Marsh & McLennan and funded by a group of 34 U.S. companies seeking difficult-to-obtain Excess Liability and Directors and Officers (D&O) insurance coverage. Meanwhile, Thomas Caldecot Chubb and his son Percy started a marine underwriting business in New York City in 1882, collecting $1,000 from 100 prominent merchants to focus on insuring ships and cargoes.

How did these two companies—one a Depression-era survivor built on maritime tradition, the other a Bermuda-born crisis solution—become a single entity? The combined company now stands as the world's largest publicly traded property and casualty insurer, with operations spanning 54 countries and assets exceeding $150 billion.

This isn't just another corporate merger story. It's about how crisis breeds opportunity, how legacy brands carry hidden value, and how an industry once dismissed as stodgy became the battleground for digital transformation and risk innovation. As Greenberg told the assembled Chubb employees that day, "I don't know any other way to show respect to somebody to begin with than to say we're going to take your name."

II. The Tale of Two Origins

The Chubb Story (1882-2015)

The year 1882 marked more than just the founding of an insurance company—it was the beginning of a philosophy that would endure for over a century. Having collected $1,000 from each of 100 prominent merchants to start their venture, Thomas Caldecot Chubb and his son Percy focused initially on insuring ships and cargoes. The Chubbs were adept at turning risk into success, often by helping their policyholders prevent disasters before they occurred. By the turn of the century, Chubb had established strong relationships with the insurance agents and brokers who placed their clients' business with Chubb underwriters.

The company's character was perhaps best articulated by Hendon Chubb, who joined his older brother Percy in 1895. Chubb & Son did not value size in itself but regarded it as a measure of what had been achieved. Upon the Company's 75th anniversary in 1957, Hendon Chubb noted, "I think there is perhaps a tendency in American business to overemphasize mere size, whereas to me it should be a by-product of a job well done."

By the mid-1970s, Chubb faced several challenging years that would ultimately define its modern identity. In 1976, Chubb responded to several years of business challenges by developing its successful focus on select markets, specialties, and—in personal lines—explicitly serving the high net worth client. This strategic pivot would culminate in what became their signature offering. In 1986, Chubb launched the famed Masterpiece personal lines policy, becoming the company's definitive high net worth product.

The Masterpiece policy was revolutionary for its time—offering extended replacement cost coverage, cash settlement options, and agreed value provisions that standard insurers wouldn't touch. It became the gold standard for insuring the homes, art collections, and automobiles of America's affluent families.

The ACE Story (1985-2015)

While Chubb was reinventing itself for the high net worth market, a different drama was unfolding in Bermuda. The mid-1980s liability insurance crisis had left corporate America scrambling for coverage. Directors and officers couldn't find insurance. Excess liability coverage had virtually disappeared from the market.

In 1984, Marsh President Robert Clements foresaw a potential excess liability crisis and had an idea to fill the void: American Casualty Excess - ACE. The solution came in the form of an unprecedented collaboration: 34 blue-chip American companies—from healthcare and pharmaceuticals to oil and gas, banking, and automotive—pooled resources to create their own insurance company.

ACE Limited was established in 1985 in response to an availability crisis in the U.S. From its inception through the 1990s, ACE grew rapidly through product diversification, strategic partnerships and acquisition.

The real transformation came in 1999. A true turning point for ACE was its 1999 acquisition of Cigna Corporation's international and domestic property and casualty business, the Insurance Company of North America (INA). The acquisition gave ACE an instant global network and simultaneously transferred INA's 200-year history to the company. INA wasn't just any acquisition—it was America's oldest stock insurance company, founded in 1792 at Independence Hall in Philadelphia, bringing with it centuries of underwriting expertise and relationships.

In the following decade and beyond, ACE progressed on its path of growth and international expansion organically and via strategic acquisition. During that time, ACE fostered its reputation as a superior underwriting company that delivered exceptional service through an unparalleled global network.

III. The Evan Greenberg Era Begins

The appointment of Evan Greenberg as ACE's CEO in 2004 marked not just a leadership change but a philosophical transformation. His arrival at ACE carried the weight of insurance royalty and family drama. Evan G. Greenberg (born April 1, 1955) is an American business executive. Greenberg is the son of Corinne Phyllis Zuckerman and Maurice R. Greenberg, the former chairman and CEO of American International Group (AIG). He is also the younger brother of Jeffrey W. Greenberg, the former CEO of Marsh & McLennan.

Greenberg's path to insurance leadership was unconventional. After graduating high school at 17, Greenberg traveled the country working odd jobs, including cooking at a nursing home and bartending. He later attended New York University and the College of Insurance but did not graduate from either.

In 1975, Greenberg started working in insurance, initially working for New Hampshire Insurance Co. in its automobile policies department. He began working for AIG later that year as an underwriter. During the 25 years he worked for AIG, Greenberg held a number of senior management positions. He ran AIG's Japan and Korea operations from 1991 to 1994, then oversaw all international property-casualty operations from New York.

Greenberg was named president and COO in 1997 and was considered the heir apparent to take over as CEO of AIG. Despite Greenberg being in line to take over the company, he left his position as president in September 2000. He spent a year away from work to spend time with his family.

The timing of his return to insurance proved fateful. After seeing the impact of the September 11 attacks on the insurance industry, with insurers affected by large claims, Greenberg decided to take the opportunity to accept then-ACE CEO Brian Duperreault's offer to join ACE. Greenberg joined ACE in November 2001 to lead the company's overseas unit.

The terrorist assault led to a huge withdrawal of global insurance capacity. But ACE, incorporated in the Cayman Islands with headquarters in Bermuda, had just raised more than $1 billion to deploy. "So when 9/11 happened, I called Evan again and said, 'We have a once-in-a-lifetime opportunity, and I'd hate to have you miss it,'" recalls Duperreault, now CEO of Bermuda-based Hamilton Insurance Group.

Greenberg quickly dispelled any concerns that he might treat ACE as a huge step down from AIG. "He didn't act like he had been No. 2 at the world's greatest insurance company," Duperreault says. "He put his head down and worked hard, which is what I hoped he would do, because I saw in him somebody who could take ACE to the next level."

In June 2003, he was promoted to president and chief operating officer, and in May 2004, was named CEO. In May 2007, he was elected Chairman of ACE. Following his promotion to CEO, Greenberg grew the company both through expansion of existing operations and through a strategy of acquisitions, acquiring 15 companies by 2015.

The Greenberg era at ACE was defined by disciplined underwriting, strategic acquisitions, and a relentless focus on profitability over market share. A primary focus of Greenberg's is the art and science of underwriting. "This is a company of underwriters," Greenberg said when asked about some of the keys to ACE's success. "We are managed by underwriters. All of senior leadership has a very strong underwriting background."

IV. The 2008 Financial Crisis: Dodging the AIG Bullet

The 2008 financial crisis served as the ultimate stress test for the insurance industry, and no company's collapse was more spectacular—or more personal for Evan Greenberg—than that of AIG.

The collapse and near-failure of insurance giant American International Group (AIG) was a major moment in the recent financial crisis. AIG, a global company with about $1 trillion in assets prior to the crisis, lost $99.2 billion in 2008. On September 16 of that year, the Federal Reserve Bank of New York stepped in with an $85 billion loan to keep the failing company from going under.

The scale of AIG's implosion was staggering. AIG had sold credit protection through its London unit in the form of credit default swaps (CDSs) on collateralized debt obligations (CDOs) but by 2008, they had declined in value. AIG's Financial Products division, headed by Joseph Cassano in London, had entered into credit default swaps to insure $441 billion worth of securities originally rated AAA. Of those securities, $57.8 billion were structured debt securities backed by subprime loans. As a result, AIG's credit rating was downgraded and it was required to post additional collateral with its trading counter-parties, leading to a liquidity crisis that began on September 16, 2008, and essentially bankrupted all of AIG.

While AIG burned through taxpayer billions, both Chubb and ACE emerged from the crisis relatively unscathed. Neither company had ventured into the exotic derivatives and mortgage-backed securities that brought down AIG. Their conservative underwriting philosophy—what some had criticized as being too cautious during the boom years—suddenly looked prescient.

In the 2008 financial crisis, Greenberg opposed taxpayer-funded bailouts for the insurance industry. He gave a statement on behalf of the American Insurance Association as its then-chairman, noting that most of the association's members were not in favor of including property and casualty insurers in the list of companies able to make use of available federal bailout funds.

The contrast was stark: AIG required a $182 billion government bailout and became a symbol of Wall Street excess. Meanwhile, ACE and Chubb maintained their underwriting discipline, avoided the mortgage securities trap, and positioned themselves to capitalize on the post-crisis consolidation opportunities.

For Evan Greenberg, watching his father's former company implode must have been both vindication and tragedy. Maurice "Hank" Greenberg had been forced out of AIG in 2005 amid accounting scandals. The son who had left AIG in 2000, passed over for the top job, was now running a competitor that had avoided the catastrophic mistakes that nearly destroyed the company his father had built.

The crisis fundamentally reshaped the insurance landscape. Companies that had seemed invincible were suddenly vulnerable. The reputation damage to the industry was severe, but it also created opportunities for well-capitalized, conservatively managed insurers. ACE and Chubb were perfectly positioned for what came next.

V. The Deal of the Century: ACE Acquires Chubb (2015-2016)

The insurance world was stunned on July 1, 2015. Following the acquisition announcement on July 1, 2015, both ACE and Chubb engaged in extensive integration planning. In July 2015, Greenberg led a deal for ACE to acquire the insurance company Chubb for $28.3 billion, which was the largest merger deal in property and casualty insurance history.

The human element added drama to the deal. Shortly prior to the deal, he broke his ankle in a horse riding accident, and he worked on the merger while recovering. Greenberg, conducting negotiations from his recovery bed, orchestrated what would become the defining transaction of his career.

ACE paid approximately $29.5 billion in the aggregate in cash and stock, based on the most recent closing price of ACE Limited shares and the number of outstanding shares of The Chubb Corporation common stock at the time of closing. Upon completion, ACE shareholders held 70% while Chubb shareholders got 30% of the new combined company.

The strategic rationale was compelling. On a pro forma basis, the company has market capitalization of $51.2 billion, annual gross written premiums of $37 billion and total assets of approximately $150 billion. Chubb operates in 54 countries and is a leader in industrial commercial and specialty P&C globally, professional lines globally, and U.S. middle market commercial P&C. The company is the #1 provider of personal P&C insurance and risk services to U.S. high net worth individuals and families and is a global leader in personal accident and supplemental health insurance.

But the most surprising aspect of the deal was what happened to the company name. Effective immediately, ACE is adopting the Chubb name globally and the company will begin trading tomorrow on the New York Stock Exchange under the symbol "CB."

The reasoning was both strategic and deeply respectful. When asked why ACE bought Chubb but used the name Chubb rather than ACE, Greenberg explained: "Because the name ACE is a name that I was looking to change. [Laughter.] It was a—it is a non-distinctive name. There's ACE Tree Company, ACE Hardware, who I thought we might do joint marketing with. There is—there is ACE Food Company. There's ACE everything. Nothing distinctive about that."

The deal received ACE and Chubb shareholder approval and all required regulatory approval, and closed on 14 January 2016. When the deal became official in January 2016, ACE adopted the Chubb name globally and Greenberg became chairman and CEO of Chubb.

The integration was remarkably smooth, aided by careful planning and cultural alignment. On the craft of insurance, "The three core truths about the new Chubb—superior underwriting, superior service and superior execution—are our North Star. Together what they say to us is superior craftsmanship. When well-managed, insurance is a precise, demanding and human craft. As craftspeople, we conceive, craft and deliver extraordinary insurance coverage and service that our customers deserve."

VI. Digital Transformation: Old Dog, New Tricks

In an era when Silicon Valley startups promised to "disrupt" every traditional industry, Chubb's response was neither panic nor denial—it was systematic transformation backed by massive investment.

The numbers tell the story of commitment. The annual ICT spending of Chubb was estimated at $1.3 billion in 2023. This isn't a company dabbling in technology; it's making a generational bet on digital capabilities.

Chubb has not hired a generic IT manager; it has placed a technologist with foundational, academic training in AI at the helm of its entire global engineering organization, responsible for software, infrastructure, cloud, cybersecurity, and corporate systems. The company appointed a Chief Data Officer with an elite pedigree—his resume includes roles as Group Chief Data Officer for HSBC, Chief Data Officer for Santander UK, and SVP and CIO of Enterprise Business Intelligence and Analytics at competitor Travelers. He now leads a formidable team of approximately 800 data professionals at Chubb, spanning data engineering, management, science, privacy, and architecture.

The transformation goes beyond hiring. In early 2023, Chubb announced the launch of a new technology services hub in Thessaloniki, Greece, which joins its other major development centers in the United States, India, and Mexico. The mission of the Thessaloniki center is explicit: to deliver innovative technologies that "enhance customer experience, increase efficiency, and accelerate the company's digital transformation." The experts at this hub are tasked with leading initiatives in precisely the areas required for AI leadership: intelligent process automation, machine learning, cloud infrastructure, data analytics, and cybersecurity.

The company's Chubb Studio platform exemplifies this digital-first approach. Chubb has developed a platform called Chubb Studio that enables it to provide API technologies to connect with partners in record time. By embedding Chubb products in the partner's ecosystem, the company is able to deliver contextual insurance offerings to customers seamlessly. To date, more than 19 million policies have been sold across the offer spectrum through Chubb Studio.

According to Lazaro, the technology has provided Chubb with a competitive advantage over other industry players. "It's a cloud-based, easy-to-use API platform that fuels our businesses and partnerships while helping us to connect with our digital distribution partners. We can create products within their platforms in a very easy and fast manner, pulling our digital underwriting, claims and service capabilities together into one place."

The practical applications are striking. Chubb is tapping the power of data analytics to analyze data and generate insights. It analyzes real-time data of insured property captured by IoT sensors, deriving insights that can help it predict threats and take action to minimize losses. The company has reduced small business underwriting questions from 30 to just 7 through intelligent data scraping—a dramatic simplification that improves customer experience while maintaining underwriting quality.

But perhaps most importantly, Greenberg sees this not as a defensive move against InsurTech startups, but as a fundamental evolution of what insurance is. As he puts it: "Chubb is an underwriting company. Chubb in the future is an underwriting and engineering company." The shift from "repair and replace" to "predict and prevent" represents a philosophical transformation as significant as any in the company's history.

The silver lining of COVID-19 is that it has forced every industry to an accelerated digital transformation. It has brought into focus the importance of operational capabilities to distribute products digitally through other channels, including ecosystem integration with other industries. For Chubb, the pandemic didn't create the digital strategy—it accelerated one already in motion.

VII. The Cyber Insurance Dominance Play

If there's one market that exemplifies Chubb's ability to turn emerging risks into profitable business lines, it's cyber insurance. Chubb Cyber Insurance is a market leader in cyber insurance, offering insurance coverage for data breaches, network security, and other cyber risks, for over 20 years.

The numbers validate the dominance. Global insurer Chubb remains the largest writer of cyber insurance in the US, with direct premiums written (DPW) in 2023 amounting to roughly $574 million, according to AM Best. In 2023, the market leader of the cyber security insurance sector in the United States was Chubb Ltd and the top 20 insurers accounted for nearly 76 percent of the U.S.

This leadership position didn't happen by accident. Chubb entered the cyber insurance market when most insurers still viewed cyber risk as too uncertain to underwrite profitably. The company built expertise gradually, learning from each breach, each claim, and each recovery. Today, that two-decade head start has created a formidable moat.

The market opportunity ahead is staggering. The Global Cyber Insurance Market size is expected to be worth around USD 90.6 Billion By 2033, from USD 12.1 Billion in 2023, growing at a CAGR of 22.3% during the forecast period from 2024 to 2033. The drivers are obvious: increasing cyber threats, stricter data protection regulations, and growing digital transformation across all industries.

Chubb's approach goes beyond simply offering policies. Chubb is collaborating with SentinelOne (NYSE: S), a leader in cybersecurity, to streamline cyber risk management practices for U.S. businesses. As part of the first phase of this collaboration, Chubb's cyber insurance policyholders with over $100 million in revenue will have the ability to share their enterprise "health assessment or security posture" data with Chubb through SentinelOne's endpoint protection and automated incident response solutions. This includes SentinelOne's WatchTower Vital Signs Report app, which securely communicates an accurate profile of a policyholder's cybersecurity posture and controls to Chubb to help streamline underwriting processes.

The company has also partnered with NetSPI for penetration testing solutions, creating an ecosystem approach to cyber risk that combines insurance with active risk mitigation. This isn't just about paying claims after breaches—it's about preventing them in the first place.

95% of Fortune 1000 companies are Chubb insured. When virtually every major corporation trusts you with their cyber risk, you're not just writing policies—you're seeing patterns, understanding threats, and building predictive models that smaller competitors simply cannot match.

The cyber insurance market also demonstrates Chubb's pricing discipline. While many insurers rushed into cyber during the hard market of 2020-2022, writing policies at any price, Chubb maintained its underwriting standards. As the market softens, those who chased growth are now facing loss ratios that threaten their programs' viability. Chubb, with its patient capital and long-term view, can weather cycles that destroy weaker competitors.

VIII. Global Expansion & Market Position Today

Today's Chubb operates at a scale that would have been unimaginable to either company's founders. The company serves customers in 54 countries, employs over 30,000 people, and has become the definition of a global insurance powerhouse.

The company's market position is formidable across multiple segments. It maintains leadership in industrial commercial and specialty P&C globally, professional lines globally, and U.S. middle market commercial P&C. In the high net worth personal lines space—the business Chubb pioneered with its Masterpiece policy—the company remains the undisputed #1 provider in the United States.

The financial performance reflects this market strength. Chubb Ltd reported a Q3 net income of $2.32 billion, or $5.70 per share, reflecting a 13.8% increase from the previous year. Core operating income was also up by 14.3%, reaching $2.33 billion, or $5.72 per share. Chubb's Q3 underwriting income increased by 11.7%, reaching $1.46 billion, while its net investment income reached a record $1.51 billion, up 14.7%. The return on equity (ROE) stood at an impressive 14.7%, indicating efficient capital utilization.

Geographic diversification has become a key strategic advantage. While North America remains the largest market, the company's international operations provide both growth opportunities and natural hedging against regional economic cycles. Asia-Pacific, in particular, represents a significant growth frontier, with rising middle-class wealth creating demand for both commercial and personal lines coverage.

The company's approach to climate risk exemplifies its evolution from pure risk-taker to risk partner. Rather than simply avoiding climate-exposed risks, Chubb has developed sophisticated modeling capabilities to price climate risk accurately while working with clients on adaptation and resilience strategies. The company's Climate+ initiative brings together renewable energy underwriting, alternative fuels coverage, and climate tech insurance—turning the energy transition into a business opportunity.

Product innovation continues across all lines. In cyber, the company has developed coverage for widespread cyber catastrophes. In personal lines, the Masterpiece product continues to evolve with coverage for digital assets, identity theft, and reputation management. In commercial lines, the company has pioneered coverage for emerging risks from autonomous vehicles to space tourism.

By 2021, Greenberg was credited in the media for having grown Chubb to the second-largest publicly listed insurance company in the U.S. and the largest non-injury insurer in the U.S. based on market value.

IX. Porter's 5 Forces Analysis

1. Threat of New Entrants: MODERATE

The insurance industry's barriers to entry remain substantial but not insurmountable. Capital requirements are significant—new entrants need hundreds of millions in capital to meet regulatory requirements and rating agency standards. The regulatory framework itself acts as a moat, with licensing requirements in each state and country creating complexity that favors incumbents.

However, InsurTech companies have found ways to enter through partnerships with existing carriers, acting as managing general agents (MGAs) or fronting arrangements. Companies like Lemonade, Root, and Hippo have raised billions in venture capital to attack specific niches. Yet their combined market share remains minimal compared to established players, and many are struggling to achieve profitability.

For Chubb, the threat is less about direct competition and more about cherry-picking. InsurTechs target the simplest, most commoditized risks—renters insurance, basic auto coverage—leaving complex commercial and high net worth personal lines to established players.

2. Bargaining Power of Suppliers: LOW

Insurance companies have few traditional suppliers, giving them significant negotiating leverage. Reinsurance represents the primary "supplier" relationship, and here Chubb's scale provides advantages. As one of the world's largest insurers, Chubb can negotiate favorable reinsurance terms and has the option to retain more risk when reinsurance pricing is unfavorable.

Technology vendors are increasingly important suppliers, but the market is highly competitive. Whether it's cloud services from Amazon and Microsoft, data analytics from multiple providers, or core system vendors, Chubb has options and the scale to negotiate favorable terms or build capabilities in-house.

The talent market for specialized underwriters and actuaries can be competitive, but Chubb's reputation and compensation structure help it attract and retain top talent.

3. Bargaining Power of Buyers: MODERATE-HIGH

Buyer power varies dramatically by segment. Large corporate buyers have significant negotiating leverage, often using brokers to create competitive bidding situations. These sophisticated buyers understand coverage terms, can self-insure portions of their risk, and can play insurers against each other.

In middle market commercial, buyer power is moderate. These businesses need insurance but lack the scale to self-insure or the sophistication to fully optimize their programs. They rely heavily on brokers for advice, and broker relationships become crucial for insurers.

High net worth personal lines customers have moderate power. While they can shop coverage, the specialized nature of their needs—art collections, multiple homes, luxury vehicles—limits their options to a handful of carriers capable of providing comprehensive coverage.

The rise of digital distribution is gradually increasing buyer power by making price comparison easier, but insurance remains a complex product where coverage terms and claims service matter as much as price.

4. Threat of Substitutes: LOW

Insurance has few true substitutes. For many types of coverage—auto liability, workers' compensation, professional liability—insurance is legally required. Even where optional, the catastrophic nature of potential losses makes insurance essential for risk-averse individuals and businesses.

Self-insurance represents the primary substitute, but it's only viable for the largest corporations with sufficient capital to absorb major losses. Even then, most self-insured companies buy excess coverage for catastrophic events.

Alternative risk transfer mechanisms like captive insurance companies, risk retention groups, and insurance-linked securities exist but complement rather than replace traditional insurance. Chubb itself participates in these markets, offering fronting services and reinsurance to captives.

5. Competitive Rivalry: HIGH

The insurance industry features intense competition among numerous players. In the U.S. alone, there are over 2,500 property and casualty insurers. Global giants like AIG, Zurich, Allianz, and AXA compete with Chubb across multiple geographies and lines of business.

Price competition is fierce in commoditized lines. Personal auto insurance, small business coverage, and standard homeowners insurance often compete primarily on price, with thin margins for all players.

However, Chubb has positioned itself in less commoditized segments where service, expertise, and capacity matter more than price. In high net worth personal lines, large commercial property, directors and officers liability, and cyber insurance, relationships and reputation create competitive advantages beyond price.

The industry's cyclical nature adds another dimension to rivalry. During "hard" markets following major losses or capital depletion, pricing power shifts to insurers. During "soft" markets with excess capital, competition intensifies and margins compress. Chubb's diversification across lines, geographies, and customer segments helps it navigate these cycles better than more concentrated competitors.

X. Hamilton's 7 Powers Framework

1. Scale Economies: STRONG

Chubb's scale advantages are undeniable. With $37 billion in annual premiums, the company can spread fixed costs—technology investments, regulatory compliance, product development—across a massive revenue base. The $1.3 billion annual technology spend would be crushing for a smaller insurer but represents manageable investment for Chubb.

Scale also provides data advantages. Every policy written, every claim processed adds to a data repository that improves risk selection and pricing. In cyber insurance, where historical data is limited, Chubb's market-leading position provides information advantages competitors cannot replicate.

The global platform creates additional economies. Products developed for one market can be adapted for others. Best practices in underwriting or claims management can be shared across geographies. Technology investments benefit the entire organization.

2. Network Effects: MODERATE

Insurance doesn't exhibit classic network effects where each additional customer makes the product more valuable for other customers. However, Chubb benefits from ecosystem network effects.

The company's relationships with brokers are self-reinforcing. Brokers prefer working with insurers that can handle all their clients' needs, creating a virtuous cycle where Chubb's broad capabilities attract more broker relationships, which bring more customers, justifying more product development.

In cyber insurance, there are data network effects. Each breach claim provides information about attack vectors, vulnerable systems, and effective responses. This knowledge benefits all insureds through better risk assessment and loss prevention recommendations.

3. Counter-Positioning: WEAK

Chubb hasn't fundamentally disrupted the traditional insurance model. The company operates through the same broker distribution channels, uses similar policy structures, and competes for the same customers as traditional competitors.

Where Chubb has succeeded is in positioning itself at the premium end of the market. While InsurTechs pursue mass-market customers with simplified products and digital distribution, Chubb focuses on complex risks requiring expertise and customization. This isn't counter-positioning so much as segment selection.

4. Switching Costs: MODERATE

Insurance switching costs are often underestimated. While personal lines customers can change insurers relatively easily, commercial insurance involves significant switching friction.

Large commercial insurance programs are complex, multi-year arrangements with customized terms and conditions. Changing insurers requires extensive underwriting, potential gaps in coverage, and relationship rebuilding. Claims history, loss prevention investments, and premium financing arrangements all create switching friction.

In high net worth personal lines, switching costs are more emotional than financial. Wealthy individuals value relationships with their insurers, especially after positive claims experiences. The complexity of insuring multiple homes, collections, and vehicles across jurisdictions makes switching daunting.

5. Branding: STRONG

The Chubb name carries weight, especially following the merger. As Greenberg noted, he was showing respect by taking the Chubb name. The 140+ year heritage provides credibility that new entrants cannot match.

In high net worth personal lines, the Masterpiece brand has become synonymous with superior coverage. "Chubb insured" has become a mark of quality, similar to "Intel Inside" in technology.

For commercial buyers, the Chubb brand signals financial strength and claims-paying ability. After watching other insurers fail or withdraw from lines of business, risk managers value the stability Chubb represents.

6. Cornered Resource: MODERATE

Chubb's specialized underwriting talent represents a semi-cornered resource. The company has systematically built expertise in complex areas—cyber, high net worth personal lines, excess casualty—where experienced underwriters are scarce.

The company's Lloyd's of London syndicate provides access to specialty business that might otherwise go to London-market competitors. Long-standing broker relationships, especially in the high net worth segment, create preferential access to desirable risks.

However, talent can be hired away, relationships can shift, and no resource is truly permanent in insurance.

7. Process Power: STRONG

This is perhaps Chubb's strongest power. The company's underwriting excellence isn't about any single factor but rather the combination of countless small optimizations developed over decades.

The underwriting process—from risk selection to pricing to terms and conditions—embodies institutional knowledge that cannot be easily replicated. The integration of data analytics with human judgment, the balance between centralized control and local autonomy, the claims handling protocols—these processes evolved over time and create sustainable advantages.

As Greenberg emphasized: "This is a company of underwriters. We are managed by underwriters. All of senior leadership has a very strong underwriting background." This isn't just about having smart people; it's about having systems that consistently produce superior risk-adjusted returns.

XI. Bull vs. Bear Case

Bull Case:

The growth trajectory in cyber insurance alone could justify optimism about Chubb's future. With the market expected to grow from $12 billion to $90 billion by 2033, Chubb's leadership position provides enormous upside. Even maintaining market share in this expansion would add billions in premium revenue.

The digital transformation investments are creating genuine competitive advantages. The ability to underwrite small commercial business with 7 questions instead of 30, to embed insurance seamlessly into partner platforms, to predict and prevent losses rather than just pay claims—these capabilities will compound over time.

Scale and diversification provide resilience that smaller competitors lack. Chubb can weather soft market cycles, absorb catastrophe losses, and invest countercyclically when competitors retreat. The company's combined ratio consistently outperforms the industry, demonstrating sustainable underwriting advantages.

The shift from a product company to a risk partner opens new revenue streams. As businesses face increasingly complex risks—cyber, climate, supply chain, reputation—they need advisors, not just insurers. Chubb's expertise positions it to capture value beyond traditional premium revenue.

Capital allocation under Greenberg has been exceptional. The company has avoided the value-destroying acquisitions that plague the industry, buying strategically and integrating successfully. The decision to adopt the Chubb name showed cultural sensitivity rare in large mergers.

Bear Case:

Climate change poses existential questions for property insurers. While Chubb has sophisticated catastrophe modeling, the increasing frequency and severity of natural disasters could overwhelm even the best risk management. Secondary perils—floods, wildfires, severe convective storms—are becoming primary losses.

InsurTech disruption, while limited so far, could accelerate. If companies like Lemonade or Root achieve profitability and scale, they could move upmarket into Chubb's profitable segments. More concerning, technology giants like Amazon or Google could enter insurance with distribution advantages Chubb cannot match.

The cyber insurance market, while growing rapidly, could face a systemic event that exceeds industry capacity. A successful nation-state attack on critical infrastructure, a widespread cloud provider breach, or a zero-day vulnerability affecting millions could produce losses that make hurricanes look manageable.

Regulatory pressures are intensifying globally. From the EU's Solvency II to increasing ESG requirements to privacy regulations, compliance costs are rising. Social inflation—the trend toward larger jury awards—is pressuring casualty lines. Some states are making it increasingly difficult to price risk appropriately.

Low interest rates, while currently improving, could return. Insurance companies are essentially spread businesses, earning returns on float. Prolonged low rates compress investment income, forcing insurers to take more underwriting risk to maintain returns.

Concentration risk in certain segments is concerning. The company's dominance in high net worth personal lines and cyber insurance creates exposure if these segments face systematic challenges.

Key Metrics to Watch:

Combined Ratio: This is the single most important metric for any P&C insurer. Chubb's ability to maintain a combined ratio below 90% while competitors struggle to stay below 95% demonstrates underwriting excellence. Watch for any sustained deterioration, especially in long-tail casualty lines where problems emerge slowly.

Cyber Insurance Loss Ratio: As the market leader in a rapidly evolving risk, Chubb's cyber loss ratio provides early warning of systemic issues. A spike in frequency or severity of cyber claims could signal market-wide problems.

Premium Growth in Emerging Markets: Asia-Pacific and Latin America represent the future growth engine. Premium growth rates in these markets, especially in middle-class personal lines and small commercial, indicate whether Chubb can capture the global insurance opportunity or remains primarily a developed-market player.

XII. Investment Playbook & Lessons

For Operators:

The Chubb story offers powerful lessons for business leaders navigating industry transformation. First, crisis creates opportunity—but only for the prepared. Both ACE and Chubb emerged from insurance market crises (1985's liability crisis and 1882's marine insurance needs). Companies that maintain strong balance sheets and operational excellence during good times can capitalize when disruption arrives.

Heritage brands carry hidden value in an age of disposable startups. Greenberg's decision to adopt the Chubb name wasn't sentiment—it was strategic recognition that trust and reputation, built over centuries, cannot be replicated with venture capital and marketing spend.

Digital transformation requires cultural change, not just technology spending. Chubb's billion-dollar technology investment works because it's paired with organizational changes—hiring AI experts, creating innovation labs, partnering with InsurTechs rather than dismissing them.

The vertical integration versus partnership decision shapes competitive position. Chubb chose partnership in cyber security (SentinelOne, NetSPI) rather than trying to become a security company. This focus allows the company to remain an underwriting specialist while accessing best-in-class capabilities.

Building moats in commodity businesses requires relentless focus on execution. Insurance is ultimately about spreading risk and paying claims—activities that seem commoditized. Yet Chubb generates superior returns through thousands of small advantages in underwriting, claims handling, and risk selection that compound over time.

For Investors:

Insurance cycles are real and predictable, creating opportunities for patient capital. The industry oscillates between hard markets (rising prices, restricted capacity) and soft markets (falling prices, excess capacity). Companies with diverse portfolios and strong balance sheets can invest countercyclically.

Underwriting culture matters more than growth rates. Insurance companies that prioritize premium growth often discover problems years later when long-tail claims emerge. Chubb's focus on underwriting profitability over market share has produced superior long-term returns.

Technology is an enabler, not a disruptor, in complex financial services. Despite billions invested in InsurTech, the fundamental insurance model remains unchanged. Technology improves efficiency and customer experience but doesn't eliminate the need for risk assessment and capital.

Management quality is paramount in insurance. The industry's long-tail nature means today's decisions won't be fully revealed for years. Evan Greenberg's 40+ year industry experience and underwriting background provide confidence that risks are being properly assessed.

Consolidation benefits accrue to disciplined acquirers. The insurance industry remains fragmented with opportunities for consolidation. However, most insurance mergers destroy value through integration challenges and cultural clashes. Chubb's successful integration demonstrates that careful planning and cultural sensitivity can capture synergies.

XIII. Epilogue: The Future of Risk

Standing at the precipice of unprecedented change, the insurance industry faces challenges that would have been science fiction just decades ago. Artificial intelligence promises to revolutionize underwriting, potentially making human judgment obsolete—or perhaps making it more valuable than ever. Machine learning models can now process millions of data points to price risk, but can they understand the human elements that often determine whether a business succeeds or fails?

Climate change poses existential questions not just for insurers but for the entire global economy. As natural disasters become more frequent and severe, the fundamental principle of insurance—spreading risk across time and geography—comes under strain. Some risks may become simply uninsurable. Chubb's response will shape not just its own future but society's ability to adapt to a changing planet.

The cyber warfare landscape is evolving from criminal enterprises seeking profit to nation-states wielding digital weapons. A successful attack on critical infrastructure could produce losses that dwarf any natural disaster. The insurance industry must grapple with covering risks that could literally bring down the global economy.

The concept of embedded insurance—coverage seamlessly integrated into products and services—could transform distribution. Imagine auto insurance that adjusts premiums in real-time based on driving behavior, or cyber insurance that automatically increases coverage when threats are detected. Chubb Studio positions the company for this future, but execution will determine success.

Public-private partnerships may become essential for systemic risks. Pandemic, cyber warfare, and climate change produce losses that exceed private market capacity. Governments and insurers must collaborate on solutions that protect society while maintaining market incentives for risk management.

The question of Chubb's independence looms large. In 2021, Greenberg led an attempted acquisition bid for The Hartford. Will Chubb remain an acquirer, or will it become a target itself? With insurance becoming increasingly critical to global economic stability, consolidation seems inevitable.

Yet through all these uncertainties, one thing remains constant: risk is inherent to human progress. Every innovation, every venture, every dream carries the possibility of loss. Insurance—boring, complex, essential insurance—makes progress possible by allowing society to take calculated risks.

Chubb's journey from marine underwriters to global risk partners mirrors society's evolution from industrial to digital age. The company that once insured sailing ships now covers satellites. The firm that started by protecting merchant cargo now shields companies from hackers halfway around the world.

As Evan Greenberg often says, insurance is a craft. Like all crafts, it requires patience, skill, and constant refinement. In a world of quarterly earnings and instant gratification, Chubb's multi-decade perspective seems almost anachronistic. Yet that long-term view—the willingness to invest billions in capabilities that won't pay off for years, the discipline to walk away from bad risks even when competitors are writing them—may be the company's greatest competitive advantage.

The future belongs not to those who eliminate risk but to those who understand it, price it, and manage it. In that future, Chubb's combination of heritage and innovation, scale and specialization, technology and human judgment positions it not just to survive but to thrive.

The story that began with Thomas and Percy Chubb collecting $1,000 from merchants to insure ships continues today with algorithms processing millions of data points to price cyber risk. It's a story of evolution, not revolution—of building on foundations rather than destroying them.

Will Chubb dominate the next century as it has the past? Will insurance itself survive in recognizable form? The answers lie not in predictions but in preparation—in building capabilities before they're needed, in maintaining discipline when others lose theirs, in remembering that behind every policy is a person or business taking a risk in pursuit of something better.

The craft of insurance endures because risk endures. And as long as humans dare to build, create, and venture into the unknown, they'll need partners to help bear the risks. For nearly 150 years, through depressions and wars, booms and busts, analog and digital ages, Chubb has been that partner.

The next chapter remains unwritten, but one thing is certain: it will be anything but boring.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube