CarGurus: From Harvard Square Townhouse to Automotive Marketplace Disruptor

I. Introduction & Episode Roadmap

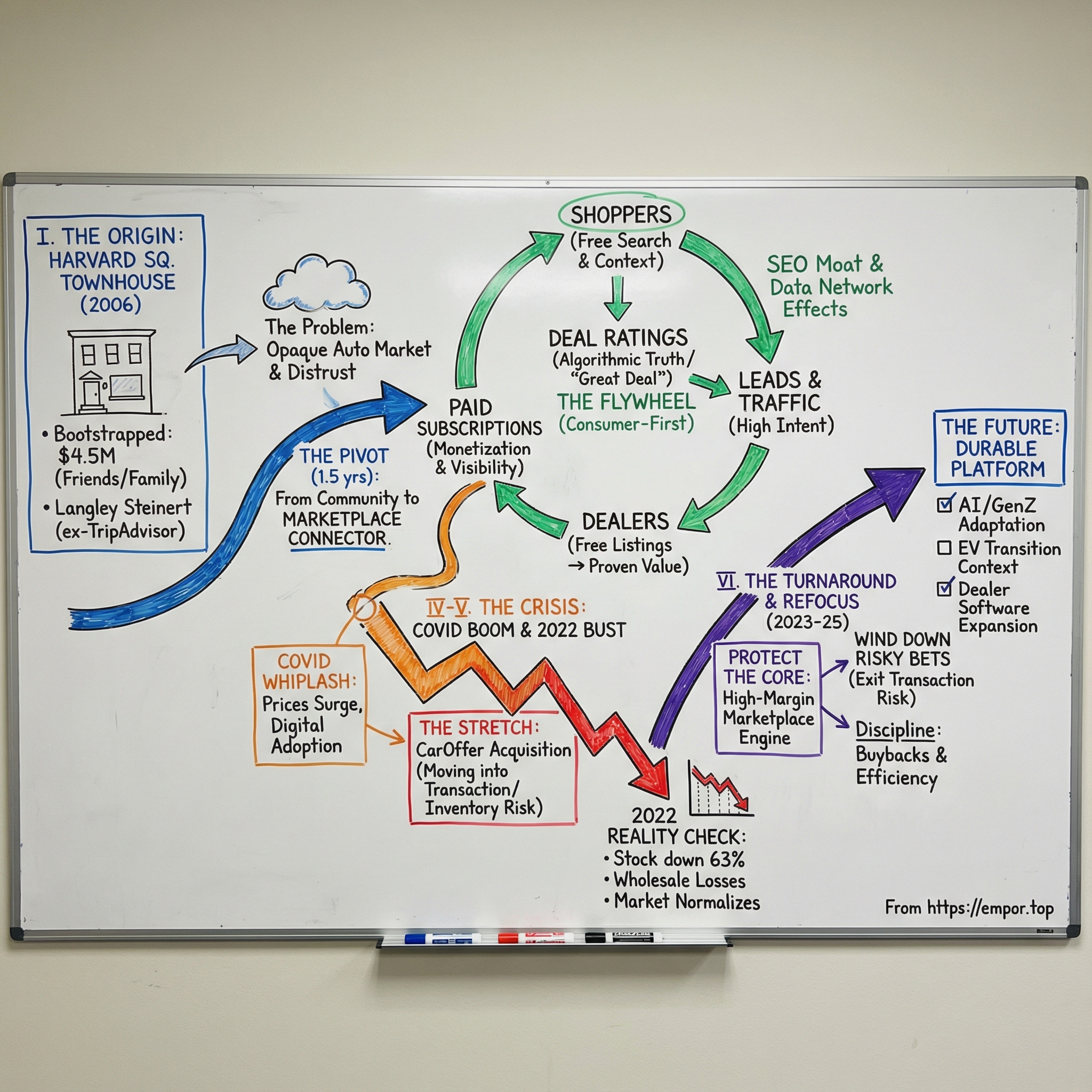

Picture a cramped townhouse on Mount Auburn Street in Harvard Square, circa 2006. Inside, a serial entrepreneur fresh off selling TripAdvisor for $210 million is hunched over a laptop with six developers, trying to make car shopping make sense. There are no laser printers. Steinert had learned in his TripAdvisor days that constraints sharpen focus. So CarGurus ran lean—bootstrapped with $4.5 million from friends and family, and intentionally steering clear of venture capital.

Fast-forward to today and that little townhouse project has become CarGurus: a company with a market cap of around $3.65 billion and more than 40 million monthly visitors. It’s the most visited automotive shopping site in the U.S., built on massive inventory and a sprawling dealer network. But the road from Harvard Square to a public company with nearly a billion dollars in annual revenue wasn’t a smooth climb. It was a set of hard-won flywheels, a few near-misses, and one very public gut check.

The hook of the CarGurus story sounds simple: how did a serial entrepreneur turn pricing transparency into a billion-dollar marketplace—and why did it almost fall apart in 2022? Answering that takes us into the messy reality of two-sided marketplaces, the leverage of algorithmic trust, and the constant temptation to stop being a neutral platform and start acting like a participant.

Because 2022 was brutal. CarGurus stock fell 63% year-to-date, while Carvana cratered 96%—a reminder that when the used-car market normalizes, it doesn’t do it gently. CarGurus made it through, but only by letting go of some ambitions and doubling down on what it did best.

So that’s where we’re headed: how you solve the cold-start problem in a marketplace, how SEO can become a distribution moat, how serial entrepreneurs recycle lessons from past wins, and how a business built on “help the consumer” survives when the cycle turns and the entire industry is forced to re-price reality.

II. Langley Steinert & The TripAdvisor Foundation

Langley Steinert was born in 1963 and took what looked like the conventional high-achiever path: Georgetown for Government and Economics, then straight into investment banking from 1985 to 1988. He learned how money moves and how deals get done. He also learned, pretty quickly, that it wasn’t going to be enough. Wall Street was a great education—and an even better elimination round. He didn’t just want to make money. He wanted to build something.

Business school at Tuck pulled him closer to software. Between his first and second years, he interned at a software company and got advice that would quietly shape his whole career: don’t sprint into founding a company on day one. Go make mistakes on someone else’s dime first. Steinert listened. He spent three years as a product manager at Lotus, then moved through early-stage startups around Boston, stacking practical lessons the way most people stack degrees.

One of those stops was Papyrus, where he was among the first executives at the company behind NASCAR Racing, the best-selling CD-ROM game in America. Another was Viaweb, where he became the fifth employee and VP of Marketing. Viaweb was run by a then little-known founder named Paul Graham, and its pitch was almost absurdly ambitious for the late ’90s: small businesses could open an online store using nothing but a web browser. In 1998, Yahoo bought Viaweb for $49 million. Graham would go on to found Y Combinator, but for Steinert, the immediate result was simpler: a front-row seat to what software could do when it made something hard suddenly feel inevitable.

After Viaweb, Steinert hit a familiar entrepreneurial pause. As he later put it, “I didn’t know what I wanted to do with my life at that point, so I did a year and a half as a partner at a venture capital firm in Cambridge, and that’s how I came to know Steve Kaufer.” That introduction mattered more than the title on his business card.

In February 2000, Steinert co-founded TripAdvisor with Stephen Kaufer, Nick Shanny, and Thomas Palka. It began as a side project with a deceptively simple idea: aggregate and share real travel opinions—especially hotel reviews—so regular people could make better decisions. The origin story was personal too: after a trip to Greece, Kaufer went looking for reliable recommendations and found mostly marketing. TripAdvisor was built in Newton, Massachusetts, and it leaned hard into user-generated content at a moment when the internet was just starting to trust strangers.

Steinert served as chairman, and in 2004 TripAdvisor was sold to IAC for $210 million. The playbook was simple, but it was a weapon: bring transparency to an opaque market by collecting the messy truth from real users. Hotels couldn’t hide behind glossy brochures when travelers were comparing notes in public.

The sale gave Steinert financial freedom—his net worth was later estimated at $522 million as of 2021—but it didn’t give him the itch-scratch of being done. He wasn’t looking to retire. He was looking for the next problem. And he needed it to be outside travel, because he’d signed what he called “a big fat non-compete.”

He also had a philosophy about motivation that sounds obvious, but isn’t. “I tell college and business school students, if you’re starting a company because you want to be the next Mark Zuckerberg and make a ton of money, you’re going to fail,” Steinert has said. “My number one rule is do it because you’re passionate about it, not for the money.”

That’s where the seed of CarGurus came from: not a spreadsheet, but a personal irritation. Buying a used car is a uniquely modern kind of stress. Is this a fair price? Is this dealer reputable? Why is the same car thousands of dollars cheaper across town? Steinert recognized the pattern immediately. Travel wasn’t the only market built on information asymmetry. Automotive might be even worse.

And if TripAdvisor proved that transparency could change behavior, then the obvious next question was: could the same approach work for cars?

III. The Birth of CarGurus: Solving Information Asymmetry

CarGurus started in 2006 in Cambridge, Massachusetts, with Langley Steinert doing what he’d done before: taking a market built on confusion and trying to drag it into the daylight. After TripAdvisor, he’d seen how powerful it was when ordinary people could compare notes. Car buying, he figured, was the same kind of problem—just with higher stakes and even less trust.

TripAdvisor launched with around $4 million. CarGurus began with about $5 million. Steinert put in his own money and raised the rest from friends and family, including Steve Kaufer. No venture capital. Not because he couldn’t have raised it, but because he didn’t want it. His advice on VC was blunt: “Stay away if you can.” Being self-funded meant CarGurus could iterate without someone constantly asking when it would “scale.”

The first version of CarGurus looked a lot like TripAdvisor on wheels. It was essentially an automotive community—a place where consumers could post reviews and questions about local dealers, repair shops, and specific car models. But the team quickly ran into a reality check: the “review-first” concept didn’t translate cleanly to how people actually buy cars. After about a year and a half, Steinert decided to pivot.

That pivot came from a signal hiding in plain sight. Dealers were interested in advertising. So CarGurus shifted from being a discussion hub to being a marketplace connector: get dealer inventory onto the site and give shoppers something they almost never had at the dealership—context.

That’s where the real insight snapped into focus. Cars are basically commodities. A specific year, make, model, mileage, and trim should have a knowable value. But the industry had been built to keep that value hazy. If you walked into a dealership without a strong sense of “market,” you were negotiating from behind.

CarGurus’ answer was to turn pricing into a data problem. The product wrapped dealer listings in “Deal Ratings” that told shoppers, in plain language, whether a car was a Great Deal, Good Deal, Fair Deal, or Overpriced compared to similar vehicles. The point wasn’t to win an argument with a salesperson. It was to help the consumer walk in already knowing where reality was.

Under the hood, those ratings were powered by algorithms and deep-data analytics that CarGurus built and refined over time. The system evaluated millions of listings, factored in location, and calculated Instant Market Value across more than 150 urban and rural markets in the U.S. It also pulled in dealer reputation signals, including thousands of verified dealership reviews from CarGurus shoppers.

And all of that was built by an intentionally small team. For the first three years, CarGurus was basically Steinert plus six developers working out of a Harvard Square townhouse. It was engineering-first by design. Steinert had started his career as a product manager, but at CarGurus, the philosophy was closer to: hire engineers who can build, but who also have opinions about what to build. The goal was to keep the feedback loop tight—code, learn, adjust—without layers getting in the way.

Steinert would later describe the lesson in a way that sounded almost like a confession, because he’d lived it twice: “Both in the case of TripAdvisor and CarGurus, our first year and a half we were pursuing the wrong product plan and the wrong revenue model… we had to pretty much scrap what we had been doing.” Many founders can’t stomach that. He saw it as the job.

Timing helped, too. By 2006, broadband was mainstream, consumers were increasingly comfortable doing serious research online, and search engines were becoming the front door to nearly every buying journey. CarGurus was built to ride that wave—an SEO-first strategy that, as we’ll see, became one of its most durable advantages.

IV. The Marketplace Flywheel: Getting Both Sides On Board

Every two-sided marketplace runs into the same deadlock on day one: shoppers won’t show up without inventory, and dealers won’t bother without shoppers. Steinert’s solution was to break the cycle from the consumer side. Build the best shopping experience, aggregate as much inventory as possible, and make the site so useful that dealers would eventually have to meet buyers where they already were.

That didn’t happen without friction. In the early days, some dealers balked at being included on CarGurus and asked to be removed. Steinert would comply, but he also coached the team to calmly walk those dealers through the math. CarGurus was already sending them meaningful lead volume for free—sometimes up to 100 leads a month. At a 10% close rate and roughly $2,500 in profit per sale, that could translate into about $25,000 of incremental profit. Once dealers saw it framed that way, the conversation shifted from “take us off your site” to “how do we get more of that?”

That set up the model CarGurus still runs on: consumers can search for free, and dealers can list for free. Then, if a dealer wants the full toolkit—more visibility, more ways to market their dealership, and more chances to connect with CarGurus’ audience—they pay for subscription services.

It’s a classic freemium flywheel, but tuned for automotive. Free listings created broad inventory coverage. Broad inventory attracted shoppers. Shoppers generated leads. Leads proved value to dealers. And proven value turned into paid upgrades for enhanced placement. Once that loop started turning, it was hard to stop.

The growth numbers started to reflect it. By 2008, CarGurus had already accumulated more than 250,000 pieces of user-submitted content and was growing traffic rapidly, reaching more than 700,000 unique monthly visitors. From 2009 to 2011, monthly visitor traffic climbed from 9 million to 21 million.

The company’s momentum showed up on the awards circuit too, landing on the Inc. 500 Fastest Growing Private Companies list in 2011, 2012, and 2013, then the Inc. 5000 in 2014, 2015, and 2016. In 2015, Forbes also named CarGurus to its Most Promising Companies list.

But automotive marketplaces don’t behave like winner-take-all platforms. Multi-homing is everywhere: dealers list across multiple sites, and consumers comparison-shop across multiple tabs. In that world, you don’t win just by having listings. You win by giving people a reason to start with you. For CarGurus, that reason was the Deal Rating algorithm—an opinionated layer of judgment on top of raw inventory.

CarGurus positioned itself as a trusted marketplace that gave shoppers third-party validation on pricing, dealer reputation, and other signals that helped them find “Great Deals from Great Dealers.” By June 30, 2017, CarGurus had built an active dealer network of more than 40,000 dealers and offered more than 5.4 million car listings—at the time, the largest selection among major U.S. online automotive marketplaces.

CFO Jason Trevisan would later describe it as “the largest platform for both consumers and dealers to find a car,” noting that more than 40,000 dealers represented over 90% of auto dealership businesses in the U.S. And critically, CarGurus wasn’t taking a cut of each car sold. It was selling access and performance through a freemium, subscription-based model.

The real “critical mass” moment wasn’t just scale—it was quality. CarGurus could point to superior lead quality because the Deal Rating system effectively pre-qualified shoppers. People clicking into a “Great Deal” listing weren’t tire-kickers; they were motivated buyers who’d already anchored on what a fair price looked like. Dealers saw better conversion than they got from other sources, and that performance gap made paying for premium placement feel less like advertising and more like buying a proven growth channel.

V. Growth & Scaling: Becoming the #1 Automotive Site

Once the flywheel started spinning, CarGurus scaled the way the best internet marketplaces do: win distribution, keep improving the product, and stay ruthlessly disciplined about what actually drives growth.

In the years leading up to the IPO, CarGurus was still chasing something it didn’t fully have yet: top-of-mind awareness. Shoppers knew legacy brands like Cars.com, Kelley Blue Book, and Autotrader. CarGurus had the better experience, but it needed more people to start their search there. And the data suggested it was working. AIM Group’s Automotive Advertising Annual 2017 reported that CarGurus had leapfrogged past Autotrader and Cars.com to become the traffic leader among third-party automotive sites.

A huge part of that was SEO—and not the fluffy “content marketing” kind. CarGurus built pages the way an algorithmic marketplace would: creating unique, data-driven content across vehicle types, local markets, and pricing contexts. That let it capture the long tail of high-intent searches competitors routinely missed. If someone typed something like “2015 Honda Accord fair price Boston,” CarGurus could meet them with a page that felt uncannily specific, because it basically was.

For years, the brand grew mostly through word-of-mouth and search. Then, in June 2017, CarGurus flipped a new switch: its first national TV campaign, following earlier pilot campaigns in Denver, Nashville, and Austin. It was the classic move of a company that already owned the bottom of the funnel deciding it was time to pour fuel on the top.

Expansion followed a similar logic: prove the playbook at home, then export it. The platform launched in 2006, and international expansion began in 2015, starting with Canada and the United Kingdom. In 2018, CarGurus bought the UK website and forum PistonHeads for an undisclosed amount—less a traditional classifieds acquisition than a shortcut to credibility, by plugging into a brand that already had a passionate enthusiast community.

Back in the core U.S. business, CarGurus also worked to deepen its ties to the dealer ecosystem. It partnered with major industry software players to strengthen dealerships’ digital marketing: dealers on CDK Global websites could get their inventory exposed on CarGurus, and dealerships could use the collaboration to serve more personalized ads to shoppers who had previously visited the platform.

Meanwhile, the product kept expanding beyond “search results and a phone number.” Price drop alerts, dealer reviews, mobile apps, and trade-in tools pushed CarGurus toward becoming a full research destination. Importantly, those features didn’t distract from the core thesis—they amplified it. The whole point was still to help consumers make informed decisions, and to make the best-priced inventory rise to the top.

Competition never let up. CarGurus went head-to-head with TrueCar, Cars.com, and AutoTrader.com. But CarGurus kept leaning into its differentiator: a consumer-first marketplace where the incentives were supposed to line up. In CarGurus’ framing, the dealers who offered strong value got better placement, shoppers got better deals, and everyone won—at least in theory.

Underneath it all was a financial posture that shaped how the company grew. CFO Jason Trevisan said CarGurus stayed away from traditional venture financing because it became cash-flow positive early. The company started with funding from friends and family, and later raised money from mutual funds rather than classic VC firms. The idea was simple: wait until the model is proven, then raise capital from a position of strength. CarGurus’ first major external funding was a Series A round in 2007 that brought in $5 million.

And by the time it was layering on national advertising, international bets, and deeper dealer integrations, it wasn’t scaling a concept anymore. It was scaling a machine.

VI. The 2017 IPO: Public Market Success

By the fall of 2017, CarGurus wasn’t just “growing fast for a classifieds site.” It was throwing off real profits, leading in traffic, and starting to look like a platform. So the company did the thing that turns a well-run machine into a public scoreboard: it went public.

CarGurus priced its IPO at $16 a share, above the expected range, and began trading on the Nasdaq under the symbol “CARG.” The market’s verdict was immediate. On its first day, the stock surged and finished up more than 70%, a rare kind of pop that signals investors weren’t just buying an offering—they were buying the story.

In total, the offering included 10,810,000 shares of Class A common stock after the underwriters exercised their option to purchase additional shares, priced at $16.00 per share before underwriting discounts. CarGurus itself issued and sold 3,205,000 shares, and selling stockholders sold another 7,605,000.

The IPO raised about $150 million and put CarGurus at a market cap north of $3 billion. And the pitch to public markets was consistent with everything the company had been building since that townhouse in Harvard Square: this wasn’t supposed to be another listings site. It was a data science company using algorithms to bring transparency to a market that had historically thrived on confusion.

Steinert framed it in familiar terms: CarGurus aimed to do for car shopping what TripAdvisor had done for hotels—make the market legible, and force better behavior through visibility. He also argued the company had a rare combination for a tech IPO: rapid growth and profitability. In a sector filled with “growth now, profits later,” CarGurus showed up with both.

The proceeds, CarGurus said, would support international growth—Canada, the U.K., and Germany—along with expanded dealer services and new tools to help consumers trade and sell cars directly to other consumers.

The fundamentals were what made the narrative credible. In 2016, the company generated $198.1 million in revenue, more than doubling from the year before, and it posted $6.5 million in profit. In 2015, it had $98.6 million in revenue and a $1.6 million loss. It was crossing the line from “promising” to “proven.”

Going public didn’t mean giving up control, though. When Steinert took CarGurus public in October 2017, he retained a controlling interest—owning 29% of the shares while keeping more than 60% of the voting power. The mechanism was a dual-class structure: Class A shares carried one vote each, while Class B shares carried ten votes each and could be converted into Class A shares. The message was clear: the market could participate, but the founder was still driving.

Early results as a public company reinforced the momentum. On Nov. 14, CarGurus reported that third-quarter net income rose 11% year over year to $2.4 million, while revenue jumped 56% to $83 million. Paying dealerships grew 37% to 26,553, with U.S. paying dealers up 29% to 24,313. International paying dealerships nearly quadrupled to 2,240 from 626 a year earlier. Average annual revenue per subscribing U.S. dealership climbed 16% to $11,526.

And the stock kept running. On September 26, 2018, CARG hit an all-time high of $57.25—nearly quadrupling from the IPO price in under a year, the kind of chart that makes an entire management team look prescient.

Even the board signaled what kind of company CarGurus believed it was becoming: a modern marketplace, guided by marketplace veterans. It included Steve Kaufer from TripAdvisor, Greg Schwartz from Zillow, and Wayfair co-founder Steve Conine—operators who’d lived through the messy reality of two-sided platforms and knew how hard they are to build, and how easy they are to lose.

VII. The Inflection Point: COVID & The Used Car Boom

In March 2020, COVID-19 hit automotive retail like a power outage. Dealerships closed their doors, foot traffic evaporated, and for a moment it looked like the whole car-buying machine might just seize up.

CarGurus’ own data captured the whiplash. In April, most shoppers said they planned to delay a purchase. By June, that share had eased, not because people suddenly felt carefree, but because the intent hadn’t disappeared. It had just been paused. As CarGurus put it after surveying more than 2,000 shoppers: over the course of the year, people delayed but didn’t cancel. At the same time, the pandemic nudged behavior in a direction that mattered a lot for an online marketplace—away from public transit and ride-hailing, and back toward personal vehicle ownership, with a growing openness to buying online.

Then the supply side broke.

Production shutdowns and a microchip shortage throttled new-car manufacturing in 2021. With fewer new cars on lots, the pressure rolled downhill into used cars. Inventory tightened, and prices climbed. On CarGurus, listings averaged $22,470—more than $1,800 higher than at the start of 2020. The growth rate cooled later, but the new baseline stayed stubbornly elevated.

CarGurus didn’t just ride the wave; it used it as a forcing function. After the COVID-induced slump, the company rebounded quickly. In the second quarter of 2021, revenue jumped to $217 million, fueled by surging demand across both new and used vehicles. And yet, even in the middle of this digital acceleration, Trevisan noted a sobering reality: pure online transactions still made up only about 1% of U.S. car sales.

But the direction of travel was clear. A March 2021 study by auto logistics firm Acertus found that 80% of shoppers said they’d now be willing to buy a new car entirely online, without even a test drive—up from roughly half before the pandemic. Industry observers could feel the timeline collapsing. “People are still reluctant to buy a car entirely online. That reluctance is diminishing very quickly,” said Peter Zollman, founder of Advanced Interactive Media Group. “COVID sped up five years of innovation and activity into three months.”

CarGurus moved to meet that moment by widening its role in the ecosystem—without crossing the line into becoming a dealer itself.

In December 2020, CarGurus announced it had entered into a definitive agreement to acquire a 51% interest in Plano, Texas-based CarOffer, valuing the business at $275 million. CarOffer was built to modernize wholesale: an instant vehicle trade platform that let dealers bid, transact, inspect, and arrange transport with far less friction than traditional auctions. The pitch was straightforward: add wholesale capabilities to CarGurus’ dealer offerings and create a more complete digital solution for dealers to sell and acquire vehicles across both retail and wholesale channels.

In January 2021, CarGurus closed the deal for that initial 51%, with the option to buy the remaining equity over the next three years. Trevisan framed it in familiar CarGurus language—transparency, data, and technology applied to another opaque corner of the market. “CarOffer is disrupting the traditional wholesale auction model in the same way that CarGurus gained our position as the leading online consumer automotive marketplace in the U.S., by leveraging technology, data and analytics to build more transparent solutions,” he said.

The broader industry was sending mixed signals. Carvana and Vroom made digital-first car buying feel real, even as their unit economics raised eyebrows. CarGurus took a different stance: don’t become the dealership. Power the dealerships.

And even as CarGurus stepped deeper into the transaction flow, it reiterated that it had no intention of turning into an independent online car dealer.

One more change landed during this period: leadership. Steinert served as CEO until January 2021, when CFO Jason Trevisan took over as CEO.

VIII. The Crisis: 2022 Collapse & Leadership Turmoil

In 2022, the market stopped believing.

CarGurus stock fell 63% year-to-date. Carvana’s collapse was even more extreme, down 96%, but the message across the industry was the same: when the used-car cycle turns, it turns fast—and it punishes anyone even adjacent to inventory risk.

For CarGurus, the drawdown got ugly. On November 9, 2022, the shares hit an all-time low of $9.14. From a peak near $57 to under $10 in a little over four years, the decline didn’t just erase gains. It called the whole story into question.

So what happened? It wasn’t one thing. It was a pile-up.

CarGurus reported softer third-quarter results and a weaker fourth-quarter outlook as auto industry trends deteriorated. At the same time, operational issues cropped up inside the newer businesses—CarOffer and IMCO—creating pressure that management expected to carry into Q4. Those headwinds squeezed EBITDA, particularly as the company worked through inventory and arbitration challenges. The one bright spot: the core Marketplace business held up, remaining relatively resilient and still generating solid EBITDA.

But the overall picture changed dramatically. CarGurus slipped into a loss-making position during the year, and that alone was enough to send many investors running. A company that had been celebrated for pairing growth with profitability suddenly looked like it had traded its identity for a set of money-losing experiments.

Wall Street’s nerves centered on Instant Max Cash Offer. IMCO let consumers sell their vehicles directly, but it also pushed CarGurus into taking inventory risk—exactly the kind of exposure its asset-light model was designed to avoid. When used car prices stopped rising and began to normalize, those positions started generating real losses. The program was still operating at negative margins, and the hit showed up quickly in the company’s profitability.

Meanwhile, dealer consolidation reduced the customer count, and the wholesale business through CarOffer ran into another kind of problem: price volatility made “instant” pricing harder to trust. Disputes and arbitration headwinds followed. In hindsight, the timing looked brutal. CarGurus had bought into CarOffer as used car prices were near peak levels—and then the market moved the other way.

All of this unfolded under a new CEO. Jason Trevisan had joined CarGurus in 2015 as CFO and stepped into the top job in 2021, also joining the board. His remit wasn’t just finance; it included strategy, operations, and product direction—exactly the mix you want when the question is no longer “how do we grow?” but “what business are we really in?”

As the company put it at the time: “Jason’s visionary leadership over the past five years, along with his deep commitment to our people and our customers, has been integral to our growth and has helped to position CarGurus for future success. Jason brings both strategic vision and strong operational expertise to the CEO role.”

Now he had to answer an existential question in public. Was CarGurus simply a classifieds site with a great algorithm? Or could it build a deeper moat by moving closer to the transaction—through trade-ins, facilitation, and wholesale?

By the end of 2022, the market was voting for “classifieds,” and it was voting loudly.

The response was what you’d expect when a company has to protect the thing that still works. Cost-cutting became unavoidable. The workforce was reduced. Initiatives were triaged, and attention snapped back to the core marketplace business—the engine that kept running even as the newer bets stumbled.

It’s tempting to lump CarGurus in with Carvana because the timing was similar and the charts looked equally scary. But the underlying risk profile wasn’t the same. Carvana’s near-death experience came from massive inventory exposure and the fixed costs of physical operations like reconditioning centers. CarGurus’ pain came from smaller, more targeted moves into transaction facilitation—moves that still mattered, and still hurt, but weren’t a fundamental indictment of the marketplace model itself.

The real problem was simpler, and more dangerous: CarGurus had stepped just far enough toward the transaction to get burned by the cycle—without stepping far enough to fully control the economics.

IX. The Turnaround & Digital Wholesale Evolution

By 2023 and 2024, Trevisan’s plan wasn’t subtle: protect the profitable Marketplace engine, repair what was broken in wholesale, and prove the company could run with discipline again—operationally and financially.

Internationally, the story quietly improved the headline results. Growth accelerated in Canada, and the U.K. reached profitability—a meaningful milestone, because it meant CarGurus was profitable in every market it operated. Meanwhile, the product mix kept shifting toward mobile: in 2023, the app generated about a quarter of leads, up from just 10% in 2020.

Then came a clean-up move that also doubled as a commitment. In November 2023, CarGurus announced a definitive agreement to buy the remaining minority equity interests in CarOffer for $75 million in an all-cash transaction, expected to close in December. CarGurus had purchased 51% in 2021, with the option to buy the rest over the following three years. Pulling that timeline forward signaled urgency: management wanted tighter integration between the two businesses and faster execution on its vision of a more transaction-enabled platform.

At the same time, CarGurus leaned into capital return. In November 2023, the company authorized $250 million in share repurchases—about 10% of shares outstanding.

Operationally, the Marketplace kept doing what it’s always done when CarGurus is healthy: grow, throw off margin, and pull dealers up the subscription stack. In Q4 2024, marketplace revenue was $210.2 million, up 15% year over year, while international revenue grew 26%. OEM advertising revenue also grew at a double-digit rate. The trade-off was that the newer lines were shrinking fast: wholesale and product revenues each fell 55%. Still, profitability snapped back hard. Gross margin expanded to 87%, up from 69% the year before. Paying dealers increased 3% to 32,010, with U.S. paying dealers up 2% and international paying dealers up 11%. U.S. quarterly average revenue per subscribing dealer rose 12% to $7,337, and international QARSD grew 17% to $2,072.

Trevisan put a bow on it: “We delivered exceptional results in 2024, with sustained revenue acceleration and significant margin expansion across geographies. Our Marketplace business achieved double-digit growth, driven by continued migration to premium tiers, strong OEM advertising demand, and growing adoption of our value-added products and services.”

Wholesale, meanwhile, was treated less like a moonshot and more like a turnaround job. In 2024, CarGurus described three priorities: improve operations, sharpen product-market fit, and restart the commercial engine. By the fourth quarter, the company pointed to better dealer-to-dealer transportation margins while maintaining high-quality inspections—less drama, fewer surprises, more predictability. It also emphasized product updates designed to use real-time market insights to improve outcomes.

By Q3 2025, the core business was still carrying the company. Consolidated revenue was $239 million, up 3% year over year. Marketplace revenue was $232 million, up 14% year over year and toward the high end of guidance. That growth was driven by dealer upgrades, broader adoption of add-on products, and higher lead quality. International revenue rose 27%, led by Canada and the U.K.

Product innovation continued, too. CarGurus launched PriceVantage, a machine learning-based pricing tool that showed early promise, including a reported 5x improvement in inventory turn time for dealers who engaged with it. The company also expanded its suite with products like CG Discover and dealership mode. Financially, adjusted EBITDA grew 21% year over year, with an adjusted EBITDA margin of 33%.

But here’s the most important signal from 2025: CarGurus was walking away from the kind of wholesale risk that had burned it. As the company wound down CarOffer’s transactions business, digital wholesale adjusted EBITDA loss widened sequentially to roughly $4 million on lower volumes—and then management made it explicit: all digital wholesale revenue was expected to cease in future reporting periods.

This was the strategic acknowledgment hiding inside the numbers. An inventory-bearing wholesale transactions model didn’t fit CarGurus’ core competencies. The company would keep wholesale relationships, but it would stop being in the business of taking transaction risk.

And the capital return story kept getting louder. CarGurus has repurchased 23% of shares outstanding since starting its buyback program—an aggressive posture that signaled management confidence while sending cash back to shareholders.

X. The Competitive Landscape: Who Are The Real Threats?

CarGurus has never competed in a quiet neighborhood. Its rivals range from the old guard of automotive classifieds to newer, flashier bets on “buy a car like you buy sneakers.” The usual list includes TrueCar, AutoTrader, Cars.com, Carvana, and Kelley Blue Book.

Start with the incumbents. AutoTrader has been around since 1997 and built its brand as a trusted destination for used cars, with a broad mix of new, used, and certified pre-owned inventory from dealers and private sellers. It’s the classic marketplace model: huge selection, powerful search tools, and an ecosystem designed to serve both shoppers and dealers.

CarGurus looks similar from a distance—big inventory, filters, photos, lead forms—but it made a very specific product choice early: put pricing context front and center. CarGurus became known for price comparison, Deal Ratings, and Instant Market Value assessments, plus anonymized communication that let shoppers engage without immediately handing over their identity. AutoTrader, meanwhile, leaned into features like instant cash offers, detailed car reviews, and dealer marketing solutions.

Cars.com is the other heavyweight. In 2021, it generated $623.7 million in revenue, up 14% year over year, with $7.7 million in profit. Both Cars.com and AutoTrader remain formidable partly because they’re deeply embedded in dealer advertising budgets. But they never fully owned CarGurus’ signature positioning: algorithmic transparency that says, “Here’s what this car should cost, and here’s how this listing stacks up.”

Then there are the disruptors who tried to change the whole retail model. Carvana and the now-collapsed Vroom made a bold promise: skip the dealership entirely. They helped prove that consumers do want convenience, but they also exposed how punishing the unit economics can be when you actually take possession of cars.

Carvana is the cleanest example. It’s famous for the vending machines, but the more important distinction is structural: Carvana doesn’t just list cars, it sells the cars it lists. That means inspections, certification, reconditioning, logistics, and, most dangerously, inventory risk. When the market normalized, the capital requirements and depreciation dynamics didn’t just hurt—they became existential. In that light, CarGurus’ less glamorous marketplace model looked far more resilient.

And the competitive pressure isn’t only other websites. The dealer landscape itself is changing. Dealers have been consolidating their marketplace partners, moving from using an average of about three platforms to under two—around 1.8. That’s a brutal dynamic if you’re a “nice-to-have” listing site, and a powerful one if you can prove you’re the best ROI. CarGurus’ pitch is exactly that: better leads, better conversion, more predictable performance.

Big Tech sits in the background like a sleeping giant. Google and Meta have the traffic, ad infrastructure, and data talent to matter here immediately. Yet neither has seriously committed to dominating automotive classifieds—likely because cars aren’t just another vertical. The space runs on messy inventory, local dynamics, and dealer relationships that horizontal platforms don’t naturally have.

Internationally, competition shifts but the playbook stays the same. CarGurus has been growing outside the U.S., with international revenue up 27% year over year, competing against major players in the U.K. and Canada by emphasizing ROI at lower price points. The strategy mirrors what worked in the U.S.: win share first, prove value, then earn the right to raise prices.

Finally, dealer consolidation is both a threat and a tailwind. Groups like Lithia and AutoNation are getting bigger, which increases their bargaining power. But it also increases their need for efficient, multi-market distribution. As dealer groups expand, a platform that can reliably move inventory and reach shoppers across geographies becomes more valuable—not less.

XI. Business Model Deep Dive: How CarGurus Makes Money

By this point in the story, the business model almost feels inevitable: CarGurus makes money by being the place shoppers start, and the place dealers can’t afford to ignore.

The company reports two operating segments: U.S. Marketplace and Digital Wholesale.

U.S. Marketplace is the engine. CarGurus runs an online automotive marketplace where consumers search new and used listings—mostly from dealers—and where those dealers get access to a huge audience of high-intent shoppers. The pitch to dealers isn’t just “we’ll put your cars online.” It’s “we’ll bring you buyers, and we’ll tell you what’s working,” with data-driven insights layered on top.

Around that core search-and-leads experience, CarGurus has built a bundle of transaction-adjacent products. Digital Deal lets shoppers begin a purchase flow right from a vehicle details page on eligible listings. Finance in Advance lets eligible consumers pre-qualify for financing. Sell My Car Top Dealer Offers lets dealers send tailored trade-in offers. And Sell My Car Instant Max Cash Offer lets consumers sell vehicles to dealers online. On top of dealers, CarGurus also sells ad products to automakers and others—things like brand reinforcement, category sponsorship, automobile segment exclusivity, and targeted exposure to specific consumer segments.

How does that translate into dollars? The Marketplace business is primarily a tiered subscription. Dealers pay monthly fees for enhanced placement and performance. The more visibility they want—and the more inventory they have—the higher the price. Premium tiers mean more impressions and more leads, and if the leads convert, the subscription feels less like “advertising” and more like a measurable acquisition channel.

You can see that “grow by expanding” strategy in the dealer economics. The company’s U.S. Quarterly Average Revenue per Subscribing Dealer increased 12% to $7,337, and international QARSD grew 17% to $2,072. The important point isn’t the metric itself—it’s what it implies: CarGurus doesn’t need to add a ton of new dealers to grow. It can grow by moving existing dealers up the stack and attaching more products.

The margin structure is what makes this model so powerful. In the fourth quarter of 2024, non-GAAP consolidated gross profit was $199 million, up about 14% year over year, and non-GAAP gross margin reached 87%, up roughly 860 basis points. That’s an exceptional profile for a marketplace: once the platform is built and the traffic is there, the incremental cost of serving another dealer dollar is low. The heavy spend is not “cost of revenue,” it’s sales and marketing to win and retain dealers, and engineering to keep the product ahead.

At the full-year level, 2024 revenue was $894.38 million, down 2.17% from $914.24 million the year prior, while earnings were $20.97 million, down 32.57%. On its face, that looks like stagnation. But the more accurate read is mix shift: the revenue decline largely reflected the intentional wind-down of lower-quality digital wholesale revenue rather than a collapse in the Marketplace. As that mix shifted toward the high-margin Marketplace business, reported margins improved meaningfully.

That pivot also changed how CarGurus used its cash. After the CarOffer experience, capital allocation tilted away from big, splashy M&A and toward share repurchases. Since initiating its buyback program, CarGurus has repurchased 23% of shares outstanding—management’s way of saying it believes the market was undervaluing the core cash-generating business.

Finally, the question that hangs over all dealer-supported marketplaces: pricing power. CarGurus’ path here has been steady rather than aggressive—expand the footprint, take more wallet share from existing dealers, and do it through a combination of dealer additions, tier upgrades, adoption of add-on products, like-for-like price increases, and improved lead quantity and quality. If that continues, CarGurus doesn’t need a new business model to grow. It just needs to keep proving, month after month, that it’s the highest-ROI line item in the dealer’s budget.

XII. Playbook: Strategic & Investing Lessons

The CarGurus story leaves you with a surprisingly reusable playbook—both for building marketplaces and for underwriting them as a business.

The Power of Algorithmic Transparency in Opaque Markets

Steinert has always been blunt about what makes CarGurus different: transparency is the point. It’s why he went after auto in the first place. As he put it, “Netflix is doing it for entertainment. Zillow and Trulia are doing it for real estate. We’re doing it for auto shopping and improving a task that has bothered consumers for decades.”

That framing matters, because CarGurus didn’t win by being a slightly better Craigslist. It won by taking a stance. The Deal Rating algorithm turned a wall of listings into something closer to a guide: here’s how this car compares, here’s what it should cost, and here’s whether the deal is actually good. That one move—making value legible—gave shoppers a reason to start on CarGurus, not just bounce between tabs.

Two-Sided Marketplace Playbook: Consumer-First Strategy

CarGurus broke the chicken-and-egg problem the way many successful marketplaces do: win the consumer first. Aggregate inventory, make the shopping experience genuinely useful, and let traffic do the persuasion.

Then it made the dealer side frictionless: free to participate, easy to see results, and simple to upgrade once the value was proven. The freemium model wasn’t just a pricing tactic—it was a distribution strategy. Get the inventory, generate the leads, and turn performance into paid subscriptions.

SEO as a Distribution Moat

A lot of marketplaces talk about “brand.” CarGurus built a quieter moat first: search. Years of creating structured, data-driven pages and accumulating domain authority turned Google into a dependable acquisition engine.

And that kind of advantage compounds. A new entrant can copy features. They can’t copy a decade of being the best answer to millions of high-intent searches.

The Founder Advantage: Financial Cushion Enabled Patient Building

Steinert has described the hidden upside of being able to bootstrap in very practical terms: “The benefit of that is twofold. Number one, when we did screw up as most startups do, we could live to see another day. And the related benefit is that we were able to retain in both cases a ton of equity in the hands of the employees and the founders.”

Because he didn’t need venture capital to survive, CarGurus could afford to be wrong early—then pivot hard from the review community idea into the marketplace model that actually worked. That patience is rarer than it sounds, and it’s often the difference between “almost” and “inevitable.”

When to Go Public: Timing Matters

CarGurus hit the public markets in October 2017 with a story Wall Street loves: category leadership, fast growth, and real profitability. It raised money and credibility before the COVID-era boom distorted the industry—and before the subsequent bust punished anything that even smelled like inventory risk.

In hindsight, the timing gave CarGurus the best of both worlds: public-market scale without having to debut in chaos.

Knowing When to Pivot: Direct-to-Consumer Was Harder Than Expected

IMCO and the CarOffer transactions business were attempts to move closer to the transaction and capture more of the value chain. But when those efforts proved harder to operate through volatility—and started pulling CarGurus toward risk it wasn’t built to hold—management eventually did the hard thing: it pulled back and refocused on the profitable core.

A lot of companies don’t die from competition. They die from stubbornness. CarGurus’ willingness to wind down what wasn’t working is a real part of the story, not a footnote.

Data Network Effects: The Flywheel Strengthens Over Time

At its best, CarGurus gets stronger in a very specific way. It connects a massive audience of shoppers with a broad dealer network, and it mediates that connection with pricing context and trust signals. That activity generates data—search behavior, listing performance, conversion signals—that improves the algorithm and the dealer tools.

More marketplace activity sharpens the ratings and recommendations. Better ratings and recommendations improve the shopper experience. A better shopper experience brings more activity. It’s a flywheel built on data and trust, and while competitors can imitate pieces of it, it’s hard to replicate the full loop at scale.

XIII. Porter's 5 Forces Analysis

Competitive Rivalry: HIGH

This is a crowded ring. CarGurus goes toe-to-toe with AutoTrader, Cars.com, TrueCar, and increasingly Facebook Marketplace, which can undercut everyone on price because it’s not really trying to be an auto company—it’s just a giant attention machine. CarGurus has real differentiation in its Deal Rating algorithm and the trust it’s built with shoppers, but dealers can list across multiple platforms with little friction. That means the fight is constant, and it’s often fought on one brutal battleground: who delivers the best ROI for a dealer’s advertising dollars.

Threat of New Entrants: MEDIUM

Building a basic listings site isn’t hard. Aggregating inventory is table stakes. What’s hard is becoming the default starting point for shoppers: earning SEO authority over time, building a consumer brand people actually trust, and developing pricing intelligence that feels credible. Google or Meta could enter if they cared to, but they haven’t made it a priority. The real barrier isn’t technology—it’s liquidity and trust, on both sides of the marketplace, at the same time.

Bargaining Power of Suppliers/Dealers: MEDIUM-HIGH

Dealers are the paying customers, and their power has been rising. Consolidation into large groups like Lithia and AutoNation increases negotiating leverage, and switching costs are low enough that a big group can credibly threaten to shift budget away. CarGurus can be essential, but the uncomfortable truth in this model is that CarGurus needs dealers more than any single dealer needs CarGurus.

Bargaining Power of Buyers/Consumers: LOW

For consumers, the product is free, so they don’t have direct pricing leverage. And because shoppers are fragmented, no one buyer can influence the market. The real “buyer power” is behavioral: switching is easy. If a better free experience showed up, people could move in a day. CarGurus’ defense is habit and trust—once shoppers believe the site helps them avoid getting ripped off, that belief creates real stickiness.

Threat of Substitutes: MEDIUM-HIGH

There are plenty of ways to shop for a car without CarGurus: dealer websites, Craigslist, Facebook Marketplace, Carvana-style retailers, and, in some cases, manufacturer direct sales. Dealer sites keep getting better, and digital retailing keeps improving across the industry. The need for third-party validation hasn’t gone away, but the path consumers take to get it keeps evolving—and that creates steady substitution pressure.

Overall Assessment: CarGurus sits in a competitive market but still has a defensible position. Brand, SEO authority, marketplace scale, and pricing intelligence create meaningful protection. But this is not winner-take-all. Multi-homing—by both dealers and shoppers—puts a ceiling on pricing power and ensures the fight never really ends.

XIV. Hamilton's 7 Powers Analysis

1. Scale Economies: MODERATE

CarGurus has real scale advantages, but they’re not absolute. The big fixed costs—technology, product development, and data infrastructure—get spread across tens of millions of shoppers, which helps. But sales and marketing don’t magically shrink as the business grows; winning and keeping dealer budgets still takes work.

And because automotive classifieds isn’t winner-take-all, scale is more like a ticket to compete than a trophy you get to keep. CarGurus, AutoTrader, and Cars.com are all big enough to play the game.

2. Network Effects: STRONG

This is still the heart of the story: more dealers create more inventory, more inventory attracts more consumers, and more consumers send more leads back to dealers. On top of that sits the second loop—data. More searches and clicks generate more signals, which can improve rankings, recommendations, and pricing context, which improves the shopping experience, which drives more activity.

As the Marketplace scaled, it also created something dealers care about just as much as leads: intelligence. A large, growing dataset paired with machine learning can become a practical advantage—helping dealers price, merchandise, and move inventory faster.

But there’s a ceiling. Multi-homing is the reality of this market. Dealers list on multiple platforms at the same time, which blunts lock-in and keeps network effects from turning into a true monopoly dynamic.

3. Counter-Positioning: WEAK

CarGurus’ “Deal Rating” approach was early and distinctive, but it wasn’t impossible to imitate. AutoTrader and Cars.com could—and did—build their own versions of pricing and transparency features. There’s no structural business model move here that incumbents can’t copy. The edge is execution and trust, not an uncopyable position.

4. Switching Costs: MODERATE

For consumers, switching costs are basically mental, not technical. If you trust CarGurus and you’re used to its interface, you’ll start there—but opening another tab is effortless.

For dealers, switching is also fairly easy because they can run multiple channels at once. The stickier part shows up when dealers begin relying on CarGurus’ data-driven tools and workflows. If the platform is helping them make pricing changes that translate into more vehicle detail page views, more leads, and faster turn times, that’s not just advertising anymore—that’s operational signal. Walking away from that creates some real friction.

5. Branding: STRONG

CarGurus built its brand around a simple promise: “Shop smart, buy smart.” Transparency isn’t a tagline here—it’s the product. That positioning helped it become the most visited automotive shopping site in the U.S., with massive inventory coverage and a broad dealer network.

And importantly, brand means different things on each side of the marketplace. Dealers tend to see CarGurus as a vendor. Consumers are more likely to see it as a guide—someone on their side, in a process that usually doesn’t feel that way.

6. Cornered Resource: WEAK TO MODERATE

Steinert’s experience and credibility helped CarGurus get off the ground, but it’s not a lasting, exclusive asset. The company’s proprietary data and algorithms have value, yet they aren’t truly “cornered.” Competitors can assemble similar datasets over time, and there aren’t meaningful patents or regulatory barriers that block them.

7. Process Power: MODERATE

CarGurus’ edge has often been how it operates: an engineering-first culture, strong SEO and performance marketing know-how, and the ability to manage dealer relationships at scale. Internally, widespread AI usage has also been positioned as a driver of faster execution and sharper insights, with the ambition of turning proprietary data and machine learning into more automation and efficiency over time.

Primary Power: Network Effects + Branding

Secondary Power: Scale Economies + Process Power

Key Vulnerability: Multi-homing and low switching costs prevent winner-take-all outcome

XV. Bull vs. Bear Case

🐂 Bull Case:

The bull thesis starts with a simple claim: CarGurus is the market leader in a trend that’s still moving in its favor. More of the car-buying journey is happening online, and CarGurus keeps showing it can turn that behavior into high-margin revenue without taking on the existential inventory risk that sank so many “digital retail” dreams.

Just as important, it’s not only a listings marketplace anymore. Newer tools are expanding the opportunity beyond the roughly $3.5 billion U.S. Marketplace segment into an additional $4 billion dealer software and data products TAM, widening the runway if CarGurus can keep earning the right to sit deeper in dealer workflows.

The proof point is the core Marketplace engine. It’s been putting up double-digit growth with strong profitability: Marketplace revenue grew about 14% year over year, and Marketplace adjusted EBITDA rose 18%. That growth came from the classic CarGurus playbook: move dealers into higher tiers, attach more add-on products, take like-for-like price increases, and keep improving lead quantity and quality. Over the same period, CarGurus added 1,989 net new dealers globally year over year.

International is another lever that still looks early. International operations posted a 27% revenue increase, with particularly strong performance in Canada and the U.K.—evidence that the model can travel, not just win once.

Then there’s capital allocation and valuation. Compared to peak-era pricing, the stock trades at more reasonable levels, backed by demonstrated profitability and cash generation. And the buybacks matter here: they’re not just financial engineering. They’re a signal that management believes the core business is durable enough to return capital aggressively while still investing in growth.

Finally, there’s AI. If CarGurus can turn its data advantage into genuinely better dealer products and a better consumer experience—pricing tools, inventory insights, and analytics that improve outcomes—it could create new revenue streams that feel less like “ads” and more like software.

🐻 Bear Case:

The bear thesis begins where automotive always begins: the cycle. Even with revenue growth in the Marketplace, CarGurus operates in a category that can swing hard when consumer sentiment drops and interest rates stay high. Dealers feel that pressure quickly, and when dealers get cautious, marketing budgets become a target.

The company also has fresh scar tissue. The wind-down of the CarOffer transactions business resulted in losses, and it reinforces a broader concern: every step closer to the transaction increases operational complexity and exposure to volatility.

Dealer consolidation is another structural headwind. Fewer, larger dealer groups means higher concentration risk and more bargaining power on the customer side. In a market with low switching costs, dealers can shift spend to alternative platforms with relatively little friction—especially if they believe lead quality is converging across competitors.

Carvana is the cautionary tale that still hangs over the entire category. CarGurus avoided Carvana’s extreme inventory risk, but the underlying lesson remains: automotive retail is harder to “tech” than it looks, and the path from browsing online to completing a purchase is still messy.

There’s also the platform risk that never completely goes away: Google. If Google decided to seriously enter automotive classifieds, it has the traffic, data, and ad infrastructure to be disruptive. It hasn’t happened—but it’s always in the background as a credible threat.

And then there’s maturity. In 2024, CarGurus revenue was $894.38 million, down 2.17% year over year. Even if you adjust for the wholesale wind-down, skeptics can argue that the business is shifting from a high-growth story to a steadier, more mature cash generator—which changes what the stock should be worth.

What to Watch:

The two most important KPIs for tracking CarGurus’ ongoing performance are:

-

Marketplace Revenue Growth Rate: This is the cleanest read on the health of the core engine. Double-digit growth suggests continued dealer adoption and expanding revenue per dealer. A sustained move to single digits would suggest maturation.

-

U.S. Quarterly Average Revenue per Subscribing Dealer (QARSD): This is the “wallet share” metric. It captures tier upgrades, add-on product adoption, and pricing. If QARSD grows consistently above inflation, it’s a sign of real pricing power and product value.

Secondary signals include net dealer additions, international revenue growth, and paying dealer churn rates.

XVI. The Road Ahead: Future Scenarios

EV Transition Impact

Electric vehicle shopping isn’t just “car shopping, but with a battery.” It tends to involve longer research cycles, fewer truly comparable vehicles, and new questions that matter a lot: range, charging access, and what ownership looks like when the technology is still moving fast. The good news for CarGurus is that its core value proposition—data, context, and transparency—should translate. The catch is that doing it well likely means building EV-specific content and tools, not just re-labeling the existing experience.

AI Disruption: ChatGPT and Conversational Search

CarGurus’ bet is that its mix of proprietary data, machine learning, predictive analytics, and agentic AI can deliver a new level of intelligence, automation, and efficiency for both dealers and consumers. AI is already central to how the company builds product, runs operations, and positions itself as an automotive tech leader.

But there’s a threat hiding in plain sight: if conversational agents become the primary way people research big purchases, the old “type a query into Google, click the blue link” funnel gets weaker. And if that funnel weakens, CarGurus’ long-built SEO advantage could erode. The company’s answer is straightforward: invest heavily in AI so it can stay useful even if the front door to the internet changes.

GenZ Shopping Behavior

Younger shoppers are increasingly starting their discovery journeys on TikTok and other social platforms, not on traditional search engines. That’s a problem for any business that grew up on SEO, because it changes where attention forms and how trust is built. For CarGurus, staying relevant may depend on adapting to social discovery—earning visibility and credibility upstream, before a shopper ever thinks to open a listings site.

Dealer Ecosystem Evolution

CarGurus is ultimately tied to the dealer system because dealers are its paying customers. If that system changes, CarGurus has to change with it. Some manufacturers continue to explore direct sales and agency models that reduce the role of traditional dealerships. Tesla has shown that a direct model can work, and others have experimented in that direction. If dealer networks shrink meaningfully, CarGurus’ customer base shrinks with them.

M&A Possibilities

Consolidation in automotive classifieds remains an open question. A merger with a major competitor like Cars.com could, in theory, create meaningful scale advantages. Private equity could also decide the category is mature enough, and cash-generative enough, to take public companies private. And in any scenario like that, CarGurus’ dual-class structure matters: Steinert retains control over decisions of this magnitude.

The Ultimate Question

So what is CarGurus becoming? A growing platform that extends into new product categories and deeper dealer workflows—or a maturing classifieds site nearing its natural ceiling?

Management is clearly arguing for the platform path, investing in dealer software and data products to broaden the business beyond listings and leads. But the post-2022 lesson is equally clear: expanding the footprint only works if the company keeps its discipline, protects profitability, and avoids drifting into risks the model was never meant to carry.

XVII. Epilogue & Reflections

Zoom out, and the CarGurus story is really Steinert’s recurring theme: take a market that runs on opacity, and make it legible. TripAdvisor did it to hotel marketing. CarGurus did it to dealer pricing. And it’s why his later work, like ApartmentAdvisor, fits the same pattern. When information is unevenly distributed, the platform that can surface the truth—at scale—has a shot to rewire behavior.

CarGurus’ simplest promise is also its most powerful. It takes the mountain of data it gathers from both sides of the marketplace, uses it to tell shoppers which listings are actually good value, and then routes that intent to the dealership. In Steinert’s words: “Our position is to help consumers find great deals from great dealers.”

That sounds obvious now, but it’s also the key differentiator. CarGurus didn’t just host listings. It took a position on value. The Deal Rating system effectively said: some cars are priced well, and some aren’t—and we’re going to tell you which is which. That editorial stance built trust with consumers, even if it sometimes frustrated dealers whose inventory landed on the wrong side of the algorithm. The trade-off was real, and it ended up being a strength.

The 2022 gut check clarified another truth: platform extension has limits. Moving from a marketplace that facilitates leads to a business that sits closer to the transaction—and absorbs more operational complexity and risk—was harder than it looked. In an industry as volatile and asset-heavy as automotive, “capture more of the value chain” can turn into “inherit more of the downside.” CarGurus’ eventual pullback was the lesson in action: in the wrong environment, sticking to core competencies beats ambitious vertical integration.

If you’re building marketplaces, CarGurus is a clean case study in the fundamentals. Start consumer-first to solve the cold start. Prove value before you monetize. Use SEO as a long-term distribution engine, not a short-term hack. And recognize that patience—enabled here by bootstrapping and later-stage funding—buys you the ability to pivot when your first plan is wrong.

If you’re investing in marketplaces, CarGurus is the reminder that a great unit-economic model can still live inside a cyclical, intensely competitive industry. These businesses can generate substantial cash flow, but they don’t get to coast. Dealers can multi-home. Competitors can copy features. Growth comes from continuous product improvement, geographic expansion, and staying, relentlessly, the best ROI line in the budget.

Steinert’s career also makes a quieter point: second acts are real. After TripAdvisor, he founded CarGurus in 2006 and built it into the second-largest and fastest-growing car-shopping site in the United States. He didn’t just repeat a win—he adapted the playbook to a different market and scaled it again.

And the story still isn’t finished. For all the progress, the digital transformation of auto retail remains early-innings. Expectations for transparency, convenience, and digital enablement are only rising. Whether CarGurus holds its leadership over the next decade will come down to the same principles that got it here: trust earned through transparency, advantage built through data-driven product, and the discipline to grow without drifting into risks it can’t afford to own.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube