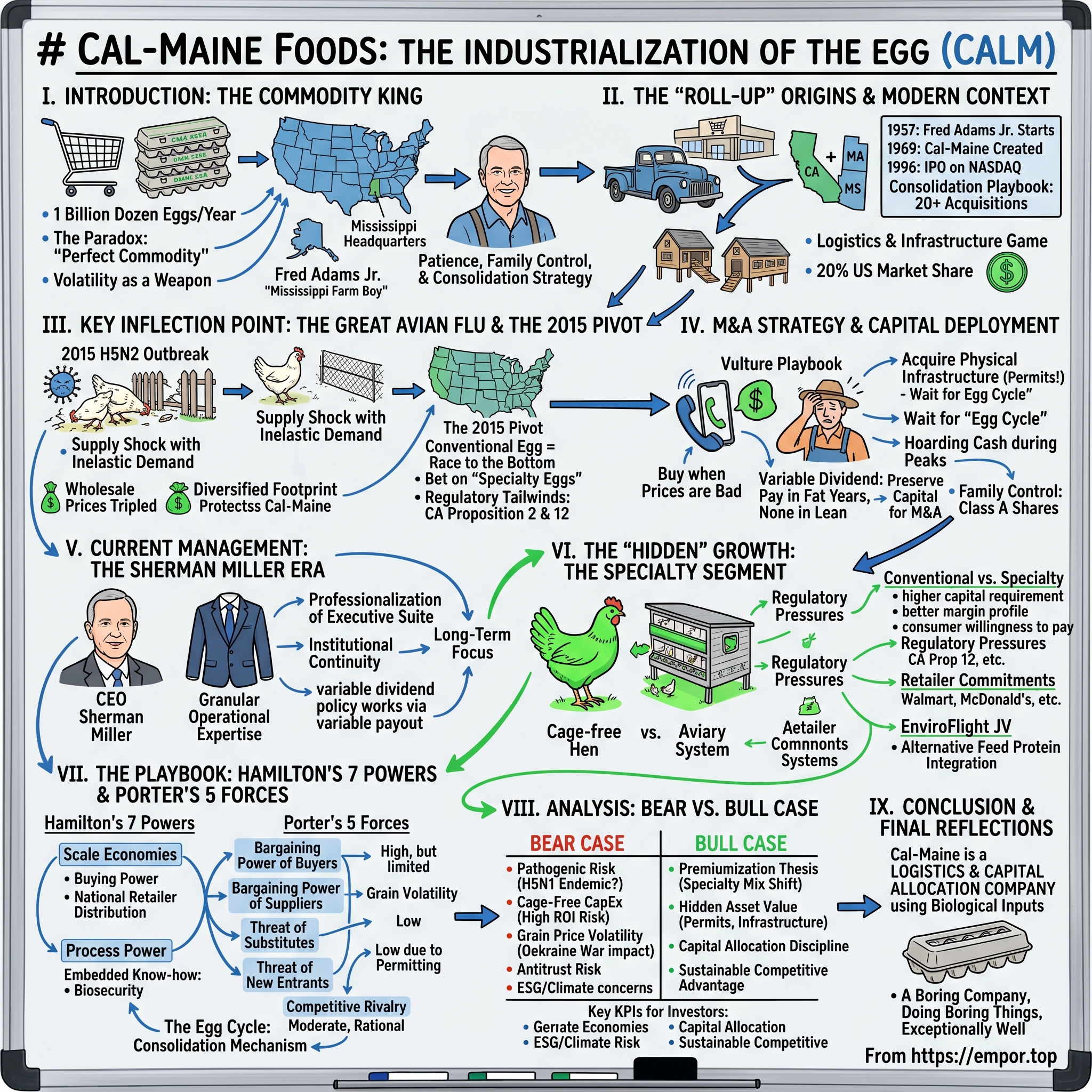

Cal-Maine Foods: The Industrialization of the Egg

I. Introduction: The Commodity King

Walk into any Walmart in Tuscaloosa, any Kroger in Cincinnati, any Costco in suburban Phoenix on a Tuesday morning. Head past the produce section, past the bakery, past the rotisserie chickens spinning under heat lamps. There, in the refrigerated case, stacked floor to eye-level in cardboard cartons of varying shades of brown and white, sit the eggs. Dozens of dozens. Maybe a hundred different SKUs depending on the store. Brown eggs. White eggs. Cage-free. Pasture-raised. Organic. Omega-3 enriched. Eggland's Best. Land O'Lakes. Great Value. Kirkland Signature. Simple Truth.

Pick up any carton. Look at the back. Find the plant code—a small string of letters and numbers stamped near the sell-by date. Roughly one in five times, that code traces back to a single Mississippi-headquartered company that almost no American consumer has ever heard of.

That company is Cal-Maine Foods, ticker symbol CALM, headquartered in Ridgeland, Mississippi—a sleepy suburb of Jackson where the local high school has more name recognition than the largest egg producer in the United States. Cal-Maine produces and sells roughly one billion dozen shell eggs per year. That's twelve billion individual eggs. Enough to give every man, woman, and child on Earth one and a half breakfasts.

And yet here's the paradox that makes Cal-Maine such a fascinating business case study. Eggs are the closest thing the modern American economy has to a "perfect commodity." A grade-A large white egg from a Cal-Maine facility in Lake City, Florida is functionally identical to a grade-A large white egg from a competitor's facility in Iowa. There is no brand premium for the underlying product. There is no proprietary technology that protects the recipe. The chicken does the work. The carton just holds twelve of them.

How does a company selling something this fungible, this commodified, this unsexy, end up with a market capitalization that has at various points exceeded four billion dollars? How does it generate billions in cash, fund a half-century of acquisitions, and survive—even thrive—through grain shocks, avian flu pandemics, and the general bipolar nature of agricultural pricing?

The answer is the story of this episode. It's a story about a Mississippi farm boy named Fred Adams who in 1957 took over a small chicken operation and decided, against every conventional wisdom of mid-century American agriculture, that the future of the egg business was not better farming but bigger logistics. It's a story about how patience, family control, and a willingness to write checks during the worst moments in the industry's history allowed one company to consolidate roughly twenty percent of an industry that had been hopelessly fragmented for centuries.

It's a story about volatility as a weapon. About the strange genius of a "variable dividend" that pays nothing in lean years and gushes cash in fat ones. About how California's animal welfare ballot initiatives accidentally became the single most important regulatory tailwind in modern egg history. And about how, in 2025, a CEO named Sherman Miller found himself running what is essentially a logistics and biosecurity company that just happens to use chickens as the manufacturing apparatus.

The roadmap for the next three hours: from a Mississippi chicken coop to the largest egg producer in the world, by way of twenty-two acquisitions, two avian flu pandemics, one Proposition 12, and a family share class structure that has kept activists at bay for four decades. Buckle up. The egg is more interesting than you think.

II. The "Roll-Up" Origins & Modern Context

The year is 1957. Eisenhower is in the White House. The interstate highway system is brand new. The American supermarket, that suburban temple of refrigerated abundance, is still in its adolescence. And in a small Mississippi town, a thirty-year-old man named Fred R. Adams Jr. takes the reins of a poultry operation that produces eggs for the local market. He has no inherited fortune. He has no MBA. What he has is a sense, increasingly out of step with his peers in mid-century American agriculture, that the egg business is about to undergo the same industrial transformation that had already remade meatpacking and dairy.

The egg industry of the 1950s looked nothing like it does today. The typical American egg producer ran a flock of a few thousand birds, sold to a regional cooperative or a local distributor, and competed primarily on the basis of geographic proximity to the consumer. There was no national egg brand. There were no national egg distribution networks of any meaningful scale. The egg, being fragile and perishable, was assumed to be a fundamentally local product.

Adams disagreed. In 1969, twelve years after taking over his initial operation, he engineered the merger that would create Cal-Maine Foods. The deal combined his Mississippi assets with operations in California and Maine, and in a stroke of branding economy that any 21st-century marketer would admire, he simply concatenated the two coastal state names. Cal-Maine. The Mississippi part was implicit. The geographic ambition was the entire point.

Through the 1970s and 1980s, Cal-Maine grew quietly. The company developed a reputation for ruthless operational discipline, for a willingness to invest in then-novel technologies like in-line egg processing equipment, and for an obsessive focus on cost per dozen produced. While competitors thought of themselves as farmers, Adams thought of himself as a manufacturer who happened to use biological inputs.

The company went public in 1996 on the NASDAQ, raising capital that would fund what became, in retrospect, the defining strategic decision of its corporate history: the consolidation playbook. Between 1989 and the present, Cal-Maine has executed more than twenty significant acquisitions of regional egg producers across the United States. Some of these deals were splashy. Most were not. The pattern was relentlessly the same. Find a regional producer, often family-owned, often capital-constrained, often demoralized by yet another collapse in egg prices. Buy the operation at a price reflecting the bottom of the cycle. Plug it into the Cal-Maine logistics network. Capture the synergies on feed purchasing, distribution, and overhead. Move on to the next target.

The "Amazon of Eggs" framing isn't quite right—Cal-Maine doesn't have a software platform, doesn't reinvent customer experience, doesn't operate on thin margins funded by a different business line. But the underlying insight is similar. Both companies recognized that a fragmented industry with poor unit economics could be transformed by a single operator willing to play the long game on scale and infrastructure.

The numerical result of this thirty-five-year consolidation effort is staggering when you sit with it. Cal-Maine's share of the U.S. shell egg market has grown from a low single-digit percentage in the late 1980s to roughly twenty percent today. In an industry where the next-largest competitor controls maybe seven or eight percent and where the long tail of small producers still numbers in the hundreds, Cal-Maine occupies a position of structural dominance that took decades to build and would require similar decades to dislodge.

The narrative shift this represents matters enormously for anyone trying to understand the modern company. Cal-Maine is not, in any meaningful sense, a farming business. It is an industrial logistics business with biological inputs. Its competitive advantages live not in the henhouses but in the contracts with grain suppliers, the distribution agreements with national retailers, the bio-security protocols at the production facilities, and the institutional patience to wait out cycles that destroy weaker hands.

Which sets up the question of how, exactly, a "weaker hand" gets destroyed in this industry. The answer arrived in spectacular fashion in 2015.

III. Key Inflection Point: The Great Avian Flu & The 2015 Pivot

In April 2015, a commercial turkey farm in Pope County, Minnesota reported unusual mortality in its flock. Within days, samples sent to the National Veterinary Services Laboratories in Ames, Iowa confirmed the worst suspicion of every poultry operator in North America: highly pathogenic avian influenza, specifically the H5N2 strain, had crossed from migratory waterfowl into domestic commercial poultry. Within weeks, the outbreak had spread across the upper Midwest. By the time it burned itself out in June 2015, more than fifty million birds had been culled, including roughly forty million egg-laying hens. The U.S. lost approximately ten percent of its entire commercial laying flock in less than ninety days.

For most egg producers, this was an apocalypse. The industry watched in horror as decades-old family operations were forced to depopulate entire complexes—euthanizing every bird on the property, then waiting through a months-long cleaning and disinfection process before they could even begin to repopulate. For producers with operations concentrated in the affected geographies, particularly Iowa, the financial damage was catastrophic. Iowa, which had been the largest egg-producing state in the country, lost roughly half of its laying capacity in a single quarter.

For Cal-Maine, the situation was very different. The company's geographic footprint had been deliberately diversified across the Southeast, Texas, and the Mid-Atlantic—regions that experienced essentially zero impact from the 2015 outbreak. While competitors were burying birds in mass graves and writing down hundreds of millions of dollars in destroyed inventory, Cal-Maine's facilities continued to hum.

What happened next was a textbook demonstration of what economists call "supply shock with inelastic demand." Egg consumption in the United States is remarkably stable. Americans eat eggs because they're cheap, versatile, and culturally embedded in breakfast routines that don't change quickly. When the supply of eggs collapses by ten percent and consumer demand barely budges, prices don't move ten percent. They explode. Wholesale egg prices in the summer of 2015 roughly tripled from their early-year baseline. Retail prices followed, and Cal-Maine, with its undamaged production base, captured the windfall.

The fiscal year that ended in May 2016 became the most profitable in the company's history to that point. Net income for fiscal 2016 reached approximately $315 million on revenue of roughly $1.9 billion—a net margin north of sixteen percent on what is supposedly a commodity business. For context, in the prior fiscal year, net income had been around $160 million on similar revenue. The avian flu had effectively doubled Cal-Maine's profitability without the company doing anything different operationally.

But the more important consequence of the 2015 outbreak was strategic, not financial. Sitting in Ridgeland in late 2015 and early 2016, watching competitors collapse and watching their own production facilities print money, Cal-Maine's leadership team confronted a deeper realization about the structure of their business.

The conventional egg—the white-shell large grade-A egg that had been the industry's bread and butter for a century—was a race to the bottom. Even with twenty percent market share, Cal-Maine couldn't escape the boom-bust cycle that defined commodity egg pricing. Volatility could be a friend during shock years, but the long-run trajectory of the conventional egg business was relentless margin compression as scale efficiencies got passed through to retailers and ultimately to consumers.

There was, however, an emerging segment of the egg market behaving very differently. Specialty eggs—a catch-all category encompassing cage-free, organic, free-range, pasture-raised, and nutritionally enhanced products like omega-3 enriched eggs—commanded retail prices that were often double or triple the conventional equivalent. The volumes were smaller. The supply chain was more complex. The capital requirements per bird were higher. But the margin profile was fundamentally different.

The strategic shift that began in earnest after 2015 was the decision to bet meaningful capital on this specialty transition. Cal-Maine's leadership recognized that California, with its 2008 Proposition 2 ballot initiative banning conventional cages, was a leading indicator of where the rest of the country was headed. Massachusetts, Washington, Oregon, Michigan—a growing patchwork of state-level regulation was pushing the industry toward cage-free production. Consumer preference, driven by everything from animal welfare concerns to the perceived health benefits of pasture-raised eggs, was reinforcing the regulatory pressure.

The pivot was not a wholesale abandonment of conventional eggs. Cal-Maine continued to produce enormous volumes of white eggs for the value-oriented consumer and the food service channel. But the marginal capital deployment increasingly flowed toward specialty production. The company began retrofitting facilities, building new cage-free housing, and—crucially—acquiring companies with specialty production capabilities that would have taken years to build organically.

Avian flu turned out to be the catalyst that exposed the limits of the old business model and the opportunity in the new one. The next decade would be about playing both sides of that trade.

IV. M&A Strategy & Capital Deployment

Picture the office of a small egg producer somewhere in the American Midwest in the spring of 2018. The walls are wood-paneled. There's a framed photograph of a long-dead patriarch on the wall behind the desk. The current owner, second or third generation, is staring at a stack of bank statements that tell a story he's been refusing to acknowledge for two years. Egg prices have been below his cost of production for most of the last eighteen months. The line of credit is maxed out. The feed bill is overdue. His daughter, the one who was supposed to take over the business, has just announced she's going to law school.

The phone rings. It's Cal-Maine.

This is, with apologies for the dramatization, roughly how the consolidation of the American egg industry has actually unfolded. Cal-Maine's M&A playbook is not glamorous. There are no investment bankers in midtown skyscrapers structuring leveraged buyouts. There are no auctions with five private equity firms bidding against each other. There is, in most cases, a relationship that has existed for years between Cal-Maine's leadership and the target's owners, and there is the patient willingness to wait until the cycle has done the financial work that makes a deal attractive.

The "vulture" framing is a little harsh. Cal-Maine doesn't predate on healthy companies. It buys when willing sellers exist, which in this industry tends to be when prices are bad and have been bad for long enough to exhaust the seller's optionality. The acquisition of Fassio Egg Farms, completed in March 2024, brought into the Cal-Maine fold a Utah-based producer with both conventional and specialty operations, expanding the company's footprint in the Mountain West where it had been underrepresented. The Meadowbrook Farms transaction added cage-free capacity in Indiana that aligned directly with the specialty pivot. ISE America, acquired in late 2023, brought roughly 4.7 million laying hens and additional cage-free capacity in the Northeast.

The pattern across these deals is instructive. Cal-Maine doesn't pay headline-grabbing premiums. It doesn't typically issue stock in transactions. It uses cash from its own balance sheet, which it has been hoarding for exactly these moments. It assumes operational responsibility quickly and integrates the acquired operations into its national logistics network. And it almost never closes existing facilities or eliminates the local management teams that came with the deal, because it understands that biosecurity and operational excellence at the facility level requires people who know the specific facility.

The financial math behind these acquisitions is dictated by what insiders call the "egg cycle." Like most agricultural commodities, eggs follow a predictable boom-bust pattern. High prices attract investment. Investment expands production. Expanded production crashes prices. Crashed prices force marginal producers out. Production contracts. Prices recover. Repeat. Historically, the cycle has run roughly four to seven years peak to peak, though specific shock events—avian flu being the most dramatic—can compress or extend any given cycle.

Cal-Maine has structured its capital allocation policy around this cycle. The company maintains a substantial cash position during peak earnings years specifically so that it has dry powder when the inevitable downturn arrives. Competitors who can't or won't maintain similar reserves end up forced sellers when the cycle turns. Cal-Maine ends up the buyer of choice because everyone in the industry knows two things: Cal-Maine has the cash, and Cal-Maine will close.

The asset-light versus asset-heavy distinction is worth dwelling on because it's where Cal-Maine's strategy becomes genuinely sophisticated. A naive observer might assume that Cal-Maine's M&A is primarily about buying brands or customer relationships. It's not. The company is buying physical infrastructure: laying houses, processing facilities, feed mills, the land underneath all of it, and—perhaps most importantly—the operating permits that allow that land to be used for industrial poultry production.

Those permits are, in modern American agriculture, the real moat. Local zoning, state environmental regulations, water usage rights, manure management permits, and the general resistance of suburbanizing rural communities to large-scale animal agriculture have made it nearly impossible to build a new commercial-scale egg complex on greenfield land in most of the country. The existing facilities, with their grandfathered permits and established operational history, are functionally irreplaceable. When Cal-Maine acquires a competitor, it's not just acquiring current production; it's acquiring optionality on future production that no greenfield project could ever match.

This dynamic creates a fascinating asymmetry in the M&A market. The replacement cost of Cal-Maine's production base, if you tried to rebuild it today on permitting basis alone, would dwarf the company's book value. Yet the company can typically acquire operating production capacity at multiples that make sense relative to current cash flow because the seller is rarely thinking about replacement cost—the seller is thinking about getting out before the next downturn.

The result is a quiet but relentless transfer of irreplaceable infrastructure from financially stressed family operators to a single dominant operator that can afford to think in twenty-year cycles. Which brings us to the family that has been at the center of this dynamic for sixty-five years and counting.

V. Current Management: The Sherman Miller Era

If you walked into the Cal-Maine corporate headquarters in Ridgeland, Mississippi during the company's annual meeting, you might be forgiven for thinking you'd wandered into a regional bank board meeting circa 1985. The executives wear conservative suits. The slide decks are unflashy. The financial discussion is precise but largely free of the buzzword inflation that characterizes presentations at most public companies. The CEO speaks in the cadence of a man who has been working in the egg business for thirty years and assumes everyone in the room understands the difference between a hatchery and a pullet house.

Sherman Miller became CEO of Cal-Maine in January 2023, succeeding Dolph Baker, who had led the company since 2010. Miller's path to the corner office was the model of an internal succession at a company that prizes institutional continuity. He joined Cal-Maine in 1996, the year the company went public. He spent the next twenty-six years rotating through operational roles—starting in production, moving through sales, eventually to chief operating officer in 2012, and then president in 2018.

Miller's reputation inside the industry is one of granular operational expertise. He is, by all accounts, the kind of CEO who can walk into a layer house and tell within thirty seconds whether the bird density is appropriate, whether the feed lines are properly calibrated, and whether the air handling system is moving the right volume of air per minute. This is not glamorous knowledge. It is the kind of knowledge that turns out to be enormously valuable when the company you run depends on the health of roughly fifty million birds spread across dozens of facilities in twenty states.

The transition from Baker to Miller was not a transition of strategic direction. The specialty egg pivot continues. The disciplined M&A program continues. The conservative balance sheet continues. What did change, modestly, was the professionalization of the executive suite. Miller has built out a senior team that includes more outside hires than Cal-Maine has historically employed, particularly in finance, supply chain, and sustainability. The company that had operated for decades as a tight-knit Mississippi family business is gradually becoming a tight-knit Mississippi family business with a more conventional public company management apparatus surrounding the family core.

The variable dividend policy is perhaps the single most distinctive feature of Cal-Maine's capital allocation philosophy and deserves a careful explanation because it is so unusual among S&P 500-adjacent companies. Most public companies that pay dividends pay them on a fixed quarterly basis. Shareholders learn to expect a particular dividend per share, and management bends over backward to maintain or modestly grow that dividend even in challenging years, because the signaling cost of cutting the dividend is enormous.

Cal-Maine does not play that game. The company's stated policy is to pay a quarterly dividend equal to one-third of net income for that quarter, but only when the company is profitable. In quarters where the company loses money, no dividend is paid. In quarters where the company is exceptionally profitable—say, during an avian flu shock year—the dividend can be enormous. In the quarter ended November 2022, when wholesale egg prices were spiking due to the H5N1 outbreak that had begun earlier that year, Cal-Maine paid a dividend that was an order of magnitude larger than its dividend in any quarter of fiscal 2020.

The genius of this policy is that it inverts the usual problem with dividends in cyclical businesses. Most companies face enormous pressure to maintain dividends through downturns, which forces them to take on debt or run down cash reserves at exactly the moments when those reserves are most valuable for opportunistic investment. Cal-Maine has none of that pressure. Its shareholders have signed up explicitly for a variable payout. Management can therefore preserve capital during downturns without facing the punishment that other CEOs would face for cutting a dividend. That preserved capital becomes the M&A war chest for the next acquisition cycle.

The variable dividend works in part because of the company's share class structure, which is the third pillar of the management architecture. Cal-Maine has dual-class shares: common shares trade publicly, while Class A shares, held primarily by the Adams and Baker families and certain related parties, carry ten votes per share. The economic stake of the controlling family is meaningful but not dominant. The voting stake is decisive. The result is that activist investors, who might otherwise look at Cal-Maine's enormous cash positions and wonder why the company isn't levering up to do buybacks or spin-offs or dividend recaps, have essentially no path to influence corporate strategy.

This family control has costs. There is no auction-driven scrutiny of management compensation. There is no perpetual threat of takeover that disciplines mediocre execution. There is no board independence in the activist-friendly sense that governance reformers would prefer. But the benefits in this particular industry have arguably outweighed the costs. Cal-Maine can plan in twenty-year cycles because no one can force it to deliver quarterly results that require optimizing for the short term. It can sit on cash through three-year troughs in the egg cycle because no activist can force a buyback. It can pivot to specialty eggs at a measured pace dictated by capital efficiency rather than narrative pressure.

The Adams legacy is the human story underneath this corporate architecture. Fred Adams Jr. died in 2020 at the age of eighty-eight, having presided over the transformation of Cal-Maine from a Mississippi farm into the largest egg producer in the country. His son-in-law Adolphus Baker—Dolph—led the company through its most consequential decade. Sherman Miller represents the next generational transition: still a lifer, still steeped in the company culture, but now operating at a scale and complexity that would have been unimaginable to Adams in 1957.

The combination of operational continuity, capital allocation discipline, and family-control insulation is what allows Cal-Maine to run the playbook we've been describing. Without any one of these three pillars, the playbook would collapse. With all three intact, the company can play offense in markets where its competitors are playing pure defense.

That offense, increasingly, is being played in a segment of the egg market that simply did not exist at meaningful scale a generation ago.

VI. The "Hidden" Growth: The Specialty Segment

The cage-free hen lives a different life than her conventional cousin. She has access to perches, to scratch areas, to nest boxes. She lives in a barn rather than a stacked cage system, sharing space with thousands of her sisters in what poultry scientists call an "aviary system." Her bones are stronger because she walks more. Her egg, once it's been cleaned, sized, and packed, looks identical to a conventional egg on a kitchen counter. But the consumer pays roughly twice as much for it. And Cal-Maine, which has spent the better part of the last fifteen years building the infrastructure to produce her egg at scale, captures meaningfully more profit per dozen than it would on the conventional alternative.

The specialty egg segment is the most important growth story inside Cal-Maine, and it's the story that most investors who haven't done the work of reading the company's filings tend to underappreciate. The company breaks its egg sales into two categories: conventional and specialty. Conventional eggs are the white-shell commodity eggs that have been the industry's mainstay for a century. Specialty eggs encompass everything else: cage-free, organic, free-range, pasture-raised, and nutritionally enhanced products such as omega-3 eggs.

In fiscal 2017, specialty eggs represented roughly twenty-five percent of Cal-Maine's volume. By fiscal 2024, that share had climbed to roughly thirty-eight percent of dozens sold and a meaningfully higher percentage of revenue—because specialty eggs sell at substantially higher unit prices. Specialty net average selling price has typically run 50 to 100 percent higher than conventional, depending on the specific category and the prevailing conventional egg market.

The margin capture is even more dramatic than the price premium implies. Specialty eggs have a fundamentally different cost structure than conventional eggs. The cost per bird is higher because the housing is more capital-intensive. The feed conversion ratio is slightly worse because the birds are more active. The mortality rates are sometimes higher in cage-free environments because the birds can injure each other. All of these inputs raise the cost of specialty production relative to conventional. But the price premium more than compensates, particularly in product categories like organic and pasture-raised where consumer willingness to pay has scaled with the broader premiumization of American food retail.

The regulatory tailwind underneath this segment cannot be overstated. California voters approved Proposition 2 in 2008, banning the confinement of egg-laying hens in conventional cages effective January 2015. Proposition 12, approved in 2018, went further—setting specific square-footage requirements for hen housing and, crucially, banning the sale within California of eggs from facilities that didn't meet the new standards, regardless of where those eggs were produced.

The interstate commerce implications of Proposition 12 were litigated all the way to the U.S. Supreme Court, which in May 2023 upheld the law in National Pork Producers Council v. Ross. The decision settled a question that had hung over the industry for years and confirmed that California's market access rules were enforceable. Other states followed: Massachusetts with Question 3 in 2016, Michigan, Oregon, Washington, Colorado, and others have layered on similar requirements with varying timelines.

The cumulative effect is that a meaningful and growing share of the U.S. egg market is legally accessible only to producers with cage-free certified production. Cal-Maine, having spent more than a billion dollars over the last decade building cage-free capacity, was uniquely positioned to serve this market. Smaller producers, who couldn't justify the capital expenditure required to retrofit conventional cage operations, were either forced to exit the affected markets entirely or to sell to consolidators—Cal-Maine chief among them.

The retailer dynamic accelerated the trend. Walmart announced in 2016 a commitment to transition to a one hundred percent cage-free egg supply chain by 2025. McDonald's, Costco, Kroger, and dozens of other major buyers made similar commitments with varying timelines. These corporate commitments, while non-binding and frequently revised, sent a clear signal to producers about where the market was headed. Cal-Maine, with both the capital and the strategic conviction, responded by building.

Specialty growth doesn't just happen in housing systems. It also happens in product innovation. Cal-Maine has invested in nutritionally enhanced eggs through products marketed under labels like Egg-Land's Best (in which the company holds a meaningful joint venture stake) and Land O'Lakes (a co-pack and licensing arrangement). These branded products carry retail margins that approach branded consumer packaged goods economics, which in the egg world is a different universe from commodity production.

The most interesting strategic move on the specialty side—and the one that hints at where the company's thinking might go over the next decade—is the joint venture with EnviroFlight, an Ohio-based company specializing in black soldier fly larvae as a sustainable feed ingredient. The basic concept is to create an alternative protein source for poultry feed that doesn't depend on the corn and soybean meal that have historically driven feed costs and feed cost volatility. Black soldier fly larvae can be raised on agricultural and food waste streams, can be produced with a fraction of the land and water inputs required for soybean cultivation, and can deliver a nutritional profile suited to poultry diets.

If alternative feed protein scales economically, it represents a genuine vertical integration play that could meaningfully alter Cal-Maine's input cost structure over the long term. Feed represents roughly fifty to sixty percent of the cost of producing an egg. Anything that reduces feed cost or feed cost volatility flows directly to margin. The EnviroFlight investment is small in dollar terms today, but the option value is significant, and it tells you something about how Cal-Maine's leadership thinks about the medium-term evolution of their business.

The conventional egg business will not disappear. The price-sensitive consumer, the food service channel, the food manufacturing channel that uses eggs as ingredients—these segments will continue to demand low-cost commodity production for the foreseeable future. But the marginal dollar of capital deployment at Cal-Maine increasingly flows toward specialty, and the marginal dollar of profit increasingly comes from specialty. Which raises the question of how investors should think about the durability of the company's competitive position in either segment.

VII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

To understand why Cal-Maine has been able to compound advantage for thirty-five years in an industry that, on its surface, looks structurally hostile to economic profit, it helps to apply two analytical frameworks that long-term investors have leaned on heavily over the past two decades.

The first is Hamilton Helmer's Seven Powers framework, which identifies seven distinct sources of durable competitive advantage. Cal-Maine doesn't possess all seven—few companies do—but it possesses two in unusual depth.

Scale Economies is the most obvious. Cal-Maine purchases an enormous amount of feed: corn, soybean meal, and various supplements. The company is among the largest individual buyers of feed ingredients in the U.S. agricultural complex, which gives it pricing leverage and access to direct relationships with grain originators that smaller producers simply cannot replicate. The same dynamic plays out in packaging procurement, in fuel and logistics contracts, in pharmaceutical procurement for flock health management, and in capital equipment purchasing. Every input cost line at Cal-Maine benefits from scale advantages that compound across the entire production base.

The distribution side amplifies the scale advantage. National retailers like Walmart, Costco, Kroger, and Albertsons need suppliers who can deliver consistent volume to dozens or hundreds of distribution centers across the country. The logistics complexity of running a national egg supply chain—coordinating production, processing, packaging, refrigerated transportation, and distribution center delivery across thousands of SKUs and dozens of geographies—is enormous. Cal-Maine has built that capability over decades. A regional producer with even excellent operations cannot replicate it without committing capital and time on a scale that few in the industry have access to.

The second power, Process Power, is more subtle but in some ways more durable. Process Power refers to embedded operational know-how that competitors cannot easily copy even when they understand the principles. Cal-Maine's biosecurity protocols are the textbook example. In an industry where a single breach of biosecurity at a single facility can result in the loss of millions of birds and tens of millions of dollars, the operational discipline required to maintain biosecurity at scale across dozens of facilities is genuinely hard. It requires culture, training, procedure, monitoring, and the kind of management attention that only comes from leaders who have seen the consequences of failure.

The 2022-2024 H5N1 outbreak, which has been more geographically widespread and longer-lasting than the 2015 H5N2 event, has tested every major egg producer's biosecurity systems repeatedly. Cal-Maine has not been immune—the company has lost birds to the outbreak at certain facilities, and the production impacts have been periodically material—but the company's overall track record relative to peers has reinforced the value of its biosecurity investments. In a world where avian influenza has become an endemic risk rather than an episodic one, the ability to prevent infection at the facility level is a competitive advantage that compounds with each cycle.

Now let's run the same analysis through Michael Porter's classic Five Forces framework, which examines industry attractiveness from five angles.

The Bargaining Power of Buyers is high in egg distribution. Walmart is reportedly Cal-Maine's largest customer. Costco, Kroger, Albertsons, and the other large food retailers individually represent meaningful concentration risk. These buyers have considerable leverage in negotiating with any single supplier, and they actively use that leverage. However, the picture flips somewhat when you consider that Cal-Maine is essentially the only egg producer with the scale to fully service these retailers' national requirements. A Walmart that wanted to drop Cal-Maine and replace it with another supplier would face enormous logistical complexity and would likely need to contract with five or six regional producers to replicate the volume, with all the associated coordination costs. This doesn't eliminate buyer power, but it asymmetrically constrains it.

The Bargaining Power of Suppliers is meaningful primarily on the feed side. Corn and soybean meal are global commodities priced in markets that no individual buyer—even Cal-Maine—can meaningfully influence. The 2022 spike in feed costs driven by the Ukraine war reminded everyone in the industry that input cost volatility is a permanent feature of the business. However, Cal-Maine's scale gives it some hedging capacity and some procurement advantage that smaller producers lack.

The Threat of Substitutes for the egg is, frankly, low. Plant-based egg alternatives like Just Egg have built a real but small market over the past decade. The category has not displaced eggs in any meaningful way and shows no signs of doing so at current price points and consumer adoption curves. Other breakfast proteins—bacon, sausage, yogurt—coexist with eggs rather than substituting for them. The egg occupies a unique nutritional and culinary position that has remained remarkably stable across decades.

The Threat of New Entrants is low, primarily because of the permitting and infrastructure dynamics discussed earlier. Building a new commercial-scale egg operation in the United States today is essentially impossible in most jurisdictions. The existing facilities are grandfathered, geographically dispersed, and held by operators with no economic incentive to sell at prices below replacement cost. New entrants face a structural barrier that no amount of capital can fully overcome.

Competitive Rivalry within the existing industry is moderate. The industry has consolidated dramatically over the past three decades, and the remaining large players have generally shown the rationality that comes with concentration. There are still occasional pricing wars during cyclical troughs, and there have been periodic legal disputes around alleged price coordination dating back more than a decade. But the day-to-day competitive intensity has declined as the industry has moved from hundreds of meaningful producers to a few dozen.

The "egg cycle" itself becomes a strategic weapon in this framework. Cal-Maine doesn't just survive cyclical volatility; it uses volatility as the mechanism through which competitive position is consolidated. Every downturn culls weak producers. Every cull creates acquisition opportunities for Cal-Maine. Every acquisition strengthens scale economies, which improves Cal-Maine's resilience in the next cycle. The flywheel turns slowly—measured in years per cycle rather than months—but it has been turning consistently for thirty-five years and shows no signs of stopping.

Which brings us to the inevitable question of what could break the flywheel.

VIII. Analysis: Bear vs. Bull Case

Every long-term investment thesis lives or dies on whether the bear case can be honestly engaged with rather than dismissed, and Cal-Maine has a serious bear case that deserves careful articulation.

The pathogenic risk is the most acute. The H5N1 strain that has been circulating in North American wild bird populations since late 2021 has proven different in important ways from prior avian influenza outbreaks. It is more geographically widespread, it persists longer in the environment, and it has demonstrated the ability to cross into mammalian hosts including dairy cattle—a development that began in early 2024 and has continued into 2026. The implications for the egg industry are uncomfortable. Biosecurity protocols designed for occasional, localized outbreaks may prove inadequate for an endemic, geographically pervasive threat. A worst-case scenario in which Cal-Maine experiences a major outbreak at one of its complexes would result in the loss of millions of birds, months of production downtime at the affected facility, and write-downs that could materially impact a quarter or two of earnings. The market knows this risk and prices it into the stock to some degree, but the tail risk is real and not fully quantifiable.

The cage-free transition CapEx is the second major bear case element. Converting conventional caged production to cage-free housing requires roughly $40-60 per bird in capital expenditure, depending on the specific configuration. Across an industry that still has perhaps 100 million birds in conventional housing, the total capital required to complete the transition runs into the billions. Cal-Maine has been investing steadily, but the ultimate ROI on this CapEx depends on retailers and consumers continuing to validate the price premiums that justify the investment. If, in a recessionary environment, consumers trade back down to conventional eggs in numbers, the cage-free assets could end up underutilized relative to the capital deployed.

The grain price volatility risk has been demonstrated repeatedly. Feed costs represent the majority of the variable cost of producing an egg. Corn and soybean meal prices respond to weather, geopolitics, and biofuel policy in ways that are almost completely outside any egg producer's control. Cal-Maine has hedging capabilities and pricing pass-through mechanisms, but in environments where feed costs spike rapidly and egg prices don't immediately follow, margins can compress meaningfully.

There are subsidiary concerns worth noting. Antitrust risk in an industry where consolidation has reached the levels Cal-Maine has helped drive is non-trivial. The company has been a defendant in egg pricing litigation in past cycles, and ongoing or future regulatory scrutiny is possible. ESG-related concerns around industrial animal agriculture continue to attract attention from a growing share of institutional investors, which could over time affect cost of capital. Climate-related concerns around heat stress on laying flocks and water availability for facility operations add another layer of long-term uncertainty.

The bull case starts with the premiumization thesis. If the average price per dozen eggs sold by Cal-Maine continues to migrate upward as the specialty mix grows, the company's revenue and margin profile begins to look quite different from a conventional commodity producer. The math is straightforward: a company selling a billion dozen at an average $2.50 with a fifteen percent net margin is generating $375 million in net income. The same company selling a billion dozen at an average $4.00 with a twenty percent net margin is generating $800 million. The path between those two states is the specialty mix shift, and it has been progressing for fifteen years.

The hidden asset value supports the bull case as well. The land underneath Cal-Maine's facilities, the operating permits attached to that land, and the irreplaceability of the existing infrastructure all represent value that doesn't show up cleanly on a balance sheet measured at historical cost. A serious sum-of-the-parts analysis that valued the production facilities at replacement cost would yield a figure substantially above current book value, although translating that hidden value into cash flow requires the company to keep operating productively, which creates a circularity.

The capital allocation discipline is itself a bull case element. Companies that maintain genuine capital discipline through cyclical industries are rare. Companies that combine capital discipline with a structural willingness to deploy aggressively at cycle bottoms are even rarer. Cal-Maine has demonstrated both for thirty-five years, and the variable dividend policy plus the family share structure creates an institutional architecture that is likely to persist for the foreseeable future.

For long-term investors trying to track the company's trajectory between annual reports, two or three KPIs deserve disproportionate attention. The first is the specialty share of dozens sold and the specialty share of revenue—the two together capture both the volume mix shift and the price premium dynamics. The second is the conventional egg net average selling price relative to feed cost, which captures the cyclical positioning and the company's ability to capture margin during favorable parts of the cycle. The third, harder to measure but worth attention, is the pace and price of M&A activity—Cal-Maine's deals reveal information about both the state of the cycle and management's view of relative value.

Comparing Cal-Maine to its peer set is instructive. The peer set is small and largely private. Rose Acre Farms, the second-largest U.S. egg producer, is privately held and provides limited public information. Versova, formed through the combination of Center Fresh Group, Fremont Farms, and other operations, is also private. Daybreak Foods, Hillandale Farms, and Michael Foods (a subsidiary of Post Holdings, which trades publicly but where eggs are a component of a larger food business) round out the major U.S. players. Cal-Maine's unique status as a pure-play, publicly traded egg producer means there is no clean public comparable—which both creates analytical challenges and contributes to the company's valuation receiving less attention than its scale would otherwise justify.

A myth-versus-reality interlude is worth a paragraph. The popular narrative around Cal-Maine, particularly during periods of high egg prices, has often been that the company is "profiteering" from consumer hardship. Congressional letters, FTC inquiries, and various media coverage during the 2022-2023 egg price spikes leaned heavily into this framing. The reality is more complicated. Cal-Maine is a price-taker on the wholesale egg market, not a price-setter. Its pricing follows USDA-published benchmark prices that reflect supply-demand dynamics across the industry. When supply collapses due to avian flu, prices rise, and producers with intact operations earn windfall profits. When supply normalizes, prices fall, and the windfall disappears. Whether one finds this dynamic objectionable on policy grounds is a separate question from whether it represents anti-competitive behavior, and the evidence for the latter has been thin.

IX. Conclusion & Final Reflections

Sit with Cal-Maine for long enough and the company starts to feel less like an agricultural producer and more like something else entirely. The customer-facing brands are mostly private label or licensed third parties. The product is identical to the competition. The regulatory environment is unforgiving. The biological inputs are unpredictable. And yet, year after year, decade after decade, the company compounds.

What Cal-Maine actually is, when you strip away the chickens and the eggs and the feed mills, is a logistics and capital allocation company that has chosen to operate in an industry with a genuinely high barrier to entry, a structural tailwind from regulatory pressure on its smaller competitors, and a rare combination of family control and public market access that allows it to play a long game most public companies cannot.

The "Acquired" framing of "Great" versus "Big" cuts to the right question. Big is undeniable: twelve billion eggs a year, twenty percent national share, billions in market cap. Great is a more demanding test that asks whether the business will continue to compound advantage for the next twenty years, not just the last twenty. The honest answer is that Cal-Maine sits in genuinely interesting territory on this question. The competitive position is durable in ways that most commodity producers can only envy. The capital allocation framework is structurally aligned with long-term value creation. The specialty pivot has more runway than the current numbers suggest. And the H5N1 reality, while a real risk, may also reinforce the company's relative position by raising the operational bar for everyone else.

Whether one finds this company genuinely great or merely structurally advantaged is a judgment call that depends on one's view of the next decade in American food retail, the trajectory of avian influenza, the durability of premium consumer willingness to pay for specialty eggs, and the continuity of the management and family-control architecture that has defined the company for sixty-eight years.

What is hard to dispute is that Cal-Maine has built something genuinely unusual. A boring company, in a boring industry, doing boring things, exceptionally well, for a very long time. The hardware happens to be a chicken. The software is the operational and capital allocation discipline that has allowed Mississippi farm boys and their successors to quietly assemble the most consolidated, most strategically positioned egg production system in the world.

Every time you walk past the egg case, that's the company you're not thinking about. Which is, in many ways, exactly how they want it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube